Today’s Regulatory Landscape: Complying with Multiple Regulations Simultaneously Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Global Market Intelligence. Not for distribution to the public. Copyright © 2016 by S&P Global Market Intelligence. All rights reserved. Hans Crockett Vice President Innovation and Thought Leadership Global Risk Services Munich, May 10 th , 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Today’s Regulatory Landscape: Complying with Multiple Regulations Simultaneously

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Global Market

Intelligence. Not for distribution to the public. Copyright © 2016 by S&P Global Market Intelligence. All rights reserved.

Hans Crockett

Vice President

Innovation and Thought Leadership

Global Risk Services

Munich, May 10th, 2016

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Overview

• The global regulatory landscape and regulatory convergence

• Regulatory reporting: Common data challenges

• Risk-focused regulations: Overview of Basel III, Solvency II, and

IFRS 9

• Staying up-to-date with regulatory developments

• Appendix: Relevant S&P Global Market Intelligence offerings

2

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

The Global Regulatory Landscape And Regulatory Convergence

3

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

A Sea Of Acronyms And Expressions

EMIR

CVA

FINREP COREP

MIFID

II

RWA

CCP

CRD IV CCAR

UCITS MAR

MAD

FASB

AIFMD MIFIR

SIFI

"Regulatory Arbitrage"

"Substituted Compliance"

Solvency

II

Basel

II & III

IFRS

FATCA

4

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Conscious efforts of the G20, FSB, CESR, EBA-ESMA-EIOPA, BCBS, IAIS etc.,

Main themes: Risk-based capital, stress testing, credit risk assessments, transparency,

independent multifactor pricing, macroeconomic scenarios, provisions, liquidity

management

• Risk-based capital adequacy and reporting – Basel, Solvency II, IORP II, CCAR, Swiss Solvency Test for Insurers

• Scenarios and stress testing – Basel, CCAR, DFAST, Solvency II (Pillar 2 / ORSA), AIFMD, UCITS IV/V, IFRS 9

• Systematic credit quality assessments – Basel, Solvency II, IORP II, AIFMD, IFRS, CRA3

• Credit-sensitive valuations – IFRS 13, Basel, Solvency II

• Provisions against expected losses – IFRS 9, FASB’s CECL

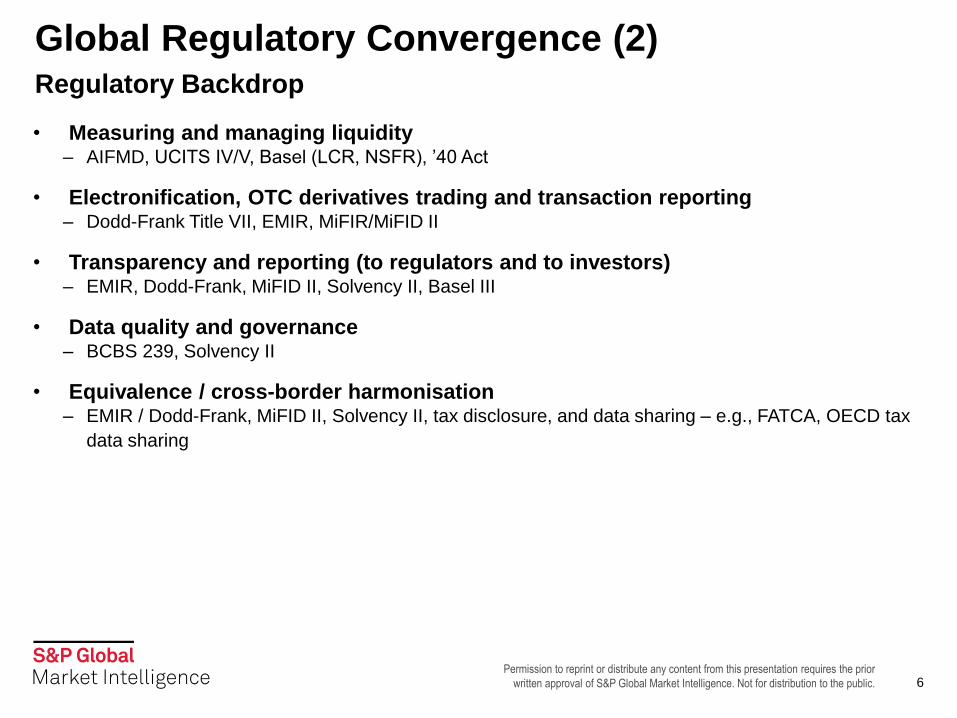

Global Regulatory Convergence (1) Regulatory Backdrop

5

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Measuring and managing liquidity – AIFMD, UCITS IV/V, Basel (LCR, NSFR), ’40 Act

• Electronification, OTC derivatives trading and transaction reporting – Dodd-Frank Title VII, EMIR, MiFIR/MiFID II

• Transparency and reporting (to regulators and to investors) – EMIR, Dodd-Frank, MiFID II, Solvency II, Basel III

• Data quality and governance – BCBS 239, Solvency II

• Equivalence / cross-border harmonisation – EMIR / Dodd-Frank, MiFID II, Solvency II, tax disclosure, and data sharing – e.g., FATCA, OECD tax

data sharing

Global Regulatory Convergence (2) Regulatory Backdrop

6

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Global banking regulation – Basel II (including ICAAP), III, IV (soon) and regional implementations (e.g., CRD IV in the EU);

DFAST, CCAR, EBA stress testing and structure of banking operations, Swiss “too big to fail” regime

– General themes: Risk-based capital, scenarios and stress testing, funding provisions, liquidity

provisions, data governance

• Global OTC derivatives reform – EMIR, Dodd-Frank Title VII and national derivative trading, trade reporting and clearing regimes

– General themes: Transparency, electronification, central clearing, collateralisation and margining

