CONSUMER EXPECTATIONS & HOW TO GROW WITH SUSTAINABILITY THE SUSTAINABILITY IMPERATIVE Claudia Suárez-Gapp The Nielsen Company June 14 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CONSUMER EXPECTATIONS & HOW TO GROW

WITH SUSTAINABILITY

THE SUSTAINABILITY IMPERATIVE

Claudia Suárez-Gapp

The Nielsen Company

June 14 2016

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

2

DEFINING SUSTAINABILITY

ENVIRONMENTAL SOCIAL GOVERNANCE

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

3

INCREASING GLOBAL EMPHASIS & POLITICAL

IMPERATIVE

Take a look at the video https://www.youtube.com/watch?v=RpqVmvMCmp0

.

WHAT DO WE KNOW?

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

5

BRANDS THAT COMMIT TO

SUSTAINABILITY HAVE

GROWN MORE THAN 4%

GLOBALLY IN THE PAST YEAR.*

*Across 1300+ brands in 13 categories in an average of 13 countries.Source: The Sustainability Imperative, Nielsen Report 2015

THE NUMBER OF CONSUMERS WILLING TO PAY MORE

FOR BRANDS COMMITTED TO POSITIVE SOCIAL AND ENVIRONMENTAL IMPACT

CONTINUES TO RISE—REACHING 66% IN 2015 (UP 11% FROM 2014)

Source: The Sustainability Imperative, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

7

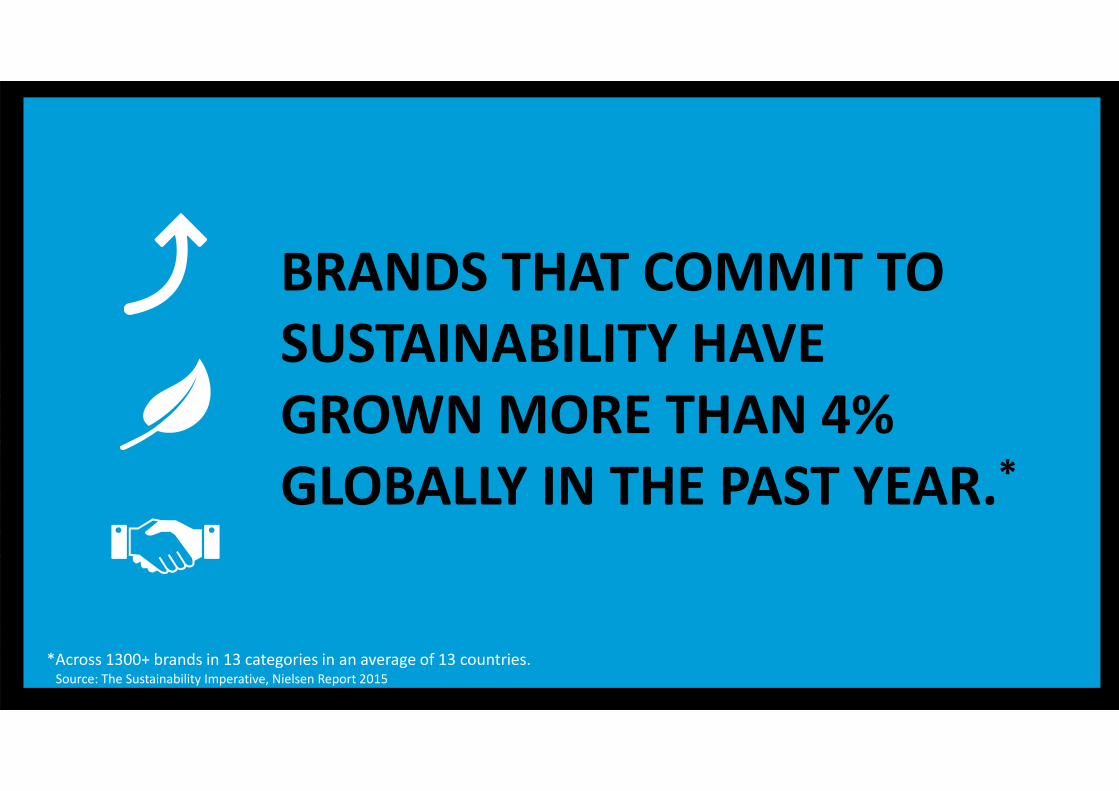

IN EU HALF OF CONSUMERS SAY THEY’RE WILLING

TO PAY MORE FOR SUSTAINABLE PRODUCTS & ITS

GROWING!

Source: The Sustainability Imperative, Nielsen Report 2015

44%

51%

70%

71%

76%

North America

Europe

Middle East/Africa

Latin America

Asia-Pacific

Percentage of Consumers Willing to Pay More for

Sustainable Products

Growth in Consumers Willing to Pay More for

Sustainable Products (YoY Point Change)

