SCBA Annual Convention Charleston Place June 7-9, 2015 Successful Acquirers, Sellers & Independents Belief Strength Purpose

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SCBA Annual ConventionCharleston Place

June 7-9, 2015

Successful Acquirers, Sellers & Independents

Belief Strength Purpose

2

Disclosure StatementsThis presentation was prepared exclusively for the South Carolina Bankers Association Annual Convention (“SCBA Annual Convention”) and for the benefit and internal use of the SCBA Annual Convention attendees to whom it is directly addressed and delivered (including such attendee’s subsidiaries and affiliates, the “Attendees”) as an informational presentation and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by Banks Street Partners, LLC (“BSP”). Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of BSP.

The information in this presentation is based upon public information and industry research and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. BSP’s opinions and estimates constitute BSP’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or industry research sources. Furthermore, BSP shall have no liability to any party for any errors or omissions that may be contained in this presentations. In addition, our analyses are not and do not purport to be appraisals of the assets, stock or business of any company, financial institution or any other entity. BSP makes no representations as to the actual value which may be paid or received in connection with any investment or other transaction nor the legal, tax or accounting effects of consummating any investment or other transaction.

For any discussion or analysis contained in this presentation that pertains to public companies (including the Attendees, if they are public companies), please note that past performance of such companies and their securities is not necessarily a guide to future performance and no representation or warranty, express or implied, is made by BSP with respect to future performance. The price or value of the securities analyzed, either directly or indirectly, may fall or rise against the interest of investors. Any recommendation or opinion contained in this report may become outdated as a consequence of changes in the environment in which the issuer of the securities under analysis operates, in addition to changes in the estimates and forecasts, assumptions and valuation methodology used herein.

IRS Circular 230 Disclosure: BSP and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with BSP of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This presentation is not to be considered a solicitation to buy or sell any securities and does not constitute a commitment by any BSP entity to underwrite, subscribe for or place any securities or to arrange credit or to provide any other services.

3

Banks Street Partners ProfessionalsSeasoned professionals with more than 140 years of combined experience and more than 500 transactions in the financial services industry

Lee BurrowsChief Executive [email protected]

Mark SaundersManaging [email protected]

Jeff AdamsManaging [email protected]

Will BrackettSenior Vice President [email protected]

Gary McNorrillCOO & Managing [email protected]

Joe MaloneySenior Vice President/[email protected]

William IzlarAnalyst [email protected]

Berkeley [email protected]

Nicole MansfieldChief Marketing Officer [email protected]

ATLANTA CHARLOTTE

Matt [email protected]

4

Banks Street Partners Recent M&A Deals

Has Merged With

December 2014

Has Agreed to Merge With

Pending

Harbor Bank Group, Inc.

Bank Holding Company of:

September 2014

Pending

Alarion Financial Services Inc.

Bank Holding Company of:

Has Merged With

Has Agreed to Merge With

Valley Financial Corporation

Bank Holding Company of:

July 2014

June 2015

Has Merged With

Has Agreed to Merge With

Georgia Commerce Bancshares, Inc.

Bank Holding Company of:

Community & SouthernHoldings, Inc.

Bank Holding Company of:

May 2015

Has Been Acquired By

Highland Financial Services, Inc.

Bank Holding Company of:

Has Agreed to be Acquired By

Pending

5

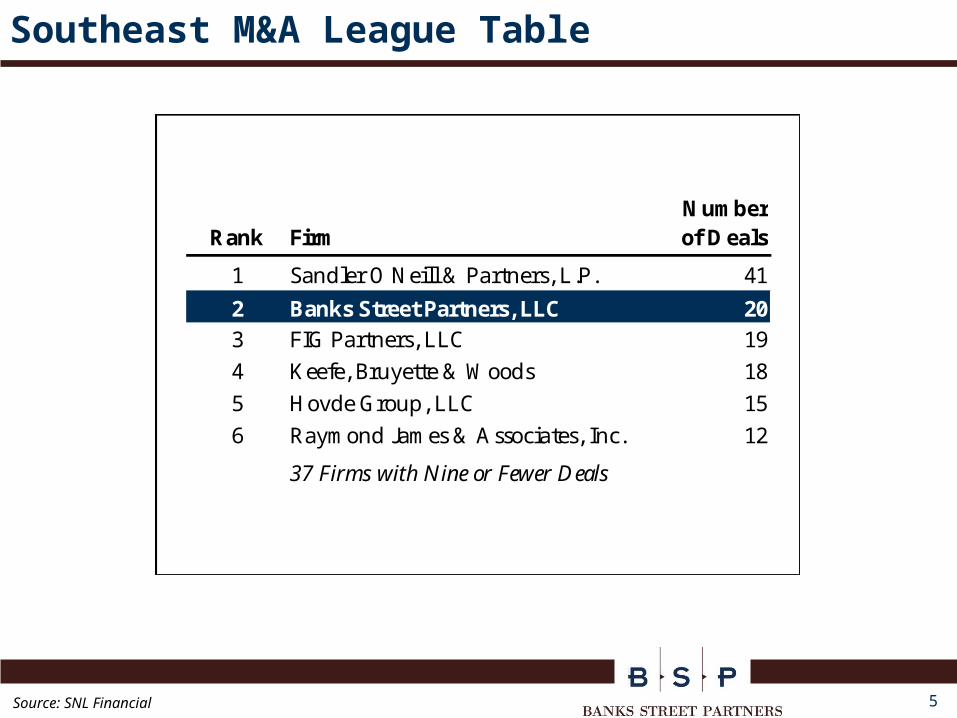

Southeast M&A League Table

Source: SNL Financial

Rank FirmNumber of Deals

1 Sandler O'Neill & Partners, L.P. 41

2 Banks Street Partners, LLC 203 FIG Partners, LLC 19

4 Keefe, Bruyette & Woods 18

5 Hovde Group, LLC 15

6 Raymond James & Associates, Inc. 12

37 Firms with Nine or Fewer Deals

Whole Bank, Branch and FDIC-assisted transactions announced between Jan. 1, 2013 and June, 1 2015 with the target located in either AL, FL, GA, NC, SC or TN

6

Table of Contents

TOPIC PAGE

M&A Market Update 7

Successful Bank Acquirers 12

Successful Sellers 25

Remaining Independent 31

M&A Market Update

8

-

5

10

15

20

25

30

-

50

100

150

200

250

300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median Deal Value/ TCE (%) Median Deal Value/ Earnings (x)

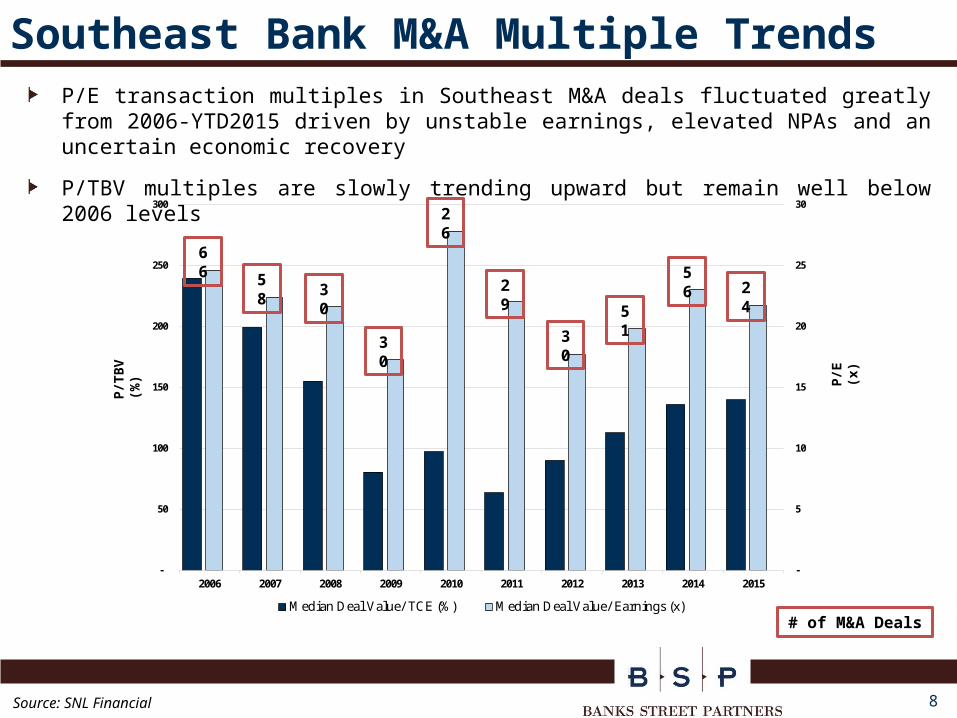

Southeast Bank M&A Multiple TrendsP/E transaction multiples in Southeast M&A deals fluctuated greatly from 2006-YTD2015 driven by unstable earnings, elevated NPAs and an uncertain economic recovery

P/TBV multiples are slowly trending upward but remain well below 2006 levels

66

# of M&A Deals

58 3

0

30

26

29

30

51

56 2

4

Source: SNL Financial

P/T

BV

(%

) P/E

(x

)

