Systems Design: Job-Order costing Chapter 3

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Systems Design:Job-Order costing

Chapter

3

© McGraw-Hill Ryerson Limited., 2001

3-2

LEARNING OBJECTIVES

1. Distinguish between process costing and job-order costing and identify companies thatwould use each costing method.

2. Identify the documents used in a job-ordercosting system.

3. Compute predetermined overhead rates andexplain why estimated overhead costs areused in the costing process.

4. Prepare journal entries to record costs in ajob-order costing system.

After studying this chapter, you should be able to:

© McGraw-Hill Ryerson Limited., 2001

3-3

LEARNING OBJECTIVES

5. Apply overhead cost to Work in Process using apredetermined overhead rate.

6. Prepare T-accounts to show the flow of costs in ajob-order costing system and prepare schedulesof cost of goods manufactured and cost of goodssold.

7. Compute under- or overapplied overhead costand prepare the journal entry to close theManufacturing Overhead account.

After studying this chapter, you should be able to:

© McGraw-Hill Ryerson Limited., 2001

3-4

LEARNING OBJECTIVES

8. (Appendix 3A) Explain the implications of basingpredetermined overhead rates on activity atcapacity vs. estimated activity.

9. (Appendix 3B) Prepare journal entries to recordthe flow of costs in a just-in-time (JIT) inventorysystem.

10. (Appendix 3C) Account for scrap and rework ofunacceptable production.

After studying this chapter, you should be able to:

© McGraw-Hill Ryerson Limited., 2001

3-5

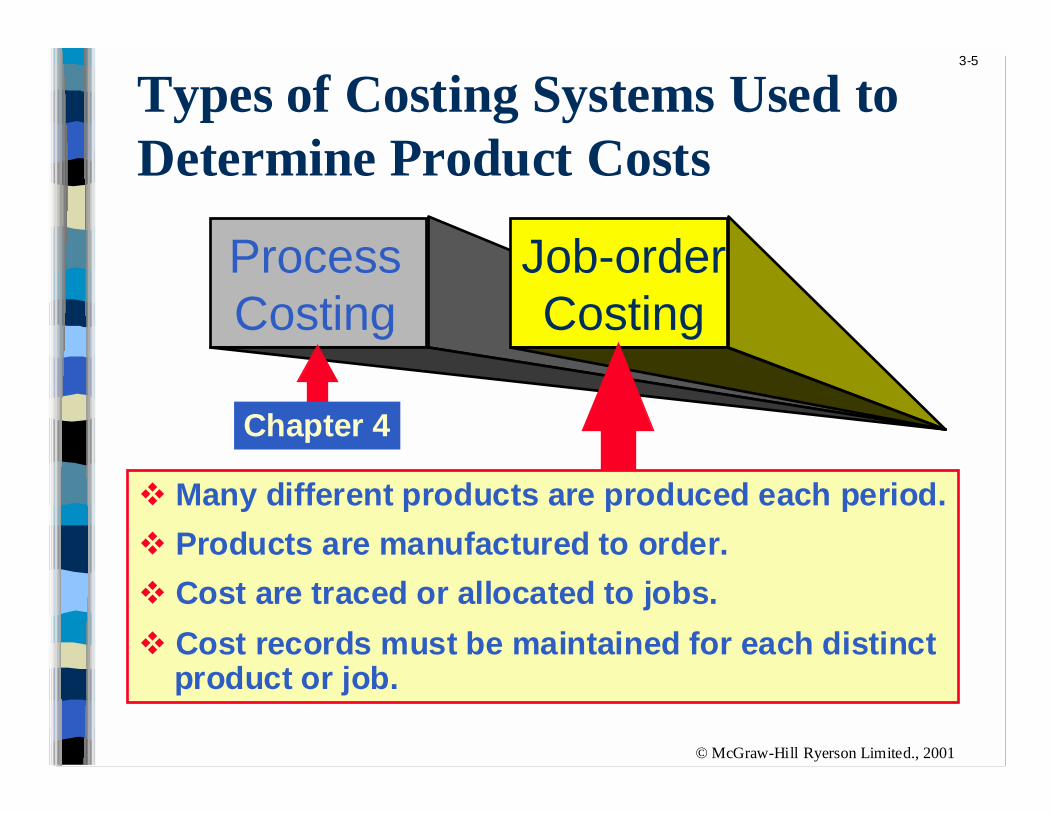

Types of Costing Systems Used toDetermine Product Costs

ProcessCosting

Job-orderCosting

! Many different products are produced each period.

! Products are manufactured to order.

! Cost are traced or allocated to jobs.

! Cost records must be maintained for each distinct product or job.

Chapter 4

© McGraw-Hill Ryerson Limited., 2001

3-6

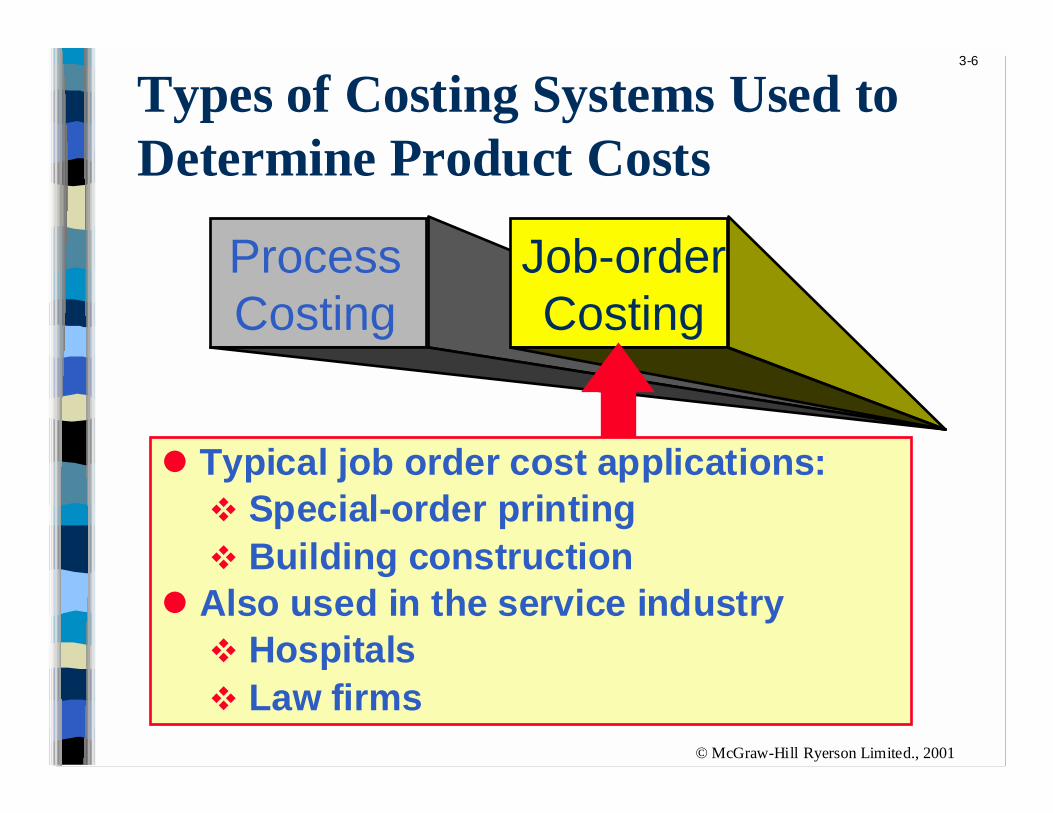

Types of Costing Systems Used toDetermine Product Costs

ProcessCosting

Job-orderCosting

" Typical job order cost applications:! Special-order printing! Building construction

" Also used in the service industry! Hospitals! Law firms

© McGraw-Hill Ryerson Limited., 2001

3-7

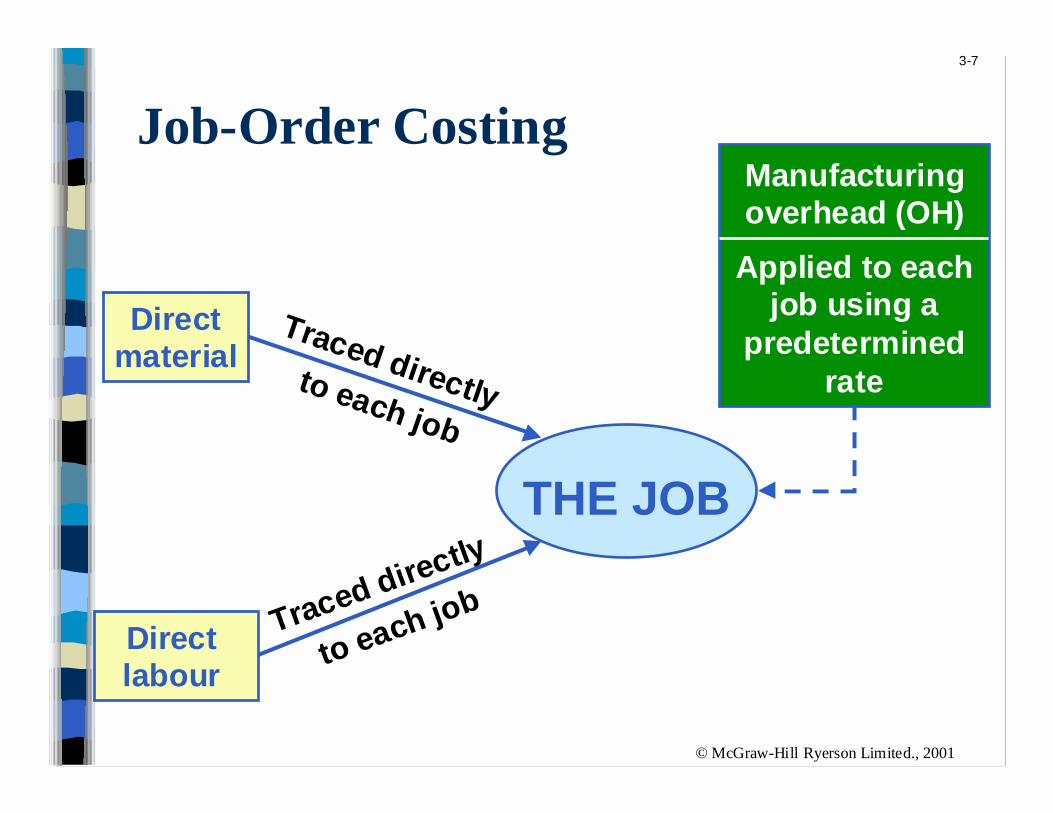

Job-Order Costing

THE JOB

Directmaterial

Direct labour

Traced directly to each job

Traced directly

to each job

Manufacturingoverhead (OH)

Applied to eachjob using a

predeterminedrate

© McGraw-Hill Ryerson Limited., 2001

3-8

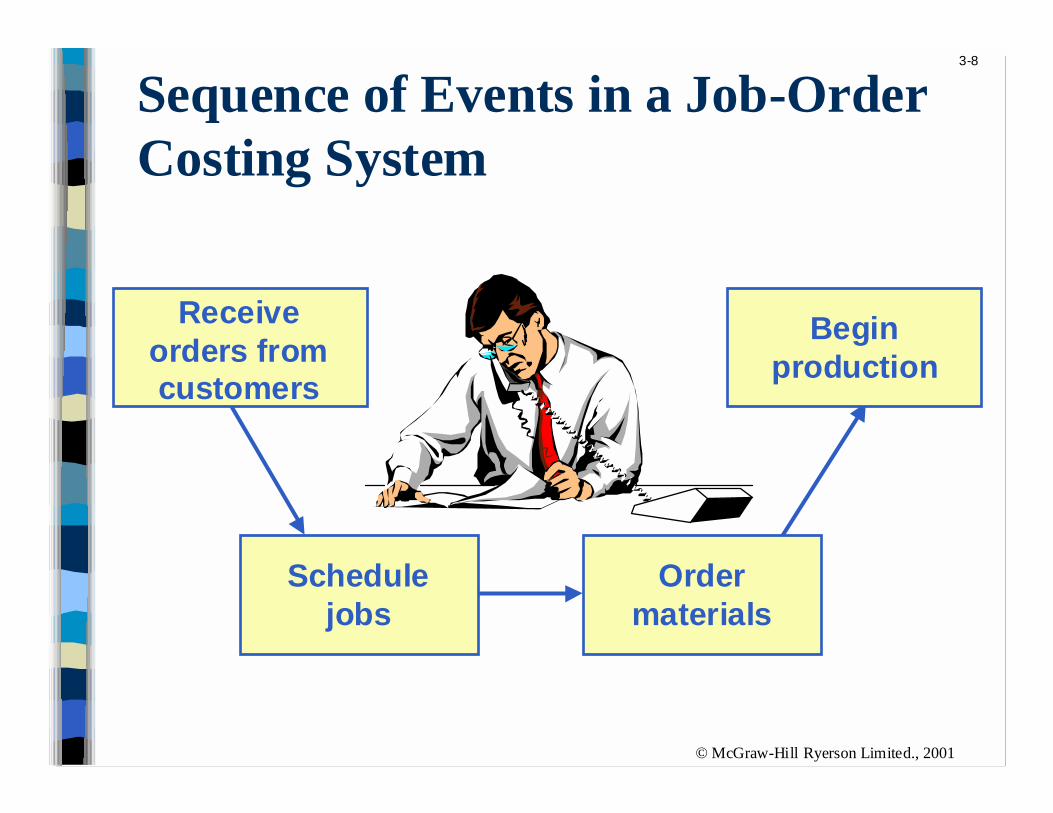

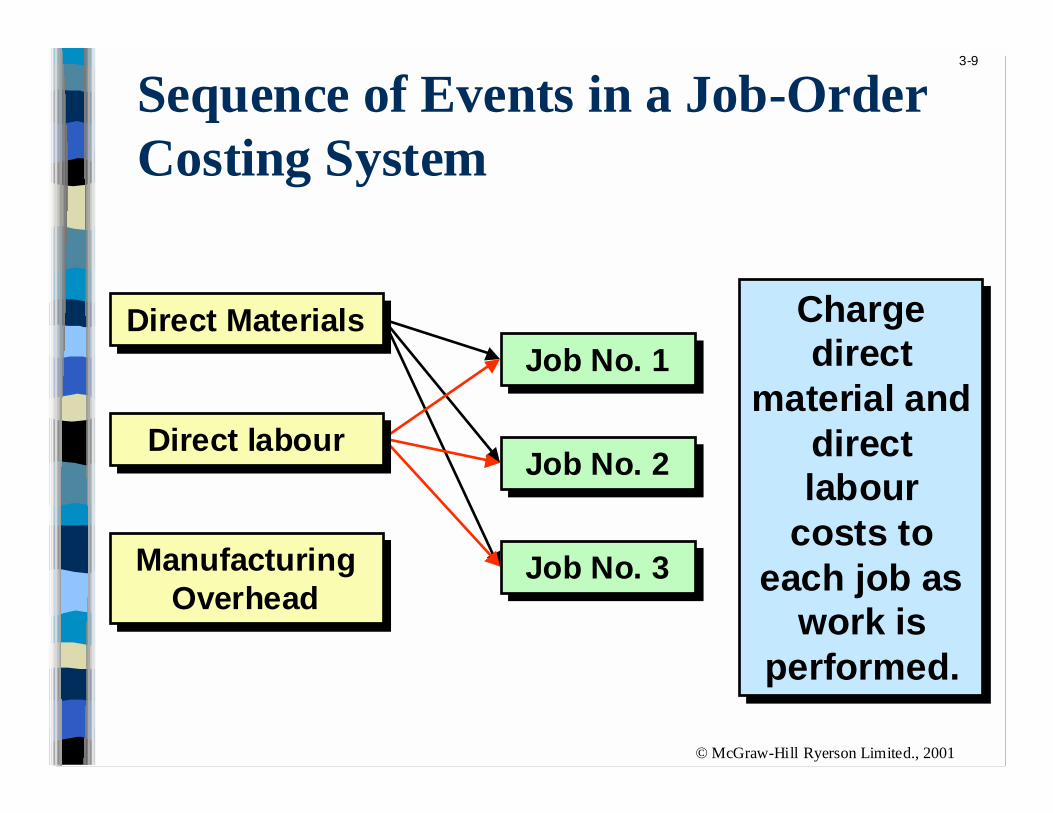

Sequence of Events in a Job-OrderCosting System

Receiveorders fromcustomers

Schedulejobs

Ordermaterials

Beginproduction

© McGraw-Hill Ryerson Limited., 2001

3-9

ManufacturingOverhead

ManufacturingOverhead

Job No. 1Job No. 1

Job No. 2Job No. 2

Job No. 3Job No. 3

Chargedirect

material anddirectlabour

costs toeach job as

work isperformed.

Chargedirect

material anddirectlabour

costs toeach job as

work isperformed.

Sequence of Events in a Job-OrderCosting System

Direct MaterialsDirect Materials

Direct labourDirect labour

© McGraw-Hill Ryerson Limited., 2001

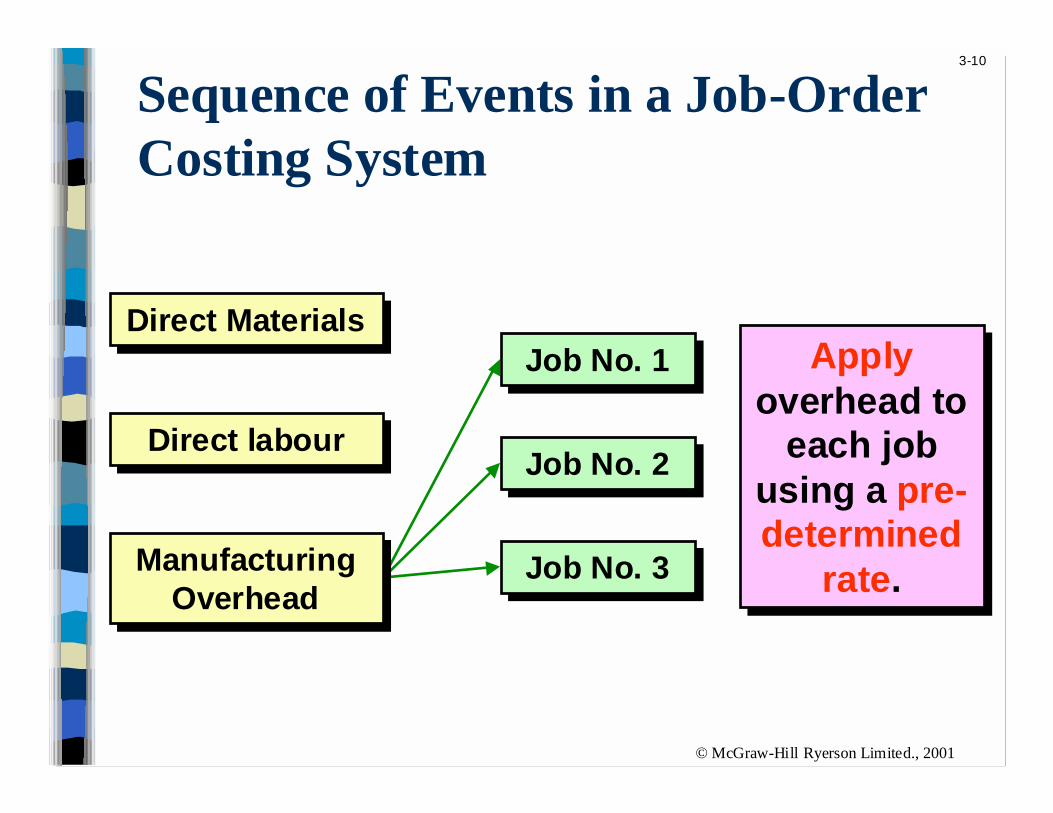

3-10

Applyoverhead to

each jobusing a pre-determined

rate.

Applyoverhead to

each jobusing a pre-determined

rate.

