MANAGED CARE DIGEST SERIES ® HOSPITALS/SYSTEMS DIGEST PUBLIC PAYER DIGEST HMO-PPO DIGEST S I N C E 1 9 8 7 2nd Edition Type 2 Diabetes Report | 2014 Central Florida Presented by in partnership with the Florida Health Care Coalition

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MANAGED CARE DIGEST SERIES®

H O S P I T A L S / S Y S T E M S D I G E S T P U B L I C P A Y E R D I G E S T H M O - P P O D I G E S TSINCE 1987

2nd Edition

Type 2 Diabetes Report|2014Central Florida

Presented by

in partnership with the

Florida Health Care Coalition

2 CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 MANAGED CARE DIGEST SERIES® www.flhcc.org

FLORIDA TYPE 2 DIABETES REPORT

CONTENTS

Steve Montgomery 407-694-3080Account Executive, Sanofi US [email protected]

Patient Demographics ................... 3–4

Use of Services ..................................... 5

ALOS/Inpatient Charges .................... 6

Professional Charges ...................... 7–8

Pharmacotherapy ........................ 9–10

Persistency/Readmissions ................. 11

ADA/EASD Position Statement ........ 12

IntroductionSanofi US (Sanofi), in conjunction with the Florida Health Care Coalition, is pleased to present the second edition of the Central Florida Type 2 Diabetes Report for 2014, an overview of key demographic, utilization, charge and pharmacotherapy measures for Type 2 diabetes patients in key local markets in central Florida. The report also provides state and national benchmarks that can help providers and employers identify opportunities to better serve the needs of their patients. All data are drawn from the Sanofi Managed Care Digest Series®.

Sanofi, as sponsor of this report, maintains an arm’s-length relationship with the organizations that prepare this report and carry out the research. The desire of Sanofi is that the information in this report be completely independent and objective.

This report features a number of examples of patient-level, disease-specific data on Type 2 diabetes that can be provided using the Managed Care Digest Series® as a resource. Type 2 diabetes (a chronic disease marked by high levels of glucose in the blood) was chosen as the focus of this resource, as the Centers for Disease Control estimates that 90% to 95% of all Americans with diabetes—translating to 5% to 7% of the U.S. population—have the Type 2 variety.

All data in this report (covering 2010 through 2013) were gathered by IMS Health, Parsippany, NJ, a leading provider of innovative health care data products and analytic services. The data provide employers with independent, third-party information against which they benchmark their own data on patient demographics, professional and facility charges, service utilization and pharmacotherapy.

MethodologyIMS Health generated data for this Managed Care Digest Series® report

Provided by Sanofi US

Bridgewater, NJ

Developed and produced by Forte Information Resources LLC

Denver, CO

www.forteinformation.com

Data provided by IMS Health

Parsippany, NJ

www.managedcaredigest.com

CONTACTS

using mostly health care professional and

institutional insurance claims, representing

more than 7.7 million unique Type 2

diabetes patients nationally in 2013 with

a diagnosis in the 250.00–250.92 range.

Data from physicians of all specialties

and from all hospital types are included.

Per-case average length of stay

and inpatient charge data come from

IMS Health’s Hospital Procedure/

Diagnosis (HPD) Database. This database

contains an extensive set of hospital

inpatient and outpatient discharge

records, including actual diagnoses

and procedures for about 75% of

discharges nationwide (including 100%

of Medicare-reimbursed discharges).

IMS Health also gathers data on

prescription activity from the National

Council for Prescription Drug Programs

(NCPDP). These data account for some

2 billion prescription claims annually,

or more than 50% of the prescription

universe. These prescription data

represent the sampling of prescription

activity from a variety of sources, including

retail chains, mass merchandisers and

pharmacy benefit managers. Cash,

mail-order, Medicaid and third-party

transactions are tracked.

DATA INTEGRITY

Data arriving into IMS Health are put

through a rigorous process to ensure

that data elements match to valid

references, such as product codes,

ICD-9 (diagnosis) and CPT-4 (procedure)

codes, and provider and facility data.

Through its patient encryption

methods, IMS Health creates a unique,

random numerical identifier for each

patient, then strips away all patient-

specific health information that is

protected under the Health Insurance

Portability and Accountability Act (HIPAA).

The identifier allows IMS Health to track

disease-specific diagnosis and procedure

activity across the various settings where

patient care is provided.

MANAGED CARE DIGEST SERIES

®

SINCE 1987

WWW.FLHCC.ORG MANAGED CARE DIGEST SERIES® CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 3

Pre-Diabetes Diabetes0%

3%

6%

9%

12%

Perc

en

tag

e o

f Po

pu

latio

n

1.2% 1.2% 1.2%

9.5%

10.7%10.4%

2008 2009 2010

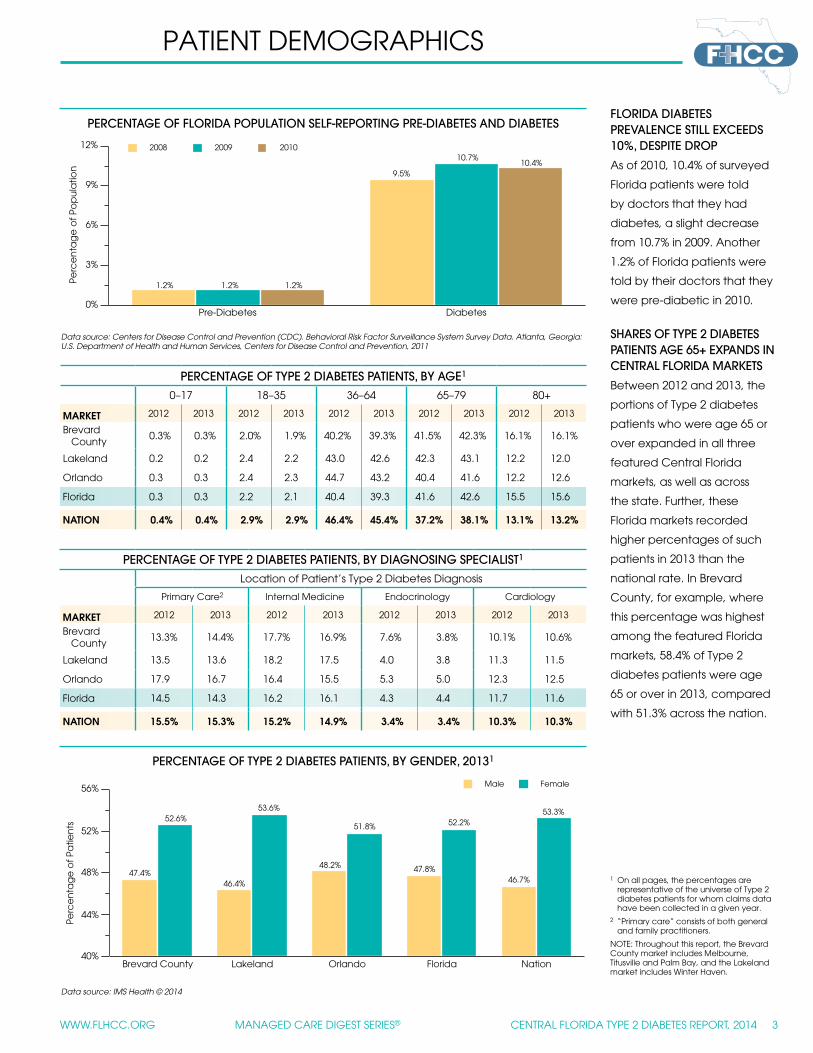

FLORIDA DIABETES PREVALENCE STILL EXCEEDS 10%, DESPITE DROP

As of 2010, 10.4% of surveyed

Florida patients were told

by doctors that they had

diabetes, a slight decrease

from 10.7% in 2009. Another

1.2% of Florida patients were

told by their doctors that they

were pre-diabetic in 2010.

