The Public Biotechnology Markets in North America Presented by TD Securities Sidney Himmel June 19, 2002

The Public Biotechnology Markets in North America Presented by TD Securities Sidney Himmel June 19, 2002.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Public Biotechnology Markets in North America

Presented by TD Securities

Sidney Himmel

June 19, 2002

2

Biotechnology: Public Equity Markets

• North American markets are not strongly receptive to biotechnology stocks at the present

time.

• Issues which are getting done are occurring in:

– Well-sponsored companies with various products in the pipeline and with a solid

management track record.

– Companies with revenues and earnings.

– Diagnostics companies with revenues.

3

60%

70%

80%

90%

100%

110%

120%

28-Sep-2001 16-Nov-2001 8-Jan-2002 26-Feb-2002 17-Apr-2002 6-Jun-2002

IndexedPrice

NASDAQ Biotech / S&P 500 NASDAQ Biotech / NASDAQ NASDAQ Biotech / DJIA TSE Pharm & Biotech / S&P TSX

Biotechnology Market OverviewBiotechnology Public Market Overview

The Good…..

The Bad…..

And the Ugly.

4

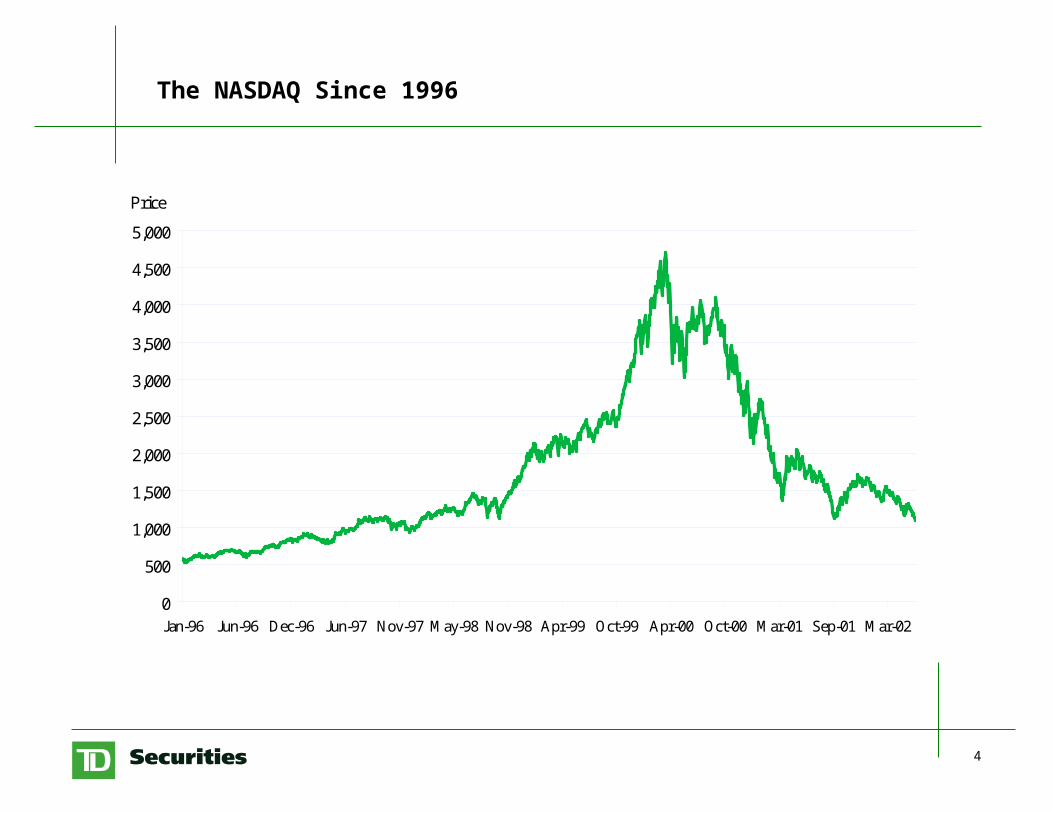

The NASDAQ Since 1996

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Jan-96 Jun-96 Dec-96 Jun-97 Nov-97 May-98 Nov-98 Apr-99 Oct-99 Apr-00 Oct-00 Mar-01 Sep-01 Mar-02

Price

5

Public Investor Concerns

• Capital losses

• Factors:

– Overvaluation? Are stocks too expensive? (Fed Model?)

– Confidence in management: a question of trust (“Never do business with anyone

you can’t trust” - J.P. Morgan).

