ACTION RESEARCH CREDIT CONNECTIONS Meeting the Infrastructure Needs of the Informal UNDP- Sector through Microfinance World Bank U a Water and In Urban India Sanitation Program 31280 South Asia Region This report describes ' the 'Action Research' | - q component of the study s4 on 'Meeting Infrastructure Needs of . the Informal Sector through Microfinance in Urban India'. The Action Research component was - designed to complement A the four case studies of existing microfinance A^. institutions providing NM credit for water supply -- N -t and sanitation to poor women in the informal _- sector and to explore the practical requirements of - microcredit for - infrastructure. Action Research was carried out between December - 1998 and April 1999. ,hk,,) -- Gujarat Mahila Housing SEWA Trust | t Q w 1 ~~~~~~~~- 9X 7'7 _ U'Illqll ! ^ ,F 0 s Emw-2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACTION RESEARCH

CREDIT CONNECTIONSMeeting the InfrastructureNeeds of the Informal

UNDP- Sector through MicrofinanceWorld Bank U aWater and In Urban IndiaSanitationProgram 31280

South Asia RegionThis report describes 'the 'Action Research' | - q component of the study s4on 'MeetingInfrastructure Needs of .the Informal Sectorthrough Microfinance inUrban India'.

The Action Researchcomponent was -

designed to complement Athe four case studies ofexisting microfinance A^.institutions providing NM credit for water supply --

N -t

and sanitation to poorwomen in the informal _-

sector and to explore thepractical requirements of -microcredit for -

infrastructure. ActionResearch was carriedout between December -

1998 and April 1999. ,hk,,) --

Gujarat MahilaHousing SEWA Trust

| t Q w 1 ~~~~~~~~- 9X 7'7 _ U'Illqll ! ^ ,F 0

s Emw-2

-

Action Research: Introduction 3

Action Research: Phase I 5

Action Research: Phase II 15

Proposed Loan Process Maps 16

Proposed Housing and Infrastructure Loan System 18

Annexures I to VI 20

The main objective of the Action Research was to:Develop a prototype housing and infrastructure finance department

model with appropriate accounting, reporting and loan evaluationsystems for financial institutions disbursing credit to poor women in theurban informal sector in India.

The Action Research was undertaken in two phases. Phase I of the Action Researchcomponent of this initiative was undertaken by working in partnership with SEWABank, Ahmedabad. Phase If involved the development of the prototype model, basedon the findings of Phase 1. The methodology and findings of the Action Researchshould provide useful pointers to microfinance institutions around the country, on howto approach the establishment of specialized infrastructure and housing services.

Rationale for the 1 00 percent maintenance costs) infrastructure loans are a new,Action Research have shown high success rates in emerging sector coupled with the

providing improved infrastructure extremely high field-level demandThere are a growing number of to poor consumers. Four examples for such loan types, grassroots

emerging microfinance institutions of such success stories are institutions are often unable toin urban India that are facilitating documented in the Field Notes cope with the growth in the sector.poor communities to access attached. Housing and infrastructure loansimproved shelter and services Field-level interviews have are characterized by longerthrough the provision of small- clearly demonstrated that demand repayment terms and are usuallyscale credit. These include credit to for credit is very high amongst the of a relatively higher volume, aspay for water connections, informal sector poor. With compared to income generation orhandpumps, electricity increasing demand at the consumption loans. Thisconnections, construct toilets and grassroots for better shelter and necessitates access to bulk re-upgrade homes. Interestingly, services, small-scale loans finance from mainstream financemicrofinance institutions are accessed from microfinance institutions for on-lending.increasingly emerging in new institutions are an effective Traditional collateral such as landpartnerships involving facilitating tool. However, title deeds are also largelymunicipalities, poor communities microfinance institutions face a unavailable within the informaland various other partners such as variety of institutional problems in sector, due to lack of legal landnon-governmental organizations accessing adequate funds for on- tenure.and donor agencies involved in lending to poor communities. Despite these distinguishingslum upgradation projects. Loans Some of these are highlighted in characteristics, most microfinancefor community or individual on-site the Issues Paper which is also institutions have not yet developedinfrastructure purposes are a fairly enclosed. a specialized system for housingnew area in India. Pilot projects Besides the existing problems in and infrastructure loans. Theyinvolving community participation accessing adequate funds, have mostly been administered viaalong with an element of the microfinance institutions also face the same systems that areconsumer's own cash contribution another major difficulty. Due to the applicable to other loan types.(proportion of capital costs and fact that shelter-related and Given the specific characteristics of

3

this loan segment, as well as the The results of such a survey may Phase II: Design of

growing size of the sector, it was be used in designing an Prototype Housing and

deemed useful to develop a appropriate, demand-responsive Infrastructure Loan

prototype housing and loaning system and to develop Department

infrastructure loan department as appropriate loan products with Following an analysis of the

an Action Research component to realistic terms and conditions results of the market survey, a

this study. attached. specialized housing and

Accordingly, a Needs infrastructure loan department

Methodology Assessment Study on the for financing institutions

'Housing Finance Needs of supplying credit to women in

The Action Research initiative Women in the Informal Sector, the urban informal sector

was conducted in two phases: Ahmedabad City' was undertaken was developed.

with the cooperation of SEWA Full documentation of the new

Phase 1: Housing Finance Bank. Full details of the Study system, job responsibilities of the

Needs Assessment Survey along with an analysis of the main related personnel and copies of

Prior to tackling the main findings are elaborated upon in the various forms to be used within

objective of designing a the section entitled 'Action the loaning system are detailed in

specialized system for housing Research: Phase 1'. the following section entitled

and infrastructure loans, a market Microfinance institutions wishing 'Action Research: Phase 11'.

survey to clearly understand the to carry out similar studies in other This model has been developed

housing and infrastructure loan cities may find the methodology along with full documentation so

market that exists among the and format of the survey a useful that it may be pre-tested, refined

target clientele of the micro- guide. and eventually replicated by

financing institution is required. microfinance institutions.