• Global insurance regulation – EU’s Solvency II, China’s C-ROSS, South Africa’s SAM, Australia’s Prudential Standards, Swiss

solvency test

– General themes: Risk-based capital requirements, internal governance and supervision, data

governance, reporting

• Accounting standards – IFRS 9, IFRS 13, FASB’s CECL

– General themes: Credit-sensitive valuation of derivatives, provisions against credit impairment, asset

classifications

Families Of Regulation (1) Regulatory Backdrop

7

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

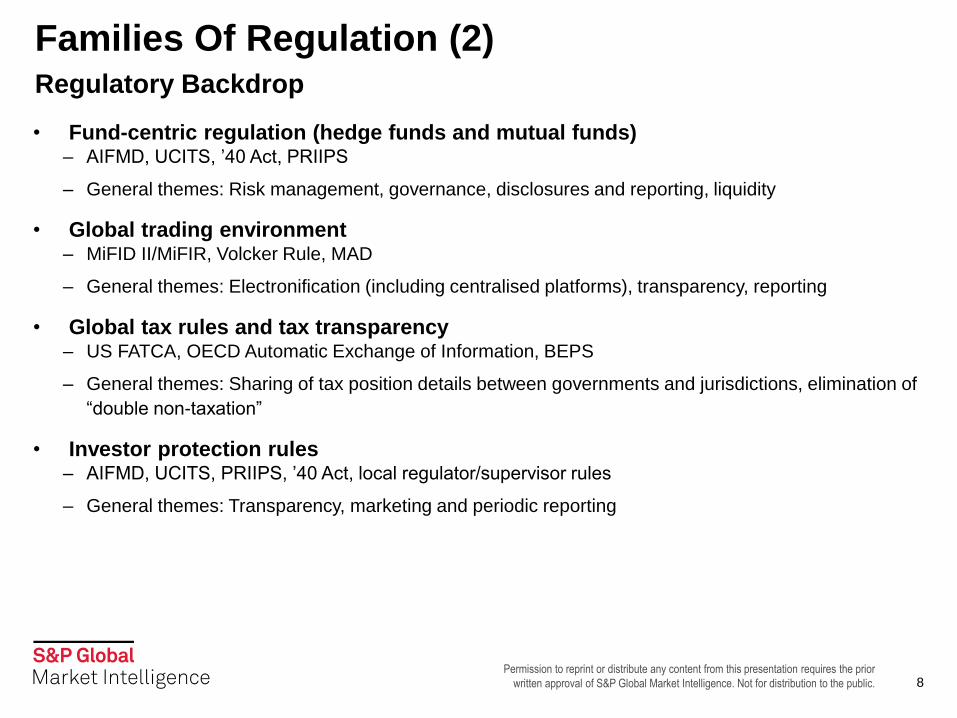

• Fund-centric regulation (hedge funds and mutual funds) – AIFMD, UCITS, ’40 Act, PRIIPS

– General themes: Risk management, governance, disclosures and reporting, liquidity

• Global trading environment – MiFID II/MiFIR, Volcker Rule, MAD

– General themes: Electronification (including centralised platforms), transparency, reporting

• Global tax rules and tax transparency – US FATCA, OECD Automatic Exchange of Information, BEPS

– General themes: Sharing of tax position details between governments and jurisdictions, elimination of

“double non-taxation”

• Investor protection rules – AIFMD, UCITS, PRIIPS, ’40 Act, local regulator/supervisor rules

– General themes: Transparency, marketing and periodic reporting

Families Of Regulation (2) Regulatory Backdrop

8

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Regulatory Reporting: Common Data Challenges

9

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

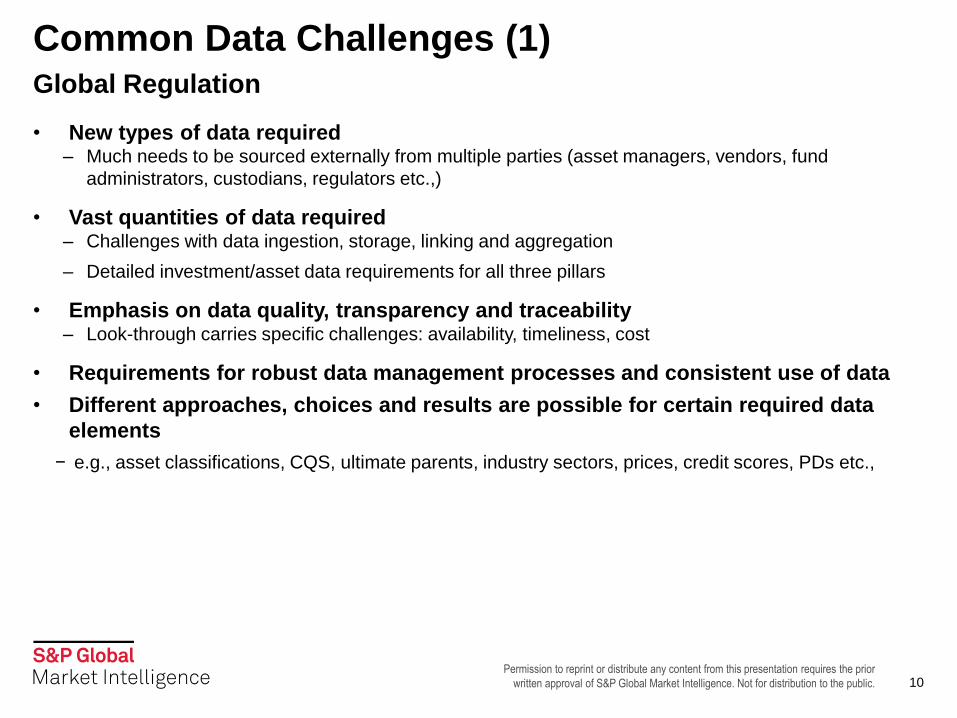

• New types of data required – Much needs to be sourced externally from multiple parties (asset managers, vendors, fund

administrators, custodians, regulators etc.,)

• Vast quantities of data required – Challenges with data ingestion, storage, linking and aggregation

– Detailed investment/asset data requirements for all three pillars

• Emphasis on data quality, transparency and traceability – Look-through carries specific challenges: availability, timeliness, cost

• Requirements for robust data management processes and consistent use of data

• Different approaches, choices and results are possible for certain required data

elements

− e.g., asset classifications, CQS, ultimate parents, industry sectors, prices, credit scores, PDs etc.,

Common Data Challenges (1) Global Regulation

10

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Licensing and redistribution issues for certain data types (e.g., credit ratings,

evaluated pricing, CUSIPs)

