8th Edition Your Online Resource for Chronic Disease Information™ www.managedcaredigest.com In this Volume New Program Characteristics and Medicaid Expansion Looking Forward to Next Generation ACOs 5,084,961 4,167,528 3,872,430 3,235,205 1,741,087 1,992,400 2,901,006 7,368,458 8,846,328 6,713,789 13.6% 4.6% 14.3% 22.8% 5.6% 9.5% 7. 8 % 10.0% 3.1% 6.4% MANAGED CARE DIGEST SERIES ® SIN C E 1 9 8 7 Public Payer Digest | 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8th EditionYour Online Resource for Chronic Disease Information™www.managedcaredigest.com

In this VolumeNew Program Characteristics and Medicaid Expansion

Looking Forward to Next Generation ACOs

5,084,9614,167,528

3,872,4303,235,2051,741,087

1,992,40 02,901,0 067,368,458 8,846,3286,713,789

13.6%4.6%

14.3%22.8%

5.6%9.5%7.8%

10.0 %3.1%6.4%

MANAGED CAREDIGEST SERIES®

SINCE 1987

Public Payer Digest | 2016

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

Leading the Health Care Discussion

The nationally renowned Sanofi Managed Care Digest Series®—now in its 30th year—is part of our

ongoing commitment to provide you with essential data on the important trends in U.S. health care.

Our goal is to help you remain on the leading edge of health care developments in America, and we

hope that this information helps you identify trends that may assist your organization, as the health care

delivery landscape continues to evolve.

Sanofi is pleased to provide you with your complimentary copy of this eighth edition of the

Public Payer Digest, the second report in the three-part Managed Care Digest Series® for 2016. This

Digest features extensive long-term trended data on, and in-depth analyses of, the Medicare and

Medicaid programs, as well as a variety of long-term care institution types. In addition, it is a rich source

of patient-level, chronic disease-specific, and hospital diagnosis-related discharge data.

Your Sanofi account executive or sales representative would be happy to provide you with additional

information on our products and services. Thank you for your commitment to the quality of health care

in America. We look forward to continuing our partnership with you in this important endeavor.

Sincerely,

Garrett Ingram U.S. Country Head of Market Access sanofi-aventis U.S. LLC A SANOFI COMPANY

Managed Care digest series® 2016

Commissioned, sponsored and underwritten by Sanofi, Bridgewater, NJ

Developed and produced by Forte Information Resources LLC, Denver, CO

Data provided by IMS Health, Parsippany, NJ

www.managedcaredigest.com

Inquiries relating to the mailing or distribution of the Managed Care Digest Series® can be addressed by calling 1-800-529-9615.

Managed Care Digest Series® is a registered trademark of Sanofi © 2016 sanofi-aventis U.S. LLC, A SANOFI COMPANY

1SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

CO

NTE

NTS

CONTENTS, VOL. 8

INTRODUCTION .................................................................................................3

EXECUTIVE SUMMARY .......................................................................................4

MEDICAREBackgrounder ..............................................................................................................................5

DemographicsMedicare Advantage Continues to Expand ............................................................................. 6

MA HMO Enrollment Edges That of MA PPOs in 2015 ................................................................ 7

UnitedHealth Remains Largest MA Organization, Grows Nearly 9% ....................................... 8

Enrollment Climbs for Medicare Advantage Plans .................................................................. 9

Medicare Inpatient Case Shares Climb for Six Selected Dxs ................................................. 10

UtilizationAdmissions Ratio Falls, ALOS Rises for Medicare HMO Members ........................................... 11

ALOS for Diabetes Mellitus Is Highest Among Profiled Dxs ...................................................... 12

Length of Stay Rises for Diabetes Mellitus Inpatient Cases ..................................................... 13

FinancialsManaged Care Share of Medicare Spending Grows ............................................................ 14

Inpatient Charges per Medicare Case Climb Steadily .......................................................... 15

Medicare Inpatient Reimbursement Increases ....................................................................... 16

Medicare Reimbursement Rate for Heart Failure Falls Again ................................................ 17

PharmacyDrug Cost Limits Shift Up for Part D Participants in 2016 .......................................................... 18

Ingredient Cost per Medicare HMO Rx Shrinks in 2015 ........................................................... 19

LIS Shares Dip Among Part D Diabetes, Oncology Patients ................................................... 20

Membership Grows for Most Top 10 PDP Enrollment States ................................................... 21

Pharmacy Costs per Staffed Bed Are Lower at Non-IHS Hospitals ........................................ 22

Part D Shares of Total Rxs Climb in 12 Common Drug Classes ............................................... 23

OOP Costs for Part D Rxs Fall for Half of Profiled Drug Classes ............................................... 24

Generic Shares of Common Medicare Prescriptions Rise ...................................................... 25

Numbers of Part D Retail Rxs Grow in Most Drug Classes ....................................................... 26

MEDICAIDBackgrounder ..................................................................................................................................... 27

Demographics

Medicaid Managed Care Penetration Nears 85% ................................................................. 28

Medicaid Portions Grow for Nearly Half of Profiled Inpatient Dxs ......................................... 29

Medicaid IP Case Portions Grow for Four Profiled Diagnoses ................................................ 30

Utilization

Hospital Days, Admit Ratios Fall at Not-for-Profit Medicaid HMOs ........................................ 31

Medicaid Discharges, Patient-Days Decline; ALOS Is Unchanged ....................................... 32

Financials

Provider Charges Climb for Medicaid Lipid Disorder Patients ............................................... 33

Pharmacy

Number of Prescriptions Dips per Member per Year for Medicaid ....................................... 34

Medicaid Portions of Retail Prescriptions Climb Steadily ........................................................ 35

Medicaid OOP Retail Rx Costs Rise for Most Drug Classes ..................................................... 36

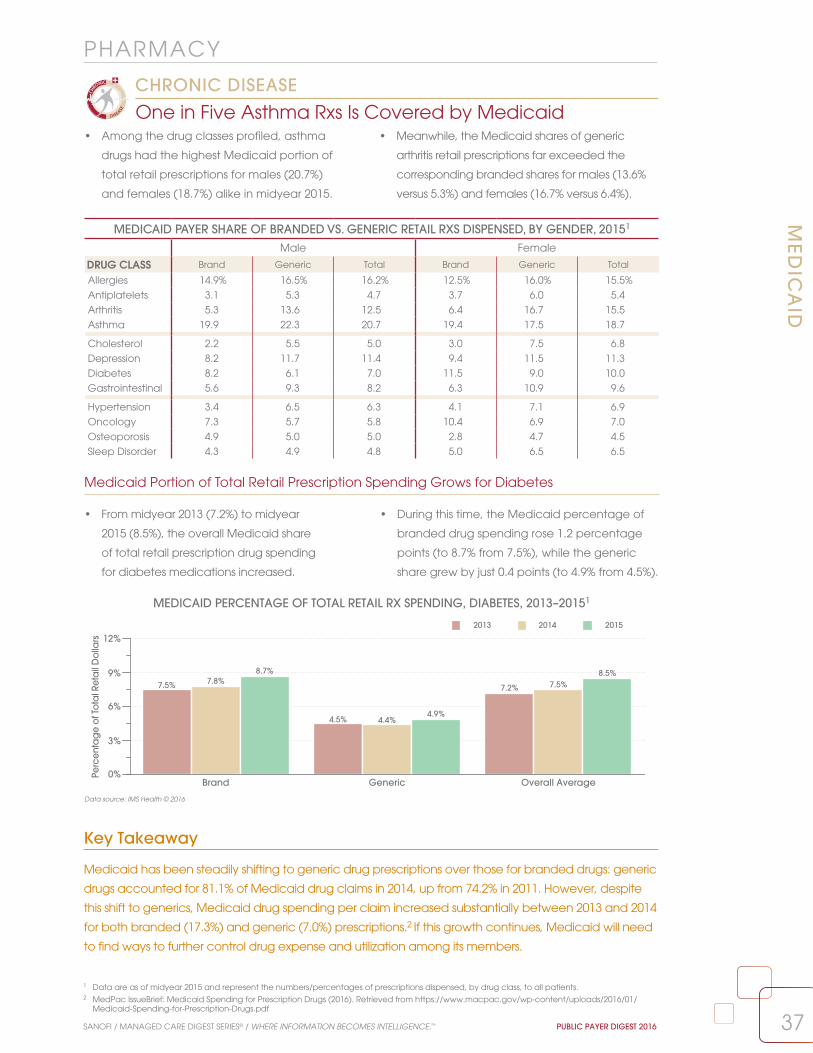

One in Five Asthma Rxs for Males Is Covered by Medicaid ................................................... 37

Vast Majority of Profiled Medicaid Drugs Are Generic ........................................................... 38

2 PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

CO

NTE

NTS LONG-TERM CARE

Backgrounder ............................................................................................................................39

Nursing Homes

DemographicsMajority of Nursing Homes Have More Than 100 Licensed Beds ........................................... 40

Genesis Has 41% More Facilities Than Its Closest Competitor ................................................ 41

UtilizationNursing Home Occupancy Rate, Patient-Days Count Fall .................................................... 42

Rates of Top Four NH Resident Conditions Surpass 50% .......................................................... 43

