1 TARGET2-Securities Gertrude Tumpel-Gugerell Member of the Executive Board of the ECB CESAME 12 February 2007

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

TARGET2-Securities

Gertrude Tumpel-GugerellMember of the Executive Board of the ECB

CESAME12 February 2007

2

Agenda

I. Introduction: The why and the how of T2S

II. Main issues

III. The way forward: Launching the project

3

I. Introduction: The why and the how of T2S

4

• Financial services are one of the sectors where Europeis lagging behind the US in productivity growth

• There is a growth potential through financial marketintegration:e.g. study by European Commission in 2006 showed thatlowering of post-trading costs between 7-18% can result inGDP growth of 0.2 to 0.6% on average over ten year horizon

• MiFID will foster competition among exchanges, broker-dealers and trading systems to deliver investor services

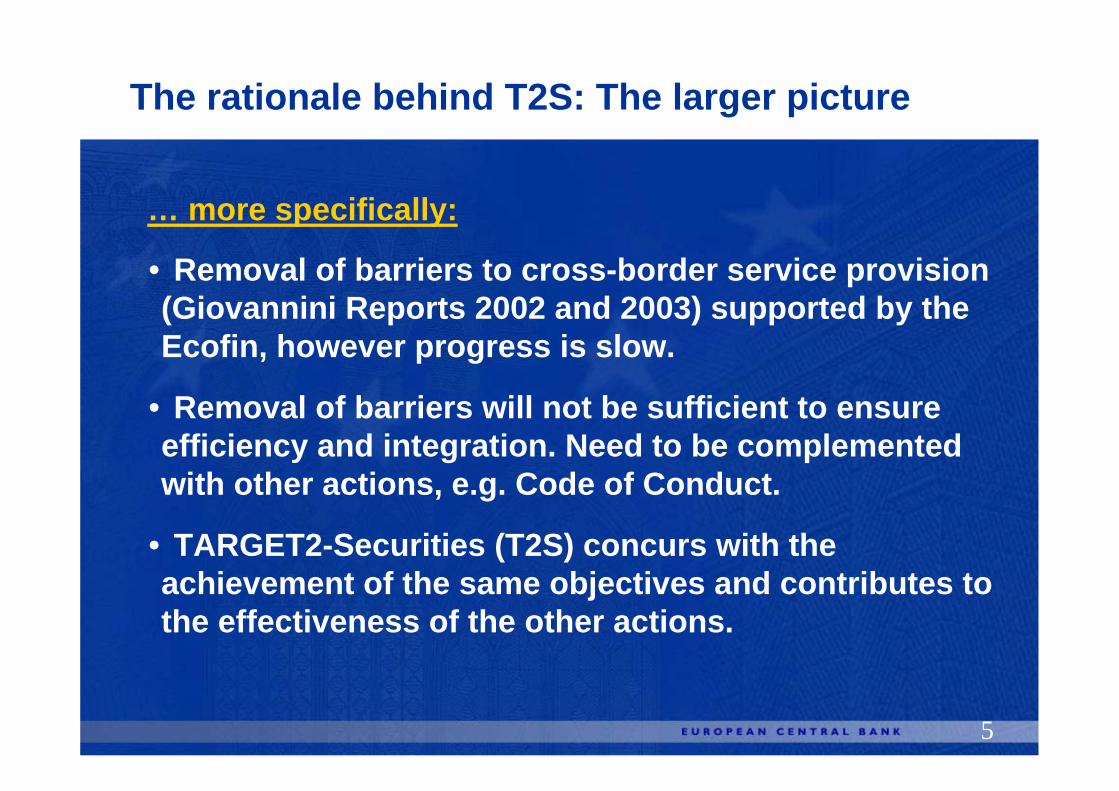

The rationale behind T2S: The larger picture

Some general observations:

5

• Removal of barriers to cross-border service provision(Giovannini Reports 2002 and 2003) supported by theEcofin, however progress is slow.