Sequence of Events in a Job-OrderCosting System

Direct MaterialsDirect Materials

Direct labourDirect labour

Job No. 1Job No. 1

Job No. 2Job No. 2

Job No. 3Job No. 3ManufacturingOverhead

ManufacturingOverhead

© McGraw-Hill Ryerson Limited., 2001

3-11

Job-Order Cost Accounting

The primarydocument fortracking the

costs associatedwith a given jobis the job cost

sheet.

Let’s investigate

© McGraw-Hill Ryerson Limited., 2001

3-12

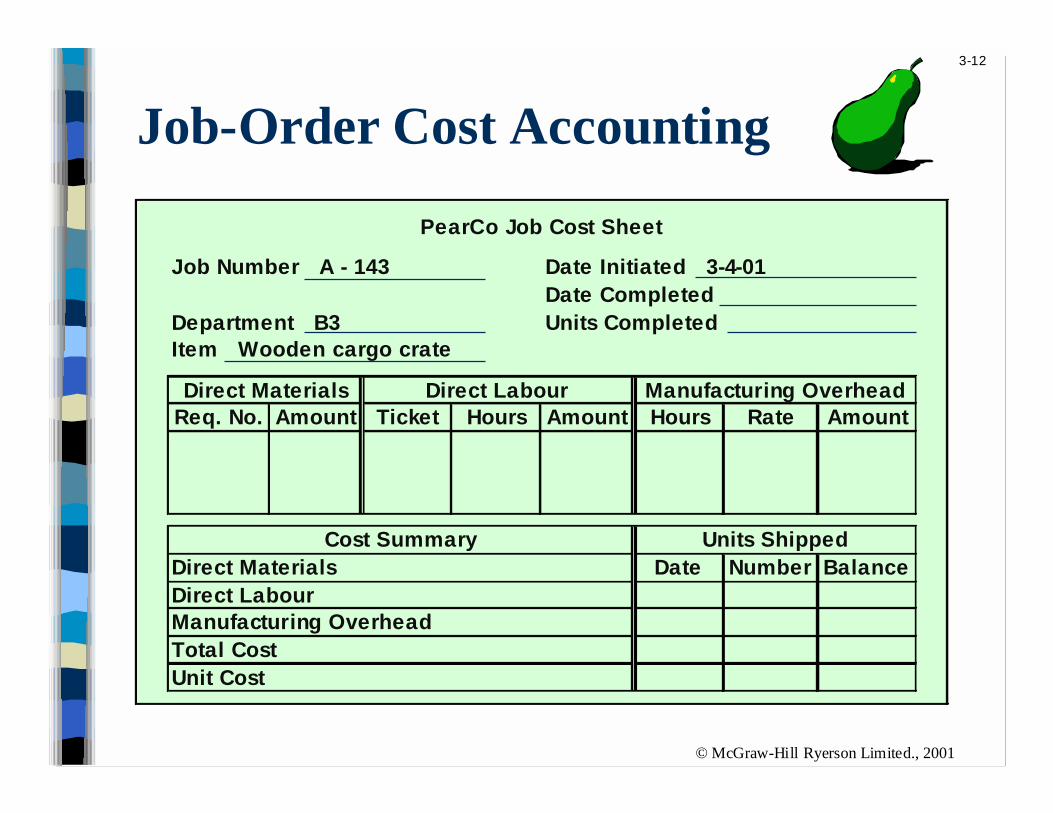

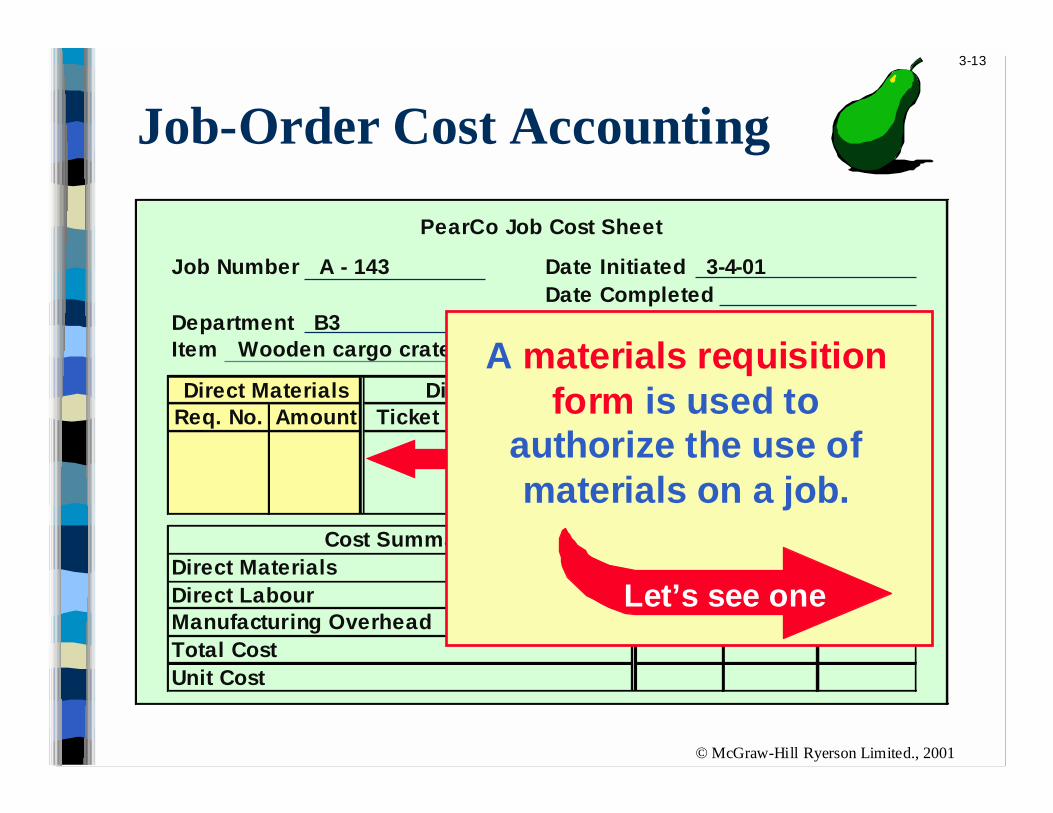

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed

Department B3 Units CompletedItem Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate Amount

Cost Summary Units ShippedDirect Materials Date Number BalanceDirect LabourManufacturing OverheadTotal CostUnit Cost

Job-Order Cost Accounting

© McGraw-Hill Ryerson Limited., 2001

3-13

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed

Department B3 Units CompletedItem Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate Amount

Cost Summary Units ShippedDirect Materials Date Number BalanceDirect LabourManufacturing OverheadTotal CostUnit Cost

Job-Order Cost Accounting

Let’s see one

A materials requisitionform is used to

authorize the use ofmaterials on a job.

© McGraw-Hill Ryerson Limited., 2001

3-14

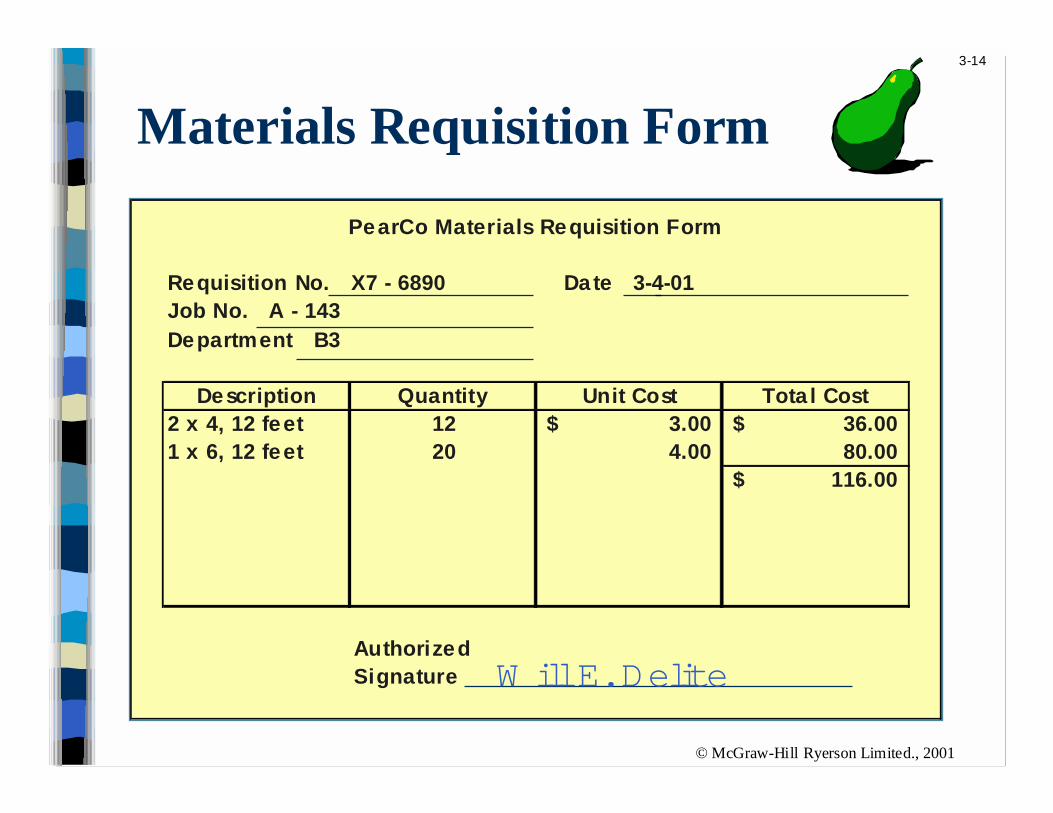

Materials Requisition Form

PearCo Materials Requisition Form

Requisition No. X7 - 6890 Date 3-4-01Job No. A - 143Department B3

Description Quantity Unit Cost Tota l Cost2 x 4, 12 feet 12 3.00$ 36.00$ 1 x 6, 12 feet 20 4.00 80.00

116.00$

Authorized Signature W ill E. Delite

© McGraw-Hill Ryerson Limited., 2001

3-15

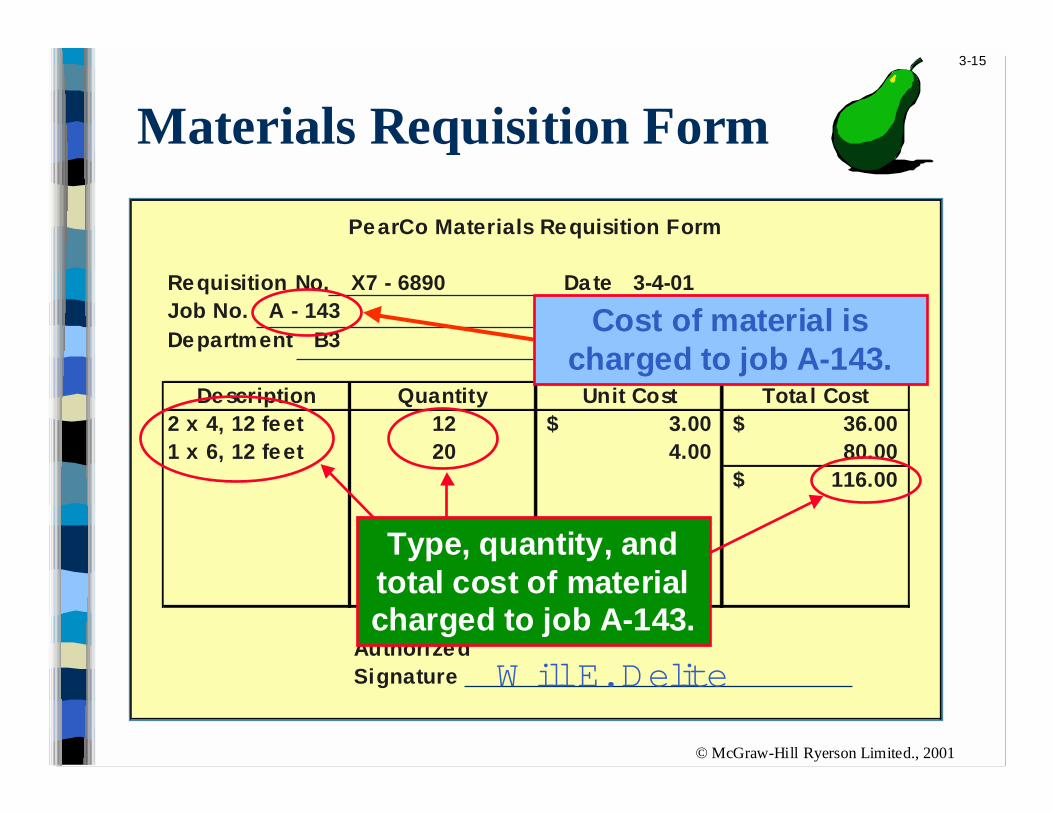

PearCo Materials Requisition Form

Requisition No. X7 - 6890 Date 3-4-01Job No. A - 143Department B3

Description Quantity Unit Cost Tota l Cost2 x 4, 12 feet 12 3.00$ 36.00$ 1 x 6, 12 feet 20 4.00 80.00

116.00$

Authorized Signature

Materials Requisition Form

W ill E. Delite

Type, quantity, andtotal cost of materialcharged to job A-143.

Cost of material ischarged to job A-143.

© McGraw-Hill Ryerson Limited., 2001

3-16

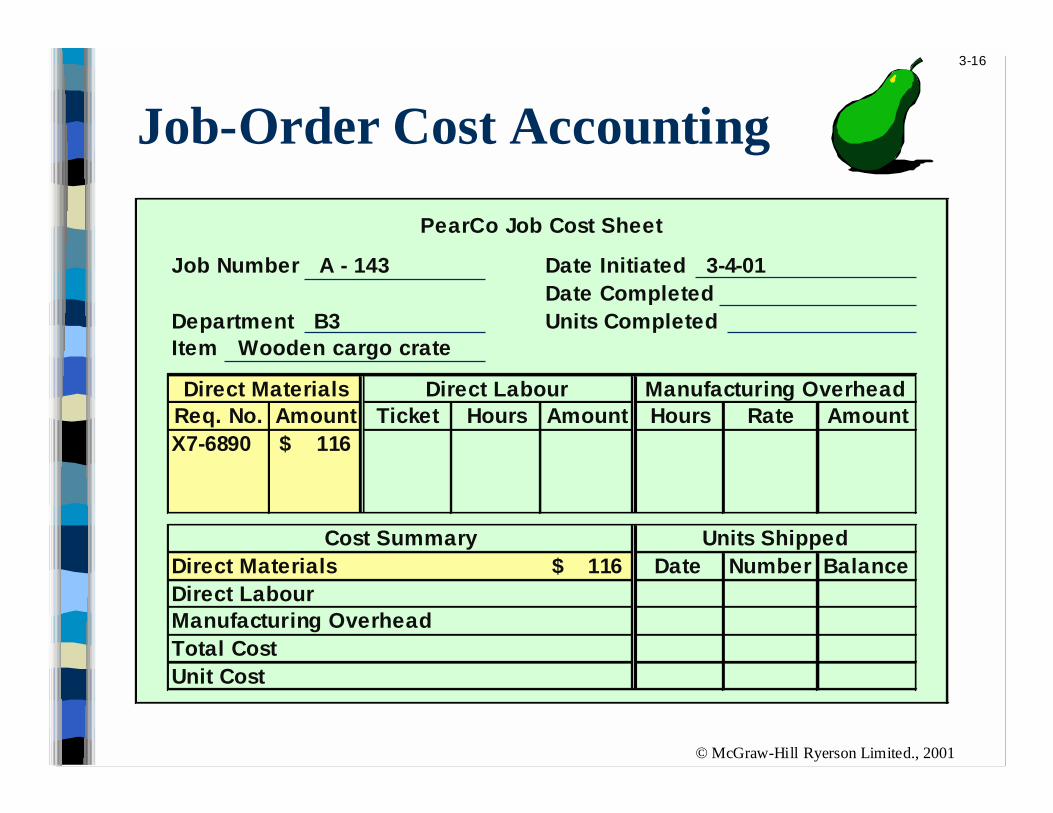

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed

Department B3 Units CompletedItem Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$

Cost Summary Units ShippedDirect Materials 116$ Date Number BalanceDirect LabourManufacturing OverheadTotal CostUnit Cost

Job-Order Cost Accounting

© McGraw-Hill Ryerson Limited., 2001

3-17

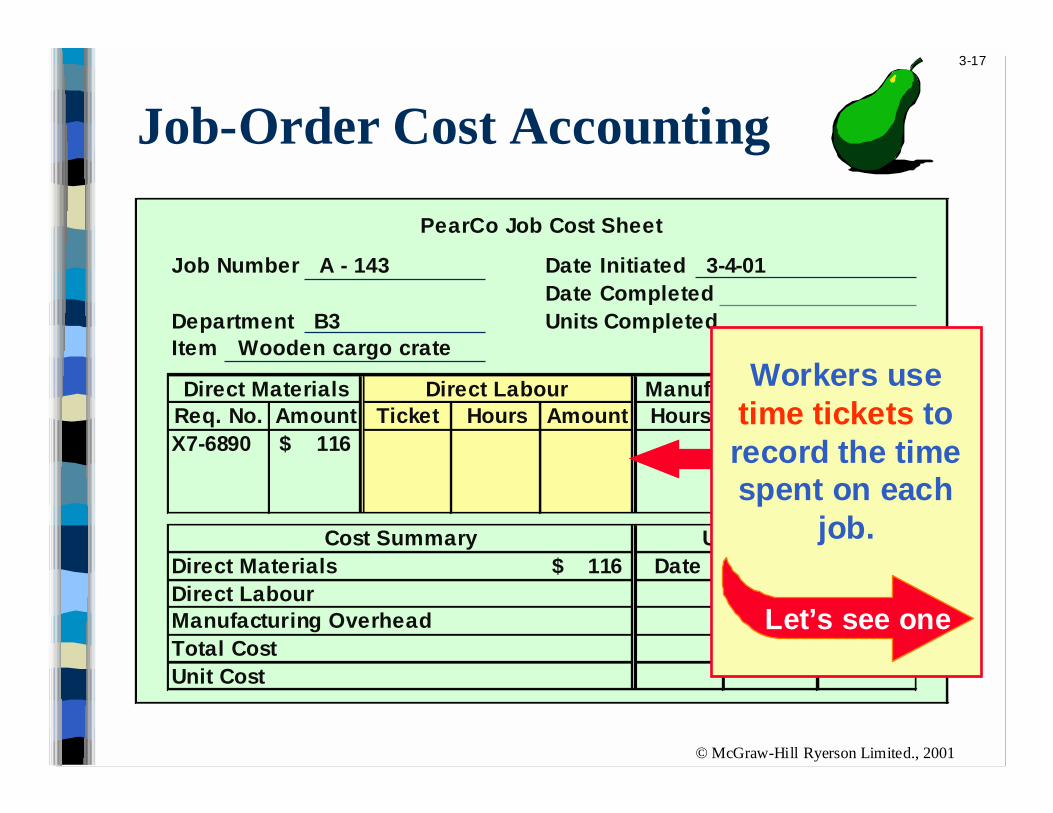

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed

Department B3 Units CompletedItem Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$

Cost Summary Units ShippedDirect Materials 116$ Date Number BalanceDirect LabourManufacturing OverheadTotal CostUnit Cost

Job-Order Cost Accounting

Workers usetime tickets torecord the timespent on each

job.

