Developing Social Audit Model

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Developing Social Audit Model

Facilitators:

Henry Clarke Kisembo

Senior Consultant

Development Associates Link International – DALI

Email: [email protected]

Tel: 0782436720 / 0704375304

Edward Rodney Wesonga

Associate Consultant

Development Associates Link International (DALI)

Email: [email protected]

Tel: 0759969111 / 0775500366

Training Objectives:

The overall objective of the training is to develop a social auditmodel with focus on the staying alive project in Uganda.

Training Outcomes:

• Participants Understand the Social Audit Model.

• Participants understand the Social Audit Process.

• Participants are able to design and administer Social Audits.

• Participants are able to translate the skills attained to communityempowerment and stakeholder engagement.

• Participants are able to develop Social Audit action Plans.

Session 1: Introduction:

Governments are facing an ever-growing demand to be moreaccountable and socially responsible and the community isbecoming more assertive about its right to be informed and toinfluence governments’ decision-making processes.

What is a Social Audit:

• Social audit is a tool through which government departments canplan, manage and measure non-financial activities and monitorboth internal and external consequences of the departments’social and commercial operations.

Social Audit: Government and CSO Initiatives

The pressure to enhance accountability could originate from twodifferent sources;

1. Government is one potential source, but the precondition is thatthe political and bureaucratic leadership is motivated to usher inreform.

2. Alternatively, the pressure for increased public accountabilitymay come from the civil society.

3. There is a wide range of ongoing people's movements and non-governmental initiatives in Developing countries for examplebarazas.

Pre-requisites for carrying out Social Audit

• State should have faith in participatory democracy

• An active and empowered civil society

• State should be accountable to the civil society

• Congenial political and policy environment

• Have an informed community

• Respect for good governance

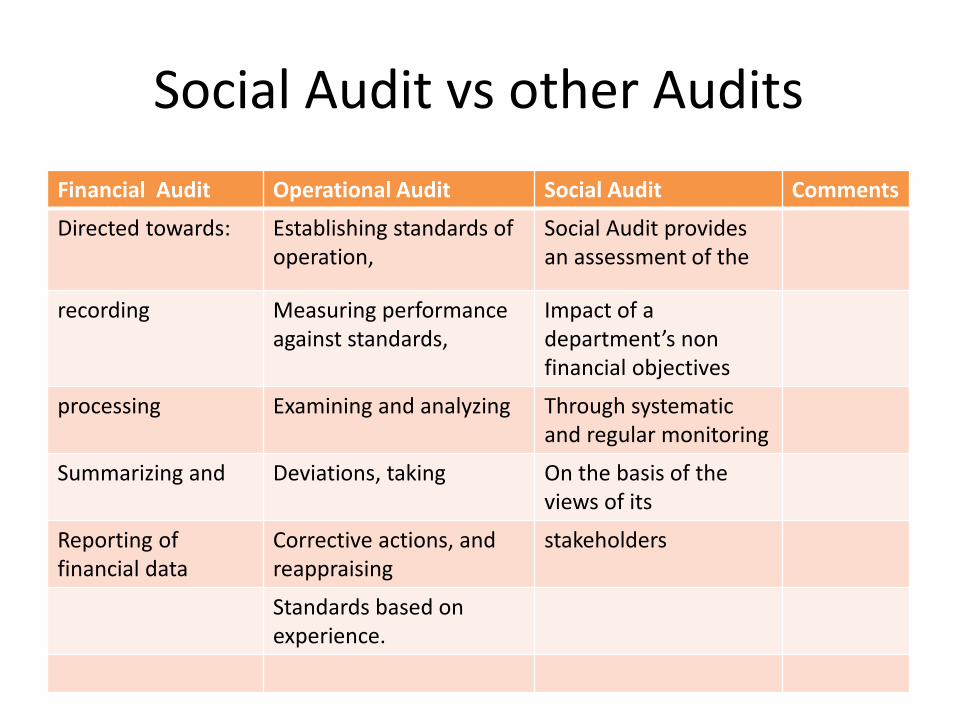

Social Audit vs other Audits

Financial Audit Operational Audit Social Audit Comments

Directed towards: Establishing standards of operation,

Social Audit provides an assessment of the

recording Measuring performance against standards,

Impact of a department’s non financial objectives

processing Examining and analyzing Through systematic and regular monitoring

Summarizing and Deviations, taking On the basis of the views of its

Reporting of financial data

Corrective actions, and reappraising

stakeholders

Standards based on experience.

Stakeholders and Social Audit

• Social auditing uses participatory techniques to involve all

stakeholders in measuring, understanding, reporting and

improving the social performance of an organization or activity.

• Stakeholders are at the centre of the concept of social audit. The

term "stakeholder" appeared for the first time in 1963 in an

internal document of Stanford Research Institute, and the

document defined stakeholders as the groups without whose

support an organization cannot realize its objectives and goals.

Session 2: Principles of Social Audit

• Multi-Perspective/Polyvocal: Aim to reflect the views (voices) ofall those people (stakeholders) involved with or affected by theorganization/department/ programme.

• Comprehensive: Aims to (eventually) report on all aspects of theorganization's work and performance.

• Participatory: Encourages participation of stakeholders andsharing of their values.

• Multidirectional: Stakeholders share and give feedback onmultiple aspects.

• Regular: Aims to produce social accounts on a regular basis sothat the concept and the practice become embedded in theculture of the organization covering all the activities.

Principles of Social Audit

• Comparative: Provides a means whereby the organization cancompare its own performance each year and against appropriateexternal norms or benchmarks; and provide for comparisons to bemade between organizations doing similar work and reporting insimilar fashion.

• Verified: Ensures that the social accounts are audited by asuitably experienced person or agency with no vested interests inthe organization.

• Disclosed: Ensures that the audited accounts are disclosed tostakeholders and the wider community in the interests ofaccountability and transparency.

Uses and Functions of Social Audit

• To monitor the social and ethical impact and performance of the

organization;

• To provide a basis for shaping management strategy in a socially

responsible and accountable way, and to design strategies;

• To facilitate organizational learning on how to improve social

performance;

• To facilitate the strategic management of institutions;

• To inform the community, public, other organizations and

institutions in the allocations of their resources;

Benefits of Social Auditing

• Affects positive organizational change:

• Increases accountability:

• An externally verified audit can add credibility to thedepartment’s efforts.

• Enhances reputation:

• Alerts policymakers to stakeholder trends:

• Provides increased confidence in social areas:

• Assists in reorienting and refocusing priorities:

Session 3: Six key steps for Social audit

1. Preparing and Using Social Accounts

2. Defining Audit Boundaries and Identifying Stakeholders.

3. Social Accounting and Book-Keeping.

4. . Social Audit and Dissemination.

5. Monitoring social accounting activities.

6. Feedback and Institutionalization of Social Audit.

Session 4: Develop Action plan together with stakeholders

1. Develop Social Audit objectives;

2. Identify Social Issues;

3. Define deliverables;

4. Develop activities to be undertaken;

5. Establish indicators;

6. Establish Means of Verification;

7. Allocate roles to institutions and individuals;

8. Define timelines;

9. Allocate resources budget resources;

Related Documents