• Where some data is “free”/in the public domain, there can be misconceptions

− Credit ratings IP, instrument identifier IP, consultation vs databasing, challenges gathering and

maintaining data up-to-date, challenges mapping to correct entities and securities

• Management’s decisions are impacted by data and how these change

− Credit ratings, classifications, ownership/corporate hierarchies, pricing availability

Common Data Challenges (2) Global Regulation

11

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Basel III

12

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Basel Regulation began in 1988 and has continued to evolve:

− BASEL I (1988): Defined Tier 1 and Tier 2 capital, introduced risk-weighted assets and the solvency

ratio. Focused mainly on credit risk (risk-weighted approach); market risk (VaR) model introduced in

1996

− BASEL II (2006): Introduced the 3-Pillar approach: Capital requirements, supervisory review and market

discipline. Major changes related to credit risk (Internal Ratings-Based Approach, IRB) and counterparty

risk on OTC derivatives (potential future exposure, IRB approach)

− BASEL “2.5” (2009): Revision of Basel II norms. Introduced stressed VaR, the Incremental Risk Charge

[IRC] to capture default and credit migration risk, and the Comprehensive Risk Measure [CRM] to

capture correlation risk. Introduced standardised charges for securitisations

− BASEL III (2010-11): Introduced multiple new components, including the addition of CVA for

counterparty risk

− BASEL IV (2013): A Fundamental Review of the Trading Book (FRTB) has been proposed. However, it

will be at least five years before this is implemented

• Today, Basel II rules are effectively still in place for the banking book (via the

Standardised and IRB approaches), while Basel 2.5 and III are replacing capital

requirements for the trading book and OTC Derivatives

Overview Of Basel Regulation: From 1988 To Today

13

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

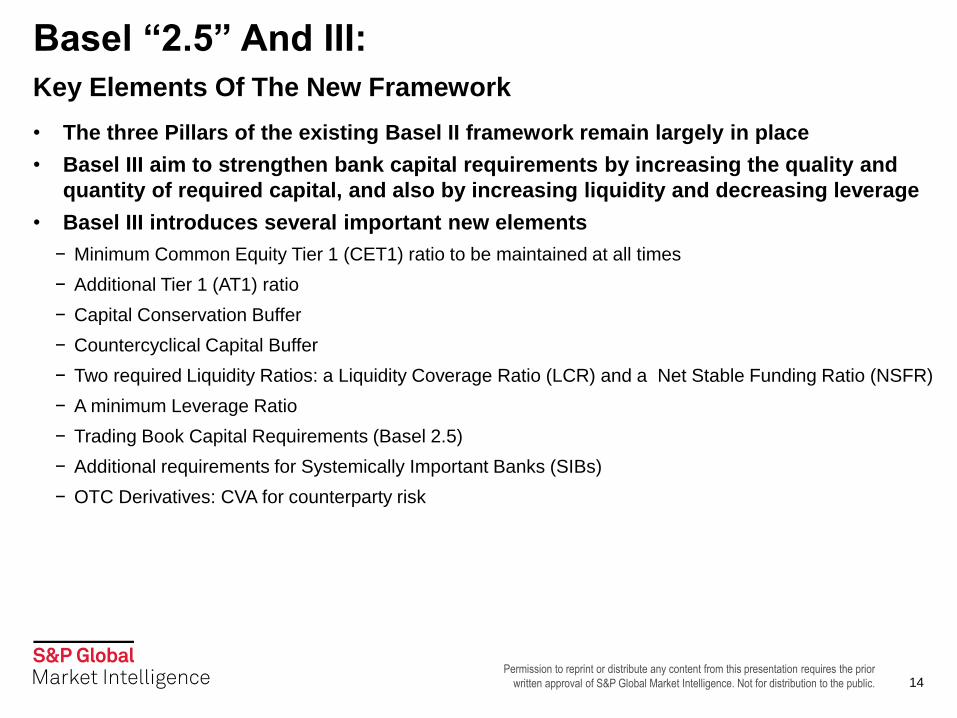

• The three Pillars of the existing Basel II framework remain largely in place

• Basel III aim to strengthen bank capital requirements by increasing the quality and

quantity of required capital, and also by increasing liquidity and decreasing leverage

• Basel III introduces several important new elements

− Minimum Common Equity Tier 1 (CET1) ratio to be maintained at all times

− Additional Tier 1 (AT1) ratio

− Capital Conservation Buffer

− Countercyclical Capital Buffer

− Two required Liquidity Ratios: a Liquidity Coverage Ratio (LCR) and a Net Stable Funding Ratio (NSFR)

− A minimum Leverage Ratio

− Trading Book Capital Requirements (Basel 2.5)

− Additional requirements for Systemically Important Banks (SIBs)

− OTC Derivatives: CVA for counterparty risk

Basel “2.5” And III:

Key Elements Of The New Framework

14

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• The CRD IV package transposes the new global standards on bank capital

(commonly known as the “Basel III agreement”) into the EU legal framework via a

regulation and a directive that entered into force on July 17th, 2013

• Banks started reporting under the new framework in January 1st, 2014. However,

some of the new provisions are being phased out to 2019

• The European Banking Authority (EBA) plays a key role in the implementation of the

new Basel regulatory framework in the European Union. Particularly, the EBA is now

mandated to produce a number of Binding Technical Standards (BTS), guidelines

and reports for the implementation of the CRD IV package

• In Europe Basel III will apply to all banks – more than 8,300 institutions

When Will Basel III Be Implemented In Europe?

15

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

The Basel Committee on Banking Supervision (2013) proposed a set of data-related principles aimed

at strengthening significantly risk management capabilities across the banking sector:

• Governance and infrastructure

− Governance

− Data Architecture and IT Infrastructure

• Risk data aggregation

− Accuracy and integrity

− Completeness

− Timeliness

− Adaptability

• Risk reporting

− Accuracy

− Comprehensiveness

− Clarity

− Frequency

− Distribution

• Supervisory review, tools and cooperation

These broad principles can readily

be extended to any kind of firms

Source: BCBS (January 2013).