• Removal of barriers will not be sufficient to ensureefficiency and integration. Need to be complementedwith other actions, e.g. Code of Conduct.

• TARGET2-Securities (T2S) concurs with theachievement of the same objectives and contributes tothe effectiveness of the other actions.

The rationale behind T2S: The larger picture

… more specifically:

6

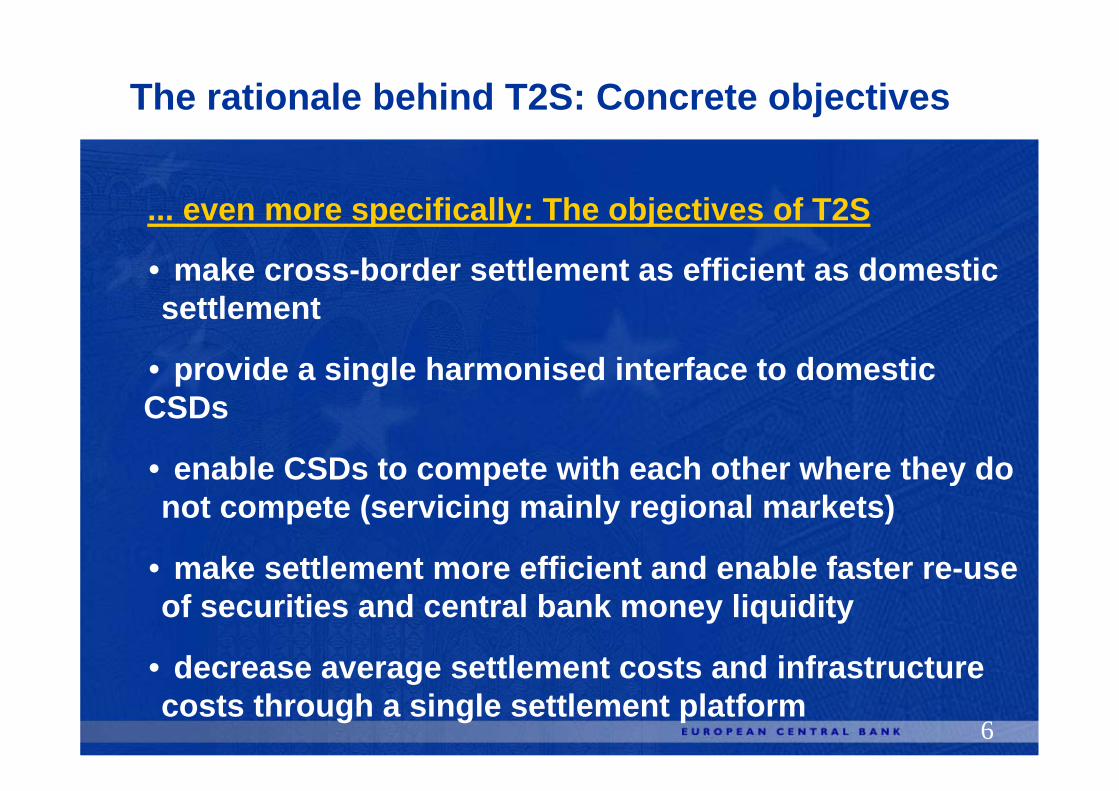

• make cross-border settlement as efficient as domesticsettlement

• provide a single harmonised interface to domestic CSDs

• enable CSDs to compete with each other where they donot compete (servicing mainly regional markets)

• make settlement more efficient and enable faster re-useof securities and central bank money liquidity

• decrease average settlement costs and infrastructurecosts through a single settlement platform

The rationale behind T2S: Concrete objectives

... even more specifically: The objectives of T2S

7

• T2S will be a single IT platform enabling euro area-widesettlement of securities in central bank money

• CSDs would “outsource” their securities accounts toT2S, which would perform the processing of theirsettlement instructions on these accounts

• CSDs would keep their customer base and continue toperform non-settlement related functions (issuance,corporate actions, custody …)

Settlement in commercial bank money out of scope of T2S (to remain with ICSDs and custodians)!