Let’s see one

© McGraw-Hill Ryerson Limited., 2001

3-18

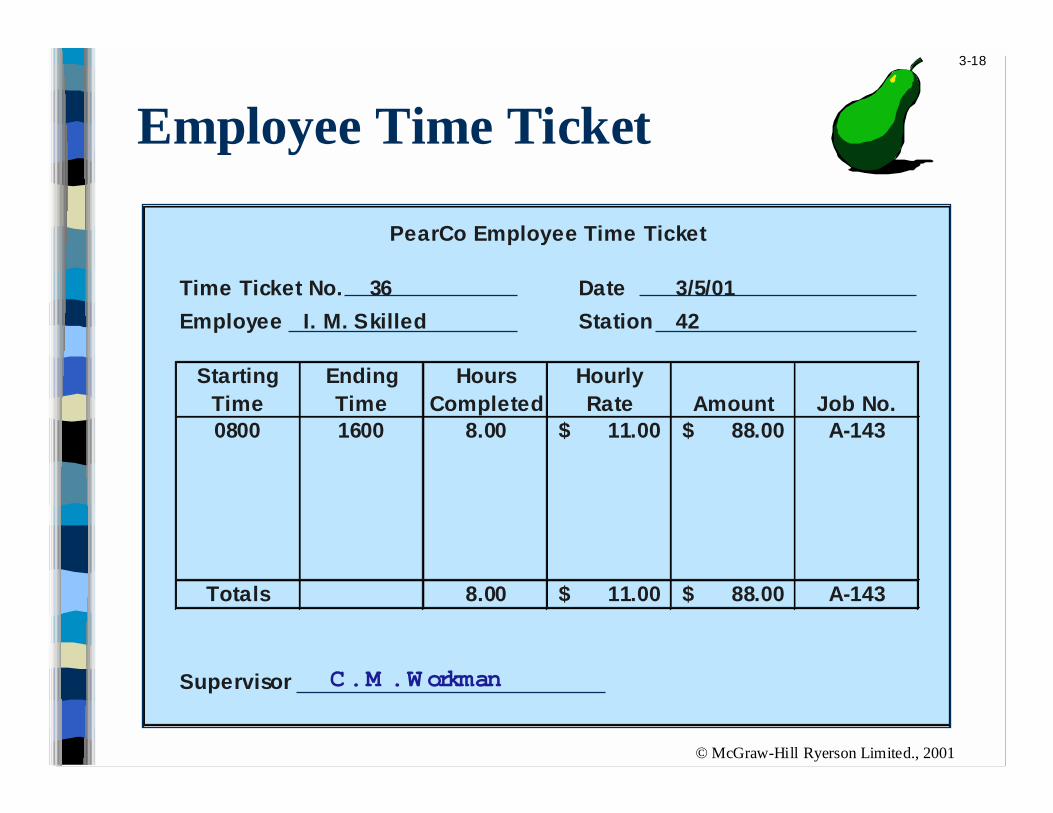

Employee Time Ticket

PearCo Employee Time Ticket

Time Ticket No. 36 Date 3/5/01

Employee I. M. Skilled Station 42

Starting Ending Hours HourlyTime Time Completed Rate Amount Job No.0800 1600 8.00 11.00$ 88.00$ A-143

Totals 8.00 11.00$ 88.00$ A-143

Supervisor C. M . W orkman

© McGraw-Hill Ryerson Limited., 2001

3-19

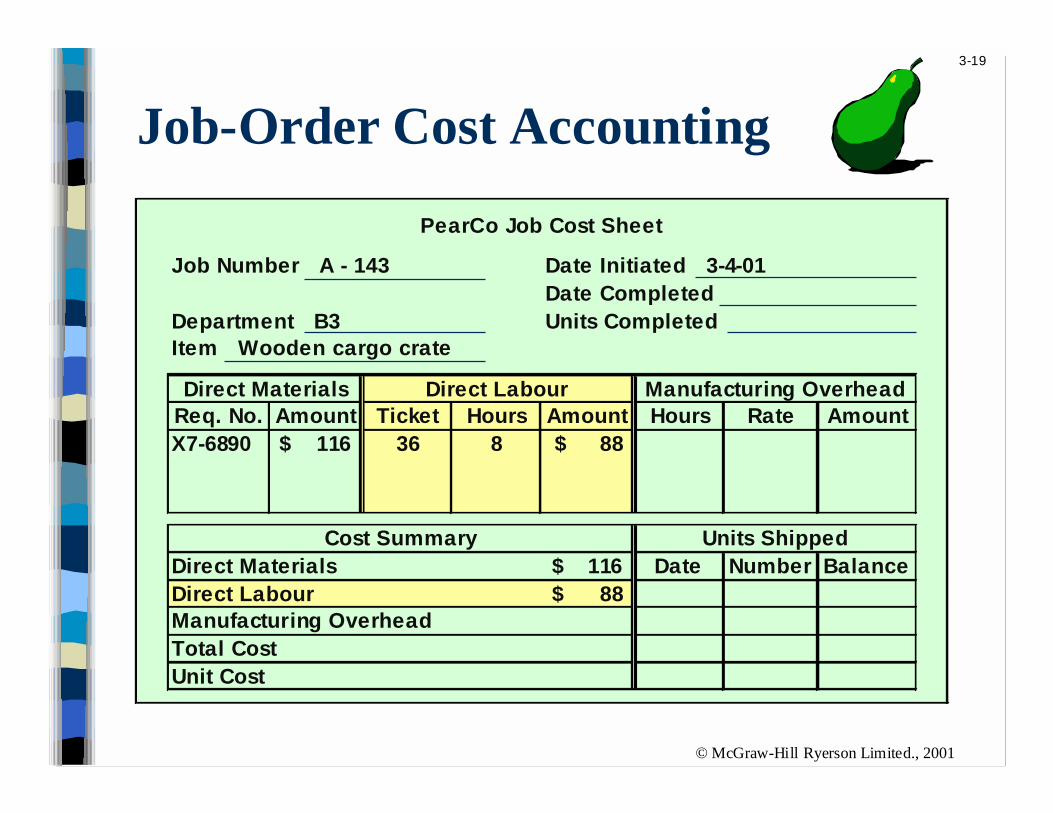

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed

Department B3 Units CompletedItem Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$ 36 8 88$

Cost Summary Units ShippedDirect Materials 116$ Date Number BalanceDirect Labour 88$ Manufacturing OverheadTotal CostUnit Cost

Job-Order Cost Accounting

© McGraw-Hill Ryerson Limited., 2001

3-20

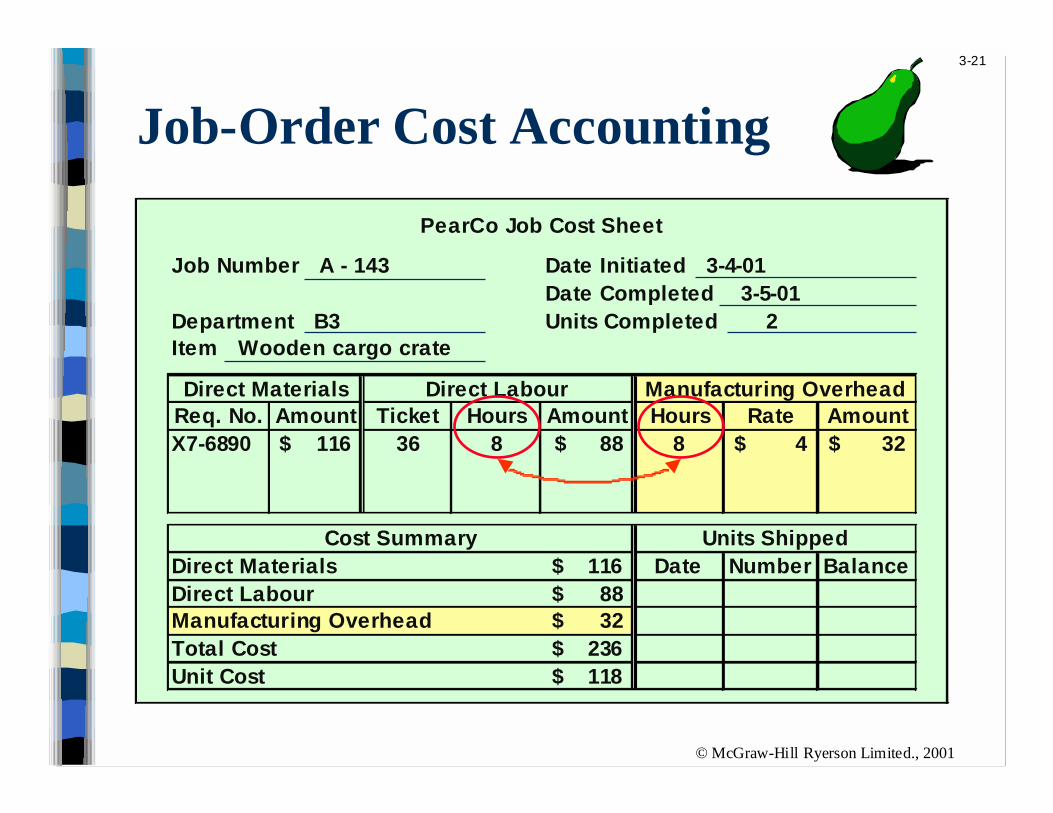

Job-Order Cost Accounting

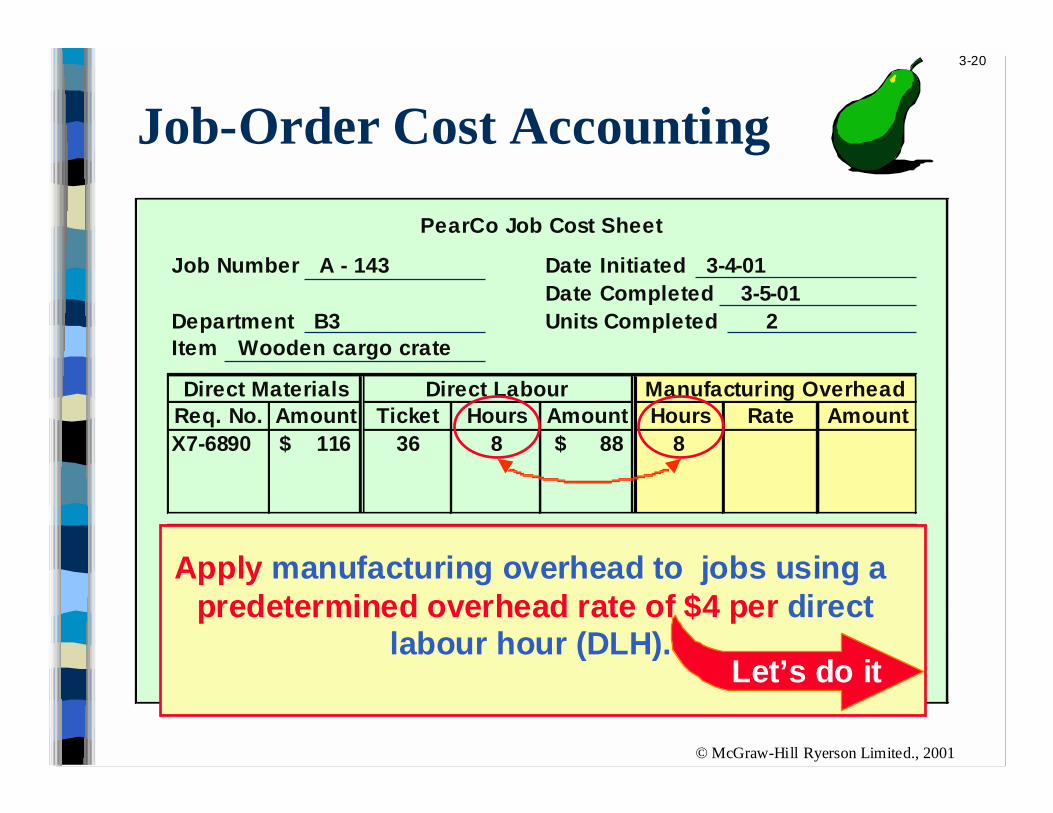

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed 3-5-01

Department B3 Units Completed 2Item Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$ 36 8 88$ 8

Cost Summary Units ShippedDirect Materials 116$ Date Number BalanceDirect Labour 88$ Manufacturing Overhead 32$ Total Cost 236$ Unit Cost 118$

Apply manufacturing overhead to jobs using a predetermined overhead rate of $4 per direct

labour hour (DLH).Let’s do it

© McGraw-Hill Ryerson Limited., 2001

3-21

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed 3-5-01

Department B3 Units Completed 2Item Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$ 36 8 88$ 8 4$ 32$

Cost Summary Units ShippedDirect Materials 116$ Date Number BalanceDirect Labour 88$ Manufacturing Overhead 32$ Total Cost 236$ Unit Cost 118$

Job-Order Cost Accounting

© McGraw-Hill Ryerson Limited., 2001

3-22

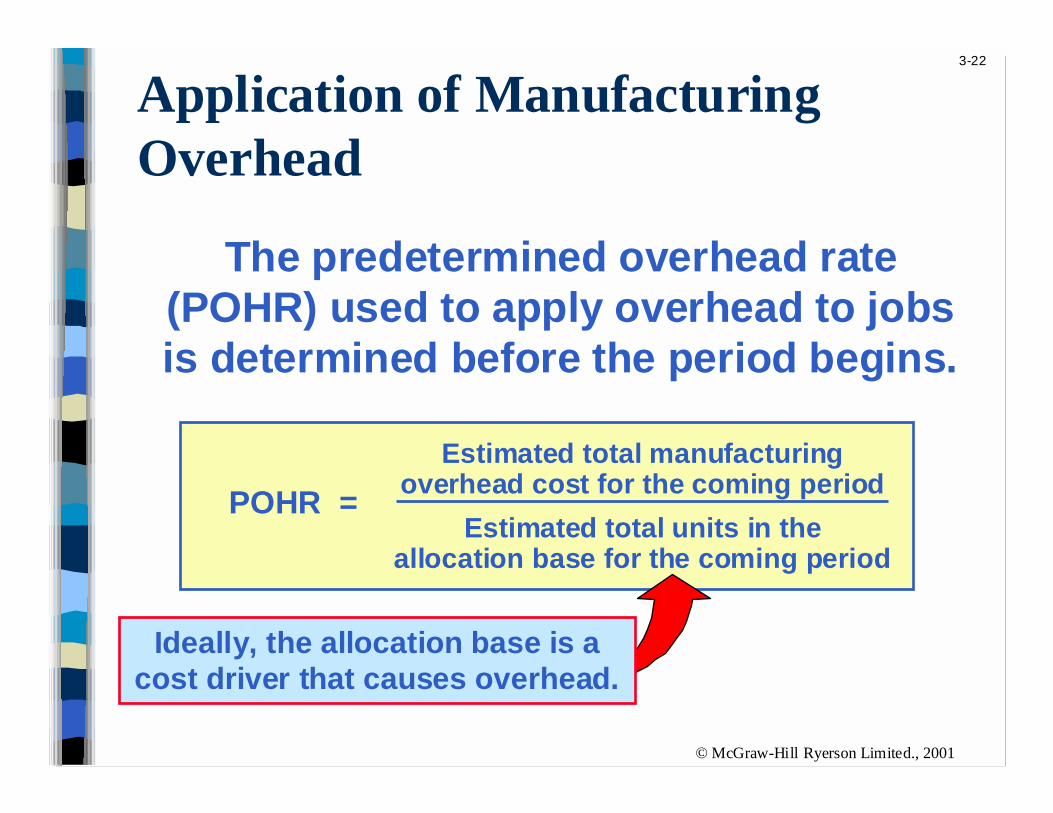

Estimated total manufacturingoverhead cost for the coming period

Estimated total units in theallocation base for the coming period

POHR =

The predetermined overhead rate(POHR) used to apply overhead to jobsis determined before the period begins.

Application of ManufacturingOverhead

Ideally, the allocation base is acost driver that causes overhead.

© McGraw-Hill Ryerson Limited., 2001

3-23

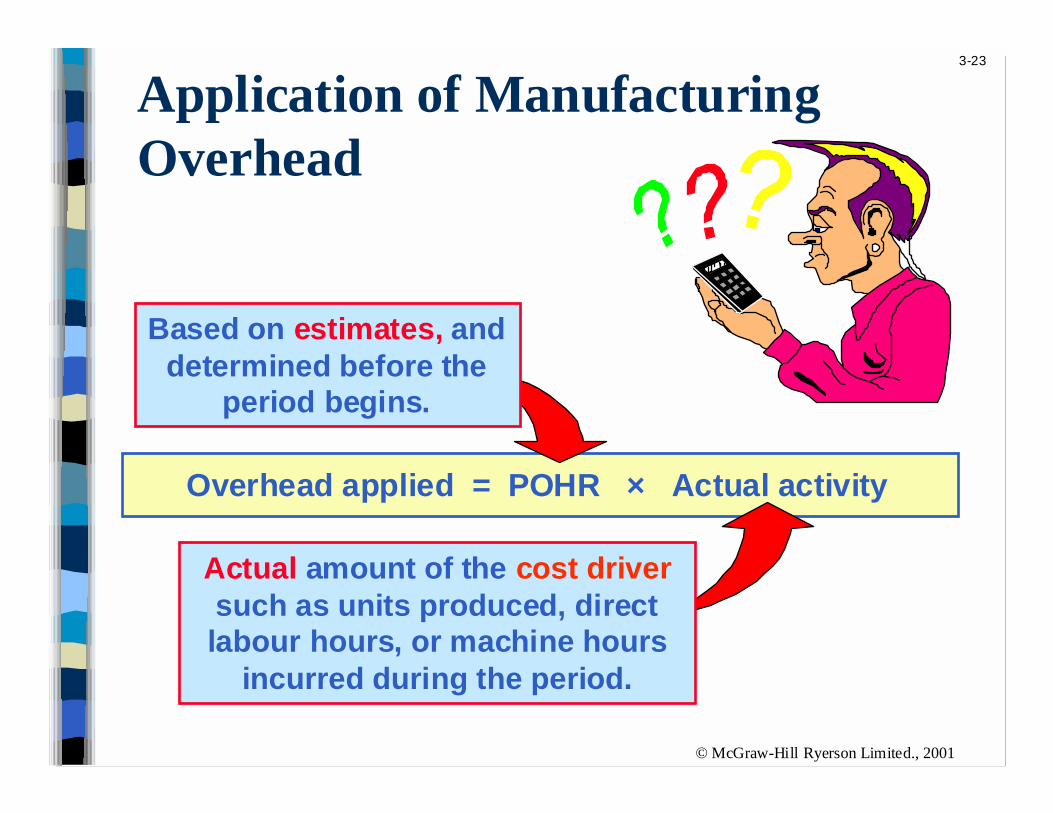

Application of ManufacturingOverhead

Overhead applied = POHR × Actual activity

Actual amount of the cost driversuch as units produced, directlabour hours, or machine hours

incurred during the period.

Based on estimates, anddetermined before the

period begins.

© McGraw-Hill Ryerson Limited., 2001

3-24

Application of ManufacturingOverhead

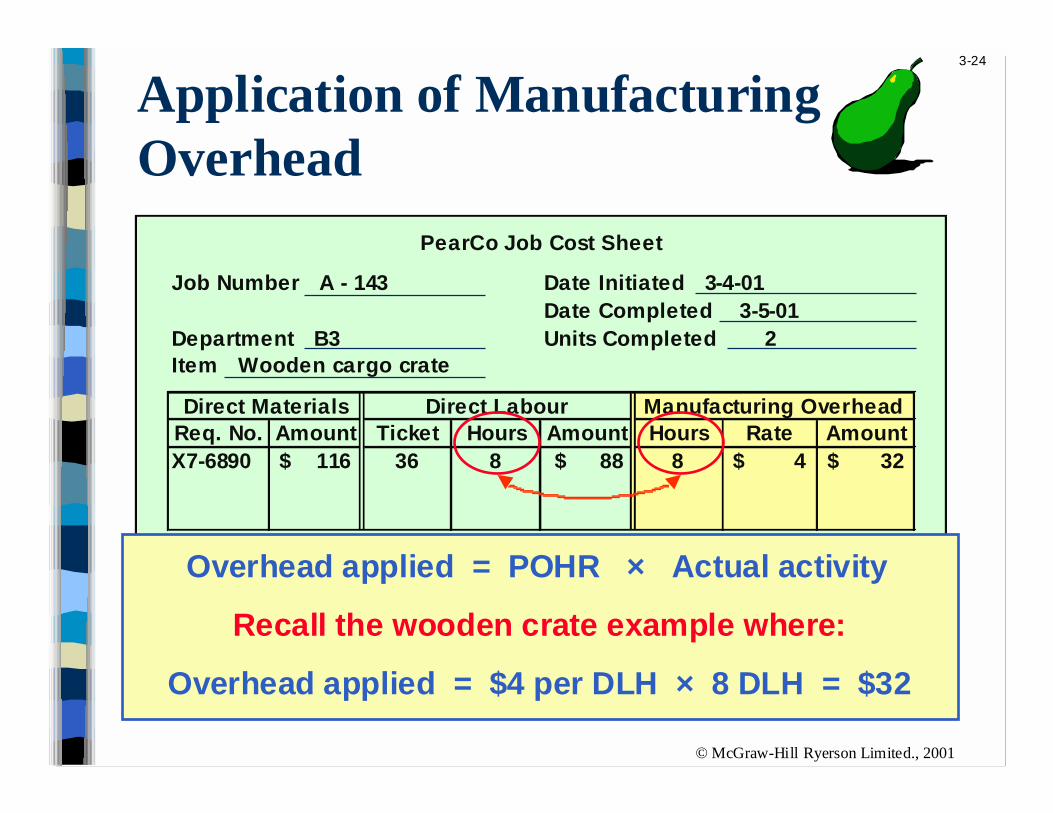

PearCo Job Cost Sheet

Job Number A - 143 Date Initiated 3-4-01Date Completed 3-5-01

Department B3 Units Completed 2Item Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-6890 116$ 36 8 88$ 8 4$ 32$

Recall the wooden crate example where:

Overhead applied = $4 per DLH × 8 DLH = $32

Overhead applied = POHR × Actual activity

© McGraw-Hill Ryerson Limited., 2001

3-25

The Need for a PredeterminedManufacturing Overhead Rate

Using a predetermined rate makes itpossible to estimate total job costs sooner.

