Can market be cooling down when China shut the door to IPOs? Kim Sunghwan a *, Tan Jin b , H eo Uk c a Kyungpook National University, Dae-gu, Korea E-mail: [email protected] b Kyungpook National University, Dae-gu, Korea E-mail: [email protected] c Kyungpook National University, Dae-gu, Korea E-mail: [email protected] Abstract In this study, the underpricing phenomena in initial public offering(IPO) of Chinese firms that were on the exchange for the period 2000-2011 was examined. The effects of shutting down IPO market on the underpricing degree of the IPO firms and compared the effects in Shanghai Stock Exchange and Shenzhen Stock Exchange were the main focus of the study. First, the number of days between the listing day and the closure of the IPO market influences the degree of underpricing negatively. In other words, as the listing day becomes closer to the closure of the IPO market, the higher the degree of the initial underpricing. Secondly, the number of days between reopening of the IPO market and the listing day influences the degree of underpricing positively. In other words, as the listing day becomes more distant from the

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Can market be cooling down when China shut the door

to IPOs?

Kim Sunghwana*, Tan Jinb, Heo Ukc

aKyungpook National University, Dae-gu, KoreaE-mail: [email protected]

bKyungpook National University, Dae-gu, KoreaE-mail: [email protected]

cKyungpook National University, Dae-gu, KoreaE-mail: [email protected]

Abstract

In this study, the underpricing phenomena in initial publicoffering(IPO) of Chinese firms that were on the exchange forthe period 2000-2011 was examined. The effects of shuttingdown IPO market on the underpricing degree of the IPO firmsand compared the effects in Shanghai Stock Exchange andShenzhen Stock Exchange were the main focus of the study.First, the number of days between the listing day and theclosure of the IPO market influences the degree ofunderpricing negatively. In other words, as the listing daybecomes closer to the closure of the IPO market, the higherthe degree of the initial underpricing. Secondly, the numberof days between reopening of the IPO market and the listingday influences the degree of underpricing positively. Inother words, as the listing day becomes more distant from the

reopening of the IPO market, the higher the degree of theinitial underpricing. Thirdly, the degree of initialunderpricing before shutting down the IPO market is higherthan after. These results were also seen in Shanghai andShenzhen Stock Exchange. The results showed that shuttingdown the IPO market can reduce the underpricing degree of theIPO firm which will ultimately lead to the IPO market’s re-stabilization.

Keywords: IPO, Underpricing, Shenzhen Stock Exchange andShanghai Stock Exchange, China

1. Introduction

Since October of 2012, listing of new stock has been ceasedin China. Without any official announcement from the Chinesegovernment, initial public offering(IPO) or stock marketlaunch is being strongly down-regulated. The end of October,2013 would be the one year marking of the Chinese IPOclosure. However, according to 20 years of Chinese stock markethistory, IPO was recorded to have shut down seven times.<Figure 1> shows the timeline of IPOs since 2000.

[Please insert Figure 1 about here]

As the Chinese economy became unstable and more capitalstarted to transfer toward the IPO market, the market beganto over-heat. It is a well known fact that the continuationof new stock listing would lead to overwhelm the demands ofinvestor and ultimately decrease the market flow. If theseseries of events occur consecutively, Chinese economy will be

forced to inhibit IPOs in order to stabilize and strengthenthe IPO and stock market. Once the market recovers, Chinesegovernment will start approving IPOs again.Moreover, shutting down of IPO market in 2012 was also causedby slow economy as well as political uncertainties prior toonce-a-decade leadership transition which was aimed atencouraging the stock market.However, the main concern in regards to the Chinese IPOmarket of 2012 and 2013 is its unclear possibility of IPOmarket re-stabilization after the closure. Considering the changes in the degree of underpricing duringIPO was one of main factors in determining the marketconditions, underpice ratio was used as a dependent variableto measure the market conditions, and the effects of shuttingdown the IPO market.The phenomenon of underpricing in IPO exists almost everycapital market in the world, an anomaly in the IPOprocess(Agrawal, 2009). Pande and Vaidyanathan(2009) reportsaverage underpricing of 22% on the day of listing which isdisappeared within the next 30 days, in their study of 55firms listed on National Stock Exchange, a leading stockexchange in India. Thus, it is undeniable that IPOunderpricing is important for investors, issuers, andinvestment bankers.Many prior studies was conducted on underpricing during IPOin different stock exchange markets around the world and themajority of them concentrated on the anatomy of its existenceto explain what causes it occur. It has been widely knownthat many underwriters set the initial offering price muchlower than the normally accepted range allowing significantlyhigher returns for IPO investments.Almost all studies across the countries found the evidence ofIPO underpricing(Agrawal, 2009). Lucas and McDonald(1990)

developed an asymmetric information model where firmspostpone their equity issue if they know they are currentlyundervalued. Chemmanur and Fulghieri(1994) support theasymmetric information model between the investment bankerand issuers. According to Agrawal(2009), there are manyimportant factors such as information asymmetry among theinvestors, firms' characteristics like age, underwriters'intention and reputation, industry classification, regulatoryenvironment, listing delay, marketing, post-IPO ownershipstructure, and intentional underpricing as documented in theliterature and supported by empirical evidences throughvarious studies.The study on Chinese IPOs underpricing will have asignificant impact on IPO studies theoretically andpractically. In China, the underpricing degree of IPO issignificantly higher than of western security market. IPOunderpricing in China is quite remarkable. Chen et al.(2004)identifies average initial underpricing of 298% in Chineseofferings between 1992 and 1997. Until recently, explanationsfor the short-term pricing performance of China’s new issuehave relied upon western traditional theory hypothesis. Thiscould not have convincingly explained plausibly due to theintrinsic traits of the Chinese stock markets. Thus, factorsin the prior studies have not been in much agreement so far. As the Chinese capital market start to open up to theoutside world, the firms decided to raise money for thecapital market, possibly through IPOs. Thus, suchunderpricing has to be dealt with significant importance.Some specific traits of the Chinese markets which lead tospecial interest of outside investors are as follows. One ofthe typical features in Chinese listed firms is that theyhave a mixed ownership structure and most of them have highconcentration of state shares. Procianoy and Cigerza’s(2011)

comparative study of emerging markets like Brazil, India andChina conveys that Chinese IPOs have the same features asother except for the amounts of short term and long termperformance. They also reported regarding to a hot-issueperiod in China. The total gross proceedings raised in IPOsissued in the Chinese Stock Exchanges(Shanghai, Shenzhen,Hong Kong and Taipei) was US$ 25.75 billion, slightly lessthan US$ 32.05 billion raised in the American Market in 2006.The Industrial & Commercial Bank of China issued the world’slargest IPO ever, raising US$ 14 billion in Hong Kong and US$5.1 billion in Shanghai Stock Exchanges in same year.According to Xu and Wang(1999), like many other formercommunist countries like Russia and other East Europeancountries such as Poland, and Hungary, China has taken manyeconomic reforms during the decades starting from late 1980sor early 1990s, gradually converting its centrally plannedeconomy towards market economy, thus termed as an economy intransition. China reformed its economy by privatizing itsstate-owned firms, which played a major role. It took twoapproaches in its reform of industrial sector: the marketapproach and the ownership approach. Unlike many EasternEuropean countries that made radical changes, China took amarket oriented approach by developing the stock markets,privatizing the state owned firms over a long period of time.They provided firms with funds from the general public.Chinese IPO firms with a mixed ownership structure, many ofthem still controlled by the state.In this paper, the effects of shutting down the IPO marketduring the underpricing and the comparison of between theShanghai Stock Exchange and Shenzhen Stock Exchange werestudied. With specific factors of IPO underpricing andpricing efficiency, the effects of factors unique to the IPOmarkets due to different environment, legal and financial

markets characteristics on the width and severity of IPOphenomenon in China can be understood.

2. Literature Review

2.1 On IPO Theory and Phenomenon With widespread phenomena of IPO underpricing across manycountries, the main focus of prior studies was on theseverity and causes of such phenomena. According to Welch andRitter(2002), firms go public primary because they have "thedesire to raise equity capital for the firm and to create apublic market in which the founders and other shareholderscan convert some of their wealth into cash at a future date."Leland and Pyle(1977) also introduced the concept ofinformation asymmetry among the investors of financialintermediaries by observing the post IPO ownership ofissuers. Chemmanur and Fulghieri(1994) support that theinvestment banker produces more information to reduceinformation asymmetry between issuers and investment banker.Zingales(1995) proposes life cycle theory in IPO, suggestingthat it is much easier for a potential acquirer to find apotential target for takeovers when it is public.When the issuer have more information than investors, “itsignals to the market by selling deliberately its shares at alower price than that the market believes they are worth,thus detering a poor quality issuer from mimicking, and theissuer can get compensation later from future issues”(Welch,1989), “favorable market responses to future dividendannouncements”(Allen and Faulhaber, 1989), or “analystcoverage”(Chemmanur, 1993). Jegadeesh, Weinstein, andWelch(1993) argued that returns after IPO can affect futureissuing act. Michaely and Shaw(1994) found no evidence of aexperienced offering will pay more dividends for underpriced

