The Need to Return to a The Need to Return to a Monetary Framework John B. Taylor Comments prepared for the National Association of Business Economics Panel on Long-Run Economic Challenges: AFd lR P ti A Federal Reserve Perspective San Francisco San Francisco January 3, 2009

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Need to Return to aThe Need to Return to a Monetary Framework

John B. Taylor

Comments prepared for the National Association of Business Economics Panel on

Long-Run Economic Challenges: A F d l R P tiA Federal Reserve Perspective

San FranciscoSan FranciscoJanuary 3, 2009

Why the Need? • Empirical evidence shows that government actions and interventions caused, prolonged, worsened the crisis. – Caused it by deviating from historical precedents andCaused it by deviating from historical precedents and principles for setting interest rates‐‐worked well for 20 years.

– Prolonged it by misdiagnosing the problems and responding i i t l b f i li idit th th i kinappropriately by focusing on liquidity rather than risk.

– Worsened it by providing support for certain financial institutions and their creditors but not others in an ad hoc way

– Details found at www.JohnBTaylor.com “The Financial Crisis and Policy Response: An Empirical Analysis of What Went Wrong”g

• But now is time to look forward, learn from the past:– Need to reinstate or establish a set of principles to prevent

i id d i d i imisguided actions and interventions .– A path back to principles should be part of current clean‐ up.

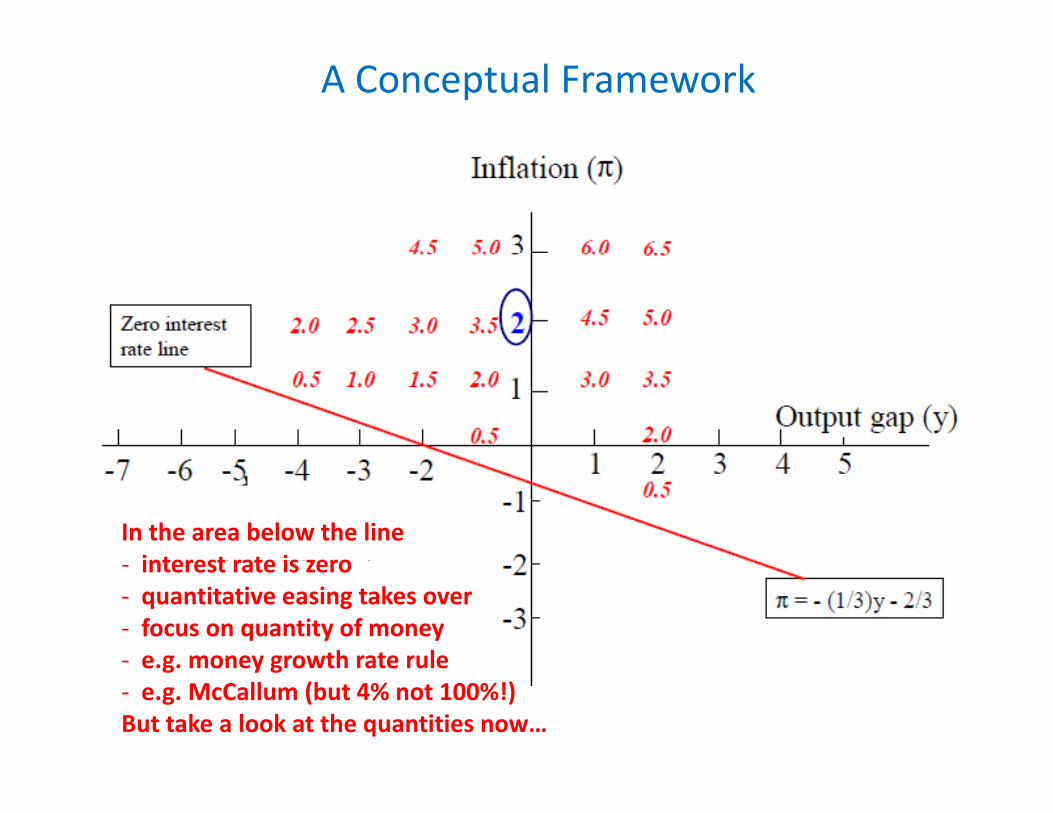

A Conceptual Framework

In the area below the lineinterest rate is zero

Ii‐ interest rate is zero ‐ quantitative easing takes over‐ focus on quantity of money‐ e g money growth rate rulee.g. money growth rate rule‐ e.g. McCallum (but 4% not 100%!)But take a look at the quantities now…

