Segmenting Supply Chain Risk Using E/CTRM Systems Unifying Theory of Commodity Hedging and Arbitrage WORKING PAPER Circulating Draft: August 5, 2012 Michael “Mack” Frankfurter Partner, IQ3 Solutions Group [email protected] The findings, interpretations and conclusions expressed in this working paper are those of the author. Working papers describe research in progress and are published to elicit comments and to further debate. Any errors are the responsibility of the author. This paper can be downloaded without charge from the Social Science Research Network eLibrary at: http://ssrn.com/abstract=2124559 Copyright © 2012 IQ3 Solutions Group. Michael “Mack” Frankfurter, Author.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Segmenting Supply Chain Risk Using E/CTRM SystemsUnifying Theory of Commodity Hedging and Arbitrage

WORKING PAPERCirculating Draft: August 5, 2012

Michael “Mack” FrankfurterPartner, IQ3 Solutions Group

The findings, interpretations and conclusions expressed in this working paper are those of the author. Working papers describeresearch in progress and are published to elicit comments and to further debate. Any errors are the responsibility of the author. Thispaper can be downloaded without charge from the Social Science Research Network eLibrary at: http://ssrn.com/abstract=2124559

Copyright © 2012 IQ3 Solutions Group. Michael “Mack” Frankfurter, Author.

Page 2 of 51

Segmenting Supply Chain Risk Using E/CTRM SystemsUnifying Theory of Commodity Hedging and Arbitrage

Abstract:

The complexity of managing physical and financial risk throughout the commodity production,

processing and merchandising chain presents numerous challenges. To solve this problem commercials are

increasingly turning to Energy and Commodity Transaction Risk Management (E/CTRM) systems. Still, risk

management functionality within these systems is reported as falling short of requirements.1 Our discussion,

in response, provides an economic framework for developing commodity risk policy and evaluation tools. In

doing so, we unify the theory of normal backwardation with theory of storage, macroeconomic general

equilibrium with multiple equilibria and microeconomic agents,2 basis trading with arbitrage strategies, and

the hedging response function with elastic/inelastic supply-demand economics. After establishing axioms and

rules of inference, we investigate the agribusiness supply chain to help illustrate application.

Keywords: Agribusiness, Arbitrage, Backwardation, Basis Risk, Contango, Cost-of-Carry, Equilibrium, ExpectationsTheory, Hedging Pressure, Multiple Equilibria, No-Arbitrage Bounds, Supply Chain, Term Structure, Theory of Storage

JEL Classification: D82, D84, E12, G13, L92, O13, Q11, Q12, Q13, Q14, Q15, Q16

1 Chris Strickland, “Where’s the ‘RM’ in ETRM? (Part One),” Energy Risk Magazine, July 9, 2012.

2 “Multiple equilibria are likely to be present in dynamic models that have a large number of microeconomic agents.”From: Masanao Aoki, New Approaches to Macroeconomic Modeling: Evolutionary Stochastic Dynamics, MultipleEquilibria, and Externalities as Field Effects, Cambridge University Press, February 1998, p. 3.

Page 3 of 51

Segmenting Supply Chain Risk Using E/CTRM SystemsUnifying Theory of Commodity Hedging and Arbitrage

1. Introduction

The premise that properly functioning futures markets serve a valuable economic purpose is

validated by government policy.3 The primary benefit is that it allows commercial producers, processors

and consumers of an underlying cash commodity to hedge.4 The secondary benefit is that it functions as a

mechanism for transparent price discovery and liquidity which in turn helps to facilitate hedging

activities. Speculation plays a role in such activities, but is not the reason why these markets exist.

It follows that the reallocation of risk affords a reduction in commodity prices because businesses

need not offset adverse price changes with increased margins on products or services. In theory, the

reallocation of risk associated with commodity inputs and outputs results in increased capacity utilization.5

In practice, the complexity of managing risk throughout the commodity production, processing and

merchandising chain presents numerous challenges. To solve this problem commercials are increasingly

turning to Energy and Commodity Transaction Risk Management (E/CTRM) systems.

We initially focus on Spurgin’s (2000) “hedging response function” which provides a behavioral,

yet intuitive, framework for modeling hedging pressure. Next, we review classical commodity theory rooted

in the writings of early 20th century commodity price theorists, and relate these ideas to the concepts of

equilibrium and disequilibrium. This imparts a foundation for exploring “multiple equilibria arbitrage”

which derives from the Sonnenschein-Mantel-Debreu theorem. We then examine basis trading and how

basis risk is segmented into risk factors, and in what way inputs and outputs impact the hedging response

function depending on elastic versus inelastic supply-demand economics. To help illustrate these concepts

we investigate the agribusiness supply chain. Last, we encapsulate these ideas into multi-factor models.

Exordium on E/CTRM Systems

E/CTRM systems refer to a category of applications, technologies and tools that assist companies in

managing business processes associated with commodity asset and resource management. Such processes

involve: commodity production, processing, warehousing and merchandising; transportation planning,

scheduling and logistics; deal capture, trading and risk management; accounting and back office

administration such as clearing and settlement on the financial side, and settlement and invoicing on the

physical side; as well as managing physical and financial regulatory and compliance requirements.

3 “Futures markets play a critically important role in the U.S. economy.” From testimony of Reuben Jeffery III,Chairman U.S. Commodity Futures Trading Commission (CFTC) on November 2, 2005 before the Committee onEnergy and Commerce, United States House of Representatives.

4 By using futures or forward contracts to hedge, a producer, processor or consumer of an underlying asset canestablish a temporary substitute for a cash market transaction that will be realized at a future date.

5 Capacity utilization is a metric used to measure the rate at which potential output levels are being met or used.Capacity utilization rates can also be used to determine the level at which unit costs will increase.

Page 4 of 51

E/CTRM software originally evolved from FERC Order 636,6 which resulted in the wholesale

markets for natural gas in 1992, and FERC Order 888,7 which deregulated the wholesale electric power

markets in North America in 1996. Since that time, E/CTRM systems have expanded its base of usage to

encompass agribusiness and mining, as well as energy industries. The types of companies which use E/CTRM

systems include agribusiness concerns, oil majors and minors, power generators and utilities, petrochemical

and refiners, large industrial end users, and investment banks and hedge funds which trade commodities.

While an in-depth review of E/CTRM technologies is outside the scope of this paper, it is worth

noting that “there is no real standard for what comprises an [E/CTRM] system.”8 This is not surprising

given the variety of physical assets, geographic regions, regulatory regimes, and types of business models

involved in the commodity supply chain. Moreover, while there are standard functionalities integrated into

the major vendor software offerings, dissimilarities within horizontal and vertical market niches makes for

heterogeneous requirements with respect to both functionality and risk management. Indeed, this observation

lends credence to the notion of “multiple equilibria arbitrage” which is presented in this paper.

Exordium on Spot Prices

Commodity pricing theory has a tendency to discuss spot prices as a single representative price.

Reality is far different, and producers, processors and merchandisers who are involved in the cash

commodity markets mostly operate “without any formal guidelines on location, time or size of trading

unit and only informal requirements for reporting transactions (Anderson, Shafer and Haberer, 1996).”9

For example, the reported spot prices for cotton “represent an average price for various qualities

at multiple levels of production, i.e., they may include producer sales, inter-merchant trading, sales to

mills and cooperative pooling.”10 Likewise, the cash markets in the “fed cattle and beef, hog and pork,

and lamb and lamb meat industries” are often dispersed geographically with “on the spot” transactions

occurring vis-à-vis “auction barn sales; video or electronic auction sales; sales through order buyers,

dealers and brokers; and direct trades”.11 The Livestock Marketing Association (LMA), which is the voice

for the livestock marketing industry on legislative and regulatory issues, provides a comprehensive list of

livestock marketing/auctioneers throughout the U.S., reflecting the geographical spread of livestock spot

6 See: http://www.ferc.gov/legal/maj-ord-reg/land-docs/restruct.asp

7 See: http://www.ferc.gov/legal/maj-ord-reg/land-docs/order888.asp

8 CommodityPoint, CTRM Software Sourcebook, UtiliPoint International, May 2011, Ver. 3.

9 Joan Evans and James M. Mahoney, “The Effects of Daily Price Limits on Cotton Futures and Options Trading,”Federal Reserve Bank of New York, Research Paper No. 9627, August 1996, pp 4-5. [Reference: Anderson, Carl G.;Shafer, C. and Haberer, M., “Producer price for cotton qualities vague,” 1996 Beltwide Cotton Conference.]

10 Ibid., Evans and Mahoney (1996), p 5.

11 Grain Inspection, Pacers and Stockyard Administration, U.S. Department of Agriculture, GIPSA Livestock andMeat Marketing Study; Volume 1: Executive Summary and Overview, Final Report. Prepared by RTI International,Health, Social, and Economics Research, RTI Project Number 0209230, January 2007, p ES-1.

Page 5 of 51

price discovery.12/13 According to LMA’s website, local auctions are a vital part of the livestock industry,

serving producers and assuring a fair, competitive cash price through the auction method.

Alternatively, the forward markets for coffee and cocoa have increasingly used so-called “price to

be fixed” (PTBF) contracts where a relevant delivery month of the futures market is chosen as a reference to

determine or fix the price of the physicals contract. This mechanism allows use of the futures market to

hedge price risk, while ensuring delivery of a specific grade at a specific time and location vis-à-vis the

PTBF agreement. The futures position, on the other hand, is never held to delivery, but offset in the market

prior to contract delivery period. Given that grade, quality and location are material factors influencing cash

prices, PTBF is a means for commercial producers and merchandisers of coffee and cocoa to mitigate basis

risk.14 Note: similar instruments exist in other agricultural markets and are called “fixed basis contracts” in

the grain markets, “executable orders” in the sugar trade, and “on-call contracts” for cotton.

Hence, it can be argued that participants in the spot markets, which are generally unobserved and

opaque, establishes pricing in the capacity of “price-takers,” not “price-makers,” notwithstanding assertions

by certain economists to the contrary.15 For example, commercial hedgers such as agribusiness (e.g.,

farmers, elevators, ranchers, stockyards) reference prices in terms of a basis differential, i.e., how much

the cash price is “over” or “under” the referenced futures price.16 A 2010 study by the International Food

Policy Research Institute (IFPRI) supports this hypothesis and concluded that “the futures markets

analyzed generally dominate the spot markets.”17 As with the above discussion on E/CTRM systems, this

observation also lends credence to the notion of “multiple equilibria arbitrage”.18

2. Hedging Response Function19

The version of the hedging response function we present in this paper assumes there are three types

of participants in the futures market for a given commodity: (i) short hedgers; (ii) long hedgers; and (iii)

speculators. Short hedgers are sellers (i.e., producers, processors or merchandisers) who are net long the

underlying cash commodity and use the futures market to fix the sale price. Long hedgers are buyers (i.e.,

consumers, processors or merchandisers) who are net short the underlying cash commodity and use the

market to fix the purchase price. Speculators are traders who enter positions for financial gain.

12 Source: http://www.lmaweb.com See LMA Membership Directory.

13 The South Dakota Department of Agriculture lists forty livestock auction markets in South Dakota in 2007.Source: http://www.livestock.doa.sd.gov/livestock_markets.aspx

14 International Trade Centre, The Coffee Guide, 2002.15 Paul Krguman, “Commodities and speculation: metallic (and other) evidence,” The New York Times, April 20,2009. Also see: Robert Samuelson, “The Fallacy of Blaming Oil ‘Speculators’,” RealClear Politics, May 2, 2012.

16 John McKissick and George Shumaker, “Understanding and Using the Basis,” University of Georgia College ofAgricultural and Environmental Sciences, Bulletin 981/Revised February 1991. [Also see: Baldwin (1986)]

17 M. Hernandez and T. Maximo, “Examining the Dynamic Relationship between Spot and Future Prices of AgriculturalCommodities,” International Food Policy Research Institute, IFPRI Discussion Paper 00988, June 2010.

18 This discussion also suggests difficulty in performing empirical studies that require historical spot price data.

19 Richard Spurgin, “Some Thoughts on the Source of Return to Managed Futures,” Clark University/CISDM, 2000.

Page 6 of 51

The model further assumes that the futures market is symmetric (i.e., a zero sum game excluding

transaction costs), and that long and short hedgers respond differently to changes in the price of a good. If

supply/demand is in equilibrium then the hedging response is symmetric, and speculative capital will not

have an expected return.20 Otherwise, whenever short hedgers respond differently to changes in price versus

long hedgers, equilibrium is out of balance resulting in either a net short hedging response or net long

hedging response. This creates a demand for speculative capital to bridge the gap between hedgers, thereby

encouraging the flow of capital into net speculative positions. Moreover, if there is no commercial hedging

activity in a market, and all risk is held by speculators, the net returns to speculative capital will be zero

before transactions costs, and negative when costs are taken into consideration. Spurgin (2000) also lists the

insurance role of commodity futures and forwards as a necessary condition for the model, whereby

commercials need to have an economic rational to hedge.21 Such economic rational is predicated on inelastic

market conditions whereby changes in a good’s price is difficult to pass along the supply chain.

