www.tjprc.org [email protected] International Journal of Accounting and Financial Management Research (IJAFMR) ISSN(P): 2249-6882; ISSN(E): 2249-7994 Vol. 4, Issue 4, Aug 2014, 13-24 © TJPRC Pvt. Ltd. STATUS OF MICROFINANCE AND ITS DELIVERY MODELS IN INDIA S. L GUPTA 1 & SHAHID AKHTER ANSARI 2 1 Director, Birla Institute of Technology, Mesra, Patna Campus, Patna, Po-Bihar Veterinary College, Patna, Bihar, India 2 Research Scholar, Department of Management, Patna, Bihar, India ABSTRACT Microfinance has developed as dignified substitute for informal credit and acts as a powerful tool for poverty alleviation. Microfinance offers loans, deposit and insurance to poorest strata of society and low income households. Microfinance institutions and self help groups had contributed significantly towards the improvement of income level of poor people and their standard of living. There are different models of microfinance to serve the poor people like Grameen Bank model, Self Help Group bank linkage programme model, Microfinance Institution model, Bank correspondent model, and Bank partnership model. At present, self help group Bank Linkage programme model and the Micro Finance Institution model for delivery of Microfinance in India is working on large scale as compare to other models. Self help group Bank Linkage programme model is recognized as largest Micro finance programme all over the world in term of coverage. This paper attempts to focus on status of Microfinance and its delivery model prevailing in India. KEYWORDS: SHGs, MFI, SBLP, GB, BCs INTRODUCTION Microfinance is financial services for under-privileged section of the society who do not have an access to formal banking system to build assets, diversify livelihood options, increase income and reduce their vulnerability to economic stress. Microfinance offers board Range of financial services as loan, saving and insurance to poor people through different microfinance Institutions. Microfinance institutions also provide social intermediation services such as training and education, organizational support, health and skills in line with their development objectives. Microfinance cannot eradicate all problems caused by poverty but it can assist to put economic resources into hands of poor and low income people enabling them to make their own financial decision thereby improving their financial soundness. Reserve Bank of India defines Micro Finance Institutions as a non deposit taking non banking financial companies (other than a company licensed under section 25 of Indian company act 1956) that fulfills the following conditions 1 : Minimum net owned fund of Rs 5 crore (For MFIs registered in the north eastern region of the country, the minimum NOF requirement shall stand at Rs. 2crore). Not less than 85% of its net assets are in the nature of “qualifying asset” Qualifying assets shall mean a loan which satisfies the following criteria 1 http://rbidocs.rbi.org.in/r docs/Publications/PDFs/88

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.tjprc.org [email protected]

International Journal of Accounting and Financial Management Research (IJAFMR) ISSN(P): 2249-6882; ISSN(E): 2249-7994 Vol. 4, Issue 4, Aug 2014, 13-24

© TJPRC Pvt. Ltd.

STATUS OF MICROFINANCE AND ITS DELIVERY MODELS IN INDIA

S. L GUPTA1 & SHAHID AKHTER ANSARI

2

1Director, Birla Institute of Technology, Mesra, Patna Campus, Patna, Po-Bihar Veterinary College, Patna, Bihar, India

2Research Scholar, Department of Management, Patna, Bihar, India

ABSTRACT

Microfinance has developed as dignified substitute for informal credit and acts as a powerful tool for poverty

alleviation. Microfinance offers loans, deposit and insurance to poorest strata of society and low income house holds.

Microfinance institutions and self help groups had contributed significantly t owards the improvement of income level of

poor people and their standard of living. There are different models of microfinance to serve the poor people like Grameen

Bank model, Self Help Group bank linkage programme model, Microfinance Institution model, Bank correspondent

model, and Bank partnership model. At present, self help group Bank Linkage programme model and the Micro Finance

Institution model for delivery of Microfinance in India is working on large scale as compare to other models . Self help

group Bank Linkage programme model is recognized as largest Micro finance programme all over the world in term of

coverage. This paper attempts to focus on status of Microfinance and its delivery model prevailing in India.