IV~~~~~~~~~~~~~~~~~~~~, | sOf t~~~~~~~~~~P7.t

4

Needs Assessment Study of the Housing and Infrastructure FinanceNeeds of Women in the Informal Sector, Ahmedabad

Introduction Research Team wonien had previously takenhousing, infrastructure or income

This section of the report The research study including generation loans from SEWA Bank,describes Phase I of the Action preparation of the questionnaire for cimounts varying fromResearch: a market survey of the and analysis of data was Rs 5,000 to Rs 10,000. Thirtyhousing and infrastructure coordinated by Smita Ghatate, women sampled were from threefinance needs of poor women in Consultant, SEWA Bank, specific areas of Ahmedabad,the informal sector. The survey Ahmedabad. namely Sanjay Nagar, Sinheshwariwas designed and completed with The field work was undertaken Nagar and Meldi Nagar. All threethe help of SEWA Bank, and coordinated by the field areas are participants of the SlumAhmedabad. workers of SEWA Bank. Networking or Parivartan

The study took four months for Program'. Thirty women residingObjectives completion, ending in March in the same localities as the

1999. Board of Directors of SEWA Bank,* To assess the housing and but yet to open accounts at theinfrastructure finance needs of Use of Pro-tested Bank, were also selected for thepoor women in the informal sector Questionnaire survey.in Ahmedabad city. Issues such as

the specific purpose of taking A structured questionnaire was Findings of the Surveyhousing or infrastructure loans, prepared and pre-tested at thethe desired loan repayment field level. Necessary modifications This section contains relevantperiod and whether the cost of were made before the final survey tables and related analysis,credit is more important or access was undertaken. In addition, summarizing the findings of theto credit is more important to field-level informal interviews survey. The findings are organizedwomen in the informal sector, will with the respondents were also under five main categories:be addressed. carried out. 1. General Information* To provide information to SEWA Annexure 1 contains a 2. Current Housing andBank, on the potential market that reproduction of the questionnaire Infrastructure Statusexists for housing and used for the survey. 3. Housing and Infrastructureinfrastructure loans within Loan Detailsits target and existing loan Sample Base 4. Unmet Housing andclientele. Infrastructure Needs* To specifically examine the In order to get a reasonable 5. The Effect of Housing andeffect of housing and infrastructure sample base, 150 respondents Infrastructure Loans on theloans on the income levels of were interviewed for the needs Productivity of Home-basedhome-based workers. assessment study. Of these, 90 Workers

'The ongoing Ahmedabad Parivartan Program brings basic infrastructure services to the slums of Ahmedabad for on-siteupgradation, in an affordable and sustainable way. The delivery and cost sharing mechanism is through a unique public-private-community partnership. For more details, refer to the publication entitled Ahmedabad Parivartan, UNDP-WorldBank and Sanitation Program - South Asia,1 999.

5

Findings of the Survey

1. General Information

Main Occupation of RespondentsMain Occupation Ne. of Respondents % of Respondents

Vendor2 40 27

Home-based worker3 50 33

Labor and services4 30 20

Housewife5 12 8

Others 18 12

Total 150 100

Distribution of Respondents by IndividualMonthly IncomelndviWdual Menthly Ne. of

In em (Rs) Respondents % of Rpond-nts

0 10 7

<300 5 3

301-600 28 19

601-900 22 15

901-1,100 30 20

1,101-1,300 12 8

1,301-1,500 20 13

1,501-1,700 01 1

1,701-1,900 01 1

>1,901 21 13

Total 150 100

Distribution of Respondents by MonthlyHousehold IncomeMNeatly Huse_bold No. of

Incen (11s) Respond*nts % of Respondents

<500 1 1

501-1,000 6 4 2Vendors include door-to-

1,001-1,500 12 8 door saleswomen as well

1,501-2,000 26 18 as stationary vendors

2,001-2,500 11 7

2,501 -3,000 17 11 (based In marketplace) of

3,001-3,500 20 13 vegetables, fruits, fish, etc.

>3,501 57 38 31ncludes bidi rollers,

Total 150 100 agarbatti makers, crafts

workers, papadrollers, etc.

Distribution of Respondents by Number of Persons 4Includes maidservants,

Living in Household ragpickers, constructionworkers and other

Ne. of Persons Ne. of Respondents % of Respondents daily wagers.

1-2 5 3 520 percent of respondents

3-4 37 25 included non-clients of

5-6 50 33 SEWA Bank. All the

7-8 41 28 housewives interviewed

Total 150 100 belonged to this samplesub-section.

6

Atl

A.~~~~~~~z

Analysis. General are either door-to-door vendors (84 percent) earn Rs 1 ,500 perinformation within designated areas, or month or less. In 88 percent of

stationary vendors based in a cases, the total household incomeOne-third of the women particular marketplace, is between Rs 1 ,500-3,500 per

surveyed are home-based workers Providers of labor and services, month. This suggests that most offor whom their home is also their including domestic servants, daily the women interviewed areworkplace and warehouse. wagers and construction workers, substantial contributors to theirParticularly for these women, make up the third category of total family income, generatingaccess to infrastructure, including occupation amongst the women between 45-1 00 percent of thewater and electricity is very interviewed (20 percent). monthly family earnings throughimportant as they are often Ninety-two percent of the their individual efforts.primary factors of production. women interviewed were engaged The average household size is

Vendors are another common in income generation activities in five to six persons (33 percent ofcategory, comprising 27 percent of the informal sector. Eight percent the families). In relation to theirthe women interviewed. These were housewives. None of those in total monthly household income,women vend a variety of products the housewife category were clients nearly 1 00 percent of theincluding fruits, vegetables, of SEWA Bank. respondents are living below thecooked food products, etc. They The majority of the women poverty line6.

6 According to the Planning Commission of India, the all-India urban poverty line for 1996-97 is defined as those with amonthly per capita income of Rs 353.44 or less. This figure is calculated on the basis of daily calorific requirements alongwith an added percentage for 'other needs' and updated annually in line with inflation. The latest update was undertakenin 1996-97.

7

Findings of the Survey

11. Current Housing Status

Distribution of Respondents by Area Distribution of Respondents by Typein which Current House is Located of Current House Construction

Type of House No. of % of Type of Current Ne. of % of

Respondents Respondents House Construction Respondents Respondents

Society7 13 9 Kuchchall 45 30

Chawl8 76 51 Semi-pucca12 64 43

Chhapura9 35 23 Pucca13 41 27

Others10 26 17 Total 150 100

Total 150 100

Distribution of Respondents byHouse Ownership Details Number of Rooms in Current

Details No. of % of Shelter"Respendents Respondents Ne. of Rooms Ne. of % of

Ownership with clear title 37 25 Respondents Respondents

Informal ownership"4 74 49 1 112 74

Rented house 39 26 2 25 17

Total 1SO 100 3 10 7>4 3 2

Total 1SO 100

Number of Respondents whose Distribution of Respondents byHouses have Special Purpose Spaces Existing Infrastructure Facilities In

(includes covered and uncovered spaces) Current Shelter

Type of Spae- Ne. of % Of Type of Infrastructure Ne. of % of

Respendents Respondent Respondents Respondents

Separate kitchen 54 36 Own bathroom 62 41

Open space 8 5 Own toilet 83 55

Workshed 6 4 Own water connection 107 71

Storage room 5 3 Own sewer connection 122 81

Not applicable 87 58 Internal electricity in home 126 84

7Society: Regular colony containing full, individual infrastructure facilities.8Chawl: Slum containing kuchcha or semi-pucca houses, with limited individual and some collective infrastructure

facilities.9 Chhapura: Slum containing only kuchcha houses with very basic, collective infrastructure facilities.10 Others include staff quarters, mohalla etc.1 Kuchcha: Mud walls and floor with thatch/tiled roof.12Semi-pucca: Mud and brick walls and floor, with asbestos/tiled roof.13Pucca: Bricks and concrete; sometimes with asbestos roof.14Informal ownership refers to settlers squatting on government owned land for 1 0 to 1 5 years (or beyond); they do not

possess any legal land ownership documents.15Covered toilet and covered kitchen are each considered to be separate rooms.

