CLARKSON RESEARCH SERVICES LTD Hamburg Schifffahrts-Dialog 17 th April 2014 Shipping Markets: In the Middle of a Revolution? Martin Stopford President, Clarkson Research Macr-managements meets micro-management

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CLARKSON RESEARCH SERVICES LTD

Hamburg Schifffahrts-Dialog 17th April 2014

Shipping

Markets:

In the Middle of

a Revolution?

Martin Stopford President,

Clarkson Research

Macr-m

anagem

ents

meets

mic

ro-m

anagem

ent

CLARKSON RESEARCH SERVICES LTD

1. Market Overview

2. The Case for Change

3. Four Questions for the Future:- 4.1 What will the trade scenario be like?

4.2 Fossil Fuels – impact of high prices?

4.3 Diminishing marginal returns?

4.4 Micromanagement -key to the future?

The challenge

is to change

The big picture trends in the shipping industry today & tomorrow

CLARKSON RESEARCH SERVICES LTD

I LOVE

SHIPPING I still don’t

seem to be

making any

money

Bankers

arrested

my ships

I made

millions on

timecharters

A charming young

man at an equity

fund offered me

$1 billion, sir

CLARKSON RESEARCH SERVICES LTD

Crude Tanker, Bulk Carrier & Container Earnings

0

20

40

60

80

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

'04

Jan

'05

Jan

'06

Jan

'07

Jan

'08

Jan

'09

Jan

'10

Jan

'11

Jan

'12

Jan

'13

Jan

'14

$000/day

Containership

Bulk Carrier $000/day

Crude Tanker $000/day

Compares average earnings over the last 12 months for crude tankers,

Bulkers & containerships under 3500 TEU

Depreciation –

over 20 yrs

OPEX

Updated March 2014

12 month earnings smooths the bumps, showing what owners are banking

Container12 month earnings trend

CLARKSON RESEARCH SERVICES LTD

-18

-13

-8

-3

2

7

12

17

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

OECD

Asia less China & JapanChina

1. Sea trade follows GNP cycles 2) Cycle every 7 years 3) Now in 6th

