4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland 1 Tax transparency and willingness to pay Joaquim Campuzano [email protected] Departament de Sociologia Universitat Autònoma de Barcelona Spain Abstract Transparency has emerged in recent years as an important development in social policy and as a mainstream anti‐corruption and prosocial behavior tool. Transparency enables citizens to develop realistic expectations about what government can and cannot do, and helps them to monitor the concrete performance of government. However, the specific effects of transparency and the precise function it plays in forming perception of fairness and efficiency in government action are still unexplored. The design of information transparency policies may be responding to citizens’ preferences, opinions and attitudes, and at the same time may modify them, thus redefining the policy making process itself. In this paper we try to explore how several dimensions of transparency may have an impact on our willingness to pay taxes, and what kind of information may help tax enforcement and a more equitable operation of the tax system. We use the term “folk transparency” as shorthand for the perspective or perception of transparency of ordinary people. We define tax morale as the intrinsic motivation or internalized willingness to pay taxes. Our problem is how folk transparency may have effects on citizens’ tax morale. To that aim, we adopt a behavioral and informational approach to tax compliance, by which information obtained through transparency measures is expected to generate a ‘virtuous circle’ between trust in the tax system and willingness to comply. We measure tax morale and trust through the proper items from the World Values Survey and the European Values Survey. The main aim is to check whether a high trust in the state and lower corruption perception lead to high tax morale. We use regression analysis using tax morale as a dependent variable and controlling for different factors. We then compare the results with an exploratory analysis on different levels of tax transparency at the national level. Key words: tax transparency, folk transparency, tax morale, tax transparency dimensions.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

1

Tax transparency and willingness to pay

Joaquim Campuzano [email protected]

Departament de Sociologia Universitat Autònoma de Barcelona

Spain

Abstract

Transparency has emerged in recent years as an important development in social

policy and as a mainstream anti‐corruption and prosocial behavior tool.

Transparency enables citizens to develop realistic expectations about what

government can and cannot do, and helps them to monitor the concrete performance

of government. However, the specific effects of transparency and the precise function

it plays in forming perception of fairness and efficiency in government action are still

unexplored. The design of information transparency policies may be responding to

citizens’ preferences, opinions and attitudes, and at the same time may modify them,

thus redefining the policy making process itself.

In this paper we try to explore how several dimensions of transparency may have an

impact on our willingness to pay taxes, and what kind of information may help tax

enforcement and a more equitable operation of the tax system. We use the term “folk

transparency” as shorthand for the perspective or perception of transparency of

ordinary people. We define tax morale as the intrinsic motivation or internalized

willingness to pay taxes. Our problem is how folk transparency may have effects on

citizens’ tax morale. To that aim, we adopt a behavioral and informational approach to

tax compliance, by which information obtained through transparency measures is

expected to generate a ‘virtuous circle’ between trust in the tax system and willingness

to comply.

We measure tax morale and trust through the proper items from the World Values

Survey and the European Values Survey. The main aim is to check whether a high trust

in the state and lower corruption perception lead to high tax morale. We use

regression analysis using tax morale as a dependent variable and controlling for

different factors. We then compare the results with an exploratory analysis on

different levels of tax transparency at the national level.

Key words: tax transparency, folk transparency, tax morale, tax transparency dimensions.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

2

1 Introduction

1.1 Background of modern taxation systems

Taxation systems have been seen as the way in which states have raised revenues, but

also as “the solution to the growing problem of inequality in modern society”

(Pechman 1983; Weber and Widalsky 1986; Witte 1985). A nation's tax system is often

a reflection of its communal values and/or the values of those in power.

As Steinmo (2003) argues, tax policy ideas, beliefs and basic normative preferences

have an important role in selecting between policy alternatives. Those ideas, beliefs

and values are held by public policy actors – being these individual or collective, public,

private or pro‐common – but also by new actors, such as social organizations, new

urban activists and social innovators, based in new governance models, such as

network governance. These new trends and new ideas in public policy making and the

changes experienced by economy – revealing new sources of revenue and new social

services needs which simply did not exist in a pre‐modern economy – challenge us to

evolve our state‐centered taxation systems and institutions.

1.2 Taxation: a question of opinion formation of political elites?

As stated Fung, A., Graham, M., Weil, D., & Fagotto, E. (2004)., “taxation processes are

characterized by information asymmetries that stand in the way of furthering fair,

effective and efficient tax systems. Such imbalances are inevitable because

government tax agencies always have exclusive access to some information and

practices and always have compelling reasons to keep much of it confidential”.

But, such asymmetries are not only related to information accessibility, they may exist

too in the aims of disclosers and users of such information. This is, in our opinion, an

essential premise to take in account in the formulation of fair transparency measures.

In short, both the apparent failure of the political structure to make efficient and fair

use of tax policy and the realities of globalization have ultimately shaped what policy

elites now believe can be done and what ought to be done. Whereas in the middle

decades of this century there was a widespread consensus that taxes should be used

as a social policy instrument that had an essential function in redistributing income

and wealth in capitalist democracies, today there appears to be a growing consensus

(among elites, at least) that taxes should not be used for these purposes (Steinmo

2003).

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

3

2 Theoretical Considerations

2.1 Attitudes towards transparency and publicity applied to taxation

In the area of personal tax transparency, several diverse actions have been taken in

different social and institutional international contexts.

Lately, stand up from the rest, the measures applied by Norway, Sweden and Finland

that for many years have published data on individual taxpayers, level of income and

tax payments, which were echoed by the media.

Similarly, in May 2008 in Italy, the earnings and taxes paid by 38 million taxpayers from

2005 were published in a web site by the Italian Tax Agency (Agenzia delle Entrate).

That caused an important stir in the media about the effect that such action could

have to greater criminal extortion and result in the closure of the site by the Italian

Office for Privacy (Garante per la protezione dei dati personali).

Both situations were criticized on the basis that open publication of personal data can

lead to more criminal extortion and tax snooping.

In October 2010, Christine Lagarde, the Managing Director of the IMF, released to the

Greek Government a list containing approximately 2,000 names of citizens who had

deposits with the Swiss branch of a major bank. A Greek weekly published the list and

this led to the editor of the publication being charged with a criminal offence, for

which he was acquitted.

In June 2012 the Danish Parliament passed laws requiring the publication of the

amount of tax paid by all companies in Denmark (Open Tax Lists). The information

published includes the level of taxable income, utilized tax losses, the estimated tax

payable for the year and the type of tax – whether it is ordinary income tax, co‐

operative tax or tonnage tax. The level of revenue and historical details of tax paid are

not disclosed on the website.

Since the 1970s, it has become a tradition in the United States for American presidents

to release their personal tax returns or at least a statement of their taxation position.

Lately, this public demand for openness and transparency has moved to presidential

candidates. This is subject to significant political scrutiny and public debate.

In the 2012 London Mayoral elections, all three candidates released their personal

income tax returns and there has been considerable political debate on whether the

UK should embrace greater publication of general tax information.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

4

Tax avoidance, in varying degrees and forms, is a common phenomenon in any State,

given that, although the control and surveillance mechanisms are very effective, there

is always some margin for fraud and tax evasion. The start of the investigation of tax

compliance was given by the model developed by Allingham and Sandmo (1972) and,

in parallel, by Srinivasan (1973), based on neoclassical economic theory. This model is

an adaptation of the "economics of crime" by G. Becker (1968), that is, an attempt to

explain deviant behavior in terms of rational choice: individual decides how much of its

income should be declared in terms of the benefit of hiding (given the tax rate) and the

costs of getting caught (given the probability of inspection and the amount of the fine).

In the last four decades, however, numerous studies have gone beyond this model,

exploring the topic in several directions:

(a) Econometric analysis of tax evasion real data (Martínez et al., 2008). However, the

quality of the data used is low, and continue to focus on purely economic factors (Alm

and Jacobson, 2007:5; Kirchler, 2007:183).

(b) Experiments. From the work of Friedland et al. (1978), experiments conducted by

economists and behavioral psychologists have become the most widely used research

technique in the area of tax compliance (Blackwell, 2010), and contribute increasingly

to determine the influence of various factors such as cognitive biases (e.g. Guala and

Mittone, 2002) and framing (Hasseldine and Hite, 2003), shame (Coricelli, 2007), the

effort in obtaining income to declare (Kirchler et al., 2009) or the degree of

participation in the decision process of the rules (Bortolami and Mittone, 2009).

(c) Survey analysis. A considerable number of studies investigate the values and

attitudes of citizens on tax fraud, from the pioneering "financial psychology" of

Schmölders (1965). Thus, in recent years we find, for example, the work of the

Australian school led by V. Braithwaite and, in particular, numerous studies on tax

morale with B. Torgler as its most prominent figure. The latter helped to demonstrate

that tax morale is correlated with demographic variables such as gender (Torgler and

Valev, 2010) and age (Braithwaite et al., 2010), but also with aspects such as trust in

institutions (Torgler, 2003), religiosity (Stack and Kposowa, 2006), nationalism (Prieto

et al., 2006), the perception of inefficiency in public spending (Mocetti and Barone,

2011) or the effective degree of local autonomy (Torgler et al., 2010). In Spain, notably

the works of De Juan (1995), Sanchez and De Juan (1994), the descriptive analysis of

IEF fiscal barometer by Delgado et al. (2001) and the tax morale studies carried out by

Llàcer and Noguera (2011), Alm and Gómez (2008), Prieto et al. (2006) , Alarcón et al.

(2009), Torgler and Martínez Vázquez (2009) and María‐Dolores et al. (2010).

(d) Simulation models based on agents. An incipient and small group of work use

agent‐based models (ABM) to explain tax evasion, giving account of social interaction

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

5

processes and phenomena emergence at an aggregate level: Mittone and Patelli

(2000), Davis et al. (2003), Bloomquist (2004, 2011), Antunes et al. (2006), Korobow et

al. (2007), Zaklan et al. (2009), Szabo et al. (2010). All these models introduce different

types of agents, endowed with adaptive capacity and memory, with a certain degree of

satisfaction in public services, embedded in social networks, etc.

(e) Qualitative research based on interviews, as case studies developed by Sigala et al.

(1999), Adams and Webley (2001), Williams (2005), and Ashby and Webley (2008).

In summary, recently has been assumed that the standard economic approach is

inherently insufficient to account for the phenomenon of tax compliance, and that

psychological, cultural, social, normative, etc. elements must be incorporated (Kirchler,

2007; Nevárez and Bergman, 2005; Fernandez Caínzos, 2006; Alvira et al., 2000).

Meanwhile, "during the current financial and economic crisis, national budgets and tax

systems are under increasing threat and the need for international tax cooperation

and common standards (i.e.," good governance in the tax area ") has become a regular

feature of international discussions. " (Europe Commission, 2009).

