Cardiff University - Cardiff Business School MSc in Marine Policy 2014/2015 BST122 Shipping Economics Professor: Dr Wessam M.T. Abouarghoub Student: Mavrokefalos Ioannis 1473023 Coursework “Choose a shipping company and discuss the different types of risks they face in the short- and long-run. Using empirical statistical data and market reports from Clarksons Shipping Intelligence Network and Lloyd’s List expand your argument to include the following: Uncertainty in supply and demand Current opportunities and future threats to the company’s core business

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Cardiff University - Cardiff Business School

MSc in Marine Policy 2014/2015

BST122 Shipping Economics

Professor: Dr Wessam M.T. Abouarghoub

Student: Mavrokefalos Ioannis 1473023

Coursework

“Choose a shipping company and discuss the different types

of risks they face in the short- and long-run. Using

empirical statistical data and market reports from

Clarksons Shipping Intelligence Network and Lloyd’s List

expand your argument to include the following:

Uncertainty in supply and demand

Current opportunities and future threats to the

company’s core business

The different type of operational and financial risks

they are exposed to in the short and long term

The level of market competitiveness”

Introduction

The motivation behind this assignment is to illustrate

the significance of the different types of risks that a ship-

owner company faces. More specifically, we will examine the

tanker segment of interest. The relationship between the

shipping trade and the oil markets is bidirectional. That

means that oil markets would not exist without ships to

transfer the oil and conversely ship-owners would not have the

opportunity to maximize their profits through tanker markets

without the oil markets’ presence. Different types of risk

arise in two periods, the short-run and the long-run. Hence,

constructive and efficient risk management must be applied in

order to avoid negative and disastrous for the shipping

companies consequences. The analysis will be supported with

empirical statistical data and market reports from Clarkson’s

Shipping Intelligence and Lloyd’s List as also online reports

from the webpage of many International Organizations like

OPEC, OECD, and IEA. The Greek shipping Company that will be

used as a benchmark in this assignment is the Tsakos Energy

Navigation Limited, a provider of Crude Oil transportation

services and operates a fleet of 54 new built crude oil

vessels.

Page 2 of 21

The benchmark Shipping Company

Page 3 of 21

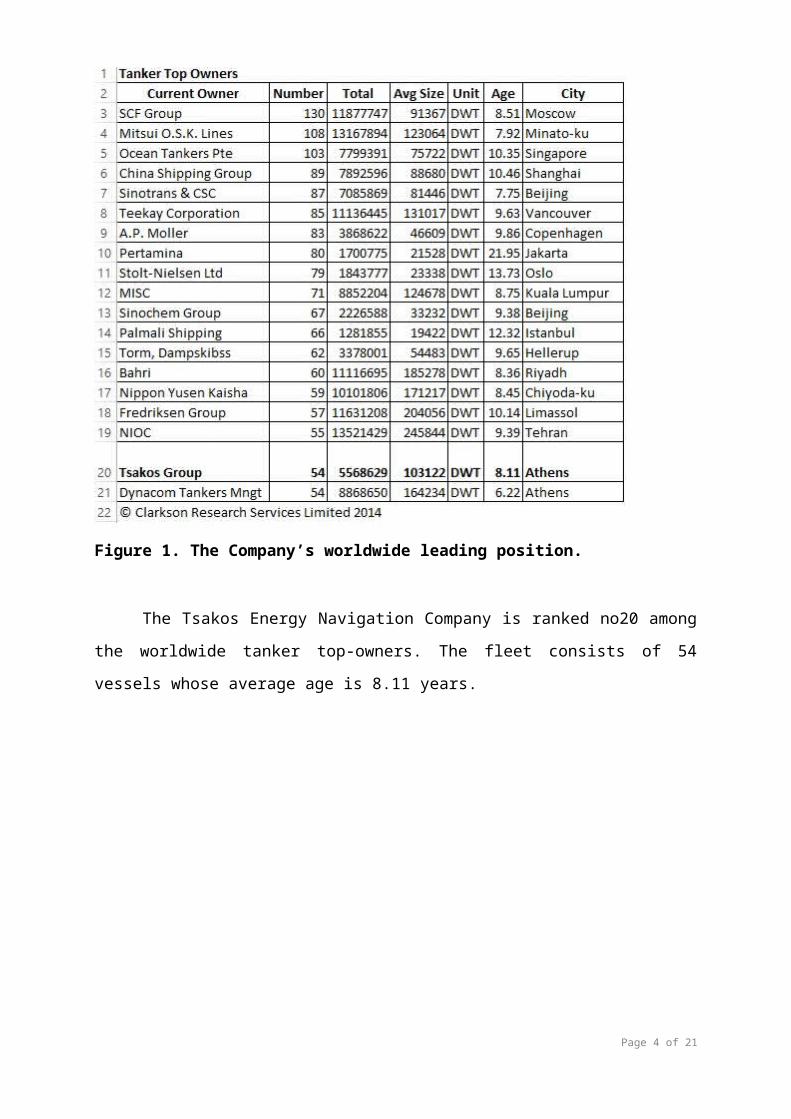

Figure 1. The Company’s worldwide leading position.

