The Rise of Equities: Consideration of Tax-Free Deals Gerald Rokoff, Partner, DLA Piper - New Yorknsideratioof

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Rise of Equities:Consideration of Tax-Free Deals

Gerald Rokoff, Partner, DLA Piper - New Yorknsideratioof

General considerations

DRAFT- Privileged and Confidential 2

Reverse Morris Trust / Morris Trust:

Separate out a business (“Sub”) that may be a drag on equity value of the distributing corporation (“Distributing”) tax-free. Debt can also be inserted that is supported by the Sub earnings which will be tax-free Distributing until principal payments are made.

A subsequent acquisition can also be done tax-free. Distributing’s shareholders must control the combined new entity but protections for the minority shareholders can be built in. Thus, the “acquiring” company’s shareholders become minority shareholders of the acquired company which can raise social / management issues that can generally be worked out

Acquisitive:

Target can be acquired or can achieve combination benefits without a lot of cash

Key issue is agreeing on value and ratio of post-closing stock ownership

Flexibility to have part-cash / part-stock deal so those that want cash get capital gain and those that want stock can get tax-free treatment

IRS will rule in this area, but an opinion of each party’s counsel will often work as well

Recent tax-free deals

DRAFT- Privileged and Confidential 3

DLA Piper Engagement: Confidential foreign Reverse Morris Trust transaction—DLA Piper represents the foreign acquiring corporation

PPG Industries, Inc. On January, 28, 2013, PPG Industries completed the separation of its commodity chemicals business and merger of its wholly-owned

subsidiary with a subsidiary of Georgia Gulf Corporation in a Reverse Morris Trust transaction. PPG Industries received a ruling from the IRS and, as a result, the transaction was generally tax free to PPG Industries and its shareholders

Tri Pointe Homes, Inc.

Per a recent announcement (November 2013), it is anticipated that Tri Pointe Homes, Inc. will acquire Weyerhaeuser Company’s homebuilding and real estate subsidiary via a Reverse Morris Trust transaction

Liberty Media In January 2014, Liberty proposed to acquire the 48 percent of Sirius it does not already own in an all-stock deal valued at more than

$10 billion, making the satellite radio provider a subsidiary of the media conglomerate

Entergy Corporation

Prior to the deal being called off due to regulatory opposition, Entergy planned to distribute its electric transmission business, which, thereafter, was to be combined with ITC Holdings Corporation. Prior to the transaction, ITC was to right-size itself by borrowing $700 million and either distribute the proceeds to its stockholders or engage in a stock buyback. In the anticipated combination of ITC and the Entergy subsidiary, former Entergy stockholders were expected to receive 50.1% of the combined entity’s equity by vote and value. Entergy had requested a ruling letter from the IRS on the transaction

RF Micro Devices

RF Micro Devices and TriQuint Semiconductor, which make radio frequency chips, announced an all-stock merger of equals on February 24, 2014, creating a chip maker with more than $2 billion in annual revenue

Reverse Morris Trust transaction - step #1

4

Distributing

Distributing Shareholders

Target

Spin-off or Split-off

Step #1: Target is either spun off or split off to the Distributing shareholders.

Tax consequences: See the following slide.

Reverse Morris Trust transaction: step #1 tax consequences

5

Spin Off: Pro-rata

Split Off: Some swap Distributing shares for Target shares (sale for accounting purposes).

The transaction is tax free under Section 355 of the Code so long as the following requirements are met:

Distributing shareholders must own at least 50.1% of both companies

Distributing must own 80% of vote and value of Target before the transaction

Active trade or business requirements

Valid business purpose

Distributing would generally bear any resulting corporate tax except where Target engages in a transaction that causes the spin off or split off to be subject to corporate tax

Reverse Morris Trust transaction: step #2

6

Distributing Shareholders

Target

Step #2: Acquirer forms a transitory US subsidiary (“Acquirer Sub”) and contributes shares of its voting stock to Acquirer Sub for stock and possibly securities tax-free. Using the Acquirer shares as consideration, Acquirer Sub then merges with and into Target, with Target surviving, and with the Distributing shareholders receiving Acquirer voting stock

Acquirer

Acquirer SubReverse

Triangular Merger

Tax consequences:

The reverse triangular merger would constitute a tax-free reorganization under Section 368(a)(2)(E) of the Code

To avoid taxation of the spin off or split off to Distributing, the Distributing shareholders, in the aggregate, would need to receive more than 50% of the outstanding Acquirer stock. There would be flexibility to reduce the value of Target – so that the Distributing shareholders’ ownership of Acquirer would not be substantially greater than the minimum majority interest of 50.1% -- by causing Target to take on debt prior to the transaction, the proceeds of which would stay with Distributing. The obligation to repay the debt would travel with Target and ultimately become an obligation of Acquirer

