© The Author 2015. Published by Oxford University Press on behalf of the Centre for Crime and Justice Studies (ISTD). All rights reserved. For permissions, please e-mail: [email protected] THE RISKS AND REWARDS OF ORGANIZED CRIME INVESTMENTS IN REAL ESTATE Marco Dugato* , Serena Favarin and Luca Giommoni Despite growing interest in organized crime’s infiltration of the legal economy, research to date has paid little attention to the investments of criminal organizations in real estate. Using data on con- fiscated assets in 8,092 Italian municipalities between 2000 and 2012, this paper aims to remedy this lack of knowledge. Applying a risk–reward approach, based on the rational choice perspective, the analysis highlights what drives Italian mafia groups’ investments in the real estate sector. The results obtained support the validity of the rational choice perspective by showing how criminal organizations weigh risks and rewards in their decisions to invest in real estate. Keywords: organized crime, real estate, risk–reward, OC investments, rational choice, decision-making process Background Enterprise theory (Smith 1975) maintains that organized crime (henceforth OC) groups are mainly providers of illicit or highly regulated goods and services (i.e. drugs, firearms, tobacco products, gambling). Since this theory’s diffusion, numerous stud- ies have examined OC groups’ involvement in illicit markets (Reuter 1985; Paoli 2002; Bouchard and Wilkins 2010; Transcrime 2013; Calderoni 2014). Besides OC groups’ role as suppliers of irregular commodities, some studies have acknowledged their involvement in legal markets as well ( Cressey 1969; Catanzaro 1988; Ianni and Reuss- Ianni 1993; Arlacchi 2007). According to some authors ( Catanzaro 1988; Centorrino and Signorino 1997), criminal organizations’ investments in the legal economy follow a previous phase of investment in the illegal economy. Hence, the investments are means to launder the proceeds of crime. Another body of thought has recognized infiltration of the legal economy as a typical feature of OC, with investments being made both in the legal and illegal sectors (Fantò 1999; Santino 2006). Although it is not easy to rec- oncile these two different approaches, it is certain that OC groups do invest in the legal economy and that their portfolios include investments in both the illegal and legal markets (Smith 1980; Becchi and Rey 1994; Finckenauer 2007; Abadinsky 2010). In the past 20 years, the threat OC has raised in the legal economy has become a priority on governments’ and international authorities’ agendas. This concern has produced a growing number of studies and recommendations (Alexander 1997; Reuter and Levi 2006; FATF 2008; Calderoni et al . 2010; Calderoni and Riccardi 2011; Unger et al . 2011; Caneppele et al . 2013; Riccardi 2014). Despite growing interest in OC’s infil- tration of the legal economy, research has paid little attention to criminal organiza- tions’ investments in real estate (Schneider 2004; Nelen 2008; van Duyne and Soudijn 2009; Unger et al . 2011; Shelley 2013). This is surprising, given the potential misuse *Marco Dugato, Serena Favarin and Luca Giommoni, TRANSCRIME Joint Research Centre on Transnational Crime, Università Cattolica del Sacro Cuore di Milano, Largo Gemelli 1 – 20123 Milan, Italy; [email protected]. doi:10.1093/bjc/azv002 BRIT. J. CRIMINOL Page 1 of 22 British Journal of Criminology Advance Access published March 6, 2015 by guest on March 8, 2015 http://bjc.oxfordjournals.org/ Downloaded from

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© The Author 2015. Published by Oxford University Press on behalf of the Centre for Crime and Justice Studies (ISTD). All rights reserved. For permissions, please e-mail: [email protected]

The Risks and RewaRds of oRganized CRime invesTmenTs in Real esTaTe

marco dugato*, serena favarin and luca giommoni

Despite growing interest in organized crime’s infiltration of the legal economy, research to date has paid little attention to the investments of criminal organizations in real estate. Using data on con-fiscated assets in 8,092 Italian municipalities between 2000 and 2012, this paper aims to remedy this lack of knowledge. Applying a risk–reward approach, based on the rational choice perspective, the analysis highlights what drives Italian mafia groups’ investments in the real estate sector. The results obtained support the validity of the rational choice perspective by showing how criminal organizations weigh risks and rewards in their decisions to invest in real estate.

keywords: organized crime, real estate, risk–reward, oC investments, rational choice, decision-making process

Background

enterprise theory (smith 1975) maintains that organized crime (henceforth oC) groups are mainly providers of illicit or highly regulated goods and services (i.e. drugs, firearms, tobacco products, gambling). since this theory’s diffusion, numerous stud-ies have examined oC groups’ involvement in illicit markets (Reuter 1985; Paoli 2002; Bouchard and wilkins 2010; Transcrime 2013; Calderoni 2014). Besides oC groups’ role as suppliers of irregular commodities, some studies have acknowledged their involvement in legal markets as well (Cressey 1969; Catanzaro 1988; ianni and Reuss-ianni 1993; arlacchi 2007). according to some authors (Catanzaro 1988; Centorrino and signorino 1997), criminal organizations’ investments in the legal economy follow a previous phase of investment in the illegal economy. hence, the investments are means to launder the proceeds of crime. another body of thought has recognized infiltration of the legal economy as a typical feature of oC, with investments being made both in the legal and illegal sectors (fantò 1999; santino 2006). although it is not easy to rec-oncile these two different approaches, it is certain that oC groups do invest in the legal economy and that their portfolios include investments in both the illegal and legal markets (smith 1980; Becchi and Rey 1994; finckenauer 2007; abadinsky 2010).

in the past 20 years, the threat oC has raised in the legal economy has become a priority on governments’ and international authorities’ agendas. This concern has produced a growing number of studies and recommendations (alexander 1997; Reuter and levi 2006; faTf 2008; Calderoni et al. 2010; Calderoni and Riccardi 2011; Unger et al. 2011; Caneppele et al. 2013; Riccardi 2014). despite growing interest in oC’s infil-tration of the legal economy, research has paid little attention to criminal organiza-tions’ investments in real estate (schneider 2004; nelen 2008; van duyne and soudijn 2009; Unger et al. 2011; shelley 2013). This is surprising, given the potential misuse

*marco dugato, serena favarin and luca giommoni, TRansCRime Joint Research Centre on Transnational Crime, Università Cattolica del sacro Cuore di milano, largo gemelli 1 – 20123 milan, italy; [email protected].

doi:10.1093/bjc/azv002 BRiT. J. CRiminol

Page 1 of 22

British Journal of Criminology Advance Access published March 6, 2015 by guest on M

arch 8, 2015http://bjc.oxfordjournals.org/

Dow

nloaded from

that oC can make of real estate. in fact, this is an attractive sector for investments for many reasons. first, the properties can be used as operational and logistical bases for oC activities (such as drug trafficking, gambling, prostitution, etc.) as well as means to re-invest the proceeds of illicit activities using fraudulent schemes. This reduces the risk of oC illicit revenues being traced by law enforcement agencies (schneider 2004; faTf 2008; abadinsky 2010). Real estate is also a safe, profitable and prestigious investment. it can be considered safe for several reasons. first, real estate lacks a supervisory insti-tution, such as the stock exchange authority, which is able to determine transactions’ lawfulness and to impose sanctions in the case of misconduct (nelen 2008). second, properties’ values are difficult to evaluate objectively, and the market often consists of a closed network (nelen 2008; shelley 2013). These factors make speculation a fairly common behaviour in this sector, with a low risk of intervention by law enforcement agencies (nelen 2008; Unger et al. 2011). Besides illegal activities, properties can also be used to gain licit earnings by being rented out or used to start businesses in the com-mercial or entertainment sectors (i.e. shops, bars, clubs, hotels, etc.). Third, real estate and house properties, in particular, can also have a highly symbolic and social mean-ing for oC members. This can be exemplified with the house of nicola schiavone, a member of the Casalesi family of Caserta, who built his own house based on the model of Tony montana’s villa in the movie Scarface (kington 2012). although this example cannot be considered a typical investment, it exemplifies how criminal organizations can use real estate as a mean to gain social consensus and prestige. hence, investments in real estate may be made not just for an economic return but also for social and reputational rewards. members of oC groups may buy houses in expensive areas or city centres in order to be recognized as important actors within the local community.

given the attractiveness of the real estate sector and the potential for criminal organ-izations to misuse it, one would expect to find equal interest in it among researchers. however, to date, the literature on the topic has mainly consisted of exploratory and descriptive studies on how oC can infiltrate the real estate sector (schneider 2004; faTf 2008; finCen 2008; shelley 2013) or on the extent of its threat to the legal econ-omy (schneider 2004; van duyne and soudijn 2009). on the one hand, the available literature highlights the numerous methods—the use of straw men, flipping real estate properties, under- or over-invoicing, use of complex loans, use of money instruments, use of fraudulent mortgage schemes—that oC can employ to gain access to real estate (schneider 2004; faTf 2008; finCen 2008; shelley 2013). Regarding the other line of inquiry, schneider (2004) and van duyne and soudijn (2009) conclude that the negli-gible data available do not allow firm conclusions to be drawn on these oC investments’ economic and financial effects on society.