KEYWORDS: SHGs, MFI, SBLP, GB, BCs

INTRODUCTION

Microfinance is financial services for under-privileged section of the society who do not have an access to formal

banking system to build assets, diversify livelihood options, increase income and reduce their vulnerability to economic

stress. Microfinance offers board Range of financial services as loan, saving and insurance to poor people through different

microfinance Institutions. Microfinance institutions also provide social intermediation services such as training and

education, organizational support, health and skills in line with their development objectives. Microfinance cannot

eradicate all problems caused by poverty but it can assist to put economic resources into hands of poor and low income

people enabling them to make their own financial decision thereby improving their financial soundness.

Reserve Bank of India defines Micro Finance Institutions as a non deposit taking non banking financial

companies (other than a company licensed under section 25 of Indian company act 1956) that fulfills the following

conditions1:

Minimum net owned fund of Rs 5 crore (For MFIs registered in the north eastern region of the country,

the minimum NOF requirement shall stand at Rs. 2crore).

Not less than 85% of its net assets are in the nature of “qualifying asset”

Qualifying assets shall mean a loan which satisfies the following criteria

1http://rbidocs.rbi.org.in/r docs/Publications/PDFs/88

14 S. L Gupta & Shahid Akhter Ansari

Impact Factor (JCC): 4.4251 Index Copernicus Value (ICV): 3.0

Loan disbursed by a MFI to borrower with a rural household annual income not exceeding Rs 60,000 or urban and

semi urban household income not exceeding Rs 1,20000.

Loan amount does not exceed Rs 35000 in the first cycle and Rs 50000 in subsequent cycles;

Total indebtedness of the borrower does not exceed Rs.50000;

Tenure of the loan not to be less than 24 months for loan amount in excess of Rs 15000 with repayment without

penalty;

Loan to be extended without collateral.

EVOLUTION OF MICROFINANCE IN INDIA

Micro finance emerged as an industry almost same time all over the world. Microfinance is broadly accepted for

improving income level of poor people. In 1970s and 1980s non government organisations provided micro credits to poor

for opening micro enterprises. In 1970s since the effort of Mohammad Yunus founder of Grameen Bank, Microfinance has

proved to be a sustainable tool for poverty alleviation.

In 2006 Mohammad Yunus was awarded noble peace prize for his effort towards the economic as well as social

development of poor people in Bangladesh. Microfinance industry in India can be traced back to mid of 1970s when

NGO‟s like PRADAN and MYRADA started promoting self help group model as a social development tool for

development of low income people.

The previous models of lending to low income people were state sponsored programmes like integrated rural

development programme (IRDP) which were designed for social welfare of the state. In 1990s Grameen bank model and

the Association for social Advancement model found rapid acceptance in Bangladesh as well as in India as a new breed for

microfinance Institutions. Popularly known as the On-lending models they had the capacity for rapid up-scaling in terms of

client reach.

They were less reliant on donation of funds. It enabled the microfinance institutions to borrow capital from large

organisations and charging individual borrower a minimum amount as a service charge and retained margin for their own

growth. The SHG model in the form of the SHG-Bank Linkage (SBLP) initiated in the 1992 by NABARD and the rapidly

growing MFI on-lending model both dominate the microfinance industry.

Apex bodies like National Agriculture and Rural Development Bank (NABARD) and Small Industries

Development Bank of India (SIDBI) are playing vital role for providing financial resources to microfinance these days.

The main vigor of microfinance in India is variety of microfinance delivery models which emerged over a period of time.