The Tsakos Energy Navigation Company is ranked no20 among

the worldwide tanker top-owners. The fleet consists of 54

vessels whose average age is 8.11 years.

Page 4 of 21

Uncertainty in Supply and Demand

As shipowners put it: «When I wake up in the morning and

freight rates are high I feel good. When they are low I feel

bad». The above statement depicts the mood of the shipowners

as formed by the freight rates, which are the result of the

equation of the supply and demand sector of the shipping

market.

The crude oil and petroleum shipping industry is a

complex procedure. It is cyclical with an inherent volatility,

regarding charter hire rates and profits. Charter hire rates

for oil product vessels remained low in 2008 with the

exception of some brief respite. Moreover, hire and spot rates

for large crude carriers remained low since 2010, even

resulting in rates well below break-even. The freight rates

for 29 of the ships owned by subsidiary companies vary and the

time charters for seven of the vessels owned by the subsidiary

companies may expire in less than six months if not renewed

(Tsakos Energy Navigation Report in Lloyd’s List

Intelligence). Consequently, the company will be subject to

changes in the charter rates which could have an impact on

earnings and the value of its vessels.

It is obvious that the factors affecting the supply and

demand for vessels are outside the company's control. The main

factor contributing to risk creation is the uncertainty in

supply and demand. As far as demand is concerned, the five

variables that influence it are (1) world economy, (2)

Page 5 of 21

seaborne commodity trades, (3) average haul, (4) random shocks

(5) transport costs. The five variables which influence the

supply side are (1) the world fleet, (2) the fleet

productivity, (3) shipbuilding production, (4) scrapping and

losses and (5) freight revenue (Stopford 2009).

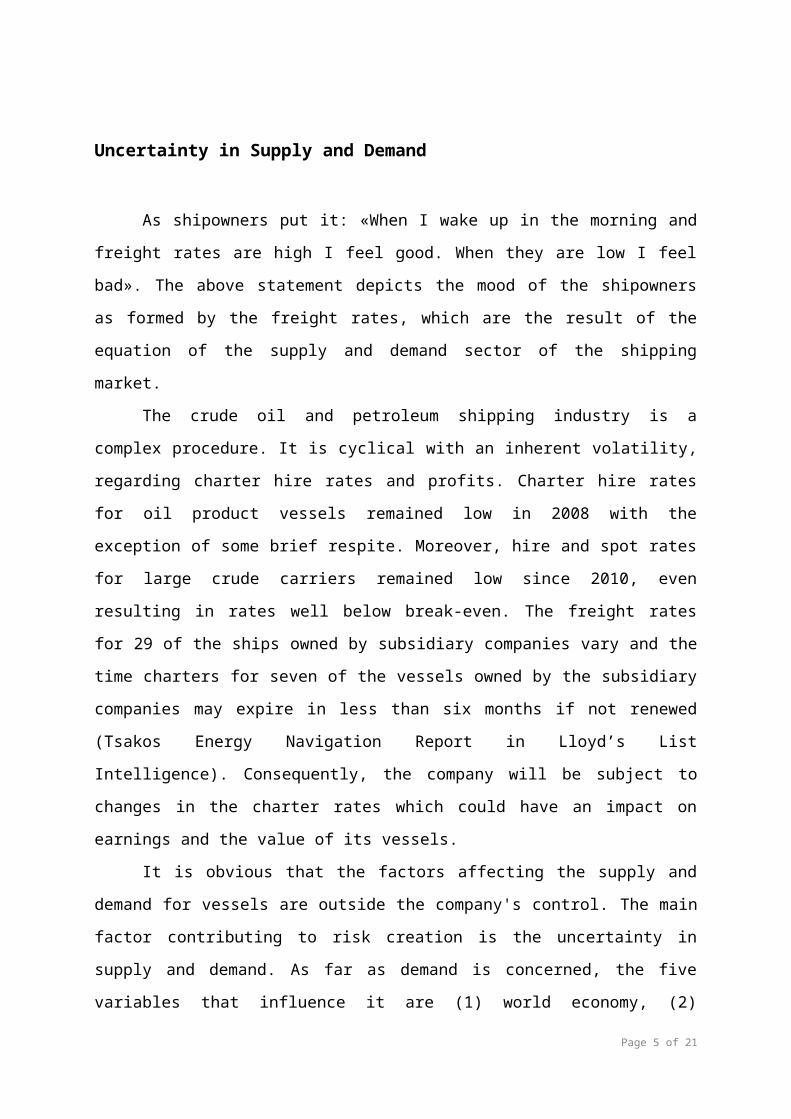

Figure 2. Key influences of Demand Side of Oil Market

(Clarkson’s).