Unger et al. (2011) have made the only attempt of empirical analysis of oC invest-ments in real estate. These scholars, using data on dutch real estate properties, devel-oped a method with which to distinguish conspicuous transactions from regular ones. according to the authors, conspicuous transactions are considered evidences of crimi-nal groups’ investments in the real estate sector. Using indirect indicators, they found that a real estate property owned by a foreigner sold to a recently established com-pany and featuring a marked fluctuation in the value of the property has a 64 per cent chance of being conspicuous (Unger et al. 2011).

despite its paucity, the available research agrees on the necessity of investigating this field further. van duyne and soudijn (2009) highlight that, at present, no basis exists

dUgaTo eT al.

Page 2 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

for ‘evidence based policy making’, and for this reason, researchers require better data from law enforcement agencies. shelley (2013: 131) states that ‘[money laundering into real estate] is an enduring but insufficiently recognised international problem’, while nelen (2008: 753) adds that ‘we are just at the beginning of exploring the very complex domain of real estate. Reliable and valid research data are scarce, as are empirical stud-ies that focus on the relationship between real estate and serious forms of crime’.

The need to investigate this field further is heightened also by the potential threat to society that oC investments raise in real estate. Under- or over-invoicing, a tech-nique oC often uses to infiltrate the real estate market (faTf 2008; Unger et al. 2011), can affect the latter by deflecting or inflating property values (schneider 2004; shelley 2013). although little evidence of country-wide distortions of the real estate and stock market exists, as fabre (2005) suggested for Japan’s economic crisis in the late 1980s, oC investments in real estate can distort local and restricted markets.

Criminal Decision-Making and Real Estate Investments

in 1986, Cornish and Clarke (1986) published The Reasoning Criminal, a collection of studies on offenders’ decision-making process. since its publication, the book’s intro-ductory chapter has become the cornerstone of the rational choice perspective in criminology, which assumes that criminals, as any other human beings, are rational actors who seek to minimize costs and maximize rewards. The rational choice perspec-tive is grounded on the economic analysis of human behaviours, which dates back to the early work of gary Becker (1968; 1978) and other theorists of the rational choice model (Barry and hardin 1982; elster 1986; Cook and levi 1990). Crime, like any other behaviour, occurs when the perceived rewards outweigh the perceived costs (Cornish and Clarke 1986; 2008). hence, offenders are decision-making agents who decide to commit a crime according to two conditional factors: risk and reward.

The rational choice theory and its application to crime has often been criticized for its assumption of the offender’s rationality. Clarke and others responded to this criti-cism by importing and developing the concept of bounded/limited rationality (simon 1990; fernandez-huerga 2008). due to a lack of information, criminals may not accu-rately calculate their behaviours’ rewards and risks (Cornish and Clarke 2008; leclerc and wortley 2014). moreover, the term ‘reward’ can have multiple meanings and does not solely indicate economic return. for instance, it can mean sexual satisfaction and revenge in child sexual abuse (Beauregard and leclerc 2007; mann and hollin 2007), vengeance in the case of homicide (luckenbill 1977) and excitement, social status and group support in that of terrorism (Clarke and newman 2006).

as leclerc and wortley (2014) emphasize, since publication of The Reasoning Criminal, the decision-making process and the influence of risk and reward have been applied across a range of offences. These include burglary (nee and meenaghan 2006), car theft (Cherbonneau and Copes 2006), drug dealing (Jacobs 1996), sexual abuse (Beauregard and leclerc 2007) and crime against passengers on public transport (smith and Cornish 2006). extending the criminal decision process to oC, finckenauer (2007: 74) pointed out that ‘[…] it is not hard to imagine the members of a criminal organization together assessing the potential risks and benefits when considering whether to enter certain criminal markets’. starting from schelling (1971), several studies have employed the rational choice perspective to study criminal groups and their activities. These includes

oC invesTmenTs in Real esTaTe

Page 3 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

studies of the activities of various oC groups—such as Russian mafias (varese 2005), the sicilian mafia (gambetta 1996), la Cosa nostra (Reuter 1984), the Japanese yakuza (hill 2006) and the Chinese Triads (Chiu 2002)—as well as recruitment (Campana and varese 2013) and punishment (smith and varese 2001) in mafia groups. furthermore, other studies have applied a situational crime prevention approach to oC (Clarke and Tilley 2010; savona et al. 2014). however, no attempts have been made to analyse the decision-making process with regard to oC’s investment in the legal economy and, in particular, in real estate, using quantitative data.

also the application of the economic principles to explain oC’s behaviours received also critiques (liddick 1999; kleemans and de Poot 2008; kleemans 2013). The sole eco-nomic perspective would, in fact, miss key elements in oC’s decision-making process, such as manipulation, violence and social relations (kleemans and van de Bunt 1999; Bruinsma and Bernasco 2004; morselli 2005; kleemans and de Poot 2008). indeed, although kleemans (2013: 626) acknowledges that ‘there is nothing wrong with the assumption that economic motives may explain criminal activities. nor […] with the assumption that people make choice’. The same kleemans (2013) points out the ‘visible hand’—manipulation, violence and social relations—drives oC decisions more often than does the ‘invisible hand’ [market mechanisms] (Reuter 1984). Therefore, sole economic profit is not enough to explain the oC decision-making process. according to this point, and to the more general critiques of the rational choice perspective, this study does not take into account sole profitability but rather focuses on the broader advantage that criminal groups may experience when investing in real estate.

The rational choice perspective therefore seems to be a suitable framework in which to respond to the need for further investigation and empirical analysis of criminal organi-zations’ investments in real estate. in particular, the offender decision-making approach can help to answer the following questions: what are the motives behind oC groups’ investments in real estate? why do they decide to invest in some areas and not in others? how do oC groups weigh costs and rewards when deciding to invest in real estate?

an approach aimed at analysing the oC decision-making process with regard to invest-ment in real estate can yield useful results in two respects. on the one hand, it can develop the rational choice perspective by applying it to new, under-explored and complex crimi-nal phenomena, such as oC investment in the legal economy. on the other hand, it can increase knowledge about oC and its criminal decision-making process. This study’s results may also bring useful elements of discussion to the current debate concerning oC groups’ spatial mobility, with a specific reference to italian mafias. The mafias’ spa-tial mobility is a recent development of the research concerning the broader field of oC (Calderoni et al., under review; sarno, forthcoming; varese 2011a; 2011b). analysing whether or not territorial control is a determinant in the decision to invest in real estate, as this study does, may help to understand whether the mafia is mainly a local (Reuter 1984; gambetta 1996) or transnational phenomenon (sterling 1994; Castells 2003).

The Present Study

This study’s purpose is to investigate quantitatively the decision-making process of oC investments. in particular, the focus of the research is on the drivers that orient italian mafias’ investments in the italian real estate sector.

dUgaTo eT al.

Page 4 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

italy is a suitable case study for several reasons. first, in countries where investments in real estate represent a tradition, a greater likelihood exists that criminal organiza-tions’ investments will follow the same patterns as observed for legal actors (shelley 2013). a recent study by Censis and aBi (2011) reports that real estate is still the main investment for many italian families. in fact, 81 per cent of italians live in a self-owned property, a percentage well above the european average of 61 per cent. secondly, pre-vious studies have already highlighted italian mafias’ inclination to invest in land, buildings and flats more than in financial stocks and shares (svimez 1997; Transcrime 2013). moreover, given the importance and pervasiveness of italian mafias in a large part of the country (Calderoni 2011; Transcrime 2013) and the frequency of cash pay-ments often used to infiltrate the legal economy and to hide the illegal origin of money (ardizzi et al. 2012), italy seems to be particularly subject to mafias’ investments in real estate.

