Smith & Williamson Investment Funds Plc An investment company with variable capital constituted as an umbrella fund with segregated liability between sub-funds under the laws of Ireland and authorised by the Central Bank of Ireland pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations 2011 as amended and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities) Regulations 2015 as amended (collectively the “Regulations”) Annual Report and Audited Financial Statements For the financial year ended December 31, 2018 No subscription can be received on the basis of financial reports. Subscriptions are only valid if made on the basis of the current Prospectus which will be accompanied by a copy of the latest available annual report and a copy of the latest available semi-annual report, if published after such annual report.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Smith & Williamson Investment Funds Plc

An investment company with variable capital constituted as an umbrella fund with

segregated liability between sub-funds under the laws of Ireland and authorised by

the Central Bank of Ireland pursuant to the European Communities (Undertakings

for Collective Investment in Transferable Securities) Regulations 2011 as amended

and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1))

(Undertakings for Collective Investment in Transferable Securities)

Regulations 2015 as amended (collectively the “Regulations”)

Annual Report and Audited Financial

Statements

For the financial year ended

December 31, 2018

No subscription can be received on the basis of financial reports. Subscriptions are only

valid if made on the basis of the current Prospectus which will be accompanied by a copy of

the latest available annual report and a copy of the latest available semi-annual report, if

published after such annual report.

Smith & Williamson Investment Funds Plc

1

Table of contents

Directors and Other Information

2

Investment Manager’s Report

3

Depositary’s Report

4

Directors’ Report

5 - 7

Independent Auditor’s Report

8 - 10

Statement of Financial Position

11 - 18

Statement of Comprehensive Income

19 - 22

Statement of Changes in Net Assets Attributable to Holders of Redeemable

Participating Shares

23 - 26

Statement of Cash Flows 27 - 30

Notes to the Financial Statements

31 - 90

Schedule of Investments

91 - 126

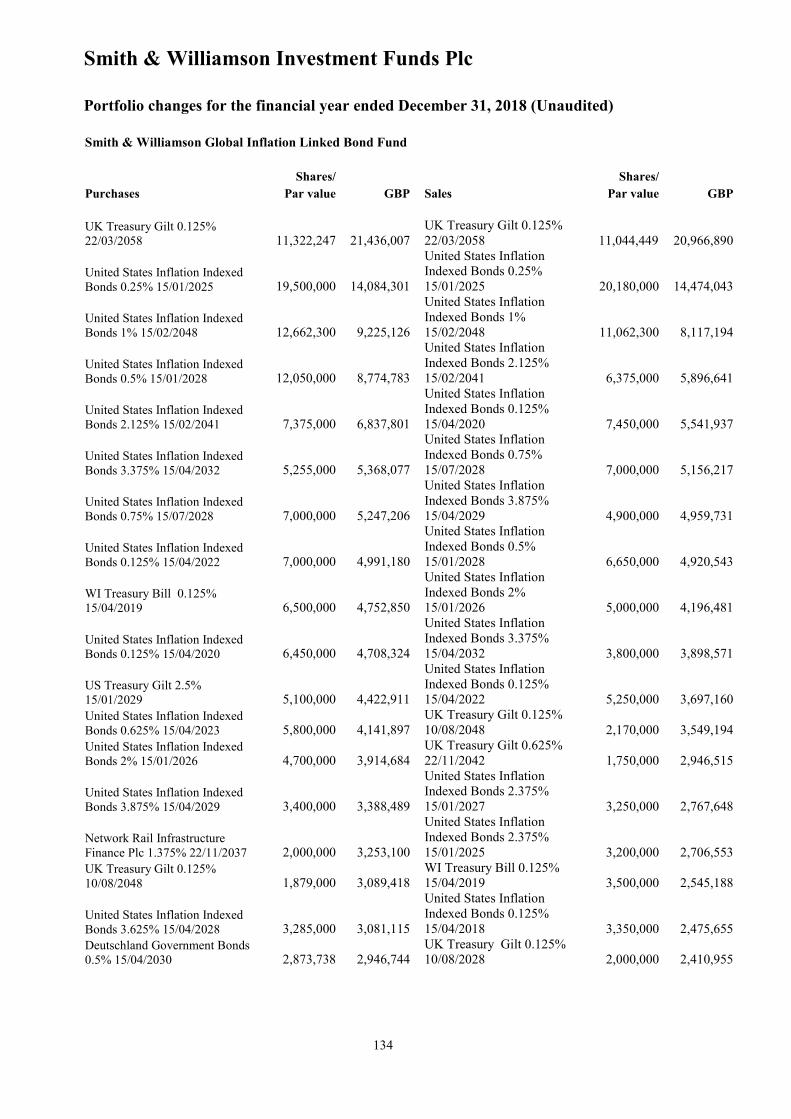

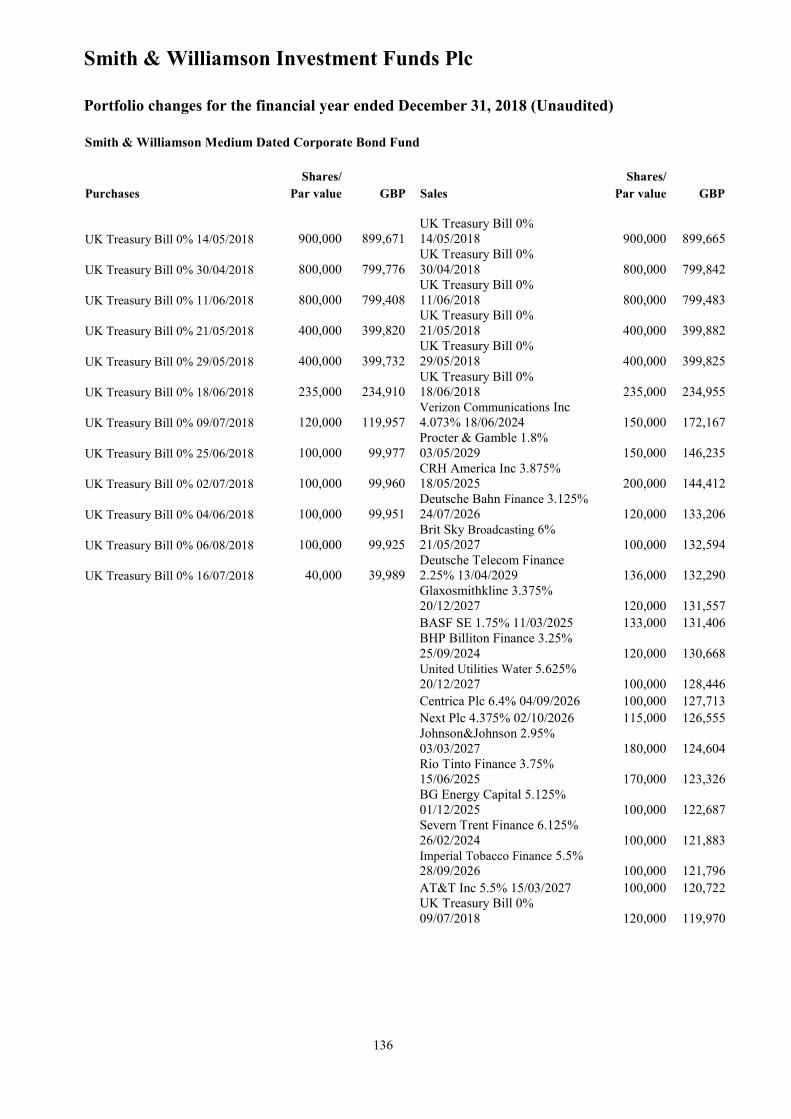

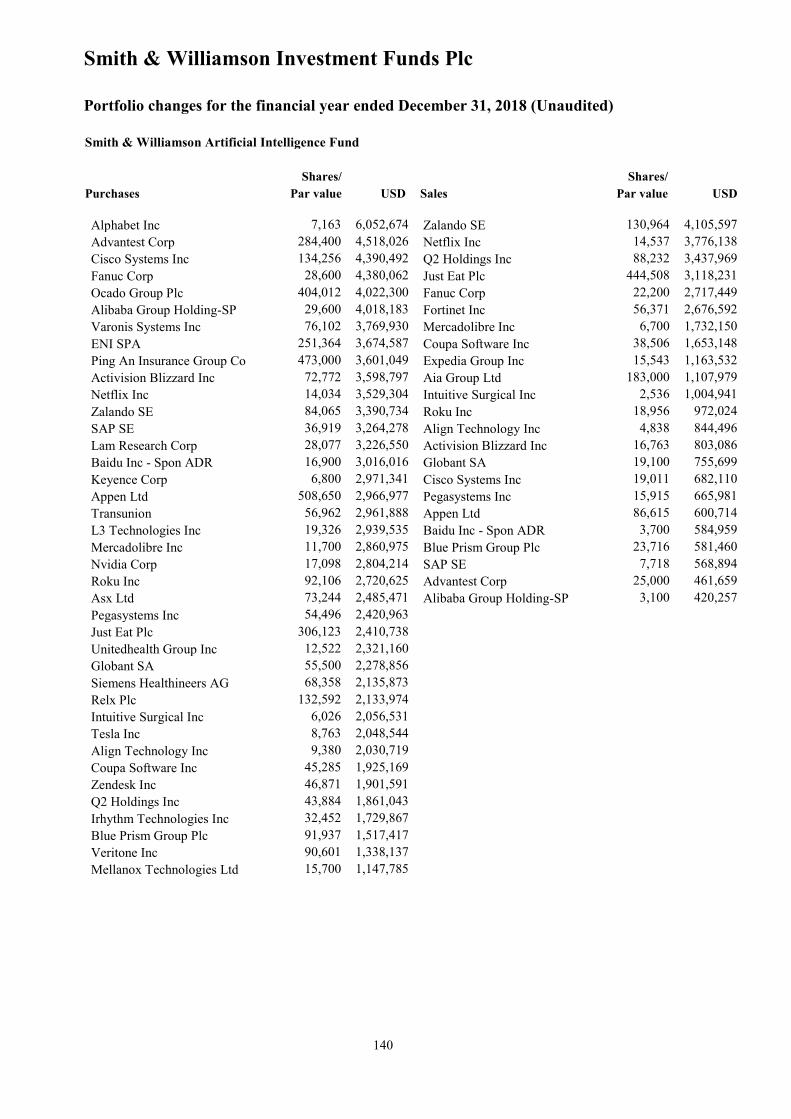

Portfolio Changes (Unaudited)

127 - 140

Unaudited Section 141 - 142

Smith & Williamson Investment Funds Plc

2

Directors and Other Information

Registered Office

Trinity Point

10-11 Leinster Street South

Dublin 2

Ireland

Investment Manager and Distributor

Smith & Williamson Investment Management LLP

25 Moorgate

London EC2R 6AY

England

Directors

Peter Blessing (Irish - Independent director)*

William Cussans (British)*

Desmond Miller (Irish - Independent director)*

Paul Wyse (Irish)*

Noel Medici (British)*

Administrator, Registrar and Transfer Agent

BNP Paribas Fund Administration Services (Ireland) Limited

Trinity Point

10-11 Leinster Street South

Dublin 2

Ireland

Depositary

BNP Paribas Securities Services, Dublin Branch

Trinity Point

10-11 Leinster Street South

Dublin 2

Ireland

Independent Auditors

Deloitte Ireland LLP

Chartered Accountants and Statutory Audit Firm

Deloitte & Touche House

Earlsfort Terrace

Dublin 2

Ireland

Legal Advisers in Ireland

A&L Goodbody Solicitors

International Financial Services Centre

North Wall Quay

Dublin 1

Ireland

Company Secretary

Goodbody Secretarial Limited

International Financial Services Centre

North Wall Quay

Dublin 1

Ireland

Manager

Smith & Williamson Investment Management (Ireland)

Limited

Trinity Point

10-11 Leinster Street South

Dublin 2

Ireland

Company Number

316015

*non-executive Director

Smith & Williamson Investment Funds Plc

3

Investment Manager’s Report

As the key worries about a possible US recession and the damage that a trade way could inflict on global growth have

receded, equity markets worldwide recovered from the lows seen at the end of 2018. Whilst markets were looking

oversold and relatively cheap, a catalyst was needed to spur the recovery, and this time it came from a reversal in

policy from the Fed, who eased fears of rising rates with a flip-flop towards no rises. We may even see a cut in rates

this year.

Following the recovery in equity markets the one question still to be answered is whether the indicators of slowing

growth that we are seeing are simply another soft patch in what has been an extremely long but slow growth cycle, or

whether we are now at a stage in the process which leads to recession and thus falls in earnings and share prices. These

worries have been compounded recently by the inversion of the US yield curve, which in the past has been a good lead

indicator of an earnings contractions approaching – but not necessarily being imminent.

But not all the indicators are negative. Indeed, there have been many positive developments that continue to point to a

slow but steady period of economic growth. Much has actually improved since the end of last year – China in

particular is responding to further stimulus, and should we see good news coming from the US – Sino trade talks, as

has recently been leaked, this could also provide added stimulus to US and Asian equities in particular. Broadly, real

rates are still very accommodative and the US is proving to be resilient. Labour markets remain very strong in key

regions, with rising wages. We are running our US and Far East positions for now.

In the UK the uncertainty caused by Brexit is helping some parts of the economy and hindering others, but as a whole

the economy isn’t doing too badly. An apparent surge in stockbuilding ahead of the original Brexit day of 29th March

boosted the Markit/CIPS manufacturing index to a 13-month high in March. In contrast, by prompting firms to delay

spending decisions, the political uncertainty contributed to the services PMI falling to its lowest level since the 2016

referendum. At face value, the two activity surveys suggest that the economy may have stagnated in Q1. The risk to

estimates that GDP rose by 0.3% in Q1 lie on the downside, but it must be remembered that the UK equity market is

still at a low valuation, suggesting much bad news is in the price.

There has been some talk that the European economy is moving into a tricky period. Bund yields in Germany have

fallen back to below zero, leading to talk about the ‘Japanification’ of Europe. There are some parallels. Inflation and

interest rates are low. Economic growth has been feeble. The banking sector looks weak. Overall, we still expect

equity markets to advance, but the relative strength from Europe is currently challenged. We have been reducing our

exposure to Europe over the past six months, and this will continue.

We are modestly bullish for equities and bonds, encouraged by global activity momentum looking to be positive, with

the US being resilient, China turning higher and Europe stabilising. However, the bottom-up analyst consensus now

expects global EPS growth of 5% in 2019, down from 7% at the start of the year, and more in-line with the 4% top-

down forecast. Gains are still expected but possibly only modest from here until the outlook for 2020 becomes clearer.

