Rural Financial Services in Kenya What is working and Why? -Betty Kibaara- International Conference on Rural Finance Research Moving Results into Policy and Practice FAO Headquarters Rome, Italy 19-21 March, 2007 Egerton University-Kenya Theme: Improvement in operational Management of Rural Finance Institutions

Rural Financial Services in Kenya What is working and Why? -Betty Kibaara- International Conference on Rural Finance Research Moving Results into Policy.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Rural Financial Services in KenyaWhat is working and Why?

-Betty Kibaara-

International Conference on Rural Finance ResearchMoving Results into Policy and Practice

FAO HeadquartersRome, Italy

19-21 March, 2007

Egerton University-Kenya

Theme: Improvement in operational Management of Rural Finance Institutions

2

Rural Financial Services in Kenya Formal organized commercial banks concentrated in the urban areas- in

1990’s most multinational banks closed rural branches

An array of informal financial systems created to fill the vacuum

Only 20% of the population have access to bank accounts in the rural areas.

Rural finance has been recognized and fast tracked under the Strategy for Revitalizing Agriculture

It is against this background that we conducted a research on selected rural finance models

3

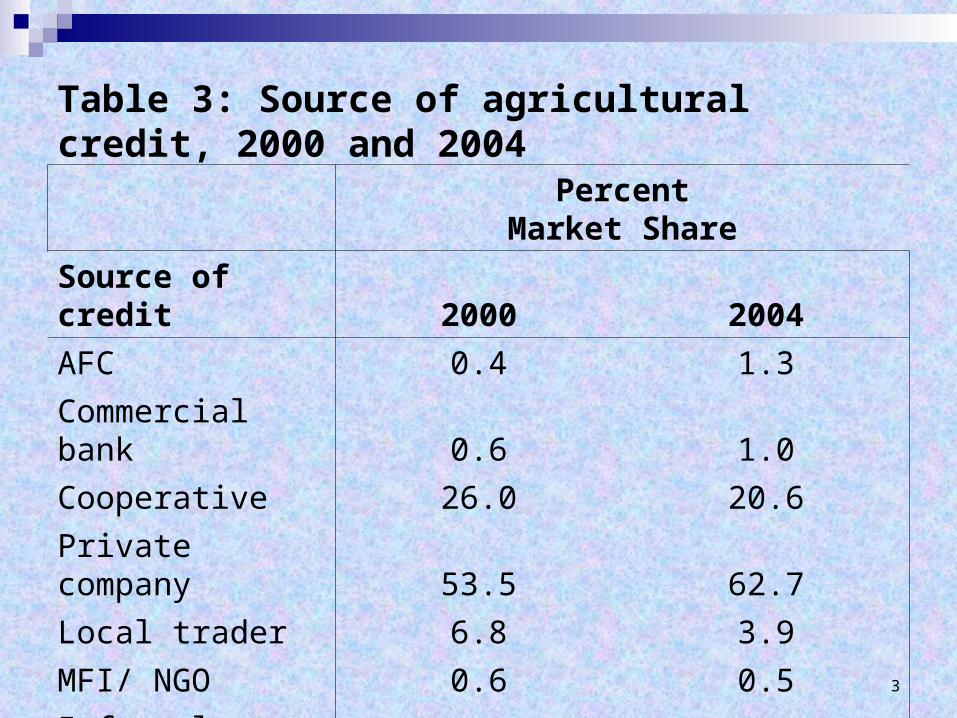

Table 3: Source of agricultural credit, 2000 and 2004

PercentMarket Share

Source of credit 2000 2004

AFC 0.4 1.3

Commercial bank 0.6 1.0

Cooperative 26.0 20.6

Private company 53.5 62.7

Local trader 6.8 3.9

MFI/ NGO 0.6 0.5

Informal money lender 12.1 9.9

100.0 100.0

4

Presentation Outline State Owned/Government Model Community Owned Model

Village Banks Mbeu Savings Association ‘Bank under a tree’

Donor Credit Guarantee Agricultural Input Stockists Credit Input Supply Voucher System

