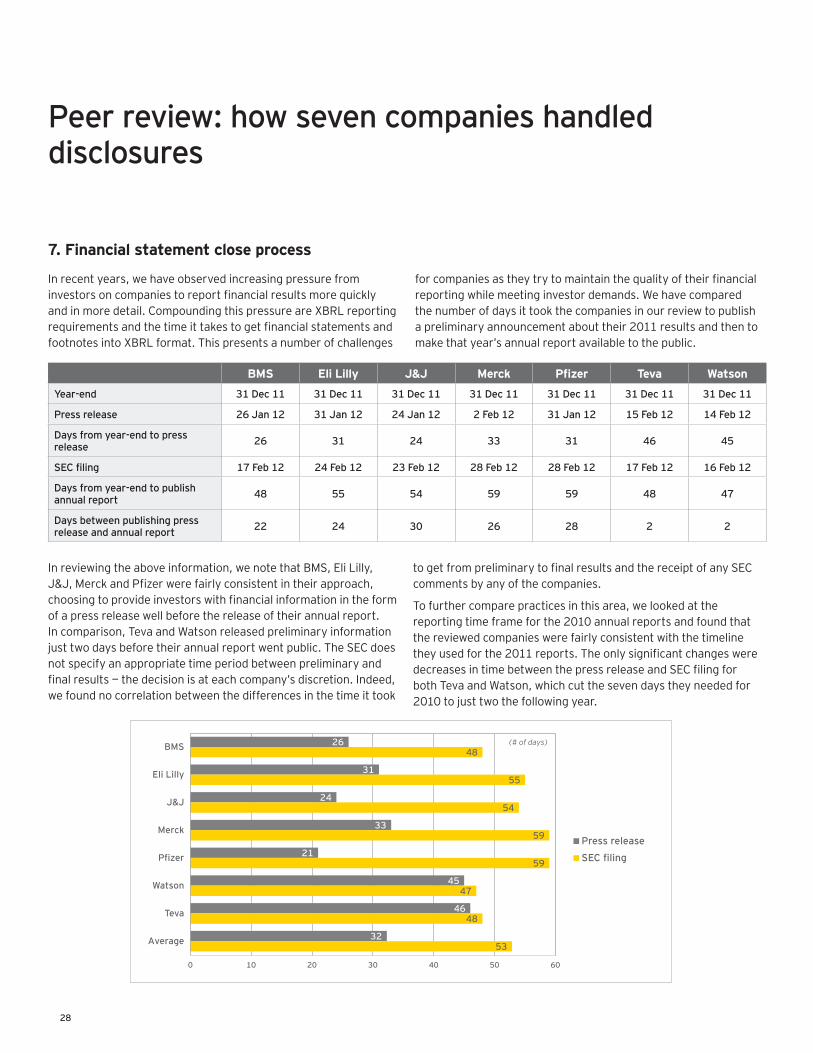

The shifting pharmaceutical industry landscape Accounting and regulatory trends affecting reporting for 2012 and planning for 2013 January 2013

Shifting pharmaceutical landscape

Aug 10, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The shifting pharmaceutical

industry landscapeAccounting and regulatory

trends affecting reporting for 2012 and planning for 2013

January 2013

2

Introduction 1

Regulatory environment: key developments and trends

• SECstaffcomments• Lessonsfromrestatements• FASBandIASBjointprojects• PCAOBupdates• FASBupdates

2

Peer review: how seven companies handled disclosures 1.Revenuerecognitionandcollaborationagreements

2.IPR&Dassetsandintellectualproperty

3.Performance

4.Riskandmitigation

5.Accountingpolicies,judgmentsandestimates

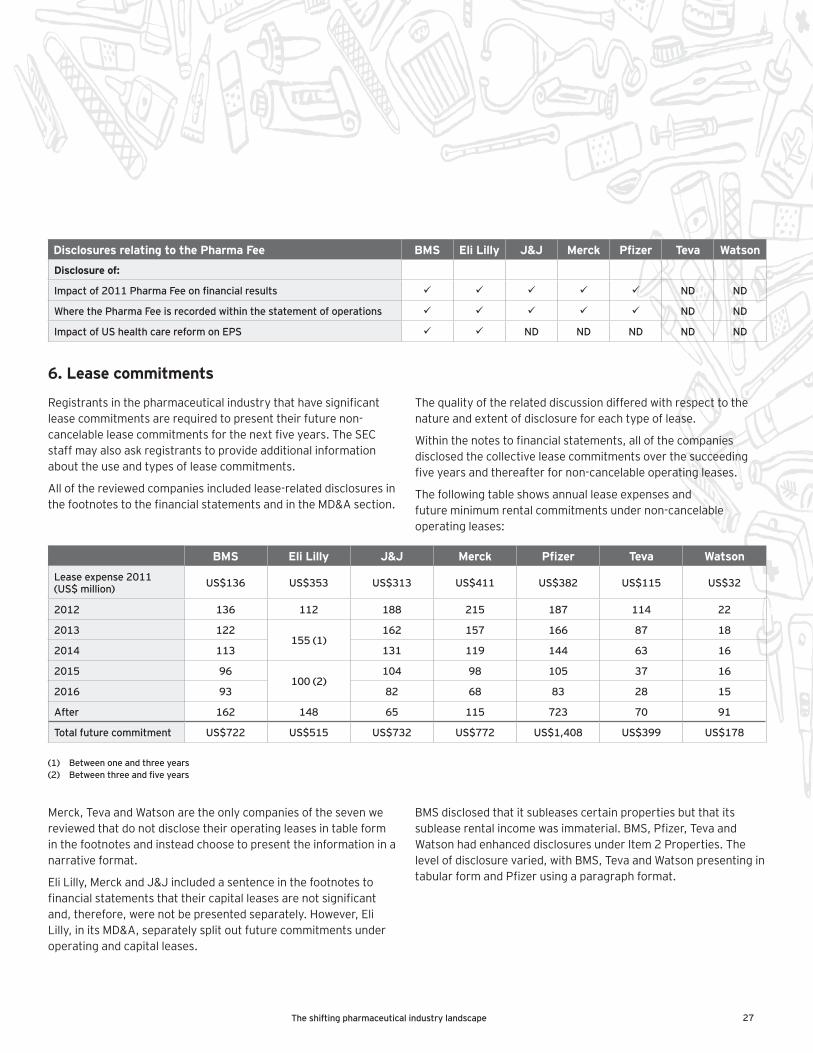

6.Leasecommitments

7.Financialstatementcloseprocess

8

Accounting landscape: a sea of change

• Focuson2013• Changeiscoming:reportingstandards• Revenuerecognition• Financialinstruments• Leases• Dodd-FrankandOTCderivatives

29

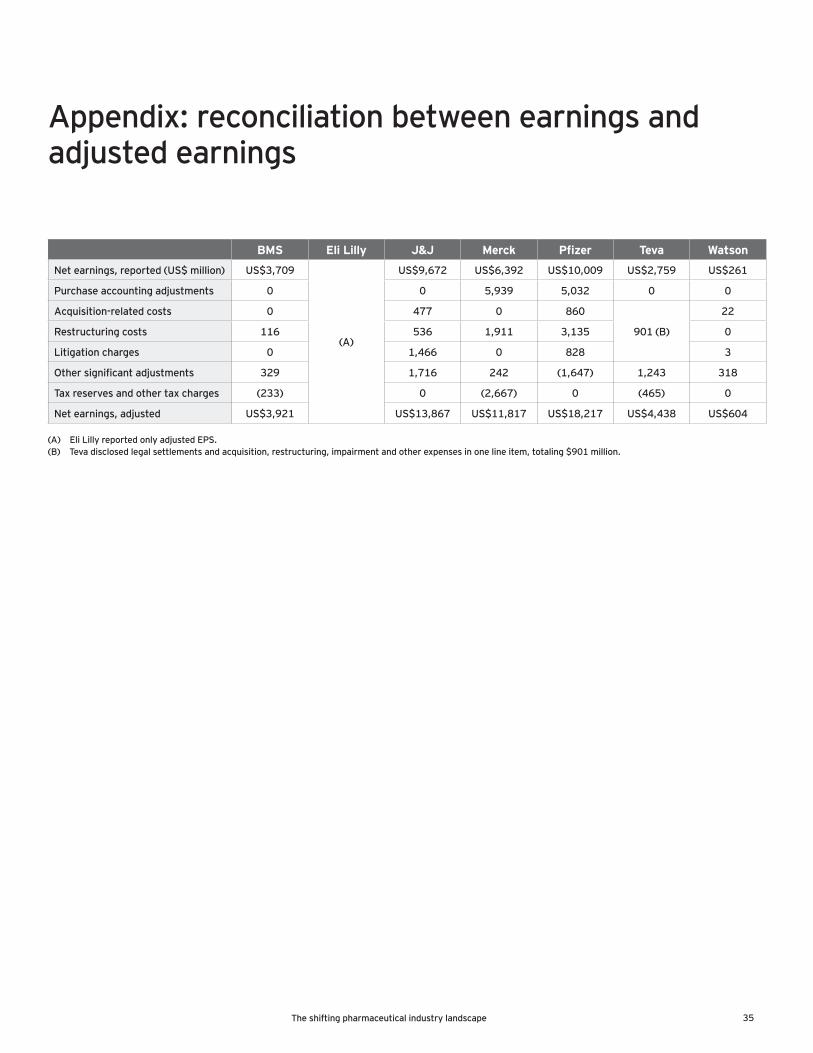

Appendix: reconciliation between earnings and adjusted earnings

35

Contents

DisclaimerThis publication has been carefully prepared but necessarily contains information in summary form and is therefore intended for general guidance only; it is not intended to be a substitute for detailed research or the exercise of professional judgment. The information presented in this publication should not be construed as legal, tax, accounting or any other professional advice or service. Ernst & Young LLP can accept no responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. You should consult with Ernst & Young LLP or other professional advisors familiar with your particular factual situation for advice concerning specific audit, tax or other matters before making any decisions.

3The shifting pharmaceutical industry landscapeThe shifting pharmaceutical industry landscape

For further information, please contact:

TimGordonFinancialAccountingAdvisoryServices(FAAS)[email protected]

GlenT.GiovannettiGlobalLifeSciencesLeader+16175851998glen.giovannetti@ey.com

ScottBrunsGlobalLifeSciencesAssuranceLeader+13176817229scott.bruns@ey.com

Cash on prescription 4

Aspartofourongoingcommitmenttoproviderelevantinsighttothepharmaceuticalindustry,wehavepreparedthisstudyofnewandloomingshiftsandtrendsinfinancialreporting.

Ouranalysisisbasedonthe2011financialreportingseasonandhighlightsaccountingandregulatoryhottopicstoconsiderasyouprepareforthe2012year-endcloseandplanfor2013andbeyond.Wehavefocusedonareasinwhichregulatorsandexternalstakeholdershaveexpressedinterestandprovidedcomment.

Ourreportisdividedintothreesections.

Thefirstsectiondiscussesdevelopmentsaffectingtheregulatoryenvironment.WeexaminerecentSecuritiesandExchangeCommission(SEC)staffcomments,offerlessonsfrommistakesthatledtofinancialrestatementsandprovideupdatesaboutongoinginitiativesfromthreeindustryregulatorybodies–theFinancialAccountingStandardsBoard(FASB),theInternationalAccountingStandardsBoard(IASB)andthePublicCompanyAccountingOversightBoard(PCAOB).

ThesecondsectionbenchmarksthedisclosurepracticesofsevenUS-basedpharmaceuticalcompanies.Fiveofthecompanies–Bristol-MyersSquibb(BMS),EliLilly,Johnson&Johnson(J&J),MerckandPfizer–primarilysellbrandedproducts.Theothertwo–TevaandWatson–primarilysellgenericproducts.Thecomparisonofwhatthesevencompaniesdisclosedandhowandwheretheymadetheirdisclosuresintheirfinancialstatements,highlightsmajorthemesfortheindustry.

Thethirdandfinalsectionofourreportsurveystheaccountinglandscapeandthelargenumberofmajorchangesthatareloomingfortheindustry.Thechangesarecertaintoaffectthestrategicprioritiesofallmajorplayersinthesector.

Bywayofprovidinggeneralcontextforthereport’sfindingsandsuggestedactions,weofferthefollowingobservations:

• Jointprojectwatch–Thestandard-settingactivitiesoftheFASBandtheIASBcontinuetomoveforward.Aspartofanumberofjointprojects,theBoardsarereviewingtheirsecondexposuredraftonrevenuerecognitionandarepreparingtoissueaseconddraftonleasesinearly2013.Otherongoingjointprojectsinvolvefinancialinstruments,insurancecontracts,consolidationandinvestmentcompanies.Duringthereviewperiod,theBoardsmaketentativedecisionsthatmaybedifferentfromearlieronesandfromthoseintheexposuredrafts.Indeed,atthispoint,theBoards’decisionsareallsubjecttochange.WeencourageyoutoactivelyfollowtheBoards’progressandtorespondtorequestsforcomment.But,whatevertheultimateshapeofthechangesturnsouttobe,atleastsomeofthechangeswillbefar-reaching.Forthatreason,manycompanieshavealreadyestablishedcross-functionalteams–drawingfromoperational,finance,accountingandinformationtechnology(IT)resources—toorganizeappropriateresponses.

• Regulatoryfocus–TheSECremainsfocusedonexpandeddisclosuresrelatingtorevenuerecognition,collaborationagreements,in-processresearchanddevelopment(IPR&D)assets,materialpatents,andresearchanddevelopmentactivities.

• Learningfromrestatements–Errorsinaccountingforincometaxes,revenuerecognitionandthepreparationofthestatementofcashflowsweretheleadingcausesofrestatementsofannualfilingsin2011inallindustries.1Understandingtheissuesthatgaverisetorestatementscanhelplifesciencescompaniesastheyperforminternalriskassessmentsandevaluatetheircontrolenvironments.Askingquestionsaboutthemorefrequentrestatementissuesalsocouldbehelpfultomanagementandauditcommitteemembers.

• Reducingcostsanddrivingefficiency–Companiescontinuetolookforwaystocutcostsanddriveefficiencieswhilebalancingriskassociatedwithregulatorycomplianceandstatutoryreporting.Giventheincreasingcomplexityandexpenseofriskmanagementandcompliance,thehunthasintensifiedtofindwaystoimproveandtransformthereportingprocesses.

Introduction

1

1Statistics were derived from our review of restatements of US public companies that are audited by the four largest accounting firms, as disclosed in annual financial statements filed during the year ended 31 December 2011.

2

Regulatory environment: key developments and trends

ThischapterfocusesonimportantshiftsintheUSpharmaceuticalindustry’sregulatorylandscape.

First,weexaminethepastyear’sSECstaffcommentstohighlightnewandcontinuingagencyconcerns.Someofthecommentsbrokenewground,whileothersservedasusefulsummariesofexistingpolicy.