Smith & Williamson Investment Management Ltd

March 2019

Smith & Williamson Investment Funds Pie

DEPOSITARY'S REPORT TO THE SHAREHOLDERS OF SMITH & WILLIAMSON INVESTMENT FUNDS PLC FOR THE FINANCIAL YEAR ENDED DECEMBER 31,2018

In our opinion, the Company has been managed during the financial year, in all material respects:

(i) in accordance with the limitations imposed on the investment and borrowing powers of the scheme by the memorandum and articles of association and by the Central Bank of Ireland under the powers granted to the Central Bank of Ireland by the European Union (Undertakings for Collective Investment in Transferable Securities) (Amendment) Regulations 2015 as amended from time to time (the "Regulations") and the Companies Act, 2014; and

(ii) Otherwise in accordance with the provisions of the memorandum and articles of associations and the Regulations.

)v0y)lo {:oJcllvV'~-BNP Paribas Securities ~e~iJs,~in Branch Trinity Point 10-11 Leinster Street South Dublin 2 Ireland April 15, 2019

4

Smith & Williamson Investment Funds Plc

5

Directors’ Report

The Directors present their annual report together with the audited financial statements for the financial year ended

December 31, 2018.

Directors’ Responsibilities Statement

The Directors are responsible for preparing the Directors’ report and the financial statements in accordance with the

Companies Act 2014 as amended (the “Act”) and the Regulations. They have elected to prepare the financial

statements in accordance with International Financial Reporting Standards as adopted by the European Union

(“IFRS”).

Under the Act, the Directors must not approve the financial statements unless they are satisfied that they give a true

and fair view of the assets, liabilities and financial position of the Company as at the financial year end date and of the

profit or loss of the Company for the financial year.

In preparing those financial statements, the Directors are required to:

select suitable accounting policies and then apply them consistently;

make judgements and estimates that are reasonable and prudent;

state whether the financial statements have been prepared in accordance with the applicable accounting standards,

identify those standards, and note the effect and the reasons for any material departure from those standards; and

prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company

will continue in business.

The Directors confirm that they complied with the above requirements in preparing the financial statements.

The Directors are responsible for keeping adequate accounting records that are sufficient to:

- correctly record and explain the transactions of the Company;

- enable, at any time, the assets, liabilities, financial position and profit or loss of the Company to be determined

with reasonable accuracy; and

- enable the Directors to ensure that the financial statements comply with the Act, and enable those financial

statements to be audited.

To achieve this, the Directors have appointed the Administrator to ensure that the requirements of the Act, are complied

with. The accounting records are maintained at the Administrator’s offices at Trinity Point, 10-11 Leinster Street South,

Dublin 2, Ireland.

They are also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the

prevention and detection of fraud and other irregularities. To help achieve this, the Directors have delegated custody of

the Company’s assets to the Depositary.

Principal Activities

The Company commenced activities on 31 March 2000 and has been approved by the Central Bank of Ireland as an

Undertaking for Collective Investment in Transferable Securities. The Company is an open ended umbrella type

investment company comprising separate sub–funds which also have separate investment objectives.

Business Review

The Investment Manager’s Report contains a review of the factors which contributed to the performance of the

Company during the financial year. The Directors do not anticipate any changes to the investment objectives of the

existing sub-funds. As at 31 December 2018, the Company had 11 active sub-funds in operation and 1 sub-fund was

terminated during the financial year.

Risks and uncertainties

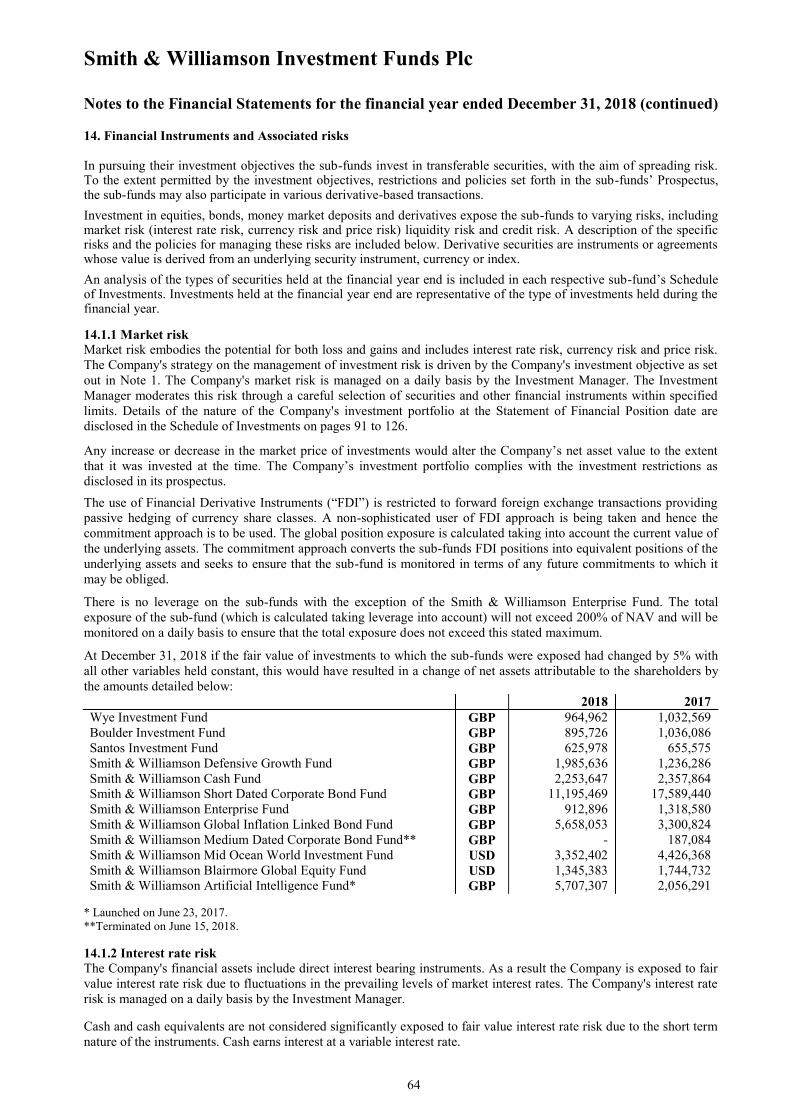

The principal risks facing the Company are described in Note 14.

Results and Distributions

The results for the financial year are set out in the Statement of Comprehensive Income on pages 19-22 and details of

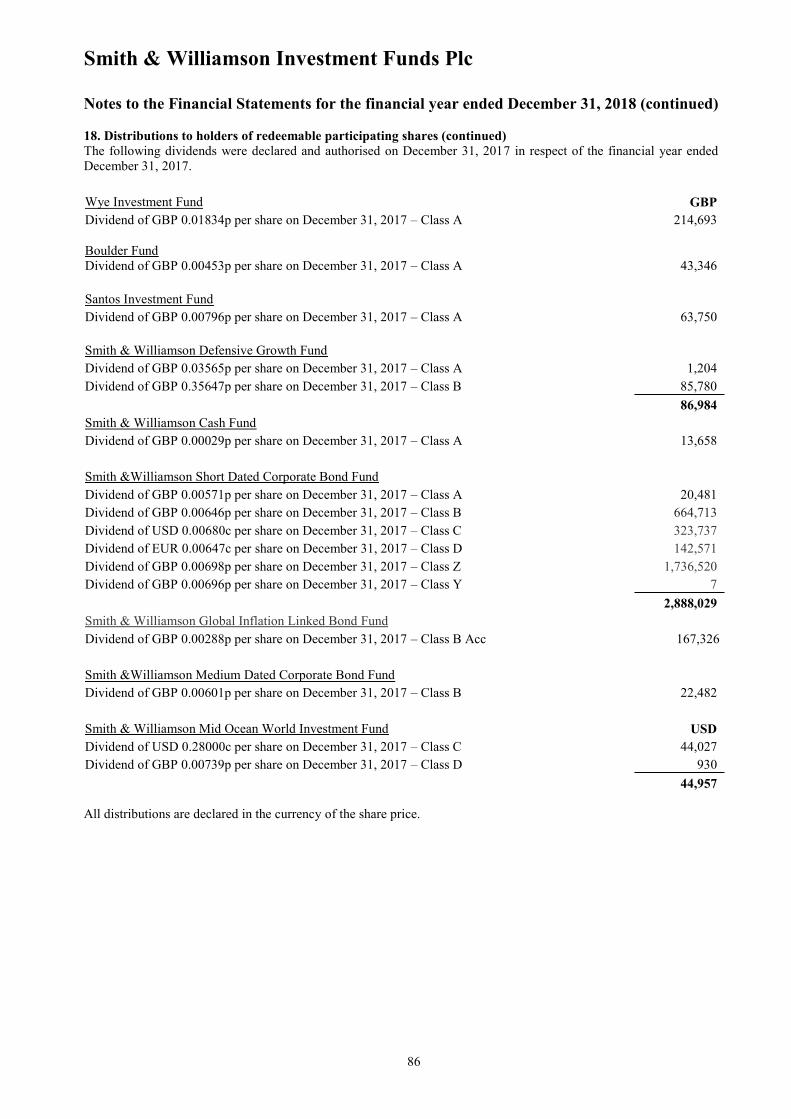

distributions to investors are set out in Note 18.

Smith & Williamson Investment Funds Plc

6

Directors’ Report (continued)

Directors

The Directors that served during the financial year are listed below. All of the Directors served for the whole of the

financial year under review.

Peter Blessing (Irish - Independent director)*

William Cussans (British)*

Desmond Miller (Irish - Independent director)*

Paul Wyse (Irish)*

Noel Medici (British)*

*non-executive Director

Directors’ Interests

As at December 31, 2018 William Cussans had a beneficial interest of 225,000 shares in the Smith &Williamson Cash

Fund. Noel Medici had a beneficial interest of 16,950 units in Smith & Williamson Global Inflation Linked Bond

Fund, 20,820 units in Smith & Williamson Enterprise Fund and 20,265 units in Smith & Williamson Artificial

Intelligence Fund.

Transactions Involving Directors

There were no contracts or arrangements of any significance in relation to the business of the Company in which the

Directors had any interest as defined in the Act at any time during the financial year ended December 31, 2018 except

for the Investment Management and Distribution Agreements between the Company and Smith & Williamson

Investment Management LLP of which Noel Medici and William Cussans are employees.

Transactions with Connected Persons

In accordance with the requirements of the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1))

(Undertakings for Collective Investment in Transferable Securities) Regulations 2015 as amended the Directors

confirm that there are arrangements in place, evidenced by written procedures to ensure that any transactions carried

out between the Company and a connected person is conducted as arm’s length and in the best interests of the

shareholders. Connected persons means the Manager, Depositary and the delegates or sub-delegates of such a

management company or depositary (excluding any non-group company sub-custodians appointed by a depositary);

and any associated or group company of such a management company, depositary, delegate or sub-delegate. The

Company’s Board of Directors are satisfied that the transactions with connected persons during the financial year were

carried out as if negotiated at arm’s length and in the best interests of the shareholders.

Accounting Records

The Directors have ensured that the proper books and records requirements under Section 281 to 285 of the

Companies Act 2014 have been complied with by outsourcing this function to a specialist provider of such services.

The books of account are held at the Company’s registered office which is Trinity Point, 10 - 11 Leinster Street South,

Dublin 2.

Directors Compliance Statement

The Directors acknowledge that they are responsible for securing the Company’s compliance with the relevant

obligations as set out in Section 225 of the Companies Act 2014. The Directors confirm that:

A compliance policy document has been drawn up that sets out policies, that in our opinion are appropriate to the

company, respecting compliance by the company with its relevant obligations,

Appropriate arrangements or structures are in place that are, in our opinion, designed to secure material

compliance with the company's relevant obligations, and

During the financial year, the arrangements or structures referred to above have been reviewed.

Smith & Williamson Investment Funds Pie

Directors' Report (continued)

Statement of Relevant Audit Information The Directors acknowledge that they are responsible for providing all relevant audit information to the Company's statutory auditors in connection with preparing their report in accordance with Section 330 of the Companies Act 2014. The Directors confirm that:

• So far as the Directors are aware, there is no relevant audit information of which the Company's statutory auditors are not aware, and

• The Directors have taken all the steps that ought to have been taken as a Director in order to make himself or herself aware of any relevant audit information and to establish that the Company's statutory auditors are aware of that information.

Audit Committee Statement Section 167 (2) of the Act, requires the Board of Directors to either establish an audit committee or decide not to establish such a committee. The Directors believe that there is no requirement to form an audit committee as: Due consideration and oversight is given to the Company's financial reporting processes, internal controls and independent auditors at the quarterly Board meetings.

Voluntary Corporate Governance Code for the Irish Funds Industry The Company has complied with all elements of the Irish Funds' Corporate Governance Code for Collective Investment

Schemes and Management Companies during the financial year ended December 31, 2018.

Significant events during the financial year Smith &Williamson Medium Dated Corporate Bond Fund was terminated on June 15,2018.

A new Prospectus was issued on August 28, 2018.

Events post financial year end There were no significant events after the financial year end.

Independent Auditor The auditors, Deloitte Ireland LLP, Chartered Accountants and Statutory Audit Firm, have signified their willingness to continue in office in accordance with Section 383(2) of the Companies Act, 2014.

Signed on behalfofthe Board

April 15, 2019

7

Deloitte. Deloitte Ireland LLP Chartered Accountants & Statutory Audit Firm

INDEPENDENT AUDITOR'S REPORT TO THE SHAREHOLDERS OF SMITH & WILLIAMSON INVESTMENT FUND PLC

Report on the audit of the financial statements

Opinion on the financial statements of Smith & Williamson Investment Fund Pie ("the company") In our opinion the financial statements:

• give a true and fair view of the assets, liabilities and financial position of the company as at December 31, 2018 and of the loss for the financial year then ended; and

• have been properly prepared in accordance with the relevant financial reporting framework, the applicable Regulations and, in particular, with the requirements of the Companies Act 2014 and the European Communities (Undertaking for Collective Investment in Transferable Securities) regulation 2011 and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in transferable Securities) Regulations 2015.

The financial statements we have audited comprise:

• the Statement of Financial Position; • the Statement of Comprehensive Income • the Statement of Changes in Net Assets attributable to holders of Redeemable Shares; • the Statement of Cash Flows; and • the related notes 1 to 25, including a summary of significant accounting policies as set out in note 2.

The relevant financial reporting framework that has been applied in their preparation is the Companies Act 2014 and Intrnational Finacnia Reporting Standards (IFRSs) as adopted by the European Union ("the relevant financial reporting framework").

Basis for opinion We conducted our audit in accordance with International Standards on Auditing (Ireland) (ISAs (Ireland)) and applicable law. Our responsibilities under those standards are described below in the "Auditor's responsibilities for the audit of the financial statements" section of our report .

We are independent of the company in accordance with the ethical requirements that are relevant to our audit of the financial statements in Ireland, including the Ethical Standard issued by the Irish Auditing and Accounting Supervisory Authority, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion .

