SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS Page 1 of 28 "It's not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for." - Robert Kiyosaki (author of ''Rich Dad, Poor Dad'') 2014 Sudiksha Joshi Sanskriti School 5/27/2014 SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

Page 1 of 28

2014

"It's not how much money you make, but how much

money you keep, how hard it works for you,

and how many generations you keep it for." -

Robert Kiyosaki (author of ''Rich Dad, Poor Dad'')

2014

Sudiksha Joshi

Sanskriti School

5/27/2014

SAVING OPTION AND THEIR RELEVANCE TO

INDIAN INVESTORS

BACKGROUND :

"An investment in knowledge pays the best interest." - Benjamin Franklin

Investing is probably the most intimidating and daunting move that an individual makes, yet if fortuitous

enough, can turn yield terrific gains and turn a person from rags to riches. Benjamin Franklin rightly said

that investment without education and research will give regrettable outcomes, in a nutshell "losses".

Savings are crucial from the perspective of an individual / firm and equally important for the economy.

For an individual , it acts as an insurance and helps overcome the crisis situations. Moreover, savings are

prerequisite for growth and developmental works in the economy. Savings rate is considered to be the

main determinant of economic growth and development. Higher savings lead to capital formation which in

turn leads to growth thereby increasing output and employment. As per the latest findings , the sustained

growth of economy is possible only when there is increase in the propensity to save and invest.

This paper analyses the reasons for an individual to save & invest , pattern of savings, evolution of

financial market and behavior of an Indian investor.

Why should an investor save?

Saving money is crucial in securing our life from uncertainties and achieving our long-term financial goals. In a world where almost everything is available only in exchange of money, buying essential things in life and securing our future comes at a price. Many a times, living from paycheck to paycheck leaves us with little additional cash to take care of our future needs. In such a scenario, inculcating a habit of saving goes a long way in ensuring that all our needs are fulfilled.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

3 | P a g e

2014

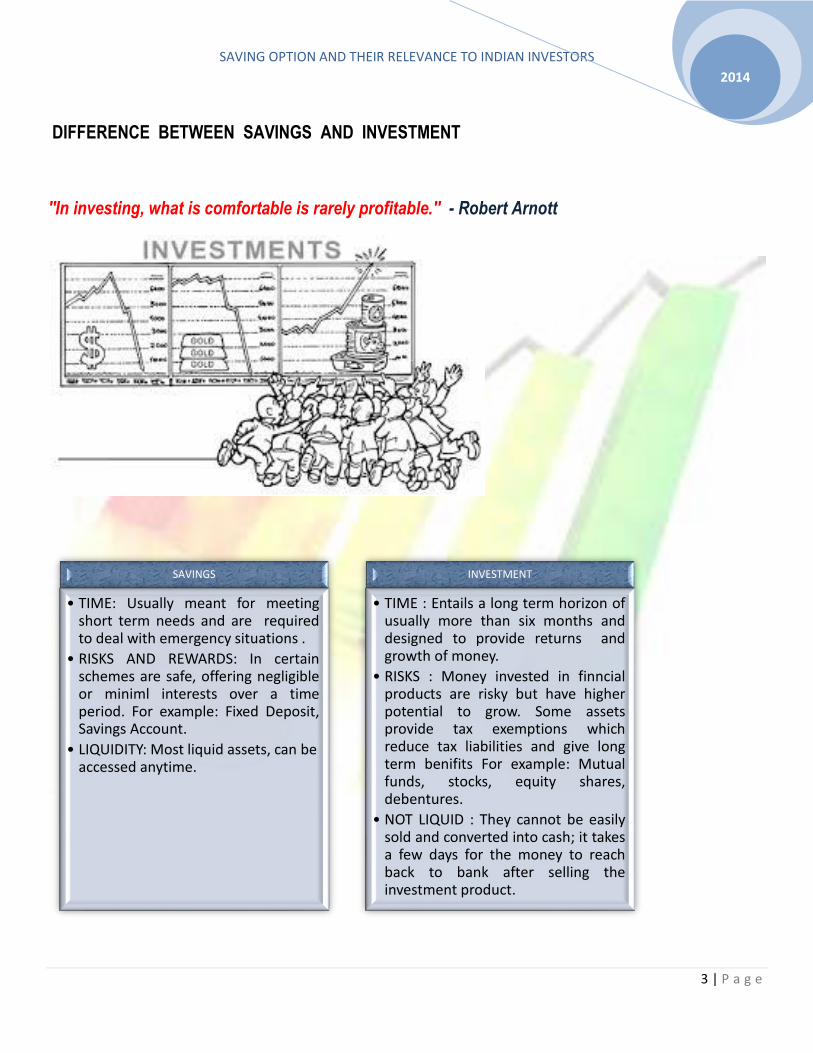

DIFFERENCE BETWEEN SAVINGS AND INVESTMENT

''In investing, what is comfortable is rarely profitable.'' - Robert Arnott

SAVINGS

• TIME: Usually meant for meeting short term needs and are required to deal with emergency situations .

• RISKS AND REWARDS: In certain schemes are safe, offering negligible or miniml interests over a time period. For example: Fixed Deposit, Savings Account.

• LIQUIDITY: Most liquid assets, can be accessed anytime.

INVESTMENT

• TIME : Entails a long term horizon of usually more than six months and designed to provide returns and growth of money.

• RISKS : Money invested in finncial products are risky but have higher potential to grow. Some assets provide tax exemptions which reduce tax liabilities and give long term benifits For example: Mutual funds, stocks, equity shares, debentures.

• NOT LIQUID : They cannot be easily sold and converted into cash; it takes a few days for the money to reach back to bank after selling the investment product.

Investment decision making - a few basic principles:

Successful investing involves making choices that meet unique needs of present and financial goals of the

future. The personal circumstances of individuals will affect their decisions. Whether saving for a home,

retirement or children's education, the need is to strategize to enable money growth. Below are 6 investing

principles to follow:

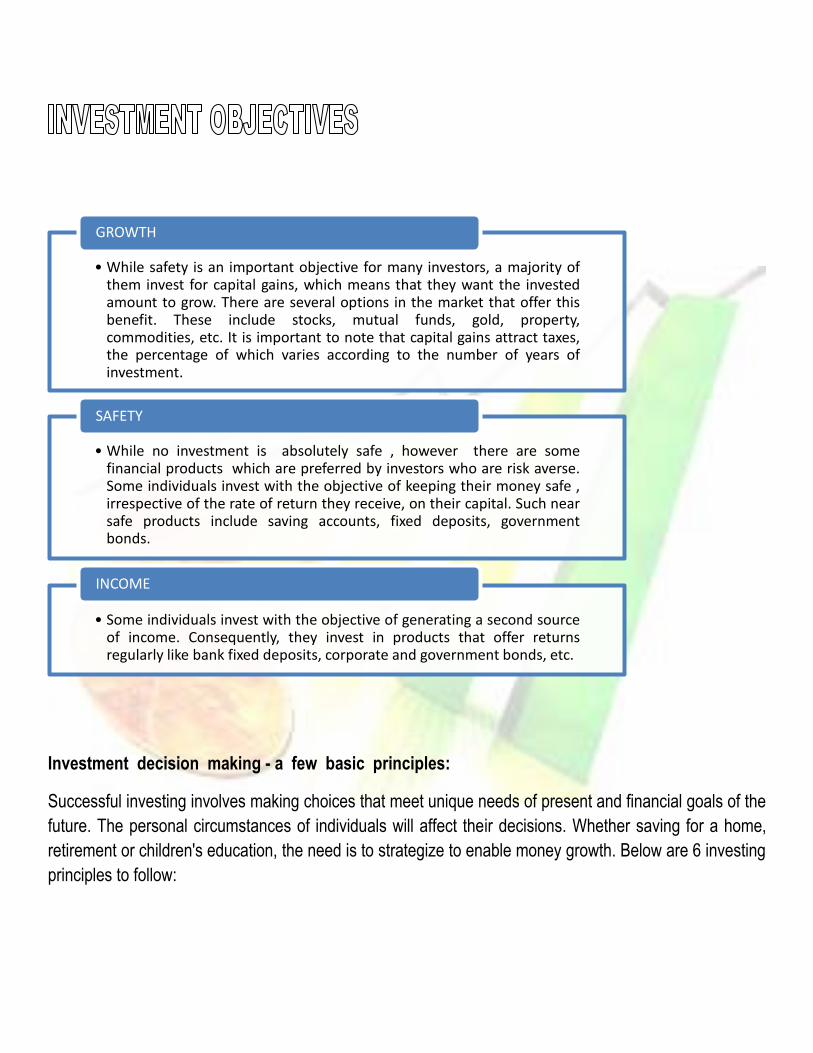

• While safety is an important objective for many investors, a majority of them invest for capital gains, which means that they want the invested amount to grow. There are several options in the market that offer this benefit. These include stocks, mutual funds, gold, property, commodities, etc. It is important to note that capital gains attract taxes, the percentage of which varies according to the number of years of investment.