IPOs. “Pricing too high might result in a winner’scurse”(Rock, 1986) or “a negative cascade”(Welch, 1992). In awinner's curse case, investors will receive a partialallocation when they are underpriced and a full allocationwhen overpriced. In an informational cascade, informedinvestors will only invest the underpriced stock and theless-informed investors will leave the market at last. vanBommel and Vermaelen(2001) found that when firms got morehigher first-day returns, they will spend more money oninvestment after the IPO. Studies like Rock(1986), Benvenisteand Spindt(1989), and Chemmanur(1993) are relevant toinformation asymmetry. Pande and Vaidyanathan(2009) using 55firms listed on National Stock Exchange in India and foundthat average underpricing of 22% on the day of listing canlasts for the next 30 days.Loughran et al.(1994) introduced the auctions, fixed priceoffers and book building methods in IPOs. Benveniste andSpindt(1989), Benveniste and Wilhelm(1990) and Sherman(2005)argued that the bookbuilding method may give a chance tounderwriters to obtain information from informed investors.With the bookbuilding method, at first, a preliminary offerprice range will be set, and then in order to measure demandthe issuer with underwriters will goes on a road show forpotential investors. Lee, Taylor, and Walter(1999) andCornelli and Goldreich(2001) argued that informed investorsrequest more allocations, and they always preferentiallyreceive more allocations. Benveniste and Busaba(1997)consider whether “book building or cascade creation is moreprofitable”.Ruud(1993), Schultz and Zaman(1994) proposed another view onthe existence of IPO underpricing, they argued that the IPOunderpricing is due to the fact that the managing underwriterwhich has to maintain the prices of IPO stocks above a

relative high level over the IPO period deliberately sellingstocks cheaper, hypothesizing market making. In this suppose,to leading to abnormally higher returns in IPO investments,the managing underwriter will make the initial offering pricemuch lower than the normally expected price. Ellis, Michaely,and O'Hara(2000) argued that market making is lucrative forthe managing underwriter. Aggarwal and Conway(2000) foundthat the Nasdaq-listed IPOs’ market share declines fromalmost 100 percent at time of IPO to less than 50 percent onaverage about half a year later, and the managing underwriteris typically the dominant market maker for this. Sherman andTitman(2002) reported that “IPO firms are always interestedin raising funds at least at accurate price of issue if notmore. The ability of underwriting with proper price leads tomaintain and acquire high quality clients”.As in Reside et al.(1994), there are more other factors caninfluence the level of IPO underpricing, such like firm’sbackground, present performance, past performance, existingshareholding pattern, etc. Agrawal(2009) found some importantfactors such as listing delay, underwriters' intention andreputation, post-IPO ownership structure, firms'characteristics, marketing, regulatory environment,information asymmetry among the investors, intentionalunderpricing, and industry classification. The author alsofound such market factors influencing the underpricing as thedemand for a new IPO, initial uncertainty of value of an IPO,signaling effect of the agents, and by the insecuritiesgenerated due to potential legal liabilities of the issuerand the underwriter. Most papers studied the underpricing in the short run IPOperformance. Short-run returns, also be called initialreturn, in initial pricing are usually measured as the first-day price return of the stock, which is the difference

between the offer price and the first-day closing price. Alot of studies research on the initial underpricing andalmost all of them show a positive average first-day return.Ljungqvist and Wilhelm(2003) found “average initial return of35.7% in a sample of IPOs issued between 1996 and 2000 in theUnited States”; Gunther e Rummer(2006) found short-run returnof 45.8% in the first trading day in Germany, which wassimilar with the IPOs in United States.

2.2 On IPO Phenomenon in China Due to many specific traits unique to the Chinesetransitional policies, economy and cultural environment, IPOphenomena in China have been an interesting area of research.Although there are many other researches on Chinese IPOs,summarization of papers discussing the effects of mainfactors on IPO underpricing are reported in <Table 4>.According to Procianoy and Cigerza(2011), IPOs are widelyresearched in Europe, the United States and the otherdeveloped financial markets, but not so well in massedemerging markets, such as China, India and Brazil. For theChinese financial market, Chen et al.(2004, a) reported anaverage initial underpricing 298% and 25% for A and B sharesissued between 1992 and 1997. They found that smaller modernindustrial firms are concentrated with indirect state sharesincluding employee shares and legal persons, but on thecontrary, larger traditional industrial firms areconcentrated with direct state shares. Smaller, growing andhigh-risk firms experienced state control reducing but thestate retains majority control over larger and strategicallyimportant firms even after their IPOs. Chan et al.(2004)document that the initial underpricing of Chinese IPOs withthe sample of 570 A shares and 39 B shares issued between1993 and 1998 near 178% and 11.6%. They found that A share

return is worse and B share return in the long-run. Toanalyze short-run and long-run performance, Chi andPadgett(2005, a) study 340 and 409 IPOs respectively issuedin 1996 and 1997, found that initial returns of 127.3% and 3years buy-and-hold-average-return of 10.7%. Chi andPadgett(2005, b) study 668 IPOs issued in Shanghai andShenzhen between 1996 and 2000, found given demand to theoffer of shares is 50 to 1. Yu and Tse(2005) reported averagefirst-day returns of 123.59% of 343 A shares issued between1995 and 1998. They tested Rock´s(1986) winner’s curse modeland found that the initial return model suits for ChineseIPOs, however, the signal hypothesis is rejected withconflicting results.Procianoy and Cigerza(2011) compared IPOs in emerging marketslike Brazil, India and China. They found that Brazilian,Indian and Chinese IPOs have the similar features but theexperiment showed different results in their amounts forshort term performance and different signal for long termperformance.

3. Research Design

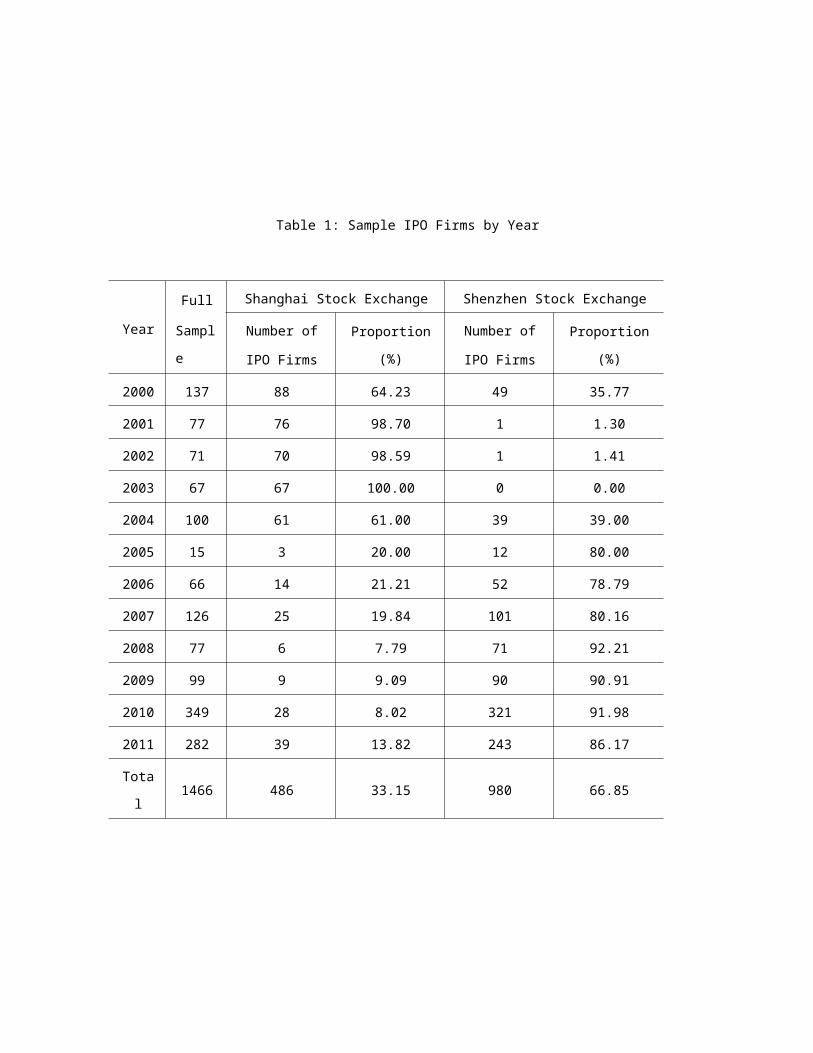

3.1 DataIn this study, Chinese firms which went public only atShanghai and Shenzhen Stock Exchanges were used for thecollection of data. The sample selection process is asfollows. First, we collected data from RESSET from 2000 to2011. Then, firms were excluded which had no financial datafor the year before they went public and firms withoutcomplete data on the variables were used in the study.The total number of observations, sum of sample firms overthe period, is 1466. Table 1 shows the number of sample firmsby year and of firms’ public offered at Shenzhen Stock

Exchange or Shanghai Stock Exchange. The study found thatmost firms went on public through Shanghai Stock Exchange,compared with Shenzhen Stock Exchange until the year 2004.The trend was reversed in year 2005 through year 2011, duringwhen most firms went on public through Shenzhen StockExchange, compared with Shanghai Stock Exchange. Also, many firms became public over the years, except for the2004, 2007, and 2010 with big jumps in the numbers of IPOfirms. On the contrary, the number of IPO firms in year 2005was only 15, sharply declining from 100 firms in the previousyear.