Conclusions relating to going concern We have nothing to report in respect of the following matters in relation to which ISAs (Ireland) require us to report to you where :

• the directors' use of the going concern basis of accounting in preparation of the financial statements is not appropriate; or

• the directors have not disclosed in the financial statements any identified material uncertainties that may cast significant doubt about the company's ability to continue to adopt the going concern basis of accounting for a period of at least twelve months from the date when the financial statements are authorised for issue.

Other information The directors are responsible for the other information. The other information comprises the information included in the Annual Report, other than the financial statements and our auditor's report thereon. Our opinion on the financial statements does not cover the other information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon .

Continued on next page/

8

Deloitte. / Continued from previous page

INDEPENDENT AUDITOR'S REPORT TO THE SHAREHOLDERS OF SMITH & WILLIAMSON INVESTMENT FUND PLC

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether there is a material misstatement in the financial statements or a material misstatement of the other information. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are requ ired to report that fact.

We have nothing to report in this regard.

Responsibilities of directors As explained more fully in the Directors ' Report, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view and otherwise comply with the Companies Act 2014, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the Company 's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the Company or to cease operations, or have no realistic alternative but to do so.

Auditor's responsibilities for the audit of the financial statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion . Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (Ireland) will always detect a material misstatement when it ex ists . Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements .

As part of an audit in accordance with ISAs (Ireland) , we exercise professional judgment and maintain professional scepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the company's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the directors.

• Conclude on the appropriateness of the directors ' use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the company's ability to continue as a going concern . If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of the auditor's report . However, future events or conditions may cause the entity ( or where relevant, the group) to cease to continue as a going concern.

Continued on nex t page/

9

Deloitte. / Continued from previous page

INDEPENDENT AUDITOR'S REPORT TO THE SHAREHOLDERS OF SMITH & WILLIAMSON INVESTMENT FUND PLC

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that the auditor identifies during the audit .

This report is made solely to the company's shareholders, as a body, in accordance with Section 391 of the Companies Act 2014. Our audit work has been undertaken so that we might state to the company's shareholders those matters we are required to state to them in an auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company 's shareholders as a body, for our audit work, for this report, or for the opinions we have formed.

Report on other legal and regulatory requirements

Opinion on other matters prescribed by the Companies Act 2014 Based solely on the work undertaken in the course of the audit, we report that :

• We have obtained all the information and explanations which we consider necessary for the purposes of our audit. • In our opinion the accounting records of the company were sufficient to permit the financial statements to be

read ily and properly audited . • The financial statements are in agreement with the accounting records. • In our opinion the information given in the directors' report is consistent with the financial statements and the

directors' report has been prepared in accordance with the Companies Act 2014.

Matters on which we are required to report by exception Based on the knowledge and understanding of the company and its environment obtained in the course of the audit, we have not identified material misstatements in the directors' report.

We have nothing to report in respect of the provisions in the Companies Act 2014 which require us to report to you if, ur opinion, the disclosures of directors' remuneration and transactions specified by law are not made.

is ian' acManus For and on behalf of Deloitte Ireland LLP Chartered Accountants and Statutory Audit Firm Deloitte & Touche House, Earlsfort Terrace, Dublin 2 Ireland

29 April 2019

10

Smith & Williamson Investment Funds Plc

11

Statement of Financial Position

as at December 31, 2018

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth Fund

Smith &

Williamson

Cash Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

Notes GBP GBP GBP GBP GBP GBP GBP

Assets

Financial assets at fair value through profit or loss 5,15 19,299,230 17,914,517 12,519,562 39,712,719 - 224,254,945 18,569,306

Cash at bank 7 80,192 157,686 187,762 2,597,868 6,731 1,657,844 13,406,091

Loans and receivables 8 - - - - 45,072,930 23,974,130 99,604,614

Debtors 6 67,260 24,089 42,661 122,564 69,989 6,083,079 214,966

Total assets 19,446,682 18,096,292 12,749,985 42,433,151 45,149,650 255,969,998 131,794,977

Current liabilities

Financial liabilities at fair value through profit or loss 5,15 - - - - - 345,557 311,390

Bank overdraft 7 - - - - - - 30,001

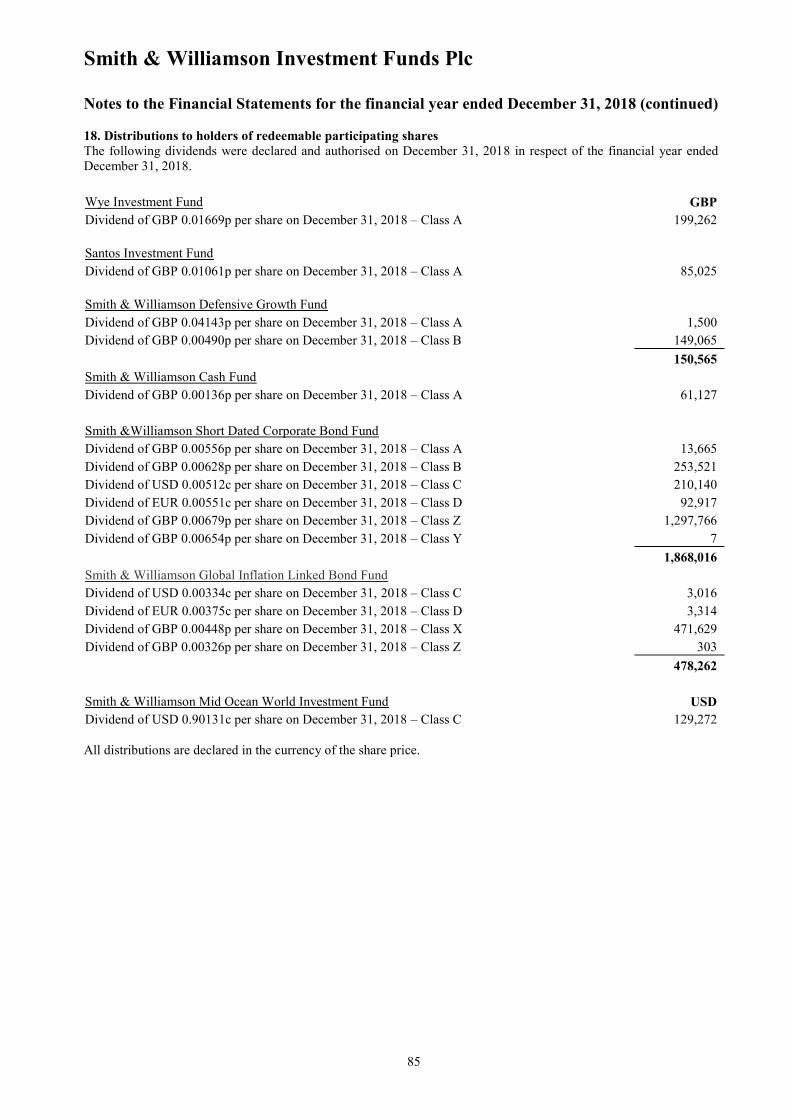

Dividends payable 18 199,262 - 85,025 150,565 61,127 1,868,016 -

Other liabilities 9 27,839 24,868 21,715 1,319,972 24,594 2,306,923 718,667

Due to shareholders - - - 121,325 5,619 36,807 30,479

Total current liabilities (excluding net assets attributable

to holders of redeemable participating shares) 227,101 24,868 106,740 1,591,862 91,340 4,557,303 1,090,537

Net assets attributable to holders of redeemable

participating shares 19,219,581 18,071,424 12,643,245 40,841,289 45,058,310 251,412,695 130,704,440

The notes 1 to 25 form an integral part of the financial statements.

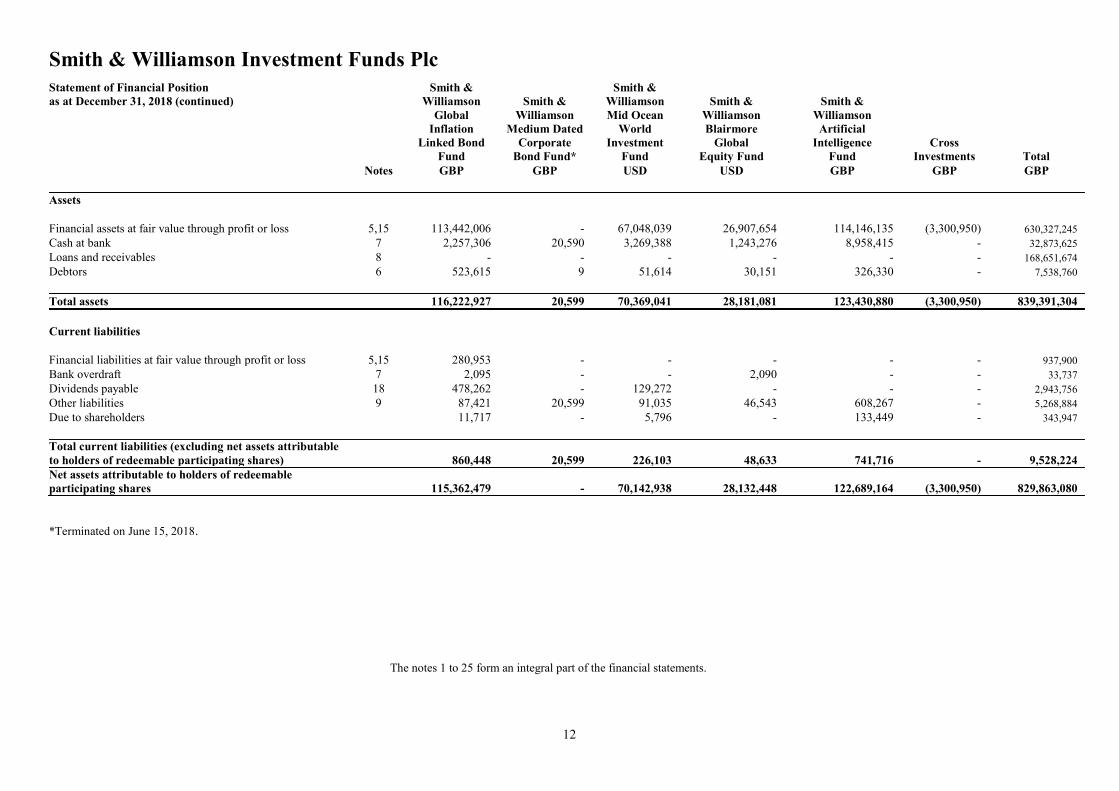

Smith & Williamson Investment Funds Plc

12

Statement of Financial Position

as at December 31, 2018 (continued)

Smith &

Williamson

Global

Inflation

Linked Bond

Fund

Smith &

Williamson

Medium Dated

Corporate

Bond Fund*

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity Fund

Smith &

Williamson

Artificial

Intelligence

Fund

Cross

Investments Total

Notes GBP GBP USD USD GBP GBP GBP

Assets

Financial assets at fair value through profit or loss 5,15 113,442,006 - 67,048,039 26,907,654 114,146,135 (3,300,950) 630,327,245

Cash at bank 7 2,257,306 20,590 3,269,388 1,243,276 8,958,415 - 32,873,625

Loans and receivables 8 - - - - - - 168,651,674

Debtors 6 523,615 9 51,614 30,151 326,330 - 7,538,760

Total assets 116,222,927 20,599 70,369,041 28,181,081 123,430,880 (3,300,950) 839,391,304

Current liabilities

Financial liabilities at fair value through profit or loss 5,15 280,953 - - - - - 937,900

Bank overdraft 7 2,095 - - 2,090 - - 33,737

Dividends payable 18 478,262 - 129,272 - - - 2,943,756

Other liabilities 9 87,421 20,599 91,035 46,543 608,267 - 5,268,884

Due to shareholders 11,717 - 5,796 - 133,449 - 343,947

Total current liabilities (excluding net assets attributable

to holders of redeemable participating shares) 860,448 20,599 226,103 48,633 741,716 - 9,528,224

Net assets attributable to holders of redeemable

participating shares 115,362,479 - 70,142,938 28,132,448 122,689,164 (3,300,950) 829,863,080

*Terminated on June 15, 2018.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

13

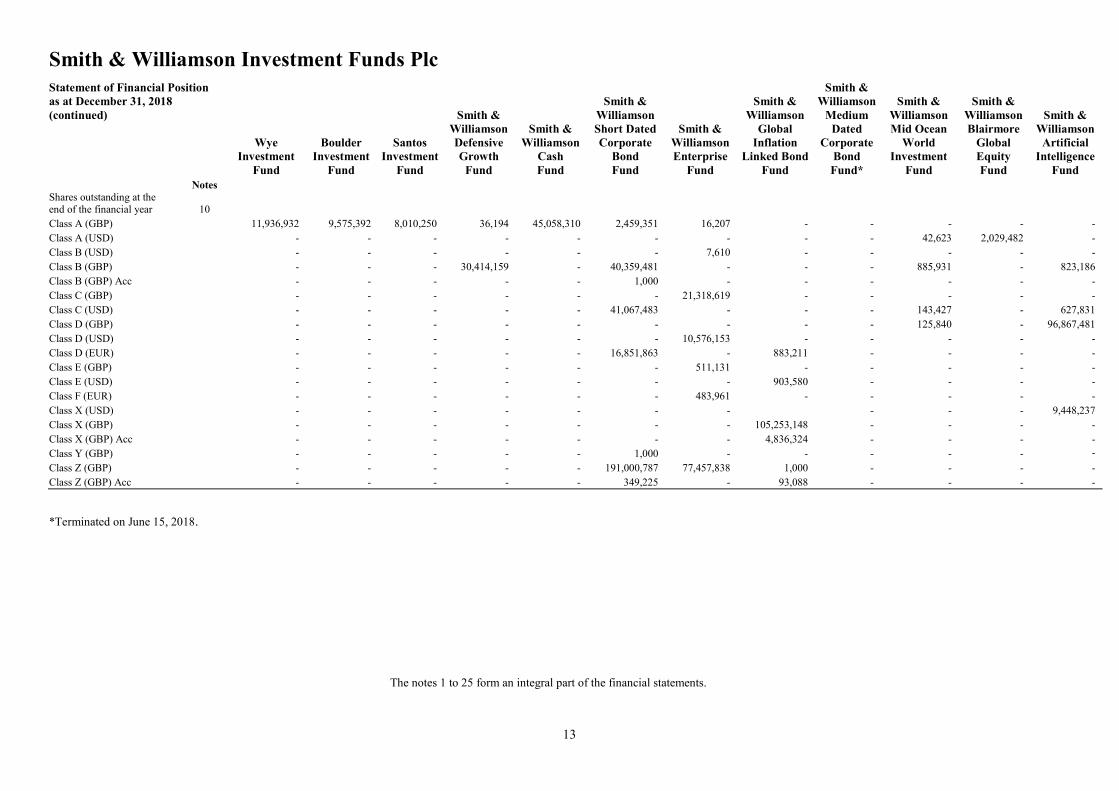

Statement of Financial Position

as at December 31, 2018

(continued)

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth

Fund

Smith &

Williamson

Cash

Fund

Smith &

Williamson

Short Dated

Corporate

Bond

Fund

Smith &

Williamson

Enterprise

Fund

Smith &

Williamson

Global

Inflation

Linked Bond

Fund

Smith &

Williamson

Medium

Dated

Corporate

Bond

Fund*

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity

Fund

Smith &

Williamson

Artificial

Intelligence

Fund

Notes Shares outstanding at the end of the financial year 10

Class A (GBP) 11,936,932 9,575,392 8,010,250 36,194 45,058,310 2,459,351 16,207 - - - - -

Class A (USD) - - - - - - - - - 42,623 2,029,482 -

Class B (USD) - - - - - - 7,610 - - - - -

Class B (GBP) - - - 30,414,159 - 40,359,481 - - - 885,931 - 823,186

Class B (GBP) Acc - - - - - 1,000 - - - - - -

Class C (GBP) - - - - - - 21,318,619 - - - - -

Class C (USD) - - - - - 41,067,483 - - - 143,427 - 627,831

Class D (GBP) - - - - - - - - - 125,840 - 96,867,481

Class D (USD) - - - - - - 10,576,153 - - - - -

Class D (EUR) - - - - - 16,851,863 - 883,211 - - - -

Class E (GBP) - - - - - - 511,131 - - - - -

Class E (USD) - - - - - - - 903,580 - - - -

Class F (EUR) - - - - - - 483,961 - - - - -

Class X (USD) - - - - - - - - - - 9,448,237

Class X (GBP) - - - - - - - 105,253,148 - - - -

Class X (GBP) Acc - - - - - - - 4,836,324 - - - -

Class Y (GBP) - - - - - 1,000 - - - - - -

Class Z (GBP) - - - - - 191,000,787 77,457,838 1,000 - - - -

Class Z (GBP) Acc - - - - - 349,225 - 93,088 - - - -

*Terminated on June 15, 2018.