GROWTH

• While no investment is absolutely safe , however there are some financial products which are preferred by investors who are risk averse. Some individuals invest with the objective of keeping their money safe , irrespective of the rate of return they receive, on their capital. Such near safe products include saving accounts, fixed deposits, government bonds.

SAFETY

• Some individuals invest with the objective of generating a second source of income. Consequently, they invest in products that offer returns regularly like bank fixed deposits, corporate and government bonds, etc.

INCOME

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

5 | P a g e

2014

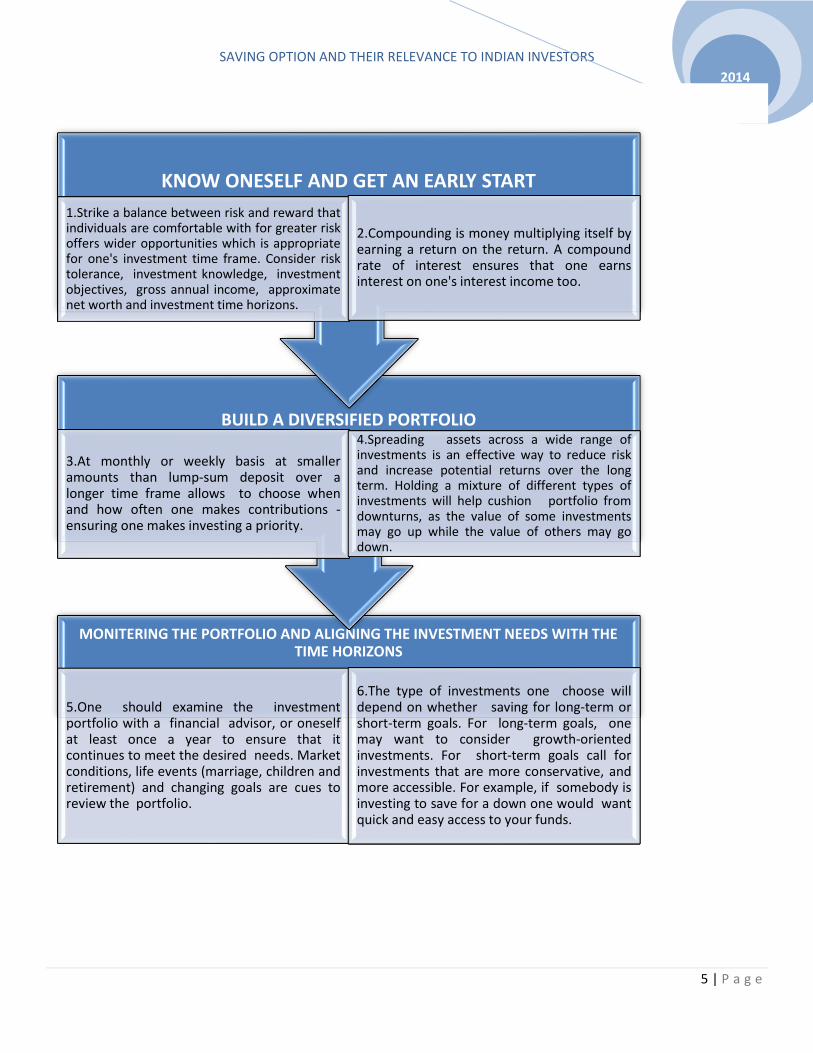

MONITERING THE PORTFOLIO AND ALIGNING THE INVESTMENT NEEDS WITH THE TIME HORIZONS

5.One should examine the investment portfolio with a financial advisor, or oneself at least once a year to ensure that it continues to meet the desired needs. Market conditions, life events (marriage, children and retirement) and changing goals are cues to review the portfolio.

6.The type of investments one choose will depend on whether saving for long-term or short-term goals. For long-term goals, one may want to consider growth-oriented investments. For short-term goals call for investments that are more conservative, and more accessible. For example, if somebody is investing to save for a down one would want quick and easy access to your funds.

BUILD A DIVERSIFIED PORTFOLIO

3.At monthly or weekly basis at smaller amounts than lump-sum deposit over a longer time frame allows to choose when and how often one makes contributions - ensuring one makes investing a priority.

4.Spreading assets across a wide range of investments is an effective way to reduce risk and increase potential returns over the long term. Holding a mixture of different types of investments will help cushion portfolio from downturns, as the value of some investments may go up while the value of others may go down.

KNOW ONESELF AND GET AN EARLY START

1.Strike a balance between risk and reward that individuals are comfortable with for greater risk offers wider opportunities which is appropriate for one's investment time frame. Consider risk tolerance, investment knowledge, investment objectives, gross annual income, approximate net worth and investment time horizons.

2.Compounding is money multiplying itself by earning a return on the return. A compound rate of interest ensures that one earns interest on one's interest income too.

INVESTMENT & SAVINGS OPTIONS AVAILABLE IN INDIAN FINANCIAL MARKET :

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER

FEATURES

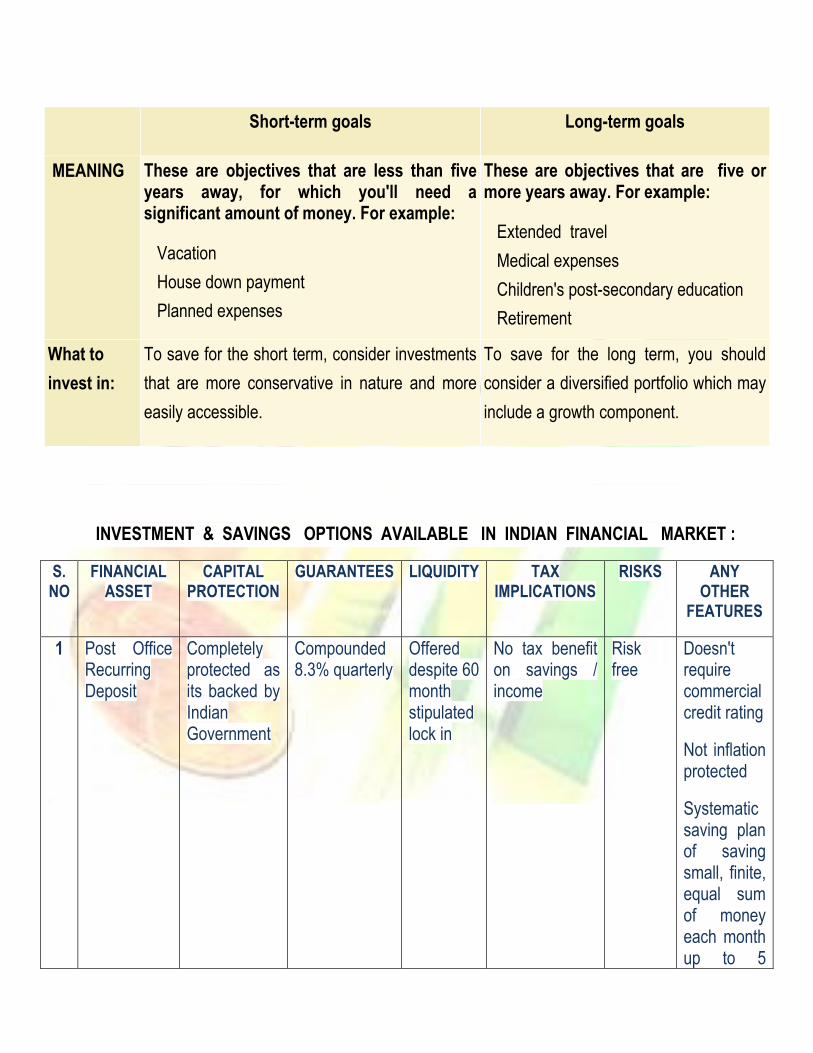

1 Post Office Recurring Deposit

Completely protected as its backed by Indian Government

Compounded 8.3% quarterly

Offered despite 60 month stipulated lock in

No tax benefit on savings / income

Risk free

Doesn't require commercial credit rating

Not inflation protected

Systematic saving plan of saving small, finite, equal sum of money each month up to 5

Short-term goals Long-term goals

MEANING These are objectives that are less than five years away, for which you'll need a significant amount of money. For example:

Vacation

House down payment

Planned expenses

These are objectives that are five or more years away. For example:

Extended travel

Medical expenses

Children's post-secondary education

Retirement

What to

invest in:

To save for the short term, consider investments

that are more conservative in nature and more

easily accessible.

