* Corresponding author. Tel.: #49-221-470-5355/48; fax: #49-221-470-5350. E-mail addresses: markus.fredebeul@uni-koeln.de (M. Fredebeul-Krein), andreas.freytag@uni-koeln.de (A. Freytag) 1 When the WTO agreement was signed in February 1997 only 69 countries committed to liberalise international trade in basic telecommunications services. In the meantime three additional countries * Barbados, Cyprus and Surinam * signed the agreement. Telecommunications Policy 23 (1999) 625}644 The case for a more binding WTO agreement on regulatory principles in telecommunication markets Markus Fredebeul-Krein*, Andreas Freytag Institut fu ( r Wirtschaftspolitik an der Universita ( t zu Ko ( ln, Pohligstr. 1, D 50969 Cologne, Germany Abstract On February 5, 1998, the WTO agreement on basic telecommunications services entered into force. Although the WTO agreement is a step into the right direction its impact might be rather modest. This is because apart from the many exemptions, which are likely to undermine market access and national treatment commitments, the regulatory provisions laid down in the WTO agreement are neither speci"c nor comprehensive enough to ensure open market access. Because there is in most cases a lack of clear de"nition as to the terms and conditions of regulatory provisions, there is a great danger that governments might nullify the commitments by abusing the regulatory requirements. ( 1999 Elsevier Science Ltd. All rights reserved. JEL classixcation: F1; L5 Keywords: WTO agreement on basic telecommunications services; International regulation 1. Introduction On February 5, 1998, the WTO agreement on basic telecommunications services, called the `Fourth Protocol to the GATSa, entered into force. In varying degrees, 72 WTO Members have pledged to open their markets to foreign competition, allowing overseas companies to buy stakes in domestic telecom companies and to abide by common rules on fair competition in telecom markets.1 The liberalisation of telecom markets will be bene"cial because it encourages a more 0308-5961/99/$ - see front matter ( 1999 Elsevier Science Ltd. All rights reserved. PII: S 0 3 0 8 - 5 9 6 1 ( 9 9 ) 0 0 0 4 7 - 6

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

*Corresponding author. Tel.: #49-221-470-5355/48; fax: #49-221-470-5350.E-mail addresses: [email protected] (M. Fredebeul-Krein), [email protected] (A. Freytag)1When the WTO agreement was signed in February 1997 only 69 countries committed to liberalise international trade

in basic telecommunications services. In the meantime three additional countries * Barbados, Cyprus and Surinam* signed the agreement.

Telecommunications Policy 23 (1999) 625}644

The case for a more binding WTO agreement on regulatoryprinciples in telecommunication markets

Markus Fredebeul-Krein*, Andreas Freytag

Institut fu( r Wirtschaftspolitik an der Universita( t zu Ko( ln, Pohligstr. 1, D 50969 Cologne, Germany

Abstract

On February 5, 1998, the WTO agreement on basic telecommunications services entered into force.Although the WTO agreement is a step into the right direction its impact might be rather modest. This isbecause apart from the many exemptions, which are likely to undermine market access and nationaltreatment commitments, the regulatory provisions laid down in the WTO agreement are neither speci"c norcomprehensive enough to ensure open market access. Because there is in most cases a lack of clear de"nitionas to the terms and conditions of regulatory provisions, there is a great danger that governments mightnullify the commitments by abusing the regulatory requirements. ( 1999 Elsevier Science Ltd. All rightsreserved.

JEL classixcation: F1; L5

Keywords: WTO agreement on basic telecommunications services; International regulation

1. Introduction

On February 5, 1998, the WTO agreement on basic telecommunications services, called the`Fourth Protocol to the GATSa, entered into force. In varying degrees, 72 WTO Members havepledged to open their markets to foreign competition, allowing overseas companies to buy stakes indomestic telecom companies and to abide by common rules on fair competition in telecommarkets.1 The liberalisation of telecom markets will be bene"cial because it encourages a more

0308-5961/99/$ - see front matter ( 1999 Elsevier Science Ltd. All rights reserved.PII: S 0 3 0 8 - 5 9 6 1 ( 9 9 ) 0 0 0 4 7 - 6

2For an analysis of the exemptions see Fredebeul-Krein and Freytag (1997).3The need for regulating the telecommunications sector is demonstrated by Vogelsang and Mitchell (1997).4The general GATS principles (Part II of GATS) include most favoured nation treatment and transparency and are

compulsory for all WTO Members. In contrast, the speci"c commitments have to be met only by those WTO Memberswhich record their commitments for a service in sector and country speci"c national schedules.

e$cient use of resources, such as capital and manpower. Furthermore, the agreement is likely topromote innovation, productivity, diversity and quality of products. For many telecommunicationusers, the transition to a multilateral trading system will bring bene"ts in terms of greater choiceand lower prices. For the majority of carriers, there will be signi"cant bene"ts in terms of creatingnew market opportunities and a more level playing "eld.

Still, the impact of the WTO agreement could prove to be rather modest. This is because manyexemptions in form of sectoral reservations, limits to foreign investment and phase-in commit-ments over various periods of time are likely to undermine market access and national treatmentcommitments.2 Therefore, the agreement will not necessarily immediately result in a rigorousliberalisation of national telecom markets. Apart from the various exemptions, another aspectraises concern about the impact of the WTO agreement on opening national markets: regulatoryprovisions. Evidence of countries having established e!ective competition in their telecom marketsdemonstrates the need for a comprehensive regulatory framework. Yet, the rather general nature ofthe WTO regulatory provisions raises doubts about whether the rules will be e$cient in ensuringopen market access. Rather, the agreement seems to leave WTO Members the choice of how tocomply with the agreement. Thus, the impact of the WTO agreement on opening national telecommarkets might depend crucially on the regulatory framework erected by the WTO Members.

The paper is organised as follows: in the second section, we will discuss the impact of theregulatory provisions in the WTO agreement on liberalising national telecom markets. Or, in otherwords: will the WTO agreement allow signatories to undermine the commitment on opening theirtelecom markets? In the third section, the reasons for the commitments being insu$cient arediscussed. We will analyse how the United States and the European Union have implemented someof the commitments made under the WTO agreement in the fourth section. Finally, we advancea case for a more binding commitment of the WTO Members as regards the further liberalisation oftelecommunication services.

2. The impact of the regulatory provisions on liberalising national markets: many incentivesto default

In order to ensure that telecom markets are fully open under a competitive market environment,various regulatory provisions have to be set up. It is impossible to completely leave telecommuni-cation to the market since there are reasons for competition failure, namely economies of scale,economies of scope and network externalities.3 Within the WTO these regulatory issues have beenaddressed in two ways: "rst, those WTO Members that have undertaken commitments to opentheir markets for basic telecommunications services became subject not only to the general GATSobligations but also to the speci"c GATS provisions of market access and national treatment.4

626 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

Fig. 1. Fourth protocol of the liberalisation of markets for basic telecommunications services.

5Sixty three countries have, in accordance with Article XVIII of the GATS, adopted these pro-competitive commonregulatory guidelines; see WTO (1998).

According to the market access commitment, WTO member states are required not to adoptor maintain measures that limit the total value of services transactions, the total number ofservice providers, service operations and natural persons that may be employed in the telecomsector. The same accounts for measures which restrict speci"c types of legal entity or which limitparticipation of foreign capital. As regards national treatment, a country may accord servicesor service suppliers of any other country treatment no less favourable than that accorded to likedomestic services and service suppliers subject to the limitations and conditions listed in a nationalschedule.