8

i ~ ~ ~ ~ ~ ~ -;I , - 1

Analysis - Current ownership documents, although those residents that are notHousing Status they had been living in the same connected to the main city

house for 10 to 15 years (and sewerage network but have builtThe base-line survey found beyond). Most of the land was their own toilets, the majority have

75 percent of the respondents either government or privately built twin-pit pour-flush latrines.currently living in kuchcha or semi- owned open spaces, on which In terms of infrastructure,pucca one-roomed houses, migrant workers had built their approximately 71 percent havelocated in slums. A total of homes. their own water connection.34 percent of the women surveyed Twenty-six percent of the However, they only have access tohave a separate kitchen. Only women surveyed lived in rented two hours of water flow per day, as9 percent of the respondents accommodations, although all it is released from the Corporationreported that they lived in a wished to have a home of their at designated times. Although'formal' society or a colony. It is own in the future. 81 percent have sewerinteresting to observe that all of Lack of space is a very real connections to their home, onlythese women were residents of problem, as is evident from the 55 percent have built their ownSanjay Nagar or Sinheshwari fact that besides a basic room, toilets. Lack of space, money,Nagar, where the Parivartan 58 percent of the respondents do adequate water for operating aProgram has been completed. not have any other 'special toilet or technical know-how isWith the provision of purpose' spaces, such as a kitchen, responsible for the fact that allcomprehensive infrastructural shed or any open space to work in. those with sewer connections havefacilities, residents now feel that Forty-one percent had their own not been able to construct theirthey are no longer living in a slum, bathroom, while 55 percent own toilets as yet. A significantbut in a regularized 'society'. reported that they had access to proportion of respondents

Only 27 percent of residents their own toilet. Those that had (84 percent) have electricityhave pucca, two- to three-roomed their own sewer connection to the connected to their house, althoughhouses. city mains (majority of slums have the majority of these connections

Half the families surveyed did these), have built pour-flush model are illegal due to lack of landnot possess any clear land (water-borne system) toilets. Of tenure.

-4~ ~

9

Findings of the Survey

Ill. Housing and Infrastructure Loan Details

Distribution of Respondents Aware Source of Awareness about Housingof SEWA Bank's Housing and and Infrastructure Loans AvailableInfrastructure Loans from SEWA BankAware of Housing and No. of % of Sowurce No. of % of

Infrastructure Loans Respondents Respondents Respondents Respondents

Yes 131 87 Employees of SEWA Union 36 24

No 19 13 Employees of SEWA Bank 42 28

Total 150 100 SEWA Bank Board of Directors 30 20

Members of SEWA Union 23 15

Not aware of SEWA Bank loans 19 13

Total 1S0 100

Distribution of Respondents by Distribution of First Loans fromTotal Number of Loans taken from SEWA Bank by PurposeSEWA Bank Purpose of No. of % of

Total Number No. ef % of Loan Respondents Respondents

of Loans Respondents Respondents Housing or infrastructure 60 40

0 31 21 Working capital for own

1 48 32 business 38 25

2 35 23 To buy equipment for own3 134 9 business 13 9

4 7 5 Consumption loan 8 5

> 4 15 10 No loan 31 21

Total 1S0 100 Total 150 100

Comparison of First Loans by AmountRequested and Amount SanctionedLoan Amount Ne. of No. of Loans

Effect of First Loans (Rs) Respondents Sanctioned

on Increased Earnings' Less than 5,000 40 71

Inreased Earnings after Ne. of % Of 5,001-10,000 31 33

Taking Firsf Loan Rwespndent Respondents 15,001-20,000 7 1

Yes 50 33 20,001-25,000 23 10

No 69 46 Morethan 25,001 12 0

No loon 31 21 No loan 31 0

Total 1S0 100 Total 150 119

16 it was difficult to obtain accurate

Sources of Additional Funds to Supplement First answers, as many respondents found

Leon and Rate of Interest Paid' it hard to remember and quantifywhether the first loan they had taken

Sources of Ne. of Monthly Rate of from SEWA Bank, had led to

Additie al Funds Respondents Interest Paid (%) increased earnings for them.

0 1 1.5 2 2.5 3 3.5 4 >4 17Only 30 of 150 respondents sought

Own savings 4 4 additional funds to supplement their

Moneylenders 4 1 2 1 first loan from SEWA Bank; 100

Friends/relatives 19 10 1 2 4 2 f

Others 3 1 1 1 percent of them had taken loans

Total 30 15 1 1 2 5 2 4 for house/infrastructureupgradation/repair.

10

Analysis - Housing scale credit, their experience is C)n the other hand, in line withand Infrastructure that first loans are usually prudential lending norms, SEWALoan Details demanded for consumption or Bank assessed each applicant's

income generation activities. SEWA loan repayment capacity and theThe majority (87 percent) of Bank's increasing track record of majority of first loans sanctioned

women surveyed are aware that facing very high demand for were only up to Rs 10,000. TheSEWA Bank disburses housing and infrastructure and/or housing maximum first loan amount wasinfrastructure loans. The most loans as the first loan, Rs 25,000 - only 8 percent ofcommon sources of information for demonstrates a shift in the women interviewed werecommunity groups about SEWA priorities of poor communities. sanctioned the maximumBank's loans are employees of Access to better housing and available.SEWA and SEWA members infrastructure through own The women surveyed werethemselves. contribution (facilitated by housing asked to provide details of any

There is a well-proportioned and infrastructure-related credit) additional funds taken fromspread among the women is a fast-growing market for external sources to supplementinterviewed, of those who have SEWA Bank. their first loan amount. This servedtaken no loans (21 percent), to Fifty of the women interviewed as a benchmark for SEWA Bank tothose who have taken more than (33 percent) said that they had understand the main sources offour loans from SEWA Bank experienced an increase in funding besides itself, available to(10 percent). Fifty-five percent of earning levels following utilization its members. Only 30 women, thatthe latter are long-term account of their first loan. These 50 women is 25 percent of the women whoholders with SEWA Bank who were all of the home-based had taken a loan from SEWAhave been customers for over workers included in the survey. Bank, had found the amount15 years. The majority of the Thus, this survey conclusively sanctioned inadequate and had towomen interviewed, however, had proves that housing and supplement it from externaltaken either one or two loans from infrastructure is a productive asset sources. Of these, 63 percentSEWA Bank. and that there is a 100 percent reported that relatives or friends

More than half the first loans correlation between increased had provided them with additionaltaken from SEWA Bank by the facilities or better housing and a loans, while 1 3 percent used theirwomen interviewed were for rise in income levels. own savings. Half of the loanshousing or infrastructure More than half the women from relatives or friends wereupgradation purposes. The (60 percent) wanted amounts interest-free, but the other halfaccuracy of this statistic is ranging from Rs 2,000-10,000 for had to pay interest rates ofreinforced by the fact that over their first loan. This reinforces the between 24 to 48 percent per52 percent of SEWA Bank's total belief that there is a substantial annum. Thirteen percent alsoloans are disbursed for housing or demand for small-scale credit (up resorted to borrowing frominfrastructure-related needs. Only to Rs 10,000), as people moneylenders in order to complete7 percent of first loans were for themselves are responsible the job for which the loan wasconsumption purposes, applied for enough to assess their own originally taken. This is significantin times of crisis such as death, repayment capacity limitations. as loans from money lenders carryillness or marriage. The balance Especially amongst the older a range of interest of between43 percent of all first loans were members of SEWA Union included 36-48 percent per annum -taken for income generation or in the survey, a total of 35 percent much higher than the currentasset creation. of the women surveyed demanded market interest rate ranging from

Historically, when microfinance Rs 15,000-25,000 for their 17 percent (SEWA Bank) toinstitutions begin disbursing small- first loan. 20 percent.