Moreover, as Naurin and Lindstedt (2006) discussed, "transparency – the release of

information about institutions that is relevant to assessment – it is a matter of great

concern for contemporary social sciences. In the field of international relations,

transparency has been recognized for its potential to contribute to the efficiency of the

system (Mitchell, 1998; Gosseries, 2006), to reduce the risks of conflict and war

(Schultz, 1998; Fearon, 1995) and as a potential surrogate measure of accountability of

international organizations (Keohane and Nye 2003, Majone 1996). Economists have

increasingly highlighted the crucial role played by the information to prevent market

failures and to achieve an efficient allocation of resources (Stiglitz 2000)."

Naurin and Lindstedt (2006) also highlight the importance of information in other

fields, such as economics, where the principal‐agent problem designates a set of

situations that arise when an economic actor – the principal or hierarch – depends on

the action, or the nature, or moral of another actor – the agent –, over which it does

not have perfect information, i.e. under conditions of asymmetric information (Miller

2005). In political philosophy, one of the major developments in democratic theory in

the last two decades has been the revival of deliberative democracy, where publicity

and the debate openness are central concepts (Elster 1998).

It is not surprising therefore that transparency has been also promoted as one of the

most important medicine against corruption – the misuse of the public function in

exchange for a personal profit – (Montinola and Jackman 2002, 151), Rose‐Ackerman

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

6

(1999), Gerring and Thacker (2004). In the last decade there has been a massive wave

of research and debate on the causes of corruption, driven partly by the growing

awareness that corruption is not only morally unacceptable but also a hindrance to the

development and growth in much of the world (Mauro 1995), Ades and Di Tella (1999),

Sandholtz and Koetzle (2000), Treisman (2000), Montinola and Jackman (2002),

Persson and Tabellini Trebbin (2003), Gerring and Thacker (2004).

Naurin and Lindstedt (2006) argue that making political institutions more transparent

can be an effective method to fight against corruption, but that making only the

information available does not prevent corruption if conditions for publicity and

accountability – such as education, freedom of press and free elections – are weak.

In all the previous scientific literature seems like we see repeated the Bentham’s

classical assertion from his essay “On publicity” on the power of “public eye”: "The

greater the number of temptations to which the exercise of political power is exposed,

the more necessary is it to give to those who possess it, the most powerful reasons for

resisting them. But there is no reason more constant and more universal than the

superintendence of the public" (Bentham 1816 [1999], 29).

Despite concern about transparency in the scientific literature and specifically in

research of corruption, few studies have tried to empirically demonstrate its effects,

let alone applied to the field of taxation.

3 Experts’ transparency and folk transparency

Last October 2013, Steve Sheffrin published his book “Tax Fairness and Folk Justice”. In

this book, the author, “brings together insights from social psychology and philosophy

to reconcile how economists think about tax fairness with how everyone else does”

(Sheffrin 2013). The author argued that many key features of the tax system are best

explained through understanding folk justice concepts and those proposals for tax

legislation ideally should reflect an understanding of both academic research and

public opinion. This book demonstrated how an understanding of "folk justice" can

deepen our understanding of how tax systems actually work and how they might

potentially be reformed.

Tax compliance is for some authors “a social contract between ordinary citizens and

the government rather than a contract among people based upon trust” (Rothstein

2001), this implies that we must analyze and focus on the perception of fairness and

transparency that citizens have from the different dimensions of fairness (in our case

of tax fairness.)

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

7

In our research we use the term “folk transparency” as shorthand for the perspective

or perception of transparency by ordinary people. We also understand for tax morale

of individuals, the "intrinsic motivation" (Feld and Frey, 2002) or "internalized

willingness" to pay taxes (Braithwaite and Ahmed, 2005). Thus, our study on the effect

that transparency, specifically the folk transparency, can have on tax morale focuses

on analyzing the effects that may have (appropriate) transparency measures applied to

taxation on the perceptions held by ordinary people and therefore in their intrinsic

motivation to pay taxes.

From the above, one point of interest in social research is the analysis of the

perception of transparency by citizens, and in this case the different dimensions of tax

transparency and its effects on tax fairness, and specifically in tax morale.

According to Sheffrin (2013) there are “three arguments for making considerations of

folk justice [– in our case the folk transparency –] central to our deliberations of social

policy. First, unless social theories and practices “resonate” with individual psychology,

they are often likely to miss their mark in behavioral comprehension. The gap between

theory and practice in property taxation makes a compelling case for this principle. The

second argument was based on “institutions.” Existing norms and practices in society

will develop and evolve based on individual psychological foundations. The ability to

grasp the logic of these institutions – for example, property tax limitations – will

require a firm understanding of their psychological foundations. Finally, and a bit more

speculatively, ideas of folk justice [– or folk transparency –] and individual psychology

may provide insights into “expert” knowledge. Social evolution has equipped

individuals and societies with special talents for succeeding in social situations; for

example, reading emotions or detecting dishonesty in social contexts. Studying the

foundations of individual folk psychology may provide insights into these realms of

knowledge, enabling us to understand the evolution of social institutions and areas in

which to rely on social expertise.”

4th G

4 T

1. E

v

c

e

m

2. P

o

s

T

3. H

4. V

5. T

w

6. In

d

7. C

b

AICP

tax s

Verti

sales

large

Fig

lobal Confere

The Deter

Exchange Eq

value for th

compliance

exchange e

money’s wo

Process Eq

opportunity

ystems incl

Third, tax ad

Horizontal E

Vertical Equ

Time‐Relate

wealth level

nter‐Group

detriment o

Compliance

basis.

A recomme

ystem, not

ical equity p

s, Social Sec

ely a matte

Inform

ational (I)

gure 1 Tax tran

ence on Transp

rminants o

quity and F

e taxes the

to function

quity. They

orth for the

uity and

to influen

lude safegu

dministrato

Equity and F

ity and Fair

ed Equity an

ls fluctuate

Equity an

f another w

Equity and

ends that e

just the inc

provided by

curity and p

r of percep

Proc

Retr

Distr

•Vertical (D

•Horizonta

nsparency dime

parency Resea

of Tax Mo

Fairness – O

ey pay. For

n effectivel

y must fee

taxes they p

Fairness –

nce how an

uards that p

rs are expec

Fairness – Si

rness – Taxe

nd Fairness –

over time.

nd Fairness

without goo

d Fairness –

equity shou

come tax, an

y progressiv

property tax

ption. Feelin

cedural (P)

ibutive (R)

ributive (D)

Dv)

l (Dh)

ensions

arch

8

orale (2)

4.1

The

Acc

Prin

reit

fair

tax

and

in b

tax

reco

dim

tax

Over the lo

a tax syste

y, taxpayer

el that, in

pay.

– First, po

nd to what

permit taxp

cted to trea

imilarly situ

es are based

– Taxes are

s – No gro

d cause.

– All taxpa

ld be evalu

nd not on a

ve income t

xes. Second

ngs about w

4‐6

Tax tran

e American

ountants,

nciples for

erates its p

ness are es

system, an

d fairness b

both the ma

laws”, (AI

ommends

mensions be

equity and

ong run tax

em based o

rs must hav

the long r

olitical proc

t extent th

ayers to ch

at taxpayers

uated taxpay

d on the ab

e not unduly

oup of tax

yers pay w

uated within

proposal‐b

tax rates m

d, whether

whether a p

6 June, 2015, L

nsparency d

Institute of

in its repo

Tax Equity

position th

sential attr

d recomme

be given du

aking and a

CPA 2007)

that the f

considered

fairness:

payers rece

n the conce

ve a positiv

un, they a

cesses give

ey are tax

allenge the

s with respe

yers are tax

ility to pay.

y distorted

xpayers is

what they o

n the conte

by‐proposal

ay be struc

a tax system

particular a

Lugano, Switz

dimensions

f Certified P

ort on “Gu

y and Fairn

hat “equity

ributes of a

ends that e

ue consider

administrati

. AICPA fu

following s

d in determ

eive approp

ept of volu

ve percepti

are getting

e taxpayer

xed. Second

e taxes asse

ect.

xed similarly

when incom

favored to

owe on a t

ext of the e

basis.

cturally offs

m is equita

aspect of th

erland

s

Public

uiding

ess “

y and

good

equity

ration

on of

urther

seven

mining

priate

ntary

on of

their

rs an

d, tax

essed.

y.

me or

o the

imely

entire

set by

ble is

he tax

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

9

system is fair or unfair are influenced by prior experiences and information (or

misinformation).

The report published by AICPA (2001), “Guiding Principles of Good Tax Policy: a

Framework for Evaluating Tax Proposals” lays out ten principles of good tax policy:

Equity and Fairness ‐ Similarly situated taxpayers should be taxed similarly.

Certainty ‐ The tax rules should clearly specify when the tax is to be paid, how it

is to be paid, and how the amount to be paid is to be determined.

Convenience of Payment ‐ A tax should be due at a time or in a manner that is

most likely to be convenient for the taxpayer.

Economy in Collection ‐ The costs to collect a tax should be kept to a minimum

for both the government and taxpayers.

Simplicity ‐ The tax law should be simple so that taxpayers can understand the

rules and comply with them correctly and in a cost‐efficient manner.

Neutrality ‐ The effect of the tax law on a taxpayer’s decisions as to how to

carry out a particular transaction or whether to engage in a transaction should

be kept to a minimum.

Economic Growth and Efficiency ‐ The tax system should not impede or reduce

the productive capacity of the economy.

Transparency and Visibility ‐ Taxpayers should know that a tax exists and how

and when it is imposed upon them and others.

Minimum Tax Gap ‐ tax should be structured to minimize non‐compliance.

Appropriate Government Revenues – The tax system should enable the

government to determine how much tax revenue will likely be collected and

when.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

10

1 Adam Smith – An Inquiry into the Nature and Wealth of Nations 2 Council of Economic Advisors – Economic Report of the President

3 Joint Economic Committee, Study by Vedder & Galloway – Some Underlying Principles of Tax Policy.

4 American Institute of Certified Public Accountants – Tax Policy Concept Statement No. 1, Guiding Principles for Good Tax Policy: A Framework for Evaluating Tax Proposals

5 Institute for Policy Innovation, Study by Hunter & Entin – A Framework for Tax Reform.

6 Government Accountability Office – Understanding the Tax Reform Debate: Background, Criteria and Questions.

Adam Smith1

1776

CEA2

1996

JEC3

1998

AICPA4

2001

IPI5

2005

GAO6

2005

Equality Fairness Fair Equity and

Fairness

Fairness Equity

Certainty Certainty

Convenience of

Payment

Convenience of

Payment

Economy in

Collection

Economy of

Collection

Simplicity Simplicity Simplicity Simplicity

Neutral

Economic Impact

Neutrality Neutrality

Economic

Efficiency

Economic Growth

and Efficiency

Economic

Efficiency

Transparent Transparency and

Visibility

Visibility Transparency

Tax Avoidance

Difficult and

Risky

Minimum Tax Gap

Appropriate

Government

Revenues

Not Costly to

Administer

Administrability

Not Costly to

Calculate

Table 1 Desirable attributes for a Tax System from Tax Policy Concept Statement No. 4

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

11

“Tax Policy Concept Statement No. 4 identifies and defines seven “dimensions” that

should be considered when assessing tax equity and fairness. This approach requires

the collection and analysis of an extensive amount of information. With the possible

exception of vertical equity, the measurements for these dimensions will be based on

soft data that are influenced by individual perceptions. When the data are analyzed,

the relative importance of the equity and fairness dimensions, as well as possible

interactions among dimensions, will depend on the scenario being considered and the

critical perspective of the analyst. This does not mean that the task is impossible, but it

is challenging.