Considering these reasons, this study applies a rational choice approach to analyse the effects of risk and reward on the italian mafias’ decisions to invest in real estate. in particular, the study analyses 8,092 italian municipalities using data between 2000 and 2012 to test three main hypotheses.

hypothesis 1a: italian mafias invest where their economic rewards are higher.

applying a rational calculation, italian mafias should acquire or build real estate prop-erties in those municipalities where their investment will be more profitable or con-venient. in particular, a criminal group’s investment in real estate can be considered cost-effective in two main situations. first, when the values of the real estate rise signifi-cantly after the purchase. This means that a property bought for a medium-low price can be resold or leased for a considerably greater amount of money. This situation is typical of areas of new urbanization, re-development or transformation. a second cir-cumstance that ensures a profitable investment is the purchase of real estate in already valuable areas. in this case, the investment’s effectiveness is not connected to change in the property’s value but to the greater quantity of revenues from illicit proceeds that can be laundered through the purchase. moreover, high incomes can derive from the legal use of the property (e.g. rents for houses or profits for shops or land).

hypothesis 1b: italian mafias invest in areas where their symbolic rewards are higher.

economic return is not the only or main reward connected to investments in real estate. indeed, the concept of reward can also have other meanings, such as prestige and social consensus. on the one hand, the acquisition of properties in an area can give a symbolic advantage to the organization by emphasizing its presence and capacity to control the area. on the other hand, mafia members may prefer to acquire proper-ties for personal use in an affluent environment to guarantee them a better quality of life and greater social prestige. Therefore, concentrations of properties in valuable municipalities not only is evidence that criminal groups invest in rich areas for eco-nomic purposes but also may be proof that they are interested in those areas due to reputational rewards.

hypothesis 2: italian mafias aim to minimize the risks of their investments.

Besides rewards, it is therefore likely that italian mafias will invest in areas where they exert closer territorial control and where the risk of law enforcement agencies’ intervention is

oC invesTmenTs in Real esTaTe

Page 5 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

lower. indeed, this study’s second main hypothesis is that criminal groups tend to acquire real estate properties in areas where they are more present and influential. This assump-tion is supported by the consideration that mafia groups may want to maintain direct con-trol of their investments, following a loss-averse behavioural scheme, and therefore seek to reduce the risks of their investments. This control can be direct or indirect. The former is applied by ensuring a physical presence (e.g. by personally collecting rents), whereas the latter can be ensured by using social or political connections to manage administrative procedures regarding the properties (e.g. renovation, variation in use classification) or to prevent counter-measures by law enforcement agencies or other authorities.

hypothesis 3: some italian mafias are more prone to invest in real estate than are others.

after testing the two main hypotheses, the study will focus on various italian mafias attitudes towards investment in real estate. Because the main mafias differ widely in organizational and operational terms, it is likely that their choices regarding invest-ments differ as well (Paoli 2002; Transcrime 2013).

Before the methodology and the analysis are presented, it should be pointed out that the existing literature often considers a criminal organization as a collective group, attributing the investments to the organization as a whole rather than to its individual members. however, this may not always be the case because individuals could decide to invest autonomously. nonetheless, given the difficulties of differentiating between investments responding to a group strategy or to personal interest, this article generi-cally refers to mafias investments in real estate, acknowledging that either individuals or the group may make them.

Data and Method

Dependent variable

in order to analyse how italian mafias invest in the real estate sector, this study uses data on confiscated properties.1 Confiscated assets are considered a proxy of mafia groups’ invest-ment decisions. Previous studies on oC investments have prompted this methodological choice. indeed, although data on confiscated assets may yield an outdated picture of the phenomenon or may overrepresent geographic areas or property categories particularly vulnerable to or targeted by law enforcement activities, they are still widely used as the most reliable proxy for oC assets (van duyne and soudijn 2009; Riccardi 2014; Transcrime 2013).

data on confiscated properties were collected from 2000 to 2011 at the municipal level through anBsC, the italian agency for the management of sized and Confiscated assets. The macro-category of real estate includes various types of goods that, given their shared characteristics, have been aggregated into three subcategories: houses, land and a residual group ‘other’, which includes garages/lock-ups, storehouses, cel-lars, shops, barns and other properties (Table 1).

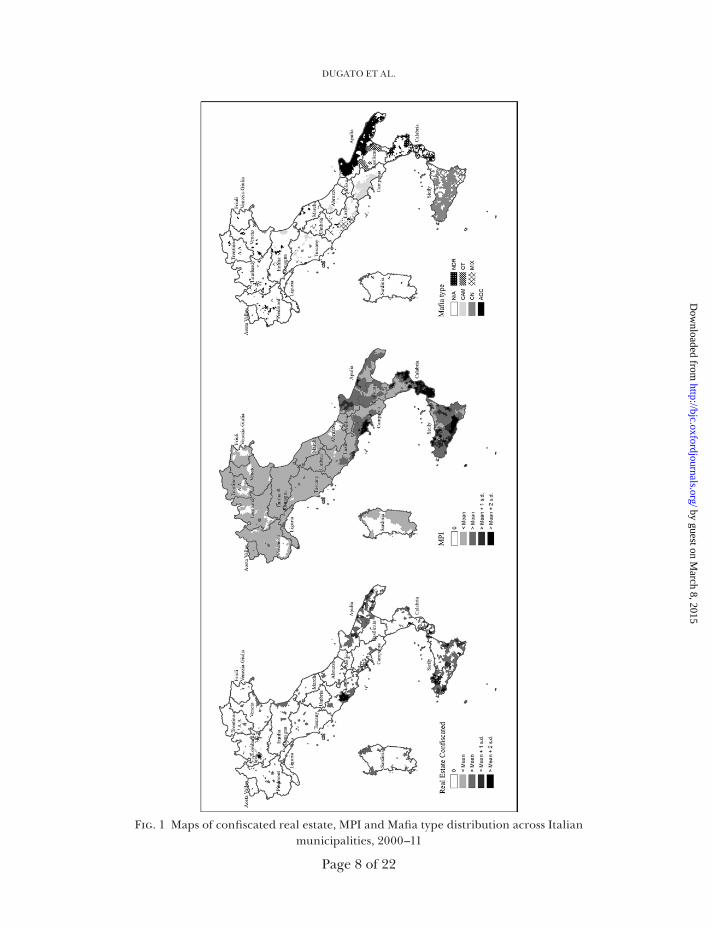

from a geographical point of view, real estate confiscations are not equally distrib-uted across regions (figure 1). The highest number of properties was confiscated in

1 it should be noted that not all of the real estate properties considered have been confiscated from members of italian mafias; indeed, the available data do not allow for distinguishing the crime that caused the confiscation. however, considering the information available and interviews with italian law enforcement representatives, and given that a large majority of confisca-tion warrants concern members of italian mafia groups, it is likely that these distortions are uninfluential (Transcrime 2013).

dUgaTo eT al.

Page 6 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

the traditional mafia territories in the south of italy. sicily is the region with the high-est amount of real estate confiscated: of 3,335 properties, 2,097 were in the province of Palermo alone. large numbers of confiscations are also recorded in Calabria (977) and Campania (729). in the north, lombardy (674) and Piedmont (67) register, the highest values even though the number of properties confiscated in the former region is more than ten times higher than the number confiscated in the latter. in Central italy, lazio (372), the region in which Rome is located, records the highest number of confiscations. The confiscated properties and their disaggregation into different categories will be the dependent variables in what follows.