Second, speci"c regulatory commitments were made under the Reference Paper within theFourth Protocol which lays out key principles for the design of national regulatory rules. Thoseprinciples include provisions on competitive safeguards, interconnection, licensing, universalservice, use of scarce resources and independence of regulatory authorities.5 Below, we analysewhether these provisions are su$cient for making the market access commitments in the telecomsector e!ective. In particular, we will investigate whether the regulatory provisions of the ReferencePaper allow WTO members to impede market entry by foreign carriers. Fig. 1 shows the structureof the Fourth Protocol.

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 627

6The de"nition of a major supplier is based on the following notions: (1) ability to a!ect materially the terms ofparticipation, (2) control over essential facilities or the position in the market and (3) the relevant market for basictelecommunications services.

2.1. Competitive safeguards

Due to historical developments, national telecom markets of most countries will continue to becharacterised by dominant carriers. These might have the market power to restrict competition atthe expense of other suppliers and of consumers. Within the GATS there are several Articles whichdeal with competition-related issues: Article VIII on monopolies and exclusive service providers,Article IX on business practices and Article XV on subsidies. Yet, since these GATS obligations arerather general in nature, they are not su$cient in assuring market access in telecom markets.Therefore, further rules were elaborated in the Reference Paper of the Fourth Protocol. These rulesaim at committing the signatories to provide e!ective safeguards against unfair competition.

Section 1 of the Reference Paper requires the signatories to maintain `appropriate measuresathat would prohibit anti-competitive activities of suppliers, which alone or together, constitutea `major suppliera.6 Examples of anti-competitive practices are (a) cross-subsidisation such asusing revenues from monopoly services to undercut prices of competitors on liberalised markets forservices, (b) using information obtained from competitors, such as through interconnectionnegotiations, with anti-competitive results, (c) holding back technical data on essential facilities andcommercially relevant information necessary for other suppliers to provide services on a timelybasis.

However, these provisions lack clarity. Apart from the three examples above, the ReferencePaper does not de"ne in which cases carriers are considered as behaving anti-competitively.Furthermore, it does not specify mechanisms for addressing potential anti-competitive practices inthe telecom services sector. Thus, any country is free to establish its own measures for preventinganti-competitive practices. This has two important consequences.

First, since the underlying de"nition of a major supplier is not limited to a supplier with controlover domestic facilities, governments will be able to impede market entry by foreign serviceproviders, which are major suppliers in their home country, by enforcing legislation directedagainst them. For instance, a country could deny market entry by foreign "rms based oncompetition grounds. It could also require them to charge minimum prices for the provision ofcertain services. Such competitive safeguard measures would have a strong protectionist driftendangering the market access commitments made under the Fourth Protocol. Due to the fact thatsuch action is often driven by political determinants for protection (such as successful lobbying bydomestic "rms), governments are likely to be inclined to pass such legislation.

Secondly, since the provisions on competitive safeguards do not specify any rules for govern-ments when they develop an appropriate regulatory framework, a country may fail to implemente!ective action for preventing anti-competitive practices by domestic suppliers with market power.In the absence of such action the cross-subsidisation of services in competitive market segmentswould be facilitated because existing monopolistic bottleneck areas would allow a dominantsupplier to make monopolistic pro"ts. If governments do not require major suppliers to createlegally separate subsidiaries or to implement independent accounting operations (the Reference

628 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

7See the controversial discussion about the interconnection rates of the Deutsche Telecom AG which has been led byAlbach and Knieps (1997) and Vogelsang (1996).

Paper does not foresee such regulatory rules), it would be di$cult to assess potential cross-subsidisation (Bronckers & Larouche, 1997). Thus, in the absence of e!ective regulatory provisionson competition safeguards, service providers with market power will be able to continue withanti-competitive practices. A signatory of the Fourth Protocol would not violate the regulatoryprovisions on competitive safeguards.

2.2. Interconnection

Another important regulatory issue as regards competitive safeguards are interconnectionguarantees. They are necessary, in order to allow new market entrants access to the network ofestablished carriers. On this issue, several provisions were made in the Reference Paper: majorsuppliers are required to provide interconnection under equitable and non-discriminatory termsand conditions, at cost-oriented rates, su$ciently unbundled, at any technically feasible point andin a timely fashion. Furthermore, they are obliged to disclose information on technical standardsand to guarantee a quality that they provide for their own services. Also, procedures for intercon-nection negotiations have to be transparent. If con#icts arise on the terms and conditions forinterconnection, a dispute settlement mechanism is foreseen.

Yet, some major issues of interconnection are not addressed. The most important shortcomingconcerns interconnection prices. Since the Reference Paper does not further specify on whichcriteria interconnection charges have to be based, cost-oriented rates may become di$cult torealise in practice. Depending on the method for allocating the costs of interconnection, pricesmight be above the economic costs of interconnection.7 For instance, under the current ReferencePaper national regulatory authorities are allowed to calculate interconnection charges on the basisof purchase costs. If they do so, the interconnection tari!s include costs, which arise due toproductive ine$ciencies and which would not be taken into account in competitive markets. Newforeign and domestic entrants would then be discriminated against. In order to prevent this, itwould be necessary to set up more speci"c pricing guidelines for access to monopolistic bottlenecksareas such as the local network (Knieps, 1997). One such rule should be that WTO Members arerequired to calculate interconnection prices according to forward looking long-run incrementalcosts. Furthermore, national regulatory authorities should be obliged to publish a referenceinterconnection o!er, including a description of the interconnection o!erings broken down intocomponents according to market needs. In order to obtain exact information on the costs andthereby minimising the information advantage of the incumbent a detailed listing of the intercon-nection charges should be required. Unless these shortcomings are overcome in a new agreement,dominant suppliers will be able to abuse their market power.

A further weakness is, that no reference is made as to which network components have to beunbundled. Therefore, con#icts might arise with interpreting the term `su$cientlya. Thus,because a supplier with signi"cant market power has a stronger bargaining position thanpotential newcomers he may enforce ine$cient terms for the provision of interconnection to rivals

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 629

8Number portability refers to the ability to change users of telecommunication services but to retain, at the samelocation, their familiar telephone number without impairment of quality, reliability or convenience when changing theoperator. Carrier selection means users can choose between the services of competing carriers on a call-by-call basis or topre-select the carrier of their choice on a permanent or default basis.

9Moreover, it is by no means clear how a necessary barrier to trade in services can be distinguished from anunnecessary one.

(Brock & Katz, 1997). The dispute settlement mechanism lacks clarity in this regard since it is notmentioned whether a national regulatory authority can impose an agreement on the parties or not.Market entry of new competitors might therefore be seriously hampered. Moreover, the regulatoryprovisions do not exclude the use of proprietary protocols for the interconnection of networks. Byallowing a dominant carrier to maintain unique or proprietary interconnection speci"cations itmight therefore be able to behave in an anti-competitive way because new entrants will be subjectto its technical preferences.