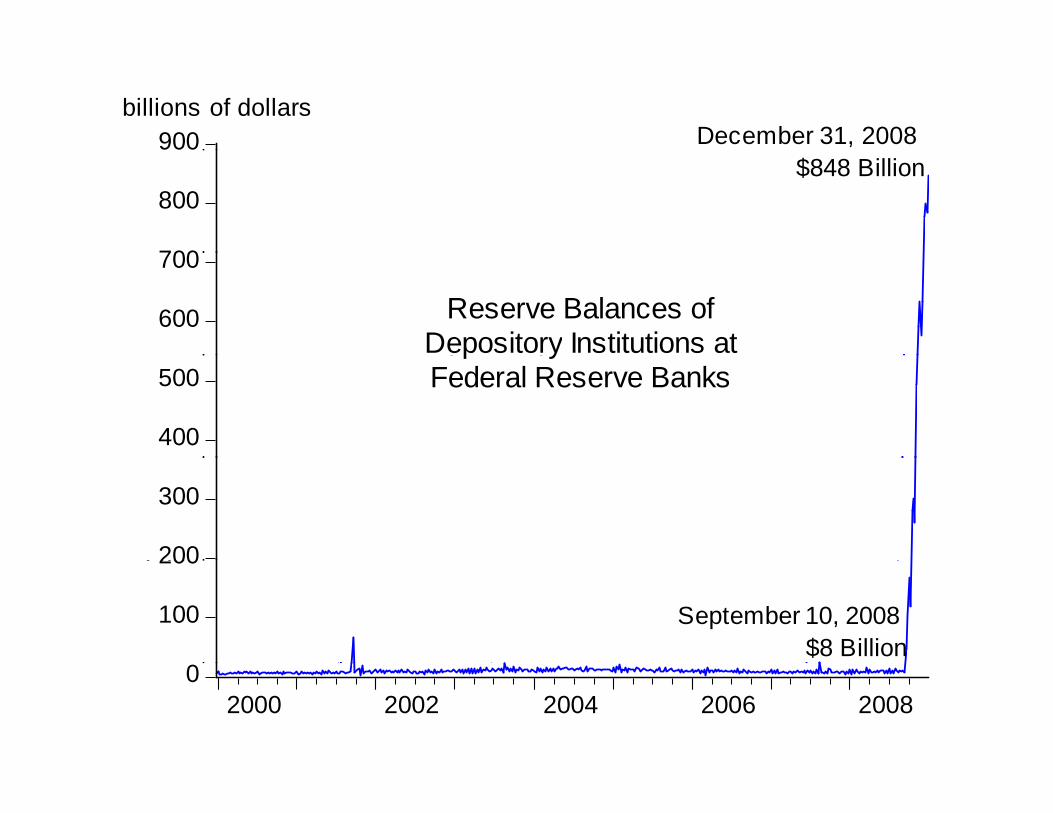

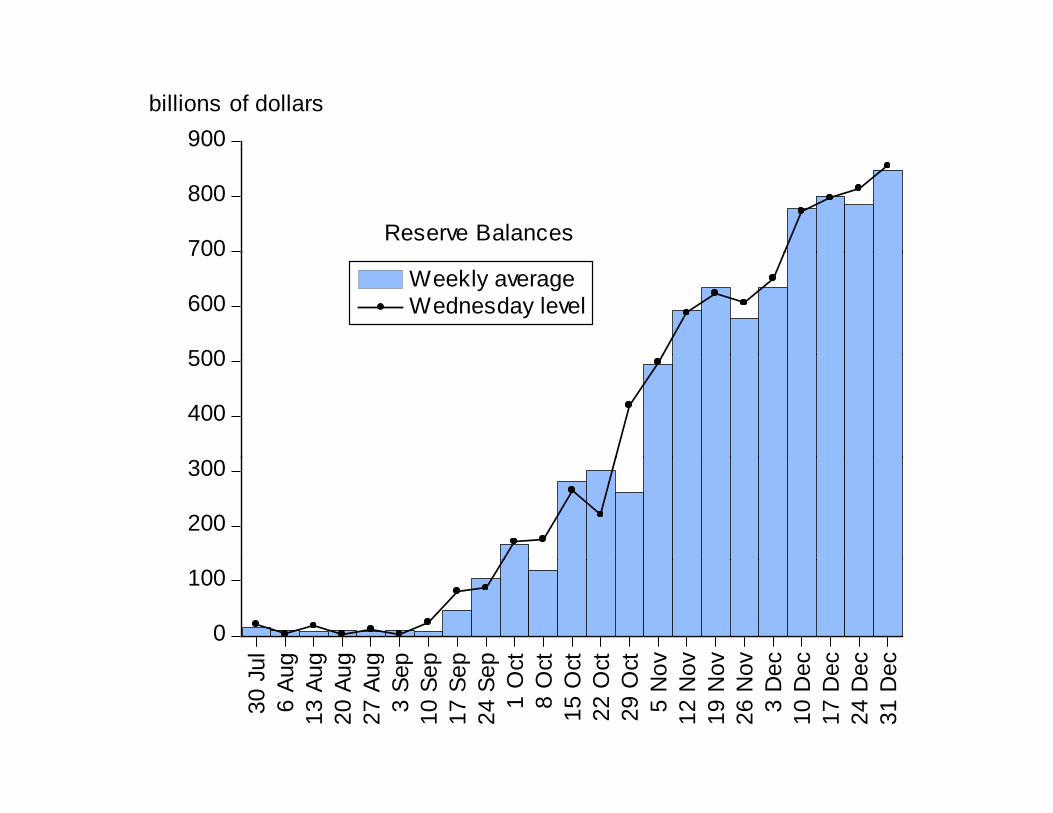

900billions of dollars

December 31, 2008900billions of dollars

December 31, 2008

700

800 $848 Billion

700

800 $848 Billion

600

700

Reserve Balances ofDepository Institutions at

600

700

Reserve Balances ofDepository Institutions at

400

500p y

Federal Reserve Banks

400

500p y

Federal Reserve Banks

200

300

200

300

100

200

September 10, 2008 $8 Billion

100

200

September 10, 2008 $8 Billion

02000 2002 2004 2006 2008

02000 2002 2004 2006 2008

900billions of dollars

700

800

Reserve Balances

500

600

700Weekly averageWednesday level

400

500

200

300

0

100

ul g g g g p p p p ct ct ct ct ct v v v v c c c c c

30 J

u6

Aug

13 A

ug20

Aug

27 A

ug3

Sep

10 S

ep17