The T2S concept: What it is and how it will work

Characteristics of T2S:

8

The concept: What T2S is and how it will work

Functional architecture of T2S

T2S platform

CSD A

CSD B

CSD C

T2SSETTLEMENT

ENGINE

TARGET2

SECURITIES CASH

CSD A ACCOUNTS

NCB C ACCOUNTS

SETTLEMENT INSTRUCTIONS

CSD C ACCOUNTS

CSD B ACCOUNTS NCB B ACCOUNTS

NCB A ACCOUNTSNCB A

NCB B

NCB C

9

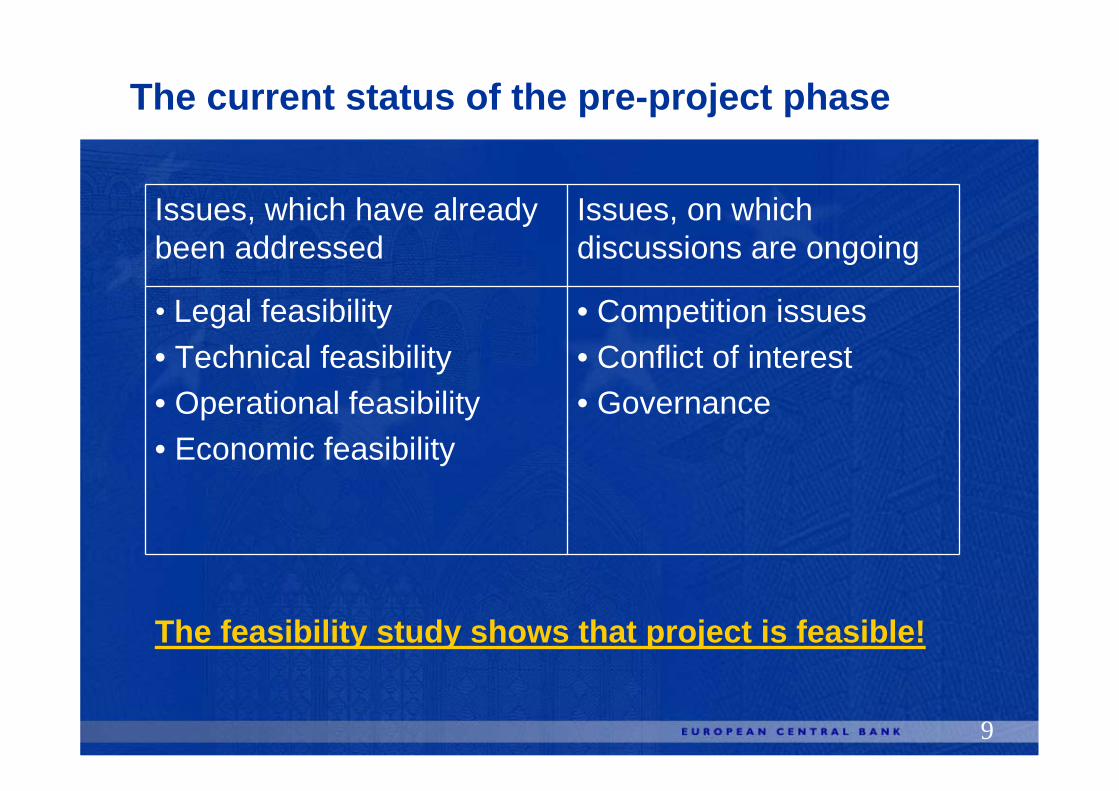

The current status of the pre-project phase

The feasibility study shows that project is feasible!