Another major shortcoming of the Reference Paper is that there is hardly any regulatoryprovision for numbering, which is crucial for new carriers to have direct access to end-users. Theonly reference is made to this issue is that numbers have to be allocated in an objective, transparent,timely and non-discriminatory manner. Yet, WTO Members are neither required to guaranteenumber portability nor carrier selection.8 If governments do not adopt any legislation on theseissues, competition between di!erent carriers will be restricted (Armstrong, 1997). Established carrierswould be able to impede market entry by new "rms because the inability to keep the same telephonenumber when changing to a dominant carrier's competitor, is due to additional costs, a disincentivefor customers to switch. The same applies to carrier selection, which is essential, if fair andnon-discriminatory competitive conditions are to be created. If users are not able to choose easilybetween the services of competing carriers entrants may have di$culties in attracting new customers.

2.3. Licensing

In nearly all countries suppliers of telecommunications services need a licence for providinga particular service. Licensing conditions, however, might create barriers to market entry. In orderto make it more di$cult for governments to discriminate against foreign competitors, the ReferencePaper requires all licensing criteria, the period of time required to reach a decision on anapplication and the terms and conditions of individual licenses to be made publicly available. Ifa license is denied, the applicant can request the reasons for denial. While these provisions willguarantee the transparency of licensing procedures, their e!ect on the opening of markets might berather weak. This is because no provisions exist on the terms and conditions for individualtelecommunications licences.

Nevertheless, one could argue that Article VI of the GATS contains such provisions. Paragraph4 requires that `2licensing requirements do not constitute unnecessary barriers to trade inservices,2a (WTO, 1995, p. 333). A WTO Member would contravene its commitments if it appliedmeasures that are not based on objective and transparent criteria, that are more burdensome thannecessary or that restrict the supply of the service. However, these provisions do not put anylicensing requirements in concrete terms.9 Thus, by obliging applicants to meet various criteria for

630 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

10For instance, there is no mechanism which guarantees that licences for scarce resources are granted in an objectivemanner (e.g. by auctioning).

the granting of a licence, a country can impose undue burdens on foreign entrants. In particular,a country could establish conditions for granting a licence which can be met by domestic "rmsmore easily than by foreign companies (such as the share of R&D spending, see Section 3.2). Also,there are neither any speci"cations as regards the situations in which a licence can be required formarket entry nor is there any upper limit for licence fees (which can therefore be very high, thusdiscouraging market entry). Moreover, while WTO members are obliged to make on licensingdecisions within a `reasonable period of timea, it is not further speci"ed as to what is meant byreasonable period. Thus a country can discriminate against foreign service providers by delayinga decision on issuing licences.

Concerning restrictions on the number of licences, the WTO agreement lacks clear rules as well.While article XVI (GATS) prohibits such limitations, in the case of scarce resources such asfrequencies there still might be the need to restrict the number of suppliers. The Reference Paper,therefore, requires countries to carry out the procedures for the allocation and use of scarceresources in an objective, transparent and non-discriminatory manner. However, rules on theactual policies of allocating these resources are not provided.10

2.4. Universal service

By establishing a universal service policy in the telecommunications sector governments pursuesocial, regional and other non-economic policy objectives. They are free to do so since the GATSrecognises `2the right of Members to regulate, and to introduce new regulations, on the supply ofservices within their territories in order to meet national policy objectives2a (WTO, 1995, p. 327).Also, according to the Reference Paper, WTO Members are allowed to de"ne any kind of universalservice obligation they wish to maintain in this area. They are only required to do so ina transparent, non-discriminatory and competitively neutral manner.

However, neither the general GATS obligations nor the Reference Paper provide more concreteguidelines for many of the various competition related aspects of universal service provision. Asa consequence, governments might be able to create barriers to market entry by requiringcomprehensive universal service obligations. For instance, no concrete guidance is provided on themaximum set of elements comprising universal services, nor on the prices that must be charged forthe services. The agreement also fails to specify how to determine the universal service provider.National regulatory authorities are neither required to establish clear principles for calculating thecosts of the universal service provision nor to develop concrete procedures by which such costs canactually be measured. National regulators are free to determine which and to what extent operatorshave to contribute to any burden associated with universal service obligations. Therefore, while notfailing to comply with the regulatory provisions under the Fourth Protocol, countries can establishrules for a universal service policy, which in practice discriminate against foreign and domesticmarket entrants.

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 631

2.5. Independent regulator

For a regulatory system to be e!ective in terms of promoting competition in national telecommarkets it is of vital importance to have an independent regulator. Without an independentregulatory authority, being able to monitor and enforce legislation, it will be di$cult to implementthe agreement. The Reference Paper requires all signatories of the agreement to set up independentregulatory agencies which are not accountable to any telecom service provider. However, there isno provision that in case of state-owned telecom companies the regulatory body has to bestructurally separated from the ministry which is exercising the ownership function over thetelecom operator. Since in many countries telecommunications operators are still state-owned andthe GATS does not require the transformation of telecommunication operators into privatecompanies (including privatisation), this gives raise to concern. Liberalisation of the telecommuni-cations sector, without privatisation of the dominant carrier, can lead to a severe con#ict of interestfor any regulatory authority a government may establish. What is also missing in the ReferencePaper is any requirement as regards the enforcement power of the regulatory authority. Ifa government does not grant adequate authority to develop and enforce pro-competitive regula-tions, e!ective application of the regulatory rules being adopted by a WTO Member will not bepossible.

3. Why market access commitments are insu7cient

Neither the general and speci"c GATS obligations nor the regulatory provisions of the ReferencePaper are su$cient for ensuring open market access by foreign (and domestic) suppliers oftelecommunication services. While the WTO regulatory commitments indeed lay the foundationsfor a pro-competitive regulation of telecommunications services, they leave WTO Members free todetermine how to comply. As there is in most cases a lack of clear de"nition concerning the termsand conditions of regulatory requirements there is a great danger of governments nullifying thecommitments by abusing the regulatory requirements (Drake & Noam, 1997). Their rather vaguenature is a signi"cant shortcoming of the WTO agreement. This situation may again erodeinternational competition in basic telecommunication services.

Thus, having an international framework without comprehensive and detailed rules, even thoseWTO Members which have committed to the regulatory principles of the Reference Paper are ableto prevent market access without o!ending WTO rules. If their governments are not willing and/orpolitically able to introduce regulatory rules for e!ective competition in the telecommunicationssector, foreign (and domestic) companies will be deterred from entering these markets. Both theGATS principles and the regulatory principles of the Reference Paper leave space for individualcountries to interpret the rules and to deny market access for foreign competitors.

It could be argued that the WTO agreement does not prevent the signatory countries fromintroducing more e!ective national regulatory frameworks for a competitive telecommunicationssector. At "rst glance, all countries should be interested in a comprehensive commitment to opendomestic telecommunications market. This is because, from an economic point of view, protection-ist measures are not desirable policy instruments. Restrictions on international trade are not"rst-best solution for capturing economic rents, which can exist in the telecommunications sector

632 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

11A variety of empirical studies gives evidence on the political economy of trade protection, e.g. Anderson andBaldwin (1981) and Hillman (1994).

12The main shareholder of the Deutsche Telekom AG, for instance, is the German government which in April 1998criticised the German Regulatory O$ce for their decision concerning interconnection pricing, see Handelsblatt (1998). Itwas successfully argued by the Ministry of Finance that the authorised prices were too low and would endanger generalpolicy objectives. The Regulatory O$ce "nally revised its decision.

due to market imperfections. Such an interventionist approach would encourage the production byless e$cient domestic "rms at the expense of more e$cient foreign "rms. Rather than promotingine$cient domestic "rms by trade restrictions it would be socially less costly to adopt a policywhich facilitates the entry of (domestic and foreign) competitors.