Sep

24 S

ep1

Oc

8 O

c15

Oc

22 O

c29

Oc

5 N

o12

No

19 N

o26

No

3 D

e10

De

17 D

e24

De

31 D

e

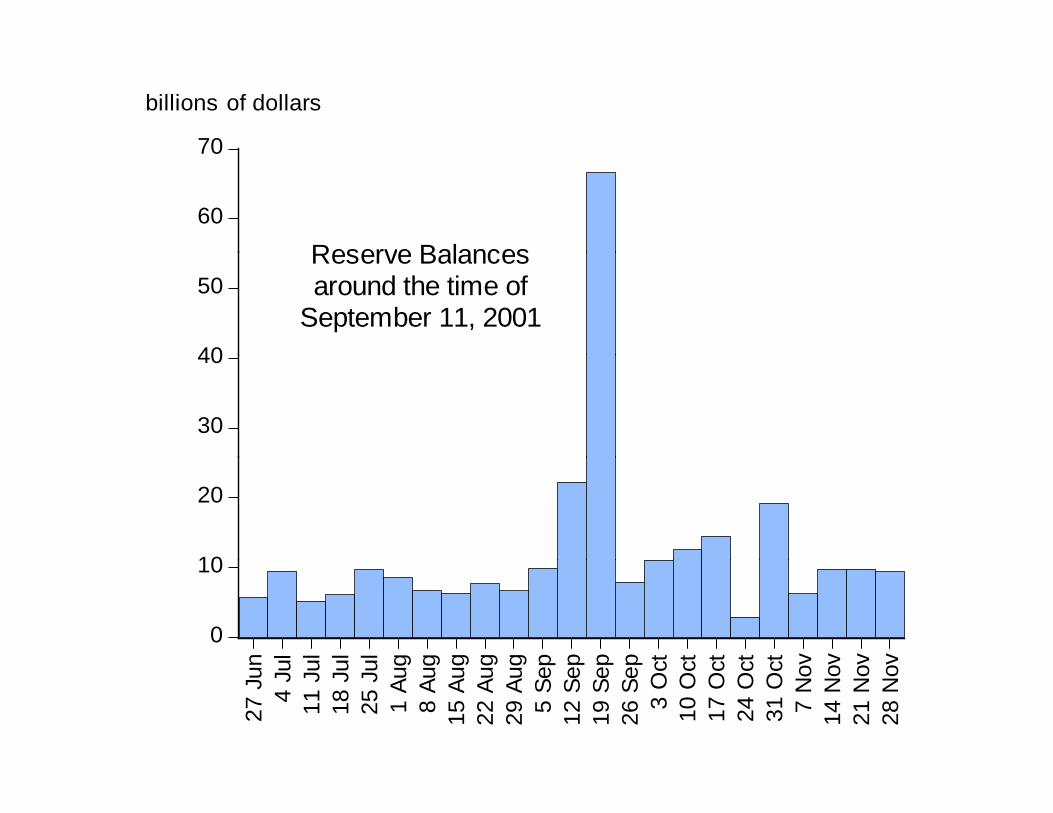

70

billions of dollars

60

70

Reserve Balances

40

50Reserve Balancesaround the time of

September 11, 2001

30

40

10

20

0

10

n ul ul ul ul g g g g g p p p p ct ct ct ct ct v v v v

27 J

un4

Ju11

Ju

18 J

u25

Ju

1 Au

g8

Aug

15 A

ug22

Aug

29 A

ug5

Sep

12 S

ep19

Sep

26 S

ep3

Oc

10 O

c17

Oc

24 O

c31

Oc

7 N

ov14

Nov

21 N

ov28

Nov

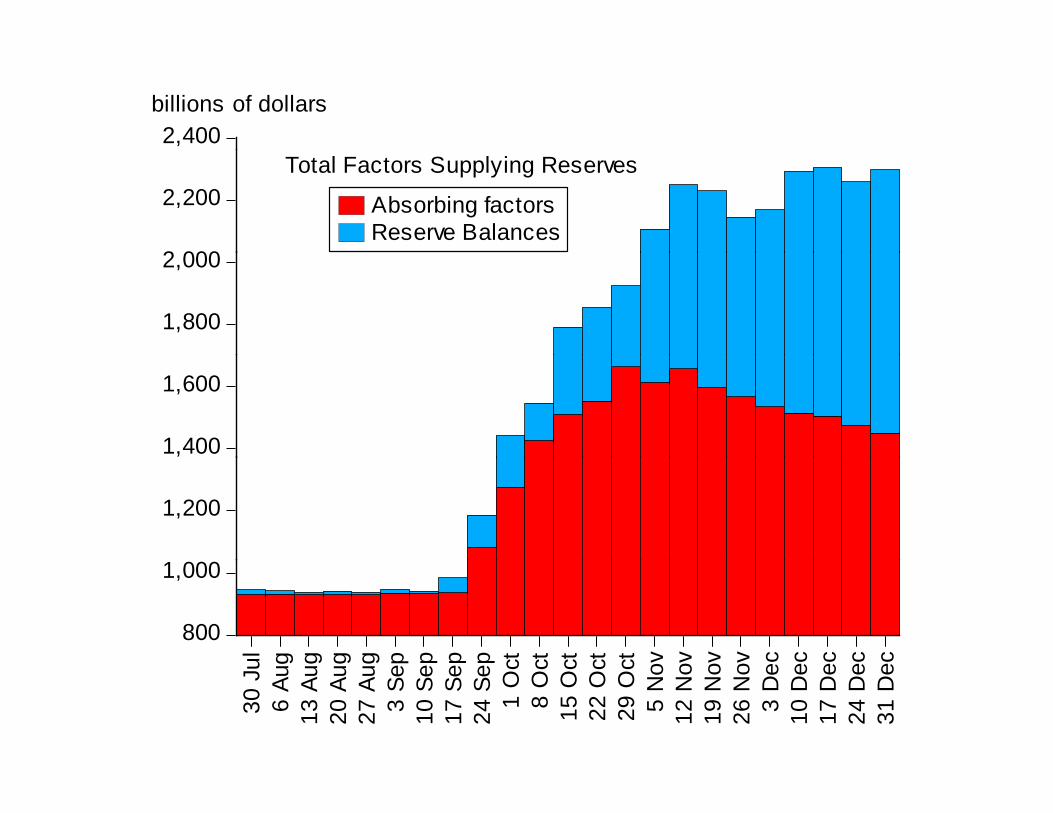

2,400billions of dollars

2 000

2,200 Absorbing factorsReserve Balances

Total Factors Supplying Reserves

1,800

2,000

1,400

1,600

1,200

800

1,000

ul g g g g p p p p ct ct ct ct ct v v v v c c c c c

30 J

u6