“BCBS 239”

The Basel Committee Risk Data Principles

16

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Solvency II

17

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

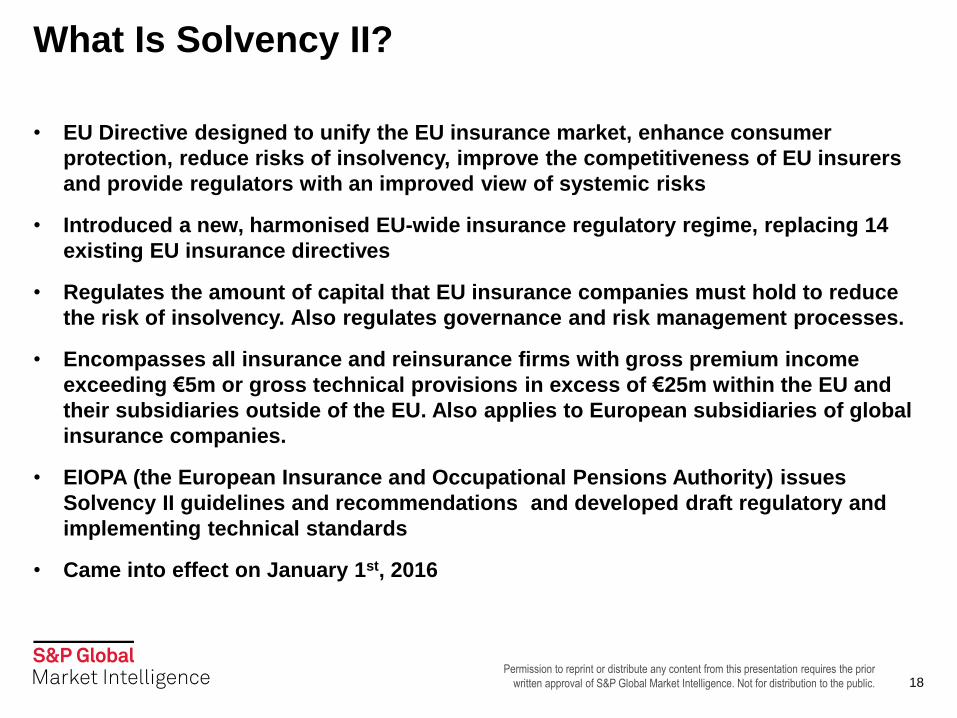

• EU Directive designed to unify the EU insurance market, enhance consumer

protection, reduce risks of insolvency, improve the competitiveness of EU insurers

and provide regulators with an improved view of systemic risks

• Introduced a new, harmonised EU-wide insurance regulatory regime, replacing 14

existing EU insurance directives

• Regulates the amount of capital that EU insurance companies must hold to reduce

the risk of insolvency. Also regulates governance and risk management processes.

• Encompasses all insurance and reinsurance firms with gross premium income

exceeding €5m or gross technical provisions in excess of €25m within the EU and

their subsidiaries outside of the EU. Also applies to European subsidiaries of global

insurance companies.

• EIOPA (the European Insurance and Occupational Pensions Authority) issues

Solvency II guidelines and recommendations and developed draft regulatory and

implementing technical standards

• Came into effect on January 1st, 2016

What Is Solvency II?

18

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Insurers must hold capital against a range of risks, not just insurance risks

• Insurers are required to identify, measure and proactively manage risks; all risks and

their interactions must be considered

• Supervisory review process

• Greater public disclosure and reporting to regulators (QRTs, FSR, SFCR, ORSA, and

National Specific Templates)

• 2016 reporting timelines:

− Insurers with December 31st, year-ends must file their first quarterly reports by May 26th, 2016

− The first annual reports are due May 20th, 2016 (based on 2015 data)

− Reporting deadlines in the first year are longer and then reduce every year for three years.

− Some smaller firms can apply for certain reporting exemptions.

What Does Solvency II Involve?

19

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

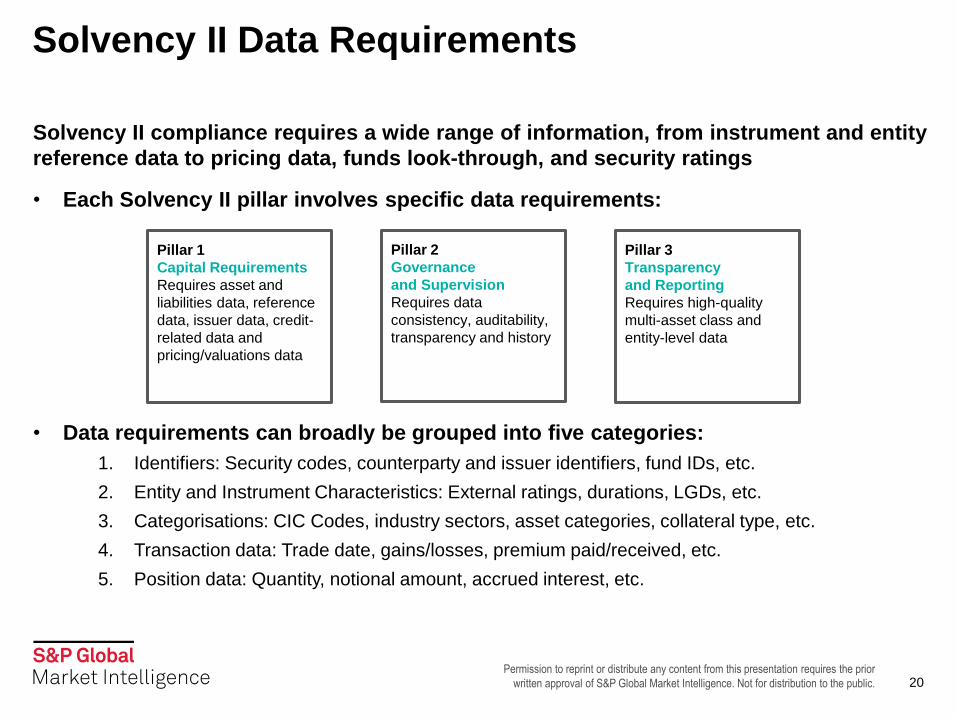

Solvency II compliance requires a wide range of information, from instrument and entity

reference data to pricing data, funds look-through, and security ratings

• Each Solvency II pillar involves specific data requirements:

• Data requirements can broadly be grouped into five categories:

1. Identifiers: Security codes, counterparty and issuer identifiers, fund IDs, etc.

2. Entity and Instrument Characteristics: External ratings, durations, LGDs, etc.

3. Categorisations: CIC Codes, industry sectors, asset categories, collateral type, etc.

4. Transaction data: Trade date, gains/losses, premium paid/received, etc.

5. Position data: Quantity, notional amount, accrued interest, etc.

Solvency II Data Requirements

Pillar 1

Capital Requirements

Requires asset and

liabilities data, reference

data, issuer data, credit-

related data and

pricing/valuations data

Pillar 2

Governance

and Supervision

Requires data

consistency, auditability,

transparency and history

Pillar 3

Transparency

and Reporting

Requires high-quality

multi-asset class and

entity-level data

20

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Solvency II And The Data Quality Challenge

• The data reported needs to be not only accurate, but also consistent with that used by

insurers for their Solvency Capital Requirement (SCR) and Minimum Capital Requirement

(MCR) calculations

• Solvency II requires asset data to be ‘complete’, ‘accurate’ and ‘appropriate’; data quality

assurance processes will be monitored by insurers and their supervisors

• Data has to meet the same quality standards irrespective of whether it is sourced internally

or externally. Insurers will want to be sure that the data obtained from their asset

managers, fund administrators and data vendors meets the required standards

• Data consistency may be challenging to achieve because different market data sources

can return different values for the same data field (although each can be accurate in its

own way)

21

Source:“CEIOPS’ Advice for Level 2 Implementing Measures on Solvency II: Technical Provisions – Article 86 f, Standards for Data Quality”, CEIOPS, October 2009.

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

IFRS 9

22

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

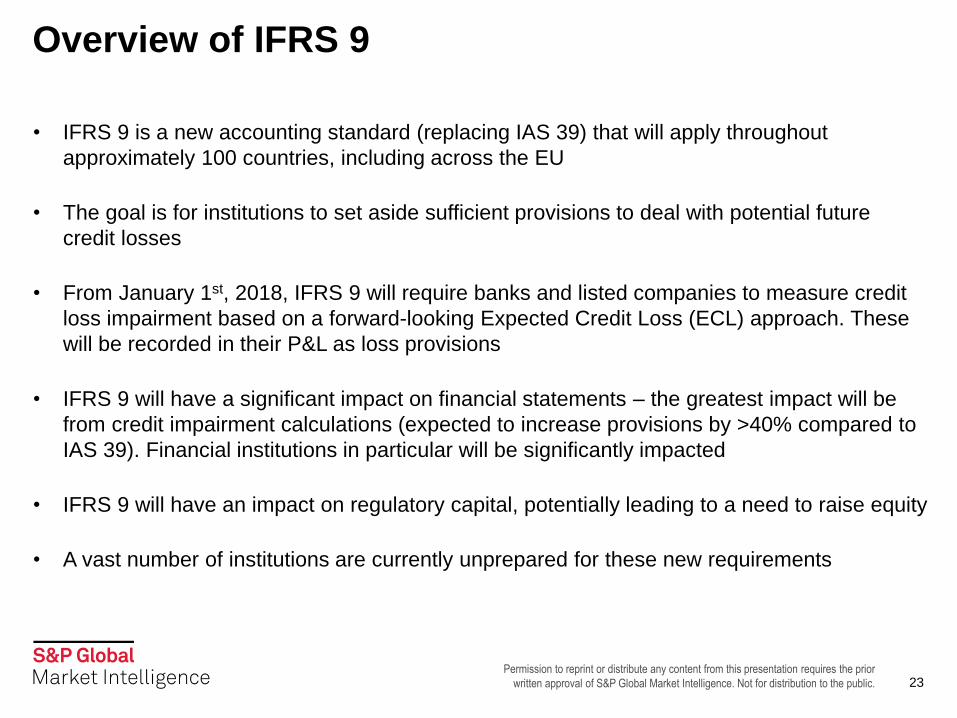

Overview of IFRS 9

• IFRS 9 is a new accounting standard (replacing IAS 39) that will apply throughout

approximately 100 countries, including across the EU

• The goal is for institutions to set aside sufficient provisions to deal with potential future

credit losses

• From January 1st, 2018, IFRS 9 will require banks and listed companies to measure credit

loss impairment based on a forward-looking Expected Credit Loss (ECL) approach. These

will be recorded in their P&L as loss provisions

• IFRS 9 will have a significant impact on financial statements – the greatest impact will be

from credit impairment calculations (expected to increase provisions by >40% compared to

IAS 39). Financial institutions in particular will be significantly impacted

• IFRS 9 will have an impact on regulatory capital, potentially leading to a need to raise equity

• A vast number of institutions are currently unprepared for these new requirements