The above findings concerning the Key influences of

Demand Side of Oil Market can be supported by the OECD - IEA

2014 report whose main findings concerning the World Oil

Demand are the following:

Page 6 of 21

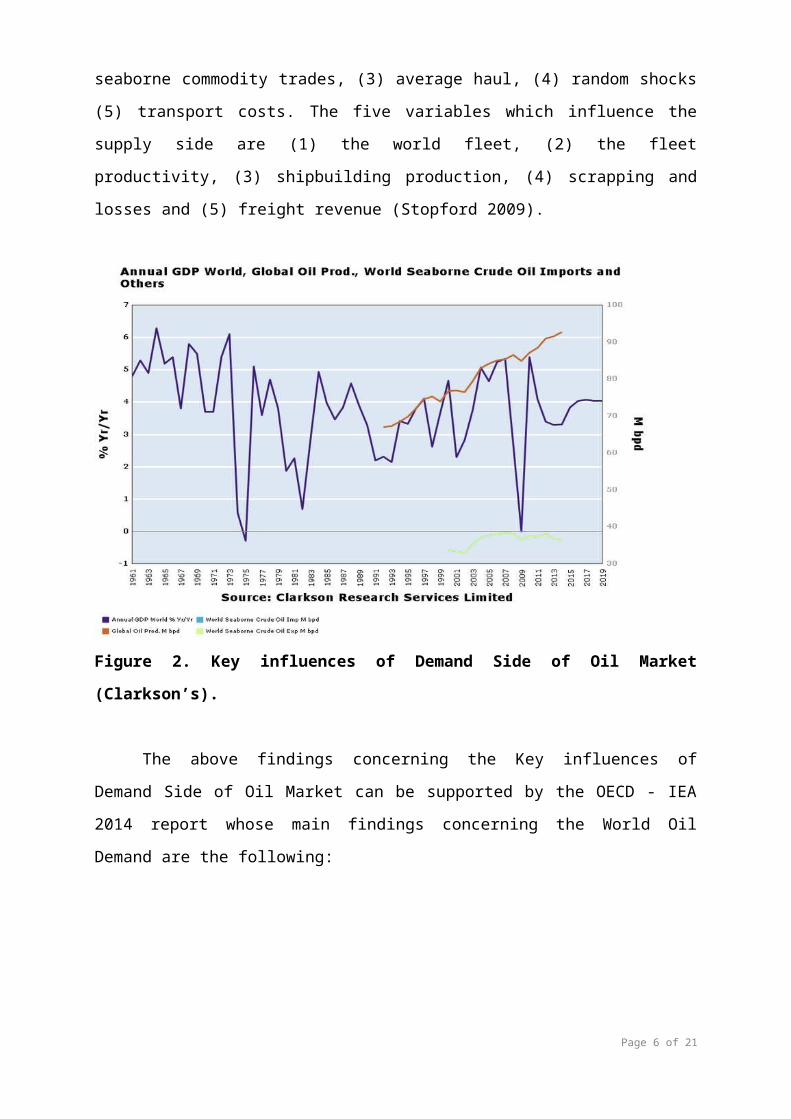

Figure 3. The prospective World Oil Demand (OECD-IEA Report

2014).

The most important findings of the Report are: (1) Global

oil supply inched up by 0.035 mb/d in October to 0.094 mb/d

and OPEC supply increased by 1.8 mb/d. (2) The OPEC output

fell by 0.15 mb/d in October to 30.60 mb/d, remaining above

the group's 30 mb/d supply target. (3) Global oil demand

evaluations for 2014 and 2015 are unaffected since last

month's Report, at 92.4 mb/d and 93.6 mb/d, correspondingly.

Development will rise from a five-year annual low of 0.68 mb/d

in 2014 to an estimated 1.1 mb/d next year (OECD-IEA Report

2014)

Figures 2 and 3 describe the stabilization and

augmentation trends that seem to prevail in Oil market Demand

while Figure 4 below shows that supply sector will expand too

in the years to come in order to support the increase of the

demand sector.