WethenreviewrestatementsofannualfilingsbyUSpubliccompaniestorevealcommonmistakesandtosuggestwaystoimproveinternalcontrols.Finally,weprovideanoverviewofrecentactionsandproposedchangesunderconsiderationbytheFASB,theIASBandthePCAOB.

SEC staff comments Inrecentyears,marketuncertaintyhasputincreasedpressureoncompaniestoimprovethetransparencyoftheirfinancialreporting.Eachyear,Ernst&YoungtrackstheSECstaffcommentsoftheSEConpubliccompanyfilingstoprovideinsightsintotheagency’sconcernsandareasoffocus.Althougheachcompany’sfactsandcircumstancesaredifferent,theeconomicconditionsand

financialreportingchallengesbusinessesfaceareoftensimilar,particularlyinthepharmaceuticalindustry.ThissectionhighlightskeyareasofSECconcern.AmorecomprehensiveanalysisisincludedinourSEC Comments and Trendspublicationlocatedatwww.ey.com/us/accountinglink.

Initscommentsrelatedtothepharmaceuticalindustry,theSECstaffhasfocusedonfivemainareas:revenuerecognition,collaborationagreements,acquiredIPR&Dassets,materialpatents,andresearchanddevelopment.WhatfollowsarehighlightsandanalysisofrecentcommentlettersthattheSEChasprovidedinthesefiveareas,aswellasupdatesandsummariesofSECpositionsinotherareasofconcern.

Revenue recognition

Revenue deductions as they relate to new product offerings

Initscommentletters,theSECstaffhaschallengedregistrantsabouttheprocesstheyusetomakereasonableestimateswhenrecognizingrevenueforthesaleofanew,noveloruniqueproducts.

Registrantsinthepharmaceuticalindustrycommonlyoffercustomersrightsofreturnorproviderebates,chargebacksorotherincentives.Registrantsmustdeterminewhethersellingpricesarefixedordeterminableinordertorecognizerevenueupon

deliveryofproductstocustomers.Inorderforfeestobefixedordeterminable,registrantsmustbeabletoreasonablyestimaterebates,chargebacksandotherincentives,aswellastheamountoffutureproductreturns.

Aspartofitsreviewprocess,theSECstaffmaypointtoinformationinForm10-Kand10-Qfilingsotherthanthefinancialstatementsandfootnotes,recentpressreleases,marketingmaterialsorrecentmanagementpresentationsthatindicateaproductisnew,noveloruniqueinsomeaspect.TheSECstaffmayrequestthatregistrantsexplainhowtheydeterminedtheirestimatesofproductreturns,rebates,chargebacksandotherincentivesintheabsenceofhistoricalinformationrelatedtoanewproduct.Baseduponadditionalinformationreceived,theSECstaffmayrequestthatregistrantsexpanddisclosuresofmanagementdiscussionandanalysis(MD&A)andcriticalaccountingestimatesintheirfuturefilings.

Disclosures relating to estimating revenue deductions

TheSECstaffcontinuestopressformorerobustdisclosureswhenestimatingrevenuedeductions.

Theconcerninthisareaistiedtothebroadrangeofjudgmentsandassumptionsusedinestimatingthesedeductions(forproductreturns,rebatesandchargebacks)andtheoftenmaterialimpactthatthesedeductionshaveonthefinancialstatements.

TheexpandeddisclosuresrequestedbytheSECincludemoreinformationaboutthenatureandamountofeachdeduction.Thedisclosuresencompassarollforwardofinformation,additionalmaterialaboutthequalitativefactorsthatmanagementconsiderswhenitestimateseachdeduction,quantitativeinformationtosupportqualitativefactorsthatareconsideredwhenmakinganestimateandunderlyingbusinessreasonsformaterialperiod-to-periodfluctuationsforeachtypeofreductionofgrossrevenue.Section1.1,onpages8and9,providesadetailedpeercomparisonrelatedtodisclosuresofrevenuedeductions.

Milestone method of revenue recognition

Ifamilestonemethodofrevenuerecognitionpolicyiselected,registrantsmustprovideadditionaldisclosuresaboutresearchanddevelopmentcomponentsofthatarrangement.Thesedisclosureswouldincludeadescriptionoftheoverallarrangement,adescriptionofeachmilestoneandrelatedcontingentconsideration,adeterminationofwhethereachmilestoneisconsideredsubstantive,thefactorstheentityconsideredindeterminingwhethermilestonesaresubstantiveandtheamountofconsiderationrecognizedduringtheperiodofthosemilestones.

3The shifting pharmaceutical industry landscape

TheSECstaffhasissuedcommentsregardingtheadequacyofdisclosuresforeacharrangementandmilestone.Manyregistrantsaggregateinformationwhentheyhavemultiplearrangementsandmilestones,whereastheSECstaffbelievesthatdisclosureonanindividuallevelofeacharrangementandmilestoneismoreappropriate.However,incertaincases,theSEChasnotobjectedtoaggregatedisclosurewhentheregistranthasassertedthatindividualmilestonesarenotmaterialandthatinformationonmilestoneswouldbemoreusefultotheusersofthefinancialstatementsonanaggregatebasis.

Multiple-element arrangements

TheSECstafffrequentlyrequestsregistrantstoexpandtheirdisclosuresaroundmultiple-elementarrangements.Companiesareaskedtoprovidebothquantitativeandqualitativeinformationregardingsignificantjudgmentsmade(andchangesinthosejudgments)regardingtheapplicationoftheSEC’sguidanceinthisarea,aswellasthespecificrequirementsofAccountingStandardsCodification(ASC)605-25-50-2.Additionally,withrespecttoidentifyingseparatedeliverableswithinamultiple-elementarrangement,theSECstaffoftenrequestsregistrantstoprovideexplanationsorfurtheranalysisaboutspecificitemswithinatransactionandwhetherthoseitemsareconsidereddeliverablesthatshouldbeaccountedforseparately.Suchitemsincludetransferofalicensetoaproductcandidate,R&Dservices,manufacturingandsupplyagreements,andparticipationinjointsteeringanddevelopmentcommittees.

Example from SEC comment letters: identifying multiple-element arrangementsInyourevaluationofdeliverables,howdidyouconsidertheobligationsofeachofyourcommittees(i.e.,jointsteeringcommitteeandjointdevelopmentcommittee)?Aretheseobligationsconsideredadeliverable?Whyorwhynot?

TheSECstaffmayalsorequestanevaluationofstand-alonevalueforeachdeliverable:

Example from SEC comment letters: separation criteriaYouindicateyoubelievethelicenseofProductXandtherelatedresearchanddevelopmentservicestobeseparatedunitsofaccounting.Pleaseprovideusyouranalysisdemonstratinghoweachunitofaccountinghadstand-alonevaluebasedontherequirementsofASC605-25-25-5a(i.e.,soldseparatelybyanyvendor,orthecustomercouldreselltheunitofaccountingonastand-alonebasis).

Concentrations of business with European government entities

GiventheongoingsovereigndebtcrisisinEurope,moreemphasishasbeenplacedontheconcentrationofcreditriskrelatedto

accounts-receivablebalancesduefromcustomersinGreece,Italy,Portugal,SpainandothercountriesintheEurozone.

TheSECstaffisaskingregistrantstoprovidemoredetaileddisclosuresabouttheamountofproductsalesbycountryandaccountsreceivableoutstandingbycountry,withaseparatelistforamountsduedirectlyfromthegovernmentorfundedbythegovernment.Inaddition,companiesmustdiscloseamountsduefromprivateparties,theamountofpast-dueaccountsreceivablebycountryandthenumberofdayspastdue.TheSECstaffhasalsorequesteddisclosureoftheamountofallowancefordoubtfulaccountsbycountry,andtheevidencethattheallowanceadequatelyaddressesthecollectibilityofcurrentandpastduereceivablesfromthesecustomers.

Section4.6onpage20providesadetailedpeercomparisonrelatedtothedisclosureofrelationshipswithcustomersintheEurozone.

TheSECstaffhasrequestedmoredetaileddisclosuresaboutreceivablesfromcountriesexperiencingeconomicchallenges:

Example from SEC comment letters: accounts receivables from European entitiesPleaseprovideusproposeddisclosuretobeincludedinfutureperiodicreportsthatbreaksouttheamountoftradereceivablesfromproductsales,andtheamountofproductsalesbycountryinItalyandSpain(andGreeceandPortugal,ifany),andalsodisclosetheamountsthatarepastduefromeachofthesecountriesseparately.Disclosetheportionineachofthesecountriesthatisduedirectlyfromthegovernmentorfundedbythegovernment.

Collaboration arrangements

Collaboration arrangement disclosures

TheSECstaffhasrequestedregistrantstoexpandtheirdisclosuresrelatedtocollaborationarrangements.TheSECstaffhasspecifiedalonglistofitemssubjecttodisclosure:identificationoftheotherpartyinthearrangement;theproductsbeingdeveloped;amountspaidorreceivedtodateunderthearrangement;aggregatepotentialmilestonepaymentstobemadeorreceivedandtheeventstriggeringthemilestones;theexistenceofroyaltyprovisions,ratesandanysalesthresholdsrelatedtotherates;andtheexistenceofannualmaintenancefees,includingdurationandterminationprovisionsandpaymentstheregistrantmayberequiredtomakeintheeventoftermination.

RegistrantswithpaymentobligationsundercollaborationarrangementsmustalsolistanypotentialpaymentsinthecontractualobligationstableintheMD&Asectiontotheextentthatapaymentisreasonablypossible.

4

Disclosuresshouldclearlydescribetheregistrant’saccountingpolicywithrespecttoalloftheaboveitems,aswellastheincomestatementpresentationandamountsattributabletocollaborationarrangementsforeachapplicableperiod.

Section1.2onpage10providesadetailedpeercomparisonrelatedtocollaborationarrangementdisclosures.

Acquired IPR&D assets

Disclosures related to acquired IPR&D assets

TheSECstaffcontinuestoissuecommentlettersrequestingadditionalinformationregardingacquiredIPR&Dassets.

Specifically,theSECstaffhasrequestedthatregistrantscontinuetoprovidethedisclosurescitedintheAmericanInstituteofCPAs’(AICPA)TechnicalPracticeAid,Assets Acquired in a Business Combination to Be Used in Research and Development Activities: A Focus on Software, Electronic Devices, and Pharmaceutical Industries.TheAICPAdraftpracticeaidfocusesonincreasedqualitativeandquantitativedisclosuresinthenotestothefinancialstatementsandondisclosuresofforward-lookinginformationwithintheMD&A.Bycontrast,thepracticeaiddoesnotrefertothenotestothefinancialstatementstoprotectacompanyfromalegalperspectiveunderthePrivateSecuritiesLitigationReformActof1995,whichdoesnotextendtofinancial-statementdisclosures.

TheSECsuggeststhatregistrantsprovidethefollowinginformationaboutacquiredIPR&D:adiscussionofthespecificnatureandfairvalueofeachsignificantacquiredproject;thecompleteness,complexityanduniquenessoftheprojectsontheiracquisitiondates;thenature,timingandestimatedcostsoftheeffortsnecessarytocompletetheprojectsandtheanticipatedcompletiondates;therisksanduncertaintiesassociatedwithcompletingdevelopment;andthemethodusedtovaluetheprojects,includingsignificantvaluationassumptions.RegistrantsmaybeaskedtoprovideadditionalinformationexplaininghowIPR&Dassetswereidentified,orwhy,baseduponotherinformationdisclosed,noIPR&Dassets,oralimitednumberofIPR&Dassetswererecorded.

Seesection2.1onpages11-12forfurtherinformationandadetailedpeercomparisonrelatedtoacquiredIPR&Dassetdisclosures.

Material patents

Disclosures related to material patents

TheSECstafffrequentlyrequestsregistrantstoprovideexpandeddisclosureaboutmaterialpatents.Thedisclosurerequest

generallyincludesadiscussionoftheproductsortechnologiesthatrelatetothepatent,thejurisdictioninwhichthepatentisgranted,theexpirationdate,identificationofpatentssubjecttolegalproceedingsandastatementsayingwhetherthepatentsareownedorleased.Additionally,theSECstaffmayrequestregistrantswithmultiplepatentstodiscloseinformationforeachpatentortoidentifyindividualpatentsthathavebeenaggregatedfordisclosurepurposesbasedonsimilarcharacteristics.

Seesection2.2onpage12forfurtherinformationandadetailedpeercomparisonofdisclosuresrelatedtomaterialpatents.

Research and development

Research and development expenses

MostregistrantsinthepharmaceuticalindustryincursignificantexpensesforR&Dactivitiestodevelopalimitednumberofnewdrugsincorrelationtothenumberofcompoundsdeveloped.Accordingly,theSECstaffcontinuestorequestregistrantstoprovidedisclosuresforoverallR&Dexpenses,notjustthoserelatedtonewproducts.Specifically,theSECstafffocusesonthestatusofmajorR&Dprojectsandtherelatedcostsincurredtodate,aswellastheestimatedcompletiondates,completioncostsandcapitalrequirements.TheSECstaffmayalsorequestdisclosuresdescribingtheextenttowhichaproject’ssuccessdependsonpartiesotherthantheregistrant,adiscussionoftheproject’sphasesandadescriptionofthenatureoftheproductsinthepipeline.TheSECstaffmayalsorequireregistrantswhodonottrackR&Dcostsbyprojecttodisclosethatfactandexplainwhythatisthecase.Suchregistrantsmustalsoprovidequantitativeorqualitativedisclosuresthatdescribetheamountofresourcesbeingusedoneachprojectorgroupofprojects.

Regulatory environment: key developments and trends

Example from SEC comment letters: research and development expensesInordertogainabetterunderstandingoftheeffectsandexpectedeffectsofyourresearchanddevelopmentactivitiesonresultsofoperationsandfinancialposition,pleaseprovideus,aspracticable,thefollowingadditionalinformationforsignificantproductsinresearchanddevelopment:

• Thecostsincurredduringeachperiodpresented.Ifyoudonotmaintainanyresearchanddevelopmentcostsbyproject,provideusotherquantitativeorqualitativedisclosurethatindicatestheamountofthecompany’sresourcesbeingusedontheproject.

• Thenatureofeffortsandstepsnecessarytocompletetheproduct.

• Therisksanduncertaintiesassociatedwithcompletingdevelopment,andtheextentandnatureofadditionalresourcesthatneedtobeobtainedifcurrentliquidityisnotexpectedtobesufficienttocompletetheproduct.

5The shifting pharmaceutical industry landscape

Seesection2.3onpages13-14forfurtherinformationandadetailedpeercomparisonrelatingtoresearchanddevelopmentexpenses.

