Saving and Paying for College

Saving and Paying for College. Agenda Influence of savings Savings options for parents o Impact on financial aid eligibility Saving options for students—while.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Saving and Paying for College

Agenda

• Influence of savings• Savings options for parents

o Impact on financial aid eligibility

• Saving options for students—while in schoolo Creating a personal spending plano Working through collegeo Impact on financial aid eligibility

• Next steps

Influence of Saving

4

Influence of Saving

• Increase college aspirations• Encourage personal responsibility• Good first step in college-planning process

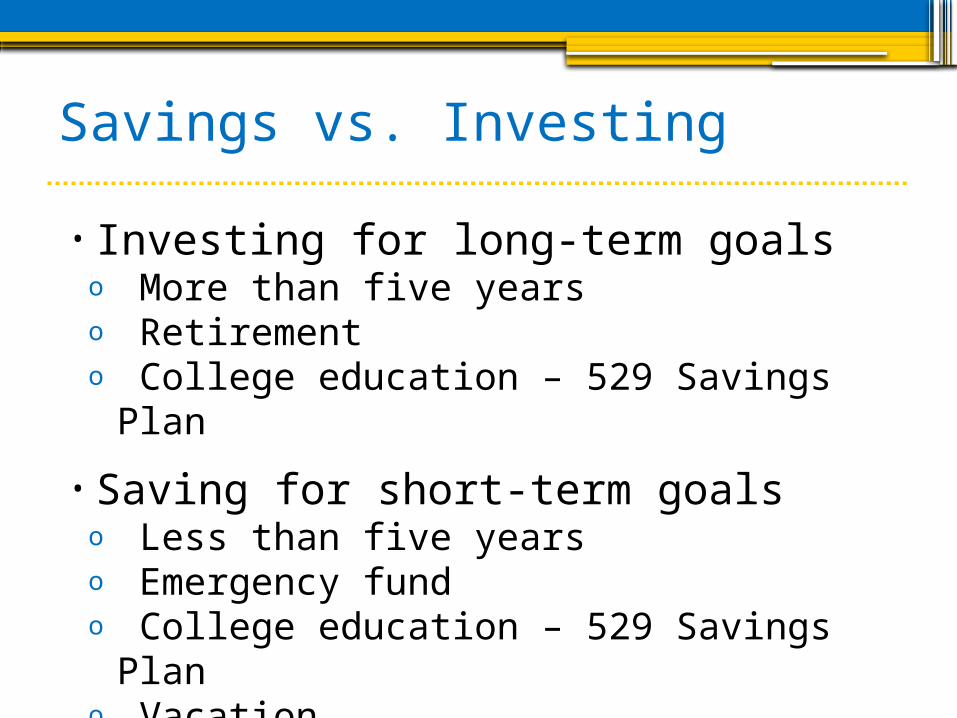

Savings vs. Investing

• Investing for long-term goalso More than five yearso Retiremento College education – 529 Savings Plan

• Saving for short-term goalso Less than five yearso Emergency fundo College education – 529 Savings Plano Vacation

Average undergraduate budget

Source: The College Board, Annual Survey of Colleges. Note: Expense categories are based on institutional budgets for students as reported by colleges and universities in the Annual Survey of Colleges. They do not necessarily reflect actual student expenditures.

Undergraduate payment resources

Source: http://trends.collegeboard.org/student_aid/report_findings/indicator/304#f84

Federal Work-Study - 1%

Pell Grants – 18%

State grants – 6%Education tax credits & deductions - 4%

- College Savings Plan - Hope and Life time learning tax credits

Private and employer grants – 4%

Institutional grants – 17%

Federal loans – 43%

Other federal grants – 8%

Savings Options for Parents

Where to Save

•Banks and credit unionso Checking accounto Savings accounto Money market accounto Certificate of deposit (CD)o College savings accounts

•Investment programso Individual retirement accounts (IRAs)o College savings accounts

Savings—Getting Started

•Checking accounto Lowest interest rateo For more frequent transactions

•Savings accounto Higher interest rates than checking

•Savings bondso Reliable, low risk option

Savings—Larger Amounts

• Individual retirement accounts (IRAs)o Traditional IRAo Roth IRA

• Money market accounto Higher rates than checking and savingso Limited number of monthly withdrawals

• Certificate of deposit (CD)o Requires minimum deposito Pays higher interest rateo No transactions for a set periodo Early withdrawal penalty

College saving accounts

•Coverdell education savings accounto Variety of investment optionso Income and contribution limits

