1 The Clorox Company Back to School Conference September 04, 2008 Don Knauss Chairman and Chief Executive Officer 2 Safe Harbor Statement Except for historical information, matters discussed in the attached document, including statements about the success of the company’s strategy and acquisitions as well as future volume, sales and earnings growth, profitability, costs, cost savings, innovation or expectations, are forward-looking statements based on management’s estimates, assumptions and projections. Important factors that could cause results to differ materially from management’s expectations are described in the company’s most recent Form 10-K filed with the SEC, as updated from time to time in the company’s SEC filings. Those factors include, but are not limited to, the company’s costs, including volatility and increases in commodity costs; increases in energy costs; general economic and marketplace conditions and events, including consumer spending levels, the rate of economic growth, and the rate of inflation; the ability of the company to implement and generate expected savings from its programs to reduce costs; consumer and customer reaction to price increases; the success of the company’s previously announced Centennial Strategy; the Company’s actual cost performance and the success of new products. The company may also use non-GAAP financial measures, which could differ from reported results using Generally Accepted Accounting Principles (GAAP). The most directly comparable GAAP financial measures and reconciliation to non-GAAP financial measures are set forth in the Company’s SEC filings including its Form 10-K and its exhibits furnished to the SEC, which is posted at www.TheCloroxCompany.com in the Investors/Financial Information/SEC Filings section.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The Clorox Company

Back to School ConferenceSeptember 04, 2008

Don KnaussChairman and Chief Executive Officer

2

Safe Harbor Statement

Except for historical information, matters discussed in the attached document, including statements about the success of the company’s strategy and acquisitions as well as future volume, sales and earnings growth, profitability, costs, cost savings, innovation or expectations, are forward-looking statements based on management’s estimates, assumptions and projections. Important factors that could cause results to differ materially from management’s expectations are described in the company’s most recent Form 10-K filed with the SEC, as updated from time to time in the company’s SEC filings. Those factors include, but are not limited to, the company’s costs, including volatility and increases in commodity costs; increases in energy costs; general economic and marketplace conditions and events, including consumer spending levels, the rate of economic growth, and the rate of inflation; the ability of the company to implement and generate expected savings from its programs to reduce costs; consumer and customer reaction to price increases; the success of the company’s previously announced Centennial Strategy; the Company’s actual cost performance and the success of new products.

The company may also use non-GAAP financial measures, which could differ from reported results using Generally Accepted Accounting Principles (GAAP). The most directly comparable GAAP financial measures and reconciliation to non-GAAP financial measures are set forth in the Company’s SEC filings including its Form 10-K and its exhibits furnished to the SEC, which is posted at www.TheCloroxCompany.com in the Investors/Financial Information/SEC Filings section.

2

3

Agenda

Business Review

Centennial Strategy

The Clorox Advantage

Business Review

3

5

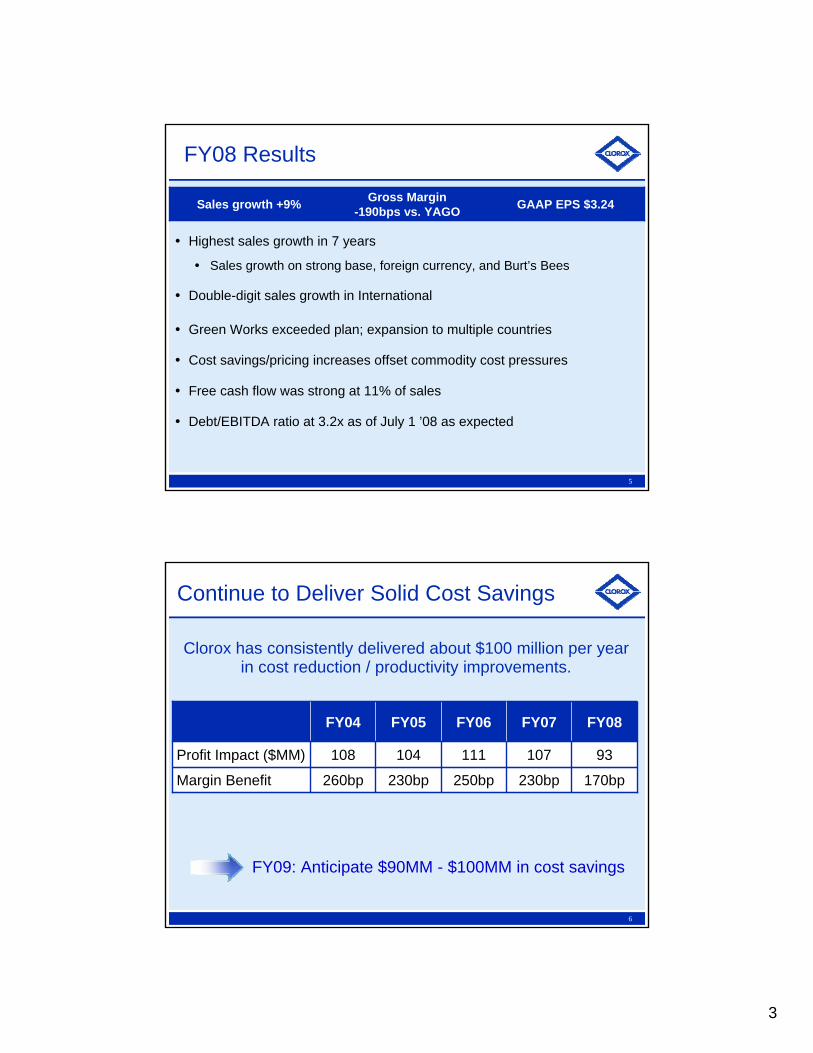

FY08 Results

Highest sales growth in 7 years

Sales growth on strong base, foreign currency, and Burt’s Bees

Double-digit sales growth in International

Green Works exceeded plan; expansion to multiple countries

Cost savings/pricing increases offset commodity cost pressures

Free cash flow was strong at 11% of sales

Debt/EBITDA ratio at 3.2x as of July 1 ’08 as expected

GAAP EPS $3.24Gross Margin-190bps vs. YAGOSales growth +9%

6

Continue to Deliver Solid Cost Savings

Clorox has consistently delivered about $100 million per year in cost reduction / productivity improvements.