year of growth

% growth

World Economy Edging Up

China slowing

OECD

recovering

Credit

Crisis Dot.com

Crisis

Updated Mar 2014

CLARKSON RESEARCH SERVICES LTD

-5%

0%

5%

10%

15%19

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

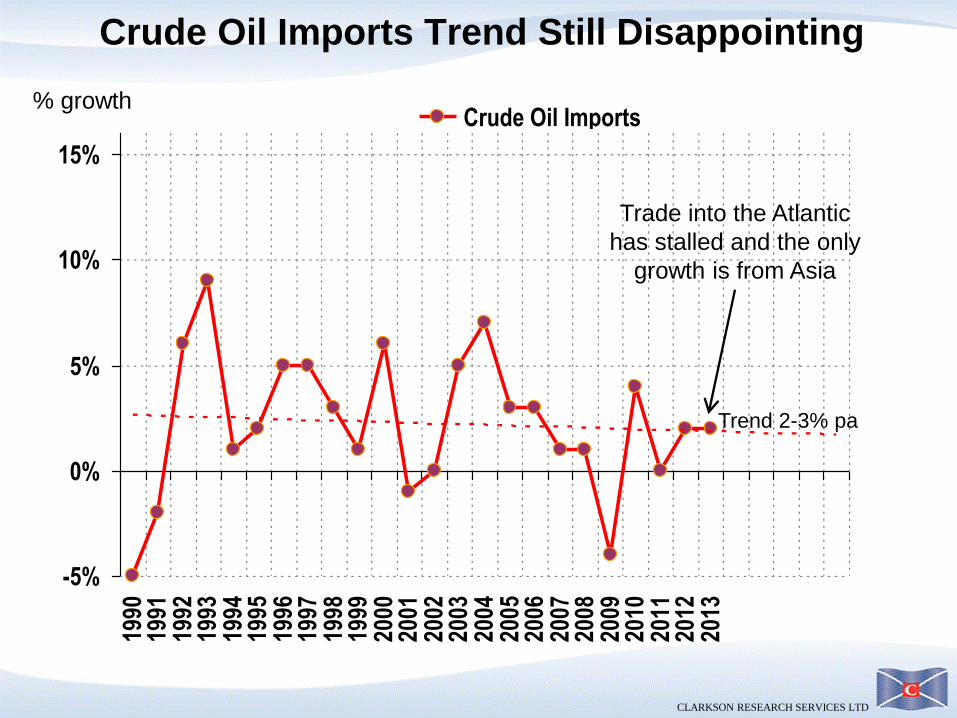

Crude Oil Imports% growth

Trend 2-3% pa

Crude Oil Imports Trend Still Disappointing

Trade into the Atlantic

has stalled and the only

growth is from Asia

CLARKSON RESEARCH SERVICES LTD

-5%

0%

5%

10%

15%19

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14

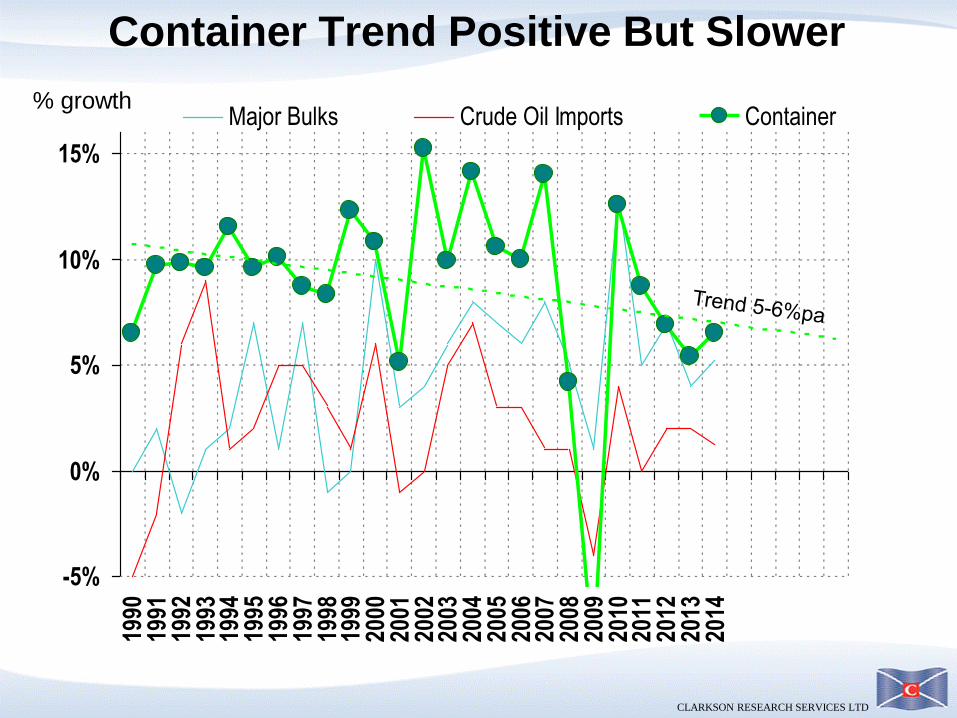

Major Bulks Crude Oil Imports% growth

Dry Bulk Growth Trend Positive

CLARKSON RESEARCH SERVICES LTD

-5%

0%

5%

10%

15%19

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14

Major Bulks Crude Oil Imports Container% growth

Container Trend Positive But Slower

CLARKSON RESEARCH SERVICES LTD

0

200

400

600

800

1,000

1,200

1,400

1,6001

96

31

96

51

96

71

96

91

97

11

97

31

97

51

97

71

97

91

98

11

98

31

98

51

98

71

98

91

99

11

99

31

99

51

99

71

99

92

00

12

00

32

00

52

00

72

00

92

01

12

01

3

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

World Merchant Fleet Growth Million dwt (year end)

Growth rate of the

fleet (right axis)

Has dropped below

4%pa but still

above 1990s rate

% fleet growth

CLARKSON RESEARCH SERVICES LTD

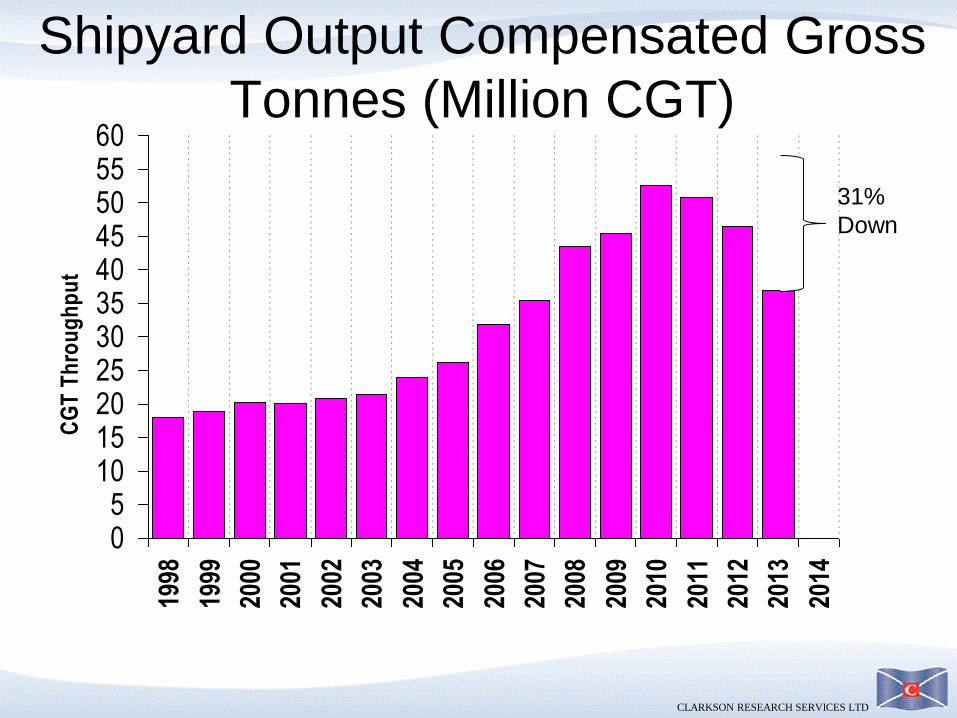

Shipyard Output Compensated Gross

Tonnes (Million CGT)

05

1015202530354045505560

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

CG

T T

hro

ug

hp

ut

31%

Down

CLARKSON RESEARCH SERVICES LTD

Laid Up Tonnage

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

M d

wt

Bulkers TankersShows tonnage of ships laid up on a monthly basis

Laid up tonnage (not

really tracked) is still low.