To save for the long term, you should

consider a diversified portfolio which may

include a growth component.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

7 | P a g e

2014

years.

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER

FEATURES

2 Bank Recurring Deposits

Optional insurance by DICGC

Fixed interest rate guaranteed for the duration of RD

Liquid, even if depositors default to pay within he account tenure

No tax advantages as interest on maturity is "income earned from other sources''

Risky when interest rate changes. For example: high interest rate for the same time due to economic growth

Banks can end RD account before maturity

Saves predefined sum of money every month for fixed tenure

MATURITY PERIOD: 6 months-10 years

Earn better interests on svings than on Savings Bank Account

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER FEATURES

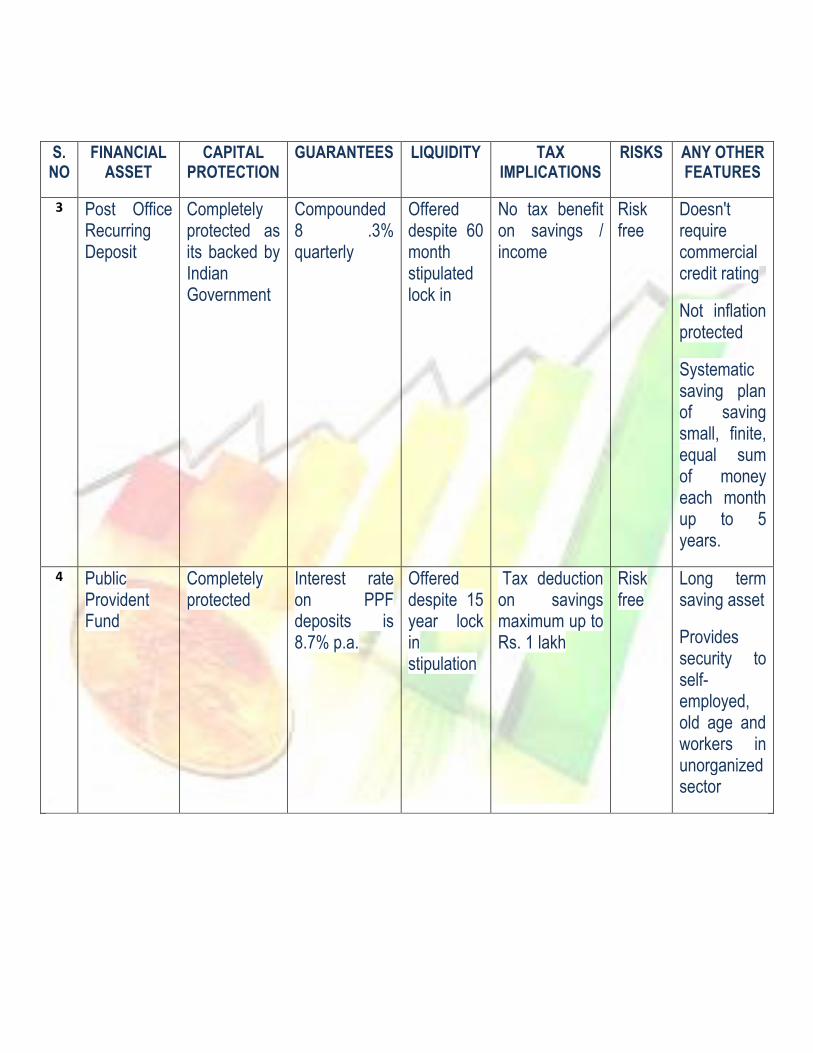

3 Post Office Recurring Deposit

Completely protected as its backed by Indian Government

Compounded 8 .3% quarterly

Offered despite 60 month stipulated lock in

No tax benefit on savings / income

Risk free

Doesn't require commercial credit rating

Not inflation protected

Systematic saving plan of saving small, finite, equal sum of money each month up to 5 years.

4 Public Provident Fund

Completely protected

Interest rate on PPF deposits is 8.7% p.a.

Offered despite 15 year lock in stipulation

Tax deduction on savings maximum up to Rs. 1 lakh

Risk free

Long term saving asset

Provides security to self-employed, old age and workers in unorganized sector

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

9 | P a g e

2014

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER

FEATURES

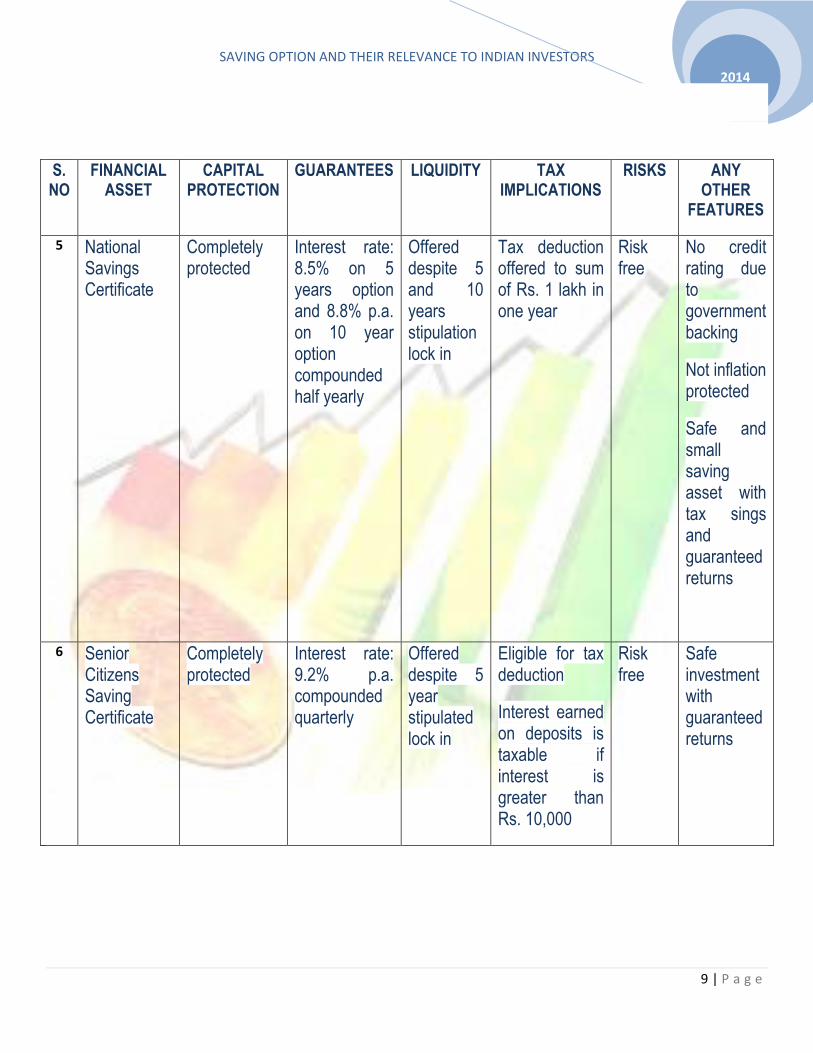

5 National Savings Certificate

Completely protected

Interest rate: 8.5% on 5 years option and 8.8% p.a. on 10 year option compounded half yearly

