TAPAN BHANJA Chamber : Advocate 6, K.S. Roy Road, 3rd Floor, Nigh Court, Calcutta Kolkata - 700 001 Mobile: 9674280298 Date: 26.02.2021 To 1. The Learned Government Pleader, High Court, Calcutta 2. Reliance Industries Ltd. Godrej Waterside, Tower-I1, 17th & 18th Floor, Block-DP, Salt Lake, Sector-V, Kolkata, Pin- 700091. Ref : WPA. No. 5866 of 2021 M/s. Ambey Mining Pvt. Ltd. & Anr. ... Petitioners Vs The State of West Bengal & Ors. .... Respondents Sir, Please find enclosed copy of the Writ Application along with all annexures, which has been filed in the Central Filing Section of the Honble High Court at Calcutta on 25.02.2021 and the same will appear before the Honble Justice Arindam Mukherjee on 03.03.2021or so soon thereafter as and when the business of the Honble Court will permit. This is for your information record necessary steps. Thanking you, Enclo. : As above. Yours Sincerely, r i C r i fil 1( 7 1 Advocate -

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TAPAN BHANJA Chamber : Advocate

6, K.S. Roy Road, 3rd Floor, Nigh Court, Calcutta

Kolkata - 700 001 Mobile: 9674280298

Date: 26.02.2021

To 1. The Learned Government Pleader,

High Court, Calcutta

2. Reliance Industries Ltd. Godrej Waterside, Tower-I1, 17th & 18th Floor, Block-DP, Salt Lake, Sector-V, Kolkata, Pin- 700091.

Ref : WPA. No. 5866 of 2021 M/s. Ambey Mining Pvt. Ltd. & Anr.

... Petitioners Vs

The State of West Bengal & Ors. .... Respondents

Sir,

Please find enclosed copy of the Writ Application along with all

annexures, which has been filed in the Central Filing Section of the Honble

High Court at Calcutta on 25.02.2021 and the same will appear before the

Honble Justice Arindam Mukherjee on 03.03.2021or so soon thereafter as

and when the business of the Honble Court will permit.

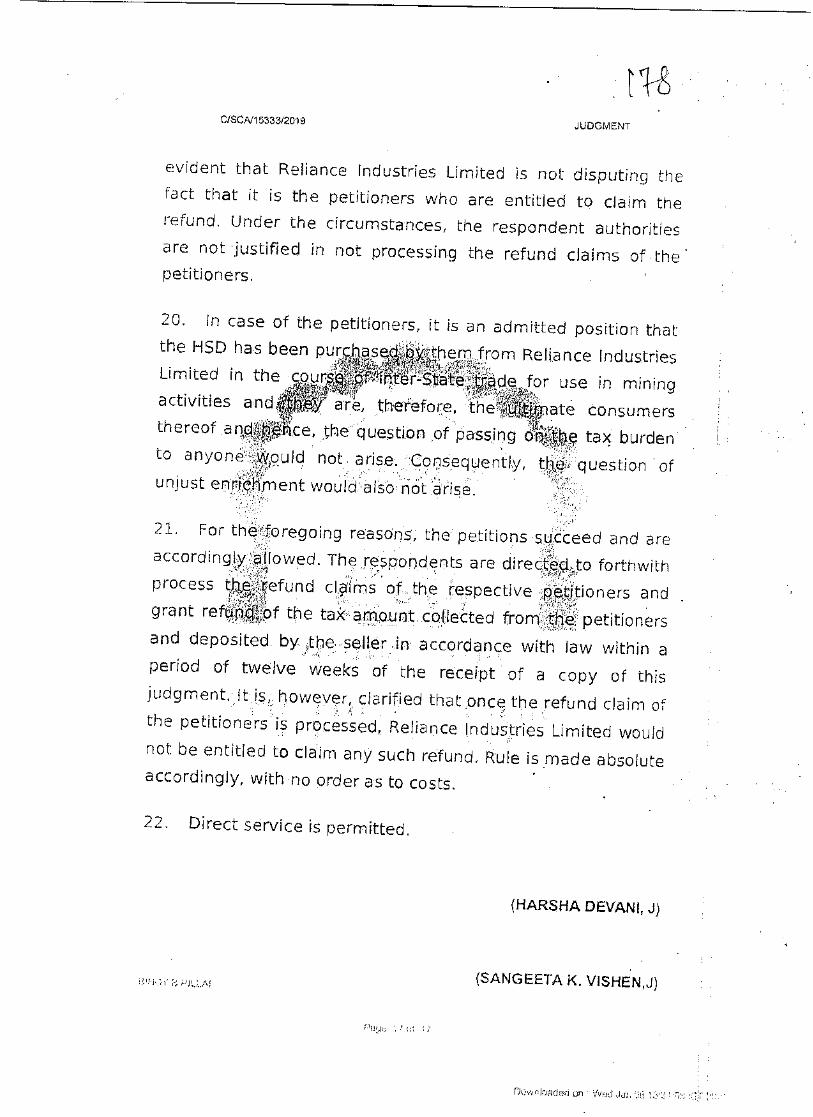

This is for your information record necessary steps.

Thanking you,

Enclo. : As above.

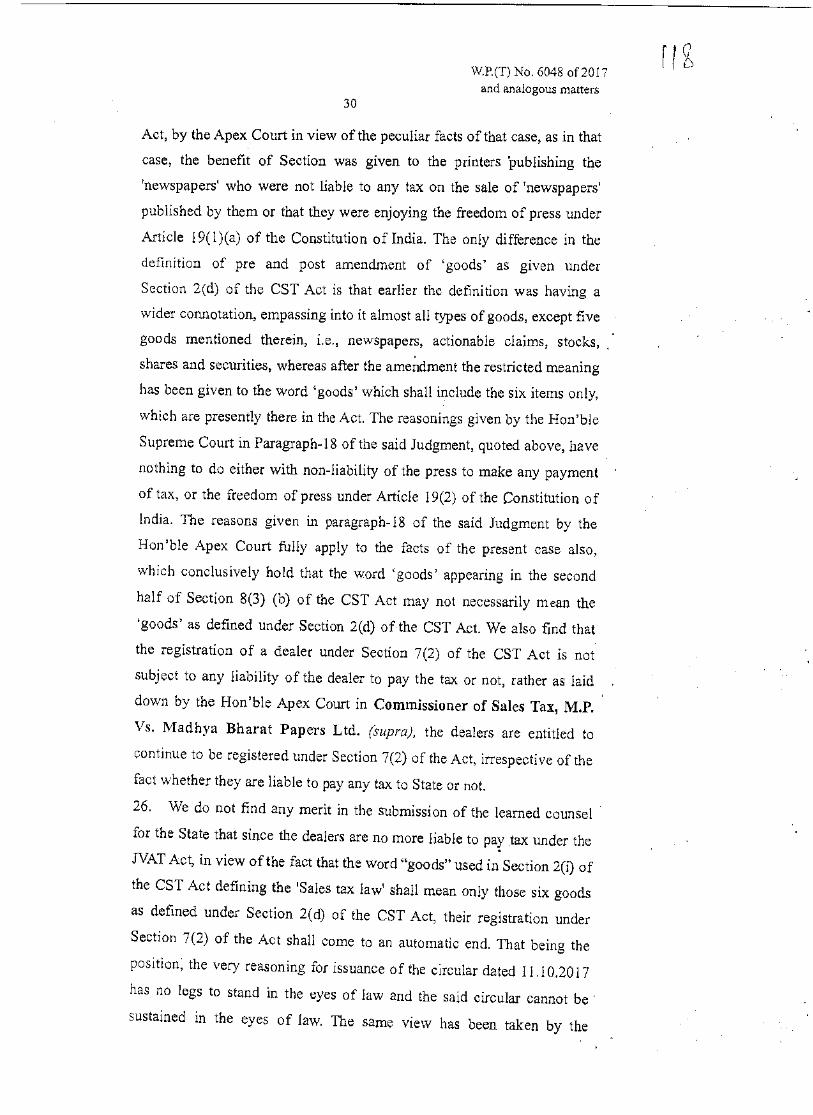

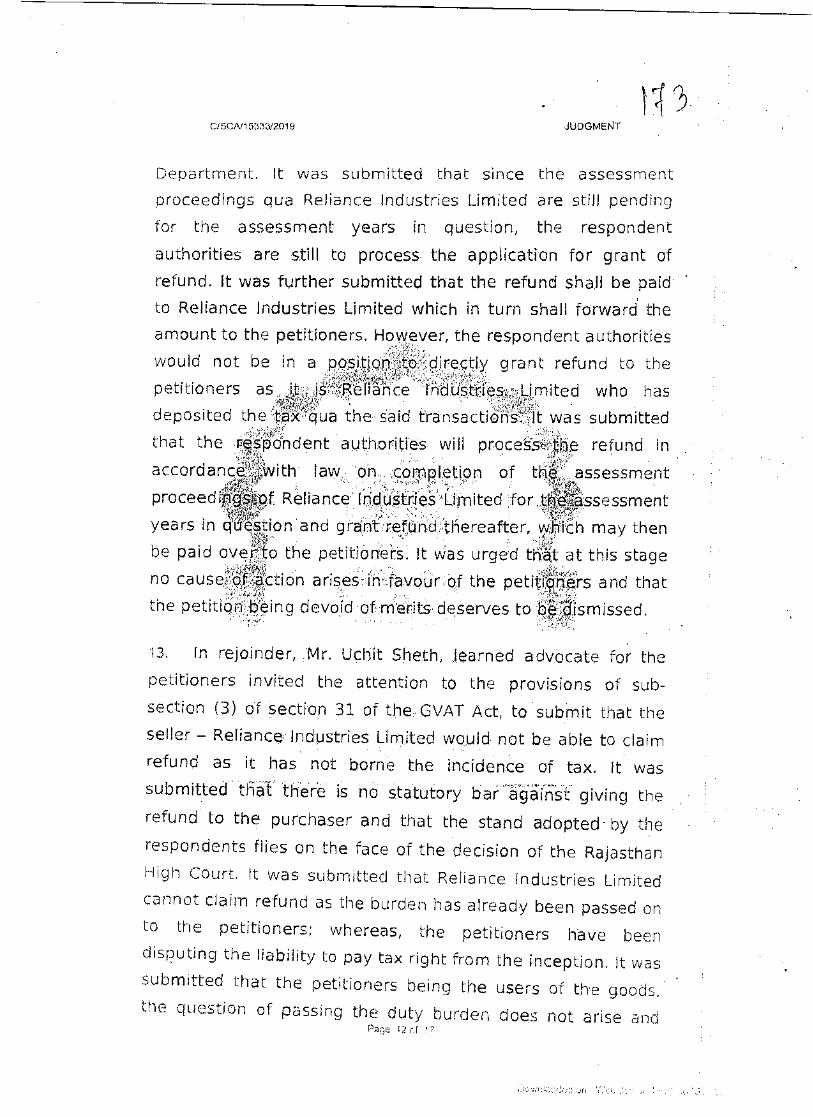

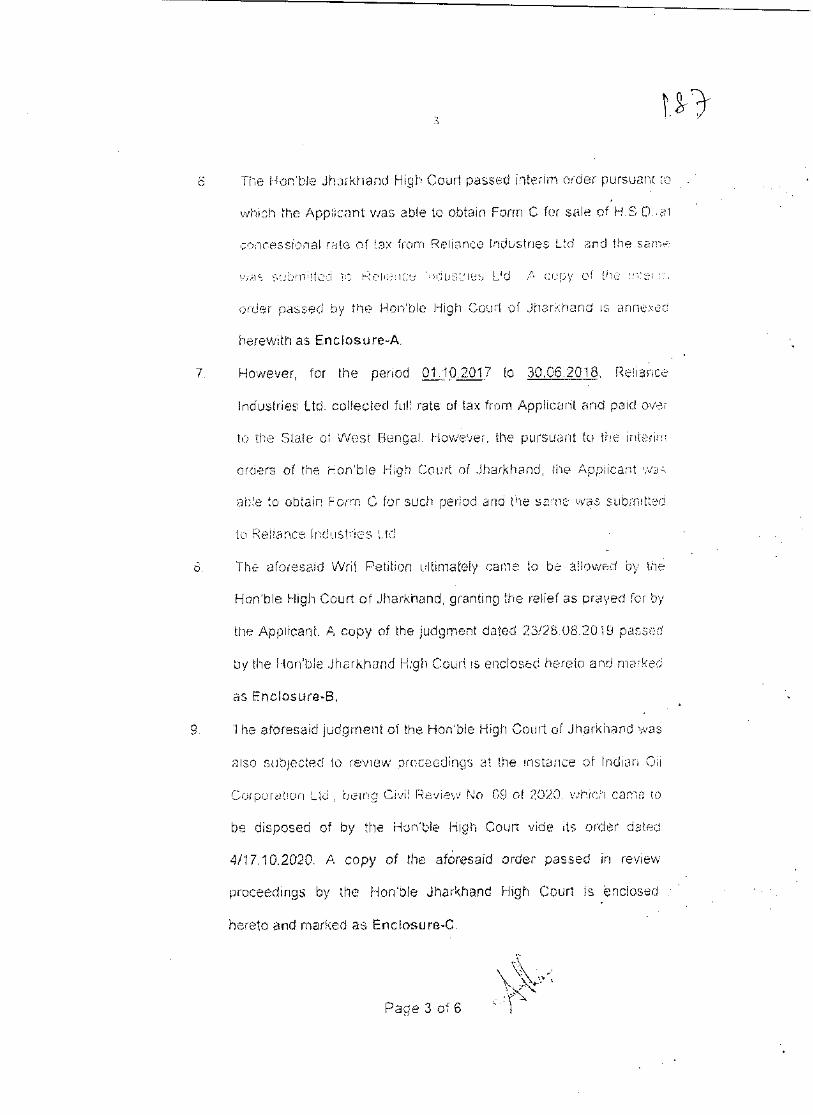

Yours Sincerely,

riCri fil1(71 Advocate -

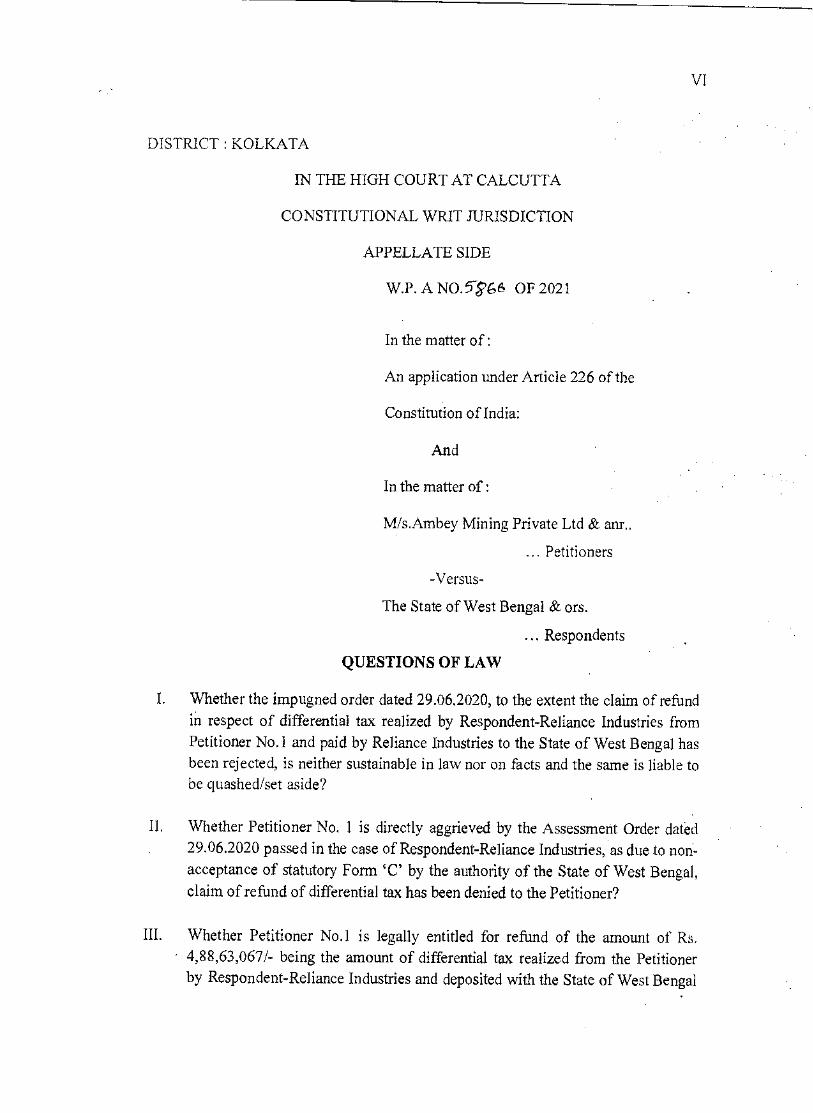

DISTRICT : KOLKATA

IN THE HIGH COURT AT CALCUTTA

CONSTITUTIONAL WRIT JURISDICTION

APPELLATE SIDE

W.P.A. NO. 5g66 OF 2021

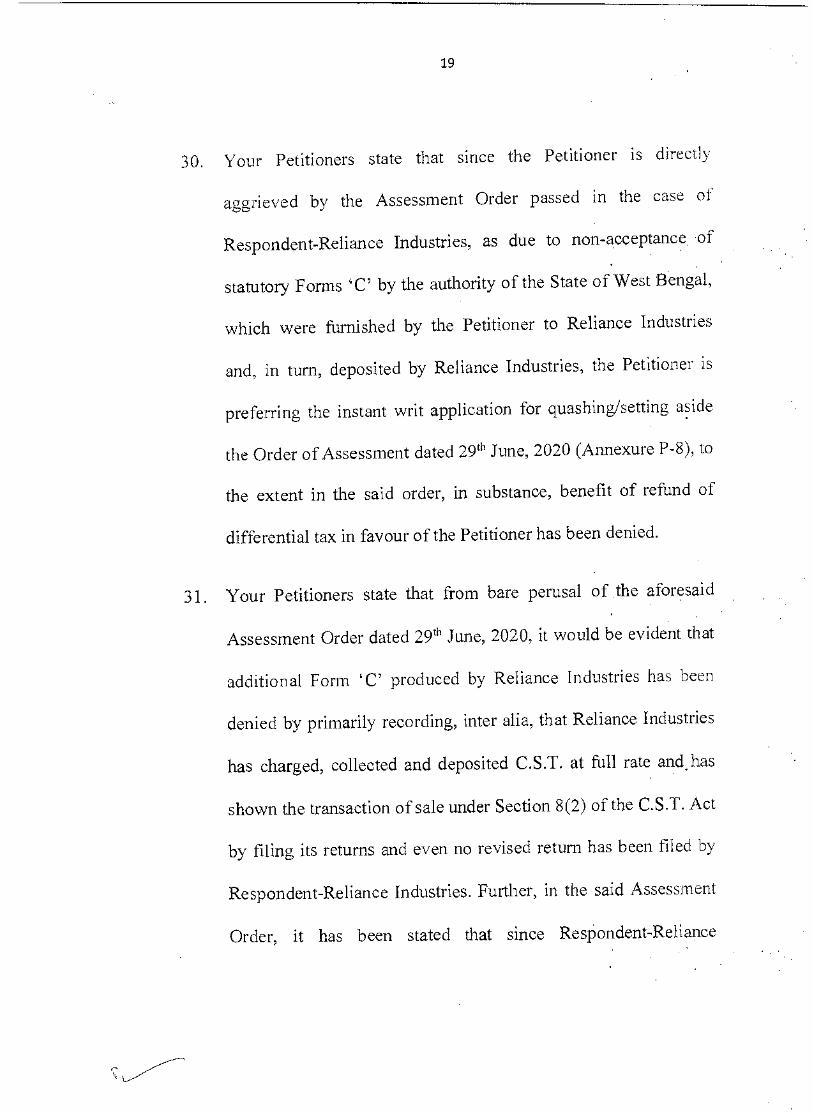

In the matter of :

An application under Article 226 of

the Constitution of India:

Subject Matter relating to :

Group IV, Head L

of the Classification List.

CAUSE TITLE

Ambey Mining Private Ltd and anr.

... Petitioners

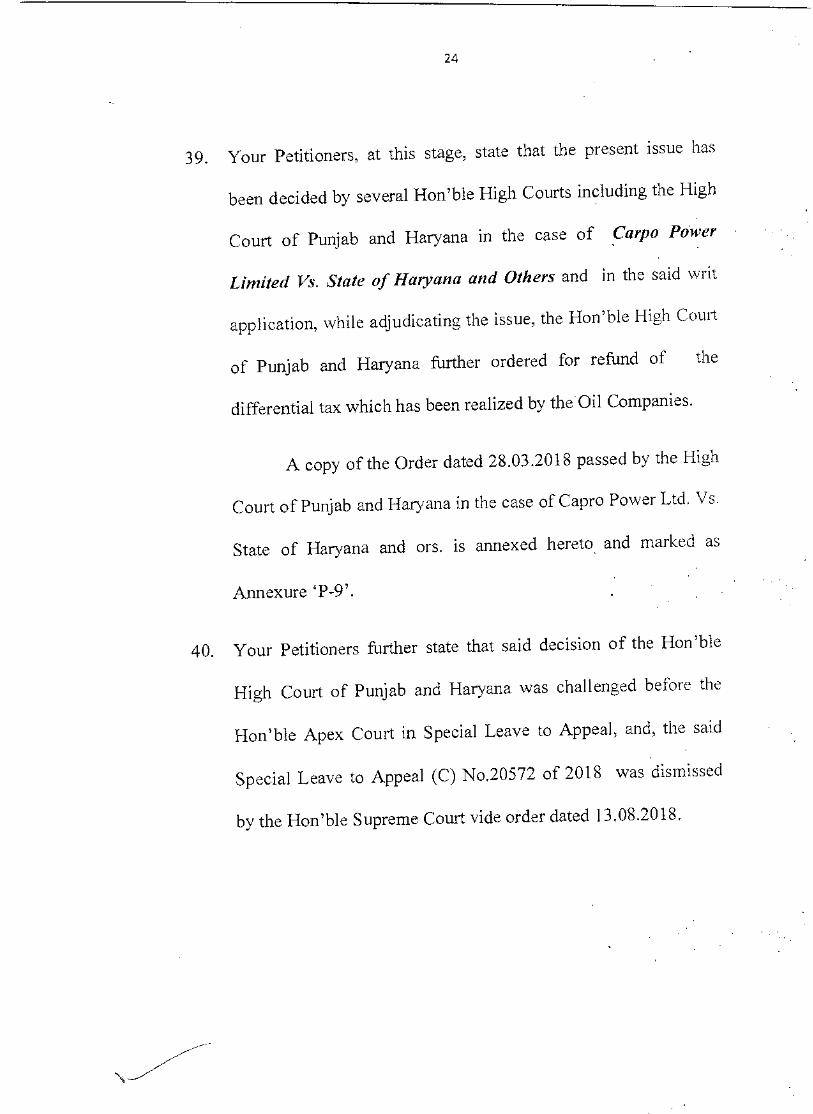

-Versus-

The State of West Bengal & ors.