Page 7 of 21

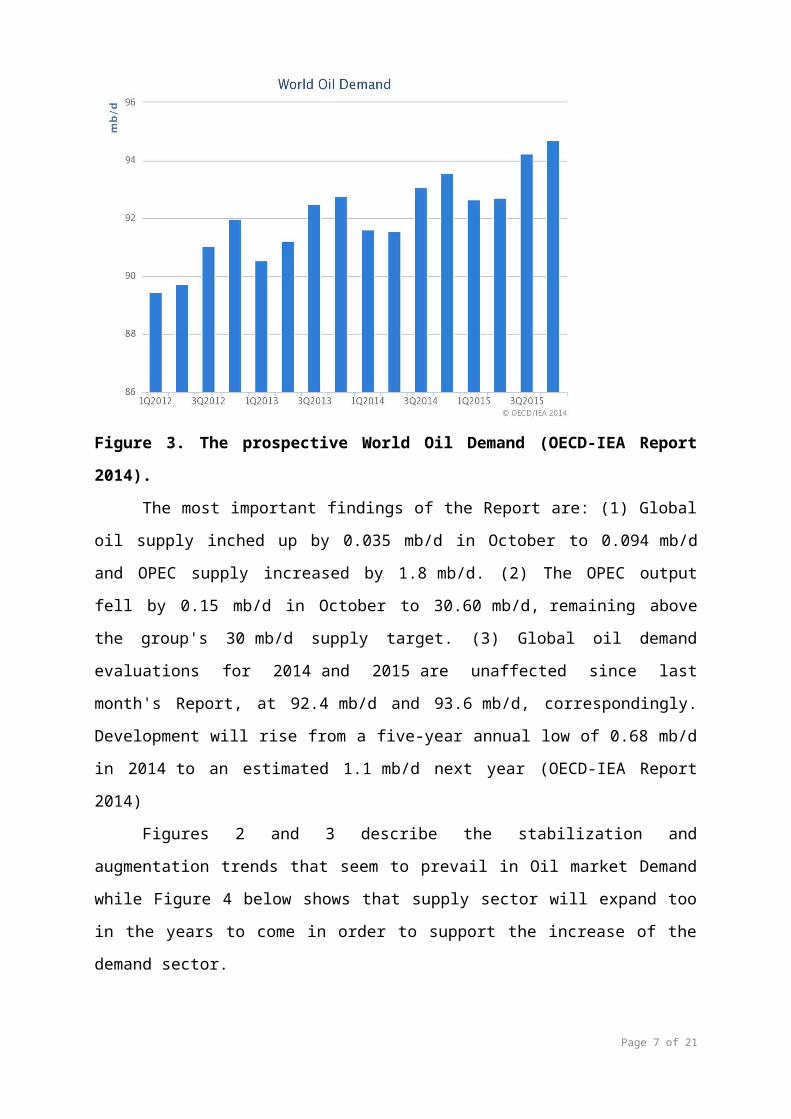

Figure 4. Key influences of Supply Side of Oil Market

(Clarksons).

The most significant conclusion of the previous chart

analysis is the trend of the shipping sector of the economy to

extend in the years to come. According to industry observers,

there has been revitalization in demand for oil globally and

if it falters, the production and the demand of crude oil and

its products will face a new pressure. Hence, the Company will

face the risk of decreased shipments and as a result the

employment of vessels and the charter rates earned from spot

charters will be affected. Eventually, on time-charters with

profit-share may rank low, or even worse deteriorated.