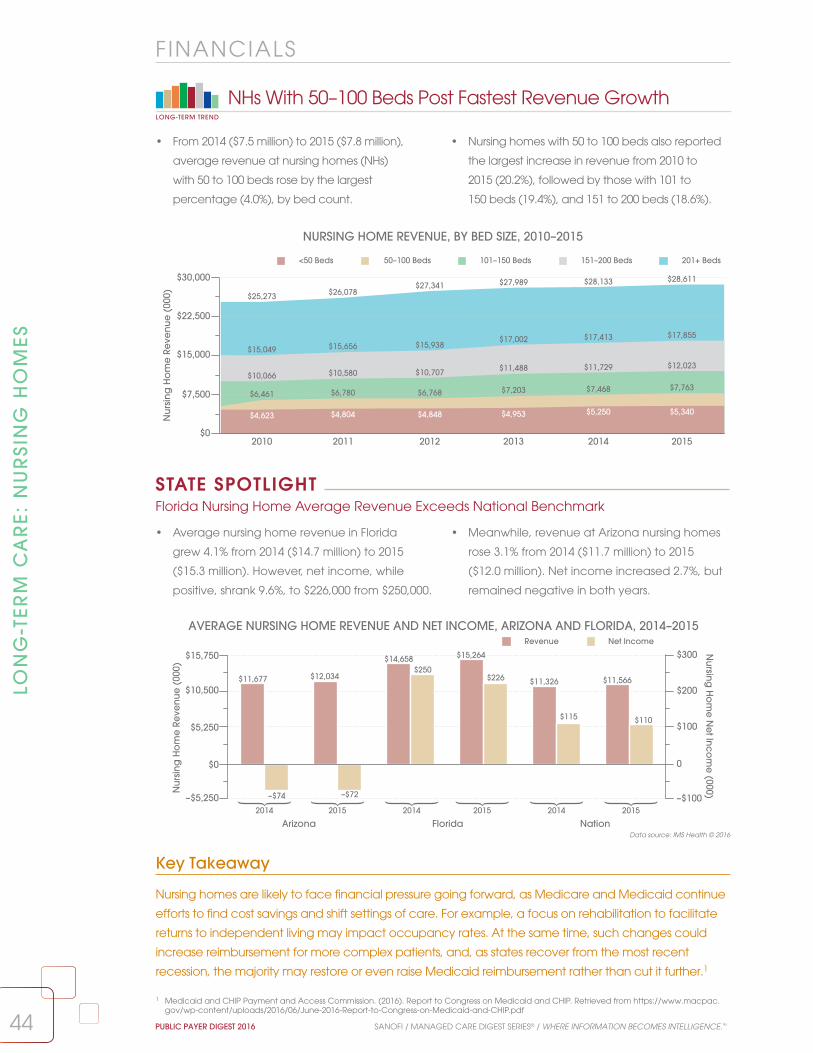

FinancialsNHs With 50–100 Beds Post Fastest Revenue Growth .............................................................. 44

Assisted Living Facilities

DemographicsNumber of ALFs Continues to Grow Slowly .............................................................................. 45

Brookdale Senior Living Is Nearly Four Times Larger Than No. 2 ALF ...................................... 46

Home Care Agencies

DemographicsHome Care Agency Count Rises for Second Year ................................................................. 47

Vast Majority of Home Care Agencies Are Not Facility Based .............................................. 48

Several Home Care Agencies Debut on List of 15 Largest Providers .................................... 49

UtilizationSkilled Nursing Remains Most Common HCA Service Provided ............................................. 50

Home Care Agency Weekly Visit Count Stays Flat ................................................................. 51

Hospital-Based SNFs

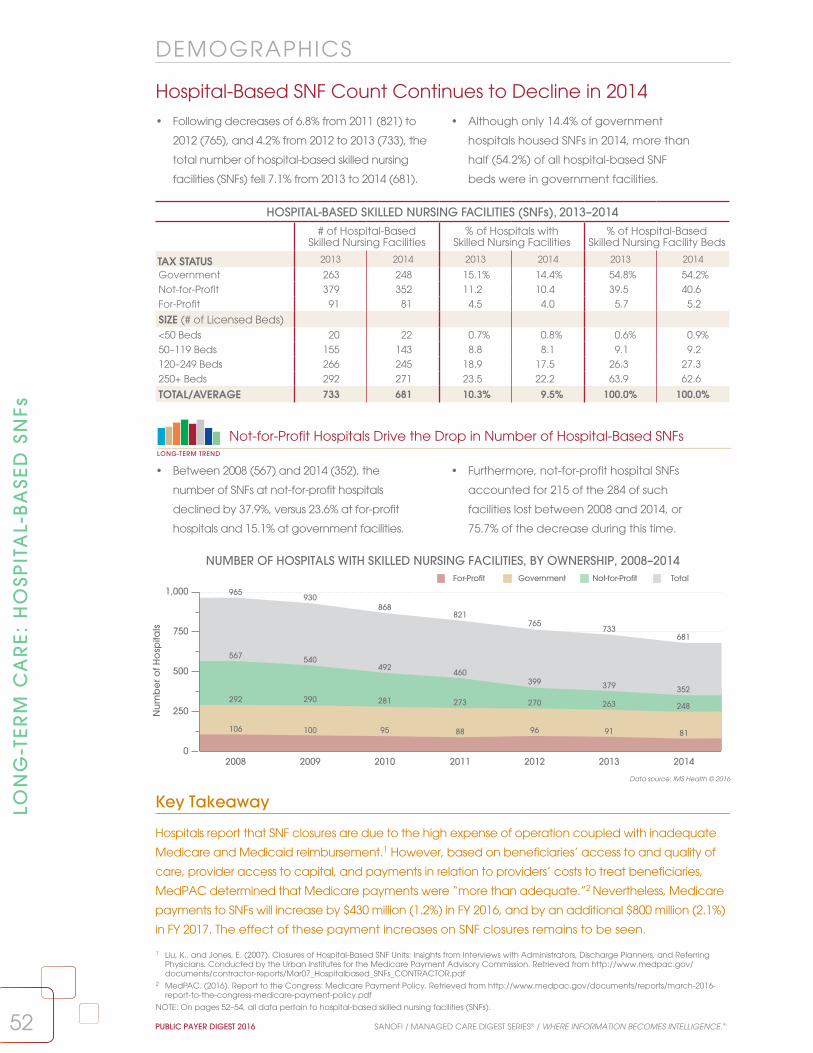

DemographicsHospital-Based SNF Count Continues to Decline in 2014........................................................ 52

UtilizationSNF Unit Average Length of Stay Declines Sharply Overall .................................................... 53

Admissions, Patient-Days Decline at Skilled Nursing Facilities ................................................ 54

LTCPPs

DemographicsLTCPP Count Grows for Fifth Consecutive Year ....................................................................... 55

UtilizationMonthly Prescriptions Continue to Decrease for LTCPPs ........................................................ 56

FinancialsRx Costs Increase More Rapidly for Independent LTCPPs ...................................................... 57

LOOKING FORWARD.......................................................................................58

RESEARCH METHODOLOGY ...........................................................................60

KEY TERMS ........................................................................................................62

REFERENCES .....................................................................................................64

CONTENTS, VOL. 8 (cont.)

Comparative information at regional, state, and local levels is available by contacting your

Sanofi account executive.

The Medicare section reviews the most important

aspects of this crucial program, including

demographic overviews of Medicare Advantage

(MA), Medicare HMOs and hospital-based

Medicare. Utilization measures are also

showcased, and feature chronic-disease specific

hospital metrics for Medicare HMO members.

The financial section includes inpatient charges

for the treatment of Medicare beneficiaries and

Medicare reimbursement rates for common

diagnoses and procedures. Pharmacy utilization,

out-of-pocket costs, and retail prescription use are

also tracked. The effects of developing payment

models such as accountable care organizations

(ACOs), the Medicare Shared Savings Program,

and Next Gen ACOs are spotlighted in this section.

The Medicaid section includes trended

data on the program and its unparalleled

expansion, and spotlights how the industry is

adapting to care for its growing population.

Demographic data on common diagnoses

and procedures for Medicaid recipients are

featured, along with inpatient payer shares

of chronic disease cases. Hospital utilization,

including discharges, patient-days and length

of stay, is tracked for Medicaid HMO members

and the Medicaid population overall. Provider

and facility charges for Medicaid recipients in

inpatient and outpatient settings are featured,

as are key pharmacy benchmarks, such as

out-of-pocket costs and retail prescription

spending for common therapeutic drug classes.

The Long-Term Care section profiles the providers

and institutions serving the senior population—

again a growing sector in the health care

industry—including nursing homes, assisted living

facilities, home care agencies, hospital-based

skilled nursing facilities, and long-term care

pharmacy providers. Demographic, utilization,

financial, and pharmacy metrics are provided,

including facility counts, admission, and

occupancy rates, and commonly provided

services. Data about the nation’s largest

long-term care chains are likewise featured.

Backgrounders for each section of the Public

Payer Digest provide an overview of the topic

at hand, and key takeaways contextualize the

metrics, examining the implications of the subjects

under discussion. The data that appear in the

Public Payer Digest continue to distinguish this

important work, as well as the Managed Care Digest Series® as a whole. Decade-long trends

of industry measures are featured throughout

this Digest, lending historical perspective to

health care topics examined. Data analyzing

the significant impact of chronic disease—

patient-level claims data and diagnosis-related

hospital discharge data—likewise appear

throughout and provide valuable insight into how

Medicare beneficiaries, Medicaid recipients, and

long-term care patients are being treated for

chronic conditions. Important industry trends and

chronic disease metrics are often examined at the

regional, state, or MSA level to highlight how health

care is managed and delivered at the local level.

Sanofi is pleased to present volume 8 of the Public Payer Digest, the second report in the Sanofi

Managed Care Digest Series® for 2016. Since 1987, the Managed Care Digest Series® has focused on

helping health care organizations develop strategies, control costs, and assess value. Now in its 30th year,

the Managed Care Digest Series® remains a trusted source for the most reliable health care data and

progressive analysis, including detailed diagnosis-related, chronic disease-specific patient claims and

hospital discharges. As the population changes and the health care industry evolves, the Managed Care Digest Series® maintains its commitment to leading the health care discussion.

Medicare and Medicaid cover more lives than ever, making the in-depth profiles in the

Public Payer Digest uniquely valuable and more relevant than ever. The 2016 edition examines

the many facets of these programs and explores how legislative reforms affect them. The Digest

also analyzes the various long-term care institutions providing health care services to a large and

growing segment of the U.S. population. The three main topics (Medicare, Medicaid, and long-term

care) of this Digest are each divided into four distinct subsections of data elements: demographics,

utilization, financials, and pharmacy. Clear analyses and insightful key takeaways bring perspective to

the Public Payer Digest’s unparalleled data sets.

3SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

INTR

OD

UC

TION

INTRODUCTION

Medicare• In 2015, Medicare insured 54.5 million

Americans, or roughly one in every six people.

Of this population, 17.3 million beneficiaries

were enrolled in Medicare Advantage (MA)

plans, a 6.1% increase from 2014 (16.3 million).

• Six of the top 10 MA organizations, by

enrollment, recorded membership growth

between 2014 and 2015.

• For only the second time since 2010, MA HMO

enrollment increased faster than that of

MA PPO plans, with enrollment in MA HMO

plans (6.5%) narrowly outpacing that of

MA PPO plans (5.6%) from 2014 to 2015.

• The number of hospital admissions per

1,000 Medicare HMO members decreased

for the second consecutive year in

2015, to 250.2 from 253.4 in 2014.

• For the 11th consecutive year, the managed

care share of total Medicare expenditures

increased, to 27.4% in 2015 from 26.7% in 2014.

• For eight of the 10 top states, by Medicare

Part D prescription drug program (PDP)

enrollment, membership counts increased from

2015 to 2016. Collectively, PDP enrollment in

these top 10 states increased by 2.1%.