Bearing this in mind, the question is why WTO Members might have an incentive not toimplement more e!ective pro-competitive regulatory frameworks in order to bene"t from liberal-ised national telecom markets. The reason for this low level of commitment can be found whenpolitical economy considerations are taken into account. The world trading system is stillcharacterised by the general opinion of exports being superior to imports. Therefore, governmentsin general have a preference for demands of import competing domestic interest groups forprotection from international competition. This is due to the fact that the interests of importcompeting industries are easier to organise than those of export sectors or consumers (Freytag,1995).11

Furthermore, the tendency to deny market access especially in telecommunication is inherent inthe market structure in most WTO Members. Since the provision of basic telecommunicationservices has been regarded as a natural monopoly, until recently in most countries there was onlyone telecom supplier. These protected suppliers behaved in a typical monopolist manner, meaningthat X-ine$ciency existed. This behaviour stems from the fact that it is not necessary to adapt toeither consumer wishes or to technological change. Recently, competitive pressures and the needfor structural change have arisen. Instead of trying to cope with structural changes, the formermonopolist normally invests in rent seeking activities. Moreover, the incumbent was state ownedand after the privatisation of these `enterprisesa, the state often is the main shareholder.12 Asa consequence, the government is only partly interested in enhancing competition and to a certainextent, is interested in the fate of the former monopolist. If the major incumbent loses market sharesand income, the state budget of many signatories will be negatively a!ected. Hence, the establishedtelecom operators can exert a high pressure on the government, even if the regulatory agency isindependent from the government.

Governments did not only have the "nancial interest in these state owned monopolies, they alsohad social objectives. People in rural areas should be provided with basic telecommunications ofthe same quality and at the same price as people in municipal regions where economies of scalewould allow for cheaper supply. Uniform prices were compulsory. Also, special groups andinstitutions such as schools, hospitals, etc., were sometimes favoured. A turn towards intensi"edcompetition would certainly lead to di!erent prices due to varying costs of production and priceelasticities of consumption in di!erently populated areas. Today, this reasoning is still in place, andmany governments try to maintain certain levels of universal service in order to meet commensur-ate demands. As long as the interests of rural population and social institutions are overrepresented

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 633

13Both have committed to liberalise essentially all basic telecom services (facilities-based and resale) for all marketsegments (local, long distance and international) across their territory. They also have signed the Reference Paper of theFourth Protocol.

14For example, the FCC reviews interconnection charges under a system of price cap regulation, see Noll (1998).Thereby changes in a carrier's rate from one year to the next are limited to increases in costs over which the carrier has nocontrol, less an o!set to re#ect expected increases in the carrier's productivity.

15For instance, the US submitted an exemption to the MFN principle for one-way satellite transmission of Direct toHome (DTH), Direct Broadcast Satellite (DBS) and digital audio services (DARS).

in parliaments, bureaucracies or governments this attitude gives reason for misuse of universalservices and discrimination against new foreign and domestic suppliers.

In the following section we will analyse whether governments are indeed inclined to implementthe WTO agreement in a way that will allow for impeding market entry by foreign carriers. To thisend, the US and the EU will be used as examples, as they are the two most important signatories ofthe Fourth Protocol in terms of market volume.13

4. Implementation of the WTO agreement in the US and the EU: worries that are not completelyexaggerated

The United States and the member states of the European Union had already committedthemselves to competitive telecom markets before they signed the Fourth Protocol. The USderegulated its long distance telecommunications market in the 1980s. With the adoption of theTelecommunications Act of 1996 the US also introduced competition in its local telecommunica-tions market by removing legal, operational and economic barriers. Following the Telecommuni-cations Act, the Federal Communications Commission (FCC) issued speci"c rules on localinterconnection, universal services and access charges.14 In recent years, the EU passed variousliberalisation and harmonisation directives committing its member states to open national tele-communication markets to competitors by January 1998. Therefore, few additional legislationshad to be adopted to fully implement the commitments made under the Fourth Protocols. In mostinstances, the two signatories have introduced regulations which go beyond those provided for inthe Reference Paper of the WTO agreement. Yet, US and EU legislation on establishing e!ectivecompetition in their telecommunications markets might still allow discrimination against potentialforeign competitors. One reason is that the US and some member states of the EU kept severalmarket access restrictions.15 The issues of licensing and universal services will be discussed below,as to whether there are also regulatory rules which allow for deterring foreign "rms from enteringthe market.

4.1. United States

In the US, until recently, the US regulatory authority FCC applied an `E!ective CompetitiveOpportunity Testa (ECO) on foreign carrier entry into the US market. The ECO-test required anassessment of whether the country of origin of a US a$liate provided competitive opportunities to

634 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

16The rules only require for applicants to provide the satellite services DTH, DBS and DARS (which are not coveredby US commitments in the WTO Basic Telecom Agreement) the FCC will continue to examine whether US satelliteshave e!ective competitive opportunities in the relevant foreign satellite markets to determine whether to allow non-USsatellites to serve the United States.

17On satellite services, the FCC will consider additional public interest factors, including spectrum availability andoperating requirements, in reviewing requests to access foreign-licensed satellites. see FCC (1997c).

18For providing telecom services on international routes the FCC adopted a `rebuttable presumptiona in favour ofentry for foreign carriers with less than "fty percent market share in each relevant foreign market from WTO Members.

US carriers for the services which the a$liate was seeking to o!er. This was a strong recourse forthe principle of reciprocity. With the enforcement of the WTO agreement the US had to abandonthe ECO test, since it did not comply with the GATS principles of most favoured nation andnational treatment. Therefore, in November 1997, the FCC adopted new rules on foreign marketentry, which became e!ective in early February 1998 (see FCC, 1997b).

These new rules do not longer require applicants from WTO members to demonstrate that theirmarkets o!er e!ective competitive opportunities.16 The ECO test is replaced with an `open entrystandarda for applicants from WTO member countries. Therefore, applicants for a licence are ingeneral required to seek FCC approval. When foreign carriers apply for submarine cable landinglicences, wireless licences and licenses for providing international simple resale and internationalfacilities-based services, the FCC presumes that market entry is pro-competitive and thus princi-pally grants authorisations. However, the FCC retains the authority to deny or condition suchentry if demanded by public interest. Public interest factors include national security, law enforce-ment, foreign policy, and trade concerns (FCC, 1997b).17 In addition, the FCC looks at thequali"cations of an applicant, including "nancial, legal, and technical capabilities, as well as theability to ful"l legal requirements. Furthermore, the FCC reserves the right to review or denyapplications based on competition grounds. If safeguards do not adequately constrain the potentialfor anti-competitive harm, the FCC can attach additional conditions to a grant of authority. If anapplication poses a `very high risk to competitiona, the FCC can even deny an application. Whilethe FCC states `that an applicant would not be denied entry based solely on market sharea,18a foreign carrier might face denial when it has `the ability upon entry, or shortly thereafter, to raiseprices by restricting outputa (FCC, 1997b, Section 52). On the whole, public interest and competi-tion factors seem like an invitation for protectionist demands.

