Hedge fund investors Long-only investors Take advantage of the upcoming LED market’s upside rally, as seasonally strong demand is to come in 2H10. Average over 50% of profit CAGR expected for LED makers Tight LED package supply will secure LED makers’ remarkable earnings growth until 2011 1 See the last page of this report for important disclosures Korea / Technology LED Industry LED demand growth to accelerate in 2H10 We foresee an LED market upside rally on seasonally strong demand to come in 2H10. The reasons are three-fold: 1) the persistent stra in on LED chip supplies should limit chip price decline; 2) domestic LED makers should show accelerating earnings growth on completed capex expansion alongside seasonally strong demand; and 3) likely robust high-end demand (e.g. 3D TVs) and increased LED TV penetration in China should drive global LED demand in 2H10. We believe LED companies still have sufficient upside if their earnings continue to meet expectations, even after outperforming the market to date. We see our Overweight rating on the sector as justifiable, given that LED makers’ average profit CAGR exceeds 50%. Our top picks for the sector are LG Innotek and Samsung Electro-Mechanics. » Strains on LED package supplies will continue into 2011 It will take about a year before ingot makers complete their capacity expansion currently underway. As such, although they will raise LED TV ingots’ portion to 50% of their total ingot output, LED supply will remain tight for the time being. We estimate demand for LED packages will be 14.4bn in 2010 but the supply forecast for 2010 (13.6bn units of LED packages) satisf ies only 95% of the demand foreca st. We expect supply (25.4bn units) will still not meet demand (25.5bn units) in 2011. » LED makers’ earnings rise rapidly on strong LED TV demand LED makers’ remarkable earnings growth of late is driven by strong demand for LED TVs. All key domestic LED makers except Seoul Semiconductor (Samsung LED, LG Innotek, and Lumens) recorded more than 80% sales contributions from their TV BLU divisions. All four companies invested a combined W1.4tn into expanding their TV BLU capex and are expected to record operating margins of over 10%. With global LED TV demand likely to soar 148%, from 37mn units in 2010 to 92mn units in 2011, we expect the LED players’ earnings uptrend to continue into 2011. » LED market drivers: 3D TVs a nd Chinese demand Since the start of the 2010 World Cup, 3D TVs have been drawing increasing attention in the market. Samsung Electronics is expected to post sales of 1m 3D TVs in August, while demand for 3D TVs is expected to reach 6m units, making up 16.2% of the global LED TV market in 2010. In addition, 3D TVs require 30% more LED chips than existing LED TVs, for high lamination and refresh rates. Coupled with 3D TV, Chinese demand for LED TVs will drive the global LED market. China is expected to constitute 20% of the global LED TV market in 3Q10, up significantly from 5% in 4Q09. Soon-Hak Lee, Korea Analyst +82 2 3774 1651 [email protected] Jubi Park, Korea Analyst +82 2 3774 1938 [email protected] Overweight 15 Jul 2010 Company Ticker Rating Price Target price Seoul Semiconductor 009150 BUY W149,000 W200,000 LG Innotek 011070 BUY W178,500 W230,000 Lumens 038060 BUY W12,450 W18,000 Hansol LCD 004710 BUY W57,800 W80,000 Note: Prices are in KRW; Price close as of (13/7/2010 close) Source for data: Bloomberg, companies, Mirae Asset Research 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 1Q10 2Q10E 3Q10E 4Q10E 1Q11E 2Q11E 3Q11E 4Q11E (mn unit) Dem a nd Su p pl y Stocks for action Supply and demand trend for LED TV LED operating margin trend by LED makers Supply and demand trend for LED TV (30) (20) (10) 0 10 20 30 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E (%) Samsung LED LG Innotek Seoul Semiconductor Lumens 0 10,000 20,000 30,000 40,000 50,000 60,000 4Q09 2Q10E 4Q10E 2Q11E 4Q11E 2Q12E 4Q12E (K units) 0 5 10 15 20 25 (%) Gl obal LED T V ( lhs) C hina (lhs) Porti on (rhs)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 1/20

Hedge fund investors Long-only investors

Take advantage of the upcoming LEDmarket’s upside rally, as seasonally

strong demand is to come in 2H10.

Average over 50% of profit CAGR

expected for LED makers

Tight LED package supply will secureLED makers’ remarkable earnings

growth until 2011

1

See the last page of this report for important disclosures

K o r e a / T e c h n o l o g y LED Industry

LED demand growth to

accelerate in 2H10We foresee an LED market upside rally on seasonally strongdemand to come in 2H10. The reasons are three-fold: 1) thepersistent strain on LED chip supplies should limit chip pricedecline; 2) domestic LED makers should show acceleratingearnings growth on completed capex expansion alongsideseasonally strong demand; and 3) likely robust high-enddemand (e.g. 3D TVs) and increased LED TV penetration inChina should drive global LED demand in 2H10. We believeLED companies still have sufficient upside if their earningscontinue to meet expectations, even after outperforming the

market to date. We see our Overweight rating on the sectoras justifiable, given that LED makers’ average profit CAGR exceeds 50%. Our top picks for the sector are LG Innotek and Samsung Electro-Mechanics.

» Strains on LED package supplies will continue into 2011

It will take about a year before ingot makers complete their capacity

expansion currently underway. As such, although they will raise LED TV

ingots’ portion to 50% of their total ingot output, LED supply will remain

tight for the time being. We estimate demand for LED packages will be

14.4bn in 2010 but the supply forecast for 2010 (13.6bn units of LED

packages) satisfies only 95% of the demand forecast. We expect supply

(25.4bn units) will still not meet demand (25.5bn units) in 2011.

» LED makers’ earnings rise rapidly on strong LED TV demandLED makers’ remarkable earnings growth of late is driven by strong demand

for LED TVs. All key domestic LED makers except Seoul Semiconductor

(Samsung LED, LG Innotek, and Lumens) recorded more than 80% sales

contributions from their TV BLU divisions. All four companies invested a

combined W1.4tn into expanding their TV BLU capex and are expected to

record operating margins of over 10%. With global LED TV demand likely to

soar 148%, from 37mn units in 2010 to 92mn units in 2011, we expect the

LED players’ earnings uptrend to continue into 2011.

» LED market drivers: 3D TVs and Chinese demand

Since the start of the 2010 World Cup, 3D TVs have been drawing

increasing attention in the market. Samsung Electronics is expected topost sales of 1m 3D TVs in August, while demand for 3D TVs is

expected to reach 6m units, making up 16.2% of the global LED TV

market in 2010. In addition, 3D TVs require 30% more LED chips than

existing LED TVs, for high lamination and refresh rates. Coupled with 3D

TV, Chinese demand for LED TVs will drive the global LED market.

China is expected to constitute 20% of the global LED TV market in

3Q10, up significantly from 5% in 4Q09.

Soon-Hak Lee, Korea Analyst

+82 2 3774 1651 [email protected]

Jubi Park, Korea Analyst

+82 2 3774 1938 [email protected]

Overweight15 Jul 2010

Company Ticker Rating PriceTarget

price

Seoul

Semiconductor 009150 BUY W149,000 W200,000

LG Innotek 011070 BUY W178,500 W230,000

Lumens 038060 BUY W12,450 W18,000

Hansol LCD 004710 BUY W57,800 W80,000

Note: Prices are in KRW; Price close as of (13/7/2010 close)

Source for data: Bloomberg, companies, Mirae Asset Research

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1Q10 2Q10E 3Q10E 4Q10E 1Q11E 2Q11E 3Q11E 4Q11E

(mn unit)

Demand Supply

Stocks for action

Supply and demand trend for LED TV

LED operating margin trend by LED makers

Supply and demand trend for LED TV

(30)

(20)

(10)

0

10

20

30

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E

(%)

Samsung LED LG Innotek Seoul Semiconductor Lumens

0

10,000

20,000

30,000

40,000

50,000

60,000

4Q09 2Q10E 4Q10E 2Q11E 4Q11E 2Q12E 4Q12E

(K units)

0

5

10

15

20

25

(%)

Globa l LED TV (lhs) China (lhs) Port ion (rhs)

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 2/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

2

C O N T E N T S

LED demand growth to accelerate in 2H10 ...................................................1 1. Executive Summary ...................................................................................3 2. LED players to maintain upbeat earnings on chip supply strain................4

Chip supply shortages for LED TV BLU to continue into 2011 4 LED makers’ earnings rising fast on strong LED TV demand 6

3. Key drivers in 2H10: 3D TVs and China......................................................8 Demand for over 20mn LED TVs expected in 2H10 8 3D TV market expansion to help increase demand for LED further 8 LED demand to be driven by wider penetration of LED TVs in China 9

COMPANY SECTION

Lumens [038060 KS, BUY]: Economies of scale achieved with China plant ........ 10 Flagging sales but improved operating margin 10 Expectations of 2H peak season 11 Profit growth through economies of scale 11

Summary financial statements 12

Hansol LCD [004710 KS, BUY]: Positive evolution continues............................ 14 2Q10 sales and operating profit to rise 35.1% QoQ, 99.6% QoQ 14 Higher sales portion of LED BLU will increase business reliability 14

Summary financial statements 16 Analyst team profile.....................................................................................18

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 3/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

3

1. Executive SummaryLED companies showed remarkable earnings growth in 1H10. Both their sales and operating

profit are showing exponential growth, as LED chip and package prices remain strong on

persistent strain on LED supply. Their notable earnings performance was fueled by Korea’s top-

2 TV and LCD panel makers’ dominant market leadership. We expect LED companies will see

another leap in earnings in 2H10, on growing LED TV demand. While the global LED TV

demand forecast for FY10 is 37m units, actual LED TV sales stood at only 10m units in 1H10.

This points to at least 20m LED TV sales globally in 2H10, and another earnings rally for key

domestic players.

We expect LED supply to remain tight through 2011. Although LED makers will raise the LED

TV BLU portion of total chip output to 50%, LED TV supply will not likely increase dramatically,

due to productivity issues. We estimate for 2010, LED package demand (14.4bn) should

outstrip supply (13.6bn units) by roughly 5%. We expect the slight undersupply of LED

packages to continue into 2011, as supply (25.4bn units) will still not meet demand (25.5bn

units). Given this supply forecast is mainly for 2” substrates, the supply strain can be resolved

earlier than expected, depending on output portions of 4” and 6” substrates. However,

considering that it will take quite some time before the chip production yield for larger-sizedsubstrates improves to the level of 2” substrates, we expect the supply to remain tight though

1H11, at least.