Other areas of consideration

Trends in the adoption of the new fair-value disclosures

WeanalyzedhowasampleofpubliccompaniesinitiallyadoptedthenewdisclosuresrequiredbyAccountingStandardsUpdate(ASU)2011-04intheir31March2012quarterlyfilings.DuetotherecentadoptionofthisASU,wenotedvariationsinpracticeastohowcompanieshadappliedtheirdisclosurerequirementsofthisstandard.Forexample,wenotedvariationsinthetypesofquantitativeinformationcompaniesdisclosedaboutsignificantunobservableinputsintheirLevel3measurements(e.g.,therangeofinputsusedandtheweighted-averageinputsforanassetclass)andinthelevelofdisaggregationofthatinformation.Thedisclosuresweremoreconsistentinotherareas,includinghowcompaniesaddressedpricinginformationfromthird-partyvendors(e.g.,pricingservices,brokers).Additionally,wenotedthatpharmaceuticalcompaniesgenerallyreportedalimitednumberofitemsincreasedatfairvalueonarecurringornonrecurringbasis,usingLevel3inputs(e.g.,impairmentoflong-livedassets,contingentconsiderationliabilities,financialinstrumentswithcharacteristicsofbothdebtandequity).

ThesenewdisclosuresmayevolveovertimeascompaniesrefinetheinformationtheyprovidebasedonleadingpracticesandfeedbackfromtheSECstaff.

Compensation committees and their use of advisers

TheSECfinalizedarulethatwillrequirenationalsecuritiesexchangestoadoptminimumlistingstandardsrelatedtocompensationcommitteesandtheiruseofadvisers.Underthesestandards,amemberofalistedcompany’scompensationcommitteemustbean“independent”memberoftheboardofdirectors,asdefinedbytheexchange.Listingstandardsmustrequirethatcompensationcommitteeshavetheauthoritytoretainadvisersandberesponsiblefortheirappointment,paymentandoversight.

2009 US GAAP XBRL taxonomy phased out

Edgarnolongeracceptsextensiblebusinessreportinglanguage(XBRL)exhibitsusingthe2009USgenerallyacceptedaccountingprinciples(GAAP)XBRLtaxonomy.Registrantsmaycontinuetousethe2011USGAAPXBRLtaxonomy,buttheSECstaffstronglyencouragescompaniestoadoptthelatestversionofthetaxonomy

fortheirXBRLexhibits(i.e.,the2012taxonomyreleasedinMarch2012).DetailsaboutthetaxonomiescanbefoundontheFASBandSECwebsites.

Accounting for and disclosure of loss contingencies

TheSECstafffrequentlychallengesregistrantsforfailingtomakerequiredfootnotedisclosureswhenlossesareconsideredreasonablypossibleorforfailingtodisclosetherangeofreasonablypossiblelosses,includingthereasonablepossibilityofalossinexcessoftheamountaccrued.TheSECstaffmaylooktoverifythataregistranthasconsideredanddisclosedanestimateoftheamountorrangeofreasonablypossiblelossesor,ifapplicable,astatementthattheamountoflosscannotbeestimated.Ifaregistrantstatesanestimateoflosscannotbemade,theSECstaffmaylookforredflagsthatmightindicateotherwise,suchastheregistrant’shistorywithsimilarlegalmattersandtheageofanypreviouslitigation.

TheSECstaffmayalsochallengetheadequacyofhistoricaldisclosureswhenlosscontingenciesaresubsequentlysettled.Inparticular,theSECstaffreviewsprior-perioddisclosuresandmayinquirewhetherpastdisclosureswereappropriateandwhetheranaccrualshouldhavebeenrecognizedinapriorperiod.

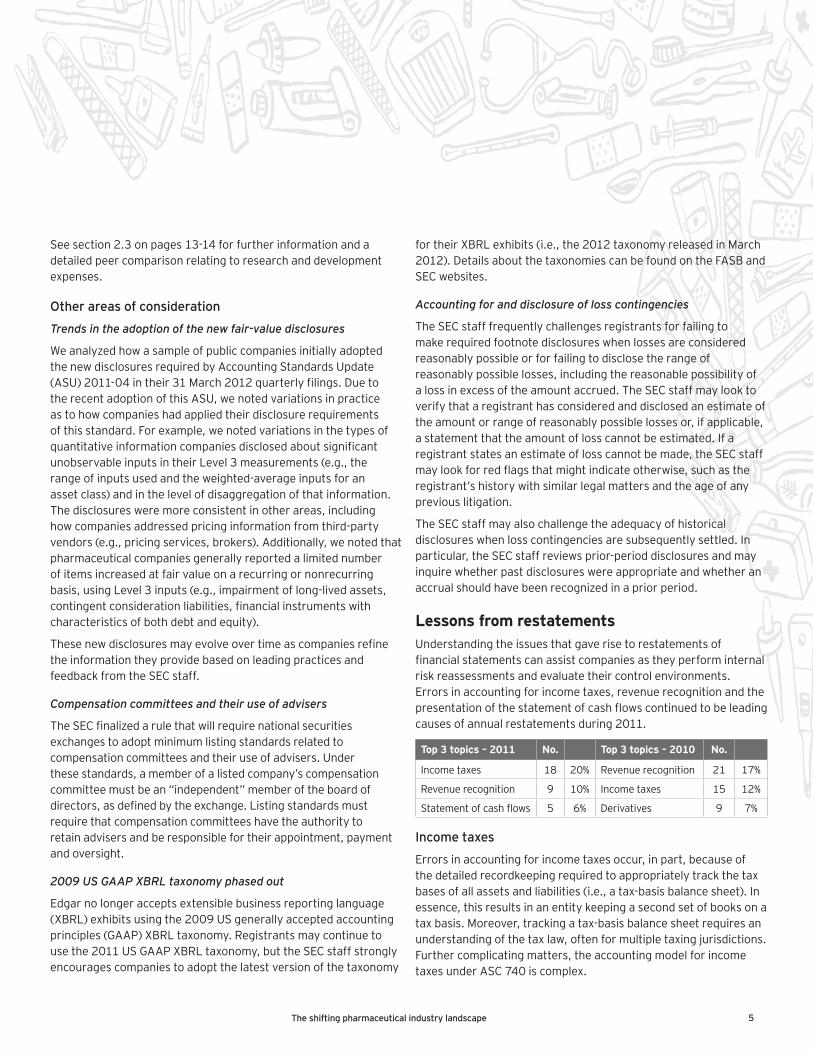

Lessons from restatementsUnderstandingtheissuesthatgaverisetorestatementsoffinancialstatementscanassistcompaniesastheyperforminternalriskreassessmentsandevaluatetheircontrolenvironments.Errorsinaccountingforincometaxes,revenuerecognitionandthepresentationofthestatementofcashflowscontinuedtobeleadingcausesofannualrestatementsduring2011.

Top 3 topics – 2011 No. Top 3 topics – 2010 No.

Incometaxes 18 20% Revenuerecognition 21 17%

Revenuerecognition 9 10% Incometaxes 15 12%

Statementofcashflows 5 6% Derivatives 9 7%

Income taxes

Errorsinaccountingforincometaxesoccur,inpart,becauseofthedetailedrecordkeepingrequiredtoappropriatelytrackthetaxbasesofallassetsandliabilities(i.e.,atax-basisbalancesheet).Inessence,thisresultsinanentitykeepingasecondsetofbooksonataxbasis.Moreover,trackingatax-basisbalancesheetrequiresanunderstandingofthetaxlaw,oftenformultipletaxingjurisdictions.Furthercomplicatingmatters,theaccountingmodelforincometaxesunderASC740iscomplex.

6

Whilethespecificcausesofrecentincometaxaccountingrestatementsvary,asignificantportionofincometaxaccountingrestatementsfellintothefollowingcategories:

• Inappropriateevaluationoftherealizabilityofdeferredtaxassets

• Incorrectidentificationorcalculationofthetaxbasis,resultingininappropriatemeasurementofdeferredtaxassetsandliabilities

• Incometaxaccountingerrorsassociatedwithintercompanytransactions

Revenue recognitionRevenuerecognitionguidanceconsistsofmorethan200piecesofliterature.Insomecases,theguidanceisgeneral,andinothersitisprescriptive.Muchoftheguidanceisspecifictocertaintransactionsorindustries.Thesefactors,combinedwithothercomplexities,makeinappropriaterevenuerecognitiononeofthemostfrequentcausesofrestatements.

Thespecificreasonsforrevenue-relatedrestatementsvary.Theyincludecalculationerrors,fraud,failuretounderstandcontractualtermsandmisapplicationofaccountingliterature.Onerecentrevenuerecognitionrestatementtrendisineffectivemonitoringofaccountingestimatesrelatedtorevenuerecognition.

Revenuerecognitionrequirestheuseofaccountingestimatesandongoingmonitoring,suchascomparingestimatesandassumptionstoactualresults.Revenuerecognitionestimatesincludedetermining:

• Productreturns

• Thestand-alonesellingpriceforseparateunitsofaccounting

• Thepatternofperformanceofacontractedservice(i.e.,determiningtheextenttowhichtheearningsprocesshasbeencompleted,includingusingtheproportionalperformancemethod)

• Theprogresstowardcompletionofcontracts,applyingthepercentage-of-completionmethod

Theseestimatesshouldbereassessedonaregularbasistodeterminewhethertheunderlyingassumptionscontinuetobeappropriate.Iftheactualresultsdonotsupporttheassumptionsusedtodeveloptheaccountingestimate,acompanyshouldevaluatewhetheranyrequiredchangereflectsachangeinestimateoranerror.

Examplesofanerrorinclude:

• Inappropriatelyapplyingassumptionsthatarenotconsistentwiththebestavailableinformation(e.g.,historicalresults)

• Notchangingtheunderlyingassumptionsinatimelymannerwhenfactsandcircumstanceschange

• Inappropriatedesignoroperatingeffectivenessofinternalcontrolsovertheseestimationprocesses

Statement of cash flows

Restatementsrelatedtothestatementofcashflowstypicallystemfromaninappropriateclassificationofcashinflowsandoutflowsbetweenoperating,investingandfinancingactivities(e.g.,inappropriateclassificationofchangesinrestrictedcashandderivative-relatedactivity).

Accountingguidanceinthisareaisexplicitwithrespecttotheproperclassificationofcertainitems;otheritemsrequiretheuseofjudgment.Forexample,whentheclassificationisnotexplicitlyaddressed,itwilloftenbebasedonthenatureoftheactivityandthepredominantsourceoftherelatedcashflow.

Other topics

Suchtopicsastheaccountingfortransactionsinvolvingfinancialinstrumentswithcharacteristicsofbothdebtandequityandfinancialstatementclassificationwerealsosignificantcontributorstorestatementsduring2011.Othertopicsfluctuateinfrequencyduetovariousfactors,includingnewaccountingpronouncements,changesinthenatureorvolumeoftransactions,andthefocusofregulators.Someexamplesfrom2011restatementsinclude:

• Businesscombinationsandtransactionsinvolvingfinancialinstrumentswithcharacteristicsofbothdebtandequity—Fortransactionsinvolvingbusinesscombinations,somecompaniesinappropriatelyaccountedforcontingentconsiderationorfailedtoidentifyintangibleassets.Inrestatementsinvolvingtransactionsinvolvingfinancialinstrumentswithcharacteristicsofbothdebtandequity,certainwarrantinstrumentswereinappropriatelytreatedasacomponentofequityinsteadofasaderivativeliability.

• Financialstatementclassification—Frequenterrorsinthisareaincludedinappropriateclassificationofincomestatementactivity(i.e.,betweenoperatingexpenses,selling,generalandadministrativeexpenses,andotherexpenses)andincorrectbalancesheetpresentationofcurrentandlong-termassetsandliabilities.

• Accountsreceivableallowances—Companiesincreasinglymadeerrorsrelatedtotheallowancefordoubtfulaccounts,includingerrorsresultingfromtheuseofaninappropriatereservemethodology(e.g.,aggregatingreceivablesthataredissimilarin

Regulatory environment: key developments and trends

7The shifting pharmaceutical industry landscape

nature)orfromtheuseofflawedorincompletefacts.Athoroughanalysisofallfactors,includinghistoricalresults,shouldbeconsideredwhenmakingjudgmentsinthisarea.

• Leases—Companiesmisappliedtheleasingguidance.Examplesincludeincorrectlyclassifyingleases(i.e.,operatingversuscapitalleasesforlessees)andinappropriatelyaccountingforsaleandleasebacktransactionsandbuild-to-suitleasetransactions.Awidevarietyofleases,coupledwiththecomplexityoftheaccountingmodel,makeleaseaccountingarecurringcauseofrestatements.

FASB and IASB joint projects

Continued redeliberations on revenue recognition

TheBoardsarereviewingmorethan40topics,includingwhetherconsiderationreceivedforthesaleofalicenseshouldberecognizedovertimeorataspecificpoint.TheBoardsdiscussedpossiblerefinementstotheimplementationguidanceonlicensesandrightstouseandaskedtheirstafftoperformadditionalanalysistohelpthemreachafinaldecision.Lifesciencescompaniesshouldmonitorthereviewtodetermineifanyrefinementstoaccountingforlicensesorrightstouseaffecttreatmentofthesetransactions.

TheBoardsalsotentativelydecidedtoremovetheproposedrequirementtomeasureandrecognizelossesononerousperformanceobligationsincustomercontracts.Instead,theytentativelydecidedtolookintoexistingguidance,eventhoughthiswouldmeanthatcurrentdifferencesbetweenUSGAAPandInternationalFinancialReportingStandards(IFRS)inthisareawouldremain.

Whilemuchislefttodiscuss,theBoardsstillplantoissueafinalstandardinthefirsthalfof2013.

PCAOB updates

Auditor independence

ThePCAOBheldanotherroundtableonauditorindependenceandmandatoryfirmrotationandbrieflyreopenedthecommentperiod.Thefeedbackwasconsistentwithotheroutreachefforts—participantsgenerallysupportedimprovingauditqualityandenhancingauditorindependencebutweregenerallyagainstmandatoryrotationoftheirauditfirms.ThePCAOBwillcontinuegatheringfeedbackthroughmoreoutreachinitiatives,whichwilllikelyextendthisprojectinto2013.

PCAOB inspection process

Inresponsetofeedbackfrompubliccompanyauditcommittees,thePCAOBissuedareleasetohelpthecommitteesunderstandmoreaboutitsinspectionsofregisteredpublicaccountingfirms.Amongotherthings,thereleaseincludedanumberofquestionsrelatedtotheinspectionprocessthatthePCAOBencouragedthecommitteestoasktheirauditors.