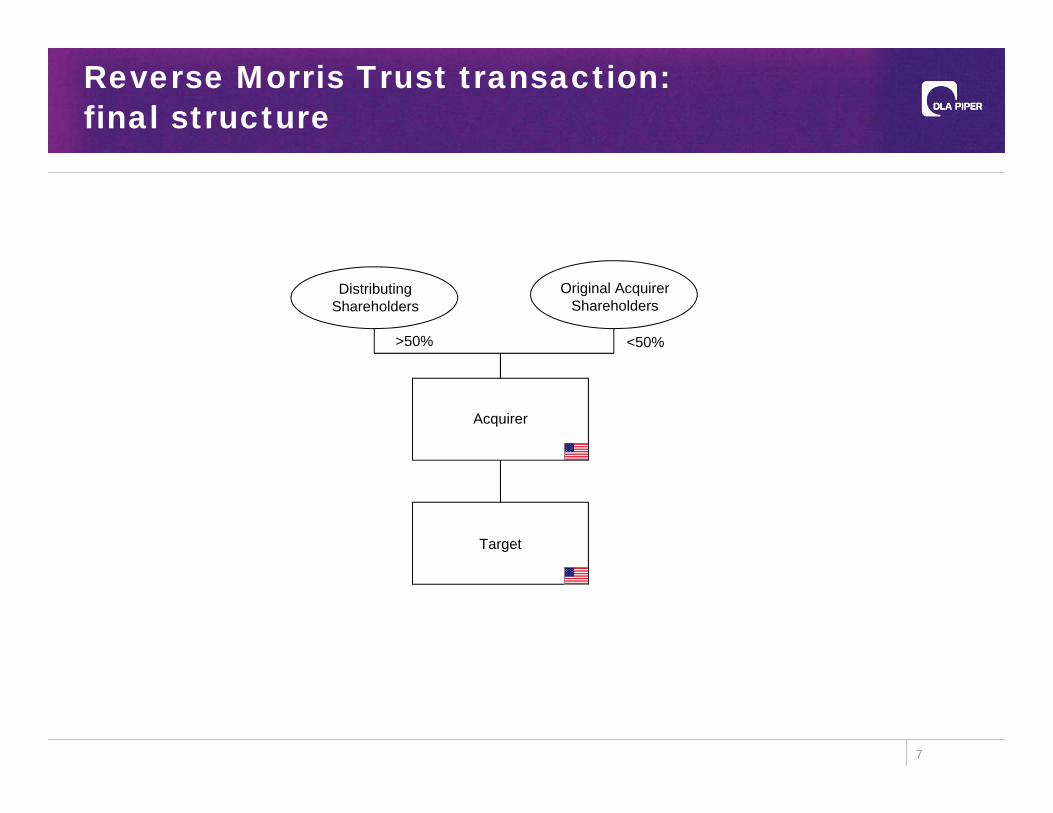

Reverse Morris Trust transaction: final structure

7

Distributing Shareholders

Target

Acquirer

>50%

Original Acquirer Shareholders

<50%

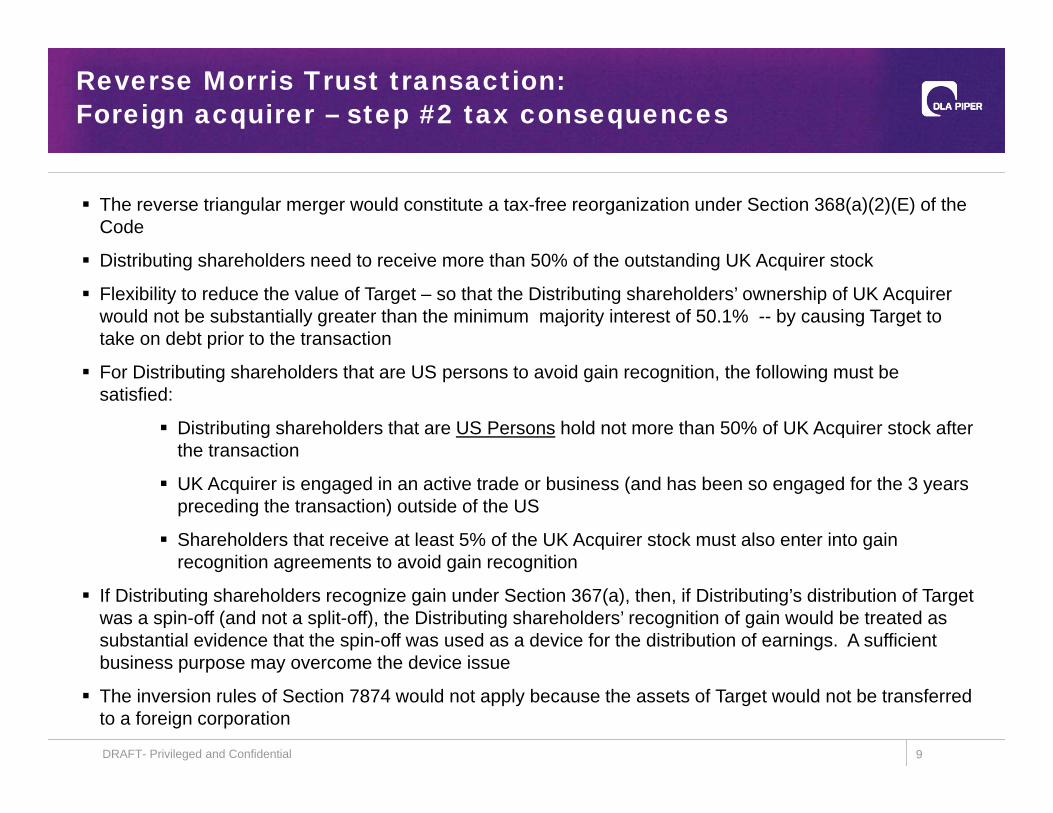

Reverse Morris Trust transaction: Foreign acquirer – step #2

DRAFT- Privileged and Confidential 8

Distributing Shareholders

Target

Step #2: UK Acquirer forms a transitory US subsidiary (“UK Acquirer US Sub”) and contributes shares of its voting stock to UK Acquirer US Sub. Using the UK Acquirer shares as consideration, UK Acquirer US Sub then merges with and into Target, with Target surviving, and with the Distributing shareholders receiving UK Acquirer voting stock

Tax Consequences: See the following slide

UK Acquirer

UK Acquirer US Sub

Reverse Triangular Merger

Reverse Morris Trust transaction: Foreign acquirer – step #2 tax consequences

DRAFT- Privileged and Confidential 9

The reverse triangular merger would constitute a tax-free reorganization under Section 368(a)(2)(E) of the Code

Distributing shareholders need to receive more than 50% of the outstanding UK Acquirer stock

Flexibility to reduce the value of Target – so that the Distributing shareholders’ ownership of UK Acquirer would not be substantially greater than the minimum majority interest of 50.1% -- by causing Target to take on debt prior to the transaction