Surplus absorbed by

slow steaming, waiting

etc

% on T/C

CLARKSON RESEARCH SERVICES LTD

World Fleet

0

20

40

60

80

100

120

140

160

180

Other

Bulk Carriers

Tankers

Not much scope for

demolition

This chart shows the fleet by year of build.

Today there is little tonnage over 20 years old to support demolition

Age profile of the world fleet

CLARKSON RESEARCH SERVICES LTD

0

10

20

30

40

50

60

70

80

90

100Ja

n-9

0

Jan-9

2

Jan-9

4

Jan '9

6

Jan-9

8

Jan-0

0

Jan-0

2

Jan-0

4

Jan '0

6

Jan '0

8

Jan '1

0

Jan '1

2

June '1

3

pri

ce $

mil

lio

n

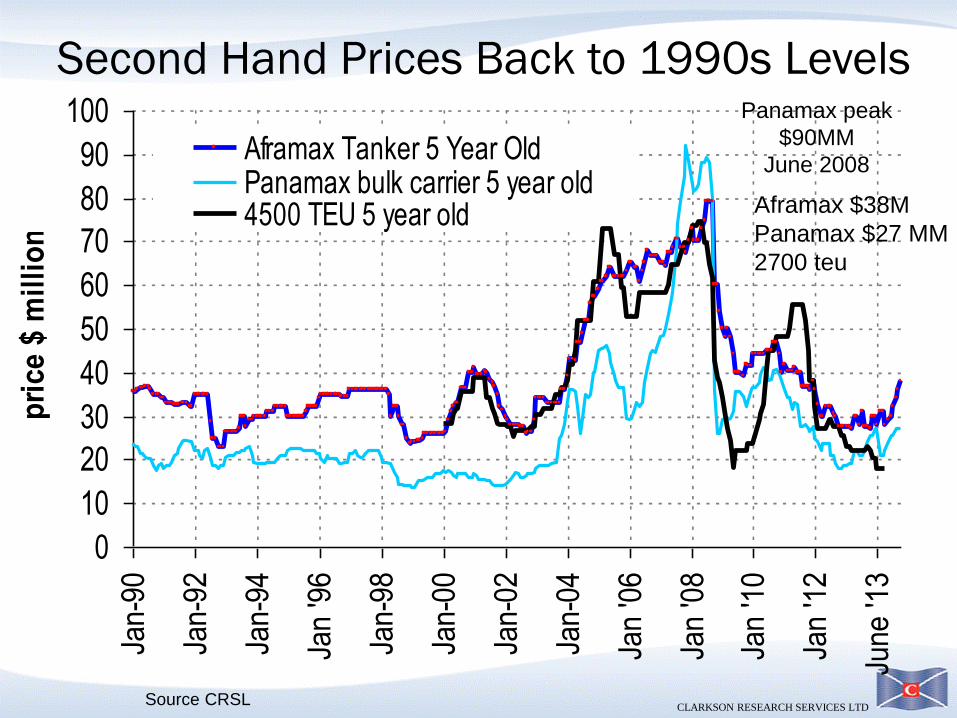

Aframax Tanker 5 Year OldPanamax bulk carrier 5 year old4500 TEU 5 year old

Panamax peak

$90MM

June 2008

Second Hand Prices Back to 1990s Levels

Source CRSL

Aframax $38M

Panamax $27 MM

2700 teu

CLARKSON RESEARCH SERVICES LTD

0

20

40

60

80

100

120

140

1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

$ millionVLCC Suezmax Aframax Tanker

Products Capesize Panamax Bulk

30,000 dwt bulker 1600 TEU 6700 TEU

Source: Compiled from several sources including Fearnleys, CRSL

Shipbuilding Prices Edging Up

Aframax

$54.5 MM

Panamax

$29.5 MM

CLARKSON RESEARCH SERVICES LTD

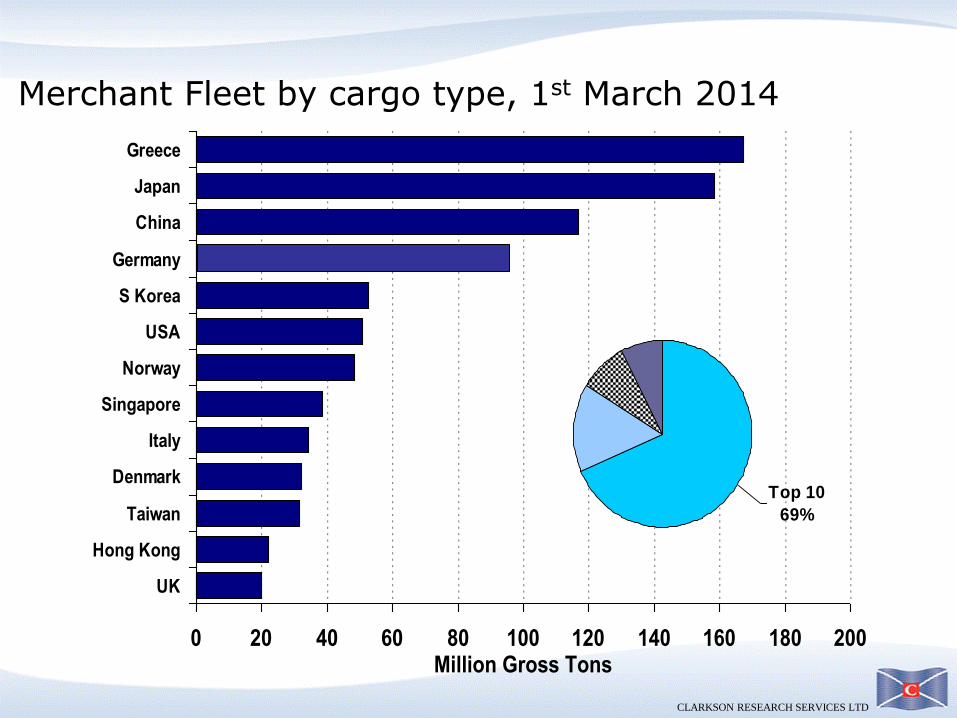

0 20 40 60 80 100 120 140 160 180 200

Greece

Japan

China

Germany

S Korea

USA

Norway

Singapore

Italy

Denmark

Taiwan

Hong Kong

UK

Million Gross Tons

Top 10

69%

Merchant Fleet by cargo type, 1st March 2014

CLARKSON RESEARCH SERVICES LTD

Shipping – Many Small Companies

Company Size** Number of

Companies

Number of

vessels m.GT

% of fleet

(no. of vessels)

% of fleet

(GT)

Ships per

Company

Small (1-5) 5,577 9,818 167.0 25% 15% 1.8

