The GREATER CHINA BUSINESS JET FLEET REPORT Year End 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The GREATER CHINA BUSINESS JET FLEET

REPORT

Year End 2013

Asian Sky Group Limited (“ASG”) is headquartered in Hong Kong with offices throughout China. It has assembled the most experienced business aviation team in the Asia-Pacific region to provide a wide range of consulting services for both fixed-wing and rotary-wing aircraft. Asian Sky Group provides access to a significant customer base around the world with the help of its exclusive partners: Avpro Inc., the largest business jet brokerage firm in the US; and AVIC International Development Corporation, the largest state-owned aviation enterprise in Mainland China.

Asian Sky Group is backed by SEACOR Holdings Inc., a publically listed US company (NYSE: “CKH”) with over US$ 1B in revenue and nearly US$ 3B in assets, and by Avion Pacific Limited, a Mainland China-based general aviation service provider with 20 years of experience and 6 offices and bases throughout China.

Asian Sky Group provides its clients with the following aviation consulting services:

1) AIRCRAFT SALES, such as acquisition or remarketing; selection of aircraft, asset financing, ownership structuring, registration and operator selection; inspections and appraisals; contractual support;

2) COMPLETION MANAGEMENT, such as cabin definition; facility selection; completion oversight; delivery and regulatory compliance; contractual support;

3) OPERATION OVERSIGHT, such as invoice analysis and owner representation;

4) LUXURY CHARTER SERVICES;

5) SPECIAL PROJECTS and

6) TRANSACTIONAL ADVISORY.

ABOUT ASIAN SKY GROUP

Beijing

Penglai

Shanghai

Hong Kong

Manila

Zhuhai

ChengduShenzhen

KualaLumpur

Singapore

Jakarta

The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

1The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

ASIAN SKY GROUP (ASG) is proud to present its “Greater China Business Jet Fleet Report” for year-end 2013. This unique report provides complete coverage of the business jet market in the Greater China region, which includes Mainland China, Hong Kong, Macau and Taiwan. The report is the second edition of the Greater China Business Jet Fleet Report following its first publication in March, 2013.

For copies of Asian Sky Group’s business aviation industry reports, please visit www.asianskygroup.com.

TABLE OF CONTENTS

EXECUTIVE SUMMARY………………………….……………….....................…..………….2KEY FINDINGS...……….…………………………………………...................…………..…….5FLEET BREAKDOWN BY:

ORIGINAL EQUIPMENT MANUFACTURER (OEM)……......................................6SIZE CATEGORY………………………………………...................................………….20OPERATOR…………......……….......………………................................…………......24AIRCRAFT REGISTRATION …………..….......................………….........……......….32AIRCRAFT AGE DISTRIBUTION..……..…………...............…................…………..40

SUPPORT INFRASTRUCTURE…………..........................................................…...46AVIATION FINANCE INSTITUTIONS…….........................................................…..56 2013 AND MARKET TRENDS..……………………..............….…......………………….57

Asian Sky Group would like to graciously acknowledge the contributions made by numerous operators, OEMs and organizations to this report, without which a reasonable level of accuracy could not have been achieved.

The report is nevertheless the second edition of its type and undoubtedly there will be perceived errors. Asian Sky Group welcomes your comments, questions and general thoughts and looks forward to producing an even better version of the report in the future.

Should you wish to reproduce or distribute any portion of this report, in part or in full, you may do so by mentioning the source as: “Asian Sky Group, a Hong Kong based business aviation consulting group”.

Thank you for your interest in this report and we hope you find the information useful. If you would like to receive further information about our services, please contact us at [email protected] or visit us at www.asianskygroup.com.

INTRODUCTION

EXECUTIVE SUMMARY

The Greater China business jet fleet grew rapidly over the last two years, rising from 203 business jets in 2011, to 371 aircraft as of year-end 2013. From 2007 to 2013 the Greater China business jet fleet has grown at a Compound Annual Growth Rate of 34%, which is significantly higher than the global rate of 5%.

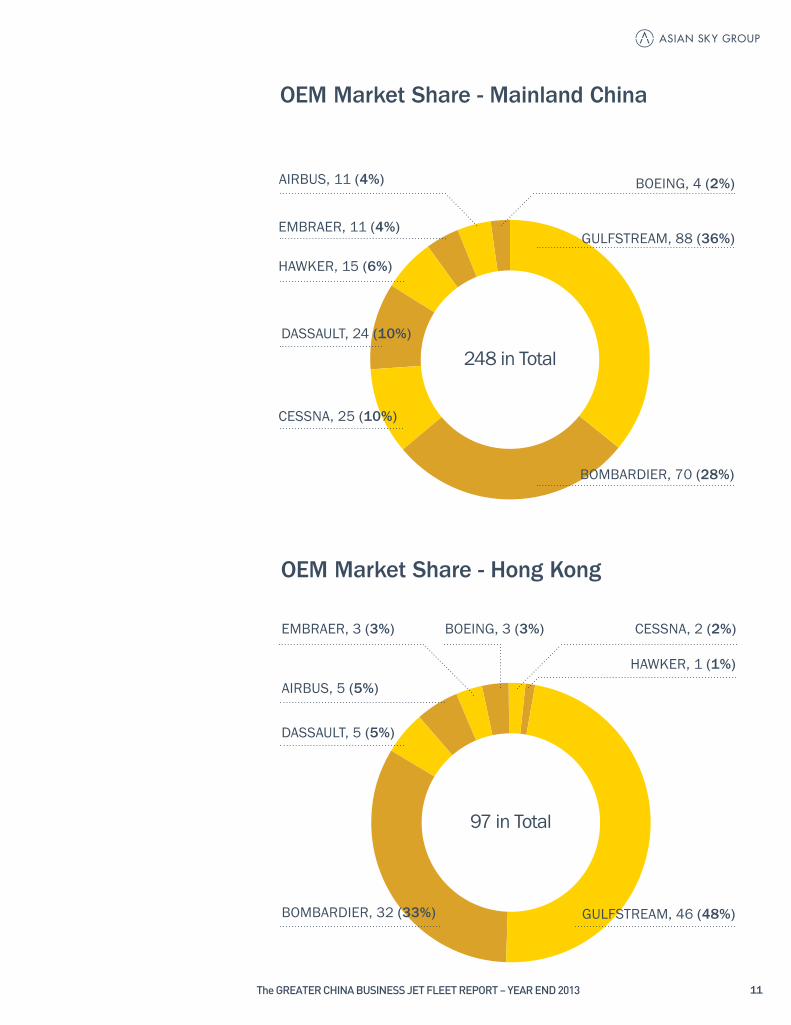

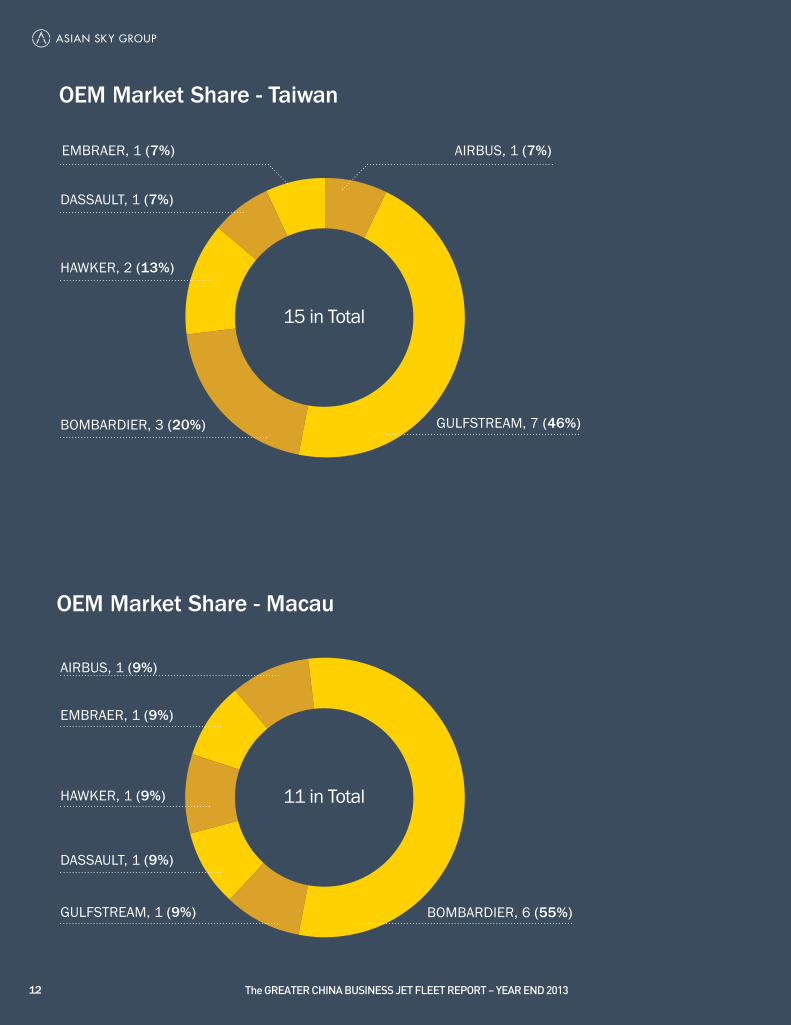

Of the 371 aircraft, 248 are based in Mainland China, 97 in Hong Kong, 15 in Taiwan and 11 are in Macau.

Demand for business jets is largely driven by robust economic growth, the rising number of high net worth individuals, increasing corporate profits, successful listing of public companies (IPOs) and government support. More and more companies are also increasingly using business jets as a tool to support corporate international growth and integration.