9

-

5

10

15

20

25

30

35

40

45

40

60

80

100

120

140

160

National Southeast Mid-Atlantic Northeast Midwest Southwest West

LTM Transaction Multiples by Region

P/TBV P/E

-

5

10

15

20

25

30

35

40

45

40

60

80

100

120

140

160

180

LTM Transaction Multiples by State

P/TBV P/E

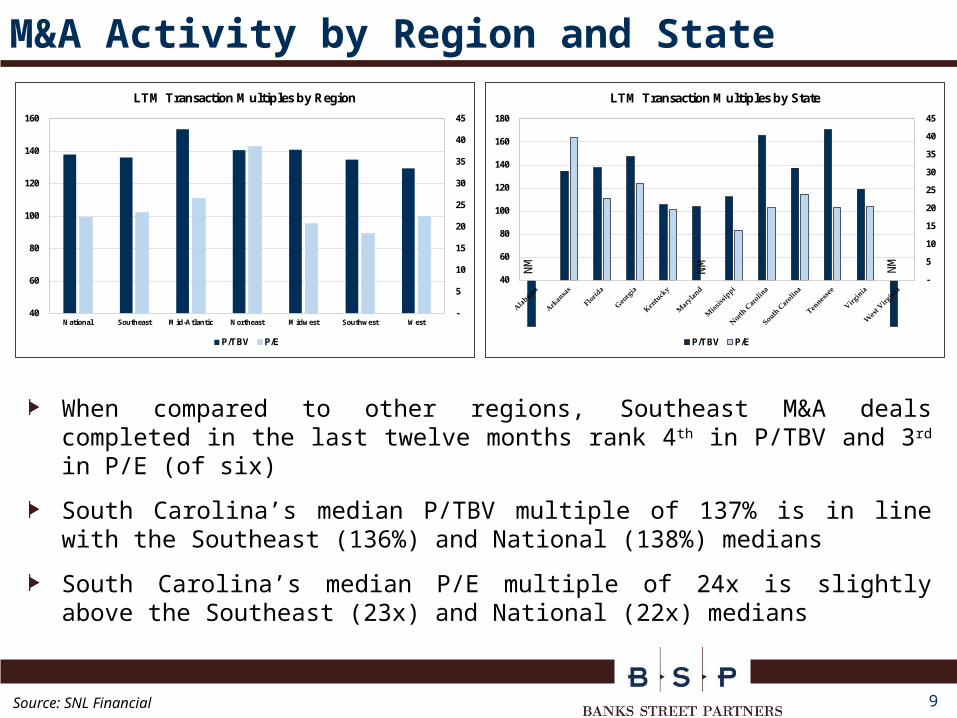

M&A Activity by Region and State

When compared to other regions, Southeast M&A deals completed in the last twelve months rank 4th in P/TBV and 3rd in P/E (of six)

South Carolina’s median P/TBV multiple of 137% is in line with the Southeast (136%) and National (138%) medians

South Carolina’s median P/E multiple of 24x is slightly above the Southeast (23x) and National (22x) medians

N M N M N M

Source: SNL Financial

10

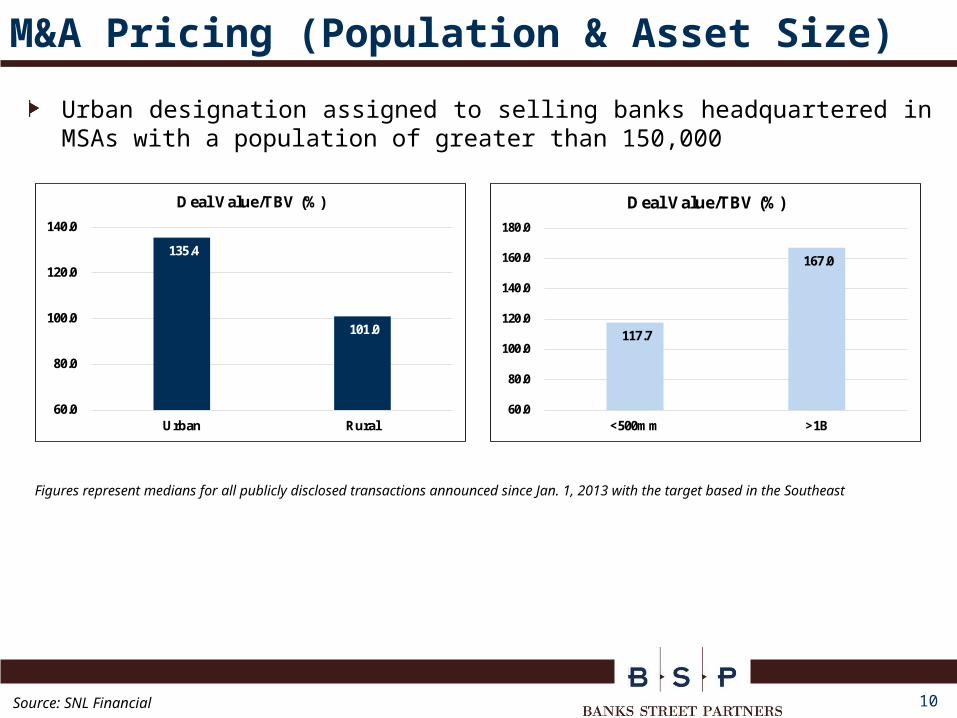

M&A Pricing (Population & Asset Size)

Urban designation assigned to selling banks headquartered in MSAs with a population of greater than 150,000

Figures represent medians for all publicly disclosed transactions announced since Jan. 1, 2013 with the target based in the Southeast

135.4

101.0

60.0

80.0

100.0

120.0

140.0

Urban Rural

Deal Value/TBV (%)

Source: SNL Financial

117.7

167.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

<500mm >1B

Deal Value/TBV (%)

11

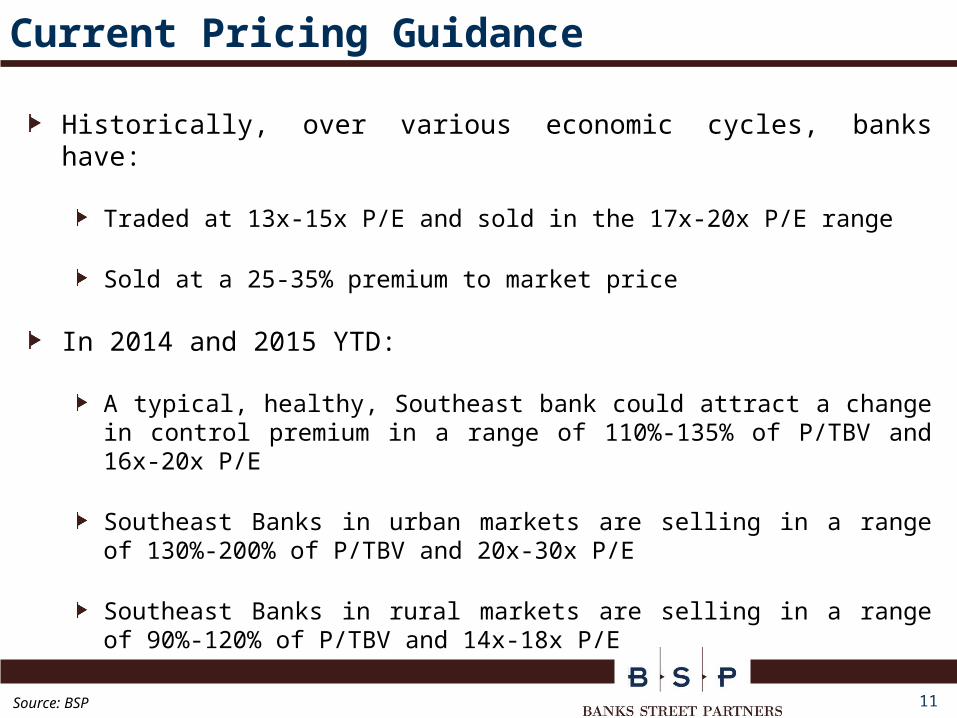

Current Pricing Guidance

Historically, over various economic cycles, banks have:

Traded at 13x-15x P/E and sold in the 17x-20x P/E range

Sold at a 25-35% premium to market price

In 2014 and 2015 YTD:

A typical, healthy, Southeast bank could attract a change in control premium in a range of 110%-135% of P/TBV and 16x-20x P/E

Southeast Banks in urban markets are selling in a range of 130%-200% of P/TBV and 20x-30x P/E

Southeast Banks in rural markets are selling in a range of 90%-120% of P/TBV and 14x-18x P/E

Source: BSP

Successful Bank Acquirers

13

Is There a Difference?

Source: The New Yorker

14

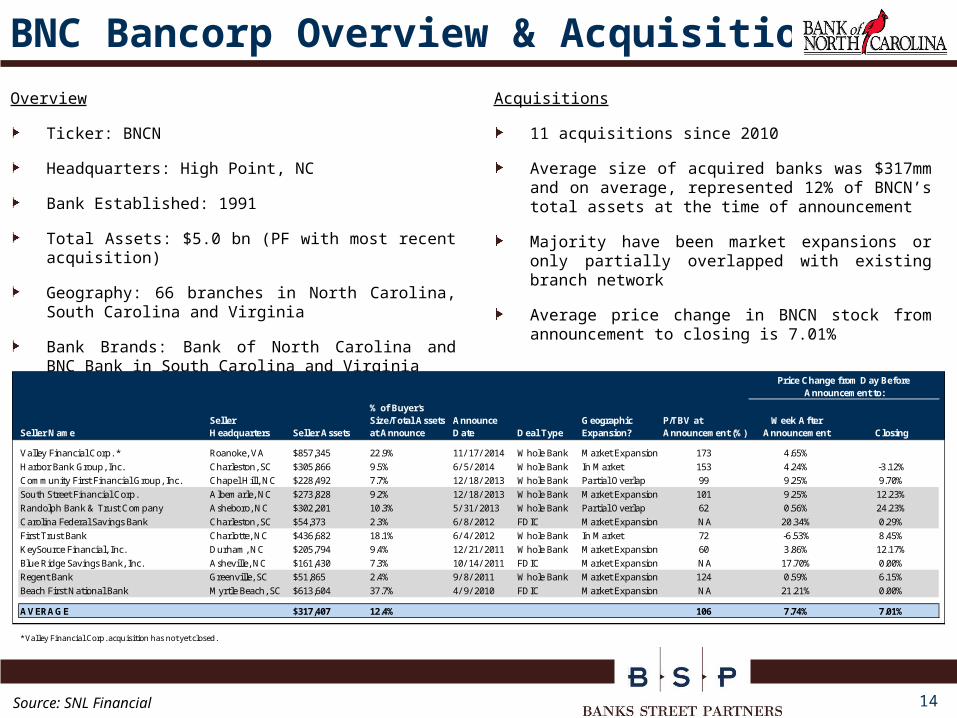

BNC Bancorp Overview & AcquisitionsAcquisitions

11 acquisitions since 2010

Average size of acquired banks was $317mm and on average, represented 12% of BNCN’s total assets at the time of announcement