AICPA hopes that this Statement will: (1) challenge tax lawmakers to more fully

consider the importance and scope of tax equity and fairness; (2) encourage tax

administrators to strive for enhanced public perceptions of tax equity and fairness; (3)

provide a useful framework for tax policy advocates and students; and (4) motivate

academic researchers to develop the measures and models needed to empirically

address equity and fairness issues.” (AICPA 2007)

4.2 Tax transparency measurement

4.2.1 Expert‐based indicators

Main indicators used to analyze the effects of lack of transparency – and other factors

producing corruption – such as Corruption Perceptions Index (CPI) by Transparency

International, and to enhance the quality of taxation policies and systems – such as the

Worldwide Governance Indicators (WGI) by World Bank, rely on expert‐based

judgements

The WGI compile and summarize information from 32 existing data sources that report

the views and experiences of citizens, entrepreneurs, and experts in the public, private

and NGO sectors from around the world, on the quality of various aspects of

governance.

WGI draw on four different types of source data: Surveys of households and firms (9

data sources including the Afrobarometer surveys, Gallup World Poll, and Global

Competitiveness Report survey); Commercial business information providers (4 data

sources including the Economist Intelligence Unit, Global Insight, Political Risk

Services); Non‐governmental organizations (11 data sources including Global Integrity,

Freedom House, Reporters Without Borders); and Public sector organizations (8 data

sources including the CPIA assessments of World Bank and regional development

banks, the EBRD Transition Report, French Ministry of Finance Institutional Profiles

Database).

WGI data sources are 70% based on experts and 30% based on surveys. Only two of

the survey based sources – the World Economic Forum Global Competitiveness Report

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

12

and the Gallup World Poll – are representative. That means that only the 16% of

representative sources used by WGI are based on surveys.

The 2013 CPI draws on data sources from independent institutions specializing in

governance and business climate analysis. The sources of information used for the

2013 CPI are based on data gathered in the past 24 months. CPI includes only sources

that provide a score for a set of countries/territories and that measure perceptions of

corruption in the public sector. Transparency International reviews the methodology of

each data source in detail to ensure that the sources used meet Transparency

International’s quality standards.

CPI data sources are also 70% based on experts and 30% based on surveys. None of

the four survey based sources are representative – all of them are based on senior or

middle management business executives’ opinions.

4.2.2 Survey (non‐expert) based indicators

The European Social Survey (ESS) is an academically driven cross‐national survey that

has been conducted every two years across Europe since 2001. The ESS questionnaire

consists of a collection of questions that can be classified into two main parts – a core

section and a rotating section. In addition, to the core section there is a supplementary

section, which contains the 21‐item human values scale as well as experimental tests.

Sampling on the ESS is guided by the requirements outlined in the Specification for

Participating countries and the following key principals:

Samples must be representative of all persons aged 15 and over (no upper age

limit) resident within private households in each country, regardless of their

nationality, citizenship or language

Individuals are selected by strict random probability methods at every stage

Sampling frames of individuals, households and addresses may be used

All countries must aim for a minimum 'effective achieved sample size' of 1,500 or

800 in countries with ESS populations of less than 2 million after discounting for

design effects

Quota sampling is not permitted at any stage

Substitution of non‐responding households or individuals (whether 'refusals', 'non‐

contacts' or 'ineligibles') is not permitted at any stage

Based on the AICPA (2001) paper on evaluation of tax proposals, AICPA (2007) paper

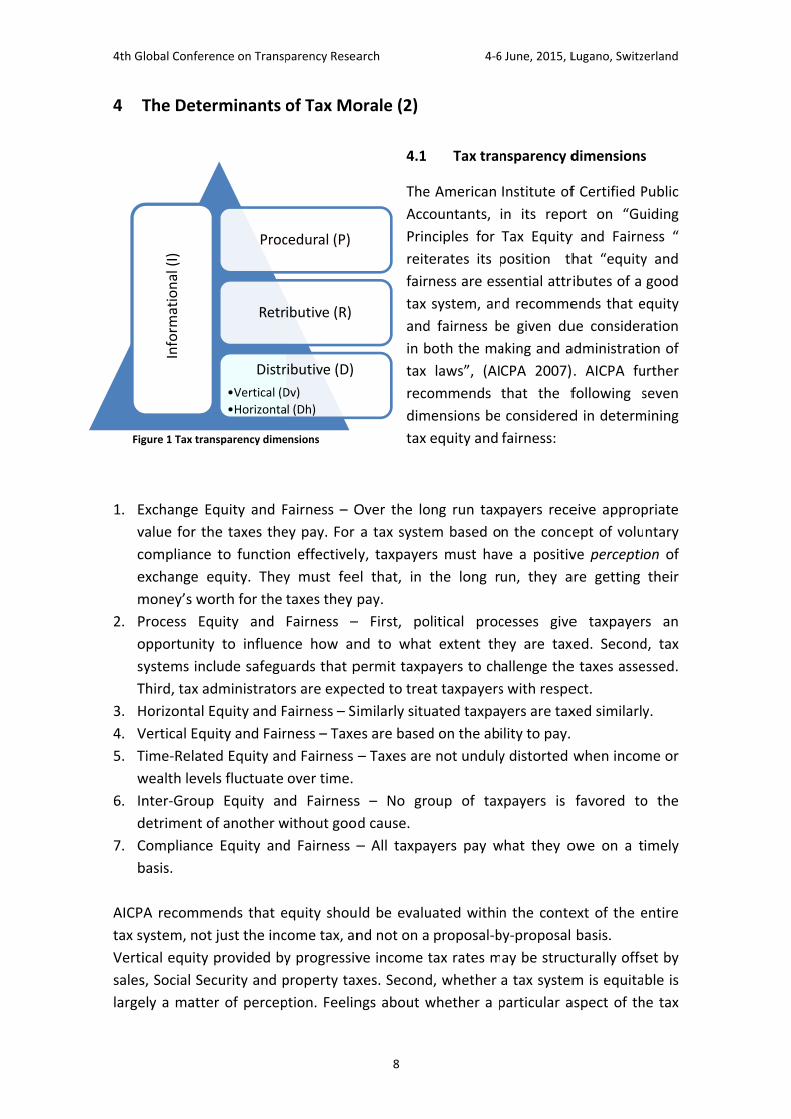

on tax equity and fairness, the definition of folk transparency, and the tax transparency

dimensions analyzed in this paper, we propose our model of tax transparency

framework (Figure 1), making a classification of the proposed measures or indicators

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

13

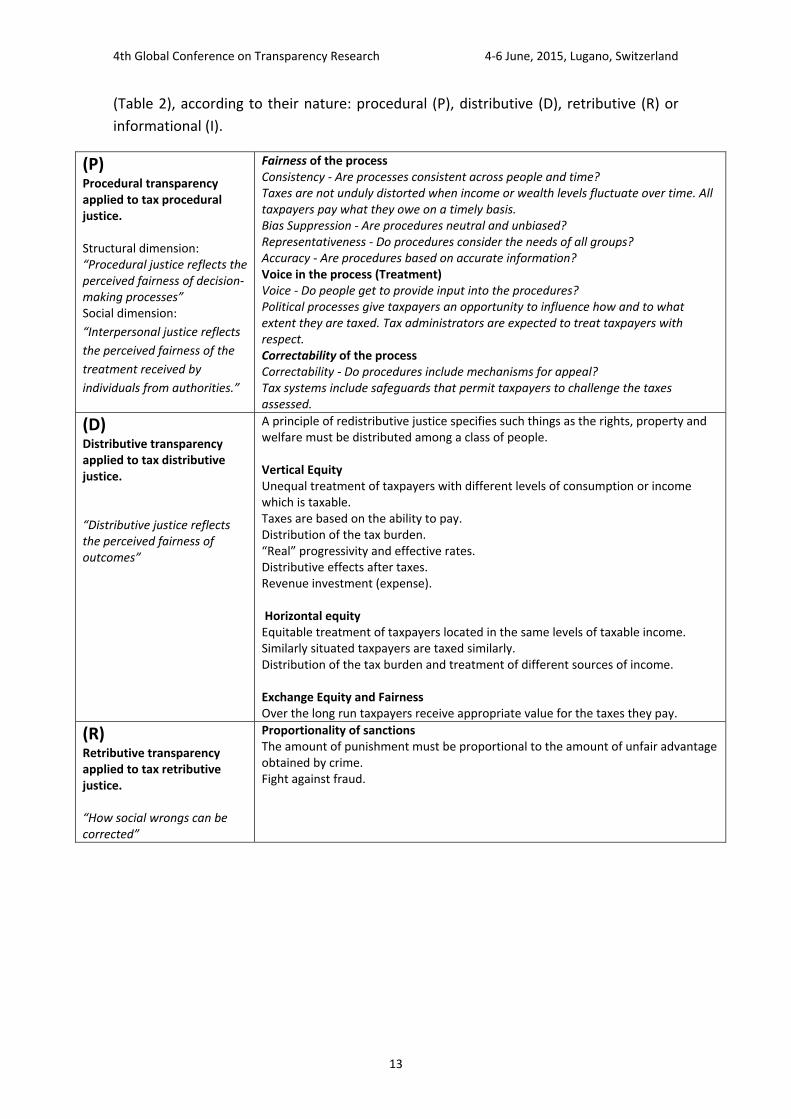

(Table 2), according to their nature: procedural (P), distributive (D), retributive (R) or

informational (I).

(P) Procedural transparency applied to tax procedural justice. Structural dimension: “Procedural justice reflects the perceived fairness of decision‐making processes” Social dimension:

“Interpersonal justice reflects

the perceived fairness of the

treatment received by

individuals from authorities.”

Fairness of the processConsistency ‐ Are processes consistent across people and time? Taxes are not unduly distorted when income or wealth levels fluctuate over time. All taxpayers pay what they owe on a timely basis. Bias Suppression ‐ Are procedures neutral and unbiased? Representativeness ‐ Do procedures consider the needs of all groups? Accuracy ‐ Are procedures based on accurate information? Voice in the process (Treatment) Voice ‐ Do people get to provide input into the procedures? Political processes give taxpayers an opportunity to influence how and to what extent they are taxed. Tax administrators are expected to treat taxpayers with respect. Correctability of the process Correctability ‐ Do procedures include mechanisms for appeal? Tax systems include safeguards that permit taxpayers to challenge the taxes assessed.