[Please insert Table 1 about here]

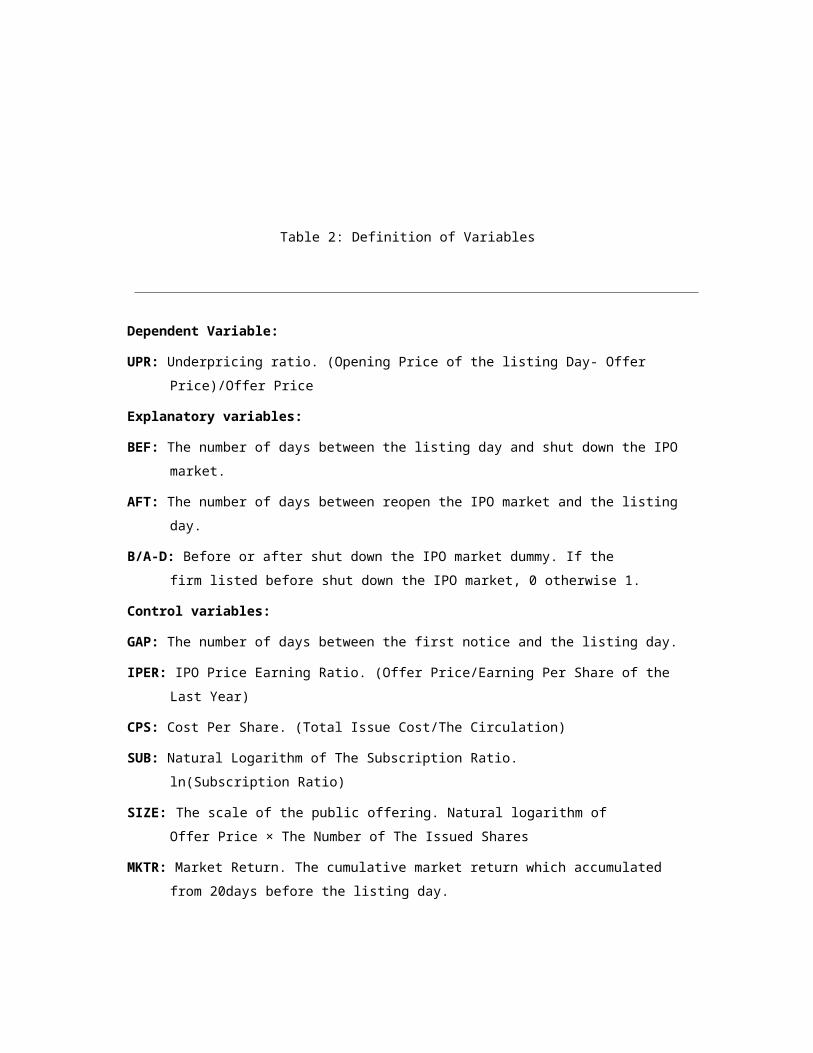

3.2 Model and VariablesIn this study, Underpricing Ratio(UPR) was used as adependent variable, representing the underpricing degree ofthe IPO firm. UPR is calculated using offer price and theopening price of the list day((Opening Price of the listingDay- Offer Price)/Offer Price). In addition, variablesrepresenting our hypotheses and control variables aresummarized in <Table 2>.

[Please insert Table 2 about here]

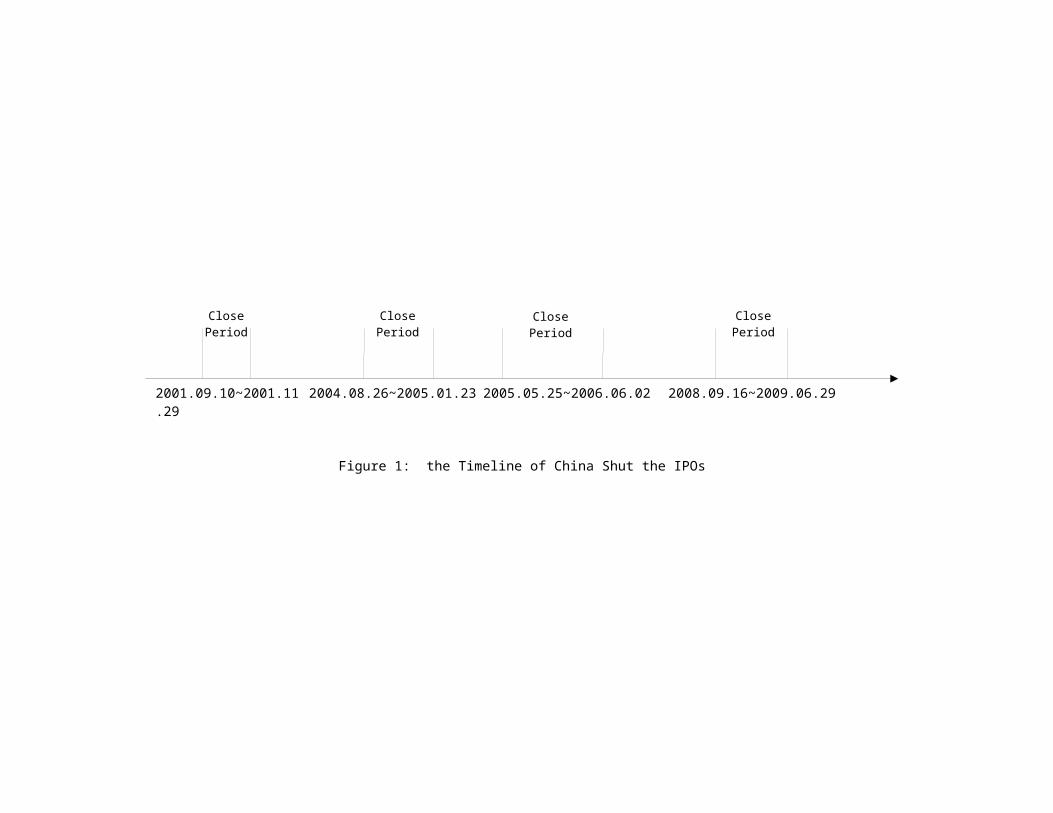

<Figure 2> shows the outcome of IPO market after the closureand the expected trend of the underpricing degree. Accordingto the prediction, when the stock market become unstable, theIPO market will start to get overwhelming and then theunderpricing degree of the IPO firm will increase. After aperiod of closure, the underpricing degree will start at arelative low level when if the method was effective

[Please insert Figure 2 about here]

Before stating the hypothesis of the study, prior studies ofthe Chinese IPO markets should be mentioned again. Chen etal.(2004) used A and B shares and separated samples forShanghai and Shenzhen, found that the lag between offeringand listing, price-to-earnings ratios and the number ofseasoned equity offerings are positively related to initialunderpricing. Chan et al.(2004) found that the number of daysbetween offering day and listing day is positively related tounderpricing, offer size and the regional development proxyof the area from the firm comes originated are negativelyrelated to underpricing. Chi and Padgett(2005, a) and Chi andPadgett(2005, b) found that government ownership and high-tech dummy are positively related to underpricing, offersize, the natural logarithm of offer size and the amount ofshares hold by public institutions are negatively related tounderpricing. Yu and Tse(2005) tested the ex ante uncertaintyhypothesis using offer size, firm age, and after-marketreturns standard-deviation, and they found that offer sizeand firm age are negatively related to underpricing whileafter-market returns standard-deviation positively related tounderpricing. <Table 3> shows us the research found regardingChinese IPOs up to now.Based on the nature of the earlier discussion, we can inferthat shutting down the IPO market can reduce the underpricingdegree of the IPO firm. Therefore we hypothesized as follows:

Hypothesis 1: The closer the listing day to start of the IPOclosure, the market will have higher degree of the initialunderpricing.

Hypothesis 1-1: In Shanghai Stock Exchange, the closer thelisting day to start of IPO closure, the market will havehigher degree of the initial underpricing.Hypothesis 1-2: In Shenzhen Stock Exchange, the closer thelisting day to the start of IPO closure, the market will havehigher the degree of the initial underpricing.

Hypothesis 2: As the listing day becomes more distant fromthe first day of market reopening, the higher the degree ofthe initial underpricing.Hypothesis 2-1: In Shanghai Stock Exchange, as the listingday becomes more distant from the first day of marketreopening, the higher the degree of the initial underpricing.Hypothesis 2-2: In Shenzhen Stock Exchange, as the listingday becomes more distant from the first day of marketreopening, the higher the degree of the initial underpricing.

Hypothesis 3: The degree of initial underpricing is highercompared to the degree of underpricing after shutting downthe IPO market.Hypothesis 3-1: In Shanghai Stock Exchange, the degree ofinitial underpricing is higher compared to the degree ofunderpricing after shutting down the IPO market. Hypothesis 3-2: In Shenzhen Stock Exchange, the degree ofinitial underpricing is higher compared to the degree ofunderpricing after shutting down the IPO market.

Accordingly, equation (1), (2) and (3) for a multiple linearregression model were used as the following expression:

UPR(i) = β0 + β1BEFi + β2GAPi + β3IPERi+ β4CPSi + β5SUBi + β6SIZEi + β7MKTRi + εi, (1)

UPR(i) = β0 + β1AFTi + β2GAPi + β3IPERi+ β4CPSi + β5SUBi + β6SIZEi + β7MKTRi + εi, (2)

UPR(i) = β0 + β1B/A-Di + β2GAPi + β3IPERi+ β4CPSi + β5SUBi + β6SIZEi + β7MKTRi + εi, (3)

Where UPR(i) = (Opening price of the listing day- Offerprice)/Offer price of firm i.

BEFi = Number of days between the listing day and shut downthe IPO market of firm i.

AFTi = Number of days between reopen the IPO market and thelisting day of firm i.