Actual overhead for the period is notknown until the end of the period.

$$

© McGraw-Hill Ryerson Limited., 2001

3-26

PearCo applies overhead based on directlabour hours. Total estimated overheadfor the year is $640,000. Total estimated

labour cost is $1,400,000 and totalestimated labour hours are 160,000.

What is PearCo’s predeterminedoverhead rate per hour?

Overhead Application Example

© McGraw-Hill Ryerson Limited., 2001

3-27

For each direct labour hour worked ona job, $4.00 of factory overhead will be

applied to the job.

Overhead Application Example

POHR = $4.00 per DLH

$640,000

160,000 direct labour hours (DLH)POHR =

Estimated total manufacturingoverhead cost for the coming period

Estimated total units in theallocation base for the coming period

POHR =

© McGraw-Hill Ryerson Limited., 2001

3-28

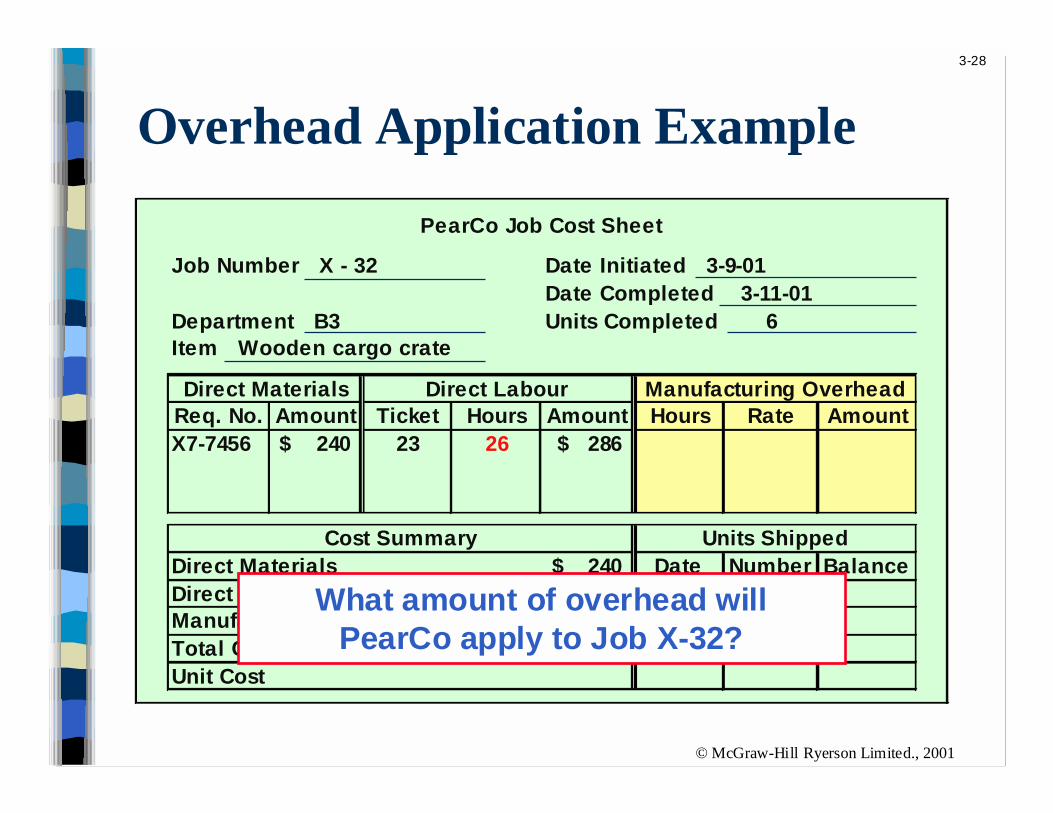

PearCo Job Cost Sheet

Job Number X - 32 Date Initiated 3-9-01Date Completed 3-11-01

Department B3 Units Completed 6Item Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-7456 240$ 23 26 286$

Cost Summary Units ShippedDirect Materials 240$ Date Number BalanceDirect Labour 286$ Manufacturing OverheadTotal CostUnit Cost

Overhead Application Example

What amount of overhead willPearCo apply to Job X-32?

© McGraw-Hill Ryerson Limited., 2001

3-29

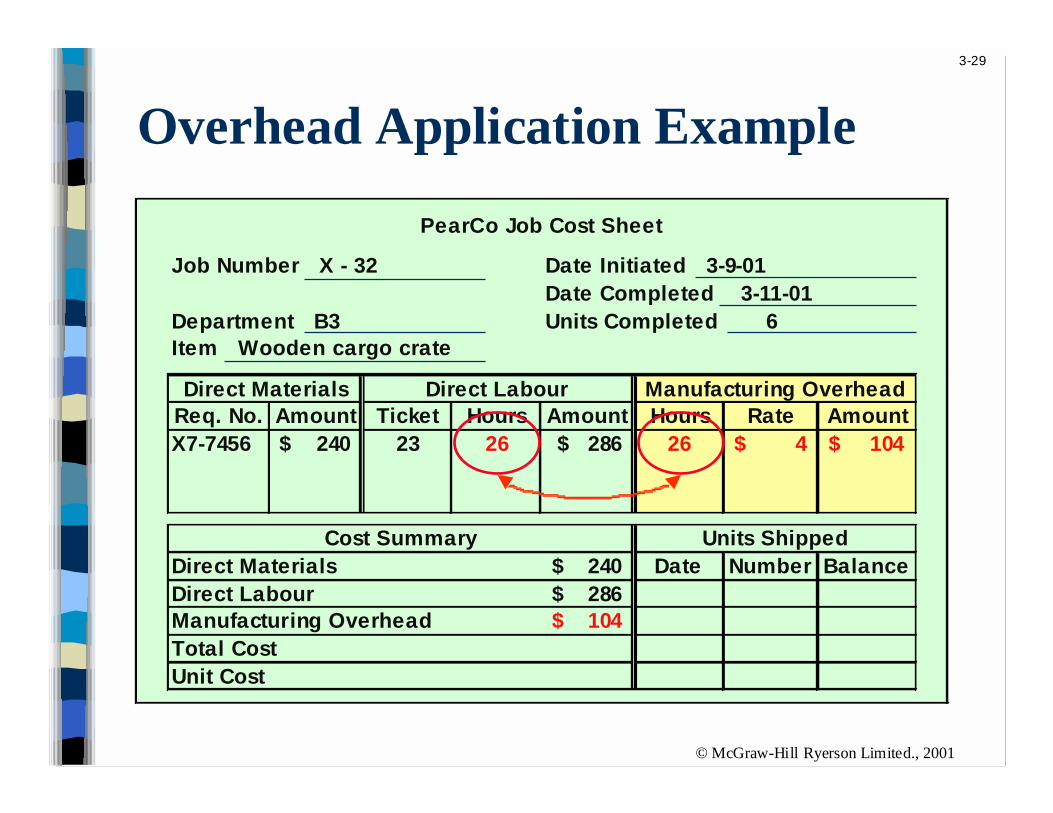

PearCo Job Cost Sheet

Job Number X - 32 Date Initiated 3-9-01Date Completed 3-11-01

Department B3 Units Completed 6Item Wooden cargo crate

Direct Materials Direct Labour Manufacturing OverheadReq. No. Amount Ticket Hours Amount Hours Rate AmountX7-7456 240$ 23 26 286$ 26 4$ 104$

Cost Summary Units ShippedDirect Materials 240$ Date Number BalanceDirect Labour 286$ Manufacturing Overhead 104$ Total CostUnit Cost

Overhead Application Example

© McGraw-Hill Ryerson Limited., 2001

3-30

Let’s summarizethe documentflow we have

been discussingin a job-order

costing system.

Job-Order CostingDocument Flow Summary

© McGraw-Hill Ryerson Limited., 2001

3-31

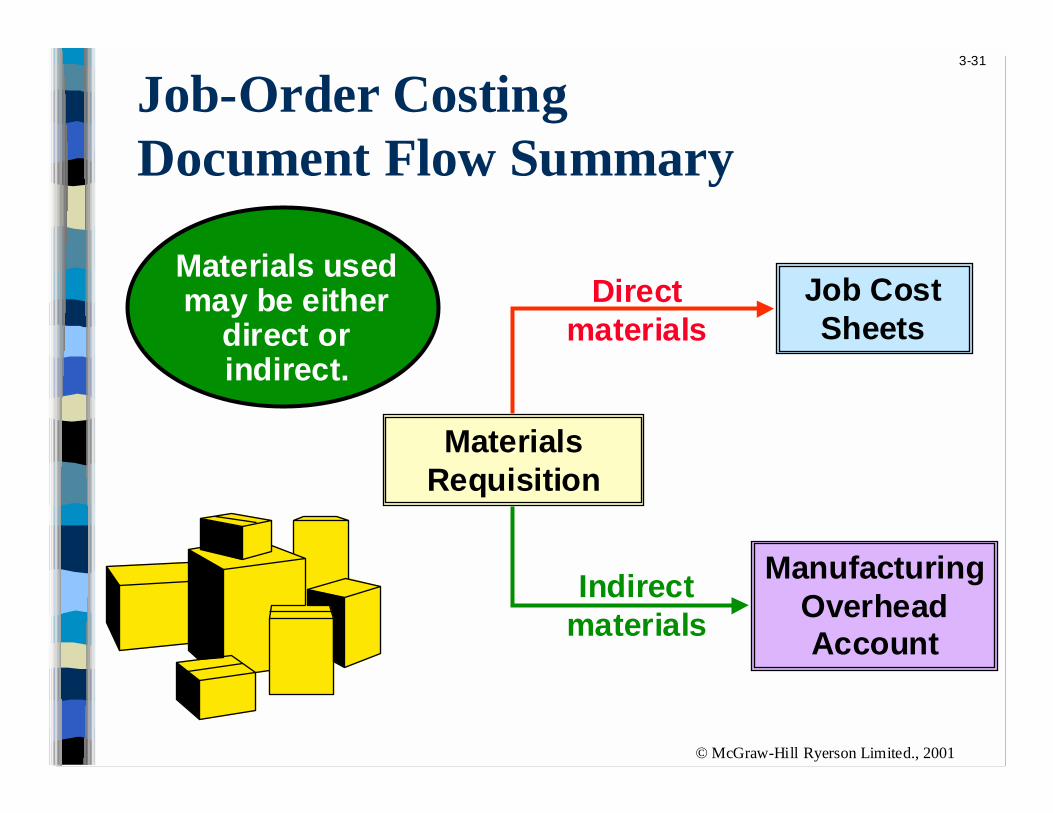

Job-Order CostingDocument Flow Summary

Job CostSheets

MaterialsRequisition

Directmaterials

Indirectmaterials

ManufacturingOverheadAccount

Materials usedmay be either

direct orindirect.

© McGraw-Hill Ryerson Limited., 2001

3-32

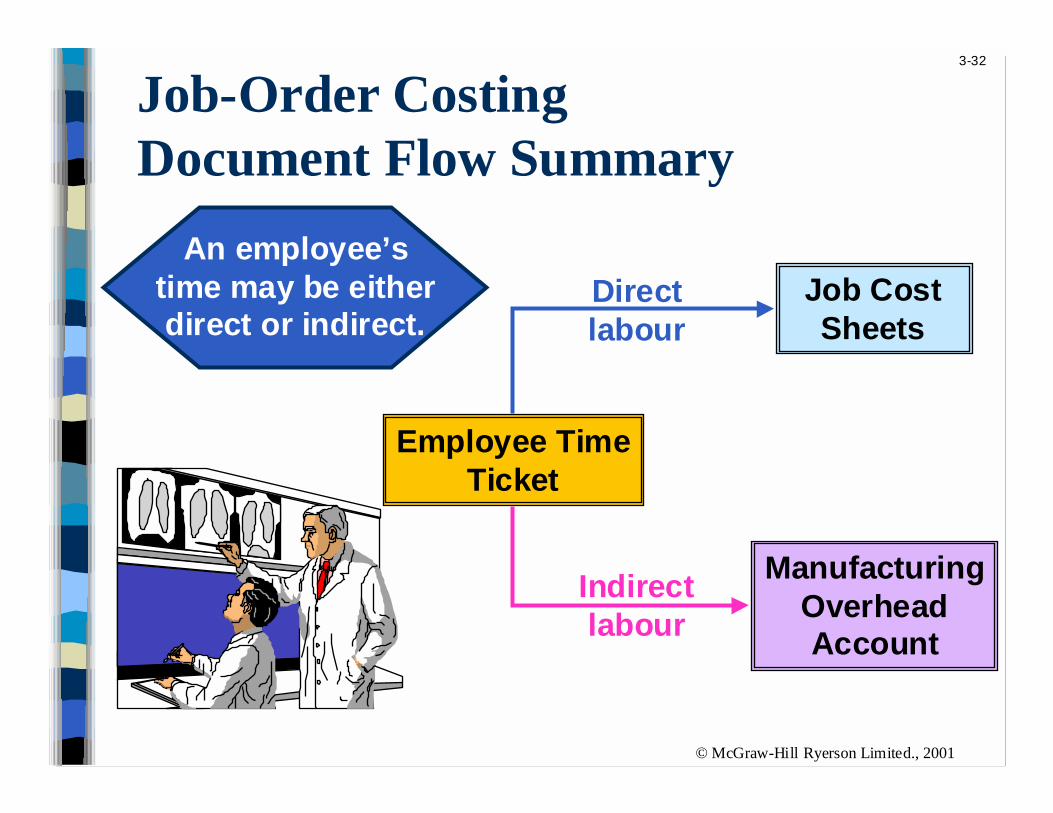

Job-Order CostingDocument Flow Summary

Job CostSheets

Employee TimeTicket

ManufacturingOverheadAccount

Directlabour

Indirectlabour

An employee’stime may be eitherdirect or indirect.

© McGraw-Hill Ryerson Limited., 2001

3-33

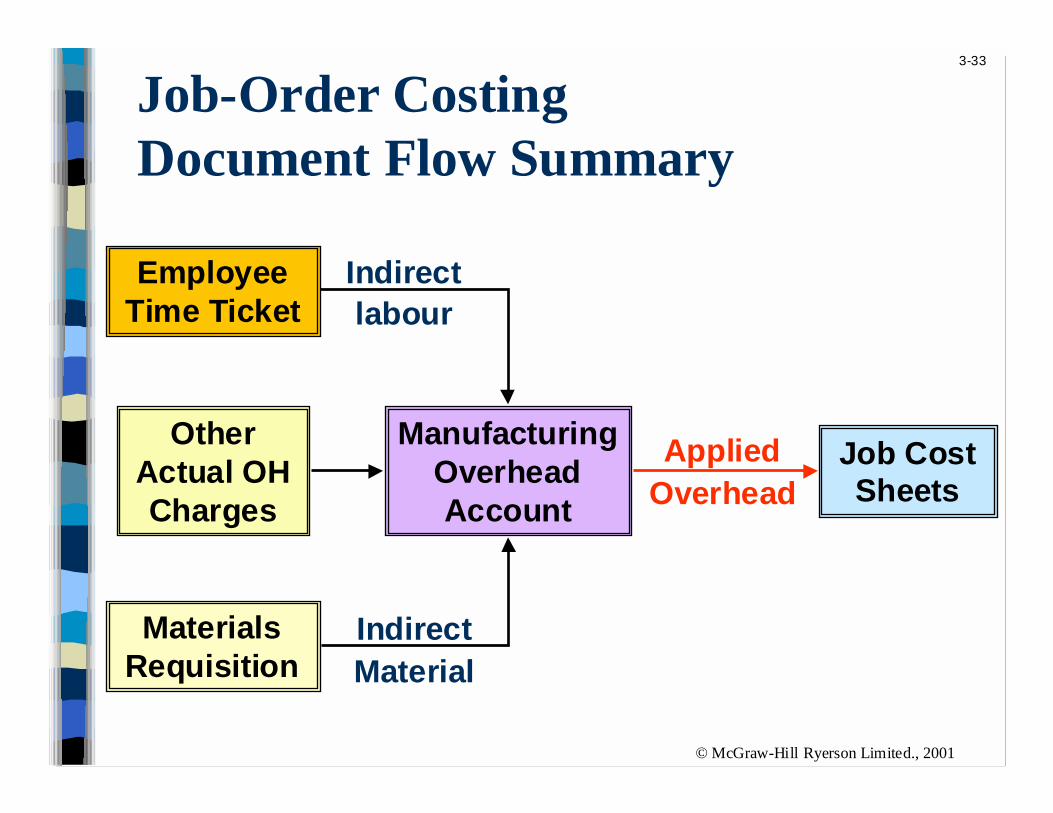

Job-Order CostingDocument Flow Summary

EmployeeTime Ticket

Job CostSheets

MaterialsRequisition

OtherActual OHCharges

IndirectMaterial

Indirectlabour

AppliedOverhead

ManufacturingOverheadAccount

© McGraw-Hill Ryerson Limited., 2001

3-34

Let’s examine thecost flows in a

job-order costingsystem. We willuse T-accountsand start with

materials.