2

7

8

11

12

North America

Middle East/Africa

Latin America

Europe

Asia-Pacific

+

ppts

ppts

ppts

ppts

ppts

+

+

+

+

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

8

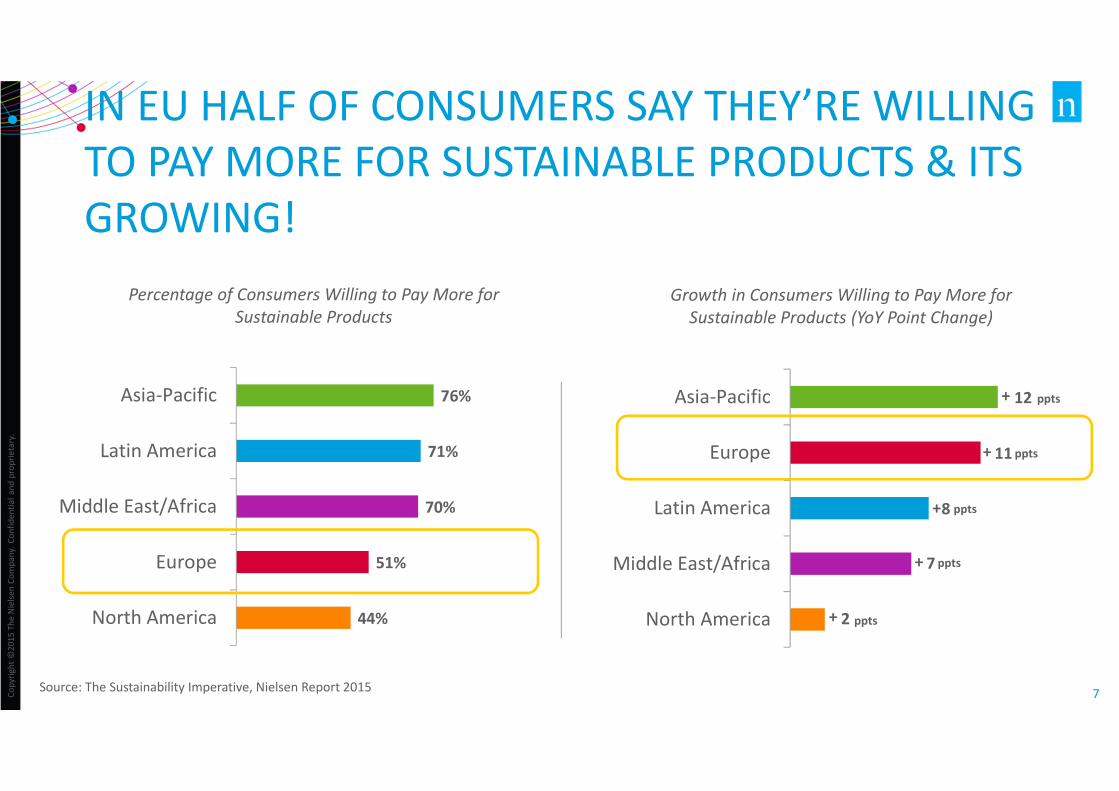

THIS TRANSLATES INTO THE MARKETS

FR ES IT

TR

41%

BE

EU

44% 40%

52%

61%

51%

Q1 2015 Percent willing to pay extra for products & services that come from companies who are committed to

positive social and environmental impact

NL UK DE

CH AT SE RU

40% 52%

61%

PT

DK

41% 58%

66% 58% 46%

42%

Source: The Sustainability Imperative, Nielsen Report 2015

WHERE DOES THE INTEREST LIE?

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

10

CONSUMERS UNDER 34 ARE WILLING TO PAY

MORE

GROWING:

GENERATION Z

72%

MOST LIKELY TO BUY:

MILLENNIALS

73%

DON’T FORGET:

BABY BOOMERS

51%

Source: The Sustainability Imperative, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