(D) Distributive transparency applied to tax distributive justice. “Distributive justice reflects the perceived fairness of outcomes”

A principle of redistributive justice specifies such things as the rights, property and welfare must be distributed among a class of people. Vertical Equity Unequal treatment of taxpayers with different levels of consumption or income which is taxable. Taxes are based on the ability to pay. Distribution of the tax burden. “Real” progressivity and effective rates. Distributive effects after taxes. Revenue investment (expense). Horizontal equity Equitable treatment of taxpayers located in the same levels of taxable income. Similarly situated taxpayers are taxed similarly. Distribution of the tax burden and treatment of different sources of income. Exchange Equity and Fairness Over the long run taxpayers receive appropriate value for the taxes they pay.

(R) Retributive transparency applied to tax retributive justice. “How social wrongs can be corrected”

Proportionality of sanctionsThe amount of punishment must be proportional to the amount of unfair advantage obtained by crime. Fight against fraud.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

14

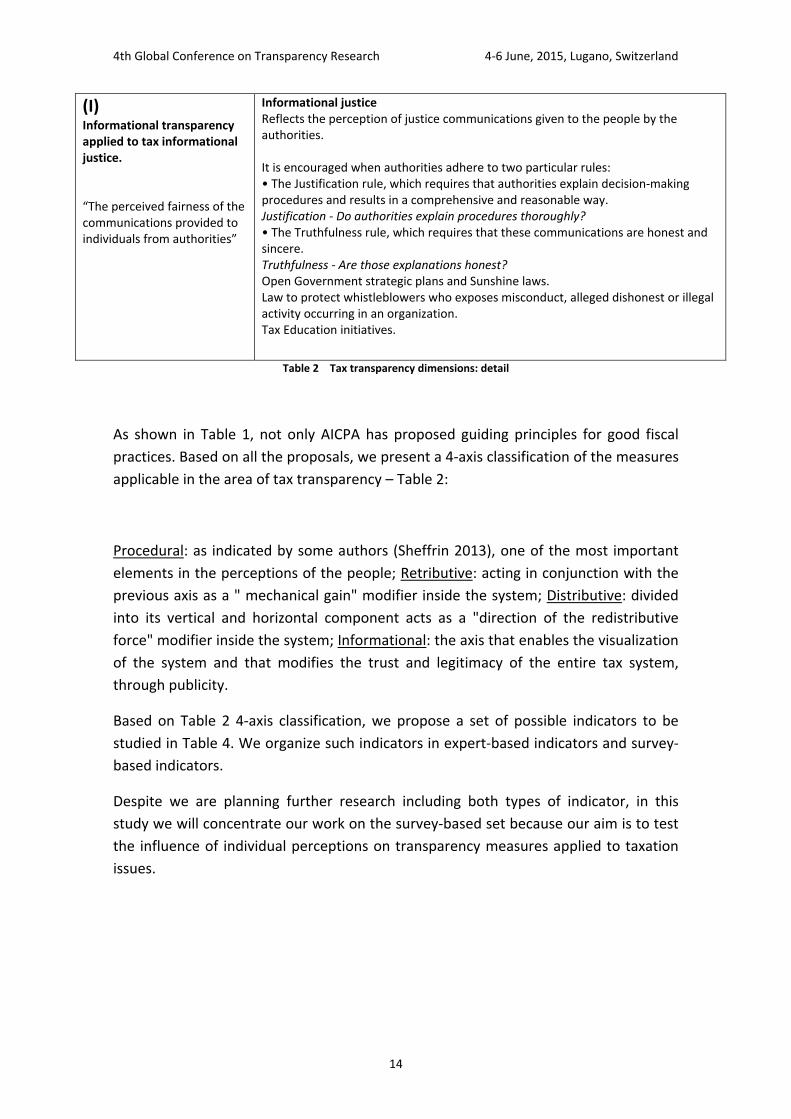

(I) Informational transparency applied to tax informational justice. “The perceived fairness of the communications provided to individuals from authorities”

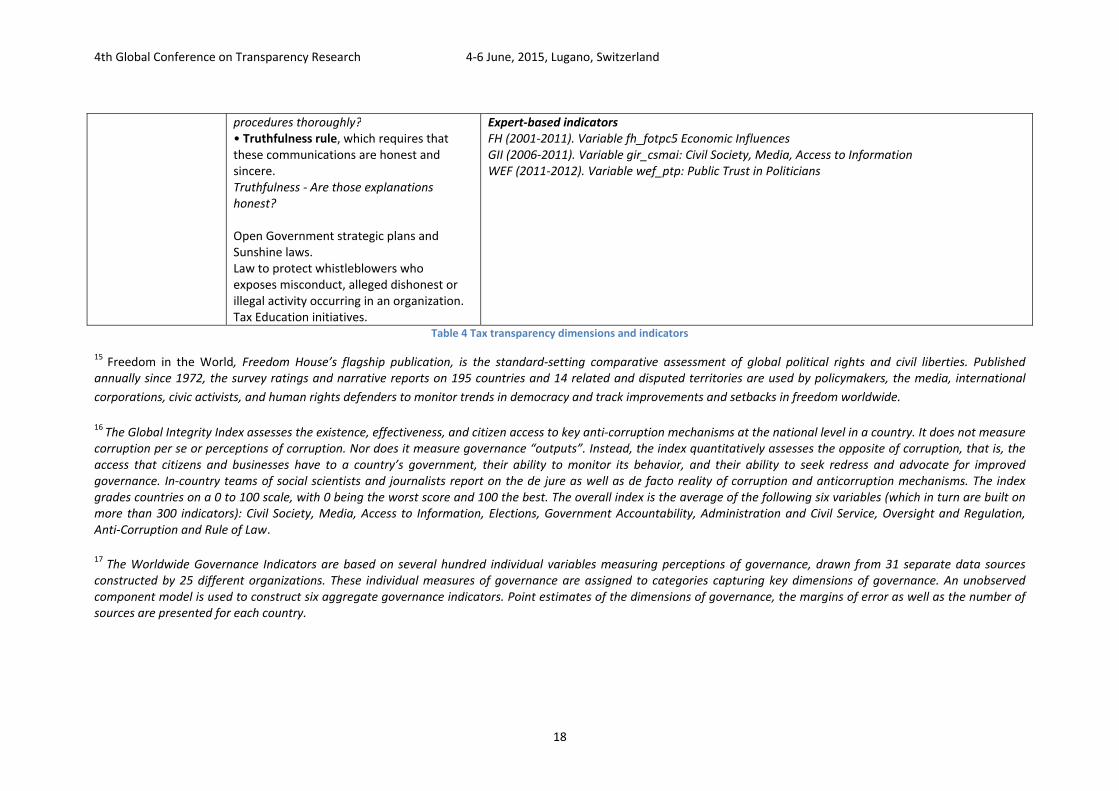

Informational justiceReflects the perception of justice communications given to the people by the authorities. It is encouraged when authorities adhere to two particular rules: • The Justification rule, which requires that authorities explain decision‐making procedures and results in a comprehensive and reasonable way. Justification ‐ Do authorities explain procedures thoroughly? • The Truthfulness rule, which requires that these communications are honest and sincere. Truthfulness ‐ Are those explanations honest? Open Government strategic plans and Sunshine laws. Law to protect whistleblowers who exposes misconduct, alleged dishonest or illegal activity occurring in an organization. Tax Education initiatives.

Table 2 Tax transparency dimensions: detail

As shown in Table 1, not only AICPA has proposed guiding principles for good fiscal

practices. Based on all the proposals, we present a 4‐axis classification of the measures

applicable in the area of tax transparency – Table 2:

Procedural: as indicated by some authors (Sheffrin 2013), one of the most important

elements in the perceptions of the people; Retributive: acting in conjunction with the

previous axis as a " mechanical gain" modifier inside the system; Distributive: divided

into its vertical and horizontal component acts as a "direction of the redistributive

force" modifier inside the system; Informational: the axis that enables the visualization

of the system and that modifies the trust and legitimacy of the entire tax system,

through publicity.

Based on Table 2 4‐axis classification, we propose a set of possible indicators to be

studied in Table 4. We organize such indicators in expert‐based indicators and survey‐

based indicators.

Despite we are planning further research including both types of indicator, in this

study we will concentrate our work on the survey‐based set because our aim is to test

the influence of individual perceptions on transparency measures applied to taxation

issues.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

15

Dimensions Essential attributes Possible Indicators

(P) Procedural transparency applied to tax procedural justice Structural dimension: “Procedural justice reflects the perceived fairness of decision‐making processes” Social dimension:

“Interpersonal justice

reflects the perceived

fairness of the

treatment received by

individuals from

authorities.”

Fairness of the processConsistency ‐ Are processes consistent across people and time? Taxes are not unduly distorted when income or wealth levels fluctuate over time. All taxpayers pay what they owe on a timely basis. Bias Suppression ‐ Are procedures neutral and unbiased? Representativeness ‐ Do procedures consider the needs of all groups? Accuracy ‐ Are procedures based on accurate information? Voice in the process (Treatment) Voice ‐ Do people get to provide input into the procedures? Political processes give taxpayers an opportunity to influence how and to what extent they are taxed. Tax administrators are expected to treat taxpayers with respect. Correctability of the process Correctability ‐ Do procedures include mechanisms for appeal? Tax systems include safeguards that permit taxpayers to challenge the taxes assessed.