Notation and Definitions

To explain the hedging response model, we use the following notation and definitions:

Let (HS) represent short hedgers (e.g., producers); let (HL) represent long hedgers (e.g., consumers);

let (ΑΔ) represent speculators; and let (AΓ) represent arbitrageurs.22

Let S0 be the current spot price of the asset; Ft be the current price for future delivery of the underlying

asset, and E(St) be the expected future spot price of the underlying asset. It is noted that S0 is a known variable

equal to a price currently obtainable in the spot market for the underlying asset; Ft is a known variable equal

to the current futures or forward contract price quoted on a futures exchange or over-the-counter market; but

that E(St) is an unknown factor which converts into S0 at some future point in time.

Symmetric relationships shall be designated by the symbol ↔ whereas asymmetric relationships

shall be designated by the symbol → or ← with the arrow designating which direction risk premia is

transferred [e.g., (HS) → (ΑΔ), means that net risk premia was transferred from short hedger to speculators,

resulting in a net excess return to speculators].

Additionally, increasing commodity price is designated by the symbol (↑), including parentheses,

whereas decreasing commodity price are designated by the symbol (↓), including parentheses.

Last, counter-trend strategies are designated by C, and trend-following strategies are designated by

T; for example, (HS)·C refers to a short hedger following a counter-trend strategy.

20 The counterpoint to a balanced hedging response is a balanced speculative response, in that a speculator enteringinto a trade versus another speculator is symmetric, while noting there may be an asymmetric gain/loss outcome.

21 When describing the insurance role as a condition, Spurgin (2000) states: “In this kind of market, the forwardprice must be consistently below the expected future spot value.” This is a reference to “normal backwardation”.

22 Spurgin (2000) cites “arbitrageurs” as a fourth type of participant whose objective is to survey financial instrumentsand take relative value positions between such vehicles. Spurgin’s definition, however, doesn’t include relativevalue positions between physical assets and financial assets; whereas we note this activity is a form of arbitrage.

Page 7 of 51

Asymmetric Scenarios

Based on the hedging response model there are four possible asymmetric scenarios stemming from

behavioral predispositions, i.e., an inclination to either lock in profits or protect against losses; or an inclination

to let profits run or let losses run.23 This framework offers insight into whether trend-following strategies T or

counter-trend strategies C initiated by speculators (ΑΔ) will be successful over time.24

Scenario [A1]

A rise (↑) in commodity price (which is beneficial to producers) generates more initiative from

producers (HS) to lock in higher prices, resulting in a net short hedging position. In theory, consumers (HL)

who are harmed from this scenario have deferred hedging, and either believe that the price increase can be

passed along to its customers, or are hoping that prices will decrease prior to transacting.

Scenario [A2]

A drop (↓) in commodity price (which is beneficial to consumers) generates more initiative from

consumers (HL) to lock in lower costs, resulting in a net long hedging position. In theory, producers (HS)

who are harmed from this scenario have deferred hedging, and are either willing to absorb reduced margins

for their customers’ benefit, or hoping that prices will increase prior to transacting.

For both scenarios [A1] or [A2], the net hedging response will follow a counter-trend strategy.

Since the net speculative position (ΑΔ) is simply the inverse of the net hedging response, we will observe a

trend-following strategy in the net speculative response. Hence, in reaction to these kinds of hedging

scenarios, higher prices (↑) will theoretically result in a net-long trend-following speculative position for

scenario [A1], and lower prices (↓) will theoretically result in a net-short trend-following speculative position

for scenario [A2]. These scenarios can be described by the following propositions: scenario [A1] is expressed

as (↑) = (HS) → (ΑΔ) corresponding to (HS)·C → (ΑΔ)·T; and scenario [A2] is expressed as (↓) = (HL) → (ΑΔ)

corresponding to (HL)·C → (ΑΔ)·T. In each scenario, risk premia or excess return is transferred to (ΑΔ).

Scenario [B1]

A rise (↑) in commodity price causes consumers (HL) to be more concerned about guarding against

margin pressure than producers (HS) are about locking in profits; hence, a net long hedging position is

established. As producers (HS) benefit from this scenario, they are less inclined to hedge because there is no

need to protect against a loss, and/or because they want exposure to the potential of increased profitability.

Scenario [B2]

A drop (↓) in commodity price causes producers (HS) to be more concerned about guarding against

margin pressure than consumers (HL) are about locking in lower costs; hence, a net short hedging position is

established. As consumers (HL) benefit from this scenario, they are less inclined to hedge because there is no

need to protect against a loss, and/or because they want exposure to the potential for better margins.

23 Analysis of behavior is beyond scope of paper. See: M. Frankfurter, “Market risk: Known and unknowns,” FuturesMagazine, December 2010. Note: Spurgin (2000) frames hedging response in economic rather than behavioral terms.

24 Spurgin (2000) refers to counter-trend strategies as “responsive strategies”.

Page 8 of 51

For both scenarios [B1] or [B2], the net hedging response will follow a trend-following strategy.

Since the net speculative position (ΑΔ) is simply the inverse of the net hedge response, we will observe a

counter-trend strategy in the net speculative position. Hence, in reaction to these kinds of hedging

responses, higher prices (↑) will theoretically result in a net-short counter-trend speculative position for

scenario [B1], and lower prices (↓) will theoretically result in a net-long counter-trend speculative position

for scenario [B2]. These scenarios are described by the following propositions: scenario [B1] is expressed as

(↑) = (HL) → (ΑΔ) corresponding to (HL)·T → (ΑΔ)·C;25 and scenario [B2] is expressed as (↓) = (HS) → (ΑΔ)

corresponding to (HS)·T → (ΑΔ)·C. In each scenario, risk premia or excess return is transferred to (ΑΔ).

Insurance Role

The insurance-like context for explaining futures prices in the commodity markets was first

proposed by Keynes (1923, 1930) in his theory of normal backwardation. Essentially, Keynes believed that

hedgers have to pay speculators a risk premium to convince them to accept their risk. The following discusses

how Keynes’ theory of normal backwardation relates to the various hedging response function scenarios.

For scenarios [A1] or [B2], a futures market dominated by producers (HS) as opposed to consumers

(HL) will result in speculators (ΑΔ) having a net long futures position. As a consequence, normal backwardation

will be the prevailing market condition, whereby the futures contract will be priced below the expected

future spot price. This assumption can be restated as the proposition: if (HS) > (HL), then Ft < E(St).

For scenarios [A2] or [B1], a futures market dominated by consumers (HL) as opposed to producers

(HS) will result in speculators (ΑΔ) having a net short futures position. As a consequence, contango26 will be

the prevailing market condition, whereby the futures contract will be priced above the expected future spot

price. This assumption can be restated as the proposition: if (HL) > (HS), then Ft > E(St).

Perfect competition describes markets in which no participant is large enough to have “market

power,” for example, (HS) ↔ (HL) and (ΑΔ) ↔ (ΑΔ). According to Spurgin (2000), liquid futures markets

must exhibit asymmetric tendencies, only then “will a futures market provide a suitable vehicle for hedgers

to manage risk, and for speculative capital to earn positive expected return.” In other words, for liquid

futures markets to attract hedgers, one side at any point in time must exert greater net influence on market

price. Thus, depending on whether long hedgers or short hedgers are price-makers or price-takers (i.e., net

hedging response), the market will be predisposed toward backwardated or contango conditions.

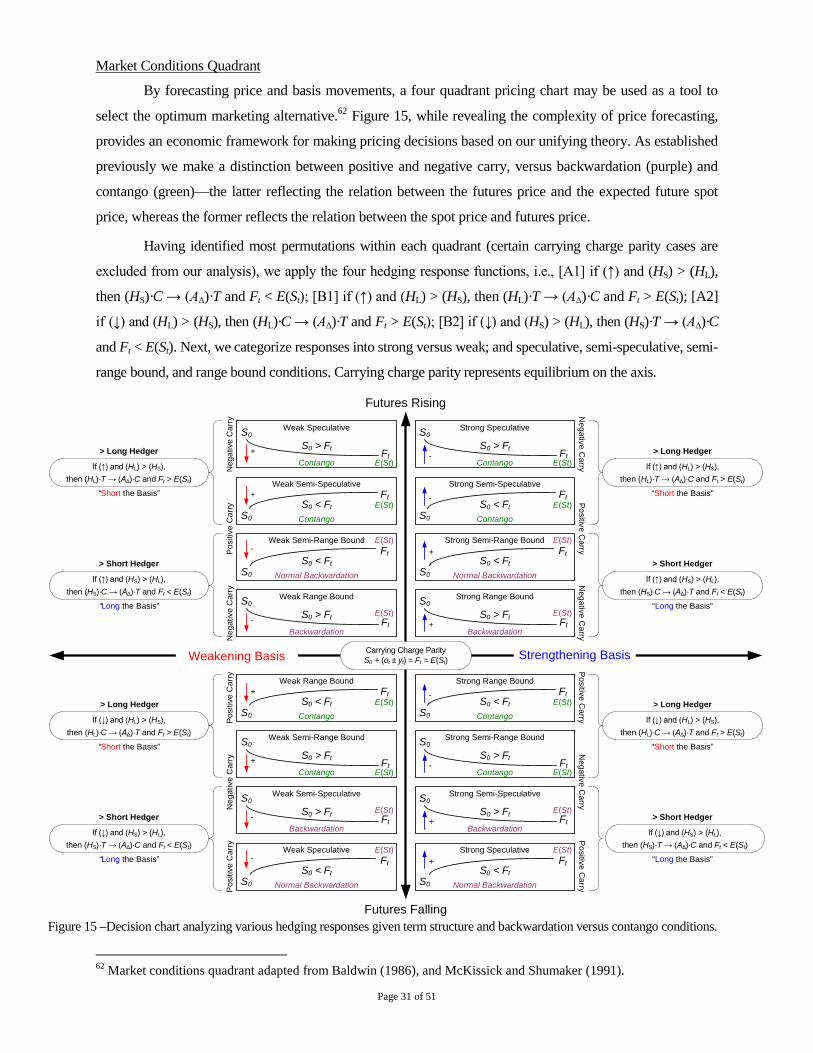

Backwardated or contango predisposition for scenarios [A1], [A2], [B1] and [B2] is as follows:

25 (↑)(HL)·T → (ΑΔ)·C is consistent with a class of participants that has been termed “investulators”. In accordancewith the hedging response function, investors in commodity assets, nominally called speculators, are in fact hedgersresponding to market conditions in the capacity of a long hedger (HL)·T, i.e., hedging against the risk of commodityinflation. See testimony of Sean Cota on behalf of the Petroleum Marketers Association of America and the NewEngland Fuel Institute before the Commodity Futures Trading Commission, Washington, D.C., July 28, 2009.

26 Although the term “contango” was never used by Keynes when describing his theory, he acknowledged that undercertain conditions E(St) can be < S0. See: Rubenstein, A History of the Theory of Investments, 2006, p 52.

Page 9 of 51

Scenarios [A1] and [B1]

[A1] If (↑) and (HS) > (HL), then (HS)·C → (ΑΔ)·T and Ft < E(St)

[B1] If (↑) and (HL) > (HS), then (HL)·T → (ΑΔ)·C and Ft > E(St)

Scenarios [A2] and [B2]

[A2] If (↓) and (HL) > (HS), then (HL)·C → (ΑΔ)·T and Ft > E(St)

[B2] If (↓) and (HS) > (HL), then (HS)·T → (ΑΔ)·C and Ft < E(St)

Symmetric Scenario

[S1/S2] If (HS) = (HL), then Ft = E(St), where [S1] (HS) ↔ (HL) and [S2] (ΑΔ) ↔ (ΑΔ)

In line with Spurgin’s assertion above, we note that less liquid contracts, such as those based on

distant delivery dates, require hedgers to offer additional risk premia in order to attract speculators.

