Certain facts, statistics and data presented in this section and elsewhere in this prospectus have been derived, in part, from various official government sources and research reports. We believe that the sources of this information are appropriate sources for such information and have taken reasonable care in extracting and reproducing such information. We have no reason to believe that such information is false or misleading or that any fact has been omitted that would render such information false or misleading. The information has not been independently verified by us, the Sole Sponsor, the Underwriters or any other party involved in the Global Offering and no representation is given as to its accuracy. Prospective investors should not place undue reliance on any of such information contained in this prospectus. SOURCES OF INFORMATION China National Textile and Apparel Council China National Textile and Apparel Council ( 中國紡織工業協會), an Independent Third Party, is a national industry organisation authorised by the PRC government providing business consultation, constructing of market intelligence system and facilitating market development for the textile industry in the PRC. Preparation of the China Textile Industry Development Report is not commissioned by our Company. Euromonitor In connection with the Global Offering, we have engaged Euromonitor to conduct detailed market analyses of, and provide reports on the yarns and bedding products markets in the PRC (the ‘‘Research Reports’’). The aggregate contractual amount for the Research Reports and services provided by Euromonitor is US$78,000, the payment of which was not contingent upon our successful Listing or on any of the results obtained from the Research Reports. The Research Reports, dated in July, November 2009 and March 2010 respectively, consists of, among others, historical data for the period from 2004 to 2009, and forecasts for the period from 2010 to 2012. Euromonitor primarily undertook top-down central research with bottom-up intelligence to present a more comprehensive and accurate picture of bedding and yarns products market in the PRC. Euromonitor assessed relevant background information that is publicly available such as annual reports and accounts published by major manufacturers and reconciled these sources against any existing information and knowledge from our Company. Euromonitor also conducted trade interviews with multiple organisations for added perspective and accuracy. Multiple secondary and primary sources were also checked to validate all data and information collected with no reliance on any single-source. Furthermore, a test of each respondent ’ s information and views against those of others is applied to ensure reliability and to eliminate bias from these sources. To ensure forecast accuracy, Euromonitor adopted its standard practice of both quantitative as well as qualitative forecasts. These forecasts allow Euromonitor to establish the terms of the market size, growth trends etc, on the basis of providing a comprehensive and in-depth review of the market development ’ s past and future, while simultaneously providing cross-checking with established government/industry figures, trade interviews, and statistical tools (e.g. regression analysis, time-series analysis, data modelling) where possible. INDUSTRY OVERVIEW – 64 –

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Certain facts, statistics and data presented in this section and elsewhere in this prospectus have

been derived, in part, from various official government sources and research reports. We believe that

the sources of this information are appropriate sources for such information and have taken

reasonable care in extracting and reproducing such information. We have no reason to believe that

such information is false or misleading or that any fact has been omitted that would render such

information false or misleading. The information has not been independently verified by us, the Sole

Sponsor, the Underwriters or any other party involved in the Global Offering and no representation

is given as to its accuracy. Prospective investors should not place undue reliance on any of such

information contained in this prospectus.

SOURCES OF INFORMATION

China National Textile and Apparel Council

China National Textile and Apparel Council (中國紡織工業協會), an Independent Third Party, is a

national industry organisation authorised by the PRC government providing business consultation,

constructing of market intelligence system and facilitating market development for the textile industry in

the PRC. Preparation of the China Textile Industry Development Report is not commissioned by our

Company.

Euromonitor

In connection with the Global Offering, we have engaged Euromonitor to conduct detailed market

analyses of, and provide reports on the yarns and bedding products markets in the PRC (the ‘‘Research

Reports’’). The aggregate contractual amount for the Research Reports and services provided by

Euromonitor is US$78,000, the payment of which was not contingent upon our successful Listing or on

any of the results obtained from the Research Reports. The Research Reports, dated in July, November

2009 and March 2010 respectively, consists of, among others, historical data for the period from 2004 to

2009, and forecasts for the period from 2010 to 2012.

Euromonitor primarily undertook top-down central research with bottom-up intelligence to present

a more comprehensive and accurate picture of bedding and yarns products market in the PRC.

Euromonitor assessed relevant background information that is publicly available such as annual reports

and accounts published by major manufacturers and reconciled these sources against any existing

information and knowledge from our Company. Euromonitor also conducted trade interviews with

multiple organisations for added perspective and accuracy. Multiple secondary and primary sources were

also checked to validate all data and information collected with no reliance on any single-source.

Furthermore, a test of each respondent’s information and views against those of others is applied to

ensure reliability and to eliminate bias from these sources.