11

Findings of the Survey

IV. Unmet Housing and Infrastructure Needs

Interest Rate at which Respondents No. of Respondents who Want Futureare Willing to Borrow Housing or Infrastructure Loans

Annual Interest No. of % of Want Future No. of % of

Rate Respondents Respondents Loan Respondents Respondents

12% 60 40 Yes 138 92

18% 85 56 No 12 8

30% 1 1 Total 150 100

No response 4 3

Total 150 100

Distribution of Respondents byUnmet Needs - Distribution of Future Infrastructure Needs inRespondents by Purpose of Future Current House1 'Housing or Infrastructure Loan" Inrastrdure No.of %of

Purpose No. of % f Needs Respondents Resp-ndents

Respondents Respondents Bathroom 86 57

Repair walls 51 34 Toilet 52 35

Repair roof 24 16 Water connection 29 19

Repair floor 4 1 27 Sewer connection 22 15

Add room 37 25 Electricity connection 24 16

Build terrace 44 29

Add bathroom 52 35

Add toilet 30 20

Water connection 06 4 Analysis - Unmet/Future Housing andSewer connection 05 3

Connection for home electricity 03 2 Infrastructure NeedsBuild/buy new house 25 17

The unmet needs for housing and infrastructure

finance among the women interviewed were assessed

by asking respondents whether they wanted housing

and/or infrastructure-related loans from SEWA Bank

Distributon of Respondenht by Lon in the near future. If so, they were asked the specific

Amount Require to Meet FutureHSousing and Infrastructure Nets purpose of the loan and acceptable interest rates that

Loan Amount Mo. of % Of they would be willing to pay for credit.

(Rs) Respondents Respondents An overwhelming 92 percent of the women stated

0-5,000 12 8 that they had demand for future housing or

5,001-10,000 5 3 infrastructure-related loans. Nearly all of them10,001-15,000 3 2

15,001-20,000 11 7 (96 percent) expressed a willingness to pay interest

20,001-25,000 22 1 5 rates of between 12-18 percent per year which is a>25,000 97 65 rtso ewe 21 ecn e erwihi Tetel 150 100 realistic demand in line with market rates of interest.

This confirms that the poor are not demanding highly

subsidized credit, a common misconception. The

women surveyed reported that they were fully aware

18Multiple responses arising from multiple unmet needs. that it was unsustainable for an institution like SEWA

'Multiple responses arising from multiple future needs. Bank to provide loans at cheaper than market rates.

12

They also gave a higher priority to women by designing specific water majority of women (87 percent)access to timely and efficient credit supply and sanitation loan reported higher amounts rangingrather than focusing on the products. In addition, a technical from Rs 1 5,000 to overabsolute cost of credit, as long as agency such as Mahila Housing Rs 25,000. A substantial 65the cost was reasonable. SEWA Trust would have to play the percent of the women stated they

Most agreed that in comparison intermediary role of engaging the needed over Rs 25,000 in loans toto other sources of credit (mainly municipality to facilitate the water satisfy their unmet housing andmoneylenders), the interest rate supply and sanitation provision, infrastructure-related needs. Ofcharged by SEWA Bank was fair upon payment by the consumer. course, they did not wish to accessand reasonable. When asked the amount of one loan for such a large amount,

The specific unmet housing and credit they required in order to but several smaller loans in future,infrastructure needs of the women meet future housing or to meet their composite shelter-interviewed covered a wide range, infrastructure-related needs, the related needs.including various aspects of houserepair - walls, roof, floor . o(50 percent) and house additions Findings of the Surveyconsisting of room and terrace(54 percent). Infrastructure V. The Effect of Housing and Infrastructure Loansupgradation loans - including the on the Productivity of Home-based Workersaddition of a toilet, bathroom,water, electricity and sewer Number of Respondents who Useconnections - were demanded by their Home as a Workplcea substantial number of use their Hemo Ne. of % ofrespondents. This again highlights as Werkplace REspeode.ns Respondentsrespondents. ~~~~~~~~Yes 50 33the significant level of demand for No 100 67infrastructure-related loans, which Tetal 150 100is a relatively new phenomenon.Only 25 of the women surveyed Distrlbution of Part of Home Usdreported that they wished to take as Workplaceloans in the future from SEWA

Part of Hoe - Ne. e4 % ofBank to buy or build a new house. REepende RepsndetsWhen specifically questioned Room 30 60

about their future infrastructure Kitchen 7 14Open space near house 8 16needs, a majority of the women Workshed 2 4

expressed a need for water- and Storage room 1 2expressed a need forwater- and Others 2 4sanitation-related services Total 50 100including building a bathroom,toilet, water and sewerconnections. Only 16 percent Distribution of Home-basereported that their main need was Workers that have Tken aro eportedr own electricity Housing or Infrastructure Loanto get their own electricity from SEWA Bankconnection. This also serves to

Tuken Hewsing si Ne.e.% ehighlight that the water supply and Infrastructure Leon Rspendents Respondentssanitation sector is highest in Yes 31 62people's priorities. As such, SEWA TNotal 50 13080Bank could significantly help these