B/A-Di = Before or after shut down the IPO market dummy. Ifthe firm listed before shut down the IPO market, 0otherwise 1.

GAPi = Number of days between the first notice and the listingday of firm i.

IPERi = Offer price/Earnings per share of the last year offirm i.

CPSi = Total issue cost/The circulation of firm i.SUBi = ln(Subscription ratio) of firm i.SIZEi = ln(Offer price × The number of the issued shares) of

firm i.MKTRi = Cumulative market return which accumulated from 20days

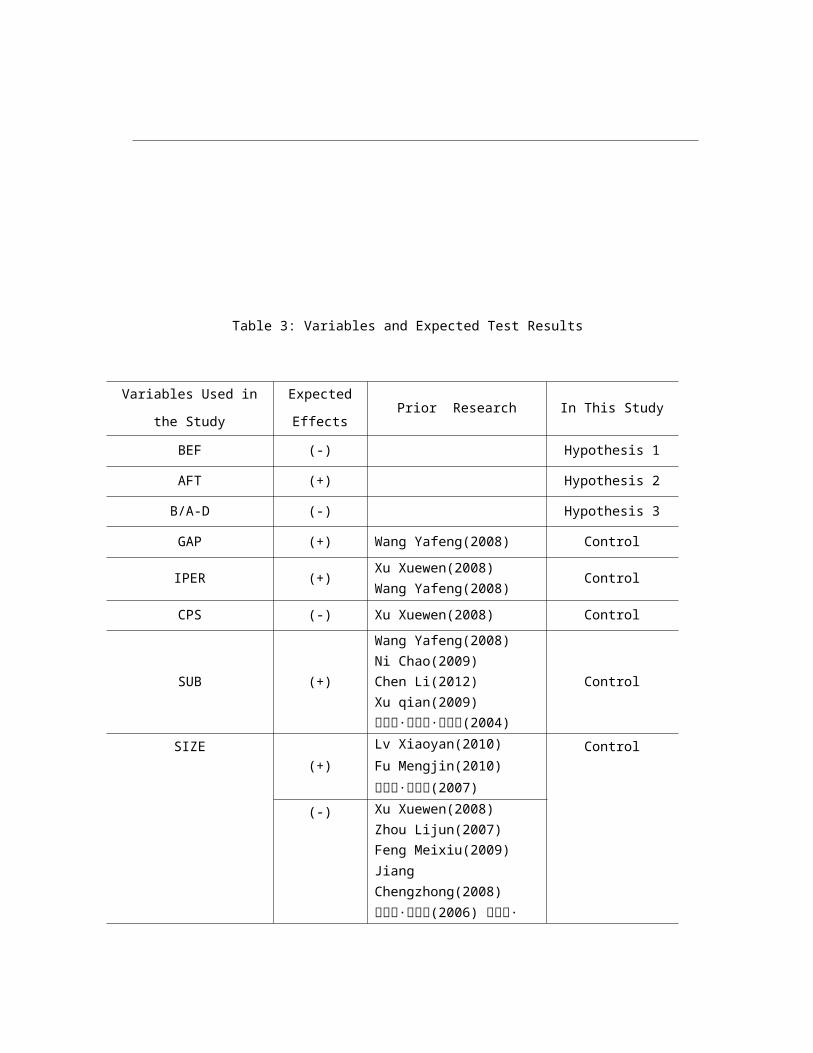

before the listing day of firm i.The variables used in this study with their notations,estimated signs in coefficients, from prior research and ourstudy are summarized in Table 3.

[Please insert Table 3 about here]

4. Test Results

4.1 Data Analysis

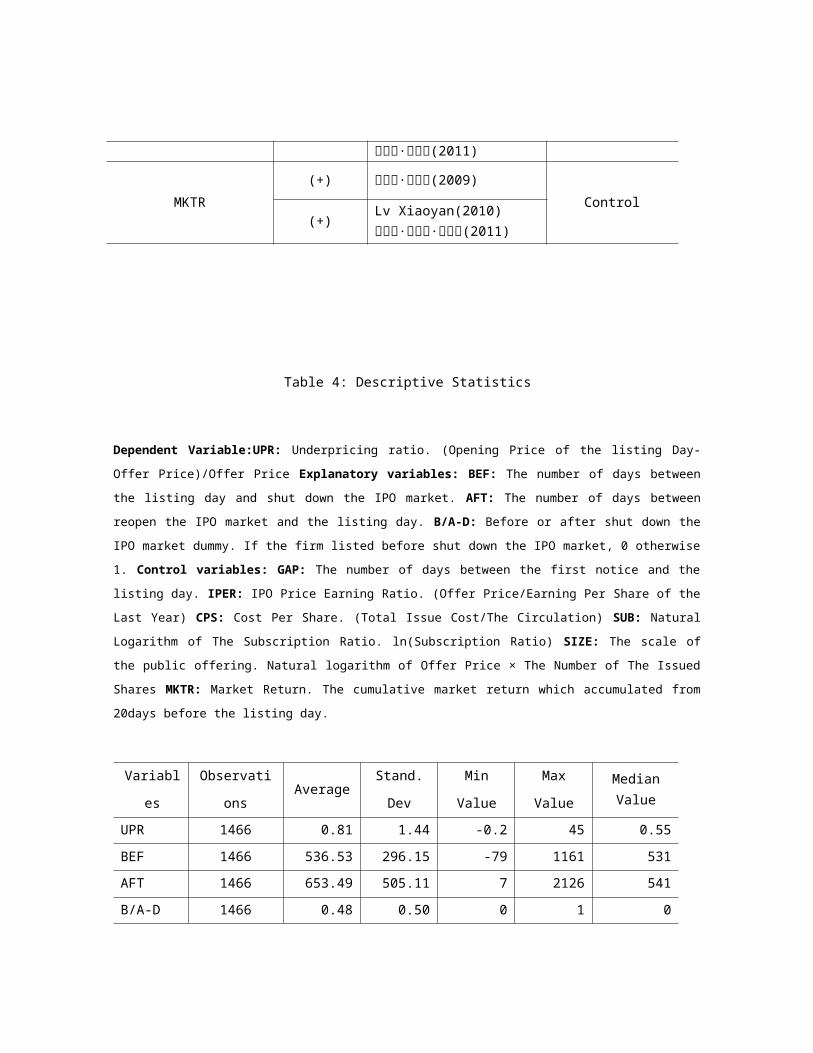

This section describes the sample data based on thestatistical analysis about firm characteristic as shown in<Table 4>. First, the dependent variance, underpricing(UPR)measured by (Opening price of the listing day- offerprice)/offer price), is on average approximately 0.8 in Chinafor the IPO firms during the sample years. The number of thedays before shutting down the IPO market(BEF) is about 536.53days on average. The number of the days after the reopeningthe IPO market(AFT) is about 653.49 days on average. Thenumber of days between the first notice and the listingday(GAP) is about 64.6 days on average. The ratio of offerprice to earning per share of the last year(IPER) is about39.9 on average. The ratio of total issue cost to thecirculation(CPS) is about 1.09 on average. The subscriptionratio(SUB) measured by the natural logarithm of subscriptionratio is about 5.34 times on average. The size of afirm(Size) measured by the natural logarithm of(offer price ×the number of the issued shares) is about 20.21 on average.The cumulative market return(MKTR) which accumulated from20days before the listing day is about 0.02% on average.

[Please insert Table 4 about here]

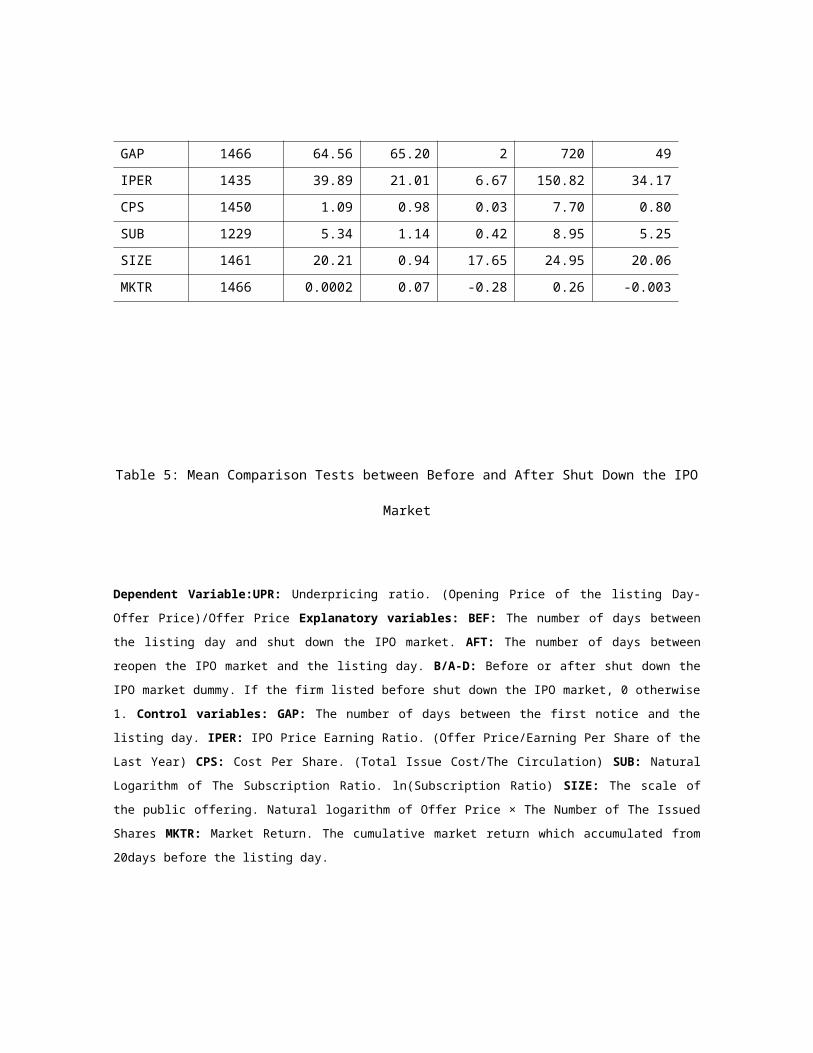

4.2 Mean Comparison Test and Correlation Analysis This section compares the degree of underpricing betweenbefore and after the closure of the IPO market as shown in<Table 5>. From the t-tests using unequal variances betweengroups, the dependent variable underpricing(UPR),subscription ratio(SUB) before shutting down the IPO marketare significantly larger than after, while the number of daysbetween the first notice and the listing day(GAP), IPO priceearning ratio(IPER), cost per share(CPS), the scale of the

public offering(SIZE), market return(MKTR) are significantlysmaller than after shutting down the IPO market.