Nevertheless, the open entry standard including both the public interest analysis and thecompetition test is consistent with GATS obligations as well as the commitments made under theReference Paper. For instance, the competitive safeguard provisions do not violate nationaltreatment obligations under Article XVII if the regulatory agency also considers competitionfactors in evaluating entry by national carriers. Article III of the GATS (transparency) does notimpose any speci"c obligations with regard to the content of national laws or regulations. It merelyrequires the publication of national laws and regulations. Article XVI (Market Access) onlyprohibits WTO Members from maintaining or adopting the types of quantitative limitations(unless such limitations are included in a WTO Member's schedule of speci"c commitments). Theregulatory provisions on competitive safeguards even require signatories of the Fourth Protocol toadopt measures in order to prevent anti-competitive behaviour. Moreover, measures to prevent

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 635

19Furthermore, the TA mandates support for customers living in rural and high cost areas, for low-income subscribersand for schools, health care providers and libraries. It further requires access to advanced telecommunications all overthe US and availability of quality services at reasonable costs.

20For instance, internet access providers are excluded from contributing to the universal service fund (Prieger, 1998,p. 66).

anti-competitive behaviour of carriers are not required to be limited to activities of only domesticsuppliers. Since the GATS does not specify a single mechanism for addressing potential anti-competitive practices in the telecommunications services sector, any country remains free to rely onits own regulatory enforcement and antitrust actions.

To sum up, while the new rules facilitate entry of foreign service providers and investors, they stillallow for considerable barriers for foreign-owned "rms wishing to invest in telecommunicationsinfrastructure and to provide telecommunications services. To a certain extent, the open entrystandard undermines the commitments made under the WTO Basic Telecom Agreement. Thestandard might undercut the presumption in favour of entry by making it easier to oppose marketaccess. The criteria set up in the open entry standard are broad and unclear. Therefore, they leavetoo much discretion with the FCC. Reserving the right to deny a license does not provideapplicants with the certainty they require. Foreign carriers seeking to enter the US market can besubject to challenges by competitors, which in return would create further delays in the granting oflicences. The standard of a `very high risk to competitiona imposes additional burdens on foreigncompanies. Since no further criteria are laid down for assessing the ability to raise prices, applicantsface uncertainty and unpredictability when trying to enter the US market.

Another potential market entry barrier to foreign (and domestic) carriers is erected by the USregulatory framework in terms of universal service provisions. This is because for collectinguniversal service contributions a universal service fund is envisaged, in which all providers oftelecommunications services are obliged to make payments (see FCC, 1997a).19 Due to the broadde"nition of universal services the size of the universal service fund imposes a high burden onservice providers. It is estimated at a lower bound of $3.7 billion and an upper bound of $11.7billion per year (Prieger, 1998, p. 63). The funding is tantamount to a revenue tax on telecommuni-cations services. Providers will be taxed, depending on the service to be o!ered ranging from 0% to17.64%.20 Thus, although the Telecommunications Act of 1996 states that all providers oftelecommunications should make an equitable and non-discriminatory contribution to the fundingof universal services, the Order does not ensure this objective. It causes ine$ciencies by distortingprices and giving certain providers an unfair competitive edge. Furthermore, the funding ofuniversal services will increase service prices and thus reduce the quantity of services consumed.For this reason and because of the signi"cant "nancial contributions of service providers, theuniversal service obligations imposed on new entrants are so burdensome that they will defeat theobjective of enhanced competition.

Nonetheless, the US rules on universal services do not violate the regulatory provisions ofthe Fourth Protocol. While it states that rules on universal services may not be unduly burden-some, it would be di$cult for a foreign government to prove that this is the case (due to theabsence of any criteria on this issue). Thus illustrates the need for more explicit internationalregulatory principles.

636 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

21The directive explicitly lists those purposes for which member states may issue individual licences: when thelicensee needs access to radio frequencies or numbers or to public or private land, when the licensee is requiredto provide universal service and other obligations under EU legislation and when the licensee has signi"cantmarket power. Moreover, the directive requires member states to set upper time limits. Restrictions to thenumber of individual licences are only permitted to the extent required to ensure the e$cient use of radiofrequencies.

22A national regulatory authority can refuse or withdraw a general authorisation or an individual licence when anapplicant does not comply with a condition attached to a licence, see Xavier (1998).

23For instance, the denial of a licence by an EU member state to carriers which might be a dominant carrier in anothercountry is not allowed, even if the carrier engages in anti-competitive behaviour at a later stage.

4.2. European Union

As a general rule, EU legislation allows third country market access to the market for telecom-munication services to be tied to service opportunities o!ered to European carriers in a thirdcountry. When a third country does not grant EU companies authorisations, rights which arecomparable to those provided by the EU for companies from that third country, the EU reservesthe right to undertake appropriate measures (OJE, 1997a). Yet, such a reciprocity approach is notpermitted to be applied when obligations under international agreements do not allow so (Art.18,3). Thus, with the entry into force of the Fourth Protocol these provisions cannot be applied toWTO members. Instead, suppliers from these countries receive the same treatment as operatorsfrom EU member states.

Although the EU directive on licensing provides a number of sound principles to guide the grantof licenses,21 the possibility cannot be ruled out, however, that member states adopt legislationwhich might discriminate against foreign applicants of a licence. This is because member states areallowed to attach several conditions to the granting of general authorisations and licences.22 Suchconditions include those linked to the allocation of numbering rights and speci"c radio frequencies,speci"c environmental and speci"c town and country planning requirements, provision of univer-sal service obligations, conditions applied to operators having a signi"cant market position,requirements related to quality, availability and permanence of the service or the network (suchas "nancial, managerial and technical competence of the applicant), and defence related require-ments. Although these conditions are more restrictive than those listed under US legislation,23they also give EU member states the opportunity to impede or deny market access to foreign"rms. This is because imposing conditions on each service provider individually in the contextof a licensing proceeding might result in unequal treatment and delay issuance of licenses. The im-plementation of the EU directive on licensing gives evidence for this assumption. For instance,in France and Italy licensing conditions require "nancial contributions to research (in Francealso to training) in the telecommunications sector, thereby impeding market access of newservice providers (European Commission, 1998). In addition, in France there are no provisionsas regards administrative procedures for granting individual licences so far. Another examplefor the creation of market entry barriers are licensing fees. Although the EU directive on licensingstates that any fees imposed on service providers may seek only to cover the administrative costs

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 637

24For instance, France requires operators with signi"cant market power to pay annual fees of 1.068.000 ECU, inGermany the fee is up to 5.362.093 ECU per year, and in Spain the annual fee is 0,1% of the annual turnover. In contrast,in the United Kingdom the maximum annual fee is only 30.021 ECU for public "xed voice telephony, see EuropeanCommission (1998, Annex III).

25The EU has adopted a rather comprehensive set of rules for universal services. Measures establish clear principlesfor the scope and pricing, possible funding mechanisms, the costing and "nancing of universal service. For a moredetailed discussion of the EU's universal service concept see Fredebeul-Krein (1998).

26See OJE (1997b). So far, apart from France and Italy no member state has introduced schemes to share the burden ofuniversal service provision, because they do not consider the provision of universal services to constitute an unfairburden on the incumbent.