• Annual cap of $2000 per yearo Student control

• 529 planso Open with as little as $15o Professionally managed investment optionso Higher income and contribution limitso Parent control

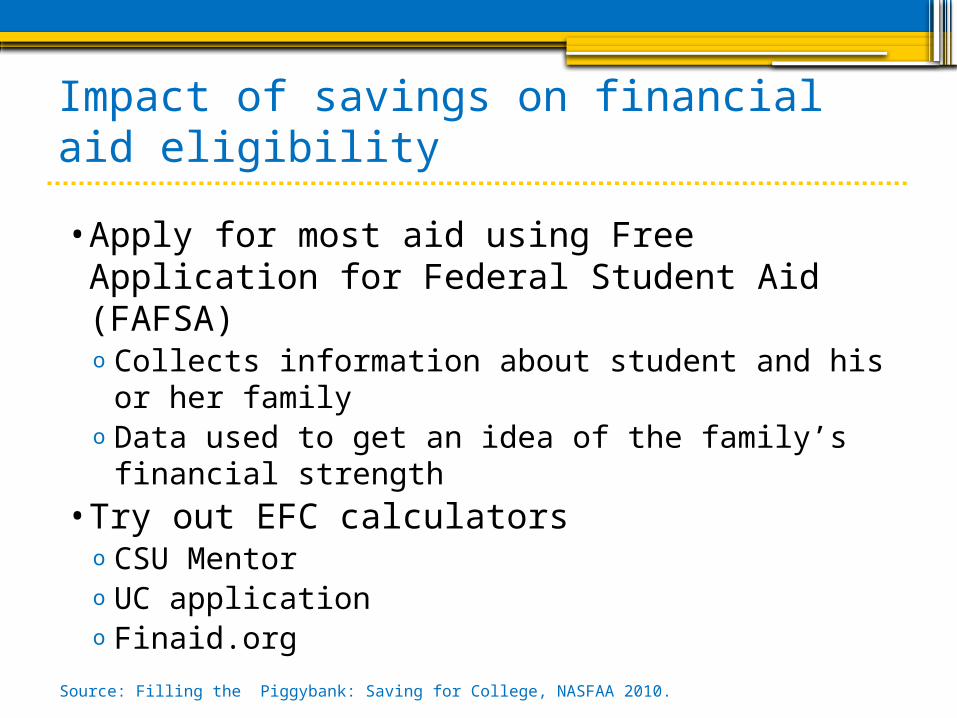

Impact of savings on financial aid eligibility

•Apply for most aid using Free Application for Federal Student Aid (FAFSA)o Collects information about student and his or

her familyo Data used to get an idea of the family’s

financial strengtho Some colleges will require the CSS profile

Source: Filling the Piggybank: Saving for College, NASFAA 2010.

Impact of savings on financial aid eligibility

•FAFSA asset questionso Current balance of cash, savings and checking accountso Net worth of investments, including real stateo Net worth of current business and/or investments farms

•Common assets not reported on FAFSAo Family homeo Family farmso Value of retirement plans and pension fundso Value of none-education IRAso Certain small businesses

Source: Filling the Piggybank: Saving for College, NASFAA 2010.

Impact of savings on financial aid eligibility

•Value of 529 plans is reported as part of net worth of investmentso Always the asset of the parent

•Parents not expected to deplete assets to pay for collegeo Certain amount of assets protected for other

uses such as retiremento Small percentage of asset above threshold

amount available for college expensesSource: Filling the Piggybank: Saving for College, NASFAA 2010.

Savings options for students • Benefits of college education

• Reducing expenses

• Working through college

• Reducing loan debt

• Impact on financial aid eligibility

Benefits of a college education

Potential incomeo High school diploma $33,800o Bachelor’s degree $55,700o Lifetime earnings difference$854,100

• Employment• Quality of life

Source: www.MyFico.com. Percentage of U.S. population scoring in each range.

Median earning & tax payments

High School Graduate

Some College Bachelor's Degree

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

After-Tax Earnings$26,70

0

After-Tax Earnings$31,000

After-Tax Earnings$32,700

Taxes$7,100

Taxes$8,700

Taxes$9,300

Data compiled by the College Board using U.S. Census Bureau, 2009 and IRS, 2008; data. The bars in this graph show median earnings at each education level. The taxes paid segments represent the estimated average federal, state, and local taxes paid at these income levels. Taxes include federal income, Social Security, state and local income and property taxes.