11

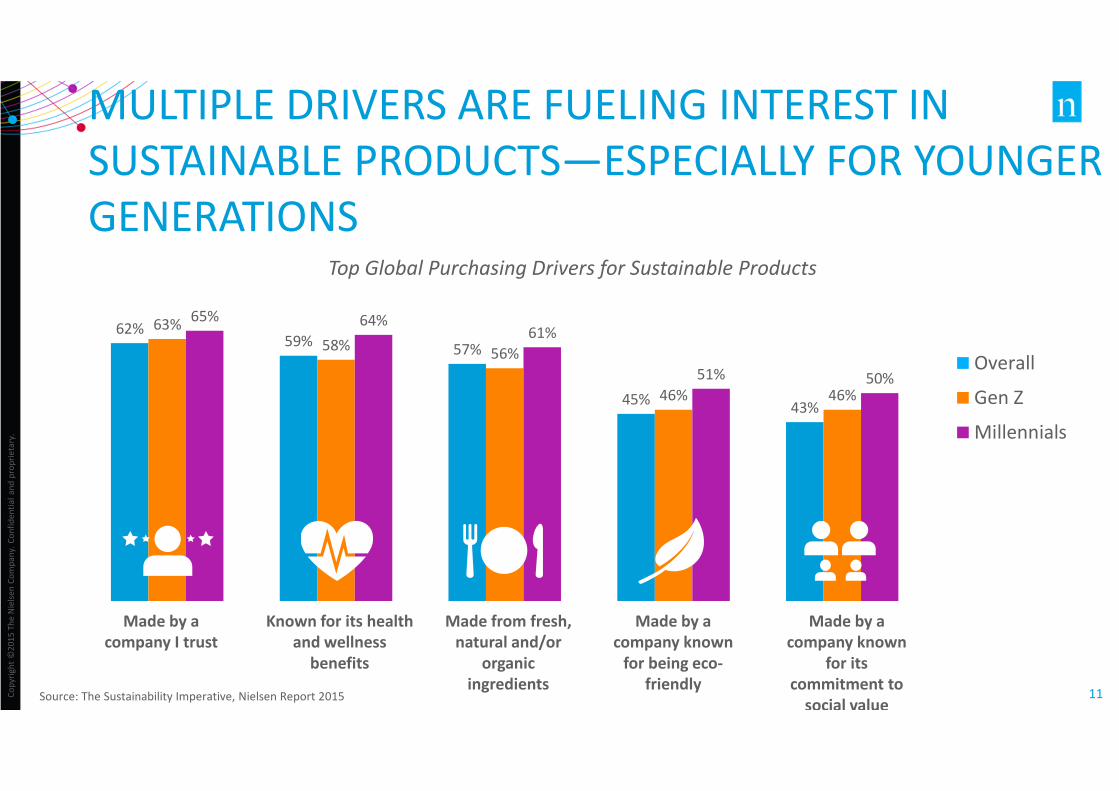

62%59%

57%

45%43%

63%

58%56%

46% 46%

65% 64%61%

51% 50%Overall

Gen Z

Millennials

MULTIPLE DRIVERS ARE FUELING INTEREST IN

SUSTAINABLE PRODUCTS—ESPECIALLY FOR YOUNGER

GENERATIONSTop Global Purchasing Drivers for Sustainable Products

Source: The Sustainability Imperative, Nielsen Report 2015

Made by a

company I trust

Known for its health

and wellness

benefits

Made from fresh,

natural and/or

organic

ingredients

Made by a

company known

for being eco-

friendly

Made by a

company known

for its

commitment to

social value

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

12

MARKETS VARY ON TRUST HIGHLIGHTING THE

NEED TO UNDERSTAND COUNTRY SPECIFICITIES

FR ES IT

TR

38%

BE

38% 55%

53%

71%

51%

NL UK DE

CH AT SE RU

39% 61%

48%

PT

DK

35% 54%

51% 61% 50%

40%

Source: The Sustainability Imperative, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

13

WHAT IS THE KEY SUSTAINABILITY PURCHASING

DRIVER FOR EUROPEAN CONSUMERS?

FRESH, NATURAL,

ORGANIC INGREDIENTS

FRESH, NATURAL, ORGANIC INGREDIENTS ARE

PARAMOUNT TO 52% OF EUROPEAN

RESPONDENTS.

Source: The Sustainability Imperative, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

14

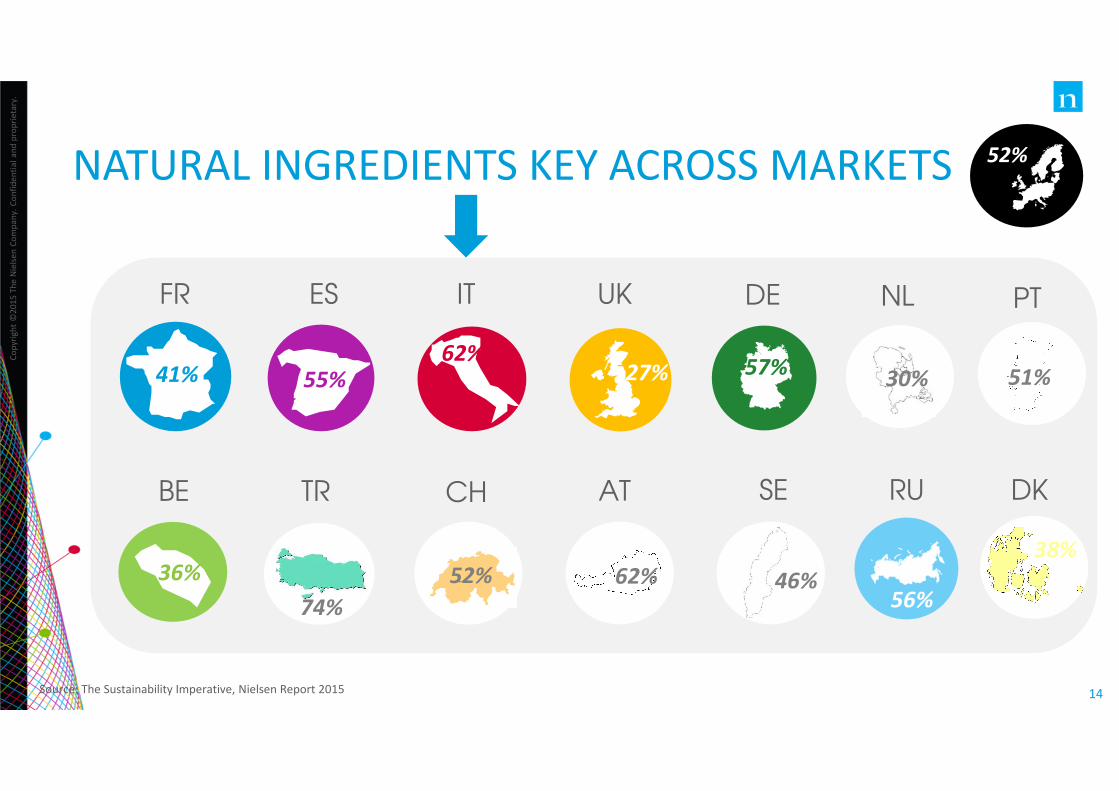

NATURAL INGREDIENTS KEY ACROSS MARKETS

FR ES IT

TR

36%

BE

41% 55%

62%

74%

52%

NL UK DE

CH AT SE RU

27% 57%

56%

PT

DK

30% 51%

52% 62% 46%

38%

Source: The Sustainability Imperative, Nielsen Report 2015

THE CURRENT STATE OF “SUSTAINABLE”