Emerging Indigenous Banking Model Beach Banking

Objective understand the operations, constraints, opportunities and possibility of replication

5

State Owned/Government Led Model: - Agricultural Finance Corporation-

Semi-government organization- budgetary allocation

Targets large scale farmers

Collapsed in the 1990’s and revamped in 2003

Offers, seasonal, developmental loans, value addition loans, and short term loans to agricultural input stockists

Challenge:-Loan Recovery, inefficiencies and financial sustainabilityOpportunity to diversify from retail to Groups/Wholesale lending

6

Donor Credit Guarantee Model -Agricultural Input Stockist-

Model involves the Donor, an NGO, an input stockists and input Manufacturer.

Strengthen the creditworthiness of the agricultural input stockists who lack capital.

NGO trains the stockists and link them up with manufacturers/distributors of inputs-get inputs on credit

Donor guarantees to pay 50% of defaulted credit

Challenge: limited guarantee -$40,000

Scaling up: The model has attracted the Agricultural Finance Corporation Now lending short term credit ( Ksh. 150,000 to Ksh.500,000)

7

Donor Guarantee -Credit Input Supply Voucher System-

Provision of agricultural inputs using vouchers reduce diversion- in Ahero Rice Irrigation Scheme

Involves a donor guarantor, an MFI, Savings and Credit Co-operatives (SACCO), Input stockists, Government and the private sector

In 2005, disbursed Ksh. 6.7 million 600 farmers

Challenge: cohesiveness of all actors in the value chainOpportunity exist for scaling up to other irrigation schemeReplication: Already replicated in Bunyala Rice Irrigation Scheme

8

Emerging Indigenous Banking Model -Equity Bank-

Bank owned by locals

Principal- take banking services closer to the people after the multinational banks pulled away from the rural areas- FIXED and MOBILE BANKS

Rural clients account for 68% of clients

Low transaction charges –No ledger fee, take digital photo.

Total clients -1 million ( over 20% of all the total deposit accounts in Kenya)

Borrowing clients, 21%

Challenges : Infrastructure, insecurity

Replication: a number of banks have have set up rural branches e.g. Family Finance, Barclays bank and Kenya Commercial banks

9

Community Owned Model Financial Service Association ‘Village Banks’

Owned by the local community- membership through shares Low densely populated areas Managed by management companies- Krep Development

Agency at a fee Donor assistance with a clear exit strategy- Institutionalization

and capacity building 70 village banks, 70,000 savers, Ksh. 82 million shareholding Proportion of client obtaining loan, 38%