Despite the high growth rate, there have been several factors hampering the growth of business aviation in Greater China. These factors include airspace restrictions; limited regional aviation support infrastructure; a shortage of locally licensed private pilots; plus the difficulty and duration required to qualifying for an Air Operator Certificate (AOC) due to strict regulatory requirements. Other aspects affecting the pace of growth are taxation policies imposed on China-registered aircraft (import duty and Value Added Tax); the expenditure sentiment currently emanating from Beijing as dictated by the Chinese Central Government; and for foreign registered aircraft, operational challenges and costs in Mainland China.

Government support is a key factor in generating continued growth in the China business aviation industry. Some regulations and taxation policies in China are strict, but viewed as necessary by the Civil Aviation Administration of China (CAAC) as a means to control the growth rate and ensure it is matched with sufficient infrastructure such as number of airports, Fixed Base Operations (FBO) facilities, Maintenance Repair and Overhaul (MRO) centers, air traffic control and other qualified aviation personnel. It is expected though that China will further ease some of the current barriers and allow the industry and its supporting infrastructure to grow in levels matching demand. China has 193 civil airports in service, of which 10 were completed in 2013. According to the CAAC, plans are to have 244 airports in service by 2020.

As China continues to ease its airspace flight regulations, more opportunity for smaller-sized business aircraft mainly used for domestic flights should appear in the future. However, the current preference to large cabin is expected to remain strong in the short term. As of year-end 2013, the Greater China fleet was strongly dominated by large cabin and long range aircraft.

China has the second largest economy in the world. It holds nearly 20% of the world’s population, 7% of the world’s billionaires and a 13% wealth annual growth rate, yet it holds less than 2% of the world’s business jets. The business aviation industry however is developing rapidly and signs of a maturing market are evident. Consequently, Asian Sky Group expects high growth to continue in 2014 as the business jet market in Greater China continues to develop and mature.

2 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

3The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Greater China Fleet – by OEM

Greater China Fleet - by Aircraft Base*

BOEING, 7 (2%)

AIRBUS, 18 (5%)

EMBRAER, 16 (4%)

HAWKER, 19 (5%)

CESSNA, 27 (7%)

DASSAULT, 31 (9%)

BOMBARDIER, 111 (30%)

GULFSTREAM, 142 (38%)

371 in Total

Mainland China Hong Kong Taiwan Macau

3%11

4%15

26%97

67%248

In this report, aircraft distribution was done according to the aircraft’s base of opera-tion and not by operator location. Some operators may be headquartered in a cer-tain location but their aircraft are based according to the preferences of the aircraft owners themselves.

371 in Total

*

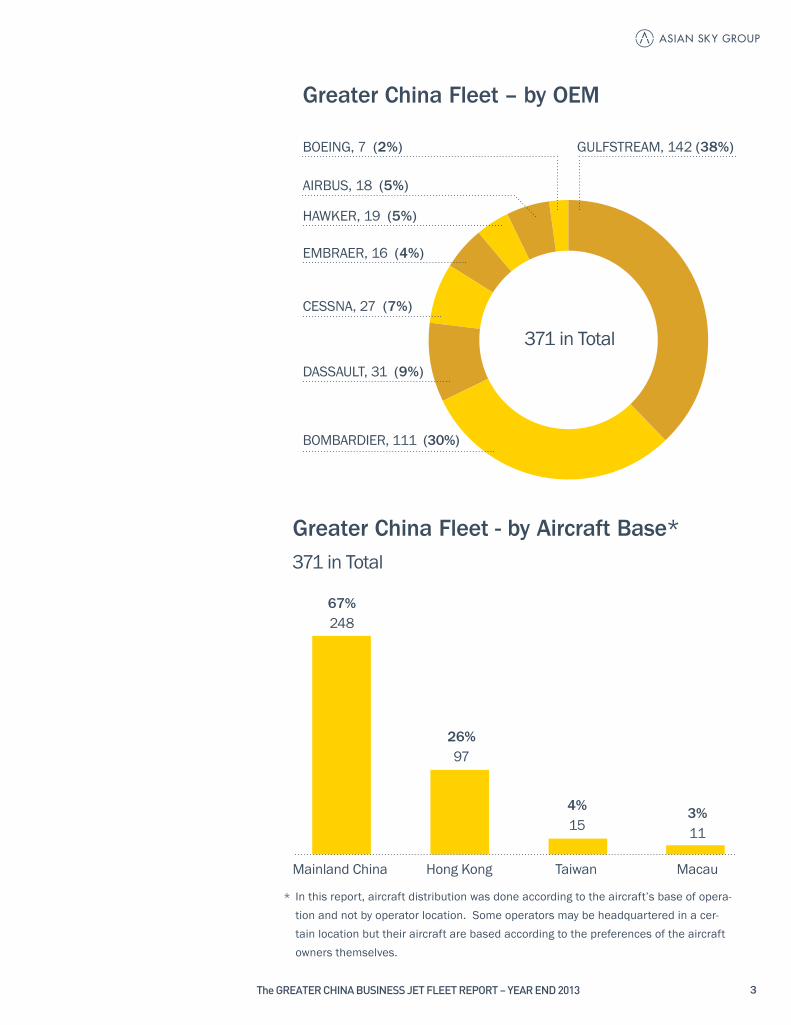

The Greater China business jet fleet grew by 21% during 2013 with the total number of aircraft reaching 371 at year-end 2013.

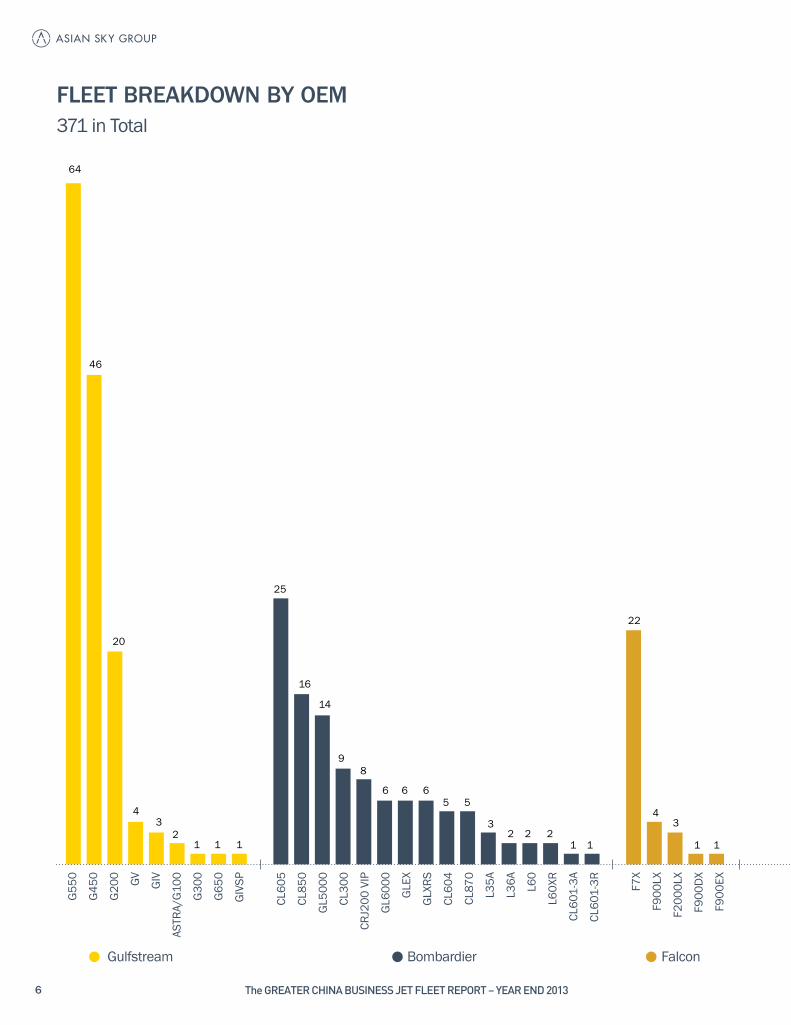

The Original Equipment Manufacturer (OEM) market leader by number of aircraft based and operated in Greater China continues to be Gulfstream with a 38% market share, followed by Bombardier with a 30% market share.

Both Gulfstream and Bombardier’s market share remained unchanged compared with year-end 2012.

The largest market share changes in 2013 were registered by Embraer, Falcon and Hawker.

• Embraer’s fleet doubled in 2013 rising from 8 to 16 aircraft based in Greater China.

• Dassault Falcon’s number of aircraft rose by over 60% with 15 additional aircraft entering into service.

• The Hawker market share in Greater China decreased from 9% to 5%.

The Gulfstream G-550 and G-450 remain the most prevalent models in Greater China with 64 and 46 aircraft respectively representing 30% of the total fleet in numbers.

The model with the highest number of new aircraft delivered in 2013 was the G-450 with 13 new deliveries followed by the Falcon 7X with 11 new aircraft delivered.

Of significant importance, the proportion of pre-owned aircraft delivered in 2013 rose to 47%, clearly demonstrating the increasing acceptance of purchasing pre-owned aircraft. The remaining 53% were new aircraft deliveries.

The 5 largest operators (HNA Group, BAA, TAG Aviation, Metrojet and Jet Aviation) make up 55% of the total number of business jets based and operating in the Greater China region.

Of the 371 aircraft in operation, 73% are under the local registrations of China, Hong Kong, Macau and Taiwan. The remaining 27% are operated under a foreign registry.