Small (6-10) 999 5,878 124.5 15% 11% 6.0

Medium (11-20) 657 7,405 192.0 19% 17% 11.3

Large (21-50) 373 8,326 300.3 21% 27% 22.3

Very Large (51-100) 101 5,196 183.7 13% 17% 51.4

XXL (100+) 22 2,899 141.2 7% 13% 131.8

Total 7,729 39,522 1108.7 5.1

*Based on Beneficial Owner, excludes unknown owners

World fleet by company size vessels >2,000 GT

**Company size based on full fleet >100 GT

CLARKSON RESEARCH SERVICES LTD

• In 1790 shipping had not changed for centuries

• Small wooden ships were built of expensive imported timber (see right)

• masts, timber spars and hessian ropes restricted size to 300 tonnes.

• Today we have MOVED ON…

Source: Biblioteque Nationale, Paris, Photo M. Cabaud Even with a crane

it took four men to

handle this bundle

So where do we go next?

CLARKSON RESEARCH SERVICES LTD

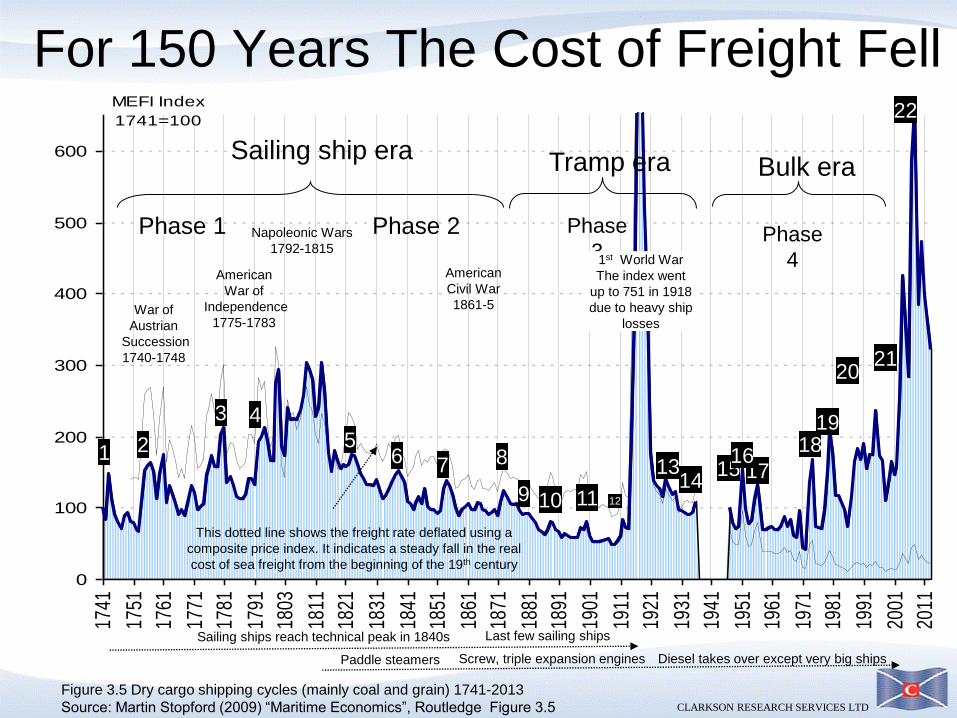

0

100

200

300

400

500

600

1741

1751

1761

1771

1781

1791

1803

1811

1821

1831

1841

1851

1861

1871

1881

1891

1901

1911

1921

1931

1941

1951

1961

1971

1981

1991

2001

2011

MEFI Index

1741=100

1 2

3 4

7 8

10 11 12

13 14 17 15

16 18

19

20 21

22

Sailing ship era

Phase 1 Phase 2

Tramp era

Phase

3

6 5

Napoleonic Wars

1792-1815

War of

Austrian

Succession

1740-1748

American

War of

Independence

1775-1783

American

Civil War

1861-5

1st World War

The index went

up to 751 in 1918

due to heavy ship

losses

Figure 3.5 Dry cargo shipping cycles (mainly coal and grain) 1741-2013

Source: Martin Stopford (2009) “Maritime Economics”, Routledge Figure 3.5

Sailing ships reach technical peak in 1840s Last few sailing ships

Paddle steamers Screw, triple expansion engines Diesel takes over except very big ships