FASB updates

Improvements to disclosure requirements

TheFASBsoughtcommentonadiscussionpaperaboutaframeworkforimprovingtheeffectivenessofdisclosuresinnotestofinancialstatements.ThepaperisnotaproposalbutratherameanstogatherstakeholderinputtohelptheBoarddevelopaproposal.TheFASB’sgoalistoimprovetheeffectivenessofdisclosuresbyclearlycommunicatingtheinformationthatisimportanttotheusersofacompany’sfinancialstatements.Toachievethisgoal,theFASBbelievesitmustdevelopaframeworkthatpromotesconsistentdecisionsaboutdisclosurerequirementsandhelpscompaniesdeterminewhichdisclosuresarerelevanttotheirsituation.

Thepaperaskedforinputonanumberofissues,including:

• AdecisionprocessthatcouldhelptheFASBestablishdisclosurerequirements

• Awaytomakedisclosurerequirementsflexiblesothateachcompanycouldtailoritsdisclosurestomeettheneedsoftheusersofitsfinancialstatements

• Ajudgmentframeworktohelpcompaniestailortheirdisclosures

• Asetoforganizationandformattingtechniquesthatwouldmakeinformationeasiertofindandunderstand

• Aframeworkforevaluatingdisclosurerequirementsforfinancialstatementscoveringinterimperiods

End of project on loss contingencies

TheFASBdecidedtodiscontinueitsprojectonlosscontingencies,aneffortthatwouldhavesignificantlyexpandedquantitativeandqualitativelosscontingencydisclosurerequirements.Invotingtodiscontinuetheproject,someBoardmembersstatedthatanyissuerelatingtolosscontingencydisclosureswasacompliancematter,notastandard-settingmatter.WeexpecttheSECstafftocontinuetochallengeregistrants’disclosuresinthisarea.

8

Inordertomakeinvestmentdecisions,itisimportantforusersoffinancialstatementstoobtainkeyinformationrelevanttoacompany,thusallowinginvestorstomakereliablecomparisonsamongcompetitors.Studieshaveshownacorrelationbetweenthetransparencyandconsistencyofacompany’sfinancialreportinganditsshare-priceperformance.

Tohelpyouprepareyour2012annualreport,wehavereviewedandcomparedaselectionofsignificant2011financialstatementsofsevenleadingcompaniesinthepharmaceuticalindustry.Fiveofthecompanies—BMS,EliLilly,J&J,MerckandPfizer—primarilysellbrandedproducts.Theothertwo—TevaandWatson—areprimarilygenericcompanies.AllsevencompaniesreporttheirfinancialresultsonthebasisofUSGAAP.

Inthefollowingsection,weprovidecommentsoncertaininformationintheirfinancialstatementsfromayearagothatmayhaverelevancetoyourupcomingfinancialstatementdisclosureconsiderations,particularlywithregardtodisclosuresthatwilllikelybethefocusofattentionforinvestorsandtheSEC.

Ourcomparisonencompassessevenfocusareas:

1.Revenuerecognitionandcollaborationarrangements

2.IPR&Dassetsandintellectualproperty

3.Performance

4.Riskandmitigation

5.Accountingpolicies,judgmentsandestimates

6.Leasecommitments

7.Financialstatementcloseprocess

Aseachofthesurveyedcompaniesinformationintheirfinancialstatementsisbasedontheirspecificfacts,circumstancesanddeterminationofmateriality,youshouldconsultwithErnst&YoungLLPorotherprofessionaladvisorsfamiliarwithyourparticularfactualsituationforadvicebeforemakinganydecisionsaboutyourspecificdisclosures.

1. Revenue recognition and collaboration arrangements

1.1 Revenue deductions

Refertotheregulatoryenvironmentsectiononpage2foradescriptionofSECreportingobservationsaboutrevenuedeductionsandrelateddisclosures.

AllcompaniessurveyedprovideddisclosuresonrevenuedeductioninMD&Aandinthenotestothefinancialstatements.

Noneofthecompaniesprovidedquantitativeinformationrelatedtothequalitativefactorsthatmanagementconsideredwhenitestimatedeachrevenuededuction.

ThecompaniesgenerallyprovidedqualitativeinformationinthenotestothefinancialstatementsandquantitativeinformationinMD&A.InadditiontothequantitativeinformationinMD&A,BMSincludedinthenotestothefinancialstatementsthereductionstotradereceivablesandalistingofaccruedrebatesandreturnliabilitiesatyear-end.

Allcompaniesprovideddetailedqualitativeinformationaroundtheirrevenuededuction.However,thelevelofquantitativeinformationwasgenerallylimitedwithonlyBMS,J&JandTevapresentingrollforwardinformationforeachrevenuededuction.J&Jwastheonlycompanythatpresentedrevenuedeductionsandrollforwardinformationbybusinesssegment.

PfizerdisclosedaggregaterevenuedeductionsforMedicaidandrelatedstaterebateprograms,Medicarerebates,performance-basedcontractrebatesandchargebacks.However,theamountsrelatedtosalesreturnsandsalesincentiveswerenotpresented.

BMSdisclosedtheamountsofrevenuedeductionatadetailedlevel,includingthefollowingbreakout:

• Chargebacksrelatedtogovernmentprograms

• Cashdiscount

• Managedhealthcarerebatesandothercontractdiscounts

• Medicaidrebates

• Salesreturn

• Otheradjustments

J&Jdisclosed,atahighlevel,theamountofrevenuedeductions,splitbetweenthefollowingcategories:

• Rebates

• Salesreturns

• Promotions

Tevadisclosed,inarollforwardformat,thefollowingrevenuedeductions:

• Reservesincludedinaccountsreceivable,net

• Chargebacks

• Returns

• Rebatesandothersalesreservesandallowances

Peer review: how seven companies handled disclosures

9The shifting pharmaceutical industry landscape

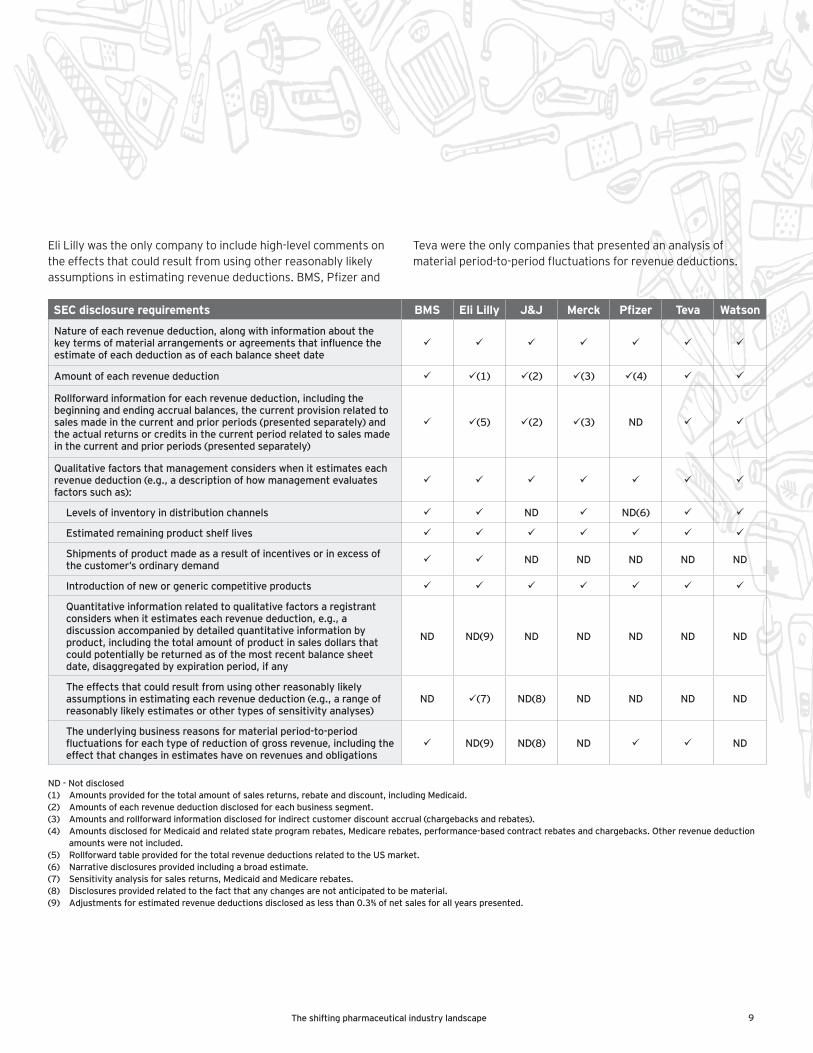

SEC disclosure requirements BMS Eli Lilly J&J Merck Pfizer Teva Watson

Nature of each revenue deduction, along with information about the key terms of material arrangements or agreements that influence the estimate of each deduction as of each balance sheet date

Amount of each revenue deduction (1) (2) (3) (4)

Rollforward information for each revenue deduction, including the beginning and ending accrual balances, the current provision related to sales made in the current and prior periods (presented separately) and the actual returns or credits in the current period related to sales made in the current and prior periods (presented separately)

(5) (2) (3) ND

Qualitative factors that management considers when it estimates each revenue deduction (e.g., a description of how management evaluates factors such as):

Levels of inventory in distribution channels ND ND(6)

Estimated remaining product shelf lives

Shipments of product made as a result of incentives or in excess of the customer’s ordinary demand ND ND ND ND ND

Introduction of new or generic competitive products

Quantitative information related to qualitative factors a registrant considers when it estimates each revenue deduction, e.g., a discussion accompanied by detailed quantitative information by product, including the total amount of product in sales dollars that could potentially be returned as of the most recent balance sheet date, disaggregated by expiration period, if any

ND ND(9) ND ND ND ND ND

The effects that could result from using other reasonably likely assumptions in estimating each revenue deduction (e.g., a range of reasonably likely estimates or other types of sensitivity analyses)

ND (7) ND(8) ND ND ND ND

The underlying business reasons for material period-to-period fluctuations for each type of reduction of gross revenue, including the effect that changes in estimates have on revenues and obligations

ND(9) ND(8) ND ND

ND - Not disclosed(1) Amounts provided for the total amount of sales returns, rebate and discount, including Medicaid. (2) Amounts of each revenue deduction disclosed for each business segment.(3) Amounts and rollforward information disclosed for indirect customer discount accrual (chargebacks and rebates).(4) Amounts disclosed for Medicaid and related state program rebates, Medicare rebates, performance-based contract rebates and chargebacks. Other revenue deduction amounts were not included.(5) Rollforward table provided for the total revenue deductions related to the US market.(6) Narrative disclosures provided including a broad estimate.(7) Sensitivity analysis for sales returns, Medicaid and Medicare rebates.(8) Disclosures provided related to the fact that any changes are not anticipated to be material.(9) Adjustments for estimated revenue deductions disclosed as less than 0.3% of net sales for all years presented.

EliLillywastheonlycompanytoincludehigh-levelcommentsontheeffectsthatcouldresultfromusingotherreasonablylikelyassumptionsinestimatingrevenuedeductions.BMS,Pfizerand

Tevaweretheonlycompaniesthatpresentedananalysisofmaterialperiod-to-periodfluctuationsforrevenuedeductions.

10

Peer review: how seven companies handled disclosures

SEC requirements BMS Eli Lilly J&J Merck Pfizer Teva Watson

Does the entity have collaboration arrangements? YES(1) YES(2) YES(3) YES(4) YES(5) YES(5) YES(6)

Nature of collaboration arrangements disclosed:LicensingCo-developmentCo-commercializationCo-manufacturingCo-marketingCo-promotionCo-distribution

—

——

—————

—

—

———

————

The table below shows which companies provide enhanced disclosures:

The identity of the other party in the arrangement ND (5) (5)

The products being developed, as applicable ND (5) (5)

Any amounts paid or received to date under the arrangement (including up-front licensing fees and milestone payments) ND ND(7) (5) ND

Under each arrangement, aggregate potential milestone payments to be made or received and the triggering events for the milestones ND ND(8) (5) ND

The existence of royalty provisions, royalty rates (or ranges within defined percentages if tiered) and any sales thresholds related to rates ND ND ND(9) ND

Duration and termination provisions, including payments the registrant may be required to make in the event of termination ND (5) ND(9) ND

Disclosure by entity

ND - Not disclosed(1) Collaboration arrangements with seven significant partners.(2) Collaboration arrangements with six significant partners. (3) Disclosed only the accounting policies used for collaboration arrangements.(4) Collaboration arrangements with two significant partners. Joint ventures with five significant partners. (5) Did not include a separate section for collaboration arrangements, which were disclosed in many places in MD&A or in notes to the financial statements.(6) Collaboration arrangement with one significant partner.(7) Disclosed in aggregate in the notes to the financial statements. (8) Disclosures in the notes to the financial statements of total amounts received and paid during the fiscal year.(9) Disclosed for major collaboration agreements.

Inthenotestothefinancialstatements,BMS,EliLillyandMerckincludedaspecificfootnoteprovidingextendeddisclosuresrelatedtotheirrespectivecollaborationarrangements.Tevaprovidedonlylimitedinformationinthenotestothefinancialstatementsaboutitscollaborationarrangements.BMSandMerckalsoincludedaspecificsectionrelatedtocollaborationarrangementsinMD&A.

J&Jdisclosedtheaccountingpoliciesrelatedtoitscollaborationarrangements.However,nodetaileddisclosuresrelatedtothesearrangementswerepresentedinthenotestothefinancialstatementsorinMD&A.EliLillytooktheapproachofdisclosingitscollaborationarrangementsinthenotestothefinancialstatementsorganizedbydrugandnotbycollaborationpartner.

1.2 Collaboration arrangements

Refertotheregulatoryenvironmentsectiononpages3-4foradescriptionofSECreportingobservationsaboutcollaborationarrangementsandrelateddisclosures.

ThetablebelowhighlightsthespecificitemstheSECstaffhasidentifiedrelatedtocollaborationarrangementsthatregistrantsshouldconsiderdisclosing.