Aircraft 5 years old or younger, make up 62% of the fleet and another 20% are between 5 and 10 years old (based on year of manufacture).

While China’s business aviation market experienced robust growth in recent years, its preference for large cabin remained unchanged in 2013. Over 75% of the fleet in Greater China is in the large aircraft size category or above.

KEY FINDINGS

5The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

6 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

FLEET BREAKDOWN BY OEMG5

50

G450

G200 GV GI

V

ASTR

A/G1

00

G300

G650

GIVS

P

CL60

5

CL85

0

GL50

00

CL30

0

CRJ2

00 V

IP

GL60

00

GLEX

GLXR

S

CL60

4

CL87

0

L35A

L36A L6

0

L60X

R

CL60

1-3A

CL60

1-3R F7

X

F900

LX

F200

0LX

F900

DX

F900

EX

64

46

20

4

25

16

14

98

6 6 65 5

32 2 2

1 1

22

43

1 1

32

1 1 1

371 in Total

Gulfstream • Bombardier • Falcon

7The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

CIT

CJ1

CIT

SOVE

REGI

NCI

T

CJ1+

CIT

EXCE

L

CIT

II

CIT

S/II

CIT

VI

CIT

XLS

CIT

CJ3

CIT

X

H400

0

H800

XP

H900

XP

H400

XP

H850

XP

BJ 4

00A

LEGA

CY 6

50

LEGA

CY 6

00

LIN

EAGE

100

0

PHEN

OM 3

00

ACJ3

19

ACJ3

18 BBJ

7

5

32 2 2 2 2

1 1

5 54

2 21

9

12

67

3 3

1

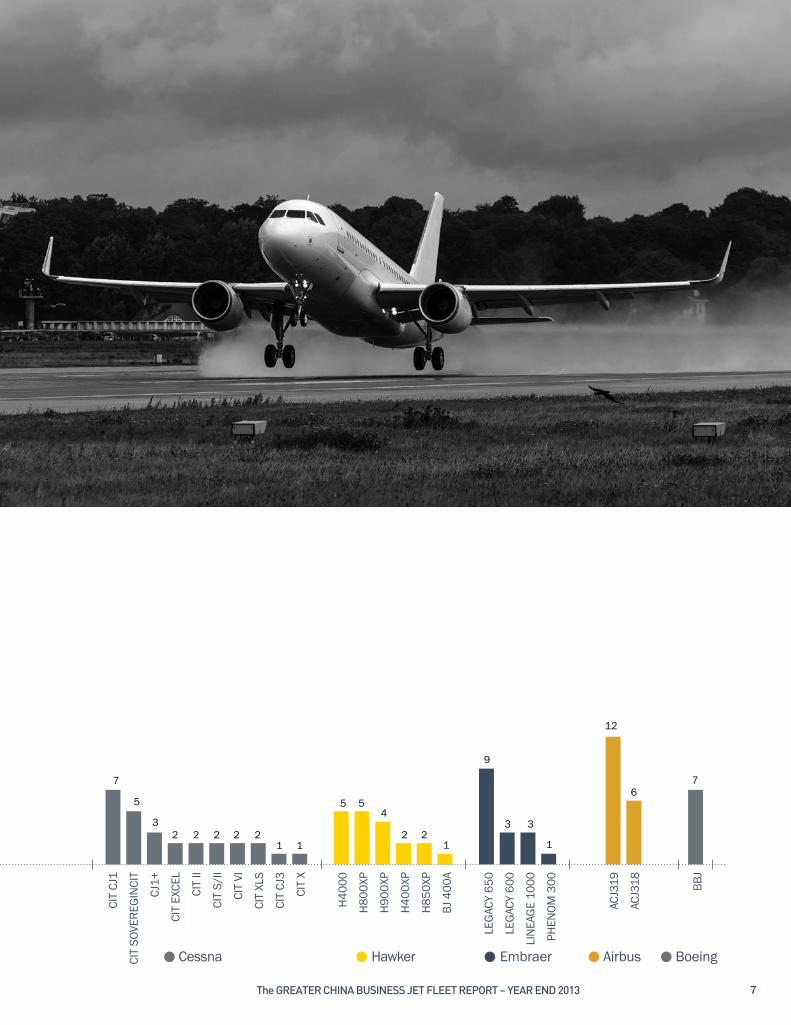

• Cessna • Hawker • Embraer • Airbus • Boeing

MACAU, 6 (5%)

Gulfstream Fleet by Region

Bombardier Fleet by Region

Dassault Fleet by Region

TAIWAN, 7 (5%)MACAU, 1 (1%)

HONG KONG, 46 (32%)

MAINLAND CHINA, 88 (62%)

TAIWAN, 3 (3%)

HONG KONG, 32 (29%)

MAINLAND CHINA, 70 (63%)

TAIWAN, 1 (3%)

MACAU, 1 (3%)

HONG KONG, 5 (16%)

MAINLAND CHINA, 24 (78%)

142 in Total

111 in Total

31 in Total

8 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Cessna Fleet by Region

Hawker Fleet by Region

Embraer Fleet by Region

HONG KONG, 2 (7%)

MAINLAND CHINA, 25 (93%)

27 in Total

TAIWAN, 2 (11%)

MACAU, 1 (5%)

HONG KONG, 1 (5%)

19 in Total

MAINLAND CHINA, 15 (79%)

TAIWAN, 1 (6%)

MACAU, 1 (6%)

HONG KONG, 3 (19%)

16 in Total

MAINLAND CHINA, 11 (69%)

9The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

10 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Airbus Fleet by Region

Boeing Fleet by Region

TAIWAN, 1 (5%)

MACAU, 1 (5%)

HONG KONG, 5 (28%)

MAINLAND CHINA, 11 (61%)

18 in Total

7 in Total

MAINLAND CHINA, 4 (57%)

HONG KONG, 3 (43%)

11The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

OEM Market Share - Mainland China

OEM Market Share - Hong Kong

BOEING, 4 (2%)AIRBUS, 11 (4%)

EMBRAER, 11 (4%)

HAWKER, 15 (6%)

DASSAULT, 24 (10%)

CESSNA, 25 (10%)

BOMBARDIER, 70 (28%)

GULFSTREAM, 88 (36%)

HAWKER, 1 (1%)

CESSNA, 2 (2%)BOEING, 3 (3%)EMBRAER, 3 (3%)

AIRBUS, 5 (5%)

DASSAULT, 5 (5%)

97 in Total

248 in Total

BOMBARDIER, 32 (33%) GULFSTREAM, 46 (48%)

OEM Market Share - Taiwan

OEM Market Share - Macau

AIRBUS, 1 (7%)EMBRAER, 1 (7%)

DASSAULT, 1 (7%)

HAWKER, 2 (13%)

BOMBARDIER, 3 (20%) GULFSTREAM, 7 (46%)

AIRBUS, 1 (9%)

EMBRAER, 1 (9%)

HAWKER, 1 (9%)

GULFSTREAM, 1 (9%) BOMBARDIER, 6 (55%)

15 in Total

11 in Total

DASSAULT, 1 (9%)

12 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

14 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Gulfstream Fleet Breakdown by Operator

Deer

Jet

Met

roje

t

BAA

Jet A

viatio

n

Chin

a Ea

ster

n

TAG

Avia

tion

Nans

han

Jet

Jet B

ear

Asia

Jet

Beijin

g Ai

rline

s

Win

Air

AIDC

AllP

oint

s Je

t

Hong

kong

Jet

Sino

Jet

Star

Jet

CAAC

Insp

ectio

n

Fortu

na Je

t

Glob

al Je

t

Man

darin

Air

Lily

Jet

45

40

35

30

25

20

15

10

5

0

GVGIVG650G550G450G300G200G100

34

2112

6

46

1

134

2

20

88

2

18

184

2

15

32

1

6

23

5

13

4

2

2

4

12

3

12

3

21

322

11

2

11

2

1

1

2

1

1

2

1

1

1

1

1

1

1

1

1

1

Total441

64461

202

142

142 in Total

Total

15The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Bombardier Fleet Breakdown by Operator 111 in Total