13

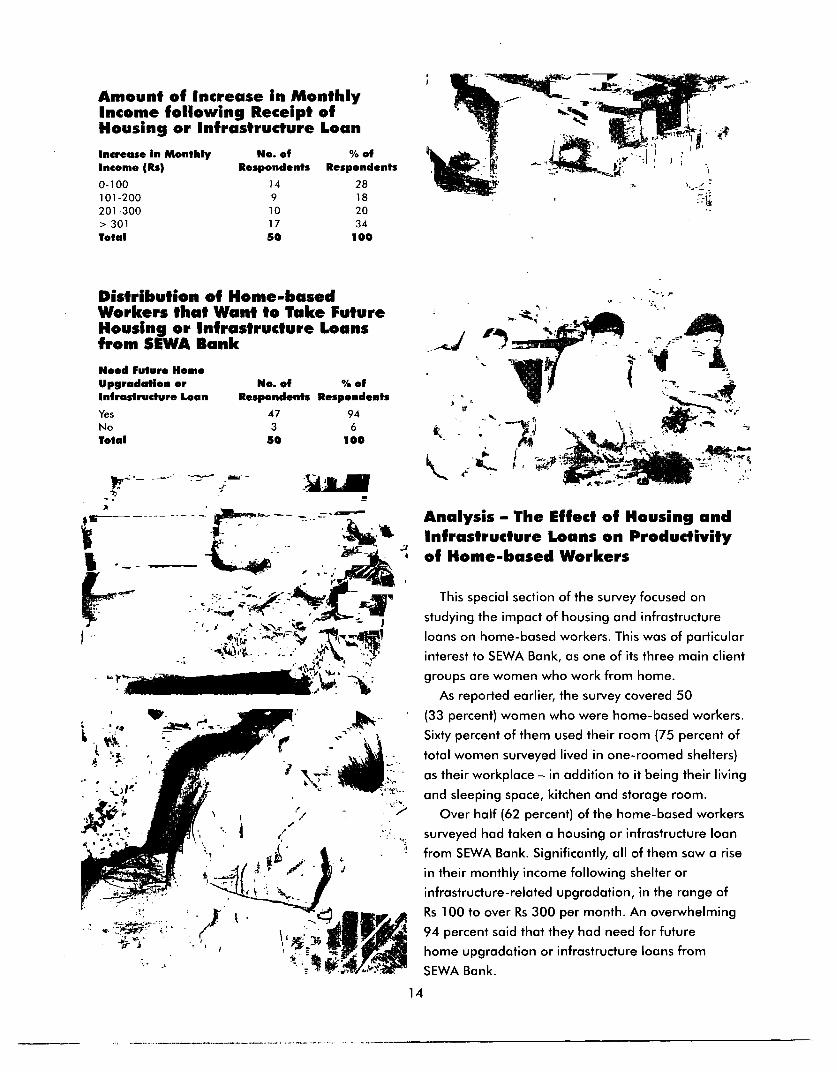

Amount of Increase in MonthlyIncome following Receipt ofHousing or Infrastructure Loan

Increase in Monthly Ne. of % ofIncome (Rs) Respondents Respondents

0-100 14 28 -

101-200 9 18

201-300 10 20

> 301 17 34

Total S0 100

Distribution of Home-basedWorkers that Want to Take Future

from SEWA Bank F

Need Future Home wUpgre dagton or No. of °/ of ll ',E

Infrastructure Loan Respondents Respondents

Yes 47 94 INo 3 6 - '

Total SO 100

--- #-^ ~ - Analysis - The Effect of Housing and| t Infrastructure Loans on Productivity

VA _ { ~~ =-z- *of Home-based Workers

> - --~ Z ~r, This special section of the survey focused on

studying the impact of housing and infrastructure

loans on home-based workers. This was of particular

52 6 tt\ 5 interest to SEWA Bank, as one of its three main client

groups are women who work from home.

As reported earlier, the survey covered 50

(33 percent) women who were home-based workers.

Sixty percent of them used their room (75 percent of

/ ' f . ' w * total women surveyed lived in one-roomed shelters)

as their workplace - in addition to it being their living

'. j'r'and sleeping space, kitchen and storage room.

,* _ " tX ~ - Over half (62 percent) of the home-based workers

,_- surveyed had taken a housing or infrastructure loan

from SEWA Bank. Significantly, all of them saw a rise

in their monthly income following shelter or

infrastructure-related upgradation, in the range of

Rs 1 00 to over Rs 300 per month. An overwhelming

i5- ; Wr, 2 ' ' g i L )94 percent said that they had need for futurehome upgradation or infrastructure loans from

SEWA Bank.

14

This section of the report water or electricity connection or important requirement within thedescribes Phase 11 of the Action building a toilet and an overall system. This also meantResearch, which involved the additional room out of the same that limiting debt:income ratiodesign of a prototype housing and loan, it would be more efficient to forrnulae need not be imposed ininfrastructure loan department. merge housing and infrastructure order to determine the extent ofThe model is applicable to loans. It was established that in loan that may be sanctioned.financial institutions that wish to the perception of the target Instead loan amount decisionsmeet the housing and clientele, the differences between would be taken to suit individualinfrastructure-related credit needs loans for on-site infrastructure loan repayment capacities, basedof poor women in the urban, versus loans for housing on individual circumstances.informal sector. The prototype is upgradation, were not very In addition to a specializedbased on the premise that clear - so to separate these loan housing and infrastructure loansindividual loans are disbursed on types was deemed unnecessary department, two complementarythe basis of a combination of and impractical. activities are also recommended:completed individual application 0 The importance of the position * Development of a centralizedforms and field visits to each of the field worker within the loan building supplies raw materialpotential loanee's home to assess system, especially in order to outlet, so that loanees have easyher genuine need for the loan and ensure high repayment rates, was access to materials at aher loan repayment capacity. identified as a key role. This is reasonable cost. Instead of cash

Following the results of Phase 1, especially true for organizations payments, appropriate loantwo important decisions were disbursing individual loans, that do utilization may be promoted by themade regarding the proposed new not rely on social or peer pressure issuance of 'materials vouchers,'system: through group formation, to which can be redeemed by clients* It was decided that since most ensure high loan repayment. The at the materials centre.housing upgradation loans to the close interaction between the field 0 Technical assistance in housinginformal sector poor are used for a worker and loan clients, through design, low-cost technologies,variety of integrated purposes, pre-loan sanction and post-loan cost estimation, buildingoften including an infrastructure utilization site visits to the client's supervision etc.component such as getting a home was identified as an

1 sAil |1 uui i.x ae

15

Proposed Loan Process Map - External(for Clients)

Proposed Loan Process Map - External (for Clients)

Complete HI Loan20 Eligible to apply for loan, if

Application Form member has regularly saved

with the organization for at least

one year

Ar 5 days

Pre-loan sanction field visit by

field worker, to applicant's home

5 days

Weekly loan sanction notice put up

on common notice board -

with details of all loan applications

sanctioned during the previous week

r 2 days

Applicant signs loan contract with

two guarantors; opens loan

account; withdraws the loan in

cash from her savings account

)r Within 3 months

Post-loan assistance

field visit by field worker

to check prope r loan utilization

Up to 5 years ngin-la

repayment

20HI Loan: Housing and/or infrastructure loan.