... Respondents

Advocate-on-Record

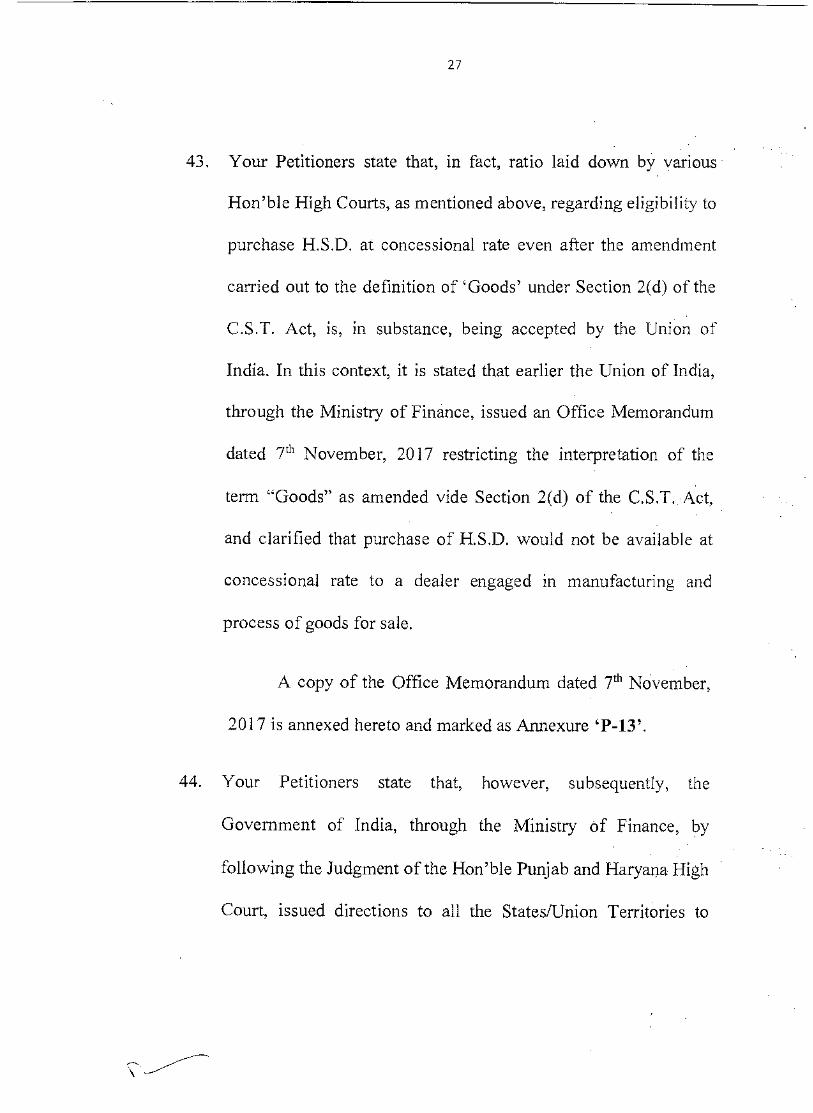

cry (2. TAPAN BHANJA Advocate High Court at Calcutta 6, K.S.Roy Road, Third floor Kolkata-700 001 Mobile No. 9674280298

14

DISTRICT : KOLKATA

IN THE HIGH COURT AT CALCUTTA CONSTITUTIONAL WRIT JURISDICTION

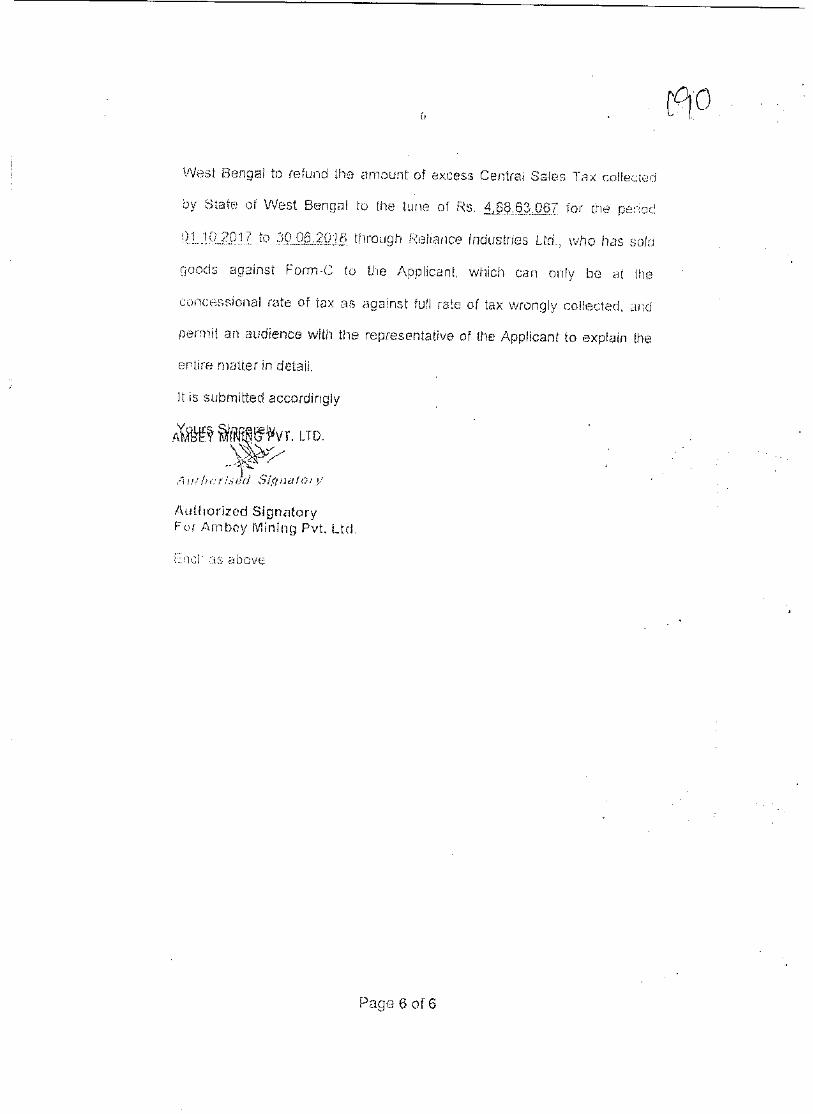

APPELLATE SIDE W.P. A NO. 536.6 (W) OF 2021

In the matter of : An application under Article 226 of the Constitution of India:

And In the matter of : M/s.Ambey Mining Private Ltd & Anr

... Petitioners -Versus-

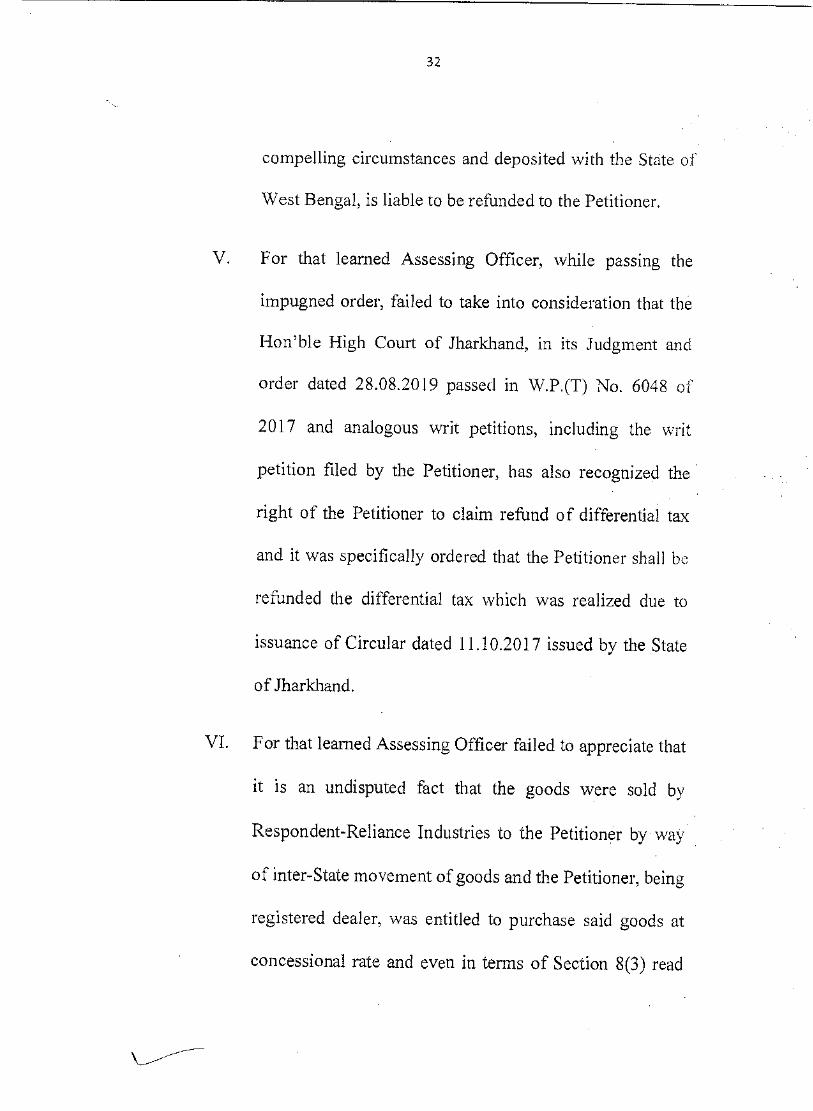

The State of West Bengal & ors. ... Respondents

INDEX

SI. No.

Description of documents. Annexure Page

1. List of dates I-VII 2. Questions of Law VIII-XII . 3. Writ Petition with Affidavit 1 - 46-7 4. Xerox copy of Registration Certificate of the

Petitioner. I 55 P-1

-1 - 5. Xerox copy of the Circular contained in Memo

No. 3750 dated 11.10.2017 issued by the State of Jharkhand.

P-2 SI - s 9-

6. Web copy of the Interim Order dated 17th May, 2018.

P-3 Sa-61 7. Sample copy of Provisional Credit Note/Credit

Note. P-4

C / - 71 I 8. Sample copies of Form 'C' obtained from the

State of Jharkhand in favour of Respondent- BPCL.