[Please insert Table 5 about here]

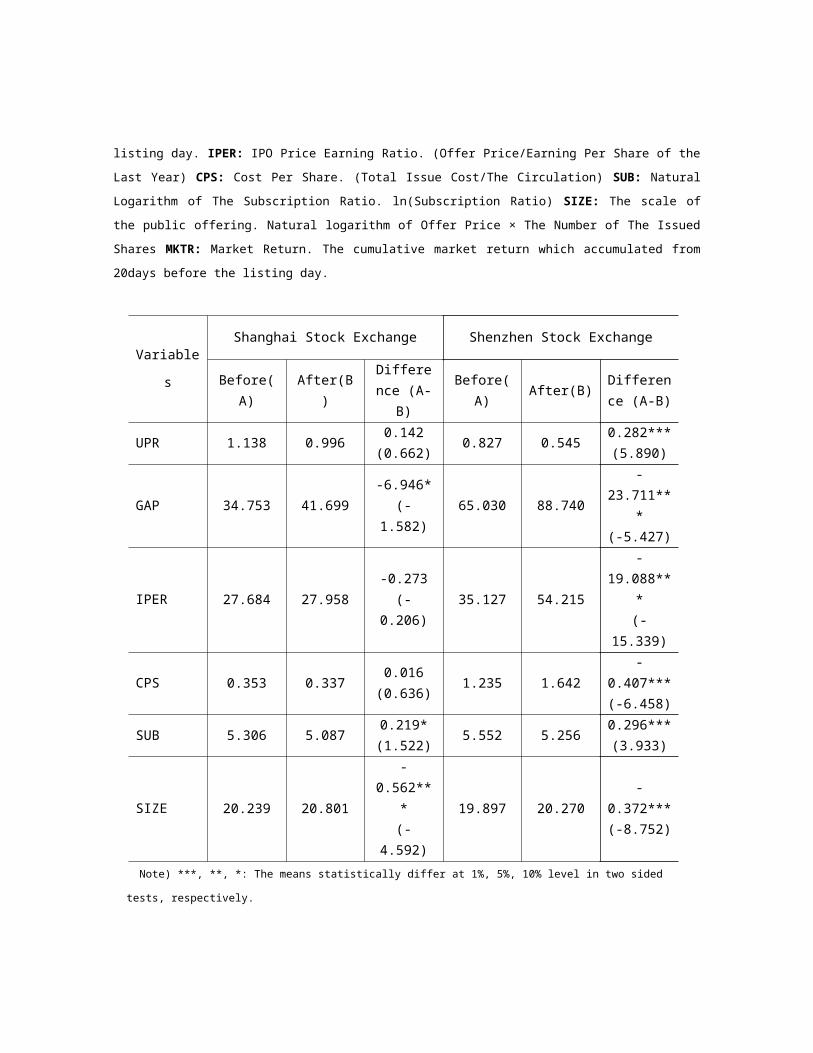

<Table 6> shows the difference of the underpricing degree inShanghai and Shenzhen Stock Exchange. First in Shanghai StockExchange, the subscription ratio(SUB) before the closure ofIPO market are significantly larger than after, while thenumber of days between the first notice and the listingday(GAP), the scale of the public offering(SIZE) aresignificantly smaller than after shut down the IPO market.The dependent variable underpricing(UPR), IPO price earningratio(IPER), cost per share(CPS) are not statisticallydifferent between the two situations. In Shenzhen StockExchange, the situation is quite similar with the situationin whole stock market. The dependent variableunderpricing(UPR), subscription ratio(SUB) before shut downthe IPO market are significantly larger than after, while thenumber of days between the first notice and the listingday(GAP), IPO price earning ratio(IPER), cost per share(CPS),the scale of the public offering(SIZE) are significantlysmaller than after shut down the IPO market.

[Please insert Table 6 about here]

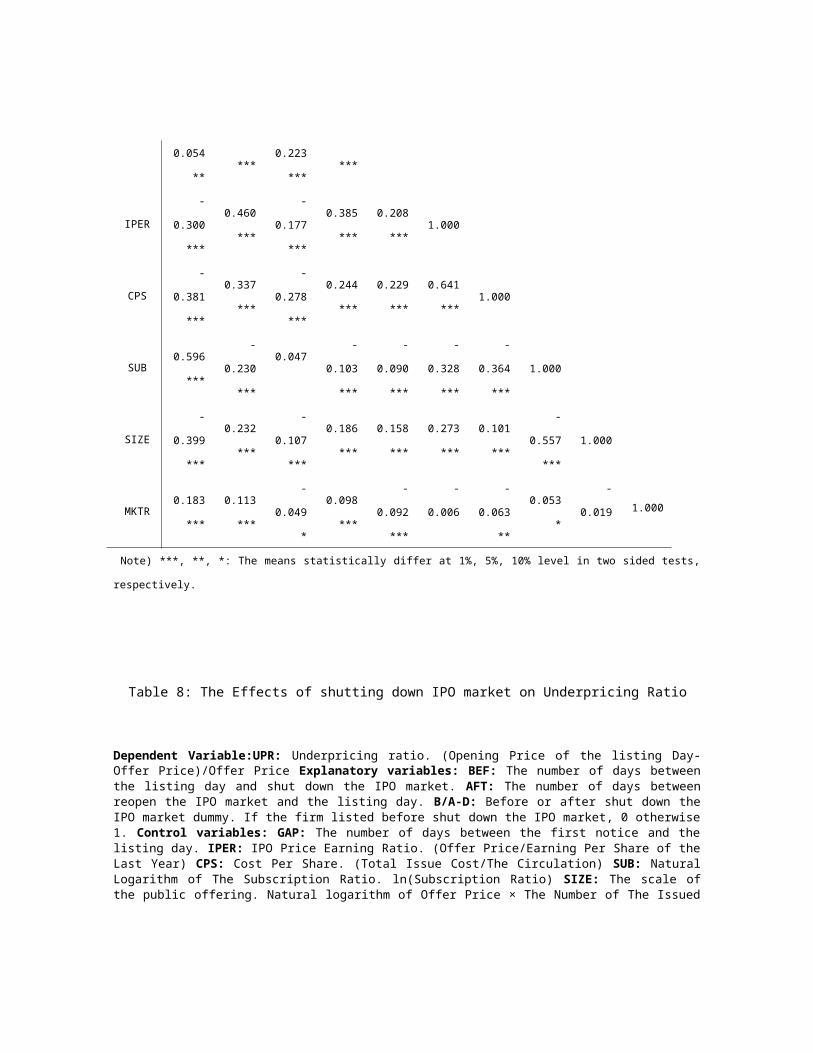

The correlations between the variables are provided in <Table7>. The correlation coefficient is in most cases 0.6 or less.For simplicity, the correlation between the dependentvariable and the other variables are discussed only. With thedependent variable underpricing(UPR), the number of the daysbefore shutting down the IPO market(BEF), before or aftershut down the IPO market dummy(B/A-D),the number of days

between the first notice and the listing day(GAP), the ratioof offer price to earning per share of the last year(IPER),the ratio of total issue cost to the circulation(CPS), andthe size of a firm(SIZE) measured by the natural logarithmare negatively correlated, while the number of the days afterreopen the IPO market(AFT), the subscription ratio(SUB) andthe cumulative market return accumulated from 20 days beforethe listing day(MKTR) are positively correlated. Somestatistically significant correlations among independentvariables require cautions in multivariate regressions withrespect to multicollinearity problems.