Offered despite 5 and 10 years stipulation lock in

Tax deduction offered to sum of Rs. 1 lakh in one year

Risk free

No credit rating due to government backing

Not inflation protected

Safe and small saving asset with tax sings and guaranteed returns

6 Senior Citizens Saving Certificate

Completely protected

Interest rate: 9.2% p.a. compounded quarterly

Offered despite 5 year stipulated lock in

Eligible for tax deduction

Interest earned on deposits is taxable if interest is greater than Rs. 10,000

Risk free

Safe investment with guaranteed returns

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER FEATURES

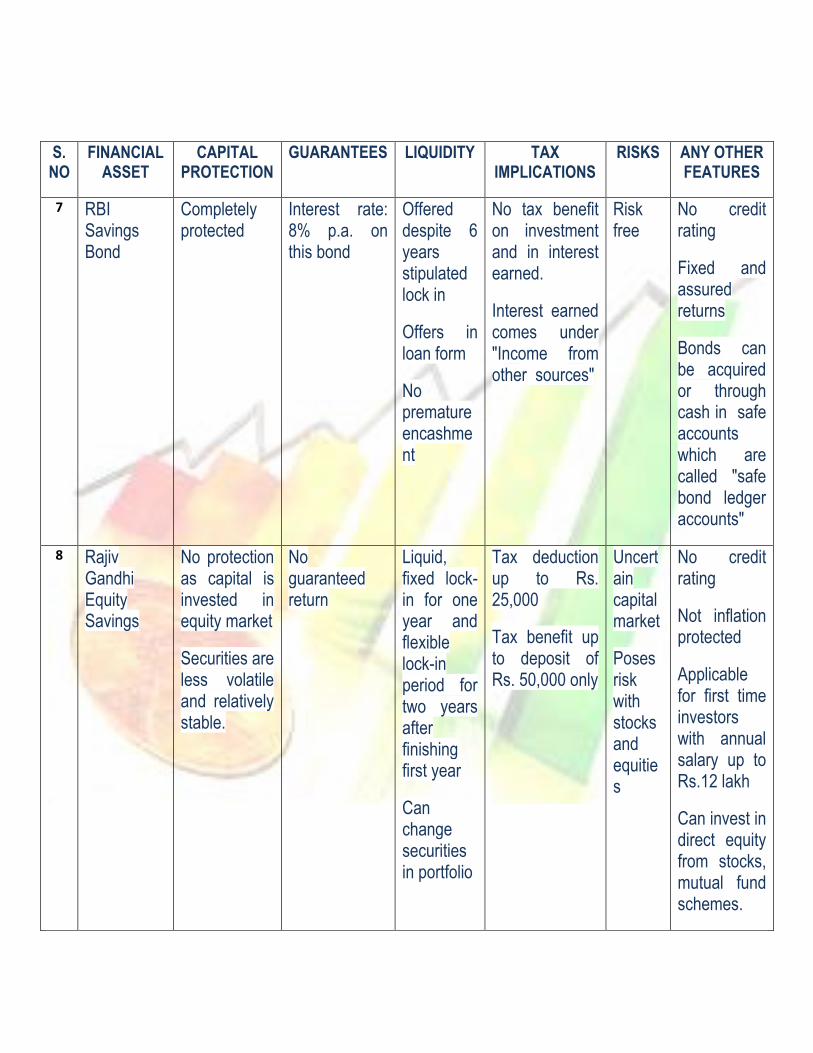

7 RBI Savings Bond

Completely protected

Interest rate: 8% p.a. on this bond

Offered despite 6 years stipulated lock in

Offers in loan form

No premature encashment

No tax benefit on investment and in interest earned.

Interest earned comes under "Income from other sources"

Risk free

No credit rating

Fixed and assured returns

Bonds can be acquired or through cash in safe accounts which are called "safe bond ledger accounts"

8 Rajiv Gandhi Equity Savings

No protection as capital is invested in equity market

Securities are less volatile and relatively stable.

No guaranteed return

Liquid, fixed lock-in for one year and flexible lock-in period for two years after finishing first year

Can change securities in portfolio

Tax deduction up to Rs. 25,000

Tax benefit up to deposit of Rs. 50,000 only

Uncertain capital market

Poses risk with stocks and equities

No credit rating

Not inflation protected

Applicable for first time investors with annual salary up to Rs.12 lakh

Can invest in direct equity from stocks, mutual fund schemes.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

11 | P a g e

2014

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER FEATURES

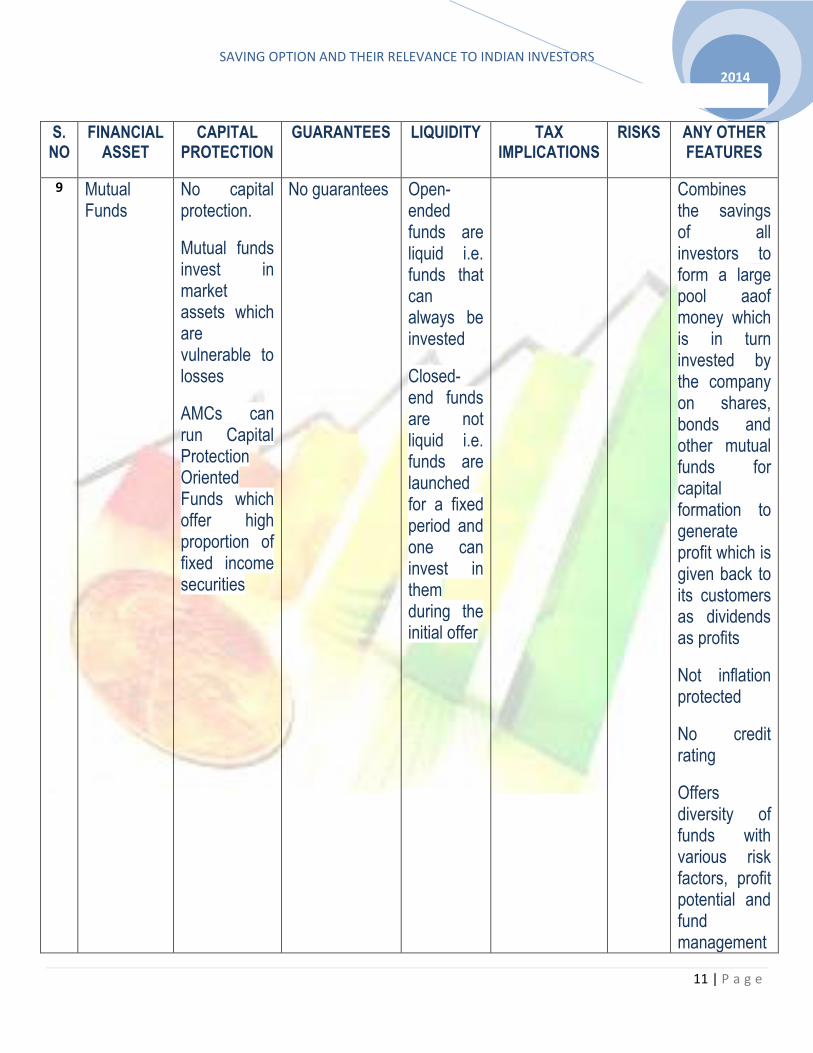

9 Mutual Funds

No capital protection.