Job-Order System Cost Flows

© McGraw-Hill Ryerson Limited., 2001

3-35

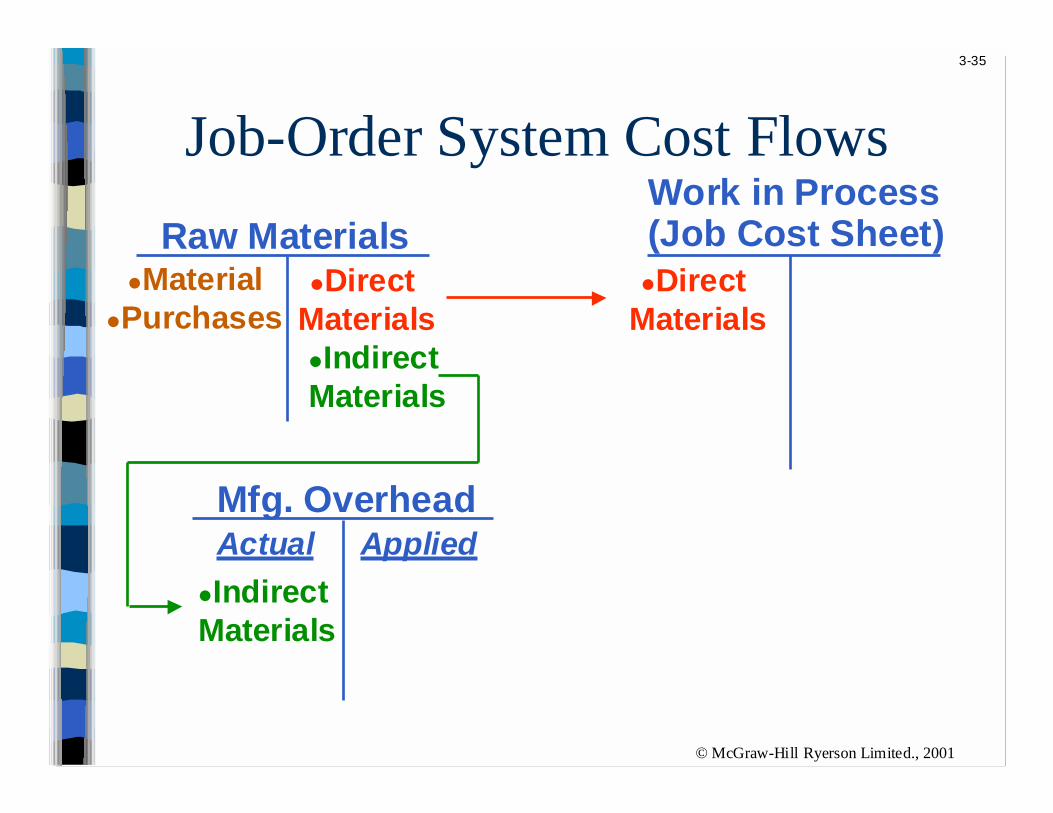

Raw Materials"Material

"Purchases"Direct

Materials"Direct

Materials

Mfg. Overhead

"Indirect Materials

Job-Order System Cost FlowsWork in Process(Job Cost Sheet)

"Indirect Materials

Actual Applied

© McGraw-Hill Ryerson Limited., 2001

3-36

Next let’s addlabour costs and

appliedmanufacturingoverhead to thejob-order costflows. Are you

with me?

Job-Order System Cost Flows

© McGraw-Hill Ryerson Limited., 2001

3-37

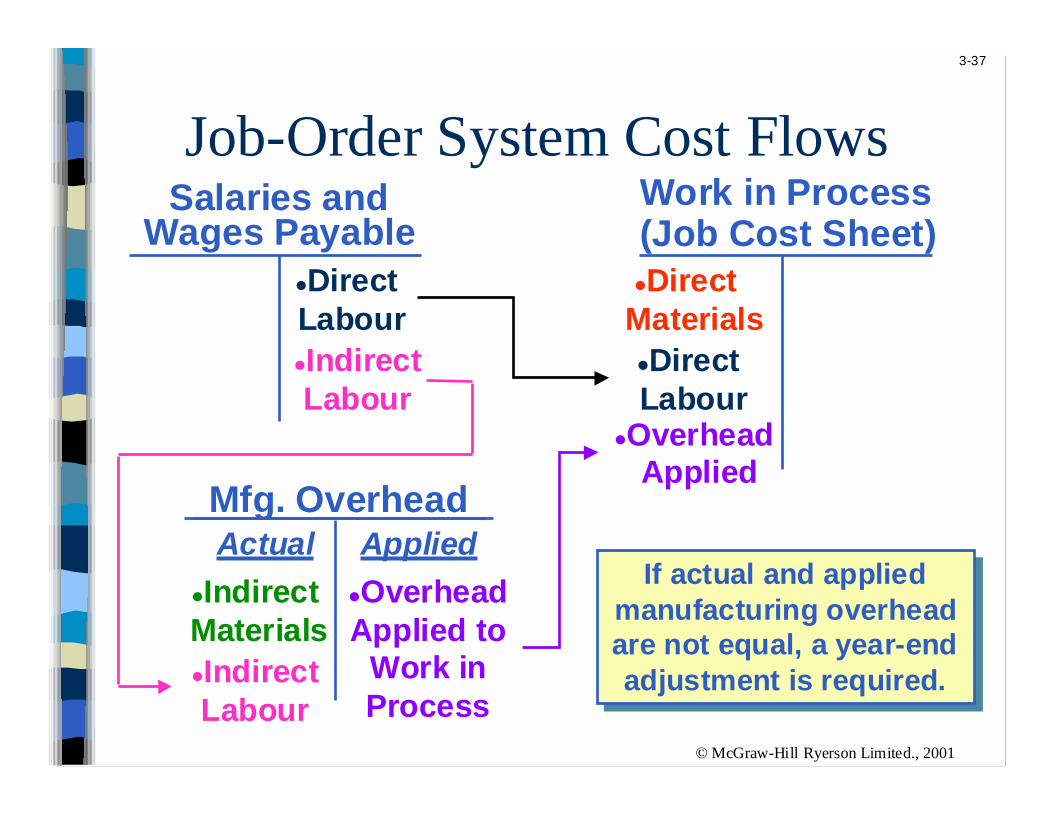

Job-Order System Cost Flows

"Direct Labour

Mfg. Overhead

Salaries andWages Payable

Work in Process(Job Cost Sheet)"Direct

Materials

"OverheadApplied to

Work inProcess

"IndirectLabour

"Direct Labour

"Overhead Applied

"IndirectLabour

"Indirect Materials

Actual AppliedIf actual and applied

manufacturing overheadare not equal, a year-endadjustment is required.

If actual and appliedmanufacturing overheadare not equal, a year-endadjustment is required.

© McGraw-Hill Ryerson Limited., 2001

3-38

Now let’scomplete the

goods and sellthem. Still with

me?

Job-Order System Cost Flows

© McGraw-Hill Ryerson Limited., 2001

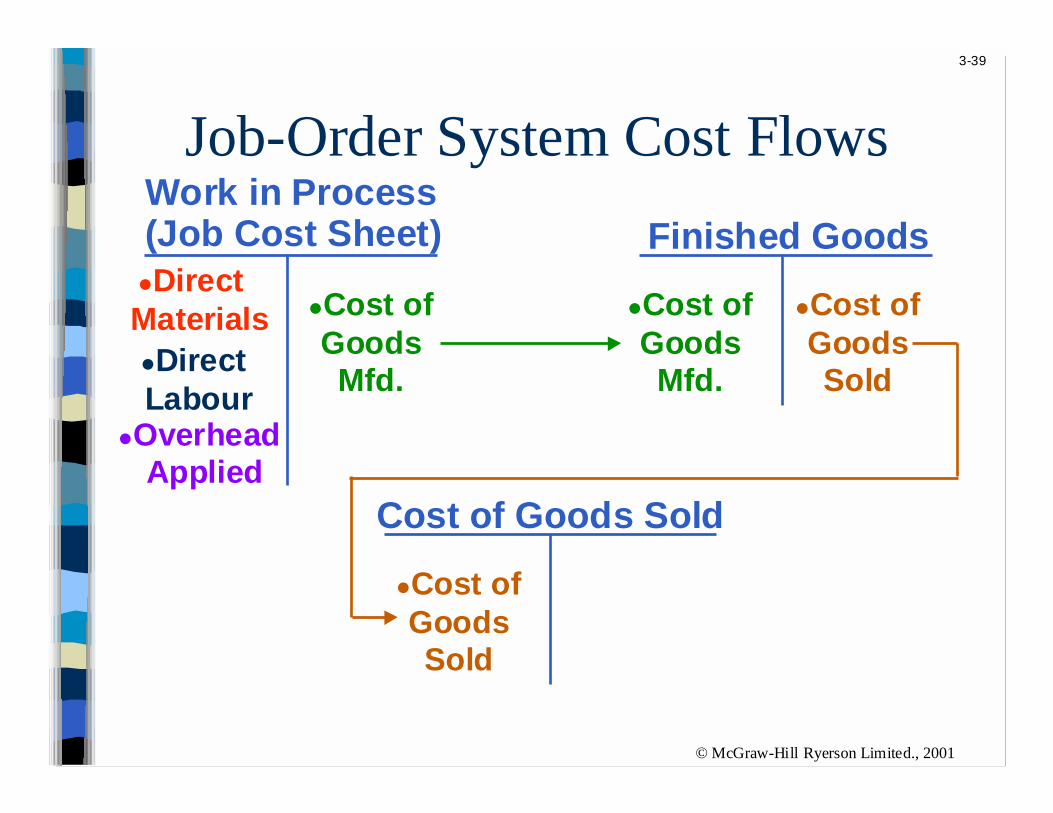

3-39

"Cost ofGoodsMfd.

Finished Goods

"Cost ofGoodsSold

"Cost ofGoodsMfd.

Cost of Goods Sold

"Cost ofGoodsSold

Job-Order System Cost FlowsWork in Process(Job Cost Sheet)"Direct

Materials"Direct Labour

"Overhead Applied

© McGraw-Hill Ryerson Limited., 2001

3-40

Let’s return toPearCo and see

what we will do ifactual and

applied overheadare not equal.

Job-Order System Cost Flows

© McGraw-Hill Ryerson Limited., 2001

3-41

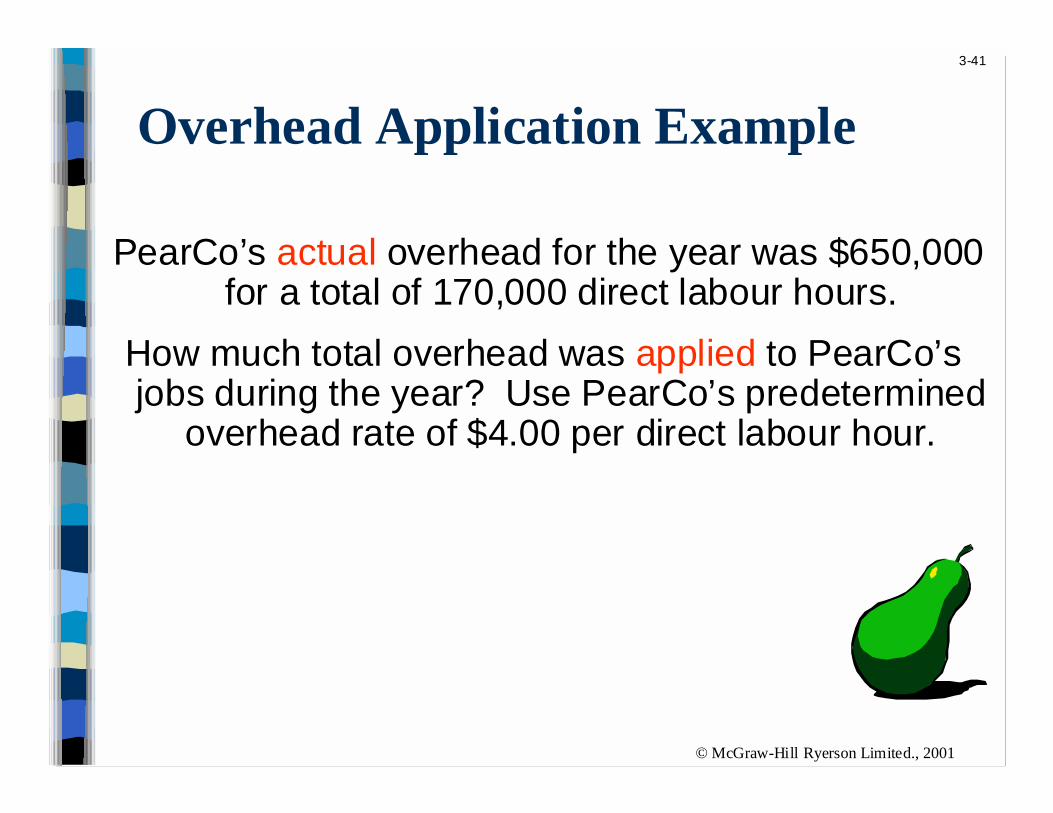

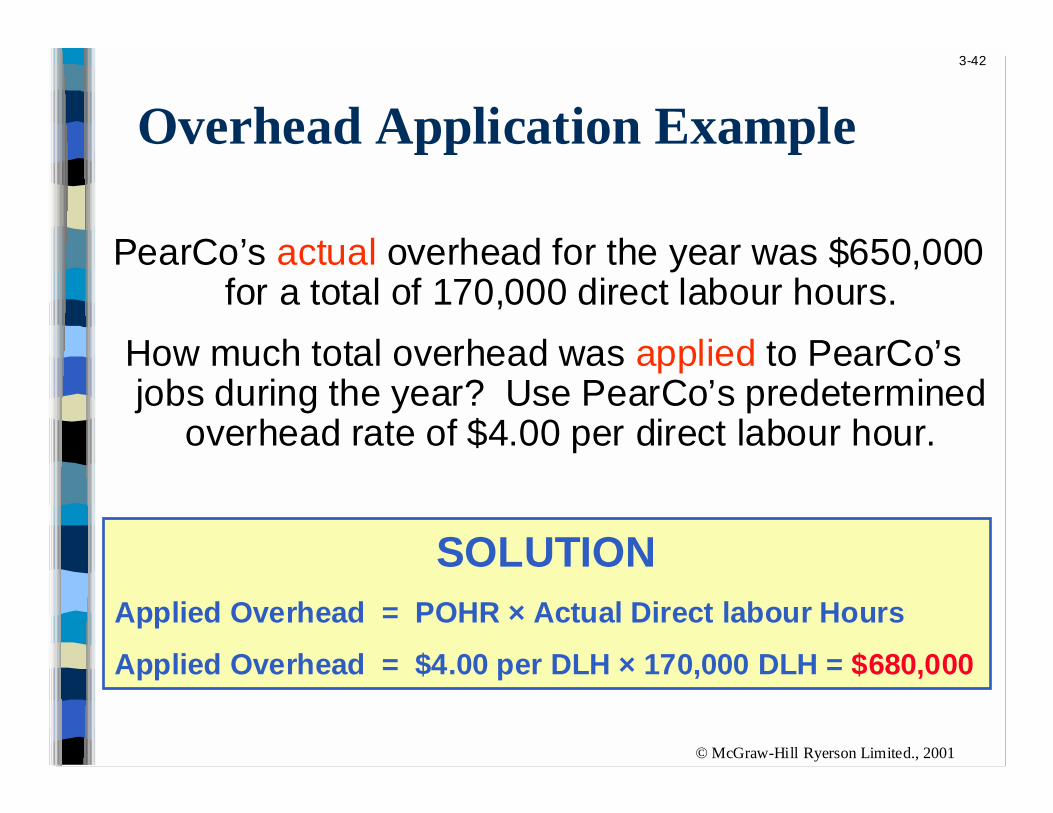

Overhead Application Example

PearCo’s actual overhead for the year was $650,000for a total of 170,000 direct labour hours.

How much total overhead was applied to PearCo’sjobs during the year? Use PearCo’s predetermined

overhead rate of $4.00 per direct labour hour.

© McGraw-Hill Ryerson Limited., 2001

3-42

Overhead Application Example

SOLUTIONApplied Overhead = POHR × Actual Direct labour Hours

Applied Overhead = $4.00 per DLH × 170,000 DLH = $680,000

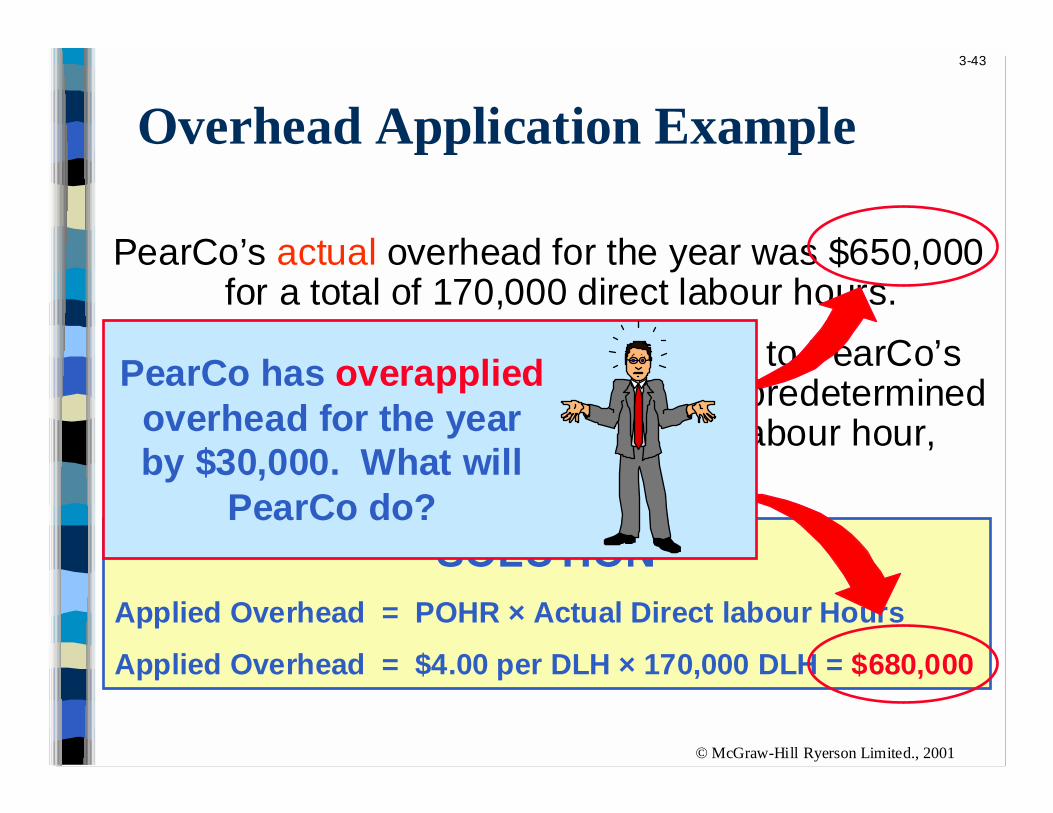

PearCo’s actual overhead for the year was $650,000for a total of 170,000 direct labour hours.

How much total overhead was applied to PearCo’sjobs during the year? Use PearCo’s predetermined

overhead rate of $4.00 per direct labour hour.

© McGraw-Hill Ryerson Limited., 2001

3-43

SOLUTIONApplied Overhead = POHR × Actual Direct labour Hours

Applied Overhead = $4.00 per DLH × 170,000 DLH = $680,000

PearCo’s actual overhead for the year was $650,000for a total of 170,000 direct labour hours.

How much total overhead was applied to PearCo’sjobs during the year? Use PearCo’s predetermined

overhead rate of $4.00 per direct labour hour,

Overhead Application Example

PearCo has overappliedoverhead for the yearby $30,000. What will

PearCo do?

© McGraw-Hill Ryerson Limited., 2001

3-44

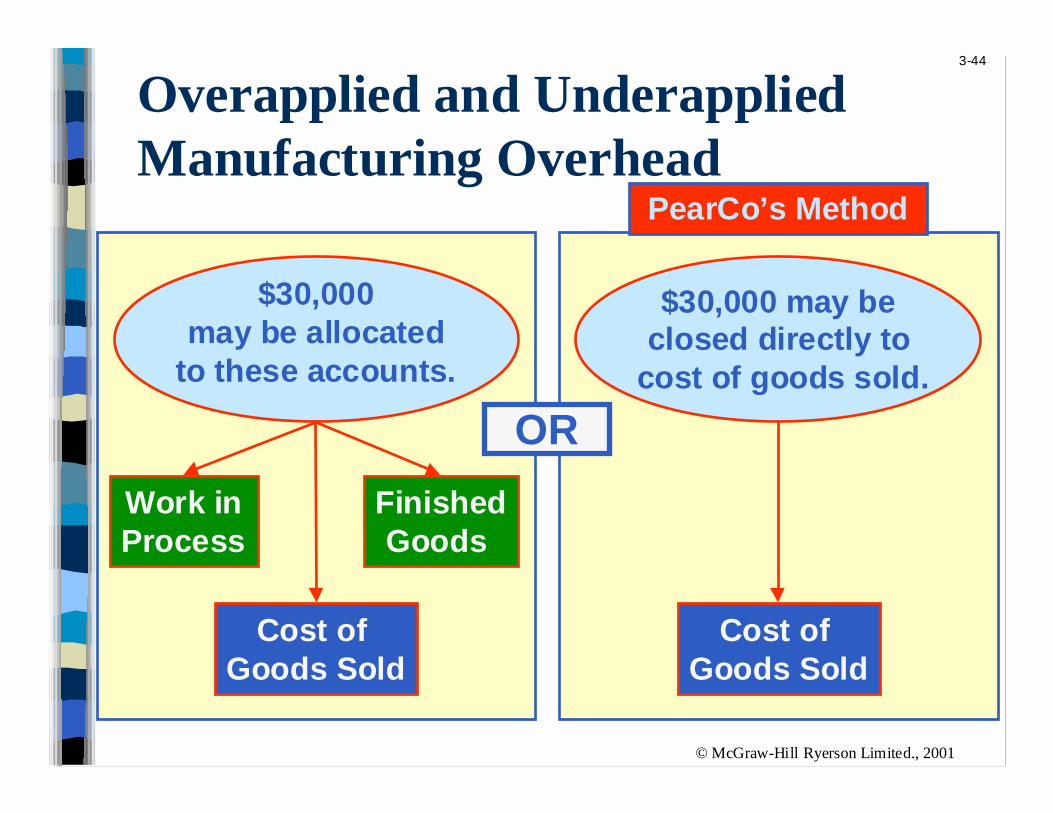

Work inProcess

FinishedGoods

Cost of Goods Sold

$30,000may be allocated

to these accounts.