For Distributing shareholders that are US persons to avoid gain recognition, the following must be satisfied:

Distributing shareholders that are US Persons hold not more than 50% of UK Acquirer stock after the transaction

UK Acquirer is engaged in an active trade or business (and has been so engaged for the 3 years preceding the transaction) outside of the US

Shareholders that receive at least 5% of the UK Acquirer stock must also enter into gain recognition agreements to avoid gain recognition

If Distributing shareholders recognize gain under Section 367(a), then, if Distributing’s distribution of Target was a spin-off (and not a split-off), the Distributing shareholders’ recognition of gain would be treated as substantial evidence that the spin-off was used as a device for the distribution of earnings. A sufficient business purpose may overcome the device issue

The inversion rules of Section 7874 would not apply because the assets of Target would not be transferred to a foreign corporation

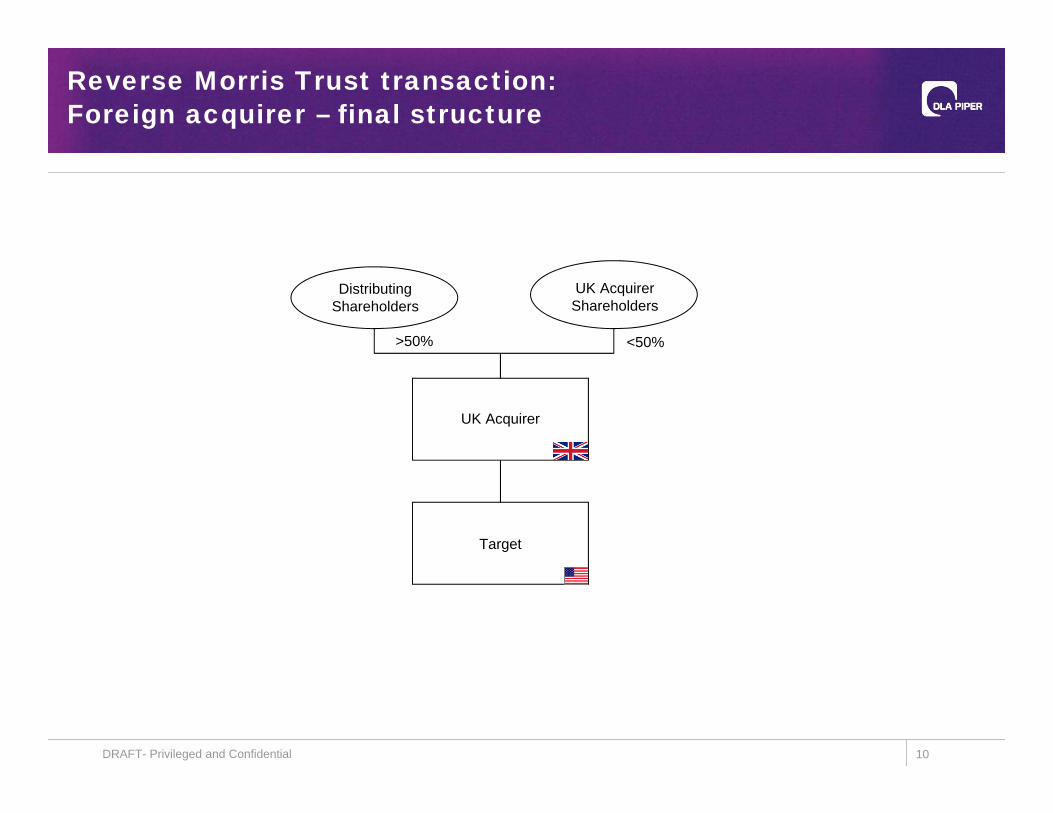

Reverse Morris Trust transaction: Foreign acquirer – final structure

DRAFT- Privileged and Confidential 10

Distributing Shareholders

Target

UK Acquirer

>50%

UK Acquirer Shareholders

<50%

Regular Morris Trust transaction

11

Basically the same transaction as a Reverse Morris Trust transaction, but Distributing contributes unwanted assets to a newly formed subsidiary and spins it off. Distributing is then acquired