Mutual funds invest in market assets which are vulnerable to losses

AMCs can run Capital Protection Oriented Funds which offer high proportion of fixed income securities

No guarantees Open-ended funds are liquid i.e. funds that can always be invested

Closed-end funds are not liquid i.e. funds are launched for a fixed period and one can invest in them during the initial offer

Combines the savings of all investors to form a large pool aaof money which is in turn invested by the company on shares, bonds and other mutual funds for capital formation to generate profit which is given back to its customers as dividends as profits

Not inflation protected

No credit rating

Offers diversity of funds with various risk factors, profit potential and fund management

quality

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER FEATURES

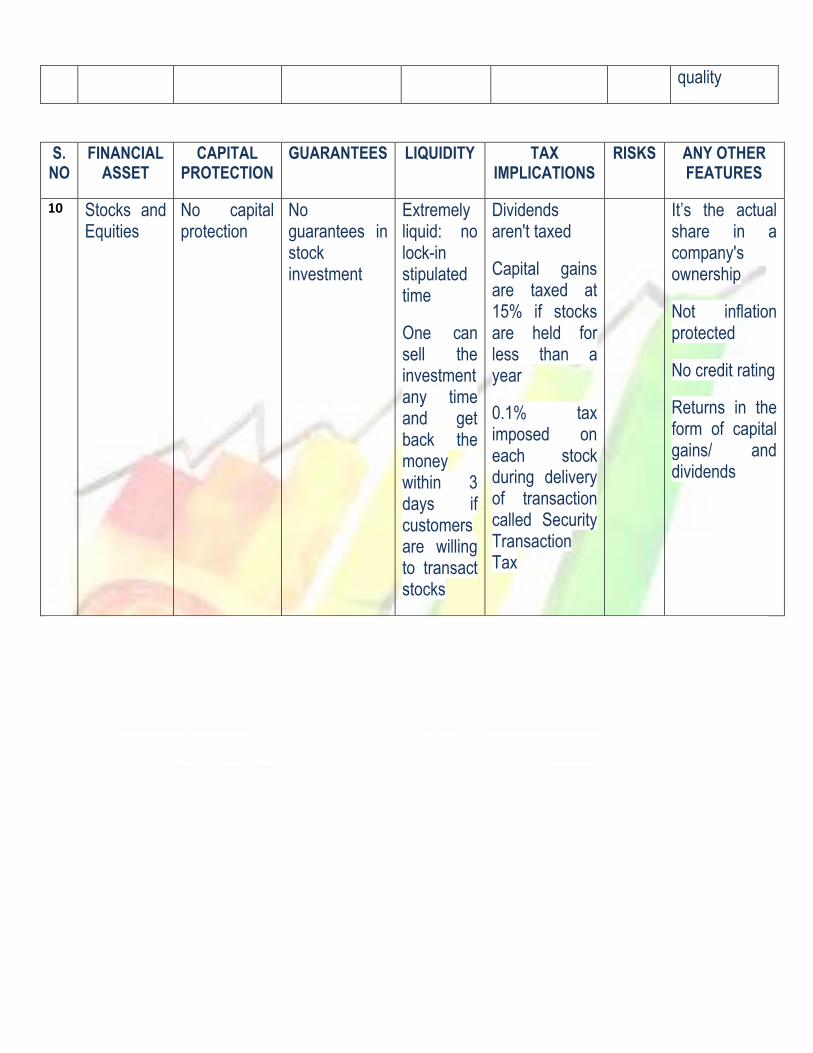

10 Stocks and Equities

No capital protection

No guarantees in stock investment

Extremely liquid: no lock-in stipulated time

One can sell the investment any time and get back the money within 3 days if customers are willing to transact stocks

Dividends aren't taxed

Capital gains are taxed at 15% if stocks are held for less than a year

0.1% tax imposed on each stock during delivery of transaction called Security Transaction Tax

It’s the actual share in a company's ownership

Not inflation protected

No credit rating

Returns in the form of capital gains/ and dividends

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

13 | P a g e

2014

S.NO

FINANCIAL ASSET

CAPITAL PROTECTION

GUARANTEES LIQUIDITY TAX IMPLICATIONS

RISKS ANY OTHER FEATURES

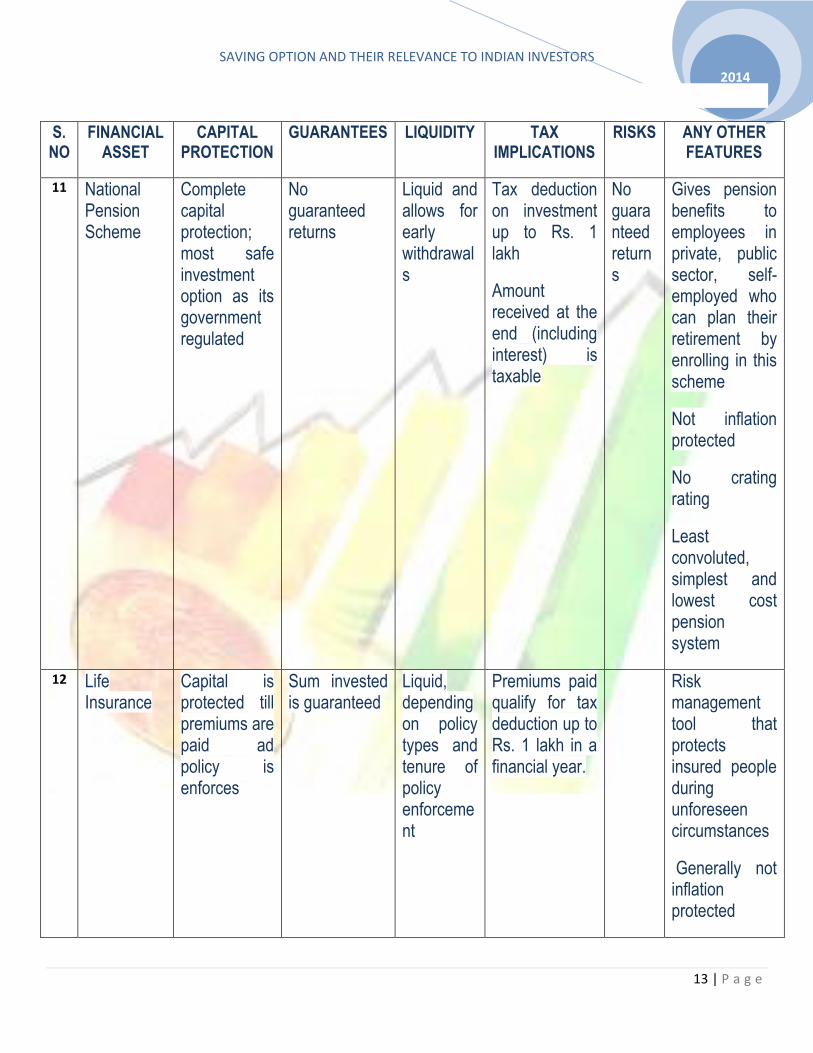

11 National Pension Scheme

Complete capital protection; most safe investment option as its government regulated

No guaranteed returns

Liquid and allows for early withdrawals

Tax deduction on investment up to Rs. 1 lakh

Amount received at the end (including interest) is taxable

No guaranteed returns

Gives pension benefits to employees in private, public sector, self-employed who can plan their retirement by enrolling in this scheme

Not inflation protected

No crating rating

Least convoluted, simplest and lowest cost pension system

12 Life Insurance

Capital is protected till premiums are paid ad policy is enforces

Sum invested is guaranteed

Liquid, depending on policy types and tenure of policy enforcement

Premiums paid qualify for tax deduction up to Rs. 1 lakh in a financial year.

Risk management tool that protects insured people during unforeseen circumstances

Generally not inflation protected

Not credit rated

INVESTOR'S BEHAVIOR - ( A Theoretical Background )

According to economic theorists , investors think and behave "rationally" when buying and selling stocks.

Generally it is presumed that investor would use all the information to form a "rational" expectation in

investment decision making. In reality, investor do not think and behave rationally. On the contrary,

investor speculate between unrealistic highs and lows and are misled by emotions , subjective thinking

and herd mentality.

The main hypothesis is " Efficient Market Hypothesis " , on which most of the academic research is

based . There are three basic theoretical arguments that form the basis of the EMH. They are:

Investor is rational.

Everybody takes careful account of all available information before making investment decision.

The third principle is that the decision maker pursue self interest.

Since stocks are always traded in stock exchange at their fair value, it is impossible for investors to buy at

deflated rates and sell at inflated rates. Hence, it's impossible for an investor to perform better than the

stock market through expert stock selection or market timing. Thereby investors can acquire higher

returns by purchasing riskier investments.

Nonetheless, resentment towards EMH exists. For example investors, such as Warren Buffett have

consistently beaten the market over long periods of time, which by definition is impossible according to the

EMH.