SHARES OF TYPE 2 DIABETES PATIENTS AGE 65+ EXPANDS IN CENTRAL FLORIDA MARKETS

Between 2012 and 2013, the

portions of Type 2 diabetes

patients who were age 65 or

over expanded in all three

featured Central Florida

markets, as well as across

the state. Further, these

Florida markets recorded

higher percentages of such

patients in 2013 than the

national rate. In Brevard

County, for example, where

this percentage was highest

among the featured Florida

markets, 58.4% of Type 2

diabetes patients were age

65 or over in 2013, compared

with 51.3% across the nation.

PATIENT DEMOGRAPHICS

Data source: IMS Health © 2014

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY GENDER, 20131

1 On all pages, the percentages are representative of the universe of Type 2 diabetes patients for whom claims data have been collected in a given year.

2 “Primary care” consists of both general and family practitioners.

NOTE: Throughout this report, the Brevard County market includes Melbourne, Titusville and Palm Bay, and the Lakeland market includes Winter Haven.

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY AGE1

0–17 18–35 36–64 65–79 80+

MARKET 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

0.3% 0.3% 2.0% 1.9% 40.2% 39.3% 41.5% 42.3% 16.1% 16.1%

Lakeland 0.2 0.2 2.4 2.2 43.0 42.6 42.3 43.1 12.2 12.0

Orlando 0.3 0.3 2.4 2.3 44.7 43.2 40.4 41.6 12.2 12.6

Florida 0.3 0.3 2.2 2.1 40.4 39.3 41.6 42.6 15.5 15.6

NATION 0.4% 0.4% 2.9% 2.9% 46.4% 45.4% 37.2% 38.1% 13.1% 13.2%

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY DIAGNOSING SPECIALIST1

Location of Patient’s Type 2 Diabetes Diagnosis

Primary Care2 Internal Medicine Endocrinology Cardiology

MARKET 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

13.3% 14.4% 17.7% 16.9% 7.6% 3.8% 10.1% 10.6%

Lakeland 13.5 13.6 18.2 17.5 4.0 3.8 11.3 11.5

Orlando 17.9 16.7 16.4 15.5 5.3 5.0 12.3 12.5

Florida 14.5 14.3 16.2 16.1 4.3 4.4 11.7 11.6

NATION 15.5% 15.3% 15.2% 14.9% 3.4% 3.4% 10.3% 10.3%

Brevard County Lakeland Orlando Florida Nation40%

44%

48%

52%

56%

Perc

en

tag

e o

f Pa

tien

ts

47.4%

52.6%

46.4%

53.6%

48.2%

51.8%

47.8%

52.2%

46.7%

53.3%

Male Female

PERCENTAGE OF FLORIDA POPULATION SELF-REPORTING PRE-DIABETES AND DIABETES

Data source: Centers for Disease Control and Prevention (CDC). Behavioral Risk Factor Surveillance System Survey Data. Atlanta, Georgia: U.S. Department of Health and Human Services, Centers for Disease Control and Prevention, 2011

4 CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 MANAGED CARE DIGEST SERIES® www.flhcc.org

MEDICARE-COVERED SHARE

OF CENTRAL FLORIDA TYPE 2

DIABETES PATIENTS EXPANDS

For all three Central Florida

markets and the state as

a whole, the percentages

of Type 2 diabetes patients

covered by Medicare grew

between 2012 and 2013.

Data source: IMS Health © 2014

FLORIDA TYPE 2 DIABETES PATIENTS ARE MORE APT TO HAVE >2 COMPLICATIONS

Despite a slight decline in

Brevard County between

2012 and 2013, the shares of

Type 2 diabetes patients with

more than two complications

topped the corresponding

national average (20.6%) in all

four profiled Florida markets

in 2013. Type 2 diabetes

patients in Lakeland, Orlando

and across the state were

more prone to be diagnosed

with cardiovascular disease,

neuropathy or nephropathy

complications than their

counterparts across the U.S.

1 Includes HMOs, PPOs, point-of-service plans and exclusive provider organizations.2 A complication is defined as a patient condition caused by the Type 2 diabetes of the patient. These conditions are a direct result

of having Type 2 diabetes. Complications of Type 2 diabetes include, but are not limited to, cardiovascular disease, hypoglycemia, nephropathy, neuropathy and retinopathy.

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY NUMBER OF COMPLICATIONS2

0 1 2 >2

MARKET 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

53.0% 54.5% 15.6% 15.8% 9.5% 9.1% 21.9% 20.7%

Lakeland 48.0 47.5 15.0 14.3 9.3 9.2 27.8 29.1

Orlando 48.8 47.6 15.0 14.4 9.6 9.7 26.7 28.3

Florida 48.7 48.0 15.9 15.2 9.7 9.6 25.7 27.2

NATION 56.0% 55.0% 15.9% 15.6% 8.7% 8.8% 19.4% 20.6%

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY PAYER

Commercial Insurance1 Medicaid Medicare

MARKET 2012 2013 2012 2013 2012 2013

Brevard County

45.1% 44.6% 10.6% 10.6% 42.4% 43.0%

Lakeland 47.6 49.1 13.4 11.2 38.1 39.1

Orlando 48.7 47.2 11.2 10.2 38.7 41.4

Florida 48.0 47.9 9.4 8.7 41.7 42.5

NATION 50.2% 48.6% 9.9% 10.4% 39.2% 40.3%

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY PAYER, 2013

PATIENT DEMOGRAPHICS

Brevard County Lakeland Orlando Florida Nation0%

14%

28%

42%

56%

Perc

en

tag

e o

f Pa

tien

ts

44.6%

10.6%

43.0%

49.1%

11.2%

39.1%

47.2%

10.2%

41.4%

47.9%

8.7%

42.5%

48.6%

10.4%

40.3%

Commercial Insurance1 Medicaid Medicare

PERCENTAGE OF TYPE 2 DIABETES, BY TYPE OF COMPLICATION, 20132

MARKETCardiovascular

DiseaseNeuropathy Nephropathy Retinopathy Hypoglycemia

Brevard County

62.6% 31.0% 34.3% 13.5% 5.3%

Lakeland 59.1 40.1 31.3 20.0 7.8

Orlando 64.9 32.9 39.2 13.7 7.4

Florida 62.6 35.9 36.5 15.1 7.1

NATION 57.4% 32.7% 31.0% 18.5% 7.9%

WWW.FLHCC.ORG MANAGED CARE DIGEST SERIES® CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 5