Aug

13 A

ug20

Aug

27 A

ug3

Sep

10 S

e17

Se

24 S

e1

Oc

8 O

c15

Oc

22 O

c29

Oc

5 N

o12

No

19 N

o26

No

3 D

e10

De

17 D

e24

De

31 D

e

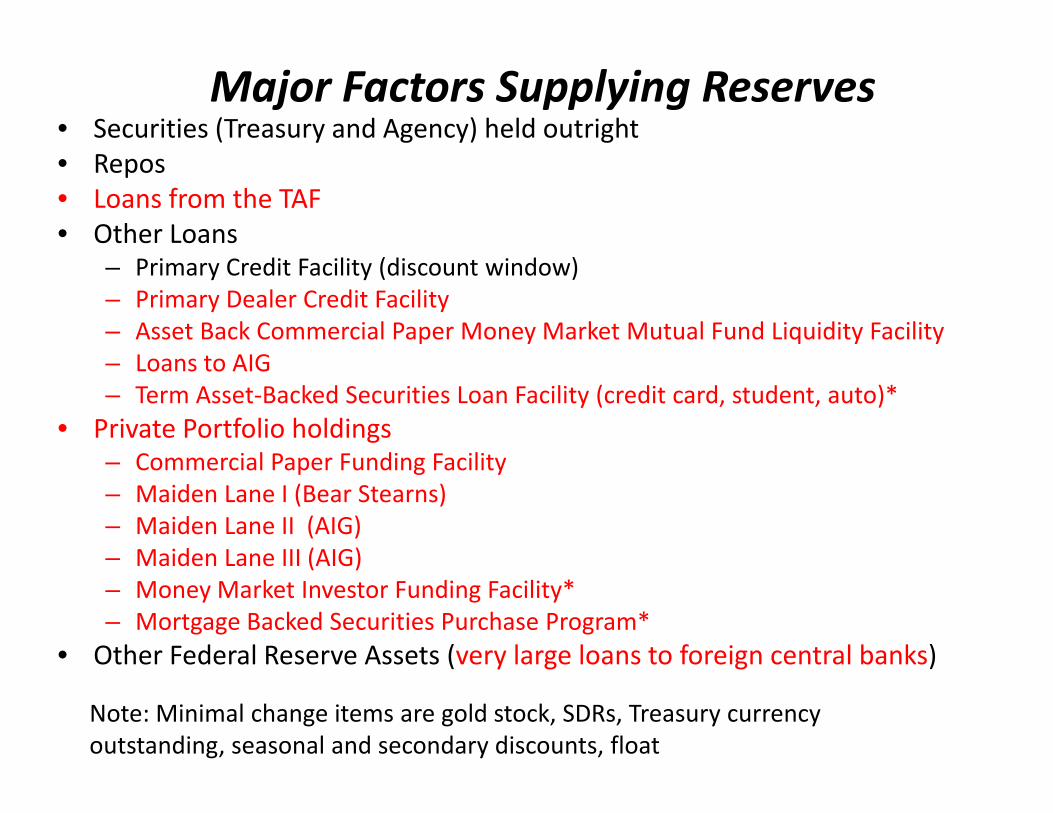

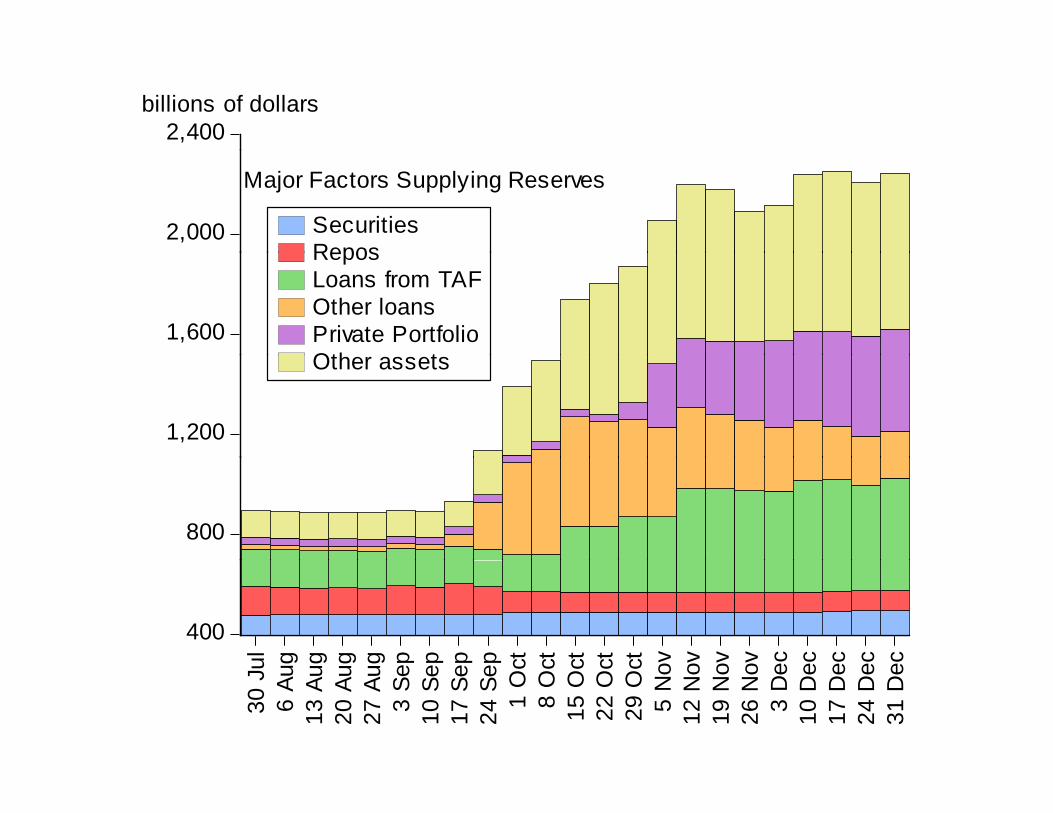

Major Factors Supplying Reserves• Securities (Treasury and Agency) held outright • Repos • Loans from the TAF• Other Loans

– Primary Credit Facility (discount window)– Primary Dealer Credit Facility– Asset Back Commercial Paper Money Market Mutual Fund Liquidity Facility

L AIG– Loans to AIG– Term Asset‐Backed Securities Loan Facility (credit card, student, auto)*

• Private Portfolio holdings Commercial Paper Funding Facility– Commercial Paper Funding Facility

– Maiden Lane I (Bear Stearns)– Maiden Lane II (AIG)– Maiden Lane III (AIG)Maiden Lane III (AIG) – Money Market Investor Funding Facility*– Mortgage Backed Securities Purchase Program*

• Other Federal Reserve Assets (very large loans to foreign central banks)Other Federal Reserve Assets (very large loans to foreign central banks)

Note: Minimal change items are gold stock, SDRs, Treasury currency outstanding, seasonal and secondary discounts, float

Not Simply Quantitative EasingNot Simply Quantitative Easing

• How will purchases under the agency MBSHow will purchases under the agency MBS program be financed?Purchases will be financed through thePurchases will be financed through the creation of additional bank reserves ‐‐ From FAQ NY Fed December 30 2008FAQ ,NY Fed, December 30, 2008.

• Sounds like Industrial Policy

M d i l P li ?• Mondustrial Policy?

