I NTANGIBLES , INVESTMENT, AND EFFICIENCY Nicolas Crouzet 1 Janice Eberly 2 1 Kellogg School of Management, Northwestern University 2 Kellogg School of Management, Northwestern University & NBER TPRI competition conference July 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTANGIBLES, INVESTMENT, AND EFFICIENCY

Nicolas Crouzet1 Janice Eberly2

1Kellogg School of Management, Northwestern University

2Kellogg School of Management, Northwestern University & NBER

TPRI competition conferenceJuly 2018

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:

1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups

2. growth in productivity, particularly among largest firmsFoster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

OVERVIEW

Two salient macro trends, since mid-1990’s

- Increasing business concentrationGutierrez and Philippon (2018) (”market power”); Autor et al. (2017)(”productivity gap”)

- Low (physical) investment, relative to QGutierrez and Philippon (2017), Alexander and Eberly (2017), Fernald et al.(2017)

This paper: explore a joint explanation for these two trends

- Productivity gains among industry leaders, associated with shift ininvestment toward non-physical (intangible) capital

- Illustration in the retail sector:1. stable markups2. growth in productivity, particularly among largest firms

Foster, Haltiwanger & Krizan (2006)

3. closely correlated growth in intangible capital

1 / 11

WHY RETAIL?HHI OF SALES, COMPUSTAT US FIRMS

.12

.14

.16

.18

1990 1995 2000 2005 2010 2015

All Excluding retail Excluding retail and oil & gas

Sales HHI in retail: .14 in 1990; .36 in 2015.Oil & gas

2 / 11

THE INVESTMENT GAP IN RETAIL

-.15

-.1

-.05

0

1990 1995 2000 2005 2010 2015year

point estimate +/- 2 s.e.

(I/K)i,t = αi + δt + X′i,tβ + εi,t

Xi,t ≡ ( Qi,t−1, (CF/K)i,t−1 )′

3 / 11

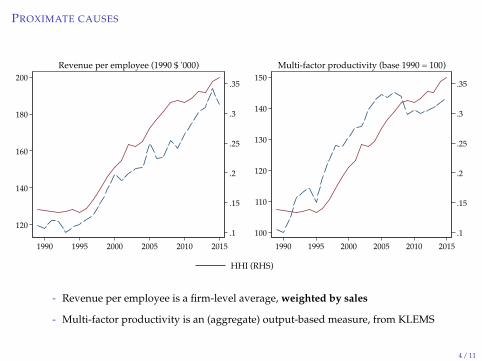

PROXIMATE CAUSES

4 / 11

PROXIMATE CAUSES

- Increasing market power of incumbents?

- Productivity gains, especially among industry leaders?

=⇒ rising concentration

4 / 11

PROXIMATE CAUSES

.1

.15

.2

.25

.3

.35

1.3

1.35

1.4

1.45

1.5

1990 1995 2000 2005 2010 2015

Markup (LHS) HHI (RHS)

Markup ≡ SalesCost of goods sold

4 / 11

PROXIMATE CAUSES

- Increasing market power of incumbents?

- Productivity gains, especially among industry leaders?

=⇒ rising concentration

4 / 11

PROXIMATE CAUSES

- Increasing market power of incumbents?

- Productivity gains, especially among industry leaders?

=⇒ rising concentration

4 / 11

PROXIMATE CAUSES

.1

.15

.2

.25

.3

.35

120

140

160

180

200

1990 1995 2000 2005 2010 2015

Revenue per employee (1990 $ '000)

.1

.15

.2

.25

.3

.35

100

110

120

130

140

150

1990 1995 2000 2005 2010 2015

Multi-factor productivity (base 1990 = 100)

HHI (RHS)

- Revenue per employee is a firm-level average, weighted by sales

- Multi-factor productivity is an (aggregate) output-based measure, from KLEMS

4 / 11

WHAT HAPPENED IN RETAIL?