P-5 series :13-- -a.a

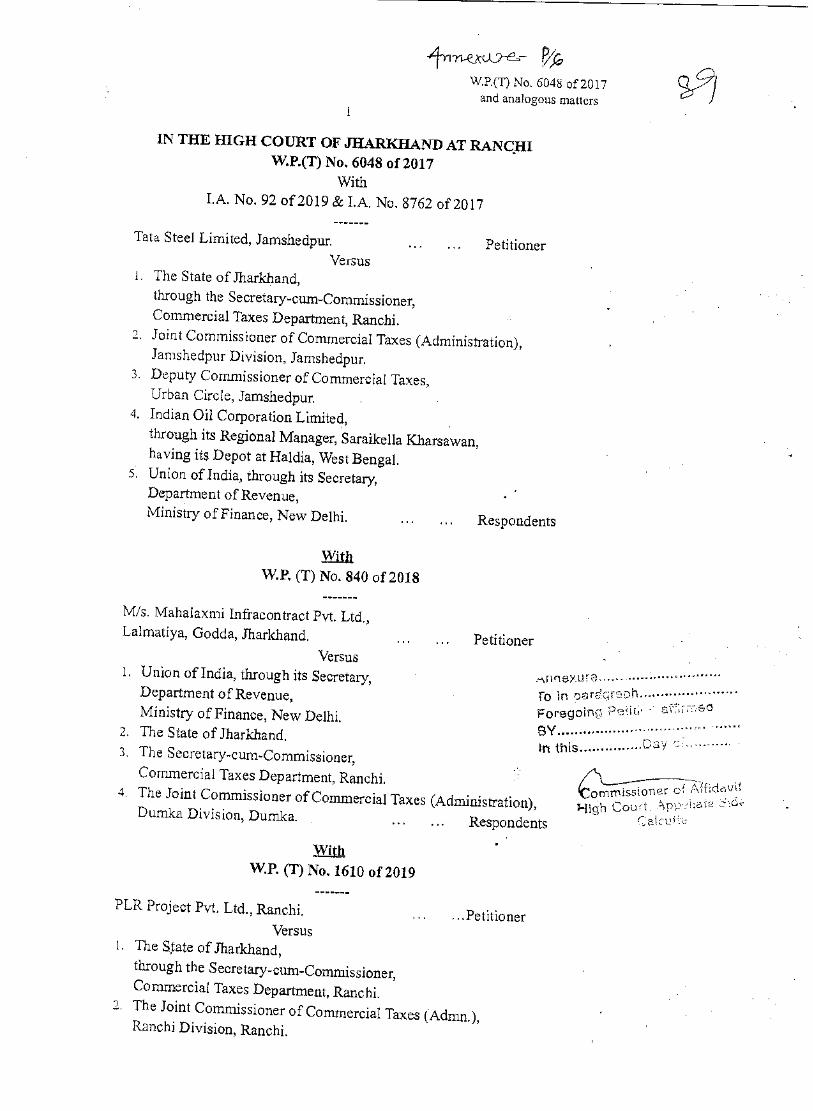

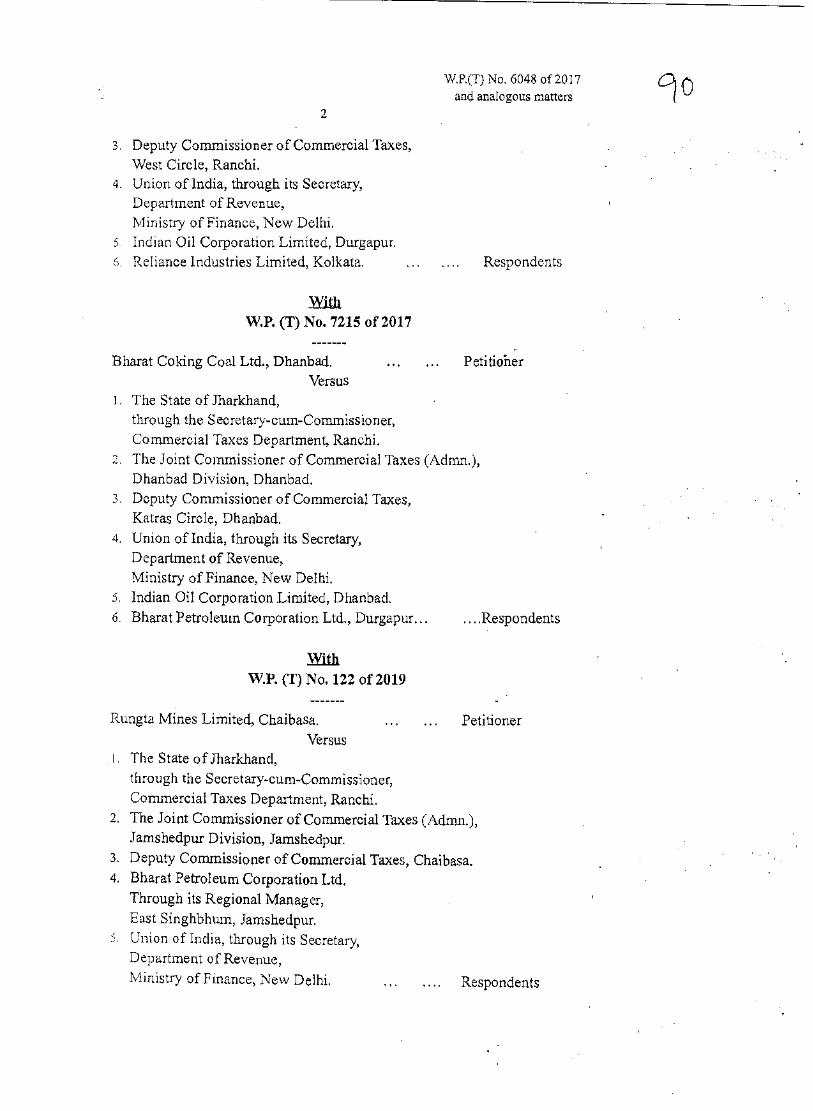

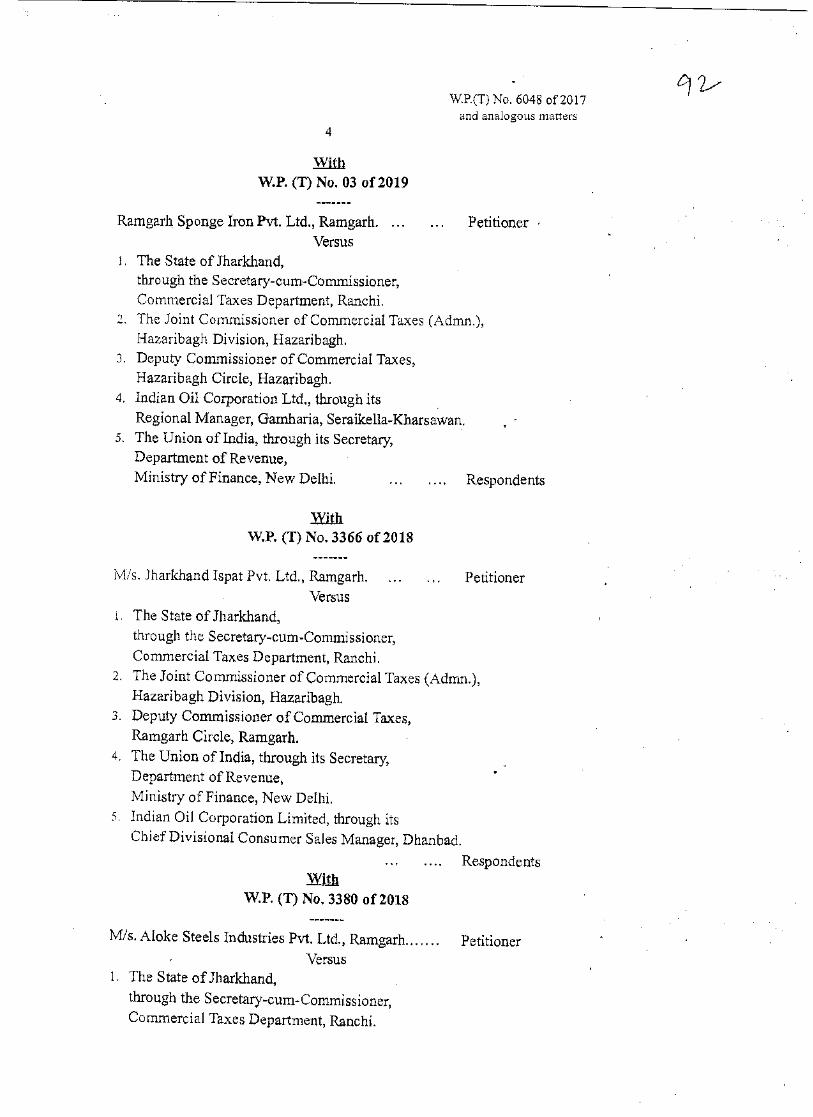

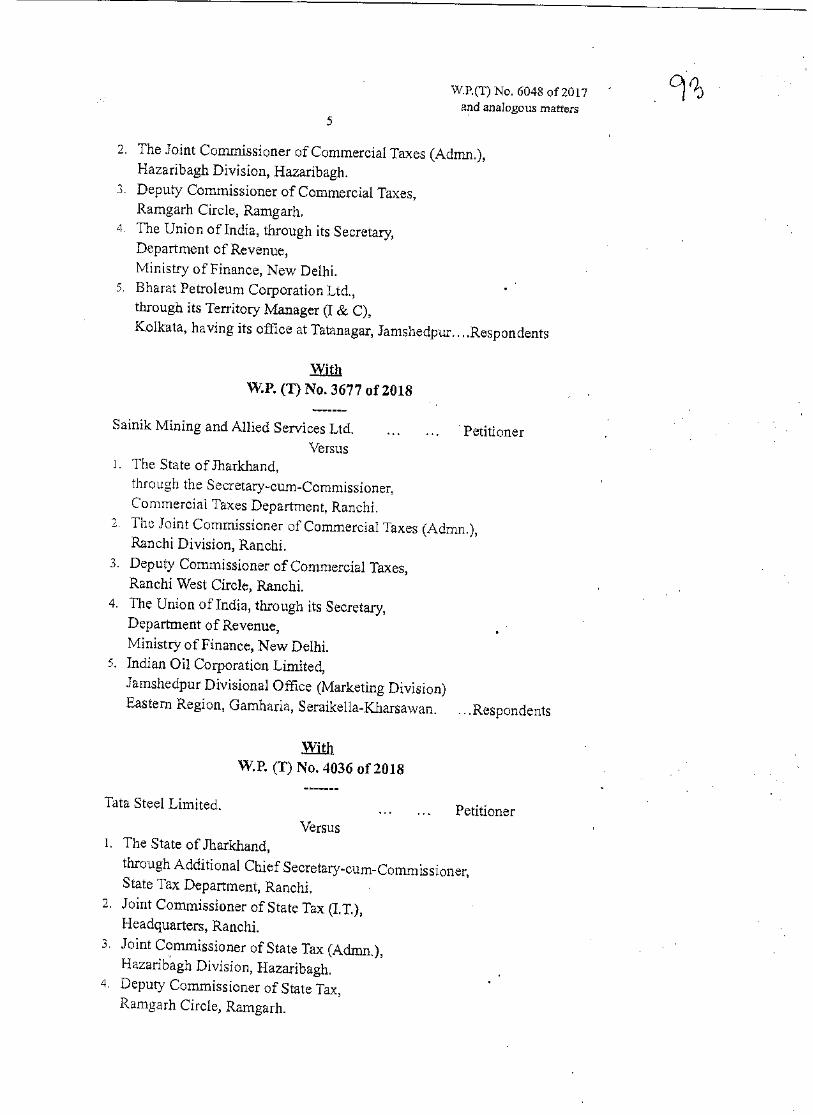

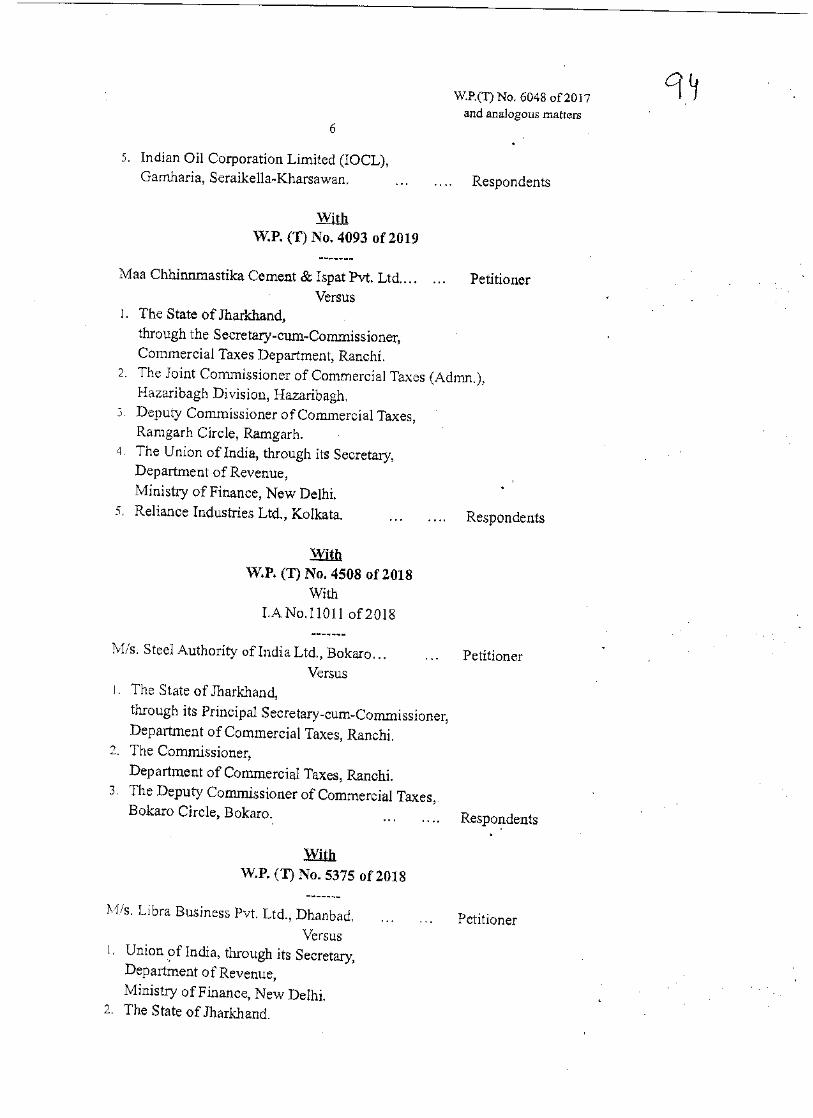

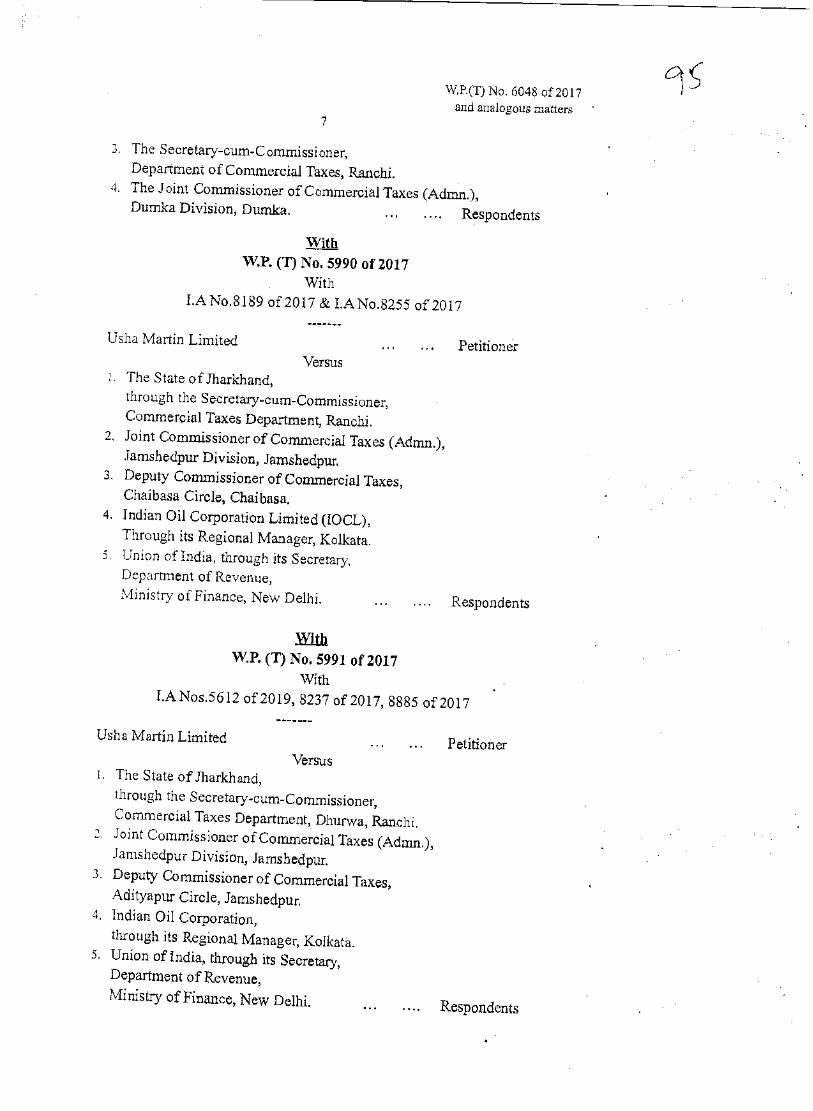

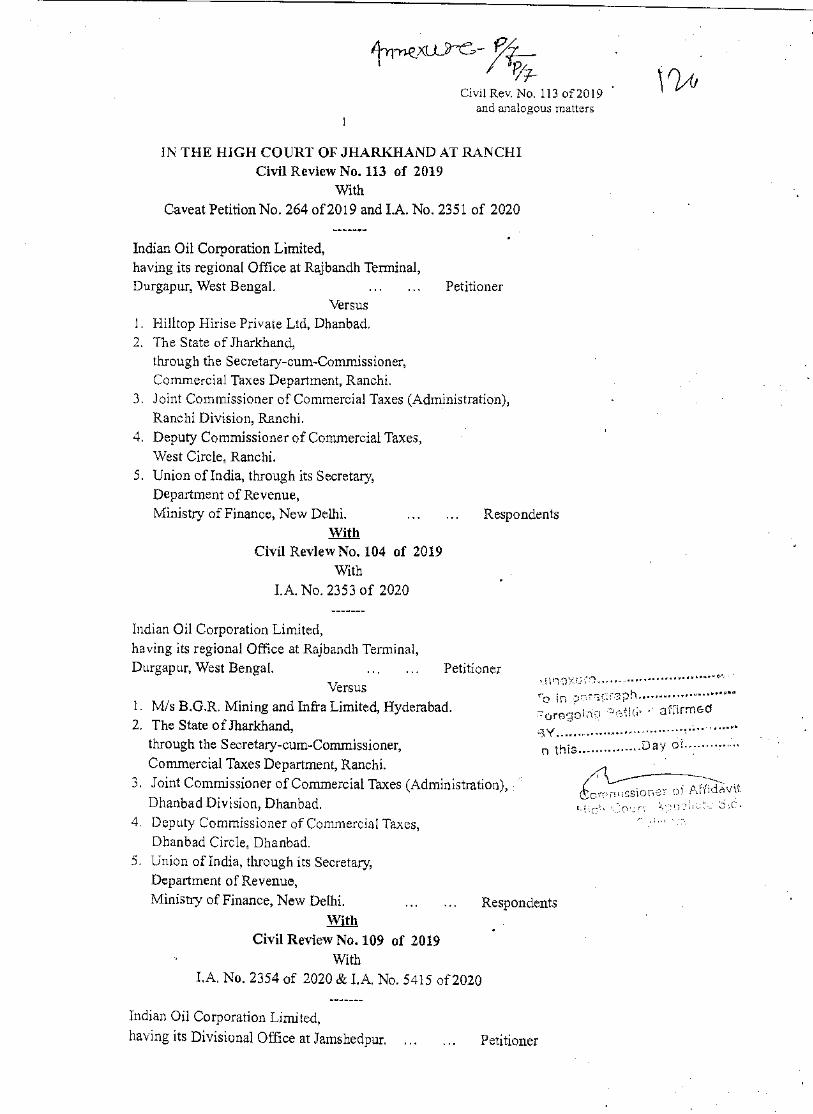

9. Web copy of the Judgment and order dated 28.08.2019 passed by Hon' ble Jharkhand High Court in W.P.(T) No. 6048 of 2017 and analogous cases

P-6 2s-9- 1)1

10. Web copy of the Order passed in Civil Review , No. 09 of 2020. 1 )1

P-7 2-0 -

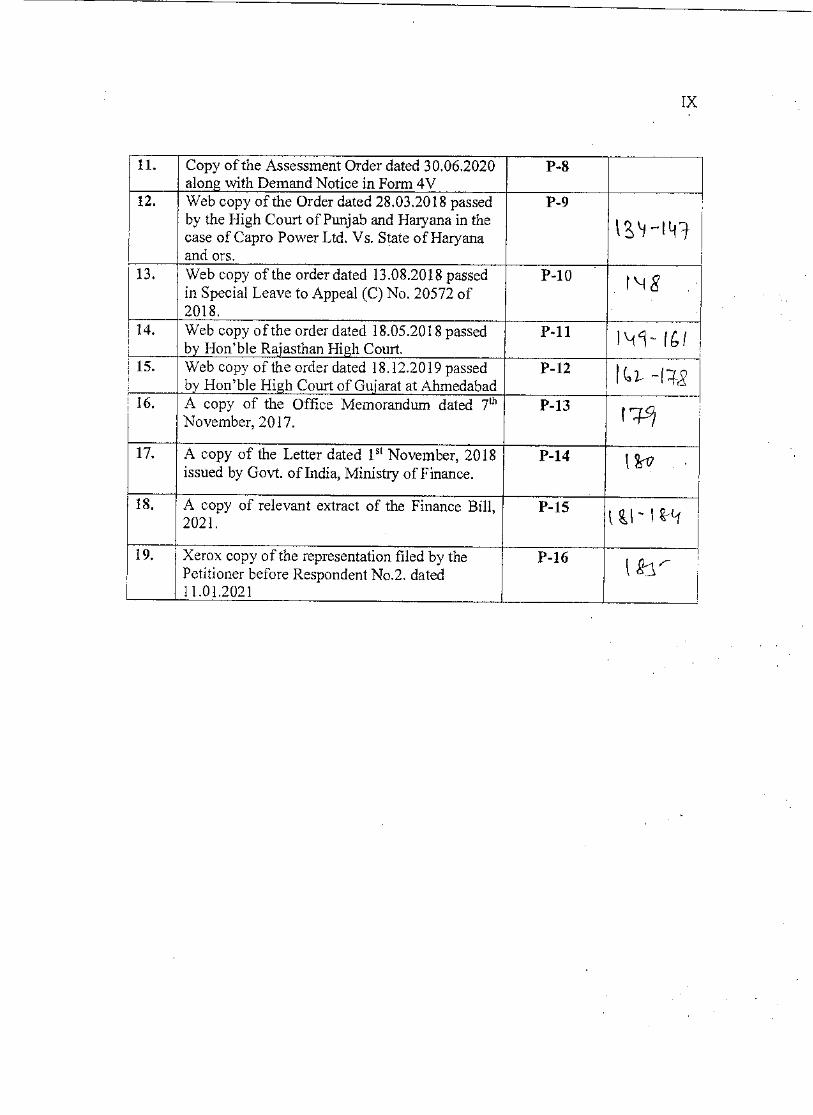

11. Copy of the Assessment Order dated 30.06.2020 along with Demand Notice in Form 4V

P-8 128 ^ I ?)3

IX

11. Copy of the Assessment Order dated 30,06.2020 along with Demand Notice in Form 4V

P-8

12. Web copy of the Order dated 28.03.2018 passed by the High Court of Punjab and Haryana in the case of Capro Power Ltd. Vs. State of Haryana and ors.

P-9

af—Iti-}

13. Web copy of the order dated 13.08.2018 passed in Special Leave to Appeal (C) No. 20572 of 2018.

P-10 r 4 8

14. Web copy of the order dated 18.05.2018 passed by Hon'ble Rajasthan High Court.

P-11 1\19- (41 15. Web copy of the order dated 18.12.2019 passed

by Hon'ble High Court of Gujarat at Ahmedabad P-12

1C2- 44g 16. A copy of the Office Memorandum dated r

November, 2017. ('r /17.

P-13

P-14 1 all A copy of the Letter dated 1" November, 2018 issued by Govt. of India, Ministry of Finance.

18. A copy of relevant extract of the Finance Bill, 2021.

P-15 l al - I VI

19. Xerox copy of the representation filed by the Petitioner before Respondent No.2. dated 11.01.2021

P-16 r gi

DISTRICT . KOLKATA

IN THE HIGH COURT AT CALCUTTA

CONSTITUTIONAL WRIT JURISDICTION

APPELLATE SIDE

W.P.A NO.5“6 OF 2021

In the matter of :

An application under Article 226 of the

Constitution of India:

And

In the matter of :

M/s.Ambey Mining Private Ltd & Ann

... Petitioners

-Versus-

The State of West Bengal & ors.

... Respondents

LIST OF DATES

21.12.1956 The Union of India has the exclusive power under Entry 84 of

List-I of the Constitution of India to levy duty of excise on

manufacture of goods and also has the power to levy tax on sales

of goods in the course of inter-state trade (inter-state sales) under

Entry 92A of List-1 of the Seventh Schedule to the Constitution.

Service Tax was levied in exercise of power under Entry 97 of

List-I. The States had the exclusive power to tax sales or

purchases within the State under Entry 54 of List-II.

iI

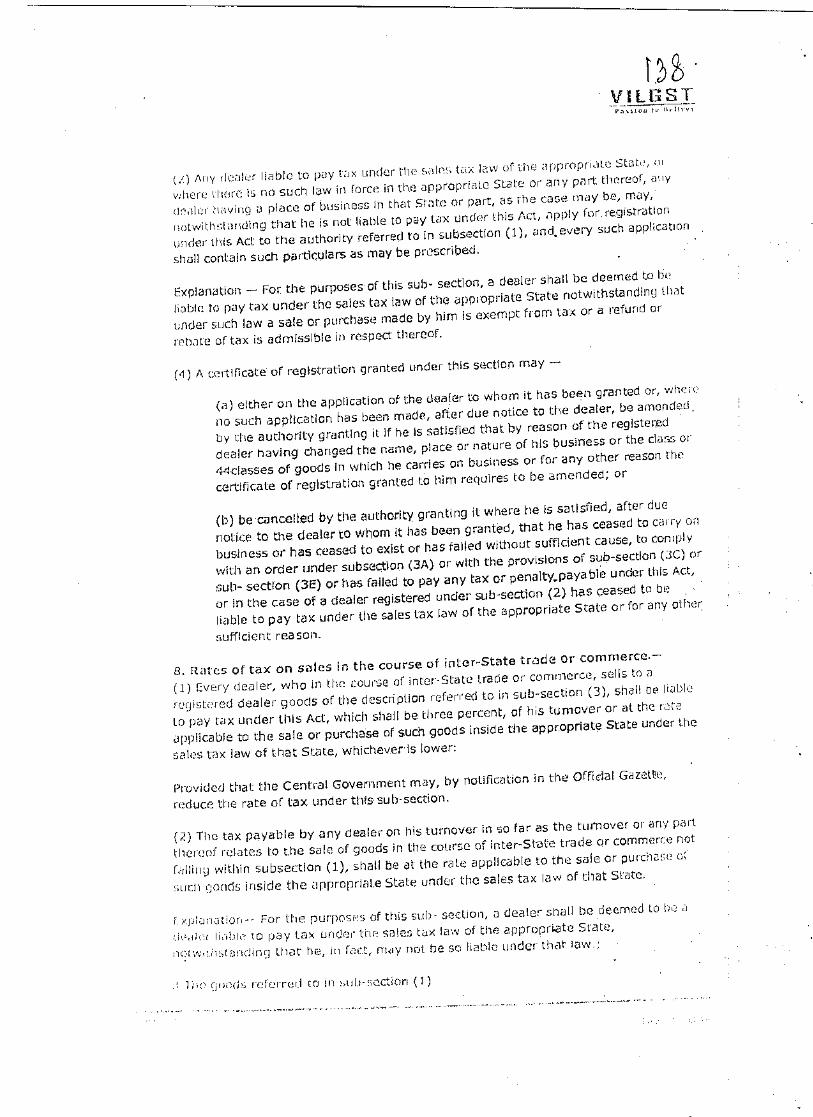

The Parliament, accordingly, enacted the Central Sales Tax Act,

1956. Section 2(d) thereof defines the term "goods" to include all

movable property except newspaper, stocks and shares. Section

6 is the charging Section. Section 8 provides for the rate of tax.

Under Section 8(1), if the sale is made to a registered dealer in

the course of inter-state sale of a class of goods mentioned in

Section 8(3), then there is a concessional rate of tax. A perusal of

Section 8(3)(b) would indicate that the class of goods which a

purchasing dealer is permitted to buy at a concessional rate

should be for either re-sale or use in the manufacture of other

goods or for use in telecommunications or mining or generation

of electricity.Registration of a dealer is provided for in Section-7.

Section 7(1) provides for compulsory registration where there is

liability under the C.S.T. Act, 1956. Section 7(2) provides for

optional registration where either a dealer is liable to pay Sales

Tax under the Sales Tax Law of an appropriate State or where he

is carrying on business.

The Petitioner got itself registered under the C.S.T. Act, 1956 in

the State of Jharkhand for Mining. H.S.D. was one of the goods

it was entitled to purchase at concessional rate. The certificate of

registration has been validated from time to time and is live and

continuing .

08.09.2016 The Constitution (101st Amendment) Act, 2016 was passed.

Article 246A and 279-A(5), which are relevant, now provide a

concurrent power to both Parliament and the States to make

laws with respect to Goods and Services Tax on the event of

supply. However, the Parliament has the exclusive power to tax

Goods or Services in the course of inter-state trade.

[11

However, six categories of Goods, including H.S.D. and Petrol

were left out from the GST regime for the time being. All other

Goods are now part of the GST regime.

05.05.2017 By the Taxation Laws (Amendment) Act, 2017, under Section

13(9)(b), the definition of 'Goods' in the C.S.T. Act was

amended to confine it to only six categories of Goods in line

with the above Constitutional Amendment. Similar Amendments

were carried out under the respective VAT Acts of the State.

01.07.2017 The Central Goods and Services Tax Act, 2017 as well as the

Jharkhand Goods and Services Tax Act were notified. Section 7

of these Acts contemplates a Tax on supply. Supply is deemed

to include a 'sale of goods'.

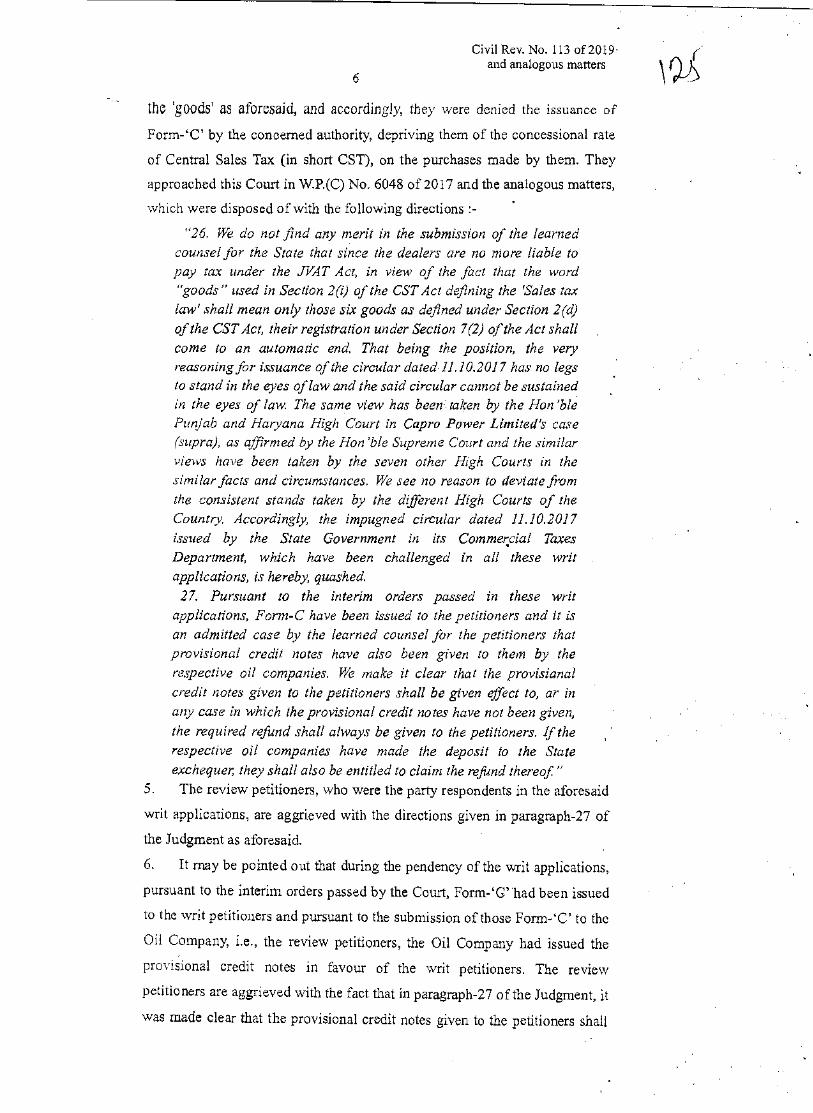

11.10.2017 State of Jharkhand issued a Circularproviding, inter alia, that in

view of the changed scenario, all registrations under the C.S.T.,

Act, ipso fact, stand nullified, in view of the fact that assesses are

no longer liable to pay tax under the Jharkhand VAT Act.

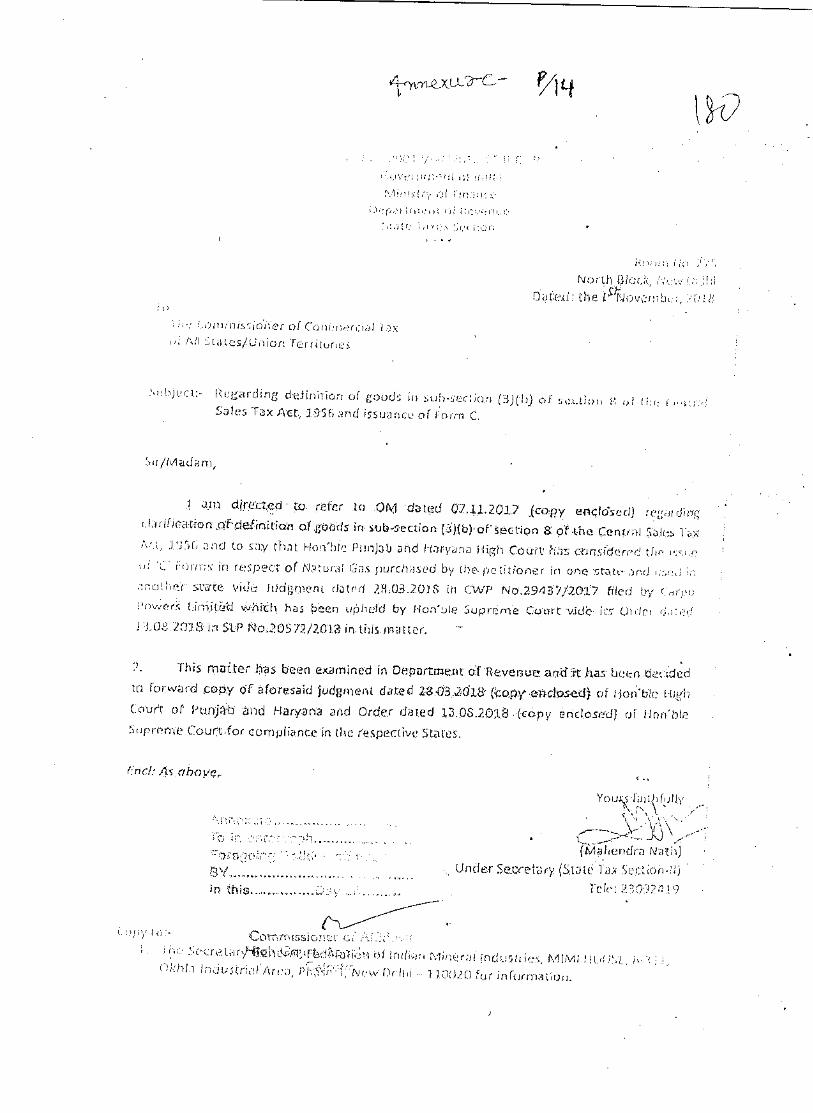

07.11.2017 Govt. of India, through the Ministry of Finance, issued an Office

Memorandum restricting the interpretation of the term 'Goods'

as amended vide Section 2(d) of the C.S.T. Act and has clarified

that purchase of H.S.D. would not be available at concessional

rate to a dealer.