COMMUNICATION

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

16

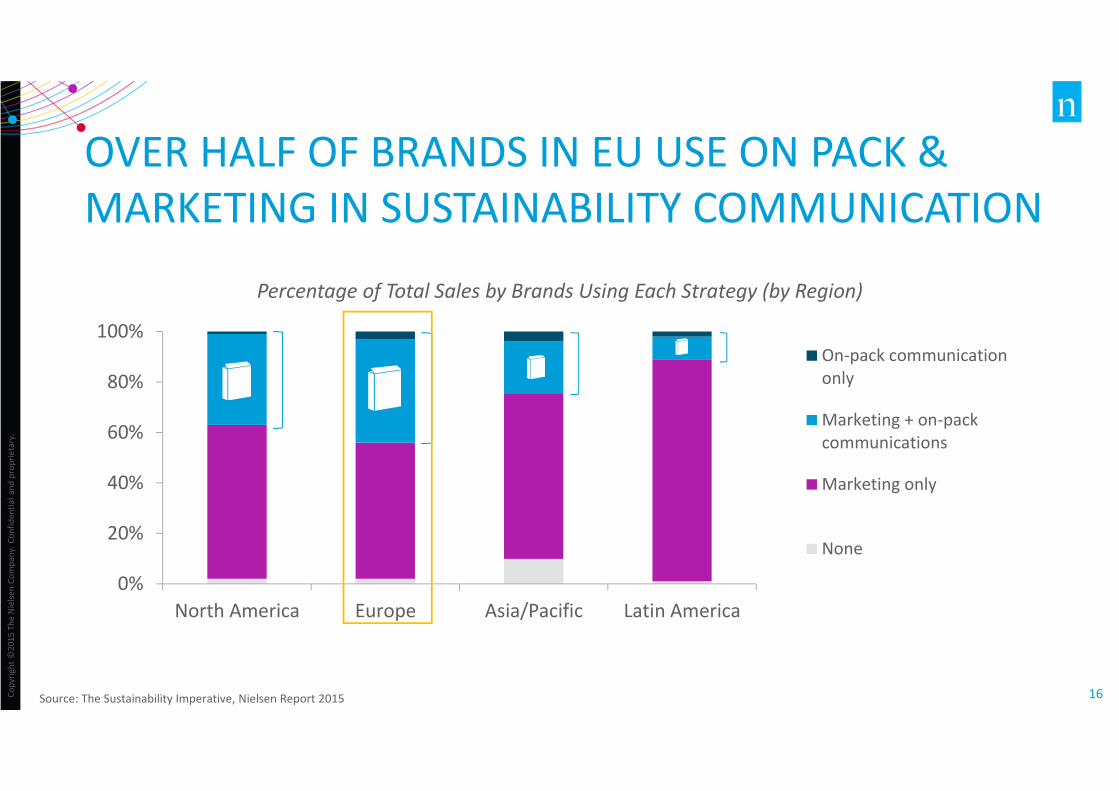

OVER HALF OF BRANDS IN EU USE ON PACK &

MARKETING IN SUSTAINABILITY COMMUNICATION

Percentage of Total Sales by Brands Using Each Strategy (by Region)

0%

20%

40%

60%

80%

100%

North America Europe Asia/Pacific Latin America

On-pack communication

only

Marketing + on-pack

communications

Marketing only

None

Source: The Sustainability Imperative, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

17

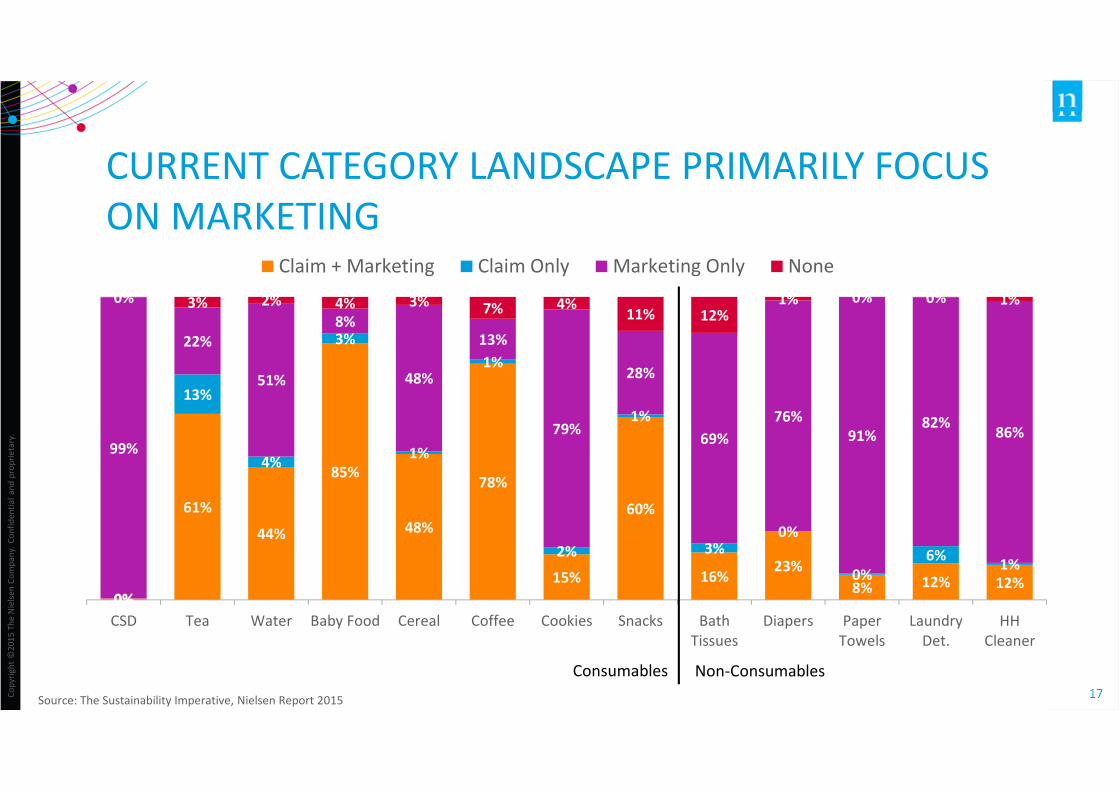

CURRENT CATEGORY LANDSCAPE PRIMARILY FOCUS

ON MARKETING

Source: The Sustainability Imperative, Nielsen Report 2015

0%

61%

44%

85%

48%

78%

15%

60%

16%23%

8% 12% 12%0%

13%

4%

3%

1%

1%

2%

1%

3%0%

0%

6%1%

99%

22%

51%

8%

48%

13%

79%

28%

69%

76%

91%82%

86%

0% 3% 2% 4% 3% 7% 4%11% 12%

1% 0% 0% 1%

CSD Tea Water Baby Food Cereal Coffee Cookies Snacks Bath

Tissues

Diapers Paper

Towels

Laundry

Det.