USE OF SERVICES

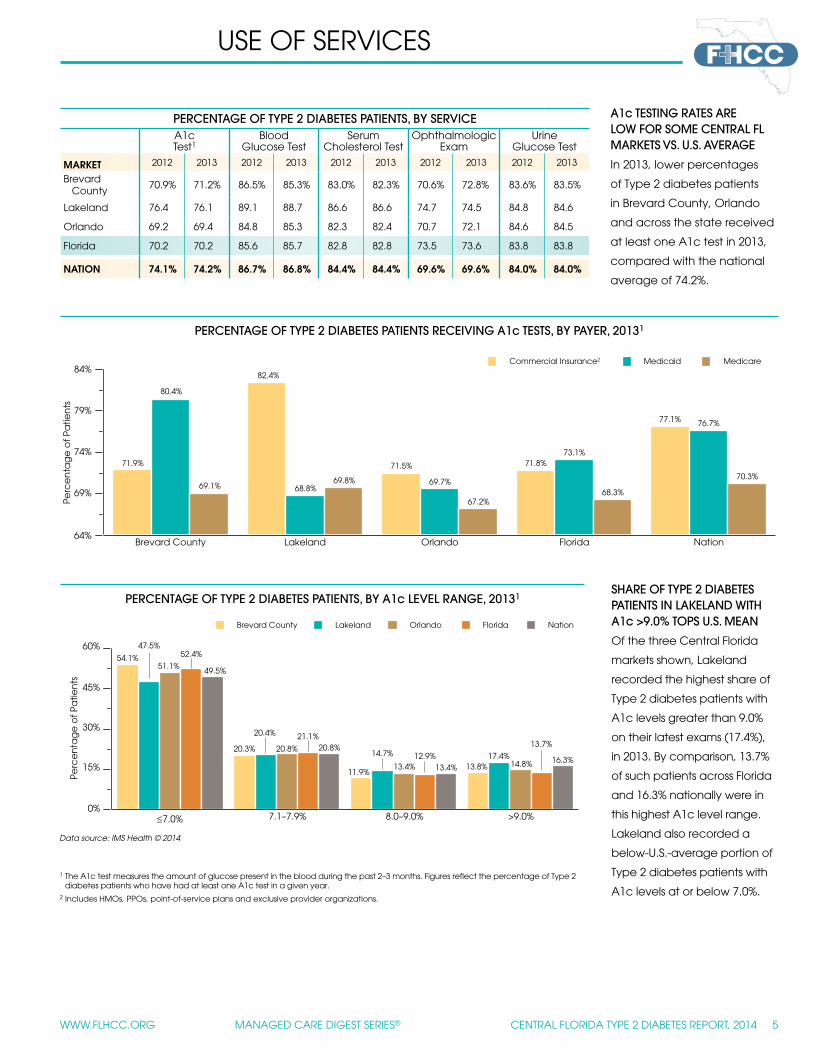

A1c TESTING RATES ARE LOW FOR SOME CENTRAL FL MARKETS VS. U.S. AVERAGE

In 2013, lower percentages

of Type 2 diabetes patients

in Brevard County, Orlando

and across the state received

at least one A1c test in 2013,

compared with the national

average of 74.2%.

1 The A1c test measures the amount of glucose present in the blood during the past 2–3 months. Figures reflect the percentage of Type 2 diabetes patients who have had at least one A1c test in a given year.

2 Includes HMOs, PPOs, point-of-service plans and exclusive provider organizations.

Data source: IMS Health © 2014

PERCENTAGE OF TYPE 2 DIABETES PATIENTS RECEIVING A1c TESTS, BY PAYER, 20131

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY SERVICEA1c Test1

Blood Glucose Test

Serum Cholesterol Test

Ophthalmologic Exam

Urine Glucose Test

MARKET 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

70.9% 71.2% 86.5% 85.3% 83.0% 82.3% 70.6% 72.8% 83.6% 83.5%

Lakeland 76.4 76.1 89.1 88.7 86.6 86.6 74.7 74.5 84.8 84.6

Orlando 69.2 69.4 84.8 85.3 82.3 82.4 70.7 72.1 84.6 84.5

Florida 70.2 70.2 85.6 85.7 82.8 82.8 73.5 73.6 83.8 83.8

NATION 74.1% 74.2% 86.7% 86.8% 84.4% 84.4% 69.6% 69.6% 84.0% 84.0%

PERCENTAGE OF TYPE 2 DIABETES PATIENTS, BY A1c LEVEL RANGE, 20131

Brevard County Lakeland Orlando Florida Nation64%

69%

74%

79%

84%

Perc

en

tag

e o

f Pa

tien

ts

71.9%

80.4%

69.1%

82.4%

68.8%69.8%

71.5%

69.7%

67.2%

71.8%73.1%

68.3%

77.1% 76.7%

70.3%

Commercial Insurance2 Medicaid Medicare

≤7.0% 7.1–7.9% 8.0–9.0% >9.0%0%

15%

30%

45%

60%

Perc

en

tag

e o

f Pa

tien

ts

54.1%

47.5%

51.1%

52.4%

49.5%

20.3%

20.4%

20.8%

21.1%20.8%

11.9%

14.7%

13.4%12.9%

13.4% 13.8%17.4%

14.8%

13.7%

16.3%

Brevard County Lakeland Orlando Florida Nation

SHARE OF TYPE 2 DIABETES PATIENTS IN LAKELAND WITH A1c >9.0% TOPS U.S. MEAN

Of the three Central Florida

markets shown, Lakeland

recorded the highest share of

Type 2 diabetes patients with

A1c levels greater than 9.0%

on their latest exams (17.4%),

in 2013. By comparison, 13.7%

of such patients across Florida

and 16.3% nationally were in

this highest A1c level range.

Lakeland also recorded a

below-U.S.-average portion of

Type 2 diabetes patients with

A1c levels at or below 7.0%.

6 CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 MANAGED CARE DIGEST SERIES® www.flhcc.org

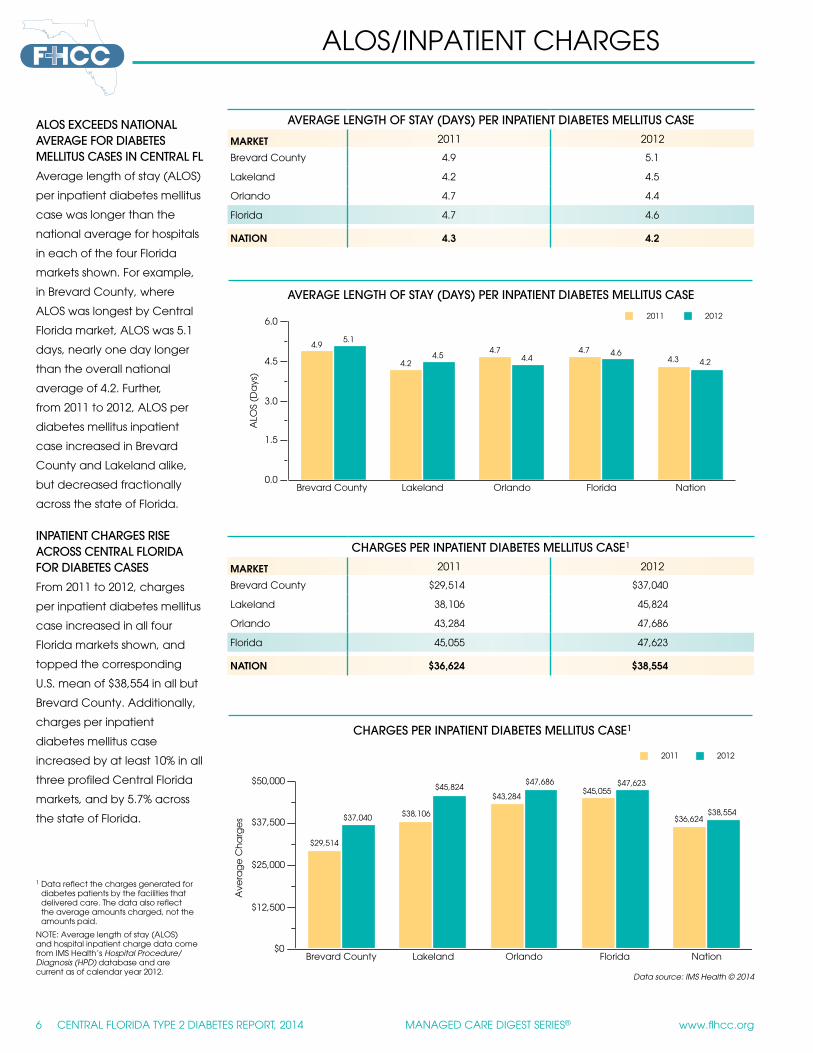

ALOS EXCEEDS NATIONAL AVERAGE FOR DIABETES MELLITUS CASES IN CENTRAL FL

Average length of stay (ALOS)

per inpatient diabetes mellitus

case was longer than the

national average for hospitals

in each of the four Florida

markets shown. For example,

in Brevard County, where

ALOS was longest by Central

Florida market, ALOS was 5.1

days, nearly one day longer

than the overall national

average of 4.2. Further,

from 2011 to 2012, ALOS per

diabetes mellitus inpatient

case increased in Brevard

County and Lakeland alike,

but decreased fractionally

across the state of Florida.

INPATIENT CHARGES RISE ACROSS CENTRAL FLORIDA FOR DIABETES CASES

From 2011 to 2012, charges

per inpatient diabetes mellitus

case increased in all four

Florida markets shown, and

topped the corresponding

U.S. mean of $38,554 in all but

Brevard County. Additionally,

charges per inpatient

diabetes mellitus case

increased by at least 10% in all

three profiled Central Florida

markets, and by 5.7% across

the state of Florida.