Majority have been market expansions or only partially overlapped with existing branch network

Average price change in BNCN stock from announcement to closing is 7.01%

Overview

Ticker: BNCN

Headquarters: High Point, NC

Bank Established: 1991

Total Assets: $5.0 bn (PF with most recent acquisition)

Geography: 66 branches in North Carolina, South Carolina and Virginia

Bank Brands: Bank of North Carolina and BNC Bank in South Carolina and Virginia

Source: SNL Financial

Seller NameSeller Headquarters Seller Assets

% of Buyer's Size/Total Assets at Announce

Announce Date Deal Type

Geographic Expansion?

P/TBV at Announcement (%)

Week After Announcement Closing

Valley Financial Corp. * Roanoke, VA $857,345 22.9% 11/ 17/ 2014 Whole Bank Market Expansion 173 4.65%

Harbor Bank Group, Inc. Charleston, SC $305,866 9.5% 6/ 5/ 2014 Whole Bank In Market 153 4.24% -3.12%

Community First Financial Group, Inc. Chapel Hill, NC $228,492 7.7% 12/ 18/ 2013 Whole Bank Partial Overlap 99 9.25% 9.70%

South Street Financial Corp. Albemarle, NC $273,828 9.2% 12/ 18/ 2013 Whole Bank Market Expansion 101 9.25% 12.23%

Randolph Bank & Trust Company Asheboro, NC $302,201 10.3% 5/ 31/ 2013 Whole Bank Partial Overlap 62 0.56% 24.23%

Carolina Federal Savings Bank Charleston, SC $54,373 2.3% 6/ 8/ 2012 FDIC Market Expansion NA 20.34% 0.29%

First Trust Bank Charlotte, NC $436,682 18.1% 6/ 4/ 2012 Whole Bank In Market 72 -6.53% 8.45%

KeySource Financial, Inc. Durham, NC $205,794 9.4% 12/ 21/ 2011 Whole Bank Market Expansion 60 3.86% 12.17%

Blue Ridge Savings Bank, Inc. Asheville, NC $161,430 7.3% 10/ 14/ 2011 FDIC Market Expansion NA 17.70% 0.00%

Regent Bank Greenville, SC $51,865 2.4% 9/ 8/ 2011 Whole Bank Market Expansion 124 0.59% 6.15%

Beach First National Bank Myrtle Beach, SC $613,604 37.7% 4/ 9/ 2010 FDIC Market Expansion NA 21.21% 0.00%

AVERAGE $317,407 12.4% 106 7.74% 7.01%

* Valley Financial Corp. acquisition has not yet closed.

Price Change from Day Before Announcement to:

15

BNC Bancorp Acquisition Map

• Legacy BNCN

• Beach First

• Regent Bank

• Blue Ridge Savings Bank

• KeySource

• First Trust

• Carolina Federal

• Randolph Bank & Trust

• South Street

• Community First

• Harbor

• Valley Financial

• Hampton Roads*

• Certus*

*Branch Acquisition

Sources: SNL Financial, ESRI

16

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

$20.00

Dec

-08

Mar

-09

Jun-0

9

Sep

-09

Dec

-09

Mar

-10

Jun-1

0

Sep

-10

Dec

-10

Mar

-11

Jun-1

1

Sep

-11

Dec

-11

Mar

-12

Jun-1

2

Sep

-12

Dec

-12

Mar

-13

Jun-1

3

Sep

-13

Dec

-13

Mar

-14

Jun-1

4

Sep

-14

Dec

-14

Mar

-15

BNCN Stock Price Trend, 2009 - Today

Harbor National Bank

Harrington Bank &Home Savings Bank

Whole Bank Acquisitions FDIC-Assisted Acquisitions

Randolph Bank & TrustFirst Trust

Bank

KeySource Bank

Regent Bank

Carolina Federal Savings Bank

Blue Ridge Savings Bank

Beach First National Bank

Source: SNL Financial

Valley Bank

17

BNC Bancorp Key Strengths

Took advantage of the financial upside associated with FDIC-assisted deals

Able to acquire even when their stock was trading at a discount to book value

All but 3 whole bank transactions were priced at or below book value at time of announcement

Strong corporate culture

Take care of management teams

Currency caught up to culture and M&A expertise

All but two transactions negotiated without auction process

Source: BSP

18

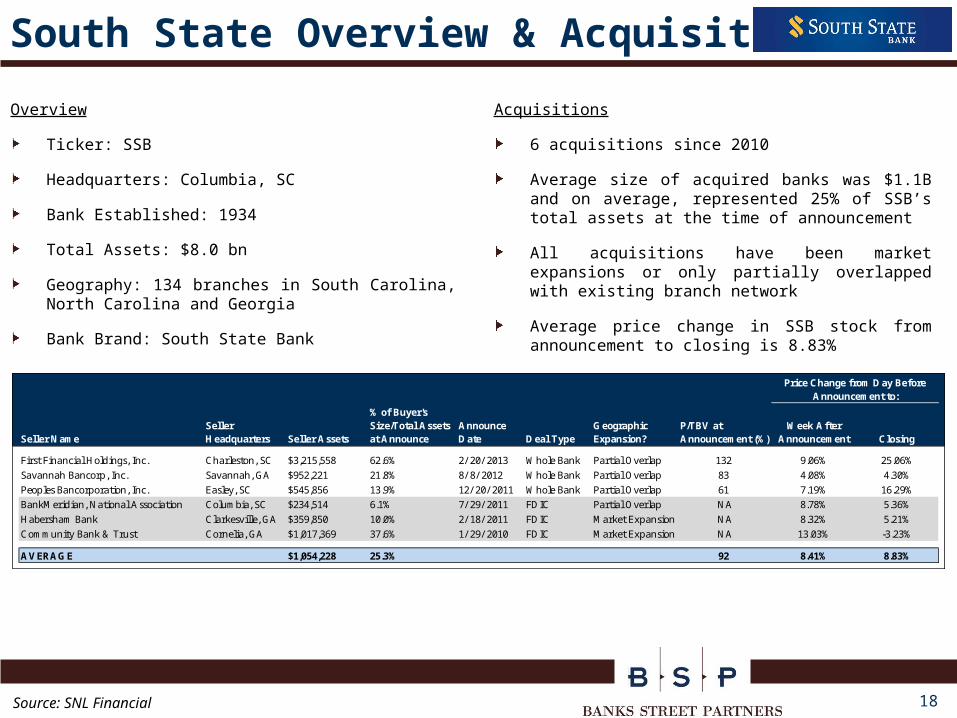

South State Overview & Acquisitions

Acquisitions

6 acquisitions since 2010

Average size of acquired banks was $1.1B and on average, represented 25% of SSB’s total assets at the time of announcement

All acquisitions have been market expansions or only partially overlapped with existing branch network

Average price change in SSB stock from announcement to closing is 8.83%

Overview

Ticker: SSB

Headquarters: Columbia, SC

Bank Established: 1934

Total Assets: $8.0 bn

Geography: 134 branches in South Carolina, North Carolina and Georgia

Bank Brand: South State Bank

Source: SNL Financial

Seller NameSeller Headquarters Seller Assets

% of Buyer's Size/Total Assets at Announce

Announce Date Deal Type

Geographic Expansion?

P/TBV at Announcement (%)

Week After Announcement Closing

First Financial Holdings, Inc. Charleston, SC $3,215,558 62.6% 2/ 20/ 2013 Whole Bank Partial Overlap 132 9.06% 25.06%

Savannah Bancorp, Inc. Savannah, GA $952,221 21.8% 8/ 8/ 2012 Whole Bank Partial Overlap 83 4.08% 4.30%

Peoples Bancorporation, Inc. Easley, SC $545,856 13.9% 12/ 20/ 2011 Whole Bank Partial Overlap 61 7.19% 16.29%

BankMeridian, National Association Columbia, SC $234,514 6.1% 7/ 29/ 2011 FDIC Partial Overlap NA 8.78% 5.36%

Habersham Bank Clarkesville, GA $359,850 10.0% 2/ 18/ 2011 FDIC Market Expansion NA 8.32% 5.21%

Community Bank & Trust Cornelia, GA $1,017,369 37.6% 1/ 29/ 2010 FDIC Market Expansion NA 13.03% -3.23%

AVERAGE $1,054,228 25.3% 92 8.41% 8.83%

Price Change from Day Before Announcement to:

19

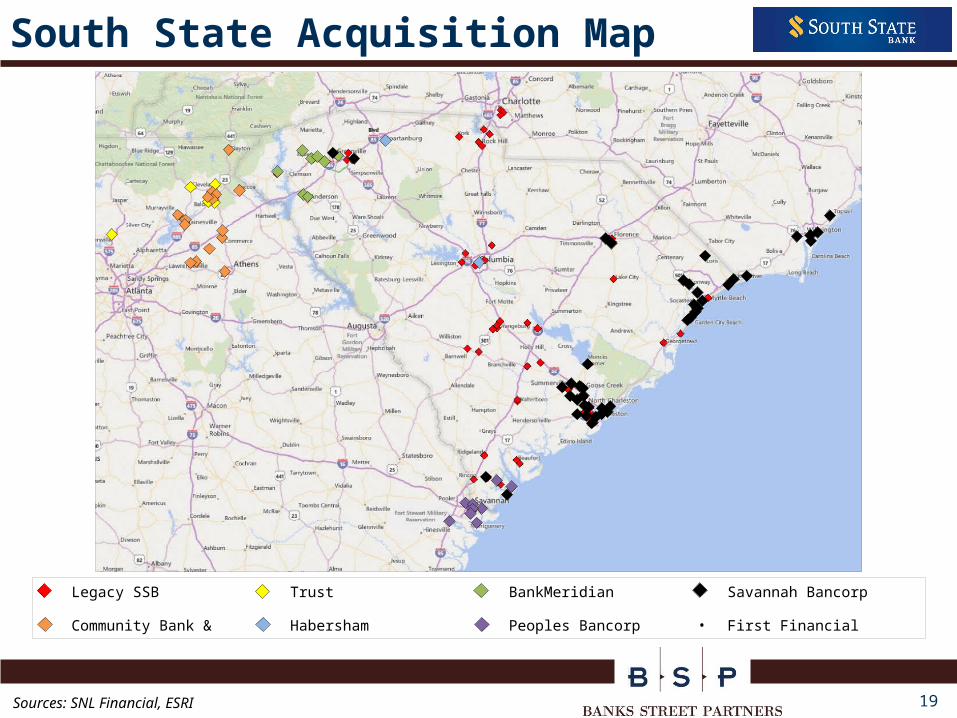

South State Acquisition Map

• Legacy SSB

• Community Bank & Trust

• Habersham

• BankMeridian

• Peoples Bancorp

• Savannah Bancorp

• First Financial

Sources: SNL Financial, ESRI

20

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

Dec

-08

Mar

-09

Jun-0

9

Sep

-09

Dec

-09

Mar

-10

Jun-1

0

Sep

-10

Dec

-10

Mar

-11

Jun-1

1

Sep

-11

Dec

-11

Mar

-12

Jun-1

2

Sep

-12

Dec

-12

Mar

-13

Jun-1

3

Sep

-13

Dec

-13

Mar

-14

Jun-1

4

Sep

-14

Dec

-14

Mar

-15

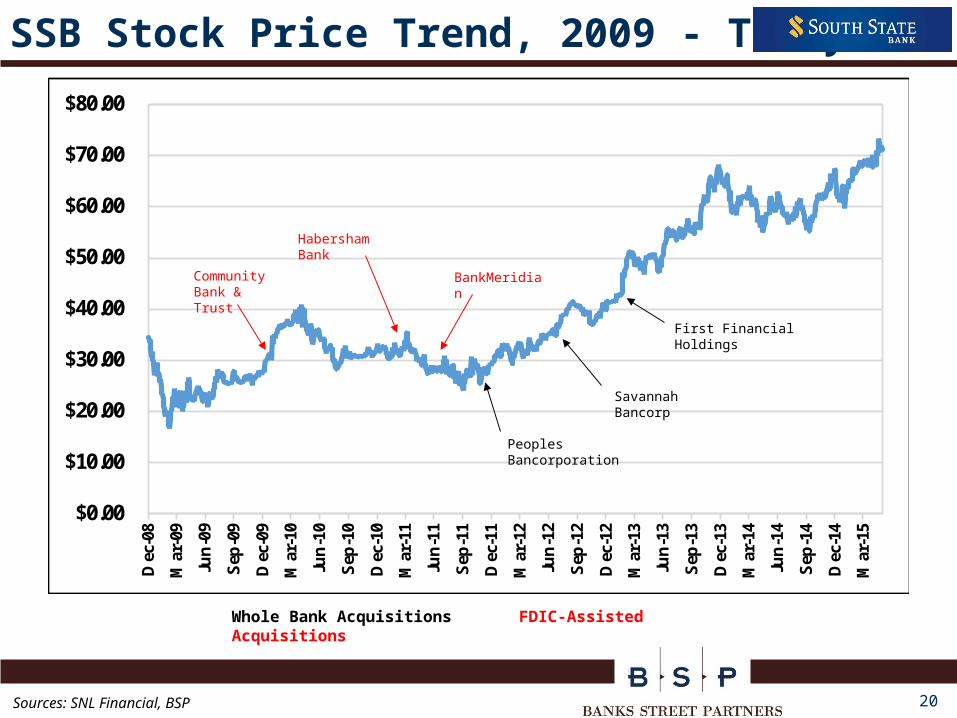

SSB Stock Price Trend, 2009 - Today

Whole Bank Acquisitions FDIC-Assisted Acquisitions

First Financial Holdings

Savannah Bancorp

Peoples Bancorporation

BankMeridian

Habersham Bank

Community Bank & Trust

Sources: SNL Financial, BSP

21

South State Key Strengths

Focused on distressed or underperforming banks

Acquired larger targets ($1B average size) who had substantial or dominant market share

All whole bank transactions but 1 were priced at a discount to book value

Largest community bank in South Carolina and adjoining states

Strong currency

Source: BSP

22

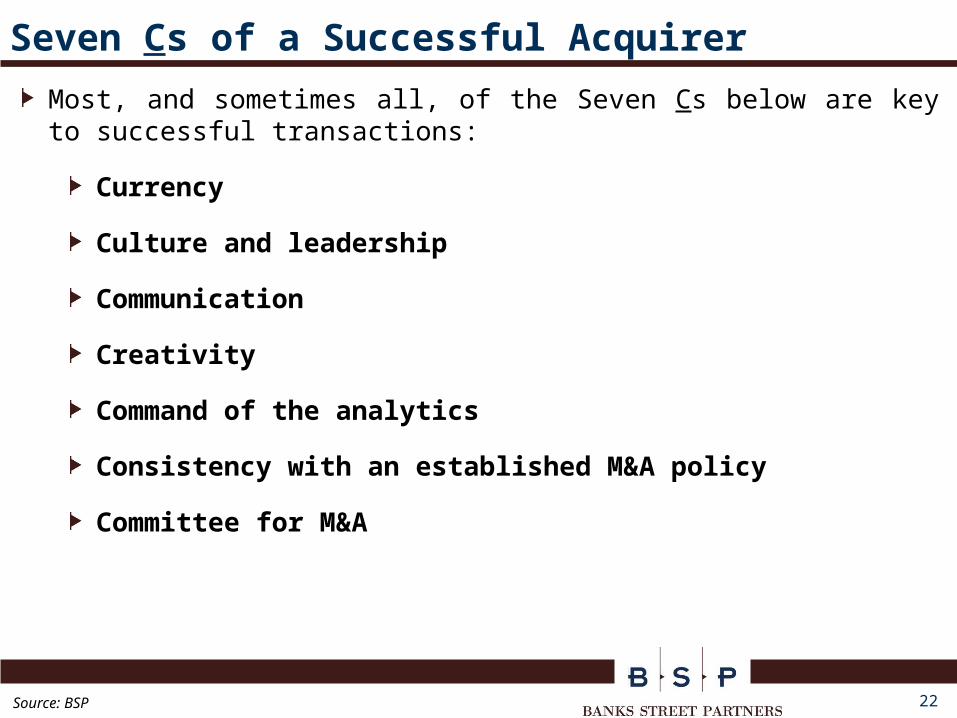

Seven Cs of a Successful Acquirer

Most, and sometimes all, of the Seven Cs below are key to successful transactions:

Currency

Culture and leadership

Communication

Creativity

Command of the analytics

Consistency with an established M&A policy

Committee for M&A

Source: BSP

23

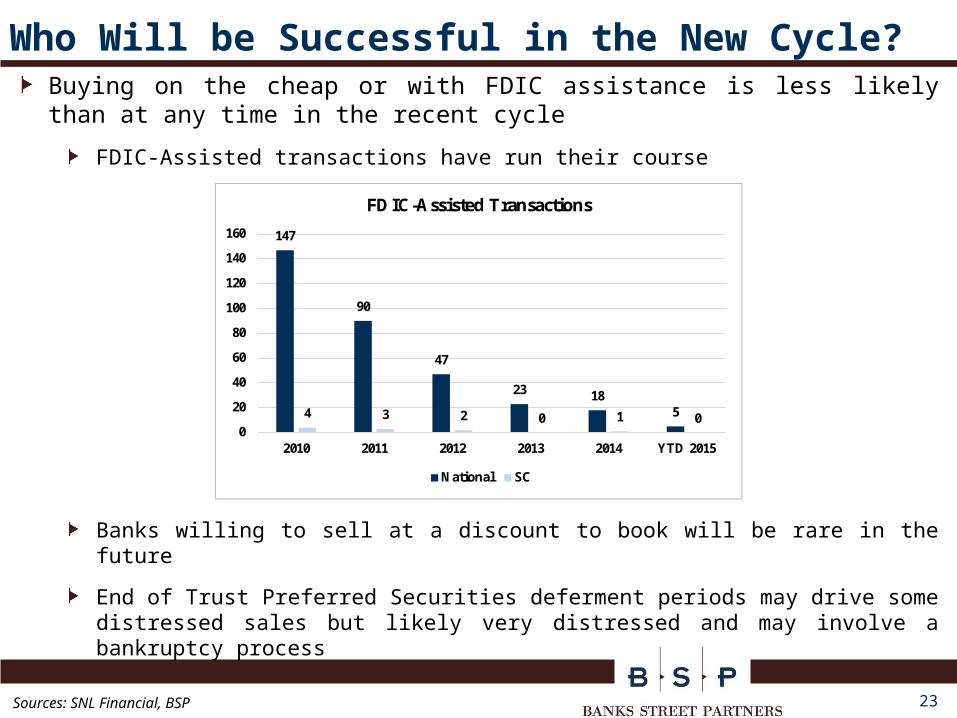

Who Will be Successful in the New Cycle?Buying on the cheap or with FDIC assistance is less likely than at any time in the recent cycle

FDIC-Assisted transactions have run their course

Banks willing to sell at a discount to book will be rare in the future

End of Trust Preferred Securities deferment periods may drive some distressed sales but likely very distressed and may involve a bankruptcy process

Sources: SNL Financial, BSP

147

90

47

23 1854 3 2 0 1 0

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 YTD 2015

FDIC-Assisted Transactions

National SC

24

Who Will be Successful in the New Cycle? (cont.)