Global ‐ Expert‐based indicatorsFreedom House15 (FH) (2009). Variable fh_fog: Functioning of Government Global Integrity Index16 (2006‐2011). Variable gir_gii: gir_ga: Government Accountability Global Integrity Index (2006‐2011). Variable gir_e: Elections Global Integrity Index (2006‐2011). Variable gir_acs: Administration and Civil Service Global Integrity Index (2006‐2011). Variable gir_or: Oversight and Regulation Workd Bank‐ Worldwide Governance Indicators17 (WGI) (2009): Variable wbgi_gee: Government Effectiveness (Estimate) Workd Bank‐ WGI (2009): Variable wbgi_ges: Government Effectiveness (Standard Errors) Workd Bank‐ WGI (2009): Variable wbgi_gen: Government Effectiveness (Number of Sources) Consistency Bias suppression Survey‐based indicators

ESS418 (2008): Welfare attitudes. Variable txadleq: Tax authorities give special advantages or deal with everyone equally Expert‐based indicators Workd Bank‐ WGI (2009): Variable wbgi_cce: Control of Corruption (Estimate) Workd Bank‐ WGI (2009): Variable wbgi_ccs: Control of Corruption (Standard Errors) Workd Bank‐ WGI (2009): Variable wbgi_ccn: Control of Corruption (Number of Sources) World Economic Forum19 (WEF) (2011.2012). Variable wef_fgo Favoritism in Decisions of Government Officials Representativeness Expert‐based indicators WEF (2011.2012). Variable wef_ji: Judicial Independence WEF (2011.2012). Variable wef_tgp: Transparency of Government Policymaking WEF (2011.2012). Variable wef_bgr: Burden of Government Regulation Accuracy Survey‐based indicators ESS4 (2008): Welfare attitudes. Variable txautef: Tax authorities, how efficient in doing their job

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

16

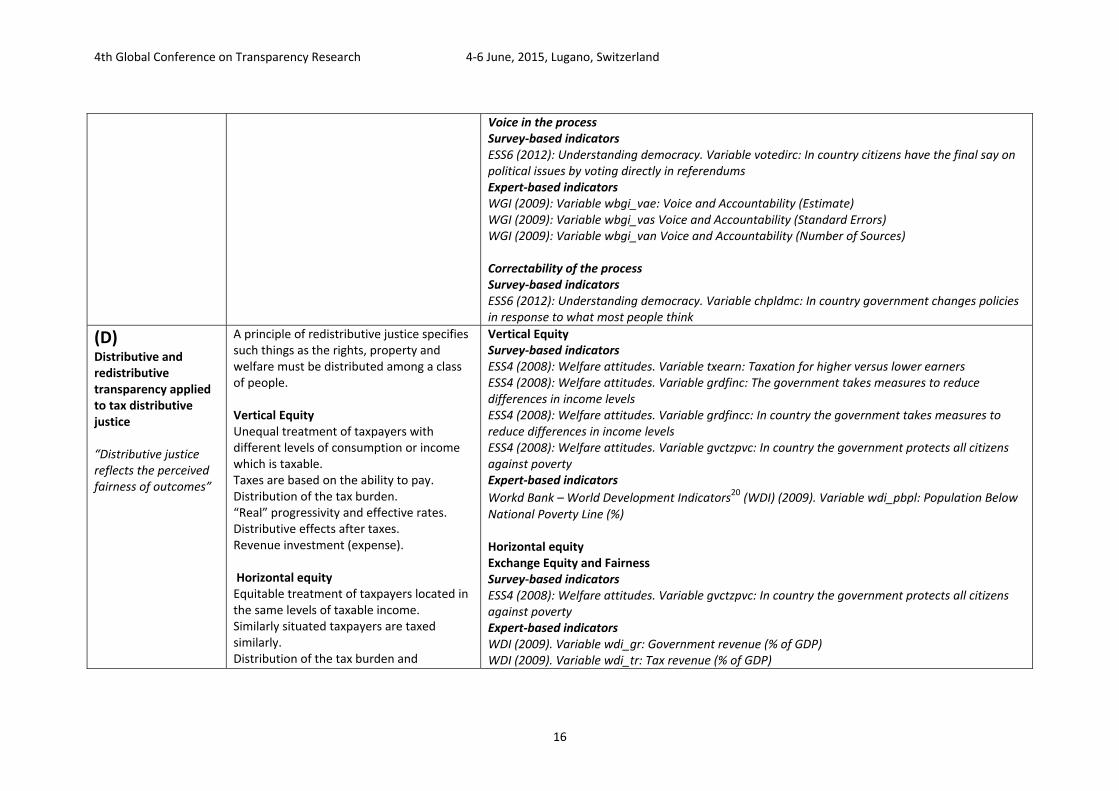

Voice in the processSurvey‐based indicators ESS6 (2012): Understanding democracy. Variable votedirc: In country citizens have the final say on political issues by voting directly in referendums Expert‐based indicators WGI (2009): Variable wbgi_vae: Voice and Accountability (Estimate) WGI (2009): Variable wbgi_vas Voice and Accountability (Standard Errors) WGI (2009): Variable wbgi_van Voice and Accountability (Number of Sources) Correctability of the process Survey‐based indicators ESS6 (2012): Understanding democracy. Variable chpldmc: In country government changes policies in response to what most people think

(D) Distributive and redistributive transparency applied to tax distributive justice “Distributive justice reflects the perceived fairness of outcomes”

A principle of redistributive justice specifies such things as the rights, property and welfare must be distributed among a class of people. Vertical Equity Unequal treatment of taxpayers with different levels of consumption or income which is taxable. Taxes are based on the ability to pay. Distribution of the tax burden. “Real” progressivity and effective rates. Distributive effects after taxes. Revenue investment (expense). Horizontal equity Equitable treatment of taxpayers located in the same levels of taxable income. Similarly situated taxpayers are taxed similarly. Distribution of the tax burden and

Vertical EquitySurvey‐based indicators ESS4 (2008): Welfare attitudes. Variable txearn: Taxation for higher versus lower earners ESS4 (2008): Welfare attitudes. Variable grdfinc: The government takes measures to reduce differences in income levels ESS4 (2008): Welfare attitudes. Variable grdfincc: In country the government takes measures to reduce differences in income levels ESS4 (2008): Welfare attitudes. Variable gvctzpvc: In country the government protects all citizens against poverty Expert‐based indicators

Workd Bank – World Development Indicators20 (WDI) (2009). Variable wdi_pbpl: Population Below National Poverty Line (%) Horizontal equity Exchange Equity and Fairness Survey‐based indicators ESS4 (2008): Welfare attitudes. Variable gvctzpvc: In country the government protects all citizens against poverty Expert‐based indicators WDI (2009). Variable wdi_gr: Government revenue (% of GDP) WDI (2009). Variable wdi_tr: Tax revenue (% of GDP)

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

17

treatment of different sources of income. Exchange Equity and Fairness Over the long run taxpayers receive appropriate value for the taxes they pay.

WDI (2009). Variable wdi_ge: Government Expense (% of GDP) WEF (2011‐2012). Variable wef_wgs: Wastefulness of Government Spending WEF (2011‐2012). Variable wef_tax: Total Tax Rate (%)

(R) Retributive transparency applied to tax retributive justice “How social wrongs can be corrected”

Proportionality of sanctionsThe amount of punishment must be proportional to the amount of unfair advantage obtained by crime. Fight against fraud.

Proportionality of sanctions Survey‐based indicators ESS5 (2010): Justice. Variable ctfrdc: How often the courts make fair, impartial decisions based on available evidence ESS5 (2010): Justice. Variable cttresa: The courts treat everyone the same ESS5 (2010): Justice. Variable cttresac: In country the courts treat everyone the same ESS5 (2010): Justice. Variable ctinplt: The courts' decisions are unduly influenced by political pressure ESS5 (2010): Justice. Variable wraccrp: More likely to be found guilty: Rich or poor falsely accused of crime ESS5 (2010): Justice. Variable ctprpwr: Courts protect rich and powerful over ordinary people Expert‐based indicators

World Bank ‐ Global Integrity Index21 (GII) (2006‐2011). Variable gir_acrl: Anti‐Corruption and Rule of Law WGI (2009): Variable wbgi_rle: Rule of Law (Estimate) WGI (2009): Variable wbgi_rls: Rule of Law (Standard Errors) WGI (2009): Variable wbgi_rln: Rule of Law (Number of Sources)

(I) Informational transparency applied to tax informational justice “The perceived fairness of the communications provided to individuals from authorities”

Informational justiceReflects the perception of justice communications given to the people by the authorities. It is encouraged when authorities adhere to two particular rules: • Justification rule, which requires that authorities explain decision‐making procedures and results in a comprehensive and reasonable way. Justification ‐ Do authorities explain

Informational justice Survey‐based indicators ESS6 (2012): Understanding democracy. Variable meprinfc: In country the media provide citizens with reliable information to judge the government Justification rule ESS6 (2012): Understanding democracy. Variable gvexpdcc: In country the government explains its decisions to voters Truthfulness rule

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

18

procedures thoroughly?• Truthfulness rule, which requires that these communications are honest and sincere. Truthfulness ‐ Are those explanations honest? Open Government strategic plans and Sunshine laws. Law to protect whistleblowers who exposes misconduct, alleged dishonest or illegal activity occurring in an organization. Tax Education initiatives.

Expert‐based indicators FH (2001‐2011). Variable fh_fotpc5 Economic Influences GII (2006‐2011). Variable gir_csmai: Civil Society, Media, Access to Information WEF (2011‐2012). Variable wef_ptp: Public Trust in Politicians

Table 4 Tax transparency dimensions and indicators

15 Freedom in the World, Freedom House’s flagship publication, is the standard‐setting comparative assessment of global political rights and civil liberties. Published annually since 1972, the survey ratings and narrative reports on 195 countries and 14 related and disputed territories are used by policymakers, the media, international

corporations, civic activists, and human rights defenders to monitor trends in democracy and track improvements and setbacks in freedom worldwide.

16 The Global Integrity Index assesses the existence, effectiveness, and citizen access to key anti‐corruption mechanisms at the national level in a country. It does not measure corruption per se or perceptions of corruption. Nor does it measure governance “outputs”. Instead, the index quantitatively assesses the opposite of corruption, that is, the access that citizens and businesses have to a country’s government, their ability to monitor its behavior, and their ability to seek redress and advocate for improved governance. In‐country teams of social scientists and journalists report on the de jure as well as de facto reality of corruption and anticorruption mechanisms. The index grades countries on a 0 to 100 scale, with 0 being the worst score and 100 the best. The overall index is the average of the following six variables (which in turn are built on more than 300 indicators): Civil Society, Media, Access to Information, Elections, Government Accountability, Administration and Civil Service, Oversight and Regulation, Anti‐Corruption and Rule of Law. 17 The Worldwide Governance Indicators are based on several hundred individual variables measuring perceptions of governance, drawn from 31 separate data sources constructed by 25 different organizations. These individual measures of governance are assigned to categories capturing key dimensions of governance. An unobserved component model is used to construct six aggregate governance indicators. Point estimates of the dimensions of governance, the margins of error as well as the number of sources are presented for each country.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

19

18 The European Social Survey (ESS) is an academically driven cross‐national survey that has been conducted every two years across Europe since 2001. The ESS questionnaire

consists of a collection of questions that can be classified into two main parts – a core section and a rotating section. In addition, to the core section there is

a supplementary section, which contains the 21‐item human values scale as well as experimental tests.

19 The World Economic Forum (WEF) is a Swiss nonprofit foundation, based in Cologny, Geneva. It describes itself as an independent international organization committed to

improving the state of the world by engaging business, political, academic, and other leaders of society to shape global, regional, and industry agendas.The Global

Competitiveness Report 2014 ‐ 2015 assesses the competitiveness landscape of 144 economies, providing insight into the drivers of their productivity and prosperity. The

Report series remains the most comprehensive assessment of national competitiveness worldwide.