[Please insert Table 7 about here]

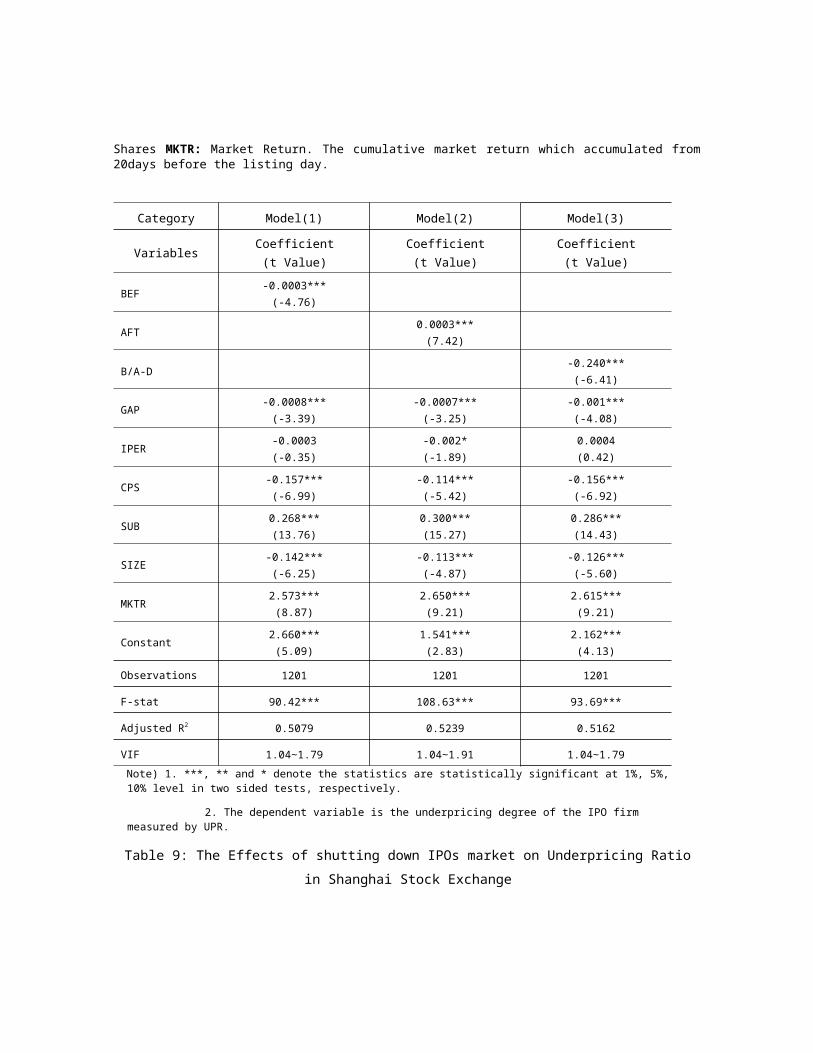

4.3 Regression AnalysisIn this section, the effects of shut down IPO market on theunderpricing degree of the IPO firms are analyzed, measuredwith underpricing ratio(UPR) using multivariate regressionmodel 1, 2 and 3. <Table 8> shows the results of threeregression models. With similar results across models,results from the last one with all the variables wereinterpreted together. The coefficients of the regressions onindependent variables in the models are significantlypositive for the number of the days after reopen the IPOmarket(AFT), the subscription ratio(SUB) and the cumulativemarket return accumulated from 20 days before the listingday(MKTR). On the contrary, the number of the days beforeshut down the IPO market(BEF), before or after shut down theIPO market dummy(B/A-D),the number of days between the firstnotice and the listing day(GAP), the ratio of total issuecost to the circulation(CPS), and the size of a firm(SIZE)measured by the natural logarithm are significantly negativewith respect to underpricing ratio(UPR). However, the ratio

of offer price to earning per share of the last year(IPER) donot show any statistically significant correlation with theinitial underpricing except in model 2. From the low VIFstatistics, one can conclude that there are no statisticallysignificant multicollinearity among independent variables.

[Please insert Table 8 about here]

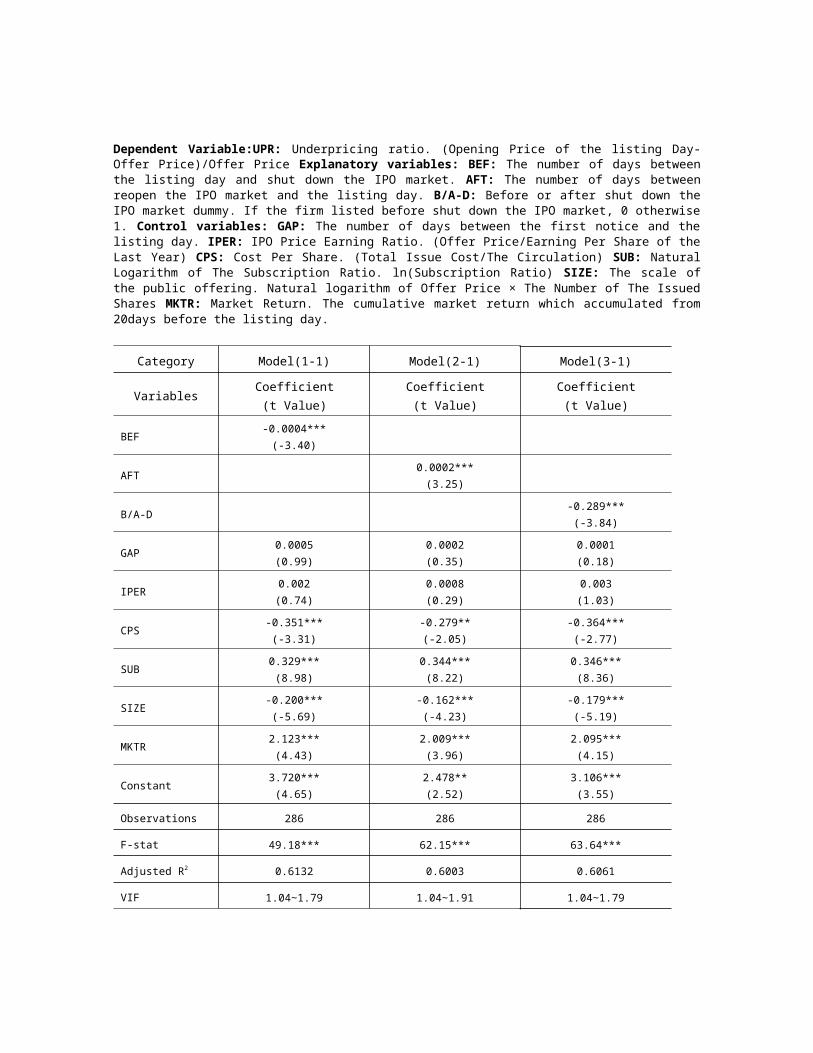

Moreover, the effects of shutting down IPO market Shanghaiand Shenzhen Stock Exchange were also analyzed. <Table 9>shows the results of the Shanghai Stock Exchange. Thecoefficients of the regressions on independent variables inthe models are significantly positive for the number of thedays after reopen the IPO market(AFT), the subscriptionratio(SUB) and the cumulative market return accumulated from20 days before the listing day(MKTR). On the contrary, thenumber of the days before shut down the IPO market(BEF),before or after shut down the IPO market dummy(B/A-D), theratio of total issue cost to the circulation(CPS), and thesize of a firm(SIZE) measured by the natural logarithm aresignificantly negative with respect to underpricingratio(UPR). However, the number of days between the firstnotice and the listing day(GAP), the ratio of offer price toearning per share of the last year(IPER) do not show anystatistically significant correlation with the initialunderpricing.

[Please insert Table 9 about here]

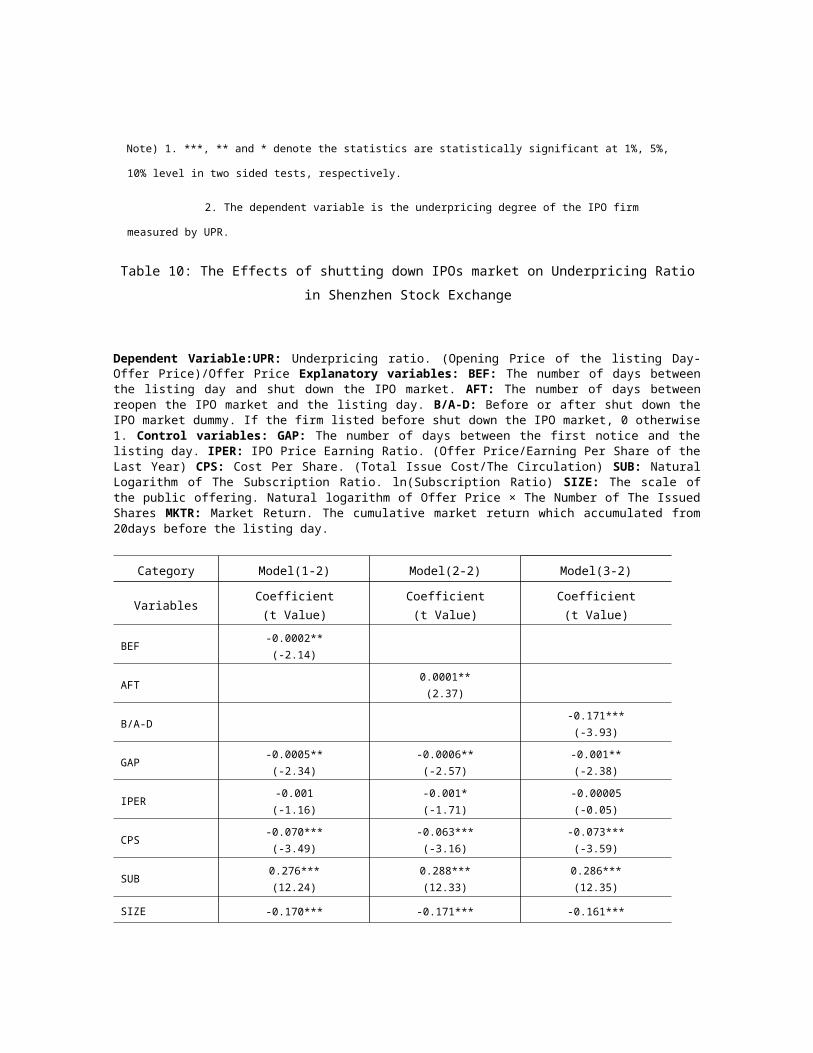

<Table 10> shows the results of the Shenzhen Stock Exchangewhich is similar to the result of the whole stock market. Thecoefficients of the regressions on independent variables inthe models are significantly positive for the number of the

days after reopen the IPO market(AFT), the subscriptionratio(SUB) and the cumulative market return accumulated from20 days before the listing day(MKTR). On the contrary, thenumber of the days before shutting down the IPO market(BEF),before or after shut down the IPO market dummy(B/A-D), thenumber of days between the first notice and the listingday(GAP), the ratio of total issue cost to thecirculation(CPS), and the size of a firm(SIZE) measured bythe natural logarithm are significantly negative with respectto underpricing ratio(UPR). However, the ratio of offer priceto earning per share of the last year(IPER) do not show anystatistically significant correlation with the initialunderpricing except in model 2-2. From the low VIFstatistics, we can conclude there are no statisticallysignificant multicollinearity among independent variables.