.1

.15

.2

.25

.3

.35

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1990 1995 2000 2005 2010 2015

Inventory coverage (months, LHS) HHI (RHS)

- 1990’s & early 2000’s: faster payment systems, more accurate pricing, betterinventory management (Walmart)

Foster, Haltiwanger and Krizan (2006)

- late 2000’s & early 2010’s: development of online retail platforms and distributedretail systems (Amazon)

- requires intangible “know-how”, not only investment in new physical capital

5 / 11

WHAT HAPPENED IN RETAIL?

.1

.15

.2

.25

.3

.35

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1990 1995 2000 2005 2010 2015

Inventory coverage (months, LHS) HHI (RHS)

- 1990’s & early 2000’s: faster payment systems, more accurate pricing, betterinventory management (Walmart)

Foster, Haltiwanger and Krizan (2006)

- late 2000’s & early 2010’s: development of online retail platforms and distributedretail systems (Amazon)

- requires intangible “know-how”, not only investment in new physical capital

5 / 11

WHAT HAPPENED IN RETAIL?

.1

.15

.2

.25

.3

.35

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1990 1995 2000 2005 2010 2015

Inventory coverage (months, LHS) HHI (RHS)

- 1990’s & early 2000’s: faster payment systems, more accurate pricing, betterinventory management (Walmart)

Foster, Haltiwanger and Krizan (2006)

- late 2000’s & early 2010’s: development of online retail platforms and distributedretail systems (Amazon)

- requires intangible “know-how”, not only investment in new physical capital

5 / 11

PRODUCTIVITY VS. MARKET POWER

Jeff Bezos (09/28/2011)

6 / 11

INTANGIBLES AND PRODUCTIVITYSECTOR-WIDE

5

10

15

20

120

140

160

180

200

1990 1995 2000 2005 2010 2015

Revenue per employee (1990 $ '000, LHS)Intangible share of total assets (%, RHS)

Acquisition flows

7 / 11

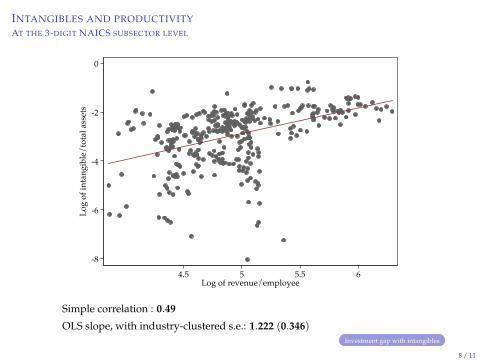

INTANGIBLES AND PRODUCTIVITYAT THE 3-DIGIT NAICS SUBSECTOR LEVEL

-8

-6

-4

-2

0

Log

of in

tang

ible

/tot

al a

sset

s

4.5 5 5.5 6Log of revenue/employee

Simple correlation : 0.49

OLS slope, with industry-clustered s.e.: 1.222 (0.346)Investment gap with intangibles

8 / 11

INTANGIBLES AND PRODUCTIVITYAT THE 3-DIGIT NAICS SUBSECTOR LEVEL — INCLUDING CAPITALIZED R&D

-8

-6

-4

-2

0

Log

of in

tang

ible

/tot

al a

sset

s

4.5 5 5.5 6Log of revenue/employee

Simple correlation : 0.57

OLS slope, with industry-clustered s.e.: 1.432 (0.320)Investment gap with intangibles