17.05.2018 Hon'ble High Court of Jharkhand passed interim order directing

for issuance of Form 'C' during pendency of the writ

applications. In view of the said interim order, supply of H.S.D.

at concessional rate was resumed by the Oil Companies.

01.11.2018 Govt. of India, through Finance Department, subsequently,

issued directions to all the States/Union Territories to follow the

decision of the Hon'ble Punjab and Haryana High Court.

IV

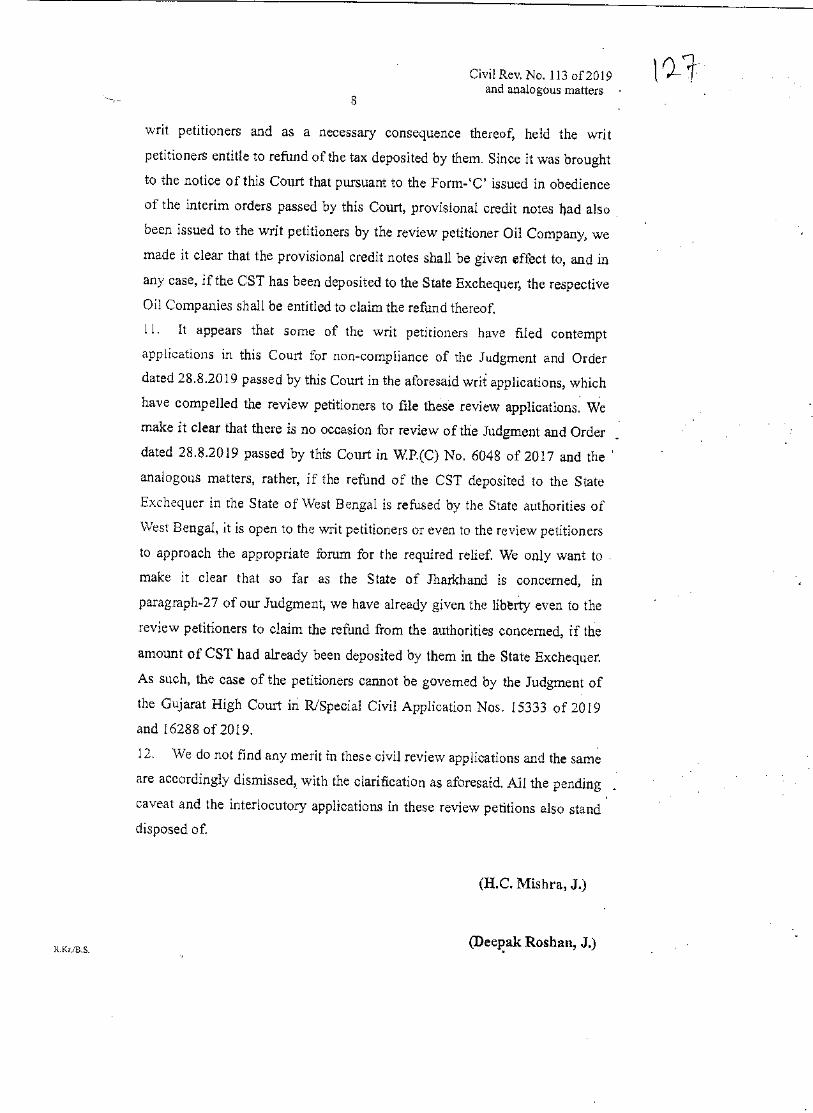

28.08.2019

17.10.2020

Ultimately, the Hon'ble High Court of Jharkhand, vide its

Judgment and order dated 28.08.2019 passed in W.P.(T) No.

6048 of 2017 and analogous cases, was pleased to quash the

Circular dated 11.10.2017 issued by the State of Jharkhand.

Against said Judgment, BPCL filed Review application before

the Hon'ble High Court of Jharkhand.

Review application filed by BPCL was dismissed by the Hon'ble

High Court of Jharkhand and liberty was given to BPCL as well

as writ petitioners, including the present Petitioner, to take steps

in accordance with law to claim refund from the authorities of

West Bengal.

30.06.2020 Petitioner was communicated a copy of the Order of Assessment

passed by Respondent No.3 for the period 01.04.2017 to

31.03.2018, wherein, despite the fact that BPCL submitted

Declaration Form `C" furnished by the Petitioner to the

authority of the State of West Bengal, said Form 'C' was not

accepted by the authority of the State of West Bengal and, thus,

consequentially, excess tax realized and deposited by BPCL to

the State of West Bengal was not ordered to be refitnded by the

authorities of the State of West Bengal.

28.03.2018 High Court of Punjab and Haryana , in the case of Capro Power Ltd. Vs. State of Haryana & on. passed order for refund of

differential tax, which has been realized by the Oil Companies.

13.08.2018 Hon'ble Supreme Court dismissed the Special Leave to Appeal,

wherein the decision of the Hon'ble High Court of Punjab and

Haryana was challenged.

VII

'V

18.05.2018

Hon'ble Rajasthan High Court quashed similar Circular issued

by the State of Rajasthan and, while quashing the said Circular,

ordered for refund of the differential tax which was realized on

account of purchase of H.S.D. at full rate of tax.

18.12.2019 Hon'ble High Court of Gujarat was pleased to allow the writ

application filed by J.K. Cement Ltd. and directed the authorities

of the State of Gujarat to directly grant refund to the purchaser as

the seller has already deposited the tax with the State authorities.

11.01.2021 Petitioner filed representation before Respondent No.2 claiming

refund of the differential tax directly from the State of West

Bengal, but, in spite of filing of said representation, till today, no

order has been passed by the Respondent-State of West Bengal.

2021 Recently, in the Finance Bill, 2021, an amendment has been

sought to be introduced and the earlier provision of Section

8(3)(d) of the C.S.T. Act is sought to be substituted vide Section

141 of the Finance B 11, 2021.

Hence, the present Writ Petition

DISTRICT KOLKATA

IN THE HIGH COURT AT CALCUTTA

CONSTITUTIONAL WRIT JURISDICTION

APPELLATE SIDE

W.P. A NO.526,8 OF 2021

In the matter of :

An application under Article 226 of the

Constitution of India:

And

In the matter of :

M/s.Ambey Mining Private Ltd & anr..

Petitioners

-Versus-

The State of West Bengal & ors.

... Respondents

QUESTIONS OF LAW

1. Whether the impugned order dated 29.06.2020, to the extent the claim of refund in respect of differential tax realized by Respondent-Reliance Industries from Petitioner No.1 and paid by Reliance Industries to the State of West Bengal has been rejected, is neither sustainable in law nor on facts and the same is liable to be quashed/set aside?

II. Whether Petitioner No. 1 is directly aggrieved by the Assessment Order dated 29.06.2020 passed in the case of Respondent-Reliance Industries, as due to non-acceptance of statutory Form 'C' by the authority of the State of West Bengal, claim of refund of differential tax has been denied to the Petitioner?

Ill. Whether Petitioner No.1 is legally entitled for refund of the amount of Rs. 4,88,63,067/- being the amount of differential tax realized from the Petitioner by Respondent-Reliance Industries and deposited with the State of West Bengal

VI

VII

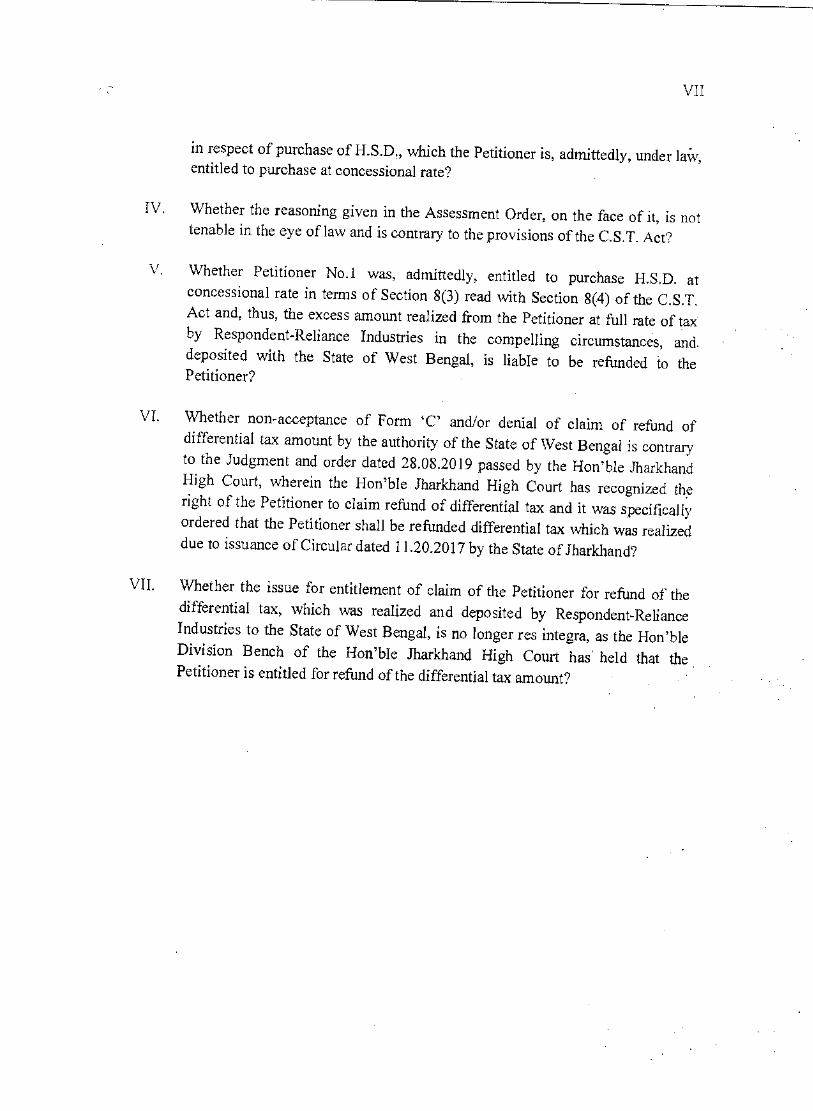

in respect of purchase of H.S.D, which the Petitioner is, admittedly, under law'', entitled to purchase at concessional rate?

IV. Whether the reasoning given in the Assessment Order, on the face of it, is not tenable in the eye of law and is contrary to the provisions of the C.S.T. Act?

V. Whether Petitioner No.I was, admittedly, entitled to purchase H.S.D. at concessional rate in terms of Section 8(3) read with Section 8(4) of the C.S.T. Act and, thus, the excess amount realized from the Petitioner at full rate of tax by Respondent-Reliance Industries in the compelling circumstances, and.

deposited with the State of West Bengal, is liable to be refunded to the Petitioner?

VI. Whether non-acceptance of Form 'C' and/or denial of claim of refund of differential tax amount by the authority of the State of West Bengal is contrary to the Judgment and order dated 28.08.2019 passed by the Hon'ble Jharkhand High Court, wherein the Hon'ble Jharkhand High Court has recognized the right of the Petitioner to claim refund of differential tax and it was specifically ordered that the Petitioner shall be refunded differential tax which was realized due to issuance of Circular dated 11.20.2017 by the State of Jharkhand?

VII. Whether the issue for entitlement of claim of the Petitioner for refund of the

differential tax, which was realized and deposited by Respondent-Reliance Industries to the State of West Bengal, is no longer res Integra, as the Hon'ble

Division Bench of the Hon'ble Jharkhand High Court has held that the Petitioner is entitled for refund of the differential tax amount?

FIE' /*

DISTRICT K• • ' *Ct

INT-c

T AT CALCUTTA

CONSTITUTIONAL WRIT JURISDICTION

APPELLATE SIDE

W.P. A. NO. 5-866 OF 2021

05P

ff

In the matter of :

An application under Article 226 of

the Constitution of India:

-AND-

In the matter of :

1. AMBEY MINING PRIVATE LIMITED,

Company registered under • the

Companies Act, 1956), having its

registered office at 8, A.J.C. Bose

Road, Circular Court, 9lb Floor,

Kolkata-700 017 (West Bengal).

2. Shyam Lal Naik, aged about 50

Years, son of Late Rabi Narayan

Naik, resident of 63,Aswini Nagar,

P.O-Regent Park, Jadavpur Police

Station , Kolkata-700040.

Petitioners

litirge:INDIA

' Nat.

2

it

The State of West Bengal, through its

Secretary, Department of Finance,

Government of West Bengals, having

its office at Nabanna (14th Floor), 325,

Sarat Chatterjee Road, Shibpur,

Howrah-711I022.

2. CoMmissioner of Commercial

Taxes, West Bengal, having its office

at 14, Beliaghata Road, Kolkata- 700

015.

3. Joint Commissioner, Commercial

Taxes, Large Taxpayer Unit, Govt. of

West Bengal, having its office at 14,

Beliaghata Road, Kolkata-700 015.

4. Reliance Industries Ltd., through its

Regional Head, having its office at

Godrej Waterside, Tower-II, 17"

18 h̀ Floor, Block-DP, Salt Lake,

Sector-V, Kolkata, PIN 700091.

1.

.... Respondents

To,

The Hon'ble Thottathil B. Radhakrishnan, the Chief Justice and His

companion Justices of the said Hon'ble Court.

The humble petition on behalf of the

petitioners, above-named,

Most Respectfully Sheweth:-

I. Your Petitioner No.1 is a company registered under the

Companies Act, 1956 and its Directors are citizens of India and,

thus, entitled to their constitutional and/or statutory. rights.

2. Your Petitioner No.2 is a citizen of India and is working as

Senior Manager of Petitioner No.1-company, Your Petitioner

No.2 is highly interested in the business.

3. Your Petitioners, in the instant writ petition, is challenging the

Assessment Order dated 29.06.2020 passed by Respondent No.3

in respect of assessment proceedings pertaining to Reliance

Industries Ltd. (hereinafter referred to as 'Reliance Industries'

3

4

for short), to the extent the claim of refund in respect of

differential tax realized by Respondent-Reliance Industries Ltd.

(hereinafter referred to as 'Reliance Industries' for short) from

the Petitioner and paid by Reliance Industries to the State of West

Bengal, has been rejected despite the fact that Respondent-

Reliance Industries already submitted Form 'C' in respect of the

said transactions and even issued Provisional Credit Notes in

favour of the Petitioner No.1-company (hereinafter referred to as

`Petitioner' for short). Your Petitioner is further prayMg for a

Writ of Mandamus directing the Respondent-State of West

Bengal to refund the amount of Rs. 4,88,63,067/- , being the

amount of differential tax realized from the Petitioner by

Respondent-Reliance Industries and deposited with the State of

West Bengal in respect of purchase of H.S.D.

4. Your Petitioners state that the Petitioner is engaged in the

business of Mining and is carrying out the said business across

various States of the country, including the State of Jharkhand.

The present issue relates to the purchase of H.S.D.by the

Petitioner-company in respect of its mining operations pertaining

5

to the State of Jharkhand, wherein the Petitioner was, admittedly

registered under the Jharkhand Value Added Tax Act, 2005 and

also under the Central Sales Tax Act, 1956 (hereinafter referred

to as `C.S.T. Act' for short).