The notes 1 to 25 form an integral part of the financial statements.

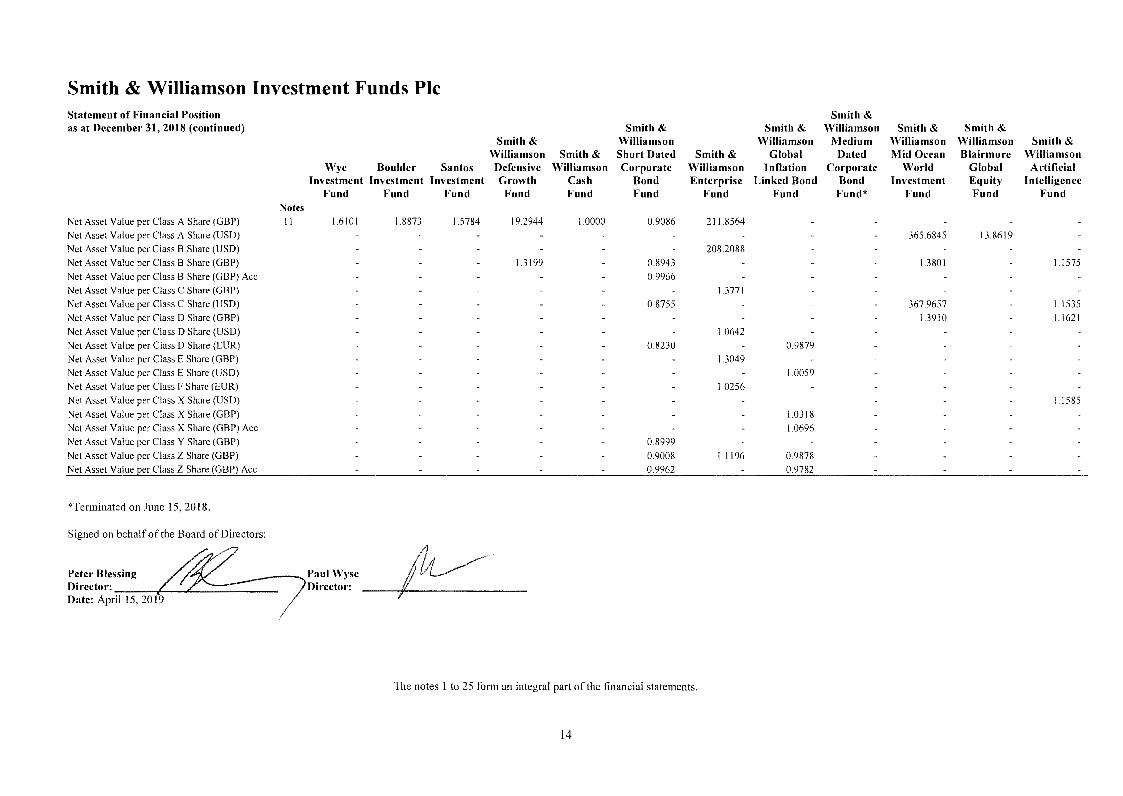

Smith & Williamson Investment Funds Pie Statement of Financial Position as at December 31, 2018 (continued)

Net Asset Value per Class A Share (GBP)

Net Asset Value per Class A Share (USD)

Net Asset Value per Class B Share (USD)

Net Asset Value per Class B Share (GBP)

Net Asset Value per Class B Share (GBP) Ace Net Asset Value per Class C Share (GBP)

Net Asset Value per Class C Share (USD)

Net Asset Value per Class D Share (GBP)

Net Asset Value per Class D Share (USD)

Net Asset Value per Class D Share (EUR)

Net Asset Value per Class E Share (GBP)

Net Asset Value per Class E Share (USD)

Net Asset Value per Class F Share (EUR)

Net Asset Value per Class X Share (USD)

Net Asset Value per Class X Share (GBP)

Net Asset Value per Class X Share (GBP) Ace

Net Asset Value per Class Y Share (GBP)

Net Asset Value per Class Z Share (GBP) Net Asset Value per Class Z Share (GBP) Ace

*Terminated on June 15. 2018.

Signed on behalf of the Board of Directors:

Notes 11

Wye Boulder Santos Investment Investment Investment

Fund Fund Fund

1.6101 1.8873 1.5784

Peter Blessing ----... Paul Wyse Director: ___ __,__________ Director: Date: April 15. 2019

Smith & Williamson Defensive Growth

Fund

19.2944

1.3199

Smith & Williamson

Cash Fund

1.0000

Smith & Williamson Short Dated Corporate

Bond Fund

0.9086

0.8943

0.9966

0.8755

0.8230

0.8999

0.9008 0.9962

Smith & Williamson Enterprise

Fund

211.8564

208.2088

1.3771

1.0642

13049

10256

I I !96

The notes 1 to 25 form an integral part of the financial statements.

14

Smith & Williamson

Global Inflation

Linked Bond Fund

0.9879

1.0059

10318

10696

0.9878 0.9782

Smith & Williamson

Medium Dated

Corporate Bond Fund*

Smith & Williamson Mid Ocean

World Investment

Fund

365.6845

13801

367.9657

13910

Smith & Williamson Blairmore

Global Equity Fund

13.8619

Smith & Williamson

Artificial Intelligence

Fund

1.1575

1 1535 l.1621

1585

Smith & Williamson Investment Funds Plc

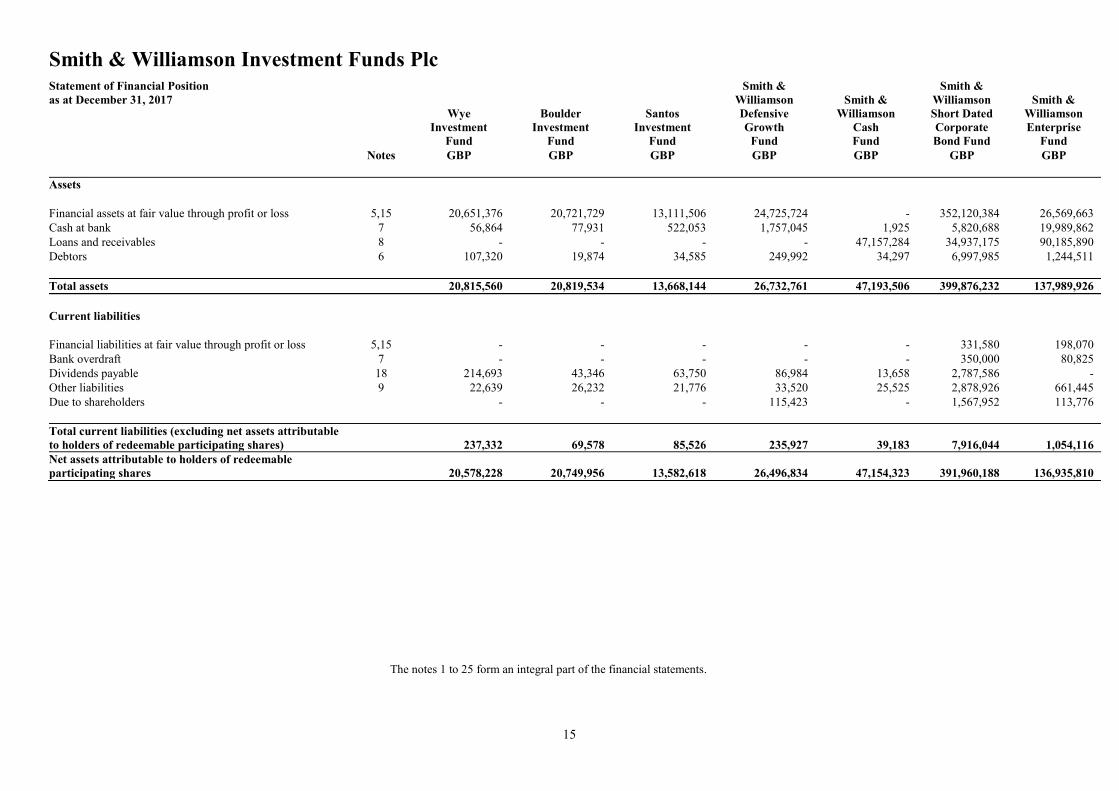

15

Statement of Financial Position

as at December 31, 2017

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth

Fund

Smith &

Williamson

Cash

Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

Notes GBP GBP GBP GBP GBP GBP GBP

Assets

Financial assets at fair value through profit or loss 5,15 20,651,376 20,721,729 13,111,506 24,725,724 - 352,120,384 26,569,663

Cash at bank 7 56,864 77,931 522,053 1,757,045 1,925 5,820,688 19,989,862

Loans and receivables 8 - - - - 47,157,284 34,937,175 90,185,890

Debtors 6 107,320 19,874 34,585 249,992 34,297 6,997,985 1,244,511

Total assets 20,815,560 20,819,534 13,668,144 26,732,761 47,193,506 399,876,232 137,989,926

Current liabilities

Financial liabilities at fair value through profit or loss 5,15 - - - - - 331,580 198,070

Bank overdraft 7 - - - - - 350,000 80,825

Dividends payable 18 214,693 43,346 63,750 86,984 13,658 2,787,586 -

Other liabilities 9 22,639 26,232 21,776 33,520 25,525 2,878,926 661,445

Due to shareholders - - - 115,423 - 1,567,952 113,776

Total current liabilities (excluding net assets attributable

to holders of redeemable participating shares) 237,332 69,578 85,526 235,927 39,183 7,916,044 1,054,116

Net assets attributable to holders of redeemable

participating shares 20,578,228 20,749,956 13,582,618 26,496,834 47,154,323 391,960,188 136,935,810

The notes 1 to 25 form an integral part of the financial statements.

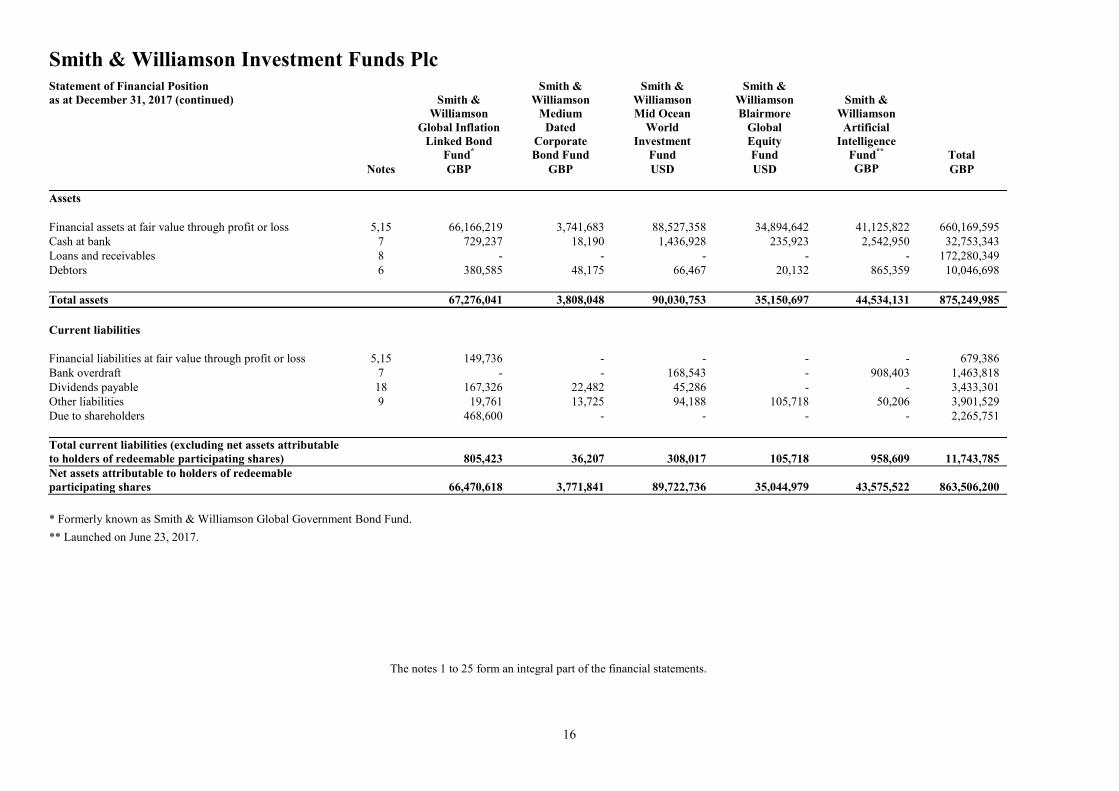

Smith & Williamson Investment Funds Plc

16

* Formerly known as Smith & Williamson Global Government Bond Fund.

** Launched on June 23, 2017.

The notes 1 to 25 form an integral part of the financial statements.