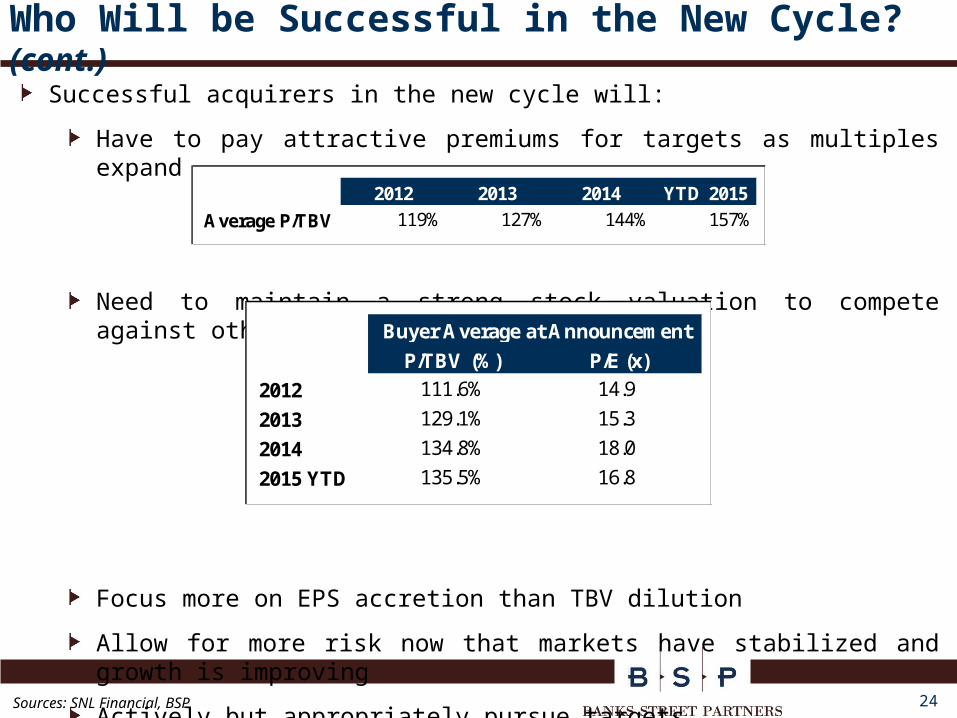

Successful acquirers in the new cycle will:

Have to pay attractive premiums for targets as multiples expand

Need to maintain a strong stock valuation to compete against other acquirers

Focus more on EPS accretion than TBV dilution

Allow for more risk now that markets have stabilized and growth is improving

Actively but appropriately pursue targetsSources: SNL Financial, BSP

2012 2013 2014 YTD 2015

Average P/TBV 119% 127% 144% 157%

P/TBV (%) P/E (x)

2012 111.6% 14.9

2013 129.1% 15.3

2014 134.8% 18.0

2015 YTD 135.5% 16.8

Buyer Average at Announcement

Successful Sellers

26

Finding the Right Partner is Key

Source: The New Yorker

27

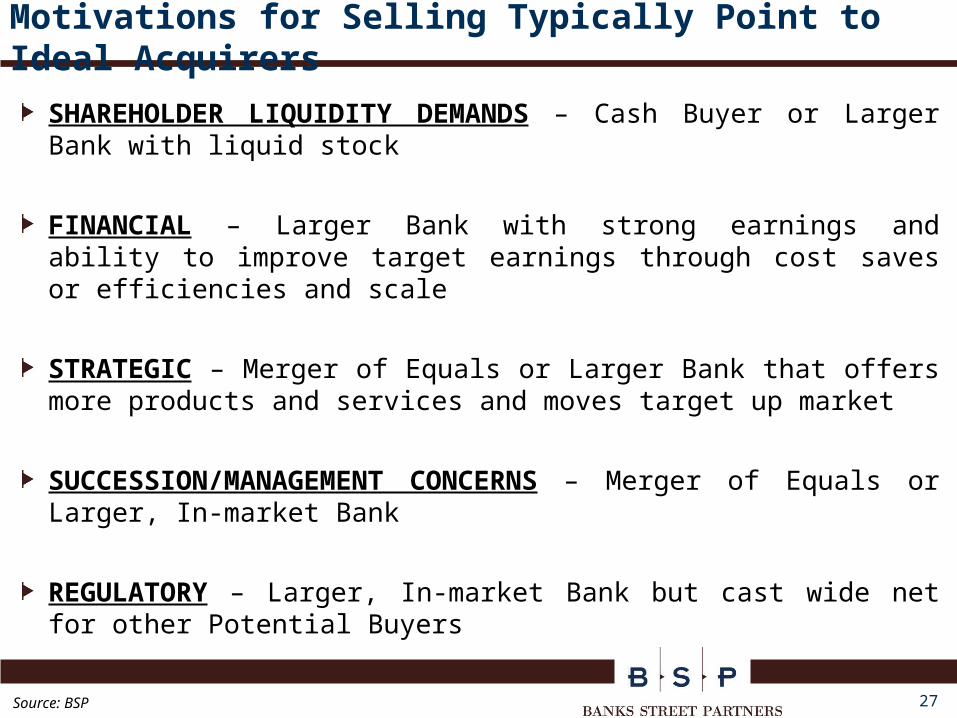

Motivations for Selling Typically Point to Ideal Acquirers

SHAREHOLDER LIQUIDITY DEMANDS – Cash Buyer or Larger Bank with liquid stock

FINANCIAL – Larger Bank with strong earnings and ability to improve target earnings through cost saves or efficiencies and scale

STRATEGIC – Merger of Equals or Larger Bank that offers more products and services and moves target up market

SUCCESSION/MANAGEMENT CONCERNS – Merger of Equals or Larger, In-market Bank

REGULATORY – Larger, In-market Bank but cast wide net for other Potential Buyers

Source: BSP

28

0

20

40

60

80

100

120

140

160

180

200

Tot

al R

eturn

(%

)

Total Return Since Announcement

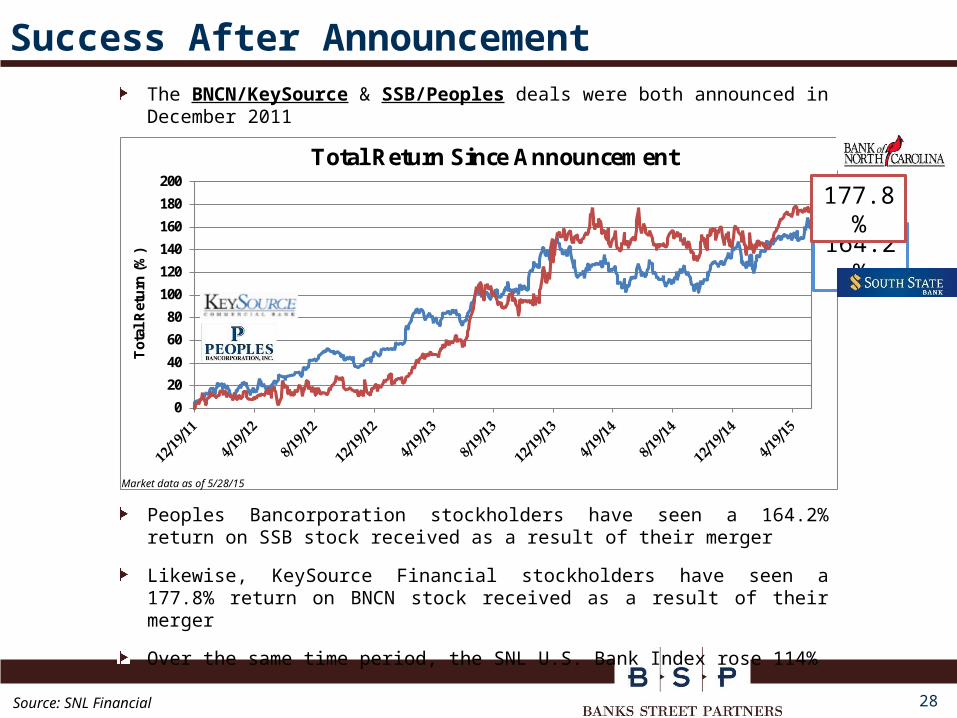

Success After Announcement

Peoples Bancorporation stockholders have seen a 164.2% return on SSB stock received as a result of their merger

Likewise, KeySource Financial stockholders have seen a 177.8% return on BNCN stock received as a result of their merger