The crucial fluctuations in demand and supply and

especially the growth of the supply are to a great extent

caused by the shipowners’- investors’ actions. Such an action

is the ordering of new vessels. Hence, the orderbook not only

contains a number of vessels under construction but the

Page 8 of 21

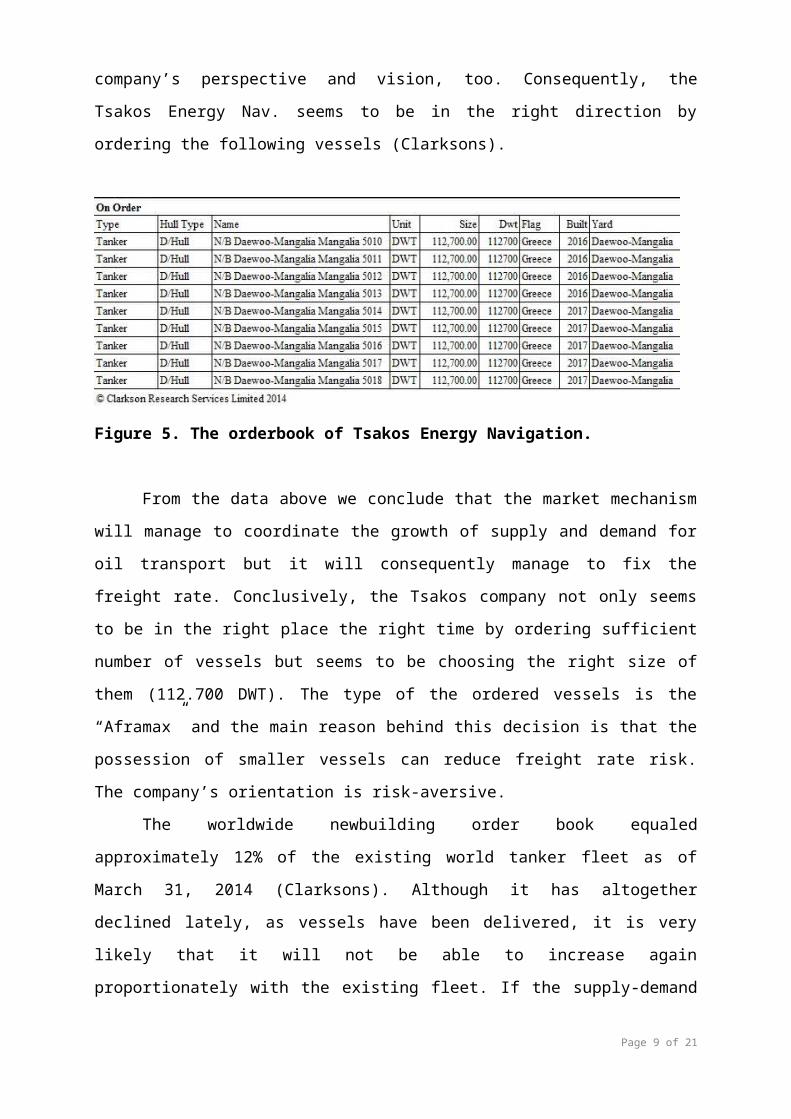

company’s perspective and vision, too. Consequently, the

Tsakos Energy Nav. seems to be in the right direction by

ordering the following vessels (Clarksons).

Figure 5. The orderbook of Tsakos Energy Navigation.

From the data above we conclude that the market mechanism

will manage to coordinate the growth of supply and demand for

oil transport but it will consequently manage to fix the

freight rate. Conclusively, the Tsakos company not only seems

to be in the right place the right time by ordering sufficient

number of vessels but seems to be choosing the right size of

them (112.700 DWT). The type of the ordered vessels is the

“Aframax” and the main reason behind this decision is that the

possession of smaller vessels can reduce freight rate risk.

The company’s orientation is risk-aversive.

The worldwide newbuilding order book equaled

approximately 12% of the existing world tanker fleet as of

March 31, 2014 (Clarksons). Although it has altogether

declined lately, as vessels have been delivered, it is very

likely that it will not be able to increase again

proportionately with the existing fleet. If the supply-demand

Page 9 of 21

ratio is disproportionate, the charter rates for the company's

vessels could drop significantly.

The Risk sources in the Shipping Industry along with

Shipping Market Cycles - Current opportunities and future

threats to the company’s core business.

“Technically, shipping risk can be defined as the

‘measurable’ liability for any financial loss arising from

unforeseen imbalances between supply and demand for sea

transport” (Stopford 2009). Additionally, Shipping companies

operate in shipping markets, where three different types of

Economic Cycles are observed: (1) short ‘business’ cycles

which last 5-10 years, (2) long shipping cycles which can last

up to 60 years and finally (3) seasonal cycles which

constitute the fluctuations of freight rates and occur within

a specific period of the year. Hence, different types of risks

are generated because of the company’s simultaneous operation

in different market cycles, which means that each risk belongs

to a specific cycle.

More specifically, shipowners may face eight different

risk types during their operation in the tanker market whichPage 10 of 21

are categorized into the following types (Kavussanos and

Visvikis 2006):

Business risk: Risk generated by volatility in freight rates

which cause uncertainty to the shipowner’s income, in other

words fluctuations in EBIT (Earnings Before Interest and

Taxes). It depends on the demand and the price of the product

sold. It is influenced by (a) freight rates, (b) voyage costs

(fuel costs, port charges, canal dues and broking

commissions), (c) operating costs (manning, repairs,

maintenance, stores, insurance and administration) and

finally, (d) exchange rates as income is counted in US dollars

while costs are counted in current exchange.

Business risk is developed in both Short and Seasonal

Cycles. These cycles (Schumpeter 1925) arise from the

fluctuations of the freight rates which are caused by changes

in the demand of sea transport. For example, in seasonal

cycles the stocking of oil in winter can peak the demand

cycles (Stopford 2009).

