The Omnichannel Experience: Innovation and Implementation

The Omnichannel Experience: Innovation and Implementation

Aug 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Omnichannel Experience: Innovation and Implementation

Andrew DowninInnovation Director, Filene Research Institute@AndrewDownin

IS THE PROMISEOF OMNICHANNELTOO GOOD TO BE TRUE?

A BUFFET OF DELIVERY CHANNELS

More Channels = More Use

2009 2010 2011 2012 20130

10

20

30

40

50

60

70

29.4 28.4 31.3 32.9 32.8

14.2 16.316.8 18.6 21.3

6.7 7.38.7

10.010.9

Branch Digital ATM/Debit

LOADING UP AT THE BUFFET

Number of items per member per month

Sour

ce: F

iser

v, 2

013

Channel Preference Depends on Activity

4% 3%

8%

74%

11%ONE SIZE(OR CHANNEL)DOES NOT FIT ALL

46%

17%

CHECKBALANCE

RESOLVE AN ISSUE 18%

15%

67%

GET ADVICE

TRANSFER FUNDS

4%

4%

7%

67%

16%

PhoneOnlineBranch/in personATMMobile/tablet

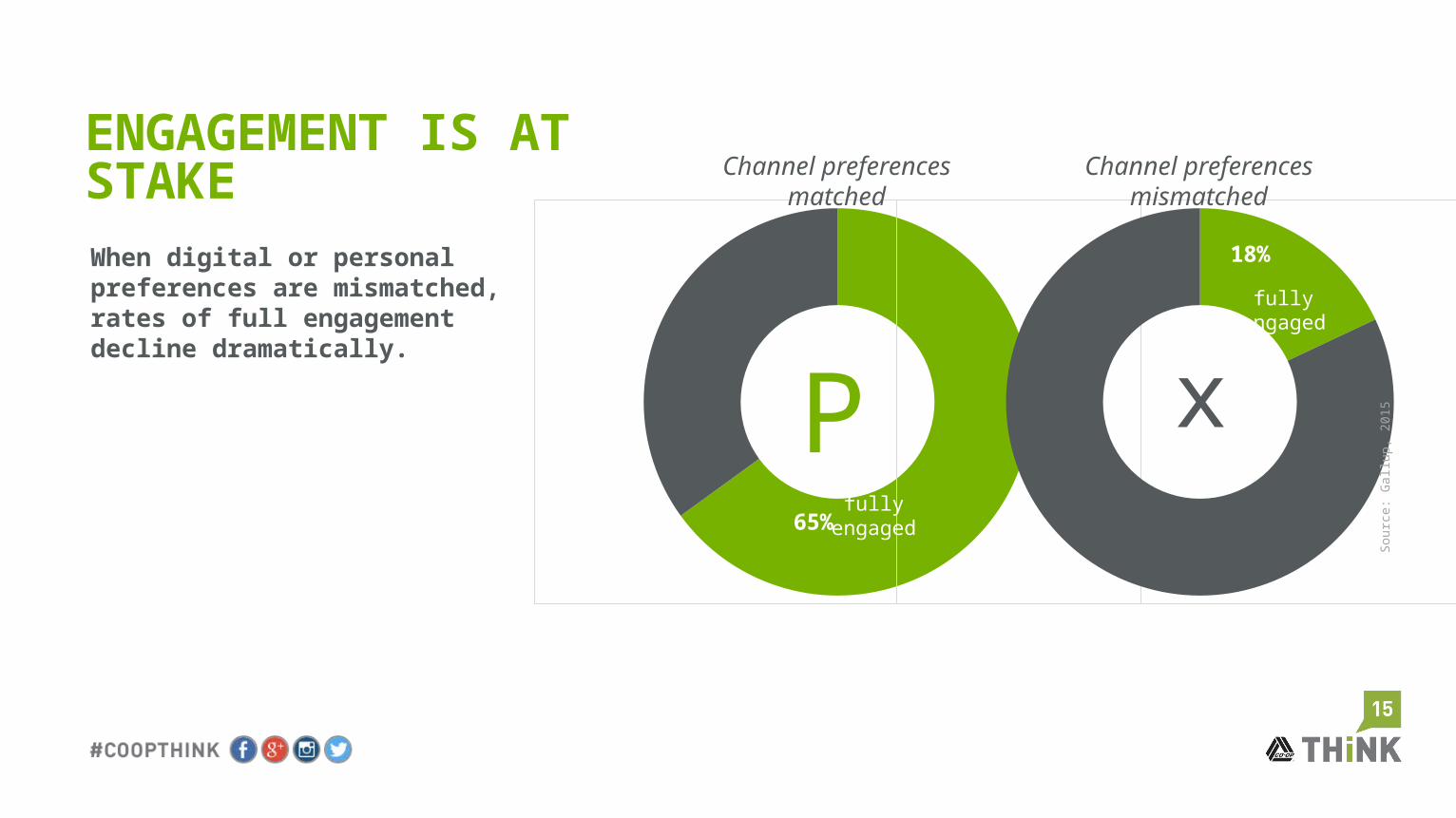

When digital or personal preferences are mismatched, rates of full engagement decline dramatically.

65%

ENGAGEMENT IS AT STAKE

18%

Sour

ce: G

allu

p, 2

015

fullyengaged

fullyengaged

xP

Channel preferences matched

Channel preferences mismatched

Limited budgets may require we focus our channel investments in what’s most desired

MATCHING INTERATIONS TO CHANNELS

High Value Transactions and

Advice

Low Value Transactions Information

• Opening/closing accounts

• Investment and retirement planning

• Fee inquiries

• Complaints

• Deposits

• Cash withdrawals

• Balances and transfers

• Statements, bills, and loan payments

• Learning about new products or services

• Loan payoff amounts

• Transaction histories

• Alerts

Employee-assisted Automated

WILL THIS DELIVERY CHANNEL INVESTMENT…• Enhance the Member experience more than other alternatives?• Help maintain competitive parity or achieve competitive differentiation?• Allow us to better acquire new Members and offer products or services to

existing Members?• Generate revenue above its installation and maintenance costs?• Allow us to reduce (or optimize) branch or call center service costs?