The Acquirer will take on Distributing’s tax risk but the allocations of liabilities can be negotiated contractually

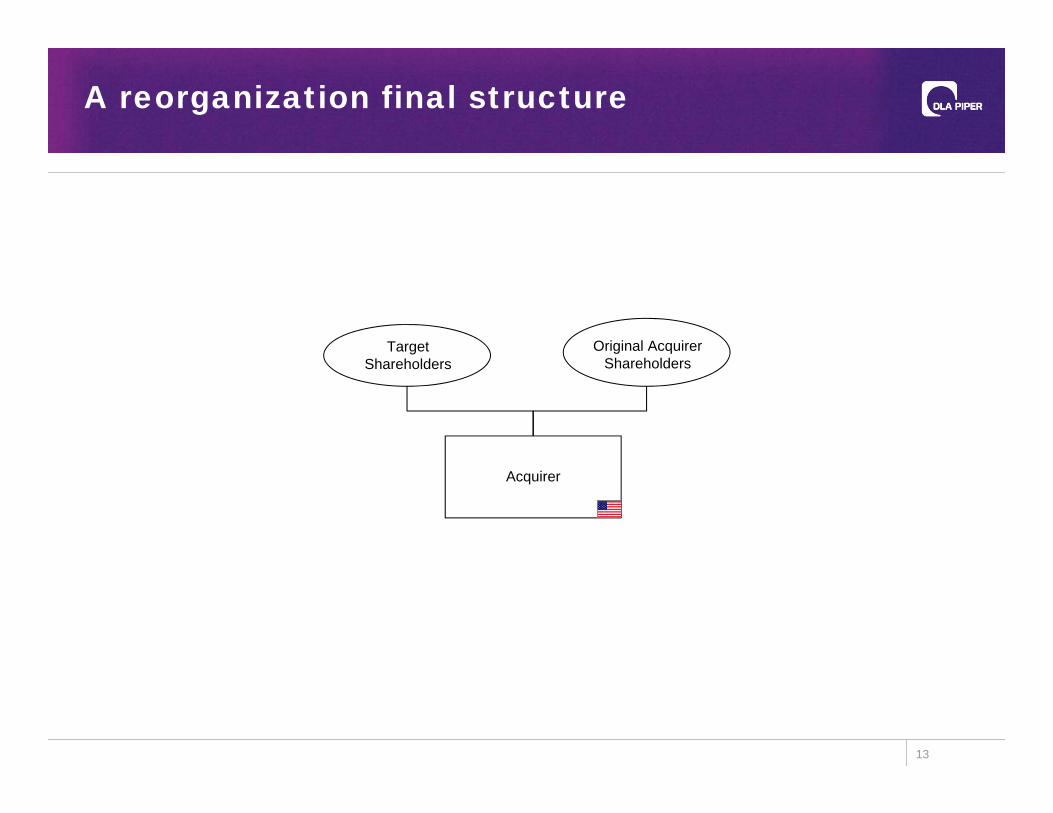

A reorganization

12

Target Shareholders

Target

Transaction: Target merges with and into Acquirer with Acquirer surviving. At least 40% of the consideration used by Acquirer consists of Acquirer’s stock

Considerations:

Generally need shareholder approval of both companies

Lots of cash

No voting stock is required

No substantially all of the properties requirement

MergerAcquirer

A reorganization final structure

13

Target Shareholders

Acquirer

Original Acquirer Shareholders

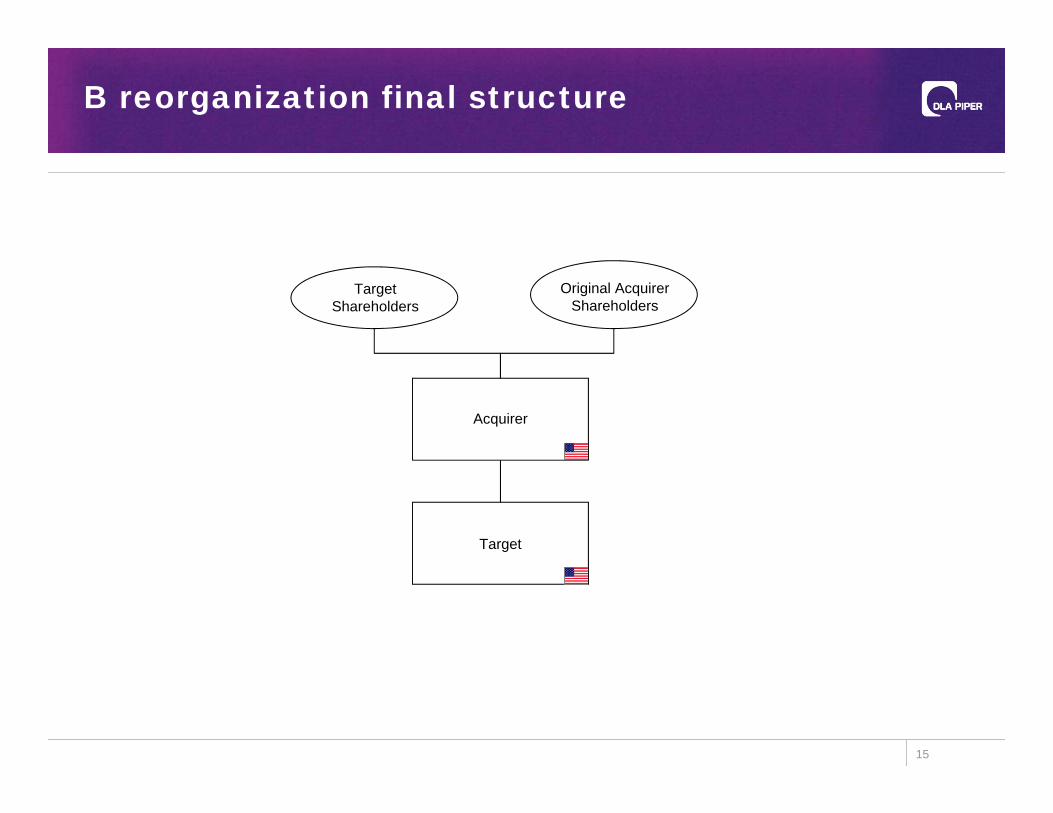

B reorganization

14

Target Shareholders

Target

Transaction: Acquirer acquires at least 80% of Target stock (vote and value) from Target shareholders solely in exchange for Acquirer voting stock

Considerations:

Generally not used because not as flexible as an (a)(2)(E)

Absolutely no cash can be used

Must use voting stockAcquirer

Acquirer voting stockTarget

stock

B reorganization final structure

15

Target Shareholders

Target

Acquirer

Original Acquirer Shareholders

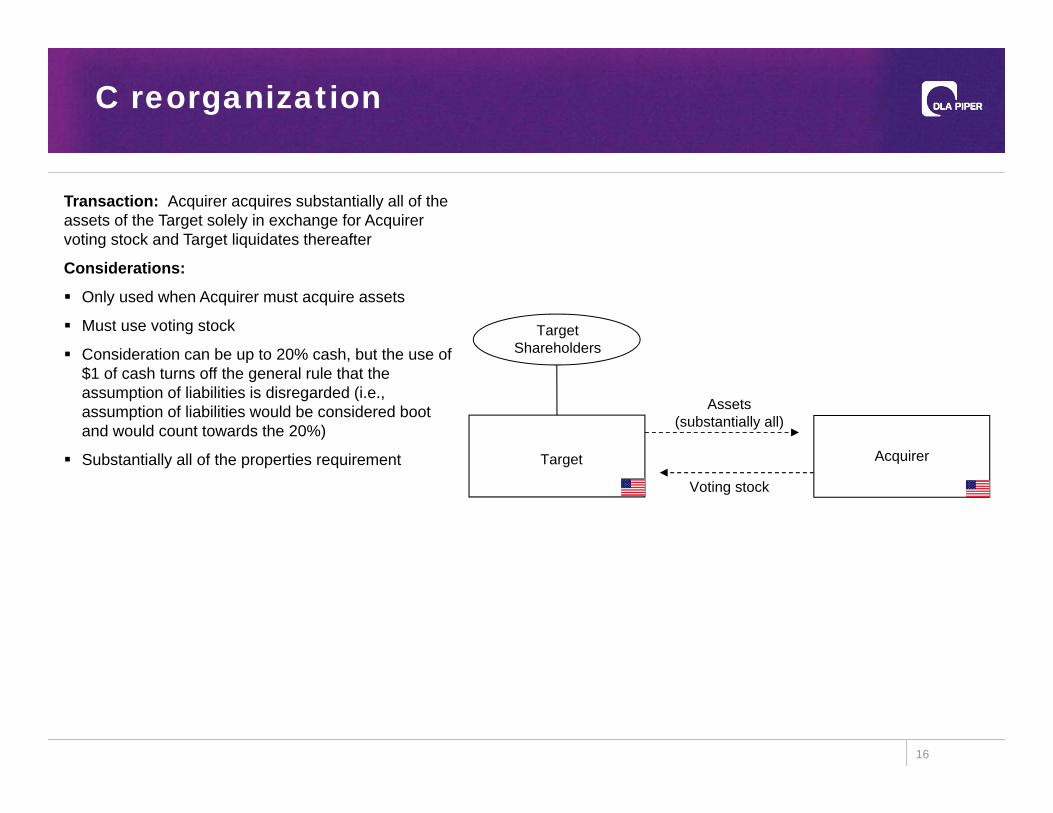

C reorganization

16

Target Shareholders

Target

Transaction: Acquirer acquires substantially all of the assets of the Target solely in exchange for Acquirer voting stock and Target liquidates thereafter