Medicaid• At the end of 2015, the Medicaid program

covered 72.4 million individuals, a 20.7%

increase in average monthly enrollment

from the 2013 pre-Affordable Care Act

(ACA) expansion baseline of 60 million.

• Medicaid recipients enrolled in a managed

care organization (MCO) represented 84.9%

of total Medicaid enrollees in 2015, up 14.6

percentage points from 2008 (70.3%).

• From 2014 to 2015, the number of hospital

days and admissions per 1,000 Medicaid HMO

members decreased at not-for-profit HMOs;

these ratios increased at for-profit HMOs.

• The average number of Medicaid hospital

discharges fell fractionally (1.1%) from 2013

(1,104.0) to 2014 (1,092.4). Meanwhile, average

length of stay (ALOS) per inpatient Medicaid

case remained unchanged, at 4.4 days.

• Average annual professional charges for

Medicaid lipid disorder patients rose by double-

digit percentages across profiled care settings

from 2013 to 2015, most notably at skilled nursing

facilities (47.8%) and emergency rooms (28.5%).

• From midyear 2014 to midyear 2015, out-

of-pocket (OOP) costs per Medicaid

retail prescription grew across eight

of the 12 featured drug classes.

Long-Term Care• Following an increase from 2013 (1.65 million) to

2014 (1.67 million), the total number of licensed

nursing home beds in the U.S. grew for a second

year, to 1.68 million in 2015 (up 1.5% since 2013).

• From 2014 (82.2%) to 2015 (81.5%), the

average occupancy rate for nursing

homes (NHs) overall declined fractionally,

as did total facility patient-days (to 32,142

from 32,553), and the total facility ALOS

rose by two days (to 180 from 178).

• NHs reported annual increases in revenue

from 2014 to 2015, regardless of bed size;

NHs with 50 to 100 beds posted the largest

percentage gains, by bed count, at 4.0%.

• After a decline over the three-year period

from 2010 to 2012, the total number of

assisted living facilities (ALFs) in the U.S.

rose, to 15,836 in 2015 from 15,447 in 2012,

topping the previous high of 15,781 in 2010.

• In 2015, a total of 11,543 home care

agencies (HCAs) were not physically

located in hospital facilities, up 4.0% from

2013 (11,104). Non-facility-based agencies

accounted for nearly 90% of all HCAs.

• ALOS at skilled nursing facilities (SNFs)

dropped 10.8% from 2013 (179.9 days) to

2014 (160.4). Overall SNF unit admissions and

patient-days also fell during this period.

4 PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

EX

EC

UTI

VE

SU

MM

AR

Y

EXECUTIVE SUMMARY

5SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

In 2015, Medicare insured 54.5 million Americans,

or roughly one in every six people in the U.S.1 A

wide variety of entities, from traditional payers

to emergent institutions like accountable care

organizations (ACOs), are aiding the program in

managing the care of this significant population.

Indeed, private managed care organizations

are assuming a greater role in handling the

health of Medicare beneficiaries, as enrollment

in Medicare Advantage (MA) plans—including

Medicare HMOs—grows alongside Medicare

membership. Yet Medicare is still very much a

public program, subject to legislative changes

and limited resources. Should these limited

resources necessitate reduced payments to

providers, physician participation may be

negatively affected. The Medicare Access and

CHIP Reauthorization Act of 2015 (MACRA) was

designed to prevent a major cut, but still set

payment updates at a rate that lags expected

cost increases.2 This, too, may impact physician

participation at a time of heightened demand.

MEDICAREBackgrounder

6.2 6.2 6.6 7.4 7.6

10.4 11.08.7

9.9 10.4 11.012.5

14.716.3

17.3

44.2 44.8 45.8 46.4 48.4 50.2 51.8 53.4 54.5

2007 2008 2009 2010 2011 2012 2013 2014 20150

7

14

40

60

Enro

llme

nt (

Mill

ion

s)

Medicare HMOs MA Plans Medicare

8.7 9.4

13.3

MA Plan and Medicare HMO Enrollment vs. Medicare Overall, 2007–20153

LONG-TERM TREND

Data sources: IMS Health and the Centers for Medicare & Medicaid Services © 2016

1 U.S. Census Bureau. (2016). U.S. and World Population Clock. Retrieved from http://www.census.gov/popclock/2 Centers for Medicare & Medicaid Services. (2016). 2016 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal

Supplemental Medical Insurance Trust Funds. Retrieved from https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2016.pdf

3 Enrollment figures are year-end totals, and do not include Medicare Advantage enrollees in Puerto Rico and U.S. territories.

TOP 10 STATES, RANKED BY MEDICARE ADVANTAGE ENROLLMENT, 2014–20151

STATE Enrollment 2014 Enrollment 2015 Percentage Change 2014–2015

California 2,230,464 2,353,403 5.5%

Florida 1,543,127 1,650,256 6.9

New York 1,193,779 1,223,595 2.5

Texas 1,084,129 1,212,507 11.8

Pennsylvania 996,122 1,022,260 2.6

Ohio 879,957 829,795 –5.7

Michigan 581,964 647,611 11.3

North Carolina 501,674 535,977 6.8

Minnesota 472,927 506,126 7.0Georgia 451,894 500,143 10.7

1 Enrollment figures are year-end totals and do not include Medicare Advantage enrollees in Puerto Rico and U.S. territories.2 Jacobsen, G., et al. (2015). Medicare Advantage 2016 Data Spotlight: Overview of Plan Changes. Retrieved from http://kff.org/medicare/

issue-brief/medicare-advantage-2016-data-spotlight-overview-of-plan-changes/

Key Takeaway

In 2016, beneficiaries enrolling in an MA plan have, on average, 19 different plans to choose from,

offered by six different insurance providers.2 Yet participants who remain with their current plans may

see an increase in cost sharing: premiums for enrollees in MA plans with a prescription drug component

will rise by 8%, and out-of-pocket limits on Parts A and B benefits will also go up.2 Plans may continue to

shift how they share costs with enrollees, as they also adjust to higher enrollment and medical costs.

4%

11%

18%

25%

32%

2

6

10

14

18

Enro

llme

nt (

Mill

ion

s)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MA

Pen

etra

tion

Total Enrollees Total Penetration

5.56.0

7.2

8.7

9.910.4

11.0

12.513.3

14.7

12.8%13.6%

16.8%

19.5%

22.1% 22.7%23.6%

25.7% 26.4%28.4%

16.3

30.5%

17.3

31.7%

MEDICARE ADVANTAGE ENROLLMENT AND PENETRATION INTO MEDICARE, 2004–20151

Data sources: IMS Health and the Centers for Medicare & Medicaid Services © 2016

66

DEMOGRAPHICSM

ED

ICA

RE

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

• Total MA membership grew from 2014 to 2015

in nine of the 10 top states (Ohio excepted).

Double-digit enrollment growth occurred in Texas

(11.8%), Michigan (11.3%), and Georgia (10.7%).

• Collectively, MA enrollment in these 10 states

increased by 5.5% from 2014 (9.9 million) to 2015

(10.5 million), accounting for more than 60% of

national enrollment in such plans in 2015.

Most States With High MA Enrollment See Continued Growth in Membership Counts

STATE SPOTLIGHT

• Medicare Advantage (MA) plans enrolled

17.3 million beneficiaries in 2015, a 6.1%

increase over 16.3 million the prior year. From

2004 (5.5 million) to 2015, total participation in

such plans has grown more than threefold.

• The MA share of beneficiaries also rose in

2015, to 31.7% from 30.5% in 2014. However,

this increase (1.2 percentage points) in

penetration represented a slowdown from the

2.1 point growth from 2013 (28.4%) to 2014.

Medicare Advantage Continues to ExpandLONG-TERM TREND

Data sources: IMS Health and the Centers for Medicare & Medicaid Services © 2016

0.0%

17.0%

34.0%

51.0%

68.0%

Ave

rag

e L

eng

th o

f Sta

y (D

ays

)

PPO HMO

2009 2010 2011 2012 2013 2014 2015

17.0%

63.9%

25.7%

60.1%

28.3%

63.6%

28.3%

65.4%

30.4%

63.8%

31.1%

63.5%

31.0%

63.8%

SHARE OF MA ENROLLMENT BY PLAN TYPE, 2009–2015

MEDICARE ADVANTAGE (MA) ENROLLMENT, BY PLAN TYPE, 2010–20151

PLAN TYPE 2010 2011 2012 2013 2014 2015HMO 7,136,633 7,919,458 8,690,663 9,388,510 10,350,493 11,024,064

PPO 2,818,592 3,526,360 3,739,660 4,481,424 5,064,674 5,347,728

PFFS 572,540 516,975 405,954 305,965 258,189 237,033

Other2 442,179 491,271 442,092 548,675 615,456 662,478TOTAL 10,969,944 12,454,064 13,278,369 14,724,574 16,288,812 17,271,303

1 Enrollment figures are year-end totals and do not include Medicare Advantage enrollees in Puerto Rico and U.S. territories.2 “Other” includes Cost, MSA, PACE, PSO (state license), and Pilot plans.3 Jacobsen, G., et al. (2015). Medicare Advantage 2016 Data Spotlight: Overview of Plan Changes. Retrieved from http://kff.org/medicare/issue-

brief/medicare-advantage-2016-data-spotlight-overview-of-plan-changes/4 Abrahams, B. (2016). The Different Types of Medicare Advantage Plans. Medicare.com. Retrieved from: https://medicare.com/medicare-

advantage/the-different-types-of-medicare-advantage-plans/

7

DEMOGRAPHICS

7

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

Key Takeaway

MA PPO plans are often less restrictive than MA HMO plans because they allow enrollees to seek

specialty care without a referral and offer partial coverage for out-of-network care.3 Such flexibility

may explain the rising share of PPO enrollment as a portion of total MA enrollment. However, given that

out-of-pocket costs for MA plans are rising,3 and that MA PPO plans usually have higher costs to begin

with,4 it remains unclear whether growth in the PPO percentage of MA enrollment has leveled off.

PPO Portion of Total MA Enrollment in 2015 Is Almost Twice That of 2009

• From 2009 (17.0%) to 2015 (31.0%), PPO

enrollment as a percentage of total MA

enrollment nearly doubled. During this

period, the share peaked at 31.1% in 2014.

• The HMO portion of total MA enrollment

remained virtually flat from 2009 (63.9%) to 2015

(63.8%). This percentage was at its highest in

2012 (65.4%) and its lowest in 2010 (60.1%).