$30,000 may beclosed directly to

cost of goods sold.

Cost of Goods Sold

Overapplied and UnderappliedManufacturing Overhead

PearCo’s Method

OR

© McGraw-Hill Ryerson Limited., 2001

3-45

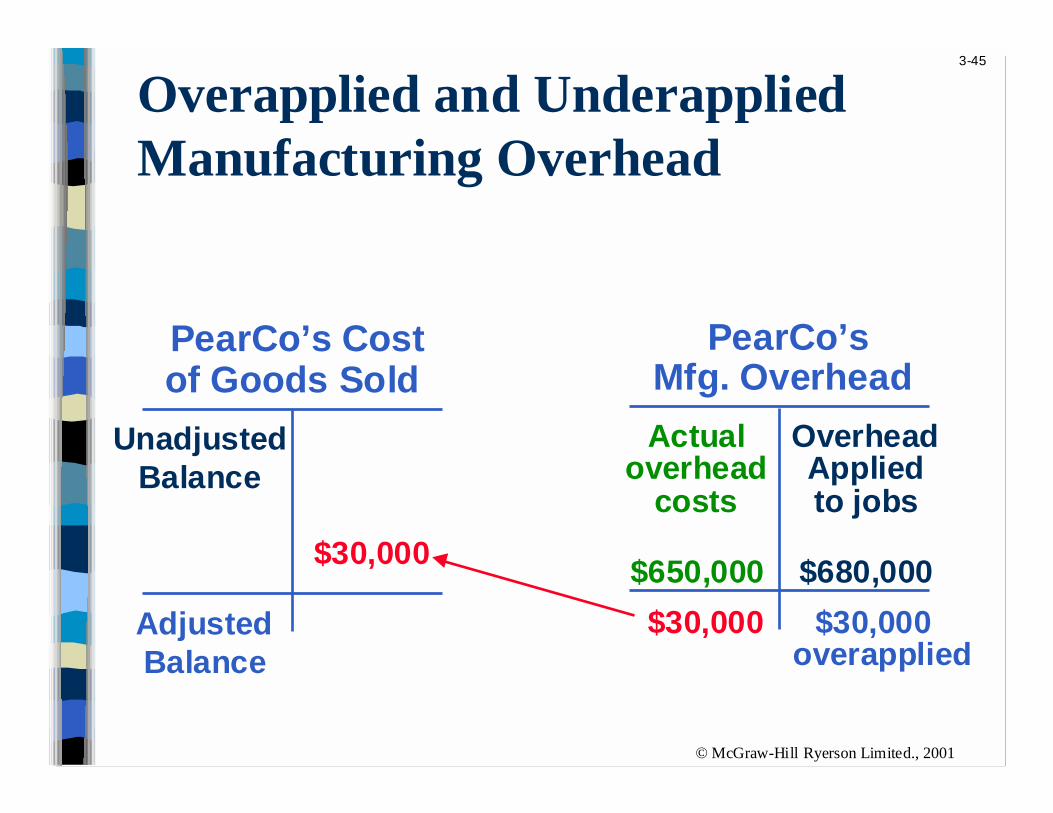

Overapplied and UnderappliedManufacturing Overhead

PearCo’sMfg. Overhead

Actualoverhead

costs

$650,000

$30,000 overapplied

PearCo’s Costof Goods Sold

UnadjustedBalance

$30,000

$30,000

AdjustedBalance

OverheadAppliedto jobs

$680,000

© McGraw-Hill Ryerson Limited., 2001

3-46

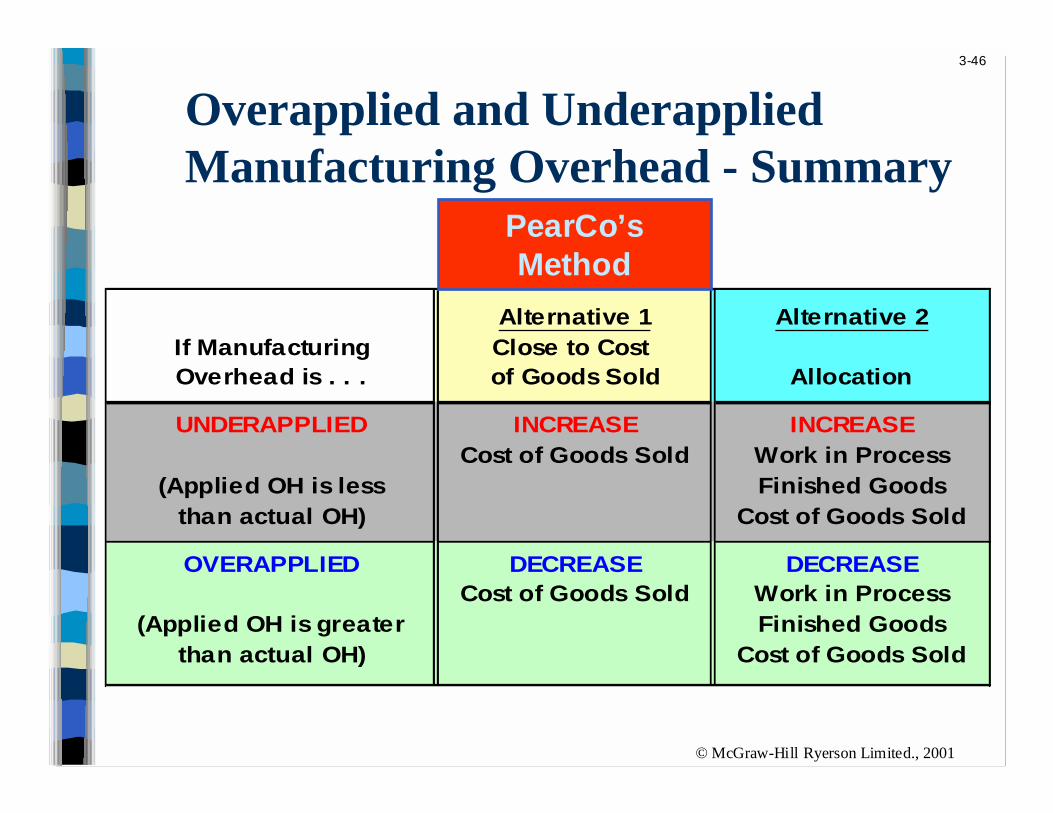

Overapplied and UnderappliedManufacturing Overhead - Summary

Alternative 1 Alternative 2If Manufacturing Close to Cost Overhead is . . . of Goods Sold Allocation

UNDERAPPLIED INCREASE INCREASECost of Goods Sold Work in Process

(Applied OH is less Finished Goodsthan actual OH) Cost of Goods Sold

OVERAPPLIED DECREASE DECREASECost of Goods Sold Work in Process

(Applied OH is greater Finished Goodsthan actual OH) Cost of Goods Sold

PearCo’sMethod

© McGraw-Hill Ryerson Limited., 2001

3-47

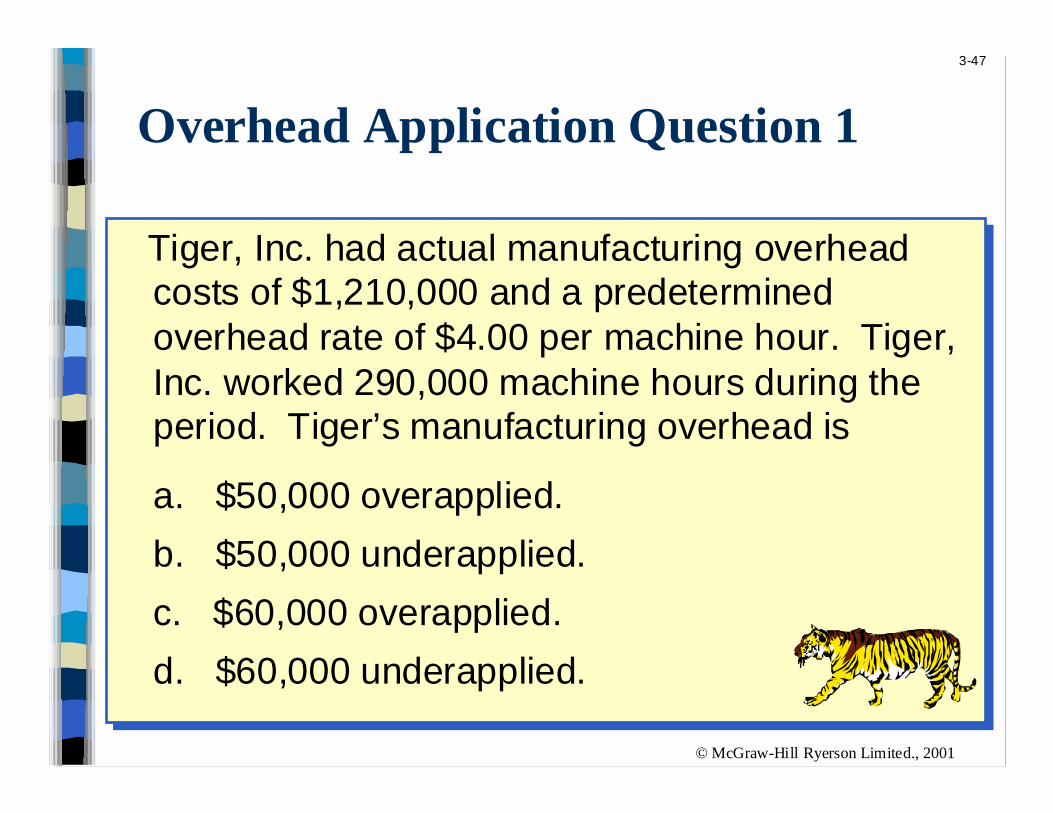

Tiger, Inc. had actual manufacturing overheadcosts of $1,210,000 and a predeterminedoverhead rate of $4.00 per machine hour. Tiger,Inc. worked 290,000 machine hours during theperiod. Tiger’s manufacturing overhead is

a. $50,000 overapplied.

b. $50,000 underapplied.

c. $60,000 overapplied.

d. $60,000 underapplied.

Tiger, Inc. had actual manufacturing overheadcosts of $1,210,000 and a predeterminedoverhead rate of $4.00 per machine hour. Tiger,Inc. worked 290,000 machine hours during theperiod. Tiger’s manufacturing overhead is

a. $50,000 overapplied.

b. $50,000 underapplied.

c. $60,000 overapplied.

d. $60,000 underapplied.

Overhead Application Question 1

© McGraw-Hill Ryerson Limited., 2001

3-48

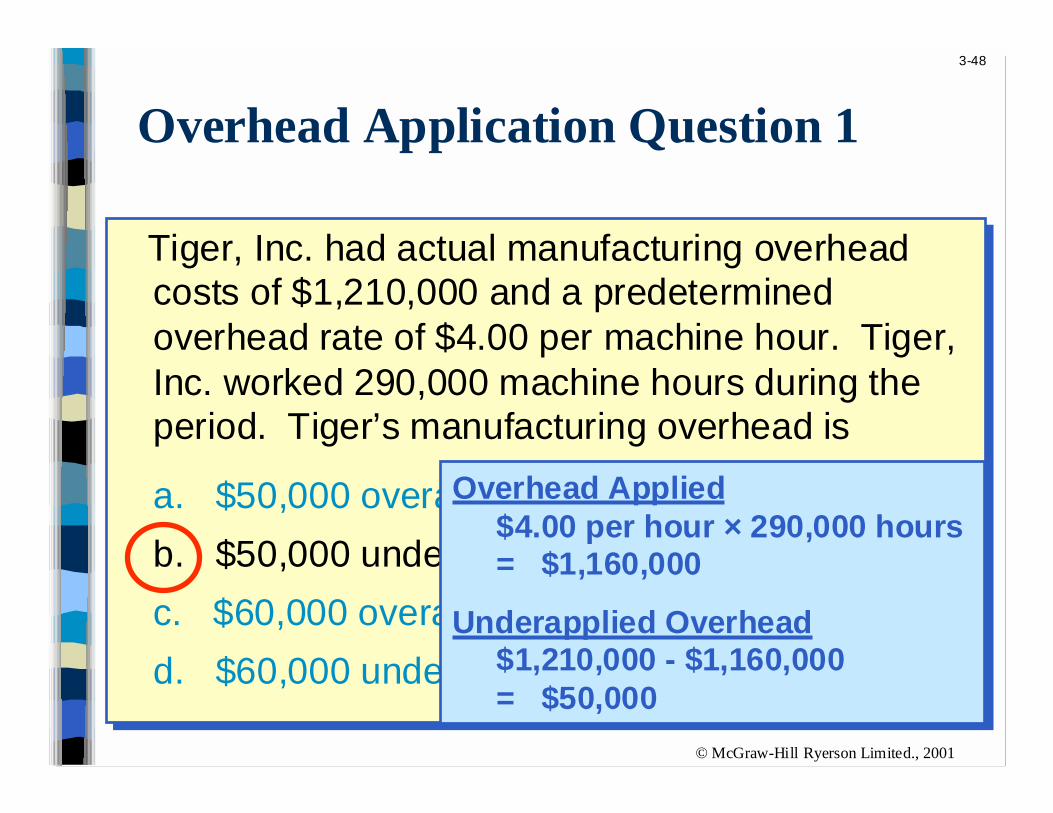

Tiger, Inc. had actual manufacturing overheadcosts of $1,210,000 and a predeterminedoverhead rate of $4.00 per machine hour. Tiger,Inc. worked 290,000 machine hours during theperiod. Tiger’s manufacturing overhead is

a. $50,000 overapplied.

b. $50,000 underapplied.

c. $60,000 overapplied.

d. $60,000 underapplied.

Tiger, Inc. had actual manufacturing overheadcosts of $1,210,000 and a predeterminedoverhead rate of $4.00 per machine hour. Tiger,Inc. worked 290,000 machine hours during theperiod. Tiger’s manufacturing overhead is

a. $50,000 overapplied.

b. $50,000 underapplied.

c. $60,000 overapplied.

d. $60,000 underapplied.

Overhead Application Question 1

Overhead Applied $4.00 per hour × 290,000 hours = $1,160,000

Underapplied Overhead $1,210,000 - $1,160,000 = $50,000

© McGraw-Hill Ryerson Limited., 2001

3-49

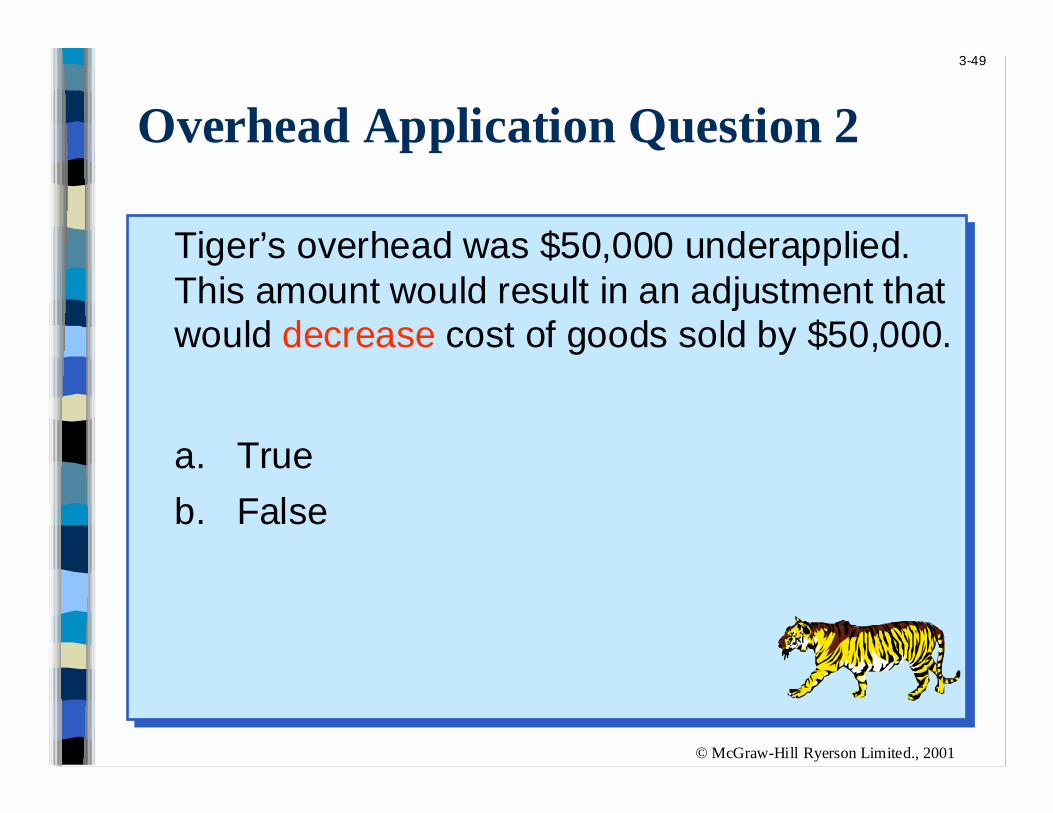

Tiger’s overhead was $50,000 underapplied.This amount would result in an adjustment thatwould decrease cost of goods sold by $50,000.

a. True

b. False

Tiger’s overhead was $50,000 underapplied.This amount would result in an adjustment thatwould decrease cost of goods sold by $50,000.

a. True

b. False

Overhead Application Question 2

© McGraw-Hill Ryerson Limited., 2001

3-50

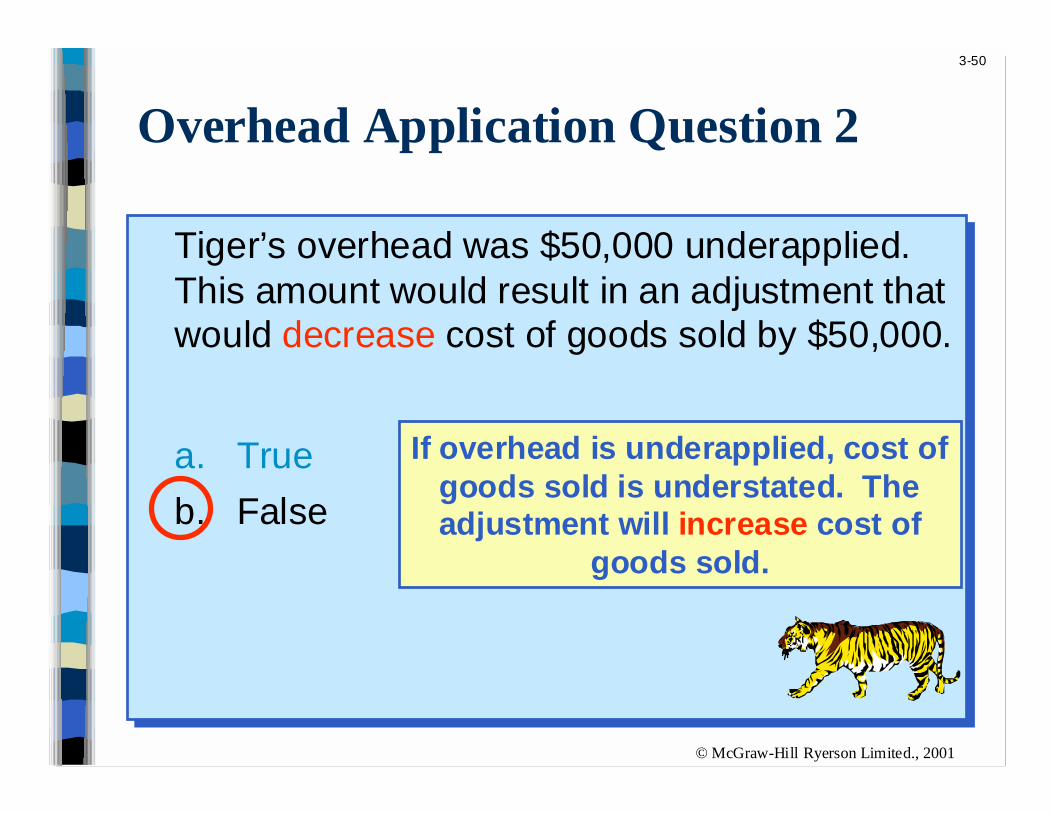

Tiger’s overhead was $50,000 underapplied.This amount would result in an adjustment thatwould decrease cost of goods sold by $50,000.

a. True

b. False

Tiger’s overhead was $50,000 underapplied.This amount would result in an adjustment thatwould decrease cost of goods sold by $50,000.

a. True

b. False

If overhead is underapplied, cost ofgoods sold is understated. Theadjustment will increase cost of

goods sold.