TAG

Avia

tion

Chin

a Un

ited

BAA

Lily

Jet

Dong

hai J

et

CARS

SM

etro

jet

Sino

Jet

Jet A

viatio

nVi

sta

Jet

Jet A

sia

Deer

Jet

Asia

Air

Med

ical

Chin

a Ea

ster

nEx

ecut

ive A

viatio

nFr

eeSk

y Avia

tion

Hanh

wa Je

tNa

nsha

n Je

tAe

gle

Avia

tion

Beijin

g Ai

rline

sEV

A Ai

rway

sGl

obal

Jet

Good

Jet

Hong

kong

Jet

Wat

erpa

rkYi

Feng

Jet

Fortu

na Je

t

25

20

15

10

5

0

GLEX/XRS/6000GL5000CL870CL850/CRJ200CL604/605CL300LJ35/36/60

48

45

122

57

12

2

34

110

2

53

10

25

755

11

3

5

11

21

5

2

2

4

1

21

4

1

3

4

1

1

222

1

1

2

11

2

2

2

2

2

1

1

2

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

Total 18145

253199

111Total

16 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Total

Total

Dassault Fleet Breakdown by Operator

BAA

Beijin

g Ai

rline

s

TAG

Avia

tion

Deer

Jet

Min

shen

g In

t’l Je

t

Glob

al Je

t

Jet A

viatio

n

Mac

au Je

t

Nans

han

Jet

10

8

6

4

2

0

FALCON 900LXFALCON 900EXFALCON 900DXFALCON 7XFALCON 2000LX

31

7

11

4

4

314

3

3

12

3

112

1

1

211

1

1

411

223

31

31 in Total

Total

Total

Cessna Fleet Breakdown by Operator

CAAC

Aca

dem

y

CAAC

Insp

ectio

n

Chin

a Un

ited

Zhon

gfei

Avia

tion

Broa

d

BAA

Chin

a Ea

ster

n

Zhiyu

an A

viatio

n

Jet A

viatio

n

Met

roje

t

1086420

750 X650 VI680 SOVEREIGN550 II/SII560 EXCEL/XLS 525 CJ1/2/3 7

7

113

2

7

1

2

3

21

3

112

11

1

111

11

1

1

12544

1127

27 in Total

17The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Total

Total

Hawker Fleet Breakdown by Operator

Embraer Fleet Breakdown by Operator

Deer

Jet

BAA

Asi

a Ai

r Med

ical

Aeg

le A

viatio

n

Chi

na E

aste

rn

Exe

cutiv

e Av

iatio

n

Jet

Asi

a

Sun

rise

Airli

nes

HAWKER 900XPHAWKER 850XPHAWKER 800XPHAWKER 400XPHAWKER 4000

324

211

22

1

111

1

1

1

1

1

1

1

1

42535

19

Chin

a Ea

ster

n

Met

roje

t

Min

shen

g In

t’l Je

t

Mac

au L

andm

ark

TAG

Avia

tion

Exec

utive

Avia

tion

Ordo

s GA

Sino

Jet

3210

Total

TotalPHENOM 300LINEAGE 1000LEGACY 650LEGACY 600

3

3

1113

3

3

1

12

11

211

1

1

1

1

1393

16

10

8

6

4

2

0

19 in Total

16 in Total

Total

Total

Total

Airbus Fleet Breakdown by Operator

Boeing Fleet Breakdown by Operator

BAA

Hong

kong

Jet

Chin

a Un

ited

Deer

Jet

Beijin

g Ai

rline

s

Chin

a Ea

ster

n

Com

lux A

viatio

n

EVA

Airw

ays

TAG

Avia

tion

Deer

Jet

EVA

Airw

ays

Hong

Kon

g Je

t

Met

roje

t

Nans

han

Jet

Beijin

g Ai

rline

s

3

2

1

0

2

1

0

ACJ319ACJ318

123

213

3

3

3

3

112

11

1

111

1

1

126

18

BBJ 2 1 1 1 1 1

7 in Total

18 in Total

7

18 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

20 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

FLEET BREAKDOWN BY AIRCRAFT SIZE CATEGORYOver 75% of the Greater China fleet is in the large size category and above. In comparison, the global market share of those categories is closer to 25%.

Aircraft Size Category Breakdown

CORPORATE AIRLINERLINEAGE 1000ACJ318ACJ319/ERBOEING BBJ

SUPER-MID SIZEBEECHJET 400AG200CHALLENGER 300HAWKER 4000CITATION X

ULTRA LONG RANGEFALCON 7XGLOBAL 6000GLOBAL EXPRESGLOBAL EXPRESS XRSGVG550G650

MID SIZEASTRA/G100CITATION SOVEREIGNHAWKER 800XPHAWKER 850XPHAWKER 900XPLEARJET 60/XR

SUPER-LARGEGIVGIV SPG450GLOBAL 5000FALCON 900EXFALCON 900DXFALCON 900LX

SUPER-LITECITATION EXCELCITATION VICITATION XLSLEARJET 35ALEARJET 36A

LARGECHALLENGER 601CHALLENGER 604CHALLENGER 605CRJ200 VIPCHALLENGER 850CHALLENGER 870LEGACY 600LEGACY 650FALCON 2000LXG300

LITECITATION CJ1/+CITATION CJ3CITATION II/SIIPHENOM 300HAWKER 400XP

CORPORATE A/L, 28 (8%)

ULTRA LR, 109 (29%)

S-LARGE, 70 (19%)

LARGE, 77 (21%)

S-MID, 35 (9%)

MID, 22 (6%)

S-LITE, 11 (3%)

LITE, 19 (5%)

371 in Total

Over 75% Large & above

21The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Corporate Airliner Category Breakdown by Model

Ultra Long-Range Category Breakdown by Model

Super-Large Category Breakdown by Model

ACJ318, 6 (21%)

ACJ319, 12 (43%)

G550, 64 (59%)

GIV, 3 (4%)

G450, 46 (66%)

GLOBAL 5000, 14 (21%)

FALCON 900LX, 4 (6%)

FALCON 900EX, 1 (1%)

FALCON 900DX, 1 (1%) GIV SP, 1 (1%)

FALCON 7X, 22 (20%)

GLOBAL 6000, 6 (5%)

GLOBAL EXPRESS, 6 (5%)

GLOBAL XRS, 6 (6%)

GV, 4 (4%) G650, 1 (1%)

BBJ, 7 (25%)

LINEAGE 1000, 3 (11%)

28 in Total

109 in Total

70 in Total

Large Category Breakdown by Model

Super Mid-Size Category Breakdown by Model

Mid-Size Category Breakdown by Model

CITATION SOVEREIGN, 5 (23%)

HAWKER 800XP, 5 (23%)HAWKER 850XP, 2 (9%)

HAWKER 900XP, 4 (18%)

LEARJET 60, 2 (9%)

LEARJET 60XR, 2 (9%) ASTRA, 2 (9%)

22 in Total

G200, 20 (57%)CHALLENGER 300, 9 (26%)

HAWKER 4000, 5 (14%)

CITATION X, 1 (3%)

35 in Total

CHALLENGER 604, 5 (7%)

CHALLENGER 605, 25 (32%)

CHALLENGER 850, 16 (21%)CHALLENGER 870, 5 (7%)

CRJ 200 VIP, 8 (10%)

LEGACY 600, 3 (4%)

LEGACY 650, 9 (12%)

FALCON 2000LX, 3 (4%) G300, 1 (1%) CHALLENGER 601, 2 (2%)

77 in Total

22 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Super-Lite Category Breakdown by Model

Lite Category Breakdown by Model

CITATION EXCEL, 2 (18%)

CITATION VI, 2 (18%)

CITATION XLS, 2 (18%)LEARJET 35A, 3 (28%)

LEARJET 36A, 2 (18%)

11 in Total

CITATION CJ1, 7 (37%)

CITATION CJ1+, 3 (16%)

BEECHJET 400A, 1 (5%)

CITATION CJ3, 1 (5%)

CITATION II, 2 (10%)

CITATION S/II, 2 (11%)

PHENOM 300, 1 (5%)

HAWKER 400XP, 2 (11%)

19 in Total

23The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

24 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

FLEET BREAKDOWN BY OPERATOR

Total Fleet Breakdown by Operator

There are 45 operators in Greater China, with 26 of them based in Mainland China, 9 in Hong Kong, 6 in Taiwan and 4 in Macau. The 5 largest operators make up 55% of the total number of business jets in Greater China.

In order to operate a locally-registered aircraft in Mainland China, one must first obtain an Aircraft Operator Certificate (AOC) or use the services of an established aircraft management company which has already obtained an AOC.

Deer

Jet

BAA

TAG

Avia

tion

Met

roje

t

Jet A

viat

ion

Chin

a Un

ited

Chin

a Ea

ster

n

Lily

Jet

Beiji

ng A

irlin

es

CAAC

Insp

ectio

n

Nan

shan

Jet

Sino

Jet

CAAC

Aca

dem

y

Dong

hai J

et

Hong

kong

Jet

Min

shen

g In

t'l Je

t

CARS

S

Jet A

sia

Exec

utiv

e Av

iatio

n

Glob

al Je

t

Jet B

ear

Vist

a Je

t

67

45

34

30

22

18

14

11 11

8 8 87 7 7 6 5 5

4 4 4 4

45 operators, 371 Aircraft in Total

18% of total fleet

12% of total fleet

25The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Asia

Air

Med

ical

Asia

Jet

Zhon

gfei

Avi

atio

n

EVA

Airw

ays

Win

Air

Aegl

e Av

iatio

n

AIDC

AllP

oint

s Je

t

Broa

d

Fort

una

Jet

Free

Sky

Avia

tion

Hanh

wa

Jet

Mac

au L

andm

ark

Star

Jet

Com

lux

Avia

tion

Good

Jet

Zhiyu

an A

viat

ion

Mac

au Je

t

Man

darin

Air

Ordo

s GA

Sunr

ise

Airli

nes

Wat

erpa

rk

YiFe

ng Je

t

3 3 3 3 32 2 2 2 2 2 2 2 2 1 1 1 1 1 1 1 1 1

Photo courtesy of Nikita Maltsev

TOP OPERATORS OVERVIEW

Hainan Airlines GroupHainan Airlines Group (HNA) is a large privately owned airline group headquartered in Haikou, Hainan Island, China. The company, together with its affiliates and subsidiaries, operates an extensive network of domestic and international aviation services. HNA Group’s business jet operations are carried out by several of its subsidiaries, namely Deer Jet and Hongkong Jet. The company offers aircraft management services, business charter, aircraft leasing, flight support and ground handling services, and is also engaged in airport management, FBO and MRO services. Most of HNA Group’s aircraft are based in Beijing, Shanghai, Tianjin, Hainan Island and Hong Kong. Its total business jet fleet numbers 74 aircraft, which makes HNA Group the largest operator of business jets in Greater China.

BAABusiness Aviation Asia Ltd. (BAA) is a business aviation services provider headquartered in Shenzhen and with bases throughout China and Hong Kong. BAA is the largest operator of privately owned business jets in Greater China. Their 45 business jets are based in various cities including Shenzhen, Hong Kong, Beijing and Taipei.