• Competition issues• Conflict of interest• Governance

• Legal feasibility• Technical feasibility• Operational feasibility• Economic feasibility

Issues, on which discussions are ongoing

Issues, which have already been addressed

10

II. Main issues

11

Competition, innovation and alternatives • T2S not a CSD, but a single settlement platform offeredto CSDs to better serve their clients (“IT outsourcing”)

• By creating a single interface to currently fragmented markets, T2S will create competition between CSDsand between CSDs and custodian banks

• Competition between settlement in central bank money(T2S) and settlement in commercial bank money (ICSDsand custodian banks) will continue to exist

12

Competition, innovation and alternatives

• T2S will stimulate innovation at custodians and (I)CSDs

• Private alternatives only partial solutions (in terms ofscale and geographical scope) and no real alternative

Conclusion:

T2S has a positive impact on competition: it maintains competition where it already exists, and it creates opportunities to compete where competition is today non-existent in practice.

This will create better conditions for competition in provision of services to the end-users of the securities infrastructure, namely the issuers and investors, in line with the objectives set in the Lisbon Agenda.

13

Conflicts of interest and governance

• Common for central banks to combine responsibilitiesof operation and oversight (US, Japan, Belgium, …)

• Eurosystem already combines operation of TARGETwith oversight of private systems such as EURO1

• Article 22 recognises compatibility of the two functions:“The ECB and NCBs may provide facilities, and the ECB

maymake regulations, to ensure efficient and sound clearing

andpayment systems”.

14

Conflicts of interest and governance

• Strict internal Eurosystem rules to avoid perception of conflict of interest (separate units, no cross-subsidies,same oversight standards)

• Standards and best practices on governance taken intodue account (involvement of users)

Conclusion:

In accordance with widely accepted central bank practice, the Eurosystem will combine provision of settlement services with oversight responsibilities.

For the T2S project governance, the Eurosystem will follow market best practice and will give CSDs and market participants major responsibilities in the governance.

15

Cost of investments and migration

• Economic feasibility study shows on basis of conservativeassumptions that T2S is economically feasible and, indeed, highly desirable

• Although single figures (e.g. communication costs)disputed, this general result not contested by market

• Total investment costs of EUR 166 million and annualrunning costs of EUR 61 million

• Average T2S fee lower than lowest CSD fee today

• One-off “migration” costs (for adapting and migrating toT2S) of about EUR 200 million, but savings of at leastEUR 185 million in operations and EUR 200 in liquidityevery year