Unemployment rates by education level

Source: The College Board. Data from Bureau of Labor Statistics, 2010. Unemployment Rates Among Individuals Ages 25 and Older, by Educational Level, 1992-2009

Typical budget

Household Expenses 80%

Taxes 17%

Extra 3%

Average Expenses Source: Consumer Expenditure Survey, Bureau of Labor Statistics

Create a personal budget

• What is a budget?o Make the most of your financial resourceso Determine your monthly income

• Create your own personal budgeto Reduce unnecessary expenditureso Better anticipate your monetary needs

• Write out a budget• Track each expense• Adopt a “spend less, save more” lifestyle• Stick to it

Ways to save – for studentsFood Clothes

• Eat out less• Share a meal• Skip daily coffee• Shop with a list• Buy generic brands• Use coupons• Buy in bulk

• Buy the basics• Shop sales• Shop thrift stores• Make minor repairs

Source: www.MyFico.com. Percentage of U.S. population scoring in each range.

Source: www.MyFico.com. Percentage of U.S. population scoring in each range.

Ways to save – for studentsTransportation Entertainment

• Economy car• Used car• Car pool• Public transportation• Walk• Ride a bike

•Entertain at home•Pack a picnic•Student discounts•Free concerts•Community events

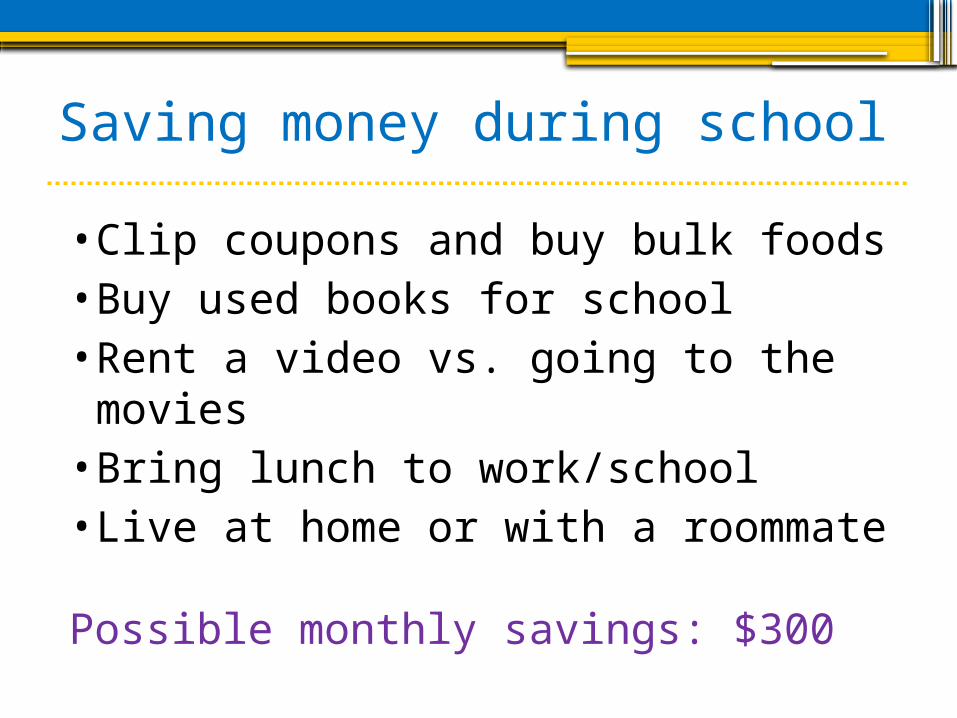

Saving money during school

• Clip coupons and buy bulk foods• Buy used books for school• Rent a video vs. going to the movies• Bring lunch to work/school• Live at home or with a roommate

Possible monthly savings: $300

Pay yourself first

Today’s habits pay off tomorrow• Include savings in your budget• Save for emergencies• Save for major purchases

Saving for college students

Start now for high school students• 18-year-old will be 23 in five years• Last year of college• $25 every two weeks

Five years of saving vs. borrowing

Savings growth calculated at 4 percent interest with contributions made for five years. Loan interest rate is 6 percent with 10-year term.