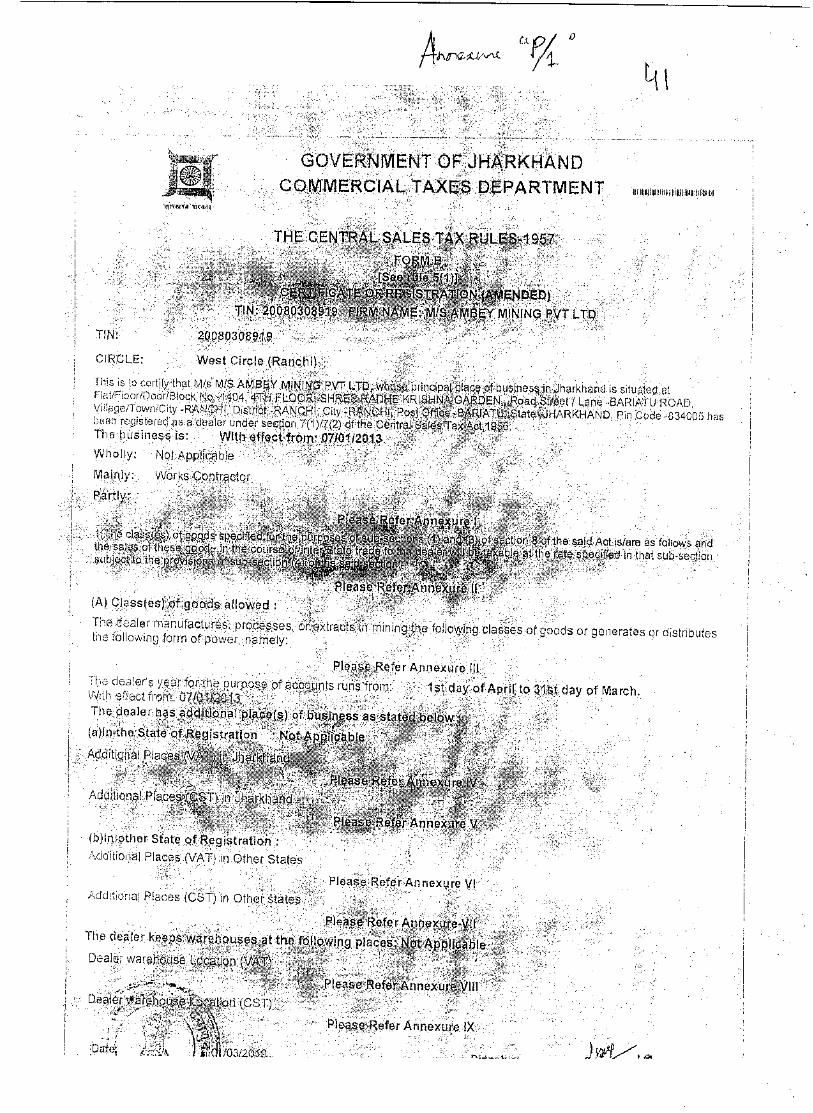

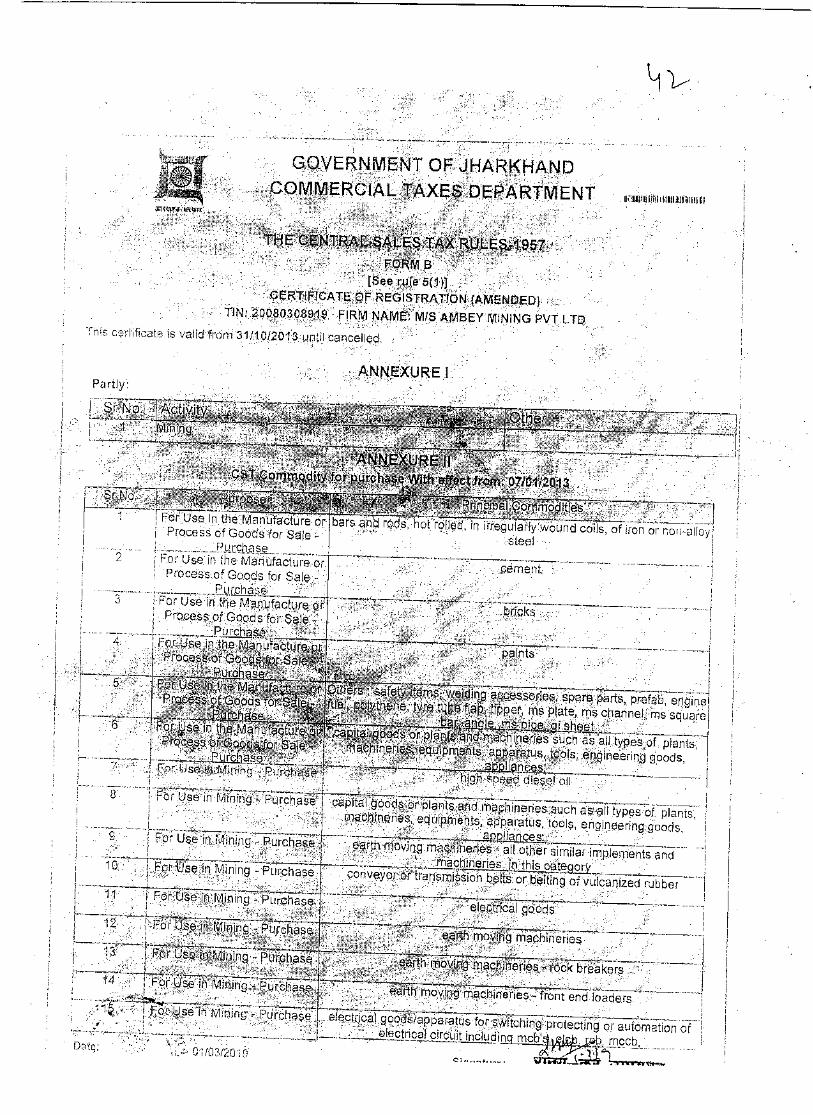

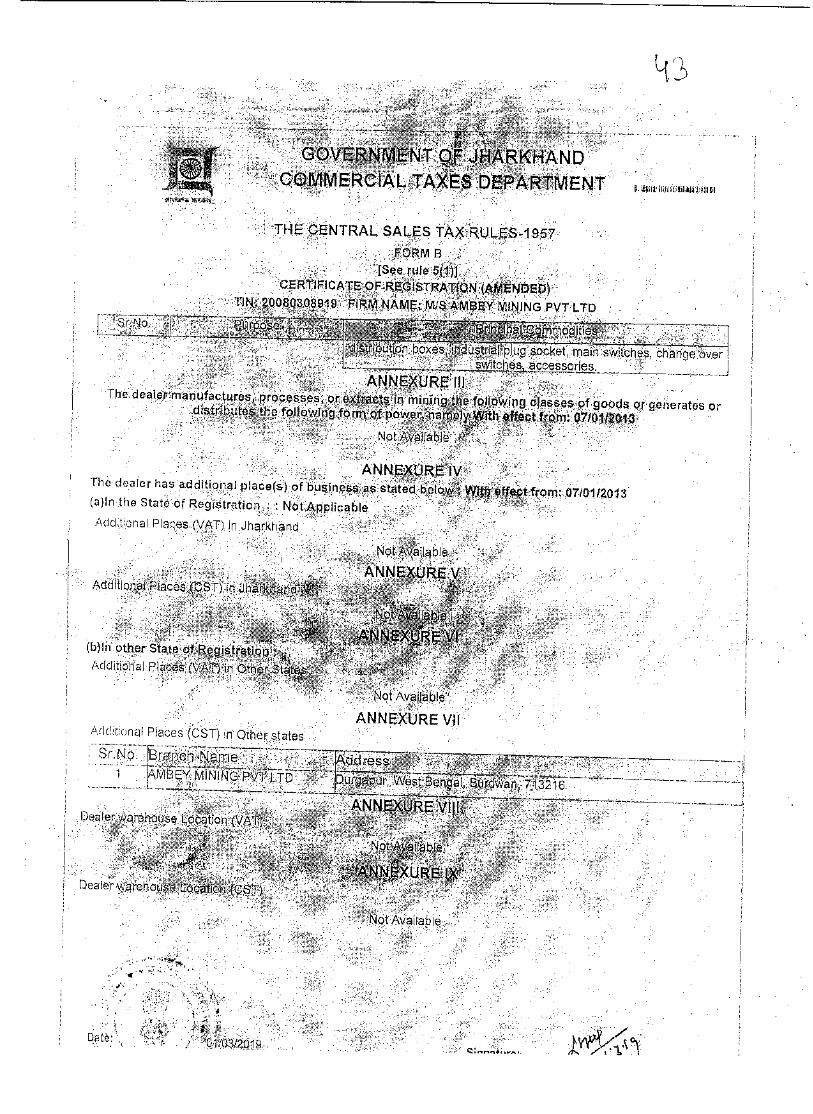

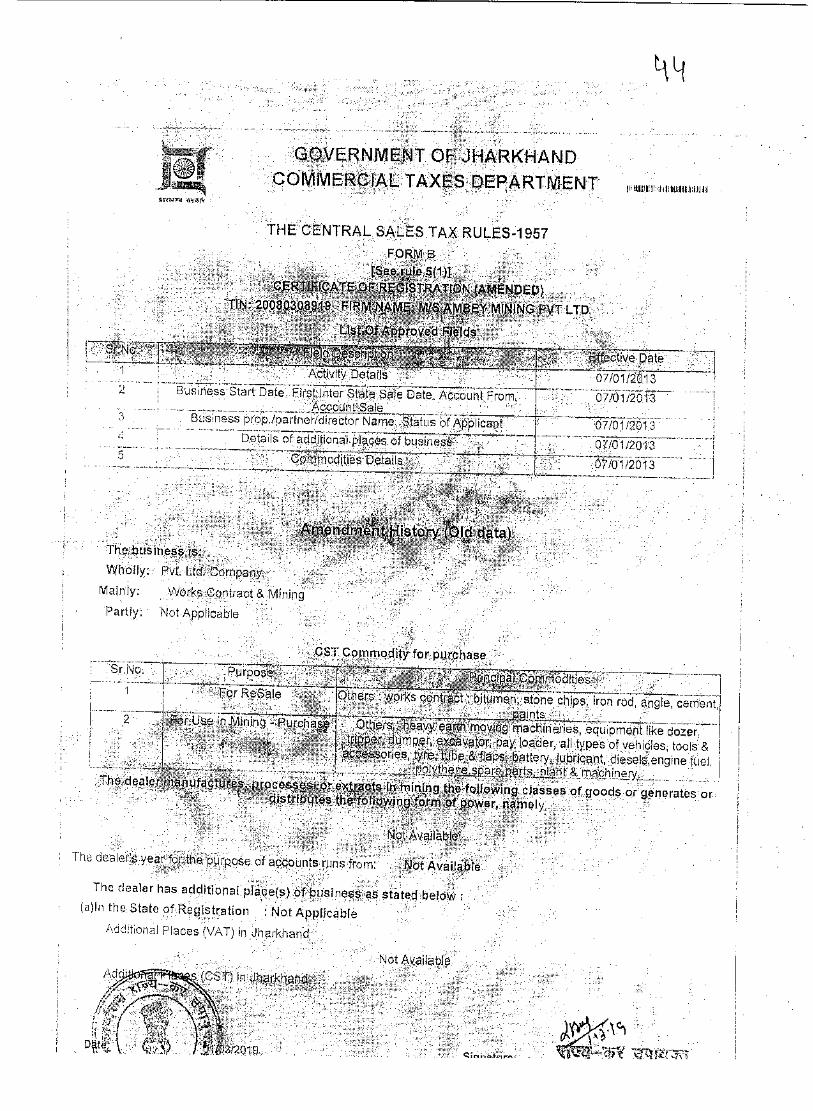

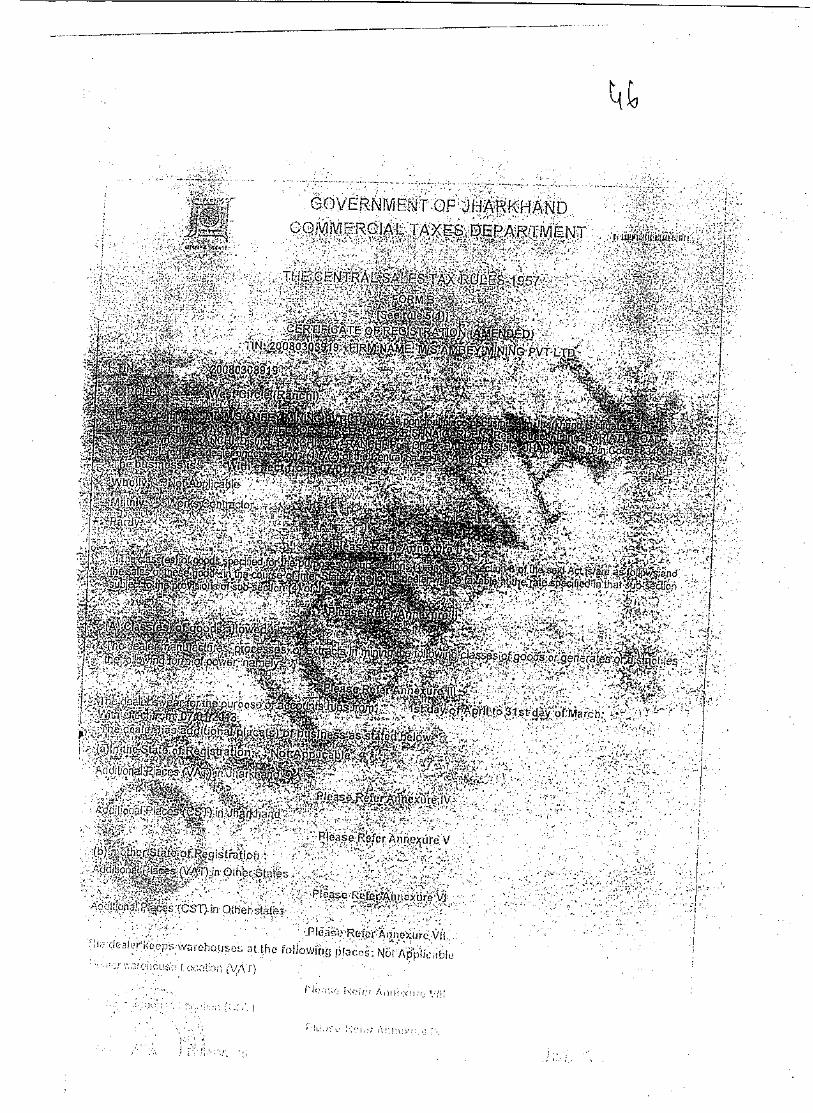

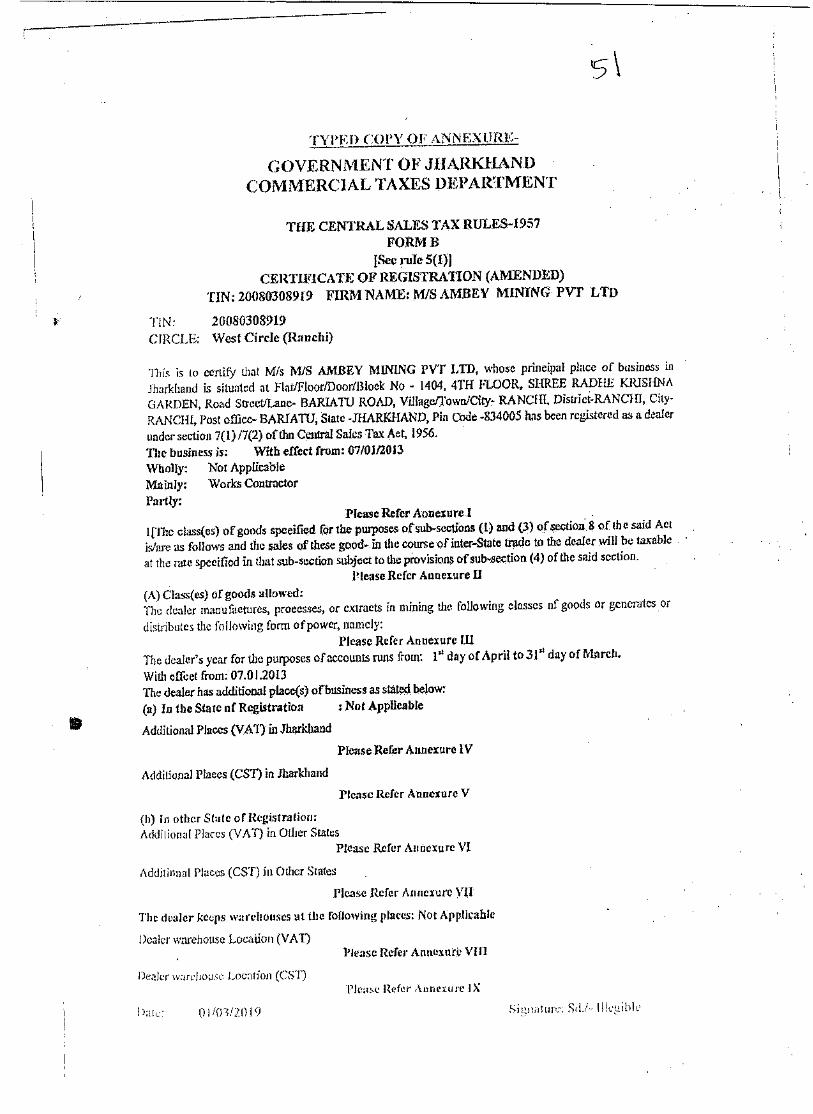

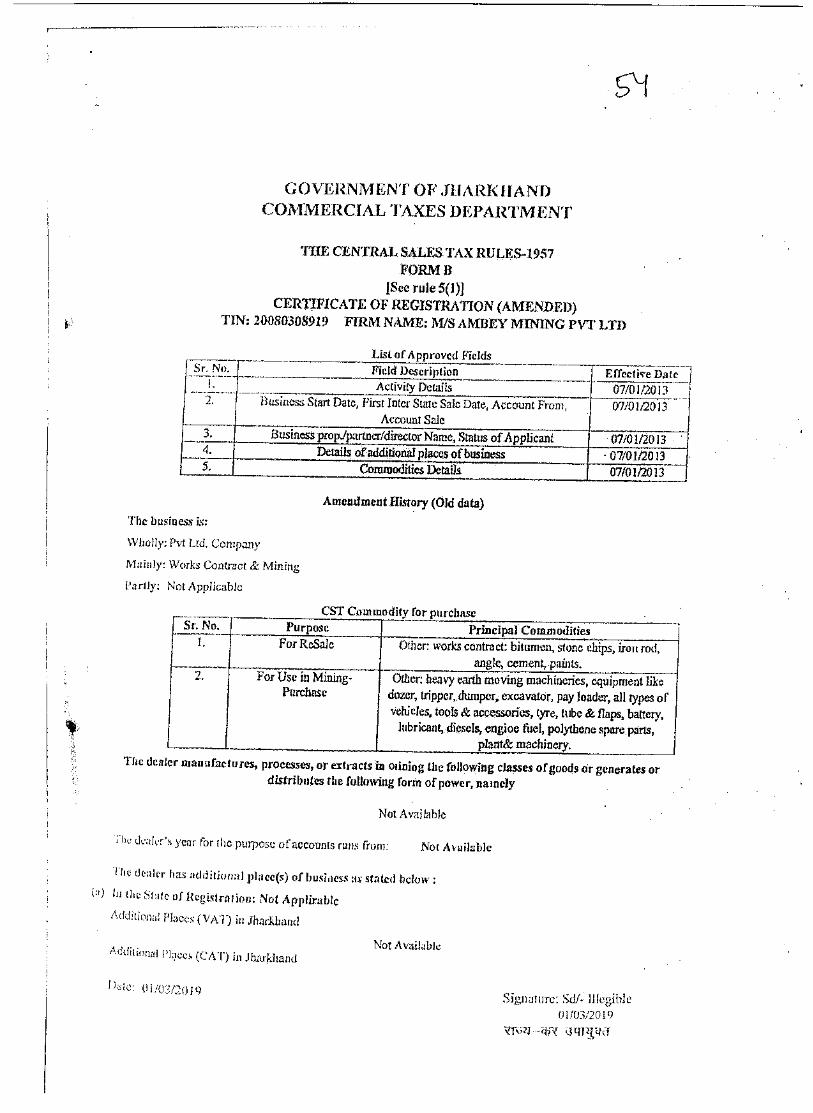

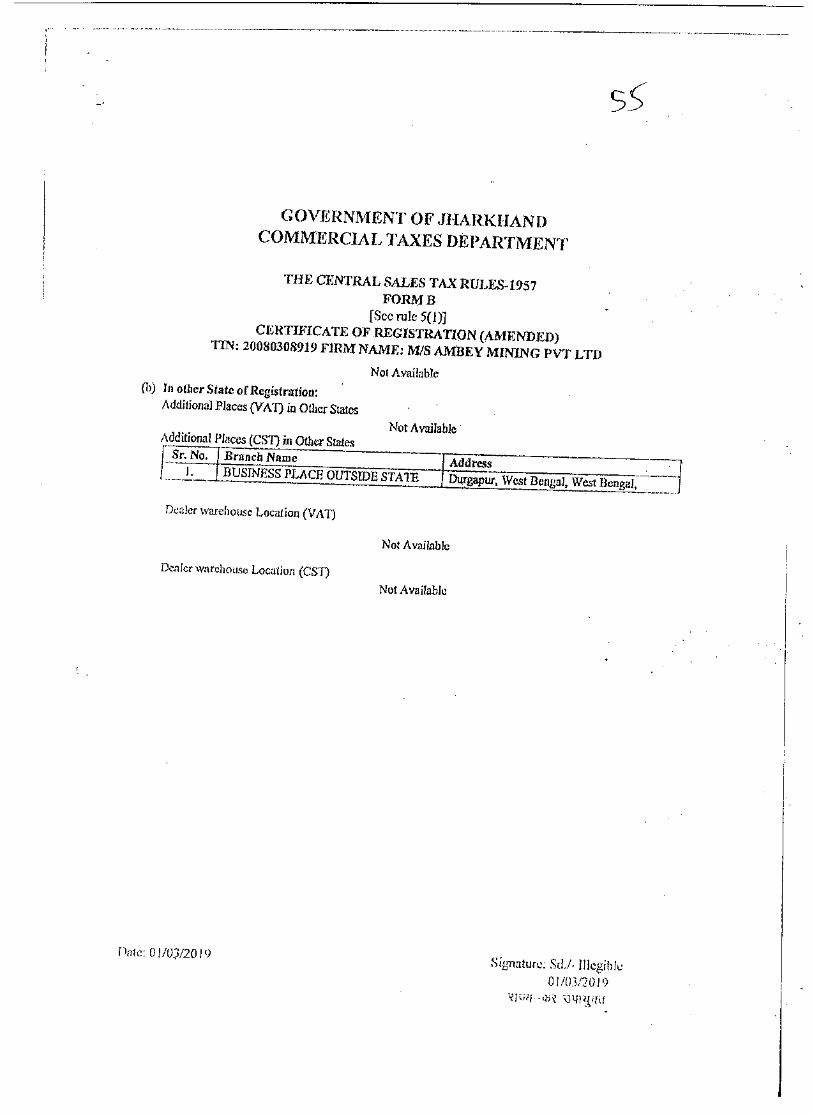

A copy of the Registration Certificate granted under the

C.S.T. Act, in respect of its mining operation in the State of

Jharkhand, is annexed hereto and marked as Annexure `13- I '

5. Your Petitioners categorically state that under the Certificate of

Registration of your Petitioner under the C.S.T. Act, the

Petitioner was entitled to purchase H.S.D. at concessional rate for

its use in mining, and, the Petitioner was regularly executing

contracts in the State of Jharkhand pertaining to mining, for

which it purchased H.S.D. at concessional rate from the Oil

Companies, situated in the State of West Bengal, including

Indian Oil Corporation Ltd., Bharat Petroleum Corporation Ltd.

and Reliance Industries Ltd. The present writ application pertains

to purchase of H.S.D. by the Petitioner from Respondent-

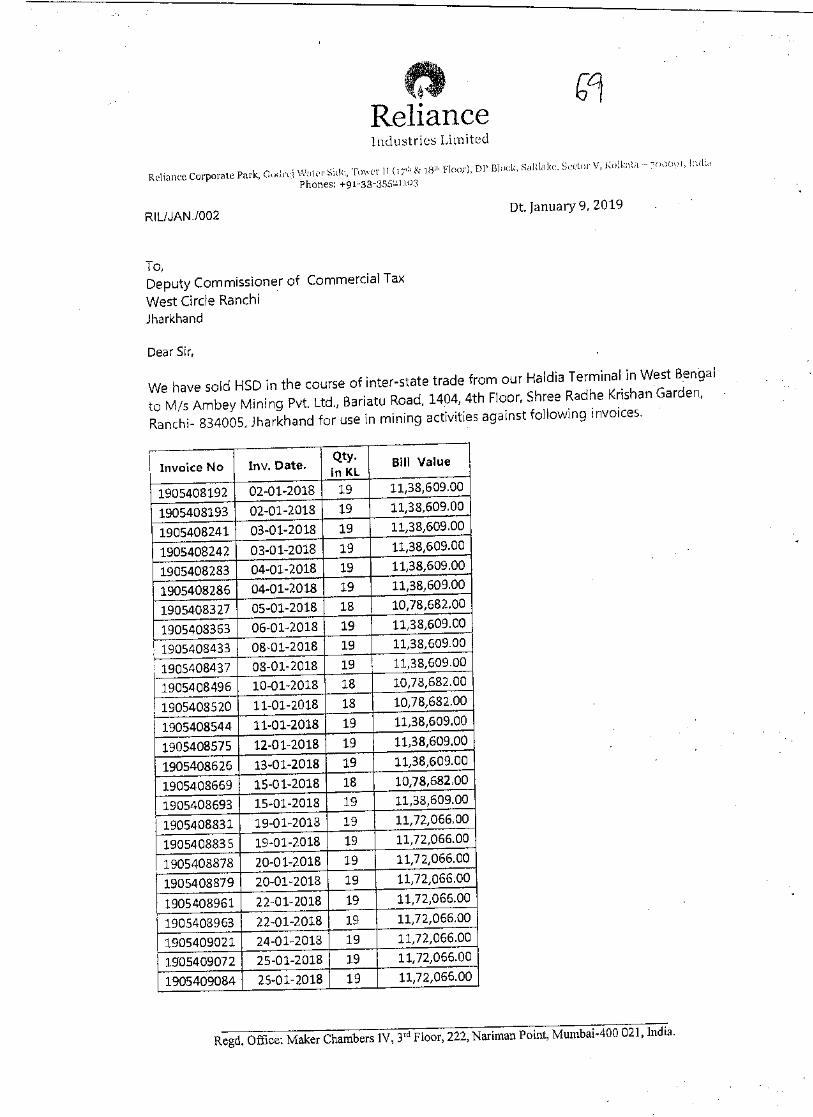

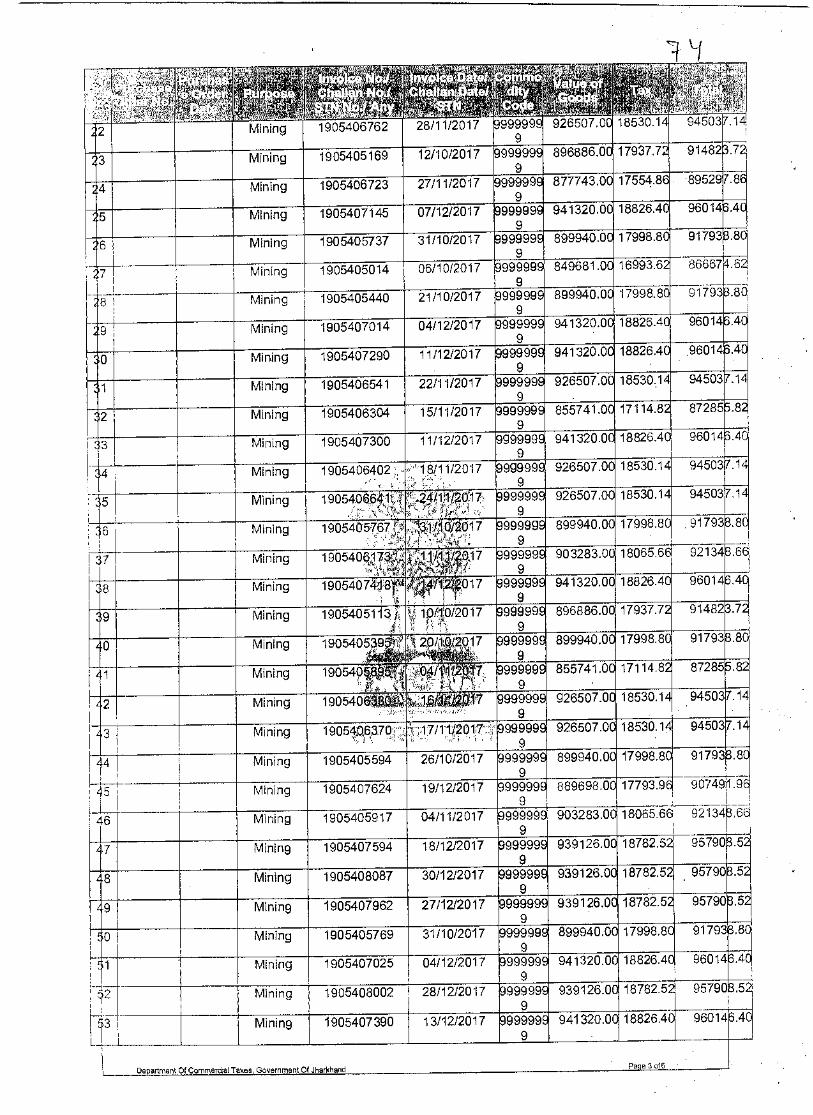

Reliance Industries, details of which are mentioned hereinafter in

subsequent paragraphs.

6

6. Your Petitioners state that the Petitioner was regularly purchasing

H.S.D. from Respondent-Reliance Industries, which was supplied

to the Petitioner by way of inter-State transaction from the State

of West Bengal to the State of Sharkhand and said purchases were

made by the Petitioner at concessional rate in terms of Sections

8(1) and 8(3) of the C.S.T. Act, and, there was absolutely no

dispute in respect of the said fact.

7. Your Petitioners state that in terms of the provisions of the C.S.T.

Act and the corresponding C.S.T. Rules, 1957, the Petitioner, in

respect of its purchases made at concessional rate, was required

to submit statutory Form 'C' to Respondent-Reliance Industries

and, in turn, the said statutory Form 'C' was deposited with the

Assessing Authority of Respondent-Reliance Industries for

completing the transaction of sale of H.S.D. at concessional rate

to the Petitioner.