20 World Development Indicators (WDI) is the primary World Bank collection of development indicators, compiled from officially recognized international sources. It presents

the most current and accurate global development data available, and includes national, regional and global estimates.

21 The Global Integrity Index assesses the existence, effectiveness, and citizen access to key anti‐corruption mechanisms at the national level in countries. It does not measure

corruption or perceptions of corruption. Instead the index is an entry point for understanding the anti‐corruption and good governance mechanisms in place in a country that

should ideally help to prevent, deter, or punish corruption.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

20

5 Empirical Approach

5.1 Data Sources

All individual‐level variables are derived from the World Values Survey (WVS 2015) and the European Values Survey (EVS 2011). WVS/EVS is the most common data source in tax morale research. “The WVS is the largest non‐commercial, cross‐national, time series investigation of human beliefs and values ever executed, currently including interviews with almost 400,000 respondents. Moreover the WVS is the only academic study covering the full range of global variations, from very poor to very rich countries, in all of the world’s major cultural zones”. (Inglehart n.d.). We employ an integrated data file provided by the WVS data archive in collaboration with EVS (ZA4804: EVS 1981‐2008 Longitudinal Data File) and make use of the 4th wave 2008‐2010 included in the data file. Our analysis is restricted to relative homogeneous European countries. Due to missing data some of the OECD countries had to be excluded. In the end, 19 countries remain in the analysis: Belgium, Czech Republic, Denmark, Finland, France, Germany, Hungary, Ireland, the Netherlands, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, Switzerland, Ukraine and the United Kingdom. The country‐level transparency measures are derived from the European Social Survey (ESS). The European Social Survey (ESS) is an academically driven cross‐national survey that has been conducted every two years across Europe since 2001. The survey measures the attitudes, beliefs and behavior patterns of diverse populations in more than thirty nations. ESS consists of core and rotating modules (themes), including the ones we use: the ESS4 (2008) module on welfare concerns the attitudes towards, and perceptions and evaluations of welfare policies in the broad sense. More specifically, it focuses on attitudes towards welfare provision, size of claimant groups, views on taxation, attitudes towards service delivery and likely future dependence on welfare. The aim of the module is to provide essential input into the interdisciplinary field of comparative studies of welfare state attitudes, to address important everyday‐life concerns by citizens, and to offer critical insights of the public legitimacy of welfare state reform; the ESS5 (2010) module that examines public trust in criminal justice and in particular in the police and the courts. Public trust in justice is crucial to the rule of law and governments need good survey‐based indicators of this trust; and the ESS6 (2012) module on democracy focused on people’s beliefs and expectations about what a democracy should be and in people’s evaluations of their own democracies.

5.2 Operationalization

5.2.1 Dependent Variable: Tax Morale

Our dependent variable tax morale is measured on the micro‐level and is derived from the WVS. The question covering tax morale is: Please tell me for the following statement whether you think it can always be justified, never be justified, or something in between: ’Cheating on taxes if you have the chance’.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

21

This question has been used very frequently in the literature to capture tax morale.

The measurement of tax morale is not free of bias, because the available data from

surveys are based on self‐reports and the respondents may tend to overstate their

degree of compliance (Andreoni et al. 1998). However, the question used in WVS is

expected to have a higher degree of honesty because it is defined less sensitive than

directly asking if a person has evaded taxes (Frey and Torgler 2007).

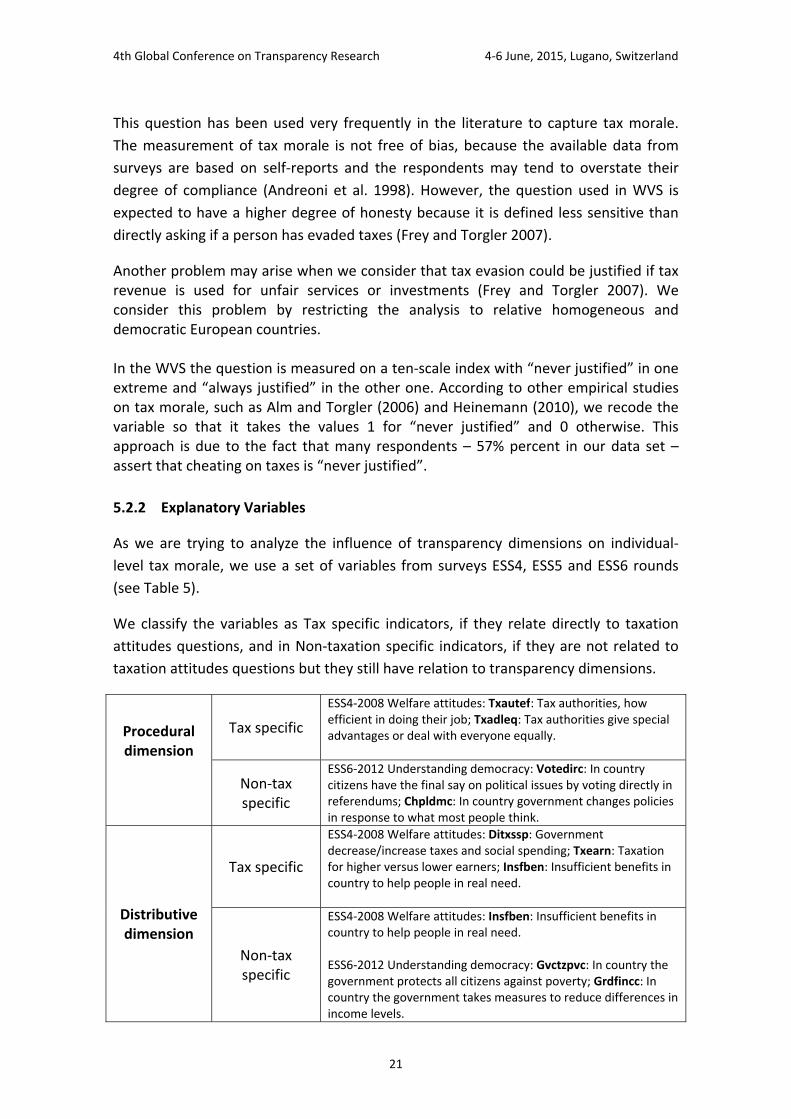

Another problem may arise when we consider that tax evasion could be justified if tax revenue is used for unfair services or investments (Frey and Torgler 2007). We consider this problem by restricting the analysis to relative homogeneous and democratic European countries. In the WVS the question is measured on a ten‐scale index with “never justified” in one extreme and “always justified” in the other one. According to other empirical studies on tax morale, such as Alm and Torgler (2006) and Heinemann (2010), we recode the variable so that it takes the values 1 for “never justified” and 0 otherwise. This approach is due to the fact that many respondents – 57% percent in our data set – assert that cheating on taxes is “never justified”.

5.2.2 Explanatory Variables

As we are trying to analyze the influence of transparency dimensions on individual‐

level tax morale, we use a set of variables from surveys ESS4, ESS5 and ESS6 rounds

(see Table 5).

We classify the variables as Tax specific indicators, if they relate directly to taxation

attitudes questions, and in Non‐taxation specific indicators, if they are not related to

taxation attitudes questions but they still have relation to transparency dimensions.

Procedural dimension

Tax specific

ESS4‐2008 Welfare attitudes: Txautef: Tax authorities, how efficient in doing their job; Txadleq: Tax authorities give special advantages or deal with everyone equally.

Non‐tax specific

ESS6‐2012 Understanding democracy: Votedirc: In country citizens have the final say on political issues by voting directly in referendums; Chpldmc: In country government changes policies in response to what most people think.

Distributive dimension

Tax specific

ESS4‐2008 Welfare attitudes: Ditxssp: Government decrease/increase taxes and social spending; Txearn: Taxation for higher versus lower earners; Insfben: Insufficient benefits in country to help people in real need.

Non‐tax specific

ESS4‐2008 Welfare attitudes: Insfben: Insufficient benefits in country to help people in real need. ESS6‐2012 Understanding democracy: Gvctzpvc: In country the government protects all citizens against poverty; Grdfincc: In country the government takes measures to reduce differences in income levels.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

22

Retributive dimension

Non‐tax specific

ESS5‐2010 Justice: Ctjbcnt: Courts doing good or bad job in country; Ctfrdc: How often the courts make fair, impartial decisions based on available evidence; Wraccrp: More likely to be found guilty: Rich or poor falsely accused of crime; Jdgcbrb: How often judges in country take bribes; Ctprpwr: Courts protect rich and powerful over ordinary people; Ctinplt: The Courts’ decisions are unduly influenced by political pressure; Wevdct: How willing to give evidence in court against the accused. ESS6‐2012 Understanding democracy: Cttresac: In country the courts treat everyone the same.

Informational dimension

Non‐tax specific

ESS6‐2012 Understanding democracy: Meprinfc: In country the media provide citizens with reliable information to judge the government; Gvexpdcc: In country the government explains its decisions to voters.

Table 5 Variables from ESS4, 5 and 6 rounds

For each explanatory variable selected, we create a dummy variable calculating the mean value for each one of the nineteen countries in the study. We also control for cultural and individual‐level effects as gender, age, marital status, employment status and highest educational level attained (8 categories), all of them from WVS/EVS data source. 5.3 Estimation strategy

We relate country‐level “folk transparency” variables to individual tax morale. We employ a binary logistic regression to account for the dichotomous character of the dependent variable, tax morale. The model contains both individual and contextual (country) level variables as regressors. Recognizing that the inclusion of country level variables might cause error terms not to be independent and uncorrelated, we report robust standard errors that account for clustering of individuals within one country at a certain point of time. Our explanatory variables differ across countries but not across individuals who live in the same country and participated in the survey at the same point of time.

6 Results

Our results are presented in table 6. We show the result of the logistic regression, which allows the interpretation of the signs of the coefficients. Looking at individual variables, we can see that women and married people have greater tax morale than men and singles, respectively. Furthermore, compared to employed individuals, we observe that being self‐employed seems to decrease tax morale, while being retired seem to have a positive impact, but marital status and educational level variables do not present significant results.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

23

The results for the “folk transparency” explanatory country‐level variables show that we obtain significant results and a positive correlation with tax morale in variables measuring the forth different dimensions tested (see Table 6).

Procedural dim.

Txautef: Tax authorities, how efficient in doing their job

Tax specific (Ts)

1.045***

Distributive dim.

Ditxssp: Government decrease/increase taxes and social spending Gvctzpvc: In country the government protects all citizens against poverty

Ts Non-tax specific (NTs)

0,094* 0,602***

Retributive dim.

Ctjbcnt: Courts doing good or bad job in countryWraccrp: More likely to be found guilty:Rich or poor falsely accused of crime Ctprpwr: Courts protect rich and powerful over ordinary people Cttresac: In country the courts treat everyone the same.

NTs NTs NTs NTs

2,526*** 4,641*** 1,016*** 0,485***

Informational dim.