Behavioral Finance is an emerging science which studies the irrational nature of investors. Most of the

investment decisions are influenced to some extent by prejudices and perceptions that do not meet the

criterion of rationality. It explains how emotions and cognitive errors influence investors and decision

making process. These researches have show that investors across the markets not only behave

irrationally sometimes but also get influenced by heuristics, social affiliations, demographic factors and

psychological biases.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

15 | P a g e

2014

Life Cycle Saving & Investment:

The Life-Cycle Hypothesis (LCH) is an economic theory that is apropos to the spending and saving habits

of people over the course of a lifetime. Its assumption is that humans consume in proportion to their

anticipated life income. For example, people save for retirement while they are earning a regular income

(rather than spending it all when it is earned).

Depending on the earning capability, age and the current level of accumulated wealth, investors are

broadly classified in one of the four stages of the life cycle: accumulation, consolidation, spending

(withdrawal), or gifting. According to the theory of Lifecycle investing, each individual will go through

various lifecycle stages, in which the investment needs are different.

Accumulation phase (Age Twenties and Thirties)

In the youth phase individuals can invest in higher risk assets and follow an aggressive investment

strategy, designed to provide maximum long term growth such as equities and mutual funds.

Consolidation Phase (Age Forties and Fifties)

In mid-life, people accumulate assets to cover the important needs like housing, children education and

marriage expenses and look for opportunities to enhance wealth generation. People have more

resources to invest in but may pursue a less risky approach such as investing in Hybrid or Debt funds.

Notwithstanding, some amount may be invested in equity shares to overcome inflation stress.

Spending Phase (Age Sixties and Seventies)

The third phase is the ‘spending’ or ‘de-accumulation phase’ in which people have retired from active

service and survive on the income and capital accumulated in the first two phases. People can't afford to

lose capital by investing in riskier options. Asset allocation will mainly be skewed towards Govt. Bonds and

securities yielding regular income.

Gifting Phase (Age Eighties and Nineties)

In this phase, people who have accumulated far more wealth than they will need for their own lifetimes,

decide to pass some of their assets on to others.

The ‘life cycle’ theory suggests that, as individuals move through these phases, their investment needs

and objectives change significantly. Furthermore, there is a transformation in investment from riskier

options to products with guaranteed returns from youth to age old phase. The aforementioned ages against each phase may vary depending on the financial status and attitude of

the individual towards work. People who retire in forties and fifties witness a skyrocketing expenditure

phase which surpasses the accumulation and consolidation phase. Also, health condition and lifestyle are

important factors in deciding the longevity of the individual. Improved healthcare facilities and comfortable

lifestyle lead to increased longevity. Since the Lifecycle theories first gained popularity , financial products have developed significantly. It is

paramount for investors of all ages to balance their investment options. Large corporations majorly

employ sophisticated risk-management strategies, however, only a small spectrum of individual investors

utilize such modern techniques to plan their investment portfolios over the four life-cycles mentioned

above.

BEHAVIOR OF INDIAN INVESTORS :

Each investor possesses different mindset when he or she decides to invest in a particular investment avenue such as stocks, bonds, mutual funds, fixed deposit, real estate, bullion etc. such that the hard earned money is secured in liquid avenue. However, the decision varies from every individual depending on their risk taking ability and their purpose for which such investments are done. Saving is prerequisite for investing. People select that option which meets their financial goals. Investment behavior reveals how investors reveals how people allocate their surplus financial resources into various instruments. Its constitutes the reason, quantity, time period and the suitability an investment. Moreover, empirical studies have shown that information is decisive factor on deciding whether to invest, which in turn affects the choice of investment and people's behavior to such decisions. In every life cycle stage, saving objective by an individual always changes which occurs due to investor's age, occupation, income level category. Empirical studies to examine investors' nature in India have concluded the following: i. Savings Objective of Individual Investors:

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

17 | P a g e

2014

People spend voluminously for their children’s marriage and education as people think it wise to save money with a specific goal to achieve in future such as, for purchasing a house, accumulating wealth for retirement life, spending for their children's marriage or education. Therefore , to achieve such financial goals, individual investors always resort to discipline and systematic savings and investments. ii. Investment options preference among Individual Investors : One of the key principle for disciplined investing is not to let the hard earned money slip through the hands. Asset preference pattern of an individual investor provides an insight into the investment attitude of investors, which influences the policy formation for garnering the individual savings. Every individual investor should decide where to invest and how much to invest and when to invest, depending on their risk profile and saving objective they set. Following important observations from studies are:

Salaried and self employed professionals save more for their post retirement life in contrast with entrepreneur class of investors who invest more on liquid funds for future contingencies.

by Barclays Wealth and Ledbury Research in April’ 2012 suggests Women were found to be more

disciplined, focused and usually more conservative than their male counterparts as they prefer to invest more in debt related instruments and in bullion. Changes in income alters the saving percentage.

FDs and investment in real estate are the most popular savings and investment avenues for male

investors whereas, whereas investment in real estate and bullion are the most preferred avenues for the female investors.

The Government sponsored small saving schemes such as national saving certificates (NSC),

public provident fund (PPF), Indian post office saving schemes, etc., have got wider acceptance and are preferred by both male and females.

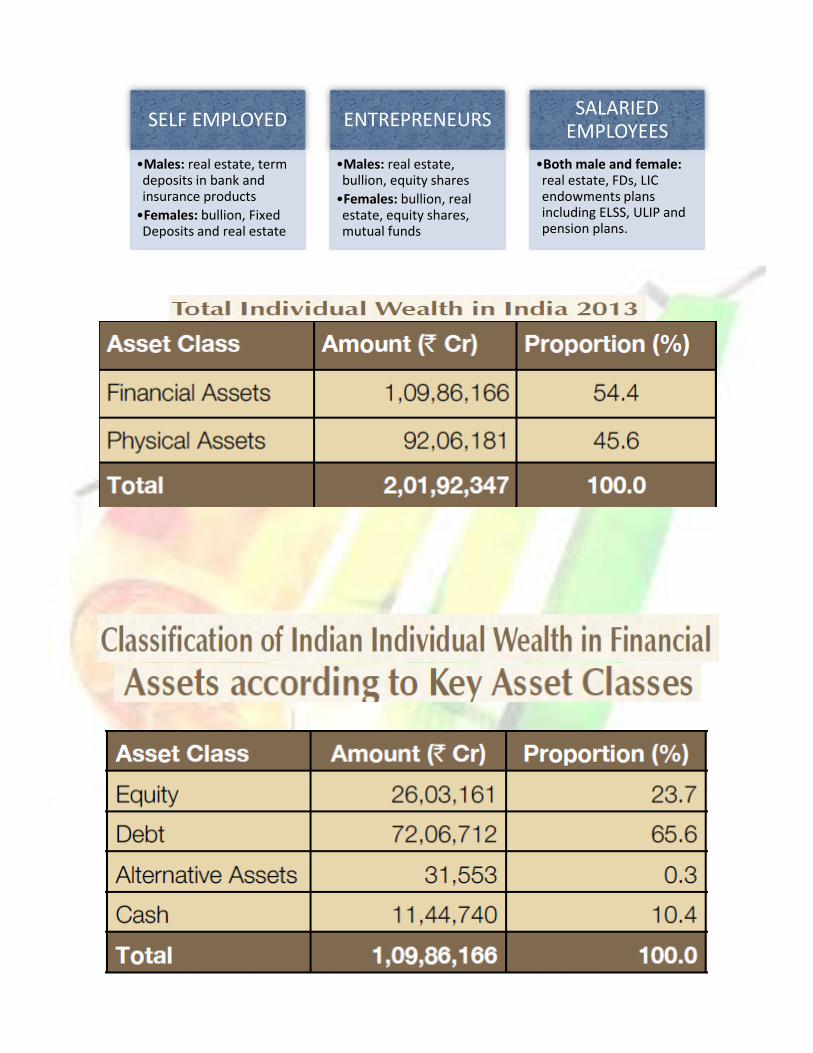

SELF EMPLOYED

•Males: real estate, term deposits in bank and insurance products

•Females: bullion, Fixed Deposits and real estate

ENTREPRENEURS

•Males: real estate, bullion, equity shares

•Females: bullion, real estate, equity shares, mutual funds

SALARIED EMPLOYEES

•Both male and female: real estate, FDs, LIC endowments plans including ELSS, ULIP and pension plans.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

19 | P a g e

2014

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

21 | P a g e

2014

CHANGING FINANCIAL SYSTEMS IN INDIA - RELEVANCE, EVOLUTION AND PRESENT STATUS

Relevance of financial system for economy : The saving and investment process in a financial framework aids economic upswing through appropriately

mobilizing savings and allocating them to the most productive uses by following a

centralized/decentralized approach or both. Economies with underdeveloped capital markets adopt a

centralized approach, whereby financial intermediaries mobilize resources from savers and allocate them

to borrowers. Banks play an imperative role as "intermediaries" whereby they deal with transaction costs

and information asymmetries in a financial system. As financial markets develop, transaction costs and

information asymmetries reduce, the decentralized approach for guiding the saving-investment process

also gains significance, and households with surplus resources increasingly invest in capital market

instruments.