Explanatory variables

according to hypotheses 1a and 1b, italian mafias’ members are likely to acquire real estate in valuable areas in order to make a cost-effective investment or to have reputa-tional rewards. as said, from an economic perspective, an investment in real estate can be considered valuable if the property’s value significantly rises after the purchase or if it is already located in a valuable area. The data available allowed only the second circumstance to be verified. indeed, the dataset of confiscated assets does not report the dates when oC purchased the properties so that changes in their values cannot be tracked. however, it was possible to collect data on average real estate values in the italian municipalities.2 it was assumed that the higher the real estate values, the more the area could be considered valuable from an economic and a reputational point of view. The average real estate values per municipality were collected for the second half of 2011 from the italian Real estate and land Registry agency (agenzia del Territorio), and they are expressed in euros per square meter (Table 1).3

Table 1 Descriptive statistics of the dependent and explanatory variables

statistics Real estate houses land other Real estate values mPi

Count 8,092 8,092 8,092 8,092 8,092 8,092sum 7,129 3,001 1,600 2,528 –a –a

mean 0.88 0.37 0.20 0.31 869.40 19.05standard deviation

15.93 7.99 1.66 7.34 469.21 64.08

min. 0 0 0 0 228.41 0max. 1,335 652 48 635 8,640.74 1,000

asums for real estate values and mPi are not informative.

2 The average real estate values were calculated while taking into account the monetary values of all types of real estate, both domestic (such as apartments, villas or independent houses) and commercial (such as, shops, warehouses, offices and sport facilities). The average value was calculated for each municipality.

3 it was not possible to obtain data on real estate values at the municipality level for all of the considered period (2000–11). This may be challenging if considering the world economic crisis that could have determined a downturn in the real estate sector. however, in italy, the crisis only partially affected this sector, resulting in a drop only in the amount of buying and sell-ing, whereas the real estate values remained fairly stable (giansante 2012). moreover, the analysis of information from several reports on this topic supports the idea that the crisis in the real estate sector was generalized and constant in all of the country and did not affect specific areas (aiTeC 2012; omi - aBi 2014). Thus, the data on 2011 can be used as a proxy for identifying the most valuable areas of the country, knowing that although the prices of lands and houses may have changed in recent years, the relative distance between the most expensive areas and the less expensive ones remained mostly constant. in other words, the relative ranking of the italian municipalities according to their real estate values remains rather stationary in the period considered.

oC invesTmenTs in Real esTaTe

Page 7 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

fig. 1 maps of confiscated real estate, mPi and mafia type distribution across italian municipalities, 2000–11

dUgaTo eT al.

Page 8 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

To test whether italian mafia groups tend to invest where it is less risky to acquire real estate, the confiscated properties were correlated with the mafia presence in the italian municipalities. This measure can be considered a proxy for direct or indirect mafia control. if a specific mafia group is present and has control over a specific municipality, it can be assumed that it is less risky for that criminal group to invest and launder money in that territory. The mafia presence was measured by means of a modified version of the mafia Presence index (mPi) developed by Transcrime (2013).4 Briefly, the index is a composite indicator resulting from the combination of four variables collected at the municipal level: mafia homicides and attempted mafia homicides from 2004 to 2011; people reported for mafia conspiracy from 2004 to 2011; municipalities and public authorities dissolved for mafia infiltration from 2000 to august 2012; and active groups reported by the italian direzione investigativa anti-mafia (dia) and the italian direzione nazionale anti-mafia (dna) from 2000 to 2011. The values range from 0, which denotes no mafia presence, to 1,000, which represents the maximum incidence (Table 1). in general, the italian mafias are pre-sent in all of the country’s regions, but areas with a very high level of mafia activity are limited and concentrated. The highest values are recorded in southern regions with a traditional mafia presence, although the intensity varies significantly even within these areas (figure 1).

The third step of the analysis considered how italian mafias differentiate their invest-ments and which groups tend to invest more in the real estate market. Because the data available on confiscated properties did not report the name of the affiliation of the previous owners, the assignment of confiscated real estate to an oC group was not directly possible. Consequently, an indirect approach was used comparing the exclusive presence of the main italian criminal organizations with the number of real estate properties confiscated. in other words, the presence of each of the main italian mafias was mapped at the municipal level starting from analysis of the dia and dna reports between 2000 and 2011.5 Those reports include detailed information on italian mafias’ activities and presence, collected through law enforcement agencies’ investiga-tions. starting from this information, a set of six dummy variables was created. They scored a value of 1 if the corresponding mafia was exclusively present in a municipal-ity and 0 otherwise. four of these variables corresponded to the main italian mafias (i.e. Camorra, Cosa nostra, apulian oC and ‘ndrangheta); one variable represented other minor organizations (e.g. Basilischi or mala del Brenta), whereas the last variable described the simultaneous presence of multiple mafias active in the same areas. These variables differ from the mPi because the latter collects information from multiple sources and represents the intensity of the presence of mafia type organizations in cer-tain municipalities without distinguishing among groups.

4 The methodology used to create the mPi is based on the original work by Calderoni (2011), which focused on measuring the mafia presence at the provincial level in all of the italian provinces from 1983 to 2009. Transcrime (2013) updated, refined and extended this index, taking new data sources into account, using data from the last available years, restricting the period observed, measuring mafia presence at the municipal level, dividing mafia presence by different types of oC and distributing the results according to the presence of the phenomenon in the surrounding areas. The index used for this study is a further elaboration by the authors and differs from the Transcrime index because it is calculated without considering the goods con-fiscated from oC.

5 The analysis identified for each municipality the number of active criminal groups and their organizations. for simplicity’s sake and considering the reports analysed, the groups were classified according to five possible types of italian mafias: Cosa nostra, Camorra, ‘ndrangheta, the apulian oC and other oC. more information can be found in the Project noP security: mafia investments. Report line 1 (Transcrime 2013).

oC invesTmenTs in Real esTaTe

Page 9 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

The mapping process produced the results shown in figure 1. The Camorra (Cam) is present without competitors in 288 (3.6 per cent) municipalities, and it is the group most exclusively present in the italian municipalities. The second mafia is the ‘ndrangheta (ndR), which exclusively appears in 272 (3.4 per cent) municipalities, followed by Cosa nostra (194, 2.4 per cent) and apulian oC (149, 1.8 per cent).

Control variables

The three above-described hypotheses concerning the risks and rewards of italian mafias’ investments in real estate were tested while controlling for the resident popula-tion, the degree of urbanization, whether or not the municipality is a provincial chief town and the oC investment in companies.

The resident population was used to control for municipality size and for the purpose of comparability. data on resident populations were collected for the year 2011 from the national statistical office (isTaT). The degree of urbaniza-tion was introduced into the analysis, considering the greater number of oppor-tunities to invest in an urban context rather than in a rural area, regardless of mafia members’ intention to buy or build a property. for this reason, not con-trolling for the level of urbanization may have a distortive effect in relation to investments in the real estate market. The italian municipalities were classified into three categories according to their degree of urbanization, as defined by the national statistical office (isTaT) in the year 2001. moreover, also, the fact that a municipality was a chief town was taken into account in order to avoid distortive effects due to these towns’ important roles in the surrounding area. indeed, the 118 provincial chief towns are usually centres of economic and political interest, and they concentrate a larger number of investments in real estate simply because they are more attractive to investors.

acquiring or creating companies is another way in which mafias can invest in the legal economy. however, these investments are likely to have drivers different from those orienting the real estate market. nevertheless, it is highly likely that where criminal groups control companies, they will also own properties and real estate functional to those economic activities (i.e. shops, barns, warehouses). Therefore, it may be that a par-ticular concentration of confiscated real estate in a municipality is not due to criminal groups’ intention to invest in the real estate market but to the presence of investments in other economic activities. This potential distortion was controlled while considering the number of confiscated companies that the anBsC collected from 2000 to 2011 in each italian municipality.

Method

given the countable nature and the skewed distribution of the dependent variables, the hypotheses were tested using a set of negative binomial regression models. This statisti-cal technique was preferred to a Poisson regression model because the dependent vari-ables considered were overdispersed, meaning that their conditional variance exceeded

dUgaTo eT al.

Page 10 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

their conditional mean (long 1997; hilbe 2011).6 The negative binomial regression is widely used for crime and criminal justice data (walker and maddan 2012).

finally, considering that using the moran’s i statistics resulted in a positive and sig-nificant spatial autocorrelation of the number of confiscated real estate among the italian municipalities, a spatially lagged dependent variable was added to each model. incorporating this factor in the models is crucial because ignoring the spatial autocor-relation of the dependent variable could lead to underestimating the real variance of the data, thus generating inefficient and biased estimates (Bailey and gatrell 1995; ward and gleditsch 2008).