Over the same time period, the SNL U.S. Bank Index rose 114%

Market data as of 5/28/15

164.2%

177.8%

The BNCN/KeySource & SSB/Peoples deals were both announced in December 2011

Source: SNL Financial

29

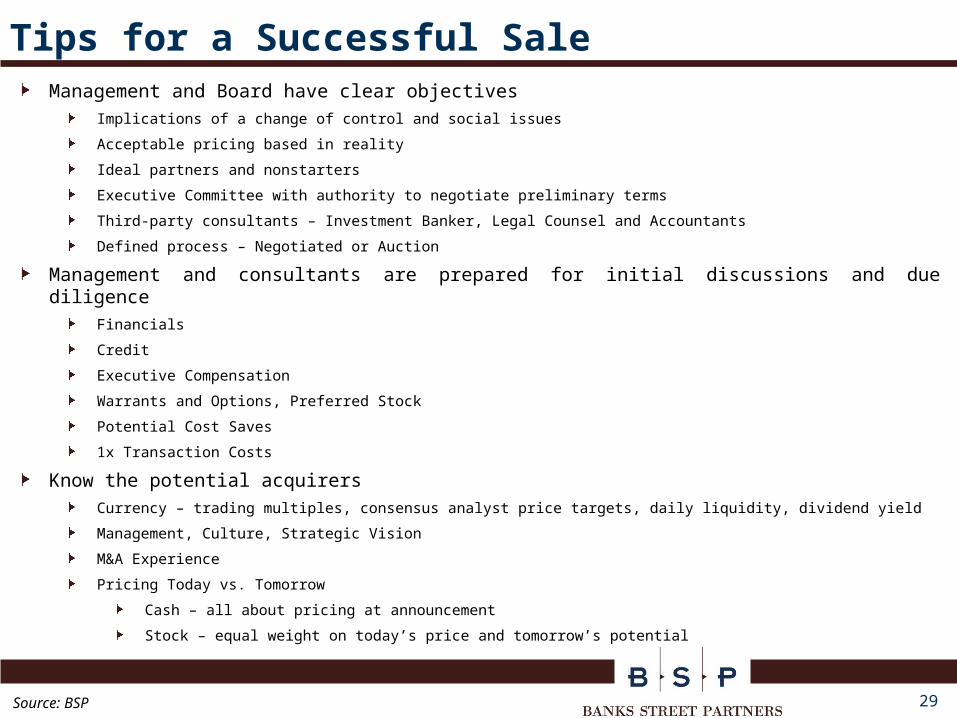

Tips for a Successful SaleManagement and Board have clear objectives

Implications of a change of control and social issues

Acceptable pricing based in reality

Ideal partners and nonstarters

Executive Committee with authority to negotiate preliminary terms

Third-party consultants – Investment Banker, Legal Counsel and Accountants

Defined process – Negotiated or Auction

Management and consultants are prepared for initial discussions and due diligenceFinancials

Credit

Executive Compensation

Warrants and Options, Preferred Stock

Potential Cost Saves

1x Transaction Costs

Know the potential acquirersCurrency – trading multiples, consensus analyst price targets, daily liquidity, dividend yield

Management, Culture, Strategic Vision

M&A Experience

Pricing Today vs. Tomorrow

Cash – all about pricing at announcement

Stock – equal weight on today’s price and tomorrow’s potential

Source: BSP

30

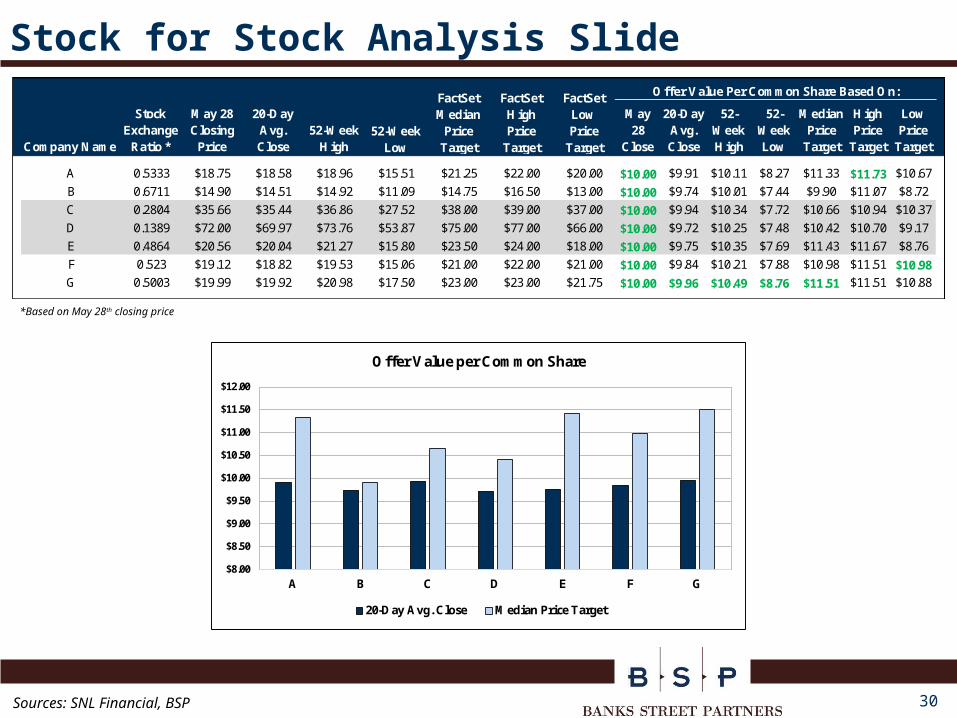

Stock for Stock Analysis Slide

*Based on May 28th closing price

Sources: SNL Financial, BSP

Company Name

Stock Exchange Ratio *

May 28 Closing Price

20-Day Avg. Close

52-Week High

May 28

Close

20-Day Avg. Close

52-Week High

52-Week Low

Median Price Target

High Price Target

Low Price Target

A 0.5333 $18.75 $18.58 $18.96 $15.51 $21.25 $22.00 $20.00 $10.00 $9.91 $10.11 $8.27 $11.33 $11.73 $10.67

B 0.6711 $14.90 $14.51 $14.92 $11.09 $14.75 $16.50 $13.00 $10.00 $9.74 $10.01 $7.44 $9.90 $11.07 $8.72

C 0.2804 $35.66 $35.44 $36.86 $27.52 $38.00 $39.00 $37.00 $10.00 $9.94 $10.34 $7.72 $10.66 $10.94 $10.37

D 0.1389 $72.00 $69.97 $73.76 $53.87 $75.00 $77.00 $66.00 $10.00 $9.72 $10.25 $7.48 $10.42 $10.70 $9.17

E 0.4864 $20.56 $20.04 $21.27 $15.80 $23.50 $24.00 $18.00 $10.00 $9.75 $10.35 $7.69 $11.43 $11.67 $8.76

F 0.523 $19.12 $18.82 $19.53 $15.06 $21.00 $22.00 $21.00 $10.00 $9.84 $10.21 $7.88 $10.98 $11.51 $10.98G 0.5003 $19.99 $19.92 $20.98 $17.50 $23.00 $23.00 $21.75 $10.00 $9.96 $10.49 $8.76 $11.51 $11.51 $10.88

FactSet Median Price Target

FactSet High Price Target

FactSet Low Price Target

Offer Value Per Common Share Based On:

52-Week Low

$8.00

$8.50

$9.00

$9.50

$10.00

$10.50

$11.00

$11.50

$12.00

A B C D E F G

Offer Value per Common Share

20-Day Avg. Close Median Price Target

Remaining Independent

32

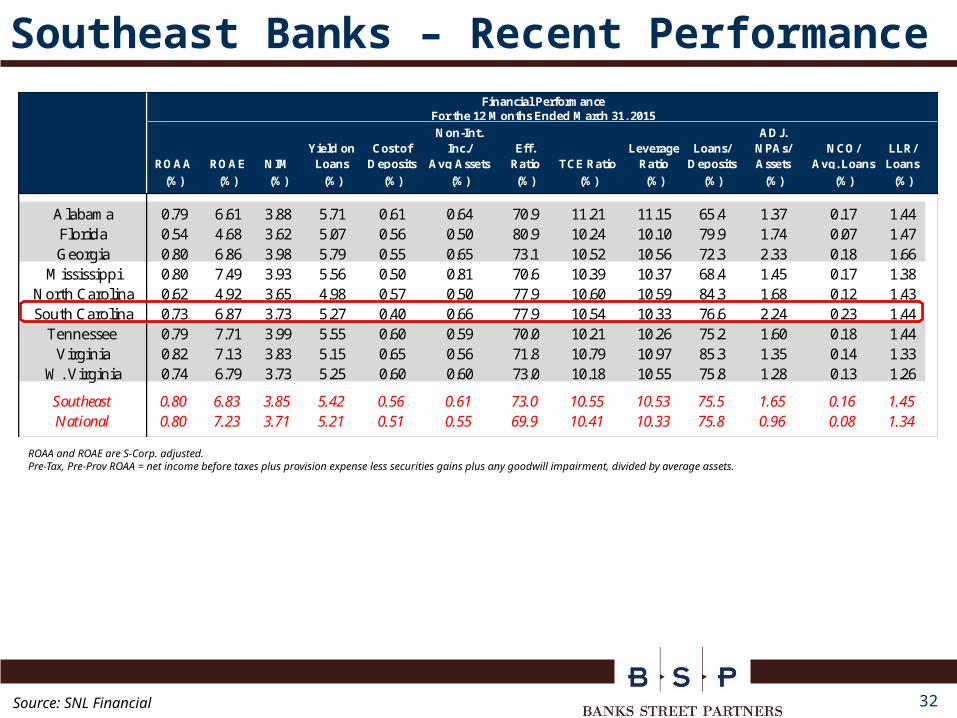

Southeast Banks – Recent Performance

ROAA and ROAE are S-Corp. adjusted.Pre-Tax, Pre-Prov ROAA = net income before taxes plus provision expense less securities gains plus any goodwill impairment, divided by average assets.