To ensure forecast accuracy, Euromonitor adopted its standard practice of both quantitative as well

as qualitative forecasts. These forecasts allow Euromonitor to establish the terms of the market size,

growth trends etc, on the basis of providing a comprehensive and in-depth review of the market

development’s past and future, while simultaneously providing cross-checking with established

government/industry figures, trade interviews, and statistical tools (e.g. regression analysis, time-series

analysis, data modelling) where possible.

INDUSTRY OVERVIEW

– 64 –

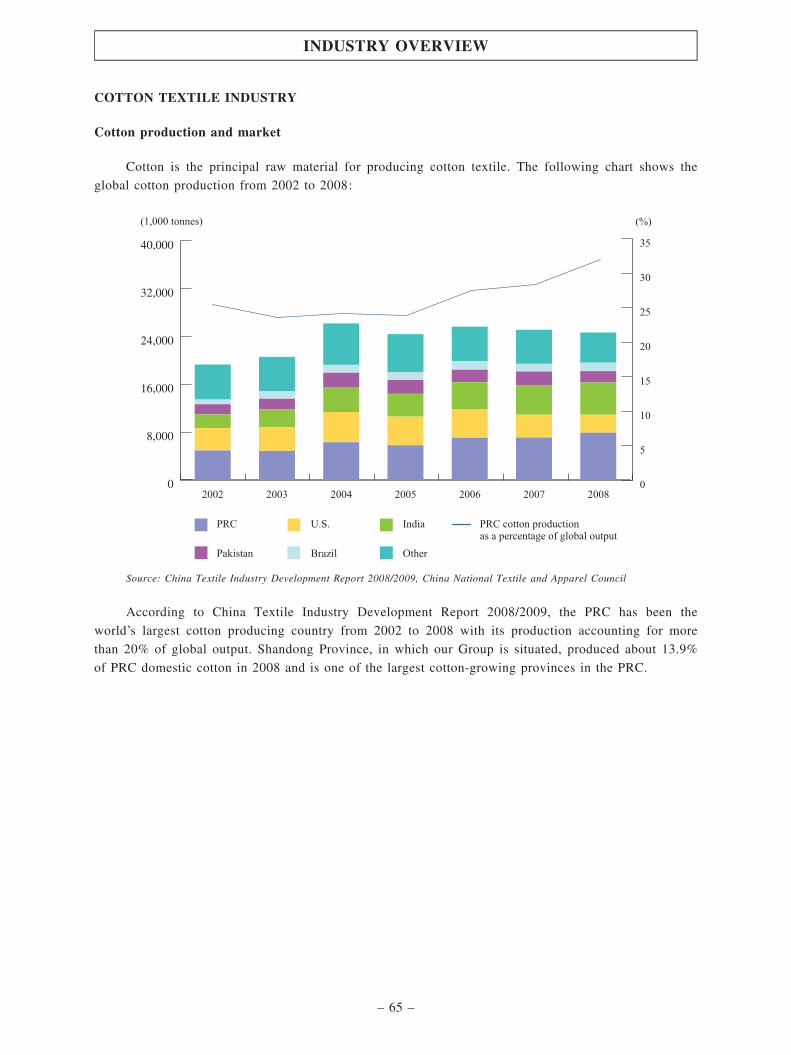

COTTON TEXTILE INDUSTRY

Cotton production and market

Cotton is the principal raw material for producing cotton textile. The following chart shows the

global cotton production from 2002 to 2008:

0

8,000

16,000

24,000

32,000

40,000

0

5

10

15

20

25

30

35

Source: China Textile Industry Development Report 2008/2009, China National Textile and Apparel Council

According to China Textile Industry Development Report 2008/2009, the PRC has been the

world’s largest cotton producing country from 2002 to 2008 with its production accounting for more

than 20% of global output. Shandong Province, in which our Group is situated, produced about 13.9%

of PRC domestic cotton in 2008 and is one of the largest cotton-growing provinces in the PRC.

INDUSTRY OVERVIEW

– 65 –

The following chart shows information relating to international and PRC cotton prices for the

periods indicated:

(Unit: RMB/tonne)

Source: China National Textile and Apparel Council

International cotton price has been stable since the end of 2004 but decreased by 35.7% from

US$0.7 per pound (or RMB10,716 per tonne) in June 2008 to US$0.45 per pound (or RMB6,781 per

tonne) in December 2008. PRC cotton price demonstrated a trend roughly similar to the international

cotton price, with a slight decrease in December 2006 and a more significant decrease of 22.6% from

RMB13,946 per tonne in June 2008 to RMB10,790 per tonne in December 2008. The difference

between domestic cotton price and international cotton price remained in the range of RMB3,000 per

tonne to RMB5,500 per tonne between 2005 and 2008.