– Accounting Issues: Relates to valuation and management issues (Enron: Arthur

Andersen).

– Research Analysts: Can they be trusted? (Merrill Lynch settlement with the New

York attorney general’s office).

• Why?

– From 1996 to 2000, investors and issuers underwent a paradigm shift which was

predictably not sustainable.

6

Hysteresis Curve of the Markets

1999 – Mid 2000

NASDAQ: 2000 5000

Annual Biotech Issues: 100

Interest Rates: 5.5%

Nortel $15.00 $80.00

Industrial Production: 126

2000 – Year-end

NASDAQ: 2470

Annualized Biotech Issues: 110 ~

Interest Rates: 4.0%

Nortel $32.00

Industrial Production: 120

1995 - 1998

NASDAQ: 1000 2000

Annual Biotech Issues: 80

Interest Rates: 5.0%

Nortel $7.00!!!

Industrial Production: 117

“Irrational Exuberance”

1994

NASDAQ: 800

Annual Biotech Issues: 49

Interest Rates: 4.0%

Nortel $5.00

Industrial Production: 100

Beginning 1994

2001 – 3rd Week of Sept 2001

NASDAQ: Bottoms at 1420

Annualized Biotech Issues: 53

Interest Rates: 2.0%

Industrial Production: 120 ~

Y2K LIQUIDITYBOOM

FIBER OPTICSCRAZE

DOT COMCRAZE

INTERNETCRAZEBEGINS

DOT COMCRASH BEGINS

FIBER OPTICSSLOWDOWN

RECESSION

7

Confidence in Management

• Sunday New York Times (June 9, 2002):

“There may be only one type of job in which somebody can commit a felony and,

after being fired as a result, still receives a severance package with many years of

salary. The job is chief executive officer of a large corporation.”

• Enron: CEO leaves.

• Tyco: CEO leaves.

• Imclone: CEO leaves.

8

9

Accounting Issues

• Investors/analysts ignored write-downs and valuation adjustments

– AOL-Time Warner: $54 billion charge.

– Quest: expecting $30 billion charge.

– Vivendi: $14 billion charge.

– JDS Uniphase: $50 billion charge.

• Misleading revenues/expenses and off-balance sheet debt:

– Enron

– Elan

– Microsoft

– Xerox

– Tyco

– Computer Associates International

– Adelphia Communications

• Rules are being applied more rigorously now.

• May affect private companies financed by venture capital as well.

10

Research Analysts

• Enron analysts interviewed by Congress.

• Henry Blodget: Internet Analyst.

– No. 1 ranked Internet analyst.

– Amazon.com target = $400.

– Merrill Lynch settles with New York state attorney general for $100 million.

• Investigations focusing on analysts and analyst compensation around the world.

• Compensation being decoupled from corporate finance around the world.

• Other investor lawsuits against brokerage houses are pending.

11

Valuations

• Must consider:– Dividends– Earnings– Earnings Growth– Discounting of Dividends:

• Warren Buffett

versus• “You just don’t get it.”

• Means

• Standard deviations

• Risk aversion

12

Valuation: The Fed Model

10-year note 5.07% (A)

Projected Earnings $52.00 (B)

S&P estimate (B/A) 1025

Actual 1027

Fairly Valued?

13

Valuations

14

A Historical Perspective on Valuations

Date P/E Dividend P/Book P/Sales 10-yr Rate EPS Growth6/13/49 5.4 7.6% 0.89 0.43 - 12.00%

10/22/57 12 4.4% 1.43 0.75 3.90% -0.08%10/25/60 16.3 3.6% 1.64 0.93 3.89% -0.05%6/26/62 14.9 3.9% 1.54 0.85 3.91% 12.00%1/3/67 14.9 3.5% 1.85 0.93 4.58% 9.00%5/26/70 12.9 4.4% 1.45 0.66 7.91% -0.09%12/6/74 7.5 5.1% 1.07 0.38 7.43% 17.50%2/28/78 8.3 5.3% 1.14 0.40 8.03% 7.00%4/21/80 6.8 5.7% 1.08 0.34 11.47% -0.08%8/12/82 7.9 6.3% 0.97 0.33 13.06% -0.14%7/24/84 9.4 4.4% 1.36 0.44 13.36% 3.00%

10/19/87 12.7 3.4% 1.92 0.58 9.52% 2.00%10/11/90 13.9 3.6% 2.24 0.60 8.72% -0.1%Average 11.0 4.7% 1.43 0.59 7.4% 4.8%

12/31/01 29-55 1.2% 5.80 1.64 5.09% 10.0%

Bear BottomsS&P Industrials

Average long-term S&P Earnings Growth 4.0 %

Sources: ISI Group; Federal Reserve Bank; Princeton University Press.