This dotted line shows the freight rate deflated using a

composite price index. It indicates a steady fall in the real

cost of sea freight from the beginning of the 19th century

9

For 150 Years The Cost of Freight Fell

Bulk era

Phase

4

CLARKSON RESEARCH SERVICES LTD

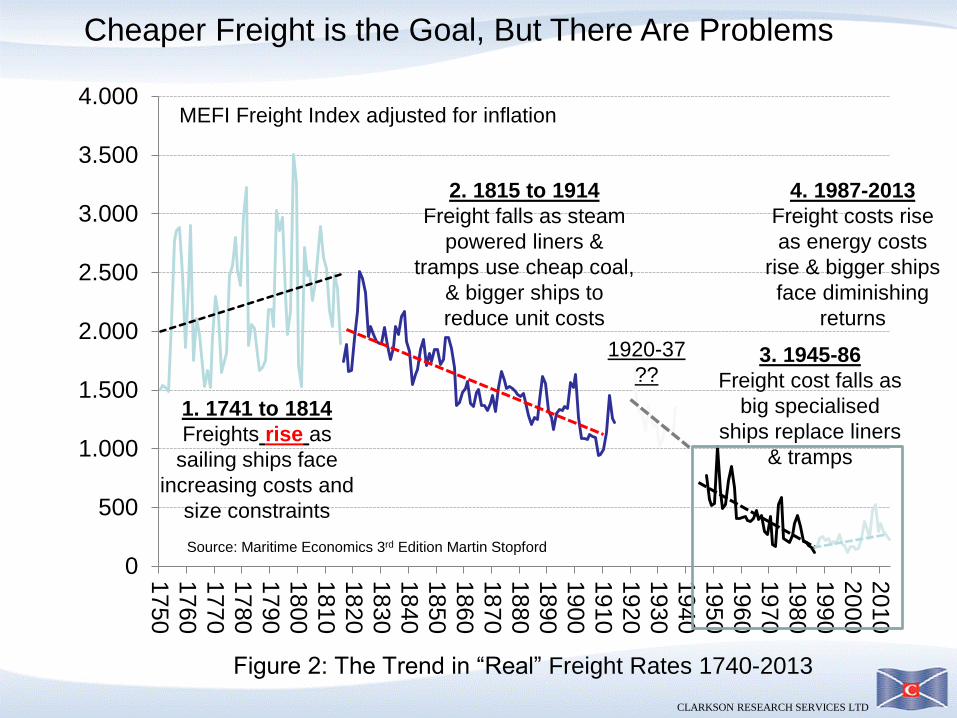

Figure 2: The Trend in “Real” Freight Rates 1740-2013

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

1750

1760

1770

1780

1790

1800

1810

1820

1830

1840

1850

1860

1870

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

Source: Maritime Economics 3rd Edition Martin Stopford

MEFI Freight Index adjusted for inflation

1. 1741 to 1814

Freights rise as

sailing ships face

increasing costs and

size constraints

2. 1815 to 1914

Freight falls as steam

powered liners &

tramps use cheap coal,

& bigger ships to

reduce unit costs

3. 1945-86

Freight cost falls as

big specialised

ships replace liners

& tramps

4. 1987-2013

Freight costs rise

as energy costs

rise & bigger ships

face diminishing

returns

1920-37

??

Cheaper Freight is the Goal, But There Are Problems

CLARKSON RESEARCH SERVICES LTD

Trends in “Real” Freight Rates 1947-2013

0

100

200

300

400

500

600

700

800

900

1000

1947

1951

1955

1959

1963

1967

1971

1975

1979

1983

1987

1991

1995

1999

2003

2007

2011

Source: Maritime Economics 3rd Edition Martin Stopford

MEFI Freight Index deflated by price index

1945-86

Mechanization of cargo

handling & bigger ships

reduce unit freight costs by

75% between 1947 and

1987

1987-2013

Rising oil fuel prices; &

diminishing returns from

bigger ships increase

freight costs by 66%

CLARKSON RESEARCH SERVICES LTD

Fifty years ago the

next phase was big

ships, big hubs and

East-West Trade.

What can be done

today to reverse

today’s rising unit

cost trend?