Domestic LED companies, particularly Samsung LED, saw their earnings rise steeply. Samsung

LED logged sales of W330bn and operating profit of W51.2bn in 1Q10, and is expected to

report a 30.7% QoQ rise in sales (W431.3bn) and an 87.3% QoQ surge in operating profit

(W95.9bn) for 2Q10. We forecast LG Innotek to report an operating margin of 7.5% for 2Q10,

as its LED division, having remained in the red until FY09, turned profitable in 1Q10. Seoul

Semiconductor expects to report sales of over W200bn and operating margin of 12% for 2Q10,

as it raised the sales contribution from TV BLU LED from 15% in 1Q10 to 40% in 2Q10.

Lumens, a supplier of LED packages to Samsung Electronics, expects to turn in an operating

margin of 9.3% for 2Q10.

In 2H10, four domestic LED makers are expected to grow rapidly, benefiting from LED TV

market growth on 3D TV sales and Chinese demand. Demand for LED chips will rise not only

because 3D TVs require 30% more LED chips than existing LED TVs, for high lamination and

refresh rates, but the proportion of LED TVs in the Chinese LCD TV market is also expected to

expand from 5% in 4Q09 to 20% in 3Q10. Before seasonally busy 3Q10, LED chip makers

have completed their capacity expansion. Given this, we expect their sales to grow 20 to 40%

QoQ, yielding double-digit operating margins in 2H10.

Our top picks for the LED sector include LG Innotek (011070, BUY, TP: W230,000), which is

seeing rapid earnings growth in its LED division, and Samsung Electro-Mechanics, which

delivers steady earnings from the LED, MLCC and substrate business divisions.

CE retailers will attempt to offset

slowing white CE sales by

boosting LCD TV sales

LED makers’ dramatic earnings

growth was powered by surging

demand for LED TV BLU. Most

domestic LED players, except

Seoul Semiconductor, generate

over 80% of sales from their LED

TV BLU divisions.

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 4/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

4

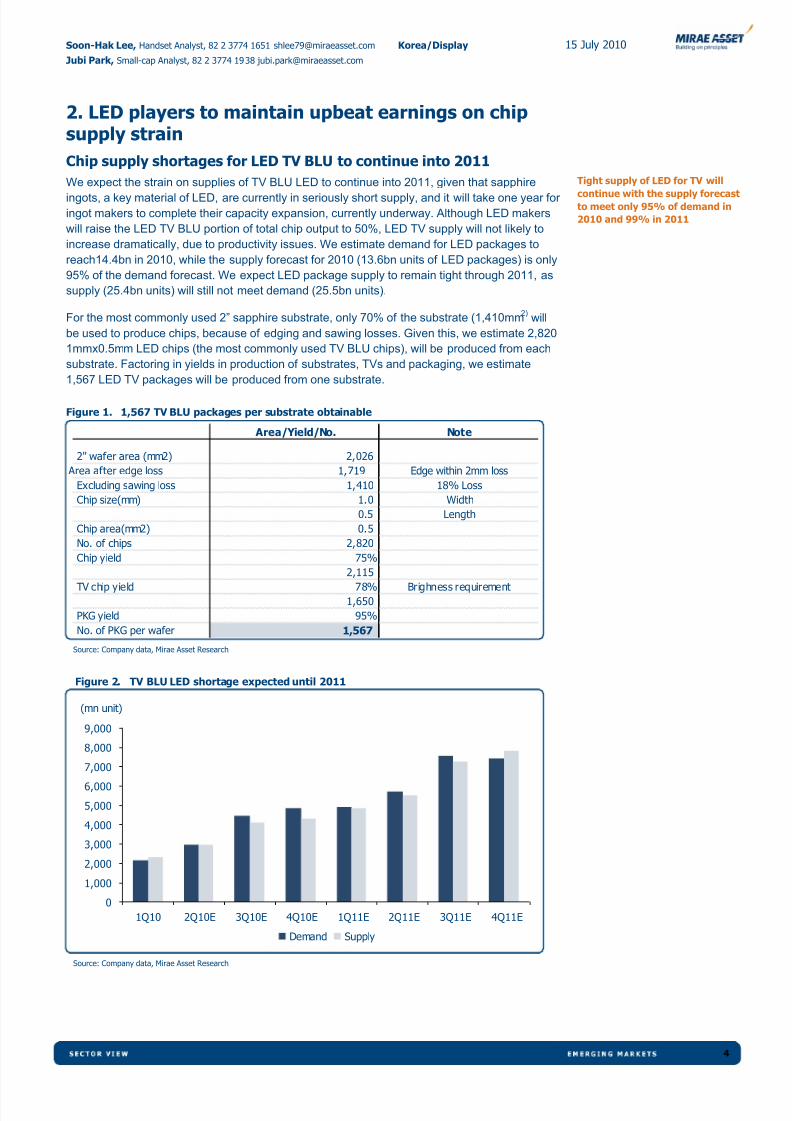

2. LED players to maintain upbeat earnings on chipsupply strain

Chip supply shortages for LED TV BLU to continue into 2011

We expect the strain on supplies of TV BLU LED to continue into 2011, given that sapphire

ingots, a key material of LED, are currently in seriously short supply, and it will take one year for

ingot makers to complete their capacity expansion, currently underway. Although LED makers

will raise the LED TV BLU portion of total chip output to 50%, LED TV supply will not likely to

increase dramatically, due to productivity issues. We estimate demand for LED packages to

reach14.4bn in 2010, while the supply forecast for 2010 (13.6bn units of LED packages) is only

95% of the demand forecast. We expect LED package supply to remain tight through 2011, as

supply (25.4bn units) will still not meet demand (25.5bn units).

For the most commonly used 2” sapphire substrate, only 70% of the substrate (1,410mm2)

will

be used to produce chips, because of edging and sawing losses. Given this, we estimate 2,820

1mmx0.5mm LED chips (the most commonly used TV BLU chips), will be produced from each

substrate. Factoring in yields in production of substrates, TVs and packaging, we estimate

1,567 LED TV packages will be produced from one substrate.

Figure 1. 1,567 TV BLU packages per substrate obtainable

Area/Yield/No. Note

2" wafer area (mm2) 2,026

Area after edge loss 1,719 Edge within 2mm loss

Excluding sawing loss 1,410 18% Loss

Chip size(mm) 1.0 Width

0.5 Length

Chip area(mm2) 0.5

No. of chips 2,820

Chip yield 75%

2,115 TV chip yield 78% Brighness requirement

1,650

PKG yield 95%

No. of PKG per wafer 1,567

Source: Company data, Mirae Asset Research

Figure 2. TV BLU LED shortage expected until 2011

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1Q10 2Q10E 3Q10E 4Q10E 1Q11E 2Q11E 3Q11E 4Q11E

(mn unit)

Demand Supply

Source: Company data, Mirae Asset Research

Tight supply of LED for TV will

continue with the supply forecastto meet only 95% of demand in

2010 and 99% in 2011

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 5/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

5

The leading global sapphire ingot makers are Rubicon (US), Monocrystal (Russia), and

Sapphire Tech (Korea). Hansol LCD has recently made a foray into the global ingot market, and

is expected to produce ingots from 2H11. We project global sapphire ingot production capacity

to reach 2.15mn/month by end-2010 and grow only 80% YoY to 3.87mn/month by end-2011.

Meanwhile, since LED TV demand is forecast to climb 148% YoY in 2011, we anticipate tight

supply to continue, even assuming that the number of LED chips required for LED TVs drops

5% each quarter.

So, will LED supplies remain tight by end-2011? We made the aforementioned LED supply

forecast based on 2” substrates. However, given that the mass-production of 4” substrates is

already underway, and that of 6” substrates is likely to begin early FY11, we anticipate the

production yield should rise further. Considering that chipmakers can produce 14% more chips

from 4” substrates, 44% more chips from 6” substrates compared with 2” substrates, we believe

supply strains can be resolved earlier than expected, depending on output portions of 4” and 6”

substrates. However, given that most ingot makers currently focus on producing 2” substrates,

their entry into the larger-sized ingot market is unlikely to accelerate. Overall, we foresee LED

chip supply shortages continuing into at least 1H11.

Figure 3. 14% and 44% productivity increase for 4” and 6” wafers

Wafer sizeRadius

(mm)

Excluding

edge loss

Effective

area(mm2)

Area after

sawing

loss(mm2)

Increase

2" 25.4 23.4 1,719 1,410

4" 50.8 48.8 7,478 6,132

6" 76.2 74.2 17,288 14,176

MOCVD

2"x42 59,214

4"x11 67,449 14%

6"x6 85,056 44%

Source: Company data, Mirae Asset Research

Figure 4. Supply and demand table for TV LED

(K units) 1Q10 2Q10E 3Q10E 4Q10E 1Q11E 2Q11E 3Q11E 4Q11E

Global LED TV 3,077 6,442 9,846 17,693 15,726 19,086 23,127 34,440

Direct type portion 18% 12% 10% 9% 9% 10% 9% 10%

Edge type portion 82% 88% 90% 91% 91% 90% 91% 90%

Direct type 548 756 960 1,645 1,441 1,834 2,180 3,362

Edge type portion 2,529 5,686 8,886 16,048 14,285 17,252 20,947 31,078

Over 40" portion 65% 51% 45% 42% 40% 41% 40% 39%

Under 40" portion 35% 49% 55% 58% 60% 59% 60% 61%

Over 40" 1,642 2,906 4,028 6,685 5,732 6,997 8,423 11,984

Under 40" 887 2,780 4,858 9,363 8,553 10,255 12,524 19,094

LED PKG necessity

Avg direct type 2,000 1,800 1,620 1,458 1,385 1,316 1,250 1,188 Avg edge type (>40") 270 257 244 231 220 209 198 189

Avg edge type (<40") 180 171 162 154 147 139 132 126

Total PKG necessity 1,698,992 2,581,601 3,325,844 5,390,925 4,510,457 5,303,424 6,053,973 8,652,261

Setmaker PKG demand 2,140,297 2,953,722 4,466,203 4,842,872 4,906,940 5,678,698 7,526,162 7,393,084

Ingot capa (K mm/m) 1,415 1,634 2,036 2,145 2,404 2,749 3,611 3,870

Utilization rate 95% 95% 95% 95% 95% 95% 95% 95%

LED BLU portion 40% 45% 50% 50% 50% 50% 50% 50%

Sapphire wafer (Q) 1,452 1,886 2,611 2,751 3,083 3,525 4,631 4,963

PKG for LED BLU 2,275,037 2,955,538 4,090,846 4,310,914 4,830,937 5,524,301 7,257,710 7,777,733

Demand - Supply 134,741 1,816 (375,356) (531,958) (76,004) (154,398) (268,452) 384,648

Source: Company data, Mirae Asset Research

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 6/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

6

LED makers’ earnings rising fast on strong LED TV demand

Domestic LED players have exhibited notable earnings improvement in 2010. We expect the

four leading domestic LED chip and packaging suppliers (Samsung LED, LG Innotek, Seoul

Semiconductor, Lumens), not including Seoul Semiconductor, to report over 100% YoY growth

in sales for FY10. In particular, Samsung LED should display the industry’s strongest earnings

growth, with sales and operating profit estimated to climb 192% YoY, and 526% YoY,respectively, in FY10. LG Innotek expects the fastest earnings turnaround in FY10, with a likely

357% YoY jump in sales and 6.8% operating profit; a dramatic turnaround from an operating

loss of 19.2% in FY09.