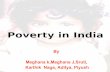

RURAL AND URBAN POVERTY IN INDIA

Poverty eradication is a major task of the Government of India, though the ministry of rural development has

implemented a number of poverty reduction programs to bring rapid growth of economy. These programmes have reduced

poverty to considerable extent the table 1 highlights the Percentage number of poor estimated by Tendulkar method using

mixed reference period

2http://planningcommission.nic.in/news/pre_pov2307.pdf

Status of Microfinance and its Delivery Models in India 15

www.tjprc.org [email protected]

Table 1

Year Poverty Ratio % Number of Poor (In million)

Rural Urban Total Rural Urban Total

1993-94 50.1 31.8 45.3 328.2 74.5 403.7

2004-05 41.8 25.7 37.2 326.3 80.8 407.1

2011-12 25.7 13.7 21.9 216.5 52.8 269.3

(Source: Government of India Planning Commission press report, 20132)

Poverty Ratio%

Figure 1

Poverty in India has been a part of the policy right from the first plan period with the primary focus begins on

agriculture and rural development. Urban development was tackled though a focus on industry . While social services such

as health and education provided for the urban population remained a concentrated focus on rural Indian in five year plans.

Urban poverty was not recognized as a concern for initial plan periods. The change towards the urban focus had seen from

the seventh plan periods onwards with attention of infrastructure environment improvements (slum upgrading) and

livelihood promotions. Subsequent plan have steadily increased the allocation for urban development . Most significant is

the recent emphasis on urban renewal evidence though the allocation under JNNURM (Jawaharlal Nehru National Urban

Renewal Mission) in the 10th

Five year Plan which has continue since then. JNNURM is the first attempt at a

comprehensive package for development and poverty alleviation in urban India Recognizing the importance of cities as

engines of economic growth.

STATUS AND STRUCTURE OF EXISTING MICROFINANCE IN INDIA

Indian Microfinance Institutions are predominantly NGOs i.e., nearly 80 % of the Microfinance Institutions

operate under the Society/Trust form which is for the not-for-profit sector with a clear development agenda. Apart from

this, other important legal forms are being used by Indian Microfinance Institutions. 10 % of organizations operate under

the company structure; 5% are section 25 companies (Section 25 of the Indian Companies Act, 1956); 2% as Cooperatives;

2% as Non Banking Finance Companies (NBFCs); and 1% as Local Area Banks (LAB) 3

.

3NABARD, R.Sunita Shree, 2013, Research Work on impact of microfinance on development of micro small enterprises

16 S. L Gupta & Shahid Akhter Ansari

Impact Factor (JCC): 4.4251 Index Copernicus Value (ICV): 3.0

Figure 2

Loan Portfolio of Self Help Groups and Micro Finance Institution (Rs. Billion)

Table 2

Year

2007 2008 2009 2010 2011 2012

Banks-SHGs 123.66 169.99 272.66 272.66 306.19 363.41

MFI 35.56 59.54 183.44 183.44 215.56 209.13

Total 158.22 229.53 456.1 456.1 521.75 572.14

(Source: NABARD, State of the Sector Report, 2012)

Figure 3

Saving of Self Help Groups with Banks Agency Wise Position as on 31st

March 2013 (Amount in Rs Lakhs)

Table 3

Sr. No Name of Agency

Total Savings of

SHG's with Bank

Out of Total- Under

SGSY

Out of TOTAL

Exclusive Women SHGs

No of

SHGs

Saving

Amount No of SHGs

Saving

Amount No of SHGs

Saving

Amount

1 Commercial Banks 4076986 553257.5 1098312 107404.11 3367566 444160.47

2 Regional Rural Banks 2038008 152710.2 758306 61018.71 1683036 128054

3 Co-operative Banks 1202557 115758.22 191193 13742.29 887917 79272.43

Total 7317551 821725.92 2047811 182165.11 5938519 651486.9

(Source: NABARD, Status of Microfinance in India 2012-13)

Status of Microfinance and its Delivery Models in India 17

www.tjprc.org [email protected]

Total saving of SHGs are Rs 821725.92 the figure is surprising that 80% of total saving is contributed by

exclusive women SHGs in India.