Multiple Price Vectors

Microfoundations literature depicts microeconomics as concerned only with individual behavior and

regards macroeconomic propositions as a consequence of the interaction between individual rational agents. In

contrast to microfoundations theory, the Sonnenschein-Mantel-Debreu theorem27 states that microeconomic

rationality assumptions have no equivalent macroeconomic implications; hence, there may be multiple price

vectors (i.e., multiple equilibria) involving Pareto efficiency. Colander et al. (2008) notes, “What makes

macroeconomics a separate field of study is the complex properties of aggregate behavior that emerges from

the interaction among subjects. Since in a complex system aggregate behavior cannot be deduced from an

analysis of individuals alone, representative-agent models fail to address the most basic questions of

macroeconomics.”28 As argued by Guesnerie (1992), “It is rational for individual players to have rational

expectations if other players have these very same rational expectations, but not necessarily otherwise.”29

Janssen (1993) concludes, “The term ‘rational expectations’ is thus rather misleading… [it] is an aggregate

hypothesis that cannot unconditionally be regarded as being based on [methodological individualism].”30

As can be inferred by the four asymmetric scenarios, it is possible, if not generally the case, that

individual behavior, in response to either rising or falling prices, may react differently at any point in time

to market conditions. Hence, in accordance with the Sonnenschein-Mantel-Debreu theorem, the behavior

27 Hugo F. Sonnenschein, “Do Walras Identity and Continuity Characterize the Class of Community Excess DemandFunctions?” Journal of Economic Theory, 6, 1973, p 345-54; Rudolf Mantel, “On the Characterization of ExcessDemand,” Journal of Economic Theory, 7, 1974, pp 348-353; Gerard Debreu, “Excess Demand Functions,” Journal ofMathematical Economics, 1, 1974, pp 15-21.

28 David Colander; Peter Howitt; Alan Kirman; Axel Leijonhufvud and Perry Mehrling, “Beyond DSGE Models: Towardan Empirically Based Macroeconomics,” American Economic Review, vol. 98(2), May 2008, p 236.

29 Maarten Janssen, “Microfoundations,” Tinbergen Institute Discussion Paper, TI 2006-041/1, p 6. [Reference: RogerGuesnerie, “An Exploration of the Eductive Justifications of the Rational Expectations Hypothesis,” AmericanEconomic Review, Vol. 82, No. 85, 1992, pp 1254-1278.]

30 Maarten Janssen, Microfoundations: A Critical Inquiry, London: Routledge, 1993, p 142.

Page 10 of 51

of hedgers and speculators [e.g., (HS)·C → (ΑΔ)·T; (HL)·T → (ΑΔ)·C; (HL)·C → (ΑΔ)·T; (HS)·T → (ΑΔ)·C;

(HS) ↔ (HL) and (ΑΔ) ↔ (ΑΔ)] may only be ascertained within the operating context of an individual agent.

Spurgin’s (2000) hedging response function, on the other hand, arises from microfoundations theory and

assumes a prevailing “net hedging response” is derived from the aggregate behavior of participants.

3. Multiple Equilibria Arbitrage

Keynes’ (1923, 1930) notion of an insurance-like risk premium posits that the quoted forward price is

driven below “anticipated future spot price” [i.e., E(St)] because the commodity is held back from market and

kept in storage.31 Hicks (1939, 1946) reckoned that consumers are generally better positioned to choose

amongst delivery alternatives as well as time their purchases; whereas producers have operational constraints,

are more exposed to commodity price fluctuations, and for that reason are under more pressure to hedge.32 The

Keynes-Hicks hypothesis depicts this attribute on the demand side for commodities as “congenital weakness”.

A major contribution to the theory of storage was Working’s (1948) research on “carry” versus “inverse-carry”

markets, with “inverse-carry” involving a producer’s commitment to deliver a commodity at a point in the

future superseding the increased reward that could result from selling that commodity in the present. As

described by Kaldor (1939), holding back a commodity in storage is referred to as “convenience yield,” and

together with congenital weakness forms the phenomenon known as “normal backwardation”.

Before proceeding, we note there are different semantics involving the terms “backwardation” and

“contango”. The definition of backwardation and contango as conventionally defined is aligned with Till’s

(2007) “term structure of the futures price curve”. This definition looks at the term structure, and compares

the nearby futures contract with such futures’ subsequent contract months. If the nearby futures contract

price F1 is trading at a premium (higher) than the second nearby or following successive delivery contracts

F2…n, the market is said to be in backwardation or an “inverse-carry” or negative carry market. If the nearby

futures contract price F1 is trading at a discount (lower) than the second nearby or following successive

delivery contracts F2…n, the market is said to be in contango or a “carry” or positive carry market. Note: the

definition of the term structure of futures price curve can be expanded to also encompass the relationship

between the current spot price S0 versus the nearby and successive futures contract prices Ft.

Conversely, Keynes (1930) statement, “The quoted forward price, though above the present spot

price, must fall below the anticipated future spot price by at least the amount of the normal backwardation,”33

expresses an uncommon interpretation. Keynes (1923, 1930) formulated his theory arguing that it is possible

to have the “expected future spot price” E(St), which in the real world is unobservable, valued above the

futures price Ft, even if the term structure exhibits positive carry, i.e., contango as conventionally defined.

31 Mark Rubenstein, A History of the Theory of Investments, Wiley Finance, 2006, pp 52-54.

32 Jodie Gunzberg and Hilary Till, “Absolute Returns in Commodity (Natural Resource) Futures Investments,”EDHEC Risk and Asset Management Research Centre, 2005, p 7.

33 John M. Keynes, A Treatise on Money, Volume II: The Applied Theory of Money, Macmillan, 1930, p 144.

Page 11 of 51

Notation and Definitions

We use the following notation and definitions in this section on multiple equilibria arbitrage:

Again, let S0 be the current spot price of the asset; Ft be the current price for future delivery of the

underlying asset, and E(St) be the expected future spot price of the underlying asset. Once more, S0 is a known

variable equal to a price currently obtainable in the spot market for the underlying asset; Ft is a known

variable equal to the current futures or forward contract price quoted on a futures exchange or over-the-

counter market; but that E(St) is an unknown factor which converts into S0 at some future point in time.

Let ot' represent marginal outlay on storage including facilities, insurance and interest; ±yt' represent

marginal convenience yield –yt' (which increases as inventories decrease), or marginal inconvenience yield

+yt' (which originates from Kaldor’s observation of long hedgers);34 ±εt' represent a marginal error term

(which is required for arbitrage opportunities to exist); and t is the time to delivery of the underlying asset.

Note: when discussing Kaldor (1939), we reference marginal financing costs it' as a separate factor; and when

discussing Brennan (1958), we reference marginal risk-aversion rt' as a separate factor.

In addition to Ft, and E(St), the following notations and conditions illustrate positive carry and

negative (inverse) carry term structures, and establish backwardation and contango as separate concepts.

Let F0 be the current futures contract price for an illiquid futures contract trading after first notice

within the delivery period but prior to final physical delivery date and contract expiry date; let F1 be the

current futures contract price for the liquid nearby future delivery, and F2, F3, and Fn be the series of futures

contract prices for the second nearby, third nearby and subsequent future deliveries. Additionally, let E(S1)

be the expected future spot price for F1 future delivery, E(S2) be the expected future spot price for F2 future

delivery, E(S3) be the expected future spot price for F3 future delivery, and E(Sn) be the expected future spot

price for Fn future delivery. Note that E(S0) is consider equivalent to S0.

Using the above notation, S0 > F1 > F2 > F3 > Fn indicates a term structure reflecting negative carry;

and S0 < F1 < F2 < F3 < Fn indicates a term structure reflecting positive carry.35

Hence, if the term structure reflects positive carry, i.e., S0 < F1 < F2 < F3 < Fn, it is also possible for

the market to simultaneously be in backwardation, i.e., F1 < E(S1), F2 < E(S2), F3 < E(S3), and Fn < E(Sn).

Likewise, if the term structure reflects negative carry, i.e., S0 > F1 > F2 > F3 > Fn, it is also possible for the

market to simultaneously be in contango, i.e., F1 > E(S1), F2 > E(S2), F3 > E(S3), and Fn > E(Sn).36

34 The concept of an “inconvenience yield” is suggested by Kaldor’s (1939) observation of conditions when hedgersare forward buyers. Relates to (↑)(HL)·T → (ΑΔ)·C and class of participants termed “investulators”. See testimony ofSean Cota before the CFTC, Washington, D.C., July 28, 2009. Also see: Frankfurter and Accomazzo (2010), “TermStructure and Roll Yield: Not Your Father’s Backwardation” http://ssrn.com/abstract=1609776

35 While backwardation and contango are conventionally used as substitute terms to describe the term structures ofthe futures price curve, Keynes’ (1930) theory of normal backwardation references the expected future spot pricerelation. In order to preserve these conceptual subtleties, we use the terms positive and negative carry as reference tothe term structure, and the terms backwardation and contango as reference to the expected future spot price relation.

36 For an exposé on possible combinations of positive carry, negative carry, backwardation and contango relationships,see Frankfurter and Accomazzo (2010) discussion on “roll yield permutations”.

Page 12 of 51

We also carry forward concepts and notation from the prior section on the hedging response

model. Let (HS) represent short hedgers (e.g., producers); let (HL) represent long hedgers (e.g., consumers);

let (ΑΔ) represent speculators; and let (AΓ) represent arbitrageurs. In addition, let the symbol designate the

purchase of an asset or holding a long position by a participant; and let the symbol designate the sale of

an asset or holding a short position by a participant. [e.g., (ΑΔ)· signifies that speculators on a net

aggregate basis “went long” by purchasing the underlying asset or related futures.]

Carrying Charge Parity

Carrying charge or “cost-of-carry” is based on the theory of storage which evolved out of the

writings of Kaldor (1939) and Working (1949). The theory assumes that holders of commodities incur a

storage cost for financing and storing inventories (including insurance), as well as a convenience benefit

(i.e., convenience yield) of being able to use inventories the moment they are commercially needed. In

combination, storage cost and convenience yield is expressed as the cost-of-carry which is derived from

Kaldor’s equation Ft – S0 = ot' + it' – yt'. Using algebra, we can then extrapolate that S0 = Ft – ot' – it' + yt';

Ft = S0 + ot' + it' – yt'; and yt' = S0 – Ft + ot' + it'.37 Alternatively, Brennan (1958) defines the net marginal

cost of storage as: mt'(St) = ot'(St) + rt'(St) – ct'(St), where ot'(St) is the marginal outlay on physical storage,

rt'(St) is the marginal risk-aversion factor, and ct'(St) is the marginal convenience yield.

Since ot' and it' are exogenous (i.e., observable), whereas rt' and yt' are indigenous (i.e., interpolated),38

we propose two alternate equations to solve for cost-of-carry based on the difference between Ft and S0. First,

Kaldor’s (1939) and Brennan’s (1958) equations can be simplified as Ft = S0 + (ot' ± yt' ± εt'), where it' is

assumed to be an integrated variable of ot', and rt' is assumed to be an integrated factor of yt', plus a marginal

error term ±εt' which is required for arbitrage opportunities. Our second variant is for theoretical purposes

only, and rewrites εt' as a second derivative, i.e., Ft = S0 + (ot' – yt' · εt'), where εt' is a marginal error term from

which ±yt' can be derived, but only as a function of whether εt' is either ≥ 1 or ≤ 1 including scenarios where

εt' = 0, in which case the cost-of-carry consists of storage outlay only.39 This second equation preserves the

traditional notion of convenience yield as – yt'. In addition, both our versions of Kaldor’s original formula

retains the idea that yt' is discernible from exogenous variables such as storage outlay and/or financing costs.

Before proceeding, in order to logically develop concepts which underlie multiple eqilibria arbitrage,

we begin our discussion by initially removing ±εt' from our alternate Ft = S0 + (ot' ± yt' ± εt') equation.

37 Working (1948, 1949), who examined futures spreads versus prevailing inventories, found that “carrying chargesbehave like prices of storage as regards their relation to the quantity of stocks held in storage.” Accordingly, hedefined the cost-of-carry as the “difference at a given time between prices of a commodity for two different dates ofdelivery,” which relates to the ‘term structure of the futures price curve’ characteristic discussed in this paper.

38 Brennan (1958) propositions that “ot and rt are increasing functions of St so that the marginal outlay and marginalrisk aversion are either constant or are increasing functions of St, i.e., ot' > 0 and ot" ≥ 0; rt' > 0 and rt" ≥ 0. ct is alsoan increasing function of St, but the marginal convenience yield declines and reaches zero at some large level of stocks,

i.e., ct' ≥ 0 and ct" ≤ 0. The net marginal cost of storage in period t may be written as: mt'(St) = ot'(St) + rt'(St) – ct'(St).”

39 The reason we insert a marginal error term into the classical equations of Kaldor (1939) and Brennan (1958),when rt' and yt' have conventionally sufficed in accounting for risk aversion behavior and convenience yield based on therelationship between Ft and S0, is because it permits modeling backwardation and contango relative to E(St).

Page 13 of 51

Physical Market Speculative Strategies

[i] If S0 + (ot' ± yt') < E(St), then (ΑΔ)··S0 enforces S0 = E(St)

[ii] If S0 + (ot' ± yt') > E(St), then (ΑΔ)··S0 (via ‘reverse repurchase’) enforces S0 = E(St)40

This first strategy capitalizes on the implied relation between S0 and E(St), wherein an equilibrium

state is achieved when S0 plus cost-of-carry equals E(St). Hence, if S0 + (ot' ± yt') < E(St), then speculators

would make a profit by taking delivery of the physical commodity today (driving up the current spot price),

with the intention of selling the commodity in the future (driving down the expected future spot price).