Statement of Financial Position

as at December 31, 2017 (continued)

Smith &

Williamson

Global Inflation

Linked Bond

Fund*

Smith &

Williamson

Medium

Dated

Corporate

Bond Fund

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity

Fund

Smith &

Williamson

Artificial

Intelligence

Fund** Total

Notes GBP GBP USD USD GBP GBP

Assets

Financial assets at fair value through profit or loss 5,15 66,166,219 3,741,683 88,527,358 34,894,642 41,125,822 660,169,595

Cash at bank 7 729,237 18,190 1,436,928 235,923 2,542,950 32,753,343

Loans and receivables 8 - - - - - 172,280,349

Debtors 6 380,585 48,175 66,467 20,132 865,359 10,046,698

Total assets 67,276,041 3,808,048 90,030,753 35,150,697 44,534,131 875,249,985

Current liabilities

Financial liabilities at fair value through profit or loss 5,15 149,736 - - - - 679,386

Bank overdraft 7 - - 168,543 - 908,403 1,463,818

Dividends payable 18 167,326 22,482 45,286 - - 3,433,301

Other liabilities 9 19,761 13,725 94,188 105,718 50,206 3,901,529

Due to shareholders 468,600 - - - - 2,265,751

Total current liabilities (excluding net assets attributable

to holders of redeemable participating shares) 805,423 36,207 308,017 105,718 958,609 11,743,785

Net assets attributable to holders of redeemable

participating shares 66,470,618 3,771,841 89,722,736 35,044,979 43,575,522 863,506,200

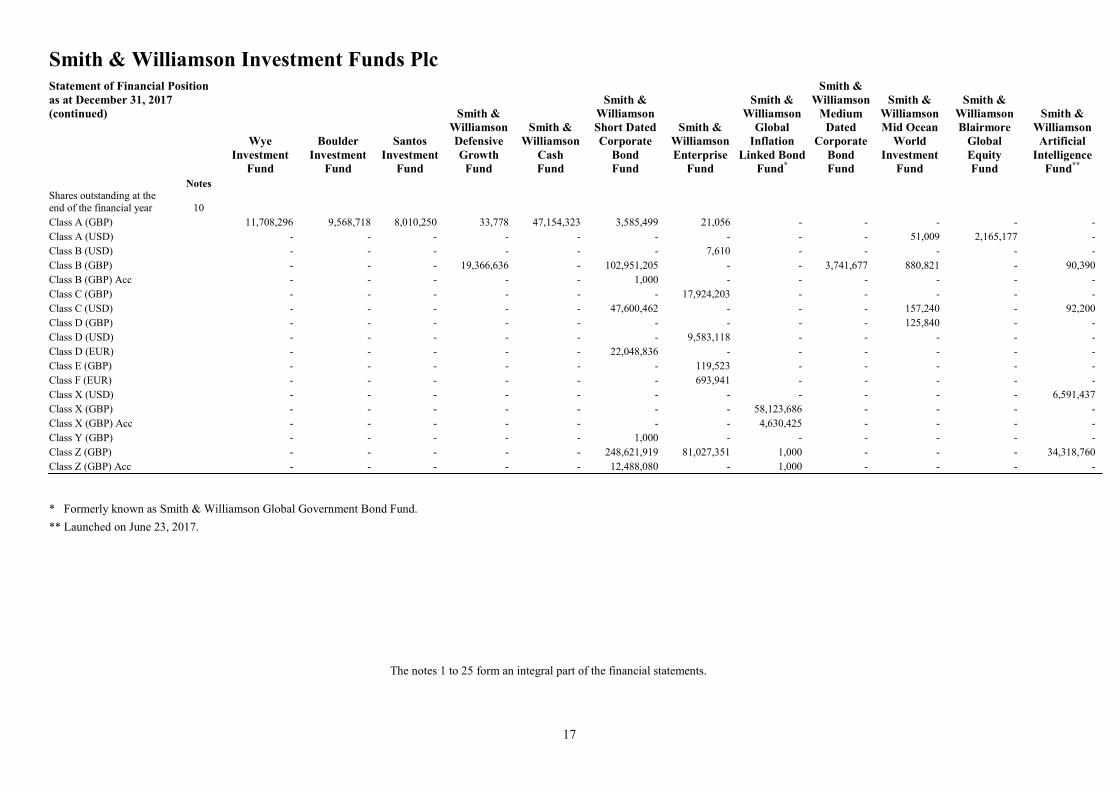

Smith & Williamson Investment Funds Plc

17

Statement of Financial Position

as at December 31, 2017

(continued)

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth

Fund

Smith &

Williamson

Cash

Fund

Smith &

Williamson

Short Dated

Corporate

Bond

Fund

Smith &

Williamson

Enterprise

Fund

Smith &

Williamson

Global

Inflation

Linked Bond

Fund*

Smith &

Williamson

Medium

Dated

Corporate

Bond

Fund

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity

Fund

Smith &

Williamson

Artificial

Intelligence

Fund**

Wye

Investment

Fund

Notes

Shares outstanding at the

end of the financial year 10

Class A (GBP) 11,708,296 9,568,718 8,010,250 33,778 47,154,323 3,585,499 21,056 - - - - -

Class A (USD) - - - - - - - - - 51,009 2,165,177 -

Class B (USD) - - - - - - 7,610 - - - - -

Class B (GBP) - - - 19,366,636 - 102,951,205 - - 3,741,677 880,821 - 90,390

Class B (GBP) Acc - - - - - 1,000 - - - - - -

Class C (GBP) - - - - - - 17,924,203 - - - - -

Class C (USD) - - - - - 47,600,462 - - - 157,240 - 92,200

Class D (GBP) - - - - - - - - - 125,840 - -

Class D (USD) - - - - - - 9,583,118 - - - - -

Class D (EUR) - - - - - 22,048,836 - - - - - -

Class E (GBP) - - - - - - 119,523 - - - - -

Class F (EUR) - - - - - - 693,941 - - - - -

Class X (USD) - - - - - - - - - - - 6,591,437

Class X (GBP) - - - - - - - 58,123,686 - - - -

Class X (GBP) Acc - - - - - - - 4,630,425 - - - -

Class Y (GBP) - - - - - 1,000 - - - - - -

Class Z (GBP) - - - - - 248,621,919 81,027,351 1,000 - - - 34,318,760

Class Z (GBP) Acc - - - - - 12,488,080 - 1,000 - - - -

* Formerly known as Smith & Williamson Global Government Bond Fund.

** Launched on June 23, 2017.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

18

Statement of Financial Position

as at December 31, 2017 (continued)

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth

Fund

Smith &

Williamson

Cash

Fund

Smith &

Williamson

Short Dated

Corporate

Bond

Fund

Smith &

Williamson

Enterprise

Fund

Smith &

Williamson

Global

Inflation

Linked Bond

Fund*

Smith &

Williamson

Medium

Dated

Corporate

Bond

Fund

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity

Fund

Smith &

Williamson

Artificial

Intelligence

Fund**

Notes

Net Asset Value per Class A Share (GBP) 11 1.7576 2.1685 1.6957 19.5027 1.0000 0.9421 225.7540 - - - - -

Net Asset Value per Class A Share (USD) - - - - - - - - - 419.4714 16.1857 -

Net Asset Value per Class B Share (USD) - - - - - - 218.3499 - - - - -

Net Asset Value per Class B Share (GBP) - - - 1.3342 - 0.9272 - - 1.0081 1.4905 - 1.0981

Net Asset Value per Class B Share (GBP) Acc - - - - - 1.0030 - - - - - -

Net Asset Value per Class C Share (GBP) - - - - - - 1.4587 - - - - -

Net Asset Value per Class C Share (USD) - - - - - 0.8941 - - - 421.6183 - 1.1624

Net Asset Value per Class D Share (GBP) - - - - - - - - - 1.4969 - -

Net Asset Value per Class D Share (USD) - - - - - - 1.1099 - - - - -

Net Asset Value per Class D Share (EUR) - - - - - 0.8637 - - - - - -

Net Asset Value per Class E Share (GBP) - - - - - - 1.3942 - - - - -

Net Asset Value per Class F Share (EUR) - - - - - - 1.0986 - - - - -

Net Asset Value per Class X Share (USD) - - - - - - - - - - - 1.1639

Net Asset Value per Class X Share (GBP) - - - - - - - 1.0570 - - - -

Net Asset Value per Class X Share (GBP) Acc - - - - - - - 1.0866 - - - -

Net Asset Value per Class Y Share (GBP) - - - - - 0.9335 - - - - - -

Net Asset Value per Class Z Share (GBP) - - - - - 0.9340 1.1860 1.0043 - - - 1.0993

Net Asset Value per Class Z Share (GBP) Acc - - - - - 1.0033 - 1.0021 - - - -

* Formerly known as Smith & Williamson Global Government Bond Fund.

** Launched on June 23, 2017.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

19

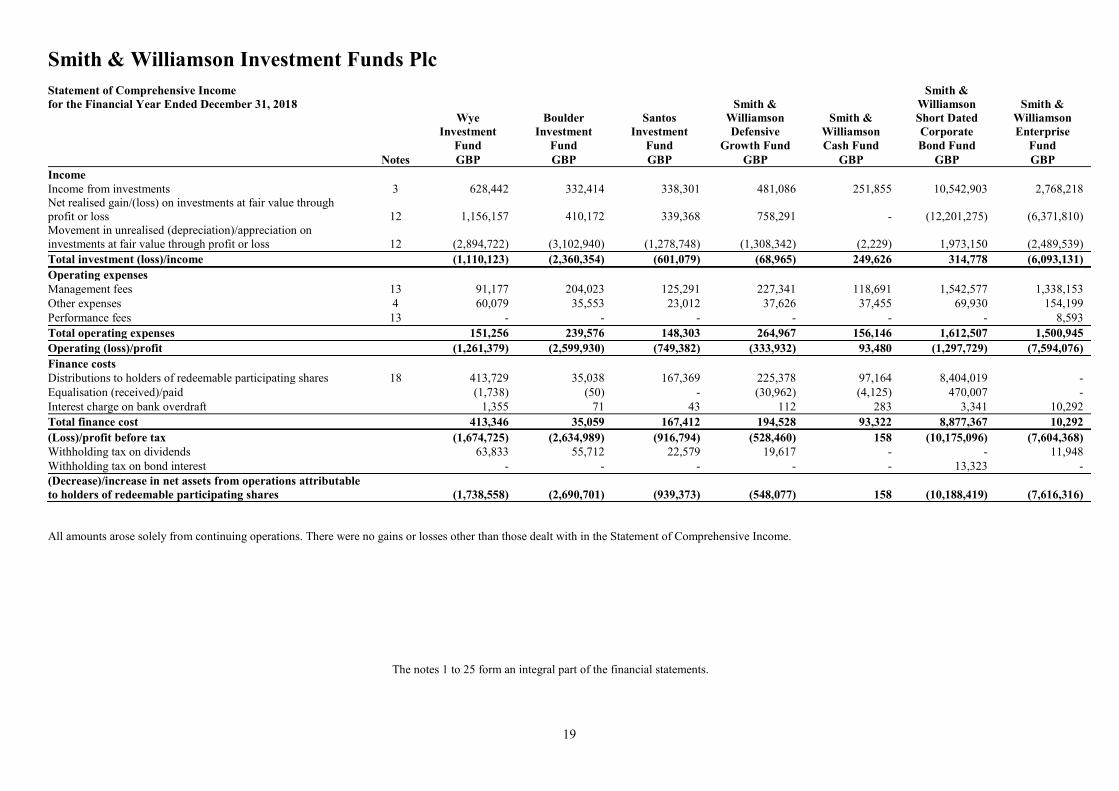

Statement of Comprehensive Income

for the Financial Year Ended December 31, 2018

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth Fund

Smith &

Williamson

Cash Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

Notes GBP GBP GBP GBP GBP GBP GBP

Income

Income from investments 3 628,442 332,414 338,301 481,086 251,855 10,542,903 2,768,218

Net realised gain/(loss) on investments at fair value through

profit or loss 12 1,156,157 410,172 339,368 758,291 - (12,201,275) (6,371,810)

Movement in unrealised (depreciation)/appreciation on

investments at fair value through profit or loss 12 (2,894,722) (3,102,940) (1,278,748) (1,308,342) (2,229) 1,973,150 (2,489,539)

Total investment (loss)/income (1,110,123) (2,360,354) (601,079) (68,965) 249,626 314,778 (6,093,131)

Operating expenses

Management fees 13 91,177 204,023 125,291 227,341 118,691 1,542,577 1,338,153

Other expenses 4 60,079 35,553 23,012 37,626 37,455 69,930 154,199

Performance fees 13 - - - - - - 8,593

Total operating expenses 151,256 239,576 148,303 264,967 156,146 1,612,507 1,500,945

Operating (loss)/profit (1,261,379) (2,599,930) (749,382) (333,932) 93,480 (1,297,729) (7,594,076)

Finance costs

Distributions to holders of redeemable participating shares 18 413,729 35,038 167,369 225,378 97,164 8,404,019 -

Equalisation (received)/paid (1,738) (50) - (30,962) (4,125) 470,007 -

Interest charge on bank overdraft 1,355 71 43 112 283 3,341 10,292

Total finance cost 413,346 35,059 167,412 194,528 93,322 8,877,367 10,292

(Loss)/profit before tax (1,674,725) (2,634,989) (916,794) (528,460) 158 (10,175,096) (7,604,368)

Withholding tax on dividends 63,833 55,712 22,579 19,617 - - 11,948

Withholding tax on bond interest - - - - - 13,323 -

(Decrease)/increase in net assets from operations attributable

to holders of redeemable participating shares (1,738,558) (2,690,701) (939,373) (548,077) 158 (10,188,419) (7,616,316)

All amounts arose solely from continuing operations. There were no gains or losses other than those dealt with in the Statement of Comprehensive Income.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

20

Statement of Comprehensive Income

for the Financial Year Ended December 31, 2018 (continued)

Smith &

Williamson

Global

Inflation

Linked Bond

Fund

Smith &

Williamson

Medium Dated

Corporate

Bond Fund*

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity Fund

Smith &

Williamson

Artificial

Intelligence

Fund

Cross

Investments Total

Notes GBP GBP USD USD GBP GBP GBP

Income

Income from investments 3 1,100,596 26,315 1,607,681 571,425 787,815 - 18,890,247

Net realised gain/(loss) on investments at fair value through

profit or loss 12 (3,311,999) (71,702) 5,626,592 2,684,989 2,138,749 - (10,928,095)

Movement in unrealised (depreciation)/appreciation on

investments at fair value through profit or loss 12 1,244,068 (45,493) (15,904,677) (7,476,761) (8,660,299) (325,901) (34,405,325)

Total investment (loss)/income (967,335) (90,880) (8,670,404) (4,220,347) (5,733,735) (325,901) (26,443,173)

Operating expenses

Management fees 13 241,456 5,694 768,169 332,982 485,280 - 5,204,522

Other expenses 4 26,914 24,780 124,948 67,119 175,718 - 789,135

Performance fees 13 - - - - - - 8,593

Total operating expenses 268,370 30,474 893,117 400,101 660,998 - 6,002,250

Operating (loss)/profit (1,235,705) (121,354) (9,563,521) (4,620,448) (6,394,733) (325,901) (32,445,423)