Cotton yarn production

According to Euromonitor, cotton yarns can be divided into the following categories according to

yarn counts.

Types of cotton yarn Description

Coarse-count cotton yarn (粗支紗) Yarn count of 18 and below

Medium-count cotton yarn (中支紗) Yarn count of 19 to 28

Fine-count cotton yarn (細支紗) Yarn count of 29 to 60

High-count cotton yarn (高支紗) Yarn count of 61 and above

INDUSTRY OVERVIEW

– 66 –

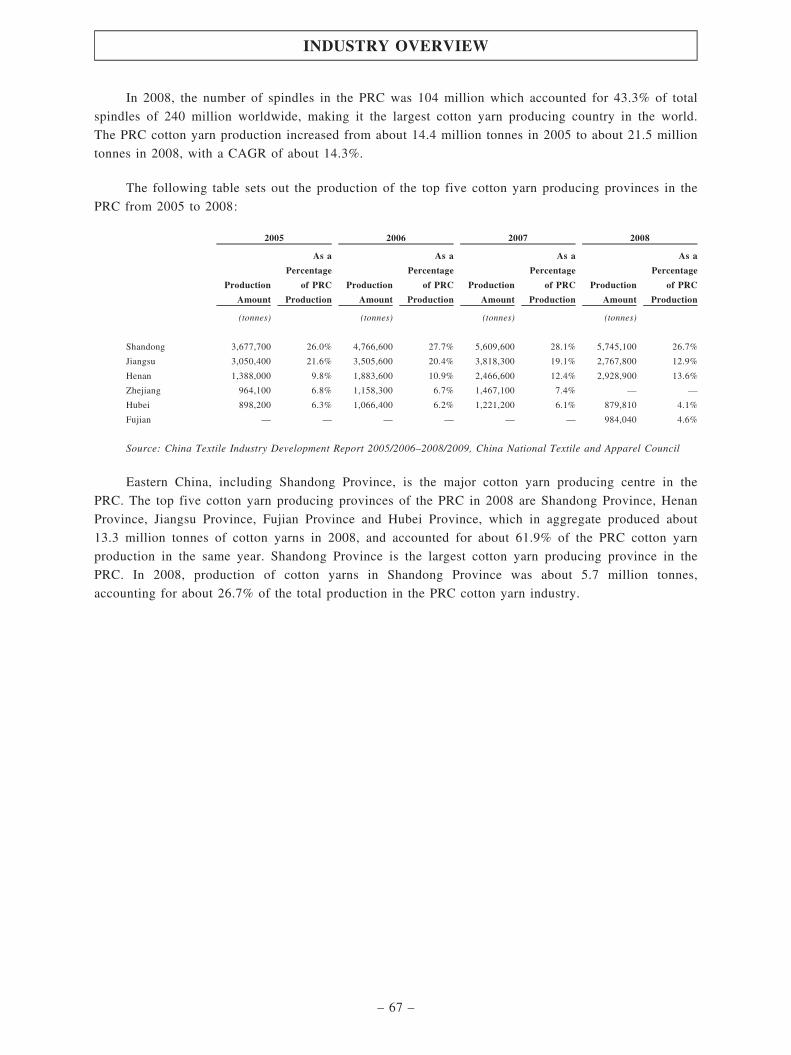

In 2008, the number of spindles in the PRC was 104 million which accounted for 43.3% of total

spindles of 240 million worldwide, making it the largest cotton yarn producing country in the world.

The PRC cotton yarn production increased from about 14.4 million tonnes in 2005 to about 21.5 million

tonnes in 2008, with a CAGR of about 14.3%.