11The shifting pharmaceutical industry landscape

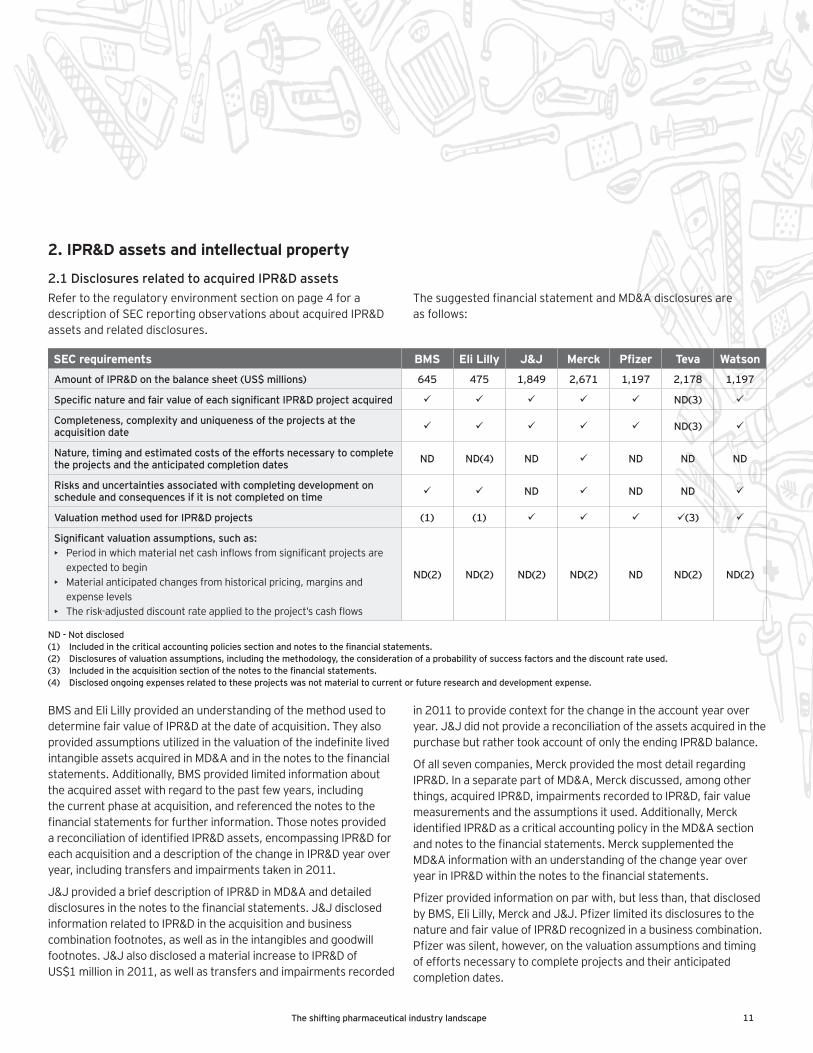

2. IPR&D assets and intellectual property

2.1 Disclosures related to acquired IPR&D assets Refertotheregulatoryenvironmentsectiononpage4foradescriptionofSECreportingobservationsaboutacquiredIPR&Dassetsandrelateddisclosures.

ThesuggestedfinancialstatementandMD&Adisclosuresareasfollows:

SEC requirements BMS Eli Lilly J&J Merck Pfizer Teva Watson

Amount of IPR&D on the balance sheet (US$ millions) 645 475 1,849 2,671 1,197 2,178 1,197

Specific nature and fair value of each significant IPR&D project acquired ND(3)

Completeness, complexity and uniqueness of the projects at the acquisition date ND(3)

Nature, timing and estimated costs of the efforts necessary to complete the projects and the anticipated completion dates ND ND(4) ND ND ND ND

Risks and uncertainties associated with completing development on schedule and consequences if it is not completed on time ND ND ND

Valuation method used for IPR&D projects (1) (1) (3)

Significant valuation assumptions, such as:• Periodinwhichmaterialnetcashinflowsfromsignificantprojectsare

expectedtobegin• Materialanticipatedchangesfromhistoricalpricing,marginsand

expenselevels• Therisk-adjusteddiscountrateappliedtotheproject’scashflows

ND(2) ND(2) ND(2) ND(2) ND ND(2) ND(2)

ND - Not disclosed(1) Included in the critical accounting policies section and notes to the financial statements.(2) Disclosures of valuation assumptions, including the methodology, the consideration of a probability of success factors and the discount rate used.(3) Included in the acquisition section of the notes to the financial statements.(4) Disclosed ongoing expenses related to these projects was not material to current or future research and development expense.

BMSandEliLillyprovidedanunderstandingofthemethodusedtodeterminefairvalueofIPR&Datthedateofacquisition.TheyalsoprovidedassumptionsutilizedinthevaluationoftheindefinitelivedintangibleassetsacquiredinMD&Aandinthenotestothefinancialstatements.Additionally,BMSprovidedlimitedinformationabouttheacquiredassetwithregardtothepastfewyears,includingthecurrentphaseatacquisition,andreferencedthenotestothefinancialstatementsforfurtherinformation.ThosenotesprovidedareconciliationofidentifiedIPR&Dassets,encompassingIPR&DforeachacquisitionandadescriptionofthechangeinIPR&Dyearoveryear,includingtransfersandimpairmentstakenin2011.

J&JprovidedabriefdescriptionofIPR&DinMD&Aanddetaileddisclosuresinthenotestothefinancialstatements.J&JdisclosedinformationrelatedtoIPR&Dintheacquisitionandbusinesscombinationfootnotes,aswellasintheintangiblesandgoodwillfootnotes.J&JalsodisclosedamaterialincreasetoIPR&DofUS$1millionin2011,aswellastransfersandimpairmentsrecorded

in2011toprovidecontextforthechangeintheaccountyearoveryear.J&JdidnotprovideareconciliationoftheassetsacquiredinthepurchasebutrathertookaccountofonlytheendingIPR&Dbalance.

Ofallsevencompanies,MerckprovidedthemostdetailregardingIPR&D.InaseparatepartofMD&A,Merckdiscussed,amongotherthings,acquiredIPR&D,impairmentsrecordedtoIPR&D,fairvaluemeasurementsandtheassumptionsitused.Additionally,MerckidentifiedIPR&DasacriticalaccountingpolicyintheMD&Asectionandnotestothefinancialstatements.MercksupplementedtheMD&AinformationwithanunderstandingofthechangeyearoveryearinIPR&Dwithinthenotestothefinancialstatements.

Pfizerprovidedinformationonparwith,butlessthan,thatdisclosedbyBMS,EliLilly,MerckandJ&J.PfizerlimiteditsdisclosurestothenatureandfairvalueofIPR&Drecognizedinabusinesscombination.Pfizerwassilent,however,onthevaluationassumptionsandtimingofeffortsnecessarytocompleteprojectsandtheiranticipatedcompletiondates.

12

Peer review: how seven companies handled disclosures

disclosuresrelatedtotherisksanduncertaintiesassociatedwithspecificdevelopmentprojectswerenotprovidedbyanyofthesevencompanies.

QualitativedescriptionsabouttheprojectsbeingdevelopedunderIPR&Dassetsweregenerallyincludedinthefinancialstatementfootnotes.However,informationontheunderlyingvaluationassumptionsanddetailedinformationonthenature,timingandestimatedcostsoftheeffortsnecessarytocompletetheprojectsweregenerallyabsentfromdisclosures,exceptforthosefromJ&JandMerck.

Draft AICPA Practice Aid for disclosures around IPR&D

Refertotheregulatoryenvironmentsectiononpage4foradescriptionofthedraftAICPAPracticeAiddisclosurerequirementsforacquiredIPR&Dassets.

2.2 Disclosures related to material patents

Refertotheregulatoryenvironmentsectiononpage4foradescriptionofSECreportingobservationsaboutmaterialpatentsandrelateddisclosures.

Registrantsareaskedtoprovidethefollowingadditionaldisclosuresformaterialpatents:

• AllcompaniesprovidedextensivedisclosuresrelatedtopatentsinMD&A,andtheyallincludedaspecificsectiononpatentsandintellectualproperty.Eachcompanyprovidedadditionalinformationrelatedtopatentswhenmakingdisclosuresinotherareas,includingproductsandrisksanduncertainties.

• Allcompaniesalsoreferredtothenotestothefinancialstatementsfordisclosuresrelatedtopatentlitigation.Furthermore,J&JincludedaclearscheduleofallpatentlitigationintheUSandasreferencedinitsAbbreviatedNewDrugApplicationfilings,andEliLillyincludedadetailedpatentlitigationdiscussionwithinitsMD&A.

Seeadditionaldetailbelowinsection4.4,protectionofpatentsandproductsales.

SEC requirements BMS Eli Lilly J&J Merck Pfizer Teva Watson

Discussion of the products or technologies that relate to the patent

Jurisdiction in which patent is granted (1)

Expiration date

Patents subject to legal proceedings

Whether patents are owned or licensed

(1) Provided only for the US market.

TevaprovidedverylimitedinformationinMD&AaboutacquiredIPR&D,limitingthediscussiontothedeterminationofIPR&Dimpairment.However,detailswereprovidedinthenotestothefinancialstatements,whichincludedareconciliationofallassetsinvolvedinamaterialacquisition,includingIPR&D,andthemethodologyandassumptionsusedtodeterminefairvaluefortheIPR&Dasoftheacquisitiondate.TevadisclosedatotalincreasetoIPR&Din2011ofmorethanUS$2million,aswellasimpairmentsrecordedandtransferstoR&Dtoprovideanunderstandingofthechangeyearoveryear.BecauseTevaisfocusedprimarilyongenericbrands—incontrasttoBMS,EliLilly,J&J,MerckandPfizer,whichfocusprimarilyonbrandedproducts—itisexpectedthatTeva’sIPR&Dactivitywouldgenerallybesmallerthanthatofitscounterparts.

Inadditiontotheabove,therisksanduncertaintiesassociatedwithIPR&DwereoftendisclosedonagenericbasisinMD&A.Detailed

13The shifting pharmaceutical industry landscape

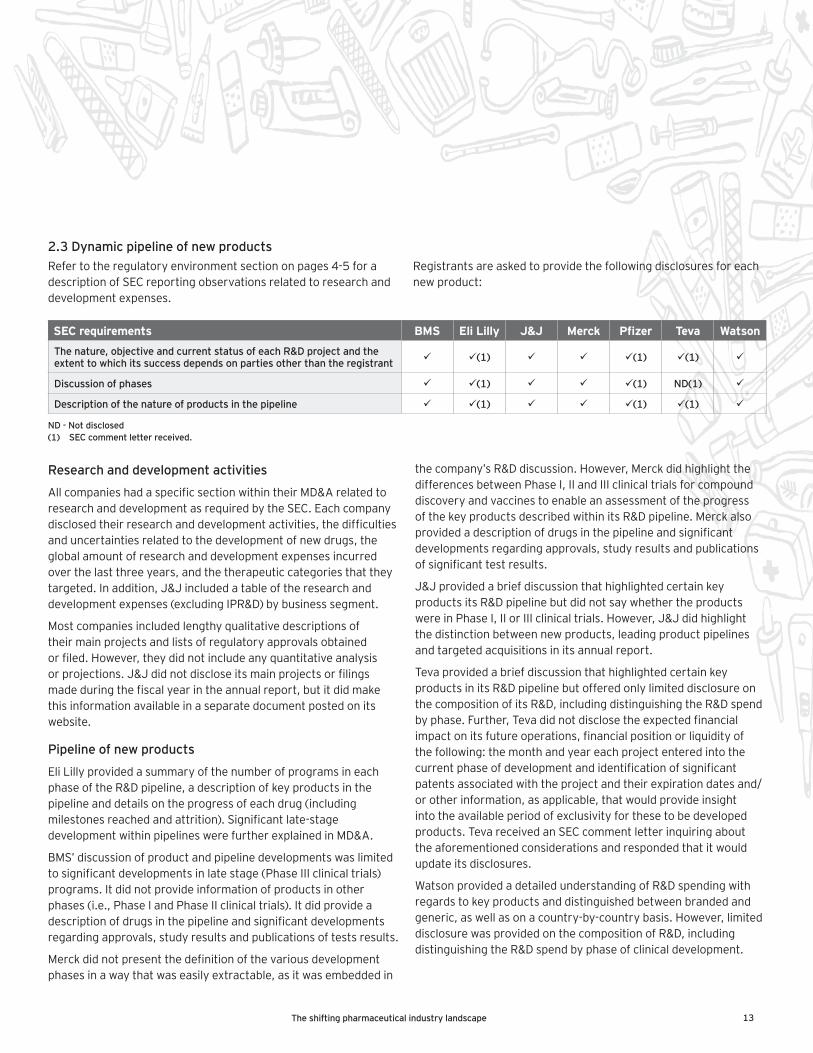

2.3 Dynamic pipeline of new products Refertotheregulatoryenvironmentsectiononpages4-5foradescriptionofSECreportingobservationsrelatedtoresearchanddevelopmentexpenses.

Registrantsareaskedtoprovidethefollowingdisclosuresforeachnewproduct:

SEC requirements BMS Eli Lilly J&J Merck Pfizer Teva Watson

The nature, objective and current status of each R&D project and the extent to which its success depends on parties other than the registrant (1) (1) (1)

Discussion of phases (1) (1) ND(1)

Description of the nature of products in the pipeline (1) (1) (1)

ND - Not disclosed (1) SEC comment letter received.

Research and development activities

AllcompanieshadaspecificsectionwithintheirMD&ArelatedtoresearchanddevelopmentasrequiredbytheSEC.Eachcompanydisclosedtheirresearchanddevelopmentactivities,thedifficultiesanduncertaintiesrelatedtothedevelopmentofnewdrugs,theglobalamountofresearchanddevelopmentexpensesincurredoverthelastthreeyears,andthetherapeuticcategoriesthattheytargeted.Inaddition,J&Jincludedatableoftheresearchanddevelopmentexpenses(excludingIPR&D)bybusinesssegment.

Mostcompaniesincludedlengthyqualitativedescriptionsoftheirmainprojectsandlistsofregulatoryapprovalsobtainedorfiled.However,theydidnotincludeanyquantitativeanalysisorprojections.J&Jdidnotdiscloseitsmainprojectsorfilingsmadeduringthefiscalyearintheannualreport,butitdidmakethisinformationavailableinaseparatedocumentpostedonitswebsite.

Pipeline of new products

EliLillyprovidedasummaryofthenumberofprogramsineachphaseoftheR&Dpipeline,adescriptionofkeyproductsinthepipelineanddetailsontheprogressofeachdrug(includingmilestonesreachedandattrition).Significantlate-stagedevelopmentwithinpipelineswerefurtherexplainedinMD&A.

BMS’discussionofproductandpipelinedevelopmentswaslimitedtosignificantdevelopmentsinlatestage(PhaseIIIclinicaltrials)programs.Itdidnotprovideinformationofproductsinotherphases(i.e.,PhaseIandPhaseIIclinicaltrials).Itdidprovideadescriptionofdrugsinthepipelineandsignificantdevelopmentsregardingapprovals,studyresultsandpublicationsoftestsresults.

Merckdidnotpresentthedefinitionofthevariousdevelopmentphasesinawaythatwaseasilyextractable,asitwasembeddedin

thecompany’sR&Ddiscussion.However,MerckdidhighlightthedifferencesbetweenPhaseI,IIandIIIclinicaltrialsforcompounddiscoveryandvaccinestoenableanassessmentoftheprogressofthekeyproductsdescribedwithinitsR&Dpipeline.Merckalsoprovidedadescriptionofdrugsinthepipelineandsignificantdevelopmentsregardingapprovals,studyresultsandpublicationsofsignificanttestresults.

J&JprovidedabriefdiscussionthathighlightedcertainkeyproductsitsR&DpipelinebutdidnotsaywhethertheproductswereinPhaseI,IIorIIIclinicaltrials.However,J&Jdidhighlightthedistinctionbetweennewproducts,leadingproductpipelinesandtargetedacquisitionsinitsannualreport.