TAG Aviation AsiaTAG Aviation Asia is headquartered in Hong Kong with a fleet of 34 business jets in Greater China. It provides private aviation services including aircraft charter, aircraft management and maintenance services. TAG’s aircraft are based in Hong Kong, China and Macau.

MetrojetEstablished in 1995, Metrojet pioneered business aviation services in Hong Kong, specialising in aircraft management, maintenance, charter, and consultancy services. Metrojet currently manages a fleet of 30 mid and large sized business jets, most of which are based in Hong Kong. Of Greater China’s operators, Metrojet has the largest fleet of aircraft based in Hong Kong. Over the past two years, Metrojet has expanded its footprint in Asia with the establishment of Metrojet Engineering Clark in Clark, The Philippines; Tajair Metrojet Aviation in Mumbai, India; and Metrojet Hanxing Zhuhai in Zhuhai, China.

Jet Aviation HKThe Jet Aviation HK fleet of 22 aircraft in Greater China is primarily based in Hong Kong. Jet Aviation provide aircraft management services together with maintenance and aircraft charter services.

26 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

27The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Top 5 Operators Fleet Breakdown by OEM

70

60

50

40

30

20

10

0

HAWKER

CESSNA

EMBRAER

DASSAULT

GULFSTREAM

BOMBARDIER

BOEING

AIRBUS

HNA Group*

11

3

48

3

3

6

74

BAA

2

1

11

18

10

3

45

TAG Aviation

2

4

5

22

1

34

Metrojet

1

3

20

5

1

30

Jet Aviation

1

2

15

4

22

13

3

5

20

106

44

4

10

205

205 in Total

Total

Total

* Including Hongkong Jet and Deer Jet

28 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

HNA Group Fleet Breakdown by ModelG

550

G45

0

G20

0

ACJ3

19

H80

0XP

GIV

F7X

GV

H90

0XP

BBJ

H40

00

H85

0XP

ACJ3

18

CL60

5

GL5

000

GL6

000

22

13

65% Gulfstream

65

4 43 3 3 3

2 21 1 1 1

74 in Total

Metrojet Fleet Breakdown by Model

G55

0

G45

0

CL60

5

G20

0

BBJ

CL60

4

CIT

SOV

L600

L650

L100

0

GL5

000

GLE

X

GV

66% Gulfstream

13

4

2 21 1 1 1 1 1 1 1 1

30 in Total

29The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Jet Aviation Fleet Breakdown by Model

G55

0

G45

0

CL60

5

GL5

000

G20

0

CIT

CJ3

F7X

F900

LX

G65

0

68% Gulfstream

8

4

2 2 21 1 1 1

22 in Total

BAA Fleet Breakdown by Model

TAG Aviation Fleet Breakdown by Model

G45

0

G55

0

F7X

CL60

5

CL85

0

F900

LX

ACJ3

18

GL6

000

G20

0

H40

00

ACJ3

19

CIT

CJ1+

F900

EX

L60X

R

GL5

000

CL85

0

CL60

5

F7X

G45

0

CL60

4

GL6

000

G55

0

ACJ3

19

L650

L100

0

F200

0LX

GL

EX

GL

XRS

L60

Largest Falcon Operator

65% Bombardier

8 87

43

8

43 3 3

2 2 21 1 1 1 1 1 1

32 2 2 2

1 1 1 1

45 in Total

34 in Total

Other Large Operators

ChINA UNITED AIRLINESCRJ 200 VIPCHALLENGER 870CITATION S/IICITATION VIACJ319

ChINA EASTERN AIRLINES ExECUTIvE AIRLEGACY 650G550G450ACJ318CHALLENGER 300CITATION SOVEREIGNGLOBAL EXPRESS XRSG-200HAWKER 800XP

LILy JETCHALLENGER 850CHALLENGER 604CHALLENGER 605GLOBAL EXPRESSGLOBAL EXPRESS XRSG200

BEIJING AIRLINESFALCON 7XG450ACJ318ACJ319GLOBAL EXPRESSG550BBJ

NANShAN JETG450BBJCHALLENGER 605FALCON 7XGLOBAL EXPRESS XRSG550

SINO JETCHALLENGER 605CHALLENGER 300LEGACY 650GLOBAL 5000GLOBAL EXPRESSG200G550

ChINA FLIGhT INSPECTION CENTRE OF CAACCITATION SOVEREIGNCITATION XLSCITATION VICITATION XG450

875213

14332111111

11521111

114211111

8311111

82111111

832111

31The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

32 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

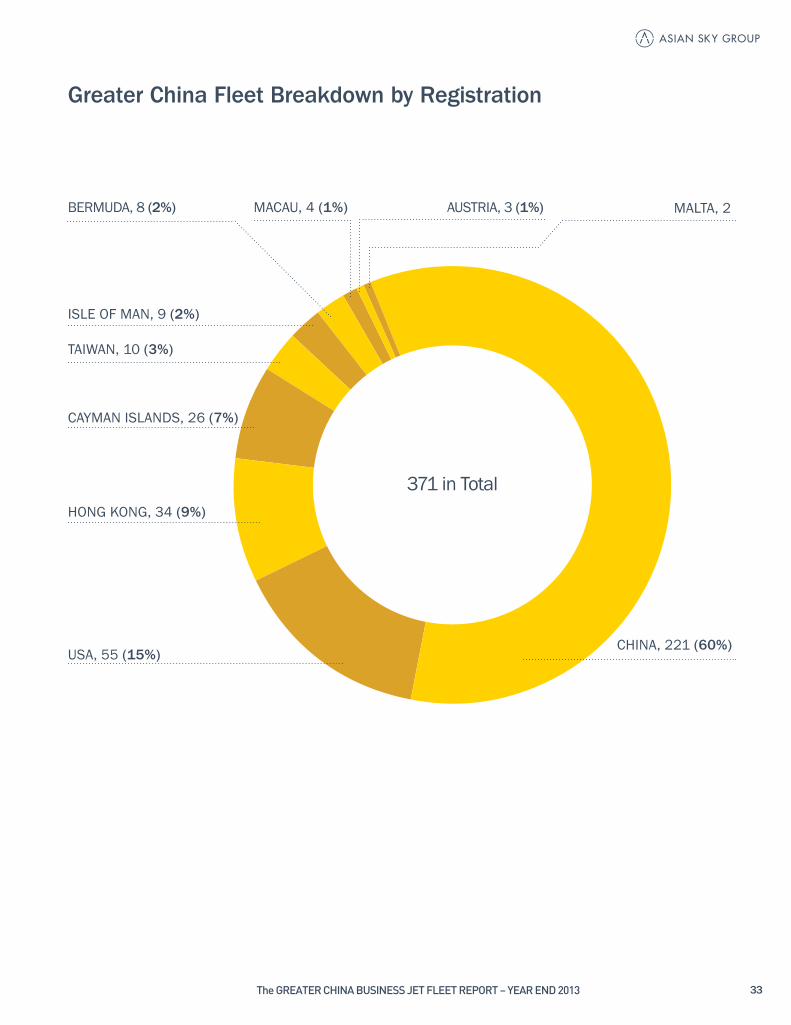

FLEET BREAKDOWN BY AIRCRAFT REGISTRATION

When considering the purchase of a business aircraft to be based in Greater China, selection of the country of aircraft registration can be a key decision.

Depending on the owner’s specific needs, there are many factors to be considered which may significantly affect the choice of registration, such as the primary routes the aircraft is intended to fly; the location of the aircraft’s base, the intended ownership period; operational and maintenance requirements; the desired operator; import tax and VAT aspects; aircraft residual values; variable costs and fees; financing requirements; and training requirements.

The operation of foreign-registered aircraft is subject to limitations in Mainland China under China’s ‘Rules Governing Foreign Civil Aircraft’. Limitations include restrictive routings, flight application processing time, application processing fees, airport access restrictions, landing and takeoff slots, and higher fees for navigation, landing, parking, ground handling and fuel.

Of all the aircraft based in Mainland China, 86% are China-registered. In comparison, only 29% of the aircraft based in Hong Kong are registered in Hong Kong.