The following table sets out the production of the top five cotton yarn producing provinces in the

PRC from 2005 to 2008:

2005 2006 2007 2008

Production

Amount

As a

Percentage

of PRC

Production

Production

Amount

As a

Percentage

of PRC

Production

Production

Amount

As a

Percentage

of PRC

Production

Production

Amount

As a

Percentage

of PRC

Production

(tonnes) (tonnes) (tonnes) (tonnes)

Shandong 3,677,700 26.0% 4,766,600 27.7% 5,609,600 28.1% 5,745,100 26.7%

Jiangsu 3,050,400 21.6% 3,505,600 20.4% 3,818,300 19.1% 2,767,800 12.9%

Henan 1,388,000 9.8% 1,883,600 10.9% 2,466,600 12.4% 2,928,900 13.6%

Zhejiang 964,100 6.8% 1,158,300 6.7% 1,467,100 7.4% — —

Hubei 898,200 6.3% 1,066,400 6.2% 1,221,200 6.1% 879,810 4.1%

Fujian — — — — — — 984,040 4.6%

Source: China Textile Industry Development Report 2005/2006–2008/2009, China National Textile and Apparel Council

Eastern China, including Shandong Province, is the major cotton yarn producing centre in the

PRC. The top five cotton yarn producing provinces of the PRC in 2008 are Shandong Province, Henan

Province, Jiangsu Province, Fujian Province and Hubei Province, which in aggregate produced about

13.3 million tonnes of cotton yarns in 2008, and accounted for about 61.9% of the PRC cotton yarn

production in the same year. Shandong Province is the largest cotton yarn producing province in the

PRC. In 2008, production of cotton yarns in Shandong Province was about 5.7 million tonnes,

accounting for about 26.7% of the total production in the PRC cotton yarn industry.

INDUSTRY OVERVIEW

– 67 –

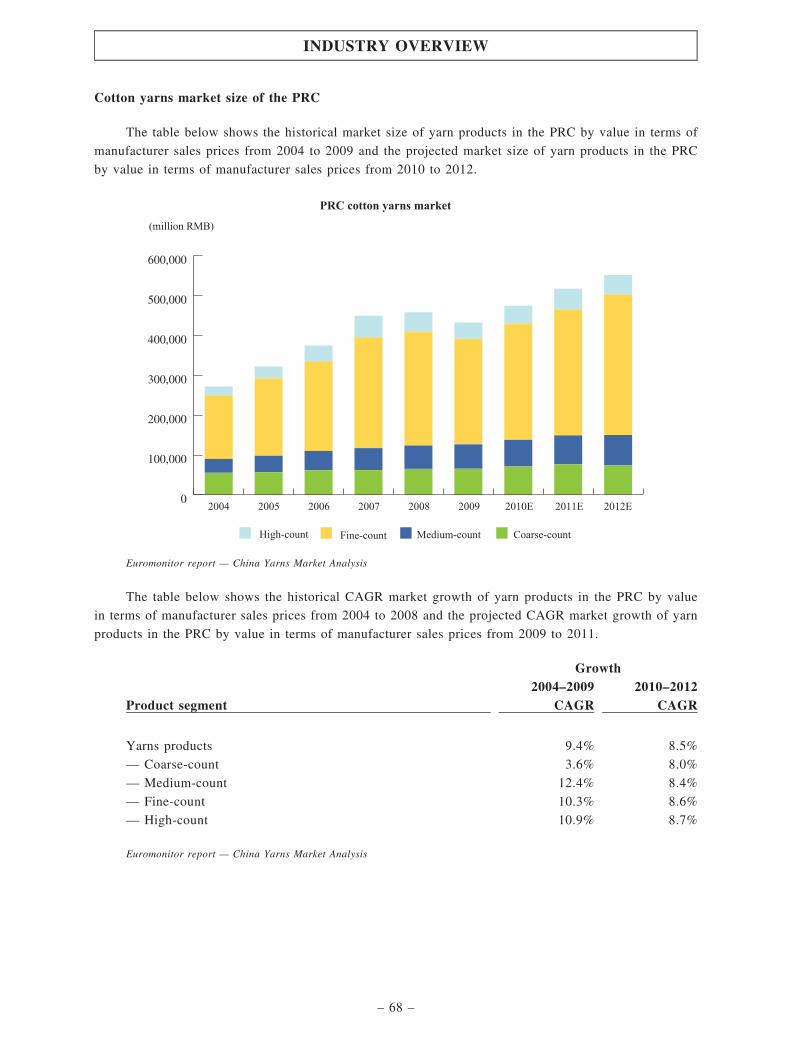

Cotton yarns market size of the PRC

The table below shows the historical market size of yarn products in the PRC by value in terms of

manufacturer sales prices from 2004 to 2009 and the projected market size of yarn products in the PRC

by value in terms of manufacturer sales prices from 2010 to 2012.

Euromonitor report — China Yarns Market Analysis

The table below shows the historical CAGR market growth of yarn products in the PRC by value

in terms of manufacturer sales prices from 2004 to 2008 and the projected CAGR market growth of yarn

products in the PRC by value in terms of manufacturer sales prices from 2009 to 2011.