TevaprovidedabriefdiscussionthathighlightedcertainkeyproductsinitsR&DpipelinebutofferedonlylimiteddisclosureonthecompositionofitsR&D,includingdistinguishingtheR&Dspendbyphase.Further,Tevadidnotdisclosetheexpectedfinancialimpactonitsfutureoperations,financialpositionorliquidityofthefollowing:themonthandyeareachprojectenteredintothecurrentphaseofdevelopmentandidentificationofsignificantpatentsassociatedwiththeprojectandtheirexpirationdatesand/orotherinformation,asapplicable,thatwouldprovideinsightintotheavailableperiodofexclusivityforthesetobedevelopedproducts.TevareceivedanSECcommentletterinquiringabouttheaforementionedconsiderationsandrespondedthatitwouldupdateitsdisclosures.

WatsonprovidedadetailedunderstandingofR&Dspendingwithregardstokeyproductsanddistinguishedbetweenbrandedandgeneric,aswellasonacountry-by-countrybasis.However,limiteddisclosurewasprovidedonthecompositionofR&D,includingdistinguishingtheR&Dspendbyphaseofclinicaldevelopment.

14

Peer review: how seven companies handled disclosures

SEC comments

SeveralofthecompaniesinthissurveyreceivedcommentsduringthepasttwoyearsrelatingtotheirR&Ddisclosures.TheSEC’scommentsweregenerallyfocusedonthefollowingareas:

1.R&Dspendingbyproject,bysegmentandbystageofdevelopment

2.FoodandDrugAdministration(FDA)approvalandpatentsassociatedwithprojectsinPhaseIIIclinicaltrials

3.ThenumberofnewdrugsinPhaseIIIclinicaltrialsandhowmanycompoundsweresubmittedforregulatoryreview

4.Theperiodoftimeittooktocompleteaclinicaltrial

5.TheimpactofR&Dprojectsonthecompany’sfutureoperationsandliquidity

3. Performance

3.1 Non-GAAP financial measures

Non-GAAPfinancialmeasures(oradjustedearnings)provideanalternativeviewofanentity’sfinancialperformance.Adjustedearningsmeasuresareusedbymanagementtoenhanceinvestors’understandingofacompany’sperformancebyadjustingfornonrecurringeventsoritemsthatdonotreflectacompany’snormaloperations.

Mostofthesurveyedcompaniesprovideddetailedexplanationsoftheadjustedearnings,akeyperformanceindicatorinthepharmaceuticalindustry.

BMSbrieflyoutlinedthepurposebehindeachlineitemincludedintheadjustedearningsreconciliation.

EliLillydiscussedadjustedearningsmainlyonanearnings-per-share(EPS)basisandprovidedonlyadjustedrevenuefigures.EliLilly’sdiscussionofnon-GAAPfinancialmeasureswasmostlyconfinedtotheproxystatementsectionofitsannualreport,whereitalsodescribedhowmanagementcompensationwasdetermined.

J&Jprovidedadetailedbreakdownofadjustmentsthroughtheuseofinformationheadingsforeachadjustment,butitdidnotincludeinformationregardingthenatureoftheadjustments,nordiditreferenceotherpartsofthefinancialstatementstoobtainmoreinformation.Overall,adjustedearningsdidnotappeartobeasignificantemphasisofJ&Jcomparedwiththeothercompanies,nordidJ&Jexcludethepurchaseaccountingadjustmentandresultingamortizationofintangibles,whichappearstobegeneralpracticeformanyUScompanies.

Merckexplainedthepurposeforusinganadjustedearningsamountforinternalpurposes,anditidentifiedtheareasinwhichadjustedincomeisevaluatedinternally.

Pfizerprovidedthemostcontextformanagement’suseofadjustedincomemeasuresforinternalpurposes,suchastheassessmentofseniormanagementcompensation,thepreparationofannualbudgetsandtheanalysisofoperatingresults.

Tevaprovidedanunderstandingoftheuseandimportanceofnon-GAAPfinancialmeasuresforinternalpurposesandofferedadetailedbreakdownoftheadjustmentstoreportedGAAPmeasures.Additionally,Tevaprovidedafullnon-GAAPincomestatement.During2011,TevadidreceiveanSECcommentletter,notingthatdisclosureofafullnon-GAAPincomestatementmayattachundueprominencetothenon-GAAPinformation.

BMS Eli Lilly J&J Merck Pfizer Teva Watson

Description of adjusted earnings Non-GAAP

earnings

(1) (2) Non-GAAP

income

Adjusted income

Non-GAAP

financial measures

Non-GAAP

earnings

Adjusted earnings presented (non-GAAP financial measures)

Breakdown of calculation of adjusted income

Explanation of the purpose of the adjusted earnings figure ND

Explanation for significant adjustments highlighted

Adjusted earnings disclosed in the MD&A section ND ND

(1) Eli Lilly provided only adjusted revenues and EPS in its proxy statement. No adjusted earnings were provided. (2) J&J provided a reconciliation of non-GAAP adjusted revenues and EPS on its website (referenced in its proxy statement).

15The shifting pharmaceutical industry landscape

3,709 4,348

9,672

6,392

10,009

2,759 456

212

(33)

4,195

5,425

8,208

1,679

(2,000)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

BMS Eli Lilly J&J Merck Pfizer Teva Watson

Adjustments included to get to adjusted earnings

US GAAP earnings

US$ millions

Adjustments to US GAAP earnings

Watsonprovidedanexplanationoftheinternalpurposesforusinganadjustedearningsmeasureandtheareasinwhichadjustedincomeisevaluatedinternally.Watsonalsoprovidedadetailedreconciliationofthenon-GAAPadjustments.

3.2 Reported earnings to adjusted earnings

PfizerandMerckemployedthemostsignificantnon-GAAPadjustmentswhencalculatingadjustedearnings.Theseadjustmentsgenerallyrelatedtopurchaseaccountingandcostsfrommaterialacquisitionsmadeduringtheyear.

Merckalsotookrestructuringcostsintoaccounttoadjustitsearnings,asdidTeva.BMSandEliLillyadjustedearningsmainlyforrestructuringcostsbutalsoincludedeliminationofassetimpairments.J&Jconsideredonlylitigationchargestoarriveatadjustedearnings.

Forfurtherinformation,pleaserefertotheappendix,onpage35.

Adjustments to US GAAP earnings

16

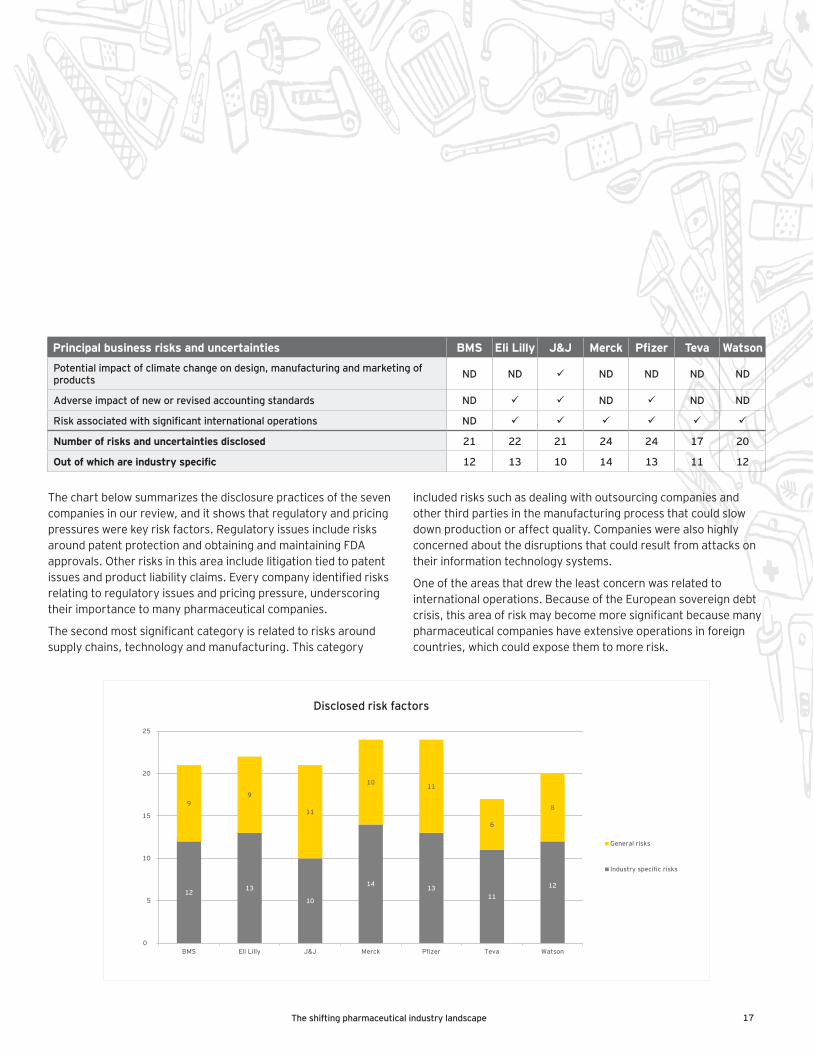

Principal business risks and uncertainties BMS Eli Lilly J&J Merck Pfizer Teva Watson

Descriptions of key risks

Industry specific risks

Intense competition around branded products

Costly and highly uncertain nature of research and development

Competition from lower-priced generic products

Loss or expiration of intellectual property in the near future ND ND ND

Unexpected developments related to safety or efficiency of products ND

Pipeline productivity and competition — ability to continuously develop or replace products

Pricing and access pressures

Current and future product liability claims ND

Regulatory environment:

Potential exposure to government price controls ND ND

Ability to obtain and maintain approval for products

Potential noncompliance issues and scrutiny from FDA and other regulators

Adverse effect from changes in laws and regulations

High dependency of revenues, cash flows and earnings on protections given by patents ND

Negative events in animal health industry ND ND ND ND ND

General risks

Manufacturing and supply-chain difficulties

Reliance on third-party and outsourcing arrangements

Prolonged economic downturn ND

Financial distress and bankruptcies experienced by significant customers ND ND ND ND

Economic factors, including inflation and fluctuating interest rates and currency values

Political and economic instability caused by terrorist attacks ND ND ND ND

Interruptions of computer systems, impairing ability to conduct business ND

Vulnerability of key company products, and their significant profits and cash flows, to adverse market events ND ND

Effect of complex and evolving tax laws, which may result in additional liabilities ND ND ND

Failure to realize the anticipated benefits of strategic initiatives and acquisitions ND

Peer review: how seven companies handled disclosures

4. Risk and mitigation

4.1 Principal business risks and uncertaintiesOurreviewincludeshowclearlytheissue,impactandmitigationofrisksanduncertaintieshavebeendisclosed.

Thefollowingcharthighlightssimilaritiesanddifferencesinthelevelofdisclosure:

17The shifting pharmaceutical industry landscape

Thechartbelowsummarizesthedisclosurepracticesofthesevencompaniesinourreview,anditshowsthatregulatoryandpricingpressureswerekeyriskfactors.RegulatoryissuesincluderisksaroundpatentprotectionandobtainingandmaintainingFDAapprovals.Otherrisksinthisareaincludelitigationtiedtopatentissuesandproductliabilityclaims.Everycompanyidentifiedrisksrelatingtoregulatoryissuesandpricingpressure,underscoringtheirimportancetomanypharmaceuticalcompanies.

Thesecondmostsignificantcategoryisrelatedtorisksaroundsupplychains,technologyandmanufacturing.Thiscategory

includedriskssuchasdealingwithoutsourcingcompaniesandotherthirdpartiesinthemanufacturingprocessthatcouldslowdownproductionoraffectquality.Companieswerealsohighlyconcernedaboutthedisruptionsthatcouldresultfromattacksontheirinformationtechnologysystems.

Oneoftheareasthatdrewtheleastconcernwasrelatedtointernationaloperations.BecauseoftheEuropeansovereigndebtcrisis,thisareaofriskmaybecomemoresignificantbecausemanypharmaceuticalcompanieshaveextensiveoperationsinforeigncountries,whichcouldexposethemtomorerisk.

Principal business risks and uncertainties BMS Eli Lilly J&J Merck Pfizer Teva Watson

Potential impact of climate change on design, manufacturing and marketing of products ND ND ND ND ND ND

Adverse impact of new or revised accounting standards ND ND ND ND

Risk associated with significant international operations ND

Number of risks and uncertainties disclosed 21 22 21 24 24 17 20

Out of which are industry specific 12 13 10 14 13 11 12

12 13

10

14 13 11

12

9 9

11

10 11

6

8

0

5

10

15

20

25

BMS Eli Lilly J&J Merck Pfizer Teva Watson

General risks

Industry specific risks

Disclosed risk factors

18

Peer review: how seven companies handled disclosures

4.2 Cost reduction, government regulations and pricing constraintsTheregulatoryenvironmentisoneofthekeyrisksidentifiedbyallthecompaniessurveyed.Reflectingthatlevelofconcern,wewouldexpecttheSECstafftorequestregistrantstoprovidemoreinformationabouttheserisksandtheirpotentialimpact.

Initsdiscussionofthebusinessenvironment,BMSprovidedextensivedisclosuresaboutgovernmentregulationsandpriceconstraints.OfparticularconcernwerethecostsincurredasaresultofFDA-imposedrequirementscoveringthetesting,safety,effectiveness,manufacturing,labeling,marketing,advertisingandpost-marketingsurveillanceofitsproducts.Similarly,BMSincurredextensivecostsforactivitiesoutsidetheUSbasedonrequirementsissuedbytheEuropeanMedicinesAgency,thecounterparttotheFDAintheEuropeanUnion(EU).Inaddition,BMSincludedaspecifickeyriskthatindicatesitfacesincreasedpricingpressureandotherrestrictionsintheUSandabroadfrommanagedcareorganizations,institutionalpurchasersandgovernmentagencies,aswellasprogramsthatcouldnegativelyaffectsalesandprofitmargins.WithinthebusinessenvironmentsectionoftheMD&A,BMSalsomentionsvariouspricingconstraintsstemmingfromgovernmentregulation.

EliLillydisclosedakeyriskrelatedtotheimpactofincreasinggovernmentpricecontrolsandotherhealthcarecost-containmentmeasures.Additionally,EliLillymentionedtheimpactofhealthcarereform,includingtheestimateddollarimpacttothefinancialstatementsandtheeffectofthisregulationwithinMD&A.

J&Jmentioned,bothinthebusinesssectionandinthe

identificationofriskfactors,theincreasingpressureonpricescausedbyregulation.However,therewaslimitedinformationabouthowthistrendwouldaffectsales,pricingandotherareasofthebusiness.