ALOS/INPATIENT CHARGES

Data source: IMS Health © 2014

CHARGES PER INPATIENT DIABETES MELLITUS CASE1

1 Data reflect the charges generated for diabetes patients by the facilities that delivered care. The data also reflect the average amounts charged, not the amounts paid.

NOTE: Average length of stay (ALOS) and hospital inpatient charge data come from IMS Health’s Hospital Procedure/Diagnosis (HPD) database and are current as of calendar year 2012.

AVERAGE LENGTH OF STAY (DAYS) PER INPATIENT DIABETES MELLITUS CASE

MARKET 2011 2012

Brevard County 4.9 5.1

Lakeland 4.2 4.5

Orlando 4.7 4.4

Florida 4.7 4.6

NATION 4.3 4.2

AVERAGE LENGTH OF STAY (DAYS) PER INPATIENT DIABETES MELLITUS CASE

Brevard County Lakeland Orlando Florida Nation0.0

1.5

3.0

4.5

6.0

ALO

S (D

ays

)

4.95.1

4.24.5

4.74.4

4.7 4.64.3 4.2

2011 2012

Brevard County Lakeland Orlando Florida Nation$0

$12,500

$25,000

$37,500

$50,000

Ave

rag

e C

ha

rge

s

$29,514

$37,040 $38,106

$45,824$43,284

$47,686$45,055

$47,623

$36,624$38,554

2011 2012

CHARGES PER INPATIENT DIABETES MELLITUS CASE1

MARKET 2011 2012

Brevard County $29,514 $37,040

Lakeland 38,106 45,824

Orlando 43,284 47,686

Florida 45,055 47,623

NATION $36,624 $38,554

WWW.FLHCC.ORG MANAGED CARE DIGEST SERIES® CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 7

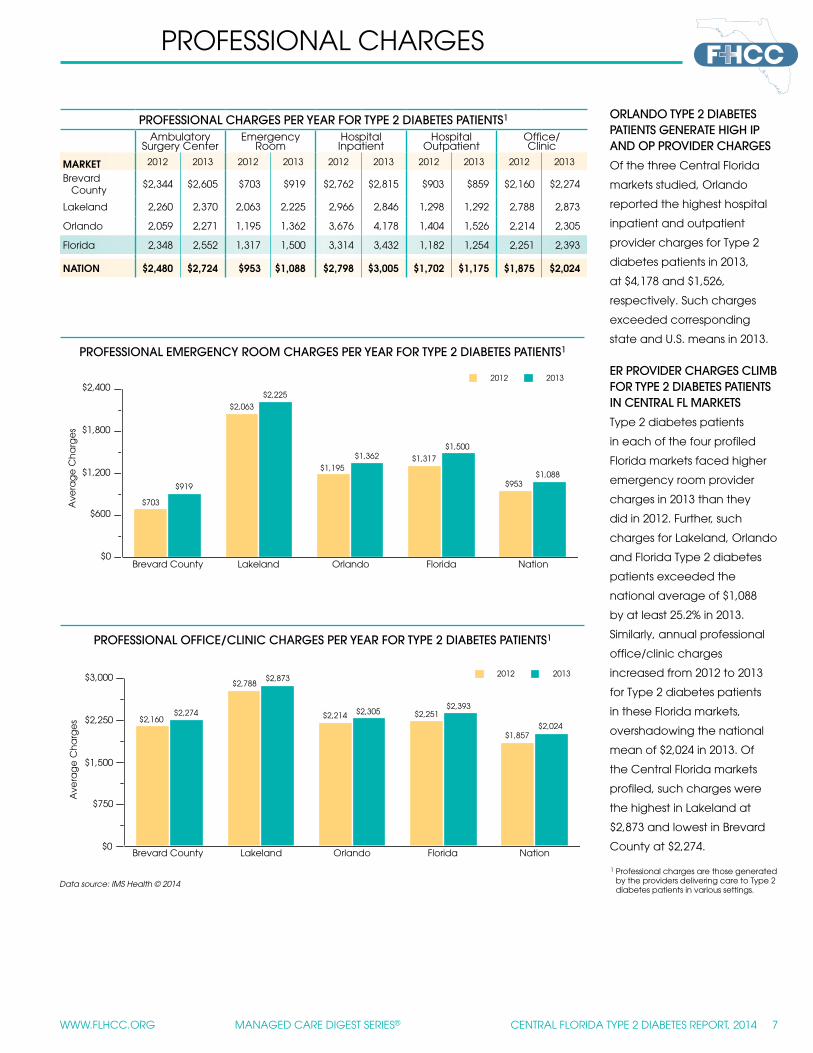

PROFESSIONAL CHARGES

Data source: IMS Health © 2014

PROFESSIONAL EMERGENCY ROOM CHARGES PER YEAR FOR TYPE 2 DIABETES PATIENTS1

PROFESSIONAL CHARGES PER YEAR FOR TYPE 2 DIABETES PATIENTS1

Ambulatory Surgery Center

Emergency Room

Hospital Inpatient

Hospital Outpatient

Office/ Clinic

MARKET 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

$2,344 $2,605 $703 $919 $2,762 $2,815 $903 $859 $2,160 $2,274

Lakeland 2,260 2,370 2,063 2,225 2,966 2,846 1,298 1,292 2,788 2,873

Orlando 2,059 2,271 1,195 1,362 3,676 4,178 1,404 1,526 2,214 2,305

Florida 2,348 2,552 1,317 1,500 3,314 3,432 1,182 1,254 2,251 2,393

NATION $2,480 $2,724 $953 $1,088 $2,798 $3,005 $1,702 $1,175 $1,875 $2,024

1 Professional charges are those generated by the providers delivering care to Type 2 diabetes patients in various settings.

ORLANDO TYPE 2 DIABETES PATIENTS GENERATE HIGH IP AND OP PROVIDER CHARGES

Of the three Central Florida

markets studied, Orlando

reported the highest hospital

inpatient and outpatient

provider charges for Type 2

diabetes patients in 2013,

at $4,178 and $1,526,

respectively. Such charges

exceeded corresponding

state and U.S. means in 2013.

ER PROVIDER CHARGES CLIMB FOR TYPE 2 DIABETES PATIENTS IN CENTRAL FL MARKETS

Type 2 diabetes patients

in each of the four profiled

Florida markets faced higher

emergency room provider

charges in 2013 than they

did in 2012. Further, such

charges for Lakeland, Orlando

and Florida Type 2 diabetes

patients exceeded the

national average of $1,088

by at least 25.2% in 2013.

Similarly, annual professional

office/clinic charges

increased from 2012 to 2013

for Type 2 diabetes patients

in these Florida markets,

overshadowing the national

mean of $2,024 in 2013. Of

the Central Florida markets

profiled, such charges were

the highest in Lakeland at

$2,873 and lowest in Brevard

County at $2,274.