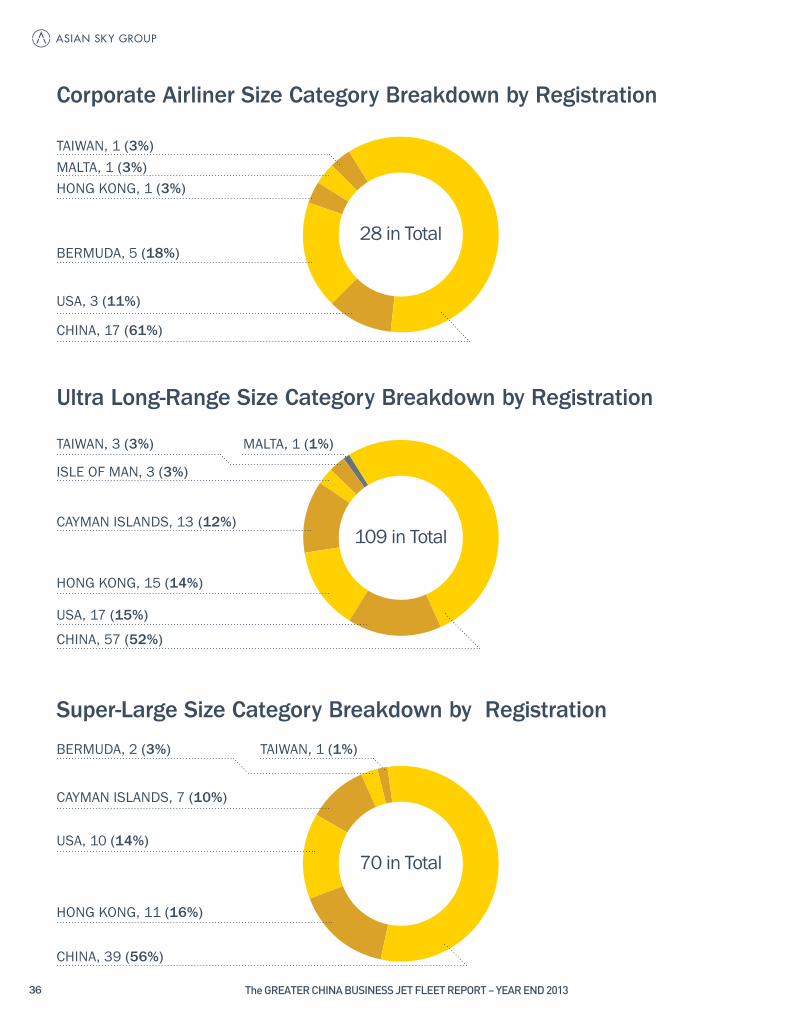

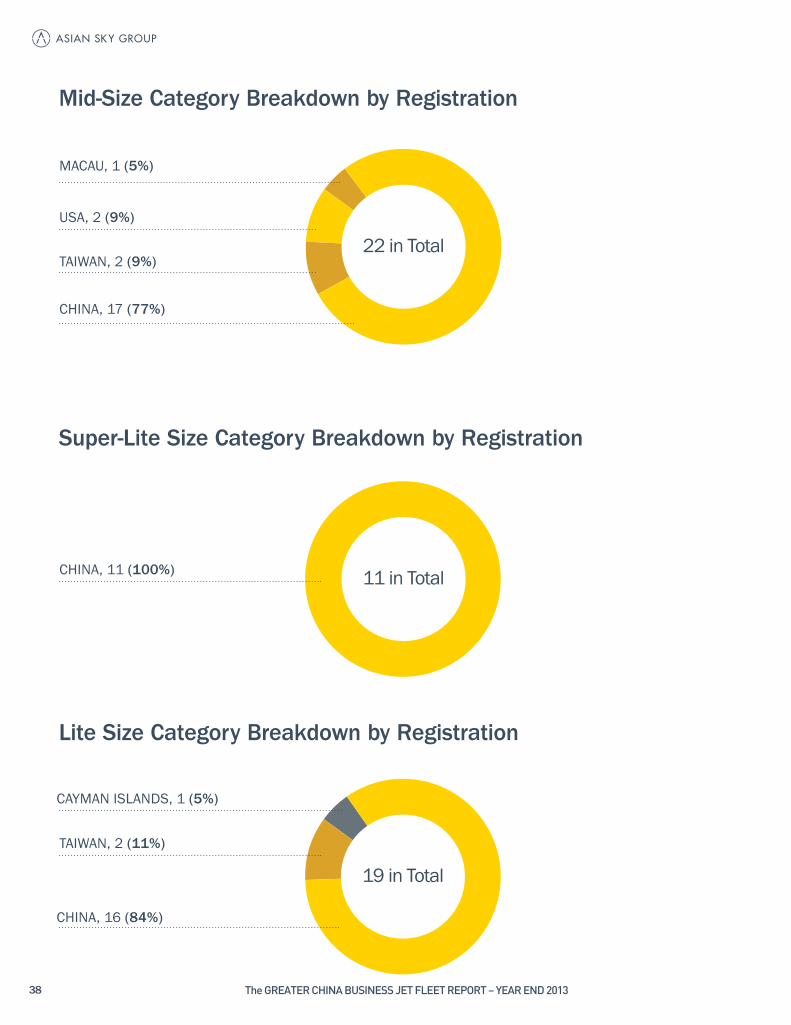

As one would expect, the majority of aircraft in the Lite size category are locally registered while in the larger categories, they are mostly registered under foreign aviation authorities.

33The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

371 in Total

Greater China Fleet Breakdown by Registration

USA, 55 (15%)

HONG KONG, 34 (9%)

CAYMAN ISLANDS, 26 (7%)

TAIWAN, 10 (3%)

ISLE OF MAN, 9 (2%)

BERMUDA, 8 (2%) MACAU, 4 (1%) AUSTRIA, 3 (1%) MALTA, 2

CHINA, 221 (60%)

Hong Kong Fleet Breakdown by Registration

USA, 29 (30%)

HONG KONG, 28 (29%)

CAYMAN ISLANDS, 21 (22%)

BERMUDA, 8 (8%)

CHINA, 6 (6%)

AUSTRIA, 3 (3%)

ISLE OF MAN, 2 (2%)

97 in Total

Mainland China Fleet Breakdown by Registration

CHINA, 214 (86%)

USA, 16 (7%)

HONG KONG, 5 (2%)

MALTA, 1

TAIWAN, 1

CAYMAN ISLANDS, 5 (3%)248 in Total

ISLE OF MAN, 6 (3%)

34 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Taiwan Fleet Breakdown by Registration

Macau Fleet Breakdown by Registration

TAIWAN, 9 (60%)

USA, 5 (33%)

CHINA ,1 (7%)

MACAU, 4 (37%)

MALTA, 1 (9%)

ISLE OF MAN, 1 (9%)

HONG KONG, 1 (9%)

USA, 4 (37%)

15 in Total

11 in Total

35The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

36 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Corporate Airliner Size Category Breakdown by Registration

Ultra Long-Range Size Category Breakdown by Registration

CHINA, 17 (61%)

CHINA, 57 (52%)

USA, 17 (15%)

HONG KONG, 15 (14%)

CAYMAN ISLANDS, 13 (12%)

ISLE OF MAN, 3 (3%)

TAIWAN, 3 (3%) MALTA, 1 (1%)

USA, 3 (11%)

BERMUDA, 5 (18%)

MALTA, 1 (3%)

HONG KONG, 1 (3%)

TAIWAN, 1 (3%)

28 in Total

109 in Total

Super-Large Size Category Breakdown by Registration

HONG KONG, 11 (16%)

USA, 10 (14%)

CAYMAN ISLANDS, 7 (10%)

BERMUDA, 2 (3%) TAIWAN, 1 (1%)

CHINA, 39 (56%)

70 in Total

37The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Large Size Category Breakdown by Registration

Super Mid-Size Category Breakdown by Registration

CHINA, 39 (51%)

CHINA, 25 (71%)

USA, 7 (20%)

HONG KONG, 2 (6%)

CAYMAN ISLANDS, 1 (3%)

USA 15, (20%)

ISLE OF MAN, 6 (8%)

HONG KONG, 5 (7%)

CAYMAN ISLANDS, 4 (5%)

MACAU, 3 (4%) AUSTRIA, 3 (4%) BERMUDA, 1 (1%)

77 in Total

35 in Total

38 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Mid-Size Category Breakdown by Registration

Super-Lite Size Category Breakdown by Registration

Lite Size Category Breakdown by Registration

CHINA, 17 (77%)

CHINA, 11 (100%)

CHINA, 16 (84%)

TAIWAN, 2 (11%)

CAYMAN ISLANDS, 1 (5%)

TAIWAN, 2 (9%)

USA, 2 (9%)

MACAU, 1 (5%)

22 in Total

11 in Total

19 in Total

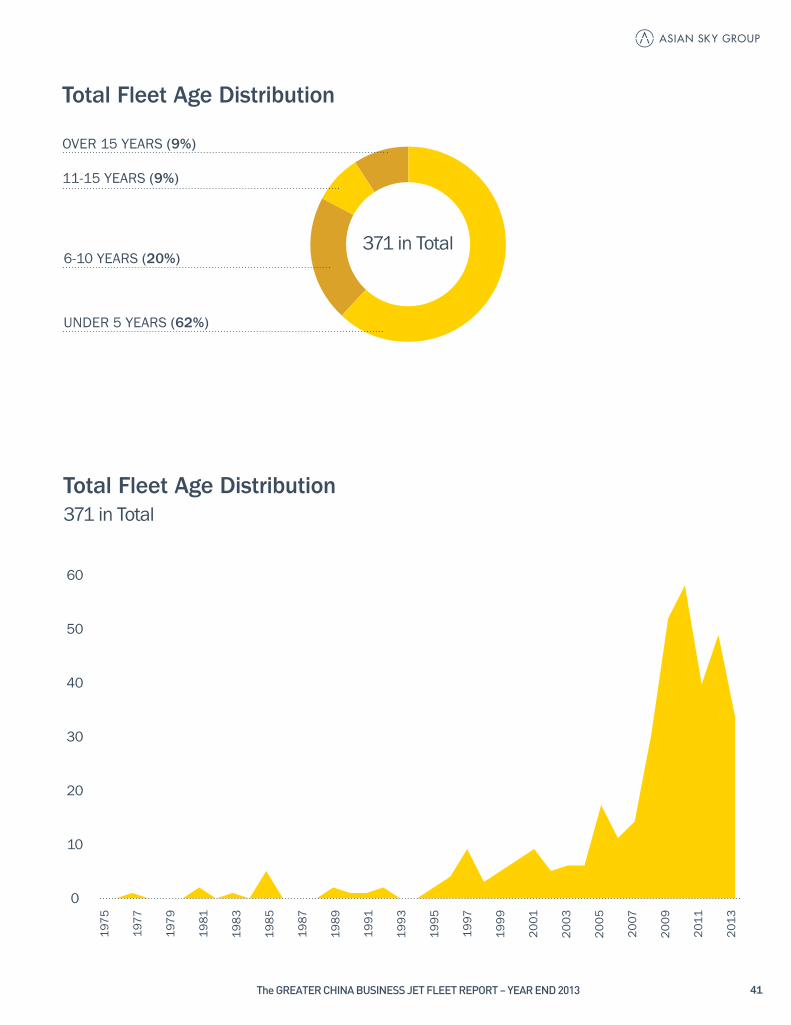

FLEET BREAKDOWN BY AIRCRAFT AGE DISTRIBUTION

Not too surprisingly, the Greater China business jet fleet is a young fleet. Over 60% of the fleet is under 5 years old, with the majority of these aircraft being long-range and large cabin aircraft.