HH

Cleaner

Claim + Marketing Claim Only Marketing Only None

Consumables Non-Consumables

Co

pyri

gh

t ©

20

12

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al a

nd

pro

pri

eta

ry.

18

75% OF RESPONDENTS READ PACKAGING LABELS

CAREFULLY

Source: Nielsen Global Health and Wellness report January 2015 / We are what we eat

Co

pyri

gh

t ©

20

12

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al a

nd

pro

pri

eta

ry.

19

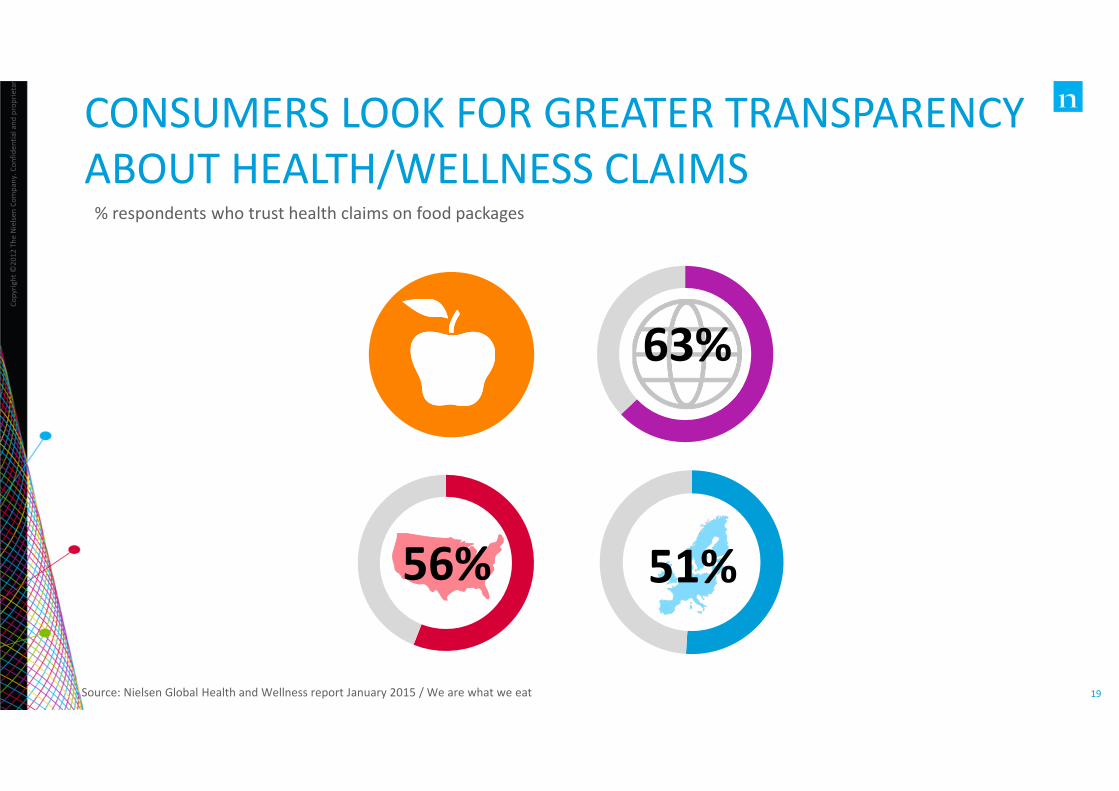

CONSUMERS LOOK FOR GREATER TRANSPARENCY

ABOUT HEALTH/WELLNESS CLAIMS

Source: Nielsen Global Health and Wellness report January 2015 / We are what we eat

% respondents who trust health claims on food packages

63%

56% 51%

Co

pyri

gh

t ©

20

12

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al a

nd

pro

pri

eta

ry.

20

FAIR TRADE/

SUSTAINABLY

SOURCED

38% SAY FAIR TRADE IS VERY IMPORTANT,

FOLLOWED BY:

ORGANIC 36%

HIGH PROTEIN 34%

FORTIFICATION 31%

AMONG THE FOLLOWING HEALTH ATTRIBUTES, WHICH

IS MOST IMPORTANT TO MILLENNIALS WHEN MAKING

A PURCHASE?

Source: Nielsen Global Generational Lifestyles Report, 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

21

CONSUMERS ARE PACK-SAVVY, SO MESSAGING ON

SUSTAINABILITY WILL BECOME INCREASINGLY

IMPORTANT

52%of consumers globally report checking

the product packaging for

sustainability claims before making a

purchase

1 IN 3 Consumers in EU report checking the

product packaging for sustainability

claims before making a purchase

Source: The Sustainability Imperative, Nielsen Report 2015

GROWTH AREAS FOR

SUSTAINABILITY

42% OF GLOBAL CONSUMERS WANT

MORE NEW PRODUCTS IN THE

MARKET THAT ARE SOCIALLYRESPONSIBLE AND

ENVIRONMENTALLYFRIENDLY

Source: Global New Product Innovation, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