THE

MESSAGE

CLARKSON RESEARCH SERVICES LTD

Europe’s Voyages of discovery

24/04/2014 ©Martin Stopford 22

Ship

pin

g D

rivers

Tomorrow’s Trade

Fossil Fuels

Mechanization

Information

MEGA TREND

ignore

Sometimes CHANGE is

the only option

CLARKSON RESEARCH SERVICES LTD

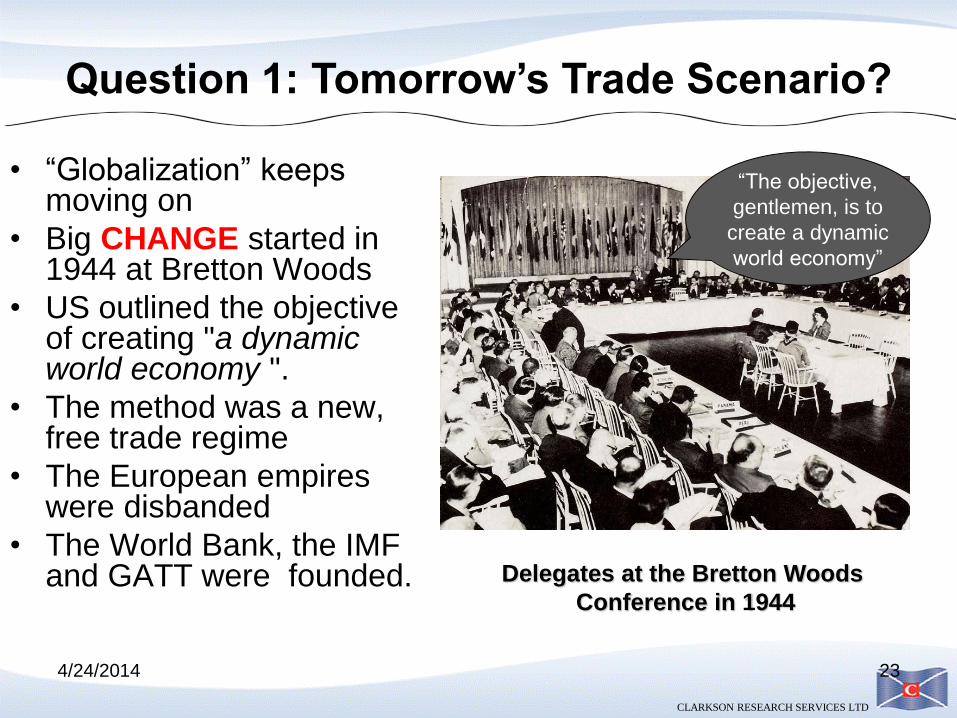

4/24/2014 23

• “Globalization” keeps moving on

• Big CHANGE started in 1944 at Bretton Woods

• US outlined the objective of creating "a dynamic world economy ".

• The method was a new, free trade regime

• The European empires were disbanded

• The World Bank, the IMF and GATT were founded. Delegates at the Bretton Woods

Conference in 1944

“The objective,

gentlemen, is to

create a dynamic

world economy”

Question 1: Tomorrow’s Trade Scenario?

CLARKSON RESEARCH SERVICES LTD

Volume of Trade is Growing

• Sea trade increased from 500 Mt in 1950 to 7 Bt in 2005 (Figure 1.11).

• Growth led by Europe and Japan.

• Multinationals expanded steel, aluminum, oil using imported materials.

• Big ships reduced sea transport costs 0

1

2

3

4

5

6

7

8

9

19

50

19

60

19

70

19

80

19

90

20

00

20

10

Bill

ion

to

ns

of

carg

o

Source: United Nations Statistical Yearbooks

Europe

S.America

N.America

Africa

Asia

M. East Oceania Russia

In 55 years after the 2nd

world war seaborne imports

grew at 4.7% per annum,

except for a major recession

1979-87 when trade did not

increase

Figure 3 Seaborne imports by region 1950-2010

CLARKSON RESEARCH SERVICES LTD

Balance of Global Trade is Changing

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1960 1970 1980 1990 2000 2010

Atlantic

Shows the of Atlantic and Pacific Trade volume as a % of world trade

Atlantic Cargo has

fallen from 80% of world

trade to 46% in 2013

Pacific cargo

has increased

from 18% to

53% in 2013

CLARKSON RESEARCH SERVICES LTD

Future Trade Scenario Problematic? It’s the Field of Dreams Scenario

0

5

10

15

20

25

30

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

Bil

lio

n t

on

s t

rad

e

Total Trade

Sea Trade Scenario

26 billion tons of trade in 2055

may be too extreme. How can

the 50% cut in carbon footprint

be achieved?

How long to double again?