15

Earnings Model with Growth and Dividend Discount Model Valuations

CONCLUSIONS:

1. Variability.

2. Valuations may well be sustainable, with anticipated share price growth, if growth assumptions are acceptable.

* We used a 6% discount rate and assumed a 16x multiple in 5 years.

2003 EPS

Estimated 5-yr EPS Growth

Rate

2003 Dividends

Estimated Value - Discounted Fed Model or DDM

Current Stock Price

Forest Labs 2.75$ 25% Nil $37.20 71.00$ Merck 3.45$ 10% 1.51$ $40-66.00 52.00$ GlaxoSmithKline 1.20$ 15% 1.27$ $28-40.00 39.50$ Wyeth 3.00$ 15% 0.96$ $30-62.00 53.00$ Pfizer 1.85$ 18% 0.60$ $21-50.00 35.00$ Bristol-Myers Squibb 1.90$ 5% 1.14$ $23-29.00 49.00$

Average $38.25 49.91$

1.30x

16

17

Fund Flows: Affect on Valuation

1. Euro versus U.S. dollar.

2. War on Terror.

3. European, Asian, and Middle East Funds Flows.

4. Free Trade: Steel

Food

Lumber

18

Biotechnology

• Stock valuations depend on:

1. Market

2. Sector

3. Company

• Declining valuations decrease institutional investor interest due to market capitalization

cut-offs.

• Worsening momentum decreases proclivity to invest in sector.

• But: YM Biosciences raised funds.

19

Positive Independent View on the Market

• Harry Dent: Demographer and Market Technician.

• Pat McKeough: Successful investor - next big move should be up but be well-

diversified.

• Value Line: Expects moderate economic growth over the next 12 to 18 months. Should

underpin a rebound in corporate earnings.

– Middle East, accounting, earnings warnings, so still proceed with caution.

20

Most Recent Biotechnology Financings in CanadaBiotechnology Public Market Overview

Closing Date Issuer Final Size (C$mm)

% of Invested Capital

News

Jan-18-2002 PanGeo Pharma Inc. $ 27.60 17% Management track record and profitable business model. Accretive acquisitions.

Jan-31-2002 Medicure Inc. $ 10.00 67% FDA approval to proceed with Phase II for lead product, MC-1. Since issue, has begun enrollment - results expected by end 2002.

Mar-08-2002 Cardiome Pharma Corp. $ 30.91 86% Issue concurrent with acquisition of Paralex, which owns several IP rights relating to cardiovascular applications of xanthine oxidase inhibitors.

Mar-21-2002 Axcan Pharma Inc. $ 90.85 13% Market expected strong growth even without acquisitions. Part of proceeds to pay balance of Enteris acquisition. One week post-issue, announced acquisition of Lacteol.

Mar-28-2002 Hemosol $ 22.05 12% FDA approval to proceed with Phase II for Hemolink (a week after Health Canada's rejection).

April-05-2002 Cytovax Biotechnologies Inc.

$ 5.35 17% Initiated Phase I trial of lead product CytovaxineTM (received Health Canada approval to proceed in January)

April-09-2002 Aeterna Laboratories Inc. $ 57.00 25% Private placement to SGF Sante, Solidarity Fund and Acqua Wellington: $35 million for acquisitions, $20 million for Neovastat development and $2 million general.

May-24-2002 Vasogen Inc. $ 17.00 8% Positive results from CHF feasibility clinical trial - first time immunotherapeutic approach had beneficial impact on morbidity and mortality. Also completed a feasibility clinical trial in moderate to severe psoriasis.

Jun-12-2002 YM Biosciences $ 15.00 29% Flotation of Preferred shares automatically convertible into commons one year post-issue if commons are listed. Amount raised was in the lower end of the range (C$15-40mm). Required distribution on both London Stock Exchange AIM and TSE.