PROFESSIONAL OFFICE/CLINIC CHARGES PER YEAR FOR TYPE 2 DIABETES PATIENTS1

Brevard County Lakeland Orlando Florida Nation$0

$600

$1,200

$1,800

$2,400

Ave

rag

e C

ha

rge

s

$703

$919

$2,063

$2,225

$1,195

$1,362 $1,317

$1,500

$953$1,088

2012 2013

Brevard County Lakeland Orlando Florida Nation$0

$750

$1,500

$2,250

$3,000

Ave

rag

e C

ha

rge

s $2,160$2,274

$2,788$2,873

$2,214 $2,305 $2,251$2,393

$1,857$2,024

2012 2013

8 CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 MANAGED CARE DIGEST SERIES® www.flhcc.org

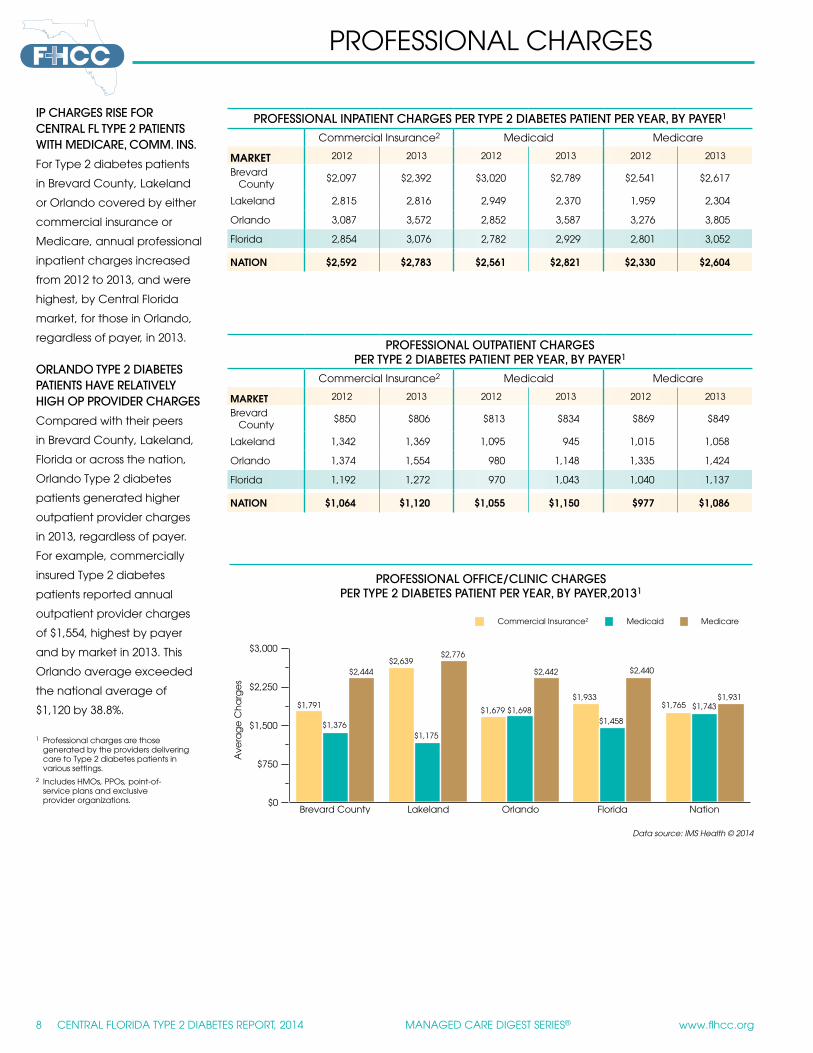

1 Professional charges are those generated by the providers delivering care to Type 2 diabetes patients in various settings.

2 Includes HMOs, PPOs, point-of- service plans and exclusive provider organizations.

PROFESSIONAL OFFICE/CLINIC CHARGES PER TYPE 2 DIABETES PATIENT PER YEAR, BY PAYER,20131

IP CHARGES RISE FOR CENTRAL FL TYPE 2 PATIENTS WITH MEDICARE, COMM. INS.

For Type 2 diabetes patients

in Brevard County, Lakeland

or Orlando covered by either

commercial insurance or

Medicare, annual professional

inpatient charges increased

from 2012 to 2013, and were

highest, by Central Florida

market, for those in Orlando,

regardless of payer, in 2013.

ORLANDO TYPE 2 DIABETES PATIENTS HAVE RELATIVELY HIGH OP PROVIDER CHARGES

Compared with their peers

in Brevard County, Lakeland,

Florida or across the nation,

Orlando Type 2 diabetes

patients generated higher

outpatient provider charges

in 2013, regardless of payer.

For example, commercially

insured Type 2 diabetes

patients reported annual

outpatient provider charges

of $1,554, highest by payer

and by market in 2013. This

Orlando average exceeded

the national average of

$1,120 by 38.8%.

PROFESSIONAL CHARGES

Data source: IMS Health © 2014

PROFESSIONAL OUTPATIENT CHARGES PER TYPE 2 DIABETES PATIENT PER YEAR, BY PAYER1

Commercial Insurance2 Medicaid Medicare

MARKET 2012 2013 2012 2013 2012 2013

Brevard County

$850 $806 $813 $834 $869 $849

Lakeland 1,342 1,369 1,095 945 1,015 1,058

Orlando 1,374 1,554 980 1,148 1,335 1,424

Florida 1,192 1,272 970 1,043 1,040 1,137

NATION $1,064 $1,120 $1,055 $1,150 $977 $1,086

PROFESSIONAL INPATIENT CHARGES PER TYPE 2 DIABETES PATIENT PER YEAR, BY PAYER1

Commercial Insurance2 Medicaid Medicare

MARKET 2012 2013 2012 2013 2012 2013

Brevard County

$2,097 $2,392 $3,020 $2,789 $2,541 $2,617

Lakeland 2,815 2,816 2,949 2,370 1,959 2,304

Orlando 3,087 3,572 2,852 3,587 3,276 3,805

Florida 2,854 3,076 2,782 2,929 2,801 3,052

NATION $2,592 $2,783 $2,561 $2,821 $2,330 $2,604

Brevard County Lakeland Orlando Florida Nation$0

$750

$1,500

$2,250

$3,000

Ave

rag

e C

ha

rge

s

$1,791

$1,376

$2,444$2,639

$1,175

$2,776

$1,679 $1,698

$2,442

$1,933

$1,458

$2,440

$1,765 $1,743$1,931

Commercial Insurance2 Medicaid Medicare

WWW.FLHCC.ORG MANAGED CARE DIGEST SERIES® CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 9

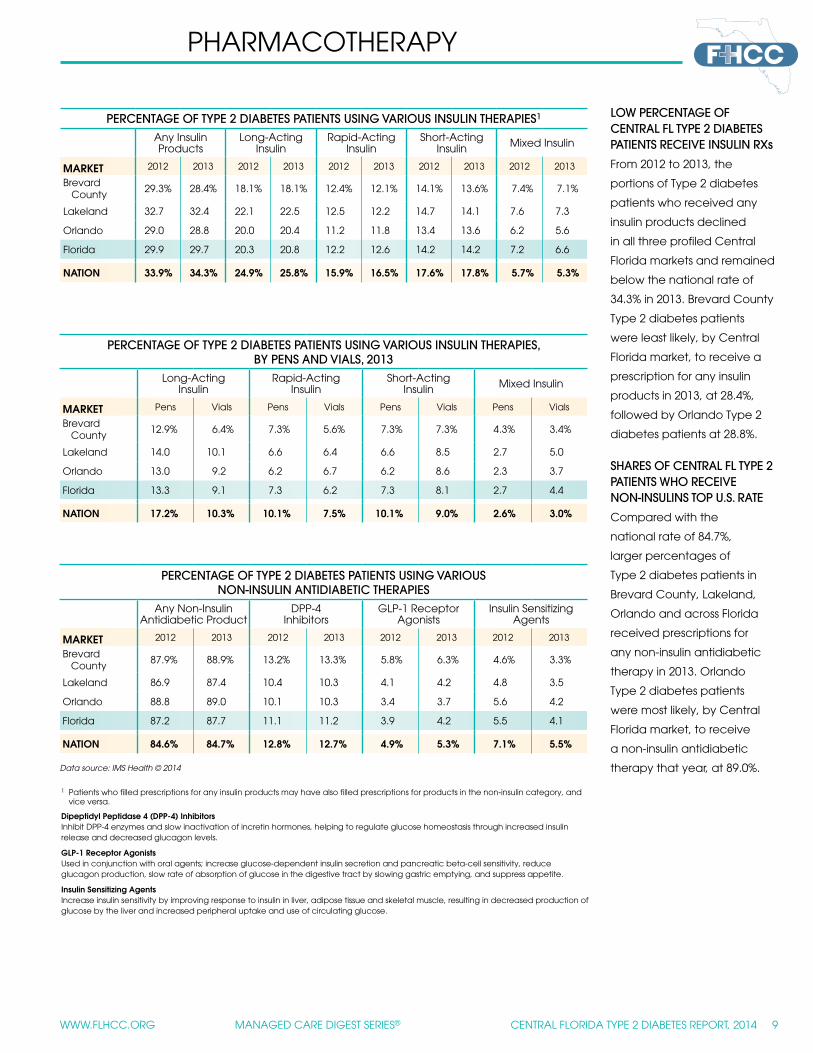

LOW PERCENTAGE OF CENTRAL FL TYPE 2 DIABETES PATIENTS RECEIVE INSULIN RXs

From 2012 to 2013, the

portions of Type 2 diabetes

patients who received any

insulin products declined

in all three profiled Central

Florida markets and remained

below the national rate of

34.3% in 2013. Brevard County

Type 2 diabetes patients

were least likely, by Central

Florida market, to receive a

prescription for any insulin

products in 2013, at 28.4%,

followed by Orlando Type 2

diabetes patients at 28.8%.