The LED market is indeed on an exponential growth path. It’s no wonder, then, that Samsung

LED and LG Innotek, with immense captive markets (Samsung LED, and LG Innotek,

respectively), are set to grow explosively, going forward. Moreover, Seoul Semiconductor and

Lumens, even without captive markets, anticipate their operating profit to surge 137% YoY and

465% YoY, respectively, in FY10.

LED players’ remarkable earnings growth has been fueled by LED TV. Samsung Electronics

secured first mover advantage in the global LED market, offering an immediate boon to

Samsung LED. Lumens’s stronger-than-expected earnings were also possible as it focused onproducing TV BLU LED to be shipped to Samsung Electronics. Seoul Semiconductor’s earnings

growth has also been accelerating as the company began to supply TV LEDs. The company is

likely to raise its sales contribution from LED TV to 50% in 4Q10 from 15% in 1Q10. LG Innotek,

increasingly focused on TV BLU, anticipates its operating margin topping 7% in 2H10 and 10%

in early FY11, when the mass production of 6” substrates will begin.

Figure 5. LED sales and TV BLU business portion trend

LED sales

(KRW bn) 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E 2009 2010E

Samsung LED 87.0 146.8 183.2 224.7 330.0 431.3 532.1 580.4 641.7 1,873.8

LG Innotek 29.9 46.2 65.6 94.4 155.1 245.5 311.5 366.6 236.1 1,078.7

Seoul Semiconductor 81.3 115.9 132.9 123.3 124.5 200.0 270.0 230.0 453.4 824.5Lumens 15.5 23.2 42.9 51.4 50.5 67.7 98.9 94.3 133.0 311.4

LED operat ing profit

(KRW bn)

Samsung LED 3.9 11.0 19.8 30.7 51.2 95.9 132.9 129.2 65.4 409.2

LG Innotek -8.0 -9.3 -11.3 -16.9 5.4 18.4 24.0 26.0 -45.4 73.9

Seoul Semiconductor 2.9 12.1 21.1 7.8 13.3 24.0 35.0 32.0 44.0 104.3

Lumens 0.2 0.2 2.1 3.2 4.1 6.3 11.4 10.5 5.7 32.3

LED OPM

(%)

Samsung LED 4.5 7.5 10.8 13.7 15.5 22.2 25.0 22.3 10.2 21.8

LG Innotek -26.8 -20.1 -17.2 -17.9 3.5 7.5 7.7 7.1 -19.2 6.8

Seoul Semiconductor 3.6 10.5 15.9 6.3 10.7 12.0 13.0 13.9 9.7 12.7

Lumens 1.4 0.9 4.9 6.2 8.1 9.3 11.6 11.1 4.3 10.4TV BLU sales

Samsung LED 52.2 95.4 128.2 168.5 267.0 349.6 424.0 443.1 444.4 1,483.8

LG Innotek 15.8 29.6 48.5 83.1 141.5 228.4 292.6 344.9 177.0 1,007.4

Seoul Semiconductor 0.0 0.0 0.0 0.0 18.0 80.0 121.0 115.0 0.0 334.0

Lumens 3.0 10.2 29.3 41.8 38.0 54.8 83.1 80.3 84.3 256.1

TV BLU portion

Samsung LED 60.0 65.0 70.0 75.0 80.9 81.1 79.7 76.3 69.3 79.2

LG Innotek 53.0 64.0 74.0 88.0 91.3 93.0 94.0 94.1 75.0 93.4

Seoul Semiconductor 0.0 0.0 0.0 0.0 14.5 40.0 44.8 50.0 0.0 40.5

Lumens 19.4 44.0 68.4 81.2 75.2 80.9 84.0 85.1 63.4 82.3

Source: Company data, Mirae Asset Research

Domestic LED makers, except

Seoul Semiconductor, expect

their LED sales to jump in excess

of 100% YoY in FY10.

LED players’ impressive earnings

growth has been fueled by robust

demand for LED TVs. For mostdomestic players, except Seoul

Semiconductor, the sales

contribution from LED TVs is over

80%.

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 7/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

7

Figure 6. Operating margin of LED business

(30)

(20)

(10)

0

10

20

30

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E

(%)

Samsung LED LG Innotek Seoul Semiconductor Lumens

Source: Company data, Mirae Asset Research

Figure 7. 20%~40% QoQ growth continues excluding slow season

(20)

0

20

40

60

80

100

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E

(%)

Samsung LED LG Innotek Seoul Semiconductor Lumens

Source: Company data, Mirae Asset Research

Figure 8. TV BLU sales surging in 2010

0

20

40

60

80

100

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E

(%)

Samsung LED LG Innotek Seoul Semiconductor Lumens

Source: Company data, Mirae Asset Research

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 8/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

8

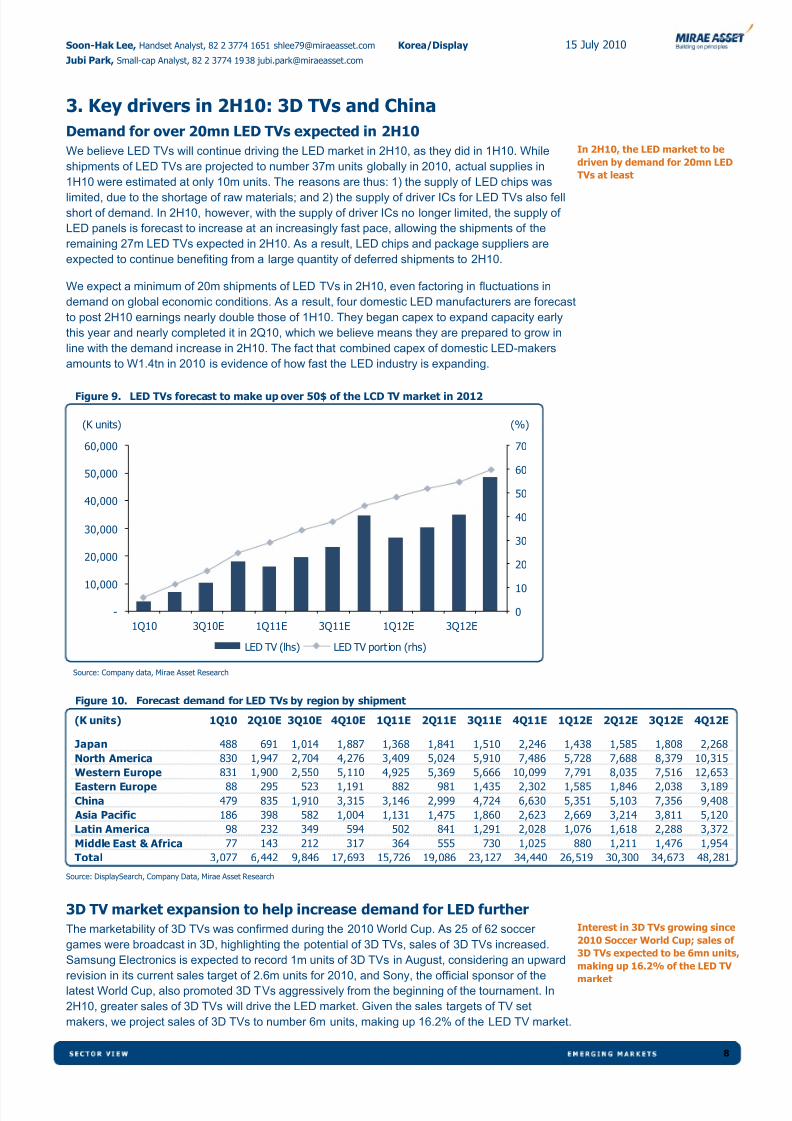

3. Key drivers in 2H10: 3D TVs and China

Demand for over 20mn LED TVs expected in 2H10

We believe LED TVs will continue driving the LED market in 2H10, as they did in 1H10. While

shipments of LED TVs are projected to number 37m units globally in 2010, actual supplies in

1H10 were estimated at only 10m units. The reasons are thus: 1) the supply of LED chips was

limited, due to the shortage of raw materials; and 2) the supply of driver ICs for LED TVs also fell

short of demand. In 2H10, however, with the supply of driver ICs no longer limited, the supply of

LED panels is forecast to increase at an increasingly fast pace, allowing the shipments of the

remaining 27m LED TVs expected in 2H10. As a result, LED chips and package suppliers are

expected to continue benefiting from a large quantity of deferred shipments to 2H10.

We expect a minimum of 20m shipments of LED TVs in 2H10, even factoring in fluctuations in

demand on global economic conditions. As a result, four domestic LED manufacturers are forecast

to post 2H10 earnings nearly double those of 1H10. They began capex to expand capacity early

this year and nearly completed it in 2Q10, which we believe means they are prepared to grow in

line with the demand increase in 2H10. The fact that combined capex of domestic LED-makers

amounts to W1.4tn in 2010 is evidence of how fast the LED industry is expanding.