8. However, your Petitioners state and submit that with effect from

1st July, 2017, Goods and Service Tax regime was implemented

in the country of India and various Taxes like Value Added Tax,

Excise Duty, Service Tax etc. were subsumed under GST regime.

9. Your Petitioners state that due to implementation of GST Regime

in India, an amendment was also brought to the provision of CST

Act, 1956, whereby clause (d) of Section-2 of the CST Act, 1956,

which contained the definition of 'goods', was amended by the

Taxation Laws (Amendment) Act, 2017 and the 'goods' defined

under Section 2(d) was confined to the following six goods only,

namely;

(1) Petroleum Crude;

(2) High Speed Diesel ( HSD);

(3) Motor Spirit( commonly known as Petrol)

(4) Natural Gases,

(5) Aviation Turbine Fuel and

(6) Alcoholic Liquor for human consumption.

10.Your Petitioners state that aforesaid amendment carried out in the

definition of 'goods' under Section- 2(d) of the CST Act, 1956

resulted into varied interpretation being adopted by one or other

State Governments with respect to eligibility of a manufacturing

or mining dealer to purchase specified goods at concessional

rates under Section- 8(1) read with Section- 8(3)(b) of the CST

Act, 1956.

8

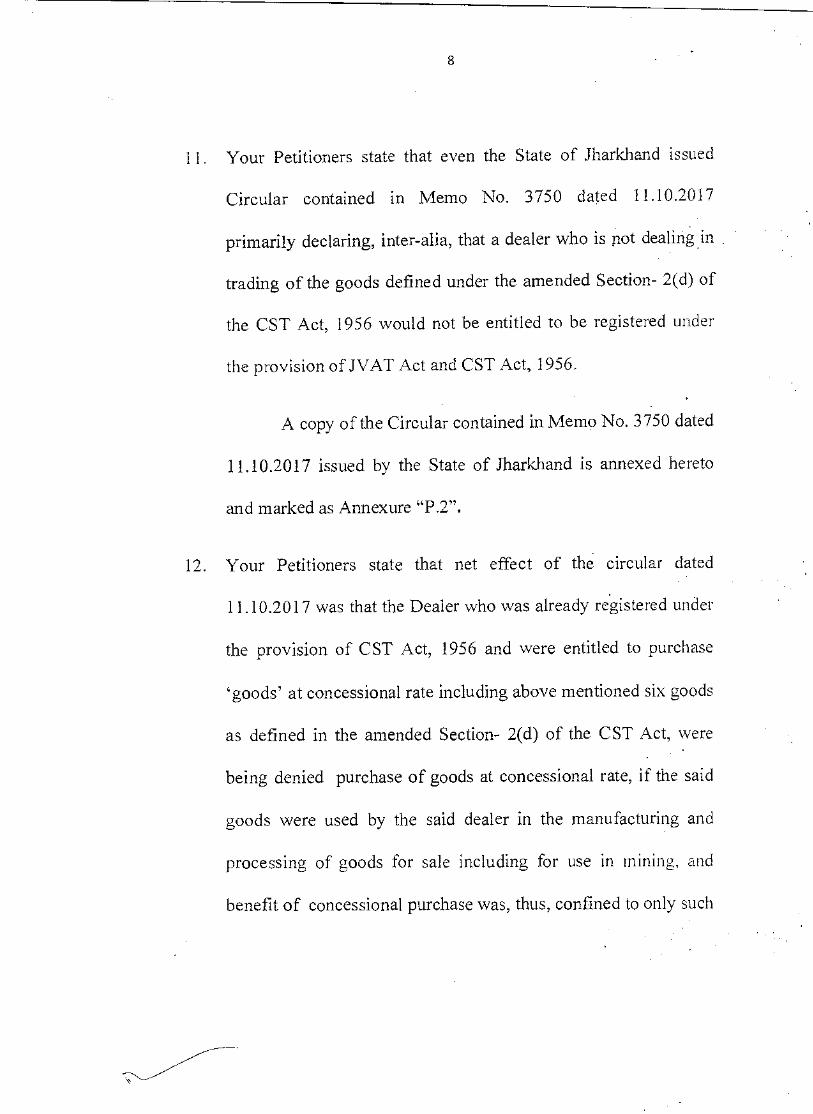

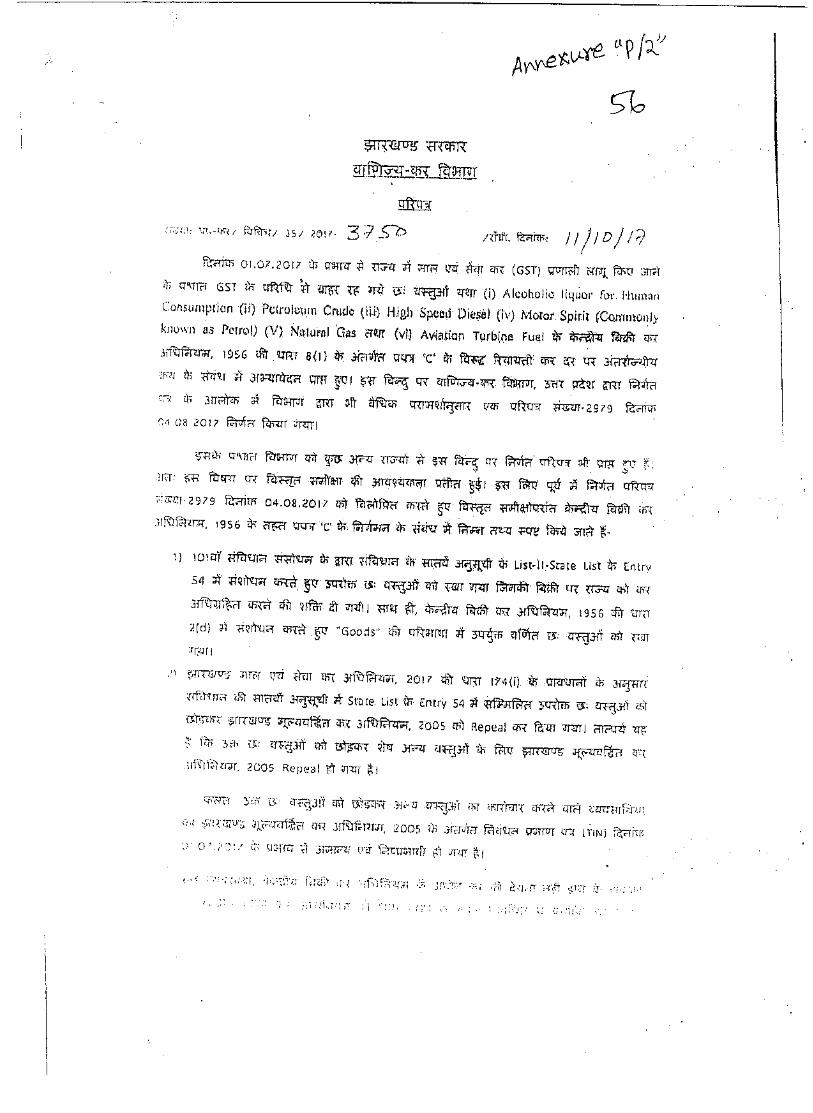

11 Your Petitioners state that even the State of Jharkhand issued

Circular contained in Memo No. 3750 dated 11.10.2017

primarily declaring, inter-alia, that a dealer who is not dealingin

trading of the goods defined under the amended Section- 2(d) of

the CST Act, 1956 would not be entitled to be registered under

the provision of JVAT Act and CST Act, 1956.

A copy of the Circular contained in Memo No. 3750 dated

11.10.2017 issued by the State of Jharkhand is annexed hereto

and marked as Annexure "P.2".

12. Your Petitioners state that net effect of the circular dated

11.10.2017 was that the Dealer who was already registered under

the provision of CST Act, 1956 and were entitled to purchase

`goods' at concessional rate including above mentioned six goods

as defined in the amended Section- 2(d) of the CST Act, were

being denied purchase of goods at concessional rate, if the said

goods were used by the said dealer in the manufacturing and

processing of goods for sale including for use in mining, and

benefit of concessional purchase was, thus, confined to only such

9

dealers who were purchasing the above referred six goods for

resale.

13. Your Petitioners state that after issuance of the aforesaid Circular

dated 11.10.2017, respective Oil Companies including Reliance

Industries stopped supplying H.S.D.at concessional rate by way

of inter-State sales to the dealers situated within the State of

Jharkhand.

14. Your Petitioners state that said Circular dated 11.10.2017 issued

by the State of.lharkhand was completely contrary to the mandate

of the provision of the CST Act, 1956 and said Circular was

challenged by several Companies before the Hon'ble High Court

of Jharkhand at Ranchi.

15. Your Petitioners state that the Petitioner also filed writ petition

before the Hon'ble High Court of Jharkhand W.P.(T) No. 7107,

inter alia, challenging the said Circular dated 11.10.2017.

16. Your Petitioners state that the several writ petitions including the

aforesaid writ petition filed by the Petitioner were taken up for

consideration by the Hon'ble High Court of Jharkhand on various

10

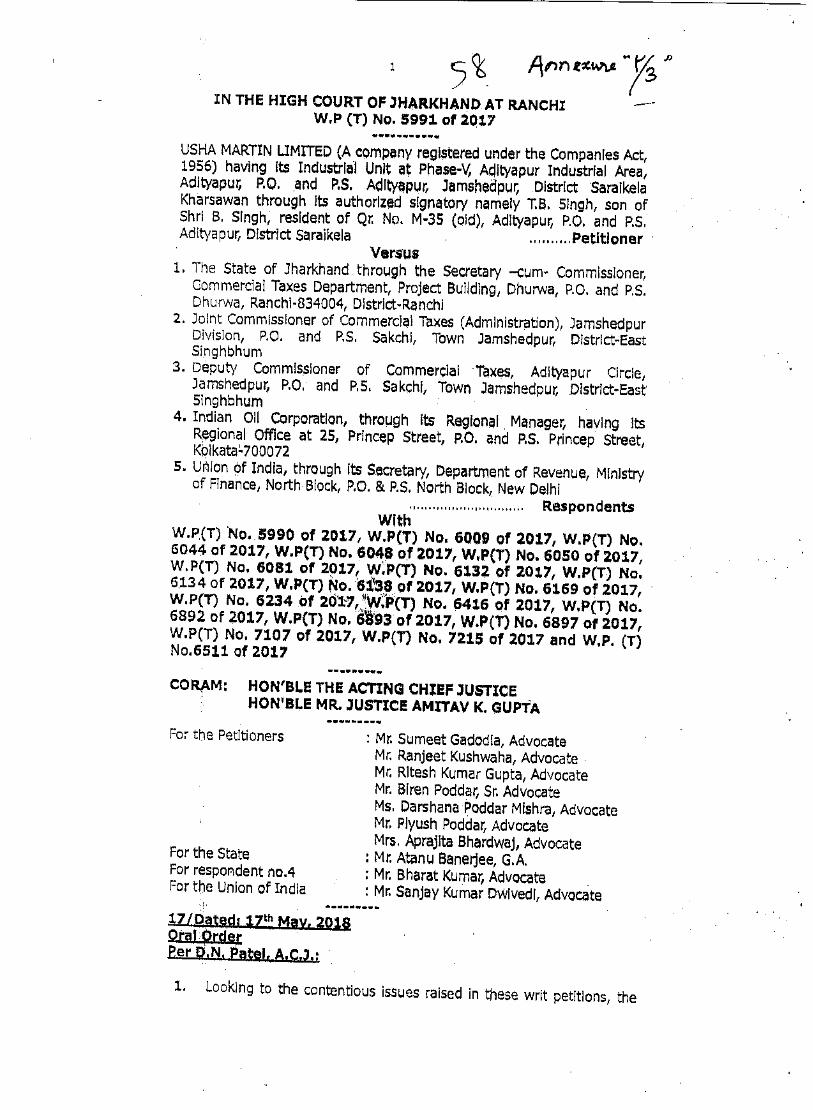

dates, and, the Hon'ble Jharkhand High Court, vide its order

dated 17111 May, 2018 passed in W.P.(T) 6048 OF 2017 and

analogous cases, including the writ application filed by the

Petitioner, was pleased to pass an interim order directing for

issuance of Form 'C' during pendency of the writ applications.

A copy of the Interim Order dated 17th May, 2018 is annexed

hereto and marked as Annexure

17. Your Petitioners state that in view of the Interim . Order passed by

the Hon'ble High Court of Jharkhand dated 17.05.2018, supply of

H.S.D at concessional rate was resumed by the Oil Companies,

but there was no uniform resumption of supply of H.S.D Oil to

all the dealers at concessional rate by the Oil Companies and

one or other conditions were being imposed by the Oil

Companies for resumption of supply at concessional rate.

18. Your Petitioners state that after implementation of the G.S.T.

regime, due to widespread confusion regarding entitlement to

purchase H.S.D. at concessional rate, including issuance of

Circular dated 11.10.2017 issued by the State of Jharkhand,

Respondent-Reliance Industries supplied H.S.D. Oil to the

Petitioner by charging full rate of tax instead of concessional rate

of tax, despite the fact that Petitioner was entitled to purchase

H.S.D. at concessional rate.

19. Your Petitioners state that after the interim order was passed by

the Hon'ble High Court of Jharkhand, your Petitioner approached

the Respondent-Reliance Industries to issue Credit Notes to the

Petitioner pertaining to differential tax realized from the

Petitioner in respect of supply of H.S.D., which was supplied at

full rate instead of concessional rate, in order to enable the

Petitioner to obtain statutory Form 'C' for the aforesaid

intervening period. Pursuant to the request made by the

Petitioner, Respondent-Reliance Industries even issued

Provisional Credit Notes/Credit Notes in favour of the Petitioner

in respect of differential tax pertaining to its above-mentioned

four business establishments in the State of Jharkhand. Your

Petitioner has been advised to annex sample copy of Provisional

Credit Note/Credit Note issued by Respondent-Reliance

Industries in favour of the Petitioner.

12

Sample copy of Provisional Credit Notes/Credit Notes are

annexed hereto and collectively marked as Annexure `P-4'.

20. Your Petitioners state that from bare perusal of the Provisional

Credit Note/Credit Note issued to the Petitioner by Respondent-

Reliance Industries, it would be evident that. Respondent-

Reliance Industries, in the said Credit Note, has specifically

stated that the Credit Notes were issued in favour of the

Petitioner in terms of the interim order passed by the Hon ble

High Court of Jharkhand in order to enable the Petitioner to

obtain Fonn 'C' and, further, it was stated that Respondent-

Reliance Industries supplied H.S.D. to the Petitioner at full tax

basis and the said amount has been deposited with the Sales Fax

authorities of the State of West Bengal. In the said Credit Note, it

was also mentioned that after Form 'C' for the intervening period

is supplied to Respondent-Reliance Industries, the same would be

submitted before the Sales Tax authorities of the State of West

Bengal at the time of assessment and, on acceptance of said Fon

`C', benefit of differential tax credit would be passed on to the

Petitioner.

13

21. Your Petitioners state that pursuant to issuance of aforesaid

Credit Notes by Respondent-Reliance Industries in favour of the

Petitioner, the Petitioner applied for statutory Form 'C' before the

authorities of the State of Jharkhand and subsequent to the said

application filed by the Petitioner, the Petitioner has been issued

statutory Form `C' for the entire intervening period, during

which, the Petitioner was compelled, for no fault of its own, to

purchase H.S.D. at full rate of tax. The Petitioners have been

advised to annex copies of Form 'C' obtained from the State of

Jharkhand in favour of the Respondent-Reliance Industries.

Copies of Form `C' obtained from the State of Jharkhand

in favour of Respondent-Reliance Industries are annexed hereto

and collectively marked as Annexure P-5 series'.

22. Your Petitioners, at this stage, categorically state herein that for

the period, during which the Petitioner was compelled to

purchase H.S.D. at full rate of tax, for no fault of its own, entire

Form 'C' for the said period have been obtained by the Petitioner

from the authorities of the State of Jharkhand and the same have

also been duly furnished by the Petitioner to Respondent-

14

Reliance Industries for depositing the same with the authorities of

the State of West Bengal.

23. Your Petitioners state that, in the meantime, the Hon'ble High

Court of Jharkhand, ultimately, vide its Judgment and order dated

28.08.2019 passed in W.P.(T) No. 6048 of 2017 and analogous

cases, including the case of the Petitioner being W.P.(T) No.7107

of 2017, was pleased to quash the circular dated 11.10.2017

issued by the State of Jharkhand . While quashing the circular

issued by the State of Jharkhand, vide paragraph-27 of the said

judgment, the Hon'ble Jharkhand High Court has further held as

under:-

"27.Pursuant to the interim orders passed in these

writ applications, Form-C have been issued to the

petitioners and it is an admitted case by the

learned counsel for the petitioners that provisional

credit notes have also been given to them by the

respective oil companies. We make it clear that the

provisional credit notes given to the petitioners

15

shall be given effect to, or in any case in which the

provisional credit notes have not been given, the

required refund shall always be given to the

petitioners. If the respective oil companies have

made the deposit to the State exchequer, they shall

also be entitled to claim the refund thereof."

A copy of the Judgment and order dated 28.08.2019 ,

passed by Hon'ble Jharkhand High Court in W.P.(T) No.

6048 of 2017 and analogous cases is annexed hereto and

marked as Annexure

24. Your Petitioners state that Indian Oil Corporation Ltd. (for short

`IOCL') filed Review Application before the Hon'ble High

Court of Jharkhand against the Judgment and order dated

28.082019 passed in W.P. 6048 of 2017 and analogous cases,

primarily praying therein for modification of the impugned order

to the extent direction was given to Oil companies including

Reliance Industries to refund the differential tax which has been

16

realized from the dealers for the period when H.S.D. was

supplied to the dealers at full rate of tax.

25. Your Petitioners further state that IOCL primarily prayed for

review of the Judgment of the Hon'ble Jharkhand High Court, by

stating, inter-alia, that IOCL deposited Form "C" with the

Assessing Authority of West Bengal, but the said authority, did

not accept the said Form "C" and accordingly, IOCL was not able

to pass-on the benefit of refund as ordered by the Hon'ble High

Court of Jharkhand vide its Judgment/order dated 28.08.2019

26. Your Petitioners state that above-mentioned Review application

was taken up for consideration by the Hon'ble High Court of

Jharkhand on 17.10.2020 and the said Review Application was

dismissed by the Hon'ble High Court of Jharkhand. However,

while dismissing the said review application, the Hon'ble High

Court of Jharkhand noted, inter-alia, that the refund claimed by

Coal Companies before the authorities of West Bengal has

already been rejected and, under the said circumstance, liberty

was given to Coal Companies as well as writ petitioners. to take

17

steps in accordance with law to claim refund from the authorities

of the West Bengal.

A web copy of the Order passed in Civil Review No. 09

of 2020 is annexed hereto and marked as Annexure

27. Your Petitioners state that the petitioner has been informed by

Respondent-Reliance Industries that Sales Tax authorities of the

State of West Bengal have not accepted Form 'C', which was

submitted by the Petitioner to Respondent-Reliance Industries

and, under the said circumstances, Respondent-Reliance

Industries advised the Petitioner to proceed directly before the

appropriate authority of the State of West Bengal for refund.

28. Your Petitioners state that the Petitioner was even communicated

a copy of the order of assessment passed by Respondent No.3 for

the period 01.04.2017 to 31.03.2018, wherein despite the fact that

Respondent-Reliance Industries submitted Declaration Form 'C'

furnished by the Petitioner to the authority of the State of West

Bengal, said Foini 'C' was not accepted by the authority of the

State of West Bengal and, thus, consequentially, excess tax

18

realized and deposited by Reliance Industries to the State of West

Bengal was not ordered to be refunded by the authorities of the

State of West Bengal.

A copy of the Assessment Order dated 29.06.2020 along

with Demand Notice in Form No.4V is annexed hereto and

collectively marked as Annexure

29. From the facts mentioned hereinabove, it would be, thus, evident

that the Petitioner was compelled to purchase H.S.D. at full rate

of tax instead of concessional rate, despite the fact that Petitioner

was not at fault and, consequentially, the Petitioner Was issued

Provisional Credit Notes/Credit Notes by Respondent-Reliance

Industries and even statutory Declaration Forms 'C' were

furnished by the Petitioner to Respondent-Reliance Industries for

the period when the Petitioner was compelled to purchase H.S.D.

at full rate of tax. Thereafter, even Respondent-Reliance

Industries deposited said Forms 'C' with the authority of the

State of West Bengal, but said Forms `C' have not been accepted

by the authority of the State of West Bengal having- an effect of

denying the benefit of refund of differential tax to the Petitioner.

18

realized and deposited by Reliance Industries to the State of West

Bengal was not ordered to be refunded by the authorities of the

State of West Bengal.

A copy of the Assessment Order dated 29.06.2020 along

with statutory Form 'C' is annexed hereto and collectively

marked as Annexure

29. From the facts mentioned hereinabove, it would be, thus, evident

that the Petitioner was compelled to purchase H.S.D. at full rate

of tax instead of concessional rate, despite the fact that Petitioner

was not at fault and, consequentially, the Petitioner was issued

Provisional Credit Notes/Credit Notes by Respondent-Reliance

Industries and even statutory Declaration Forms 'C' were

furnished by the Petitioner to Respondent-Reliance Industries for

the period when the Petitioner was compelled to purchase H.S,D.

at full rate of tax. Thereafter, even Respondent-Reliance

Industries deposited said Forms 'C' with the authority of the

State of West Bengal, but said Forms 'C' have not been accepted

by the authority of the State of West Bengal having an effect of

denying the benefit of refund of differential tax to the Petitioner.

19

30. Your Petitioners state that since the Petitioner is directly

aggrieved by the Assessment Order passed in the case of

Respondent-Reliance Industries, as due to non-acceptance of

statutory Forms 'C' by the authority of the State of West Bengal,

which were furnished by the Petitioner to Reliance Industries

and, in turn, deposited by Reliance Industries, the Petitioner is

preferring the instant writ application for quashing/setting aside

the Order of Assessment dated 29th June, 2020 (Annexure P-8), to

the extent in the said order, in substance, benefit of refund of

differential tax in favour of the Petitioner has been denied.

31. Your Petitioners state that from bare perusal of the aforesaid

Assessment Order dated 29th June, 2020, it would be evident that

additional Form 'C' produced by Reliance Industries has been

denied by primarily recording, inter alia, that Reliance Industries

has charged, collected and deposited C.S.T. at full rate and. has

shown the transaction of sale under Section 8(2) of the C.S.T. Act

by filing its returns and even no revised return has been filed by

Respondent-Reliance Industries. Further, in the said Assessment

Order, it has been stated that since Respondent-Reliance

20

Industries has not revised and amended its Invoices charging

C.S.T. @ 2%, nor has issue Credit Note against the balance

amount of C.S.T., additional Form 'C' submitted by Respondent-

Reliance Industries cannot be accepted.

32. Your Petitioners state and submit that aforesaid reasoning given

in the aforesaid Assessment Order, on the face of it, is not tenable

in the eye of law and is contrary to the statutory provisions of the

C.S.T. Act.