Merckidentifiedariskduetoincreasedregulationfromthegovernmentandasecondrisk,frompricingpressures,thatcitedgovernmentasakeyriskfactor.InthehealthcareenvironmentportionoftheMD&Asection,Merckalsocitedpricingpressuresbutlinkedthemtoglobaleffortstowardhealthcarecostcontainment,healthcarereformintheUSandotherregulatoryefforts.

Pfizeridentifiedkeyrisksrelatingtopricingpressuresfromhealthcarereformandhealthcarelegislation.ItalsocitedgovernmentregulationandmanagedcaretrendsandthepotentialimpactoftheserisksinboththeUSandabroad.Additionally,MD&Areferencedthe2011financialreport,whichincludedfurtherdiscussionofthesetopicsinitsfinancialreviewanalysis.

Tevaidentifiedakeyriskindicatingthatitsrevenuesandprofitsfromgenericproductstypicallydeclinedasaresultofcompetitionfromotherpharmaceuticalcompaniesandofincreasedgovernmentpricingpressures.Tevaalsodiscussedotherrisksrelatingtohealthcarereformandgovernmentregulation,inadditiontoprovidingextensivedisclosuresabouttheimpactofregulationbothwithintheUSandinternationally.

Watsondidnotidentifyspecificrisksfrompricingpressurestiedtoregulations.However,Watsondidprovidesomediscussionontheimpactofregulationonitsbusiness.

19The shifting pharmaceutical industry landscape

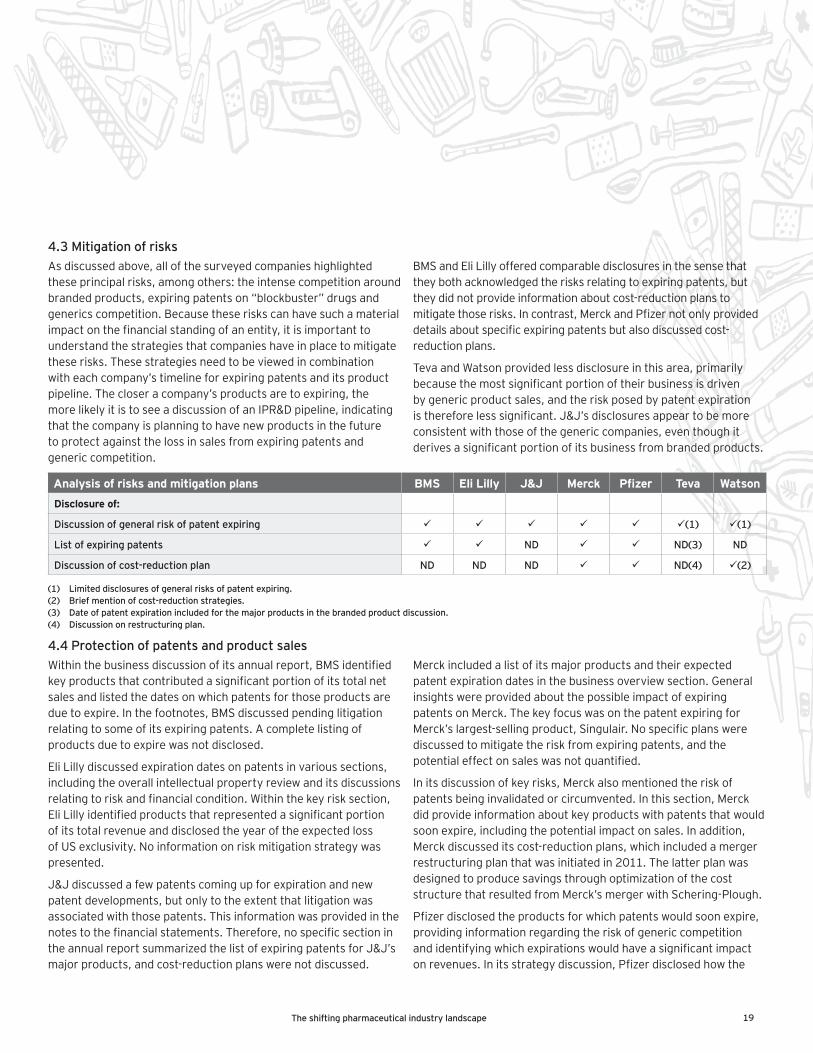

4.3 Mitigation of risks Asdiscussedabove,allofthesurveyedcompanieshighlightedtheseprincipalrisks,amongothers:theintensecompetitionaroundbrandedproducts,expiringpatentson“blockbuster”drugsandgenericscompetition.Becausetheseriskscanhavesuchamaterialimpactonthefinancialstandingofanentity,itisimportanttounderstandthestrategiesthatcompanieshaveinplacetomitigatetheserisks.Thesestrategiesneedtobeviewedincombinationwitheachcompany’stimelineforexpiringpatentsanditsproductpipeline.Thecloseracompany’sproductsaretoexpiring,themorelikelyitistoseeadiscussionofanIPR&Dpipeline,indicatingthatthecompanyisplanningtohavenewproductsinthefuturetoprotectagainstthelossinsalesfromexpiringpatentsandgenericcompetition.

BMSandEliLillyofferedcomparabledisclosuresinthesensethattheybothacknowledgedtherisksrelatingtoexpiringpatents,buttheydidnotprovideinformationaboutcost-reductionplanstomitigatethoserisks.Incontrast,MerckandPfizernotonlyprovideddetailsaboutspecificexpiringpatentsbutalsodiscussedcost-reductionplans.

TevaandWatsonprovidedlessdisclosureinthisarea,primarilybecausethemostsignificantportionoftheirbusinessisdrivenbygenericproductsales,andtheriskposedbypatentexpirationisthereforelesssignificant.J&J’sdisclosuresappeartobemoreconsistentwiththoseofthegenericcompanies,eventhoughitderivesasignificantportionofitsbusinessfrombrandedproducts.

Analysis of risks and mitigation plans BMS Eli Lilly J&J Merck Pfizer Teva Watson

Disclosure of:

Discussion of general risk of patent expiring (1) (1)

List of expiring patents ND ND(3) ND

Discussion of cost-reduction plan ND ND ND ND(4) (2)

(1) Limited disclosures of general risks of patent expiring.(2) Brief mention of cost-reduction strategies.(3) Date of patent expiration included for the major products in the branded product discussion.(4) Discussion on restructuring plan.

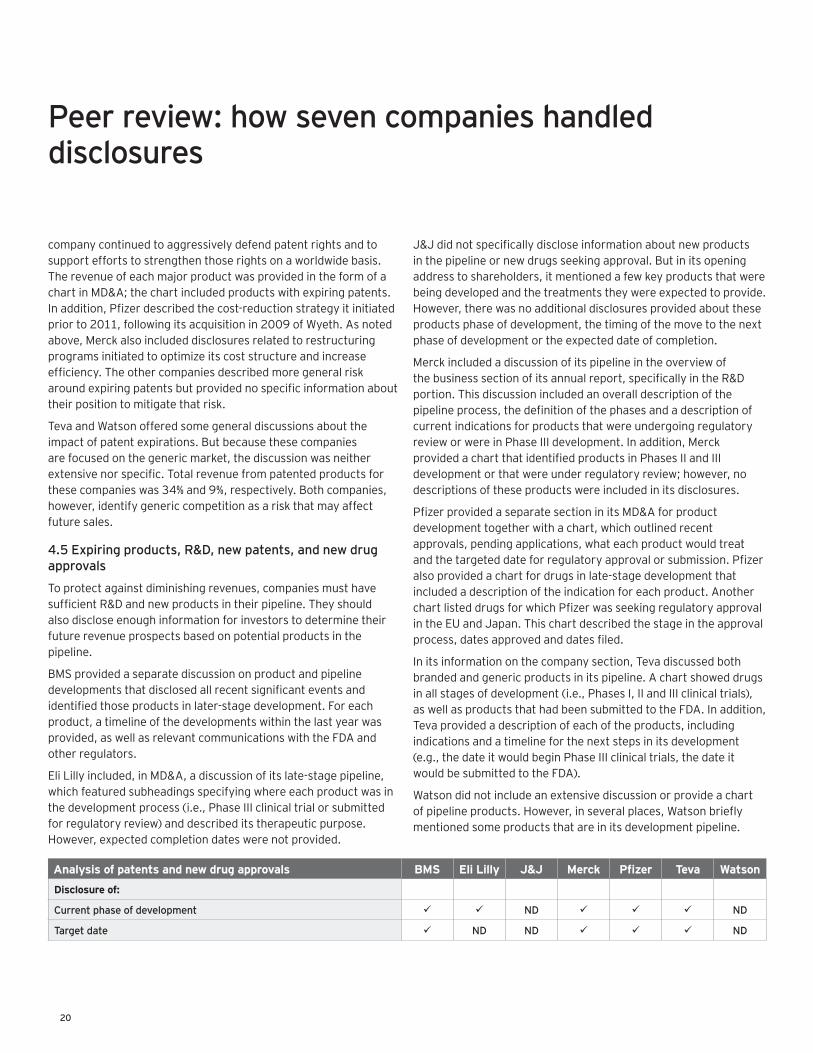

4.4 Protection of patents and product salesWithinthebusinessdiscussionofitsannualreport,BMSidentifiedkeyproductsthatcontributedasignificantportionofitstotalnetsalesandlistedthedatesonwhichpatentsforthoseproductsareduetoexpire.Inthefootnotes,BMSdiscussedpendinglitigationrelatingtosomeofitsexpiringpatents.Acompletelistingofproductsduetoexpirewasnotdisclosed.

EliLillydiscussedexpirationdatesonpatentsinvarioussections,includingtheoverallintellectualpropertyreviewanditsdiscussionsrelatingtoriskandfinancialcondition.Withinthekeyrisksection,EliLillyidentifiedproductsthatrepresentedasignificantportionofitstotalrevenueanddisclosedtheyearoftheexpectedlossofUSexclusivity.Noinformationonriskmitigationstrategywaspresented.

J&Jdiscussedafewpatentscomingupforexpirationandnewpatentdevelopments,butonlytotheextentthatlitigationwasassociatedwiththosepatents.Thisinformationwasprovidedinthenotestothefinancialstatements.Therefore,nospecificsectionintheannualreportsummarizedthelistofexpiringpatentsforJ&J’smajorproducts,andcost-reductionplanswerenotdiscussed.

Merckincludedalistofitsmajorproductsandtheirexpectedpatentexpirationdatesinthebusinessoverviewsection.GeneralinsightswereprovidedaboutthepossibleimpactofexpiringpatentsonMerck.ThekeyfocuswasonthepatentexpiringforMerck’slargest-sellingproduct,Singulair.Nospecificplanswerediscussedtomitigatetheriskfromexpiringpatents,andthepotentialeffectonsaleswasnotquantified.

Initsdiscussionofkeyrisks,Merckalsomentionedtheriskofpatentsbeinginvalidatedorcircumvented.Inthissection,Merckdidprovideinformationaboutkeyproductswithpatentsthatwouldsoonexpire,includingthepotentialimpactonsales.Inaddition,Merckdiscusseditscost-reductionplans,whichincludedamergerrestructuringplanthatwasinitiatedin2011.ThelatterplanwasdesignedtoproducesavingsthroughoptimizationofthecoststructurethatresultedfromMerck’smergerwithSchering-Plough.

Pfizerdisclosedtheproductsforwhichpatentswouldsoonexpire,providinginformationregardingtheriskofgenericcompetitionandidentifyingwhichexpirationswouldhaveasignificantimpactonrevenues.Initsstrategydiscussion,Pfizerdisclosedhowthe

20

Peer review: how seven companies handled disclosures

companycontinuedtoaggressivelydefendpatentrightsandtosupporteffortstostrengthenthoserightsonaworldwidebasis.TherevenueofeachmajorproductwasprovidedintheformofachartinMD&A;thechartincludedproductswithexpiringpatents.Inaddition,Pfizerdescribedthecost-reductionstrategyitinitiatedpriorto2011,followingitsacquisitionin2009ofWyeth.Asnotedabove,Merckalsoincludeddisclosuresrelatedtorestructuringprogramsinitiatedtooptimizeitscoststructureandincreaseefficiency.Theothercompaniesdescribedmoregeneralriskaroundexpiringpatentsbutprovidednospecificinformationabouttheirpositiontomitigatethatrisk.

TevaandWatsonofferedsomegeneraldiscussionsabouttheimpactofpatentexpirations.Butbecausethesecompaniesarefocusedonthegenericmarket,thediscussionwasneitherextensivenorspecific.Totalrevenuefrompatentedproductsforthesecompanieswas34%and9%,respectively.Bothcompanies,however,identifygenericcompetitionasariskthatmayaffectfuturesales.

4.5 Expiring products, R&D, new patents, and new drug approvals

Toprotectagainstdiminishingrevenues,companiesmusthavesufficientR&Dandnewproductsintheirpipeline.Theyshouldalsodiscloseenoughinformationforinvestorstodeterminetheirfuturerevenueprospectsbasedonpotentialproductsinthepipeline.

BMSprovidedaseparatediscussiononproductandpipelinedevelopmentsthatdisclosedallrecentsignificanteventsandidentifiedthoseproductsinlater-stagedevelopment.Foreachproduct,atimelineofthedevelopmentswithinthelastyearwasprovided,aswellasrelevantcommunicationswiththeFDAandotherregulators.

EliLillyincluded,inMD&A,adiscussionofitslate-stagepipeline,whichfeaturedsubheadingsspecifyingwhereeachproductwasinthedevelopmentprocess(i.e.,PhaseIIIclinicaltrialorsubmittedforregulatoryreview)anddescribeditstherapeuticpurpose.However,expectedcompletiondateswerenotprovided.

J&Jdidnotspecificallydiscloseinformationaboutnewproductsinthepipelineornewdrugsseekingapproval.Butinitsopeningaddresstoshareholders,itmentionedafewkeyproductsthatwerebeingdevelopedandthetreatmentstheywereexpectedtoprovide.However,therewasnoadditionaldisclosuresprovidedabouttheseproductsphaseofdevelopment,thetimingofthemovetothenextphaseofdevelopmentortheexpecteddateofcompletion.

Merckincludedadiscussionofitspipelineintheoverviewofthebusinesssectionofitsannualreport,specificallyintheR&Dportion.Thisdiscussionincludedanoveralldescriptionofthepipelineprocess,thedefinitionofthephasesandadescriptionofcurrentindicationsforproductsthatwereundergoingregulatoryrevieworwereinPhaseIIIdevelopment.Inaddition,MerckprovidedachartthatidentifiedproductsinPhasesIIandIIIdevelopmentorthatwereunderregulatoryreview;however,nodescriptionsoftheseproductswereincludedinitsdisclosures.