Figure 9. LED TVs forecast to make up over 50$ of the LCD TV market in 2012

-

10,000

20,000

30,000

40,000

50,000

60,000

1Q10 3Q10E 1Q11E 3Q11E 1Q12E 3Q12E

(K units)

0

10

20

30

40

50

60

70

(%)

LED TV (lhs) LED TV port ion (rhs)

Source: Company data, Mirae Asset Research

Figure 10. Forecast demand for LED TVs by region by shipment

(K units) 1Q10 2Q10E 3Q10E 4Q10E 1Q11E 2Q11E 3Q11E 4Q11E 1Q12E 2Q12E 3Q12E 4Q12E

Japan 488 691 1,014 1,887 1,368 1,841 1,510 2,246 1,438 1,585 1,808 2,268

North America 830 1,947 2,704 4,276 3,409 5,024 5,910 7,486 5,728 7,688 8,379 10,315

Western Europe 831 1,900 2,550 5,110 4,925 5,369 5,666 10,099 7,791 8,035 7,516 12,653

Eastern Europe 88 295 523 1,191 882 981 1,435 2,302 1,585 1,846 2,038 3,189

China 479 835 1,910 3,315 3,146 2,999 4,724 6,630 5,351 5,103 7,356 9,408

Asia Pacific 186 398 582 1,004 1,131 1,475 1,860 2,623 2,669 3,214 3,811 5,120

Latin America 98 232 349 594 502 841 1,291 2,028 1,076 1,618 2,288 3,372

Middle East & Africa 77 143 212 317 364 555 730 1,025 880 1,211 1,476 1,954

Total 3,077 6,442 9,846 17,693 15,726 19,086 23,127 34,440 26,519 30,300 34,673 48,281

Source: DisplaySearch, Company Data, Mirae Asset Research

3D TV market expansion to help increase demand for LED further

The marketability of 3D TVs was confirmed during the 2010 World Cup. As 25 of 62 soccer

games were broadcast in 3D, highlighting the potential of 3D TVs, sales of 3D TVs increased.

Samsung Electronics is expected to record 1m units of 3D TVs in August, considering an upwardrevision in its current sales target of 2.6m units for 2010, and Sony, the official sponsor of the

latest World Cup, also promoted 3D TVs aggressively from the beginning of the tournament. In

2H10, greater sales of 3D TVs will drive the LED market. Given the sales targets of TV set

makers, we project sales of 3D TVs to number 6m units, making up 16.2% of the LED TV market.

In 2H10, the LED market to be

driven by demand for 20mn LED

TVs at least

Interest in 3D TVs growing since

2010 Soccer World Cup; sales of

3D TVs expected to be 6mn units,making up 16.2% of the LED TV

market

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 9/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

9

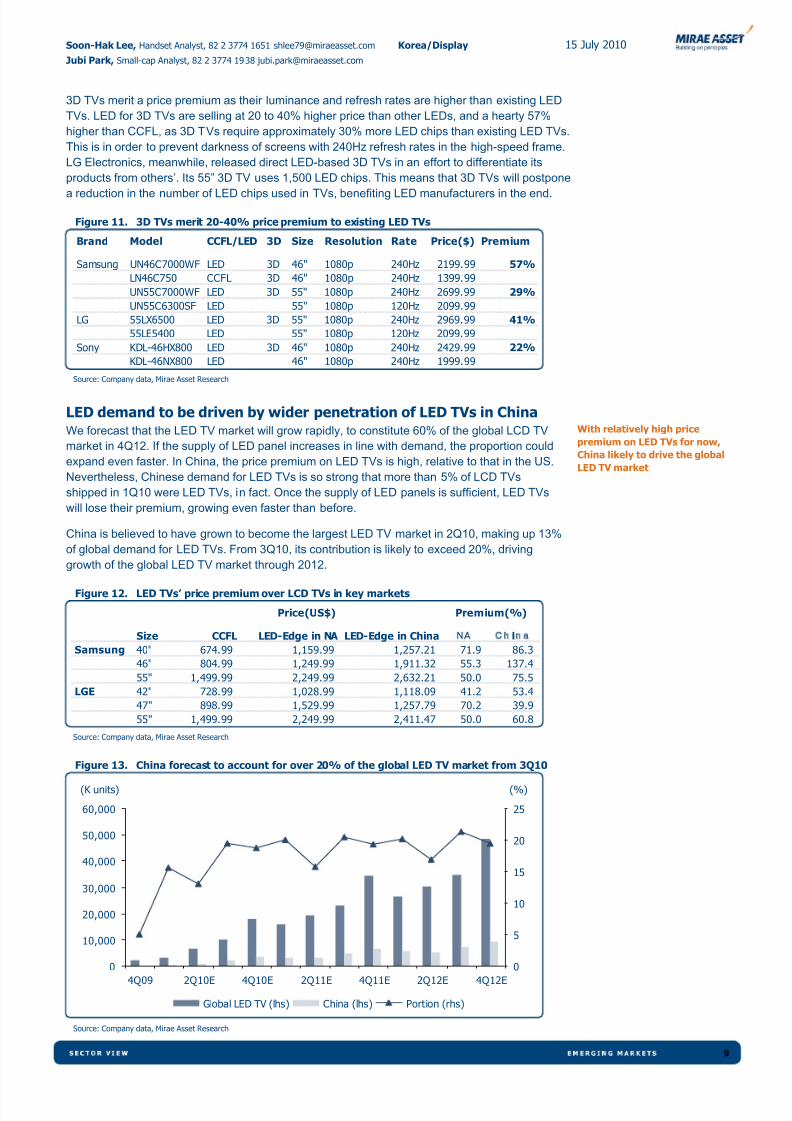

3D TVs merit a price premium as their luminance and refresh rates are higher than existing LED

TVs. LED for 3D TVs are selling at 20 to 40% higher price than other LEDs, and a hearty 57%

higher than CCFL, as 3D TVs require approximately 30% more LED chips than existing LED TVs.

This is in order to prevent darkness of screens with 240Hz refresh rates in the high-speed frame.

LG Electronics, meanwhile, released direct LED-based 3D TVs in an effort to differentiate its

products from others’. Its 55” 3D TV uses 1,500 LED chips. This means that 3D TVs will postpone

a reduction in the number of LED chips used in TVs, benefiting LED manufacturers in the end.

Figure 11. 3D TVs merit 20-40% price premium to existing LED TVs

Brand Model CCFL/LED 3D Size Resolution Rate Price($) Premium

Samsung UN46C7000WF LED 3D 46" 1080p 240Hz 2199.99 57%

LN46C750 CCFL 3D 46" 1080p 240Hz 1399.99

UN55C7000WF LED 3D 55" 1080p 240Hz 2699.99 29%

UN55C6300SF LED 55" 1080p 120Hz 2099.99

LG 55LX6500 LED 3D 55" 1080p 240Hz 2969.99 41%

55LE5400 LED 55" 1080p 120Hz 2099.99

Sony KDL-46HX800 LED 3D 46" 1080p 240Hz 2429.99 22%

KDL-46NX800 LED 46" 1080p 240Hz 1999.99

Source: Company data, Mirae Asset Research

LED demand to be driven by wider penetration of LED TVs in ChinaWe forecast that the LED TV market will grow rapidly, to constitute 60% of the global LCD TV

market in 4Q12. If the supply of LED panel increases in line with demand, the proportion could

expand even faster. In China, the price premium on LED TVs is high, relative to that in the US.

Nevertheless, Chinese demand for LED TVs is so strong that more than 5% of LCD TVs

shipped in 1Q10 were LED TVs, in fact. Once the supply of LED panels is sufficient, LED TVs

will lose their premium, growing even faster than before.

China is believed to have grown to become the largest LED TV market in 2Q10, making up 13%

of global demand for LED TVs. From 3Q10, its contribution is likely to exceed 20%, driving

growth of the global LED TV market through 2012.

Figure 12. LED TVs’ price premium over LCD TVs in key markets

Size CCFL LED-Edge in NA LED-Edge in China NA Ch in a

Samsung 40" 674.99 1,159.99 1,257.21 71.9 86.3

46" 804.99 1,249.99 1,911.32 55.3 137.4

55" 1,499.99 2,249.99 2,632.21 50.0 75.5

LGE 42" 728.99 1,028.99 1,118.09 41.2 53.4

47" 898.99 1,529.99 1,257.79 70.2 39.9

55" 1,499.99 2,249.99 2,411.47 50.0 60.8

Price(US$) Premium(%)

Source: Company data, Mirae Asset Research

Figure 13. China forecast to account for over 20% of the global LED TV market from 3Q10

0

10,000

20,000

30,000

40,000

50,000

60,000

4Q09 2Q10E 4Q10E 2Q11E 4Q11E 2Q12E 4Q12E

(K units)

0

5

10

15

20

25

(%)

Global LED TV (lhs) China (lhs) Portion (rhs)

Source: Company data, Mirae Asset Research

With relatively high price

premium on LED TVs for now,

China likely to drive the global

LED TV market

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 10/20

Hedge fund investors Long-only investors

Lumens is underappreciated compared

with other LED shares like SEMCO and

Seoul Semiconductors

The front LED industry is expected to

enjoy robust growth in the long term.

Lumens will continue to grow in theLED TV and lighting categories

10

Earnings review

See the last page of this report for important disclosures

K o r e a / T e c h H a r d w a r e & E q u i p m e n t

Lumens ׀ 038060 KS

Economies of scale achievedwith China plantWe maintain our Buy rating and target price of W18,000 on

Lumens. The reasons for our positive view are threefold: (1)

the company widened operating margin in 2Q10, despite

sales slightly below estimates due to sluggish European

markets and delayed operation of its Chinese plant; (2) we

expect Lumens to improve profitability through economies of scale achieved after it expanded production capacity for LED

packages to 170m units per month, ahead of peak season;

and (3) the fall in LED package prices will be limited due to

the shortage of LED raw materials. We are encouraged that

Topaz, in which Lumens has a 44.3% stake, is expected to

benefit from insufficient supply of ultra-bright-light guide

plates (LGP), a key component of LED TVs. Our target price

implies 16.5x FY11E EPS, which is undemanding, given

three-year EPS CAGR of 108%.

» Flagging sales but improved operating margin

» Expectations of 2H peak season

» Profit growth through economies of scale

Flagging sales but improved operating margin

For 2Q10, we expect Lumens to post sales of W67.7bn, 10% below our

estimate of W75.2bn, as (1) set makers adjusted inventories due to the

European economic slowdown; and (2) operation of the company’s plant

in Kun Shan, China was delayed for two months. However, operating

margin is estimated at 9.3%, ahead of our estimate, and operating profit

is estimated at W6.3bn, 6.7% shy of our initial projection of W6.8bn. We

maintain our target price, expecting the company to yield an operating

margin of 11%, owing to economies of scale achieved once its Chinese

plant comes on-stream.