33. Your Petitioners state that it is an undisputed fact that he goods

were sold by Respondent-Reliance Industries to the Petitioner by

way of inter-State movement of goods and the Petitioner, being

registered dealer, was entitled to purchase said goods at

concessional rate and even in terms of Section 8(3) read with

Section 8(4) of the C.S.T. Act, Declaration Form 'C' has been

duly furnished by the Petitioner to Respondent-Reliance

Industries, which was, in turn, deposited by Reliance Industries

with the authority of the State of West Bengal. Thus, the

Petitioner and/or Respondent-Reliance Industries have fulfilled

all conditions pertaining to concessional sale or purchase and

21

merely because, at the time of raising of Invoices, under

compelling circumstances, tax was charged at full rate, cannot be

considered as a valid ground for denying the benefit of refund to

the Petitioner of the differential tax, as, admittedly, the Petitioner

was entitled to purchase H.S.D. at concessional rate.

34. Your Petitioners state and submit that from bare perusal of the

Judgment and order dated 28.08.2019 passed by the Hon'ble

Jharkhand High Court in W.P.(T) No. 6048 of 2017 and

analogous cases (Annexure- 6), it would be evident that the

Hon'ble Jharkhand High Court, in the said order, has also

recognized the right of the Petitioner to claim refund of the

differential tax and it was specifically ordered that the Petitioner

shall be refunded the differential tax which was realized from it

due to issuance of the Circular dated 11.10.2017 issued by the

State of Jharkhand.

35. Your Petitioners state and submit that even the Hon'ble High

Court of Jharkhand, while dismissing the review application,

clearly noted, inter alia, that the refund claimed by Respondent-

Reliance Industries before the authorities of the State of West

22

Bengal was rejected and, under the said circumstances,, the

Petitioner along with Respondent-Reliance Industries were given

liberty to take steps in accordance with law to claim refund from

the authorities of the State of West Bengal.

36. Your Petitioners, at this stage, state and submit that the issue as to

whether the Petitioner is entitled to claim refund of the

differential tax, which was realized and deposited by

Respondent-Reliance Industries to the State of West Bengal, is no

longer res Integra, as the Hon'ble Division Bench of the Hon'ble

Jharkhand High Court has held that the Petitioner is entitled for

refund of the said amount. However, since Respondent-Reliance

Industries has already deposited said tax with the State of West

Bengal, refund could have been granted in favour of the

Petitioner by Respondent-Reliance Industries after having

received the said amount of refund from the State of West

Bengal.

37. Your Petitioners reiterate that since the impugned Assessment

Order dated 30' June, 2020 has a direct and immediate bearing

on the claim of refund of the Petitioner and, in substance, denies

23

the right of refund of the Petitioner of differential tax, the

Petitioner is entitled to maintain the instant writ application

before this Hon'ble Court challenging the said Assessment Order,

with a consequential direction to the Respondent-State of West

Bengal to accept statutory Form 'C' furnished by the Petitioner in

respect of its inter-State transaction and to, consequentially,

refund the differential tax realized and deposited with the State of

West Bengal by Respondent-Reliance Industries.

38. Your Petitioners state that the Petitioner has no alternative

remedy of preferring an Appeal against the Assessment Order

dated 30th June, 2020, as under the provisions of Section 9(2) of

the C.S.T. Act read with the provisions of Appeal under Section

79 of the West Bengal Sales Tax Act, 1994, it is only a dealer

registered with the Respondent-State of West Bengal, which can

prefer Appeal against an Assessment Order. Under the said

circumstances, the Petitioner has only remedy to approach

directly before this Hon'ble Court for claiming refund of

differential tax realized from the Petitioner for no fault of the

Petitioner.

24

39. Your Petitioners, at this stage, state that the present issue has

been decided by several Hon'ble High Courts including the High

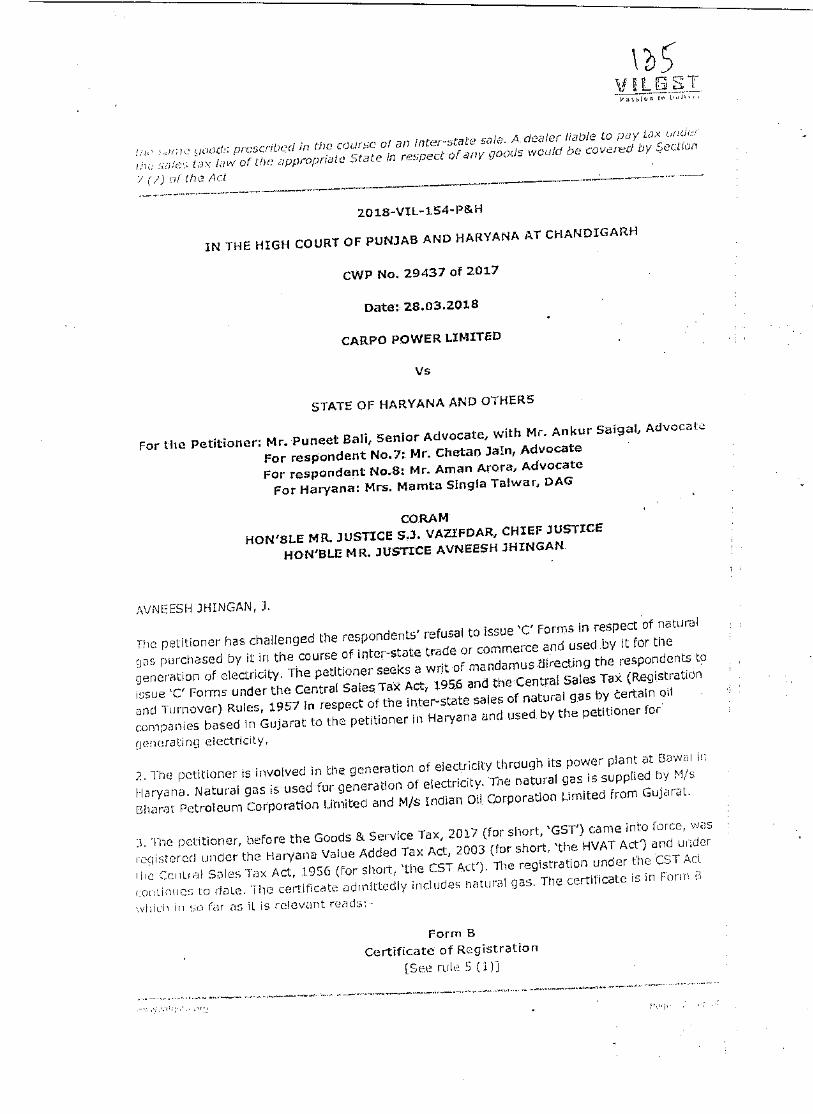

Court of Punjab and Haryana in the case of Carpo Power

Limited Vs. State of Haryana and Others and in the said writ

application, while adjudicating the issue, the Hon'ble High Court

of Punjab and Haryana further ordered for refund of the

differential tax which has been realized by the Oil Companies

A copy of the Order dated 28.03.2018 passed by the High

Court of Punjab and Haryana in the case of Capro Power Ltd. Vs.

State of Haryana and ors. is annexed hereto and marked as

Annexure `P-9'.

40. Your Petitioners further state that said decision of the Hon'ble

High Court of Punjab and Haryana was challenged before the

Hon'ble Apex Court in Special Leave to Appeal, and, the said

Special Leave to Appeal (C) No.20572 of 2018 was dismissed

by the Hon'ble Supreme Court vide order dated 13.08.2018.

25

A copy of the order dated 13.08.2018 passed in Special

Leave to Appeal (C) No. 20572 of 2018 is annexed hereto and

marked as Annexure

41. Your Petitioners further state that, similarly, the Hon'ble

Rajasthan High Court vide its judgment and order dated

18.05.2018, quashed the similar circular issued by the State of

Rajasthan and, while quashing the said circular, further ordered

for refund of the differential tax which was realized on account

of purchase of H.S.D. at full rate of tax.

A copy of the order dated 18.05.2018 passed by Hon'ble

Rajasthan High Court is annexed hereto and marked as Annexure

`P- 11'.

42. Your Petitioners, at this stage, most humbly state and submit that

pursuant to the Judgment and order passed by Hon'ble Rajasthan

High Court, one J.K. Cement Ltd approached the Hon'ble High

Court of Gujrat at Ahmedabad by filing writ application claiming

direct refund of tax which was collected from the said Company-

J.K. Cement Ltd by its seller and deposited with the authorities of

26

the State of Gujarat. In the said writ petition it was primarily

contended, inter-alia, that said Company- J.K. Cement Ltd was

entitled under law to purchase H.S.D. at concessional rate, but,

under compelling circumstances, it purchased H.S.D. by paying

full rate of tax and, thereafter, subsequently, issued Declaration

Form "C" to the seller which supplied H.S.D. at full rate of tax. It

was, thus, contended inter-alia that since, subsequently, Form

"C" was obtained by said J.K. Cement Ltd , it is entitled under

law to claim direct refund from the authorities of the State of

Gujrat as the seller-Reliance Industries Ltd had already

deposited the tax with the State of Gujrat. The Hon'ble High

Court of Gujrat at Ahmedabad, vide order dated 18.12.2019, was

pleased to allow the said writ application and directed the

authorities of the State of Gujrat to directly grant refund to the

purchaser as the seller has already deposited the tax with the

State authorities.

A copy of the order dated 18.12.2019 passed by Hon'ble

High Court of Gujarat at Ahmedabad is annexed hereto and

marked as Annexure T-12'.

27

43. Your Petitioners state that, in fact, ratio laid down by various

Hon'ble High Courts, as mentioned above, regarding eligibility to

purchase H.S.D. at concessional rate even after the amendment

carried out to the definition of 'Goods' under Section 2(d) of the

C.S.T. Act, is, in substance, being accepted by the Union of

India. In this context, it is stated that earlier the Union of India,

through the Ministry of Finance, issued an Office Memorandum

dated Th November, 2017 restricting the interpretation of the

term '"Goods" as amended vide Section 2(d) of the C.S.T. Act,

and clarified that purchase of H.S.D. would not be available at

concessional rate to a dealer engaged in manufacturing and

process of goods for sale.

A copy of the Office Memorandum dated 7th November,

2017 is annexed hereto and marked as Annexure `13-131.

44. Your Petitioners state that, however, subsequently, the

Government of India, through the Ministry of Finance, by

following the Judgment of the Hon'ble Punjab and Haryana High

Court, issued directions to all the States/Union Territories to

28

follow the decision of the Hon'ble Punjab and Haryana High

Court, vide its letter dated 1st November, 2018.

A copy of the Letter dated 1' November, 2018 issued by

Govt. of India, Ministry of Finance is annexed hereto and marked

as Annexure 'P-14'.

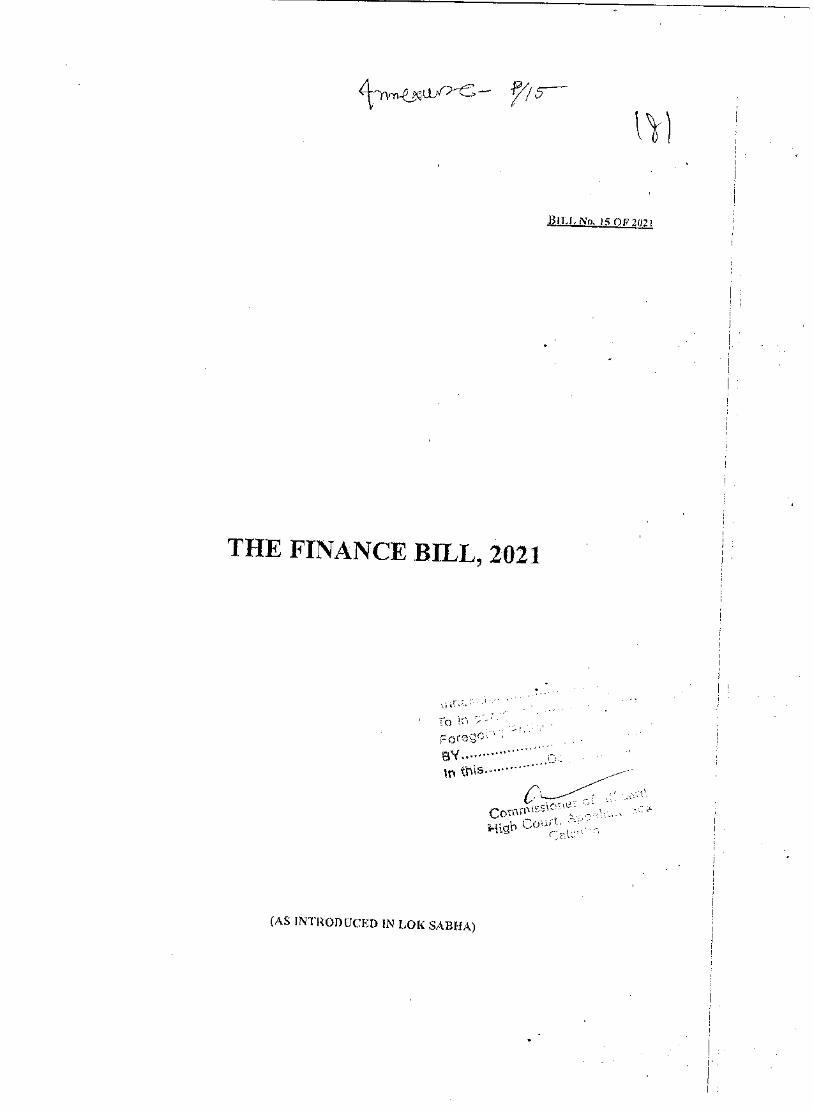

45. Your Petitioners state that, recently, in the Finance Bill, 2021, an

amendment has been sought to be introduced and the earlier

provision of Section 8(3)(d) of the C.S.T. Act is sought to be

substituted vide Section 141 of the Finance Bill, 2021.

A copy of relevant extract of the Finance Bill, 2021 is

annexed hereto and marked as Annexure 'P.15'.

46. Your Petitioners state that the Finance Bill, 2021, as aforesaid,

itself demonstrates that prior to incorporation of the aforesaid

proposed amendment, your Petitioner was entitled to purchase

H.S.D. at concessional rate, but was denied the said purchase for

no fault of your Petitioner and, under the said circumstances,

your Petitioner is entitled to claim refund of differential tax,

29

which has been wrongly realized from it and deposited with the

State of West Bengal.

47. Your Petitioners, at this stage, state that the Petitioner even filed

a detailed representation before Respondent No.2 claiming refund

of the differential tax directly from the State of West Bengal, but

in spite of filing of said representation, till today, no order h s

been passed by the Respondent-State of West Bengal.

A copy of the representation filed by the Petitioner before

Respondent No.2 on 14.01.2021 is annexed hereto and marked as

Annexure T-16'.

48. Your Petitioners state and submit that the Petitioner is entitled for

refund of an amount of Rs, 4,88,63,067/- in respect of its

business operation in the State of Jharkhand for the period when

the Petitioner was compelled to purchase H.S.D. at full rate of

tax, despite the fact that the Petitioner was entitled, under law. to

purchase H.S.D. at concessional rate.

49. Your Petitioners further state that the Petitioner has not passed on

the burden of full rate of tax realized from it by Respondent-

30

Reliance Industries and the entire amount of differential tax has

been paid by the Petitioner at its own. Hence, the question of

principle of unjust enrichment would not be applicable in the

instant case, if the amount of differential tax paid by the

Petitioner is refunded to it.

50. In the light of the foregoing submissions, Your Petitioners submit

that the Assessment Order passed in the case of the Respondent-

Reliance Industries is liable to be quashed and set aside by this

Honible Court and, further, consequentially, direction is liable to

be issued to the Respondent-State of West Bengal to directly

refund the amount of differential tax amounting to Rs.

4,88,63,067/-, which has been realized and deposited by

Respondent-Reliance Industries into the State exchequer of the

State of West Bengal.

5I. Your Petitioners, prefer this writ application on, amongst others,

the following

GROUNDS

31

For that the impugned Assessment Order dated 29th June,

2020 is neither sustainable in law nor on facts and the

same is liable to be quashed/set aside.

II For that the Petitioner s directly aggrieved by the

Assessment Order passed in the case of Respondent-

Reliance Industries, as due to non-acceptance of statutory

Form 'C' by the authority of the State of West Bengal,

claim of refund of differential tax has been denied to the

Petitioner.

III. For that the reasoning given in the Assessment Order, on

the face of it, is not tenable in the eye of law and is

contrary to the provisions of the C.S.T. Act.

IV. For that the Petitioner was, admittedly, entitled to

purchase H.S.D. at concessional rate in terms of Section

8(3) read with Section 8(4) of the C.S.T. Act and, thus,

the excess amount realized from the Petitioner at full rate

of tax by Respondent-Reliance Industries in the

32

compelling circumstances and deposited with the State of

West Bengal, is liable to be refunded to the Petitioner.

V. For that learned Assessing Officer, while passing the

impugned order, failed to take into consideration that the

Hon'ble High Court of Jharkhand, in its Judgment and

order dated 28.08.2019 passed in W.P.(T) No. 6048 of

2017 and analogous writ petitions, including the writ

petition filed by the Petitioner, has also recognized the

right of the Petitioner to claim refund of differential tax

and it was specifically ordered that the Petitioner shall be

refunded the differential tax which was realized due to

issuance of Circular dated 11.10.2017 issued by the State

of Jharkhand.

VI. For that learned Assessing Officer failed to appreciate that

it is an undisputed fact that the goods were sold by

Respondent-Reliance Industries to the Petitioner by way

of inter-State movement of goods and the Petitioner, being

registered dealer, was entitled to purchase said goods at

concessional rate and even in terms of Section 8(3) read

33

with Section 8(4) of the C.S.T. Act, Declaration Form C

has been duly furnished by the Petitioner to Respondent-

Reliance Industries, which was, in turn, deposited by

Reliance Industries with the authority of the State of West

Bengal. Thus, the Petitioner and/or Respondent-Reliance

Industries have fulfilled all conditions pertaining to

concessional sale or purchase and merely because, at the

time of raising of Invoices, under compelling

circumstances, tax was charged at full rate, cannot be

considered as a valid ground for denying the benefit of

refund to the Petitioner of the differential tax, as,

admittedly, the Petitioner was entitled to purchase H.S.D.

at concessional rate.

VII. For that learned Assessing Officer failed to appreciate that

the issue as to whether the Petitioner is entitled to claim

refund of the differential tax, which was realized and

deposited by Respondent-Reliance Industries to the State

of West Bengal, is no longer res integra, as the Hon'ble

Division Bench of the Hon'ble Jharkhand High Court has

34

held that the Petitioner is entitled for refund of the said

amount.

VIII. For that learned Assessing Officer failed to take into

consideration that the present issue has been decided by

several Hon'ble High Courts including the High Court of

Punjab and Haryana in the case of Carpo Power Limited

Vs. State of Haryana and Others and in the said writ

application, while adjudicating the issue, the Hon'ble

High Court of Punjab and Haryana further ordered for

refund of the differential tax which has been realized by

the Oil Companies.

IX. For that learned Assessing Officer also failed to take into

consideration, that, similarly, the Hon'ble Rajasthan. High

Court vide its judgment and order dated 18.05.2018,

quashed the similar circular issued by the State of

Rajasthan and, while quashing the said circular, further

ordered for refund of the differential tax which was

realized on account of purchase of H.S.D. at full rate of

tax.

35

For that pursuant to the Judgment and order passed by

Hon'ble Rajasthan High Court, one J.K. Cement Ltd.

approached the Hon'ble High Court of Gujarat at

Ahmedabad by filing writ application claiming direct

refund of tax which was collected from the said

Company- J.K. Cement Ltd by its seller and deposited

with the authorities of the State of Gujarat. In the said writ

petition it was primarily contended, inter-alia, that said

Company- J.K. Cement Ltd was entitled under law to

purchase H.S.D. at concessional rate, but, under

compelling circumstances, it purchased H.S.D. by paying

full rate of tax and, thereafter, subsequently, issued

Declaration Form "C to the seller which had supplied

H.S.D. at full rate of tax. It was, thus, contended inter-alia

that since, subsequently, Form "C" was obtained by said

J.K. Cement Ltd , it is entitled under law to claim direct

refund from the authorities of the State of Gujarat as the

seller-Reliance Industries Ltd had already deposited the

tax with the State of Gujarat. The Hon'ble High Court of

36

Gujarat at Ahmedabad, vide order dated 18.12.2019, was

pleased to allow the said writ application and directed the

authorities of the State of Gujarat to directly grant refund

to the purchaser as the seller has already deposited the tax

with the State authorities.

XI. For that since the impugned Assessment Order dated 20

June, 2020 has a direct and immediate bearing on the

claim of refund of the Petitioner and, in substance, denies

the right of refund of the Petitioner of the differential tax,

the Petitioner is entitled to maintain the instant writ

application before this Hon'ble Court challenging the said

Assessment Order, with a consequential direction to the

Respondent-State of West Bengal to accept statutory

Form 'C' furnished by the Petitioner in respect of its inter-

State transaction and to, consequentially, refund the

differential tax realized and deposited with the State of

West Bengal by Respondent-Reliance Industries

XII. For that other grounds, if any, shall be urged at the time of

hearing of this writ application.

37

52. Your Petitioner states that your Petitioner has no alternative and

efficacious remedy than to approach this Hon'ble Court for

seeking refund of the differential tax from the State of West

Bengal, as the Petitioner cannot challenge independently in

Appeal the Assessment Order passed by Respondent No.3 in the

case of Reliance Industries.

53. All the records are lying and Respondents are working for gain in

Calcutta within the Appellate Side Jurisdiction of this Hon'ble

Court and, as such, this Hon'ble Court has jurisdiction to

entertain and try this application in its Appellate Side.

54. Your Petitioners state that your Petitioners have not moved any

application either in this Hon'ble Court or before any other Court

on the self-same fact and/or cause of action which is the subject-

matter of the present writ application.

55. This application is made bona fide and for the ends of justice.

56. That balance of convenience is entirely in favour of orders being

passed, as prayed for herein.

38

In the circumstances as above, Your

Petitioners humbly pray Your Lordships for

the following orders

(a) For issuance of an appropriate writ/order/

direction, including Writ of Certiorari for

quashing/setting aside the impugned order

dated 29.06.2020 passed by Respondent No.3

in the case of Respondent-Reliance Industries

pertaining to the Assessment Year 2017-18,

to the extent submission of Additional Form

`C' by Respondent-Reliance Industries

pertaining to the Petitioner has been denied

in the Assessment Order having

consequential effect of denying the benefit of

refund of the differential tax to the Petitioner.

(b) For a Writ, in the nature of Mandamus,

directing the Respondent-State of West

Bengal to refund the amount of

Rs.4,88,63,067/-, being the amount of

39

differential tax realized from the Petitioner

by Respondent-Reliance Industries and

deposited with the State of West Bengal in

respect of purchase of H.S.D., which the

Petitioner is, admittedly, under law, entitled

to purchase at concessional rate.

(c) Rule Nisi in terms of prayer (a) and (b)

above.

(d) Such further and/or other order or orders be

passed and/or direction or directions be given

as to this Hon'ble Court may be deemed fit

and proper.

And for this Act of Kindness, Your Petitioners, as in duty bound,

shall ever pray.

For Ambey Mining Pvt. Ltd.