This shows 30 years,

averaging 2.25% pa

Cargo doubled from 5 bn to

10bn tonnes in 18 years

4.4%pa

CLARKSON RESEARCH SERVICES LTD

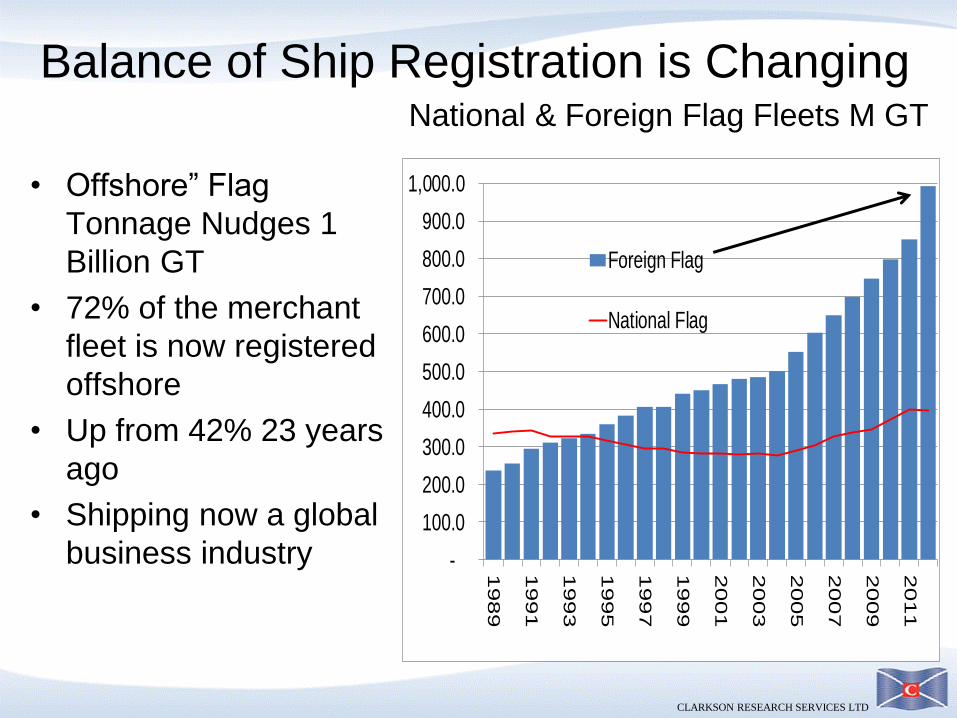

Balance of Ship Registration is Changing

• Offshore” Flag

Tonnage Nudges 1

Billion GT

• 72% of the merchant

fleet is now registered

offshore

• Up from 42% 23 years

ago

• Shipping now a global

business industry -

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1,000.0

1989

19

91

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Foreign Flag

National Flag

National & Foreign Flag Fleets M GT

CLARKSON RESEARCH SERVICES LTD

Question 2: Fossil Fuel – Impact of High Prices?

• Cheap and plentiful oil made sea

transport cheap.

• But in the last decade the

situation has changed:-

1. Bunker oil prices have trebled

2. Emission and carbon footprint

problems are escalating

• Both raise technical challenges

• The industry is not well equipped to

meet them

Source: Rollo Thompkins

CLARKSON RESEARCH SERVICES LTD

Today’s Oil Prices are Problematic

0

10

20

30

40

50

60

70

80

90

100

110

120

13018

6118

6718

7318

7918

8518

9118

9719

0319

0919

1519

2119

2719

3319

3919

4519

5119

5719

6319

6919

7519

8119

8719

9319

9920

0520

11

$ p

er b

arre

l

$ money of the day

Cheap oil encouraged bigger, faster ships

Bigger ships

can’t deal

with this cost

increase

CLARKSON RESEARCH SERVICES LTD

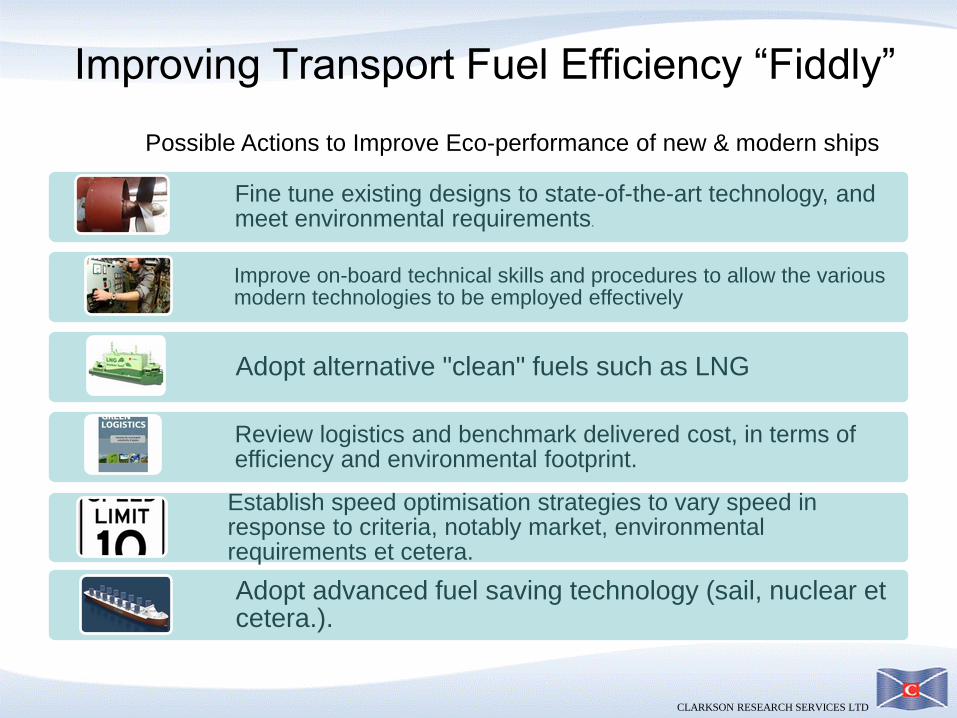

Improving Transport Fuel Efficiency “Fiddly”

Fine tune existing designs to state-of-the-art technology, and meet environmental requirements.

Improve on-board technical skills and procedures to allow the various modern technologies to be employed effectively

Adopt alternative "clean" fuels such as LNG

Review logistics and benchmark delivered cost, in terms of efficiency and environmental footprint.

Establish speed optimisation strategies to vary speed in response to criteria, notably market, environmental requirements et cetera.

Adopt advanced fuel saving technology (sail, nuclear et cetera.).

Possible Actions to Improve Eco-performance of new & modern ships

CLARKSON RESEARCH SERVICES LTD

Question 3: Diminishing Marginal Returns?

• In 1950 mechanization of

cargo handling was urgently

needed to carry rapidly

growing trade

• Ships were spending half

their time handling cargo

• Multinational cargo

companies drove the

process.

• Bigger, faster ships;

integrated cargo handling;

coastal processing plants

produced major cost savings

4/24/2014 31

Malcolm McLean, 1956, inventor of containerisation Complex cargo handling on Norwegian liner 1954 –

Ports were congested & ships unproductive

CLARKSON RESEARCH SERVICES LTD

Diminishing Returns From Size Increase

• Mechanization technology

is mature.

• Economies of scale face

diminishing returns.