• The percent rise in MA HMO enrollment from

2014 to 2015 (6.5%) narrowly surpassed that of

MA PPO plans (5.6%), marking only the second

time since 2010 that MA HMO enrollment

increased more than that of MA PPO plans.

• From 2010 (2,818,592) to 2015 (5,347,728),

MA PPO enrollment climbed 89.7%, notably

faster than the percent rise in MA HMO

enrollment (54.5%; to 11,024,064 from 7,136,633).

Conversely, enrollment in PFFS plans declined.

MA HMO Enrollment Edges That of MA PPOs in 2015LONG-TERM TREND

88

DEMOGRAPHICSM

ED

ICA

RE

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

10 LARGEST MEDICARE ADVANTAGE ORGANIZATIONS, BY ENROLLMENT, 20152

0 900,000 1,800,000 2,700,000 3,600,000

MA Enrollment

Health Net Inc.

Highmark Inc.

Blue Cross Blue Shield of Michigan

WellCare Health Plans Inc.

Cigna

Anthem Inc.

Aetna Inc.

Kaiser Foundation Health Plan Inc.

Humana Inc.

UnitedHealth Group Inc. 3,505,904

3,253,465

1,347,939

1,278,486

627,252

505,800

405,911

355,136

295,946

291,897

ENROLLMENT BY PLAN TYPE, HUMANA INC., 2011–20152

2011 2012 2013 2014 20150

900,000

1,800,000

2,700,000

3,600,000

MA

En

rollm

en

t

696,032

23,629460,778

271,476

880,512

72,854

797,783

241,478

1,028,549

45,768

816,903

211,252

1,312,628

17,522

880,213

19,376 174,942

1,582,841

5,659

986,012

17,556 156,719

489,875

330,992391,030

528,897

504,678

HMO HMO-POS Local PPO Medicare-Medicaid Plan HMO PFFS3 Regional PPO

MA Enrollment in Humana HMOs and Local PPOs Doubles From 2011 to 2015

• Over the five years profiled, Humana MA

enrollment more than doubled in HMO (to

1.6 million in 2015 from 696,032 in 2011) and

local PPO (to 986,012 from 460,778) plans.

• Meanwhile, membership in Humana’s HMO-POS

and PFFS plans fell over this time frame by 76.1%

and 42.3%, respectively. Humana regional

PPO enrollment rose by a modest 3.0%.

Data source: Centers for Medicare & Medicaid Services © 2016

UnitedHealth Remains Largest MA Organization, Grows Nearly 9%

• UnitedHealth Group was again the largest

Medicare Advantage (MA) organization,

by enrollment, in 2015, with more than

3.5 million members, up 8.7% from 2014.1

• Six of the top 10 MA organizations, by enrollment,

recorded membership increases between 2014

and 2015. Membership in Humana and Aetna

MA plans each rose by 10.9% during this period.

PLAN SPOTLIGHT

1 See the Public Payer Digest for 2015.2 Data are current as of end-of-year 2015.3 Private fee-for-service4 Merle, R., and Johnson, C. (2016). Justice Department Sues to Block Two Health-Care Mega-Mergers. The Washington Post. Retrieved from

https://www.washingtonpost.com/news/business/wp/2016/07/21/justice-department-sues-to-block-anthem-acquisition-of-cigna/

Key Takeaway

In 2015, two health plan mergers (Aetna with Humana and Anthem with Cigna) totaling $85 billion

were announced. In July 2016, the U.S. Department of Justice sued to block these deals, citing lack

of competition for both commercial and MA plans. Although the corporations argue that merging

provides network expansion and efficiencies for consumers, these groundbreaking deals may not pass

regulatory scrutiny, unless the companies make structural changes to alleviate antitrust concerns.

1 CMS. (2016). Medicare Shared Savings Program Accountable Care Organizations. Retrieved from https://data.cms.gov/ACO/2016-Medicare-Shared-Savings-Program-Accountable-C/i683-k66m

2 Dawe, C., et al. (2016). Today’s Most Attractive National ACO Model Is Offered by . . . CMS. Health Affairs. Retrieved from: http://healthaffairs.org/blog/2016/04/15/todays-most-attractive-national-aco-model-is-offered-bycms/

3 See page 7 of this Public Payer Digest.

Data source: Centers for Medicare & Medicaid Services © 2016

Data source: IMS Health © 2016

9

DEMOGRAPHICS

9

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

Key Takeaway

In its Next Generation ACO pilot, the Centers for Medicare & Medicaid Services (CMS) attempted

to address provider criticisms of the Shared Savings Program, including the percentage of

savings providers are entitled to receive, beneficiary assignment processes, network design,

and risk adjustment.2 If the Next Generation model succeeds, it could be the catalyst that

prompts greater provider acceptance of, and participation in, the ACO program.

MEDICARE ADVANTAGE ENROLLMENT VS. MEDICARE HMO ENROLLMENT, 2007–2015

2007 2008 2009 2010 2011 2012 2013 2014 20154

8

12

16

20

Enro

llme

nt (

Mill

ion

s)

Medicare HMOsMedicare Advantage Plans

6.2 6.2 6.67.4 7.6

8.79.4

10.411.08.7

9.910.4

11.0

12.513.3

14.7

16.317.3

Enrollment Climbs for Medicare Advantage (MA) Plans LONG-TERM TREND

• From 2007 (6.2 million) to 2015 (11.0 million), the

number of MA HMO enrollees increased 77.4%.

Total MA enrollment rose 98.8%, to 17.3 million

from 8.7 million, during the same time period.

• Between 2007 and 2008, the MA HMO

percentage of total MA enrollment fell from

71.3% to 63.6%. Since then, this portion of MA

enrollment has never risen above 65.5%.3

Concentration ofACOs by State

1–7

8–15

16–23

24–31

32–39

40+

Next Gen ACOs

0

2

2

22

2

1

11

1

1

1

1

1

CONCENTRATION OF SSP ACCOUNTABLE CARE ORGANIZATIONS (ACOs), 20161

Next Generation ACOs Debut in 13 States as Part of CMS Pilot Program

ACO SPOTLIGHT

1010

DEMOGRAPHICS

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

ME

DIC

AR

E

1 Percentages do not sum to 100% because there is also an “other” payer category that is not shown, which includes self-pay, charity, workers’ compensation, and unknown payer sources.

2 Includes HMOs, PPOs, point-of-service plans, and exclusive provider organizations.3 Graham, J. (2013). Medicare to Cover More Mental Health Costs. New York Times. Retrieved from http://newoldage.blogs.nytimes.

com/2013/12/27/medicare-to-cover-more-mental-health-costs/?_r=0

Data source: IMS Health © 2016

NUMBER AND PERCENTAGE OF INPATIENT CASES PER HOSPITAL PER YEAR, BY PAYER TYPE, 2013–20141

Medicare Medicaid Commercial Insurance2

# of Cases % of Cases # of Cases % of Cases # of Cases % of Cases

DISEASE STATE 2013 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013 2014

ACS 120.7 123.1 68.2% 66.4% 15.4 19.3 6.4% 8.1% 39.7 43.2 19.1% 20.2%

Angina 23.3 37.1 65.5 66.4 4.5 8.4 7.7 7.2 8.7 17.3 19.8 21.7

Asthma 163.0 132.2 35.8 37.2 120.8 89.4 26.3 24.3 126.3 113.5 28.0 30.9

Breast Cancer 18.7 86.3 44.1 45.3 6.9 32.9 13.4 11.9 17.0 85.8 37.6 38.6

Depression 132.9 38.8 35.7 42.9 95.2 22.1 24.8 21.9 98.8 26.7 25.8 25.1

Diabetes Mellitus 799.0 578.8 61.3 60.6 150.9 113.5 11.6 11.6 239.7 200.2 18.8 20.8

Hypertension 1,160.9 926.7 60.0 59.3 182.8 153.0 9.4 9.6 417.0 383.5 22.1 24.4

Lipid Disorders 625.8 640.7 64.5 64.3 59.1 72.1 5.7 6.8 234.3 243.0 23.6 23.9

Osteoarthritis 109.8 55.5 59.0 58.9 8.7 7.6 3.5 3.5 63.5 35.2 32.3 33.3

Prostate Cancer 27.2 40.2 64.9 67.4 3.5 5.7 3.5 2.5 15.3 24.9 27.3 27.3

Rheumatoid Arthritis 51.6 45.4 67.1 67.1 7.1 6.9 7.2 6.6 17.3 18.2 20.7 22.7

Stroke 133.8 37.2 70.6 72.7 14.4 4.9 6.2 4.7 33.8 13.1 16.4 18.0

CHRONIC DISEASE

MEDICARE PAYER SHARE OF INPATIENT CASES, 2010–2014

20%

35%

50%

65%

80%

Perc

en

tag

e o

f Ca

ses

2010 2011 2012 2013 2014

Asthma Depression Prostate Cancer Stroke

33.9% 34.3% 34.1%

35.8%

37.2%

35.3% 35.5% 36.0%

35.7%

42.9%

62.7% 62.0% 63.7% 64.9%67.4%

70.6% 70.0% 70.2% 70.6% 72.7%

LONG-TERM TREND

Key Takeaway

As required by the Medicare Improvements for Patients and Providers Act of 2008, Medicare began

covering 80% of beneficiaries’ outpatient psychological counseling costs in 2014—the same amount

as that of most other medical services.3 Lower patient costs may have prompted more beneficiaries to

seek psychological care, perhaps leading to a rise in diagnoses that resulted in inpatient treatment.

• The Medicare percentages of inpatient

cases per hospital increased from 2013 to

2014 for angina, asthma, breast cancer,

depression, prostate cancer, and stroke.

• Of the profiled disease states, stroke (72.7%)

accounted for the largest share of inpatient

Medicare cases and asthma (37.2%)

made up the smallest portion in 2014.

Medicare Inpatient Case Shares Climb for Six Selected Dxs

• From 2010 (35.3%) to 2014 (42.9%), the

Medicare portion of inpatient depression

cases grew 7.6 percentage points, with most

of the growth occurring from 2013 to 2014.

• Similarly, after remaining virtually flat from 2010

through 2013 (70.6%), the share of Medicare

inpatient stroke cases expanded 2.1 percentage

points from 2013 to 2014, reaching 72.7%.

Medicare Percentage of Inpatient Depression Cases Increases Rapidly

11

UTIL IZATION

11

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

Data source: IMS Health © 2016

Key Takeaway

Hospital admissions per 1,000 Medicare HMO members fell 9.2% from 2013 to 2015, indicating that

efforts to shift care away from the inpatient setting may be working. However, after also dropping

from 2013 to 2014, both hospital days and ALOS increased from 2014 to 2015. This may be attributable

to a variety of factors, but it is quite possibly a reflection of the balance hospitals are trying to strike

between the cost of extended inpatient stays and the penalties they face for excess readmissions.