Results and Discussion

The first negative binomial regression model (model 1) reported in Table 2 analysed the relationship between the amount of real estate confiscated and real estate values in the italian municipalities. with all of the control variables kept constant, it emerges that the two variables are not significantly correlated. hence, italian mafias do not seem to adopt a merely rational approach and do not invest in real estate in those areas of the country where their rewards could be greater.

Table 2 summarizes the results of the regression model (model 2), which included the mPi as an indicator of the presence of mafia groups. The findings support the hypothesis that italian mafias tend to invest in areas where they can better control their investments, thus minimizing their risks. The incidence Rate Ratio (iRR) suggests that the number of real estate properties in a municipality increases by approximately 113 per cent with every one-unit increase in the mPi. This relation-ship seems robust and highly significant. another interesting result of the regres-sion model is that, controlling for the presence of mafia groups, the average real estate value appears positively and significantly associated with the incidence of the investments. indeed, the iRR value indicates that a one-unit increase in real

Table 2 negative binomial regression models testing the relationships between the number of confiscated real estate (dependent variable), the real estate values and the mPi in the italian municipalities (N = 8,092)

model 1 model 2

Β iRR β iRR

Real estate values 0.073 1.076 0.221** 1.247mPi – – 0.757*** 2.132Real estate (lag) 0.144** 1.155 0.087*** 1.091Population 0.417 e-04*** 1.000 0.366 e-04*** 1.000degree of urbanization 0.401 1.493 0.436*** 1.546Chief town −1.187 0.305 −0.759 0.468Confiscated companies 0.863 2.370 0.678*** 1.969Constant −2.894 0.055 −3.068*** 0.046BiC −64721.26 −64957.79mcfadden’s R2 0.103 0.130

*** p < 0.01, ** p < 0.05, * p < 0.1.

6 The overdispersion was assessed using a test of significance of the dispersion parameter (α). for all of the regression models, this parameter was significant, evidencing the overdispersion of the dependent variables.

oC invesTmenTs in Real esTaTe

Page 11 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

estate values is connected to an increase of about 25 per cent in the counts of con-fiscated properties.

a comparison of the outcomes of these two regression models suggests that the reward is probably only a secondary factor in orienting mafias’ investments, whereas the primary driver of their choices seems to be risk reduction. indeed, the signifi-cance of the connection between real estate values and mafias’ investments, with the presence of the criminal groups kept constant, could be interpreted as mafia groups’ tendency to prefer guaranteed investments with a lower risk. only when the investments can be considered safe do they consider the possible rewards and seek to maximize their return.

further questions now arise: what kind of reward has greater weight in the decision to purchase a property? are the economic revenues more important than are other fac-tors, social or symbolic? in fact, considering that the available data do not distinguish between real estate purchased for personal use or for purely economic reasons, it can-not be excluded that this outcome simply denotes mafia members’ intent to purchase properties that could guarantee a higher quality of life, provide social prestige or show their influence in the area.

as already mentioned, the information available cannot be used to test these last arguments directly. however, the regression models reported in Table 3 suggest an indirect approach. The basic assumption is that social and symbolic motives are likely to affect almost exclusively the choice to invest in houses. other kinds of real estate, such as land, parking lots or industrial buildings, which have a clearer commercial or economic function, are less likely to be purchased for reasons other than monetary returns. Therefore, the following negative binomial regression models replicate the same analysis as model 2 (Table 2), but they consider differ-ent categories of real estate as dependent variables—respectively, houses, land and other properties.

Table 3 negative binomial regression models testing the relationships between the number of confiscated real estate by type (dependent variables), the real estate values and the mPi in the italian municipalities (N = 8,092)

model 3 (houses) model 4 (lands) model 5 (others)

β iRR Β iRR β iRR

Real estate values 0.267*** 1.306 0.120 1.128 0.095 1.100mPi 0.641*** 1.899 0.527*** 1.694 0.667*** 1.948houses (lag) 0.112*** 1.119 – – – –land (lag) – – 0.653*** 1.920 – –other (lag) – – – – 0.121** 1.128Population 0.31 e-04** 1.000 0.106 e-041.000 0.291 e-04*** 1.000degree of urbanization 0.410** 1.507 0.185 1.203 0.652*** 1.919Chief town −0.753 0.471 −0.048 0.953 −0.728 0.483Confiscated companies 0.578*** 1.783 0.670*** 1.954 0.560*** 1.750Constant −3.741*** 0.024 −3.863***0.021 −4.209*** 0.015BiC −67706.05 −68989.05 −68033.35mcfadden’s R2 0.175 0.168 0.165

***p < 0.01, **p < 0.05, * p < 0.1.

dUgaTo eT al.

Page 12 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

The findings summarized in Table 3 seem to suggest, though indirectly, the impor-tance of social and symbolic factors in influencing oC choices, rather than economic ones. indeed, the results show that real estate values remain significantly associated only with the presence of houses. in particular, the number of houses confiscated in a municipality increases by approximately 30 per cent with every one-unit increase in the average real estate value. instead, for lands and other properties, the association between the number of real estate properties and their economic value is non-significant.

These results could be interpreted in different ways. on one side, they may suggest that italian mafias invest for economic purposes only in houses, whereas other motiva-tions drive the acquisition of lands and other properties. however, this interpretation seems doubtful for two reasons. first, the nature of these latter categories suggests that non-economic motives should be marginally influential for these types of investment. in other words, lands or warehouses are less likely to be purchased to gain prestige or social consensus with respect to villas or residential buildings that can be more easily intended as a means for showing wealth or social status or for providing or renting resi-dences to affiliates or the local population.

second, houses represent less than half (42 per cent) of the italian mafias’ confis-cated properties. This value probably also comprises a relevant share of members’ pri-vate residences, thus reducing the number of houses that could actually be considered pure economic investments. Therefore, the share of houses purchased or built for eco-nomic reasons is relatively low in comparison with the other categories. This is espe-cially true if considering houses as the unique and preferred type of mafias’ investment in the real estate sector.

on the other hand, these findings may confirm that among the possible rewards, prestige and social consensus are likely to be more important than economic profit is for italian mafias. of course, these findings and interpretations have to be considered cautiously because the available data do not allow the possibility to directly verify them.

The last hypothesis concerns italian mafias’ differing behaviours regarding their investments in real estate. Table 4 reports the results of the negative binomial regres-sion model including the six dummies, which identify the exclusive presence of the various mafias in the municipalities (model 6). Before these outcomes are analysed, two considerations are in order. first, the dummy variables do not express the inten-sity of each organization’s presence in the area, only its presence. Thus, the resulting coefficients should be read while considering an equal level of mafias’ threats, as the effect of the mPi is kept constant. second, the reference category is the absence of identified criminal groups in the municipality. These results suggest that the presence of almost all of the italian mafias, irrespectively of whether this presence is high or low, is positively and significantly associated with a number of real estate properties higher than that recorded on average in the municipalities not affected by this criminal phenomenon.

This is not surprising, given that only 4.6 per cent of the municipalities for which it was impossible to retrieve information on a mafia presence recorded at least one real estate investment. it is likewise unsurprising that the only type of mafia presence not significantly different from the absence of criminal groups is the ‘other’ category (oT), which comprises marginal groups.

By contrast, the mafias that seem to have stronger connections with investments in real estate are Cosa nostra (Cn), apulian oC (aoC) and the combined presence of

oC invesTmenTs in Real esTaTe

Page 13 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

several mafias in the same area (miX). in particular, the exclusive presence of Cosa nostra groups in a municipality increases the count of real estate investments by approximately 1,050 per cent more than that of those municipalities that do not record any mafia group. with regard to apulian oC, this increase amounts to almost 736 per cent, whereas in the miscellaneous situations, the change is about 611 per cent. several possible explanations exist for these findings. firstly, the results regarding Cosa nostra are not surprising, bearing in mind that sicily (i.e. Cosa nostra’s native region) is the italian region with the largest number of confiscated goods (Transcrime 2013). moreover, Cosa nostra has traditionally invested in the construction sector (sacco 2010). This peculiarity is clearly reflected by the high number of companies confiscated from Cosa nostra in the construction sector (42 per cent of the total), compared with the lower percentages for other mafias (e.g. 21 per cent for Camorra, 23 per cent for ‘ndrangheta and 5 per cent for apulian oC) (Transcrime 2013).