Fiscal year ending Dec-09A Dec-10E Dec-11E Dec-12E

Revenue (KRWb) 133.0 311.4 456.9 551.3

Op EBIT (KRWb) 5.72 32.33 52.27 65.81

Net income (KRWb) 5.20 27.47 43.16 54.57

Norm profit (KRWb) 5.20 27.47 43.16 54.57

EPS (KRW) 153 692 1,087 1,374

EPS growth NA 351.0% 57.1% 26.4%

Norm P/E (x) 82.17 18.22 11.59 9.17

EV/EBITDA (x) 29.70 12.20 8.03 6.07

Dividend yield 0.00% 0.00% 0.79% 1.19%

P/B (x) 4.88 4.34 3.24 2.46

ROE 9.4% 27.1% 32.0% 30.5%

Net debt/equity 36.6% 21.7% 4.5% (17.8%)

Cons EPS (KRW) 153 714 1,017 1,374

Prev EPS (KRW) 135 752 991 1,287

Target price W18,000

Current price (13 July 2010) W12,600

Upside/downside 42.9%

Consensus target price W17,000

Difference from consensus 5.9%

Forecast earnings & valuation

BUY 16 July 2010

Market cap (Wbn/US$mn) 500.5/409.0

Shares outstanding 39.72mn

Free float 68.8%

52-week price high/low W4,110 –15,900

Daily average turnover (3M) US$28.30mn

Performance 1M 3M 12M

Absolute 10.5% 18.9% 195

Relative to KOSPI 7.0% 17.5% 173.7%

Absolute (US$) 11.6% 8.9% 207.2%Major shareholders

Kyung-Jae Lee 11.5%

Hanmi Semiconductor Inc. 7.6%

2,900

4,900

6,900

8,900

10,900

12,900

14,900

16,900

Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Jul-10

66

116

166

216

266

316

366

416Price Close Relati ve to .KS11 (RHS)

Performance

Trading data

Source for data: Company, Bloomberg, Mirae Asset Research

Earnings quality score

Earnings Quality Score

Historical Earnings Stability

Consensus Forecast Certainty

Consensus Forecast Accuracy

38

50

48

50

0 25 50 75 100

Sector Average: 55

BUY 11 May 2010

BUY 12 Apr 2010

Soon-Hak Lee, Korea Handset Analyst, 82 2 3774 1651 [email protected]

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 11/20

Soon-Hak Lee, Korea Handset Analyst, 82 2 3774 1651 [email protected] Lumens 16 July 2010

038060 KS

11

Expectations of 2H peak season

We estimate sales of LED TVs at 10mn units globally in 1H10 versus a full-year sales estimate

of 37m units. We believe set makers will begin to build up their parts inventories ahead of

seasonally strong 2H10, in which China’s National Day and Black Friday fall, allowing LED

markers to continue to enjoy booming sales. Assuming that sales of at least 20m LED TVs are

possible, and given that the company has more than 20% of market share within Samsung

Electronics, we forecast the company will enjoy sales of nearly W100bn each quarter.

Profit growth through economies of scale

As it has completed capacity expansion at its Chinese plant, the company is now able to supply

170m LED packages a month, which is enough to manufacture 1.7m LED TVs per quarter.

Capacity expansion will reduce the company’s fixed costs and help it improve operating margin.

The company’s mass production strengthens its chip purchasing power, and its strategic

business tie-up with Taiwan-based LED chip makers helps it to maintain stable chip supplies,

limiting a rise in chip prices. 3Q10 sales and operating profit are projected to be a record

W98.9bn and W11.4bn, respectively.

Figure 14. 2Q10 earnings forecast revisions

Before Revision After Revision

(W bn, %) 2Q10E 2Q10E Diff. (%, %p) 1Q10 QoQ (%,%p) 2Q09 YoY (%, %p)

Revenue 75.2 67.7 -10.0% 50.5 34.1% 23.2 192.4%

OP 6.8 6.3 -6.7% 4.1 54.7% 0.2 2965.2%

Pre-tax profit 6.3 6 -9.2% 3.4 67.0% 0.1 4326.5%

NP 5.8 5 -9.2% 2.7 92.2% 0.5 870.2%

Operating Margin 9.0% 9.3% 0.3 8.1% 1.2 0.9% 8.5

Net Margin 7.7% 7.8% 0.1 5.4% 2.4 2.4% 5.5 Source: Company data, Mirae Asset Research

Figure 15. Revision of annual earnings forecasts

(W bn, %) 2010E 2011E 2010E 2011E 2010E 2011E

Revenue 340.2 442.4 311.4 456.9 -8.5% 3.3%

OP 35.1 49.8 32.3 52.5 -7.8% 5.4%

Pre-tax profit 33.4 48.7 30.3 50.8 -9.1% 4.3%

NP 30.3 41.4 27.5 43.2 -9.2% 4.3%

EPS (KRW) 762.1 1,041.8 691.6 1,086.7 -9.2% 4.3%

Operating Margin 10.3% 11.2% 10.4% 11.5% 0.1 0.2

Net Margin 8.9% 9.4% 8.8% 9.4% (0.1) 0.1

Before Revision After Revision Difference (%, %p)

Source: Company data, Mirae Asset Research

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 12/20

Soon-Hak Lee, Korea Handset Analyst, 82 2 3774 1651 [email protected] Lumens 16 July 2010

038060 KS

12

Summary financial statements

Profit & Loss

(KRWb) Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Revenue 75 133 311 457 551 Cost of goods sold (62) (113) (255) (373) (451)

Gross profit 13 20 57 84 101

SG and A (10) (14) (24) (31) (35)

Op profit 3 6 32 52 66

Op EBITDA 8 15 43 63 77

Depreciation (3) (7) (10) (10) (10)

Amortisation (2) (2) (1) (1) (1)

Op EBIT 3 6 32 52 66

Net interest (1) (2) (2) (2) (1)

Associates and JCEs - - 0 2 2

Other income (5) 1 (0) (2) (2)

Net exceptional income - - - - -

Profit before tax (3) 4 30 51 64

Tax 1 1 (3) (8) (10) Post-tax profit (2) 5 27 43 55

Minorities - - - - -

Preferred dividends

Net income (2) 5 27 43 55

Norm profit (2) 5 27 43 55

Dividends - - - (4) (6)

Retained earnings (2) 5 27 39 49

Source: Company data, Mirae Asset Research estimates

Cashflow

(KRWb) Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Op EBITDA 8 15 43 63 77

Decrease in working capital (13) (24) (20) (16) (3) Other operating cashflow (1) 1 4 (6) (6)

Operating cashflow (6) (8) 27 40 68

Tax paid 1 1 (3) (8) (10)

Net interest (1) (2) (2) (2) (1)

Dividends received - - 0 2 2

Cashflow (6) (9) 22 33 59

Capital expenditure (8) (45) (15) (12) (12)

Net acquisitions - - - - -

Net investments (4) (1) (5) (3) (2)

Other investing cashflow 8 (17) 2 3 2

Investing cashflow (4) (63) (19) (13) (11)

Dividends paid - - - (4) (6)

Increase in equity 7 60 0 - (0)

Increase in debt 26 20 3 - -

Other financing cashflow (26) (2) 3 2 1 Financing cash flow 7 79 7 (2) (5)

Beginning cash 13 9 16 26 44

Total cash generated (4) 6 10 18 43

Forex effects

Ending cash 9 16 26 44 87

Source: Company data, Mirae Asset Research estimates

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 13/20

Soon-Hak Lee, Korea Handset Analyst, 82 2 3774 1651 [email protected] Lumens 16 July 2010

038060 KS

13

Balance Sheet

(KRWb) Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Current assets 33 99 173 220 278

Cash and equivalents 9 16 26 44 87

Receivables 10 37 75 87 97

Inventories 11 34 52 67 71

Other current assets 4 12 21 22 23 Non current assets 28 83 84 89 92

Net operating fixed assets 13 51 46 46 47

Interest in associates

Other non-current ssets 15 32 38 43 45

Total assets 62 182 257 309 370

Current liabilities 27 64 104 116 128

Payables 8 38 83 95 106

ST debt 16 17 14 14 14

Other current liabilities 3 8 7 7 8

Total non-current liabilities 12 31 39 39 39

LT debt 11 30 38 38 38

Other non-current liabilities 1 0 1 1 1

Total liabilities 39 94 142 154 166

Issued capital 15 20 20 20 20

Share premium reserve 22 65 65 65 65 Reserves/Adjustments (19) (7) 1 1 1

Retained earnings 5 10 29 69 117

Minorities - - - - -

Other equity - - - - -

Shareholders' equity 23 88 115 155 203

Source: Company data, Mirae Asset Research estimates

Key Ratios

Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Turnover growth 507.3% 77.4% 134.1% 46.7% 20.7%

Gross profit growth 187.5% 50.6% 187.3% 47.8% 20.6%

Operating profit growth 8.4% 86.6% 465.1% 61.7% 25.9%

EBITDA growth (9.6%) 381.7% 178.4% 46.7% 21.0%EPS growth (120.3%) NA 351.0% 57.1% 26.4%

Norm BPS growth (61.1%) 222.7% 12.5% 34.0% 31.4%

Gross margin 17.4% 14.8% 18.1% 18.3% 18.3%

Operating margin 4.1% 4.3% 10.4% 11.4% 11.9%

EBITDA margin 4.3% 11.6% 13.8% 13.8% 13.9%

EBIT margin (2.3%) 4.7% 10.4% 11.5% 11.9%

Net income margin (2.47%) 3.91% 8.82% 9.45% 9.90%

ROE (9.3%) 9.4% 27.1% 32.0% 30.5%

ROA (4.4%) 4.3% 12.5% 15.2% 16.1%

Net debt/equity 80.2% 36.6% 21.7% 4.5% (17.8%)

Interest cover ratio 2.55 2.56 11.05 18.10 22.78

Dividend payout ratio 0.0% 0.0% 0.0% 9.2% 10.9%

Inventory days 62.3 108.7 74.0 65.2 57.5

Account receivable days 47.0 101.8 87.7 69.8 64.4

Account payable days 47.8 123.0 118.8 92.5 86.3Reported EPS (KRW) -66 153 692 1,087 1,374

EPS (KRW) -66 153 692 1,087 1,374

Reported BPS (KRW) 800 2,582 2,905 3,892 5,116

Norm BPS (KRW) 800 2,582 2,905 3,892 5,116

DPS (KRW) 0.0 0.0 0.0 100.0 150.0

Cashflow per share (KRW) -230 -271 561 826 1,492

Reported P/E (x) NA 82.17 18.22 11.59 9.17

Norm P/E (x) NA 82.17 18.22 11.59 9.17

P/B (x) 15.75 4.88 4.34 3.24 2.46

P/CF NA NA 22.46 15.25 8.45

EV/EBITDA (x) 116.1 29.7 12.2 8.0 6.1

EV/Operating Cashflow (x) NA NA 19.48 12.65 6.80

EV/Sales (x) 4.97 3.45 1.69 1.11 0.84

Dividend yield 0.00% 0.00% 0.00% 0.79% 1.19%

Source: Company data, Mirae Asset Research estimates

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 14/20

Hedge fund investors Long-only investors

Watch for growing sales visibility backed

by the rapidly growing LED proportion

of total BLU output

We see positive implications for its

transformation to an LED company

once it successfully enters its sapphire

ingot and solar cell businesses

14

Earnings review

See the last page of this report for important disclosures

K o r e a / T e c h H a r d w a r e & E q u i p m e n t

Hansol LCD ׀ 004710.KS

Positive evolution continuesWe maintain our Buy rating and target price of W80,000 on

Hansol LCD based on three principle investment points: (1)

the rapidly increasing proportion of LEDs used in total

backlight unit (BLU) output, leading to (2) growing sales

visibility; and (3) Hansol’s prospects for successful entry into

new businesses, including LED sapphire ingots and solar cell

modules. We see our target P/E of 14x 12-month forward

EPS of W5,570 undemanding given the likelihood Hansol will

successfully enter new business lines and the company’s

overall business stability supported by steady LED BLU sales

(comprising 64% of total sales).