SHARES OF CENTRAL FL TYPE 2 PATIENTS WHO RECEIVE NON-INSULINS TOP U.S. RATE

Compared with the

national rate of 84.7%,

larger percentages of

Type 2 diabetes patients in

Brevard County, Lakeland,

Orlando and across Florida

received prescriptions for

any non-insulin antidiabetic

therapy in 2013. Orlando

Type 2 diabetes patients

were most likely, by Central

Florida market, to receive

a non-insulin antidiabetic

therapy that year, at 89.0%.Data source: IMS Health © 2014

PERCENTAGE OF TYPE 2 DIABETES PATIENTS USING VARIOUS INSULIN THERAPIES1

Any Insulin Products

Long-Acting Insulin

Rapid-Acting Insulin

Short-Acting Insulin Mixed Insulin

MARKET 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

29.3% 28.4% 18.1% 18.1% 12.4% 12.1% 14.1% 13.6% 7.4% 7.1%

Lakeland 32.7 32.4 22.1 22.5 12.5 12.2 14.7 14.1 7.6 7.3

Orlando 29.0 28.8 20.0 20.4 11.2 11.8 13.4 13.6 6.2 5.6

Florida 29.9 29.7 20.3 20.8 12.2 12.6 14.2 14.2 7.2 6.6

NATION 33.9% 34.3% 24.9% 25.8% 15.9% 16.5% 17.6% 17.8% 5.7% 5.3%

PERCENTAGE OF TYPE 2 DIABETES PATIENTS USING VARIOUS NON-INSULIN ANTIDIABETIC THERAPIES

Any Non-Insulin Antidiabetic Product

DPP-4 Inhibitors

GLP-1 Receptor Agonists

Insulin Sensitizing Agents

MARKET 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

87.9% 88.9% 13.2% 13.3% 5.8% 6.3% 4.6% 3.3%

Lakeland 86.9 87.4 10.4 10.3 4.1 4.2 4.8 3.5

Orlando 88.8 89.0 10.1 10.3 3.4 3.7 5.6 4.2

Florida 87.2 87.7 11.1 11.2 3.9 4.2 5.5 4.1

NATION 84.6% 84.7% 12.8% 12.7% 4.9% 5.3% 7.1% 5.5%

PERCENTAGE OF TYPE 2 DIABETES PATIENTS USING VARIOUS INSULIN THERAPIES, BY PENS AND VIALS, 2013

Long-Acting Insulin

Rapid-Acting Insulin

Short-Acting Insulin Mixed Insulin

MARKET Pens Vials Pens Vials Pens Vials Pens Vials

Brevard County

12.9% 6.4% 7.3% 5.6% 7.3% 7.3% 4.3% 3.4%

Lakeland 14.0 10.1 6.6 6.4 6.6 8.5 2.7 5.0

Orlando 13.0 9.2 6.2 6.7 6.2 8.6 2.3 3.7

Florida 13.3 9.1 7.3 6.2 7.3 8.1 2.7 4.4

NATION 17.2% 10.3% 10.1% 7.5% 10.1% 9.0% 2.6% 3.0%

PHARMACOTHERAPY

1 Patients who filled prescriptions for any insulin products may have also filled prescriptions for products in the non-insulin category, and vice versa.

Dipeptidyl Peptidase 4 (DPP-4) Inhibitors Inhibit DPP-4 enzymes and slow inactivation of incretin hormones, helping to regulate glucose homeostasis through increased insulin release and decreased glucagon levels.

GLP-1 Receptor Agonists Used in conjunction with oral agents; increase glucose-dependent insulin secretion and pancreatic beta-cell sensitivity, reduce glucagon production, slow rate of absorption of glucose in the digestive tract by slowing gastric emptying, and suppress appetite.

Insulin Sensitizing Agents Increase insulin sensitivity by improving response to insulin in liver, adipose tissue and skeletal muscle, resulting in decreased production of glucose by the liver and increased peripheral uptake and use of circulating glucose.

10 CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 MANAGED CARE DIGEST SERIES® www.flhcc.org

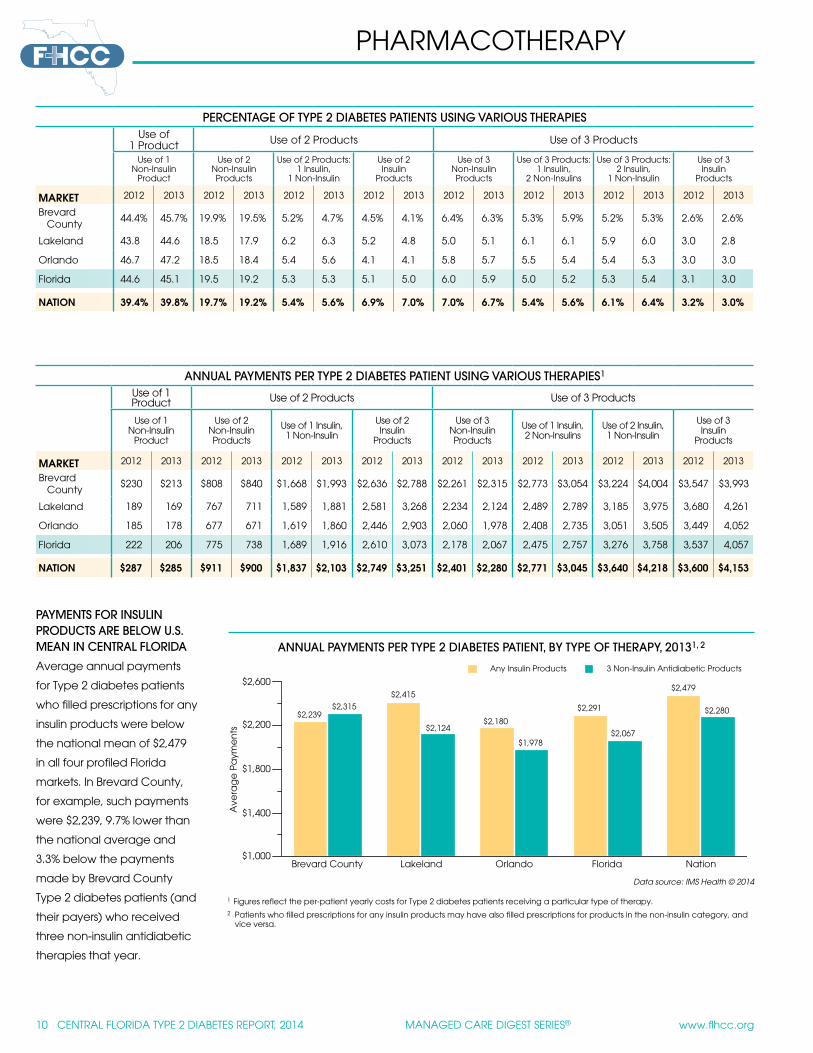

PAYMENTS FOR INSULIN PRODUCTS ARE BELOW U.S. MEAN IN CENTRAL FLORIDA

Average annual payments

for Type 2 diabetes patients

who filled prescriptions for any

insulin products were below

the national mean of $2,479

in all four profiled Florida

markets. In Brevard County,

for example, such payments

were $2,239, 9.7% lower than

the national average and

3.3% below the payments

made by Brevard County

Type 2 diabetes patients (and

their payers) who received

three non-insulin antidiabetic

therapies that year.