Overhead Application Question 2

© McGraw-Hill Ryerson Limited., 2001

3-51

Let’s look atsummary journalentries for a job-

order costingsystem. We’ll omit

the numbers so that we can focus

on accounts.

Job-Order Costing – TypicalAccounting Entries

© McGraw-Hill Ryerson Limited., 2001

3-52

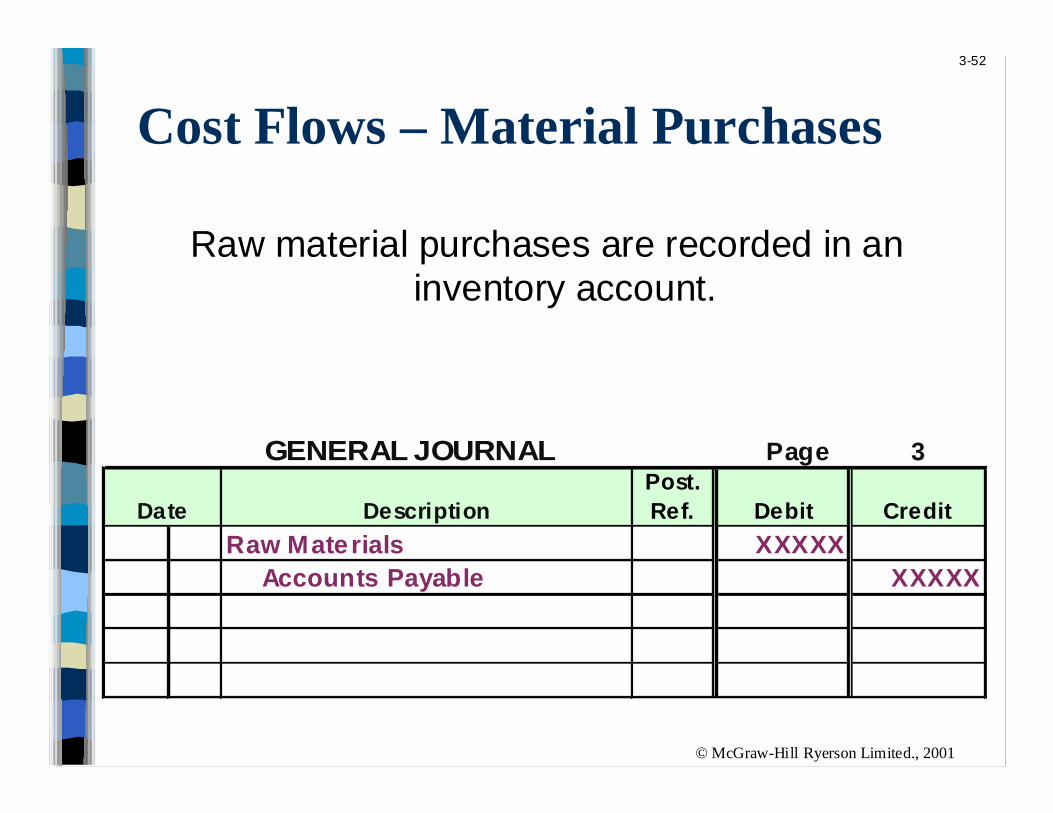

Cost Flows – Material Purchases

Raw material purchases are recorded in aninventory account.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Raw Materials XXXXX Accounts Payable XXXXX

© McGraw-Hill Ryerson Limited., 2001

3-53

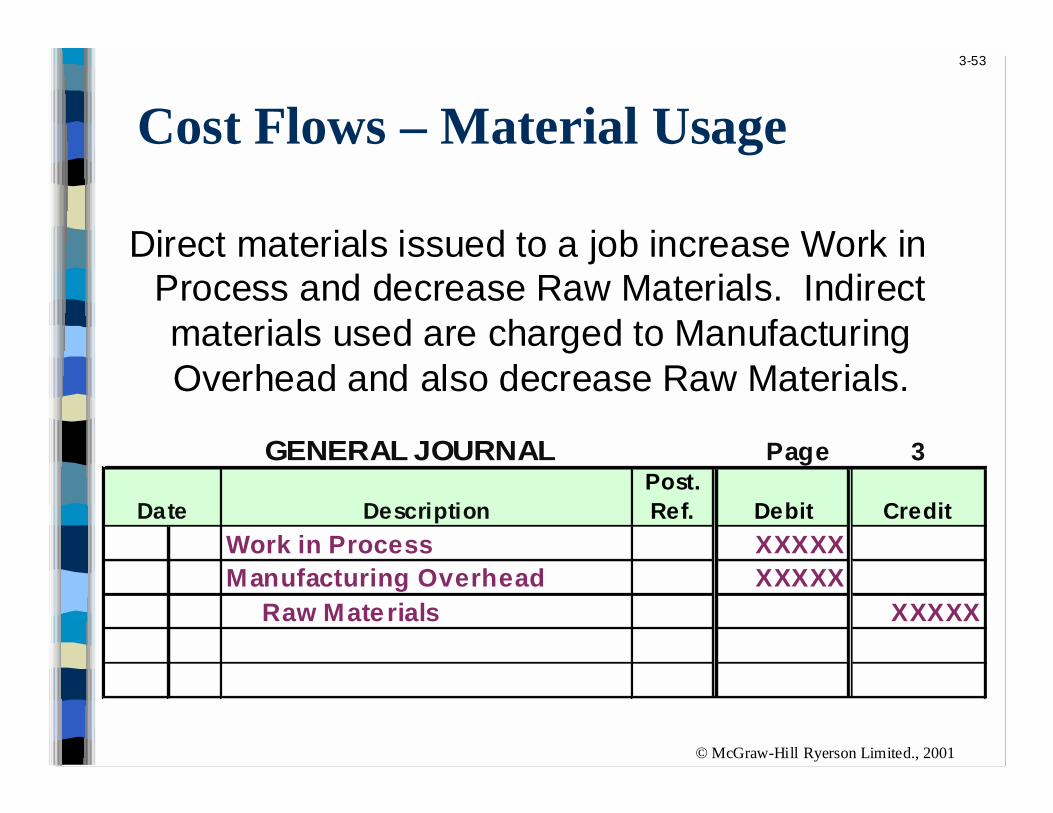

Direct materials issued to a job increase Work inProcess and decrease Raw Materials. Indirectmaterials used are charged to ManufacturingOverhead and also decrease Raw Materials.

Cost Flows – Material Usage

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work in Process XXXXXManufacturing Overhead XXXXX Raw Materials XXXXX

© McGraw-Hill Ryerson Limited., 2001

3-54

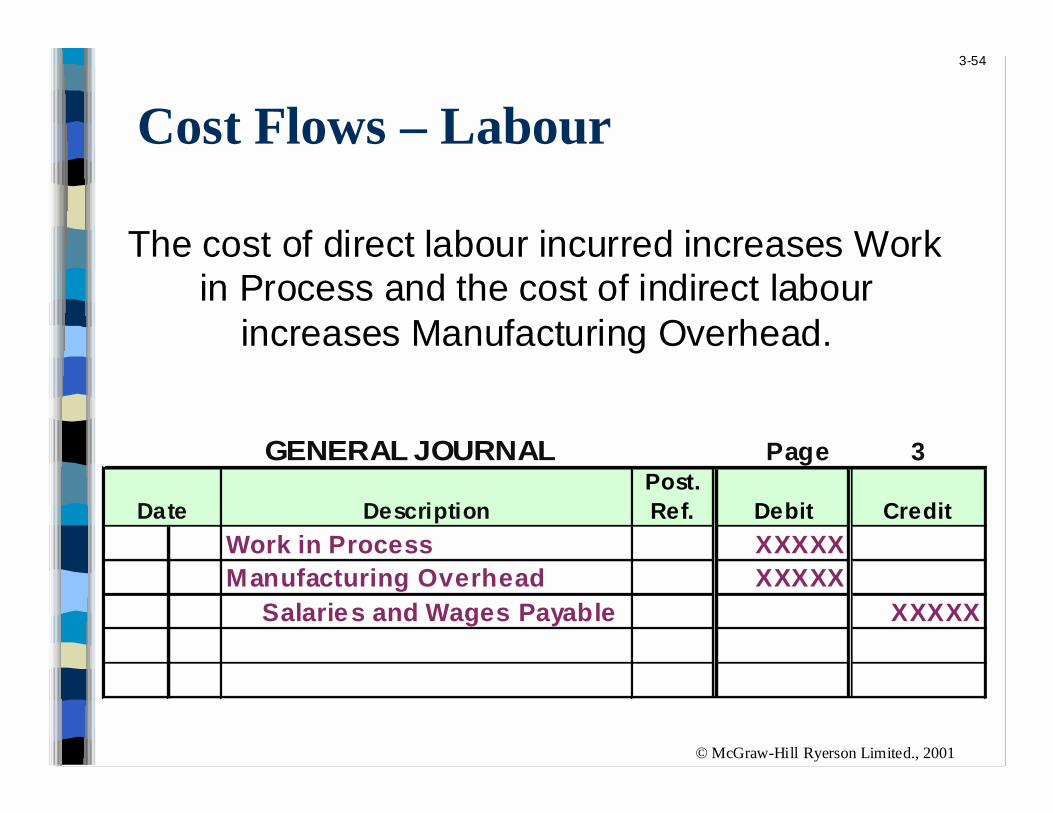

Cost Flows – Labour

The cost of direct labour incurred increases Workin Process and the cost of indirect labour

increases Manufacturing Overhead.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work in Process XXXXXManufacturing Overhead XXXXX Salaries and Wages Payable XXXXX

© McGraw-Hill Ryerson Limited., 2001

3-55

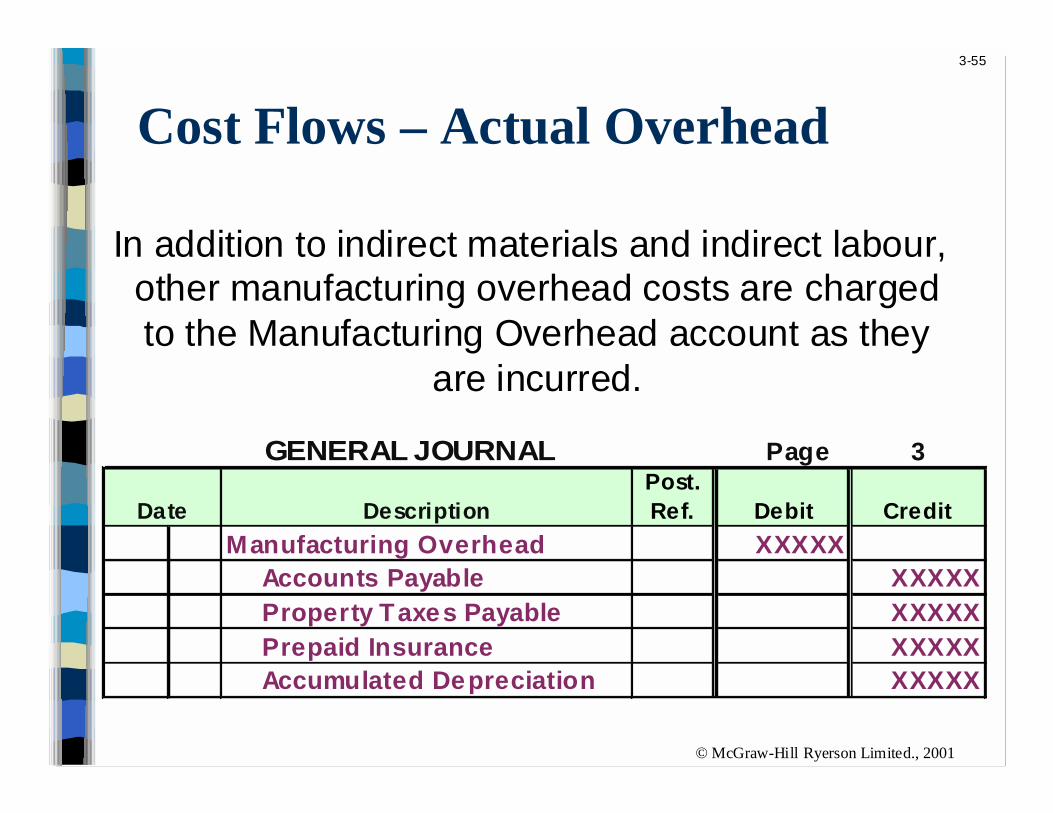

Cost Flows – Actual Overhead

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Manufacturing Overhead XXXXX Accounts Payable XXXXX Property Taxes Payable XXXXX Prepaid Insurance XXXXX Accumulated Depreciation XXXXX

In addition to indirect materials and indirect labour,other manufacturing overhead costs are chargedto the Manufacturing Overhead account as they

are incurred.

© McGraw-Hill Ryerson Limited., 2001

3-56

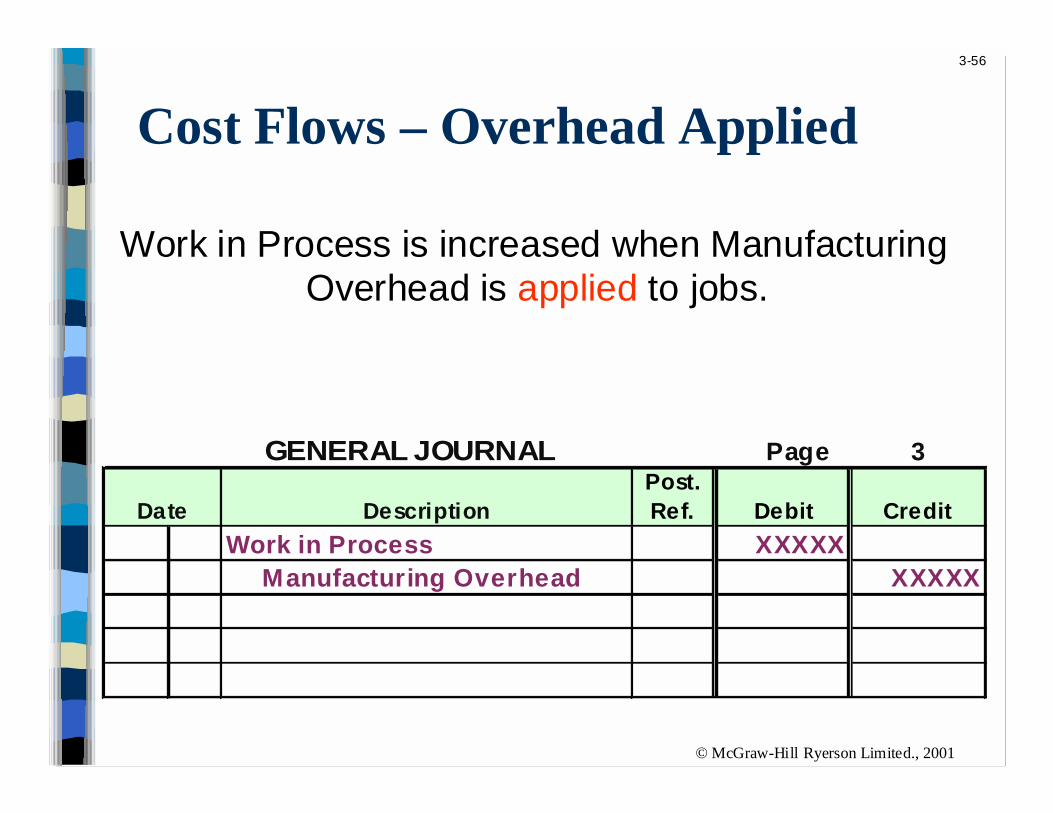

Cost Flows – Overhead Applied

Work in Process is increased when ManufacturingOverhead is applied to jobs.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Work in Process XXXXX Manufacturing Overhead XXXXX

© McGraw-Hill Ryerson Limited., 2001

3-57

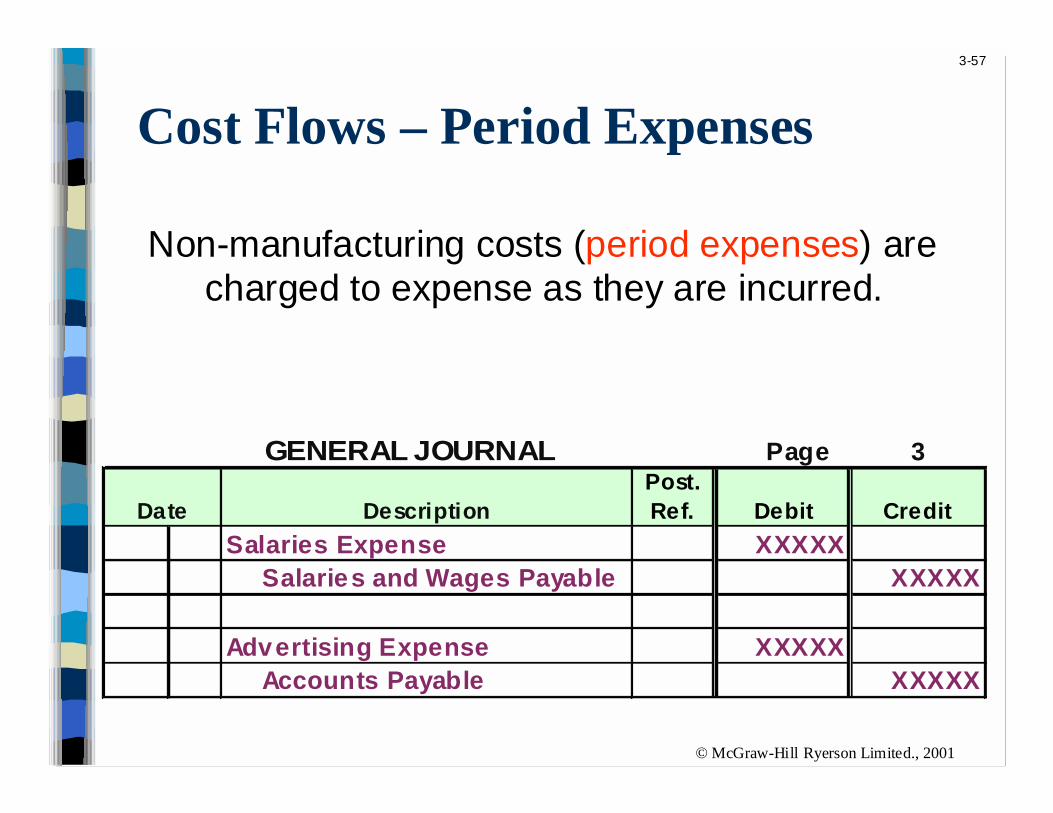

Cost Flows – Period Expenses

Non-manufacturing costs (period expenses) arecharged to expense as they are incurred.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Salaries Expense XXXXX Salaries and Wages Payable XXXXX