27Fixed operators are obliged to pay 0.27 ECU/100 per minute to the incumbent, mobile operators 0.15 ECU/100 perminute, see European Commission (1998, p. 25).

incurred in the issue, some member states require licensees to pay fees which are far above thosecosts.24

Also EU legislation on universal services does not completely prevent member states fromadopting national rules which might discriminate against certain service providers.25 For instance,while the interconnection directive requires member states to ensure that incumbents are compen-sated not more than the net costs of the universal service obligation,26 such a regulatory provisioncannot exclude a potential overcompensation, since it lacks clear rules on calculating those netcosts. If only one carrier is required to provide universal services it has an information monopolyon the arising costs. Thereby, the operator can estimate the costs higher than they actually are. Byreceiving excessive payments to cover de"cits, it would have a competitive edge over its competi-tors. For instance, France has issued a decree on universal service "nancing, according to whichoperators have to pay access de"cit charges to the incumbent irrespective of their market powerand the costs of the universal service obligation.27 Only if EU legislation had required ex-antede"cit payments which are calculated on expected costs, it would have been guaranteed thata discrimination of competitors against the universal service provider would not take place. Thus,although the EU has adopted a detailed regulatory framework for the provision of universalservices, which goes far beyond the provisions laid down in the Reference Paper of the FourthProtocol, new competitors may still be discriminated against.

To conclude, the EU institutions have forced the member countries via directives to introducepro-competitive legislation. Thereby the European Union goes far beyond the commitments madewithin the WTO. Yet it still makes use of the loopholes of the multilateral framework. Notwith-standing this pro-competitive European framework, EU Members try to impose barriers to foreigncarriers. These barriers are not restricted to countries outside the EU, but, in general, a!ectcountries of both inside and outside the EU.

5. Towards a new international regulatory framework for trade in telecommunications services

It has been argued in Section 2 that public choice reasons make it politically di$cult and (partly)undesirable for governments to commit to an economically "rst-best regulatory framework.

638 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

Instead, from a government's point of view vagueness and intransparency is very attractive. Section4 clari"ed that even countries with a rather strong commitment like the US and the EU aretempted hinder foreign "rms from entering the domestic markets. Although they are committed toopen their markets to competition, foreign (and domestic) "rms might depend on the government'swillingness to let them enter the market.

One should not, however, be too critical with the WTO for the weaknesses identi"ed above. Thehistory of liberalisation of world trade reveals that it took eight GATT rounds to reach today'sopenness in trade of goods and services. Each round has been characterised by* partly modest,partly remarkable * progress in liberalisation. Therefore, we do not argue that the e!orts ofliberalisation in a multilateral framework is useless. Rather, the system can and certainly will beimproved. In this section, we provide reasons why it can be in the interest of governments to opt fora multilateral agreement on stronger commitment despite the political pressure laid upon them.

5.1. The solution: strong commitments in a multilateral setting

If WTO Members do not commit themselves satisfactorily to open and competitive markets,enforcement of market access within the WTO will become di$cult to realise. This holds evenwhen considering that the WTO dispute settlement mechanism (DSM) was remarkably improvedin the Uruguay Round (Thomas, 1996). Denying market access is not necessarily an o!ence againstthe agreement. Instead, the analysis in Sections 2 and 3 has revealed that WTO Members can signthe WTO agreement and at the same time protect their own enterprises from foreign competition.Hence, the main problem of trade in telecommunications (as of trade in services in general) does notlie in the weakness of the legal enforcement of WTO rules and agreements, as may be the generalopinion (Drake & Noam, 1997, p. 815). Rather, the agreement itself is too loose.

Hence, governments face a problem. Even if they are aware of the economic bene"ts of opentelecommunication markets and are willing to liberalise, they are often unable to pursue anadequate open market policy. This is because they are under pressure of well organised incumbentsthat try to prevent comprehensive liberalisation. Moreover, neglecting social issues like universalservice can be politically costly for a government. The political sovereignty of governments isconstrained by rent seeking groups (Tumlir, 1985).

However, not committing to competition can also be disadvantageous. One reason for govern-ments to change their behaviour is given by the enormous potential of technological change whichlies in the market for telecommunication services. This potential is exogenous from the govern-ments' point of view. Moreover, it is a threat to the sustainability of regulations, even a threat toincumbent suppliers on protected domestic markets. Governments might lose control over themarkets, if they close their eyes to this fact. Therefore, instead of trying to stop these dynamics, itmakes * not only economically but also politically * sense to be among those who design therules for it. This is where the multilateral trading order helps.

Given that many leading suppliers of telecommunications are multinational enterprises, it makessense to co-ordinate regulatory action internationally. Moreover, mutual commitment, or rathera deal with mutual concessions, has its merits: think of the negotiations on liberalisation asstrategic interaction with two or more players. If one country has already opened its markets toforeign competition it abandons potential threats. It has no power to discipline other countries.Thus, it is politically prudent not to rely on unilateral action.

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 639

28This should not be mixed up with the general understanding of reciprocity which is often used in a tit-for-tatmanner. There are serious economic problems related to this interpretation of reciprocity see Krugman (1997).

29For a theoretical analysis of international regulatory rules for telecommunications services markets see Fredebeul-Krein (1999).

Only mutual commitment will discipline countries that have problems with introducing com-petition in their domestic markets because of a strong telecom lobby and/or "scal interests. Undermutual commitment they can argue that other countries open their markets as well. Commitmentcan be used to credibly discourage domestic lobbies. For this purpose, concessions (on a multilat-eral level) could help to enforce the opening of telecommunications markets.28

In a nutshell, governments can regain internal sovereignty by external commitment. If theycommit themselves to consequently open their telecommunication markets in a binding multilat-eral agreement which is enforceable through the DSM, their internal position is strengthened. Theless discretionary power that is left by the agreement, the lower the degree of political pressure thatwill be put on governments to close markets for foreign "rms, and the greater will be the economicbene"ts generated through open markets. This logic of multilateral negotiations on trade policyhas been applied regularly in the past. It can be applied again to close the loopholes in the WTOregulatory framework that have been identi"ed above.

Another important argument in favour of multilateral, mutual commitment is one we havealready seen in the past agreements. It is nearly impossible to return to the status-quo ante aftera multilateral agreement has been enforced. The level of liberalisation which has been reached insuch an agreement de"nes the minimum level of market opening. If one country commitsunilaterally, it will be easier to deviate from this commitment (Kawamoto, 1997). This can be calledthe `ratchet e!ecta of mutual commitment in a multilateral setting.

5.2. Proposal for a new regulatory agreement

Hence, there are good reasons for following the multilateral track to stronger commitment.Unilateral action can weaken a country's negotiation position. Bilateral talks on liberalising theindustry are prohibited by Article V GATS. Therefore, we suggest the need for new multilateraltalks on telecommunications which will end up in a WTO agreement with stronger commitmentsby all WTO Members.