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$25 biweekly saving

Interest earned

Interest paid

Loan amount

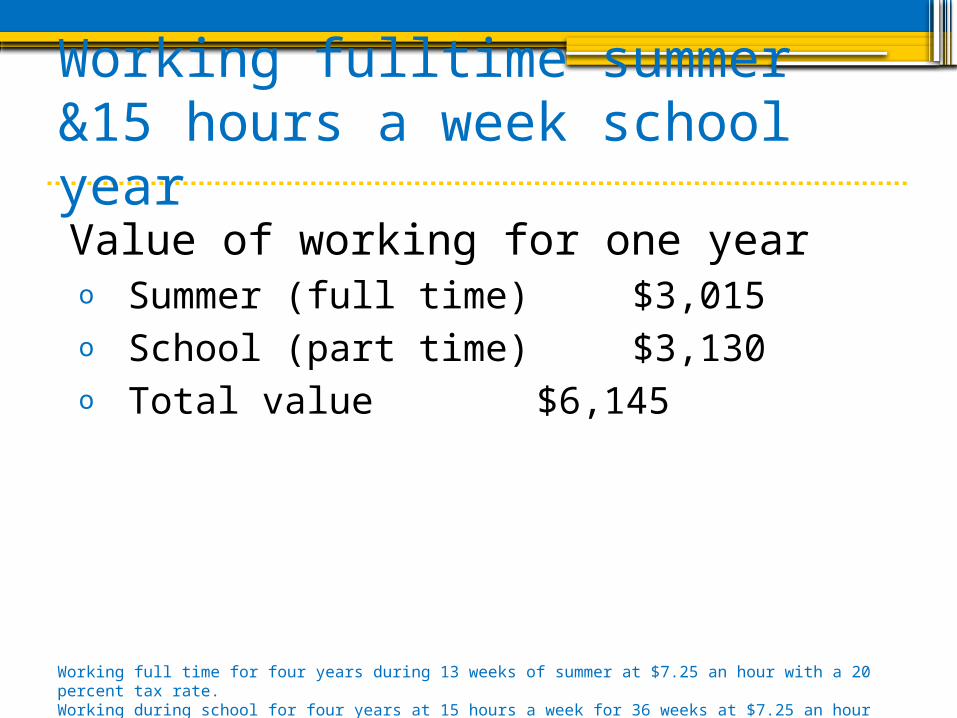

Working fulltime summer &15 hours a week school year

Value of working for one yearo Summer (full time) $3,015o School (part time) $3,130o Total value $6,145

Working full time for four years during 13 weeks of summer at $7.25 an hour with a 20 percent tax rate. Working during school for four years at 15 hours a week for 36 weeks at $7.25 an hour with a 20 percent tax rate.

Value over four years

Working F/T each summer$12,060

Working P/T during school$12,520

Total value$24,580

Pay tuition instead of borrowing• Student loan payment• Save about $135 or $270 monthly for 10 yearWorking full time for four years during 13 weeks of summer at $7.25 an hour with a 20 percent tax

rate. Working during school for four years at 15 hours a week for 36 weeks at $7.25 an hour with a 20 percent tax rate. Student loan payment based on a $12,240 loan at 6 percent interest re-paid over 10 years.

Value over four years

Working F/T each summer$12,060

Working P/T during summer$12,520

Saving $15 biweekly for five years $3,600

Budgeting to save $150 a month $7,200

• Roommate, transportation, used books, bringing lunches, etc.

Total possible money for college:$35,380

Working full time for four years during 13 weeks of summer at $7.25 an hour with a 20 percent a tax rate. Working during school for four years at 15 hours a week for 36 weeks at $7.25 an hour with a 20 percent tax rate. Saving $15 biweekly for five years at 4 percent interest.

Reduce Direct Loan debt in school

•Borrow only what is needed, not total eligibility

•Reduce/cancel/return remaining disbursement/s if not needed

•Prepay during school and grace•Pay unsubsidized interest during school or

grace before capitalization at repayment

Impact of savings on financial aid eligibility

•Apply for most aid using Free Application for Federal Student Aid (FAFSA)o Collects information about student and his or her

familyo Data used to get an idea of the family’s financial

strength•Try out EFC calculators

o CSU Mentoro UC applicationo Finaid.org

Source: Filling the Piggybank: Saving for College, NASFAA 2010.