The Greater China business jet fleet only started to grow significantly from 2003. The market initially belonged to the Mid-Size and Super Mid-Size category of aircraft. From 2010 onwards however, the Large category and up began their dominance.

Also of note is that Bombardier was one of the early pioneers in the Greater China market. In more recent years however, it has had to cede this advantage and see Gulfstream’s market share surpass its own. Other early pioneers like Cessna and Hawker have also suffered throughout the years, in this case due to a lack of products in the Large category and up.

The aircraft age distributions shown in the following charts are based on the aircraft’s year of manufacture (YOM) and therefore do not reflect the time of delivery and entry into service of pre-owned aircraft.

40 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

41The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Total Fleet Age Distribution

UNDER 5 YEARS (62%)

6-10 YEARS (20%)

11-15 YEARS (9%)

OVER 15 YEARS (9%)

Total Fleet Age Distribution

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

60

50

40

30

20

10

0

371 in Total

371 in Total

42 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

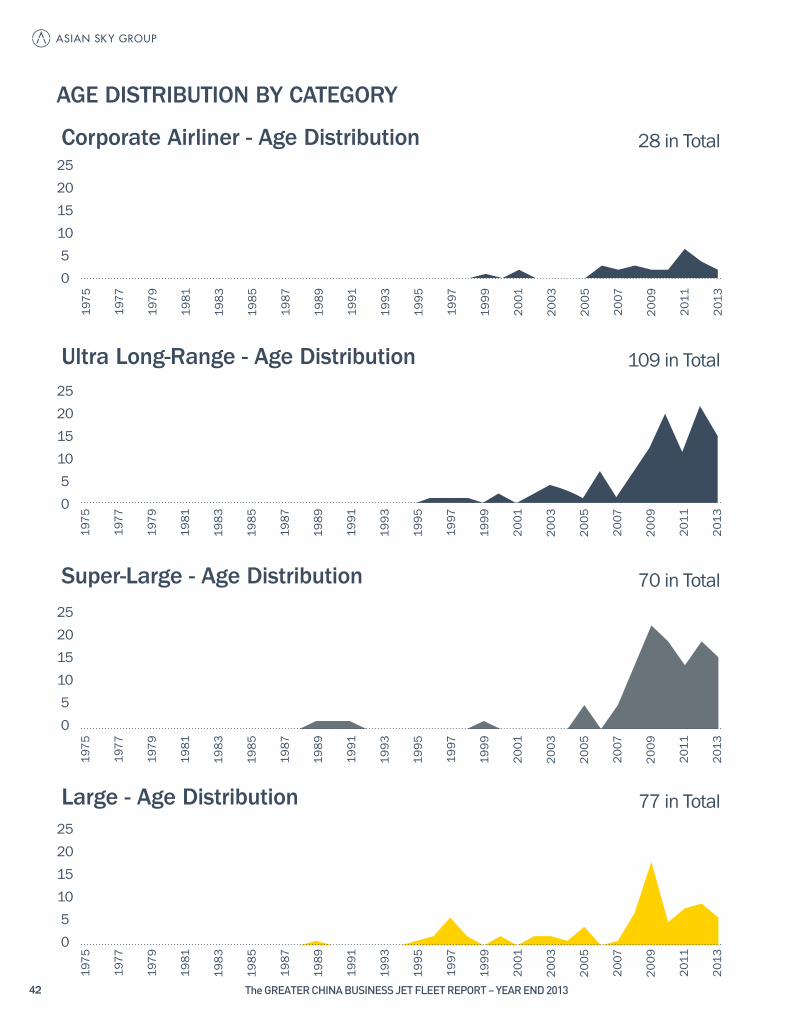

AGE DISTRIBUTION BY CATEGORY

Corporate Airliner - Age Distribution

Ultra Long-Range - Age Distribution

Super-Large - Age Distribution

Large - Age Distribution

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2520151050

2520151050

2520151050

2520151050

70 in Total

109 in Total

28 in Total

77 in Total

43The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Super Mid-Size - Age Distribution

Mid-Size - Age Distribution

Super-Lite - Age Distribution

Lite - Age Distribution

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2520151050

2520151050

2520151050

2520151050

19 in Total

11 in Total

22 in Total

35 in Total

44 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

Gulfstream Age Distribution

Bombardier Age Distribution

Dassault Age Distribution

Cessna Age Distribution

2520151050

2520151050

2520151050

2520151050

142 in Total

111 in Total

31 in Total

27 in Total

AGE DISTRIBUTION BY OEM

45The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Hawker Age Distribution

Embraer Age Distribution

Airbus Age Distribution

Boeing Age Distribution

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2520151050

2520151050

2520151050

2520151050

19 in Total

16 in Total

18 in Total

7 in Total

46 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

SUPPORT INFRASTRUCTURE

Support Facilities - Bombardier

OEMs realize that a key factor in the buyers’ selection of an aircraft is the OEM’s local support infrastructure and regional presence. The following maps show each OEM’s maintenance facilities, training centers, completion centers and their locations in Greater China.

Another important part of the business aviation support infrastructure are FBO facilities and services. Airports in major cities in China, in a bid to attract more business aviation interest, have or are setting up business aviation terminals. Some airports have put in place special channels for business aviation passengers and some others, while having no dedicated facilities, are planning such facilities to support business aircraft requirements. Hong Kong, Macau and Taipei all have fully established FBO facilities in operation. The last map shows the current FBO facilities and their locations in Greater China.

Authorized Maintenance Center

ExecuJet Haite AviationLearjet 60, Challenger 604/605, Global

Metrojet

Challenger 300, Challenger 604/605, Global

STAECOChallenger 604/605, Global

Hawker Pacific Global

Tianjin

Hong Kong

Jinan

Shanghai

47The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Support Facilities - Dassault Falcon

ShanghaiHawker Pacific F2000, F2000DX, F2000EX, F2000LX, F2000S, F900DX, F900EX, F900LX, F7X

Jet Aviation

F2000DX, F2000EX F2000LX, F2000S, F900DX, F900EX, F900LX, F7X

Hong Kong

Authorized Maintenance Center

48 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Support Facilities - Gulfstream

Authorized Maintenance Center

Training Center

Gulfstream Beijing Service CenterG200, G450, G550

CAEG450, G550

MetrojetG100, G150, G200, G300/G400, G350/G450, G500/G550, GIV/GIV-SP, GV

Jet Aviation

G450, G550, G650

Flight SafetyG450, G550

Beijing

Shanghai

Hong Kong

49The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Support Facilities - Cessna

Authorized Maintenance Center

Beijing DINGSHI GA Tech Service CenterCitation XLS, Citation Sovereign, Citation X

Hawker Pacific Citation XLS + family, Citation Sovereign, Citation X

Beijing

Shanghai

50 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Support Facilities - Embraer

Authorized Maintenance Center

Training Center

Execujet Haite AviationLegacy 600, Legacy 650, Lineage 1000

Lufthansa Hainan Airline Center

Legacy 650 maintenance level II training

Zhuhai XiyangyiTraining Center

Legacy 650, Lineage 1000

Metrojet

Legacy 600, Legacy 650, Lineage 1000

Hainan Airline Training CenterLegacy 650, Lineage 1000

Tianjin

Xi’an

Zhuhai Hong Kong

Sanya

51The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Support Facilities - Airbus

Authorized Maintenance Center

Training Center

Completion Center

AMECO

ACJ318, ACJ319, ACJ320

STARCO

ACJ318, ACJ319, ACJ320

Lufthansa Technik

Components

ST Aerospace Technologies (Xiamen)

Components

TAECOACJ318, ACJ319, ACJ320

TAECO

ACJ318, ACJ319, ACJ320

Airbus Service CenterACJ318, ACJ319, ACJ320

Beijing Training Center

ACJ318, ACJ319, ACJ320

Beijing

Shanghai

Shenzhen

Xiamen

52 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Support Facilities - Boeing

China Service Center

BBJ

Boeing Shanghai Aviation Service Center

BBJ

TAECO

BBJ

Shanghai Training Campus

BBJ

Beijing

Shanghai

Xiamen

Authorized Maintenance Center

Training Center

Completion Center

53The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Fixed Base Operations (FBO) - Greater China

Beijing CJET FBO

Shanghai Hawker Pacific Business Aviation Center

Taipei Eva Sky Jet Center

Taoyuan Business Aviation Center

Executive Aviation FBO

Hong Kong BACMacau BusinessAviation Center

Deer Jet Sanya FBO

Deer Jet Haikou FBO

Deer Jet Changsha FBO

Deer Jet Shenzhen FBO

Fixed Base Operations Facility

54 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Global Completion Facilities - OEM Completion Centers