• Cost saving of 5,000 dwt

size increase falls from

12% to 1.4% (blue bars)

• New ways to cut transport

costs are needed

• “Micro management” is the

best possibility

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0% -

50

100

150

200

250

35

50

65

80

95

11

0

12

5

14

0

15

5

17

0

Saving % (right axis)

Unit Cost/$/dwt (left axis)

Bulk carrier size 000 Dwt

Figure 6: Bulk Carrier Economies of Scale

BLUE BARS SHOW COST SAVINGS

DIMINISH AS SHIPS GETS BIGGER

CLARKSON RESEARCH SERVICES LTD

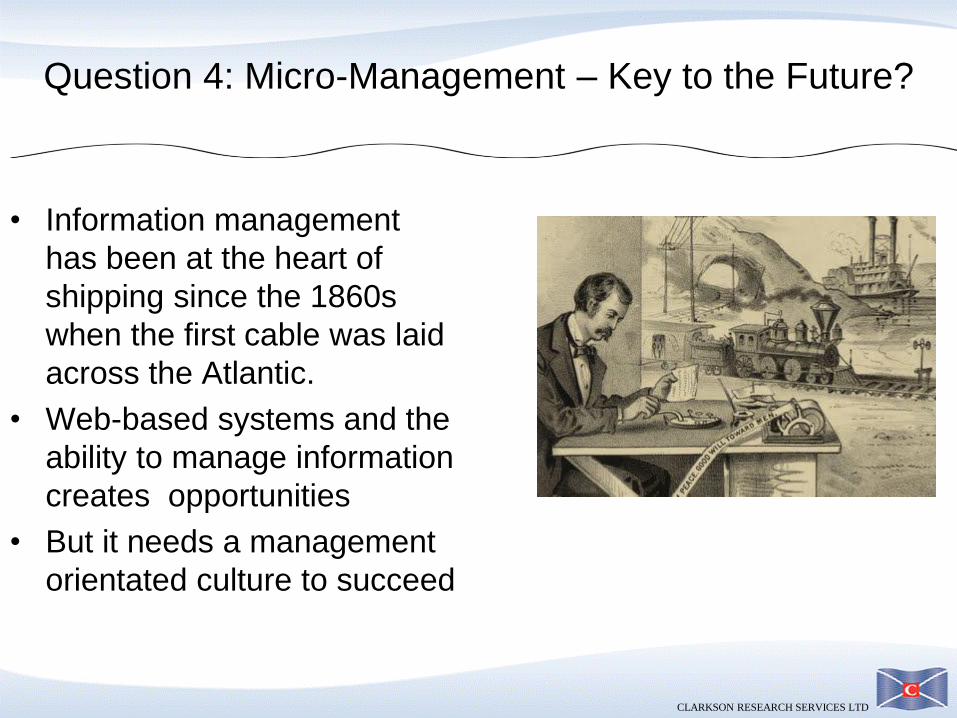

Question 4: Micro-Management – Key to the Future?

• Information management

has been at the heart of

shipping since the 1860s

when the first cable was laid

across the Atlantic.

• Web-based systems and the

ability to manage information

creates opportunities

• But it needs a management

orientated culture to succeed

CLARKSON RESEARCH SERVICES LTD

Information Technology & Micro-Management

Fibre optic cable network

Gordon

Moore

Invented “Moore’s Law”

CLARKSON RESEARCH SERVICES LTD

• The sea transport business is at the end of a

major phase dominated by mechanization of

cargo transport

• Today’s market based system focusses too

much on capital and not enough on the

management of transport

• After a century of freight cost reduction, freight

costs increasing due to the diminishing

marginal return on investment in ever-bigger

ships and rising fuel cost

• If cargo volume doubles in 30 years we need

more efficient transport; cheaper freight;

smaller carbon footprint; zero pollution,

• Shipping needs a vision: micro management of

freight transport, building on the information

revolution--- and more engineers!

• But to do this the shipping industry needs a

management REVOLUTION

Shipping cycles

manage

investment, but

investors

MANAGE

strategy

CLARKSON RESEARCH SERVICES LTD

Seven Pressures for Change

1. Ship Technology Mature

2. Low returns

3. Energy costs high & rising

4. Climate Change

5. Geopolitics

6. Market driven business

7. China maturing

When Alexander saw the breadth of his domain he wept, for there

were no more worlds to conquer

CLARKSON RESEARCH SERVICES LTD

150 Years of Global Information….

10

33 33

39

50

90 90 92

90 89 89 89

-

10

20

30

40

50

60

70

80

90

100

1870

1883

1884

1885

1886

1900

1901

1902

1903

1904

1905

1906

Number messages (millions)

• In 1855 the first cable was laid across the Atlantic, but after 40 days it stopped working.

• In 1866 another successful trans-Atlantic cable was laid.

• In 1871 a cable was laid to India and Hong Kong

• By 1897 162,000 nautical miles of cable had been laid

• The impact on shipping logistics was profound

Source: Encyclopaedia Britannica 1910

CLARKSON RESEARCH SERVICES LTD

020406080

100120140160180200220240

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

20

20

20

25

20

30

20

35

Oil

Pri

ce/b

arr

el

Oil Price Future actual

1993 forecast 1994 forecast

1995 forecast 1998 forecast

2000 forecast 2004 forecast

2006 forecast 2007 forecast

2008 forecast 2010 "Current Policies"

Source: BP energy review

2008

2007

2006

Oil Price Estimates “Unreliable”

2010

2005 & earlier

Related Documents