Assuming perfect markets and rational expectations (i.e, market participants are risk neutral, know perfectly

the cost-of-carry, and transaction costs are zero), this is the raison d'etre that imposes equilibrium between S0

and E(St). However, since E(St) is in the future and therefore an unknown, this strategy is by definition

speculation, and for that reason determining the theoretical price of E(St) necessitates interpolation.

Futures Market Speculative Strategies

[iii] If Ft < E(St), then (ΑΔ)··Ft enforces Ft = E(St)

[iv] If Ft > E(St), then (ΑΔ)··Ft enforces Ft = E(St)

The second strategy capitalizes on the implied relation between Ft and E(St), wherein an equilibrium

state is achieved when Ft is equal to E(St). Hence, if Ft < E(St), then speculators would make a profit by

purchasing the futures contract (driving up the futures contract price), with the intention of taking delivery

and selling the commodity at the then prevailing spot price (driving down the expected future spot price).

Conversely, since it is easy to short futures contracts, if Ft > E(St), then speculators could also make a

profit by shorting the future contract (driving down the futures contract price), with the intention of making

delivery in the future by purchasing the commodity at the then prevailing spot price (driving up the

expected future spot price). Assuming perfect markets and rational expectations, this is the raison d'etre

that imposes equilibrium between Ft and E(St). In conventional practice, expectations or risk-neutral theory

holds that Ft functions as the price discovery mechanism and current indication of E(St).41

Carrying Charge Parity

[v] Ft = S0 + (ot' ± yt') = E(St), where:

If S0 + (ot' ± yt') < E(St), then (ΑΔ)··S0 enforces S0 = E(St);

If S0 + (ot' ± yt') > E(St), then (ΑΔ)··S0 (via ‘reverse repurchase’) enforces S0 = E(St);

If Ft < E(St), then (ΑΔ)··Ft enforces Ft = E(St); or

If Ft > E(St), then (ΑΔ)··Ft enforces Ft = E(St)

40 Since it is logistically difficult to borrow/short physical assets, if (ΑΔ)··S0 is unenforceable, then S0 + (ot' ± yt') > E(St)suggests directional bias. Note: innovation has led to practice of repurchase agreements on certain physical commodities.

41 Two schools of thought underlie pricing theory: Neo-Walrasian, which emphasizes rational expectations, and Post-Keynesian, which presumes markets are “messy and uncertain”. Telser (1958), who is of the former school, states,“Although hedgers may be willing to pay speculators to bear the risks of price changes, they need not do so ifspeculators are eager to speculate... I accept the hypothesis that the futures price equals the expected spot price.”Kaldor (1972), on the other hand, opined otherwise in his paper, “The Irrelevance of Equilibrium Economics”.

Page 14 of 51

Assuming perfect markets and rational expectations, an equilibrium state is achieved when S0 plus

cost-of-carry equals Ft, and S0 plus cost-of-carry equals E(St), therefore Ft is equal to E(St). The only issue is

that within the paradigm of general equilibrium, carrying charge parity creates a logical fallacy…

Issue of Causal Relativity

Let’s assume Telser’s (1958) expectations theory that “the futures price equals the expected spot

price,” and in accordance with rational expectations and its allied assumption, the efficient market hypothesis

(EMH), the current futures price reflects equilibrium from which participants act as price-takers.

If Ft = S0 + (ot' ± yt') = E(St) expresses equilibrium, and the cost-of-carry (ot' ± yt') is determined from

the delta Ft – S0 as Kaldor (1939) propositioned, which then is used to infer the value of E(St) such that the

delta between S0 and E(St) also equates to (ot' ± yt'), how do we know when the fundamentals underlying

either ot' or yt' have shifted, noting that yt' is inferred by netting ot' from Ft – S0, as opposed to when an

arbitrage opportunity exists because Ft ≠ S0 + (ot' ± yt'), noting that arbitrage is what enforces equilibrium?

Hence, we posit that the viability of using Ft or S0 as a control condition to determine (ot' ± yt') much

less E(St) is suspect, if for the mere reason that one could inversely argue that rational expectations

minimizes the usefulness of carrying charge parity as a mechanism from which economic agents can make

arbitrage decisions. As Muth (1961) posited, “The way expectations are formed depends specifically on the

structure of the relevant system describing the economy.” In other words, models based on rational

expectations assume a predetermined equilibrium around which expectations are formed [e.g., Telser’s

Ft = E(St) or Kaldor’s Ft – S0 = (ot' ± yt')], which in effect reverses the model’s line of causation. Apropos of

carrying charge parity, Telser’s (1958) assumption eliminates arbitrageurs’ incentive to enforce Ft = E(St).

However, if there are situations, as Keynes (1930) suggests (and which the hedging response function

assumes), where Ft = S0 + (ot' ± yt') < E(St), or Ft = S0 + (ot' ± yt') > E(St), or alternatively Ft – S0 ≠ (ot' ± yt'),

then either: (i) incentive exists for arbitrageurs’ to enforce Ft = E(St); (ii) there is an unaccounted factor(s)

which should be incorporated into the model; and/or (iii) equilibrium cannot be determined from inherited

properties of individual behavior—ergo, there may be more than one price vector (i.e., multiple equilibria).

That’s why for practitioners applicability of carrying charge parity is largely dependent on whether

rational expectations is presumed to accurately reflect how the real world works, in which case the model is

ineffective because of circular reasoning;42 or whether markets are imperfect and rational expectations is a

deficient assumption, in which case there are real world opportunities to arbitrage for carrying charge parity.

The remainder of this paper is predicated on the latter conviction. We now reintroduce ±εt' into

proposition Ft = S0 + (ot' ± yt' ± εt') ≠ E(St) to indicate the existence of arbitrage opportunities.

42 “Fortunately, there is a simpler explanation – the model was wrong. Of course, all models are wrong. The onlymodel that is not wrong is reality and reality is not, by definition, a model.” From: Andrew G. Haldane, “Why BanksFailed the Stress Test,” Executive Director of Financial Stability, Bank of England; the basis for a speech given atthe Marcus-Evans Conference on Stress-Testing, February 9-10, 2009.

Page 15 of 51

Equilibrium Arbitrage Pressures

The problem facing arbitrageurs43 seeking to effect carrying charge parity is determining whether

t' = 0 and the fundamentals involving ot' and/or yt' have shifted; or t' < 0 or t' > 0 and there exists an

arbitrage opportunity. Since relationships between S0, Ft, E(St), ot', and yt' are recursive, in order to discover

if the market is mispriced, an arbitrageur must rely on real world observation in estimating exogenous

variables such as ot'. Conversely, the issue facing speculators with respect to speculative strategies is estimating

whether the market’s current implied cost-of-carry is accurate, which facilitates interpolation of E(St); or

estimating whether the market’s implied cost-of-carry is inaccurate and there exists a speculative opportunity.

In keeping with definitions established above, positive carry and negative carry shall reference the

term structure of the future price curve, whereas backwardation and contango shall reference the relation

between futures or forward prices and the expected future spot price. In this way, the seeming contradiction

between normal backwardation and theory of storage is reconciled, and semantics are clarified.

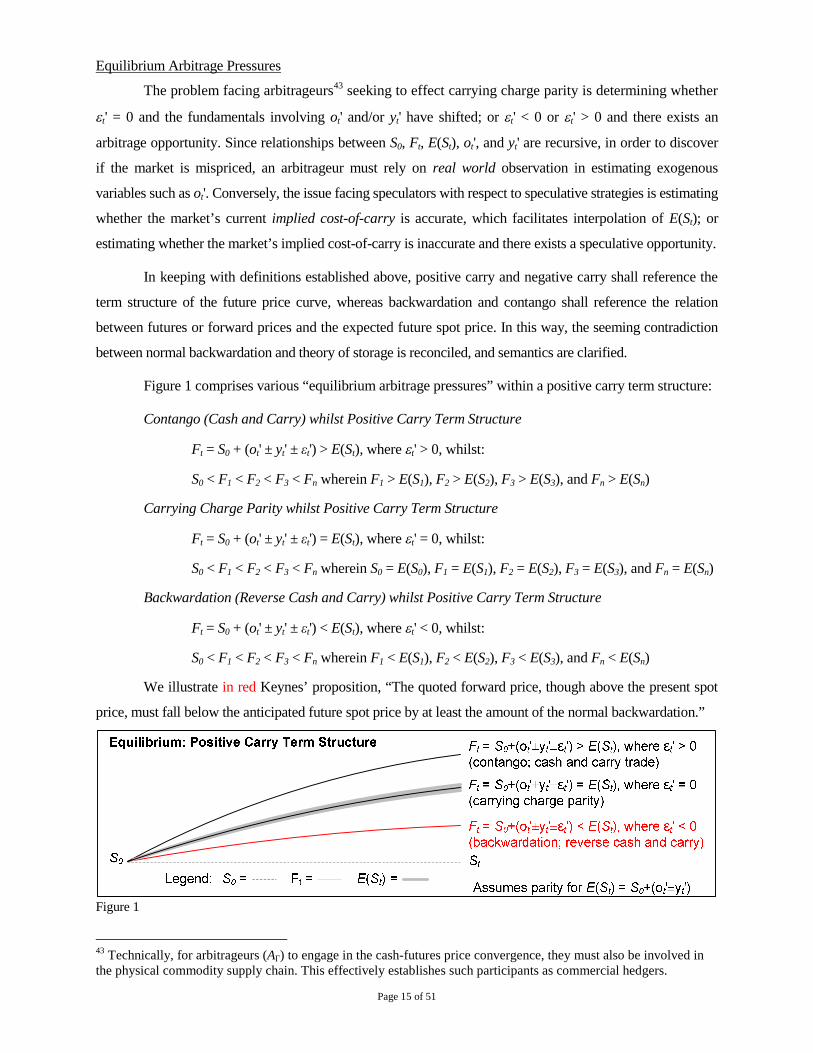

Figure 1 comprises various “equilibrium arbitrage pressures” within a positive carry term structure:

Contango (Cash and Carry) whilst Positive Carry Term Structure

Ft = S0 + (ot' ± yt' ± εt') > E(St), where t' > 0, whilst:

S0 < F1 < F2 < F3 < Fn wherein F1 > E(S1), F2 > E(S2), F3 > E(S3), and Fn > E(Sn)

Carrying Charge Parity whilst Positive Carry Term Structure

Ft = S0 + (ot' ± yt' ± εt') = E(St), where t' = 0, whilst:

S0 < F1 < F2 < F3 < Fn wherein S0 = E(S0), F1 = E(S1), F2 = E(S2), F3 = E(S3), and Fn = E(Sn)

Backwardation (Reverse Cash and Carry) whilst Positive Carry Term Structure

Ft = S0 + (ot' ± yt' ± εt') < E(St), where t' < 0, whilst:

S0 < F1 < F2 < F3 < Fn wherein F1 < E(S1), F2 < E(S2), F3 < E(S3), and Fn < E(Sn)

We illustrate in red Keynes’ proposition, “The quoted forward price, though above the present spot

price, must fall below the anticipated future spot price by at least the amount of the normal backwardation.”

Figure 1

43 Technically, for arbitrageurs (AΓ) to engage in the cash-futures price convergence, they must also be involved inthe physical commodity supply chain. This effectively establishes such participants as commercial hedgers.