Growth

Product segment2004–2009

CAGR2010–2012

CAGR

Yarns products 9.4% 8.5%

— Coarse-count 3.6% 8.0%

— Medium-count 12.4% 8.4%

— Fine-count 10.3% 8.6%

— High-count 10.9% 8.7%

Euromonitor report — China Yarns Market Analysis

INDUSTRY OVERVIEW

– 68 –

According to market research conducted by Euromonitor, for the year of 2009, the top 5

companies ranking in the fine-count and high-count yarns industry accounted for 2.6% of the total

market share, with the highest ranking company accounting for 1.3% of the total market share while we

ranked as the fourth largest yarns manufacturer in terms of sales value of fine-count and high-count

yarns in the PRC, accounting for 0.2% of the total market share.

Development trends of the cotton textile industry in the PRC

The two major leading objectives for current cotton textile industry are ‘‘scientific development’’

and ‘‘industry upgrade’’, which emphasise improvement in equipment standard, reduction in labour costs

and enhancement of productivity. The cotton yarn industry in the PRC is expected to have the following

development trends:

Demand for fine-count and high-count yarn

Domestic consumption of cotton textiles, in particular high-end textile products, has been driven

by the growth of economy and improvement in living standards in the PRC. Since the outbreak of the

financial crisis in 2008, the market demand for fine-count and high-count yarns and cotton clothes made

from those yarns has decreased, especially in the US market, resulting in a decrease in export for cotton

textile products and cotton clothes. However, as the pace of urbanisation in China increases, the demand

for high-count and premium high-count textile products from urban population is expected to gradually

increase. Fine-count and high-count yarns is expected to experience further growth in the long run.

Increased use of compact spinning

Compact spinning is performed by adding a condenser unit between the drafting zone and the yarn

formation zone that uses air flow to group the fibre strands horizontally. The yarns formed are less

hairy, smoother, tighter, firmer and more balanced and stronger than the ordinarily combed cotton yarns.

Compact yarns can increase the efficiency of weaving machines and save dyes and sizing and desizing

costs, making the fabrics more environmentally friendly. Compact spinning is most suitable for

producing high-count yarns and the yarns produced can be used for producing high grade dyed fabrics

and knitted fabrics. High grade dyed fabrics are commonly used in luxury men shirts with significant

growth prospects.

Development of blended spinning

Blended spinning is the future development trend in the yarn spinning industry, and is one of the

highly recommended development directions for the cotton textile industry stipulated in the

revitalization plan for textile industry proposed by the PRC government. The focus is expected to be

development of fibre blended with different yarns and new materials to enhance the fabric’s

functionalities.

The prosperity of the textile industry is crucial to domestic economic development, stimulate

export, create job opportunities, increase the income of farmers and accelerate the pace of urbanisation.

In order to further develop the textile industry, the central government has convened three meetings

since 19 November 2008 and issued ‘‘Plan for Adjusting and Promoting Textile Device Manufacturing

INDUSTRY OVERVIEW

– 69 –

Industry’’ (《紡織和裝備製造業調整振興規劃》) on 4 February 2009 and ‘‘Notice on Adjusting the

Export Tax Rebate’’ (《關於提高輕紡電子信息等商品出口退稅率的通知》(財稅[2009]43號)) on 25 March

2009, pursuant to which the PRC government is expected to implement the following measures:

. Stimulation of domestic demand and exploration of international market.

. Technological upgrade and development proprietary brands.

. Acceleration of replacement of outdated machinery.

. Focusing on production of high value-added productions with advanced technologies and

lower consumption of resources.

. Providing the financial supports and tax incentives: effective from 1 April 2009, the rate of

export tax rebate of certain textile products and clothing increased to 16%.

BEDDING INDUSTRY

Home textile market in the PRC

According to Euromonitor, home textile products include bedding and home furnishing products

such as curtains, sofa/table covers and table runners.

In recent years, the national income and living standards have improved steadily due to fast

economic growth. As a result, the domestic home textile market has also steadily increased with an

annual growth of approximately 20%. By 2008, the domestic retail value of the home textile industry

had hit RMB300 billion. The future demand for home related textiles is robust, and its market capacity

and potential is the most promising within the textile industry.

Despite the global financial crisis, the domestic bedding products market continued its strong

growth in 2008 due to growing demand after the real estate market boom. Weaker import demand from

overseas markets also forced many export oriented manufacturers to shift their focus to domestic

markets, which contributed to the home textile market growth in China in late 2008.