1 Figures reflect the per-patient yearly costs for Type 2 diabetes patients receiving a particular type of therapy.2 Patients who filled prescriptions for any insulin products may have also filled prescriptions for products in the non-insulin category, and

vice versa.

PERCENTAGE OF TYPE 2 DIABETES PATIENTS USING VARIOUS THERAPIESUse of

1 Product Use of 2 Products Use of 3 Products

Use of 1 Non-Insulin

Product

Use of 2 Non-Insulin Products

Use of 2 Products: 1 Insulin,

1 Non-Insulin

Use of 2 Insulin

Products

Use of 3 Non-Insulin Products

Use of 3 Products: 1 Insulin,

2 Non-Insulins

Use of 3 Products: 2 Insulin,

1 Non-Insulin

Use of 3 Insulin

Products

MARKET 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

44.4% 45.7% 19.9% 19.5% 5.2% 4.7% 4.5% 4.1% 6.4% 6.3% 5.3% 5.9% 5.2% 5.3% 2.6% 2.6%

Lakeland 43.8 44.6 18.5 17.9 6.2 6.3 5.2 4.8 5.0 5.1 6.1 6.1 5.9 6.0 3.0 2.8

Orlando 46.7 47.2 18.5 18.4 5.4 5.6 4.1 4.1 5.8 5.7 5.5 5.4 5.4 5.3 3.0 3.0

Florida 44.6 45.1 19.5 19.2 5.3 5.3 5.1 5.0 6.0 5.9 5.0 5.2 5.3 5.4 3.1 3.0

NATION 39.4% 39.8% 19.7% 19.2% 5.4% 5.6% 6.9% 7.0% 7.0% 6.7% 5.4% 5.6% 6.1% 6.4% 3.2% 3.0%

ANNUAL PAYMENTS PER TYPE 2 DIABETES PATIENT USING VARIOUS THERAPIES1

Use of 1 Product Use of 2 Products Use of 3 Products

Use of 1 Non-Insulin

Product

Use of 2 Non-Insulin Products

Use of 1 Insulin, 1 Non-Insulin

Use of 2 Insulin

Products

Use of 3 Non-Insulin Products

Use of 1 Insulin, 2 Non-Insulins

Use of 2 Insulin, 1 Non-Insulin

Use of 3 Insulin

Products

MARKET 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013

Brevard County

$230 $213 $808 $840 $1,668 $1,993 $2,636 $2,788 $2,261 $2,315 $2,773 $3,054 $3,224 $4,004 $3,547 $3,993

Lakeland 189 169 767 711 1,589 1,881 2,581 3,268 2,234 2,124 2,489 2,789 3,185 3,975 3,680 4,261

Orlando 185 178 677 671 1,619 1,860 2,446 2,903 2,060 1,978 2,408 2,735 3,051 3,505 3,449 4,052

Florida 222 206 775 738 1,689 1,916 2,610 3,073 2,178 2,067 2,475 2,757 3,276 3,758 3,537 4,057

NATION $287 $285 $911 $900 $1,837 $2,103 $2,749 $3,251 $2,401 $2,280 $2,771 $3,045 $3,640 $4,218 $3,600 $4,153

Data source: IMS Health © 2014

ANNUAL PAYMENTS PER TYPE 2 DIABETES PATIENT, BY TYPE OF THERAPY, 20131, 2

PHARMACOTHERAPY

$1,000

$1,400

$1,800

$2,200

$2,600

Ave

rag

e P

aym

en

ts

Brevard County Lakeland Orlando Florida Nation

$2,239$2,315

$2,415

$2,124$2,180

$1,978

$2,291

$2,067

$2,479

$2,280

Any Insulin Products 3 Non-Insulin Antidiabetic Products

WWW.FLHCC.ORG MANAGED CARE DIGEST SERIES® CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 11

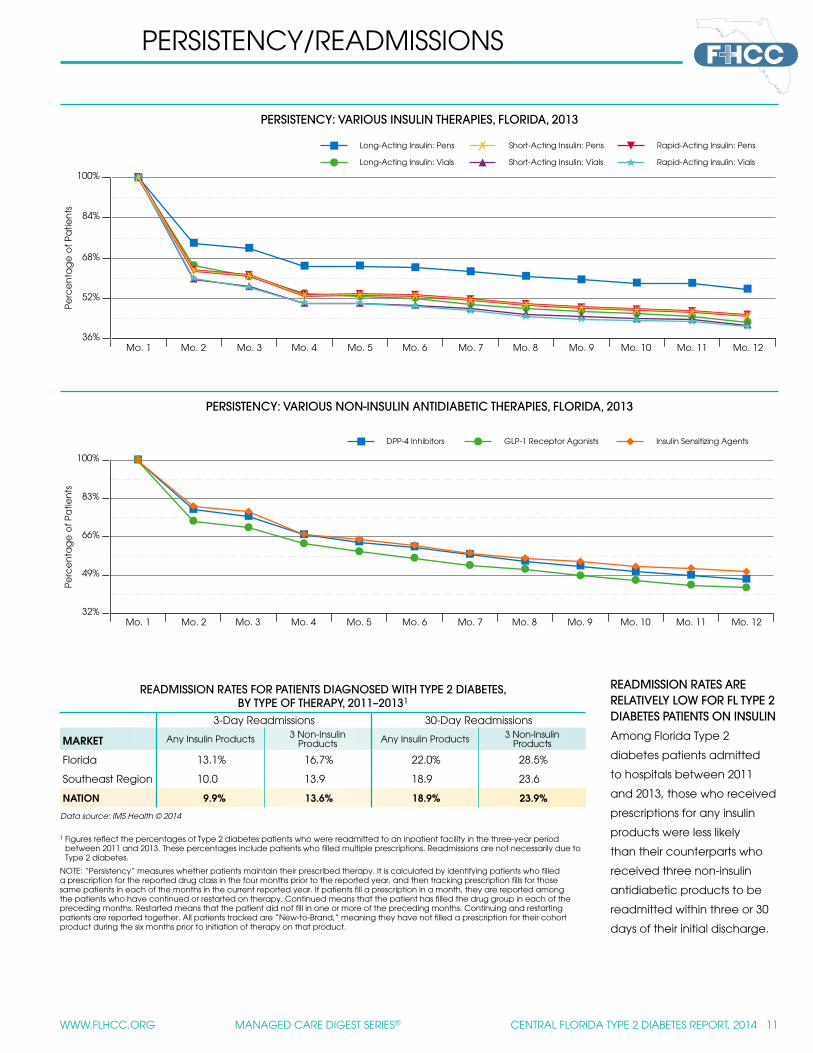

READMISSION RATES FOR PATIENTS DIAGNOSED WITH TYPE 2 DIABETES, BY TYPE OF THERAPY, 2011–20131

3-Day Readmissions 30-Day Readmissions

MARKET Any Insulin Products 3 Non-Insulin Products Any Insulin Products 3 Non-Insulin

Products

Florida 13.1% 16.7% 22.0% 28.5%

Southeast Region 10.0 13.9 18.9 23.6

NATION 9.9% 13.6% 18.9% 23.9%

PERSISTENCY/READMISSIONS

READMISSION RATES ARE RELATIVELY LOW FOR FL TYPE 2 DIABETES PATIENTS ON INSULIN

Among Florida Type 2

diabetes patients admitted

to hospitals between 2011

and 2013, those who received

prescriptions for any insulin

products were less likely

than their counterparts who

received three non-insulin

antidiabetic products to be

readmitted within three or 30

days of their initial discharge.