Admissions Ratio Falls, ALOS Rises for Medicare HMO Members

• The number of hospital admissions per 1,000

Medicare HMO members fell in 2015, to 250.2

from 253.4 in 2014. This was the second year of

decline, following an increase from 2012 to 2013.1

• Even as admission counts fell, average

length of stay (ALOS) per Medicare hospital

admission continued to rise, reaching 6.7 days

in 2015, from 6.6 in 2014 and 6.3 in 2013.1

NUMBER OF HOSPITAL DAYS PER 1,000 MEDICARE HMO MEMBERS, 2005–20152

UTILIZATION RATES FOR MEDICARE HMO MEMBERS, 2014–20152

Hospital Days per 1,000 Medicare HMO Members

Hospital Admissions per 1,000 Medicare HMO Members

ALOS (Days) per Medicare

Hospital Admission

MD Encounters per Medicare

HMO Member3

Ambulatory Visits per Medicare

HMO Member3

TAX STATUS OF HMO 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015

For-Profit 1,685.0 1,732.2 252.0 247.0 6.8 7.0 10.4 10.3 4.9 5.5

Not-for-Profit 1,530.0 1,536.5 256.5 257.1 6.1 6.0 9.8 8.9 4.0 4.1

OVERALL AVG. 1,638.3 1,672.4 253.4 250.2 6.6 6.7 10.2 9.9 4.7 5.0

Medicare HMO Hospital-Days Ratio Increases at For-Profit HospitalsLONG-TERM TREND

• Hospital days per 1,000 Medicare HMO members

at for-profit hospitals climbed 47 days from

2014 (1,685) to 2015 (1,732), compared with just

seven (to 1,537 from 1,530) at not-for-profits.

• Although the rate of growth in the hospital-

days ratio at not-for-profit facilities from 2005

to 2015 (32.7%) was more than three times

that of their for-profit counterparts (10.8%).

1 See the Public Payer Digest for 2014 and 2015.2 Only HMOs that enroll Medicare beneficiaries are included.3 Ambulatory visits differ from physician encounters. Ambulatory visits are visits by an HMO member to an HMO clinic or physician’s office that do not

require the services of a physician. Such visits are usually made for tests, prescription refills, immunizations, etc. The term “physician encounter” is self-explanatory.

1,000

1,250

1,500

1,750

2,000

Nu

mb

er o

f Da

ys

1,5631,642

1,5731,527

1,558

1,6181,645

1,597

1,7631,685

1,732

1,158

1,342 1,355

1,452

1,601

1,5901,639

1,616

1,645

1,530 1,537

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

For-Profit Not-for-Profit

1212

UTIL IZATION

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

ME

DIC

AR

E

Data source: IMS Health © 2016

• In 2014, average length of stay (ALOS) per

inpatient (IP) Medicare diabetes mellitus

case exceeded those of the other profiled

diagnoses, regardless of hospital size or

multihospital system (MHS) ownership.

• For six of the nine profiled diagnoses, ALOS

for inpatient Medicare cases at non-MHS-

owned facilities surpassed the corresponding

means for MHS-owned hospitals, as well

as the overall averages, in 2014.

ALOS for Diabetes Mellitus Is Highest Among Profiled Dxs

CHRONIC DISEASE

2012

Ave

rag

e L

en

gth

of S

tay

(Da

ys)

2013 2014

0

1

2

3

4

In a Highly IntegratedHealth System

Not in a Highly IntegratedHealth System

Overall Average

3.6

— 2.5 —

3.7

2.6 2.7

3.6

— 2.5 —

AVERAGE LENGTH OF STAY (DAYS) PER INPATIENT PROSTATE CANCER CASE, 2012–2014

AVERAGE LENGTH OF STAY (DAYS) PER MEDICARE HOSPITAL INPATIENT CASE, 2014

SIZE ACS Angina Asthma Breast Cancer

Diabetes Mellitus

Hyper-tension

Prostate Cancer

Rheu-matoid Arthritis

Stroke

<50 Beds 1.9 — 3.7 2.2 3.9 2.5 1.5 — 3.5

50–119 Beds 2.3 2.0 3.9 2.5 4.4 2.5 1.9 — 3.5

120–249 Beds 2.4 2.5 4.2 2.7 5.0 2.7 2.7 3.0 4.0

250+ Beds 2.5 2.2 4.3 2.9 5.6 2.7 2.5 3.6 4.6

MHS OWNERSHIP

MHS Owned 2.4 2.2 4.2 2.8 5.0 2.7 2.5 3.6 4.0

Non-MHS Owned 2.7 2.4 4.3 3.3 4.8 2.9 2.9 3.1 3.9

OVERALL AVG. 2.4 2.2 4.2 2.8 4.9 2.7 2.5 3.5 4.0

ALOS Declines for Inpatient Prostate Cancer Cases in Integrated, Non-Integrated Facilities

• Regardless of affiliation with a highly integrated

health care system, ALOS per inpatient

prostate cancer case decreased from 2012

to 2014. Nationally, ALOS for such cases fell

to 2.5 days from 3.6 days during this time.

• ALOS per inpatient prostate cancer case at

hospitals not belonging to a highly integrated

health system (2.7 days) remained above that

of hospitals in highly integrated systems as well

as the overall average in 2014 (both 2.5 days).

Key Takeaway

That diabetes inpatients had the highest ALOS of the profiled disease states, regardless of

hospital size or ownership, might reflect the complicated nature of the disease. Diabetes patients

often have multiple comorbidities, and a recent study found that 27% of such patients had

undiagnosed conditions, which could lead to poor outcomes and increased hospital utilization.1

1 Lin, P. (2015). Multiple Chronic Conditions in Type 2 Diabetes Mellitus. Prevalence and Consequences. AJMC.com. Retrieved from http://www.ajmc.com/journals/issue/2015/2015-vol21-n1/multiple-chronic-conditions-in-type-2-diabetes-mellitus-prevalence-and-consequences/p-3

NOTE: Some length-of-stay data were unavailable for angina and rheumatoid arthritis.

13

UTIL IZATION

13

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

Data source: Centers for Medicare & Medicaid Services © 2016

Key Takeaway

Driven by provisions in the Affordable Care Act, the Centers for Medicare & Medicaid Services (CMS)

have been working since October 2012 to reduce hospital readmissions via payment cuts for facilities

with higher-than-expected readmission rates. Payers are also incentivized to reduce readmissions, as

their Medicare Star ratings are partly dependent on this measure. CMS efforts appear to be paying off:

readmissions among Medicare fee-for-service members fell by roughly 14% from 2011 to 2013.

• For six of the eight regions (South Central

and South Atlantic excepted), average

length of stay (ALOS) per inpatient diabetes

mellitus case increased from 2013 to 2014.

• ALOS was highest for diabetes cases, by region,

in the Mid-Atlantic, at 5.9 days in 2014. This

region also had the highest ALOS for asthma,

hypertension, prostate cancer, and stroke.

ACUTE HOSPITAL READMISSIONS, MEDICARE FEE-FOR-SERVICE, 2008–2013

Length of Stay Rises for Diabetes Mellitus Inpatient Cases

CHRONIC DISEASE

• The number of Medicare FFS inpatient

readmissions within 30 days of an acute hospital

stay fell again in 2013, to 1,656,930, the third

consecutive annual drop since 2010 (1,949,430).

• Of these 1.7 million readmissions in 2013, 74.5%

(1.2 million) were for patients age 65 and over,

though readmissions among patients in this

age group also declined (data not shown).1

1 Health Indicators Warehouse. (2016). Acute Hospital Readmissions (Number). Retrieved from http://www.healthindicators.gov/Indicators/Acute-hospital-readmissions-number_278/Profile/ClassicData

NOTE: Some length-of-stay data were unavailable for the Mountain, East North Central, and New England regions.

Data source: IMS Health © 2016

2008 2009 2010 2011 2012 20131,600

1,700

1,800

1,900

2,000

Num

be

r of R

ea

dm

issi

ons

(00

0)

Inpatient Readmissions

1,992

1,945 1,9491,929

1,820

1,657

Number of Medicare Fee-for-Service (FFS) Inpatient Readmissions Declines AgainLONG-TERM TREND

AVERAGE LENGTH OF STAY (DAYS) PER MEDICARE HOSPITAL INPATIENT CASE, BY REGION, 2013–2014

Angina Asthma Diabetes Mellitus

Hyper-tension

Prostate Cancer

Rheuma-toid Arthritis Stroke

REGION 2013 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013 2014

Pacific 1.5 1.9 4.0 3.9 4.9 5.0 2.6 2.4 2.4 2.2 2.5 2.7 3.9 3.9

Mountain 1.6 — 3.8 3.9 4.3 4.6 2.3 2.3 2.4 2.4 3.2 — 3.5 3.5

West North Central 1.9 2.4 4.0 3.8 4.4 4.5 2.4 2.7 2.3 2.2 2.7 3.7 3.5 3.4

East North Central 2.6 — 4.0 4.0 4.4 4.5 2.7 2.6 2.5 2.6 3.6 3.2 3.8 3.7

South Central 2.3 2.5 4.3 4.3 4.8 4.8 2.7 2.7 2.5 2.5 3.9 3.5 4.0 4.1

New England — — 4.1 3.9 4.7 4.8 2.9 2.9 2.5 2.4 4.0 3.9 3.7 3.8

Mid-Atlantic 2.3 2.4 4.8 4.6 5.7 5.9 3.1 3.0 3.2 3.3 3.7 3.8 4.9 4.8

South Atlantic 2.4 2.1 4.3 4.3 5.0 5.0 2.6 2.6 2.4 2.5 3.7 3.4 4.3 4.2

MANAGED CARE PORTION OF TOTAL MEDICARE EXPENDITURES, 2004–20152

METHODS OF PHYSICIAN COMPENSATION USED BY MEDICARE HMOs, 2012–20153,4

Not-for-Profit For-Profit Overall Average

METHOD 2012 2013 2014 2015 2012 2013 2014 2015 2012 2013 2014 2015

Salary 17.3% 17.0% 14.8% 14.5% 1.9% 1.9% 1.8% 1.9% 7.0% 6.9% 6.4% 6.6%

Fee-for-Service 53.8 50.9 50.8 50.0 61.9 61.7 62.5 61.9 59.2 58.1 58.4 57.5

Capitation 71.2 71.7 72.1 72.6 70.5 67.3 67.0 68.6 70.7 68.8 68.8 70.1

Bonus Program 38.5 41.5 39.3 38.7 12.4 13.1 12.5 13.3 21.0 22.5 22.0 22.8

Profit Sharing 5.8 7.5 6.6 6.5 1.9 1.9 1.8 1.9 3.2 3.8 3.5 3.6

0%

7%

14%

21%

28%

Ma

na

ge

d C

are

Sh

are

of

Tota

l Me

dic

are

Exp

en

ditu

res

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

12.8%14.0%

15.8%

18.0%

21.0%22.1% 22.2% 22.8%

24.9% 25.2%26.7% 27.4%

1414

FINANCIALSM

ED

ICA

RE

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

Key Takeaway

As enrollment in Medicare Advantage plans continues to grow (see page 5), so too does the

managed care portion of the program’s expenditure. Medicare’s expense in this category has

expanded, and the payer has also invested more in value-based reimbursement initiatives, such as

those that reward higher Star ratings. Medicare managed care plans subject to these arrangements

will likely be on the lookout for more ways to share risks with the physicians in their networks.