Financial systems are crucial for capital formation. It is universally accepted that capital formation is indispensible to a speedy economic development. The main function of the financial systems is to collect savings and invest them in industries, stimulating the capital formation and accelerating the economy.

There are 3 processes of capital formation : i. Savings: The ability by which resources are set aside and become available for other purposes. ii. Finance: The activity by which the resources either assembled from those released by domestic savings , obtained from abroad, or created as bank deposit and then placed in the hands of the investors for industries. iii. Investment: The activity by which these resources are actually committed to production. Thus, the volume of capital formation depends on effective mobilization of savings and the efficiency of financial organization / systems in channelizing these savings into most desirable productive form . Evolution of Indian Financial Systems: An efficient and developed financial system is important for rapid economic growth of any country. However, the structures differ widely depending on political economic condition of the country. The planned economic development in India had greatly influenced the course of financial development. The liberalization/deregulation/ globalization of the Indian economy since the early nineties have had important implications for the future course of development of the financial systems. The evolution of Indian financial system falls into three distinct phases : Phase I : Pre 1951 India financial market is one of the oldest in the world . The history of Indian capital markets dates back 200 years toward the end of the 18th century when India was under the rule of the East India Company. 1951: Planning Commission set up, mixed economy established, changes in the decrepit financial system The development of the capital market in India concentrated around Mumbai where around 200 to 250 securities brokers were active during the second half of the 19th century. The securities exchanges of Mumbai, Ahmadabad and Kolkata were established as early as the 19th century. Despite , early start, there were serious limitations and the financial system was not responsive to opportunities for industrial development particularly the growth to new and innovative enterprise.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

23 | P a g e

2014

Phase II : 1951 to Mid Eighties One aspect of the changes was the progressive transfer of the institutions from private to public ownership. Some of the steps in this direction were -

Nationalization of RBI , Setting up of State Bank Of India by taking over the Imperial bank Of India, Nationalization and merging of 245 life insurance companies into state owned Life Insurance

company(LIC), which emerged as the largest reservoir of long term savings in the country Setting up of UTI. Developmental banks such as IDBI, IFCI,ICICI etc were conceived for directing capital into chosen

areas of industry in accordance with the planning priorities. The banking policies and practices were molded to the tune of planning processes and they were

encouraged to finance the industries. Extensive legal reforms were carried out to protect investors and

infuse confidence in industrial securities.

1960s: Nationalization of 14 major private banks, which would mobilize deposits from the household

sector. This has bolstered the financial savings of the household sector and hence the overall saving rate.

Notwithstanding the liberalisation of the financial sector and increased competition from various other

saving instruments, banks continue to play a dominant role in the financial intermediation of the Indian

economy. The deregulation of interest rates has opened up new avenues for banks to mobilize funds at

competitive rates. Moreover, banks, reckoned as the ultimate platform for clearing and settling for all

financial transactions, provide accounts and resources to other sectors including other financial

intermediaries.

A serious drawback with developmental financial institutions was that they depended resources from RBI and government could not mobilize enough savings that would enable the banks to meet the industrial requirements. The securities/capital market was still a marginal institution. Early 1960s: set up of 8 Securities Exchanges in Mumbai, Ahmadabad and Kolkata apart from Madras, Kanpur, Delhi, Bangalore and Pune. Phase III : Post Nineties 1991: Capital market orientation/reforms undertaken. The Indian financial system has witnessed a profound transformation since the launching of new economic policies .The developmental process shifted to free market economies and the government's role of distributing finance and credit has nosedived. The capital market had emerged as the main agency for earmarking resources to all Indian segments: public, private sector, and is facing competition with the state governments.

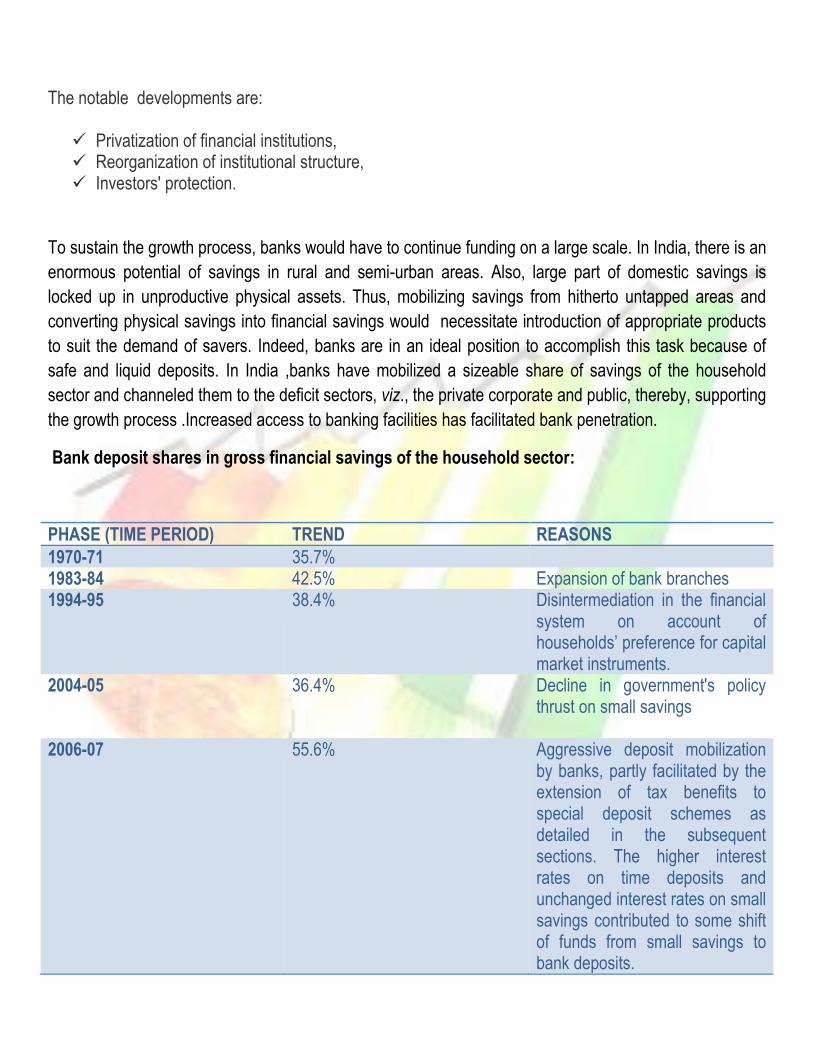

The notable developments are: Privatization of financial institutions, Reorganization of institutional structure, Investors' protection.

To sustain the growth process, banks would have to continue funding on a large scale. In India, there is an

enormous potential of savings in rural and semi-urban areas. Also, large part of domestic savings is

locked up in unproductive physical assets. Thus, mobilizing savings from hitherto untapped areas and

converting physical savings into financial savings would necessitate introduction of appropriate products

to suit the demand of savers. Indeed, banks are in an ideal position to accomplish this task because of

safe and liquid deposits. In India ,banks have mobilized a sizeable share of savings of the household

sector and channeled them to the deficit sectors, viz., the private corporate and public, thereby, supporting

the growth process .Increased access to banking facilities has facilitated bank penetration.