» 2Q10 sales and operating profit to rise 35.1% YoY, 99.6% YoY

» Higher portion of LED BLU sales will lead to greaterincrease business reliability

» Entry into new businesses is positive

» Buy rating and target price of W80,000 m aintained

2Q10 sales and operating profit to rise 35.1% QoQ,99.6% QoQWe expect Hansol LCD to report a 35.1% QoQ rise in sales (W377.3bn)

and 99.6% QoQ jump in operating profit (W5.9bn) for 2Q10. Such

upbeat 2Q10 earnings, should they be realized, would be due mainly a

surge in LED BLU portion in total BLU shipments from 35% in 1Q10 to

59.4% in 2Q10. We raised our FY10 full-year sales estimate for the

company by 15%, to roughly W1.5tr, as LED BLU is forecast to

represent over 50% of Hansol’s total BLU output in FY10. Meanwhile,

we lowered our FY10 operating profit forecast for Hansol to W22bn, toreflect cost hikes on the increased sales proportion of LED BLU.

Higher sales portion of LED BLU w ill increasebusiness reliability

We anticipate the company’s LED BLU shipments to rise steadily in

2H10 as global LED TV shipments are forecast to be 27m units, 2.7

times larger than the figure recorded in 1H10. Rising ASP of LED BLU

Fis ca l y ea r e nd in g De c- 09A De c-1 0E De c-1 1E De c-1 2E

Revenue (KRWb) 1,102 1,492 1,655 1,925

Op EBIT (KRWb) 11.24 22.02 34.60 41.78

Net income (KRWb) 21.16 35.59 46.03 53.38

Norm profit (KRWb) 21.16 35.59 46.03 53.38

EPS (KRW) 3,233 5,078 6,142 7,122

EPS growth 234.7% 57.1% 21.0% 16.0%

Norm P/E (x) 17.94 11.42 9.44 8.14EV/EBITDA (x) 11.87 8.00 6.03 5.12

Dividend yield 0.396% 0.000% 0.413% 0. 413%

P/B (x) 3.01 2.03 1.78 1.47

ROE 18.0% 21.8% 20.7% 19.7%

Net debt/equity 0. 3% (7.2%) (15.8%) (17.5%)

Cons EPS (KRW) 3,233 5,405 6,368 7,122

Prev EPS (KRW) 3,344 6,082 6,988 7,421

Jubi Park, Handset Analyst, +82 2 3774 1938 [email protected]

Forecast earnings & valuation

B U Y 16 July 2010 BU Y

19 May 2010

Market cap (Wbn/US$mn) 347.3/286.0

Shares outstanding 6.33mn

Free float 78.5%

52-week price high/low W19,474 –61,966

Daily average turnover (3M) US$10.10mn

Performance 1M 3M 12M

Absolute 3.2% 43.4% 162

Relative to -0.4% 42.0% 136.3%

Absolute (US$) 6.0% 32.9% 183.4%

Major shareholders

Hansol Paper 12.7%

Samsung Investment 6.5%

15,00020,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Ju l-10

53

78

103

128

153

178

203

228

253

278

303Price Close Re lative to .KS11 (RHS)

Performance

Trading data

Source for data: Company, Bloomberg, Mirae Asset Research

Earnings qual i ty score

Earnings Quality Score

Historical Earnings Stability

Consensus Forecast Certainty

Consensus Forecast Accuracy

23

50

43

30

0 25 50 75 100

Sector Average: 55

Target price W80,000

Current pr ice (13 July 2010) W57,800

Upside/downside 38.4%

Consensus target price W72,500

Difference from consensus 10.3%

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 15/20

Jubi Park, Handset Analyst, 82 2 3774 1938 [email protected] Hansol LCD 16 July 2010

004710 KS

15

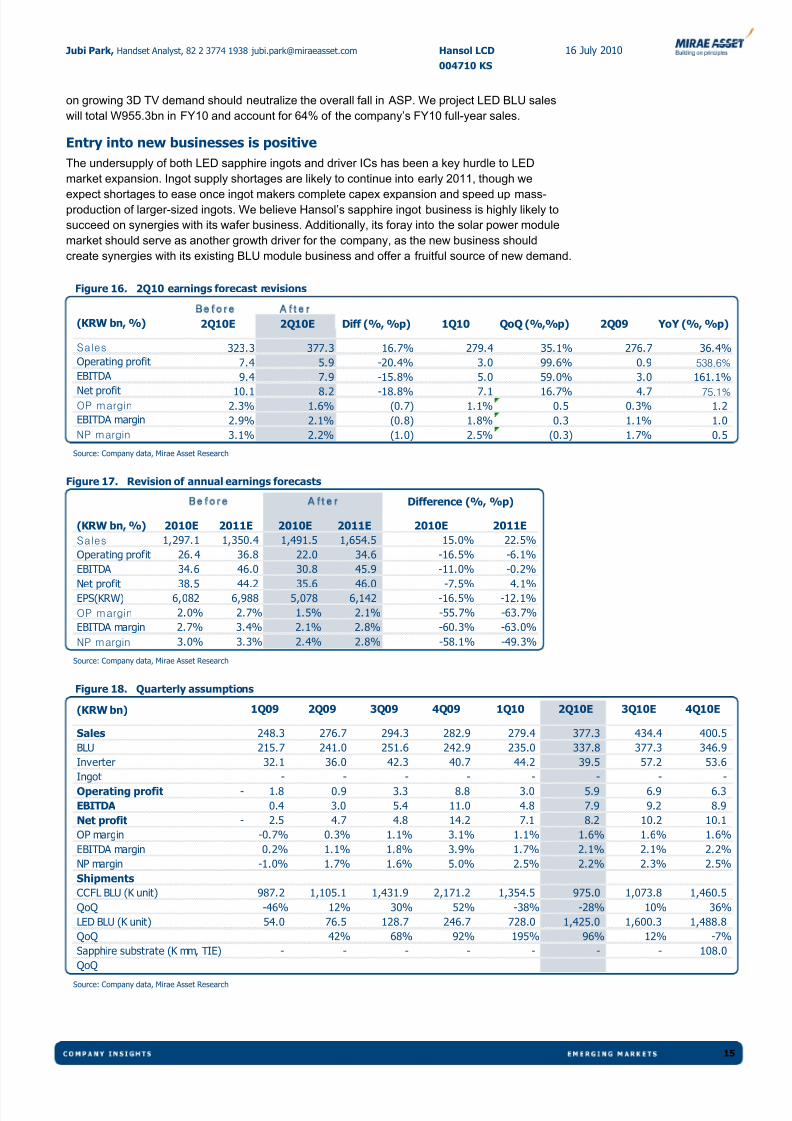

on growing 3D TV demand should neutralize the overall fall in ASP. We project LED BLU sales

will total W955.3bn in FY10 and account for 64% of the company’s FY10 full-year sales.

Entry into new businesses is positive

The undersupply of both LED sapphire ingots and driver ICs has been a key hurdle to LED

market expansion. Ingot supply shortages are likely to continue into early 2011, though we

expect shortages to ease once ingot makers complete capex expansion and speed up mass-production of larger-sized ingots. We believe Hansol’s sapphire ingot business is highly likely to

succeed on synergies with its wafer business. Additionally, its foray into the solar power module

market should serve as another growth driver for the company, as the new business should

create synergies with its existing BLU module business and offer a fruitful source of new demand.

Figure 16. 2Q10 earnings forecast revisions

Be fore A fte r

(KRW bn, %) 2Q10E 2Q10E Diff (%, %p) 1Q10 QoQ (%,%p) 2Q09 YoY (%, %p)

Sales 323.3 377.3 16.7% 279.4 35.1% 276.7 36.4%

Operating profit 7.4 5.9 -20.4% 3.0 99.6% 0.9 538.6%

EBITDA 9.4 7.9 -15.8% 5.0 59.0% 3.0 161.1%

Net profit 10.1 8.2 -18.8% 7.1 16.7% 4.7 75.1%

OP margin 2.3% 1.6% (0.7) 1.1% 0.5 0.3% 1.2

EBITDA margin 2.9% 2.1% (0.8) 1.8% 0.3 1.1% 1.0

NP margin 3.1% 2.2% (1.0) 2.5% (0.3) 1.7% 0.5

Source: Company data, Mirae Asset Research

Figure 17. Revision of annual earnings forecasts

(KRW bn, %) 2010E 2011E 2010E 2011E 2010E 2011E

Sales 1,297.1 1,350.4 1,491.5 1,654.5 15.0% 22.5%

Operating profit 26. 4 36.8 22.0 34.6 -16.5% -6.1%

EBITDA 34.6 46.0 30.8 45.9 -11.0% -0.2%Net profit 38.5 44.2 35.6 46.0 -7.5% 4.1%

EPS(KRW) 6,082 6,988 5,078 6,142 -16.5% -12.1%

OP margin 2.0% 2.7% 1.5% 2.1% -55.7% -63.7%

EBITDA margin 2.7% 3.4% 2.1% 2.8% -60.3% -63.0%

NP margin 3.0% 3.3% 2.4% 2.8% -58.1% -49.3%

Be fore A fte r Difference (%, %p)