Data source: IMS Health © 2016

• For the 11th consecutive year, the managed care

share of total Medicare expenditures increased

in 2015, to 27.4% from 26.7% the prior year. Since

2004, this percentage has grown by 14.6 points.

• The amount Medicare spent on managed care

grew by 8.6% from 2014 ($155.9 billion) to 2015

($169.3 billion), while fee-for-service expenditures

rose by 2.7% (to $376.9 billion; data not shown).1,2

Expanding Percentage of Medicare HMOs Compensate Physicians via Capitation

• In 2015, the portion of all Medicare HMOs

using capitation to reimburse physicians

increased slightly, to 70.1%, but did not match

the corresponding 2012 measure of 70.7%.

• Not-for-profit Medicare HMOs were more

likely than their for-profit counterparts to use

capitation in 2015, though this share grew

faster at for-profit plans from 2014 to 2015.

1 Centers for Medicare & Medicaid Services (CMS). (2014). CMS Financial Report Fiscal Year 2014: Transforming Health Care for All Americans. Retrieved from https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/CFOReport/Downloads/CMS-Financial-Report-for-Fiscal-Year-2014.pdf

2 CMS. (2015). CMS Financial Report Fiscal Year 2015: Keeping Us Healthy for 50 Years. Retrieved from https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/CFOReport/Downloads/2015_CMS_Financial_Report.pdf

3 Only HMOs that enroll Medicare beneficiaries are included.4 HMOs gave multiple answers. Totals add up to more than 100%. Other reimbursement methods used by HMOs included discounted fee-for-service,

fee schedules, per diems, and return of risk pools/withholds.

Managed Care Share of Medicare Spending GrowsLONG-TERM TREND

Data source: Centers for Medicare and Medicaid Services, 2016

15

FINANCIALS

15SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

ME

DIC

AR

E

Inpatient Charges per Medicare Case Climb SteadilyLONG-TERM TREND

Key Takeaway

Starting in 2013, Medicare began releasing data for inpatient charges for common procedures at

hospitals around the nation, revealing that charges for the same services can vary wildly. For example,

in 2013, a joint replacement costs an average of $5,300 in Ada, Oklahoma, and $223,000 in Monterey

Park, California.3 Medicare reimbursements also vary depending on the hospital, with differences

driven by average patient morbidity, as well as local costs at the hospitals themselves.3

Data source: IMS Health © 2016

HOSPITAL INPATIENT CHARGES PER MEDICARE CASE, 2010–20141

DISEASE STATE 2010 2011 2012 2013 2014 % Change 2010–2014

ACS $22,250 $23,507 $25,593 $26,994 $31,141 40.0%

Angina 18,721 20,354 21,651 25,747 27,369 46.2

Diabetes Mellitus 33,715 35,651 37,730 41,226 44,170 31.0

Hypertension 17,745 18,887 19,766 22,443 24,603 38.6

Osteoarthritis 47,346 49,488 51,635 50,054 55,241 16.7

Stroke 34,859 37,392 39,270 42,024 44,477 27.6

• From 2010 to 2014, average hospital inpatient

charges per Medicare case grew nearly every

year across all of the profiled disease states,

increasing the most for angina (46.2%).

• Although charges for Medicare hypertension

cases remained lower than those for other

diagnoses shown, they rose 38.6%, a larger jump

than for osteoarthritis (16.7%) and stroke (27.6%).

AMI Stroke Hypertension$0

$23,000

$46,000

$69,000

$92,000

Ch

arg

es

pe

r Ca

se

$16,999

$30,874

$56,061

$86,715

$15,957

$25,087

$38,239

$48,463

$5,737

$23,096 $22,954 $25,264

CMI <1.0 CMI 1.0 to <1.2 CMI 1.2 to <1.5 CMI 1.5+

HOSPITAL INPATIENT CHARGES PER MEDICARE CASE, BY SEVERITY, 20141,2

1 Charge data are per-case averages for inpatients with a particular diagnosis of interest. Charges may be for treatment related to other diagnoses. Data reflect the total charges billed by the hospital for the entire episode of care, and may include accommodation, pharmacy, laboratory, radiology, and other charges not billed by the physician. Data do not necessarily indicate final amounts paid.

2 Severity is approximated by the case mix index (CMI), which is a statistical measure of the average amount of resources consumed per Medicare inpatient case at a hospital. Hospitals that tend to treat more resource-intensive (i.e., severe) cases will have a higher calculated CMI.

3 Daly, R. (2013). CMS data show wide variation in hospital billing. Modern Healthcare. Retrieved from http://modernhealthcare.com/article/20130508/NEWS/305089960

Hospital Case Mix Index Drives Up Charges for Select Cardiovascular Diagnoses

• In 2014, for all three cardiovascular diagnoses

profiled, hospitals with the most severe case

mix index (CMI; 1.5 or more) generated the

highest charges per inpatient Medicare case.

• For example, inpatient charges per AMI

case were $86,715 for hospitals with a CMI of

1.5 or above, more than five times those for

facilities with a CMI of less than 1.0 ($16,999).

1616

FINANCIALS

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

ME

DIC

AR

E

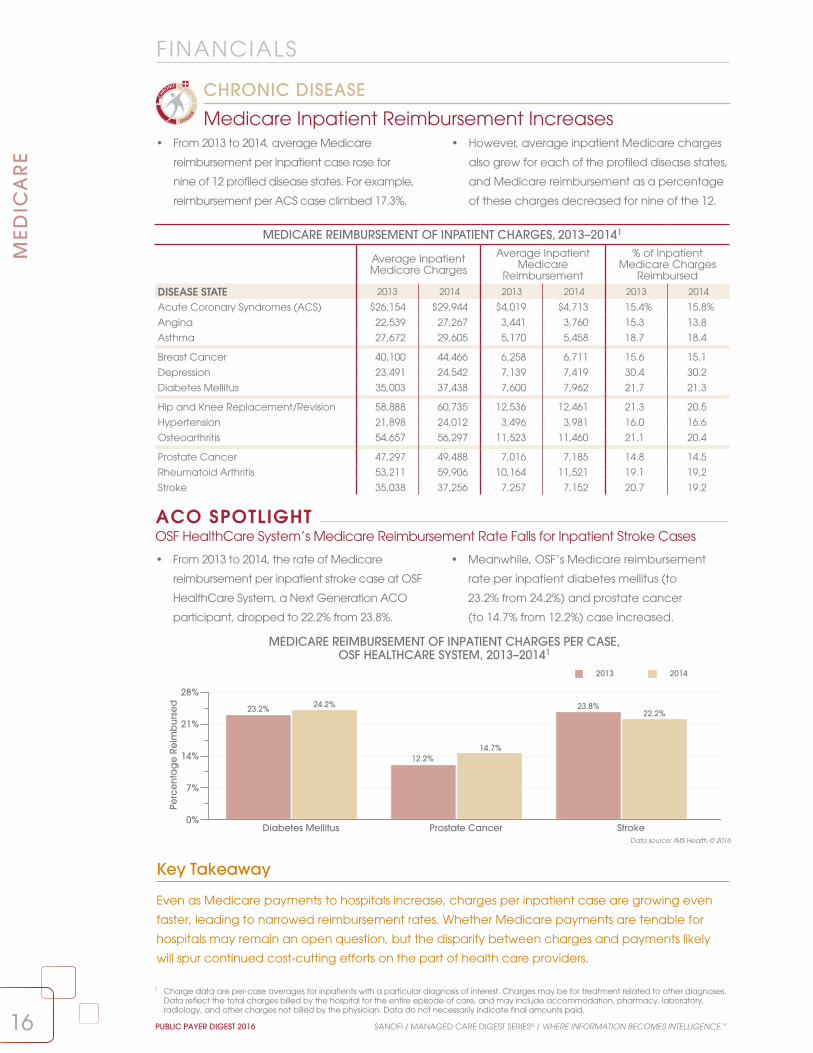

• From 2013 to 2014, average Medicare

reimbursement per inpatient case rose for

nine of 12 profiled disease states. For example,

reimbursement per ACS case climbed 17.3%.

• However, average inpatient Medicare charges

also grew for each of the profiled disease states,

and Medicare reimbursement as a percentage

of these charges decreased for nine of the 12.

Medicare Inpatient Reimbursement Increases

CHRONIC DISEASE

1 Charge data are per-case averages for inpatients with a particular diagnosis of interest. Charges may be for treatment related to other diagnoses. Data reflect the total charges billed by the hospital for the entire episode of care, and may include accommodation, pharmacy, laboratory, radiology, and other charges not billed by the physician. Data do not necessarily indicate final amounts paid.

Key Takeaway

Even as Medicare payments to hospitals increase, charges per inpatient case are growing even

faster, leading to narrowed reimbursement rates. Whether Medicare payments are tenable for

hospitals may remain an open question, but the disparity between charges and payments likely

will spur continued cost-cutting efforts on the part of health care providers.