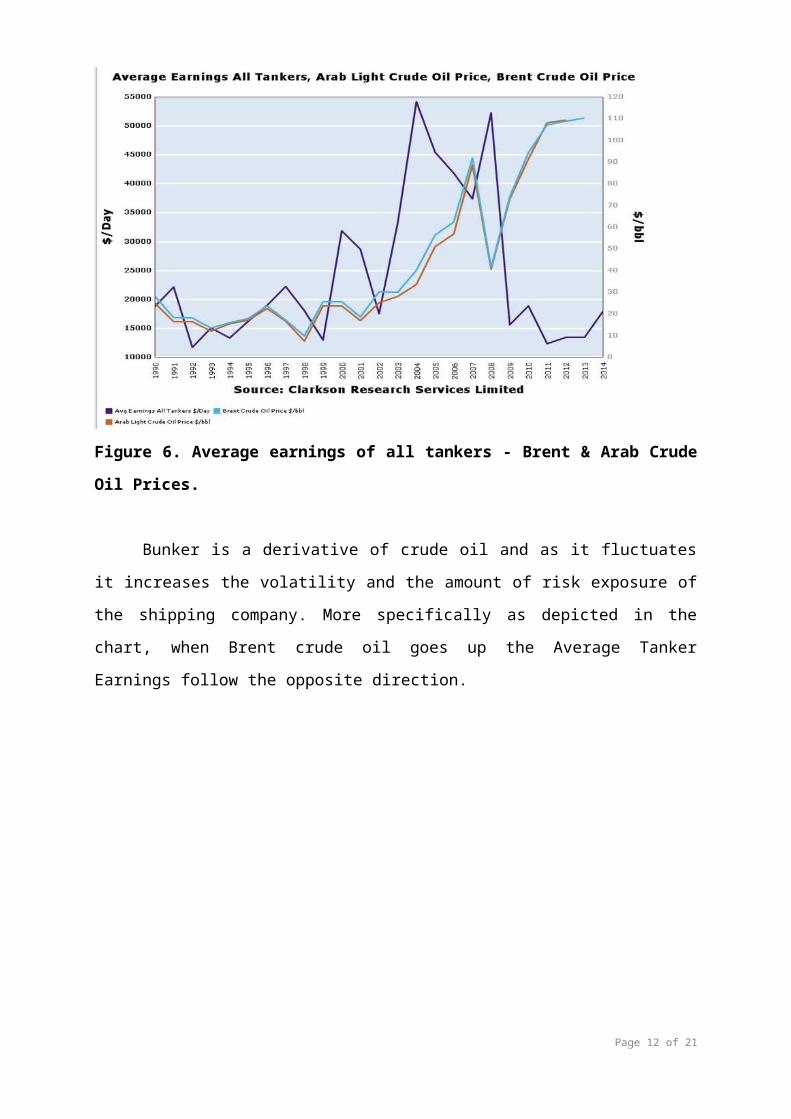

Furthermore, in Figure 6 below we distinguish the bunker price

fluctuations.

Page 11 of 21

Figure 6. Average earnings of all tankers - Brent & Arab Crude

Oil Prices.

Bunker is a derivative of crude oil and as it fluctuates

it increases the volatility and the amount of risk exposure of

the shipping company. More specifically as depicted in the

chart, when Brent crude oil goes up the Average Tanker

Earnings follow the opposite direction.