TOTAL $275.76

21

Harry Dent’s Demographics-Based Market Projection

22

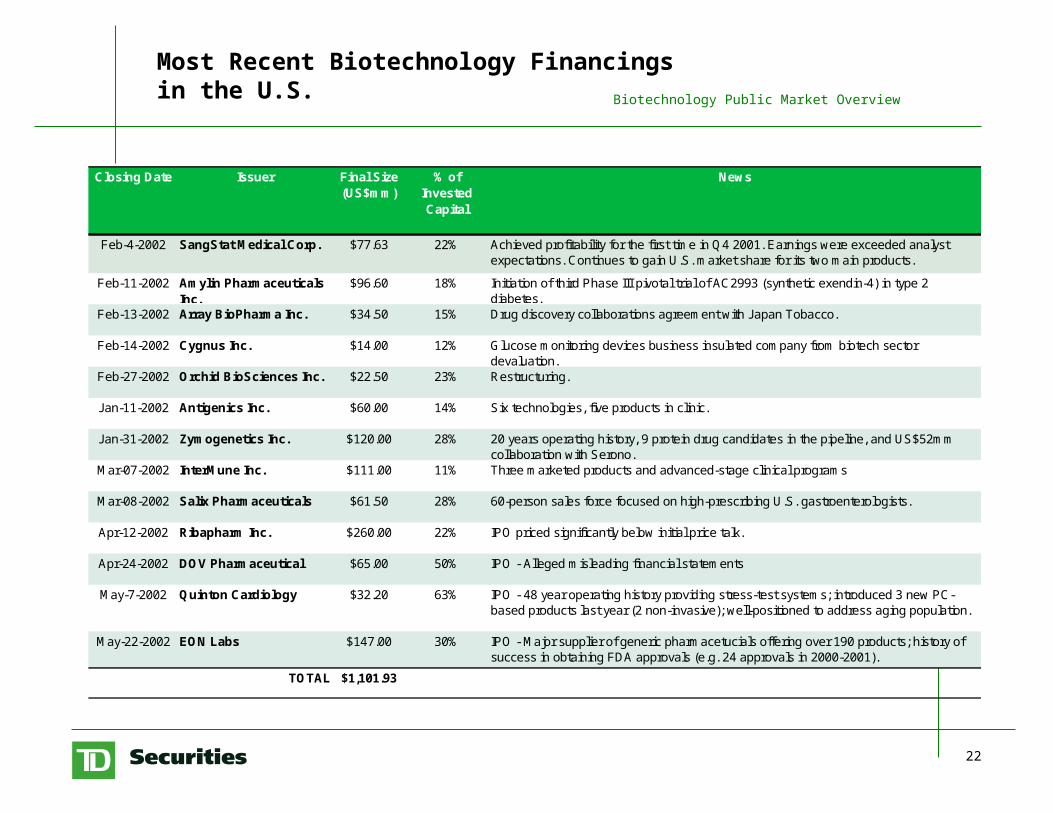

Most Recent Biotechnology Financings in the U.S.Biotechnology Public Market Overview

Closing Date Issuer Final Size (US$mm)

% of Invested Capital

News

Feb-4-2002 SangStat Medical Corp. $77.63 22% Achieved profitability for the first time in Q4 2001. Earnings were exceeded analyst expectations. Continues to gain U.S. market share for its two main products.

Feb-11-2002 Amylin Pharmaceuticals Inc.

$96.60 18% Initiation of third Phase III pivotal trial of AC2993 (synthetic exendin-4) in type 2 diabetes.

Feb-13-2002 Array BioPharma Inc. $34.50 15% Drug discovery collaborations agreement with Japan Tobacco.

Feb-14-2002 Cygnus Inc. $14.00 12% Glucose monitoring devices business insulated company from biotech sector devaluation.

Feb-27-2002 Orchid BioSciences Inc. $22.50 23% Restructuring.

Jan-11-2002 Antigenics Inc. $60.00 14% Six technologies, five products in clinic.

Jan-31-2002 Zymogenetics Inc. $120.00 28% 20 years operating history, 9 protein drug candidates in the pipeline, and US$52mm collaboration with Serono.

Mar-07-2002 InterMune Inc. $111.00 11% Three marketed products and advanced-stage clinical programs

Mar-08-2002 Salix Pharmaceuticals $61.50 28% 60-person sales force focused on high-prescribing U.S. gastroenterologists.

Apr-12-2002 Ribapharm Inc. $260.00 22% IPO priced significantly below initial price talk.

Apr-24-2002 DOV Pharmaceutical $65.00 50% IPO - Alleged misleading financial statements

May-7-2002 Quinton Cardiology $32.20 63% IPO - 48 year operating history providing stress-test systems; introduced 3 new PC-based products last year (2 non-invasive); well-positioned to address aging population.

May-22-2002 EON Labs $147.00 30% IPO - Major supplier of generic pharmacetucials offering over 190 products; history of success in obtaining FDA approvals (e.g. 24 approvals in 2000-2001).

TOTAL $1,101.93

Related Documents