16

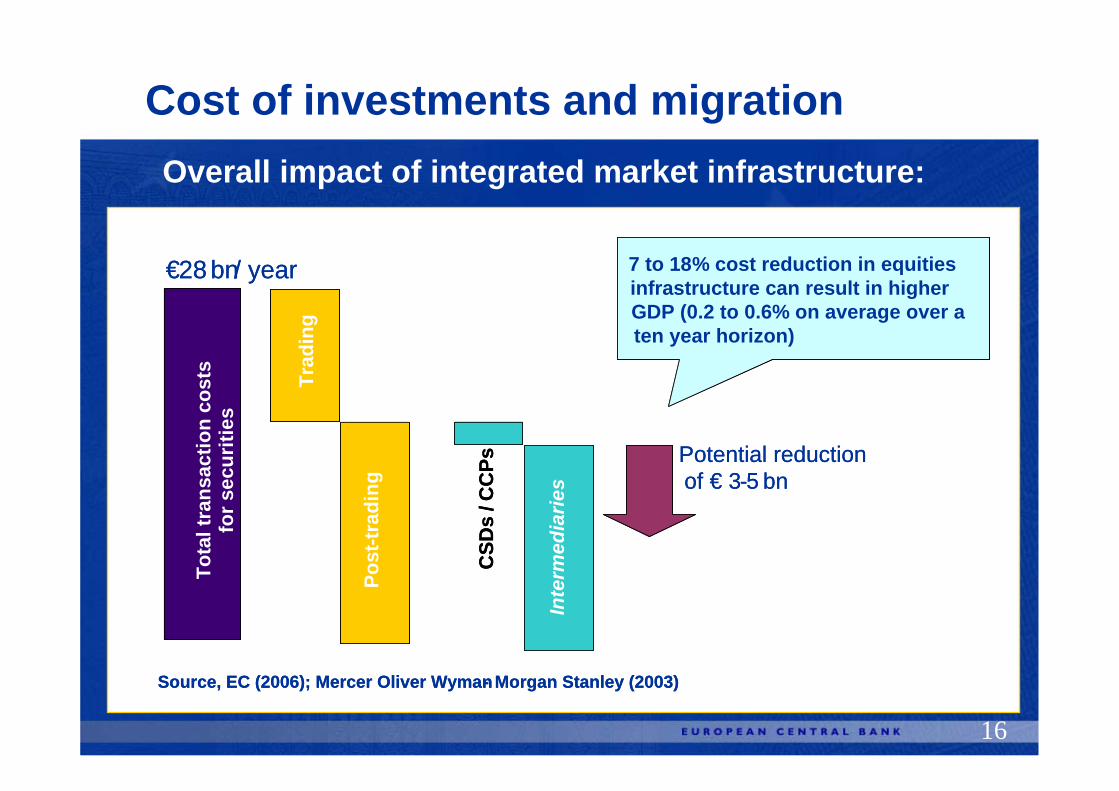

Overall impact of integrated market infrastructure:

Cost of investments and migration

Source, EC (2006); Mercer Oliver Wyman- Morgan Stanley (2003)

Tota

l tra

nsac

tion

cost

sfo

r sec

uriti

es

CSD

s/ C

CPs

Post

- trad

ing

Trad

ing

Inte

rmed

iarie

s

Potential reduction of € 3-5 bn

€28 bn/ year 7 to 18% cost reduction in equities infrastructure can result in higher GDP (0.2 to 0.6% on average over a ten year horizon)

Source, EC (2006); Mercer Oliver Wyman- Morgan Stanley (2003)

Tota

l tra

nsac

tion

cost

sfo

r sec

uriti

es

CSD

s/ C

CPs

Post

-trad

ing

Trad

ing

Inte

rmed

iarie

s

Potential reduction of € 3-5 bn

€28 bn/ year 7 to 18% cost reduction in equities infrastructure can result in higher GDP (0.2 to 0.6% on average over a ten year horizon)

17

Impact on market participants: main benefits

T2S creates two main sources of cost savings to market participants:

Reduction in the number of settlement enginesat CSD level

Reduction in CSD infrastructure costsReduction in custodian back-office costs

(number of interfaces)

Reduction in domestic (CSD) feesReduction in cross-border (custodian)

fees

Cost of investments and migration

18

Impact on non-euro area

• T2S to offer securities settlement services in euro

• T2S open to CSDs outside the euro area settling ineuro central bank money

• Inclusion of other EU currencies depending onwillingness of central bank of issue

Conclusion:

CSDs and market participants outside the euro area will also be able to benefit from T2S if they wish.

19

III. The way forward: Launching the project

20

Governing Council will discuss feasibility study in February/March 2007 and:

• take into account ECOFIN conclusions (27 February)

• decide on way forward of the project

• launch public consultation to prepare the UserRequirements

The way forward: Launching the T2S project

21

The way forward: phases of the T2S project (tentative)

Phase 1 Phase 2 Phase 3

•• User Requirements• Detailed Functional Specifications

(DFS)• Architectural Specifications• Decision on Migration Policy

March 2007

• T2S Development & Implementation

• Units and Modules Testing

• Fine Tuning (DF S)

• UAT Testing • Integration,

performance, interface & back up testing

• Migration Options• Final Deployment

T2S Production

March2013

Governing Council Decision

Public consultation

Related Documents