Finance costs

Distributions to holders of redeemable participating shares 18 869,041 429 392,816 - - - 10,506,414

Equalisation (received)/paid (101,443) 1,055 7,201 2,530 (813) - 339,220

Interest charge on bank overdraft 6,732 19 4,843 - 6,813 - 32,689

Total finance cost 774,330 1,503 404,860 2,530 6,000 - 10,878,323

(Loss)/profit before tax (2,010,035) (122,857) (9,968,381) (4,622,978) (6,400,733) (325,901) (43,323,746)

Withholding tax on dividends - 332,584 87,729 137,421 625,954

Withholding tax on bond interest - - - - - 13,323

(Decrease)/increase in net assets from operations attributable

to holders of redeemable participating shares (2,010,035) (122,857) (10,300,965) (4,710,707) (6,538,154) (325,901) (43,963,023)

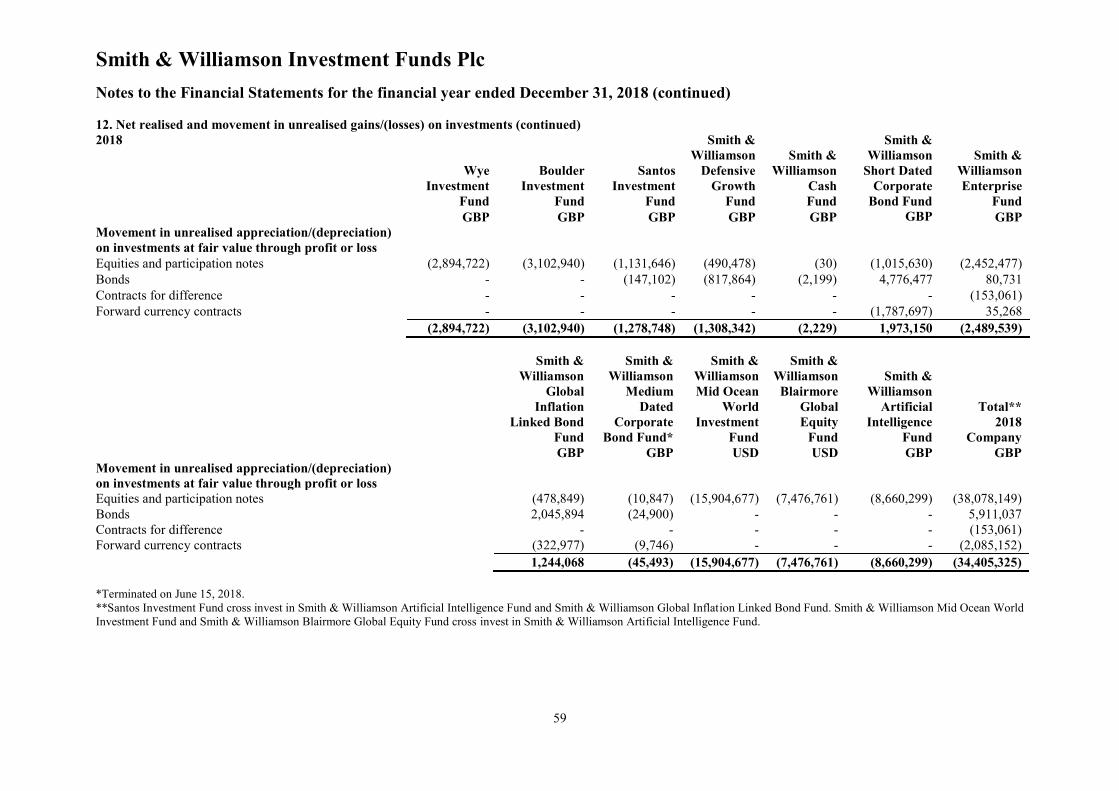

*Terminated on June 15, 2018.

All amounts arose solely from continuing operations. There were no gains or losses other than those dealt with in the Statement of Comprehensive Income.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

21

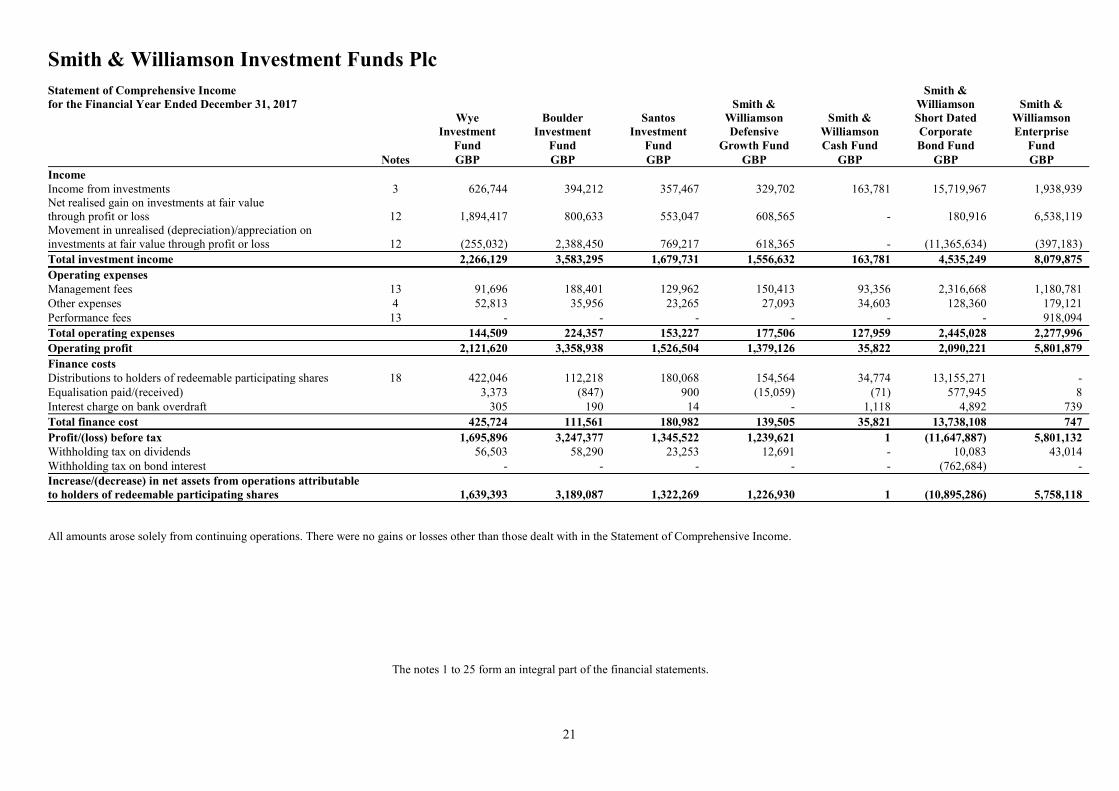

Statement of Comprehensive Income

for the Financial Year Ended December 31, 2017

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth Fund

Smith &

Williamson

Cash Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

Notes GBP GBP GBP GBP GBP GBP GBP

Income

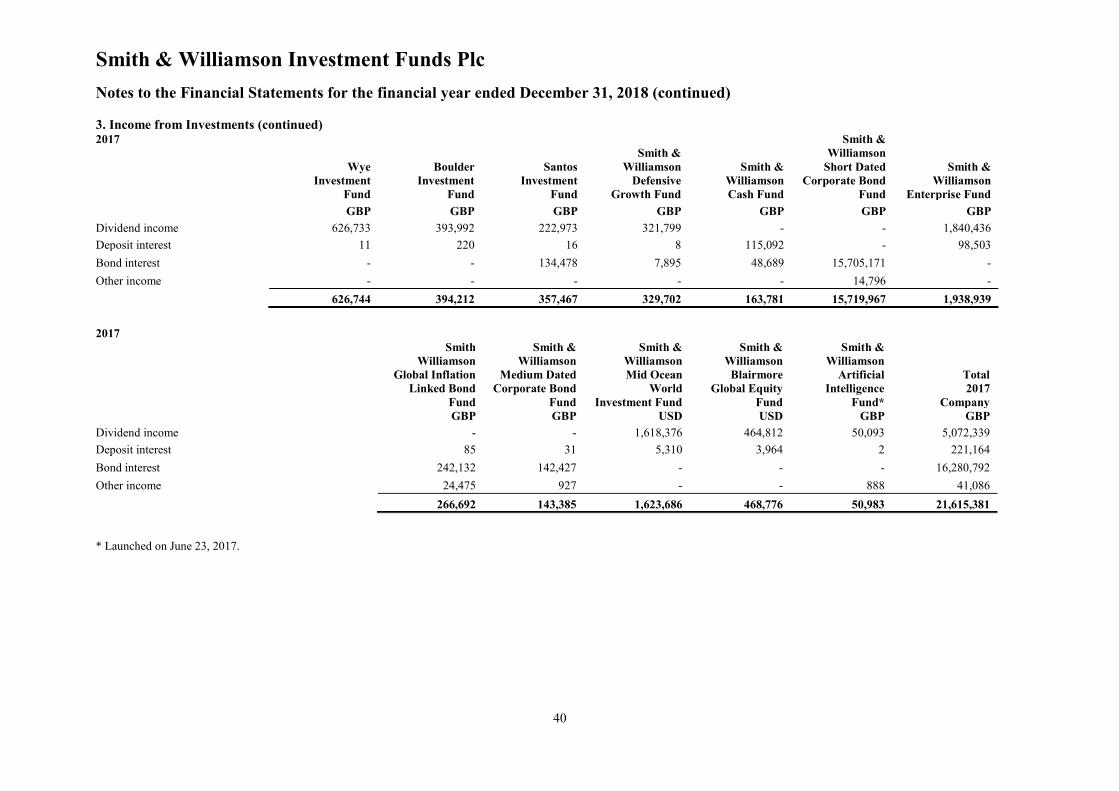

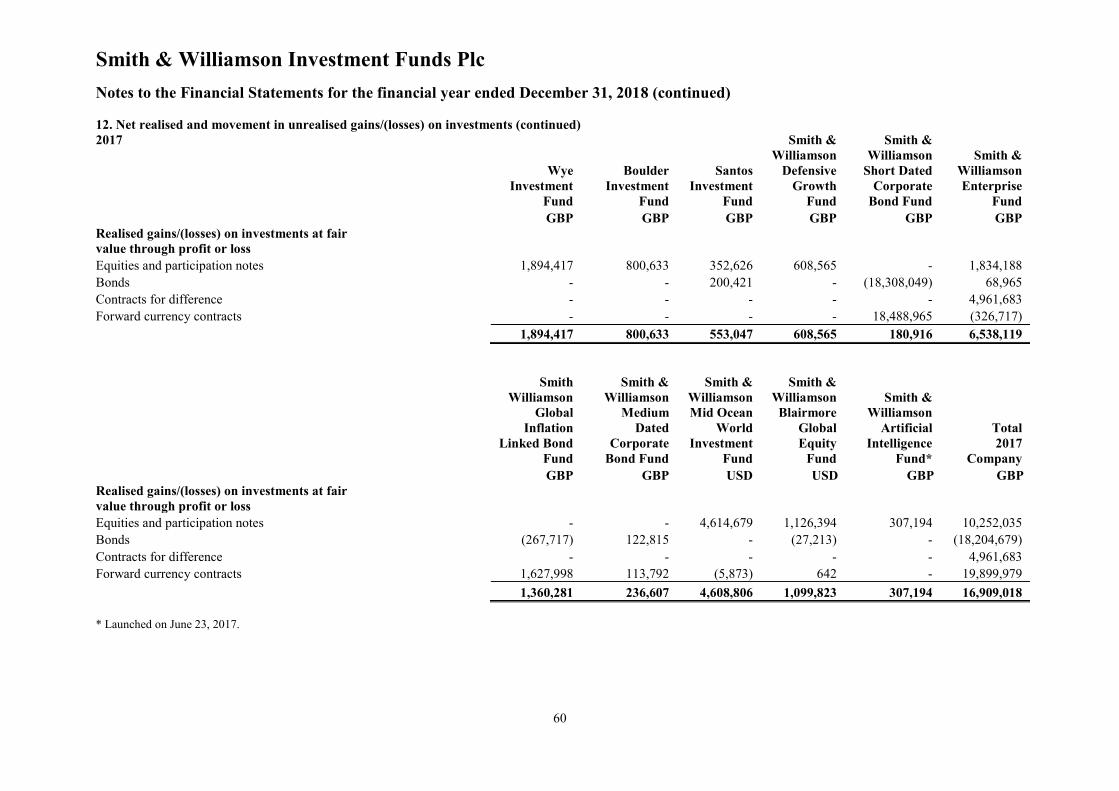

Income from investments 3 626,744 394,212 357,467 329,702 163,781 15,719,967 1,938,939

Net realised gain on investments at fair value

through profit or loss 12 1,894,417 800,633 553,047 608,565 - 180,916 6,538,119

Movement in unrealised (depreciation)/appreciation on

investments at fair value through profit or loss 12 (255,032) 2,388,450 769,217 618,365 - (11,365,634) (397,183)

Total investment income 2,266,129 3,583,295 1,679,731 1,556,632 163,781 4,535,249 8,079,875

Operating expenses

Management fees 13 91,696 188,401 129,962 150,413 93,356 2,316,668 1,180,781

Other expenses 4 52,813 35,956 23,265 27,093 34,603 128,360 179,121

Performance fees 13 - - - - - - 918,094

Total operating expenses 144,509 224,357 153,227 177,506 127,959 2,445,028 2,277,996

Operating profit 2,121,620 3,358,938 1,526,504 1,379,126 35,822 2,090,221 5,801,879

Finance costs

Distributions to holders of redeemable participating shares 18 422,046 112,218 180,068 154,564 34,774 13,155,271 -

Equalisation paid/(received) 3,373 (847) 900 (15,059) (71) 577,945 8

Interest charge on bank overdraft 305 190 14 - 1,118 4,892 739

Total finance cost 425,724 111,561 180,982 139,505 35,821 13,738,108 747

Profit/(loss) before tax 1,695,896 3,247,377 1,345,522 1,239,621 1 (11,647,887) 5,801,132

Withholding tax on dividends 56,503 58,290 23,253 12,691 - 10,083 43,014

Withholding tax on bond interest - - - - - (762,684) -

Increase/(decrease) in net assets from operations attributable

to holders of redeemable participating shares 1,639,393 3,189,087 1,322,269 1,226,930 1 (10,895,286) 5,758,118

All amounts arose solely from continuing operations. There were no gains or losses other than those dealt with in the Statement of Comprehensive Income.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

22

Statement of Comprehensive Income

for the Financial Year Ended December 31, 2017 (continued)