170bp

93

FY08

230bp

107

FY07

111104108Profit Impact ($MM)

260bp

FY04

250bp

FY06

230bp

FY05

Margin Benefit

FY09: Anticipate $90MM - $100MM in cost savings

4

7

Solid Performance Year-over-YearAccelerating top line and strong free cash flow

11%12%11%(3)14%18%Free Cash Flowas a % of sales

+9%

10%(2)

4%

FY07

+8%(2)10%(2)26%10%EPS growth

5%

FY04

6%

FY06

5%

FY05

9%Sales growth (1)

FY08

-5%(4)EP growth

(1) Reconciliation between sales as-reported and sales excluding divestitures is shown on a later slide.(2) Compares FY06 EPS of $3.05 (excl. $0.11 stock option accounting costs and $0.05 CEO transition costs) plus $0.12 of FAS123-R expense vs. FY05 EPS of $2.88.

Compares FY07 EPS of $3.23 plus $0.02 of incremental FAS123-R expense and $0.09 of ITSM costs vs. FY06 EPS of $3.05 (excl. $0.11 stock option accounting costs and $0.05 CEO transition costs). Compares FY08 EPS of $3.59 (excl. $0.26 restructuring-related charges and $0.09 Burt’s Bees dilution) to FY07 EPS of $3.33

(3) Excludes $150mm IRS settlement in July, 2005.(4) Includes impact from Burt’s Bees acquisition; excluding Burt’s Bees EP growth is +6%

8

FY09 Outlook

Key ConsiderationsExcluding Burt’s Bees, sales growth: +4-6%Volume expected to be about flat for the yearGross margin: Down in 1st half and up in 2nd half

Commodity cost increases of $180-200 millionAnticipate cost savings of $90-100 millionPricing to recover at least 75% of commodity cost increases

GAAP EPS (1)

$3.60-3.75Gross MarginFlat vs. YAGO

Sales growth +6-8%

(1) Current Outlook as of Aug 1, 2008

5

9

Centennial Strategy

We make everyday life better, everyday

Maximize economic profit across categories, customers and countries

Be best at building big-share brands in economically-attractive midsized categories

Double-Digit annual

Economic Profit growth

MISSION

OBJECTIVES

GOAL STRATEGIES

Be a high-performance organization of enthusiastic owners

Win with superior capabilities in Desire, Decide and Delight

Accelerate growth both in and beyond the core

Relentlessly drive out waste

• 3-5% annual Sales Growth

• EBIT +50bp to +75bp annually

10

Delivering on our Centennial Strategy

Innovation with an integrated 3D approach is driving growth behind key consumer trends

Health and Wellness

Sustainability

Convenience

Multicultural marketplace

6

11

Solid Innovation Track Record

(1) Reconciliation between sales as-reported and sales excluding divestitures is shown in the appendix of this presentation.

+2.0% from InnovationAnnual Goal

FY08FY07FY06FY05FY04

9%4%6%5%5%Total Clorox Sales(1)

(excluding divestitures)

2.8%2.3%2.4%3.4%2.6%Growth from Innovation

12

Innovating Behind Key Consumer Trends

Convenience

Health & Wellness

Multicultural

Sustainability

7

13

DelightDesire Decide

Communication

• “Tailgating at Home”

• ESPN Sponsorship

R&D

• Preferred taste to gas

• Burns longer

In-Store

Strong retail activation across

channels

Integrated 3Ds

Insight: Health & Wellness - Meals at home create a healthier environment

Strategy: Inspire and enable shoppers to prepare and enjoy more quality meals at home with family

14

Decide: Strong Retail Activation

8

15

Delivering on our Centennial Strategy

Innovation with an integrated 3D approach is driving growth behind key consumer trends

Resources focused on higher growth and higher margin businesses

16

Burt’s Bees Success

Since transaction closed:

Sales +30% vs. YAGO; added +2pts of growth

Record high market share of 27%(1), +5.5points

Successful launch in 500+ Wal-Mart stores

Launched into Australia

(1) NPC category 54 weeks ending 5/3/08

9

The Clorox Company 17

Decide:Best in Class

display drives

conversion

18

Innovation continues to Delight

10

19

20

Consumption FDKT +16% (1)

FY08 Sales +>20%

Record year!

Brita Results

(1) Category Dollar Sales (FDKT) – 52weeks ending 6/29/08

11

21

Leveraging Sustainability across 3Ds

22

International is High Growth Engine

(1) Reconciliation between sales as-reported and sales excluding divestitures is shown in the appendix of this presentation.

FY08FY07FY06FY05FY04

9%4%6%5%5%Total Clorox (1)

12%

3%

16%9%14%11%Clorox International

4% 5%5% 8%Clorox North America

12

23

Grow International Share of Total Sales

FY04 - % of Total Sales

Domestic 84%

International 13%

Canada 3%

Domestic 79%

International 16%

Canada 5%

Goal: Increase International to at least 20% of total sales by 2013

FY08 - % of Total Sales

24

Delivering on our Centennial Strategy

Innovation with an integrated 3D approach is driving growth behind key consumer trends

Resources focused on higher growth and higher margin businesses

Delivering improved Store Level Results (AMPS) including grocery

13

25

X = Formally designated Captain (lead advisor); lead manufacturer in drawing POG and finalizing assortmentTL = Thought Leader where no formal Captain exists; Strongest TL role amongst manufacturers

Source: IRI, Customer Purchase Data

Earned 19 new Retail Advisory roles this year17 in the Grocery Channel

Category Advisory Services Role: Gained 7 in top 7 customers

Superior Service Drives Leadership

NEWNEWXNEWXNEWSuper Valu

XXXNEWXNEWSafeway

TLTLTLTLTLTLTLTLTLTLKroger

XTLXXXXXFamily Dollar

XXXXXXXDollar General

XTLXXXXXTarget

XXXXNEWXXWal-Mart

AutoBBQ &

MarinadesSalad

DressingChar-coalLaundryLitterBritaGlad

Trash

Glad Food Bags/ Wraps

Home-Care

26

+1%

FY05 FY06 FY07 FY08

Grocery Sales Results FY085 point turnaround since FY05!