23

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

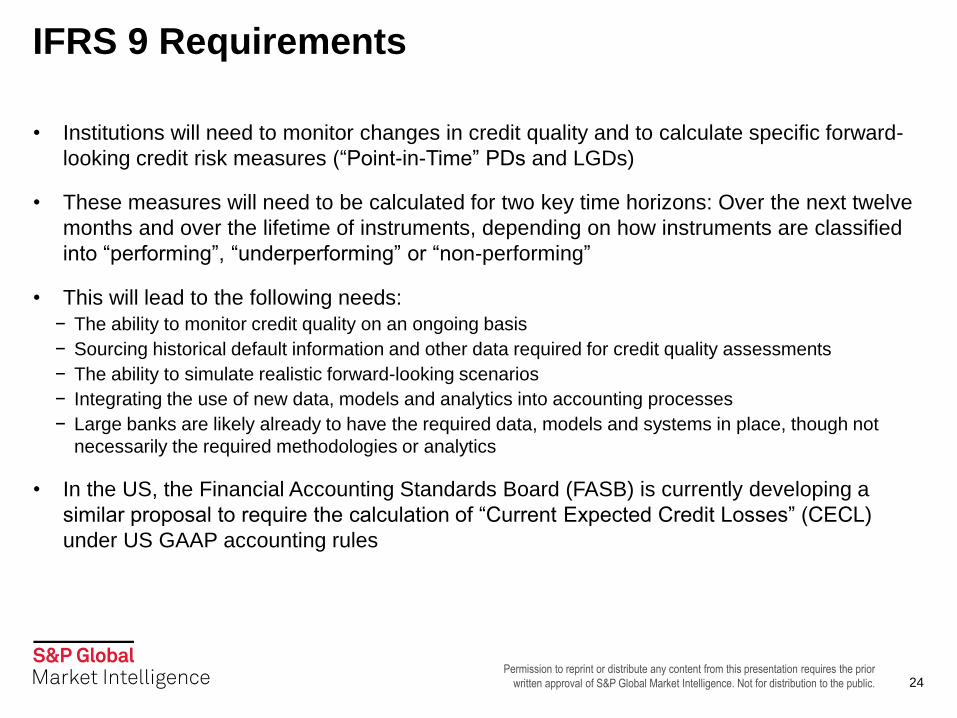

IFRS 9 Requirements

• Institutions will need to monitor changes in credit quality and to calculate specific forward-

looking credit risk measures (“Point-in-Time” PDs and LGDs)

• These measures will need to be calculated for two key time horizons: Over the next twelve

months and over the lifetime of instruments, depending on how instruments are classified

into “performing”, “underperforming” or “non-performing”

• This will lead to the following needs:

− The ability to monitor credit quality on an ongoing basis

− Sourcing historical default information and other data required for credit quality assessments

− The ability to simulate realistic forward-looking scenarios

− Integrating the use of new data, models and analytics into accounting processes

− Large banks are likely already to have the required data, models and systems in place, though not

necessarily the required methodologies or analytics

• In the US, the Financial Accounting Standards Board (FASB) is currently developing a

similar proposal to require the calculation of “Current Expected Credit Losses” (CECL)

under US GAAP accounting rules

24

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

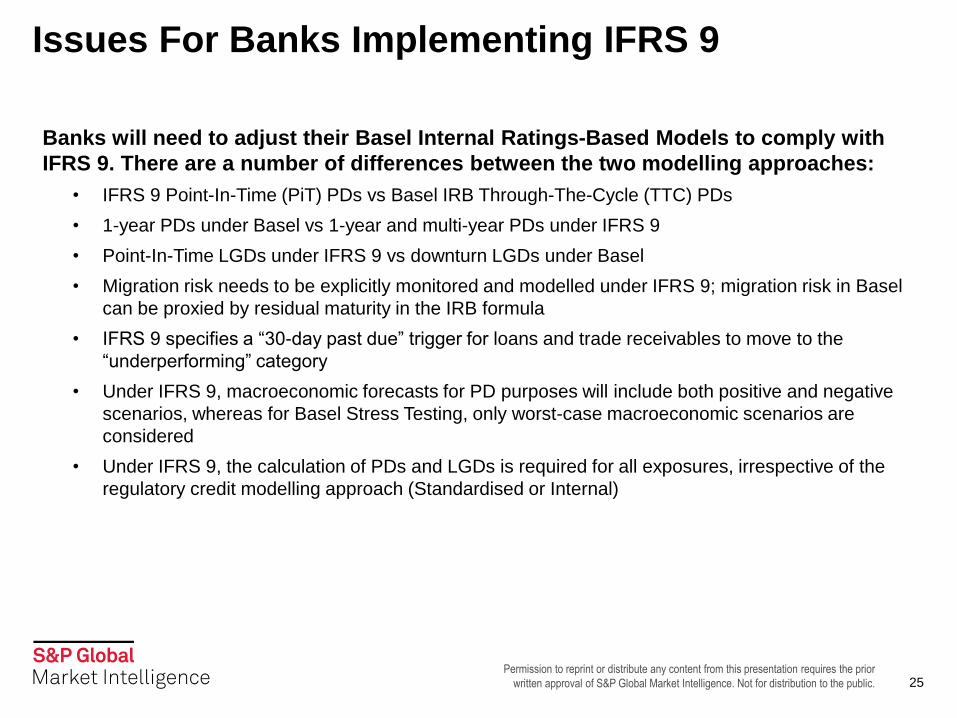

Issues For Banks Implementing IFRS 9

Banks will need to adjust their Basel Internal Ratings-Based Models to comply with

IFRS 9. There are a number of differences between the two modelling approaches:

• IFRS 9 Point-In-Time (PiT) PDs vs Basel IRB Through-The-Cycle (TTC) PDs

• 1-year PDs under Basel vs 1-year and multi-year PDs under IFRS 9

• Point-In-Time LGDs under IFRS 9 vs downturn LGDs under Basel

• Migration risk needs to be explicitly monitored and modelled under IFRS 9; migration risk in Basel

can be proxied by residual maturity in the IRB formula

• IFRS 9 specifies a “30-day past due” trigger for loans and trade receivables to move to the

“underperforming” category

• Under IFRS 9, macroeconomic forecasts for PD purposes will include both positive and negative

scenarios, whereas for Basel Stress Testing, only worst-case macroeconomic scenarios are

considered

• Under IFRS 9, the calculation of PDs and LGDs is required for all exposures, irrespective of the

regulatory credit modelling approach (Standardised or Internal)

25

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Interactions Between Regulations

• Addressing multiple regulations simultaneously will require robust data infrastructures that

provide transparent and auditable outputs. Associated technology costs are likely to

increase

• Common data requirements exist across multiple regulations (e.g., LEIs and independent

valuations across Solvency II, EMIR, CRD IV, AIFMD, Dodd-Frank Title VII etc.,)

• Basel III and Solvency II both alter the preferred mix of bonds, including asset-backed

bonds

• IFRS 9 and CECL Credit Impairment provisions interact with Basel requirements

• EMIR will require highly-quality collateral (e.g., cash and highly-rated bonds)

• AIFMD, CRD IV, Dodd-Frank and Solvency II set similar conditions on retained ownership

of securitised instruments

• MiFID II, Dodd-Frank Title VII and EMIR will lead to new independent sources of pricing for

certain instruments (including specific OTCs)