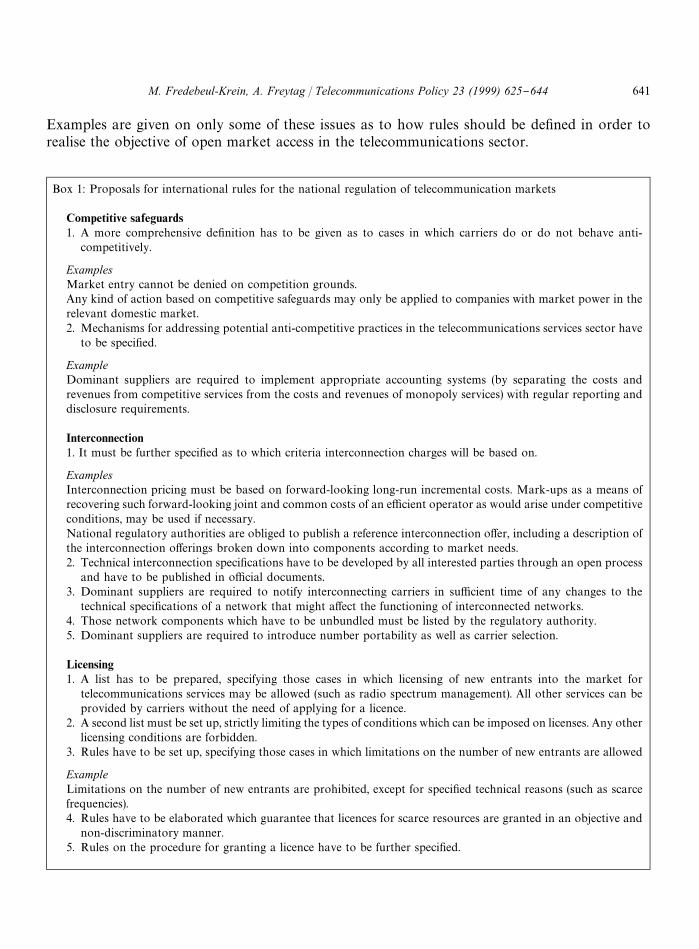

This agreement should consist of more comprehensive rules for a multilateral regulatoryframework on international trade in telecommunications services. Implementing these rules wouldcontribute to overcoming the shortcomings of the current agreement. In order to prevent countriesfrom discriminating against foreign service providers, a future regulatory reference model withinthe WTO should contain more detailed regulatory provisions. As a reference model we thereforesuggest to adopt additional rules to the existing set of guidelines in the coming multilateralnegotiations. Based on the shortcomings of the current Reference Paper as analysed in section two,in the following box we suggest various issues to be addressed by a future negotiation round ontelecommunications services. They are not meant to be detailed regulatory provisions but rathera "rst approximation to a binding international set of rules in telecommunications (see Box 1).29

640 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

Examples are given on only some of these issues as to how rules should be de"ned in order torealise the objective of open market access in the telecommunications sector.

Box 1: Proposals for international rules for the national regulation of telecommunication markets

Competitive safeguards1. A more comprehensive de"nition has to be given as to cases in which carriers do or do not behave anti-

competitively.

ExamplesMarket entry cannot be denied on competition grounds.Any kind of action based on competitive safeguards may only be applied to companies with market power in therelevant domestic market.2. Mechanisms for addressing potential anti-competitive practices in the telecommunications services sector have

to be speci"ed.

ExampleDominant suppliers are required to implement appropriate accounting systems (by separating the costs andrevenues from competitive services from the costs and revenues of monopoly services) with regular reporting anddisclosure requirements.

Interconnection1. It must be further speci"ed as to which criteria interconnection charges will be based on.

ExamplesInterconnection pricing must be based on forward-looking long-run incremental costs. Mark-ups as a means ofrecovering such forward-looking joint and common costs of an e$cient operator as would arise under competitiveconditions, may be used if necessary.National regulatory authorities are obliged to publish a reference interconnection o!er, including a description ofthe interconnection o!erings broken down into components according to market needs.2. Technical interconnection speci"cations have to be developed by all interested parties through an open process

and have to be published in o$cial documents.3. Dominant suppliers are required to notify interconnecting carriers in su$cient time of any changes to the

technical speci"cations of a network that might a!ect the functioning of interconnected networks.4. Those network components which have to be unbundled must be listed by the regulatory authority.5. Dominant suppliers are required to introduce number portability as well as carrier selection.

Licensing1. A list has to be prepared, specifying those cases in which licensing of new entrants into the market for

telecommunications services may be allowed (such as radio spectrum management). All other services can beprovided by carriers without the need of applying for a licence.

2. A second list must be set up, strictly limiting the types of conditions which can be imposed on licenses. Any otherlicensing conditions are forbidden.

3. Rules have to be set up, specifying those cases in which limitations on the number of new entrants are allowed

ExampleLimitations on the number of new entrants are prohibited, except for speci"ed technical reasons (such as scarcefrequencies).4. Rules have to be elaborated which guarantee that licences for scarce resources are granted in an objective and

non-discriminatory manner.5. Rules on the procedure for granting a licence have to be further speci"ed.

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 641

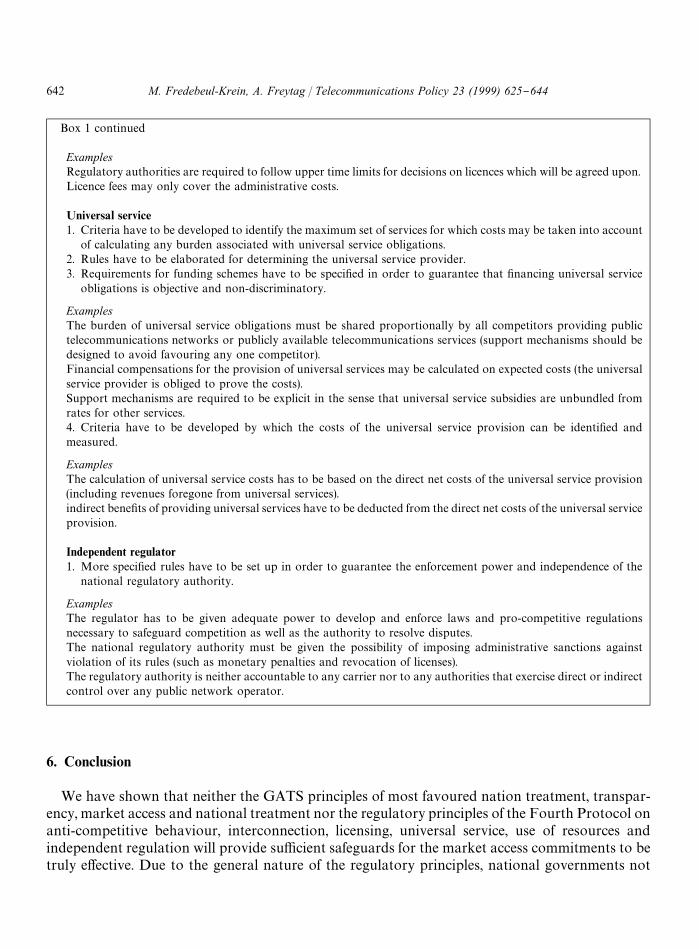

Box 1 continued

ExamplesRegulatory authorities are required to follow upper time limits for decisions on licences which will be agreed upon.Licence fees may only cover the administrative costs.

Universal service1. Criteria have to be developed to identify the maximum set of services for which costs may be taken into account

of calculating any burden associated with universal service obligations.2. Rules have to be elaborated for determining the universal service provider.3. Requirements for funding schemes have to be speci"ed in order to guarantee that "nancing universal service

obligations is objective and non-discriminatory.

ExamplesThe burden of universal service obligations must be shared proportionally by all competitors providing publictelecommunications networks or publicly available telecommunications services (support mechanisms should bedesigned to avoid favouring any one competitor).Financial compensations for the provision of universal services may be calculated on expected costs (the universalservice provider is obliged to prove the costs).Support mechanisms are required to be explicit in the sense that universal service subsidies are unbundled fromrates for other services.4. Criteria have to be developed by which the costs of the universal service provision can be identi"ed andmeasured.

ExamplesThe calculation of universal service costs has to be based on the direct net costs of the universal service provision(including revenues foregone from universal services).indirect bene"ts of providing universal services have to be deducted from the direct net costs of the universal serviceprovision.

Independent regulator1. More speci"ed rules have to be set up in order to guarantee the enforcement power and independence of the

national regulatory authority.