0% +5 ptsor

~$65MM in sales

14

27

The Clorox Advantage

Strong brands consumers trust

Focus on consumer value equation

Strong brand support to drive 3Ds

Realistic assumptions for managing input costs

28

Focus on Consumer Value Equation

Value is key – pricing only a componentInnovationDecisive product winsPrice relative to competition

In most recent quarter ended, saw share growth in 4 of 8 categories in tracked channels(1)

(1) Based on IRI Custom Scanner data for P13 ended 6/29/08

Building Consumer Lifetime Loyalty

15

29

Strong Brand Support to Drive 3Ds

• Investment in target range 9% - 10% of sales

• Spend differentially by business and by brand

• Improved TV advertising ROI 20% since FY05

• Continued strong investment in trade support

• R&D investment supports decisive product wins

Building Consumer Lifetime Loyalty

30

Managing Input Costs

Pricing & Mix

Cost Savings

Buying powerGlobal sourcing

Supplier diversification

Hedging where available

Innovation and TechnologyExpand/qualify different grades of resin

Materials innovation

Control administrative spending

16

31

Resin Fact Base

Polyethylene: Key market price drivers

Supply/Demand and feedstock costs

Global capacity expansion 2007 to 2012: ~+35%(1)

New Middle East capacity: late 2H CY2008

Export demand remains high…But is slowing with strengthening USD

Domestic demand down ~7.5% vs. YAGO

(1) Global polyolefins capacity expansion per CMAI, April 2008

32

Returning Cash to Shareholders

(1) FY06 FCF excludes $150mm IRS settlement in July, 2005.(2) Share repurchases calculated net of cash received from option exercises. FY05 share repurchases used in calculation includes the impact of the Henkel

transaction.

Over the last 6 years, Clorox has returned 136% of free cash flow to shareholders through share repurchases and dividends.

39%

562

FY07 FY08FY06FY05FY04FY03($MM)

189%47%389%46%106%% Returned to Shareholders: Share Repurchases, Dividends (2)

560492614729600Free Cash Flow (1)

17

33

Focused on Driving Shareholder Value

Cash flow remains strong

Use cash to pay down debt near term, leverage flexibility longer-term for growth

Support dividend growth

Disciplined capital spending

EP is lens for resource allocation

34

Key Messages

Delivered solid performance in FY08 –accelerated top line growth while managing well through difficult cost environment.

Centennial strategy is working

Clorox continues to be advantaged

Focused on driving shareholder value

18

Appendix

36

Index to Appendix

87-88CCEM………………………………...

56 (US), 65 (International)Big Share Brands………..……..……

80-85Burt’s Bees…………………………..

61-65International………………………….

50-51Gross Margin Mapping….…............

49Restructuring……………………..….

46-48FY09 Outlook………….……..…......

43-45FY08 Reconciliations…………….…PageTopic

723Ds – Grocery……………….……...

55Sales Pie Chart…………….....…..…

52-53Commodities…………..………..….

89-90Pricing………………………………...

76-78Green Works………….……………..

19

FY08 Resultsand FY09 Outlook

38

FY08 Sales Reconciliation

FY08 FY07Base business sales growth 4.7% 3.5%

Foreign Exchange 1.2% 0.2%Private label business exit -0.1% 0

Sales growth before acquisitions 5.8% 3.7%

Burt's Bees 2.1% 0Bleach Acquisiton 0.9% 0.7%

Total Sales Growth 8.8% 4.4%

20

39

FY08 Gross Margin Reconciliation

FY07 Gross Margin 43.1% FY06 Gross Margin 42.2%

Commodities -2.7% Commodities -1.1%Logistics & Manufacturing -1.1% Logistics & Manufacturing -1.0%

Cost Savings 1.7% Cost Savings 2.3%Pricing 0.8% Pricing 1.5%Other 0.3% Other -0.8%

FY08 Gross Margin before one-time charges 42.1% FY07 Gross Margin 43.1%

Burt's Bees Inventory Step-up -0.4% 0%Restructuring-related charges -0.5% 0%

FY08 Gross Margin 41.2% FY07 Gross Margin 43.1%

Change vs. Prior Year -190bp Change vs. Prior Year 90bp

Change vs. Prior Year ex-charges -100bp

40

FY08 Diluted EPS Reconciliation

FY08 FY07Base EPS $3.59 $3.33

Restructuring-related Charges (0.26) -Burt's Bees (0.09) -

IT Services Transition charges and asset impairment - (0.10)Discontinued Ops - 0.03GAAP EPS $3.24 $3.26

21

41

FY09 Outlook

Key ConsiderationsExcluding Burt’s Bees acquisition, sales growth: +4-6%

Includes 2pts from innovation which includes Green Works1st half sales growth stronger than 2nd half due to Burt’s Bees

Announced pricing to recover ~75% of commodity cost increasesVolume expected to be about flat for the year

1st half volume up modestly (Burt’s less pricing impact), 2nd half about flat

Gross margin expected to be down in 1st half and up in 2nd halfCost Savings: $90 to $100 millionCommodities: $180 to $200 million unfavorableRestructuring: Manufacturing network consolidation continuing into FY09, charges of $14-$17 million in COGS vs. FY08 charge of $23 millionBurt’s Bees Inventory Step-Up not repeating: +$19 million benefit to GM

FY09 Outlook

GAAP EPS (1)

$3.60-3.75Gross MarginFlat vs. YAGO

Sales growth +6-8%

(1) Current Outlook as of Aug 1, 2008

42

FY09 Sales Outlook

Base Sales growth before acquisitions(1) 4% 6%

Burt's Bees 2% 2%

Total Sales Growth 6% 8%

Outlook Range

(1) Base sales includes +2% from innovation and also captures impact of pricing, existing private label business and foreign exchange.

22

43

FY09 Diluted EPS Outlook

(1) Outlook is net of restructuring charges of $0.09-$0.11 ($20-25mm pretax) which are primarily related to the previously announced consolidation of the company's manufacturing network.