Savings of SHGs with Banks Region-Wise/ State-Wise/ Agency-Wise Position as on 31 March 2013

Northern Region (Amount in Rs Lakh)

Table 4

Sr.

No Region/State

Commercial Banks Regional Rural Banks Cooperative Banks Total

No. of Savings No. of Savings No. of Savings No. of Savings

SHGs Amount SHGs Amount SHGs Amount SHGs Amount

A NORTHERN REGION

1 Chandigarh 609 95.11 0 0 0 0 609 95.11

2 Haryana 19011 1646.25 19281 2080.32 4288 304.16 42580 4030.73

3 Himachal

Pradesh 25233 2143.52 7737 1072.48 20272 1061.92 53242 4277.92

4 Jammu &

Kashmir 2854 279.08 1646 445 1296 246.41 5796 970.49

5 New Delhi 3589 327.65 0 0 198 20.4 3787 348.05

6 Punjab 24235 2817.91 5085 353.45 5740 464.12 35060 3635.48

7 Rajasthan 92940 7734.13 56573 3272.57 82250 4754.04 231763 15760.74

Total 168471 15043.65 90322 7223.82 114044 6851.05 372837 29118.52

(Source: NABARD, Status of microfinance in India 2012-13)

Figure 4

North Eastern Region (Amount in Rs Lakh)

Table 5

Sr. No Region/State

Commercial Banks Regional Rural

Banks

Cooperative

Banks Total

No. of Savings No. of Savings No. of Savings No. of Savings

SHGs Amount SHGs Amount SHGs Amount SHGs Amount

B NORTH EASTERN REGION

1 Assam 87203 7037.21 159147 3458 24722 255.55 271072 10750.76

2 Arunachal

Pradesh 3074 155.44 1538 227.68 421 28.97 5033 412.09

3 Manipur 4929 102.55 6106 110.3 1621 22.39 12656 235.24

4 Meghalaya 3264 228.21 3550 245.47 2759 41.98 9573 515.66

5 Mizoram 1128 46.56 1336 547.12 653 18.53 3117 612.21

6 Nagaland 3219 147.36 746 13.23 4513 25.26 8478 185.85

7 Sikkim 3529 79.48 0 0 NA NA 3529 79.48

8 Tripura 10438 219.34 NA NA NA NA 10438 219.34

Total 116784 8016.15 172423 4601.8 34689 392.68 323896 13010.63

(Source: NABARD, Status of microfinance in India 2012-13)

18 S. L Gupta & Shahid Akhter Ansari

Impact Factor (JCC): 4.4251 Index Copernicus Value (ICV): 3.0

Figure 5

Eastern Region (Amount in Rs Lakh)

Table 6

Sr.

No Region/State

Commercial

Banks

Regional Rural

Banks Cooperative Banks Total

No. of Savings No. of Savings No. of Savings No. of Savings

SHGs Amount SHGs Amount SHGs Amount SHGs Amount

C EASTERN REGION

1 A & N

Islands (UT) 925 64.68 0 0 4292 81.06 5217 145.74

2 Bihar 138637 12724.83 132253 4242.81 0 0 270890 16967.64

3 Jharkhand 57850 5712.25 27484 1977.67 0 0 85334 7689.92

4 Odisha 206331 18181.06 242789 19431.46 73717 4215.29 522837 41827.81

5 West Bengal 267132 25673.25 196558 34885.93 123131 12135.69 586821 72694.87

Total 670875 62356.07 599084 60537.87 201140 16432.04 1471099 139325.98

(Source: NABARD, Status of Microfinance in India 2012-13)

Figure 6

Status of Microfinance and its Delivery Models in India 19

www.tjprc.org [email protected]

Central Region (Amount in Rs Lakh)

Table 7

Sr.