24

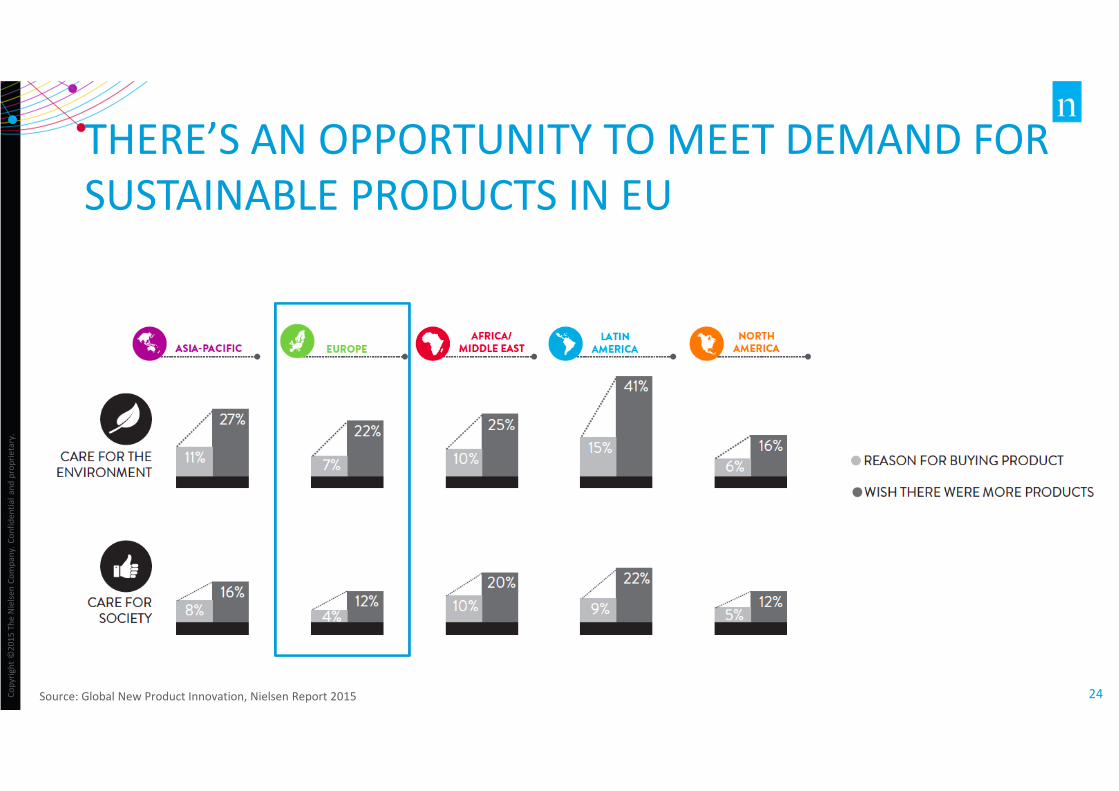

THERE’S AN OPPORTUNITY TO MEET DEMAND FOR

SUSTAINABLE PRODUCTS IN EU

Source: Global New Product Innovation, Nielsen Report 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

25

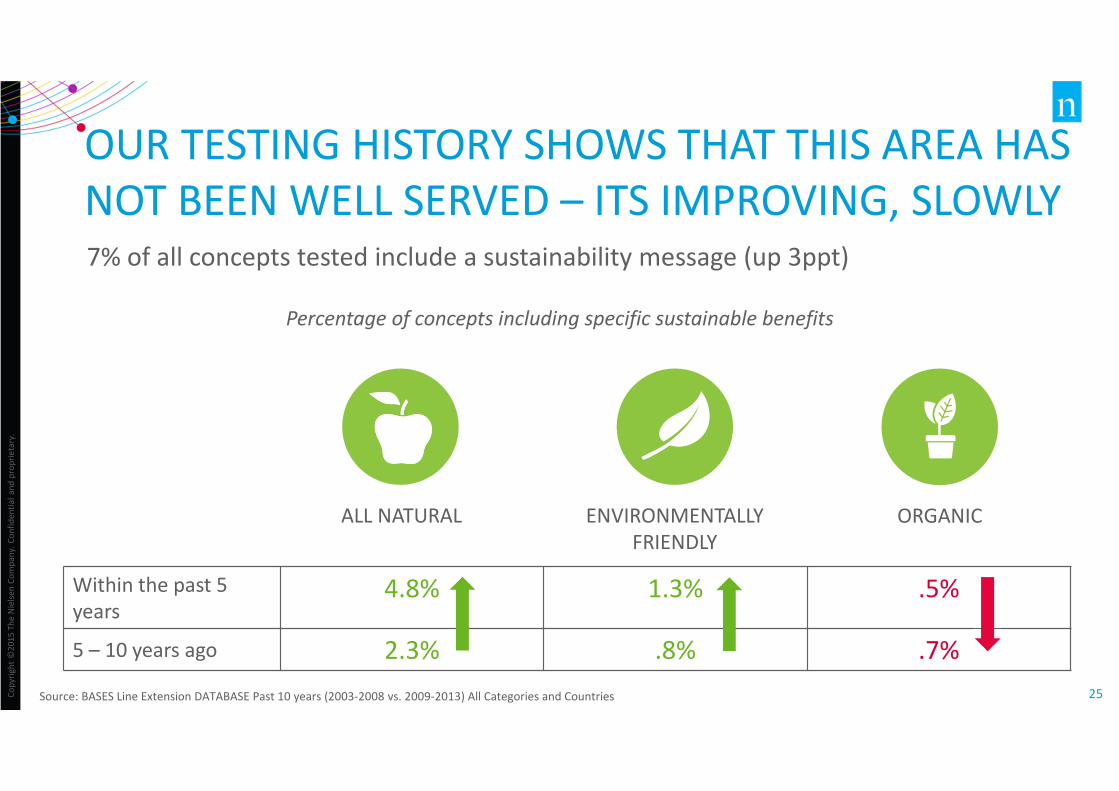

OUR TESTING HISTORY SHOWS THAT THIS AREA HAS

NOT BEEN WELL SERVED – ITS IMPROVING, SLOWLY7% of all concepts tested include a sustainability message (up 3ppt)