The interpretation for apulian oC is more complex. however, the reason for this result may be that this organization is less likely than other mafias to extend its influ-ence beyond its traditional borders. Thus, it probably prefers to purchase real estate in its own territory, which can be directly controlled, rather than invest outside of it. This behaviour is also confirmed when comparing various italian criminal organiza-tions’ preferences with regard to investment in companies. almost 91 per cent of the companies that apulian oC confiscated are located in the apulia region, whereas the percentage of companies belonging to ‘ndrangheta members confiscated in Calabria (i.e. the ‘ndrangheta’s native region) is slightly above 51 per cent of the total.7

a separate explanation is required for the municipalities recording a multiple pres-ence of italian mafias. in most cases, those areas are medium or big cities located

7 analysis was conducted by the authors on data regarding confiscated companies in italy (1983–2012). source: anBsC.

Table 4 negative binomial regression model testing the relationships between the number of confiscated real estate (dependent variable), the real estate values, the mPi and the type of mafia present in the italian municipalities (N = 8,092)

model 6

β iRR

Real estate values 0.318*** 1.374mPi 0.391*** 1.478Cam 0.847** 2.334Cn 2.445*** 11.534aoC 2.123*** 8.357ndR 1.563*** 4.774oT 0.393 1.481miX 1.961*** 7.109Real estate (lag) 0.049*** 1.050Population 0.114 e-04 1.000degree of urbanization 0.573*** 1.773Chief town −0.011 0.989Confiscated companies 0.549*** 1.732Constant −3.413*** 0.033BiC −65079.70mcfadden’s R2 0.150

*** p < 0.01, ** p < 0.05, * p < 0.1.

dUgaTo eT al.

Page 14 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

outside of the regions that mafias have traditionally influenced. Therefore, their attrac-tiveness is due to their average greater wealth and mafias’ potential opportunity to expand their influence in other areas of the country.

in conclusion, in order to better define this analysis’ findings and help the reader to understand them, Table 5 presents a summary of the study’s main hypotheses and results.

Conclusion

This study had two main objectives. on the one hand, it sought to increase knowledge about oC’s investments in the real estate sector. a review of the existing literature has highlighted that to date, this topic has been largely neglected despite its great impor-tance and its potential consequences. on the other hand, this study applied a risk–reward approach to analyse quantitatively the main drivers of investment decisions of this kind. indeed, also considering the promising results obtained by analyses of other complex crimes (i.e. drug trafficking), this perspective could provide important new insights into the problem and improve the targeting of counter-measures. These pur-poses have been pursued in exploring the case of italian mafias’ investments in the real estate sector.

The outcomes of the analysis support this approach’s validity, and they suggest inter-esting findings on the behaviours of italian mafias when they invest in the legal econ-omy. first, risk seems to be the primary factor orienting their decisions. The choice of the area in which to invest seems closely correlated with the organization’s capacity to control that area, thus reducing potential costs and threats. otherwise, the reward appears to be only a secondary driver. in particular, although the results obtained are only partial and further analysis is needed, the analysis seems to suggest that the eco-nomic return is less important than are rewards of other kinds, such as prestige, social consensus or the ability to mark an organization’s presence in the territory. moreover, an indirect analysis of the behaviours of individual organizations highlights that

Table 5 Summary of the main hypotheses and results

hypotheses Results of the analysis

Rewards 1a - italian mafias invest in areas where their economic rewards are higher.

• Italian mafias do not invest in real estate in those areas where their rewards could be greater.

• The reward seems only a secondary factor in orienting mafias’ investments.

1b - italian mafias invest in areas where their symbolic rewards are higher.

• Some evidences seem to support the hypothesis that symbolic rewards are more influential than economic ones are.

Risk 2 - italian mafias invest while trying to minimize the risks of their investments.

• The possibility of controlling the investments and reducing their risks appears to be the primary driver guiding the italian mafias’ investments in real estate.

differences among italian mafias

3 - some italian mafias are more prone to invest in real estate than others are.

• The presence of Cosa Nostra, Apulian OC and the combined presence of several mafias in the same area seems to have stronger connections to investments in real estate.

oC invesTmenTs in Real esTaTe

Page 15 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

different criminal groups may have different approaches. indeed, some mafias (i.e. Cosa nostra and apulian oC) seem more prone to invest in real estate than others are.

obviously, this analysis focused only on italian mafias, and therefore, the results obtained may not be generalized to other criminal groups or syndicates worldwide. however, this study introduces a new approach to the analysis of the topic that, aside from the individual findings that may only have local relevance, could be applicable to other geographical contexts or investment sectors.

moreover, this research supports the idea that, according to the rational choice theory, criminal organizations could be considered rational actors weighing risks and rewards. The findings obtained confirm those of previous research on the criminal decision-making process. indeed, studies on drug dealers (Reuter and kleiman 1986) or burglars have noted that, from the offenders’ perspective, ‘losses are felt more acutely than gains’ (wortley 2014: 242). in other words, although almost all criminal groups decide to com-mit a crime in order to gain a reward, the risk of losing control over the property or of law enforcement agencies’ intervention seems to be the primary driver of their decisions.

moreover, this study seems to support to the current literature regarding mafia groups’ mobility. Two opposite views exist concerning this. The first argues that the mafia is a local phenomenon and a ‘trademark’ that is difficult to export (Reuter 1984; gambetta 1996). The second states that globalization offers several opportunities for criminal groups to move across territories and settle in new countries (williams 1994; Castells 2003; shelley et al. 2003). The literature shows that in some instances, mafia groups can successfully move to new territories (varese 2006; morselli et al. 2011; varese 2011a), although their settlement can take place under certain conditions and in different forms.8 This study shows that mafia groups do move across territories, but their decision to invest in new areas is highly dependent on perceived risks and ter-ritorial control. according to Campana (2011a: 224), mafias in their decision to move to new territories can transplant their core business (supply of protection) or diversify their activities and engage just in some specific activities, such as investment in legal activities (Campana 2011a; 2011b). however, this study shows that even the sole deci-sion to invest in real estate (functional diversification) is unlikely if mafia groups are not active in the territory. as varese (2011a: 20) points out, ‘investments can go wrong, and the bosses back home cannot easily verify claims and reports. This situation gener-ates specific incentives for bosses to go abroad to monitor transactions with legitimate entrepreneurs directly’. mafia groups may invest in new areas due to profitability and the investment’s possible rewards. however, their decision to invest in these territories seems conditional upon the minimization of the risks.

These conclusions also have important consequences in terms of policy recommen-dations to counter oC. academics and practitioners often see oC from two divergent perspectives: one oriented towards how they make profits (with investments in legal or illegal markets), the other more oriented towards their activities relative to territorial control (violence, homicide, racketeering, etc.) or social consensus. in this perspec-tive, Block (1980) conceptually divides oC into power syndicates, which aim to achieve territorial control, and enterprise syndicates finalized at the accumulation of wealth.

8 varese (2006; 2011a; 2011b) and, similarly, sciarrone and storti (2014) identified intentional (resource-seeking, investment-seeking and market-seeking) and unintentional movements (generalized migration, forced resettlement, escaping mafia wars or police repression) as well as local conditions facilitating territorial expansion (the demand for illegal protectors and develop-ment of new markets).

dUgaTo eT al.