• Strong interactions between Insurers and the Fund Management industry, favouring

“transparent” funds that are UCITS and AIFMD compliant

• CRA3 has implications on credit quality assessment methods throughout all types of

institutions that use credit ratings, including the fund management industry

26

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Staying Up-To-Date With Regulatory Developments

27

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

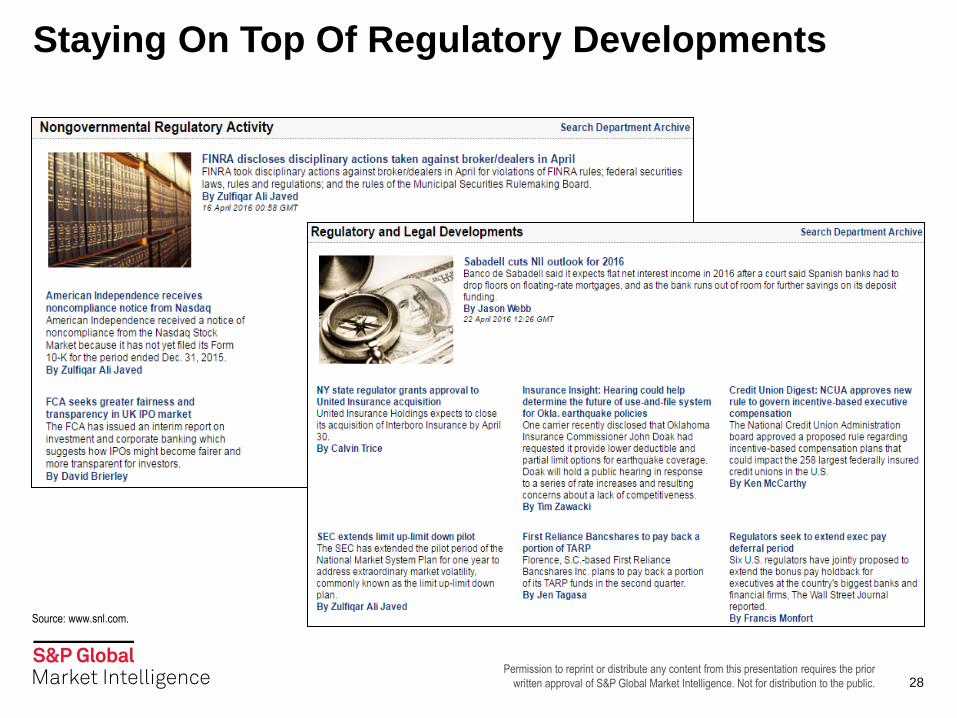

Staying On Top Of Regulatory Developments

Source: www.snl.com.

28

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Regulatory News Commentary

29

Source: www.snl.com.

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Regulatory Profiles For Selected Markets

30

Source: www.snl.com.

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Appendix: Relevant S&P Global Market

Intelligence Offerings

31

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Asset and Entity Classifications and Identification Codes: multiple security and entity

identification and classification schemes are in use. Clients need to be able to quickly map

between these for consistency and to analyse concentration risk.

• Ultimate Parent, Parent and Subsidiary Relationships: very complex relationships can

exist. In order to asses concentration risks, these relationships need to be mapped and

understood.

• S&P Global Market Intelligence’s Solution: Cross Reference Services

− Our Business Entity Cross Reference Services link multiple entity identification schemes and help

identify Ultimate Parents

− Our Global Instrument Cross Reference Services link multiple security identification and

classification schemes

− Our Industry Sector Cross Reference Services provide multiple entity classification schemes

− Our Company Relationships package helps identify and map complex corporate relationships

Reference Data

32

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Credit Ratings: referenced for investment assets and used to calculate capital

requirements (under the Basel and Solvency II Standard Approach/Formula).

• Credit Risk Analytics: proven methodologies and tools to score and track credit health

and risk across both rated and unrated investments (relevant for Internal Models).

• S&P Global Market Intelligence’s Solution: Credit Ratings, Indicators and Models

− Standard & Poor’s Credit Ratings: We are the official source for access to credit ratings and research

from Standard & Poor’s Global Ratings

− We also offer credit ratings from other ratings agencies, which can be delivered through a single feed

alongside Standard & Poor’s Global Ratings

− Credit analytics: We offer robust credit models to help score, track and benchmark credit risk across

both rated and unrated investments. In addition to models that calculate Probabilities of Default (PD),

we offer an extensive historical database of actual default rates, ratings transitions, recovery rates, and

Loss Given Default (LGD).

− Internal ratings methodologies: Our credit assessment scorecards deliver a fully documented and

transparent credit scoring process; outputs are mapped to the Standard & Poor’s credit ratings scale

− Independent model validation: Our validation services can be used to test the efficacy, soundness and

performance of your credit risk models rigorously and consistently

Credit Risk Offerings

33

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Credit Models

Expert Judgment Quantitative Fundamentals-Based Models Quantitative Market Signals Models

Public

Ratings

Scoring Template

(Fundamental)

Scoring Model

(Fundamental)

Probability of

Default

(Fundamental)

Peer

Analysis Model

Market Signals

CDS spreads

Market Signals

Stock Price

(Volatility & Returns)

Pro

du

ct

Standard & Poor’s

Ratings Services Scorecards CreditModel™

PD Model

Fundamentals

Credit Health

Panel

Market Derived

Signals (MDS)*

PD Model

Market Signals

Pri

ma

ry

Me

as

ure

Credit ratings* Credit Score -

Mapped to

“bucketed” PD

percentage

Credit Score -

Mapped to

“bucketed” PD

percentage

Continuous PD

percentage -

Mapped to credit

score

Relative score

Custom score

Credit Score -

Mapped to PD

percentage

PD percentage -

Mapped to credit

score

Des

ign

Analyst, committee

driven & credit

methodology driven

• Segment-focus

expert judgment

modeling

• Calibrated on

ratings

• Segment-focus

quantitative

modeling

• Calibrated on

ratings

• Segment-focus

quantitative

modeling

• Calibrated on

empirical defaults

• Fundamental-

based scores

and ratios for

peer group

assessment

• Market derived

signals based on

credit default swaps

• Calibrated on

empirical defaults

• Market derived

signals based on

stock price volatility

and returns

• Calibrated on

empirical defaults

DN

A

Medium/Long-term Medium/Long-term Medium/Long-term Medium-term Medium-term Short-term