Page 16 of 51

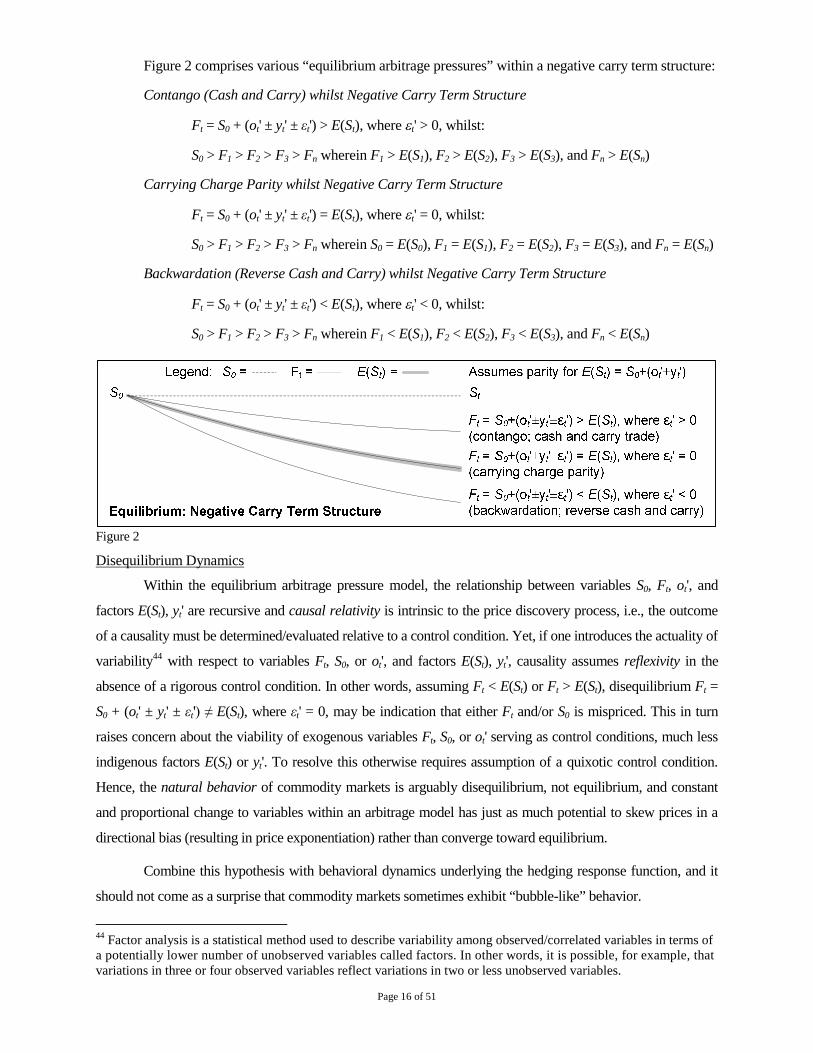

Figure 2 comprises various “equilibrium arbitrage pressures” within a negative carry term structure:

Contango (Cash and Carry) whilst Negative Carry Term Structure

Ft = S0 + (ot' ± yt' ± εt') > E(St), where t' > 0, whilst:

S0 > F1 > F2 > F3 > Fn wherein F1 > E(S1), F2 > E(S2), F3 > E(S3), and Fn > E(Sn)

Carrying Charge Parity whilst Negative Carry Term Structure

Ft = S0 + (ot' ± yt' ± εt') = E(St), where t' = 0, whilst:

S0 > F1 > F2 > F3 > Fn wherein S0 = E(S0), F1 = E(S1), F2 = E(S2), F3 = E(S3), and Fn = E(Sn)

Backwardation (Reverse Cash and Carry) whilst Negative Carry Term Structure

Ft = S0 + (ot' ± yt' ± εt') < E(St), where t' < 0, whilst:

S0 > F1 > F2 > F3 > Fn wherein F1 < E(S1), F2 < E(S2), F3 < E(S3), and Fn < E(Sn)

Figure 2

Disequilibrium Dynamics

Within the equilibrium arbitrage pressure model, the relationship between variables S0, Ft, ot', and

factors E(St), yt' are recursive and causal relativity is intrinsic to the price discovery process, i.e., the outcome

of a causality must be determined/evaluated relative to a control condition. Yet, if one introduces the actuality of

variability44 with respect to variables Ft, S0, or ot', and factors E(St), yt', causality assumes reflexivity in the

absence of a rigorous control condition. In other words, assuming Ft < E(St) or Ft > E(St), disequilibrium Ft =

S0 + (ot' ± yt' ± εt') ≠ E(St), where εt' = 0, may be indication that either Ft and/or S0 is mispriced. This in turn

raises concern about the viability of exogenous variables Ft, S0, or ot' serving as control conditions, much less

indigenous factors E(St) or yt'. To resolve this otherwise requires assumption of a quixotic control condition.

Hence, the natural behavior of commodity markets is arguably disequilibrium, not equilibrium, and constant

and proportional change to variables within an arbitrage model has just as much potential to skew prices in a

directional bias (resulting in price exponentiation) rather than converge toward equilibrium.

Combine this hypothesis with behavioral dynamics underlying the hedging response function, and it

should not come as a surprise that commodity markets sometimes exhibit “bubble-like” behavior.

44 Factor analysis is a statistical method used to describe variability among observed/correlated variables in terms ofa potentially lower number of unobserved variables called factors. In other words, it is possible, for example, thatvariations in three or four observed variables reflect variations in two or less unobserved variables.

Page 17 of 51

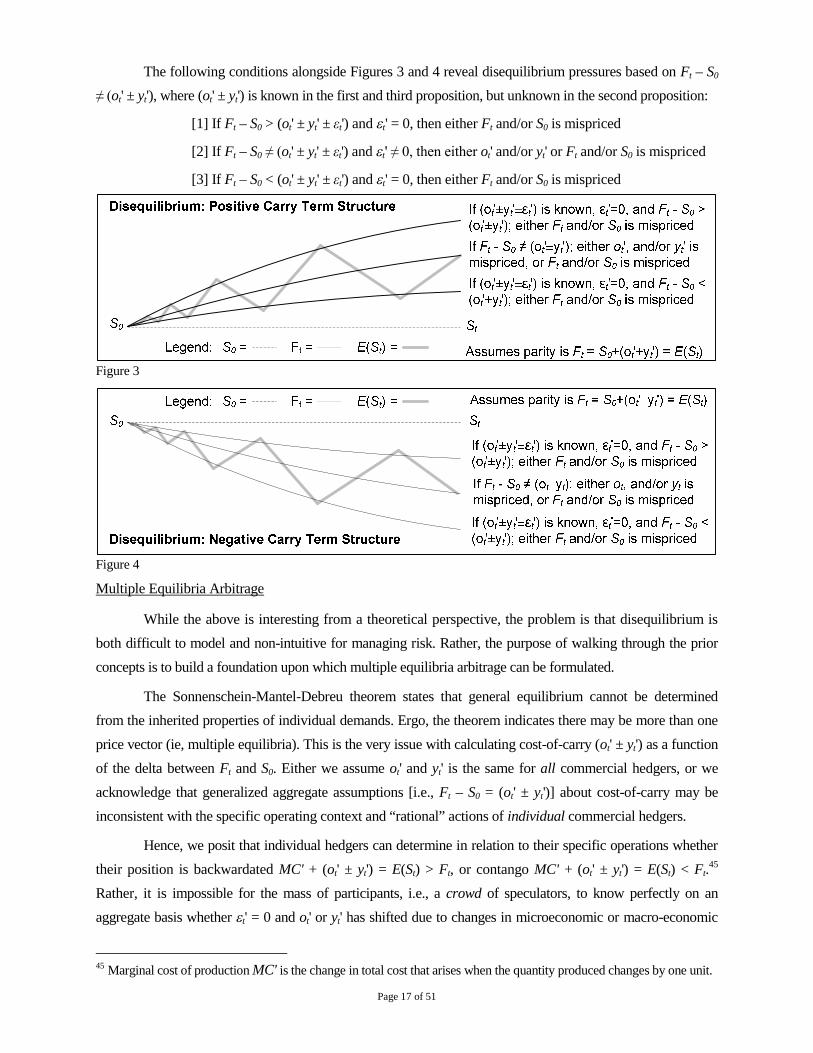

The following conditions alongside Figures 3 and 4 reveal disequilibrium pressures based on Ft – S0

≠ (ot' ± yt'), where (ot' ± yt') is known in the first and third proposition, but unknown in the second proposition:

[1] If Ft – S0 > (ot' ± yt' ± εt') and t' = 0, then either Ft and/or S0 is mispriced

[2] If Ft – S0 ≠ (ot' ± yt' ± εt') and t' ≠ 0, then either ot' and/or yt' or Ft and/or S0 is mispriced

[3] If Ft – S0 < (ot' ± yt' ± εt') and t' = 0, then either Ft and/or S0 is mispriced

Figure 3

Figure 4

Multiple Equilibria Arbitrage

While the above is interesting from a theoretical perspective, the problem is that disequilibrium is

both difficult to model and non-intuitive for managing risk. Rather, the purpose of walking through the prior

concepts is to build a foundation upon which multiple equilibria arbitrage can be formulated.

The Sonnenschein-Mantel-Debreu theorem states that general equilibrium cannot be determined

from the inherited properties of individual demands. Ergo, the theorem indicates there may be more than one

price vector (ie, multiple equilibria). This is the very issue with calculating cost-of-carry (ot' ± yt') as a function

of the delta between Ft and S0. Either we assume ot' and yt' is the same for all commercial hedgers, or we

acknowledge that generalized aggregate assumptions [i.e., Ft – S0 = (ot' ± yt')] about cost-of-carry may be

inconsistent with the specific operating context and “rational” actions of individual commercial hedgers.

Hence, we posit that individual hedgers can determine in relation to their specific operations whether

their position is backwardated MC' + (ot' ± yt') = E(St) > Ft, or contango MC' + (ot' ± yt') = E(St) < Ft.45

Rather, it is impossible for the mass of participants, i.e., a crowd of speculators, to know perfectly on an

aggregate basis whether t' = 0 and ot' or yt' has shifted due to changes in microeconomic or macro-economic

45 Marginal cost of production MC' is the change in total cost that arises when the quantity produced changes by one unit.

Page 18 of 51

influences, or whether t' < 0 or t' > 0 and an arbitrage opportunity exists. Thus, the Sonnenschein-Mantel-

Debreu theorem, involving multiple equilibria and Pareto efficiency, corroborates that at any point in time

market conditions may reflect pricing that provide arbitrage opportunities Ft = S0 + (ot' ± yt' ± εt') ≠ E(St).

Further, contrary hedging responses by individual bona fide hedgers to aggregate market pricing may reflect

perfectly “rational” responses given an individual hedger’s specific position and operating context.

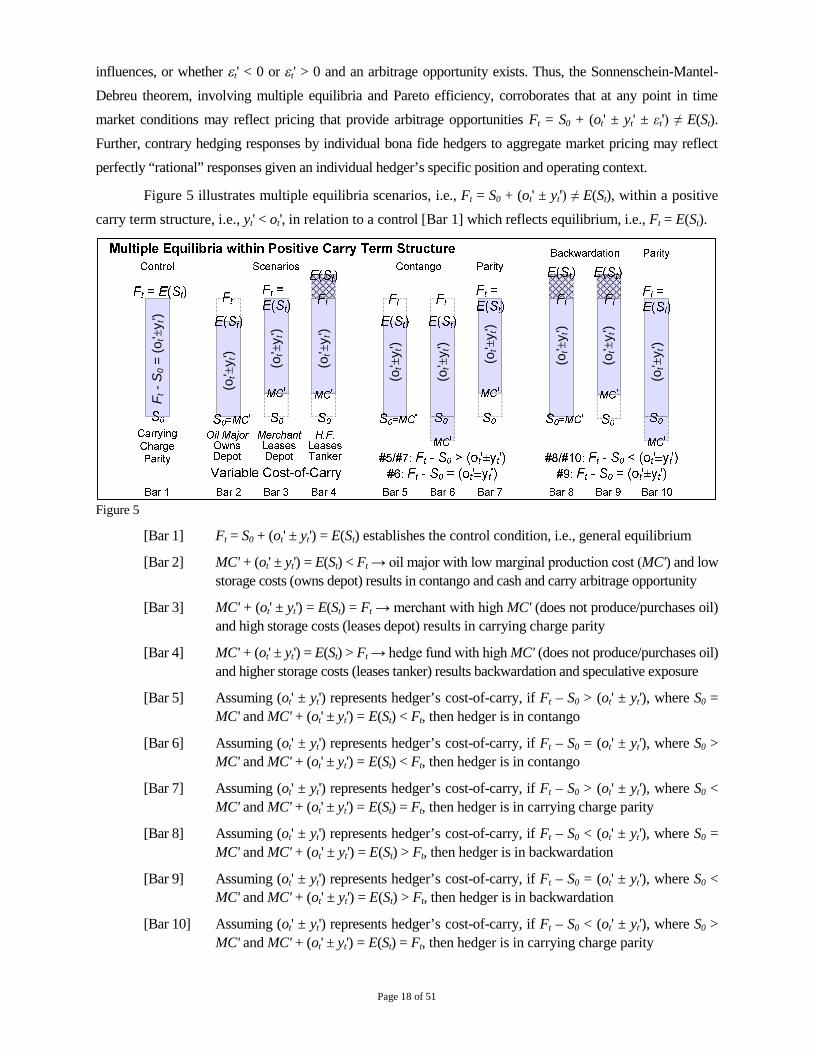

Figure 5 illustrates multiple equilibria scenarios, i.e., Ft = S0 + (ot' ± yt') ≠ E(St), within a positive

carry term structure, i.e., yt' < ot', in relation to a control [Bar 1] which reflects equilibrium, i.e., Ft = E(St).