1 6

Proposed Loan Process Map - Internal(for Housing and Infrastructure Department Personnel)

HI Loan Coordinator meets each HI Loan Coordinator postsapplicant personally and helps details of sanctioned loans on

her complete the Loan the organization's notice board;Application Form assists applicant to complete

loan contractand related formalities

Completed Loan Application Forms _ Nare sorted daily, on area basis and HI Loan Coordinator issues

distributed to field workers for 'loan sanction voucher'pre-sanction field visit in applicant's name and

I . . opens a loan account for her

Field worker visits applicant'shome and completes

Pre-Loan Sanction Form Applicant collects loan amount incash from her savings account (less

t f savings lien/administrative charges)

HI Loan Coordinatorreceives completed Pre-Loan

Sanction Forms from field worker;applies her judgement and * HI Loan Coordinator is

completes the Loan responsible for timelyEvaluation Form, stating amount of loan recovery in conjunction

loan to be sanctioned, if any with field workers

HlLan Supervisor reviews allcompleted forms and sanctions or

denies loan; Managing Directordouble checks and accepts or

denies loan

17

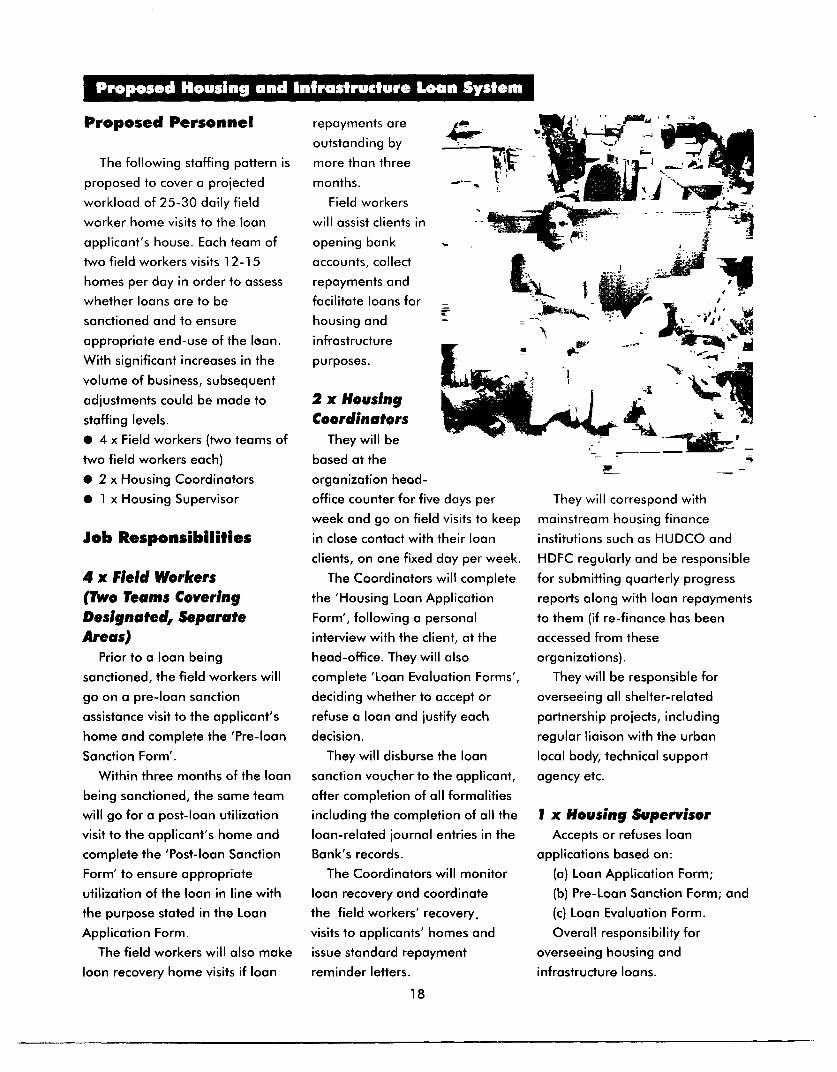

Proposed Personnel repayments are

outstanding by

The following staffing pattern is more than three

proposed to cover a projected months. I '1workload of 25-30 daily field Field workers

worker home visits to the loan will assist clients in

applicant's house. Each team of opening bank e

two field workers visits 12-15 accounts, collect

homes per day in order to assess repayments and v iwhether loans are to be facilitate loans for 1 - -

sanctioned and to ensure housing and =

appropriate end-use of the loan. infrastructure

With significant increases in the purposes.

volume of business, subsequent d

adjustments could be made to 2 x Housing |

staffing levels. Coordinators

*4 x Field workers (two teams of They willI be -

two field workers each) based at the

* 2 x Housing Coordinators organization head-

* 1 x Housing Supervisor office counter for five days per They will correspond with

week and go on field visits to keep mainstream housing finance

Job Responsibilities in close contact with their loan institutions such as HUDCO and

clients, on one fixed day per week. HDFC regularly and be responsible

4 x Field Workers The Coordinators will complete for submitting quarterly progress

(Two Teams Covering the 'Housing Loan Application reports along with loan repayments

Designated, Separate Form', following a personal to them (if re-finance has been

Areas) interview with the client, at the accessed from these

Prior to a loan being head-office. They will also organizations).

sanctioned, the field workers will complete 'Loan Evaluation Forms', They will be responsible for

go on a pre-loan sanction deciding whether to accept or overseeing all shelter-related

assistance visit to the applicant's refuse a loan and justify each partnership projects, including

home and complete the 'Pre-loan decision. regular liaison with the urban

Sanction Form'. They will disburse the loan local body, technical support

Within three months of the loan sanction voucher to the applicant, agency etc.

being sanctioned, the same team after completion of all formalities

will go for a post-loan utilization including the completion of all the 1 x Housing Supervisor

visit to the applicant's home and loan-related journal entries in the Accepts or refuses loan

complete the 'Post-loan Sanction Bank's records. applications based on:

Form' to ensure appropriate The Coordinators will monitor (a) Loan Application Form;

utilization of the loan in line with loan recovery and coordinate (b) Pre-Loan Sanction Form; and

the purpose stated in the Loan the field workers' recovery, (c) Loan Evaluation Form.

Application Form. visits to applicants' homes and Overall responsibility for

The field workers will also make issue standard repayment overseeing housing and

loon recovery home visits if loan reminder letters. infrastructure loans.

18

Proposed Housingand InfrastructureLoan System l

Pre-loan Sanction* Completion of Loan ApplicationForm by Housing Coordinator,

following personal interview withthe applicant.

* Completed Application Formssorted by area on a daily basis and *handed over to the field workersfor home visit.

* Field workers complete Pre-loan : Sanction Form following theirvisit to the applicant's home, and isubmit it to the HousingCoordinator. 0 Housing Coordinator opens a generates housing loan progress

loan account for the applicant and reports every month and passesLoan Approval/Refusal posts the necessary journal entries these repayment reports to the* Housing Coordinator completes including the insurance premium; Housing Coordinator.the Loan Evaluation Form, based she updates the loan account 0 Standard letters requestingon an interview with loanee and every quarter. payment of installments that areother documentation. * Loanee collects her loan in cash due are issued for loans that are* Housing Supervisor receives from the cashier. one to three months overdue.copies of applicant's file * Repayments that are more thancontaining all completed forms Post-loan Utilization three months overdue are notifiedand sanctions or refuses loan. * Housing Coordinator gives a list to the area field worker for a* Managing Director double of daily loans disbursed to field home visit in order to investigatechecks and sanctions or refuses workers. the cause behind the delayedloan. * Field workers visit the applicant repayments; the field workers and* Housing Coordinator posts at her home and complete a Post- Housing Coordinators jointlysanctioned applicant's names on loan Sanction Form detailing loan monitor repayments closely.the organization's public notice utilization, within one month of Annexures 2-5 contain copies ofboard. loan receipt. the various forms designed for

* Housing Coordinator checks use by the prototype Housing andLoan Disbursement whether all the loans have been Infrastructure Loan Department.* Applicants come to Housing used for the purpose stated on the Annexure 6 contains theCoordinator along with two Application Form and accordingly proposed 'Rules and Regulations'guarantors to sign the loan posts a quarterly interest rebate of regarding housing andcontract, and are given a copy of 4 percent. If not, she imposes the infrastructure loans. A copy ofthe 'Housing Loan Rules and necessary penalties (see these regulations should beRegulations'. Annexure 6). provided to all loan clients and* Housing Coordinator issues a explained to them by the Housingloan sanction voucher with the Loan Recovery Loan Coordinator at the time ofloan amount clearly written on it. * The loan recovery department loan application.