In recent years the home textile market in China has shown significant development, benefitting

from the rapid growth of the domestic real estate market and improvement in residential housing

conditions and living standards. Booming tourism and strong demand overseas have also contributed to

the growth of this industry. According to Euromonitor, it is widely believed by national experts that the

Chinese home textile industry has much room for expansion and a huge market capacity.

INDUSTRY OVERVIEW

– 70 –

The chart below shows the retail market size of home textile products in the PRC from 2004 to

2009:

Euromonitor report — China Bedding and Home Textile Market Analysis

Overview of the PRC bedding products market

The bedding industry is a sub-sector of the home textile industry. With the reform of the housing

system and the constant improvement of people’s living standards and aesthetic consciousness,

consumers are attaching greater importance to bedding products and pose higher requirements for

product quality and materials. This urges the industry to constantly develop new products and establish

identifiable brand images.

As soft interior decorations, bedding products have progressively become the focus of the textile

industry and a field valued by consumers. The domestic bedding products market has made some

outstanding progress in recent years, with the retail value of domestic bedding products soaring from

RMB42 billion in 2004 to RMB106 billion in 2009, representing a CAGR of 20.2%.

INDUSTRY OVERVIEW

– 71 –

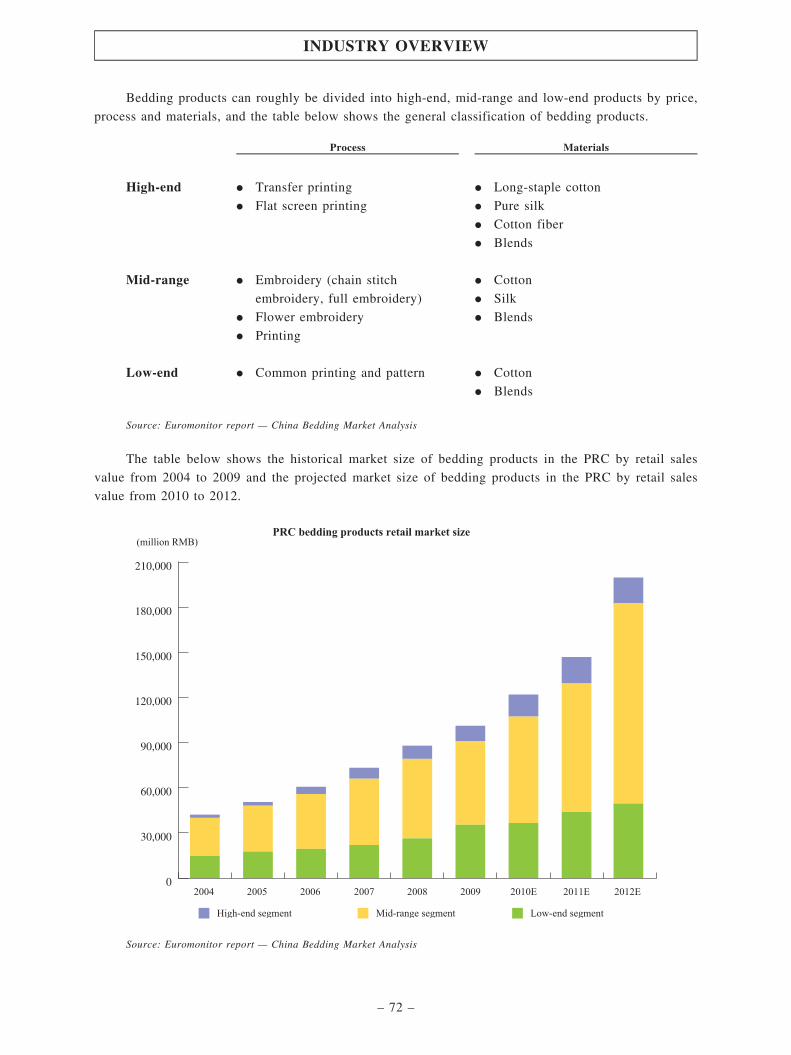

Bedding products can roughly be divided into high-end, mid-range and low-end products by price,

process and materials, and the table below shows the general classification of bedding products.

Process Materials

High-end . Transfer printing

. Flat screen printing

. Long-staple cotton

. Pure silk

. Cotton fiber

. Blends

Mid-range . Embroidery (chain stitch

embroidery, full embroidery)

. Flower embroidery

. Printing

. Cotton

. Silk

. Blends

Low-end . Common printing and pattern . Cotton

. Blends

Source: Euromonitor report — China Bedding Market Analysis

The table below shows the historical market size of bedding products in the PRC by retail sales

value from 2004 to 2009 and the projected market size of bedding products in the PRC by retail sales

value from 2010 to 2012.