NO Region/State

Commercial

Banks

Regional Rural

Banks

Cooperative

Banks Total

No. of Savings No. of Savings No. of Savings No. of Savings

SHGs Amount SHGs Amount SHGs Amount SHGs Amount

D CENTRAL REGION

1 Chhattisgarh 39281 2429.1 52497 3432.64 6715 274.22 98493 6135.96

2 Madhya Pradesh 72436 7976.83 72897 3809.21 14124 535.15 159457 12321.2

3 Uttar Pradesh 152501 23928.7 242460 14672.9 8971 599.22 403932 39200.8

4 Uttarakhand 12348 2742.32 15576 1438.46 12392 582.79 40316 4763.57

Total 276566 37076.9 383430 23353.2 42202 1991.38 702198 62421.5

(Source: NABARD, Status of microfinance in India 2012-13)

Figure 7

Western Region (Amount in Rs Lakh)

Table 8

Sr.

No Region/State

Commercial Banks Regional Rural

Banks

Cooperative

Banks Total

No. of Savings No. of Savings No. of Savings No. of Savings

SHGs Amount SHGs Amount SHGs Amount SHGs Amount

E WESTERN REGION

1 Goa 1499 1800.01 0 0 1630 12.86 3129 1812.87

2 Gujarat 51525 15861.17 18501 4876.93 2645 1300.53 72671 22038.63

3 Maharashtra 118161 84581.33 38579 22807.92 62911 15511.13 219651 122900.4

Total 171185 102242.5 57080 27684.85 67186 16824.52 295451 146751.9

Source: NABARD, Status of Microfinance in India 2012-13)

20 S. L Gupta & Shahid Akhter Ansari

Impact Factor (JCC): 4.4251 Index Copernicus Value (ICV): 3.0

Figure 8

Southern Region

Table 9

Sr.

No Region/State

Commercial Banks Regional Rural

Banks

Cooperative

Banks Total

No. of Savings No. of Savings No. of Savings No. of Savings

SHGs Amount SHGs Amount SHGs Amount SHGs Amount

F SOUTHERN REGION

1 Andhra

Pradesh 935510 1250875 406615 491336.2 14595 5893.27 1356720 1748105

2 Karnataka 166642 195486.2 115864 91678.54 96799 42193.26 379305 329358

3 Kerala 109892 133797.3 19347 11312.42 24097 22718.48 153336 167828.2

4 Lakshadweep 12 3.36 0 0 0 0 12 3.36

5 Puducherry 11576 11509.67 1456 1328.62 927 1385.81 13959 14224.1

6 Tamil Nadu 376602 411231.6 38900 27243.17 96357 65543.02 511859 504017.7

Total 1600234 2002903 582182 622899 232775 137734 2415191 2763536

(Source: NABARD, Status of microfinance in India 2012-13)

Figure 9

Status of Microfinance and its Delivery Models in India 21

www.tjprc.org [email protected]

DELIVERY MODEL OF MICROFINANCE

The availability of credit and banking facilities to the poor and underprivileged segment of the society can be

reached through Microfinance. The Government and the Reserve Bank have taken several initiatives, from time to time,

such as nationalisation of banks, prescription of priority sector lending norms and concessional interest rate for the weaker

section of society. It was, however, realised that further direct efforts were required to address the credit needs of poor

people. In response to this requirement, the Micro finance movement started in India with the introduction of SHG bank

linkage programme (SBLP) in the early 1990s. At present, there are mainly two models for delivery of Microfinance in

India SBPL model and the MFI model.

The SBPL model had more borrowers and loans outstanding in comparison with other models of Microfinance.

SBPL model is recognized as largest Microfinance programme in all over the world as per its coverage. Apex Institutions

like RBI, SIDBI, and NABARD have also taken a number of steps to drive movement of Microfinance programs in India.

The developments relating to evolution of various models of the Micro finance movement are detailed in the present

section. The Micro finance sector started getting recognition in India after the launch of the SBLP.