19

Structured Questionnaire Used for 'Housing andInfrastructure Finance Needs Assessment Survey'(Ahmedabad City) - Market Research

General Information How many rooms are there In the current

shelter?

Name:

Main occupation: Do you have any of the following:

Vendor (i) Toilet

Home-based worker (specify) (ii) Separate kitchen

(iii) Kitchen garden

Crafts worker L (iv) Workshed

Bidi roller L (v) Storage room LI

Construction worker l

Others (specify) LI Do you use your home as a workplace? If so, how

and which part of your home?

Supplementary occupation:Vendor O

Home-based worker (specify) LDo you or anyone in your family own the house in

Crafts worker L which you are presently living?

Bidi roller L Yes

Construction worker LI No

Others (specify) 1

If not, what rent do you pay and what collateral

Current income (Rs per month): did you give?

* Of the woman

* Of the family

Size of the household: If you are occupying common land, have you ever

Adult: M F faced threats of eviction?

Children: M F

Type of the current shelter: Do you plan to buy a plot of land for housing?

a. (i) Society L Yes L

(ii) Chawl LI No L

(iii) Chhapura L]

(iv) Footpath m If yes, when?

(v) Others (specify) Z

b. (i) Kuchha l Do you plan to buy or build your own house?

(ii) Semi-pucca I Yes L

(iii) Pucca LI No L

20

How much savings do you have with SEWA Bank (if Repayment status:any)? Fully paid up

Currently repaying

DefaultHow long have you been saving with SEWA Bank?

(i) Less than one year N How did you know about the loans available from(ii) One year W SEWA Bank?(iii) Two years [](iv) More than two years

Do you know that SEWA Bank also gives loans forhousing and infrastructure?

Loan Details

Year and month that current loan was made Do you want a housing or Infrastructure loan?available from SEWA Bank, if any: * If so, why?

* For how much?Purpose:

* If not, why not?

Amount required: Did anybody from SEWA Bank visit your housebefore sanctioning your first loan?

Amount sanctioned:

Did you face any difficulties in getting the loan?

Total amount spent on this episode:

Did you need any guarantors for the loan? Wasthis a problem?

Has this loan increased your earnings In any way?If so, by how much per month?

Housing History

Source, amount and rate of interest charged, on Where did you live before this house?excess amount spent (besides loan):

Amount Rate of

(Rs) Interest (%) Have you ever borrowed for housing orSelf infrastructure from any source?Moneylender

Friends and relatives C

Others Is getting access to credit more important, or thecost of credit more Important to you?

How long did it take to get the loan from SEWABank, after applying for it?

21

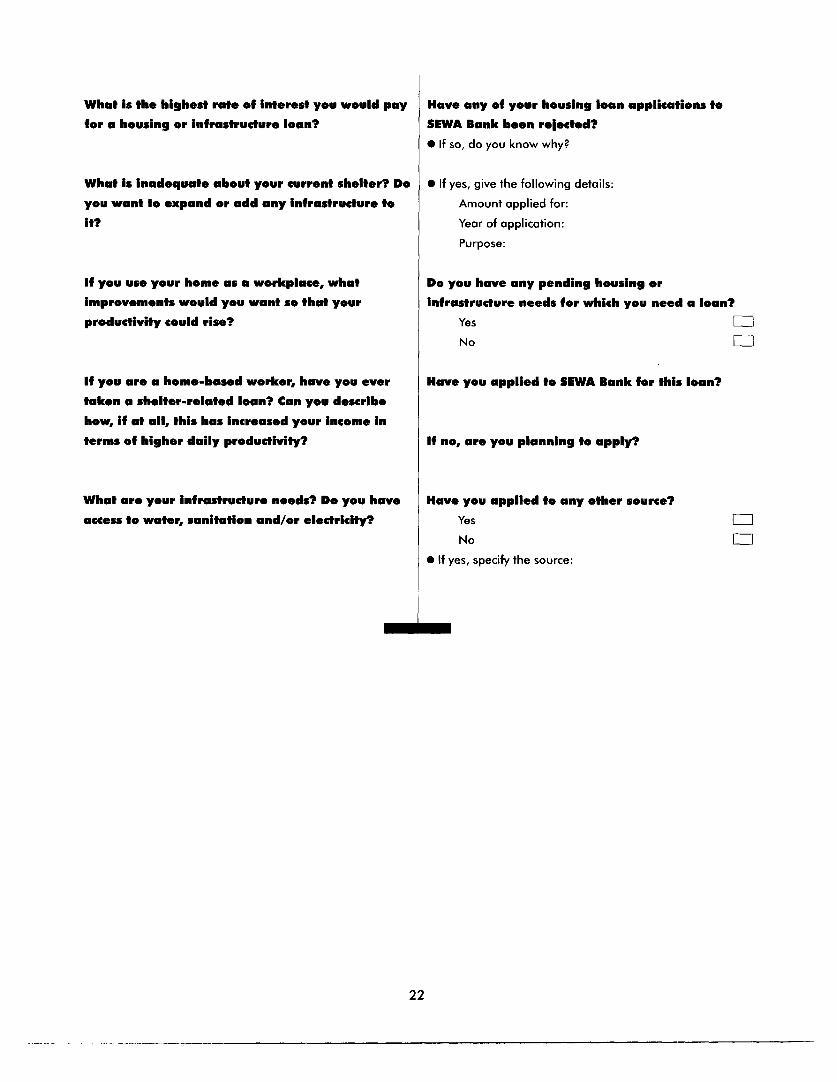

What is the highest rate of interest you would pay Have any of your housing loan applications to

for a housing or infrastructure loan? SEWA Bank been rejected?

e If so, do you know why?

What is inadequate about your current shelter? Do If yes, give the following details:

you want to expand or add any infrastructure to Amount applied for:

It? Year of application:

Purpose:

If you use your home as a workplace, what Do you have any pending housing or

improvements would you want so that your infrastructure needs for which you need a loan?

productivity could rise? Yes

No

If you are a home-based worker, have you ever Have you applied to SEWA Bank for this loan?

taken a shelter-related loan? Can you describe

how, if at all, this has increased your income in

terms of higher daily productivity? If no, are you planning to apply?