1-0—'n--- ---

Authorisedr l'11 ? \--

L.jc i^{ (3'-.. L._

Certify that deponent herein is duly authorized and competent to affirm the petition on behalf of the petitioners herein

a7oLa."7,7

Advocate

40

AFFIDAVIT

I, Shyam Lal Naik, son of Late Rabi Narayan Naik, aged about 50 Years, by faith-Hindu, Occupation-Service, resident of 63, Aswini Nagar, P.O-Regent Park, Jadavpur Police Station Kolkata-700040 and 8, A.J.C. Bose Road, Circular Court, 9th Floor, Kolkata-700 017 (West Bengal), do hereby solemnly affirm and say as follows:-

1. I am Senior Manager of the Petitioner no.1 and the petitioner no.2 herein, as such, well acquainted with the facts and circumstances of the case. I am authorized and/or competent to initiate proceedings, sign petitions and affirm affidavits for and on behalf of Petitioner Nos. 1 and 2 herein. I am affirming this affidavit for and on behalf of the petitioners above named.

2. The statements contained in the paragraphs 41-03 of the foregoing petition are true to my knowledge and those contained in paragraphs 4.,1til6,te),,z1/25-,z6,2J3,,25,39,E046 thereof are based on information derived by me from the records of the Petitioner-company above-named and believed by me to be true and d_ those contained in paragraphs 5+s to, tQA-1:. ‘5,n,153 21301,a'aVe my humble submissions before this Hon'ble Court.

k"--- me'-- Prepared in my office Deponent is known to me

yow &-Lor Advocate Clerk to

Advocate Solemnly affirmed before me on this The 'Aday of February, 2021.

Certify that all annexures are legible

Advocate

COMMISSIONER der„Aft tt`

torarn,sxsccoi:oar.. tl .“ uu. „ NP-Ptta

eiSn c

TISIr.i908p Y.MINING,PVT

TUN: 20.08030S91R.

THE..CENTR4L.W.4,

GOVERNMENT OF JHARKHAND COMMERCIAL TAXES DEPARTMENT

Ca% 4) 14,1187O)A.I.Nok

CIRCLE: West Circle (Ranch° • . •

s is is fa:day that Mis M/S AMBRY MINING-PVT LTD, Wh4sfinfincipalplaa)v of hysinestinulharkhand is aitualcci riatfnidudOcarfPloc), No •'404 4Th FILOCR)),•SHRZE.,IRARI-M'KRiSRSI4OAROEN.,Road Puree( I Lane -BARIATU ROAD, sinfociTown:Oin -RANcd•Ii, District -RANQI-11, City 7 r14,N,CHIs Post •Offibil•;12ARIAllAStatelf;JHARKHAND, Pin Code Dacca has ! tddi rtd.cdstered as a dealer under section 7(1)/7(2)•Oftlie cantral..Saleitaxteti190. • ' The business is: With effe.CHTtorso 07101.12013.. ..." • .4 • Wholly: Not Appli(Rbie ' .

Mainly:. VVorks-Conpactor

Partly; •

cia;s0)i°4‘.),Vid the alas eflheswygne whicaadto thaidayfSid

is/are as follows and d in that sub-section

(A) Class(es)fof.goods alloWed :

IThe Onaler Manufactures. processes, dOextracts mining. the following classes of goods or generates or distributes tne following form of power, namely:

Pla Refer Annexure III . flan denier's year for liTs purpose of accounts runsfrom; 1st day of April to 31st ay of March. With eddat frond o7Atiii:4c0. .::..;, . The dealer has additional pl4qtf(p) of I59).4,1 ss assta4pQrycI .. — (a)In)the'State 'ofRegistration : NoS gab

. AcIditignOlPla ‘..Th '' r

AdaNional Place

(b)In other State of Registration : Additional Places (VAT)) rn Other States

Please Refer Annexure VI Afklifidr Places (CST) in Other' states,

90e(41e)Yli y. The dealer keepswarehouses at the.fdliowlpgp)sces40,33,R(I46)1 .

fPleaseRefer:Annexurmy111 Dealer%

Deale) warehouse LocAtic, (

Pleise•Refer Annexure IX

[See wie'5(1)1 GESTIFICATB,OF REGISTRATION (AMENDED}

TIN 200003089,49 FIRM NAMEIMIS AMBEY MINING PVT LTO n r_. fificate rs valid ni 31/10/2013 until cancelled

Partly.

3

- - GOVERNMENT OF. JHARKHAND ?MIIERCIAL, 'AXE,S`, DEPARTMENT

Fon Use In the Mann acture Cr Process of Goods (or Sale

u.prohase _ . For Use In he Manufacture or Process_of Cocos for Sale,-

Purchase For Use in the MaNrfactyrq 9r PrOoess of Goads for Ste le-

jnp a' tuf Put_ Fpwse

co

• d

bars and rods, hot rolled, inregularly(Wound cods, of con or nornalloy steel

F arch PI

Fo Use In Nifining - Purch

TrOsein, Mining Purchase IPurch

For bSejn Mining Parches

Spare parts. prefab, engine' s plate, ms channel, Ms square

9h et'

such as all types:of plants a„wus,„„Vols engineering goods,

td diesel oil

apital goodkor piants,amd hlap'hrnenesauchaselM types of plants, pcgolgnenes, equipments„ apparatus tools, engineenng goods, I

a ha ces rtt rnaggneries - all other similar implements and

-macninenes In this category conveyor 6 transmission belts or belting of vulcanized rubber

cal goods

cement

rng Purchasee

dr yfse Mi g. Pxyre

se urch se

D(Cq: r'1(03/20 l,

g macbini ies

akers

h mo ,,cbg machineries-end loaders

efectocal g-O-Wslairparatus for sWitching protecting or automation of electrical cwoult including mob rnccb,

4.1cl tunal Places (CST) !di Other states

ST No 113ridieli:Nime ddresa: AiMgeMTOINlia.)Sciititr "Tr

Dealer

Dealer v, retie

Not Available'

ANNEXURE VII

of Available •

wani:7:13216

aster,

ANN;)1PROIY.; The dealer has additional place(s) of tiusiness.,as statea.lielq4^1:

(a)In the State of Registration : No ?n9t1plcble • • Add.t't•nal Places (VAT) in Jharkhand

Additio r:?fac6o:( s:fl• b J.

(b)In other Slate.o,

Additional Place

from; 07/01/2013

KHA ND cppitmeketAL.,TAt DOARTMENT 4111111a1.10111 111

'THE CENTRAL SALES TAX. RULES-1957 -

FORM

egli.OICAT4.9Ff-SR741le 5 rliAt1T)IfII;IS/NDE a). ' TI ?;00833.013919 NAME: M/S.AllIpEt PVT LTD MINING

I Tqfrpopealk •

The deal

tbOon poxem1d4Irje.plug.socket; -main swatches, changeover • • -•'••• t. "tclies accessories. . . . , awl „. ; a ssorie s.

ANNEPRE; Ili : anufactures. processes; oral 0tgd,14 nlinirlige fpllnwiva otaeses, pf goods or generates or distribiii.e4the follOWIttIor fiiatweala j'e ith iltiopt107/01/013

Not Available A

YERNIMENT OEJHARKHAND

CO MERSIAL TAXES DEPARTMENT 11111111 11l1WNnilllll

THE CENTRAL SALES TAX.RULES-1957

Activity Details

Business Start Date Firskinter State Sale Date. Account From, AccounhSele

Business prop /partner/director Name talusof Applicant

Details of addhfional Pjeces of busiriear Wifficairtifes Deta4p.

dtive pate ) '07/01/2013

07/01/20.13

07/01/2013

07/01(2013

07/01/2013

Thebusiness)!

Wholly: PVt. Ltd, pany, Mainly: Works Contract & Mining Partly. Not Applicable

Sr IVo pur,o, , •,,„Fpr Re-Sale

odlties

Thekdeal

tone chips, iron rod, angle cement)

Cg machineiles, equipment like dozer for, pay loader, all types of vehicles, tools & flapsiipattenj, lubricant diesekalengine fael acageits,plant krilachineryd ___ )

ing classes;ollp of goods or 9enerates or 'over, sgirely

The d purpose of accounts runs from

The dealer has additional piaoe(s) of business esstate

(a)in the State of Registration : Not Applicable

Add tional Places (VAT) in Jharkhand

yeah ro

Additional Place

pkiir CSTj in Cu

ta In other State of Registration

Additional Plates ;VATitn0.therGtates

•;•., •

SUSI $,P4:4 0 . STATE : lY

er.wajehouso LoCatien..(VAT)•.• • .• - .• ....

90 'Bengal

Ot P,va

Dealer vLaaahouse Location (CST)

„Net Available •

,G9VERNKNT.OFAHARKHAND COMMOMIAOTA ARTMENT

7

, ule 5(14J- C,EVyttGATE OF REGISTRATION (AMENDED)

TIN: 26080368919 FIRM NAME: MIS AMBEY MINING PVT

Not Avertable •.

TD

Not Available

GOVERNMENT OF JI-jARKHAND GOMMRROI 17 ,T.AXE:,q4RARTIVIENT

;or ad Pr

jY

Emicopt !en olh'pr-:stares

CCSTjir Othe eta

,PleainneNothtr AnthozureV1i

Howlett p teens: Not Albethicable

GOVERNIVIEN1 Of- JHARECHAND

COMtVIPRMAL T4Xc-S.-.0gPARTVIETNT . .

teFo2PIA,Tdtto' FIN:206§0540.19. 'Fi

0'14 .. 'rorn 4rittc;4

'79%

aOk ?! — thiirehesw. 'Iv= PR:

)f. tfrt.1Ciri ntectucal 9`6.

lry

6:3ii id baz1..e i r

nse

in kiln'

QQyTEBNPIEIT QF ,JE*RKE-141S1p,:: CQ ERCIAL TlEStDJAfARTIANT

s

COVE,- RNMENT OF JHARKI-iAND COMMERCIAL TAXES.OPARTIVIEPT L Iifljjg

HE

.'"

CENTRAL SATES TAX: :$1,-4LEE-T$...57:

41174.4.T4 _1,„Ly,v...:"." -•-:rlfit.1400174‘16, 4V1444:***fre a

4:0 AtS;77,M encr,, • A „

citCc

I ••2(114e,da'a a

re, .4%... I.-

t"....se1:6?-%"'exl-r&64.

n Ith .• -

AI • ',Fr 2 savor ood .

No

ori3trin0s, .bjdw ^ .

WAY; inc

t,k;

TYPED COPY OF ANNEXHIM-

GOVERNMENT OF JHARKHAND • 1

COMMERCIAL TAXES DEPARTMENT I

TEIE CENTRAL SALES TAX RULES-I957 FORM B

)Sec rule 5(1)]

CERTIFICATE OP REGISTRATION (AMENDED) TIN: 20080308919 FIRM NAME: MIS AMBEY MINING PVT LTD

TIN: 20080308919 CIRCLE: Wes! Circle (Bauchi)

This is to certify that MIs M/S AMBEY MINING PVT LTD, whose principal place of business in Jharkhanti is situated at Fla/Floor/Door/Block No - 1404, 4TH FLOOR, SHREE RADHE KRISHNA GARDEN, Road Street/Lane- BARIATU ROAD, Village/Town/City- RANCID, District-RANCID, City-RANCID, Post office- BARIATU, Slate -JHARKHAND, Pin Code -834005 has been registered as a dealer under section 7(1)/7(2) of the Central Sales Tax Act, 1956.

The business is: With effect from: 07/01/2013 Wholly: Not Applicable Mainly: Works Contractor Partly:

Please Refer Annexure 1 liThe class(es) of goods specified for the purposes of sub-sections (1) and (a) of section 8 of the said Act Were as follows and the sales of these good-.in die course of inter-State trade to the dealer will be taxable at the rate specified in that sub-section subject to the provisions of sub-section (4) of the said section.

Please Refer Annexure

(A) Changes) of goods allowed: The dealer manufactures, processes, or extracts in mining the following classes of goods or generales or

distributes the following form of power, namely: Please Refer Anuexure LH

The dealer's year for the purposes of accounts runs from: 1" day of April to 31m day of March.

With effect from: 07.01.2013 The dealer has additional place(s) of business as stated below:

(a) la the Slate of Registration : Not Applicable

Additional Places (VAT) in Jharkhand

Please Refer Annexure IV

Additional Places (CST) in Jharkhand

Please Refer Annexure V

(Ii) In other Stale of Registration: Additional Places (VAT) in Other States

Please Refer Annexure VI

Additioual Plasm (CST) in Other States -

Please Refer Antimony VII

The dealer keeps warehouses at the following places: Not Applicable

Dealer warehouse Location (VAT) Please Refer Annexure Vtll

Dealer warehouse Location (CST) Please Refer Annexure IX

Dil[e: 0 1103120 19 Si enan nuihl

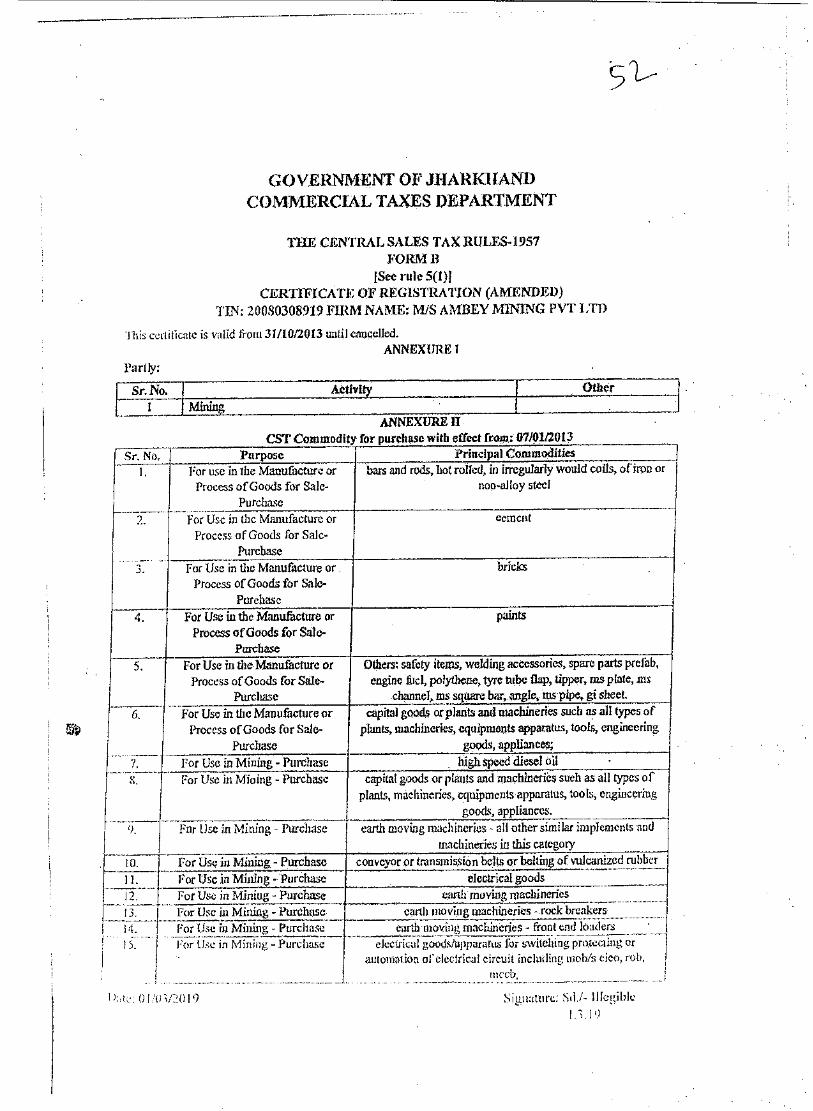

51--

GOVERNMENT OF JHARKIIAND COMMERCIAL TAXES DEPARTMENT

TIN CENTRAL SALES TAX RULES-1957 FORME

[See rule 5(1)I CERTIFICATE OF REGISTRATION (AMENDED)

TIN: 20080308919 FIRM NAME: M/S AMBEY MINING PVT LTD

this certificate is valid from 31/10/2013 until carMelled ANNEXURE

Partly:

Sr. No.

ANNEXURE Commodit for ur h c with effect r : 07/

Sr. No, Purpose Principal Commodities 1 For use in the Manufacture or

Process of Goods for Sale- Purchase

d r hot rolled, in irregularly would coils, of iron or non-alloy stem!

For Use in the Manufacture or Process of Goods for Sale-

Parch

cement

For Usc in the Manufacture or Process of Goods for Sale-

Purchase

bricks

For Use w the /vfanufacture or Process of Goods for Sale-

Purchase For Use us th thufacture o

Process of Goods for Sale- Rectum°

Others: safety items, welding accessories, spare parts prefab, engine fuel, polythene, tyre wile flap, tipper, ms plate, ins

channel, ms square bar, angle, ths pipe, gi sheet.

For Use in the Manubseture o Process of Goods for Sale-

Purchase

capital goods orplants and machineries such as all types of plants, machineries, equipments apparatus, tools, engineering

goeds, appliances; For Use in Mining - Purchase highspeed diesel oil For Use in Mining - Purchase capital goods or plants and inachillerreS such as all tYPes of

plants, machineries, equipments apparatus, tools, engineering goods, appliances.

or Use in Mining - Parches earth moving machineries - all other similar implements and machineries in this category

tO. IMr Use in Mining - Purchase conveyor or transmission belts or belting of vulcanized rubber

11. For Use in Mining - Purchase electrical goods ; 1 a For Use in Mining - Purchase earth moving machineries

For Use in Mining - Purchase earth moving machineries - rock breakers . .

For Use in Mining - Purchase For Use in Mining - Purchase

earth moving machineries - front end loaders • electrical gomisruppurarim for switching protecting or demotion olelcdrical circuit including niohis oleo, rob,

moth,

0

Signature: Stl. Illegible.

Principal Commodities

istribution boxes, industrial plug socket, main switches, chance over switches, accessories.

r. No. I Purpose

53

GOVERNMENT OF MARK/IAND

COMMERCIAL TAXES DEPARTMENT

THE CENTRAL SALES TAX RULES-I957 FORM B

iSce rule 5(1)] CERTIFICATE OF REGISTRATION (AMENDED)

TIN: 20080308919 FIRM NAME: M/S AMBEY MINING PVT LTD

ANNEXURE IN

The dealer manufactures, processes, or extracts in mining the following classes of goods or generates or distributes the following form of power, namely With effect from: 07/01/2013

Not Available

ANNEXURE IV

The dealer has additional place(s) of business as stated below; With effect from: 07/01/2011

(a) In l lie state of Registration :Not Applicable Additional Places (VAT) in lharkhand

Additional Places (CST) in Jbarkhand

(b) In other State Of Registration: Additional Places WAD in Other States

Not Available

ANNEX URE V

Not Available

ANNEXURE. Vt

Not Available

ANNEXURE VII

Arida lona laces (CST) in Other settee Sr. No. Bra nth Name Address

I. AMBEY MINING PVT LTD Durgapur, WistBengal, Burdwao,

ANNEXURE VIII

Dwlor warehouse Location (VAT) Not Available

ANNEXURE IX

Dealer warehouse Location (CST)

Nut Available

Signature: Si Ill bl fl I /03/20 19

GOVERNMENT OF MARI< HAND

COMMERCIAL TAXES DEPARTMENT

TUE CENTRAL SALES AX RULES-1957 FORM It

ISee rule 5(1)1 CERTIFICATE OF REGISTRATION (AMENDED)

TIN: 2008030S919 FIRM NAME: M/S A MEV MINING PVT LTD

List of Approved Fields Sr. No. Field Doscription Effective Date

/20 I. Activity Details 07/0113 ' 2. Business Start Date, First Inter State Sac Date, Account From, 07/01/2013

Account Sale 3. Business prop/partner/director Name, Status ofApplcani 4. Details of additional places of business 5. Commodities Details

Amendment History (Old data) The business is:

Wholly: Part Ltd. Company

Mainly: Works Contract & Mining

Partly: Not Applicable

CST Commodity for purchase Sr. No. Purpose Principal Commodities

1. For ReSale Other: works contract: bitumen, stone chips, iron rod, angle, cement, paints.

2. For Use in Mining- Other: heavy earth moving machineries, equipment like Purchase dozer, tripper; dumper, excavator, pay loader, all types of

vehicles, tools & accessories, tyre, rube 84 flaps, battery, lubricant, diesels, engine fuel, polythene spare parts,

plant& machinery. The dealer manufactures, processes, or extracts in mining the following classes of goods or generates or

distributes the following form of power, namely

Not Available

in:de:ler's year for the purpose of accounts runs from: Not &unable

Tile ilea I Cr has additional pl a CC(*) of business :is staled below : Ur) In the State of Itegislration: Not Applicable

Additional Places (VA1) in Jharkband

Not Available cos (C'AT) in Jharkhand

ithe.: i0312019

Signature: SLY- Illegible 0110:V201n

zrvn SIR a Illgani

GOVERNMENT OF MARKIIAND COMMERCIAL TAXES DEPARTMENT

THE CENTRAL SALES TAX RULES-1957 FORM B

[See rule 5an CERTIFICATE OF REGISTRATION (AMENDED)

TIN: 20080308919 FIRM NAME: MIS AMBEY MINING PVT LTD

Nor Available (b) In other State of Registration:

Additional Places (VAT) in Other States

Additional Places (CST) in Other States Sr. No. Branch Name

I. BUSINESS PLACE OUTSIDE STATE

Dealer warehouse Location (VAT)

Not Available

Dealer hot Location (CST)

Not Available

Not Available

01/9,3/20 I 9 Signature: Sd/ Illegible

0 I /01120 I 9

/4\revAme "Ph i

711TistErg

g_ff'DiviaT-ESTf 03:71

greq

L00 Rift4/ 35/ 3017, 3,7S—e, ////o/19

Fct-pizr, 01.07.2017 .(aTcrsffq 7,74 al 13161 Thi PTZ' (GST1 C3717111 'Rea f91,1C1 „REA 131 13,1116 GST tn7 tlfkirt" ZR 47-67 Iv 4'4 ZSi 494 QM (I) Alcoholic: liquor fur. Human Consumption (ii) Petroleum Crude OW High Speed Diesel (ft) Motor. Spirit (Commonly known as ()carol) (V) (Salurel Gas air (vii Aviation Torb(ne Fug1 tk **II felgt err

1956 URT BO) * aret*F1 arra - itzt ltmrer: 4'7 tr{ 3t̀ rtri.141-4 Zit9.1 314 arargrer44 arg f9 97 41rai,4.m-T Pqn, ref crazr bm 1°-217-1 3ll 41 A Ft1711-.11 61341 511frgf* 4tleRtZ,11-1 71111447 1:11z11-2979 ft-Frqt

01 08 201? a rt femur 13771

131R1.3i crnT1F FM,37T n To. wzr Trym 317 fly (IT irka: WR11117 tP. 'c'1311. 1' 111, 2f T: n11F fa4:1 n f47/inf Z74/H7 4i11 3(1019.4<nrir #1 frnt( cradl :Tull? nir(117 311.3711•2979 11V-FizR 04.08/2017 iM 112ctiarnT 21511#

q ft-qw• mehRia itair (11.1. 31RIf1-1171 T 195 6 * ar-qi c• fThAtHa rk #tiv ItRi at-cr ,Fcreifwd 7E11 t'