Ft-

S0

=(o

t'±y

t')

(ot'±

yt')

(ot'±

y t')

(ot'±

y t')

(ot'±

yt')

(ot'±

yt')

(ot'±

y t')

(ot'±

y t')

(ot'±

y t')

(ot'±

y t')

Figure 5

[Bar 1] Ft = S0 + (ot' ± yt') = E(St) establishes the control condition, i.e., general equilibrium

[Bar 2] MC' + (ot' ± yt') = E(St) < Ft → oil major with low marginal production cost (MC') and low

storage costs (owns depot) results in contango and cash and carry arbitrage opportunity

[Bar 3] MC' + (ot' ± yt') = E(St) = Ft → merchant with high MC' (does not produce/purchases oil)

and high storage costs (leases depot) results in carrying charge parity

[Bar 4] MC' + (ot' ± yt') = E(St) > Ft → hedge fund with high MC' (does not produce/purchases oil)

and higher storage costs (leases tanker) results backwardation and speculative exposure

[Bar 5] Assuming (ot' ± yt') represents hedger’s cost-of-carry, if Ft – S0 > (ot' ± yt'), where S0 =

MC' and MC' + (ot' ± yt') = E(St) < Ft, then hedger is in contango

[Bar 6] Assuming (ot' ± yt') represents hedger’s cost-of-carry, if Ft – S0 = (ot' ± yt'), where S0 >

MC' and MC' + (ot' ± yt') = E(St) < Ft, then hedger is in contango

[Bar 7] Assuming (ot' ± yt') represents hedger’s cost-of-carry, if Ft – S0 > (ot' ± yt'), where S0 <

MC' and MC' + (ot' ± yt') = E(St) = Ft, then hedger is in carrying charge parity

[Bar 8] Assuming (ot' ± yt') represents hedger’s cost-of-carry, if Ft – S0 < (ot' ± yt'), where S0 =

MC' and MC' + (ot' ± yt') = E(St) > Ft, then hedger is in backwardation

[Bar 9] Assuming (ot' ± yt') represents hedger’s cost-of-carry, if Ft – S0 = (ot' ± yt'), where S0 <

MC' and MC' + (ot' ± yt') = E(St) > Ft, then hedger is in backwardation

[Bar 10] Assuming (ot' ± yt') represents hedger’s cost-of-carry, if Ft – S0 < (ot' ± yt'), where S0 >

MC' and MC' + (ot' ± yt') = E(St) = Ft, then hedger is in carrying charge parity

Page 19 of 51

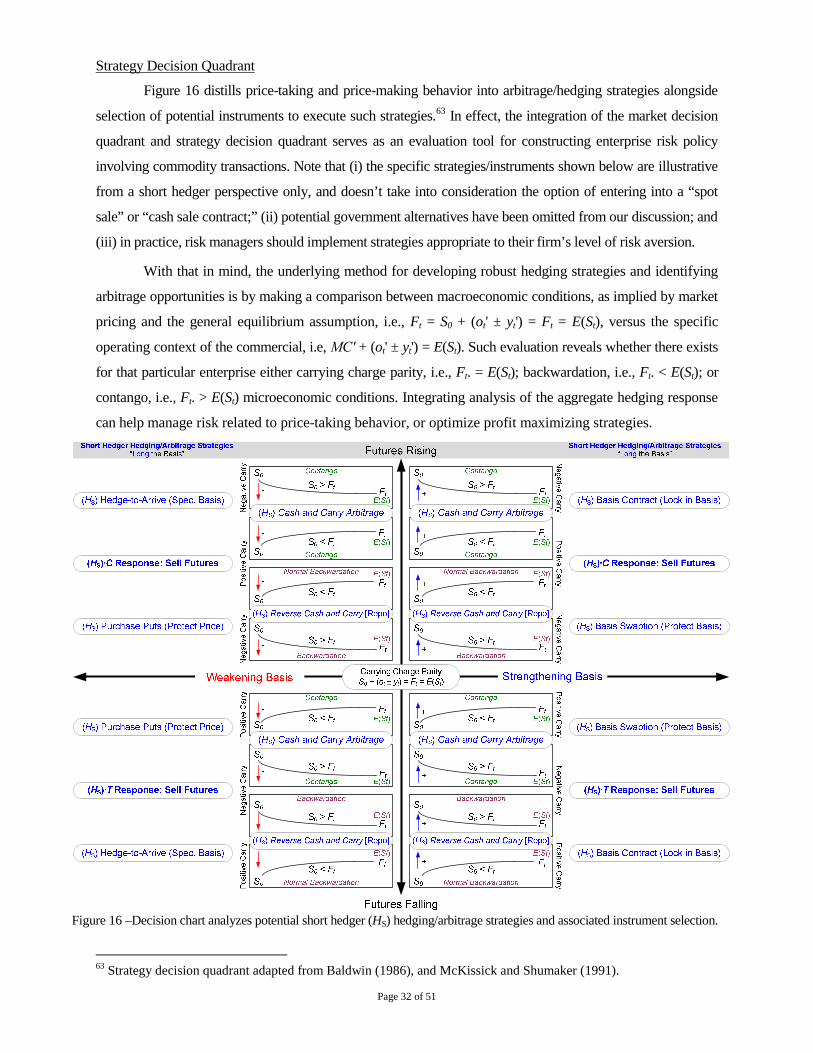

4. Framework for Basis Trading

The body of theory presented above provides the underpinnings for developing multiple equilibria

multi-factor propositions.46 Propositions do not operate in a vacuum, however; rather they function within

boundary conditions. In combination, conditions, propositions and constraints47 provide context for managing

individual microeconomic basis risk exposure, and helps optimize basis trading strategies (e.g., position,

pricing, position entry/exit, marketing alternatives). This section adds basis concepts to our unifying theory.

Notation and Definitions

Let (HS) represent short hedgers (e.g., producers); let (HL) represent long hedgers (e.g., consumers);

let (ΑΔ) represent speculators; and let (AΓ) represent arbitrageurs. Additionally, let the symbol designate

the purchase of an asset or holding a long position by a participant; and let the symbol designate the

sale of an asset or holding a short position by a participant. [e.g., (ΑΔ)· signifies that speculators on a net

aggregate basis “went long” by purchasing the underlying asset or related futures.]

We also add the following set of notations in order to model basis trading. Let Bt represent basis

wherein the futures price is subtracted from the spot price, i.e., Bt = S0 – Ft. In addition, let (–) represent

basis under, i.e., Bt·(–); let (+) represent basis over, i.e., Bt·(+); let represent strengthening basis, i.e., Bt·;

and let represent weakening basis, i.e., Bt·. These concepts are explained below.

Increasing instrument prices [e.g., S0, S1, Ft, etc.] are represented by the symbol (↑), including

parentheses; decreasing instrument prices are represented by the symbol (↓), including parentheses; and

sideway instrument prices are represented by the symbol (→), including parentheses [e.g., S0·(→)]. In

addition, let (↑↑), including parentheses, designate instrument prices that are rising faster; and let (↓↓),

including parentheses, designate instrument prices that are falling faster [e.g., S0·(↓↓)].

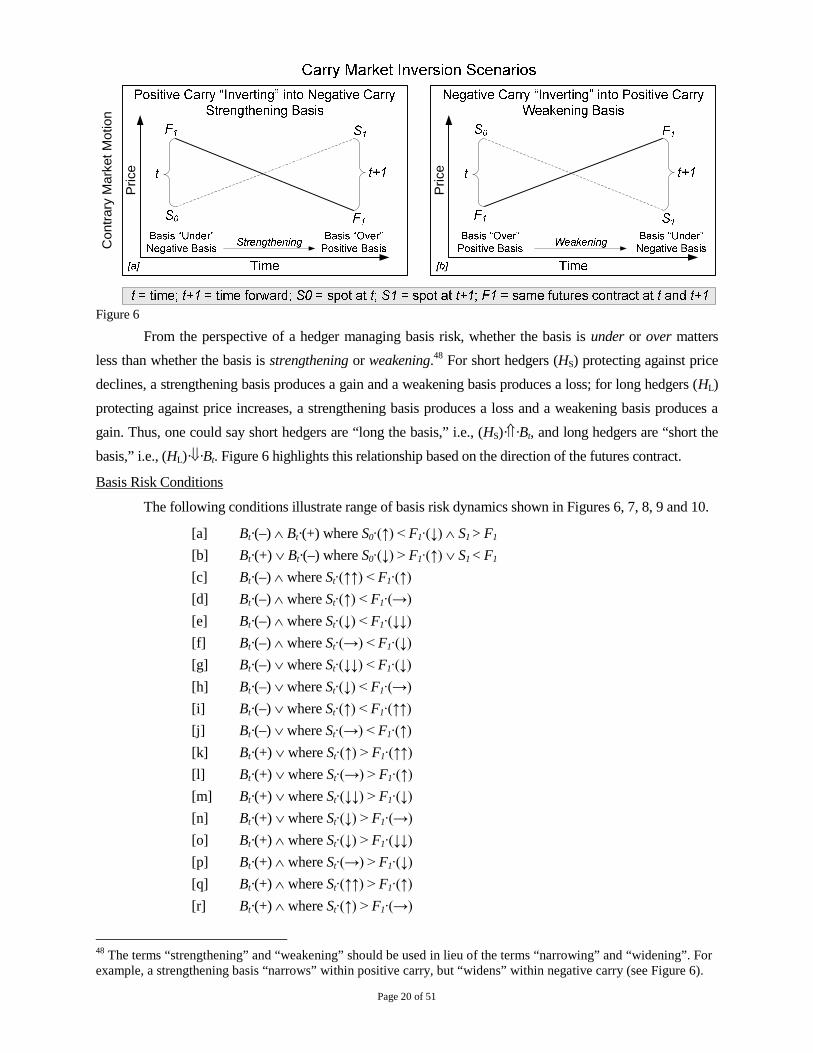

Principles of Basis Trading

“Basis” is defined as the difference between a specified local cash price and a futures or forward

price for a specified delivery period and location, i.e., S0 – Ft. Factors that influence basis include, but are

not limited to supply/demand, substitution, unequal borrowing/lending rates, warehousing (storage), insurance,

and transportation. Such aspects are investigated in the following section on Segmenting the Supply Chain.

In practice, basis Bt is conveyed in terms of a futures or forward contract spread “under” or “over”

the cash price S0, with basis under related to positive carry, and basis over related to negative carry. Figure 6

illustrates the inverse relationship between positive carry and negative basis, and negative carry and positive

basis. Basis occurs because supply/demand factors in local cash markets are different from the futures market.

46 Single-factor models attempts to account for contingencies like changes in interest rate or inflation, and are basedon equations in which one economic factor explains market phenomena and/or equilibrium asset prices. Multi-factormodels employ multiple factors in its computations to explain market phenomena and/or equilibrium asset prices.

47 “Condition” is defined as a set of boundaries that is used to simulate a large system; whereas “constraint” is adiscrete condition that a solution requires in order to satisfy an optimization problem.

Page 20 of 51

Price

Price

Contr

ary

Mark

etM

otio

n

Figure 6

From the perspective of a hedger managing basis risk, whether the basis is under or over matters

less than whether the basis is strengthening or weakening.48 For short hedgers (HS) protecting against price

declines, a strengthening basis produces a gain and a weakening basis produces a loss; for long hedgers (HL)

protecting against price increases, a strengthening basis produces a loss and a weakening basis produces a

gain. Thus, one could say short hedgers are “long the basis,” i.e., (HS)··Bt, and long hedgers are “short the

basis,” i.e., (HL)··Bt. Figure 6 highlights this relationship based on the direction of the futures contract.

Basis Risk Conditions

The following conditions illustrate range of basis risk dynamics shown in Figures 6, 7, 8, 9 and 10.

[a] Bt·(–) Bt·(+) where S0·(↑) < F1·(↓) S1 > F1

[b] Bt·(+) Bt·(–) where S0·(↓) > F1·(↑) S1 < F1

[c] Bt·(–) where St·(↑↑) < F1·(↑)

[d] Bt·(–) where St·(↑) < F1·(→)

[e] Bt·(–) where St·(↓) < F1·(↓↓)

[f] Bt·(–) where St·(→) < F1·(↓)

[g] Bt·(–) where St·(↓↓) < F1·(↓)

[h] Bt·(–) where St·(↓) < F1·(→)

[i] Bt·(–) where St·(↑) < F1·(↑↑)

[j] Bt·(–) where St·(→) < F1·(↑)

[k] Bt·(+) where St·(↑) > F1·(↑↑)

[l] Bt·(+) where St·(→) > F1·(↑)

[m] Bt·(+) where St·(↓↓) > F1·(↓)

[n] Bt·(+) where St·(↓) > F1·(→)

[o] Bt·(+) where St·(↓) > F1·(↓↓)

[p] Bt·(+) where St·(→) > F1·(↓)

[q] Bt·(+) where St·(↑↑) > F1·(↑)

[r] Bt·(+) where St·(↑) > F1·(→)

48 The terms “strengthening” and “weakening” should be used in lieu of the terms “narrowing” and “widening”. Forexample, a strengthening basis “narrows” within positive carry, but “widens” within negative carry (see Figure 6).