Gvexpdcc: In country the government explains its decisions to voters.

NTs 2,311***

Table 6 Results summary (∗ < 0.10, ∗∗ < 0.05, ∗ ∗ ∗ < 0.01)

6.1 Robustness Checks

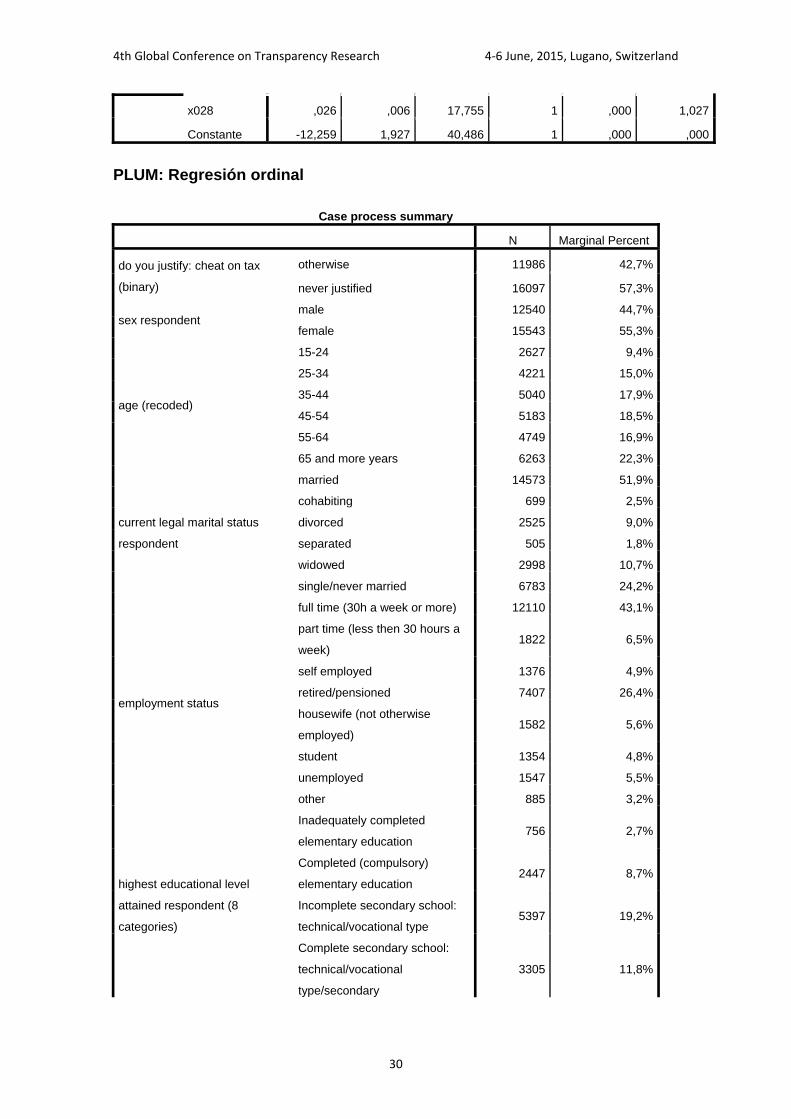

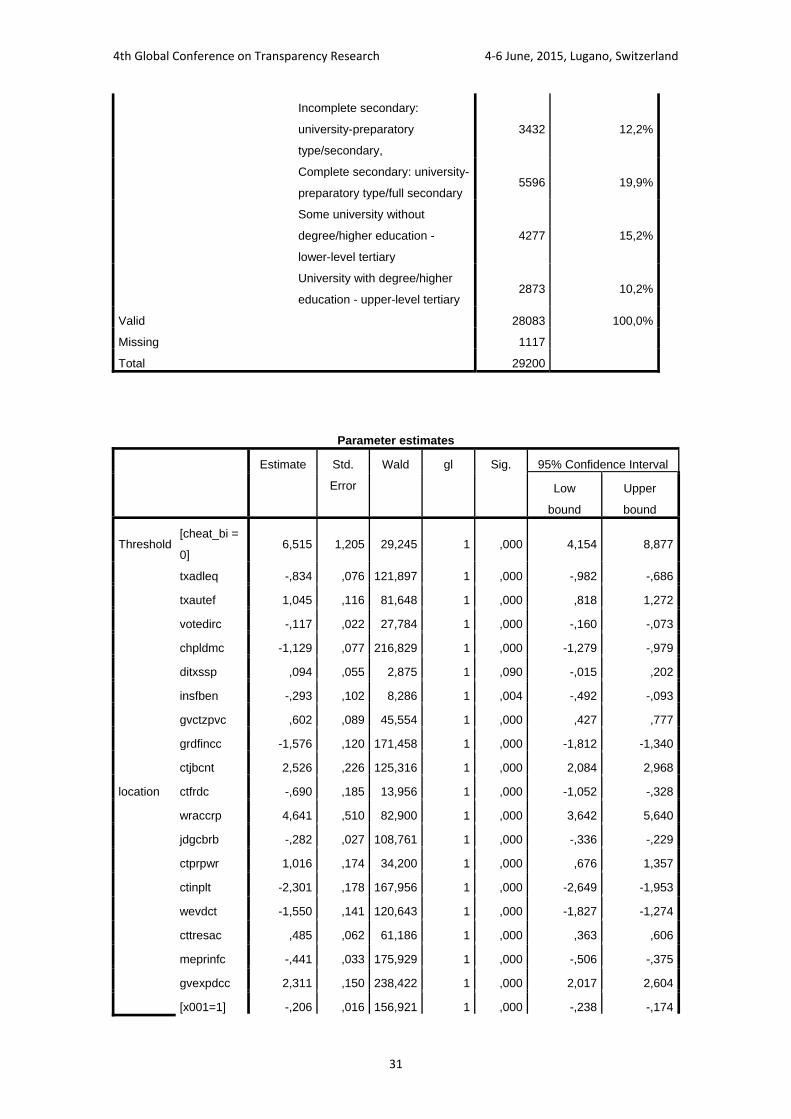

In order to further establish the link between tax morale and “folk transparency” dimensions, we ran a probit model instead of the logistic regression. In fact, we run a PLUM (Probit model, using the ordinal procedure, specifying probit link) by the ordinal variables (x001 x003r x007 x028 x025) and with the explanatory variables (txadleq, txautef, votedirc, chpldmc, ditxssp, insfben, gvctzpvc, grdfincc, ctjbcnt, ctfrdc, wraccrp, jdgcbrb, ctprpwr, ctinplt, wevdct, cttresac, meprinfc and gvexpdcc). The detailed results —presented in appendix—show that our original results remain unaffected.

7 Conclusion

Understanding determinants of folk transparency dimensions and its effect on tax morale at individual level is an important piece of the puzzle in order to explain why people pay taxes, and it can help to fight tax evasion. In this study we explore the concept of folk transparency, proposing a theoretical framework based on transparency dimensions related to social justice concept and applied to the concrete field of taxation. We tested this framework in an exploratory study on the impact of transparency measures on tax morale – an innovative link based on behavioral and informational asymmetry. Our analysis shows that an individual’s tax morale seems to be correlated with several transparency measures in each of the transparency dimensions proposed. Our results are consistent with previous studies that relate quality of government indicators –

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

24

most of them based on the views and experiences of experts – and the generation of trust and the trust as determinant for creating tax morale. Our analysis has implications for public policy makers. In the public and media discussion, tax transparency measures are often considered to be damaging from an economic point of view or from a privacy‐protection point of view and at the result of its application is at least dubious or not clear enough for politicians and tax authorities. We are able to show, however, that tax transparency might also yield positive outcomes. Properly transparency measures in taxation, therefore, contribute to less tax evasion and higher perceived fairness and equality. Note, however, that we are not able to identify a causal relationship. The causality could also go the other way: because of higher tax morale (and inequality aversion) of their citizens, the governments can increase tax burden and / or tax revenues ruling more efficient and trustable tax agencies that explain decision‐making procedures and results in a comprehensive, reasonable, honest and sincere way. Although shown to have high significance, research on the determinants of tax morale is as yet insufficient. While individual‐level factors explaining different levels of tax morale have been analyzed quite frequently, literature on contextual level factors is not satisfactory. Further research has to investigate the behavioral and informational determinants of information transparency and its relation to tax evasion, such as social contagion through exposure and information framing effects in social and personal decisions. Furthermore, the impacts of different types of transparency measures on tax morale have to be considered—ideally in extensive cross‐country approaches. More research also has to devote itself to establish further the link between tax morale measured in surveys and actual compliance behavior.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

25

REFERENCES

Adams, C.J. i Webley, P. (2001): “Small business owners‟ attitudes on VAT compliance in the UK”,

Journal of Economic Psychology, 22: 195‐216.

AICPA (2001), “Guiding Principles of Good Tax Policy: a Framework for Evaluating Tax Proposals, Tax

Division of the American Institute of Certified Public Accountants, Inc., New York.

AICPA (2007): “Guiding Principles for Tax Equity and Fairness”, Tax Division of the American Institute of

Certified Public Accountants, Inc., New York.

Alarcón, L., de Pablos, Garre, E. (2009): "Análisis del comportamiento de los individuos ante el fraude

fiscal. Resultados obtenidos a partir de la Encuesta del Observatorio Fiscal de la Universidad de Murcia",

Principios, 13: 55‐84.

Allingham, M.G. i Sandmo, A. (1972): “Income tax evasion: a theoretical analysis”, Journal of Public

Economics, 1: 323–338.

Alm, J. i Gómez, J.L. (2008), “Social Capital and Tax Morale in Spain”, Economic Analysis & Policy, 38 (1):

73‐87.

Alm, J., Jacobson, S. (2007): “Using Laboratory Experiments in Public Economics”, National Tax Journal,

60(1): 129‐152.

Alm, J., B. Torgler (2006). Culture differences and tax morale in the United States and in Europe. Journal

of Economic Psychology 27 (2), 224 – 246.

Alvira, F., García, J. i Delgado, M. L. (2000): Sociedad, impuestos y gasto público. La perspectiva del

contribuyente. Madrid: CIS.

Andreoni, J., B. Erard, and J. Feinstein (1998). Tax compliance. Journal of Economic Literature 36 (2), 818

– 860.

Antunes, L., Balsa, J., Moniz, L., Urbano, P., Palma, C.R. (2006), “Tax compliance in a simulated

heterogeneous multi‐agent society”, J.S. Sichman y L. Antunes (eds.): MABS 2005. LNCS (LNAI), 3891.

Heidelberg: Springer.

Ashby, J. S. I Webley, P. (2008): „But everyone else is doing it: A closer look at the occupational

taxpaying culture of one business sector‟, Journal of Community and Applied Social Psychology, 18:

194–210.

Becker, G.S. (1968): “Crime and Punishment: An Economic Approach”, Journal of Political Economy,

76:169‐217.