Initial Outlook (May 1, 2008) GAAP EPS(1) $3.75 $3.90

Greater Commodities / Other -0.15 -0.15

Current Outlook (Aug 1, 2008) GAAP EPS(1) $3.60 $3.75

Outlook Range

44

Restructuring-Related ChargesFY08 & FY09: Supply Chain Consolidation: U.S. Homecare & International

Annual savings of $22MM-$24MM when fully implemented Total capital investment of $52MM (~$29MM in FY08 and ~$23MM in FY09)

FY08:Other charges taken in light of Centennial StrategyExit private label food bags business

--($6 - $8)($36)Restructuring line

Announced Actions

--($20 - $25)($59)Pretax Profit

$22 - $24$18 - $19($14 - $17)($23)COGS

$MM FY11FY10FY09(2)FY08 Actual(1)

(1) FY08 includes ~$48MM in non-cash charges. (2) FY09 as of Aug 1, 2008

Anticipate $20MM - $30MM annually in charges as a normal course of business

23

45

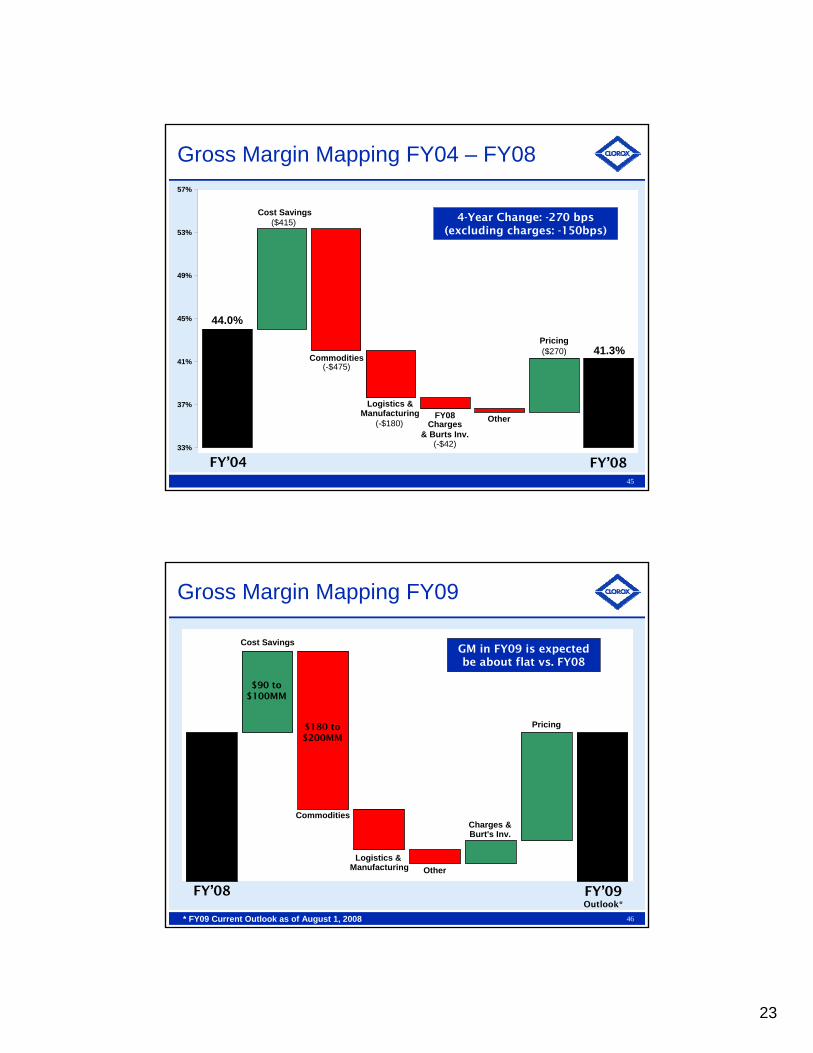

FY’08FY’04

41.3%

OtherFY08Charges

& Burts Inv.(-$42)

Logistics & Manufacturing

(-$180)

Commodities(-$475)

Cost Savings($415)

Pricing($270)

44.0%

33%

37%

41%

45%

49%

53%

57%

Gross Margin Mapping FY04 – FY08

4-Year Change: -270 bps(excluding charges: -150bps)

46

FY’09Outlook*

FY’08

Gross Margin Mapping FY09

* FY09 Current Outlook as of August 1, 2008

$180 to $200MM

$90 to $100MM

GM in FY09 is expected be about flat vs. FY08

Charges &Burt's Inv.

OtherLogistics &

Manufacturing

Commodities

Cost Savings

Pricing

24

47

*FY05

ActualFY06

ActualFY07

ActualFY08

ActualFY09

Outlook

$170

$106

$62

$137

$180 - $200

Commodity Cost Trends FY05 to FY09

* FY09 Current Outlook as of August 1, 2008

Cumulative cost increase FY05 – FY08 = $475million

48

Unfavorablewith 1H > 2H+10%~60%Net impact - Raw Materials & Packaging

~40%Manufacturing, logistics & warehousing

Impact to COGS(% Change vs. YAGO)

% of COGS

About Flat

+19%

+51%

+17%

FY08 FY09 OutlookAug 1, 2008

~30%Other raw materials & packaging (1)

+25% to +30%3-4%Starch, Solvent, Clay

+40% to +50%1-2%Soybean Oil, Corn Syrup, Buttermilk, Egg

+15% to +20%20-25%Resin, Linerboard, Chlor-Alkali

+4% to +6%2-3%Pine Oil, Substrate, Silicone

100%Total COGS

Total raw materials and packaging represents about 60% of COGS

Continued upward pressure from volatile commodity costs

Commodities PressureAnticipate $180-200 million in FY09 on top of ~$135 million in FY08

(1) Includes other commodity items as well as other materials such as triggers, purchased bottles, and labels

25

Clorox Background

50

Total FY08 Sales of $5.3 Billion

* FY08 includes 7 months of sales of Burt’s Bees. **Sales of Professional Products Division allocated to each business unit

International (16%)

Canada (5%)

Burt's Bees (2%)*

Dressings & Sauces (8%)

Charcoal (9%)

Cat Litter (7%)

Glad (16%)

Auto (4%)

Brita (4%)

Laundry (12%)

Home Care (17%)

26

51

Source: IRI Custom Scanner Data; 52 weeks ended 6/29/08

Big-Share Brands – North America

31%#1Clorox Toilet Bowl

37%#2Liquid-Plumr

11%#2Clorox Clean-up Spray

29%#1Pine-Sol

Leadership Brands – Home Care

20%#1Tilex / Clorox (Bath)

48%#1Clorox Wipes

50%#1Armor All

66%#1Clorox Bleach

39%#1STP Oil / Fuel Additives

22%#1Glad

Other Leadership Brands

14%#2Hidden Valley dressings

29%#2Fresh Step / Scoop Away

34%#1Clorox 2 for Colors

68%#1Brita

77%#1Kingsford / Matchlight

52

Total U.S. Market Share (1)

(1) Selected publicly-traded US consumer companies

Source: IRI Syndicated Scanner Data; 52 weeks ended 6/15/08

P&G

Clorox

Unilever

Colgate

Reckitt

Church & Dwight

0% 5% 10% 15% 20% 25% 30%

We Know How to Win with Consumers

27

53

Top 122007 PoweRanking® Composite - Manufacturers

North America $ Sales (B)