Source: Euromonitor report — China Bedding Market Analysis

INDUSTRY OVERVIEW

– 72 –

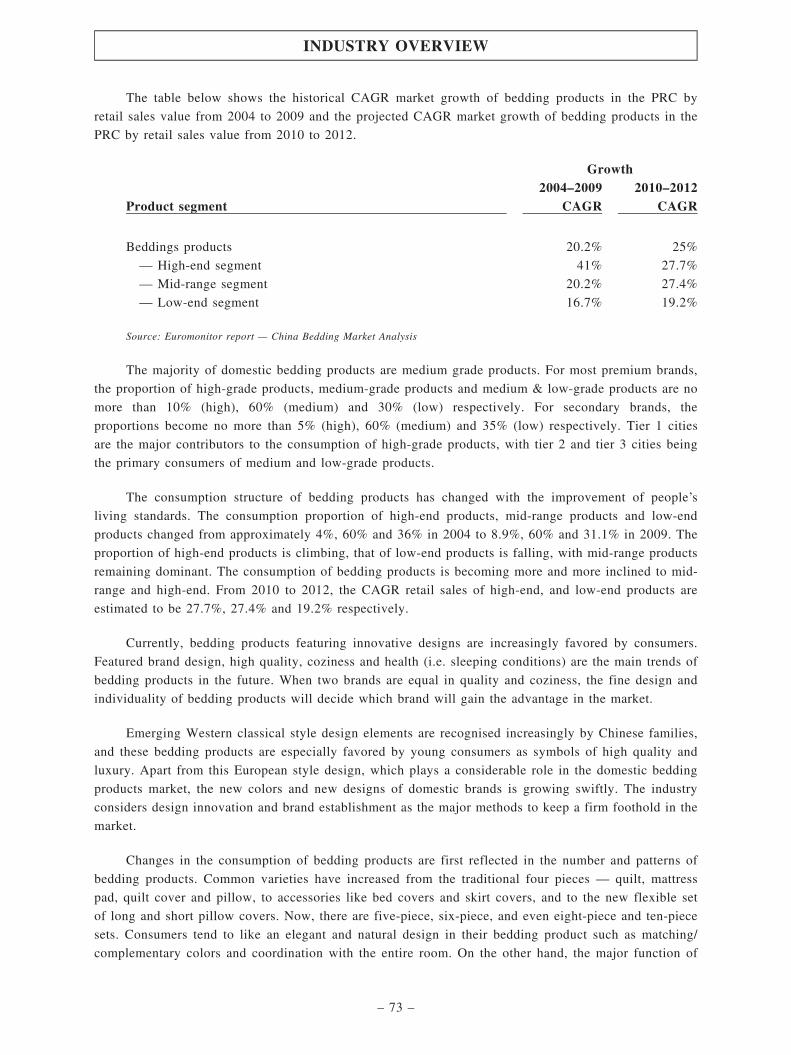

The table below shows the historical CAGR market growth of bedding products in the PRC by

retail sales value from 2004 to 2009 and the projected CAGR market growth of bedding products in the

PRC by retail sales value from 2010 to 2012.

Growth

Product segment2004–2009

CAGR2010–2012

CAGR

Beddings products 20.2% 25%

— High-end segment 41% 27.7%

— Mid-range segment 20.2% 27.4%

— Low-end segment 16.7% 19.2%

Source: Euromonitor report — China Bedding Market Analysis

The majority of domestic bedding products are medium grade products. For most premium brands,

the proportion of high-grade products, medium-grade products and medium & low-grade products are no

more than 10% (high), 60% (medium) and 30% (low) respectively. For secondary brands, the

proportions become no more than 5% (high), 60% (medium) and 35% (low) respectively. Tier 1 cities

are the major contributors to the consumption of high-grade products, with tier 2 and tier 3 cities being

the primary consumers of medium and low-grade products.

The consumption structure of bedding products has changed with the improvement of people’s

living standards. The consumption proportion of high-end products, mid-range products and low-end

products changed from approximately 4%, 60% and 36% in 2004 to 8.9%, 60% and 31.1% in 2009. The

proportion of high-end products is climbing, that of low-end products is falling, with mid-range products

remaining dominant. The consumption of bedding products is becoming more and more inclined to mid-

range and high-end. From 2010 to 2012, the CAGR retail sales of high-end, and low-end products are

estimated to be 27.7%, 27.4% and 19.2% respectively.