Advertising Expense XXXXX Accounts Payable XXXXX

© McGraw-Hill Ryerson Limited., 2001

3-58

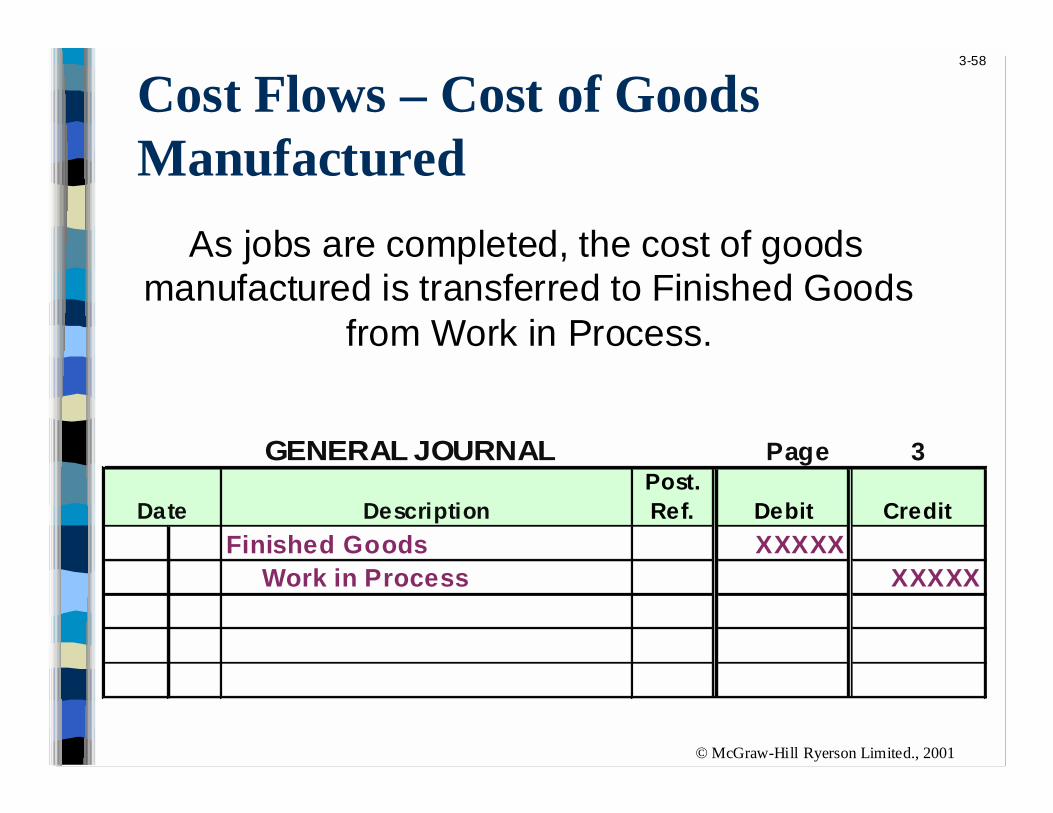

Cost Flows – Cost of GoodsManufactured

As jobs are completed, the cost of goodsmanufactured is transferred to Finished Goods

from Work in Process.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Finished Goods XXXXX Work in Process XXXXX

© McGraw-Hill Ryerson Limited., 2001

3-59

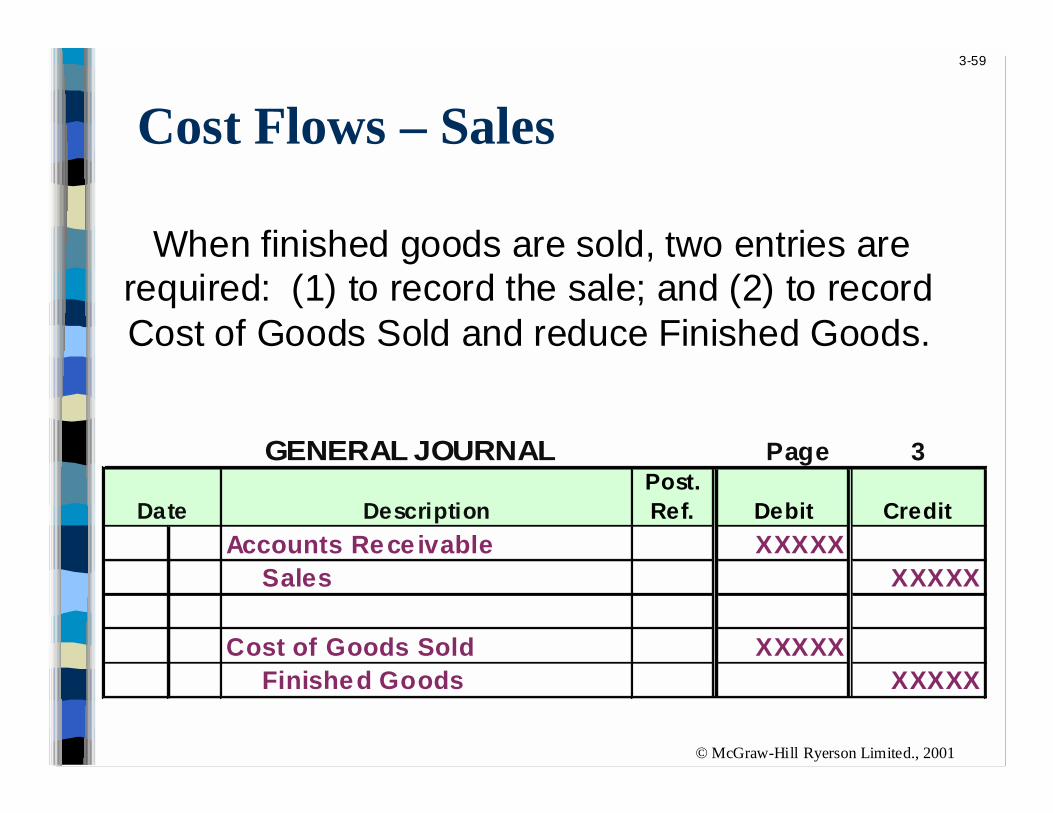

Cost Flows – Sales

When finished goods are sold, two entries arerequired: (1) to record the sale; and (2) to recordCost of Goods Sold and reduce Finished Goods.

GENERAL JOURNAL Page 3

Date DescriptionPost. Ref. Debit Credit

Accounts Rece ivable XXXXX Sales XXXXX

Cost of Goods Sold XXXXX Finished Goods XXXXX

The PredeterminedOverhead Rate and

Capacity

Appendix

3A

© McGraw-Hill Ryerson Limited., 2001

3-61

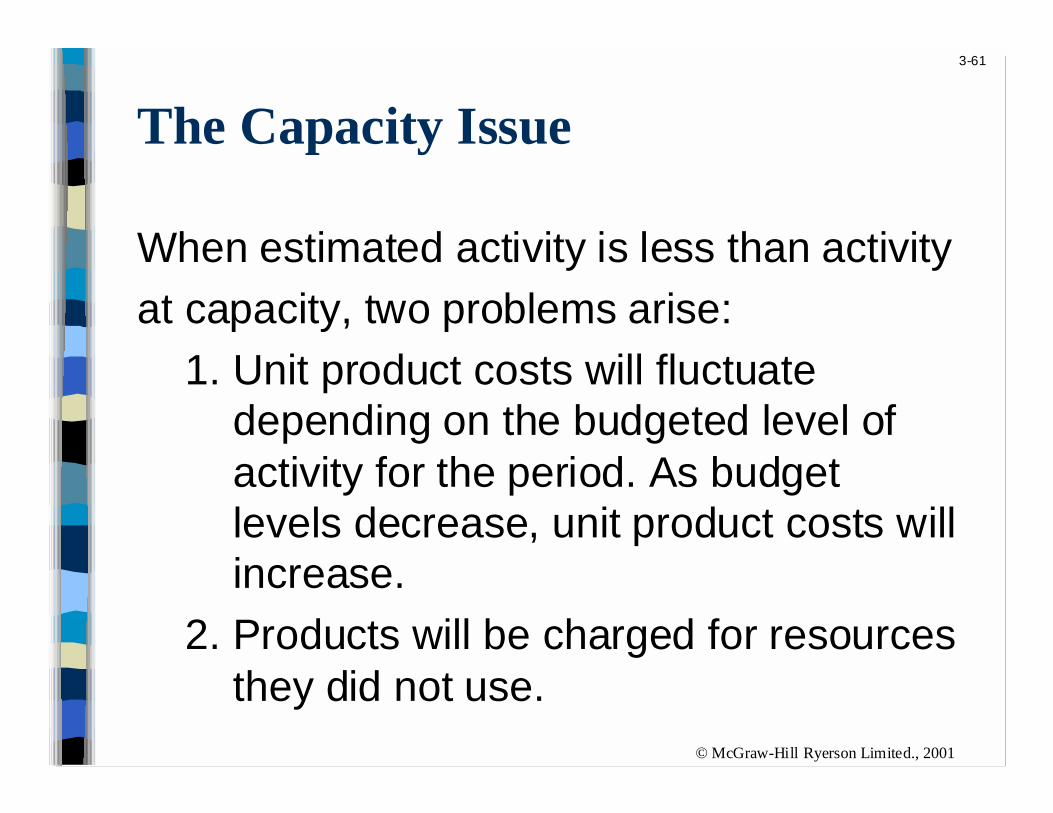

The Capacity Issue

When estimated activity is less than activity

at capacity, two problems arise:

1. Unit product costs will fluctuate depending on the budgeted level ofactivity for the period. As budget levels decrease, unit product costs willincrease.

2. Products will be charged for resourcesthey did not use.

Cost Flows in aJIT System

Appendix

3B

© McGraw-Hill Ryerson Limited., 2001

3-63

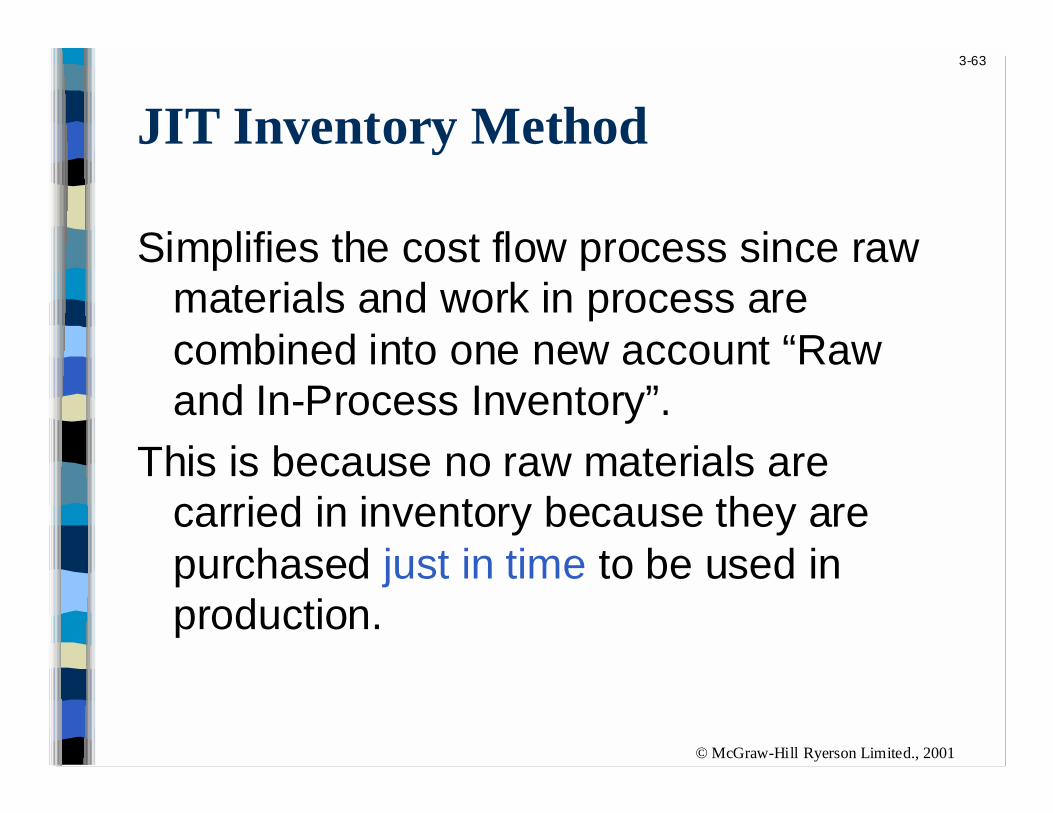

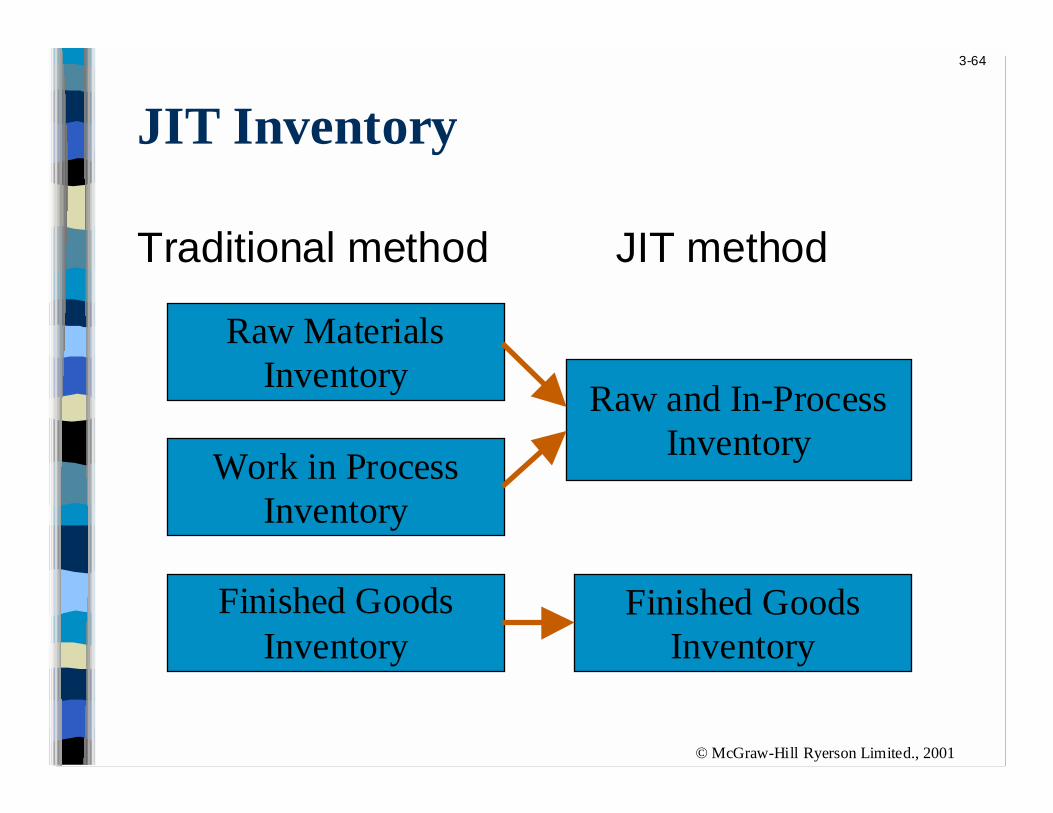

JIT Inventory Method

Simplifies the cost flow process since rawmaterials and work in process arecombined into one new account “Rawand In-Process Inventory”.

This is because no raw materials arecarried in inventory because they arepurchased just in time to be used inproduction.

© McGraw-Hill Ryerson Limited., 2001

3-64

JIT Inventory

Traditional method JIT method

Raw MaterialsInventory

Work in ProcessInventory

Finished GoodsInventory

Raw and In-ProcessInventory

Finished GoodsInventory

Scrap and Rework

Appendix

3C

© McGraw-Hill Ryerson Limited., 2001

3-66

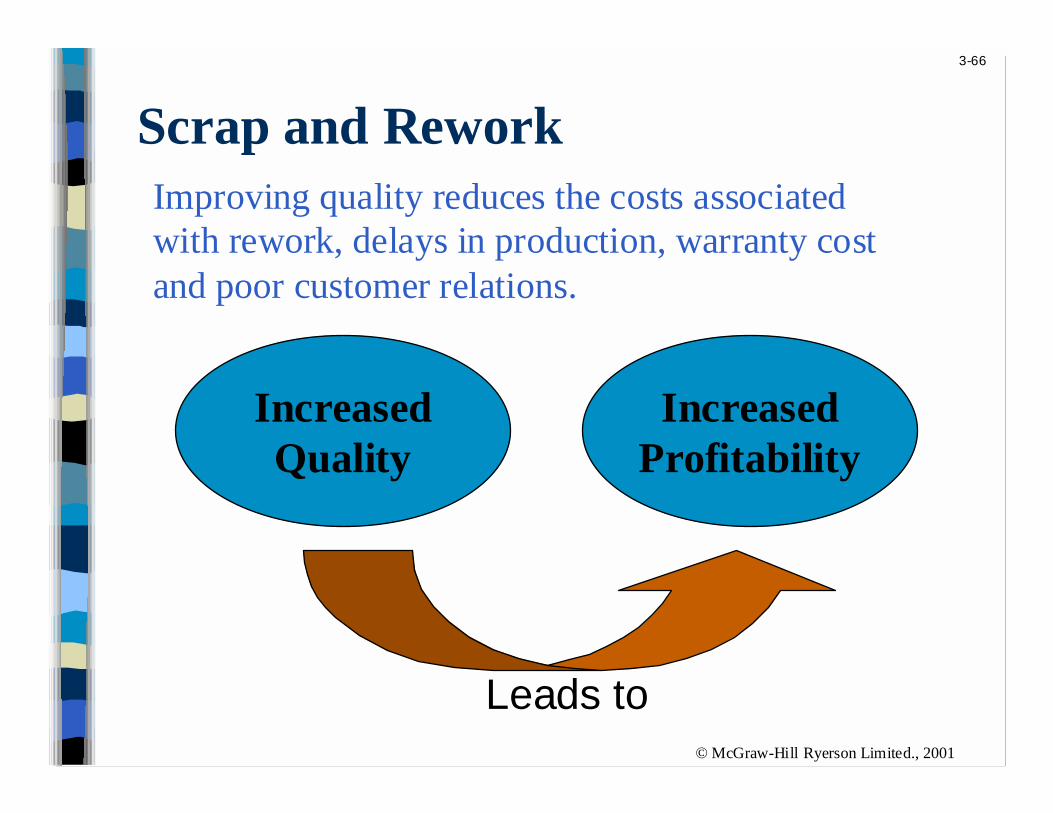

Scrap and Rework

IncreasedQuality

IncreasedProfitability

Leads to

Improving quality reduces the costs associatedwith rework, delays in production, warranty costand poor customer relations.

© McGraw-Hill Ryerson Limited., 2001

3-67

No Recovery

Where there is no recovery from scrapunits, the total loss from scrap can be:

1. Allocated across all good units, or

2. Charged to overhead and in turn charged to all jobs.

© McGraw-Hill Ryerson Limited., 2001

3-68

With Recovery

1. When items are sold for scrap, the scraprecovery could be credited to:

(a) the job, or

(b) manufacturing overhead.

2. When some rework is undertaken, thematerials and labour involved in the reworkcould be charged to:

(a) the job, or

(b) manufacturing overhead and spread over all the jobs.

© McGraw-Hill Ryerson Limited., 2001

3-69

End of Chapter 3

Related Documents