[Please insert Table 10 about here]

5. Conclusion

In this study, the underpricing phenomena in initial publicoffering(IPO) of Chinese firms that were on the exchange forthe period 2000-2011 was examined. The effects of shuttingdown IPO market on the underpricing degree of the IPO firmsand compared the effects in Shanghai Stock Exchange andShenzhen Stock Exchange were the main focus of the study. First, the number of days between the listing day and theclosure of the IPO market influences the degree ofunderpricing negatively. In other words, as the listing daybecomes closer to the closure of the IPO market, the higherthe degree of the initial underpricing. Also, symmetric

result was obtained from Shanghai and Shenzhen Stock Exchangedata.Secondly, the number of days between reopening of the IPOmarket and the listing day influences the degree ofunderpricing positively. In other words, as the listing daybecomes more distant from the reopening of the IPO market,the higher the degree of the initial underpricing. Thisresult was also correlated with the Shanghai and ShenzhenStock Exchange data.Thirdly, the degree of initial underpricing before shuttingdown the IPO market is higher than after. This result wasalso seen in Shanghai and Shenzhen Stock Exchange. Theresults showed that shutting down the IPO market can reducethe underpricing degree of the IPO firm which will ultimatelylead to the IPO market’s re-stabilization.

ReferencesAgrawal, D. "IPO UNDERPRICING: A LITERATURE REVIEW1" Electroniccopy available at: http://ssrn.com/abstract=1724762Aggarwal, R. and P. Rivoli, "Fads in the IPO Market?",Financial Management, 19, 1990, 45-57.Aggarwal, R., "Stabilization Activities by Underwriters AfterInitial Public Offerings", Journal of Finance, 55, 2000, 1075-1103.AGGARWAL, R.; LEAL, R.; HERNANDEZ, L. The after- marketperformance of initial public offerings in Latin America.Financial Management, 22, 42-53, 1993.

ALLEN, F.; FAULHABER, G.R. Signalling by underpricing in theIPO market. Journal of Financial Economics, 23, 303-323, 1989.Beatty, R. and J. Ritter, "Investment Banking Reputation andUnderpricing of Initial Public Offerings", Journal of FinancialEconomics, 15, 1986, 213-232.Benveniste, L. and P. Spindt, "How Investment BankersDetermine the Offer Price and Allocation of New Issues",Journal of Financial Economics, 24, 1989, 243-361. BOYCKO, M.; SHLEIFER, A. e VISHNY, R. A Theory ofPrivatization. Economic Journal 106, 309-319, 1996.CHEN, Gongmeng; FIRTH, Michael; KIM, Jeong-Bon. IPOUnderprcing in China’'s New Stock Markets. Journal of MultinationalFinancial Management, 14, 283-302, 2004. CHAN, K.; WANG, J.;WEI, K.C.J. Underpricing and long-term performance of IPOs inChina. Journal of Corporate Finance 10, 409-430, 2004.CHI, Jing and PADGETT, Carol(A). The performance and long-runcharacteristics of the Chinese IPO market. Pacific EconomicReview, 10, 451-169, 2005.CHI, Jing and PADGETT, Carol(B). Short-run underpricing andits characteristics in Chinese Initial public offering(IPO)markets. Research in International Business and Finance, 19, 71-93,2005.Hu, G. J. and M. Goergen, "A Study of OwnershipConcentration, Control and Evolution of Chinese IPO firms",SSRN Working Paper, 2001, 1-34.Ljungqvist, A.; Wilhelm, W.J. Jr.(2003), “"IPO Pricing in theDot‐.com Bubble”", The Journal Of Finance, Vol. 58, No. 2, April,pp. 723‐.752.Marchand, J.; Roufagalas J.(1996), “"Search andUncertainty‐.Determinants of the Degree of Underpricing ofInitial Public Offerings”", Journal of Economics and Finance, Vol.20, No. 1, spring, pp. 47‐.64.Pande, Alok; Vaidyanathan, R.(2009), “"Determinants of IPO

Underpricing in the National Stock Exchange in India”", TheICFAI Journal of Applied Finance, Vol. 15, No. 1, 2009, pp. 14-30.Prasad, D.; Vozikis, G.S.; Ariff, M.(2006), “"GovernmentPublic Policy, Regulatory Intervention, and Their Impact onIPO Underpricing: The Case of Malaysian IPOs”", Journal of SmallBusiness Management, Vol. 44, No. 1, pp. 81‐.98.Purnanandam, A. and B. Swaminathan, "Are IPOs ReallyUnderpriced?", The Review of Financial Studies, 17, 2004, 811-848.Reside, M.A.; Robinson, R.M.; Prakash, A.J.; Dandapani, K.(1994), “"A Tax‐.Based Motive for the Underpricing of InitialPublic Offerings”", Managerial and Decision Economics, Vol. 15, pp.553‐.561.Ritter, J., "The Long Run Performance of Initial PublicOfferings", Journal of Finance, 46, 1991, 3-28.Ritter, J. and Welch, I., "A Review of IPO Activity, Pricing,and Allocations", Journal of Finance, 57, 2002, 1795-1828.Rock, K., "Why New Issues Are Underpriced", Journal of FinancialEconomics, 15, 1986, 187-222.Ruud, J. S., "Underwriter Price Support and IPO UnderpricingPuzzle", Journal of Finance, 34, 1993, 135-151.Schultz, P. H. and M. A. Zaman, "Aftermarket Support andUnderpricing of Initial Public Offerings", Journal of FinancialEconomics, 35, 1994, 199-219.

Table 1: Sample IPO Firms by Year

Year

Full

Sampl

e

Shanghai Stock Exchange Shenzhen Stock Exchange

Number of

IPO Firms

Proportion

(%)

Number of

IPO Firms

Proportion

(%)

2000 137 88 64.23 49 35.77

2001 77 76 98.70 1 1.30

2002 71 70 98.59 1 1.41

2003 67 67 100.00 0 0.00

2004 100 61 61.00 39 39.00

2005 15 3 20.00 12 80.00

2006 66 14 21.21 52 78.79

2007 126 25 19.84 101 80.16

2008 77 6 7.79 71 92.21

2009 99 9 9.09 90 90.91

2010 349 28 8.02 321 91.98

2011 282 39 13.82 243 86.17

Tota

l1466 486 33.15 980 66.85

Table 2: Definition of Variables

Dependent Variable:

UPR: Underpricing ratio. (Opening Price of the listing Day- Offer Price)/Offer Price

Explanatory variables:

BEF: The number of days between the listing day and shut down the IPO market.

AFT: The number of days between reopen the IPO market and the listing day.

B/A-D: Before or after shut down the IPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise 1.

Control variables:

GAP: The number of days between the first notice and the listing day.

IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of the Last Year)

CPS: Cost Per Share. (Total Issue Cost/The Circulation)

SUB: Natural Logarithm of The Subscription Ratio. ln(Subscription Ratio)

SIZE: The scale of the public offering. Natural logarithm of Offer Price × The Number of The Issued Shares

MKTR: Market Return. The cumulative market return which accumulated from 20days before the listing day.

Table 3: Variables and Expected Test Results

Variables Used in

the Study

Expected

EffectsPrior Research In This Study

BEF (-) Hypothesis 1

AFT (+) Hypothesis 2

B/A-D (-) Hypothesis 3

GAP (+) Wang Yafeng(2008) Control

IPER (+) Xu Xuewen(2008)Wang Yafeng(2008) Control

CPS (-) Xu Xuewen(2008) Control

SUB (+)

Wang Yafeng(2008) Ni Chao(2009) Chen Li(2012) Xu qian(2009)신신신·신신신·신신신(2004)

Control

SIZE(+)

Lv Xiaoyan(2010) Fu Mengjin(2010)신신신·신신신(2007)

Control

(-) Xu Xuewen(2008)Zhou Lijun(2007)Feng Meixiu(2009) Jiang Chengzhong(2008)신신신·신신신(2006) 신신신·

신신신·신신신(2011)

MKTR(+) 신신신·신신신(2009)

Control(+) Lv Xiaoyan(2010)

신신신·신신신·신신신(2011)

Table 4: Descriptive Statistics

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and thelisting day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The IssuedShares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Variabl

es

Observati

onsAverage

Stand.