(Point-in-time)

Short-term

(Point-in-time)

Co

ve

rag

e

•Global Coverage

•Daily monitored

• 6k companies

• Global Coverage

• No pre-scores

• Global Coverage

• Weekly pre-scored

• 36k+ companies

• Global Coverage

• Weekly pre-scored

• 370k+ companies

• Global Coverage

• Daily pre-scored

• 210k companies

• Rated Companies

w/ CDS coverage

• Daily pre-scored

• >1k companies

• Listed Companies

• Daily pre-scored

• 38k companies

Inp

uts

Rigorous analysis of

any relevant

qualitative and

quantitative inputs

• Qualitative and

quantitative inputs

• Country risk

• Industry risk

• Economic risk

• Sovereign risk

• Financial

statements +

quantifiable inputs

• Country risk

• Industry risk

• Economic risk

• Sovereign risk

• Financial

statements +

quantifiable inputs

• Country risk

• Industry risk

• Economic risk

• Sovereign risk

• Financial

Statements

• Operational

• Solvency

• Liquidity

• CDS spreads

• Industry risk

• Economic risk

• Sovereign risk

• Equity, Financials

• Country risk

• Industry risk

• Economic risk

• Sovereign risk

*From Standard & Poor’s Global Ratings. S&P Global Market Intelligence, as well as its products and services are analytically and editorially separate and independent from other analytical areas at S&P,

including S&P Global Ratings. For illustrative purposes only.

34

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Credit And Market Risk Assessments

S&P Global Market Intelligence deliver key data and analytics which help banks comply with requirements

related to credit and market risk on multi-asset classes.

• For trading books, market risk data is required to estimate volatility and VaR-based risk statistics

• For Banking books, historical fundamental data, estimates, ratings, and probability of default models

are required to comply with the Internal Ratings-Based (IRB) approach and the new IFRS 9 accounting

principle

• Credit default swap spreads are needed to calculate the new Credit Value Adjustment (CVA) capital

charge formulas for ITC derivatives

Credit And Market Risk Assessments

Ratings Credit Analytics and PD and LGD

Credit Assessment Scorecards Fundamental Data

• Credit ratings

• Credit research

• Low latency ratings alerts

• Ratings press releases

• Default, transition and recovery data

• PD Model Fundamental for public and

private companies

• CreditModel 2.6

• PD Model Market Signals (equity-

based)

• CDS-based signals for entities

• PD and LGD credit Assessment

Scorecards for low-default portfolios

• Standardised global company data

• Extended global fundamentals

• Ratings fundamentals (CreditStats

Direct)

• Industry sector classifications

• Internal Ratings Development

35

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• LEI: Legal Entity identifier used to identify counterparties, issuers and ultimate parent entities (to

monitor concentration risk) - S&P Global Market Intelligence’s Business Entity Cross Reference Service

includes LEI codes and mappings to ultimate parent entities

• NACE: European Standard Industry Classification - S&P Global Market Intelligence’s Industry Sector

Cross-Referencing Services offerings include multiple standard industry classification schemes (e.g.,

NACE and GICS)

• CIC: Complementary Identification Code for asset classification - S&P Global Market Intelligence’s

offerings also include core data required to construct CIC codes (whose determination can involve

subjective elements)

• Instrument characteristics and risk-related metrics including multi-level pricing and valuations

data, security terms & conditions, instrument identifier cross reference services, and Duration metrics

• Credit Risk measures and indicators including S&P Ratings, external ratings (from multiple ratings

agencies), Credit Models, Scorecards, Loss Given Default (LGD) measures, historical default

statistics, Probabilities of Default (PDs), Ratings transition matrices, and market-derived signals

• Other relevant S&P Global Market Intelligence’s offerings include transparency measures, corporate

actions, company fundamentals, and yield curves

Solvency II – Specific Examples

36

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

http://www.spcapitaliq.com/client-solutions/regulatory-solutions

Engaging The Market On Timely Regulatory Issues Ongoing Market Interaction Supporting The Development Of Regulatory Solutions

Source: www.spcapitaliq.com.

37

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

• Attractive Standard & Poor’s credit rating universe, from the source

• Credit Models and Credit Analytics trained on extensive data and Standard & Poor’s

methodologies

• We are originators for significant datasets

• Data available on multiple feeds and platforms

• Most data available in a relational database, linked and mapped, ready to use, bringing

together key external datasets required (e.g., ratings/credit, company financials, cross-

reference services, pricing, and security reference data)

• Single vendor relationship for multiple needs

• Extensive experience in sourcing, aggregating, scrubbing, managing and delivering market

and reference data

• Strong Cross-Referencing offering, including links to ultimate parents

• Commercial offers specific to ratings redistribution by asset managers, fund administrators,

custodians and other relevant third parties for regulatory compliance purposes

Benefits

38

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Thank You

Hans Crockett

Vice President

Innovation and Thought Leadership

Global Risk Services

39

Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Copyright © 2016 by S&P Global Market Intelligence. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified,

reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of S&P Global Market

Intelligence or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors,

officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any

data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED

TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT

THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event

shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses

(including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility

of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P Global

Market Intelligence’s opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any

investment decisions, and do not address the suitability of any security. S&P Global Market Intelligence assumes no obligation to update the Content following publication in any form or

format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making

investment and other business decisions. S&P Global Market Intelligence does not act as a fiduciary or an investment advisor except where registered as such. While S&P Global Market

Intelligence has obtained information from sources it believes to be reliable, S&P Global Market Intelligence does not perform an audit and undertakes no duty of due diligence or

independent verification of any information it receives.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business

units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public

information received in connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its

opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and

www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our

ratings fees is available at www.standardandpoors.com/usratingsfees.

STANDARD & POOR’S, S&P and S&P Capital IQ are registered trademarks of Standard & Poor’s Financial Services LLC. CAPITAL IQ is registered trademark of Capital IQ, Inc. All

other product or service names may be the property of their respective owners.

40

Related Documents