North America $ Sales (B)

We Know How to Win with Customers

CompositeRanking

CompositeRanking

45

3639

16

12

CompetitorsCompetitors

27

52.8%

35.0%

28.8%

21.8%

14.3%11.0% 9.7% 9.4% 9.2%

5.8% 5.7% 5.5%

$4.0$6.1$12.0$7.0$9.9$7.3$34.7$17.3$10.3$25.7$23.1$34.4

54

Total Shareholder Return – 10 years

-40%

0%

40%

80%

120%

Jun'98

Jun'99

Jun'00

Jun'01

Jun'02

Jun'03

Jun'04

Jun'05

Jun'06

Jun'07

Jun'08

TOTAL SHAREHOLDER RETURNS

CLOROX

PEERS

S&P 500

First BrandsAcquisition +34%

+103%

+33%

Assumes reinvestment of dividends TEN YEARS

28

International

56

International Strategy

Track record of profitable growthSales CAGR ’03 – ’08: 12%Operating profit CAGR ’03 – ’08: 11%

We will use EP to drive country and category choices and resource allocation• Maximize growth in the Americas and Australia / NZ first• Broaden the footprint of brands and countries: opportunity in

mid-sized countries where multi-nationals do not or are less focused

• Increase International to at least 20% of company sales by 2013

We will gain share by winning in Desire, Decide and Delight

29

57

Mexico

Australia

Puerto Rico

Argentina

S. Korea

Chile

Key:

Tier II 14 %

Tier I 80 %

Venezuela

Peru

Colombia

Costa Rica/Panama

New Zealand

Hong Kong

S. Africa

Philippines

Tier III 6 %

China ( south)

11

Ecuador

Uruguay

Dominican Rep.

Where we play outside of U.S.

58

Where we play - International

FY08 ActualNet Customer Sales by Region

Latin America

67%

EME8%

Asia5%

ANZA20%

Bleach & Laundry35%

Other6%

Auto9%

Bags & Wraps17%

Home Cleaning

33%

FY08 ActualNet Customer Sales by Category

30

59

• Bleach and Home Cleaning primarily in Latin America

• Bags & Wraps and Auto Care primarily in Australia and New Zealand

• 90% of sales in four core categories

• 80% of sales are in Tier 1 countries

Bleach

Core Categories - International

Home Cleaning

Bags & Wraps Auto Care

60

Big-Share Brands - International

Handy Andy – New Zealand #1 53%

Poett - Chile #1 46%

Poett - Perú #1 43%

Mistolin – Venezuela #1 27%

Mistolin – Panama #1 26%

Handy Andy – Australia #1 25%

Poett – Argentina #2 26%

Poett – Costa Rica #2 24%

Mistolin – Puerto Rico #2 21%

Leadership Brands – Home CareAjax - Ecuador #1 92%

Clorox - Puerto Rico #1 92%

Clorox - Saudi Arabia #1 85%

Ayudin- Argentina #1 74%

Clorox – Panama #1 74%

Los Conejos – C.Rica #1 65%

Ajax- Dominican Rep #1 60%

Clorox – Peru #1 53%

Agua Jane – Uruguay #1 50%

Clorinda - Chile #1 42%

Clorox - Hong Kong #1 40%

Clorox - Egypt #1 35%

Nevex – Venezuela #1 32%

Clorox - Chile #2 38%

Clorox - Colombia #2 24%

Clorox - Mexico #2 17%

Leadership Brands – Bleach

Armor All - Australia #1 68%

GLAD- Hong Kong #1 61%

GLAD New Zealand #1 47%

GLAD - Australia #1 32%

Armor All – Mexico #2 23%

Other Leadership Brands

Source: Nielsen, IRI, Howarth, or Aztec (depending on country) 13 weeks ending 5/31/08

31

Centennial Strategy

62

Where to Play

Be the Best at Building Big-Share Brands in Economically-Attractive, Mid-Sized Categories

Best

Big-Share Brands

Economically Attractive

Mid-SizedCategories

Big-company capabilities across the 3Ds

#1 or strong #2 share

- The market has good profit and it is growing- Our superior capabilities in the 3Ds create a clear right to win

- Large enough to be material to the company- Small enough to avoid large-scale players

32

63

Annual Financial Goals

Annual Goals

+50bp to +75bpEBIT Margin2.

3% - 5%Organic Sales Growth1.

Incremental or Adjustments to Goals:M&A activity and any new geographies would be incrementalImpact of any portfolio reshaping would be adjustments to targets

64

Targeted Capital Structure

Over time - Operate at higher leverage levelsRange 2.5x to 3.0x Debt/EBITDA

Interim - Return cash to shareholders if not needed for the business

Share repurchasesCompleted ASR Q1 FY08 (Aug. 2007)

Dividend increase: +15% May 08 on top of +29% May 07Payout ratio: 57%(1)

Yield: 3.2%(2)

(1) Based on FY08 Diluted EPS of $3.24 (continuing operations).(2) Based on stock price as of close Aug 27, 2008 ($58.42)

33

65

Key Credit Metrics

FY FY FY CY FYCredit Statistics 2005 2006 2007 2007 2008Total Debt $2,483 $2,274 $2,036 $3,763 $3,476EBITDA $998 $967 $1,049 $1,062 $1,067Total Debt / EBITDA 2.49x 2.4x 1.9x 3.5x 3.3x*

Book Equity ($552) ($156) $170 ($554) ($349)Debt % of Book Capitalization 129% 107% 92% 117% 111%

EBITDA Interest Coverage** 12.6x 7.6x 9.3x 7.9x 6.3xEBIT / Interest** 10.2x 6.2x 7.6x 6.5x 5.1x

Free Cash Flow / Debt** 25% 15% 28% 15% 16%FCF after Dividends / Debt** 17% 7% 19% 9% 10%

Free Cash Flow as % of sales 14% 7% 12% 11% 11%FCF after Dividends as % of sales 9% 4% 8% 7% 6%

Credit Ratings (S&P/Moodys) A- / A3 A- / A3 A- / A3 BBB+ / Baa2 BBB+/Baa2CP Ratings (S&P/Moodys) A-2 / P-2 A-2 / P-2 A-2 / P-2 A-2 / P-2 A-2/P-2* At July 1, 2008, Debt/EBITDA ratio was 3.2x** ttm

66

Be a high-performance organization of enthusiastic owners

Win with superior capabilities in Desire, Decide and Delight

Accelerate growth both in and beyond the core

Relentlessly drive out waste

Centennial Strategy

We make everyday life better, everyday

Maximize economic profit across categories, customers and countries

Be best at building big-share brands in economically-attractive midsized categories

Double-Digit annual

Economic Profit growth

MISSION

OBJECTIVES

GOAL STRATEGIES

Win with superior capabilities in Desire, Decide and Delight• Consistently make decisive product wins the basis for competition by

delivering consumer-preferred ideas, designs and technology.