Source: SNL Financial

ROAA ROAE NIMYield on Loans

Cost of Deposits

Non-Int. Inc./

Avg AssetsEff.

Ratio TCE Ratio Leverage

RatioLoans/

Deposits

ADJ. NPAs/Assets

NCO/Avg. Loans

LLR/Loans

(%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%)

Alabama 0.79 6.61 3.88 5.71 0.61 0.64 70.9 11.21 11.15 65.4 1.37 0.17 1.44Florida 0.54 4.68 3.62 5.07 0.56 0.50 80.9 10.24 10.10 79.9 1.74 0.07 1.47Georgia 0.80 6.86 3.98 5.79 0.55 0.65 73.1 10.52 10.56 72.3 2.33 0.18 1.66

Mississippi 0.80 7.49 3.93 5.56 0.50 0.81 70.6 10.39 10.37 68.4 1.45 0.17 1.38North Carolina 0.62 4.92 3.65 4.98 0.57 0.50 77.9 10.60 10.59 84.3 1.68 0.12 1.43South Carolina 0.73 6.87 3.73 5.27 0.40 0.66 77.9 10.54 10.33 76.6 2.24 0.23 1.44

Tennessee 0.79 7.71 3.99 5.55 0.60 0.59 70.0 10.21 10.26 75.2 1.60 0.18 1.44Virginia 0.82 7.13 3.83 5.15 0.65 0.56 71.8 10.79 10.97 85.3 1.35 0.14 1.33

W. Virginia 0.74 6.79 3.73 5.25 0.60 0.60 73.0 10.18 10.55 75.8 1.28 0.13 1.26

Southeast 0.80 6.83 3.85 5.42 0.56 0.61 73.0 10.55 10.53 75.5 1.65 0.16 1.45National 0.80 7.23 3.71 5.21 0.51 0.55 69.9 10.41 10.33 75.8 0.96 0.08 1.34

Financial PerformanceFor the 12 Months Ended March 31, 2015

33

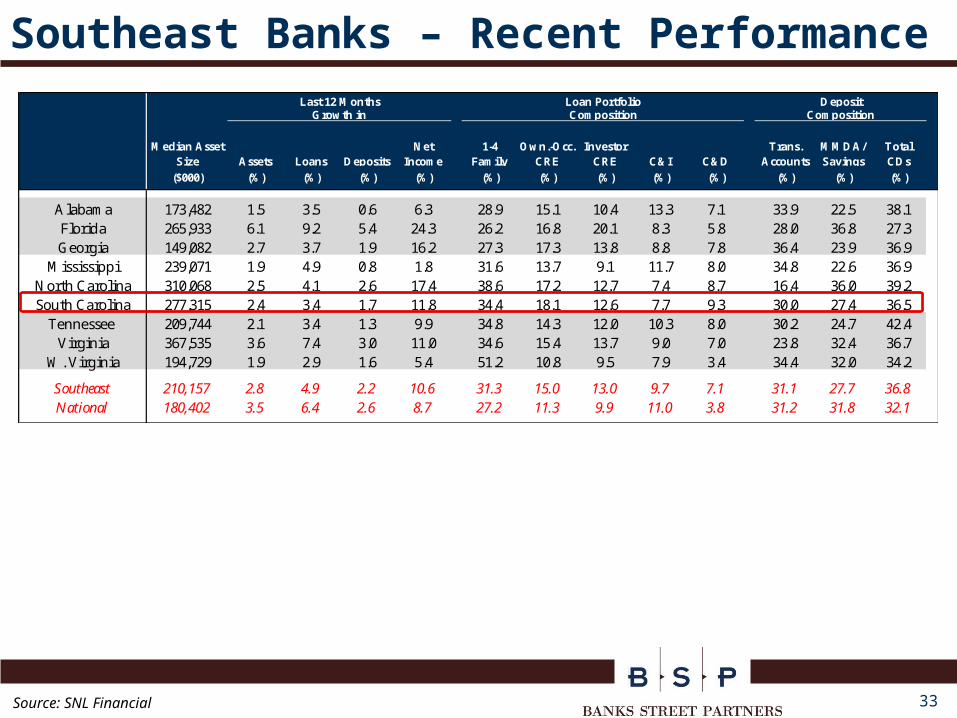

Southeast Banks – Recent Performance

Source: SNL Financial

Median Asset Size Assets Loans Deposits

Net Income

1-4 Family

Own.-Occ. CRE

Investor CRE C&I C&D

Trans. Accounts

MMDA/Savings

Total CDs

($000) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%)

Alabama 173,482 1.5 3.5 0.6 6.3 28.9 15.1 10.4 13.3 7.1 33.9 22.5 38.1Florida 265,933 6.1 9.2 5.4 24.3 26.2 16.8 20.1 8.3 5.8 28.0 36.8 27.3Georgia 149,082 2.7 3.7 1.9 16.2 27.3 17.3 13.8 8.8 7.8 36.4 23.9 36.9

Mississippi 239,071 1.9 4.9 0.8 1.8 31.6 13.7 9.1 11.7 8.0 34.8 22.6 36.9North Carolina 310,068 2.5 4.1 2.6 17.4 38.6 17.2 12.7 7.4 8.7 16.4 36.0 39.2South Carolina 277,315 2.4 3.4 1.7 11.8 34.4 18.1 12.6 7.7 9.3 30.0 27.4 36.5

Tennessee 209,744 2.1 3.4 1.3 9.9 34.8 14.3 12.0 10.3 8.0 30.2 24.7 42.4Virginia 367,535 3.6 7.4 3.0 11.0 34.6 15.4 13.7 9.0 7.0 23.8 32.4 36.7

W. Virginia 194,729 1.9 2.9 1.6 5.4 51.2 10.8 9.5 7.9 3.4 34.4 32.0 34.2

Southeast 210,157 2.8 4.9 2.2 10.6 31.3 15.0 13.0 9.7 7.1 31.1 27.7 36.8National 180,402 3.5 6.4 2.6 8.7 27.2 11.3 9.9 11.0 3.8 31.2 31.8 32.1

Last 12 Months Loan Portfolio DepositGrowth in Composition Composition

34

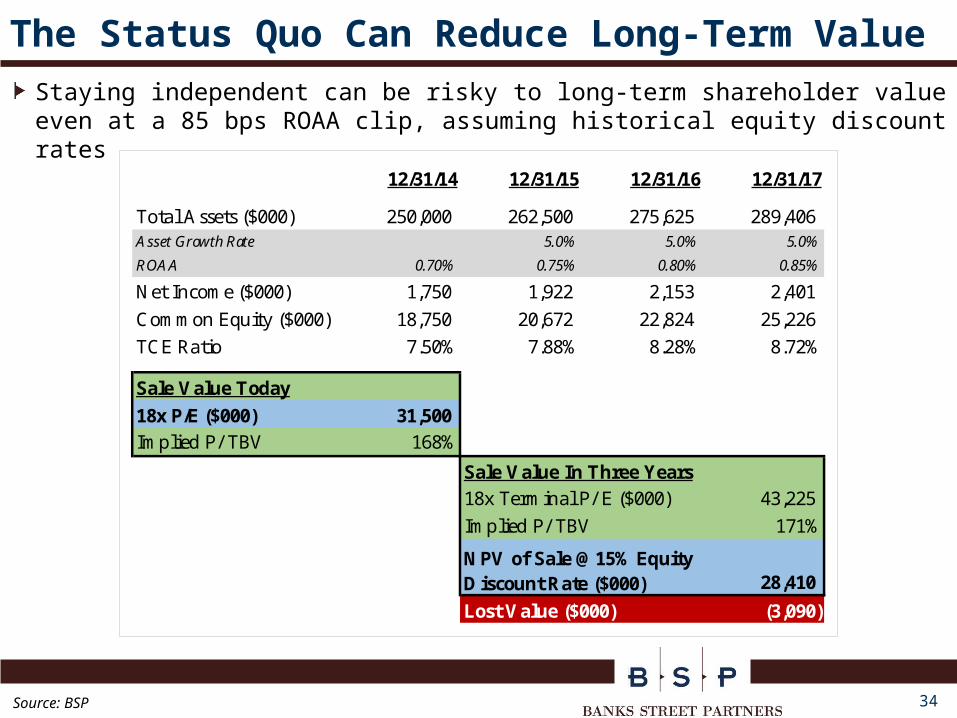

The Status Quo Can Reduce Long-Term Value

Staying independent can be risky to long-term shareholder value even at a 85 bps ROAA clip, assuming historical equity discount rates

Source: BSP

12/31/14 12/31/15 12/31/16 12/31/17

Total Assets ($000) 250,000 262,500 275,625 289,406 Asset Growth Rate 5.0% 5.0% 5.0%

ROAA 0.70% 0.75% 0.80% 0.85%

Net Income ($000) 1,750 1,922 2,153 2,401

Common Equity ($000) 18,750 20,672 22,824 25,226

TCE Ratio 7.50% 7.88% 8.28% 8.72%

Sale Value Today

18x P/E ($000) 31,500 Implied P/ TBV 168%

Sale Value In Three Years18x Terminal P/ E ($000) 43,225

Implied P/ TBV 171%

28,410

Lost Value ($000) (3,090)

NPV of Sale @ 15% Equity Discount Rate ($000)