Dev

Min

Value

Max

ValueMedianValue

UPR 1466 0.81 1.44 -0.2 45 0.55 BEF 1466 536.53 296.15 -79 1161 531 AFT 1466 653.49 505.11 7 2126 541 B/A-D 1466 0.48 0.50 0 1 0

GAP 1466 64.56 65.20 2 720 49 IPER 1435 39.89 21.01 6.67 150.82 34.17 CPS 1450 1.09 0.98 0.03 7.70 0.80 SUB 1229 5.34 1.14 0.42 8.95 5.25 SIZE 1461 20.21 0.94 17.65 24.95 20.06 MKTR 1466 0.0002 0.07 -0.28 0.26 -0.003

Table 5: Mean Comparison Tests between Before and After Shut Down the IPO

Market

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and thelisting day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The IssuedShares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Variables Before(A) After(B)Difference(A

-B) t stat

UPR 0.958 0.651 0.308 4.100***GAP 52.231 77.726 -25.495 -7.626***IPER 32.037 48.196 -16.159 -15.773***CPS 0.864 1.343 -0.479 -9.570***SUB 5.467 5.230 0.238 3.641***SIZE 20.042 20.393 -0.352 -7.216***MKTR -0.007 0.008 -0.015 -3.781***Note) ***, **, *: The means statistically differ at 1%, 5%, 10% level in two sided tests,

respectively.

Table 6: Mean Comparison Tests between Before and After Shut Down the IPO

Market

In Shanghai and Shenzhen Stock Exchange

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and the

listing day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The IssuedShares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Variable

s

Shanghai Stock Exchange Shenzhen Stock Exchange

Before(A)

After(B)

Difference (A-

B)

Before(A) After(B) Differen

ce (A-B)

UPR 1.138 0.996 0.142(0.662) 0.827 0.545 0.282***

(5.890)

GAP 34.753 41.699-6.946*

(-1.582)

65.030 88.740

-23.711**

*(-5.427)

IPER 27.684 27.958-0.273(-

0.206)35.127 54.215

-19.088**

*(-

15.339)

CPS 0.353 0.337 0.016(0.636) 1.235 1.642

-0.407***(-6.458)

SUB 5.306 5.087 0.219*(1.522) 5.552 5.256 0.296***

(3.933)

SIZE 20.239 20.801

-0.562**

*(-

4.592)

19.897 20.270-

0.372***(-8.752)

Note) ***, **, *: The means statistically differ at 1%, 5%, 10% level in two sided

tests, respectively.

Table 7: Correlation Matrix between Variables

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and thelisting day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The IssuedShares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Variab

lesUPR BEF AFT B/A-D GAP IPER CPS SUB SIZE MKTR

UPR 1.000

BEF

-

0.121

***

1.000

AFT0.109

***

-

0.654

***

1.000

B/A-D

-

0.107

***

0.818

***

-

0.684

***

1.000

GAP - 0.351 - 0.196 1.000

0.054

*****

0.223

******

IPER

-

0.300

***

0.460

***

-

0.177

***

0.385

***

0.208

***1.000

CPS

-

0.381

***

0.337

***

-

0.278

***

0.244

***

0.229

***

0.641

***1.000

SUB0.596

***

-

0.230

***

0.047-

0.103

***

-

0.090

***

-

0.328

***

-

0.364

***

1.000

SIZE

-

0.399

***

0.232

***

-

0.107

***

0.186

***

0.158

***

0.273

***

0.101

***

-

0.557

***

1.000

MKTR0.183

***

0.113

***

-

0.049

*

0.098

***

-

0.092

***

-

0.006

-

0.063

**

0.053

*

-

0.019 1.000

Note) ***, **, *: The means statistically differ at 1%, 5%, 10% level in two sided tests,

respectively.

Table 8: The Effects of shutting down IPO market on Underpricing Ratio

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and thelisting day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The Issued

Shares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Category Model(1) Model(2) Model(3)

Variables Coefficient(t Value)

Coefficient(t Value)

Coefficient(t Value)

BEF -0.0003***(-4.76)

AFT 0.0003***(7.42)

B/A-D -0.240***(-6.41)

GAP -0.0008***(-3.39)

-0.0007***(-3.25)

-0.001***(-4.08)

IPER -0.0003(-0.35)

-0.002*(-1.89)

0.0004(0.42)

CPS -0.157***(-6.99)

-0.114***(-5.42)

-0.156***(-6.92)

SUB 0.268***(13.76)

0.300***(15.27)

0.286***(14.43)

SIZE -0.142***(-6.25)

-0.113***(-4.87)

-0.126***(-5.60)

MKTR 2.573***(8.87)

2.650***(9.21)

2.615***(9.21)

Constant 2.660***(5.09)

1.541***(2.83)

2.162***(4.13)

Observations 1201 1201 1201

F-stat 90.42*** 108.63*** 93.69***

Adjusted R2 0.5079 0.5239 0.5162

VIF 1.04∼1.79 1.04∼1.91 1.04∼1.79Note) 1. ***, ** and * denote the statistics are statistically significant at 1%, 5%, 10% level in two sided tests, respectively.

2. The dependent variable is the underpricing degree of the IPO firm measured by UPR.

Table 9: The Effects of shutting down IPOs market on Underpricing Ratioin Shanghai Stock Exchange

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and thelisting day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The IssuedShares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Category Model(1-1) Model(2-1) Model(3-1)

Variables Coefficient(t Value)

Coefficient(t Value)

Coefficient(t Value)

BEF -0.0004***(-3.40)

AFT 0.0002***(3.25)

B/A-D -0.289***(-3.84)

GAP 0.0005(0.99)

0.0002(0.35)

0.0001(0.18)

IPER 0.002(0.74)

0.0008(0.29)

0.003(1.03)

CPS -0.351***(-3.31)

-0.279**(-2.05)

-0.364***(-2.77)

SUB 0.329***(8.98)

0.344***(8.22)

0.346***(8.36)

SIZE -0.200***(-5.69)

-0.162***(-4.23)

-0.179***(-5.19)

MKTR 2.123***(4.43)

2.009***(3.96)

2.095***(4.15)

Constant 3.720***(4.65)

2.478**(2.52)

3.106***(3.55)

Observations 286 286 286

F-stat 49.18*** 62.15*** 63.64***

Adjusted R2 0.6132 0.6003 0.6061

VIF 1.04∼1.79 1.04∼1.91 1.04∼1.79

Note) 1. ***, ** and * denote the statistics are statistically significant at 1%, 5%,

10% level in two sided tests, respectively.

2. The dependent variable is the underpricing degree of the IPO firm measured by UPR.

Table 10: The Effects of shutting down IPOs market on Underpricing Ratioin Shenzhen Stock Exchange

Dependent Variable:UPR: Underpricing ratio. (Opening Price of the listing Day-Offer Price)/Offer Price Explanatory variables: BEF: The number of days betweenthe listing day and shut down the IPO market. AFT: The number of days betweenreopen the IPO market and the listing day. B/A-D: Before or after shut down theIPO market dummy. If the firm listed before shut down the IPO market, 0 otherwise1. Control variables: GAP: The number of days between the first notice and thelisting day. IPER: IPO Price Earning Ratio. (Offer Price/Earning Per Share of theLast Year) CPS: Cost Per Share. (Total Issue Cost/The Circulation) SUB: NaturalLogarithm of The Subscription Ratio. ln(Subscription Ratio) SIZE: The scale ofthe public offering. Natural logarithm of Offer Price × The Number of The IssuedShares MKTR: Market Return. The cumulative market return which accumulated from20days before the listing day.

Category Model(1-2) Model(2-2) Model(3-2)

Variables Coefficient(t Value)

Coefficient(t Value)

Coefficient(t Value)

BEF -0.0002**(-2.14)

AFT 0.0001**(2.37)

B/A-D -0.171***(-3.93)

GAP -0.0005**(-2.34)

-0.0006**(-2.57)

-0.001**(-2.38)

IPER -0.001(-1.16)

-0.001*(-1.71)

-0.00005(-0.05)

CPS -0.070***(-3.49)

-0.063***(-3.16)

-0.073***(-3.59)

SUB 0.276***(12.24)

0.288***(12.33)

0.286***(12.35)

SIZE -0.170*** -0.171*** -0.161***

(-4.46) (-4.46) (-4.23)

MKTR 2.723***(8.12)

2.732***(8.26)

2.788***(8.37)

Constant 2.895***(3.53)

2.716***(3.27)

2.625***(3.20)

Observations 915 915 915

F-stat 62.59*** 58.90*** 63.29***

Adjusted R2 0.4897 0.4902 0.4973

VIF 1.04∼1.79 1.04∼1.91 1.04∼1.79Note) 1. ***, ** and * denote the statistics are statistically significant at 1%, 5%,

10% level in two sided tests, respectively.

2. The dependent variable is the underpricing degree of the IPO firm measured by UPR.

2001.09.10~2001.11.29

2005.05.25~2006.06.022004.08.26~2005.01.23 2008.09.16~2009.06.29

ClosePeriod

ClosePeriod

ClosePeriod

ClosePeriod

Figure 1: the Timeline of China Shut the IPOs

... . . . . . 3 2 1 0 ... . . . 3 2 1 00 1 2 3 . . . . . .. 0 1 2 3 . . . ... DAY

ClosePeriod AfterAfterClose

PeriodBefore

Expected trend of the underpricing degree

Figure 2: When China Shut Down the IPO Market

Before

Related Documents