• Drive growth in grocery by selectively investing against five service capabilities with the top 25 customers.

• Deliver integrated consumer communications around a core idea for each brand that is relevant to our targets, both in and out of the store

• 3-5% annual Sales Growth

• EBIT +50bp to +75bp annually

34

67

Driving Profitable Growth in Grocery

Expand our 5 Value-Creating Services to a broader customer base

Consumer & Shopper InsightsCategory Advisory ServicesRetail Consumer MarketingSupply ChainRetail Coverage

Increase investment in PeopleCross-functional Customer Business Centers

Approximately 30 FTEs

68

2007 PoweRanking®:Clorox Top 10 Customer Team

Clorox PoweRanking® ResultsClorox PoweRanking® Results

Strategic PartnersStrategic Partners All Other RetailersAll Other Retailers

309Most important consumer brands

208Most helpful consumer information/ best category management

156Most innovative marketing approach

108Best shopper marketing programs

104Best sales force/customer teams

136Company Strategy

115Best supply chain management

558Best combination growth & profitability

146Overall compositeRankRank

35

69

Decisive Product Wins Drive Growth

YesNoAchieved Statistical Win Against Best

Competition

5%5%No

80%Recent Examples:Carbon LitterForceFlex TrashKingsford Surefire Charcoal

10%Yes

% of FY07 Sales from Product InnovationSu

cces

s

60/40 Wins create 10x NPVIncrease products with 60/40 win: 30% of sales today to 50% by 2013

70

Be a high-performance organization of enthusiastic owners

Win with superior capabilities in Desire, Decide and Delight

Accelerate growth both in and beyond the core

Relentlessly drive out waste

Centennial Strategy

We make everyday life better, everyday

Maximize economic profit across categories, customers and countries

Be best at building big-share brands in economically-attractive midsized categories

Double-Digit annual

Economic Profit growth

MISSION

OBJECTIVES

GOAL STRATEGIES

Accelerate growth both in and beyond the core• More aggressively extend our brands into new categories and

channels with emphasis on professional products opportunities.• Accelerate growth in the Americas and Australia/New Zealand first,

and explore new geographies second.• Capitalize on trends of health & wellness, convenience, sustainability

and ethnicity.• Leverage financial strength and develop capabilities to grow beyond

the core.

• 3-5% annual Sales Growth

• EBIT +50bp to +75bp annually

36

71

• Exceeding initial plan and garnered ~50% share of natural cleaning segment (1)

• Launched 1st extension – liquid dish wash detergent

• Customer reaction and interest across channels continues to be enthusiastic– 2008 Wal-Mart Sustainability Innovation Award– 2008 GMA Award for Innovation and Creativity

• Established alliance with Sierra Club – product labels feature Sierra Club logo

Leading the way with Green Works

(1) FDKT 13 weeks ending 6/29/08

72Launched January 2008!

37

73

Introducing Dish DetergentLaunched August ‘08

Burt’s Bees AcquisitionExtending our Reach

38

75

Burt’s Bees Overview

A leading brand in the growing $6.4B Natural Personal Care (NPC) segment

Products across many Natural Personal Care categories including lip care, facial care and body care

Unique capability in developing and manufacturing products with natural ingredients

$170MM in 2007 (est.) net sales with roughly 90% in US and balance concentrated Canada, UK and Taiwan

Profitability metrics at the high-end of Personal Care

30%+ EBITDA Margin

385 employees. 1 manufacturing facility, 1 distribution center and headquarters in Raleigh-Durham, North Carolina

76

Other

Re vlon I nc

Co lomer U SA

Co mbe In c

Estee Lauder

John Fri eda

Wella Corp

Alberto-Culver Co

John Paul Mitchell

Clairol Inc

Unilever

Procter& Gamble

L'Oreal

Other

LVMH

AM C osm etics I nc

Neutr ogen a C orp

Chanel SAMary Kay Inc

Del Pharmaceuticals Inc

Avon Products Inc

CliniqueLaboratories Inc

Procter& Gamble

Revlon Inc

EsteeLauder

L'Oreal

Other

Private Label

Beiersdorf Inc

Kao Brands CoMary Kay Inc

Johnson & Johnson

Limited Brands Inc

UnileverNeutrogena Corp

CliniqueLaboratories Inc

Estee Lauder

AvonProducts Inc

Procter& Gamble

L'Oreal

Other

Na tur e's Gat e

Tom's of Maine

Burt's BeesHain- Celestial*

AvedaThe Body Shop

Other

Clinique Lab oratories Inc

Liz Claiborne Inc

LVMHCosmopoli tan Cosmetics

Chanel SACoty Inc

Elizabeth Arden Co

AvonProducts Inc

LimitedBrands Inc

LancasterGroup

EsteeLauder

L'Oreal

Other

Johnson& Johnson

Roche

Allergan

AvonProducts Inc

EsteeLauder

L'Oreal

Procter&

Gamble

OtherChurch &

Dwight Co Inc

PrivateLabel

Johnson& Johnson

GlaxoSmithKline

PfizerInc

Colgate-Palmol ive Co

Procter&

Gamble

Other

ClairolInc

L'Oreal

B eier sdor f I nc

R evlon I nc

Bic Corp

SC Jo hnson & So n Inc

Private LabelColgate-Palmolive Co

Combe Inc

Schick-WilkinsonSword

Unilever

Procter&

Gamble

Other

Jo hnson & Jo hnson

Avo n Pr oducts In c

Procter& Gamble

Colgate-Palmolive Co

DialLimitedBrands

Inc

Unilever

Other

K ao B ra nds C o

A von

P rodu cts I nc

RevlonInc

Church& DwightCo Inc

Col

gate-

Pal

mol

ive

Co

Uni lever

Procter&

Gamble

Oth er

Est eeLaud er

L'O real

Tann

ing

Resea

rch

Neu

tro

gena

Cor

pSu

n P

har

mac

eut

ical

s C

orp

Other

Pri

vate

Label

BicCorp

SC

Joh

nson

& S

on

Inc

Sch

ick-

Wil

kins

on Sw

ord

Oth

erRoc

he

Alle

rgan

Avo

n Pro

du

cts I

nc

Est

ee L

aud

erL'

Ore

alPr

octe

r & G

amble

Hair Care Cosmetics Skin Care NaturalPersonal

Care

Fragrances Cosme-ceuticals

OralCare

Men'sCare

Bath &Shower

Deod

ora

nts

Sunca

reD

epila

tori

es

Baby

care

$10.1B $8.1B $7.6B $6.4B $6.0B $5.7B $4.7B $4.6B $4.4B $2.2

B

$1.1

B$0.9

B$0.