Airbus ACJ Family

Challenger & Global

Learjet

Falcon

Legacy 600/650, Lineage 1000 and Phenom 100/300

Phenom 100/300

Gulfstream

Gulfstream

Gulfstream

Gulfstream

Gulfstream

Cessna

Airbus

Bombardier

Dassault

Embraer

Gulfstream

Cessna

Toulouse, France

Montreal, QC, Canada

Wichita, KS, USA

Little Rock, AR, USA

Sao Paulo, Brazil

Melbourne, FL, USA

Appleton, WI, USA

Brunswick, GA, USA

Dallas, TX, USA

Long Beach, CA, USA

Savannah, GA, USA

Wichita, KS, USA

55The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Global Completion Facilities - Independent Completion Centres

Aeria Luxury InteriorsAltitude Aerospace InteriorsAMAC Aerospace

BaySys Technologies

Bizjet

Comlux Completion USADuncan Aviation

Gore Design Completions

Greenpoint TechnologiesInnotech AviationHillaero Modification Centre

JCB Aero

Jet Aviation

Kvand Aircraft InteriorsL-3 Platform Integration

Lufthansa Technik

PATS Aircraft Systems

Sabena TechnicsSR Technics

ST AerospaceStandard Aero, Associated Air CentreTAECO Aerospace Company

San Antonio, TX, USAAuckland, New ZealandBasel, Switzerland

Melfa, VA, USA

Tulsa, OK, USA

Indianapolis, IN, USALincoln, NE, USA

San Antonio, TX, USA

Kirkland, WA, USAMontreal, QC, CanadaLincoln, NE, USA

Auch, France

Basel, Switzerland /St. Louis, MS, USA

Moscow, RussiaWaco, TX, USA

Hamburg, Germany

Georgetown, DE, USA

Cedex, FranceZurich, Switzerland

Paya Lebar, SingaporeDallas, TX, USAXiamen, P.R. China

Boeing and AirbusBoeing BBJ and 787Boeing 747/777/787, Airbus A330/340/380Boeing BBJ, 737/757/777/787, Airbus 340 and Embraer 135Boeing BBJ, 737CL, 737NG, Airbus ACJ Family and GulfstreamBoeing BBJ and Airbus ACJ FamilyFalcon, Gulfstream, Global, Challenger, Hawker, Learjet, Citation, EmbraerBoeing BBJ, 767, 787 and Airbus ACJ, A330, A340Boeing BBJBombardier Global & ChallengerLearjet, Citation, Hawker, Beechjet, Diamond, FalconBoeing BBJ (B737 series) and Airbus ACJ (A320 series)Boeing BBJ, 757/767/787/747, Airbus 318/319/320/321 /330/340/350/380, Bombardier, Gulfstream, Falcon, HawkerTu-134, TU-154B, M, YAK-40,YAK-42Boeing 707/737/747/757, Airbus A310/340, GulfstreamAirbus ACJ Family, Boeing 737CL/NG,747,767,777,787Boeing BBJ, 727, Lineage 1000 and Bombardier CRJ200Airbus, Boeing, Bombardier, and EmbraerAirbus A320, A330, A340, A380, Boeing 737NGBoeing BBJ and Airbus ACJBoeing BBJ and Airbus ACJBoeing BBJ and Airbus ACJ

56 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

AVIATION FINANCE SERVICE PROVIDERS IN GREATER CHINA

NAME

GE Capital

CIT

BNP Paribas

UBS

Citi Bank

Bank of America

Credit Suisse

Goldman Sachs

Minsheng Bank

Industrial and Commercial Bank (ICBC)

Bank of China (BOC Aviation)

Industrial Bank

China Construction Bank

China Development Bank

China Merchants Bank

Bank of Communication

Agriculture Bank of China

Changjiang Leasing

Dragon Aviation Leasing

AVIC Leasing

Shanghai Guojin Leasing

Tianjin Bangyin Leasing

China Aircraft Leasing

China Huarong Financial Leasing

China Trust

CITIC Bank

Chailease Finance

OFFICE LOCATION

International

International

International

International

International

International

International

International

China

China

China

China

China

China

China

China

China

China

China

China

China

China

China

China

Taiwan

Taiwan

Taiwan

FINANCE LEASE

••••••••••

•••••••

••••••••

OPERATING LEASE

•••

•

••••

••

•

Greater China Fleet Growth 2007-2014*

2007

6491

114143

203

307

371

445

2008 2009 2010 2011 2012 2013 2014 EST

* Fleet size for year-end 2012 is based on ASG revised numbers.

The Greater China business jet industry has been growing steadily over the past several years with 2013 achieving a 21% growth rate in terms of the number of business jets added to its installed fleet. This growth rate is significantly higher than the global business jet industry growth rate of under 5%.

Of note, 47% of aircraft delivered into Greater China during 2013 were pre-owned aircraft. This number is significantly higher than in recent years and is a sign of a maturing market plus demonstrates the growing acceptance and understanding of the value of pre-owned aircraft. Driving this pre-owned growth are concerns such as new aircraft delivery lead times, pricing and taxation.

Asian Sky Group expects 2014 to show comparable growth to previous years with expectations that the Greater China business aviation market will grow by 20% and reach around 445 aircraft by the end of 2014. This projection is based on orders placed in previous years and expected deliveries.

Hanging over the market in 2014 however, which may significantly impact the number of orders booked and therefore future deliveries, are the taxes and austerity measures put in place by the Central Government in Beijing. These measures will have a direct effect on buying sentiments. Additionally, the tax measures which introduce a more clearly defined tax structure for when business jets are imported into Mainland China, will result in more owners opting for countries of registration other than Mainland China. Given space constraints in Hong Kong and Macau, more buyers may opt for a Taiwanese registration which will still allow direct private flights between Taiwan and Mainland China.

500

450

400

350

300

250

200

150

100

50

0

2013 AND MARKET TRENDS

57The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

58 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Aircraft Additions in 2013

New and Pre-Owned Aircraft Additions 2013

G450G550

F7XCL605CL850G6000G5000

L650ACJ319CL604

SovereignG200

BBJGXRSL600

F900LXL1000

ACJ318CRJ200VIP

GEXG100

Cit XLSCit VICit X

H4000CL300G650

F2000P300

Cit CJ1

135 7

114

3

41 3

2

1

1

1

1

111111111

111

1

2

2

22

22

3

3

351

1

6

PRE-OWNED, 50 (47%)

NEW, 56 (53%)

106 in Total

106 in Total

Additions are defined as an operator or owner receiving an aircraft. Deductions being an operator losing an aircraft.*

New Pre-Owned

11

59The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Aircraft Additions and Deductions in 2013

Additions

Aircraft Deductions 2013 by Type

Deductions

Net Additions

-40 -20 0 20 40 60 80 100 120-60

-42

106

64

G450

G200

GIV/SP

Cit XLS

Cit Sovereign

CL605

GL EX

GL XRS

G6000

CRJ200VIP

F2000

H750

H800/850

H900/XP

H4000

L1000

ACJ318

-6

-4

-1

-1

-1

-1

-3

-4

-2

-2

-1

-1

-1

-5

-4

-3

-2

42 in Total

64 Net Additions

Net Fleet Growth by OEM 2012-2013

Market Share Change by OEM 2012-2013

Gulfstream, Bombardier and Airbus maintained their market shares during 2013. Embraer and Dassault saw a significant rise in relative numbers, while Hawker continued to see a decrease in their market share. The Embraer fleet added 8 aircraft, doubling its Greater China fleet.

Gulfstream

Gulfstream

117

38% 38%

30% 30%

6%8% 8% 7% 9%

5%3%

4% 5% 5%

1% 2%

142

21%

92111

21%19

31

63%

26 2719

816

100%

14 184 7

75%

100%

80%

60%

40%

20%

0%

150

100

50

0

2012

2012

2013 Growth

2013

40%

35%

30%

25%

20%

15%

10%

5%

0%

29%27

4%-30%

Bombardier

Bombardier

Dassault

Dassault

Cessna

Cessna

Hawker

Hawker

Embraer

Embraer

Airbus

Airbus

Boeing

Boeing

64 in Total

60 The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

Net Fleet Growth by Size Category 2012-2013

Market Share Change by Size Category 2012-2013

CORPORATE A/L

CORPORATE A/L

100%

80%

60%

40%

20%

0%

40%

35%

30%

25%

20%

15%

10%

5%

0%

ULTRA LR

ULTRA LR

S-LARGE

S-LARGE

LARGE

LARGE

S-MID

S-MID

MID

MID

S-LITE

S-LITE

LITE

LITE

20 28

40%

82

109

33%

5270

35%

6177

26%34 35

3%-20% -7%

27 2214 11 17 19

12%

7% 8%

27%29%

17%19% 20% 21%

11%9% 9%

6%5%

3%6% 5%

64 in Total

2013 Growth

150

100

50

0

2012

2012 2013

61The GREATER CHINA BUSINESS JET FLEET REPORT – YEAR END 2013

ASIAN SKY GROUP Suite 3905, Far East Finance Centre, 16 Harcourt RoadAdmiralty, Hong Kong

Telephone +852 2235 9222Facsimile +852 2528 2766

www.asianskygroup.com

The information contained in this report is provided free of charge for reference only. While such information was compiled using the best available data as of December 2013, ASG makes no warranties, either expressed or implied, concerning the accuracy, completeness, reliability, or suitability of such information. ASG is not responsible for, and expressly disclaims any and all liability for damages of any kind, either direct or indirect, arising out of use, reference to, or reliance on any information contained within this report.

STRATEGIC PARTNER

Related Documents