Page 12 of 21

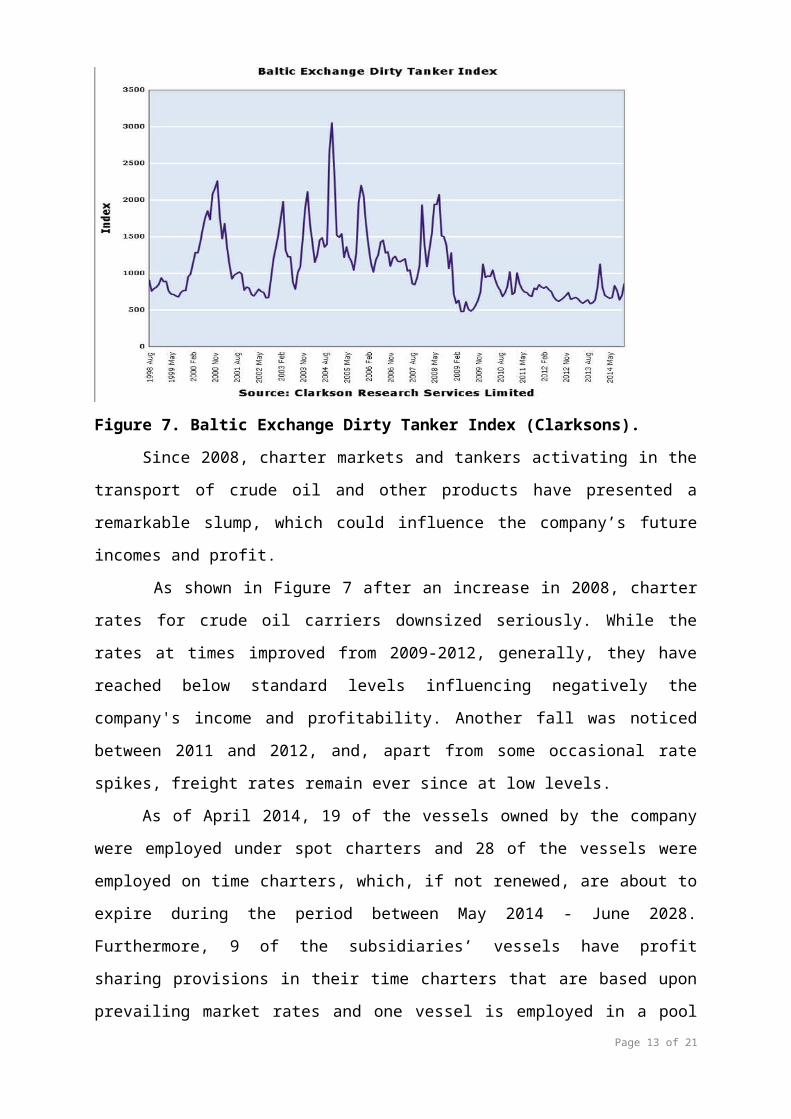

Figure 7. Baltic Exchange Dirty Tanker Index (Clarksons).

Since 2008, charter markets and tankers activating in the

transport of crude oil and other products have presented a

remarkable slump, which could influence the company’s future

incomes and profit.

As shown in Figure 7 after an increase in 2008, charter

rates for crude oil carriers downsized seriously. While the

rates at times improved from 2009-2012, generally, they have

reached below standard levels influencing negatively the

company's income and profitability. Another fall was noticed

between 2011 and 2012, and, apart from some occasional rate

spikes, freight rates remain ever since at low levels.

As of April 2014, 19 of the vessels owned by the company

were employed under spot charters and 28 of the vessels were

employed on time charters, which, if not renewed, are about to

expire during the period between May 2014 - June 2028.

Furthermore, 9 of the subsidiaries’ vessels have profit

sharing provisions in their time charters that are based upon

prevailing market rates and one vessel is employed in a poolPage 13 of 21

arrangement at variable rates (Lloyd’s List, Google Finance).

If low charter rates in the market reappear, in 2014, the

charter revenue from these vessels, and the EBIT will be

affected.

Liquidity Risk: Risk raised by the company’s failure to sell

company’s assets in a short time at market prices.

Default Risk: Risk caused by the company’s incapability to repay

its debt on borrowed funds (i.e. bonds).

Financial Risk: It is that type of risk generated by the way that

the shipping company finances its investments. Too much

borrowing increases the leverage which leads to a simultaneous

increase to the debt. Because of the fact that shipping market

is cyclical, high degree of leverage combined with high degree

of funds leads to disastrous consequences for the shipping

company’s finance. Hence, disruptions in global financial

markets and the ensuing legislative activity may have an

unfavourable impact on companies.

In recent years, global recession and credit markets

constitute the framework within which shipping companies

operate. The markets are influenced in such a way that fiscal

balances are threatened, public debt increases, supply of

credit falls and deleveraging in banking is a reality. Thus,

together with the current decline in charter rates and vessel

values, this economic situation is evidently full of risks

that can lead the company to unsuccessful and ineffective

operations and to unpredictable financial conditions, cash

flows or share prices.Page 14 of 21

Derivatives and Financial Risk Management (Alizadeh and Nomikos 2009)

upon Tsakos Energy Navigation

To manage being exposed to fluctuations of interest

rates, the Company enters into investment rate swap contracts

associated with its binding borrowings and bunker swap

contracts of bunker prices associated with the consumption of

bunkers by its vessels. Interest rate and bunker price

differentials under these swap agreements are considered to be

part of Interest and finance costs, net. All derivatives are

taken in the consolidated financial statements at their

objective value. On the inception date of the derivative

contract, the Company evaluates the derivative as a cash flow

hedge. Any change in the objective fair value of a derivative

that has the standards of a cash flow hedge is registered in

other income or loss until earnings are influenced by the

foreseen transaction.

Changes in the fair value of invalid derivative

instruments as well as the inefficient part of designated

derivative instruments are reported in profits in the

corresponding period. Registered gains or losses due to early

termination of undesignated derivative tools are also

considered as earnings in the period of termination of the

derivative instrument.

Typically, all risk- management objectives and policies

for undertaking various hedge procedures and all relationships

between hedging instruments and hedged items have to be

documented by the company.The Company also formally estimates,

both at the hedge’s beginning and on a permanent basis,Page 15 of 21

whether the derivatives used in hedging are extremely

effective in starting changes in cash flow of hedged items

(Gray 1986). When it is decided that derivatives are not

satisfactorily effective as a hedge or that it does not serve

its purpose anymore as a hedge, the company may decide to stop

hedging. Under these conditions, the net gain or loss remains

in accumulated other comprehensive income or loss and is

reclassified into earnings for the corresponding period,

unless there is not a probability for the forecasted

transaction.