Page 21 of 51

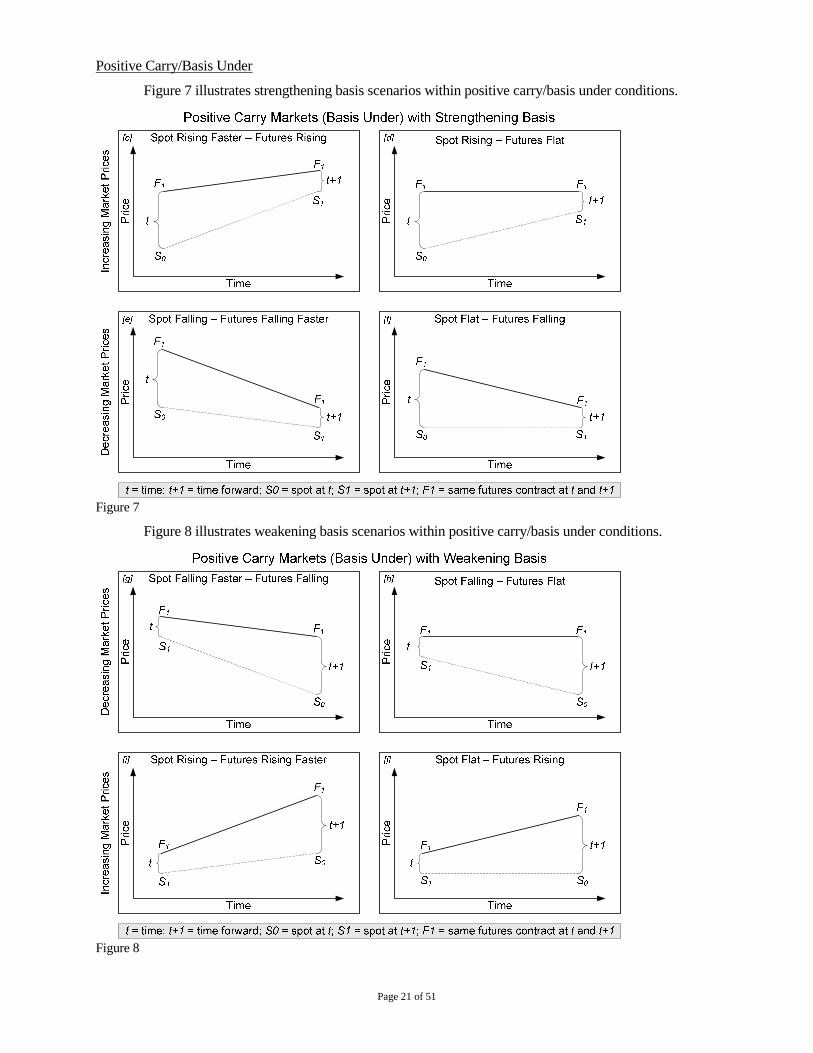

Positive Carry/Basis Under

Figure 7 illustrates strengthening basis scenarios within positive carry/basis under conditions.

Figure 7

Figure 8 illustrates weakening basis scenarios within positive carry/basis under conditions.

Figure 8

Page 22 of 51

Negative Carry/Basis Over

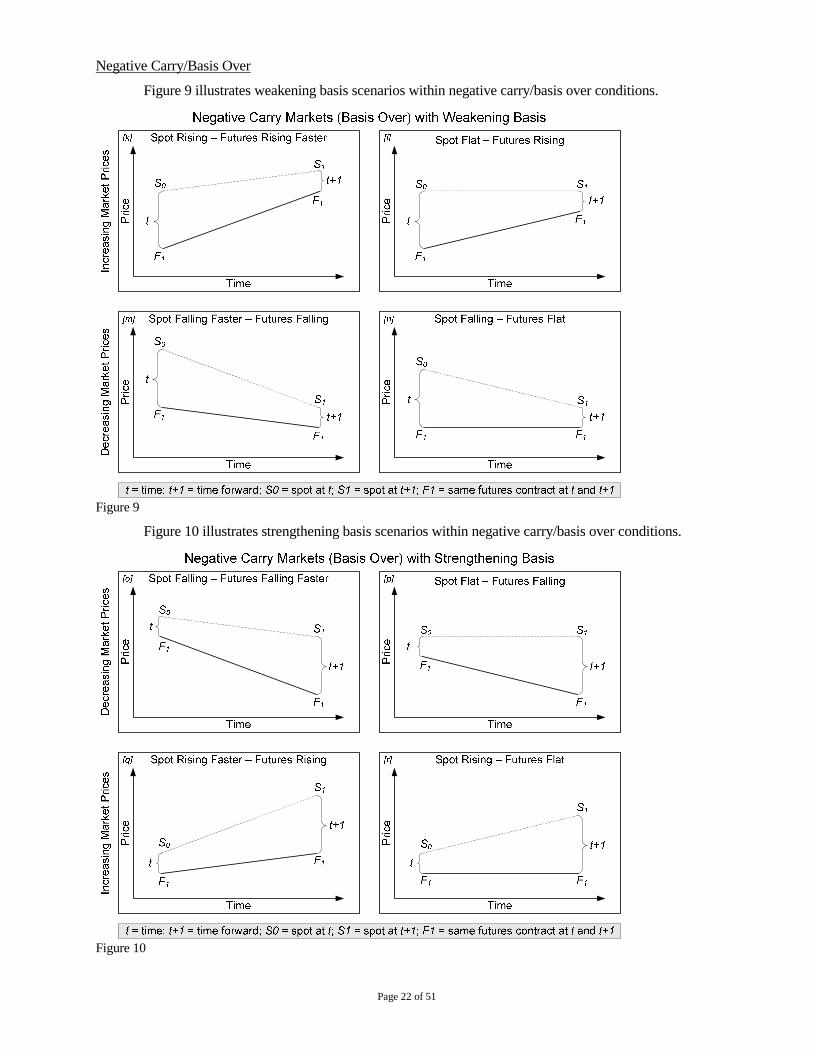

Figure 9 illustrates weakening basis scenarios within negative carry/basis over conditions.

Figure 9

Figure 10 illustrates strengthening basis scenarios within negative carry/basis over conditions.

Figure 10

Page 23 of 51

Basis Trading Strategies

Hedgers can make better choices about when to market, where to market, and how to lock in prices

by following basis closely. Basis for storable products is influenced by two things: (i) the cost of getting the

commodity from point of production to point of delivery for domestic use or export/international use; and (ii)

local/regional supply-demand for a commodity as compared to global macroeconomic dynamics.

The first step in to compare the basis currently offered for the expected time of delivery with the

basis historically offered around such delivery time. As an example, factors that account for basis variation in

the grain markets include charges for elevation, cleaning, storage, and inspection (together known as elevator

tariffs). Interest rates also influence a farmer's net farm gate price, with storage length being a related factor—

the longer grain is stored, the higher the interest and storage charges will be.49

Consumers such as processors also use basis to attract commodities when they require it. Buyers

who, on any particular day, offer a higher local cash price than their competitors are in effect offering a

stronger basis than their competitors. As an example, a merchandiser with an export sale to deliver canola in

two months will encourage producer deliveries to its elevator system by strengthening the basis. The higher

cash price relative to the futures price will attract deliveries to that particular dealer. Conversely, an elevator

with excess grain in-store will discourage farm deliveries by weakening the basis. The lower cash price

signals producers to hold back deliveries to that particular warehouse, or make delivery to other elevators.

As basis is a signal of market forces, it serves as an important gauge as to whether a producer

should: (i) store and maintain title to the commodity (e.g., “on-farm storage” or “lease storage);” (ii) “spot

sale” at the nearby market price; (iii) contract to sell the commodity at the nearby bid, i.e., “cash sale

contract;” (iv) “forward contract” whereby terms are agreed upon in advance by the buyer and seller; (v)

enter into a “futures contract” in which the terms are standardized by the exchange’s contract specifications;

(vi) use a “fixed basis contract” that fixes the quantity, delivery period and basis, but leaves futures price

risk unhedged to be established at a later date; (vii) use a “hedge-to-arrive” (HTA) contract which fixes the

quantity, delivery period and futures price, but leaves the basis unhedged to be established at a later date;50

(viii) enter into a “minimum price contract” which in effect is a fixed basis contract with an embedded

option to allow upside participation; or (ix) enter into a contract which facilitates movement of a commodity

without establishing either a basis or futures price, variously known as “delayed price contract,” “no price

established,” “price later,” or “deferred price contract”.

For added flexibility, commercial hedgers can use various option strategies (e.g., calls and/or puts) to

hedge price risk, and then either maintain title to the commodity, or enter into a contract (e.g., basis contract).

49 Charlie Pearson, “Basis – How Cash Grain Prices are Established,” Alberta Agriculture and Rural Development,Provincial Crops Market Analyst. Published July 21, 2006; reviewed and revised on August 4, 2011.

50 Hedge-to-arrive contracts range from relatively simple, low-risk non-rolling versions in which basis risk is themain area of risk exposure, to much more complex types that allow producers to roll (change delivery dates) andpermit the next year’s crop to be priced initially with old-crop futures contracts.

Page 24 of 51

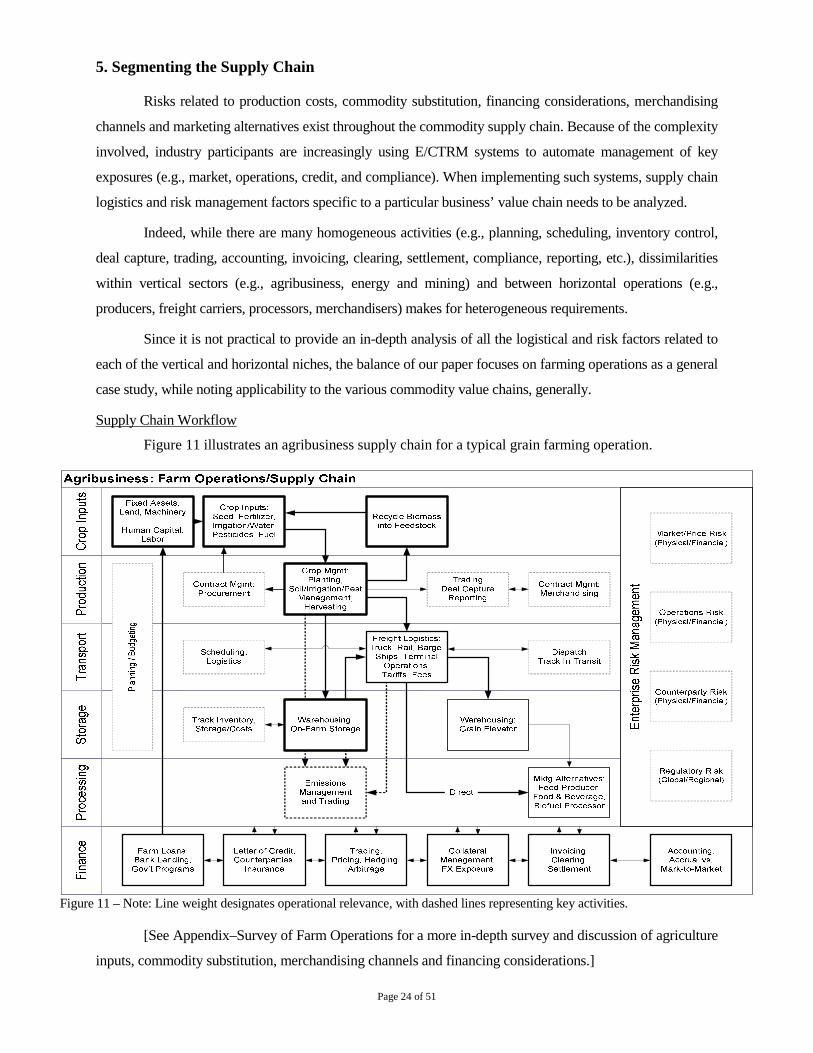

5. Segmenting the Supply Chain

Risks related to production costs, commodity substitution, financing considerations, merchandising

channels and marketing alternatives exist throughout the commodity supply chain. Because of the complexity

involved, industry participants are increasingly using E/CTRM systems to automate management of key

exposures (e.g., market, operations, credit, and compliance). When implementing such systems, supply chain

logistics and risk management factors specific to a particular business’ value chain needs to be analyzed.

Indeed, while there are many homogeneous activities (e.g., planning, scheduling, inventory control,

deal capture, trading, accounting, invoicing, clearing, settlement, compliance, reporting, etc.), dissimilarities

within vertical sectors (e.g., agribusiness, energy and mining) and between horizontal operations (e.g.,

producers, freight carriers, processors, merchandisers) makes for heterogeneous requirements.

Since it is not practical to provide an in-depth analysis of all the logistical and risk factors related to

each of the vertical and horizontal niches, the balance of our paper focuses on farming operations as a general

case study, while noting applicability to the various commodity value chains, generally.

Supply Chain Workflow

Figure 11 illustrates an agribusiness supply chain for a typical grain farming operation.