9 / 11

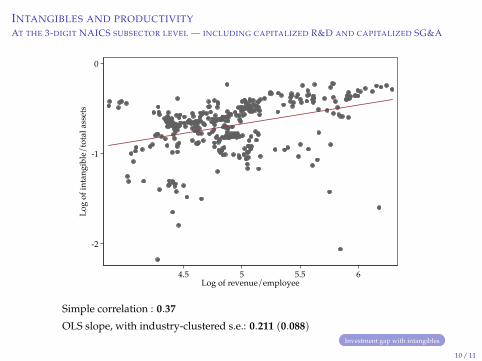

INTANGIBLES AND PRODUCTIVITYAT THE 3-DIGIT NAICS SUBSECTOR LEVEL — INCLUDING CAPITALIZED R&D AND CAPITALIZED SG&A

-2

-1

0

Log

of in

tang

ible

/tot

al a

sset

s

4.5 5 5.5 6Log of revenue/employee

Simple correlation : 0.37

OLS slope, with industry-clustered s.e.: 0.211 (0.088)Investment gap with intangibles

10 / 11

CONCLUSION

In the US retail sector

- Higher concentration

- Large productivity gains, esp. among industry leaders

- Despite this fact, physical investment remains low

- But higher productivity strongly correlated with intangible investment

Unanswered questions

- How widespread is this phenomenon, beyond retail?

- Does intangible investment only lead to productivity gains, or could itserve to increase market power?

brand value

11 / 11

CONCLUSION

In the US retail sector

- Higher concentration

- Large productivity gains, esp. among industry leaders

- Despite this fact, physical investment remains low

- But higher productivity strongly correlated with intangible investment

Unanswered questions

- How widespread is this phenomenon, beyond retail?

- Does intangible investment only lead to productivity gains, or could itserve to increase market power?

brand value

11 / 11

PLAN

MORE

Alexander, L. and J. Eberly (2017). Investment hollowing out. IMF EconomicReview forthcoming.

Autor, D., D. Dorn, L. F. Katz, C. Patterson, and J. V. Reenen (2017).Concentrating on the fall of the labor share. American EconomicReview 107(5), 180–185.

Fernald, J. G., R. E. Hall, J. H. Stock, and M. W. Watson (2017). Thedisappointing recovery of output after 2009. Brookings Papers on EconomicActivity.

Gutierrez, G. and T. Philippon (2017). Investment-less growth: An empiricalinvestigation. Brookings Papers on Economic Activity forthcoming.

Gutierrez, G. and T. Philippon (2018). Declining competition and investmentin the us. Technical report, NBER working paper.

CONCENTRATION IN THE OIL & GAS SECTORHHI OF SALES, COMPUSTAT US FIRMS

.12

.14

.16

.18

1990 1995 2000 2005 2010 2015

All Excl. oil and gas Excl. retail and oil & gas

Concentration in retail

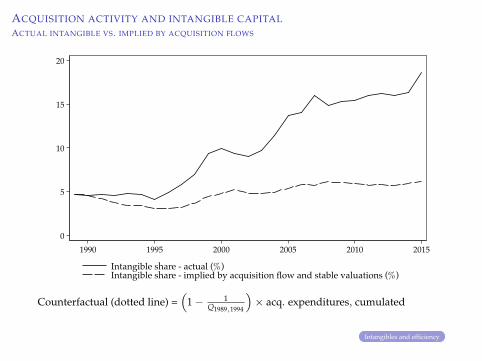

ACQUISITION ACTIVITY AND INTANGIBLE CAPITALACTUAL INTANGIBLE VS. IMPLIED BY ACQUISITION FLOWS

0

5

10

15

20

1990 1995 2000 2005 2010 2015

Intangible share - actual (%)Intangible share - implied by acquisition flow and stable valuations (%)

Counterfactual (dotted line) =(

1− 1Q1989,1994

)× acq. expenditures, cumulated

Intangibles and efficiency

INTANGIBLES AND THE INVESTMENT GAPTIME EFFECTS IN INVESTMENT/Q REGRESSION, INCLUDE INTANGIBLE INVESTMENT

-.15

-.1

-.05

0

1990 1995 2000 2005 2010 2015year

Physical investmentPhysical plus intangible investment, with +/- 2 s.e. band

Intangible investment = net change in balance sheet intangibles + R&D + advertising

Intangibles and productivity

Related Documents