Considerations:

Only used when Acquirer must acquire assets

Must use voting stock

Consideration can be up to 20% cash, but the use of $1 of cash turns off the general rule that the assumption of liabilities is disregarded (i.e., assumption of liabilities would be considered boot and would count towards the 20%)

Substantially all of the properties requirement

Assets (substantially all)

Acquirer

Voting stock

C reorganization final structure

17

Target Shareholders

Acquirer

Original Acquirer Shareholders

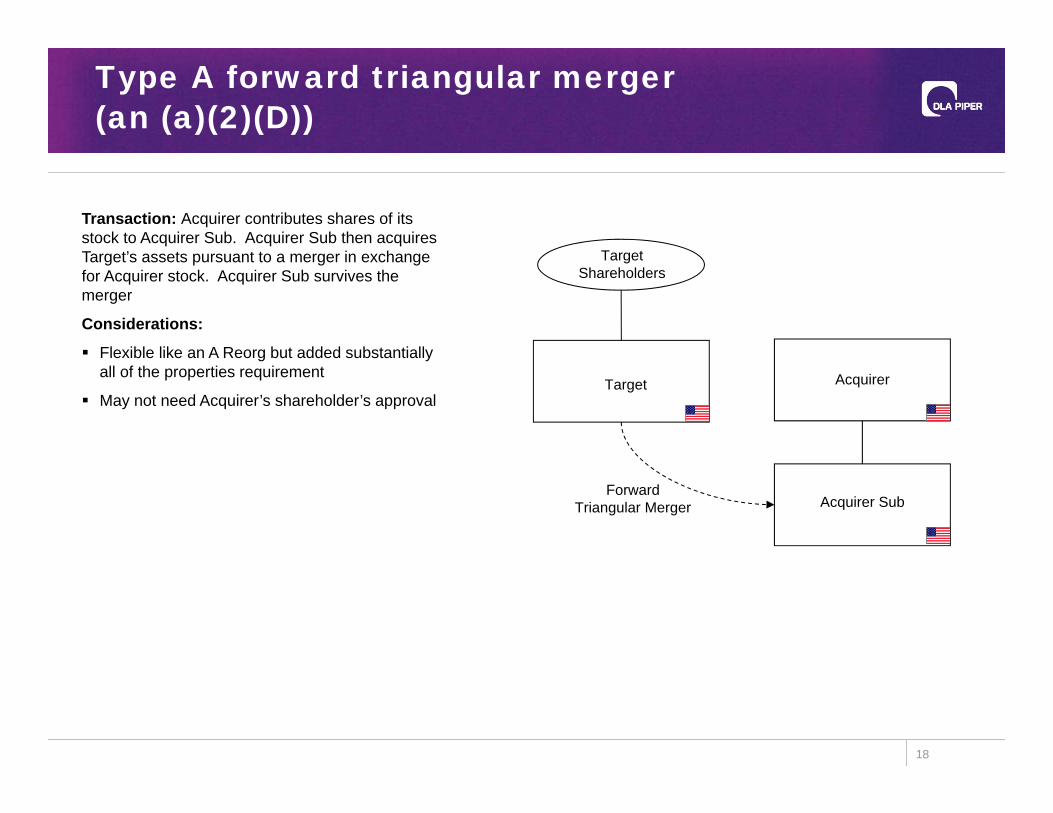

Type A forward triangular merger (an (a)(2)(D))

18

Target Shareholders

Target

Transaction: Acquirer contributes shares of its stock to Acquirer Sub. Acquirer Sub then acquires Target’s assets pursuant to a merger in exchange for Acquirer stock. Acquirer Sub survives the merger

Considerations:

Flexible like an A Reorg but added substantially all of the properties requirement