All over the world lot of basic effort had been step forwarded since 1980s which set a framework for

Microfinance efforts in India. The approaches for delivery of Microfinance are varied in nature. There is no specific model

which fits into all conditions rather there is an easy and elastic approach needed to meet the credit requirement of poor

people. Each model has to be modified as per different situation and local requirements. Various delivery models have

been adopted by Microfinance institutions and they can be categorized in to following broad categories.

SHG-Bank Linkage Model

A SHG is a small group of about 10-20 persons from a homogeneous class of rural and urban poor which

promoted savings among members and used these resources for meeting their credit needs The group is democratically

formed and elects its own leaders . The vital features of SHGs are it consists of members belonging to the same community

or society and having common economic goal.

Their aims for formation of SHG include economic welfare of all members.

Under the SBLP, the following three different models have emerged in India:

Model I: SHGs promoted, guided and financed by banks.

Model II: SHGs promoted by NGOs/ Government agencies and financed by banks.

Model III: SHGs promoted by NGOs and financed by banks using NGOs/formal agencies as financial

intermediaries.

Micro Finance Institution Model

The MFI model in India is characterised by a diversity of institutional and legal forms. MFIs in India exist in a

variety of forms like trusts registered under the Indian Trust Act, 1882/Public Trust Act, 1920; societies registered under

the Societies Registration Act, 1860; Co-operatives registered under the Mutually Aided Cooperative Societies Acts of the

States; and nonbanking financial companies (NBFC)-MFIs, which are registered under Section 25 of the Companies Act,

22 S. L Gupta & Shahid Akhter Ansari

Impact Factor (JCC): 4.4251 Index Copernicus Value (ICV): 3.0

1956 or NBFCs registered with the Reserve Bank. These MFIs are scattered across the country and due to the multiplicity

of registering authorities .

Federated Self Help Group Model

Self Help Groups are successful in empowering women by providing direct and indirect benefits to them.

SHGs are small in size generally 10 – 15 members having limited in the types of financial services they can provide to its

members. Federation of SHGs have more than 1000 members In Federated SHG model, there is a three tier structure the

first tire is the SHG, the second tier is a cluster and the third tier is an apex body, which represents the entire SHG. At the

cluster level, each SHG is represented by two of its members . The apex body usually made up of 10 – 15 members and

they form the link between the SHGs and the NGO which is supporting to them. With the help of federations and NGO

with limited resources, it has impact on a large number of poor people. Examples of Federated Self Help Group model are

PRADAN, Chaitanya and SEWA.

Bank Partnership Mode

In this model, the bank is the lender and the MFI acts as an agent for handling items of work relating to credit

monitoring, supervision and recovery, while the borrower is the individual. In Bank Partnership model Microfinance

institutions acts as an agent of bank. Microfinance institutions are only concerned with dealing with clients for granting

loan to final repayment. In this model MFI for larger funding access holds the borrower loan on its account for some time

and refinance through the mean of securitization.

Grameen Bank Model

In 1970s Grameen Bank model was launched in village area of Bangladesh to empower the poor people through

Microfinance. After great success of GB Model it was created as formal Bank under special Law in 1983. The bank is

owned by the poor burrowers mostly women. The Grameen bank eliminates the concept of collateral security for taking

loan from bank and upturned the conventional banking practice. It is formed on mutual trus t and provides credit facilities

for self employment and profit making activities to low income people. The main feature of Grameen bank model is it

provides door step service to poor people. In India Grameen bank model was adopted by CASHPOR financia l and

technical limited, SHARE Microfinance limited, and Activist for social alternatives (ASA).

Some of the significant features of Grameen bank model are

Low transaction costs,

Loans are collateral free,

Repayment of loans in small and short interval.

Quick loan sanctions with little or no paper works

Repayment of loans in small amount is one of the major reasons of high loan recovery rate of a Grameen Bank.