Data source: IMS Health © 2014

1 Figures reflect the percentages of Type 2 diabetes patients who were readmitted to an inpatient facility in the three-year period between 2011 and 2013. These percentages include patients who filled multiple prescriptions. Readmissions are not necessarily due to Type 2 diabetes.

NOTE: “Persistency” measures whether patients maintain their prescribed therapy. It is calculated by identifying patients who filled a prescription for the reported drug class in the four months prior to the reported year, and then tracking prescription fills for those same patients in each of the months in the current reported year. If patients fill a prescription in a month, they are reported among the patients who have continued or restarted on therapy. Continued means that the patient has filled the drug group in each of the preceding months. Restarted means that the patient did not fill in one or more of the preceding months. Continuing and restarting patients are reported together. All patients tracked are “New-to-Brand,” meaning they have not filled a prescription for their cohort product during the six months prior to initiation of therapy on that product.

PERSISTENCY: VARIOUS INSULIN THERAPIES, FLORIDA, 2013

PERSISTENCY: VARIOUS NON-INSULIN ANTIDIABETIC THERAPIES, FLORIDA, 2013

Mo. 1 Mo. 2 Mo. 3 Mo. 4 Mo. 5 Mo. 6 Mo. 7 Mo. 8 Mo. 9 Mo. 10 Mo. 11 Mo. 1232%

49%

66%

83%

100%

Perc

en

tag

e o

f Pa

tien

ts

DPP-4 Inhibitors GLP-1 Receptor Agonists Insulin Sensitizing Agents

Mo. 1 Mo. 2 Mo. 3 Mo. 4 Mo. 5 Mo. 6 Mo. 7 Mo. 8 Mo. 9 Mo. 10 Mo. 11 Mo. 1236%

52%

68%

84%

100%

Perc

en

tag

e o

f Pa

tien

ts

Long-Acting Insulin: Pens

Long-Acting Insulin: Vials

Short-Acting Insulin: Pens

Short-Acting Insulin: Vials

Rapid-Acting Insulin: Pens

Rapid-Acting Insulin: Vials

12 CENTRAL FLORIDA TYPE 2 DIABETES REPORT, 2014 MANAGED CARE DIGEST SERIES® www.flhcc.org

Sanofi U.S. LLC, as sponsor of this report, maintains an arm’s-length relationship with the organizations that prepare the report and carry out the research for its contents. The desire of Sanofi U.S. is that the information in this report be completely independent and objective.

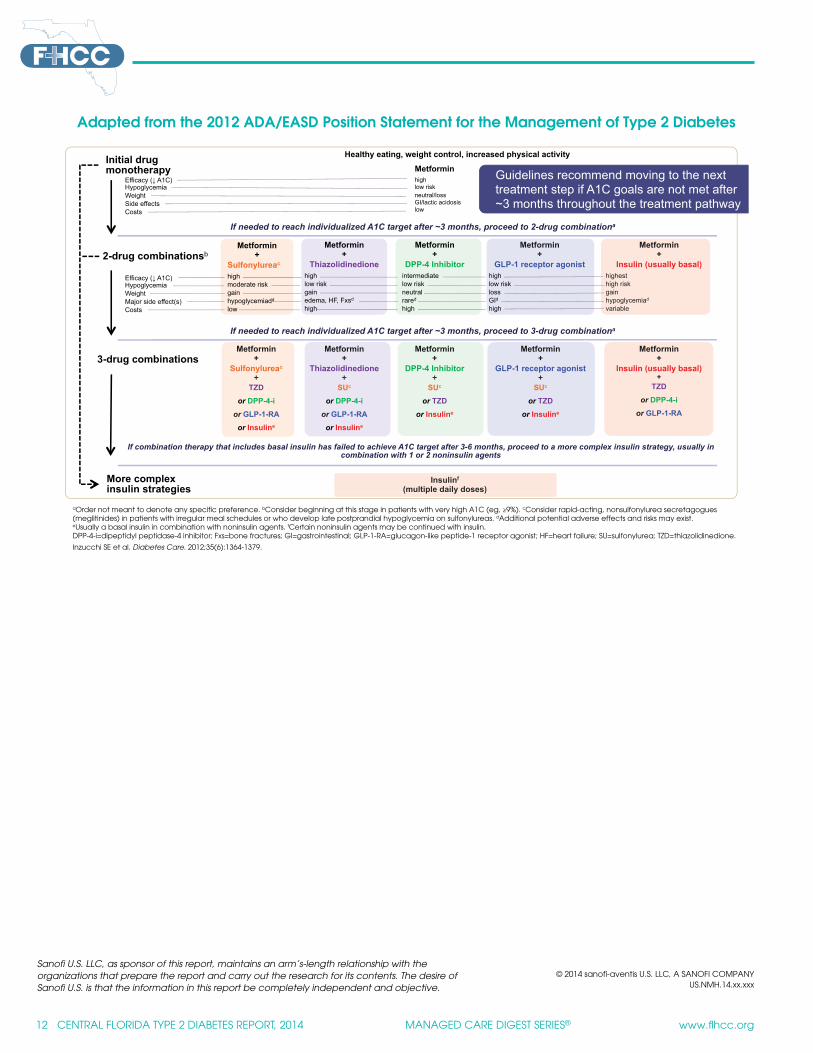

Adapted from the 2012 ADA/EASD Position Statement for the Management of Type 2 Diabetes

Metformin +

Thiazolidinedione

high low risk gain edema, HF, Fxsd

high

Metformin +

DPP-4 Inhibitor intermediate low risk neutral rared

high

Metformin +

Insulin (usually basal)

highest high risk gain hypoglycemiad

variable

Metformin +

GLP-1 receptor agonist

high low risk loss GId

high

2-drug combinationsb

If needed to reach individualized A1C target after ~3 months, proceed to 3-drug combinationa

Efficacy ( A1C) Hypoglycemia Weight Major side effect(s) Costs

Metformin +

Sulfonylureac high moderate risk gain hypoglycemiadd

low

Healthy eating, weight control, increased physical activity

Metformin high low risk neutral/loss GI/lactic acidosis low

If needed to reach individualized A1C target after ~3 months, proceed to 2-drug combinationa

Initial drug monotherapy

Efficacy ( A1C) Hypoglycemia Weight Side effects Costs

3-drug combinations Metformin

+ GLP-1 receptor agonist

+ SUc

or TZD

or Insuline

Metformin +

Insulin (usually basal)

+ TZD

or DPP-4-i

or GLP-1-RA

Metformin +

DPP-4 Inhibitor +

SUc

or TZD

or Insuline

Metformin +

Thiazolidinedione +

SUc

or DPP-4-i

or GLP-1-RA

or Insuline

Metformin +

Sulfonylureac +

TZD

or DPP-4-i

or GLP-1-RA

or Insuline

More complex insulin strategies

Insulinf

(multiple daily doses)

If combination therapy that includes basal insulin has failed to achieve A1C target after 3-6 months, proceed to a more complex insulin strategy, usually in combination with 1 or 2 noninsulin agents

Guidelines recommend moving to the next treatment step if A1C goals are not met after ~3 months throughout the treatment pathway

aOrder not meant to denote any specific preference. bConsider beginning at this stage in patients with very high A1C (eg, ≥9%). cConsider rapid-acting, nonsulfonylurea secretagogues(meglitinides) in patients with irregular meal schedules or who develop late postprandial hypoglycemia on sulfonylureas. dAdditional potential adverse effects and risks may exist.eUsually a basal insulin in combination with noninsulin agents. fCertain noninsulin agents may be continued with insulin.DPP-4-i=dipeptidyl peptidase-4 inhibitor; Fxs=bone fractures; GI=gastrointestinal; GLP-1-RA=glucagon-like peptide-1 receptor agonist; HF=heart failure; SU=sulfonylurea; TZD=thiazolidinedione.

Inzucchi SE et al. Diabetes Care. 2012;35(6):1364-1379.

© 2014 sanofi-aventis U.S. LLC, A SANOFI COMPANYUS.NMH.14.xx.xxx

Related Documents