Page 16 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

This study has shown that these two perspectives are intrinsically related because oC organizations’ economic choices are strongly influenced by the risks they face, and their investments could be limited by acting against their traditional activities and reducing their territorial control (Campana 2011a; varese 2011a). several reports have highlighted the relevance of anti-money laundering regulations in fighting illicit finan-cial flow and oC (van der does de willebois et al. 2011; faTf and oeCd 2012; Unger et al. 2014). however, as Campana (2011a: 224) underlines: ‘implementing a tight dis-cipline against money laundering […] may have an impact in tackling the investments in the legal economy of a given group. Yet this measure will have little impact on the same group […]. Conversely, it is the core business [illegal protection and extra-legal governance] that guarantees and almost uninterrupted stream of criminal revenues’.

furthermore, this study has a methodological importance. The past 30 years have seen a vast amount of studies on oC and mafia phenomena. nevertheless, few attempts have been made to analyse these phenomena using an empirical and quantitative approach (lavezzi 2008; Calderoni 2011; Caneppele et al. 2013). The shortage of avail-able data and methodological drawbacks have probably hindered scholars and academ-ics from making such attempts. This study has shown how, using proper methods and data, empirical and quantitative approaches can improve knowledge about oC and help to provide policy recommendations.

of course, this study has its limitations. firstly, the available data and information do not allow for more precise and disaggregated analyses. for instance, it was not possible to precisely track real estate properties from their building to their con-fiscation. missing information about the affiliation of the owners of the properties prevents precise attribution of investments to mafia groups. This lack of information may have had a distortive effect on the results, so it was not possible to analyse some dynamics of the decision-making process in detail. moreover, the availability of only data on confiscated assets may have biased the final findings by removing a part of the phenomenon (i.e. unidentified properties) and concealing some alternative or emerging behaviours. finally, the available data refer only to assets located in italy. Therefore, it was not possible to investigate if italian mafias act differently in other countries.

in conclusion, the findings that emerged from this analysis are promising. however, given the analysis’ limits, further research on the factors orienting criminal organiza-tions’ decision-making process is needed. improving the analysis by using more sophis-ticated techniques or detailed data may yield a more thorough understanding of the issue and more effective counteracting policies. indeed, understanding what factors are crucial for criminal organizations’ investments may help law enforcement agencies or other relevant stakeholders to strengthen control and work to reduce the attractive-ness of specific areas or sectors.

References

abadinsky, h. (2010), Organized Crime. wadsworth/Cengage learning.aiTeC (2012), Il mercato immobiliare italiano: tendenze recenti e prospettive. aiTeC.alexander, B. (1997), ‘The Rational Racketeer: Pasta Protection in depression era

Chicago’, The Journal of Law and Economics, 40: 175–202.

oC invesTmenTs in Real esTaTe

Page 17 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

ardizzi, g., Petraglia, C., Piacezzo, m. and Turati, g. (2012), Measuring the Underground Economy With the Currency Demand Approach: A Reinterpretation of the Methodology, With an Application to Italy. Banca d’italia.

arlacchi, P. (2007), La mafia imprenditrice: dalla calabria al centro dell’inferno. il saggiatore.Bailey, T. C. and gatrell, a. C. (1995), Interactive Spatial Data Analysis. John wiley & sons.Barry, B. and hardin, R. (1982), Rational Man and Irrational Society? An Introduction and

Sourcebook, 1st edn. sage Publications, inc.Beauregard, e. and leclerc, B. (2007), ‘an application of the Rational Choice approach

to the offending Process of sex offenders: a Closer look at the decision-making’, Sexual Abuse: A Journal of Research and Treatment, 19: 115–33.

Becchi, a. and Rey, g. m. (1994), L’economia criminale. laterza.Becker, g. s. (1968), ‘Crime and Punishment: an economic approach’, Journal of Political

Economy, 76: 169–217.——. (1978), The Economic Approach to Human Behavior. The University of Chicago Press.Block, a. a. (1980), East Side West Side. Organizing Crime in New York 1930–1950. University

College Cardiff Press.Bouchard, m. and wilkins, C. (2010), Illegal Markets and the Economics of Organized Crime.

Routledge.Bruinsma, g. and Bernasco, w. (2004), ‘Criminal groups and Transnational illegal

markets’, Crime, Law and Social Change, 41: 79–94.Calderoni, f. (2011), ‘where is the mafia in italy? measuring the Presence of the mafia

across italian Provinces’, Global Crime, 12: 41.——. (2014), ‘mythical numbers and the Proceeds of organised Crime: estimating mafia

Proceeds in italy’, Global Crime, 15: 138–63.Calderoni, f., dugato, m. and Riccardi, m. (2010), ‘mafia inc.: analysis of the invest-

ments of the italian mafia’. Presented to the 10th annual Conference of the european society of Criminology, 8–11 september, liege, Belgium.

Calderoni, f. and Riccardi, m. (2011), ‘The investments of organized Crime in italy: an exploratory analysis’. Presented to the 67th american society of Criminology, 16–19 november, washington dC.

Campana, P. (2011a), ‘eavesdropping on the mob: The functional diversification of mafia activities across Territories’, European Journal of Criminology, 8: 213–28.

——. (2011b), ‘assessing the movement of Criminal groups: some analytical Remarks’, Global Crime, 12: 207–17.

Campana, P. and varese, f. (2013), ‘Cooperation in Criminal organizations: kinship and violence as Credible Commitments’, Rationality and Society, 25: 263–89.

Caneppele, s., Riccardi, m. and standridge, P. (2013), ‘green energy and Black economy: mafia investments in the wind Power sector in italy’, Crime, Law and Social Change, 59: 319–39.

Castells, m. (2003), ‘The global Criminal economy’, in e. mclaughlin, h. gordon and J. muncie, eds, Criminological Perspectives: Essential Readings, 516–26. sage.

Catanzaro, R. (1988), Il delitto come impresa. Storia sociale della mafia. liviana.Censis and aBi. (2011), Gli italiani e il mattone. Censis, aBi - associazione Bancaria

italiana.Centorrino, m. and signorino, g. (eds) (1997), Macroeconomia della mafia. la nuova italia

scientifica.

dUgaTo eT al.

Page 18 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

Cherbonneau, m. and Copes, h. (2006), ‘“drive it like you stole it”: auto Theft and the illusion of normalcy’, British Journal of Criminology, 46: 193–211.

Chiu, Y. k. (2002), ‘global Triads: myth or Reality?’, in m. R. Berdal and m. serrano, eds, Transnational Organized Crime and International Security: Business as Usual? , 183–93. lynne Rienner Publisher.

Clarke, R. v. and Tilley, n. (eds) (2010), Situational Prevention of Organized Crimes. willan Publishing.

Clarke, R. v. g. and newman, g. R. (2006), Outsmarting the Terrorists. greenwood Publishing group.

Cook, k. s. and levi, m. (1990), The Limits of Rationality. University of Chicago Press.Cornish, d. and Clarke, R. v. (2008), ‘The Rational Choice Perspective’, in R. wortley

and l. mazerolle, eds, Environmental Criminology and Crime Analysis (Crime Science Series), 19–47. willan Publishing.

Cornish, d. B. and Clarke, R. v. (eds) (1986), The Reasoning Criminal: Rational Choice Perspectives on Offending (Research in Criminology). springer-verlag.

Cressey, d. R. (1969), Theft of the Nation: The Structure and Operations of Organized Crime in America. harper & Row.

elster, J. (1986), Rational Choice. Blackwell.fabre, g. (2005), Prospering on Crime: Money Laundering and Financial Crisis (working Paper

no. 9). Centre for east and south-east asian studies, lund University.fantò, e. (1999), L’impresa a partecipazione mafiosa. Economia legale ed economia criminale.

edizioni dedalo.faTf. (2008), Money Laundering & Terrorist Financing Through the Real Estate Sector. faTf.faTf and oeCd. (2012), International Standards on Combating Money Laundering and the

Financing of Terrorism & Proliferation. The FATF Recommendations. faTf and oeCd.fernandez-huerga, e. (2008), ‘The economic Behavior of human Beings: The

institutionalist/Post-keynesian model’, Journal of Economic Issues, 42: 709–26.finCen. (2008), Suspected Money Laundering in the Residential Real Estate Industry. An

Assessment Based Upon Suspicious Activity. financial Crimes enforcement network – United states department of the Treasury.

finckenauer, J. o. (2007), Mafia and Organized Crime: A Beginner’s Guide. oneworld Publications.

gambetta, d. (1996), The Sicilian Mafia: The Business of Private Protection. harvard University Press.

giansante, l. (2012), Il mercato immobiliare in Italia nella crisi. Università Politecnica delle marche.

hilbe, J. m. (2011), Negative Binomial Regression, 2nd edn. Cambridge University Press.hill, P. B. e. (2006), The Japanese Mafia: Yakuza, Law, and the State. oxford University Press.ianni, f. a. J., and Reuss-ianni, e. (1993), La criminalità organizzata come tipica impresa crimi-

nale: un nuovo indirizzo teorico presented to the conference “Tendenze della criminalità organizzata e dei mercati illegali internazionali”, napoli.