Credit Risk: Risk created by the wrong and crucial decisions of the

business that may cause breach of agreement from the

charterers’ side to pay their obligations to the shipowners.

Market Risk: Risk faced by companies listed in the stock exchange

(i.e Tsakos Energy Navigation). It is caused by the changes in

stock prices, freight and interest rates.

Political Risk: Risk caused by political decisions and reasons such

as wars, political unrests and canal closures. For instance,

the Korean War of 1950, the Livian Revolution of 2011, the

Suez Canal closures of 1956, 1967 and 1973 and the two Gulf

Wars.

Technical and Physical Risk: Risk that every operating shipping

company faces and refers to the possibility of breaking down

the ship. Such incidents can lead to additional costs which

affect the shipowner’s income and can also damage the

business' reputation.Page 16 of 21

The term Long Shipping Cycles (Kondratieff 1925) refers

to the long-term social, technical (technological) and

political changes that take place in the shipping industry.

Political, technical and physical risks occur in Long Shipping

Cycles.

Page 17 of 21

The level of market competitiveness

Fleet operation is a process taking place in a highly

competitive global tanker industry and markets. Competition in

the tanker industry is immense and depends on a variety of

factors such as the willingness of potential charterers to

accept the available tankers. After the expiration of standing

charters there may be lack of new appealing contract rates. In

2013, the company derived approximately 52% of its profit from

time charters, as compared to 50% in 2012. As the current

period charters on nine of the vessels owned by subsidiary

companies expire in the remainder of the current year, re-

chartering these vessels at attractive rates may not be

possible given the depressed condition of the charter market.

If there are not appealing period charter opportunities

because of the competitiveness in the market, the company

would revert to chartering the vessels owned by subsidiary

companies in spot market, which is at low levels for some time

and is subject to continuous fluctuations. If a vessel owned

by a subsidiary company cannot be hired at a sustainable rate,

the vessel might be laid up until the rate becomes attractive

again. The lay-up being in progress, the vessel will keep on

cutting down on running costs such as crew wages, insurance

fees and maintenance costs.

Other factors include, the age of vessels, their price,

their size and general condition. Among the company's

competitors are the owners of VLCC, Suezmax, Aframax, Panamax,

Handymax and Handysize tankers. Other competitors include

owners in the shuttle tanker and LNG markets, who are

Page 18 of 21

independent tanker companies. Finally, there are some national

and independent oil companies that appear with great financial

status and capital resources.

References/Bibliography

Amir H. Alizadeh, Nomikos N (2009) Shipping derivatives and risk

management, 1st edn., New York: Palgrave Macmillan.

James Whiteside Gray (1986) Financial Risk Management in the Shipping

Industry, 1st edn., London: Fairplay Publications.

Manolis G. Kavussanos, Ilias D. Visvikis (2006) Derivatives and Risk

Management in Shipping, 1st edn., London: Witherby.

Page 19 of 21

Martin Stopford (2008) Maritime economics, 3rd edn., Abingdon,

Oxon: Routledge.

Nikolai Kondratieff (1984) Long Wave Cycle,: Richardson &

Snyder.

Overstone (1998) Correspondents Of Lord Overstone, 1st edn.,

Cambridge: Thoemmes Continuum.

Schumpeter, J.A (1939) Business Cycles: A Theoretical,

Historical and Sttistical Analysis of the Capitalist Process,

New York: McGraw-Hill.

E-references

(2014), The vision of captain P. Tsakos (translation from

Greek), Available at: http://www.epixirimatias.gr/2014/11/t-k-

t.html (Accessed: 16th November 2014).

Clarksons (2014) Shipping Intelligence Network 2010, Available

at: http://www.clarksons.net/sin2010/ (Accessed: 15th November 2014).

Google Finance (2014) Tsakos Energy Navigation Ltd.

(NYSE:TNP), Available at: https://www.google.com/finance?

cid=670768 (Accessed: 23rd November 2014).

Lloyd's List Intelligence (2014), Available at:

http://www.lloydslist.com/ll/ (Accessed: 15th November 2014).

Page 20 of 21

Nigel Lowry (2014) TEN eyes ‘half a dozen’ more crude tankers, Available

at: http://www.lloydslist.com/ll/sector/tankers/article446437.ece/ (Accessed:

25th November 2014).

OECD - IEA (2014) World Oil Demand, Available at:

https://www.iea.org/oilmarketreport/omrpublic/ (Accessed: 20th November

2014).

Page 21 of 21

Related Documents