Source: Company data, Mirae Asset Research

Figure 18. Quarterly assumptions

(KRW bn) 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10E 3Q10E 4Q10E

Sales 248.3 276.7 294.3 282.9 279.4 377.3 434.4 400.5

BLU 215.7 241.0 251.6 242.9 235.0 337.8 377.3 346.9

Inverter 32.1 36.0 42.3 40.7 44.2 39.5 57.2 53.6 Ingot - - - - - - - -

Operating profit 1.8- 0.9 3.3 8.8 3.0 5.9 6.9 6.3

EBITDA 0.4 3.0 5.4 11.0 4.8 7.9 9.2 8.9

Net profit 2.5- 4.7 4.8 14.2 7.1 8.2 10.2 10.1

OP margin -0.7% 0.3% 1.1% 3.1% 1.1% 1.6% 1.6% 1.6%

EBITDA margin 0.2% 1.1% 1.8% 3.9% 1.7% 2.1% 2.1% 2.2%

NP margin -1.0% 1.7% 1.6% 5.0% 2.5% 2.2% 2.3% 2.5%

Shipments

CCFL BLU (K unit) 987.2 1,105.1 1,431.9 2,171.2 1,354.5 975.0 1,073.8 1,460.5

QoQ -46% 12% 30% 52% -38% -28% 10% 36%

LED BLU (K unit) 54.0 76.5 128.7 246.7 728.0 1,425.0 1,600.3 1,488.8

QoQ 42% 68% 92% 195% 96% 12% -7%

Sapphire substrate (K mm, TIE) - - - - - - - 108.0

QoQ

Source: Company data, Mirae Asset Research

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 16/20

Jubi Park, Handset Analyst, 82 2 3774 1938 [email protected] Hansol LCD 16 July 2010

004710 KS

16

Summary financial statements

Profit & Loss

(KRWb) Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Revenue 1,096 1,102 1,492 1,655 1,925 Cost of goods sold (1,029) (1,052) (1,420) (1,571) (1,827)

Gross profit 67 50 71 84 98

SG and A (47) (39) (49) (49) (56)

Op profit 19 11 22 35 42

Op EBITDA 30 20 31 46 54

Depreciation (11) (9) (9) (11) (12)

Amortisation - - - - -

Op EBIT 19 11 22 35 42

Net interest (1) (0) (0) (0) (0)

Associates and JCEs 1 18 16 16 15

Other income (10) (5) 2 4 6

Net exceptional income - - - - -

Profit before tax 10 23 40 54 63

Tax (3) (2) (4) (8) (9) Post-tax profit 6 21 36 46 53

Minorities - - - - -

Preferred dividends

Net income 6 21 36 46 53

Norm profit 6 21 36 46 53

Dividends (2) (2) - (2) (2)

Retained earnings 5 20 36 44 52

Source: Company data, Mirae Asset Research estimates

Cashflow

(KRWb) Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Op EBITDA 30 20 31 46 54

Decrease in working capital 19 (5) (14) 5 (31) Other operating cashflow 0 (11) (18) (15) (8)

Operating cashflow 50 3 (2) 36 15

Tax paid (3) (2) (4) (8) (9)

Net interest (1) (0) (0) (0) (0)

Dividends received 1 18 16 16 15

Cashflow 47 19 9 44 20

Capital expenditure (4) (3) (36) (27) (9)

Net acquisitions - - - - -

Net investments (18) 5 (8) 5 3

Other investing cashflow (0) (0) 5 4 1

Investing cashflow (22) 2 (39) (19) (5)

Dividends paid 2 2 - 2 2

Increase in equity - - 5 - -

Increase in debt (15) (6) 2 - -

Other financing cashflow 2 (13) 41 (2) (3) Financing cash flow (11) (17) 47 (0) (1)

Beginning cash 0 13 17 33 57

Total cash generated 13 4 16 24 13

Forex effects

Ending cash 13 17 33 57 70

Source: Company data, Mirae Asset Research estimates

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 17/20

Jubi Park, Handset Analyst, 82 2 3774 1938 [email protected] Hansol LCD 16 July 2010

004710 KS

17

Balance Sheet

(KRWb) Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Current assets 72 84 168 193 246

Cash and equivalents 13 17 33 57 70

Receivables 35 37 89 86 115

Inventories 16 21 36 39 49

Other current assets 8 9 11 11 12 Non current assets 142 147 194 220 229

Net operating fixed assets 108 95 122 139 136

Interest in associates

Other non-current ssets 34 52 71 81 93

Total assets 215 231 362 413 475

Current liabilities 93 91 146 151 161

Payables 46 64 120 125 134

ST debt 21 16 18 18 18

Other current liabilities 26 11 8 9 9

Total non-current liabilities 13 14 15 17 18

LT debt 2 1 1 1 1

Other non-current liabilities 11 14 15 16 17

Total liabilities 106 106 161 168 179

Issued capital 32 32 36 36 36

Share premium reserve 15 15 51 51 51 Reserves/Adjustments (0) (3) (3) (3) (3)

Retained earnings 62 82 116 160 212

Minorities - - - - -

Other equity - - - - -

Shareholders' equity 109 126 201 245 296

Source: Company data, Mirae Asset Research estimates

Key Ratios

Dec-08A Dec-09A Dec-10E Dec-11E Dec-12E

Turnover growth 47.2% 0.6% 35.3% 10.9% 16.3%

Gross profit growth 75.7% (24.2%) 41.4% 17.7% 16.3%

Operating profit growth 90.3% (41.2%) 95.9% 57.1% 20.8%

EBITDA growth (10.7%) 47.0% 53.0% 34.0% 13.9%EPS growth (33.9%) 234.7% 57.1% 21.0% 16.0%

Norm BPS growth 1.0% 15.9% 48.7% 14.2% 21.1%

Gross margin 6.07% 4.57% 4.78% 5.07% 5.07%

Operating margin 1.74% 1.02% 1.48% 2.09% 2.17%

EBITDA margin 1.99% 2.91% 3.28% 3.97% 3.89%

EBIT margin 0.98% 2.12% 2.70% 3.28% 3.27%

Net income margin 0.58% 1.92% 2.39% 2.78% 2.77%

ROE 5.8% 18.0% 21.8% 20.7% 19.7%

ROA 2.9% 9.5% 12.0% 11.9% 12.0%

Net debt/equity 9.0% 0.3% (7.2%) (15.8%) (17.5%)

Interest cover ratio 9.05 11.44 30.62 50.91 61.48

Dividend payout ratio 25.0% 7.1% 0.0% 3.9% 3.4%

Inventory days 5.61 7.37 9.16 9.01 9.84

Account receivable days 11.74 12.30 21.70 18.92 21.89

Account payable days 16.28 22.14 30.74 29.06 26.90Reported EPS (KRW) 966 3,233 5,078 6,142 7,122

EPS (KRW) 966 3,233 5,078 6,142 7,122

Reported BPS (KRW) 16,605 19,241 28,614 32,664 39,547

Norm BPS (KRW) 16,605 19,241 28,614 32,664 39,547

DPS (KRW) 241.7 229.5 0.0 239.3 239.3

Cashflow per share (KRW) 7,106 2,878 1,285 5,842 2,655

Reported P/E (x) 60.05 17.94 11.42 9.44 8.14

Norm P/E (x) 60.05 17.94 11.42 9.44 8.14

P/B (x) 3.49 3.01 2.03 1.78 1.47

P/CF 8.16 20.16 45.14 9.93 21.85

EV/EBITDA (x) 17.88 11.87 8.00 6.03 5.12

EV/Operating Cashflow (x) 7.8 109.7 NA 11.0 26.1

EV/Sales (x) 0.355 0.345 0.263 0.239 0.199

Dividend yield 0.417% 0.396% 0.000% 0.413% 0.413%

Source: Company data, Mirae A sset Research estimates

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 18/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

18

Analyst team profile

Soon Hak LeeH A N D S E T A N A L Y S T

After graduating from Hanyang University with BA in Electronic & Electrical Engineering,

Soonhak worked at Samsung Electronics in handset technology planning for 5 years. He joined

Mirae Asset Securities as handset analyst in January 2010. Soonhak is currently covering

Korean handset industry and component sectors.

Jubi ParkS M A L L - C A P A N A L Y S T

After earning an MBA degree at Seoul National University, Jubi joined Mirae Asset in Korea in2009 to assist the technology research. Jubi is also a graduate of The University of California,

Los Angeles, majoring in business economics and has previously worked with the audit

department of BDO Daejoo Accounting Corporation as an AICPA for two years.

+82 2-3774-1651/ 10-3090-6846

+822-3774-8940/ 10-7185-8940

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 19/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

19

Recommendations

By stock (12 months)

Buy: A target price + 10% or more above the current price,

Hold: Target price within - 10% to +10% of the current price

Reduce: A target price of –10% or less below the current price

By industry

Overweight: over +10% of the current industry index

Neutral: -10% to +10% of the current industry index

Underweight: -10% or less than the current industry index

Earnings quality score

Earnings Quality Score = 0.70*(Historical Earnings Stability) + 0.15*(Consensus Forecast Certainty) + 0.15*(Consensus Forecast Accuracy)

1. Historical Earnings Stability

- The variability of the net profit growth rate (YOY) over the last 20 quarters was translated into percentage terms.

- Earnings growth variability was calculated based on MAD (Median Absolute Deviation), rather than SD (Standard Deviation) in order to

minimize distortion from outliers.

- The lower the earnings growth variability, the higher this indicator.

2. Consensus Forecast Certainty

- The gap between analysts' views on 12-month forward EPS was translated into percentage terms.

- The gap is calculated by dividing the SD of 12-month forward EPS with the average value.

- The narrower the gap is, the higher this indicator.

3. Consensus Forecast Accuracy- The median value of absolute EPS surprise over the last 3-year was translated into percentage terms.

- EPS surprise was calculated based on 'the actual figure at the end of the year / the consensus estimate at the beginning of the year - 1'.

- The lower the absolute EPS surprise, the higher this indicator.

* Reference

1) Consensus Forecast Certainty and Consensus Forecast Accuracy were applied only to companies with more than 5 years of EPS estimates.

2) We gave the average score of 50 to cases in which the aforementioned indicators could not be produced.

Compliance Notice

This report is distributed to our clients only, and none of the report material may be copied or distributed to any other party. While Mirae AssetSecurities have taken all reasonable care to ensure its reliability, we do not guarantee that it is accurate or complete. Therefore, Mirae AssetSecurities shall not be liable for any result from the use of this report. This report has never been provided to any institutional investor or thirdparty. This report has been prepared without any undue external influence or interference, and accurately reflects the personal views of theanalyst on the company herein.