35

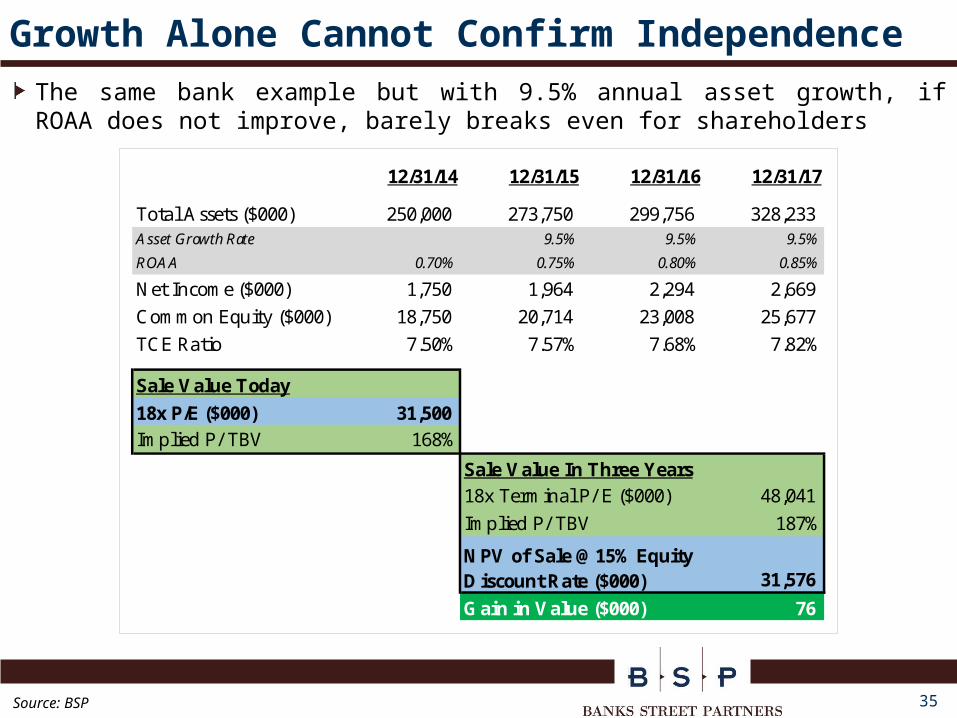

Growth Alone Cannot Confirm IndependenceThe same bank example but with 9.5% annual asset growth, if ROAA does not improve, barely breaks even for shareholders

12/31/14 12/31/15 12/31/16 12/31/17

Total Assets ($000) 250,000 273,750 299,756 328,233 Asset Growth Rate 9.5% 9.5% 9.5%

ROAA 0.70% 0.75% 0.80% 0.85%

Net Income ($000) 1,750 1,964 2,294 2,669

Common Equity ($000) 18,750 20,714 23,008 25,677

TCE Ratio 7.50% 7.57% 7.68% 7.82%

Sale Value Today

18x P/E ($000) 31,500 Implied P/ TBV 168%

Sale Value In Three Years18x Terminal P/ E ($000) 48,041

Implied P/ TBV 187%

31,576

Gain in Value ($000) 76

NPV of Sale @ 15% Equity Discount Rate ($000)

Source: BSP

36

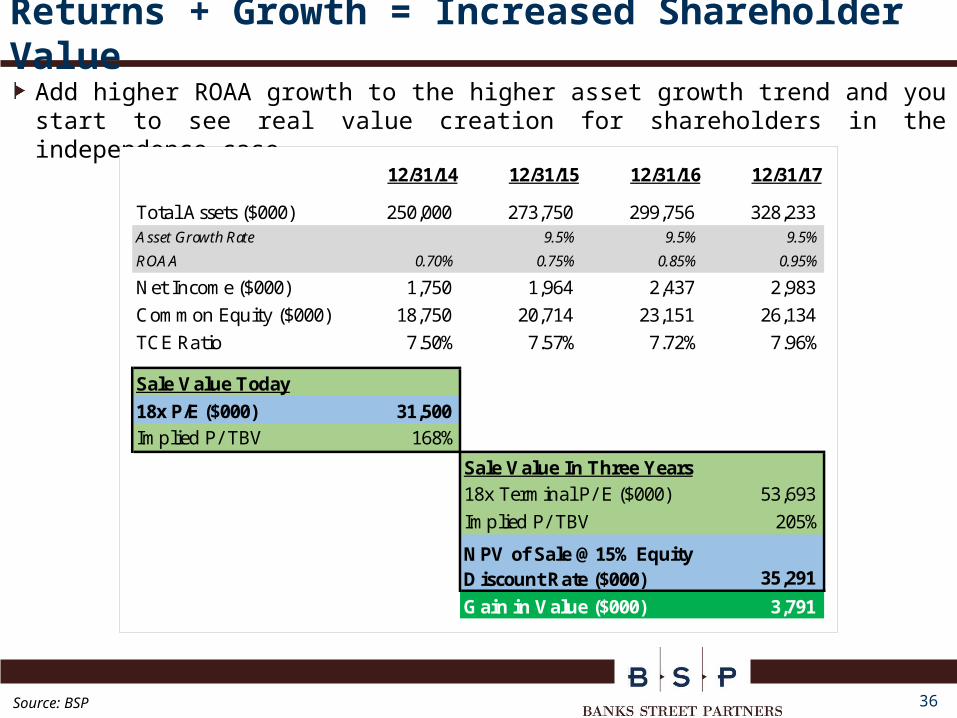

Returns + Growth = Increased Shareholder Value

Add higher ROAA growth to the higher asset growth trend and you start to see real value creation for shareholders in the independence case

12/31/14 12/31/15 12/31/16 12/31/17

Total Assets ($000) 250,000 273,750 299,756 328,233 Asset Growth Rate 9.5% 9.5% 9.5%

ROAA 0.70% 0.75% 0.85% 0.95%

Net Income ($000) 1,750 1,964 2,437 2,983

Common Equity ($000) 18,750 20,714 23,151 26,134

TCE Ratio 7.50% 7.57% 7.72% 7.96%

Sale Value Today

18x P/E ($000) 31,500 Implied P/ TBV 168%

Sale Value In Three Years18x Terminal P/ E ($000) 53,693

Implied P/ TBV 205%

35,291

Gain in Value ($000) 3,791

NPV of Sale @ 15% Equity Discount Rate ($000)

Source: BSP

37

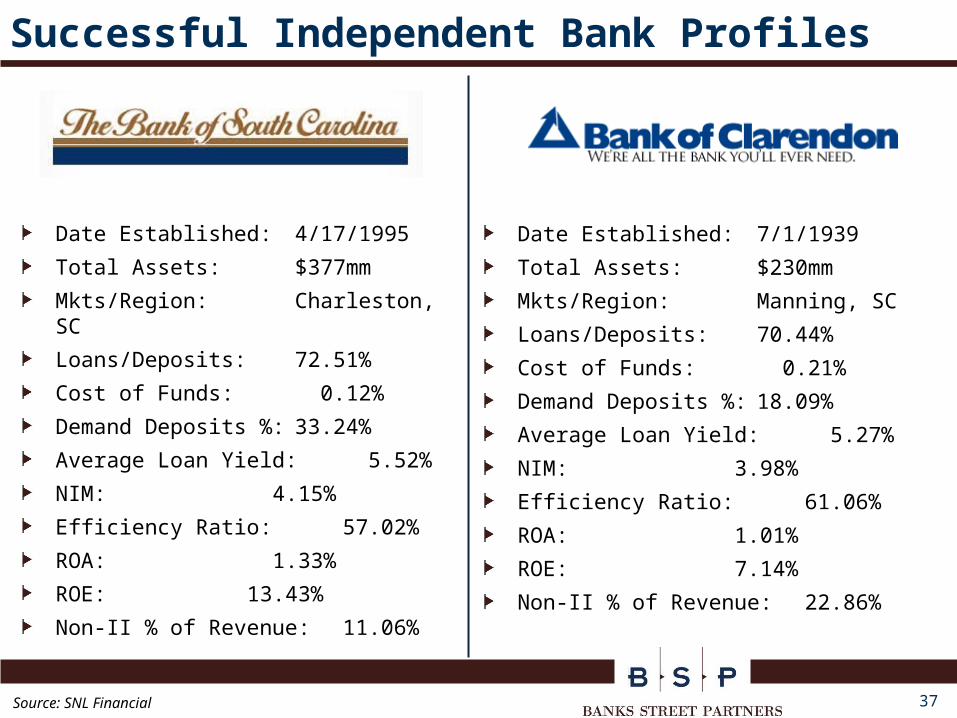

Successful Independent Bank Profiles

Date Established: 4/17/1995

Total Assets: $377mm

Mkts/Region:Charleston, SC

Loans/Deposits: 72.51%

Cost of Funds: 0.12%

Demand Deposits %: 33.24%

Average Loan Yield: 5.52%

NIM: 4.15%

Efficiency Ratio: 57.02%

ROA: 1.33%

ROE: 13.43%

Non-II % of Revenue: 11.06%

Date Established: 7/1/1939

Total Assets: $230mm

Mkts/Region: Manning, SC

Loans/Deposits: 70.44%

Cost of Funds: 0.21%

Demand Deposits %: 18.09%

Average Loan Yield: 5.27%

NIM: 3.98%

Efficiency Ratio: 61.06%

ROA: 1.01%

ROE: 7.14%

Non-II % of Revenue: 22.86%

Source: SNL Financial

1380 West Paces Ferry Rd. NW, Suite 2060Atlanta, GA 30327

(404) 848-1571

200 Providence Rd., Suite 207Charlotte, NC 28207

Related Documents