What are your infrastructure needs? Do you have Have you applied to any other source?

access to water, sanitation and/or electricity? YesNo

_ If yes, specify the source:

22

Housing and Infrastructure Loan Application Form(To be completed by loan applicant)

Personal Information Are the assets rented? If so, what is the monthlyrental amount?

Name:

House Details

Addross: Type of house:Kuchha [Pucca m

Age: Semi-pucca

Marital status: Ownership/Legal tenureMarried Own houseSingle Other's name (specify)Widowed RentedSeparated E If rented, what is the monthly rental?

If there is no ownership document, onEducational qualifications: whose land is the house located?

* Savings Account No: How many rooms:* Total Savings: Rs One

TwoFamily Details Three I

More than three [Total number of family members:

Loanee Total area of house:Spouse 100 sq ft Children 100-200 sq ft Other family members 150-200 sq ft LiTotal members 201-300 sq ft -

More than 300 sq ft Occupation Details

Purpose of LoanOwn occupation and monthly income:

PurposeHusband's occupation and monthly income: * House repair

* House extensionTotal family monthly income: * Infrastructure (specify)

* New houseDo you own any of the assets/machinery used in * Others (specify)your/your spouse's occupation?

23

Total cost estimate Do you have any outstanding debts? If so, how much

do you repay per month and what is the total amount

Loan amount requested due?

Monthly repayment capacity Do you own any other assets? Please describe.

Loan History Information I hereby declare that I have carefully read all the

terms and conditions cited above and they are

Type of loan acceptable to me.

* Secured

* Unsecured

Loan amount Signature of Signature of Date

Date of receipt and source of loan Loanee Loan Coordinator

Date of full loan repayment

24

Pre-loan Sanction Form(To be completed by housing loan field worker at the time of first site visit)

Name: House type - windows:Wooden

Address: Metal/ironNo window

Type of current house: Purpose of loan (specify):Society Current housing and infrastructure need:Chow/ Total estimated cost:Chhapura Loan amount requested:Footpath

Others (specify) W If cost estimate has been undertaken,by whom:

House type - walls: SelfBricks and cement RelativeBricks and mud [ MasonThatching/wood walls Technical agencyKuchcha with cement plastering OthersKuchcho (mud)

Others W Does the applicant want technical help with building/repairing the house/adding infrastructure? If so,

House type - flooring: exactly what help?Tiles CIlStone W Does the applicant have a current loan outstandingCement and plaster W with the savings and credit organization/any otherMud W debtor? If so, how much is due?Others

In your opinion, should the loan be sanctioned?House type - roofing: If yes, for what amount ?

Cement/pucca W If not, why not?Iron

Asbestos W Any other remarks.Wood

Tent

Plastic sheetNone C Field worker's Signature:Others

Date of Home Visit:

25

Loan Evaluation Form(To be completed by the Housing and Infrastructure Loan Coordinator)

Name of loan applicant: Should the loan be sanctioned?

Does the applicant have regular savings with If no, why not ?

the savings and credit organization? Current

balance in Savings Account:Amount of loan to be sanctioned:

Amount of loan requested:What lien should be retained on the loan ?.

(Usually 20 percent of loan amount; if other amount,

Does the applicant have any current loans please explain why)

outstanding with the organization?

Any other remarks?

If so, is the loan application to be relected?

Loan Amount Sanctioned

Approval of Housing Coordinator Signature Date

Approval of Housing Supervisor Signature Date

Approval of Managing Director Signature Date

26

Post-loan Sanction Form(To be completed within three months of loan receipt by housing loanfield worker)

Name: Describe the physical effect of the housing orinfrastructure loan on the loanee's house orservices available:

Address: Before

After

Date of receipt of loan from the savings and If the loane Is a home-based worker, hascredit organization: the housing loan helped to increase her

monthly income? If so, by how many rupeesper month?

Loan amount received:

Check loanee's pass book for loan repaymentsStated purpose of loan at time of application: Are repayments on time?

If not, why not?

How many repayments are outstanding?Check receipts for materials and labor, if How does the loanee plan to repay the loan andany? clear her outstandings?

Check: Yes No

Any other comments:In your opinion, has the loan been utilized asper the purpose stated to the organization?

Field worker's signature: Date:

27

Suggested Rules and Regulations for Housing andInfrastructure Finance Loans(Maximum loan amounts, repayment terms, penalties, etc may be adapted byspecific financing organizations)

1. Loans may be for any amount between Rs 1,000 on a quarterly basis.

and Rs 25,000.7. If a loan is used for any purpose other than (2)

2. Loans from the housing and infrastructure loans above, the entire loan will attract a higher interest

department must be used for the stated purpose only, rate of 1 7 percent. In addition, a cash penalty will be

including: charged (for example, between Rs 500 to Rs 1,000).

House repair/maintenance

House expansion, e.g. addition of rooms 8. The organization will hold a lien (usually 20

Addition of infrastructure, e.g. electricity/water/ percent) over the savings account of each loanee with

toilet/drainage an outstanding housing loan. When the loan is fully

To build a new house/buy a plot repaid after five years, the savings account will

become operational again and the credited interest

3. All loans are repayable in five years. rebate may be withdrawn, in a lump sum.

4. An applicant is only eligible for a housing loan, if 9. House insurance will be mandatory for all housing

she has been saving REGULARLY with the loan beneficiaries. The organization will directly

organization for one year or more. withdraw the insurance premium from the client's

savings account.

5. Only one loan per account holder is allowed at

one time. This includes related accounts held by 10. Each applicant taking a first-time loan from the

children or relatives of the account holder. organization will be required to buy 5 percent of the

loan amount in the form of shares in the

6. The interest rate charged on housing loans will organization. In addition, a transaction fee of Rs 40

be the same as that charged on all other loan (loans < Rs 5,000) or Rs 60 (loans > Rs 5,000) will be

types - currently 1 7 percent per annum. However, charged, along with a nominator fee of Rs 5 per

housing loans will get a rebate of 4 percent per guarantor. These charges will be directly debited from

annum, credited to the loanee's savings account the loan amount.

28

I

F ;v.. JJ;jA !t- ; -,~~~~~Nuu 0

a -- - t 7 r t ' -<~~IL-"V

*_________ L.

aw iK;i\'l.. ,

For more information, please contact:

UNDP-World Bank Water and SanitationProgram - South Asia

55 Lodi Estate, New Delhi 11 0 003, India

Tel: (91)-(0)11-4690488/9 Fax: (91)-(0)11-4628250E-mail: [email protected]

Gujarat Mahila Housing SEWA Trust

404, 4th Floor, Sakhar-IV, Opposite Town Hall, Ashram Road,

Ahmedabad - 380 009, IndiaTel: (91)-(0)79-6581659 Fax: (91)-(0)79-5506446

E-mail: [email protected]

Designed by Media Workshop and printed at PS Press Services Pvt Ltd, Ema I gdapressObol net. in

Related Documents