8B

Total =$62.4B

0%

20%

40%

60%

80%

100%

Perc

ent

of T

ota

l

Share of Top 5 62% 65% 41% 17% 50% 49% 80% 64% 57%

90%

57%

74%

48%

U.S. Natural Personal Care Market Is Highly Fragmented & Lacks Entrenched Scale Players

U.S. Retail Personal Care Product Market, 2006

*Notes: Hain-Celestial includes Jason, Para, Zia, Alba and Avalon brands.Uses 2005 competitor share on total 2006 sales. Tom’s of Maine is owned by Colgate-Palmolive and The Body Shop is owned by L’Oreal.

Source: Euromonitor; Datamonitor; Nutrition Business Journal

39

77

Natural Personal Care Is Large and Rapidly Growing

Cosm

ece

utica

ls

Natu

ral

Per

sonal Care

Men

's C

are

Baby C

are

Sunca

re

Deo

dora

nts

Skin

Car

e

Del

ipato

ries

Hairca

re

Colo

r C

osm

etic

s

Fra

gra

nce

s

Ora

l Car

e

Bath

and S

how

er

11.0%

9.3%

5.9% 5.7%

4.3%

3.6%3.1%

1.7% 1.5% 1.5%

0.9%

-0.1%-0.5%

-3%

0%

3%

5%

8%

10%

13%

2003-2

006 C

AG

R

U.S. Personal Care Product Category Growth Rates, 2003-2006

Projected growth of natural personal careis 7.7% for 2006-2010

U.S. Personal Care market was $62B in 2006, with historical growth rates of 3.2% (2003-2006)Natural Personal Care (NPC) is large ($6.4B) and one of the fastest growing sub-categoriesNPC is also global – NPC growing double digit rates across Europe and Asia

Source: Euromonitor; Datamonitor; Nutrition Business Journal

78

Burt’s Bees Market Share by Category, Natural Food Channel Only

Source: SPINS as of 10/07

Burt’s Bees Has Leading Presence

Lip Care Foot Care Kits/Gifts Baby Care Other Skin Care

45.2%42.7%

39.6%

17.8%

10.2%

0%

10%

20%

30%

40%

50%

Burt

's B

ees

Mar

ket

Shar

e

Market Position No. 1 No. 1 No. 1 No. 2 No. 2

40

79

Lip

• Lip Balm

• Lip Shimmers

• Lip Gloss

Face

• Day Creams

• Night Creams

• Eye Creams

• Serums

• Cleaners

• Toners

• Scrubs

• Acne

Body

• Body Lotions

• Hand Creams

• Foot Creams

• Oils

• Moisturizing Mists

• Body Wash

• Soaps

• Scrubs

Hair

• Shampoos

• Conditioners

• Hair Treatment

Baby

• Powder

• Oil

• Lotions

• Ointments

• Bath

• Shampoo

• Soap

Outdoor & Natural

Remedies

• Ointments

• Insect Relief

• Sun Care

• Lip Balm

GiftsKits

Burt’s Bees Portfolio

80

DelightDesire Decide

Build a truly authentic brand with sustained

marketing support

Enhance product innovation and

expand into new segments

Expand distribution and

in-store presence

How We Will Grow The Business

International Component – Continue to grow in existing markets; look to enter new, high potential markets

41

81

Be a high-performance organization of enthusiastic owners

Win with superior capabilities in Desire, Decide and Delight

Accelerate growth both in and beyond the core

Relentlessly drive out waste

Centennial Strategy

We make everyday life better, everyday

Maximize economic profit across categories, customers and countries

Be best at building big-share brands in economically-attractive midsized categories

Double-Digit annual

Economic Profit growth

MISSION

OBJECTIVES

GOAL STRATEGIES

Relentlessly drive out waste• Continue to drive value through the CCEM program, with

significant focus on Buy, Make and Ship.• Minimize the cost of processes that are not a source of our

competitive advantage• Use environmental sustainability lens to accelerate cost

savings and reduce the Company's environmental footprint

• 3-5% annual Sales Growth

• EBIT +50bp to +75bp annually

82

Solid Track Record in Delivering Savings

Clorox has consistently delivered about $100 million per year in cost reduction / productivity improvements.

170bp

93

FY08

230bp

107

FY07

111104108Profit Impact ($MM)

260bp

FY04

250bp

FY06

230bp

FY05

Margin Benefit

Anticipate $80MM - $90MM ongoing annual savings

42

83

Cost Management Program (CCEM)is SustainableMajor Initiatives

World Class Manufacturing & Distribution

Network Optimization

Materials and Product Sourcing

Product Design Optimization

Trade Spending Efficiency

Productivity/Sourcing

84

Pricing

Clorox has aggressively taken pricing to offset rising inflationary and commodity cost increases.

150bp

77

FY07

55944520Profit Impact ($MM)

30bp

FY04

160bp

FY06

70bp

FY05 FY08

80bpMargin Benefit

Note: During FY08 and FY09, Clorox will have taken pricing on slightly more than 50 % of its portfolio. List of price increases by brand and date can be found at Clorox’s investor page at http://investors.thecloroxcompany.com

43

85

Example: Price Premium Trend

(1) Total US FDmx

Wtd Base Price Per Volume For Glad Base Kitchen Trash Bags AndPrivate Label Kitchen Trash Bags in Total U.S (Fdmx)

0.00

0.04

0.08

0.12

0.16

10/0

7/05

02/0

7/06

06/0

7/06

10/0

7/06

02/0

7/07

06/0

7/07

10/0

7/07

02/0

7/08

06/0

7/08

Wtd

Bas

e Pr

ice

Per V

olum

e

Clorox

Private Label

Kitchen Trash – Pricing per Volume (1)

Wtd Base Price Per Volume For Clorox Bleach AndPrivate Label Bleach In Total U.S. - Fdmx

0.00

0.01

0.01

0.02

0.02

0.0310

/07/

05

02/0

7/06

06/0

7/06

10/0

7/06

02/0

7/07

06/0

7/07

10/0

7/07

02/0

7/08

06/0

7/08W

tdB

ase

Pric

e Pe

r Vol

ume

Clorox

PrivateLabel

Liquid Bleach – Pricing per Volume (1)

In most categories

where we track

private label,

trend is base

price gap is flat or

declining

over last 3 years

Other

44

87

Private Label ShareUS total PL share has been relatively flat in recent years; with only a modest increase in recent monthsGrowth in private label is in Club (16% share of PL); plays to Clorox’s strength as Club typically carries private label and #1 brand.