ExamplesThe regulator has to be given adequate power to develop and enforce laws and pro-competitive regulationsnecessary to safeguard competition as well as the authority to resolve disputes.The national regulatory authority must be given the possibility of imposing administrative sanctions againstviolation of its rules (such as monetary penalties and revocation of licenses).The regulatory authority is neither accountable to any carrier nor to any authorities that exercise direct or indirectcontrol over any public network operator.

6. Conclusion

We have shown that neither the GATS principles of most favoured nation treatment, transpar-ency, market access and national treatment nor the regulatory principles of the Fourth Protocol onanti-competitive behaviour, interconnection, licensing, universal service, use of resources andindependent regulation will provide su$cient safeguards for the market access commitments to betruly e!ective. Due to the general nature of the regulatory principles, national governments not

642 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

having introduced rules for e!ective competition on their national markets will still be able to deterforeign companies from entering their telecom markets without violating WTO rules. The varyingincentives governments have to impede market access to foreign carriers make it rather likely thatthis will happen as long as there is no stronger binding WTO agreement on telecommunicationservices.

In those signatory countries which have introduced national regulatory frameworks aimed atreinforcing competition in the telecommunications sector, the market entry of foreign competitorswill give an additional stimulus for competition in national telecom markets. Yet, it has beendemonstrated that even these countries will be able to discriminate against foreign telecommunica-tion operators. Especially unclear and broad licensing criteria, being in line with the commitmentsmade under the Fourth Protocol, allow countries to keep discretion regarding access to theirnational telecom markets.

Public choice reasons make it politically di$cult and (partly) undesirable for governments tocommit themselves unilaterally. Instead, from a government's point of view vagueness andintransparency is very attractive. To join the WTO agreements and to liberalise such a dynamicsector publicly demonstrate that the government is able to handle complex challenges. At the sametime, obstructing foreign "rms entering the domestic markets allows the existing telecommunica-tions lobby to earn rents. If the state is shareholder of the incumbent supplier, it can earn someadditional revenues on the expense of consumers.

Thus, despite the economic bene"ts of unilateral liberalisation there is a case for a newmultilateral agreement on regulatory provision which causes the WTO Members to credibly andstrongly commit themselves to open markets. Having such rules and conditions embodied in aninternational treaty guarantees that they are not subject to frequent or unforeseeable changes atnational level. This is probably the most important advantage of an agreement within the WTO.Stable policy provides a favourable environment for both foreign and domestic investors. In thepast, telecom operators have tended to favour short-term investment opportunities, preciselybecause of the perceived absence of a stable policy environment. To con"rm market openingmeasures in a binding international treaty, helps to assure foreign and domestic investors that thecountry is committed to liberalisation.

Acknowledgements

Financial help by the Friedrich Flick FoK rderungsstiftung is gratefully acknowledged. In addi-tion, we want to thank Juergen B. Donges, JoK rg Mallossek, Hans Willgerodt, Ralf Zimmermannand three anonymous referees for very helpful comments.

References

Albach, H. & Knieps, G. (1997). Kosten und Preise in wettbewerblichen Ortsnetzen. Freiburger Studien zur NetzoK konomie,2, Baden-Baden.

Anderson, K. & Baldwin, R. E. (1981). The political market for protection in industrial countries: Empirical evidence.World Bank Staw Working Papers 492, Washington D.C.

Armstrong, M. (1997). Competition in telecommunications. Oxford Review of Economic Policy, 13, 1.

M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644 643

Brock, G. W., & Katz, M. L. (1997). Regulation to promote competition: A "rst look at the FCC's implementation of thelocal competition provisions of the Telecommunications Act of 1996. Information Economics and Policy, 9, 2.

Bronckers, M., & Larouche, P. (1997). Telecommunications services and the World Trade Organisation. Journal of WorldTrade, 31, 3.

Drake, W. J., & Noam, E. M. (1997). The WTO deal on basic telecommunications. Telecommunications Policy, 21, 9}10.European Commission (1998). Third report on the implementation of the telecommunications regulatory package. Commun-

ication from the Commission to the Council and the European Parliament, Brussels.FCC (1997a). Report and order in the matter of federal-state joint board on universal service. Federal Communications

Commission, FCC 97-157, 5 August.FCC (1997b). Foreign participation order. Federal Communications Commission, FCC 97-398, A 59, 25 November.FCC (1997c). International satellite services order. Federal Communications Commission, FCC 97-399, 25 November.Fredebeul-Krein, M. (1998). Das Universaldienstkonzept der EuropaK ischen Union in der Telekommunikation. Wir-

tschaftsdienst, 78, 8.Fredebeul-Krein, M. (1999). Internationale Regeln fu( r nationale=ettbewerbs- und Regulierungspolitiken auf dem Markt

fu( r ¹elekommunikationsdienste. KoK ln: mimeo.Fredebeul-Krein, M., & Freytag, A. (1997). Telecommunications and WTO discipline. An assessment of the WTO

agreement on telecommunication services. Telecommunications Policy, 21(6), 477}491.Freytag, A. (1995). The European market for protectionism: New competitors and new products. In L. Macmillan,

Gerken, London, & Basingstoke, Competition Among Institutions.Handelsblatt (1998). StaatssekretaK r Stark kritisiert Scheurle. Handelsblatt, 27 April.Hillman, A. L. (1994). ¹he political economy of protection. New York: Harwood Academic Publishers.Kawamoto, A. (1997). Regulatory reform on the international trade policy agenda. Journal of World Trade, 31, 4.Knieps, G. (1997). Costing and pricing of interconnection services in a liberalised European telecommunications market.

Discussion Paper No. 39, Freiburg.Krugman, P. (1997). What should trade negotiators negotiate about? Journal of Economic Literature, 35, 113}120.Noll, A. M. (1998). The costs of competition. FCC telecommunication orders of 1997. Telecommunications Policy, 22, 1.OJE (1997a). Directive 97/13/EC of the European Parliament and of the Council of 10 April 1997 on a common

framework for general authorisations and individual licences in the "eld of telecommunications services. OzcialJournal of the European Communities, May 7 (L 117), Art. 18.

OJE (1997b). Directive 97/33/EC of the European Parliament and of the Council on interconnection in telecommunica-tions with regard to ensuring universal service and interoperability through application of the principles of opennetwork provision (ONP). Ozcial Journal of the European Communities, July 26 (L 199), Annex III.

Prieger, J. (1998). Universal service and the Telecommunications Act of 1996. Telecommunications Policy, 22, 1.Thomas, C. (1996). Litigation process under the GATT dispute settlement system. Journal of World Trade, 30, 2.Tumlir, J. (1985). Protectionism. Washington D.C: American Enterprise Institute for Public Policy Research.Vogelsang, I. (1996). Kosten des Ortsnetzes. HuK rth: mimeo.Vogelsang, I., & Mitchell, B. M. (1997). Telecommunications competition. The last ten miles. Cambridge/MA: The MIT

Press.WTO (1995). The results of the Uruguay Round of Multilateral Trade Negotiations: The legal texts. Geneva.WTO (1998). WTO deal will ring in the changes. Press Release No. 87, Geneva.Xavier, P. (1998). The licensing of telecommunications suppliers. Beyond the EU Directive. Telecommunications Policy,

22, 6.

644 M. Fredebeul-Krein, A. Freytag / Telecommunications Policy 23 (1999) 625}644

Related Documents