Bentham, J. (1816)[1999] Political Tactics. Edited by Michael James, Cyprian Blamires, Catherine Pease‐

Watkin and Jeremy Works of Jeremy Bentham Bentham. Oxford [Oxfordshire]: New York :: Clarendon

Press; Oxford University Press.

Bergman, M. i Nevárez, A. (2005): “¿Evadir o pagar impuestos? Una aproximación a los mecanismos

sociales del cumplimiento”, Política y Gobierno, 12 (1): 9‐40.

Blackwell, C. (2010), “A Meta‐Analysis of Tax Compliance Experiments”, J. Alm, J. Martinez‐Vázquez y B.

Torgler (eds.): Developing Alternative Frameworks for Explaining Tax Compliance. New York y London:

Routledge.

Bloomquist, K. M. (2004): Modeling taxpayers’ response to compliance improvement alternatives. Paper

at the Annual Conference of the North American Association for Computational Social and

Organizational Science (NAACSOS), Pittsburgh, PA.

Bloomquist, K. M. (2011): “Tax Compliance as an Evolutionary Coordination Game: An Agent‐Based

Approach”, Public Finance Review, 39: 25.

Bortolami, F. i Mittone, L. (2009): Does Participating in a Collective Decision Affect the Levels of

Contributions Provided? An Experimental Investigation. CEEL Working Paper 2‐09, Computable and

Experimental Economics Laboratory, Trento.

Braithwaite, V., Ahmed, E. (2005), “A threat to tax morale: the case of Australian higher education

policy”, Journal of Economic Psychology, 26: 523‐540.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

26

Braithwaite, V., Reinhart, M. i Smart, M. (2010): “Tax non‐compliance among the under‐30s: Among the

Under‐30s: Knowledge, Obligation or Skepticism?”, B. Torgler, J. Alm i J. Martinez (eds): Developing

Alternative Frameworks for Explaining Tax Compliance, Avoidance and Evasion. London: Routledge.

Coricelli, G. et al (2007): “Tax Evasion: Cheating Rationally or Deciding Emotionally?”, Forschungsinstitut

zur Zukunft der Arbeit, Discussion Paper No. 3103.

Elffers, H., R. H. Weigel, and D. J. Hessing (1987). The consequences of different strategies for measuring

tax evasion behavior. Journal of Economic Psychology 8 (3), 311 – 337

Elster, J. (1998) "Deliberation and Constitution Making." In Deliberative Democracy, edited by Jon Elster.

Cambridge: Cambridge University Press.

ESS Round 6: European Social Survey Round 6 Data (2012). Data file edition 2.1. Norwegian Social

Science Data Services, Norway – Data Archive and distributor of ESS data.

ESS Round 5: European Social Survey Round 5 Data (2010). Data file edition 3.2. Norwegian Social

Science Data Services, Norway – Data Archive and distributor of ESS data.

ESS Round 4: European Social Survey Round 4 Data (2008). Data file edition 4.3. Norwegian Social

Science Data Services, Norway – Data Archive and distributor of ESS data.

Europe Comission. (2009). Communication from the Commission to the Council, the European

Parliament and the European Economic and Social Committee ‐ Promoting Good Governance in Tax

Matters.

EVS (2011). European Values Study 1981‐2008, Longitudinal Data File. GESIS Data Archive, Cologne,

Germany, ZA4804 Data File Version 2.0.0 (2011‐12‐30) DOI:10.4232/1.11005.

Fearon, J. D. (1995) "Rationalist Explanations for War." International Organization 49, no. 3: 379‐414.

Feld, L. P., i Frey, B. S. (2002). The Tax Authority and the Taxpayer. In An Exploratory Analysis, paper

presented the 2002 Annual Meeting of the European Public Choice Society Belgirate.

Fernández Caínzos, J.J. (2006): Sociología de la Hacienda Pública, Instituto de Estudios Fiscales, Madrid.

Frey, B. S., Torgler, B (2007) Tax morale and conditional cooperation, Journal of Comparative Economics

Friedland, N., Maital, S. i Rutenberg, A. (1978): “A Simulation Study of Income Tax Evasion”, Journal of

Public Economics, 10: 107‐116.

Fung, A., Graham, M., Weil, D., & Fagotto, E. (2004) The Political Economy of Transparency: What makes

disclosure policies effective?. Available at SSRN 766287.

Gerring, J. I Thacker S. C. (2004) "Political Institutions and Corruption: The Role of Unitarism and

Parliamentarism." British Journal of Political Science 34 (2004): 295‐330.

Gosseries, A. (2006). Debate : Transparency, 12, 83–133.

Guala, F. i Mittone, L (2002): Experiments in Economics: Testing Theories vs. the Robustness of

Phenomena. Technical Report 9, CEEL (Computable and Experimental Economics Laboratory), University

of Trento.

Hasseldine, J. i Hite, PA. (2003): “Framing, gender and tax compliance”, Journal of Economic Psychology,

24: 517–533.

Heinemann, F. (2010). Economic crisis and morale. European Journal of Law and Economics, 1 – 15.

Inglehart, R. (n.d.). Values change the world. http://worldvaluessurvey.org/ (accessed April 2015).

Juan, A. J. de (1995): “Manifestaciones del comportamiento fraudulento en España. Análisis de causas y

estrategias preventivo‐correctoras”, Información Comercial Española. Revista de Economía, 741: 55‐65.

Keohane, Robert O., and Joseph S. Nye (2003) "Redefining Accountability for Global Governance." In

Governance in a Global Economy : Political Authority in Transition, edited by Miles Kahler and David A.

Lake. Princeton, N.J. :: Princeton University Press.

Kirchler, E. (2007): The Economic Psychology of Tax Behaviour. Cambridge: Cambridge University Press.

Kirchler, E. et al.. (2009), “Effort and Aspirations in Tax Evasion: Experimental Evidence”, Applied

Psychology 58 (3): 488‐507.

Korobow, A. et al. (2007): “An Agent‐Based Model of Tax Compliance with Social Networks”, National

Tax Journal, LX (3): 589‐610.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

27

Llàcer, T. i Noguera, J.A. (2011): “Resentimiento fiscal: una propuesta de mecanismo explicativo de la

relación entre edad y moral fiscal”, ponencia presentada en el III Congreso de la Red Española de Política

Social (REPS), Pamplona.

Majone, G. (1996) Regulating Europe, London: Routledge.

María‐Dolores, R. et al (2010): “Tax Morale in Spain: A Study into Some of Its Principal Determinants”,

Economic Analysis & Policy, 38 (1).

Martínez, P., Castillo, A.M. i Rastrollo, M.A. (2008): “Los enfoques de análisis de la evasión fiscal. Una

revisión actual de la investigación”, Cuadernos de Ciencias económicas y empresariales. Papeles de

trabajo, 35.

Miller, G. J. (2005) "The Political Evolution of Principal‐Agent Models." Annual Review of Political Science

8: 203‐25.

Mitchell, R. B. (1998) "Sources of Transparency: Information Systems in International Regimes."

International Studies Quarterly 42, no. 1: 109‐30.

Mittone, L. i Patelli, P. (2000): “Imitative behaviour in tax evasion”. B. Stefansson & F. Luna (Eds.):

Economic simulations in swarm: Agent‐based modelling and object oriented programming. Amsterdam:

Kluwer.

Mocetti, S. I Barone, G. (2011): “Tax Morale and Public Spending Inefficiency”, International Tax and

Public inance, 1‐26.

Montinola, G. R., i Jackman, R. W. (2002) "Sources of Corruption: A Cross‐Country Study." British Journal

of Political Science 32 (2002): 147‐70.

Naurin, D., i Lindstedt, C. (2006). Transparency against corruption. A cross‐country analysis. 20th World

Congress of the International Political Science Association

Pechman, J. (1983) Federal tax policy (Washington, DC: Brookings Institution).

Persson, Torsten, Guido Tabellini, i Trebbi (2003) "Electoral Rules and Corruption " Journal of the

European Economic Association Volume 1, no. Number 4: pp. 958‐89.

Prieto, J., Sanzo, M.J. i Suárez, J. (2006): “Análisis económico de la actitud hacia el fraude fiscal en

España”, Hacienda Pública Española/ Revista de Economía Pública, 177: 107‐128.

Rothstein, B. (2001) “Trust, social dilemmas, and collective memories: on the rise and decline of the

Swedish model,” Journal of Theoretical Politics, 12:477‐499.

Sánchez, I. i Juan, A. de (1994): “Análisis experimental del cumplimiento fiscal”, Papeles de Trabajo, 1.

Madrid: IEF.

Schmölders, G. (1965): Problemas de psicología financiera. Madrid: Editorial de Derecho Financiero.

Srinivasan, T. N. (1973): “Tax evasion: A model”, Journal of Public Economics, 2 (4): 339‐46.

Schultz, K. A. (1998) "Domestic Opposition and Signaling in International Crises." American Political

Science Review 92, no. 4: 829‐44.

Sheffrin, S.M. (2013) Tax Fairness and Folk Justice, Cambridge University Press

Sigala, M., Burgoyne, C.B. i Webley, P. (1999): „Tax communication and social influence: Evidence from a

British sample‟, Journal of Community & Applied Social Psychology, 9: 237‐241.

Slemrod, J. (2003): “Trust in Public Finance”, en Cnossen, S. y Werner Sim, H. (eds), Public Finance and

Public Policy in the New Century, MIT Press, Cambridge.

Slemrod, J. (2006). “Taxation and Big Brother: Information, Personalization, and Privacy in 21st Century

Tax Policy.” Fiscal Studies, March, 27(1):1–15

Stack, S. i Kposowa, A. (2006): “The Effect of Religiosity on Tax Fraud Acceptability: A Cross‐National

Analysis”, Journal for the Scientific Study of Religion, 45 (3): 325–351.

Steinmo, S. (2003) The evolution of policy ideas: tax policy in the 20th century. The British Journal of

Politics & International Relations, 5(2), 206‐236.

Stiglitz, J. E. "The Contributions of the Economics of Information to Twentieth Century Economics."

Quarterly Journal of Economics 115, no. 4 (2000): 1441‐78.

4th Global Conference on Transparency Research 4‐6 June, 2015, Lugano, Switzerland

28

Szabó, A. Gulyás, L. i Tóth, I. J. (2010): “Simulating Tax Evasion with Utilitarian Agents and Social

Feedback”, International Journal of Agent Technologies and Systems, 2 (1): 16‐30.

Tabibnia, G., Satpute, A. B., & Lieberman, M. D. (2008): The sunny side of fairness: Preference for

fairness activates reward circuitry (and disregarding unfairness activates self‐control

circuitry). Psychological Science, 19, 339‐347.

Torgler, B. (2003): “Tax Morale, Rule‐Governed Behaviour and Trust”, Constitutional Political Economy,

14: 119– 140.