Smith &

Williamson

Global Inflation

Linked Bond

Fund*

Smith &

Williamson

Medium Dated

Corporate Bond

Fund

Smith &

Williamson Mid

Ocean World

Investment

Fund

Smith &

Williamson

Blairmore

Global Equity

Fund

Smith &

Williamson

Artificial

Intelligence

Fund** Total

Notes GBP GBP USD USD GBP GBP

Income

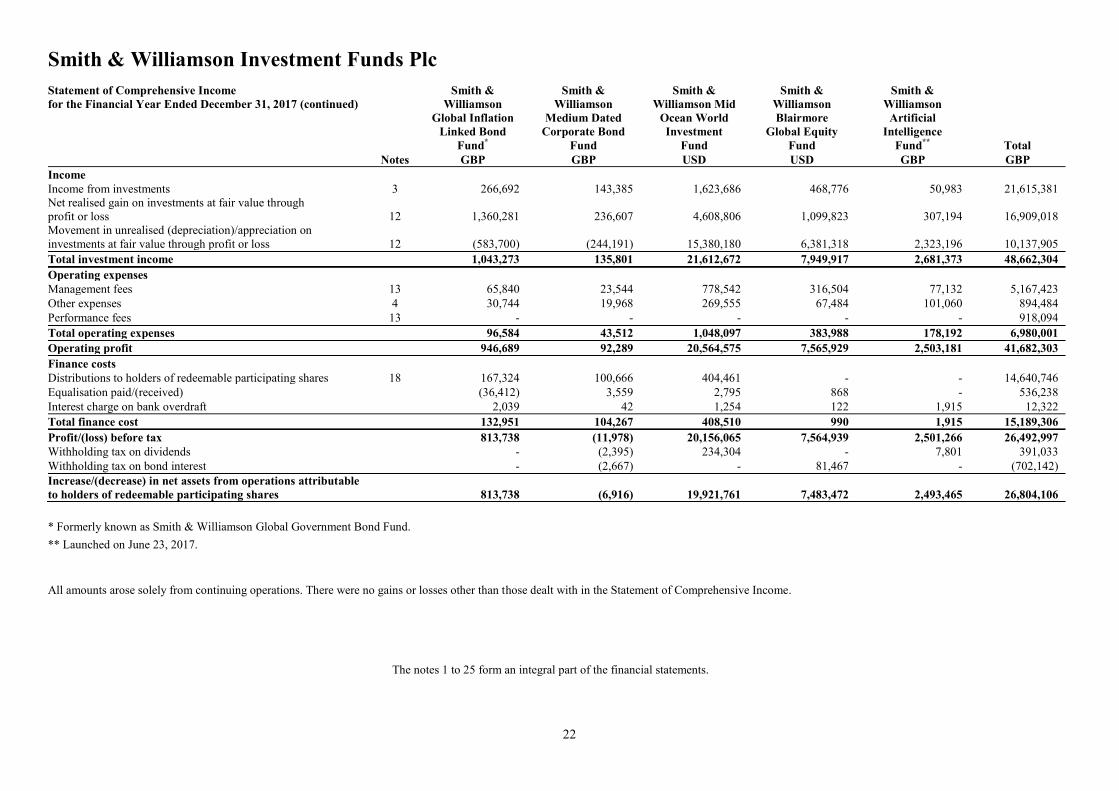

Income from investments 3 266,692 143,385 1,623,686 468,776 50,983 21,615,381

Net realised gain on investments at fair value through

profit or loss 12 1,360,281 236,607 4,608,806 1,099,823 307,194 16,909,018

Movement in unrealised (depreciation)/appreciation on

investments at fair value through profit or loss 12 (583,700) (244,191) 15,380,180 6,381,318 2,323,196 10,137,905

Total investment income 1,043,273 135,801 21,612,672 7,949,917 2,681,373 48,662,304

Operating expenses

Management fees 13 65,840 23,544 778,542 316,504 77,132 5,167,423

Other expenses 4 30,744 19,968 269,555 67,484 101,060 894,484

Performance fees 13 - - - - - 918,094

Total operating expenses 96,584 43,512 1,048,097 383,988 178,192 6,980,001

Operating profit 946,689 92,289 20,564,575 7,565,929 2,503,181 41,682,303

Finance costs

Distributions to holders of redeemable participating shares 18 167,324 100,666 404,461 - - 14,640,746

Equalisation paid/(received) (36,412) 3,559 2,795 868 - 536,238

Interest charge on bank overdraft 2,039 42 1,254 122 1,915 12,322

Total finance cost 132,951 104,267 408,510 990 1,915 15,189,306

Profit/(loss) before tax 813,738 (11,978) 20,156,065 7,564,939 2,501,266 26,492,997

Withholding tax on dividends - (2,395) 234,304 - 7,801 391,033

Withholding tax on bond interest - (2,667) - 81,467 - (702,142)

Increase/(decrease) in net assets from operations attributable

to holders of redeemable participating shares 813,738 (6,916) 19,921,761 7,483,472 2,493,465 26,804,106

* Formerly known as Smith & Williamson Global Government Bond Fund.

** Launched on June 23, 2017.

All amounts arose solely from continuing operations. There were no gains or losses other than those dealt with in the Statement of Comprehensive Income.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

23

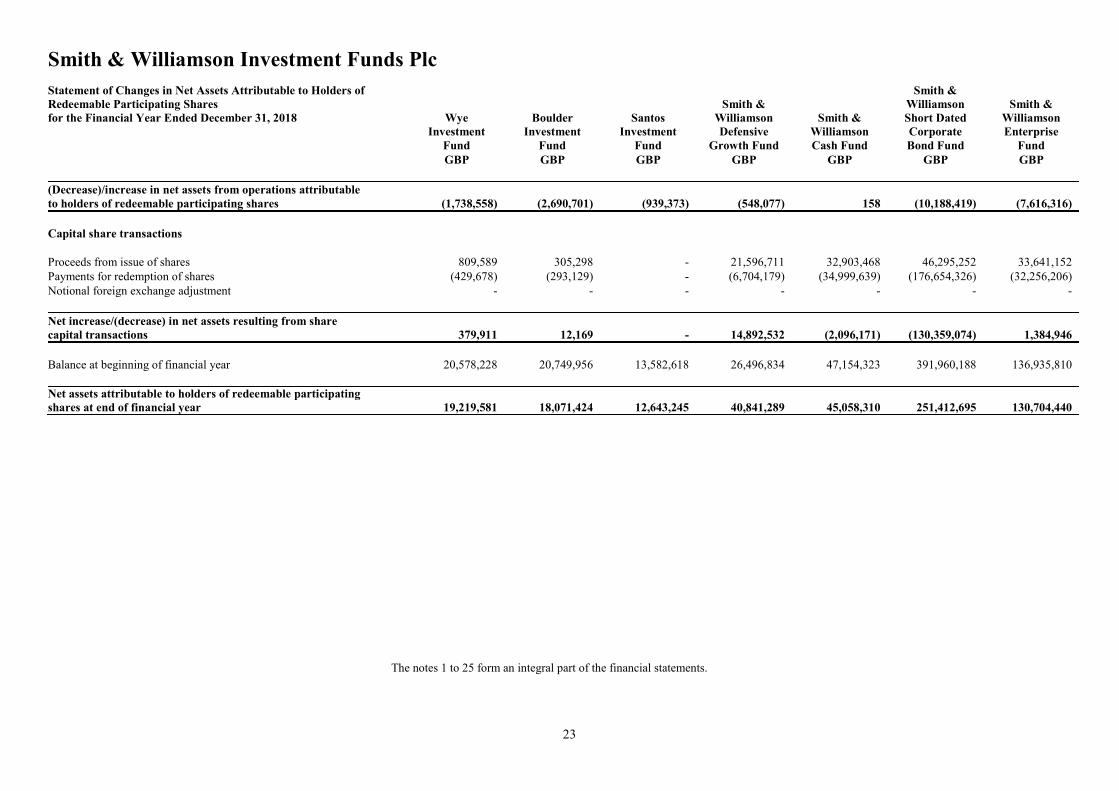

Statement of Changes in Net Assets Attributable to Holders of

Redeemable Participating Shares

for the Financial Year Ended December 31, 2018

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth Fund

Smith &

Williamson

Cash Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

GBP GBP GBP GBP GBP GBP GBP

(Decrease)/increase in net assets from operations attributable

to holders of redeemable participating shares

(1,738,558) (2,690,701) (939,373) (548,077) 158 (10,188,419) (7,616,316)

Capital share transactions

Proceeds from issue of shares 809,589 305,298 - 21,596,711 32,903,468 46,295,252 33,641,152

Payments for redemption of shares (429,678) (293,129) - (6,704,179) (34,999,639) (176,654,326) (32,256,206)

Notional foreign exchange adjustment - - - - - - -

Net increase/(decrease) in net assets resulting from share

capital transactions

379,911 12,169 - 14,892,532 (2,096,171) (130,359,074) 1,384,946

Balance at beginning of financial year 20,578,228 20,749,956 13,582,618 26,496,834 47,154,323 391,960,188 136,935,810

Net assets attributable to holders of redeemable participating

shares at end of financial year 19,219,581 18,071,424 12,643,245 40,841,289 45,058,310 251,412,695 130,704,440

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

24

Statement of Changes in Net Assets Attributable to Holders of

Redeemable Participating Shares

for the Financial Year Ended December 31, 2018 (continued)

Smith &

Williamson

Global

Inflation

Linked Bond

Fund

Smith &

Williamson

Medium Dated

Corporate

Bond Fund*

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity Fund

Smith &

Williamson

Artificial

Intelligence

Fund

Cross

Investments Total

GBP GBP USD USD GBP GBP GBP

(Decrease)/increase in net assets from operations attributable

to holders of redeemable participating shares

(2,010,035) (122,857) (10,300,965) (4,710,707) (6,538,154) (325,901) (43,963,023)

Capital share transactions

Proceeds from issue of shares 57,380,470 14,264 89,633 2,254 101,150,185 (2,861,809) 291,303,409

Payments for redemption of shares (6,478,574) (3,663,248) (9,368,466) (2,204,078) (15,498,389) - (285,646,011)

Notional foreign exchange adjustment - - - - - (113,240) 4,662,505

Net increase/(decrease) in net assets resulting from share

capital transactions

50,901,896 (3,648,984) (9,278,833) (2,201,824) 85,651,796

10,319,903 (2,975,049)

Balance at beginning of financial year 66,470,618 3,771,841 89,722,736 35,044,979 43,575,522 - 863,506,200

Net assets attributable to holders of redeemable participating

shares at end of financial year 115,362,479 - 70,142,938 28,132,448 122,689,164 (3,300,950) 829,863,080

*Terminated on June 15, 2018.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

25

Statement of Changes in Net Assets Attributable to Holders of

Redeemable Participating Shares

for the Financial Year Ended December 31, 2017

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth

Fund

Smith &

Williamson

Cash Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

GBP GBP GBP GBP GBP GBP GBP

Increase/(decrease) in net assets from operations attributable

to holders of redeemable participating shares

1,639,393 3,189,087 1,322,269 1,226,930 1 (10,895,286) 5,758,118

Capital share transactions

Proceeds from issue of shares 563,361 912,773 - 9,561,051 34,678,592 162,731,491 41,070,510

Payments for redemption of shares (1,172,187) (202,638) (303,660) (2,244,922) (37,819,166) (272,387,110) (36,207,593)

Notional foreign exchange adjustment - - - - - - -

Net (decrease)/increase in net assets

resulting from share capital transactions

(608,826) 710,135 (303,660) 7,316,129 (3,140,574) (109,655,619) 4,862,917

Balance at beginning of financial year 19,547,661 16,850,734 12,564,009 17,953,775 50,294,896 512,511,093 126,314,775

Net assets attributable to holders of redeemable participating

shares at end of financial year 20,578,228 20,749,956 13,582,618 26,496,834 47,154,323 391,960,188 136,935,810

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

26

Statement of Changes in Net Assets Attributable to Holders of

Redeemable Participating Shares

for the Financial Year Ended December 31, 2017 (continued)

Smith &

Williamson

Global Inflation

Linked Bond

Fund*

Smith &

Williamson

Medium Dated

Corporate

Bond Fund

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity

Fund

Smith &

Williamson

Artificial

Intelligence

Fund** Total

GBP GBP USD USD GBP GBP

Increase/(decrease) in net assets from operations attributable

to holders of redeemable participating shares

813,738 (6,916) 19,921,761 7,483,472 2,493,465 26,804,106

Capital share transactions

Proceeds from issue of shares 64,961,157 93,467 59,687,737 20,938 41,591,037 402,490,496

Payments for redemption of shares (1,231,812) (1,174,053) (72,408,790) (2,352,802) (508,980) (411,258,509)

Notional foreign exchange adjustment - - - - - (8,330,519)

Net (decrease)/increase in net assets resulting from share

capital transactions

63,729,345 (1,080,586) (12,721,053) (2,331,864) 41,082,057 (17,098,532)

Balance at beginning of financial year 1,927,535 4,859,343 82,522,028 29,893,371 - 853,800,626

Net assets attributable to holders of redeemable participating

shares at end of financial year 66,470,618 3,771,841 89,722,736 35,044,979 43,575,522 863,506,200

* Formerly known as Smith & Williamson Global Government Bond Fund.