Data source: IMS Health © 2016

MEDICARE REIMBURSEMENT OF INPATIENT CHARGES PER CASE, OSF HEALTHCARE SYSTEM, 2013–20141

MEDICARE REIMBURSEMENT OF INPATIENT CHARGES, 2013–20141

Average Inpatient Medicare Charges

Average Inpatient Medicare

Reimbursement

% of Inpatient Medicare Charges

Reimbursed

DISEASE STATE 2013 2014 2013 2014 2013 2014

Acute Coronary Syndromes (ACS) $26,154 $29,944 $4,019 $4,713 15.4% 15.8%

Angina 22,539 27,267 3,441 3,760 15.3 13.8

Asthma 27,672 29,605 5,170 5,458 18.7 18.4

Breast Cancer 40,100 44,466 6,258 6,711 15.6 15.1

Depression 23,491 24,542 7,139 7,419 30.4 30.2

Diabetes Mellitus 35,003 37,438 7,600 7,962 21.7 21.3

Hip and Knee Replacement/Revision 58,888 60,735 12,536 12,461 21.3 20.5

Hypertension 21,898 24,012 3,496 3,981 16.0 16.6

Osteoarthritis 54,657 56,297 11,523 11,460 21.1 20.4

Prostate Cancer 47,297 49,488 7,016 7,185 14.8 14.5

Rheumatoid Arthritis 53,211 59,906 10,164 11,521 19.1 19.2

Stroke 35,038 37,256 7,257 7,152 20.7 19.2

• From 2013 to 2014, the rate of Medicare

reimbursement per inpatient stroke case at OSF

HealthCare System, a Next Generation ACO

participant, dropped to 22.2% from 23.8%.

• Meanwhile, OSF’s Medicare reimbursement

rate per inpatient diabetes mellitus (to

23.2% from 24.2%) and prostate cancer

(to 14.7% from 12.2%) case increased.

OSF HealthCare System’s Medicare Reimbursement Rate Falls for Inpatient Stroke CasesACO SPOTLIGHT

Diabetes Mellitus Prostate Cancer Stroke0%

7%

14%

21%

28%

Perc

en

tag

e R

eim

bu

rse

d

2013 2014

23.2% 24.2% 23.8%22.2%

12.2%14.7%

17

FINANCIALS

17SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

ME

DIC

AR

E

MEDICARE REIMBURSEMENT OF HEART FAILURE INPATIENT PER-CASE CHARGES, 2011–20141

• Average Medicare reimbursement per

inpatient heart failure case decreased

in each of the profiled years, to 24.8% of

average charges in 2014 from 28.5% in 2011.

• Meanwhile, average Medicare charges per

inpatient heart failure case increased each

year from 2011 to 2014. Such charges rose 20.1%

during this period, to $29,735 from $24,767.

Medicare Reimbursement Rate for Heart Failure Falls Again

CHRONIC DISEASE

$0

$9,000

$18,000

$27,000

$36,000

Ch

arg

es/

Reim

bu

rse

me

nt

Average Charges Average Reimbursement Percentage Reimbursed

28.5% 27.9%25.2% 24.8%

2011 2012 2013 2014

$24,767

$7,049

$25,932

$7,228

$28,855

$7,279

$29,735

$7,358

1 Charge data are per-case averages for inpatients with a particular diagnosis of interest. Charges may be for treatment related to other diagnoses. Data reflect the total charges billed by the hospital for the entire episode of care, and may include accommodation, pharmacy, laboratory, radiology, and other charges not billed by the physician. Data do not necessarily indicate final amounts paid.

2 CMS. (2015). FY 2016 IPPS Hospitals Readmission Reduction Program Supplemental Data File (Final Rule and Correction Notice). Retrieved from http://www.cms.gov/Medicare/Medicare-Fee-for-Service-Payment/AcuteInpatientPPS/Downloads/FY2015-FR-Readmit-Supp-Data-File.zip

3 The total number of hospitals evaluated and penalized may include institutions that have closed or merged with other facilities. Evaluated hospitals include those in Maryland, even though they were exempted from penalties.

Percentage of Hospitals Penalized for Excess Readmissions Grows

• From 2015 to 2016, the share of hospitals

assessed a penalty for excess readmissions under

the Hospital Readmissions Reduction Program

(HRRP) increased, to 78.8% from 75.9%.

• The share of penalized hospitals assessed the

smallest penalty rose (to 80.8% from 79.8%) during

this period, as did the share of hospitals receiving

the largest penalty (to 4.3% from 4.1%).

Key Takeaway

In 2015, chronic obstructive pulmonary disease (COPD) and hip or knee replacement were added to

the set of conditions on which CMS rates hospital readmission performance. This expansion may have

contributed to the increased share of hospitals receiving penalties for 2016 Medicare reimbursement.

PERCENTAGE (NUMBER) OF HOSPITALS PENALIZED UNDER THE HOSPITAL READMISSIONS

REDUCTION PROGRAM, FY 20162,3

Not Penalized

Penalized

78.8%(2,592)

21.2%(697)

PERCENTAGE (NUMBER) OF PENALIZED HOSPITALS, BY REIMBURSEMENT PENALTY, FY 20162,3

0.01–1.0% Reimbursement Penalty

1.01–2.0% Reimbursement Penalty

2.01–3.0% Reimbursement Penalty 4.3%(111)

80.8%(2,095)

14.9%(386)

Data source: Centers for Medicare & Medicaid Services © 2016

Data source: IMS Health © 2016

2015Penalized: 75.9% (2,638)

Not Penalized: 24.1% (838)

20150.01–1.0%: 79.8% (2,105)

1.01–2.0%: 16.1% (424)

2.01–3.0%: 4.1% (109)

Patient pays 25%of drug cost

Patient pays 5% of drug cost

Annualdeductible

2016

Initial Phase4 Coverage Gap (the “donut hole”)1,2 Catastrophic Phase

Enrollee Drug Company Part D Drug Plan

45% 50%

45% 50% 5%

5%

2016

2017

2018

2019

Patient pays 25%of drug cost

Patient pays 5% of drug cost

Annualdeductible2020

Initial Phase Coverage Gap (the “donut hole”) Catastrophic Phase

50%

50%

50%

10%

15%

20%

40%

35%

30%

50%25% 25%

$360 Max $3,310 $4,850

STANDARD MEDICARE PRESCRIPTION DRUG BENEFIT, 2016–20203

1818

ME

DIC

AR

E

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

Data source: Centers for Medicare & Medicaid Services © 2016

Less Than a Third of Part D Patients on Diabetes Rxs Reach the Coverage Gap

• In 2014, 41.6% of Florida Part D participants who

filled diabetes drugs reached the coverage gap,

the highest share among the profiled states. In

California, this percentage was 21.1%.

• Nationally, 17.2% of Part D participants who

received diabetes drugs were dual-eligible; 15.3%

received a low-income subsidy. Neither group

was subject to the coverage gap in 2014.

Drug Cost Limits Shift Up for Part D Participants in 2016

• Medicare raised per-enrollee spending limits for

the initial phase of coverage in 2016 (to $3,310

from $2,960 in 2015), as well as the upper limit

of the coverage gap (to $4,850 from $4,700) for

the standard prescription drug benefit.

• In 2016, participants in their initial phase pay

25% of total costs for covered drugs, until a total

expenditure of $3,310. In the coverage gap,

enrollees’ share of drug expenses is 45% for

branded drugs and 58% for generics.

PHARMACY

1 For brand-name drugs, patient pays 45% of drug cost, manufacturer pays 50%. Out-of-pocket (OOP) spending that counts toward coverage gap up to catastrophic coverage includes both patient and manufacturer spending (95% of drug price). Also included in OOP costs are payments made by patient for covered prescription if plan has a coverage gap. Excluded from OOP costs are plan spending on drug cost (5% of drug price), plan premium, and plan spending on pharmacy dispensing fee (patient pays 55% of fee).

2 For generic drugs, patient pays 58% of drug price. This is the only expense that counts toward OOP spending in the coverage gap. Manufacturer’s contribution of 42% of drug price does not count toward OOP maximum.

3 Centers for Medicare & Medicaid Services. (2016). Costs in the Coverage Gap. Retrieved from http://www.medicare.gov/part-d/costs/coverage-gap/part-d-coverage-gap.html

4 Patient and drug spending combined, to include deductible ($360 maximum), copayments, and coinsurance.

PERCENTAGE OF DIABETES PATIENTS, BY COVERAGE GAP STATUS, 2014

Subject to Coverage Gap Not Subject to Coverage Gap

MARKET Did Not Reach Coverage Gap

Voluntary—Reached Coverage Gap Dual Eligible Low-Income Subsidy

California 29.7% 21.1% 44.5% 4.5%

Florida 36.0 41.6 8.1 14.1

New York 37.5 31.2 20.0 11.2

Ohio 46.9 27.6 10.2 15.3

Pennsylvania 46.5 22.7 18.1 12.7

Texas 28.0 37.1 13.2 21.6

NATION 36.4% 31.0% 17.2% 15.3%

STATE SPOTLIGHT

1919

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

Ingredient Cost per Medicare HMO Rx Shrinks in 2015

• Average ingredient costs per prescription for

Medicare HMO members fell to $56.80 in 2015

from $57.80 in 2013; during the same period,

the share of Medicare HMOs that penalized

physicians for prescribing policy violations rose.

• Despite a decrease in ingredient costs per

prescription, and a growing generic share of

drugs dispensed, the pharmacy percentage

of total operating costs at Medicare HMOs

increased only fractionally during this time.

PHARMACY BENCHMARKS AND POLICIES FOR HMOs WITH MEDICARE MEMBERS, 2013–20151,2

PHARMACY BENCHMARKS 2013 2014 2015

No. of Prescriptions per Member per Year 29.4 29.9 29.7

Average Ingredient Cost per Prescription $57.80 $57.20 $56.80

Pharmacy Costs as % of Total Operating Costs 14.2% 14.8% 14.8%

% of Prescriptions Filled With Generics 78.1% 78.7% 78.8%

PHARMACY POLICIES% of HMOs Allowing Choice of Branded or Generic

Pharmaceuticals 90.3% 91.5% 90.0%% of HMOs Penalizing Physicians for Violations of

Prescribing Policy 13.6% 15.5% 15.4%

Key Takeaway

The spike in the share of generic prescriptions dispensed starting in 2012 is largely attributable

to the number of branded drugs that lost patent protection between 2011 and 2013. However,

the greater complexity of biologics could impact this trend. It is more difficult and expensive

to produce biosimilar biologics than chemical compound drugs, limiting generic drug makers’

ability to rapidly bring to market generic replacements for biologics that go off patent.3

Data source: IMS Health © 2016

PHARMACY

1 Data are as of midyear 2015 and represent the numbers/percentages of prescriptions dispensed, by drug class, to all patients.2 Only HMOs that enroll Medicare beneficiaries are included.3 The Economist. (2015). Going Large: A Wave of New Medicines Known as Biologics Will Be Good for Drugmakers, but May Not Be So Good for

Health Budgets. Retrieved from: http://www.economist.com/node/21637387/print

Number of Rxs Dispensed per Medicare HMO Member Rises 20.2% From 2006LONG-TERM TREND

• From 2006 (24.7) to 2015 (29.7) the average

annual number of prescriptions dispensed

per Medicare HMO member climbed 20.2%.