2,400billions of dollars

2,000 SecuritiesRepos

Major Factors Supplying Reserves

1,600

ReposLoans from TAFOther loansPrivate PortfolioOth t

1,200

Other assets

800

400

ul g g g g p p p p ct ct ct ct ct v v v v c c c c c

30 J

u6

Aug

13 A

ug20

Aug

27 A

ug3

Se10

Se

17 S

e24

Se

1 O

c8

Oc

15 O

c22

Oc

29 O

c5

No

12 N

o19

No

26 N

o3

De

10 D

e17

De

24 D

e31

De

700billions of dollars

600 Other Federal Reserve Assets

500

300

400

200

100

02003 2004 2005 2006 2007 2008

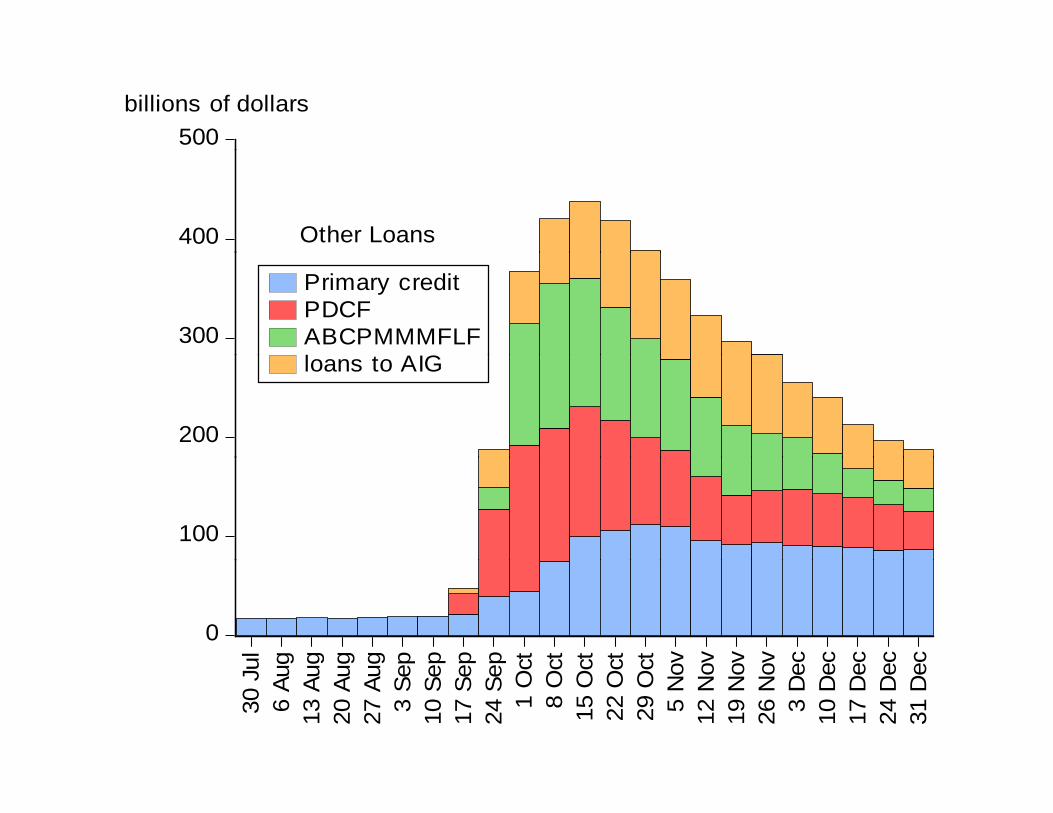

500billions of dollars

400 Other Loans

300

Primary creditPDCFABCPMMMFLFl t AIG

200

loans to AIG

100

0

ul g g g g p p p p ct ct ct ct ct v ov ov ov c c c c c

30 J

u6

Aug

13 A

ug20

Aug

27 A

ug3

Sep

10 S

ep17

Sep

24 S

ep1

Oc

8 O

c15

Oc

22 O

c29

Oc

5 N

o12

No

19 N

o26

No

3 D

e10

De

17 D

e24

De

31 D

e

200billions of dollars

Wednesday Levels

160

PDCFReserve Balances

y

120

80 Change from Sept 10 to Sept 17:PDCF +$59 780B

40

PDCF +$59.780B Reserve Balances +$57.728B

0

l g g g g p p p p t

30 Ju

l6 A

ug13

Aug

20 A

ug27

Aug

3 Sep

10 S

ep17

Sep

24 S

ep1 O

ct

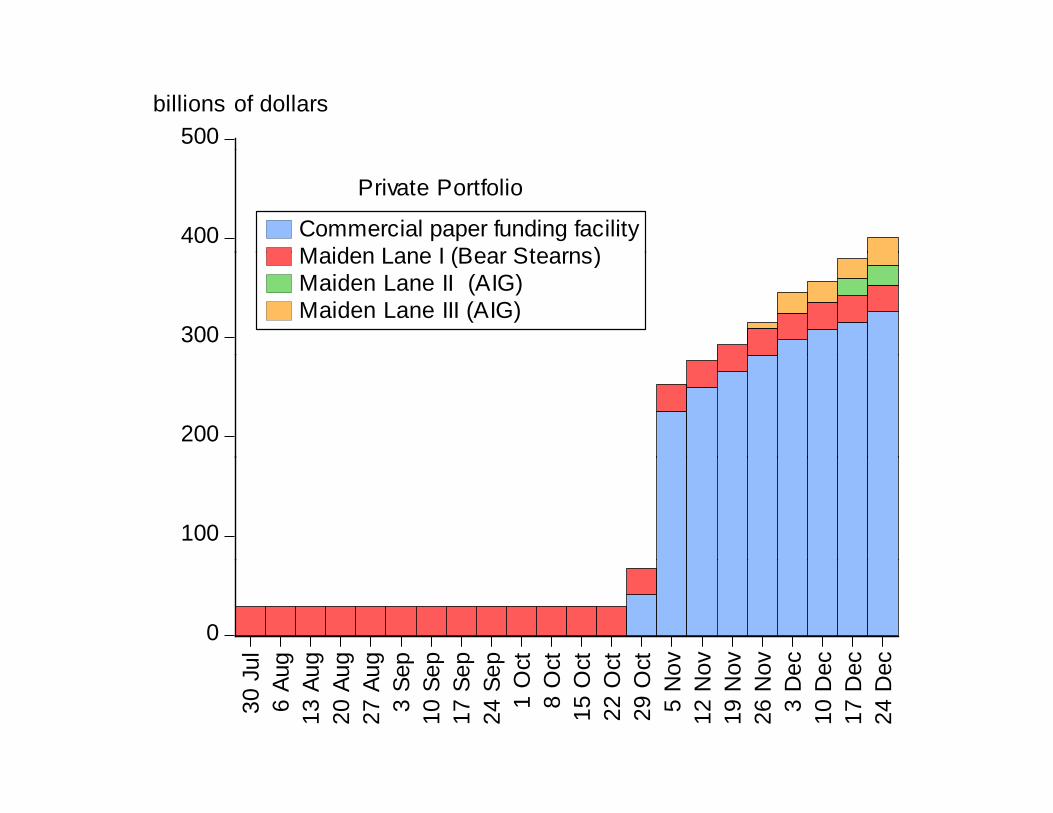

500billions of dollars

400 Commercial paper funding facilityMaiden Lane I (Bear Stearns)

Private Portfolio

300

Maiden Lane I (Bear Stearns)Maiden Lane II (AIG)Maiden Lane III (AIG)