Next steps•Getting started•Resources

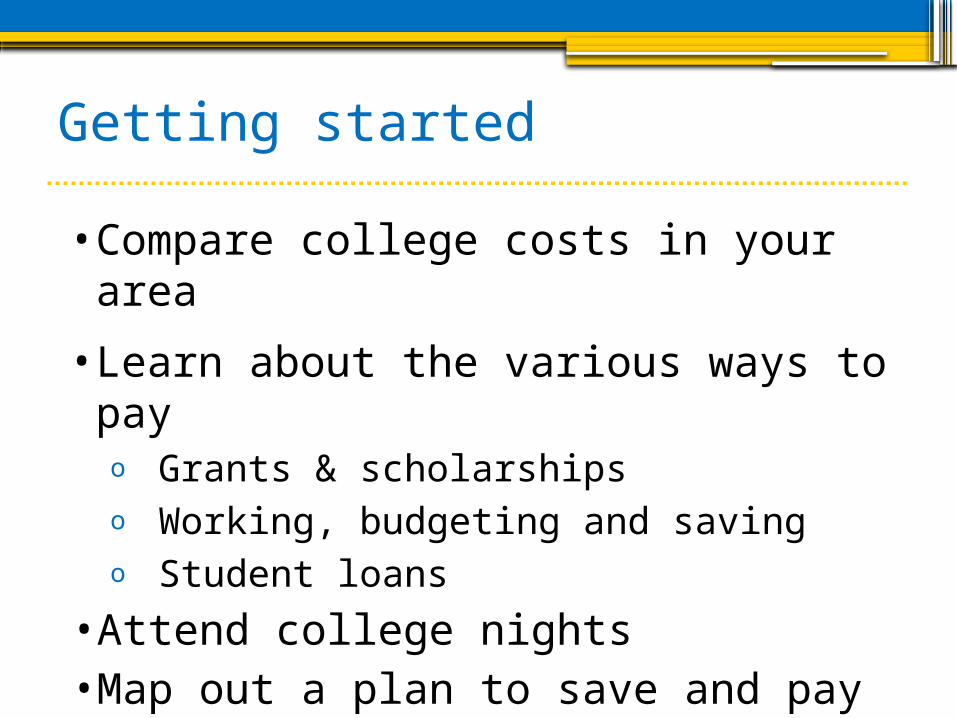

Getting started

• Compare college costs in your area

• Learn about the various ways to payo Grants & scholarshipso Working, budgeting and savingo Student loans

•Attend college nights•Map out a plan to save and pay for college

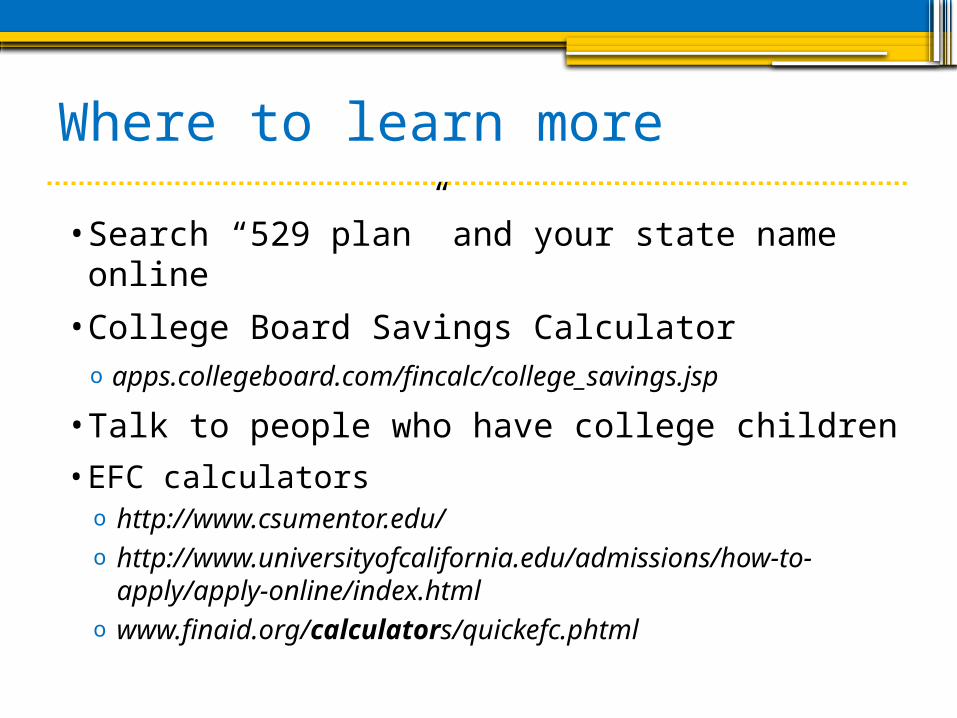

Where to learn more

•Search “529 plan” and your state name online

•College Board Savings Calculatoro apps.collegeboard.com/fincalc/college_savings.jsp

•Talk to people who have college children

•EFC calculatorso http://www.csumentor.edu/o http://www.universityofcalifornia.edu/admissions/how-to-apply/apply-online/index.html

o www.finaid.org/calculators/quickefc.phtml

Questions?

Related Documents