PfizerprovidedaseparatesectioninitsMD&Aforproductdevelopmenttogetherwithachart,whichoutlinedrecentapprovals,pendingapplications,whateachproductwouldtreatandthetargeteddateforregulatoryapprovalorsubmission.Pfizeralsoprovidedachartfordrugsinlate-stagedevelopmentthatincludedadescriptionoftheindicationforeachproduct.AnotherchartlisteddrugsforwhichPfizerwasseekingregulatoryapprovalintheEUandJapan.Thischartdescribedthestageintheapprovalprocess,datesapprovedanddatesfiled.

Initsinformationonthecompanysection,Tevadiscussedbothbrandedandgenericproductsinitspipeline.Achartshoweddrugsinallstagesofdevelopment(i.e.,PhasesI,IIandIIIclinicaltrials),aswellasproductsthathadbeensubmittedtotheFDA.Inaddition,Tevaprovidedadescriptionofeachoftheproducts,includingindicationsandatimelineforthenextstepsinitsdevelopment(e.g.,thedateitwouldbeginPhaseIIIclinicaltrials,thedateitwouldbesubmittedtotheFDA).

Watsondidnotincludeanextensivediscussionorprovideachartofpipelineproducts.However,inseveralplaces,Watsonbrieflymentionedsomeproductsthatareinitsdevelopmentpipeline.

Analysis of patents and new drug approvals BMS Eli Lilly J&J Merck Pfizer Teva Watson

Disclosure of:

Current phase of development ND ND

Target date ND ND ND

21The shifting pharmaceutical industry landscape

4.6 Eurozone

Refertotheregulatoryenvironmentsectiononpage3foradescriptionofSECreportingobservationsregardingconcentrationsofbusinesswithEuropeangovernmententities.

Inlimitedcircumstances,wehaveseensomelifesciencescompaniesindicatethattheyhavegonetoacashbasisofrevenuerecognitionforsalesintoEuropeancountries.However,wedidnotseethatapproachtakenbyanyofthesevencompanieswesurveyedforthisstudy.AsthesituationintheEurozonecontinuedtoevolve,first-andsecond-quarterfilingsfor2012werereviewedtodeterminewhetherthesurveyedcompaniesmadesignificantchangesintheirdisclosures.Nonewerenoted,exceptinthecasesofJ&JandMerck,whichindicatedthattheycollectedasignificantportionofreceivablesinEuropeinthesecondquarter.

DisclosuresaroundconcentrationsofcreditriskinEuropehavebecomeincreasinglymoresignificantastheeconomicconditionswithintheEurozonehavedeteriorated.WiththeexceptionofTeva,allofthesurveyedcompaniesincludeddisclosuresrelatingtorisksofreceivableswithintheEurozone.Specifically,J&J,MerckandPfizerdisclosedtheamountofreceivableswithinthecountries

ofGreece,Italy,PortugalandSpain.Further,MerckandPfizerdisclosedtheamountofreceivablesoutstandinginexcessofoneyear.

Manycompaniesdidnotadjusttheirallowanceforthesereceivables,butsomehavetakenalternatestepstoensurethatthereceivableswouldbecollected.Thesestepsincludedfactoringspecificreceivables,amoveadoptedbyBMSandMerck,andrestructuringreceivablesintosovereigndebtofthedebtornation,asteptakenbyPfizer.Inlimitedinstances,BMSdeferredaportionofitsrevenueforsalesintotheEurozone.

Basedonourreviewoffirst-andsecond-quarterfilingsin2012,wenotedthatJ&JandMerckbothcollectedasignificantportionoftheoutstandingreceivablesfromcertainEurozonecountriesthatwerepreviouslydisclosedintheannualfiling.However,disclosuresdidnotseemtohaveincreasedduringthesubsequentreportingperiod.AstheEurozonesituationplaysout,companieswillneedtoensurethatappropriateconcentrationsofEurozonecreditrisksand/orchangestoaccountingpoliciesareappropriatelydisclosed.

Analysis of concentration of credit risk in Europe BMS Eli Lilly J&J Merck Pfizer Teva Watson

Disclosure of:

Risk due to receivables in Europe ND

Total exposure due to receivables in Europe ND ND (2) (2) (1) ND ND

Receivables in excess of one year in Europe ND ND ND (2) ND ND

(1) Disclosure includes an aggregate amount for all receivables in Greece, Ireland, Italy, Portugal and Spain. (2) Disclosed as aggregate amounts for Greece, Italy, Portugal and Spain.

22

Peer review: how seven companies handled disclosures

5. Accounting policies, judgments and estimates

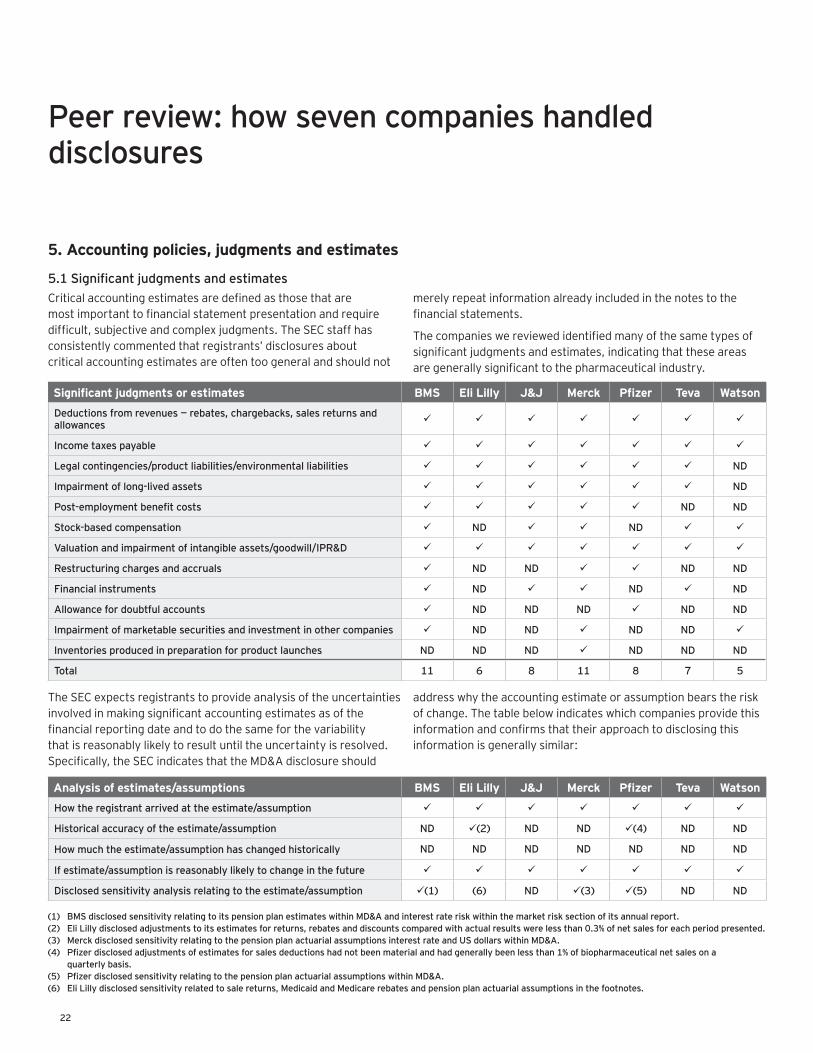

5.1 Significant judgments and estimatesCriticalaccountingestimatesaredefinedasthosethataremostimportanttofinancialstatementpresentationandrequiredifficult,subjectiveandcomplexjudgments.TheSECstaffhasconsistentlycommentedthatregistrants’disclosuresaboutcriticalaccountingestimatesareoftentoogeneralandshouldnot

merelyrepeatinformationalreadyincludedinthenotestothefinancialstatements.

Thecompanieswereviewedidentifiedmanyofthesametypesofsignificantjudgmentsandestimates,indicatingthattheseareasaregenerallysignificanttothepharmaceuticalindustry.

Significant judgments or estimates BMS Eli Lilly J&J Merck Pfizer Teva Watson

Deductions from revenues — rebates, chargebacks, sales returns and allowances

Income taxes payable

Legal contingencies/product liabilities/environmental liabilities ND

Impairment of long-lived assets ND

Post-employment benefit costs ND ND

Stock-based compensation ND ND

Valuation and impairment of intangible assets/goodwill/IPR&D

Restructuring charges and accruals ND ND ND ND

Financial instruments ND ND ND

Allowance for doubtful accounts ND ND ND ND ND

Impairment of marketable securities and investment in other companies ND ND ND ND

Inventories produced in preparation for product launches ND ND ND ND ND ND

Total 11 6 8 11 8 7 5

TheSECexpectsregistrantstoprovideanalysisoftheuncertaintiesinvolvedinmakingsignificantaccountingestimatesasofthefinancialreportingdateandtodothesameforthevariabilitythatisreasonablylikelytoresultuntiltheuncertaintyisresolved.Specifically,theSECindicatesthattheMD&Adisclosureshould

addresswhytheaccountingestimateorassumptionbearstheriskofchange.Thetablebelowindicateswhichcompaniesprovidethisinformationandconfirmsthattheirapproachtodisclosingthisinformationisgenerallysimilar:

Analysis of estimates/assumptions BMS Eli Lilly J&J Merck Pfizer Teva Watson

How the registrant arrived at the estimate/assumption

Historical accuracy of the estimate/assumption ND (2) ND ND (4) ND ND

How much the estimate/assumption has changed historically ND ND ND ND ND ND ND

If estimate/assumption is reasonably likely to change in the future

Disclosed sensitivity analysis relating to the estimate/assumption (1) (6) ND (3) (5) ND ND

(1) BMS disclosed sensitivity relating to its pension plan estimates within MD&A and interest rate risk within the market risk section of its annual report.(2) Eli Lilly disclosed adjustments to its estimates for returns, rebates and discounts compared with actual results were less than 0.3% of net sales for each period presented.(3) Merck disclosed sensitivity relating to the pension plan actuarial assumptions interest rate and US dollars within MD&A.(4) Pfizer disclosed adjustments of estimates for sales deductions had not been material and had generally been less than 1% of biopharmaceutical net sales on a

quarterly basis.(5) Pfizer disclosed sensitivity relating to the pension plan actuarial assumptions within MD&A.(6) Eli Lilly disclosed sensitivity related to sale returns, Medicaid and Medicare rebates and pension plan actuarial assumptions in the footnotes.

23The shifting pharmaceutical industry landscape

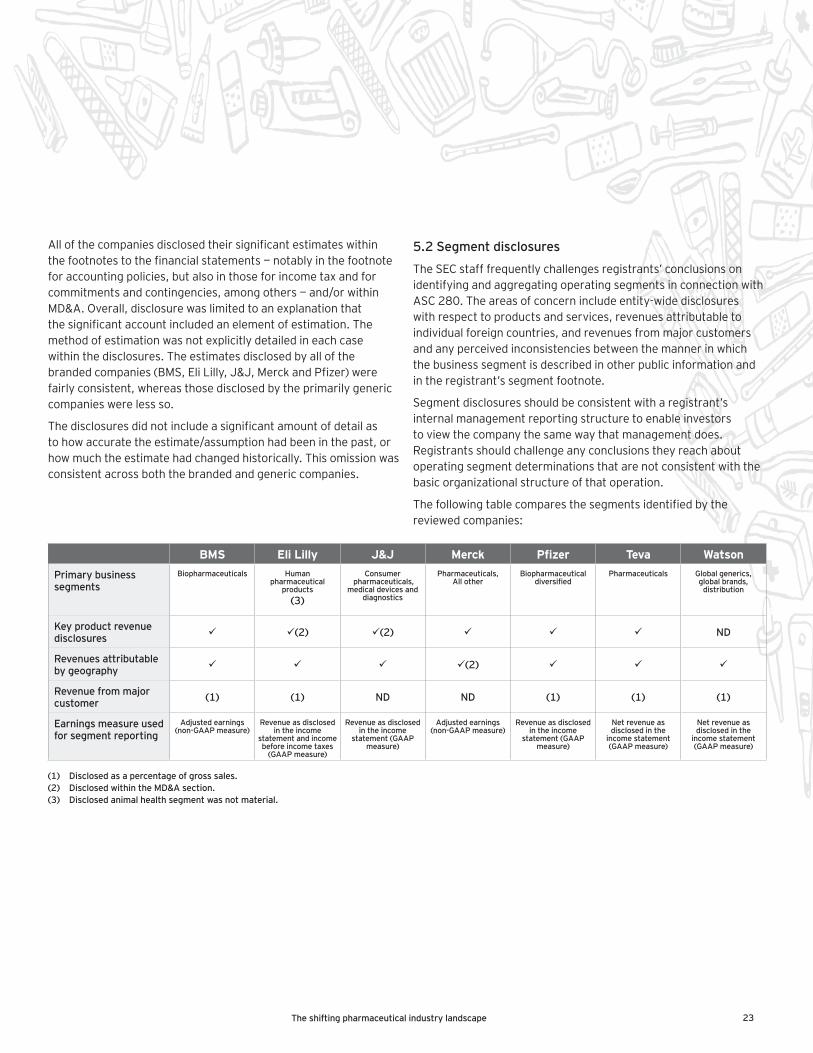

Allofthecompaniesdisclosedtheirsignificantestimateswithinthefootnotestothefinancialstatements—notablyinthefootnoteforaccountingpolicies,butalsointhoseforincometaxandforcommitmentsandcontingencies,amongothers—and/orwithinMD&A.Overall,disclosurewaslimitedtoanexplanationthatthesignificantaccountincludedanelementofestimation.Themethodofestimationwasnotexplicitlydetailedineachcasewithinthedisclosures.Theestimatesdisclosedbyallofthebrandedcompanies(BMS,EliLilly,J&J,MerckandPfizer)werefairlyconsistent,whereasthosedisclosedbytheprimarilygenericcompanieswerelessso.

Thedisclosuresdidnotincludeasignificantamountofdetailastohowaccuratetheestimate/assumptionhadbeeninthepast,orhowmuchtheestimatehadchangedhistorically.Thisomissionwasconsistentacrossboththebrandedandgenericcompanies.

5.2 Segment disclosures

TheSECstafffrequentlychallengesregistrants’conclusionsonidentifyingandaggregatingoperatingsegmentsinconnectionwithASC280.Theareasofconcernincludeentity-widedisclosureswithrespecttoproductsandservices,revenuesattributabletoindividualforeigncountries,andrevenuesfrommajorcustomersandanyperceivedinconsistenciesbetweenthemannerinwhichthebusinesssegmentisdescribedinotherpublicinformationandintheregistrant’ssegmentfootnote.

Segmentdisclosuresshouldbeconsistentwitharegistrant’sinternalmanagementreportingstructuretoenableinvestorstoviewthecompanythesamewaythatmanagementdoes.Registrantsshouldchallengeanyconclusionstheyreachaboutoperatingsegmentdeterminationsthatarenotconsistentwiththebasicorganizationalstructureofthatoperation.