Currently, bedding products featuring innovative designs are increasingly favored by consumers.

Featured brand design, high quality, coziness and health (i.e. sleeping conditions) are the main trends of

bedding products in the future. When two brands are equal in quality and coziness, the fine design and

individuality of bedding products will decide which brand will gain the advantage in the market.

Emerging Western classical style design elements are recognised increasingly by Chinese families,

and these bedding products are especially favored by young consumers as symbols of high quality and

luxury. Apart from this European style design, which plays a considerable role in the domestic bedding

products market, the new colors and new designs of domestic brands is growing swiftly. The industry

considers design innovation and brand establishment as the major methods to keep a firm foothold in the

market.

Changes in the consumption of bedding products are first reflected in the number and patterns of

bedding products. Common varieties have increased from the traditional four pieces — quilt, mattress

pad, quilt cover and pillow, to accessories like bed covers and skirt covers, and to the new flexible set

of long and short pillow covers. Now, there are five-piece, six-piece, and even eight-piece and ten-piece

sets. Consumers tend to like an elegant and natural design in their bedding product such as matching/

complementary colors and coordination with the entire room. On the other hand, the major function of

INDUSTRY OVERVIEW

– 73 –

bedding products has shifted from preservation of warmth to health care. Functional products now

swarm the market. Instead of the single sheet warmth preserving bedding products like duvet and dacron

hollow cotton that have been snubbed recently, new bedding products with the function of health care

use pure cotton fabrics, and most stuffing and fabrics are indicated to be antimicrobial and

mitedispelling.

Competitive environment of the PRC bedding products market

Currently there are more than 1,000 enterprises specialised in the manufacturing of bedding

products. They are mainly located in Guangdong, Shanghai, Shandong, Zhejiang and Jiangsu. The

bedding product market is characterized by strong regionality, which means many brands are well

known in certain regions or are locally dominant but are unknown in other areas. According to

Euromonitor, the top 5 bedding products enterprises accounted for about 6.3%, 6.3%, 6.4% and 6.8% for

2006, 2007, 2008 and 2009 respectively in terms of retail sales value in the PRC bedding products

market. For the year of 2009, our Company is ranked by Euromonitor as the eighth largest bedding

products manufacturer in terms of retail sales value in the PRC bedding product market, accounting for

0.4% of the total market share.

Large bedding products enterprises mainly adopt self-operation stores plus franchised outlets as

their marketing channel, while the major distribution channels of bedding products still involve

traditional retail channels such as hypermarkets, bedding product specialists, supermarkets and

department stores where customers can test the products. Emerging retail channels like online shopping

and TV shopping do not have the edge in bedding products sales in spite of their convenience. This is

because consumers are not able to check the quality of the products, not to mention the fact that color

variation exists between graphics displayed on the Internet and TV which do not always align with the

coloration of the real products. The chart below illustrates the retail channel contribution of total

bedding product sales value from 2006 to 2009.

INDUSTRY OVERVIEW

– 74 –

Euromonitor report — China Bedding and Home Textile Market Analysis

The chart below illustrates the contribution of bedding products distribution channels by retail

sales value of bedding products manufacturers from 2006 to 2009.

Euromonitor report — China Bedding and Home Textile Market Analysis

INDUSTRY OVERVIEW

– 75 –

With decades of development, the PRC bedding products market has changed significantly. Some

relatively strong domestic brands have emerged while foreign brands have started to enter the Chinese

market, which mainly focus on high-end demographics. The chart below illustrates the market share of

domestic bedding brands and foreign bedding brands by retail sales value from 2006 to 2009.

Euromonitor report — China Bedding and Home Textile Market Analysis

Compared with other industries, the PRC bedding products industry is still in a state of ‘‘large

industry, but small enterprises’’ with a very fragmented market. Most famous brands still distribute their

products regionally rather than nationwide. Some adequately funded enterprises have completed their

preliminary layout of retail outlets across the country, aiming to achieve nationwide brand status and

popularity. Other local brands have achieved strong sales results and are now striving to extend their

markets to other provinces and municipalities.

INDUSTRY OVERVIEW

– 76 –

At present, the PRC bedding products retail industry has not been affected seriously by the

financial crisis, and remains steady in spite of heavy export pressure. The chart below illustrates the

proportion of bedding products produced in the PRC for domestic consumption and exports by sales

value from 2006 to 2009.

Euromonitor report — China Bedding and Home Textile Market Analysis

INDUSTRY OVERVIEW

– 77 –

Related Documents