Source: BASES Line Extension DATABASE Past 10 years (2003-2008 vs. 2009-2013) All Categories and Countries

Percentage of concepts including specific sustainable benefits

ENVIRONMENTALLY

FRIENDLY

ALL NATURAL ORGANIC

Within the past 5

years4.8% 1.3% .5%

5 – 10 years ago 2.3% .8% .7%

YOUR BUSINESS – AND REPUTATION –

DEPEND ON IT

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

27

SOCIAL RESPONSIBILITY IS ONE OF THE TOP MOST

INFLUENTIAL FACTORS FOR REPUTATION

emotional appeal

Financial

PerformanceVision &

Leadership

Workplace

Environment

High Product

Quality

social responsibility

Source: Nielsen - Harris Poll Reputation Quotient U.S. Study, 2015

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

28

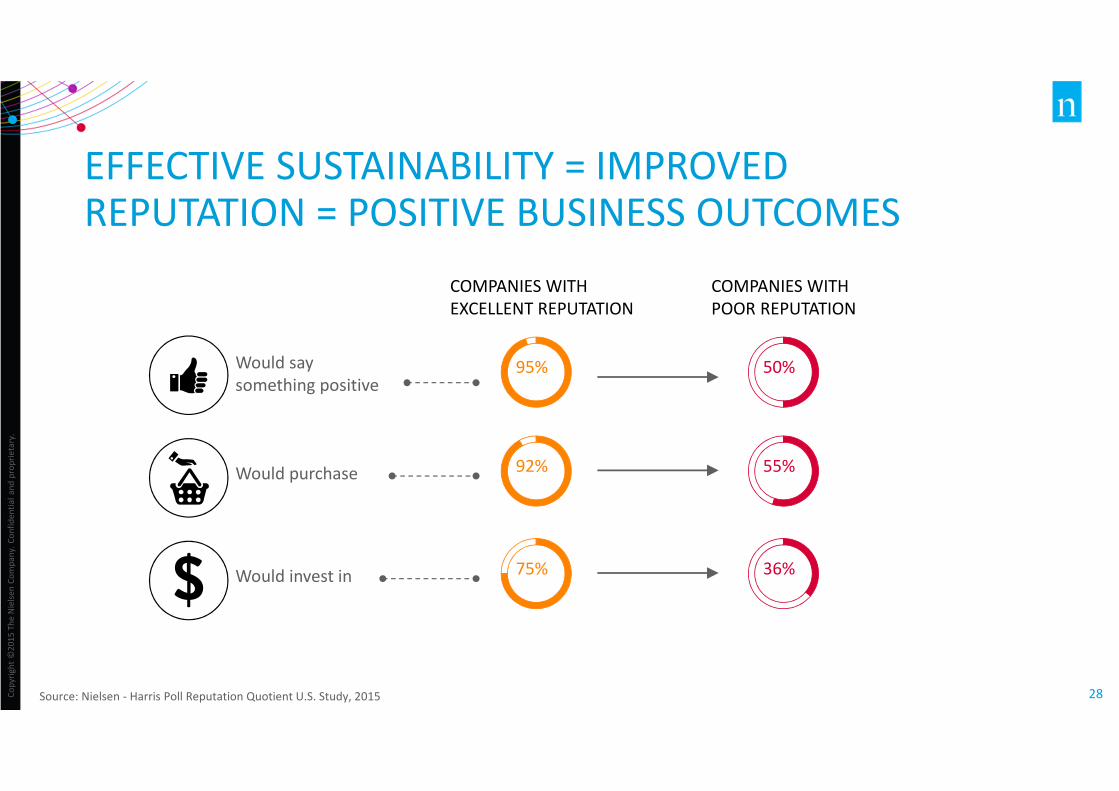

EFFECTIVE SUSTAINABILITY = IMPROVED REPUTATION = POSITIVE BUSINESS OUTCOMES

Source: Nielsen - Harris Poll Reputation Quotient U.S. Study, 2015

Would say

something positive

Would purchase

Would invest in

COMPANIES WITH

EXCELLENT REPUTATION

COMPANIES WITH

POOR REPUTATION

95%

92%

75%

50%

55%

36%

Co

pyri

gh

t ©

20

15

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al

an

d p

rop

rie

tary

.