US Private Label Share of CPG Spending: All Outlet

15.9%21.3%2007

21.1%21.1%20.6%20.5%Unit15.2%

2004

15.7%

2006

15.5%

2005 200852wks ending 3/30/YY (1)

16.4%Dollar

(1) IRI June 2008 and Mar 2008

Private Label Share in Clorox Categories: FDMx

14.3%

2007

13.2%

2004

14.2%

2006

13.7%

2005 200852wks ending 6/15/YY (1)

14.5%Dollar

Private Label share in Clorox categories has seen only modest growth.

88

Reconciliation:Sales excl. Divestitures & Acquisitions

($MM) FY02 FY03 FY04 FY05 FY06 FY07 FY08

Sales - as reported 3,859 3,986 4,162 4,388 4,644 4,847 5,273Sales growth 3% 4% 5% 6% 4% 9%

Less: Divested businesses 64 16 0 0 0 0 0Less: Acquisitions 0 0 0 0 0 31 146

Sales - excl. divestitures & acquisitions 3,795 3,970 4,162 4,388 4,644 4,816 5,127Sales growth 5% 5% 5% 6% 4% 6%

45

89

Environmental SustainabilityEnvironmental stewardship has always been a core value and focus of The Clorox Company

The Chlorine Institute in 2005 recognized The Clorox Company's U.S. bleach plants for "master" environmental achievement. Most recently, in 2007, the Institute recognized Clorox’s domestic plants with Chlorine Institute's Safety and Environmental Excellence Award for nine years without a reportable chlorine release (reportable release standard is very low, at only +10 lbs. of chlorine released).

In 2006, The Clorox Company created the position of Vice President – Sustainability & Innovation. This executive is responsible for leveraging Clorox’s environmental sustainability opportunities.

The Clorox Company recently increased its commitment to address it’s greenhouse gas (GHG) emissions. We are currently undertaking a comprehensive inventory of our energy usage and emissions at 35 of our manufacturing plants, warehouses and key offices in North America.

The Clorox Company is an active member of two Wal*Mart Sustainable Value Networks: Packaging and Chemical-Intensive Products.

In 2006, the West Virginia Department of Environmental Protection recognized our Kingsford plant in Parsons, West Virginia with an Environmental Excellence Award. We were the only company in West Virginia with more than 100 employees to receive this award.

90

Environmental SustainabilityPackaging

More than 90 percent of our product cartons (not corrugated cases) are now made from 100 percent recycled content (minimum 35 percent post-consumer content and the remainder reused scraps/waste).

Plastic resin in the 96oz Clorox® liquid bleach bottles was reduced by 10g in 2005, translating to about 3.8MM less lbs of HDPE resin used per year.

Clorox ® Liquid Bleach

The Clorox Company is recognized as having best practice chlorine handling practices by the U.S. EPA and Homeland Security government agencies. We share our patented chlorine rail car safety valve with other companies free of charge.

Glad® ProductsGlad® ForceFlex® technology provides a stronger trash bag that stretches while saving over 1 million pounds of plastic film per year.

The Glad business does not throw out any rejected product or scrap plastic. Almost all waste resin is either reclaimed or sent to a third party for recycling.

Bleach has saved more lives than any other substance made by man** Due to reduction in waterborne disease as reported by Dr. Abel Wolman, Former

President, American Public Health Association

46

91

Environmental SustainabilityKingsford® Charcoal

Kingsford® charcoal with Sure Fire Grooves®, introduced in FY 05, enabled a 10% decrease in material use and 5% reduction in transportation from its previous briquette.

Kingsford® charcoal is an industry leader in environmental controls and sustainability. Operations include:State-of-the-art air-emission controls that include a post-combustion chamber for the wood-charring operation, and dust collectors in other parts of the operation to control particulate emissions.

Recycling of recovered dust and broken briquettes generated during manufacturing.

Containment and reuse of process water in the manufacturing operation.

Char is produced in retort kilns that recycle energy and minimize air emissions.

Plants purchase waste wood for our charcoal from area wood products businesses diverting it from the waste stream.

Brita® ProductsPlastic: A single Brita® pour-through filter can replace 300 standard 0.5 L (16.9 ounce) containers of bottled water.

A Brita® pour-through filter and pitcher (40 gal or 151 liter capacity) uses only about 1 lb. of plastic resin.

300 bottles needed for that same 40 gallons would use about 15 lbs. of plastic resin.

Transportation: One truck can only hold ~ 40,000 lbs. or 5,000 gallons of bottled water.In contrast, a truck can hold 120,960 filters, or the equivalent of 4.8 Million gallons of filtered water.

92

Diversity Leadership

Diversity partnerships with 25 professional organizations

No. 6 in California for percentage of female executive leaders

100% on Human Rights Campaign’s Corporate Equality Index for 2nd year

Hosted 10 Bay Area Diversity Summits events

Employees featured in: Black EOE Journal, Diversity Matters, Ebony, Hispanic Business, Hispanic Network, Oakland Tribune, Out Now, Professional Woman’s, San Francisco Chronicle, and Wall Street Journal

47

Related Documents

![WELCOME [files.shareholder.com]files.shareholder.com/downloads/ACIW/5800322185x0x707102/...PAPER BILLS/ CHECKS MOBILE ONLINE BRANCH POS ATM CHANNELS ACI UNIVERSAL PAYMENTS Global Markets](https://static.cupdf.com/doc/110x72/5aa109037f8b9ac67a8b46d7/welcome-files-files-bills-checks-mobile-online-branch-pos-atm-channels-aci.jpg)