200

100

0

ul g g g g p p p p ct ct ct ct ct v v v v c c c c

30 J

u6

Aug

13 A

ug20

Aug

27 A

ug3

Sep

10 S

e17

Se

24 S

e1

Oc

8 O

c15

Oc

22 O

c29

Oc

5 N

o12

No

19 N

o26

No

3 D

e10

De

17 D

e24

De

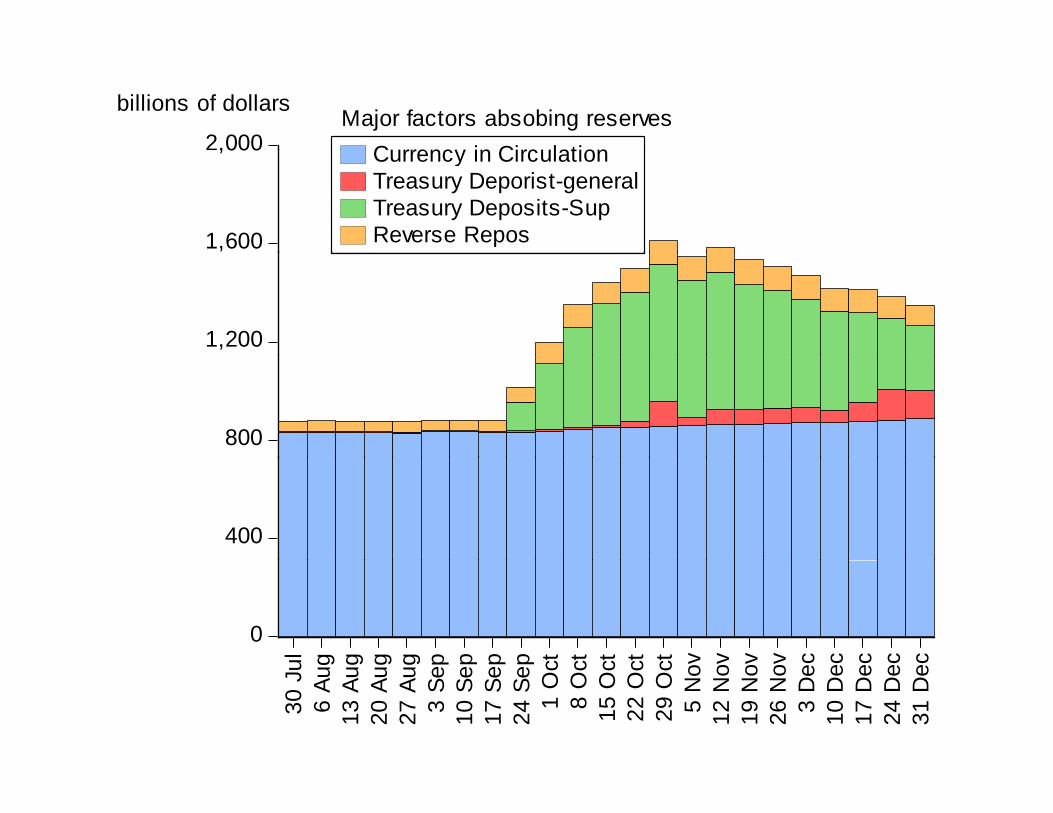

2,000 Currency in CirculationMajor factors absobing reservesbillions of dollars

1,600

,000 Currency in CirculationTreasury Deporist-generalTreasury Deposits-SupReverse Repos

1,200

800

400

0

ul g g g g p p p p ct ct ct ct ct v v v v c c c c c

30 J

u6

Aug

13 A

ug20

Aug

27 A

ug3

Sep

10 S

ep17

Sep

24 S

ep1

Oc

8 O

c15

Oc

22 O

c29

Oc

5 N

ov12

Nov

19 N

ov26

Nov

3 D

ec10

Dec

17 D

ec24

Dec

31 D

ec

Role of the TreasuryRole of the Treasury

• Originally Treasury borrowed $500B andOriginally Treasury borrowed $500B and deposited at Fed thereby absorbing reserves– Effectively Treasury is borrowing to finance y y gpurchases in certain sectors

• Supplemental accounts are being drawn down– If MBS program and TALF go to full amounts that will be equal to $700 B.

• May require more Treasury borrowing or Fed borrowing itself to finance.

Other viewsOther views• Fed accommodated increased demand for reserves by banks, as in 9/11, /– Interest on reserves or flight to safety– Dates are off for interest on reserves story– And interest rates fell as reserves were increased– And interest rates fell as reserves were increased

• Fed accommodated increased demand for monetary aggregates– True that both currency and demand deposits rose,

• reflecting lower interest rates and flight from money market mutual funds,

B t th h l th ld h i d th– But they rose much less than would have required the observed increase in reserve balances.