29

67% OF GLOBAL CONSUMERS

WANT TO WORK for

COMPANIES that are GIVING

BACK to SOCIETYSource: Global Shopper survey - Nielsen Report Q1 - 2015

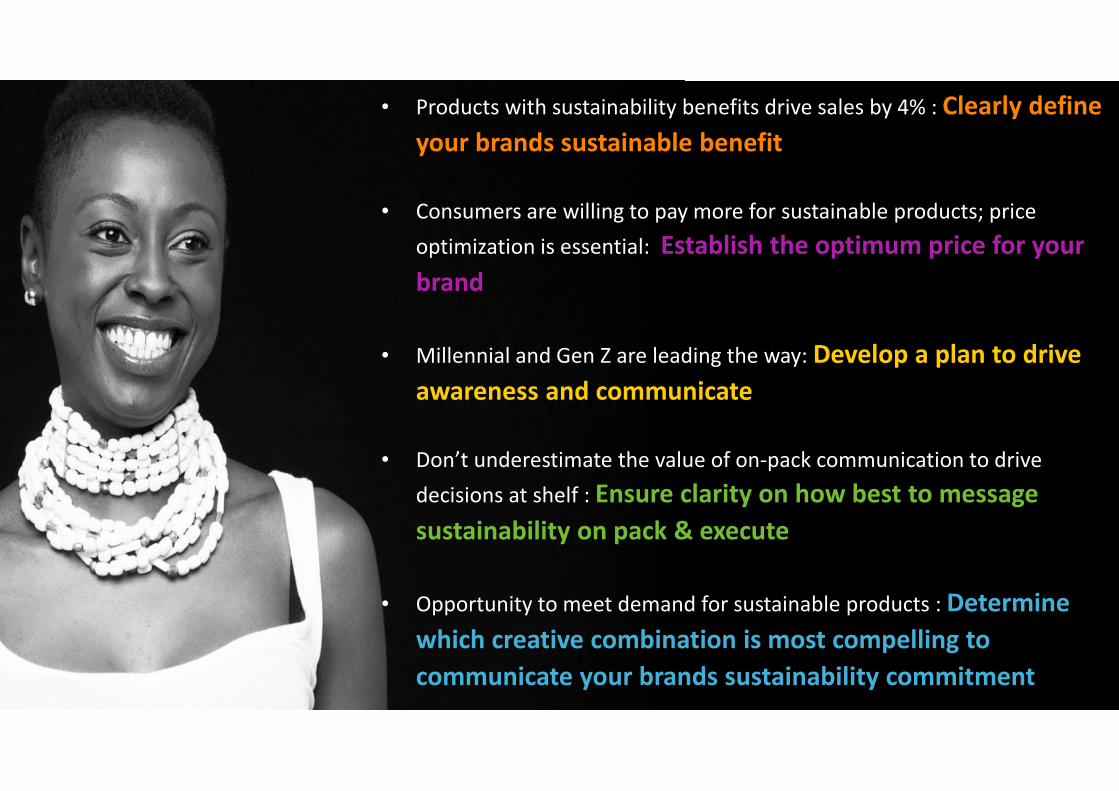

• Products with sustainability benefits drive sales by 4% : Clearly define

your brands sustainable benefit

• Consumers are willing to pay more for sustainable products; price

optimization is essential: Establish the optimum price for your

brand

• Millennial and Gen Z are leading the way: Develop a plan to drive

awareness and communicate

• Don’t underestimate the value of on-pack communication to drive

decisions at shelf : Ensure clarity on how best to message

sustainability on pack & execute

• Opportunity to meet demand for sustainable products : Determine

which creative combination is most compelling to

communicate your brands sustainability commitment

THANK YOU

[email protected] FIND OUT MORE OF WHAT WE DO AT NIELSEN CLICK :

HTTPS://WWW.YOUTUBE.COM/WATCH?V=EF6IOXR-SJU&FEATURE=YOUTU.BE

Co

pyri

gh

t ©

20

14

Th

e N

iels

en

Co

mp

an

y.

Co

nfi

de

nti

al a

nd

pro

pri

eta

ry.

32

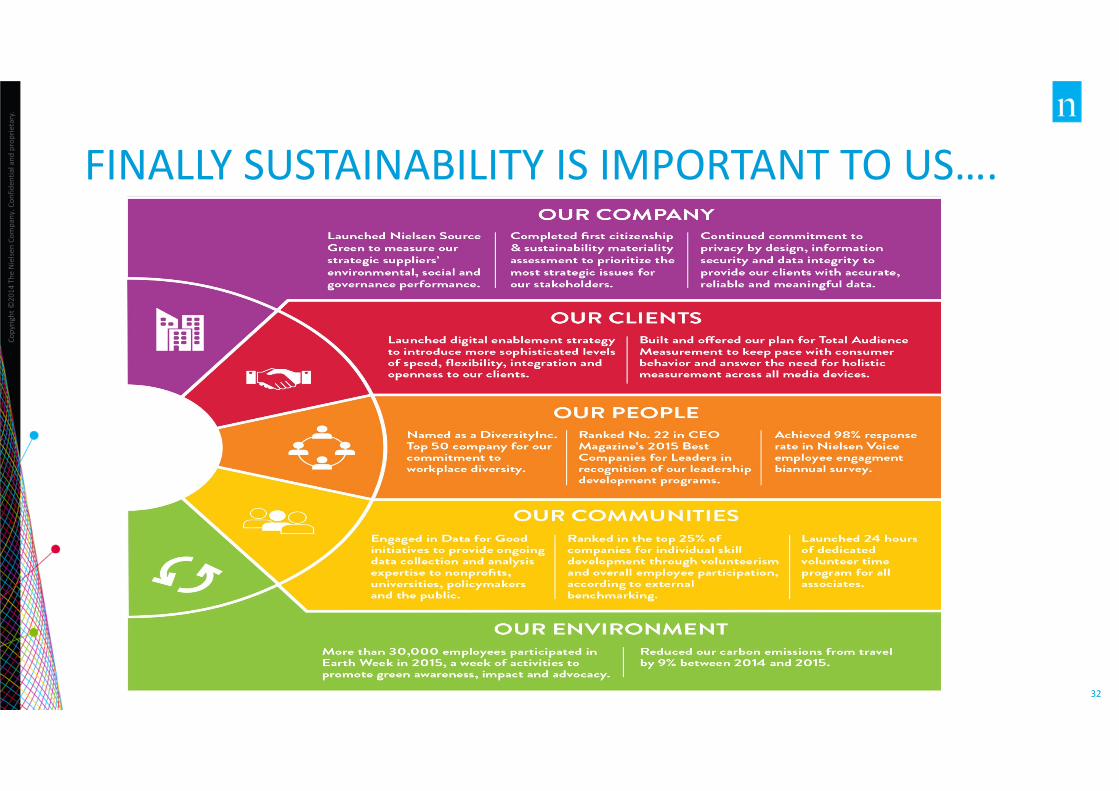

FINALLY SUSTAINABILITY IS IMPORTANT TO US….

Related Documents