** Launched on June 23, 2017.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

27

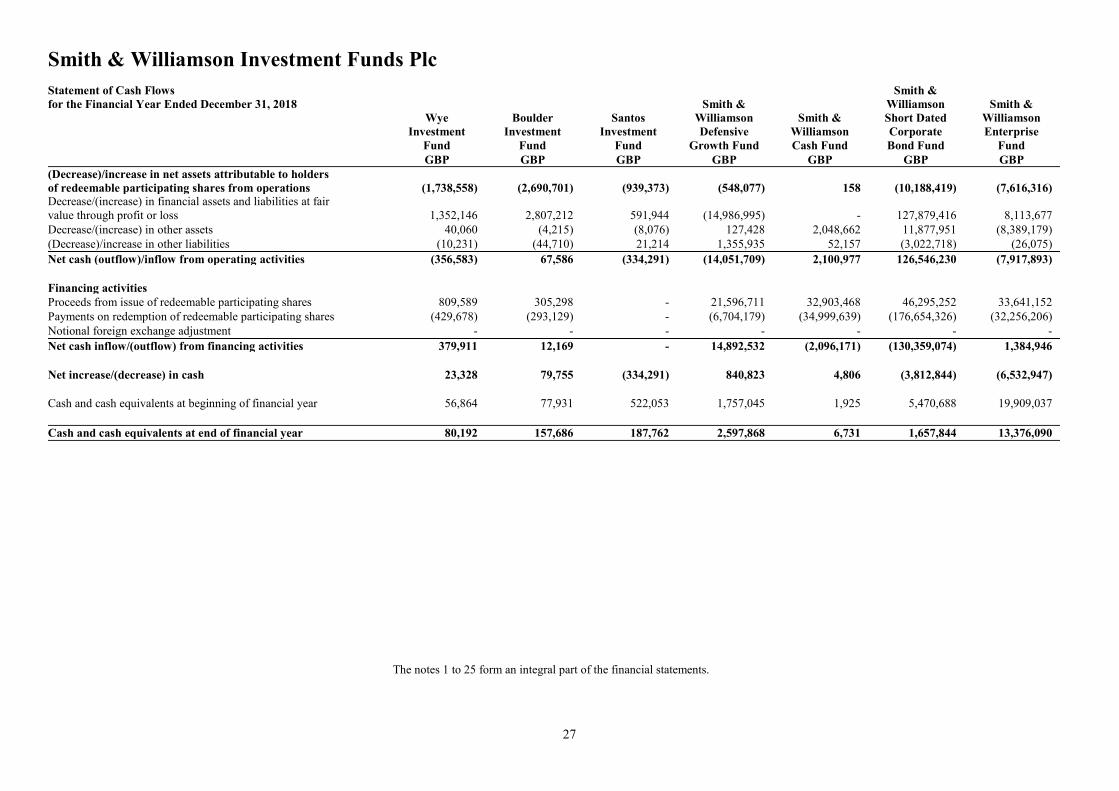

Statement of Cash Flows

for the Financial Year Ended December 31, 2018

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth Fund

Smith &

Williamson

Cash Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

GBP GBP GBP GBP GBP GBP GBP

(Decrease)/increase in net assets attributable to holders

of redeemable participating shares from operations (1,738,558) (2,690,701) (939,373) (548,077) 158 (10,188,419) (7,616,316)

Decrease/(increase) in financial assets and liabilities at fair

value through profit or loss 1,352,146 2,807,212 591,944 (14,986,995) - 127,879,416 8,113,677

Decrease/(increase) in other assets 40,060 (4,215) (8,076) 127,428 2,048,662 11,877,951 (8,389,179)

(Decrease)/increase in other liabilities (10,231) (44,710) 21,214 1,355,935 52,157 (3,022,718) (26,075)

Net cash (outflow)/inflow from operating activities (356,583) 67,586 (334,291) (14,051,709) 2,100,977 126,546,230 (7,917,893)

Financing activities

Proceeds from issue of redeemable participating shares 809,589 305,298 - 21,596,711 32,903,468 46,295,252 33,641,152

Payments on redemption of redeemable participating shares (429,678) (293,129) - (6,704,179) (34,999,639) (176,654,326) (32,256,206)

Notional foreign exchange adjustment - - - - - - -

Net cash inflow/(outflow) from financing activities 379,911 12,169 - 14,892,532 (2,096,171) (130,359,074) 1,384,946

Net increase/(decrease) in cash 23,328 79,755 (334,291) 840,823 4,806 (3,812,844) (6,532,947)

Cash and cash equivalents at beginning of financial year 56,864 77,931 522,053 1,757,045 1,925 5,470,688 19,909,037

Cash and cash equivalents at end of financial year 80,192 157,686 187,762 2,597,868 6,731 1,657,844 13,376,090

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

28

Statement of Cash Flows

for the Financial Year Ended December 31, 2018 (continued)

Smith &

Williamson

Global

Inflation

Linked Bond

Fund

Smith &

Williamson

Medium Dated

Corporate

Bond Fund*

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity Fund

Smith &

Williamson

Artificial

Intelligence

Fund

Cross

Investments Total

GBP GBP USD USD GBP GBP GBP

(Decrease)/increase in net assets attributable to holders

of redeemable participating shares from operations (2,010,035) (122,857) (10,300,965) (4,710,707) (6,538,154) (325,901) (43,963,023)

Decrease/(increase) in financial assets and liabilities at fair

value through profit or loss (47,144,570) 3,741,683 21,479,319 7,986,988 (73,020,313) 3,300,950 30,100,864

Decrease/(increase) in other assets (143,030) 48,166 14,853 (10,019) 539,029 - 6,136,613

(Decrease)/increase in other liabilities (78,287) (15,608) 86,629 (59,175) 691,510 - (1,043,994)

Net cash (outflow)/inflow from operating activities (49,375,922) 3,651,384 11,279,836 3,207,087 (78,327,928) 2,975,049 (8,769,540)

Financing activities

Proceeds from issue of redeemable participating shares 57,380,470 14,264 89,633 2,254 101,150,185 (2,861,809) 291,303,409

Payments on redemption of redeemable participating shares (6,478,574) (3,663,248) (9,368,466) (2,204,078) (15,498,389) - (285,646,011)

Notional foreign exchange adjustment - - - - - (113,240) 4,662,505

Net cash inflow/(outflow) from financing activities 50,901,896 (3,648,984) (9,278,833) (2,201,824) 85,651,796 (2,975,049) 10,319,903

Net increase/(decrease) in cash 1,525,974 2,400 2,001,003 1,005,263 7,323,868 - 1,550,363

Cash and cash equivalents at beginning of financial year 729,237 18,190 1,268,385 235,923 1,634,547 - 31,289,525

Cash and cash equivalents at end of financial year 2,255,211 20,590 3,269,388 1,241,186 8,958,415 - 32,839,888

*Terminated on June 15, 2018.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

29

Statement of Cash Flows

for the Financial Year Ended December 31, 2017

Wye

Investment

Fund

Boulder

Investment

Fund

Santos

Investment

Fund

Smith &

Williamson

Defensive

Growth

Fund

Smith &

Williamson

Cash

Fund

Smith &

Williamson

Short Dated

Corporate

Bond Fund

Smith &

Williamson

Enterprise

Fund

GBP GBP GBP GBP GBP GBP GBP

Increase/(decrease) in net assets attributable to holders

of redeemable participating shares from operations

1,639,393 3,189,087 1,322,269 1,226,930 1 (10,895,286) 5,758,118

(Increase)/decrease in financial assets and liabilities at fair

value through profit or loss

(986,300) (3,833,125) (648,730) (7,941,230) - 110,945,753 (10,294,640)

(Increase)/decrease in other assets (54,042) 24,623 32,176 (218,628) 3,160,367 (19,435,791) (6,803,694)

Increase/(decrease) in other liabilities 30,825 (45,873) (28,602) 111,591 (18,748) 1,771,682 59,464

Net cash inflow/(outflow) from operating activities 629,876 (665,288) 677,113 (6,821,337) 3,141,620 82,386,358 (11,280,752)

Financing activities

Proceeds from issue of redeemable participating shares 563,361 912,773 - 9,561,051 34,678,592 162,731,491 41,070,510

Payments on redemption of redeemable participating shares (1,172,187) (202,638) (303,660) (2,244,922) (37,819,166) (272,387,110) (36,207,593)

Notional foreign exchange adjustment - - - - - - -

Net cash (outflow)/inflow from financing activities (608,826) 710,135 (303,660) 7,316,129 (3,140,574) (109,655,619) 4,862,917

Net increase/(decrease) in cash 21,050 44,847 373,453 494,792 1,046 (27,269,261) (6,417,835)

Cash and cash equivalents at beginning of financial year 35,814 33,084 148,600 1,262,253 879 32,739,949 26,326,872

Cash and cash equivalents at end of financial year 56,864 77,931 522,053 1,757,045 1,925 5,470,688 19,909,037

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

30

Statement of Cash Flows

for the Financial Year Ended December 31, 2017 (continued)

Smith &

Williamson

Global Inflation

Linked Bond

Fund*

Smith &

Williamson

Medium Dated

Corporate Bond

Fund

Smith &

Williamson

Mid Ocean

World

Investment

Fund

Smith &

Williamson

Blairmore

Global

Equity Fund

Smith &

Williamson

Artificial

Intelligence

Fund** Total

GBP GBP USD USD GBP GBP

Increase/(decrease) in net assets attributable to holders of

redeemable participating shares from operations 813,738 (6,916) 19,921,761 7,483,472 2,493,465 26,804,106

(Increase)/decrease in financial assets and liabilities at fair value

through profit or loss (64,166,316) 805,106 (7,086,446) (6,056,105) (41,125,822) (19,232,594)

(Increase)/decrease in other assets (374,770) 12,526 178,463 7,994 (865,359) (24,365,625)

Increase/(decrease) in other liabilities 645,584 (7,809) (1,187,526) 47,295 50,206 1,628,359

Net cash inflow/(outflow) from operating activities (63,081,764) 802,907 11,826,252 1,482,656 (39,447,510) (15,165,754)

Financing activities

Proceeds from issue of redeemable participating shares 64,961,157 93,467 59,687,737 20,938 41,591,037 402,490,496

Payments on redemption of redeemable participating shares (1,231,812) (1,174,053) (72,408,790) (2,352,802) (508,980) (411,258,509)

Notional foreign exchange adjustment - - - - - (8,330,519)

Net cash (outflow)/inflow from financing activities 63,729,345 (1,080,586) (12,721,053) (2,331,864) 41,082,057 (17,098,532)

Net increase/(decrease) in cash 647,581 (277,679) (894,801) (849,208) 1,634,547 (32,264,286)

Cash and cash equivalents at beginning of financial year 81,656 295,869 2,163,186 1,085,131 - 63,553,811

Cash and cash equivalents at end of financial year 729,237 18,190 1,268,385 235,923 1,634,547 31,289,525

* Formerly known as Smith & Williamson Global Government Bond Fund.

** Launched on June 23, 2017.

The notes 1 to 25 form an integral part of the financial statements.

Smith & Williamson Investment Funds Plc

31

Notes to the Financial Statements for the financial year ended December 31, 2018

1. Company background

Smith & Williamson Investment Funds Plc (the “Company”) is an authorised umbrella fund with segregated liability

between sub-funds pursuant to the Regulations. The Company was incorporated on November 30, 1999 as an open-

ended investment company with variable capital under the Regulations. The Company began trading on March 31,

2000.

The investment objective of Wye Investment Fund, Boulder Investment Fund and Santos Investment Fund is to achieve long term growth of capital through investment in stocks (which may include fixed interest stocks), shares, collective investment schemes and investment trust companies in the UK and overseas stock markets, and through investment in cash and money market instruments throughout the world.

The investment objective of Smith & Williamson Defensive Growth Fund is to achieve long-term steady capital growth by adopting a policy to normally invest at least 50% of the assets in zero dividend preference shares (zeros), which are a class of share issued by Split Capital Investment Trusts, and synthetic zeros (closed-ended investment companies listed on Recognised Markets that display the same characteristics as conventional zeros). The sub-fund may also invest in other transferable securities, money market instruments, deposits, collective investment schemes and warrants.

The investment objective of Smith & Williamson Cash Fund and Smith & Williamson Short Dated Corporate Bond Fund is to achieve a high rate of interest and ready access to capital.

The investment objective of Smith & Williamson Enterprise Fund is to achieve long term capital appreciation with low risk and low volatility. The investment objective of Smith & Williamson Global Inflation Linked Bond Fund is to achieve total returns in excess of the sub-funds benchmark, the FTSE Actuaries Government Securities UK Gilts All Stocks Index, by investing the majority of its Net Asset Value in debt securities.

The investment objective of Smith & Williamson Medium Dated Corporate Bond Fund is to achieve income returns and ready access to capital by investing the majority of its Net Asset Value in a variety of Sterling, US Dollar and Euro medium-dated investment grade corporate bonds. This Fund closed on June 15, 2018.

The investment objective of Smith & Williamson Mid Ocean World Investment Fund is investing the majority of its Net Asset Value in equity and equity-related securities and debt securities.

The investment objective of the Smith & Williamson Blairmore Global Equity Fund is to achieve capital appreciation through investment in an actively managed long-only portfolio consisting primarily of global equities.

The investment objective of the Smith & Williamson Artificial Intelligence Fund is to achieve capital appreciation through investing primarily in equity and equity-related securities issued by companies.

The following table provides the date of commencement of trading and closing for the various sub-funds established by the Company (the “sub-funds”):

Date of Trading Closure Date

Wye Investment Fund May 24, 2000

Boulder Investment Fund October 19, 2000

Santos Investment Fund July 2, 2002

Smith & Williamson Defensive Growth Fund September 28, 2004

Smith & Williamson Cash Fund March 18, 2008

Smith & Williamson Short Dated Corporate Bond Fund April 29, 2009

Smith & Williamson Enterprise Fund January 15, 2010

Smith & Williamson Global Inflation Linked Bond Fund May 25, 2012

Smith & Williamson Medium Dated Corporate Bond Fund July 13, 2012 June 15, 2018

Smith & Williamson Mid Ocean World Investment Fund April 1, 2014

Smith & Williamson Blairmore Global Equity Fund December 31, 2014

Smith & Williamson Artificial Intelligence Fund June 23, 2017

Smith & Williamson Investment Funds Plc

32

Notes to the Financial Statements for the financial year ended December 31, 2018 (continued)

2. Significant Accounting Policies

The significant accounting policies adopted by the Company are as follows:

(a) Basis of Preparation

These financial statements have been prepared in accordance with International Financial Reporting Standards

(“IFRS”) as adopted by the European Union (“EU”), applicable law comprising the Irish Companies Act 2014 as

amended, and the Regulations.

The Company has initially applied IFRS 9 from January 1, 2018. IFRS 15 Revenue from Contracts with Customers is

also effective from January 1, 2018 but does not have a material effect on the Company’s financial statements.

New standards and amendments effective after 1 January 2018:

IFRS 9, “Financial instruments”, addresses the classification, measurement and recognition of financial assets and

financial liabilities. An updated version of IFRS 9 was issued on November 10, 2013. It replaces the parts of IAS 39

that relate to the classification and measurement of financial instruments. IFRS 9 requires financial assets to be

classified into two measurement categories: those measured at fair value and those measured at amortised cost. The

determination is made at initial recognition. The classification depends on the entity’s business model for managing its

financial instruments and the contractual cash flow characteristics of the instrument. For financial liabilities, the

standard retains most of the IAS 39 requirements. The main change is that, in cases where the fair value option is taken

for financial liabilities, the part of a fair value change due to an entity’s own credit risk is recorded in other

comprehensive income rather than the income statement, unless this creates an accounting mismatch. The effective

mandatory date in place for IFRS 9 is 1 January 2018. The Company classifies its financial assets as being at fair value

through profit or loss in accordance with its business model as its financial assets are managed and their performance

evaluated on a fair value basis in accordance with the documented investment strategy. The adoption of IFRS 9 did not

have a significant effect on the financial statements (refer to below for further detail).

IFRS 9 Financial Instruments (effective for annual periods beginning on or after January 1, 2018)

In the current year the Company has adopted IFRS 9 “Financial Instruments”. Comparative figures for the period

ended December 31, 2017 have not been restated. Therefore, financial instruments in the comparative period are still

accounted for in accordance with IAS 39 Financial Instrument: Recognition and Measurement.

Classification of financial instruments effective from January 1, 2018 (IFRS 9)