Figure 11 – Note: Line weight designates operational relevance, with dashed lines representing key activities.

[See Appendix–Survey of Farm Operations for a more in-depth survey and discussion of agriculture

inputs, commodity substitution, merchandising channels and financing considerations.]

Page 25 of 51

Profit Maximization

Profit maximization is the process by which a firm determines the price and output level that returns

the greatest profit. There are two methods for determining maximization: (i) total revenue less total cost

which focuses on minimizing this difference; and (ii) marginal revenue less marginal cost, specifically

when marginal cost equals marginal revenue indicating that total profit has reached maximum point.

Production Costs

Marginal cost at each level of production includes any additional costs required to produce the next

unit. In practice, marginal costs include all “short run” costs that vary with the level of production whereas

“long run” costs are considered fixed costs. If the cost function is differentiated d,51 the marginal cost MC′ is

the cost of the next unit produced, where Q represents the production quantity, VC represents variable costs,

FC represents fixed costs, and TC represents total costs, i.e., MC′ = dTC / dQ = d(FC + VC) / dQ. Since

fixed costs do not vary with production quantity, it drops out of the equation when it is differentiated, i.e.,

d(FC + VC) / dQ = dVC / dQ.52 On the other hand, average total cost ATC, which is the total cost divided by

the number of units produced, includes fixed costs, i.e., ATC = (FC + VC) / Q.

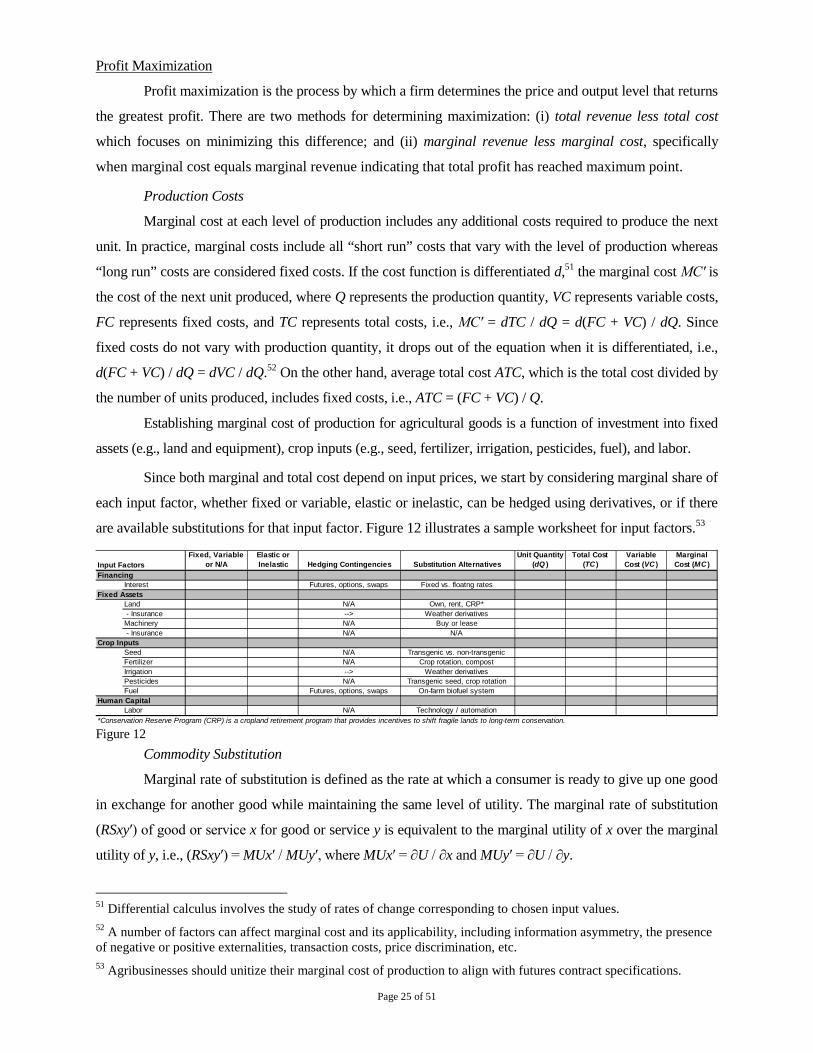

Establishing marginal cost of production for agricultural goods is a function of investment into fixed

assets (e.g., land and equipment), crop inputs (e.g., seed, fertilizer, irrigation, pesticides, fuel), and labor.

Since both marginal and total cost depend on input prices, we start by considering marginal share of

each input factor, whether fixed or variable, elastic or inelastic, can be hedged using derivatives, or if there

are available substitutions for that input factor. Figure 12 illustrates a sample worksheet for input factors.53

Input Factors

Fixed, Variable

or N/A

Elastic or

Inelastic Hedging Contingencies Substitution Alternatives

Unit Quantity

(dQ )

Total Cost

(TC )

Variable

Cost (VC )

Marginal

Cost (MC )

Financing

Interest Futures, options, swaps Fixed vs. floatng rates

Fixed Assets

Land N/A Own, rent, CRP*

- Insurance --> Weather derivatives

Machinery N/A Buy or lease

- Insurance N/A N/A

Crop Inputs

Seed N/A Transgenic vs. non-transgenic

Fertilizer N/A Crop rotation, compost

Irrigation --> Weather derivatives

Pesticides N/A Transgenic seed, crop rotation

Fuel Futures, options, swaps On-farm biofuel system

Human Capital

Labor N/A Technology / automation

*Conservation Reserve Program (CRP) is a cropland retirement program that provides incentives to shift fragile lands to long-term conservation.

Figure 12

Commodity Substitution

Marginal rate of substitution is defined as the rate at which a consumer is ready to give up one good

in exchange for another good while maintaining the same level of utility. The marginal rate of substitution

(RSxy′) of good or service x for good or service y is equivalent to the marginal utility of x over the marginal

utility of y, i.e., (RSxy′) = MUx′ / MUy′, where MUx′ = ∂U / ∂x and MUy′ = ∂U / ∂y.

51 Differential calculus involves the study of rates of change corresponding to chosen input values.

52 A number of factors can affect marginal cost and its applicability, including information asymmetry, the presenceof negative or positive externalities, transaction costs, price discrimination, etc.

53 Agribusinesses should unitize their marginal cost of production to align with futures contract specifications.

Page 26 of 51

Financing Considerations

Capital budgeting is the process used to determine major capital investment or expenditures. There

are a variety of methods used to measure incremental cash flows, including net present value and modified

internal rate of return. The net present value (NPV) method measures excess or shortfall of cash flows in

present value terms. Given the period, cash flow (t, Ct) pairs, where n is a positive integer, and N is the total

number of periods, NPV is given by ∑ Ct / (1+r)t, where t is the time of the cash flow; r is the rate of return

that could be earned on an investment with similar risk; and Ct is net cash flow (i.e., the amount of inflow

minus outflow) at time t. Using the secant method, the internal rate of return (IRR) r is given by rn+1 = rn –

NPVn ((rn – rn–1) / (NPVn – NPVn–1)), where rn is considered the nth approximation of the IRR.

Since IRR does not consider the cost of capital, it should not be used to compare projects of different

duration. Modified Internal Rate of Return (MIRR) does consider the cost of capital and provides a better

indication of a project’s efficiency in contributing to the firm’s discounted cash flow. MIRR is calculated as

MIRR = n√(FV / –PV) – 1, where n is the number of equal periods at the end of which the cash flows occur

(not the number of cash flows), PV is present value (at the beginning of the first period), and FV is future value

(at the end of the last period). Like the internal rate of return, the modified internal rate of return cannot be

validly used to rank-order projects of different sizes, however, there exist variants of the modified internal rate

of return which can be used for such comparisons [Shull (1992) and Hajdasinski (1995)].54

Let’s consider a key issue facing farms and grain companies that use futures to hedge their physical

inventory is how to cope with margin calls from short futures positions. Since futures are marked-to-market

daily whereas physical inventory does not produce a cash event until sold, volatile upside markets can force

short hedgers to draw down banking credit lines in order. This credit line drawdown had several

implications: (i) it results in less credit available to meet working capital needs; (ii) it results in substantial

interest costs; and (iii) if a commercial draws down their credit they may be forced to liquidate their futures

positions at large losses which can cause major financial issues and even bankruptcy.

In response, the agribusiness industry has instituted the use of purchase and sales agreements (i.e.,

repurchase agreements), whereby a counterparty offers to buy physical grain from an elevator, for example

and swap the futures with the elevator for a designated amount of time. At the same time, the elevator agrees

to repurchase the commodity from the counterparty at a pre-specified date in the future, and at a fixed basis

to the futures price representing the cost of money. During this transaction the commodity remains in

storage and only the warehouse receipts exchange hands while the counterparty pays storage leasing costs

which is deducted from the repurchase price. Meanwhile, the warehouse receipts serve as collateral for the

counterparty, and cash infusion from the repurchase agreement to the hedger provides funds which can be

used as working capital or reinvestment in short-term notes. Thus, in addition to outgoing cash flows and

financing rates, farming operations may also earn investment income on cash reserves.

54 D. M. Shull, “Efficient capital project selection through a yield-based capital budgeting technique” The EngineeringEconomist 38(1), 1992, 1-18. M. Hajdasinski, “Remarks in the context of the case for the generalized net presentvalue formula” The Engineering Economist 40(2), 1995, 201-210.

Page 27 of 51

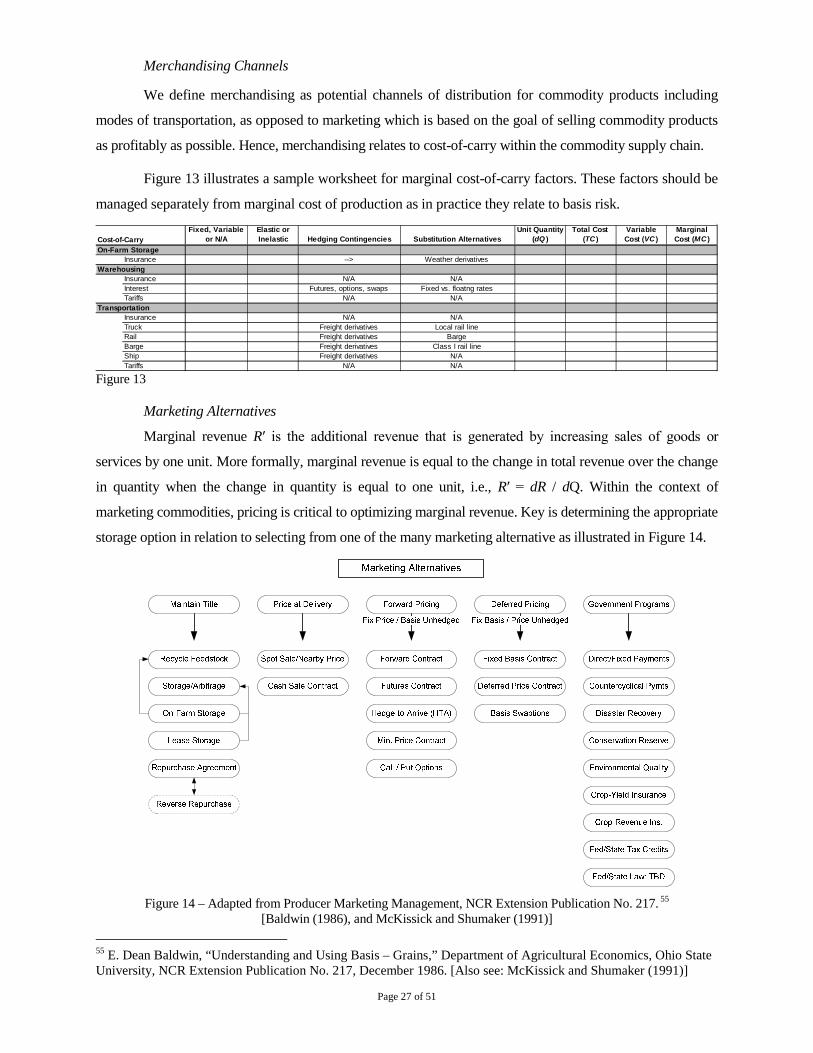

Merchandising Channels

We define merchandising as potential channels of distribution for commodity products including

modes of transportation, as opposed to marketing which is based on the goal of selling commodity products

as profitably as possible. Hence, merchandising relates to cost-of-carry within the commodity supply chain.

Figure 13 illustrates a sample worksheet for marginal cost-of-carry factors. These factors should be

managed separately from marginal cost of production as in practice they relate to basis risk.

Cost-of-Carry

Fixed, Variable

or N/A

Elastic or

Inelastic Hedging Contingencies Substitution Alternatives

Unit Quantity

(dQ )

Total Cost

(TC )

Variable

Cost (VC )

Marginal

Cost (MC )

On-Farm Storage