• The percentage of prescriptions that were filled

with generic drugs at Medicare HMOs also

grew, to 78.8% in 2015 from 49.6% in 2006.

NUMBER OF PRESCRIPTIONS PER MEDICARE HMO MEMBER PER YEAR AND PERCENTAGE OF PRESCRIPTIONS FILLED WITH GENERICS, 2006–20151,2

40%

50%

60%

70%

80%

Perc

en

tag

e o

f Presc

riptio

ns

0

8

16

24

32

Nu

mb

er o

f Pre

scrip

tion

s

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

24.725.6

27.2

30.0 29.6 29.929.3 29.4 29.9 29.7

49.6%

53.6%55.1%

58.5%

63.2%

63.7%

76.9%78.1% 78.7% 78.8%

Total Medicare Prescriptions Percentage of Prescriptions Filled with Generics

2020

ME

DIC

AR

E

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

Data source: IMS Health © 2016

Key Takeaway

In 2014, Part D participants filling prescriptions in the coverage gap paid just under half (47.5%)

of their out-of-pocket expenses for branded drugs and nearly three-fourths (72%) of their generic

costs.1 Whether Medicare is able to continue assuming larger shares of costs for drugs filled during

the gap—as called for under the Affordable Care Act (ACA)—depends not just on how well the

program manages future prescription expenses, but also on the long-term viability of the ACA itself.

Monthly Out-of-Pocket Costs for California Part D Oncology Rxs Top U.S. Averages

• Regardless of their coverage gap status, Part D

enrollees in California who received oncology

prescriptions had higher monthly out-of-pocket

costs than their counterparts nationally in 2014.

• For example, California oncology patients with

Part D coverage paid roughly $93 a month

during the coverage gap for prescriptions in

2014, 10.9% higher than the U.S. mean of $83.60.

LIS Shares Dip Among Part D Diabetes, Oncology Patients

• From 2013 to 2014, the percentages of Medicare

Part D enrollees who were dual eligible or low-

income subsidy (LIS) declined among those who

filled diabetes, cholesterol, or oncology drugs.

• Less than a third of Part D patients receiving

prescriptions in any of the profiled categories

reached the coverage gap in 2014; among

these classes, this share was lowest for cholesterol.

PHARMACY

PERCENTAGE OF PART D PATIENTS, BY COVERAGE GAP STATUS, 2013–2014

Dual Eligible Low-Income Subsidy Did Not Reach the Coverage Gap

Reached the Coverage Gap

DRUG CLASS 2013 2014 2013 2014 2013 2014 2013 2014

Diabetes 19.1% 17.2% 15.9% 15.3% 38.1% 36.4% 26.9% 31.0%

Cholesterol 14.9 13.5 12.9 12.2 48.2 46.5 24.0 27.8

Oncology 12.6 10.7 13.0 12.2 48.4 46.8 25.8 30.1

2013

California Nation

2014 2013 2014$0

$25

$50

$75

$100

Ou

t-of-P

oc

ket C

ost

s

$40.23

$79.48

$88.39

$37.02

$71.65

$92.70

$36.81

$60.06

$82.47

$35.18

$60.29

$83.60

Did Not Reach the Coverage Gap Before the Gap During the Gap

PART D MONTHLY OUT-OF-POCKET COSTS, BY COVERAGE GAP STATUS, ONCOLOGY, 2013–2014

CHRONIC DISEASE

STATE SPOTLIGHT

1 See the Public Payer Digest for 2014, page 19.

21

PHARMACY

21

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

0%

25%

50%

75%

100%PDP PenetrationMA Penetration

Pen

etra

tion

Ra

te

MN HI OR CA FL

43.7%

55.2%

26.4%

45.8%

31.2%

44.4%

37.2%

41.4%

35.4%

40.8%

0%

25%

50%

75%

100%

ND VT DE IA SD

PDP PenetrationMA Penetration

Pen

etra

tion

Ra

te

67.2%

18.8%

66.5%

7.6%

65.6%

9.3%

63.6%

17.4%

61.8%

20.6%

TOP 10 STATES, BY MEDICARE PDP ENROLLMENT, 2015–20161

STATE Enrollment 2015 Enrollment 2016 Enrollment Change 2015–2016

% of Total PDP Enrollment

California 2,049,217 2,139,382 4.4% 8.7%

Texas 1,572,794 1,578,834 0.4 6.4

Florida 1,406,540 1,456,163 3.5 5.9

New York 1,391,896 1,428,702 2.6 5.8

Michigan 1,097,544 1,091,790 –0.5 4.4

Illinois 1,042,146 1,079,166 3.6 4.4

Pennsylvania 1,036,172 1,064,450 2.7 4.3

Ohio 1,032,188 1,019,985 –1.2 4.1

New Jersey 880,828 898,562 2.0 3.7

North Carolina 788,192 803,424 1.9 3.3

Key Takeaway

Nearly 76% of the nation’s eligible Medicare beneficiaries were enrolled in either an MA or PDP

plan as of March 2016, though PDP plans constituted a larger portion of total Part D membership.

As Part D plans evolve, it is likely they will continue to attract even higher percentages of Medicare

beneficiaries, thus increasing the program’s share of all pharmacy expenses nationally.

Data source: Centers for Medicare & Medicaid Services © 2016

1 Data are as of March of the year listed.

Membership Grows for Most Top 10 PDP Enrollment States

• For eight of the 10 top states, by

Medicare Part D prescription drug

program (PDP) enrollment, membership

counts increased from 2015 to 2016.

• Collectively, PDP enrollment in these top

10 states increased by 2.1%; as of March

2016, more than half (51.0%) of the nation’s

PDP enrollees were in these states.

Medicare Advantage Penetration Exceeds 55% in Minnesota

• As of March 2016, 55.2% of eligible Minnesota

Medicare beneficiaries were in a Medicare

Advantage (MA) plan; MA and PDP plans

enrolled 98.9% of the state’s eligible population.

• In the other four states with the highest

MA penetration rates, MA and PDP plans

together accounted for no more than

78.6% of all eligible Medicare members.

STATE SPOTLIGHT

MA AND PDP PENETRATION, 20161

TOP FIVE STATES, BY MA PENETRATION TOP FIVE STATES, BY PDP PENETRATION

2222

PHARMACYM

ED

ICA

RE

PUBLIC PAYER DIGEST 2016 SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™

Key Takeaway

Pharmacy cost per staffed bed rose 0.7% from 2014 to 2015, and pharmacy cost per discharge

climbed a more notable 8.2% during this period. The fractional increase in the former may reflect a

more precipitous reduction in bed counts than in admissions, as hospitals seek to reconcile projected

overcapacity and operating costs.1 Growth in the latter could be influenced by efforts to reduce

readmissions and improve medication therapy management—and outcomes—across transitions of

care. For example, by beginning post-acute care therapeutic regimens before patients are discharged.

Data source: IMS Health © 2016

Pharmacy Costs per Staffed Bed Are Lower at Non-IHS Hospitals

• In 2014, average pharmacy cost per staffed

bed was lower for hospitals that were not

affiliated with an integrated health system (IHS;

$48,862) than for hospitals that were ($61,508).

• However, average pharmacy cost

per discharge was slightly higher at

non-IHS hospitals ($1,537) than at

their IHS counterparts ($1,511).

PHARMACY COSTS PER STAFFED BED, ALLINA HEALTH VS. NATION, 2013–2014

PHARMACY COSTS PER DISCHARGE, ALLINA HEALTH VS. NATION, 2013–2014

$0

$22,000

$44,000

$66,000

$88,000

Pha

rma

cy

Co

sts

pe

r Sta

ffed

Be

d

2013 2014

Allina Health Nation

$82,462$86,890

$55,789 $56,166

Pharmacy Costs per Discharge Drop Steeply at Allina Health Hospitals

• Average pharmacy cost per discharge at Allina

Health hospitals fell 24.3%, from 2013 ($2,025)

to 2014 ($1,533), even as it rose 8.2% across all

hospitals nationally (from $1,406 to $1,521).

• Meanwhile, average pharmacy cost per

staffed bed grew 5.4% at Allina Health, to

$86,890 from $82,462, and notably exceeded

the national average of $56,166 in 2014.

ACO SPOTLIGHT

$1,000

$1,260

$1,520

$1,780

$2,040

Pha

rma

cy

Co

sts

pe

r Dis

cha

rge

2013 2014

Allina Health Nation

$2,025

$1,533

$1,406

$1,521

AVERAGE TOTAL STAFFED BEDS AND PHARMACEUTICAL EXPENSES, PER HOSPITAL, 2014

SIZE Average Total Staffed Beds

Average Pharmacy Cost per Staffed Bed

Average Pharmacy Cost per Discharge

<50 Beds 24.9 $49,419 $1,686

50–119 Beds 81.6 54,782 1,418

120–249 Beds 177.9 58,625 1,407

≥250 Beds 421.4 67,981 1,512

MHS OWNERSHIP

MHS Owned 188.4 61,144 1,488

Non-MHS Owned 76.2 48,130 1,588

INTEGRATED SYSTEM AFFILIATION

In an IHS 181.1 61,508 1,511

Not in an IHS 104.6 48,862 1,537

OVERALL AVG. 149.8 $56,166 $1,521

1 Evans, M. (2015). Hospitals Face Closures as “New Day in Health Care” Dawns. Modern Healthcare. http://www.modernhealthcare.com/article/20150221/MAGAZINE/302219988

23

PHARMACY

23

ME

DIC

AR

E

SANOFI / MANAGED CARE DIGEST SERIES® / WHERE INFORMATION BECOMES INTELLIGENCE.™ PUBLIC PAYER DIGEST 2016

Data source: IMS Health © 2016

• From 2013 to 2015, the Medicare Part D

percentages of the total number of

retail prescriptions filled rose in each of

the 12 profiled therapeutic classes.

• The 2015 Part D share for osteoporotics (55.4%)

was the highest of the classes, up from 49.7% in

2013; hypertensives again accounted for the

largest number of prescriptions filled.

Key Takeaway

It stands to reason that, as more eligible Medicare beneficiaries sign up for Part D plans, the

program would naturally record an increase in total numbers of prescriptions filled at retail, which

certainly occurred from 2013 to 2015. On the one hand, Part D’s growing shares of retail pharmacy