• Money multiplier fell sharply

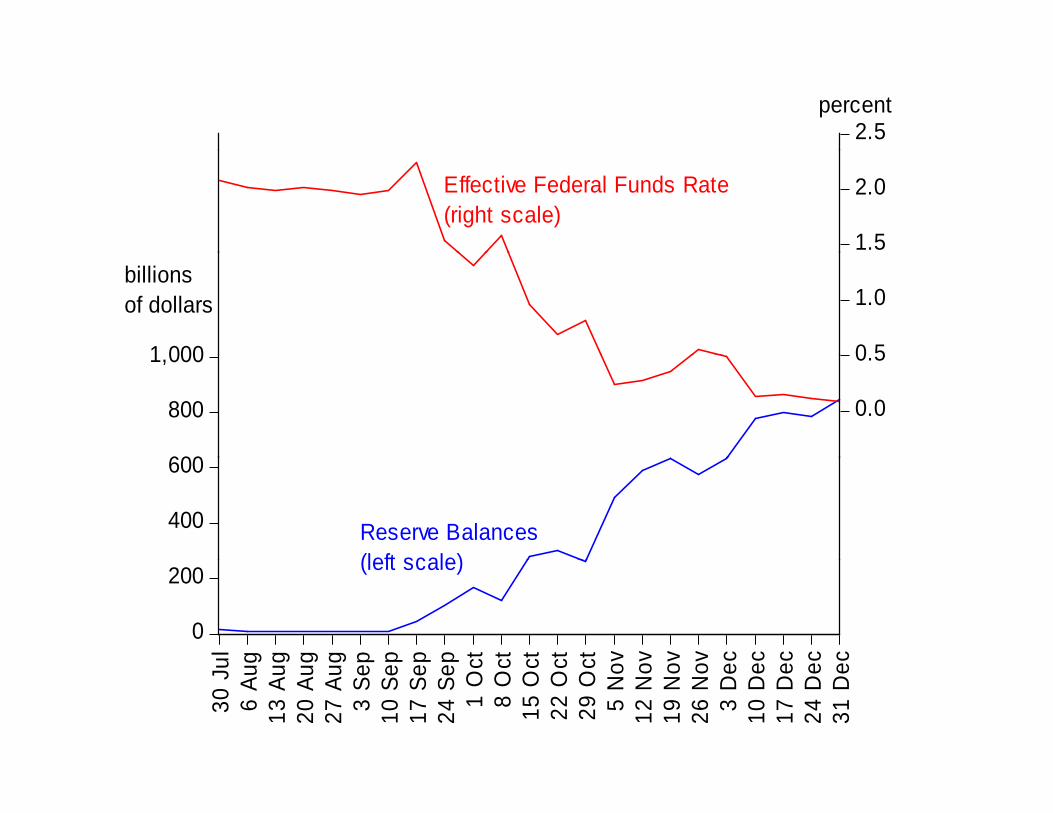

2.5percent

1.5

2.0Effective Federal Funds Rate(right scale)

1 000 0 5

1.0billionsof dollars

600

800

1,000

0.0

0.5

400

600

Reserve Balances(left scale)

0

200

ul g g g g p p p p ct ct ct ct ct v v v v c c c c c

(left scale)

30 J

u6

Au13

Au

20 A

u27

Au

3 Se

10 S

e17

Se

24 S

e1

Oc

8 O

c15

Oc

22 O

c29

Oc

5 N

o12

No

19 N

o26

No

3 D

e10

De

17 D

e24

De

31 D

e

820billions of dollars billions of dollars

500

800t450

780

800currency componentof money supply(right scale)

350

400 780

300

350 760

250

740

c n b r r y n l g p t t v c

demand deposits componentof money supply (left scale)

26 D

ec23

Jan

20 Feb

19 M

ar16

Apr14

May

11 Ju

n9 J

ul6 A

ug3 S

ep1 O

ct29

Oct

26 N

ov24

Dec

1,800

billions of dollars

1,600

,

1,400

M1

1 000

1,200

800

1,000

currency + reserve balances

600

Dec Jan

Feb

Mar AprMay Ju

n Jul

Aug Sep Oct OctNov Dec

26 D

e23

Ja20

Fe19

Ma

16 A

p14

Ma

11 Ju 9 J

u6 A

ug3 S

e1 O

c29

Oc

26 N

o24

De

2.0

1.8

R ti f M1 t

1 4

1.6 Ratio of M1 to currencyplus reserve balances

1.2

1.4

1.0

1.2

0.8

ec an eb ar Apr ay un Jul ug ep Oct Oct ov ec

26 D

ec23

Jan

20 Feb

19 M

ar16

Apr

14 M

ay11

Jun

9 Ju

6 Aug

3 Sep

1 Oct

29 O

ct26

Nov

24 D

ec

ConclusionsG t b k t t li f k f t• Get back to a monetary policy framework fast– Start by reducing the growth of the monetary base, then bring reserve balances downthen bring reserve balances down

– Stipulate that goal is to exit from helping particular sectors: monetary policy, not mondustrial policy secto s: o eta y po cy, ot o dust a po cy

– Refrain from Fed borrowing or Treasury borrowing for Fed to finance loans to certain markets and sectors

• If not, then radical reforms are needed– Monetary independence?– Congressional oversight?– Role of district banks?– Section 13(3) “unusual and exigent circumstances” ?

Related Documents