Banking Correspondents Model

In January 2006, the Reserve Bank permitted banks to utilise the serv ices of NGOs, MFIs (other than NBFCs) and

other civil society organisations as intermediaries in providing financial and banking services through the use of business

Status of Microfinance and its Delivery Models in India 23

www.tjprc.org [email protected]

facilitator and business correspondent (BC) models . The Bank correspondent‟s model permits bank to do transaction at

closer areas of rural population. Thus BC model addressed the problems of poor people from remote areas. The BC model

uses the MFI‟s ability to get close to poor clients – a necessity for savings mobilisation from the poor – while relying on

the financial strength of the bank to safeguard the deposits. Union finance minister in union budget 2008-09 allowed banks

to appoint retired bank employee or retired government employee as business correspondents (BC).

CONCLUSIONS

Economic and financial services institutions long term growth is depend on the manner that Financial Institutions

approaches and taps untapped rural areas in India. Microfinance is often portrayed in literature as a tool that allows

individuals excluded from the financial system to get access to sources of funding, which will help for theirs development

and growth. From the above study it can be viewed that Self help Groups are playing vital role in delivery of microfinance

services which leads to increase the saving habits of poorest strata of society and contributing towards the development of

poor people in India.

REFERENCES

1. Anand Vishal, (2014), Microfinance: State-of-the-art Paradigm for Women's Empowerment in Bihar,

IOSR Journal of Humanities And Social Science (IOSR-JHSS) Volume 19, Issue 1, Ver. XI (Feb. 2014),

PP 05-08.

2. Sunitha. S, (2014) A comprehensive study on micro finance institutions in India, GALAXY International

Interdisciplinary Research Journal GIIRJ, Vol. 2 (2), FEBRUARY (2014).

3. Banarjee Abhijit et al, (2014) The miracle of microfinance? Evidence from a randomized evaluation

(http://economics.mit.edu/files/5993)

4. Mishra Sibanjan et.al, (2013), Microfinance: A tool for poverty alleviation, American International Journal of

Research in Humanities, Arts and Social Sciences page 236-238.

5. Nasir Sibhatullah, (2013), Microfinance in India: Contemporary Issues and Challenges. Middle-East Journal of

Scientific Research 15 (2): 191-199, 2013.

6. Status of Microfinance in India (2012-13) (https://www.nabard.org/english/allpublication.aspx)

7. Mahanta Padmalochan et.al, (2012) Status of microfinance in India - a review International Journal of

Marketing, Financial Services & Management Research Vol.1 Issue 11, November 2012, ISSN 2277 3622.

8. Bansal Kumar Ajit et.al, (2012) Microfinance and poverty reduction in India. Integral Review- A Journal of

Management ISSN: 2278-6120, Volume 5, No. 1, June-2012,pp 31-35

9. Sharma Manoranjan,(2012) Resuscitating Rural Financial Institutions in India: Catalytic Role of Micro Finance

(oii.igidr.ac.in:8080/ jspui/handle/2275/215)

10. SAGE Publication India pvt. Ltd., (2012) Micro finance India Social performance Report‟.

11. Ramesh s Arunachalam, (2011) „The Journey of Indian Microfinance‟ Rawat Publication.

24 S. L Gupta & Shahid Akhter Ansari

Impact Factor (JCC): 4.4251 Index Copernicus Value (ICV): 3.0

12. Muhammad Yunus et.al,(2010) Building Social Business Models: Lessons from the Grameen Experience,

(www.hec.edu/.../Article%20LRP%20Yunus%20Moingeon%20Lehmann)

13. Imai Kotsushi et.al, (2010) Microfinance and Household Poverty Reduction: New evidence from India,

Economics Discussion Paper Series EDP-1008 Economics School of Social Sciences The University of

Manchester,

14. Kumar Manish et.al, (2010) Micro-Finance as an Anti Poverty Vaccine for Rural India International Review of

Business and Finance ISSN 0976-5891 Volume 2 Number 1 (2010), pp. 29–35

15. V. S. Somnath, (2009) ‘Micro finance Redefining future‟, Excel books, New Delhi.

Related Documents