OMNICHANNEL GONE WRONG?

ideas

innovation

implementation

150+ CONCEPTS

TECHNOLOGY AS AN ENABLER OF TRANSPARENCY

THE LONG ROAD TO HOMEOWNERSHIP• Significant driver of primary financial institution

(PFI) status among credit union Members• Lowest satisfaction as measured by Net Promoter

Score (NPS=67.6%)

HOMEASEProactively updating Members throughout the murky mortgage process

HOMEASE

• Automatically and proactively provides mortgage updates at key milestones

• Improves Member satisfaction with a key product line

• Enhances operational efficiency by reducing inbound calls (from 6.1 to 4.4 per member during prototype test)

• Currently in pilot testing with D+H

A NEW HIERARCHY OF PFM NEEDS IS EMERGING

Where is my money?

How am I doing?

What should I be doing? Instruct

Interpret

Inform

CENTSUSLeveraging mobileto connect financialbehaviors with emotions

CENTSUS

• Integrates with existing online banking or payment card transaction detail

• Prompts Member to document their emotional satisfaction 24 to 48 hours after a purchase

• Connects emotional patterns with financial behaviors

• Prompts Members to ‘spend happier’ with proactive, timely push notifications

ZEROHOUR

Uniting bricks and clicks for a richbranch experience

ZEROHOUR

• Leverages iBeacon technology to pinpoint individual Member location• Greets Members upon branch approach and queues up transaction details• Presents finely targeted, location-based marketing messages tied to credit

union objectives and member preferences• Supplements the branch experience rather than replacing it

WHAT’S THE i3 TRICK?

THE FILENE METHOD

Insights Problem Identification Ideation Prototyping

& TestingImplemen-

tation

WHAT CAN YOU DO TOMORROW?• Understand Member delivery channel preferences• Optimize specific channels to create exceptional experiences that fit within

credit union resources and strategy• Mine the Filene i3 catalog for relevant concepts• Collaborate with other credit unions• Break down creativity barriers and embrace calculated risk• Apply for Filene i3 – now through May 15!

Thank [email protected] 608.661.3746

Related Documents