May not need Acquirer’s shareholder’s approvalAcquirer

Acquirer SubForward

Triangular Merger

(a)(2)(D) reorganization final structure

19

Target Shareholders

Acquirer Sub

Acquirer

Original Acquirer Shareholders

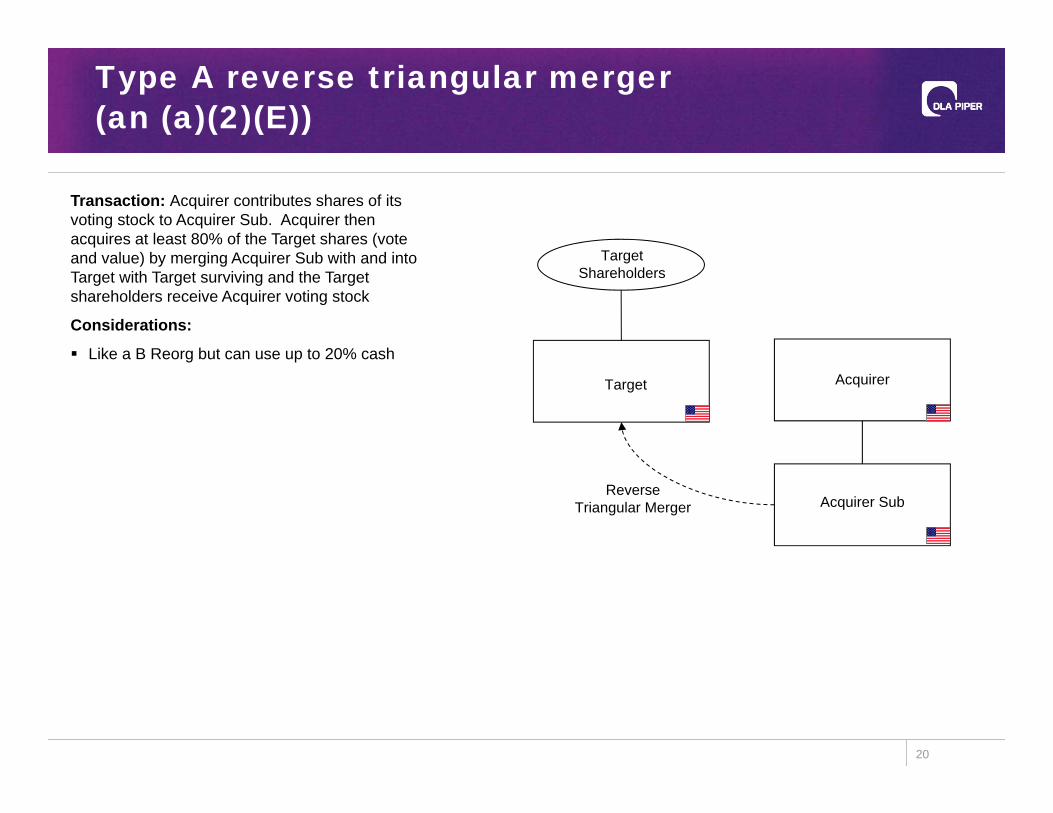

Type A reverse triangular merger (an (a)(2)(E))

20

Target Shareholders

Target

Transaction: Acquirer contributes shares of its voting stock to Acquirer Sub. Acquirer then acquires at least 80% of the Target shares (vote and value) by merging Acquirer Sub with and into Target with Target surviving and the Target shareholders receive Acquirer voting stock

Considerations:

Like a B Reorg but can use up to 20% cashAcquirer

Acquirer SubReverse

Triangular Merger

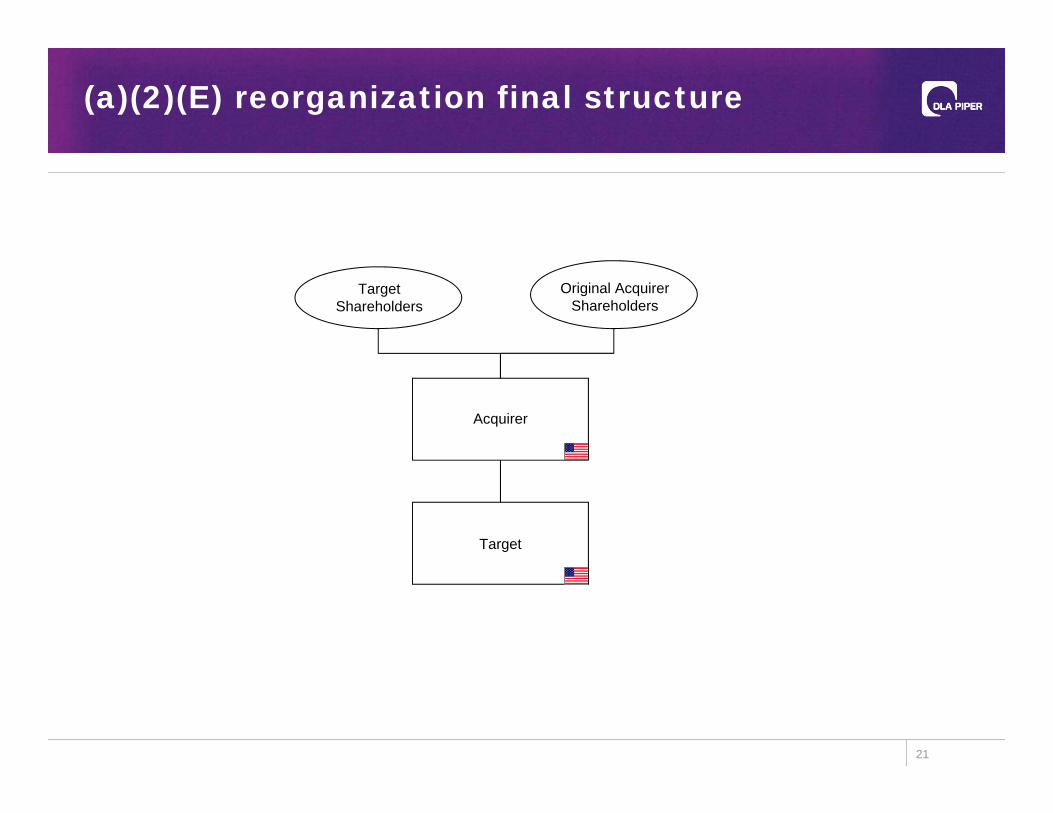

(a)(2)(E) reorganization final structure

21

Target Shareholders

Target

Acquirer

Original Acquirer Shareholders

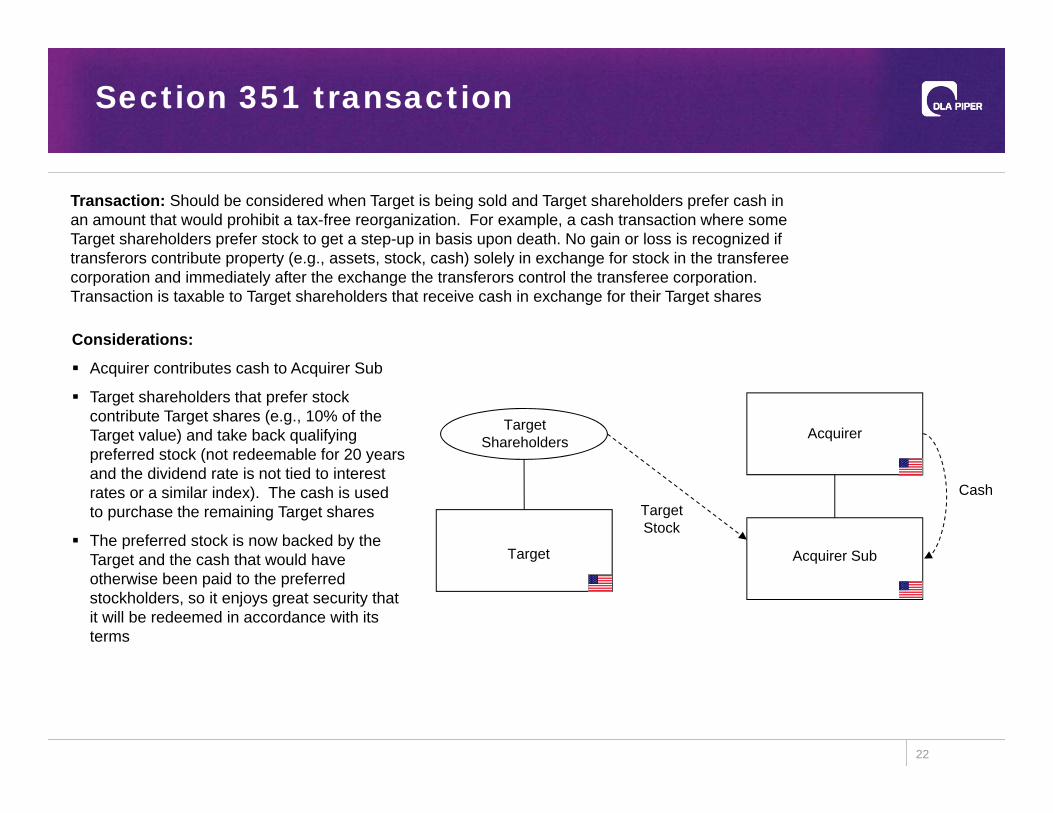

Section 351 transaction

22

Target Shareholders

Target

Transaction: Should be considered when Target is being sold and Target shareholders prefer cash in an amount that would prohibit a tax-free reorganization. For example, a cash transaction where some Target shareholders prefer stock to get a step-up in basis upon death. No gain or loss is recognized if transferors contribute property (e.g., assets, stock, cash) solely in exchange for stock in the transferee corporation and immediately after the exchange the transferors control the transferee corporation. Transaction is taxable to Target shareholders that receive cash in exchange for their Target shares

Acquirer

Acquirer Sub

CashTarget Stock

Considerations:

Acquirer contributes cash to Acquirer Sub

Target shareholders that prefer stock contribute Target shares (e.g., 10% of the Target value) and take back qualifying preferred stock (not redeemable for 20 years and the dividend rate is not tied to interest rates or a similar index). The cash is used to purchase the remaining Target shares

The preferred stock is now backed by the Target and the cash that would have otherwise been paid to the preferred stockholders, so it enjoys great security that it will be redeemed in accordance with its terms

Section 351 transaction final structure

23

Target Shareholders that were not cashed out

Acquirer Sub

Acquirer

Target

IRS Circular 230

24

IRS Circular 230 Disclosure

To ensure compliance with requirements imposed by the IRS, we inform you that any US federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.

March 2013 25

Gerald RokoffDLA Piper

1251 Avenue of the Americas27th Floor

New York, NY 10020Office Phone: 212.335.4535

Circular 230 Notice: In compliance with U.S. Treasury Regulations, please be advised that any taxadvice given herein (or in any attachment) was not intended or written to be used, and cannot

be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing orrecommending to another person any transaction or matter addressed herein.

Related Documents