Bank deposit shares in gross financial savings of the household sector:

PHASE (TIME PERIOD) TREND REASONS

1970-71 35.7% 1983-84 42.5% Expansion of bank branches 1994-95 38.4% Disintermediation in the financial

system on account of households’ preference for capital market instruments.

2004-05 36.4% Decline in government's policy thrust on small savings

2006-07 55.6% Aggressive deposit mobilization by banks, partly facilitated by the extension of tax benefits to special deposit schemes as detailed in the subsequent sections. The higher interest rates on time deposits and unchanged interest rates on small savings contributed to some shift of funds from small savings to bank deposits.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

25 | P a g e

2014

1980 and 1990s onwards: generalized propensity towards mutual funds. Along these lines, tax

benefits were provided under Section 80M of the Income Tax Act. Under this section, the dividend

received by the companies was exempted from the income tax so long as the dividend paid by them was

more than the dividend received. Consequently, corporates invested large funds in the then Unit Scheme-

64 (US-64) of the erstwhile Unit Trust of India (UTI).

1987-88 and 1995-96: set up of 21 new mutual funds with 128 new schemes. Individual investors

were also attracted to units of mutual funds. Facing aggressive competition from newly established mutual

funds, UTI also followed a brisk policy of launching new schemes, especially during the latter half of the

1980s to meet investor’s diverse income and liquidity needs.

Mutual funds and direct investments in shares may provide higher returns than interest rates on bank

deposits, so people switched the household financial savings from bank deposits to shares and

debentures and units of mutual funds. Deposits mobilized by NBFCs during this phase also grew rapidly.

1970-80: Two-fold rise in NBFCs

1980-90: Eight-fold rise in NBFCs

1990-94: annual growth of financial assets increased to 44.6%. Alternatively, the share of bank

deposits in financial savings of the household sector plummeted during the same time frame.

An empirical study conducted for India also found that Mutual funds, non-convertible debentures (NCDs),

life insurance policies of LIC and small savings surrogated time/term deposits of scheduled commercial

banks.

October 1997: Deregulation of deposit rates by removing the links with the Bank Rate. Consequently,

the Reserve Bank gave the freedom to commercial banks to fix their own interest rates on domestic term

deposits of various maturities. Banks were encouraged to put a flexible interest rate system on deposits

(with a fixed rate option) in practice as early as possible in April 2002. Now banks have complete freedom

in fixing their domestic deposit rates, except interest rate on savings deposits, which continues to be

regulated and is currently stipulated at 3.5%.

Distinct and diverse bank features have ascended bank deposits over different time periods. In the phase

beginning immediately after nationalization of banks, bank deposit growth accelerated sharply as banks

were rapidly expanding their network to the village level to tap savings from rural areas.

Second phase, (1984-1995): Bank deposit growth decelerated as banks faced increased competition

from alternative saving instruments, especially capital market instruments (shares/debentures/units of

mutual funds) and non-banking financial companies. This was the phase of disintermediation as savings

were increasingly deployed in alternative saving instruments.

Third phase, (1995 - 2004): Further deceleration of bank deposits. They faced competition from post

office deposits, which carried significantly higher tax-adjusted returns than bank deposits. Nonetheless,

bank deposits maintained their share in the savings of the household sector.

Both ownership pattern and maturity pattern underwent considerable changes. Bank deposits held by the

Government and corporate sectors rose significantly, resulting in the slip of deposit shares by household

sector even as the share of banks deposits in household sector financial savings remained broadly

unchanged. The share of term deposits in total deposits increased attributed to the increment in the share

of the Government and the corporate sectors, as the share of the household sector in term deposits

declined. However, within term deposits, there was a significant shortening of maturity profile in favor of

short-term deposits.

SAVING OPTION AND THEIR RELEVANCE TO INDIAN INVESTORS

27 | P a g e

2014

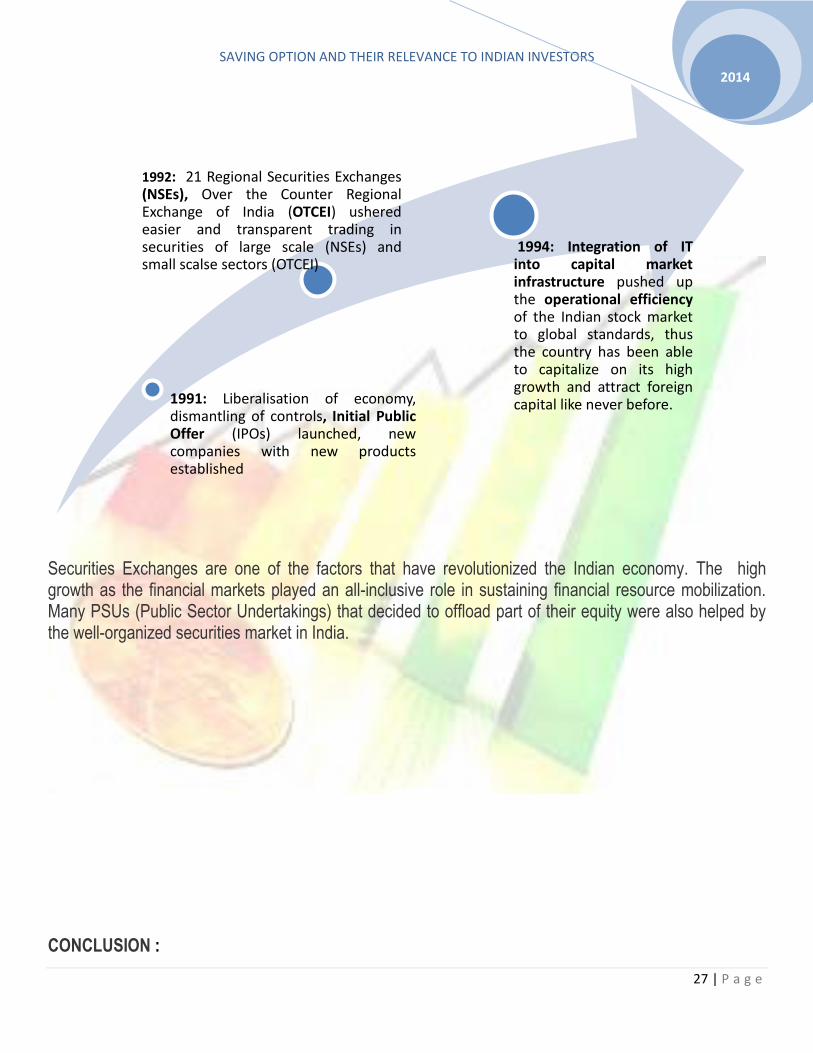

Securities Exchanges are one of the factors that have revolutionized the Indian economy. The high growth as the financial markets played an all-inclusive role in sustaining financial resource mobilization. Many PSUs (Public Sector Undertakings) that decided to offload part of their equity were also helped by the well-organized securities market in India.

CONCLUSION :

1991: Liberalisation of economy, dismantling of controls, Initial Public Offer (IPOs) launched, new companies with new products established

1992: 21 Regional Securities Exchanges (NSEs), Over the Counter Regional Exchange of India (OTCEI) ushered easier and transparent trading in securities of large scale (NSEs) and small scalse sectors (OTCEI)

1994: Integration of IT into capital market infrastructure pushed up the operational efficiency of the Indian stock market to global standards, thus the country has been able to capitalize on its high growth and attract foreign capital like never before.

Savings are important for individual as well as the economy. A high level of savings helps the economy to

progress on a continuous growth path since investment is mainly financed out of savings. In view of the

importance of savings , there have been extensive studies on various aspects of savings including the

behavioral side of it.

In India, the household sector has been the major contributor towards savings. The ultimate motives for

savings are provision for retirement and taking care of emergencies.

The measures vis-à-vis nationalizing banks and insurance companies for banks to reach out to

hinterlands, instituting UTI, strengthening the cooperative credit institution , deregulating the interest

rates etc have swelled in savings and their mobilization rates. With the development of capital market ,

there has been a skyrocketing preference for saving in market related instruments such as mutual funds

and equity due to maximum returns even though they are subject to market risks and losses. For risk

averse like salaried persons, NSC, government bonds are quite popular. Various tax saving schemes

have also elevated households' savings.

''I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.'' - Warren Buffett

Related Documents