Jacobs, B. a. (1996), ‘Crack dealers’ apprehension avoidance Techniques: a Case of Restrictive deterrence’, Justice Quarterly, 13: 359–81.

kington, T. (2012), ‘Capo di tutto tacky: italian mobster’s luxury villa seized’, The Guardian, may 7.

kleemans, e. R. (2013), ‘organized Crime and the visible hand: a Theoretical Critique on the economic analysis of organized Crime’, Criminology Criminal Justice, 13: 615–29.

oC invesTmenTs in Real esTaTe

Page 19 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

kleemans, e. R. and de Poot, C. J. (2008), ‘Criminal Careers in organized Crime and social opportunity structure’, European Journal of Criminology, 5: 69–98.

kleemans, e. R. and van de Bunt, h. g. (1999), ‘The social embeddedness of organized Crime’, Transnational Organized Crime, 5: 19–36.

lavezzi, a. m. (2008), ‘economic structure and vulnerability to organised Crime: evidence from sicily’, Global Crime, 9: 198–220.

leclerc, B. and wortley, R. (2014), ‘The Reasoning Criminal: Twenty-five Years on’, in B. leclerc and R. wortley, eds, Cognition and Crime: Offender Decision Making and Script Analyses, 1–11. Routledge.

liddick, d. (1999), ‘The enterprise “model” of organized Crime: assessing Theoretical Propositions’, Justice Quarterly, 16: 403–30.

long, s. J. (1997), Regression Models for Categorical and Limited Dependent Variables, Advanced Quantitative Techniques in the Social Sciences. sage Publications, inc.

luckenbill, d. f. (1977), ‘Criminal homicide as a situated Transaction’, Social Problems Journal, 25: 176–86.

mann, R. e. and hollin, C. R. (2007), ‘sexual offenders’ explanations for Their offending’, Journal of Sexual Aggression, 13: 3–9.

morselli, C. (2005), Contacts, Opportunities, and Criminal Enterprise, 1st ed. University of Toronto Press, scholarly Publishing division.

morselli, C., Turcotte, m. and Tenti, v. (2011), ‘The mobility of Criminal groups’, Global Crime, 12: 165–88.

nee, C. and meenaghan, a. (2006), ‘expert decision making in Burglars’, British Journal of Criminology, 46: 935–49.

nelen, h. (2008), ‘Real estate and serious forms of Crime’, International Journal of Social Economics, 35: 751–62.

omi-aBi (2014), Rapporto Immobiliare 2014. agenzia delle entrate.Paoli, l. (2002), ‘The Paradoxes of organized Crime’, Crime, Law and Social Change, 37:

51–97.Reuter, P. (1985), The Organization of Illegal Markets: An Economic Analysis. national institute

of Justice.Reuter, P. and levi, m. (2006), ‘money laundering’, Crime and Justice: A Review of Research,

34: 289–375.Reuter, P. h. (1984), Disorganized Crime. The Economics of the Visible Hand. miT Press.Reuter, P. h. and kleiman, m. a. R. (1986), ‘Risks and Prices: an economic analysis of

drug enforcement’, Crime Justice, 7: 289–340.Riccardi, m. (2014), ‘when Criminals invest in Businesses: are we looking in the Right

direction? an exploratory analysis of Companies Controlled by mafias’, in s. Caneppele and f. Calderoni, eds, Organized Crime, Corruption and Crime Prevention - Essays in Honor of Ernesto U. Savona, 197–206. springer international Publishing switzerland.

sacco, s. (2010), La mafia in cantiere. L’incidenza della criminalità organizzata nell’economia: una verifica empirica nel settore delle costruzioni. edizioni Pio la Torre.

santino, U. (2006), Dalla mafia alle mafie: scienze sociali e crimine organizzato. Rubbettino.sarno, f. (forthcoming). ‘identifying Patterns of mafia mobility: The Presence of the

italian mafias in europe’ [Phd dissertation]. Università Cattolica del sacro Cuore.savona, e., giommoni, l. and mancuso, m. (2014), ‘human Trafficking for sexual

exploitation in italy’, in B. leclerc and R. wortley, eds, Cognition and Crime Offender Decision Making and Script Analyses, 140–63. Routledge.

dUgaTo eT al.

Page 20 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

schelling, T. C. (1971), ‘what is the Business of organized Crime?’, The American Scholar, 40(4): 643–52.

schneider, s. (2004), ‘organized Crime, money laundering, and the Real estate market in Canada’, Journal of Property Research, 21: 99–118.

sciarrone, R. and storti, l. (2014), ‘The Territorial expansion of mafia-Type organized Crime. The Case of the italian mafia in germany’, Crime, Law and Social Change, 61: 37–60.

shelley, l. (2013), Money Laundering into Real Estate (INSIDE TraCCC Issue 2). Terrorism, Transnational Crime and Corruption Center (TraCCC).

shelley, l., Picarelli, J. and Corpora, C. (2003), ‘global Crime inc.’, in m. k Cusimano, ed., Beyond Sovereignty: Issues for a Global Agenda, 146–66. Thomson wadsworth, florence kentucky.

simon, h. a. (1990), ‘invariants of human Behavior’, The Annual Review of Psychology, 41: 1–20.

smith, a. and varese, f. (2001), ‘Payment, Protection and Punishment the Role of information and Reputation in the mafia’, Rationality and Society, 13: 349–93.

smith, d. C. (1975), The Mafia Mystique. Basic Books.——. (1980), ‘Paragons, Pariahs, and Pirates: a spectrum-Based Theory of enterprise’,

Crime Delinquency, 26: 358–86.smith, m. J. and Cornish, d. B. (2006), Secure and Tranquil Travel: Preventing Crime and

Disorder on Public Transport. University College london, Jill dando institute of Crime science.

sterling, C. (1994), Crime Without Frontiers: The Worldwide Expansion of Organized Crime and the Pax Mafiosa. little Brown & Co.

svimez [associazione per lo sviluppo dell’industria nel mezzogiorno]. (1997), Rapporto 1997 sull’economia del Mezzogiorno. il mulino.

Transcrime. (2013), Project NOP Security 2007–2013: Mafias Investments. Report Line 1. italian ministry of interior.

Unger, B., ferwerda, J., nelen, h. and Ritzen, l. (2011), Money Laundering in the Real Estate Sector: Suspicious Properties. edward elgar Publishing.

Unger, B., ferwerda, J., van den Broek, m. and deleanu, i. (2014), The Economic and Legal Effectiveness of the European Union’s Anti-Money Laundering Policy. edward elgar Publishing.

van der does de willebois, e., halter, e. m., harrison, R. a., won Park, J. and sharman, J. C. (2011), The Puppet Masters. How the Corrupt Use Legal Structures to Hide Stolen Assets and What to Do About It. The world Bank & UnodC.

van duyne, P. C. and soudijn, m. R. J. (2009), ‘hot money, hot stones and hot air: Crime-money Threat, Real estate and Real Concern’, The Journal of Money Laundering Control, 12: 173–88.

varese, f. (2005), The Russian Mafia: Private Protection in a New Market Economy, 1st edn. oxford University Press.

——. (2006), ‘how mafias migrate: The Case of the ‘ndrangheta in northern italy’, Law & Society Review, 40: 411–44.

——. (2011a), Mafias on the Move: How Organized Crime Conquers New Territories. Princeton University Press.

——. (2011b), ‘mafia movements: a framework for Understanding the mobility of mafia groups’, Global Crime, 12: 218–31.

oC invesTmenTs in Real esTaTe

Page 21 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

walker, J. T. and maddan, s. (2012), Statistics in Criminology and Criminal Justice: Analysis and Interpretation, 4th edn. Jones & Bartlett learning.

ward, m. d. and gleditsch, k. s. (2008), Spatial Regression Models (Quantitative Applications in the Social Sciences). sage Publications.

williams, P. (1994), ‘Transnational Criminal organisations and international security’, Survival, 36: 96–113.

wortley, R. (2014), ‘Rational Choice and offender decision making. lessons from the Cognitive sciences’, in B. leclerc and R. wortley, eds, Cognition and Crime Offender Decision Making and Script Analyses, 237–52. Routledge.

dUgaTo eT al.

Page 22 of 22

by guest on March 8, 2015

http://bjc.oxfordjournals.org/D

ownloaded from

Related Documents