[Analyst: Soon-Hak Lee] [Analyst: Jubi Park]Securities Held by the Analyst

Stock Analyst TypeNumber of

SharesPurchase

PricePurchase

Date

Holdings of share of

over 1%

Participationin Issuance

of Securities

Involvementwith

Affiliates

Treasury Stock Held

N/A

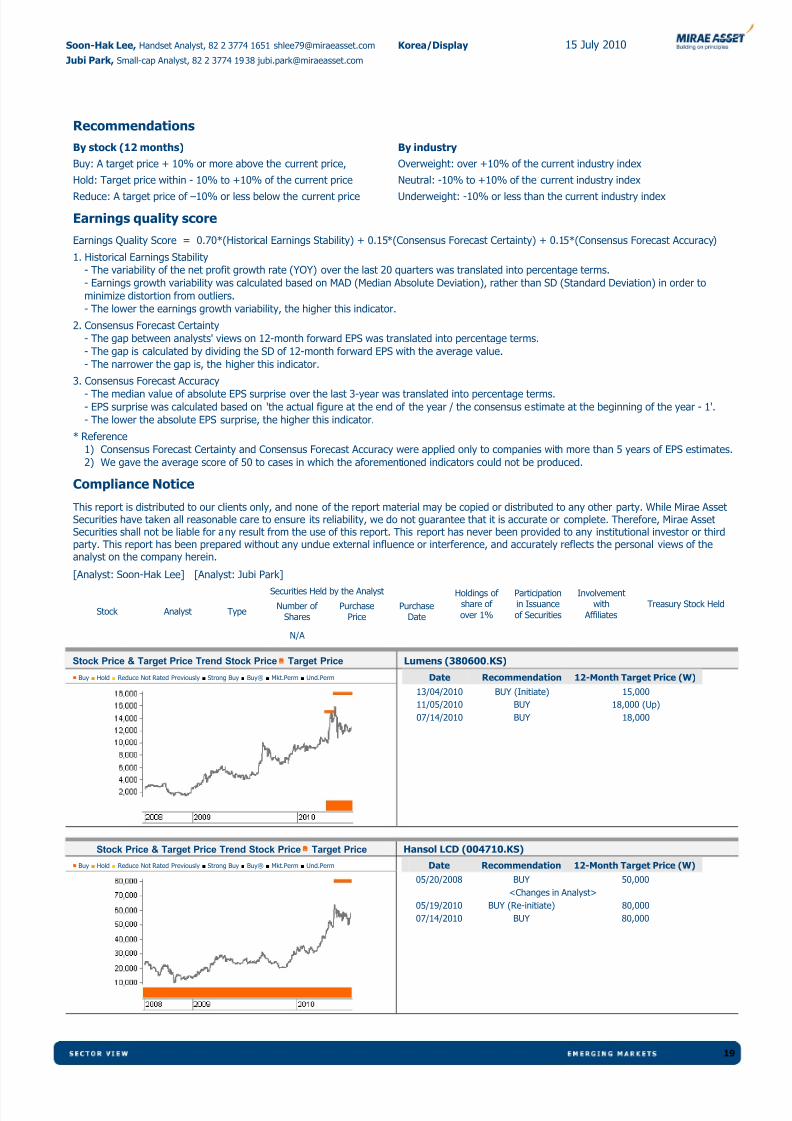

Stock Price & Target Price Trend Stock Price Target Price Lumens (380600.KS)

■ Buy ■ Hold ■ Reduce Not Rated Previously ■ Strong Buy ■ Buy® ■ Mkt.Perm ■ Und.Perm Date Recommendation 12-Month Target Price (W)

13/04/2010 BUY (Initiate) 15,000

11/05/2010 BUY 18,000 (Up)

07/14/2010 BUY 18,000

Stock Price & Target Price Trend Stock Price Target Price Hansol LCD (004710.KS)

■ Buy ■ Hold ■ Reduce Not Rated Previously ■ Strong Buy ■ Buy® ■ Mkt.Perm ■ Und.Perm Date Recommendation 12-Month Target Price (W)

05/20/2008 BUY 50,000

<Changes in Analyst>

05/19/2010 BUY (Re-initiate) 80,000

07/14/2010 BUY 80,000

8/7/2019 Sector_LED_20100715_Mirae

http://slidepdf.com/reader/full/sectorled20100715mirae 20/20

Soon-Hak Lee, Handset Analyst, 82 2 3774 1651 [email protected] Korea/Display 15 July 2010

Jubi Park, Small-cap Analyst, 82 2 3774 1938 [email protected]

Required Disclosure

The views expressed in this report accurately reflect the personal views of the analysts about the subject securities and listed corporations. Each analyst declares that neither he/she nor his/her associate serves as an officer or has any financial interests in relation to the listed corporation reviewed by the analyst. None of the listed corporations reviewed or any third party has provided or agreed to provide any compensation or other benefits in connection

with this report to any of the analysts of Mirae Asset Securities (HK) Limited (“MAHK”). MAHK confirms that it, whether individually or as a group, (i) does not own 1% or more financial interests in any of the listed corporations reviewed; or (ii) does not have any individual employed by or associated with any member companies of MAHK Group serving as an officer of any listed corporation reviewed. MAHK is not involved in making a market in the securities of the covered stocks. MAHK has no investment banking relationship with the stocks covered within the preceding 12 months.

This disclosure statement is made pursuant to paragraph 16 of the “Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission”.

Disclaimer

This report was originally prepared and issued by MAHK for distribution to their professional, accredited and institutional investor customers. It is notdirected to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other

jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject MAHK and itssubsidiaries and affiliates (collectively MAHK Group) to any registration or licensing requirement within such jurisdictions. None of the material, nor itscontents, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express writtenpermission of MAHK Group. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks orservice marks of MAHK Group.

The information, opinion and material presented in this report are provided for general information purposes only and shall not be used or consideredas an offer or the solicitation of an offer to sell or to buy or subscribe for securities, other financial instruments or any derivative related to such

securities or instruments. MAHK Group may not have taken any steps to ensure that the securities referred to in this report are suitable for anyparticular investor. The contents of this report do not constitute investment advice to any person and such person shall not be treated as a customer of MAHK Group by virtue of receiving this report.

Information and opinions presented in this report have been obtained or derived from sources believed by MAHK Group to be reliable, but MAHK Groupmakes no representation or warranty, express or implied as to their accuracy, fairness or completeness and MAHK Group accepts no liability for anydirect or consequential loss arising from the use of the material presented in this report unless such liability arises under specific statutes or regulations.This report is not to be relied upon in substitution for the exercise of independent judgment. MAHK Group may have issued other reports that areinconsistent with, and reach different conclusions from, the information presented in this report. The reports reflect the different assumptions, viewsand analytical methods of the analysts who prepared them. For the avoidance of doubt, views expressed in this report do not necessarily representthose of MAHK Group and may not imply comparable future performance.

This report may provide the addresses of, or contain hyperlinks to, various websites. To the extent that this report refers to material outside MAHK Group’s own website, MAHK Group has not reviewed the linked sites and takes no responsibility for the content contained therein. Such address orhyperlink (including addresses or hyperlinks to MAHK Group own website material) is provided solely for your convenience and information and thecontent of the linked sites does not in any way form part of this report. Accessing such websites shall be at your own risk.

MAHK Group may, to the extent permitted by law, participate or invest in financing transactions with the issuer(s) of the securities referred to in thisreport, perform services for or solicit business from such issuers, and/or have a position or effect transactions in the securities or other financialinstruments thereon. MAHK Group may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the researchor analysis on which they are based, before the material is published. MAHK Group, its officers or directors and the analysts preparing this report (eachan Analyst and collectively the Analysts) may have relationships with, financial interests in or business relationships with any or all of the companiesmentioned in this report (each a listed corporation and collectively the listed corporations)

Information, opinions and estimates are provided on an “as in” basis without warranty of any kind and may be changed at any time without priornotice. There can be no assurance that future events or results will be consistent with any such opinion. Nothing in this report constitutes investment,legal, accounting or tax advice nor a representation that any investment or strategy is suitable or appropriate to your individual circumstances. Nothing

in this report constitutes a personal recommendation to you.

This report has been prepared by the research analyst(s) licensed by the Securities and Futures Commission in Hong Kong. The research analysts arenot employees or associated persons of any corporation mentioned in this report. These research analysts are not registered as research analysts withFINRA or the NYSE, but are licensed persons in compliance with Hong Kong regulatory requirements. Those research analysts may not be associatedpersons of Mirae USA and may not be subject to FINRA Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, publicappearances and trading securities held by a research analyst account. This report has been prepared by MAHK for distribution in Hong Kong; in Koreaby its holding company named Mirae Asset Securities Co. Ltd; in Vietnam by its joint venture company named Mirae Asset Securities (Vietnam) JointStock Company; in the United Kingdom by its subsidiary named Mirae Asset Securities (UK) Ltd; in the United States by its subsidiary named Mirae

Asset Securities (USA) Inc.This information may only be issued or passed on to any person in the United Kingdom if that person is of a kind described in Article 19 of the FinancialServices and Markets Act 2000 (Financial Promotions) Order 2001 or otherwise pursuant to exemptions to section 21 of the Financial Services andMarket Act 2000. In addition, no person who is an Authorised Person may issue or pass on this information, or otherwise promote MAHK Group, to anyperson in the United Kingdom other than under the rules of the Financial Services Authority (FSA) applicable to such Authorised Persons. This reportand any information, material and contents herein are intended for general circulation only and do not take into account the specific investmentobjectives, financial situation or particular needs or any particular person.

Any U.S. recipient of this report that would like further information regarding any security discussed herein should contact Mirae Asset Securities (USA)Inc. Furthermore, any recipient of this report that would like to effect any transaction in any security discussed herein should contact and place theorders with Mirae Asset Securities (USA) Inc. which, without in any way limiting the foregoing, accepts responsibility (solely for purposes of an withinthe meaning of Rule 15a-6 under the SEC Act of 1934) for this report and its dissemination in the United States.

Investments in general and, derivatives, in particular, involve numerous risks, including, inter alia, market risk, counterparty default risk and liquidityrisk. In some cases, securities and other financial instruments may be difficult to value or sell and reliable information about the value or risks related tothe security or financial instrument may be absent. The investment(s) mentioned in this report may not be suitable for all investors and a personreceiving or reading this report should seek advice from a financial adviser regarding the suitability of such investment(s), taking into account thespecific investment objectives, financial situation or particular needs of that person, before making a commitment to purchase any of such

investment(s). The suitability of any particular investment or strategy whether opined on, or referred to in this report or otherwise will depend on aperson’s individual circumstances and objectives and should be confirmed by such person with his advisers independently before adoption orimplementation thereof.

This document may not be taken or transmitted into or distributed in Japan, Canada or the People’s Republic of China.

Copyright 2009 MAHK Group. All rights reserved.