10

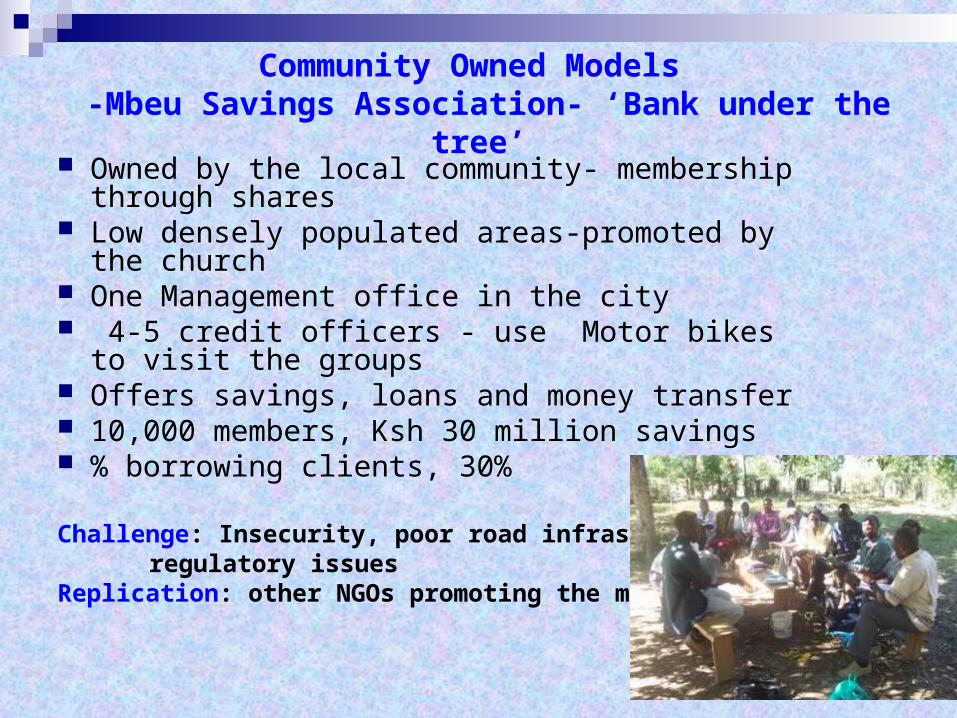

Community Owned Models -Mbeu Savings Association- ‘Bank under the tree’

Owned by the local community- membership through shares

Low densely populated areas-promoted by the church One Management office in the city 4-5 credit officers - use Motor bikes to visit the

groups Offers savings, loans and money transfer 10,000 members, Ksh 30 million savings % borrowing clients, 30%

Challenge: Insecurity, poor road infrastructure, regulatory issues

Replication: other NGOs promoting the model

11

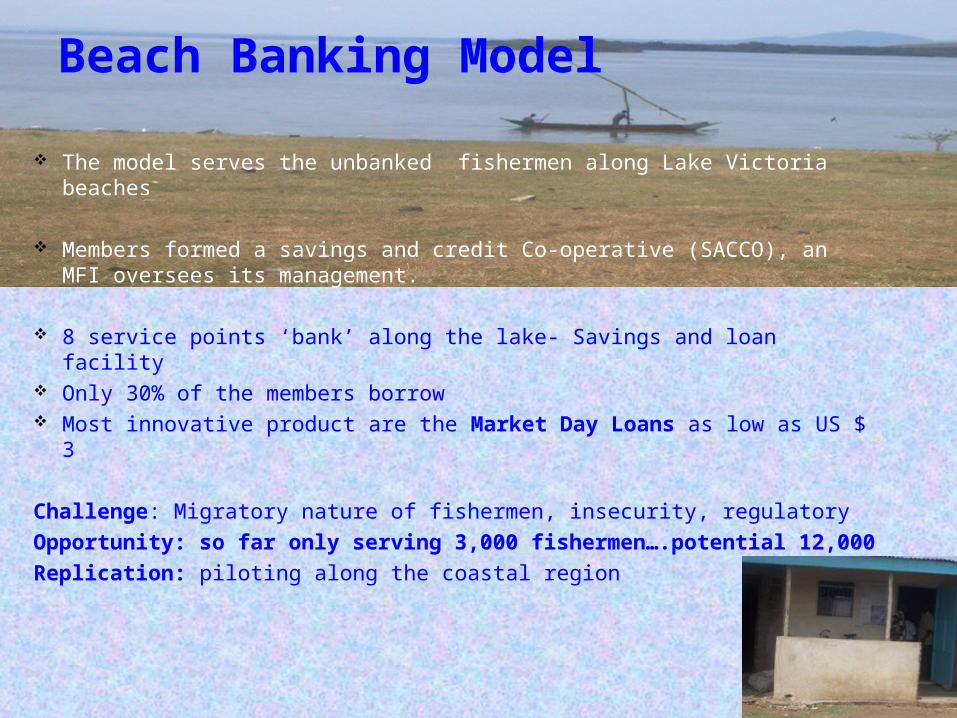

Beach Banking Model

The model serves the unbanked fishermen along Lake Victoria beaches

Members formed a savings and credit Co-operative (SACCO), an MFI oversees its management.

8 service points ‘bank’ along the lake- Savings and loan facility Only 30% of the members borrow Most innovative product are the Market Day Loans as low as US $ 3

Challenge: Migratory nature of fishermen, insecurity, regulatory

Opportunity: so far only serving 3,000 fishermen….potential 12,000

Replication: piloting along the coastal region

12

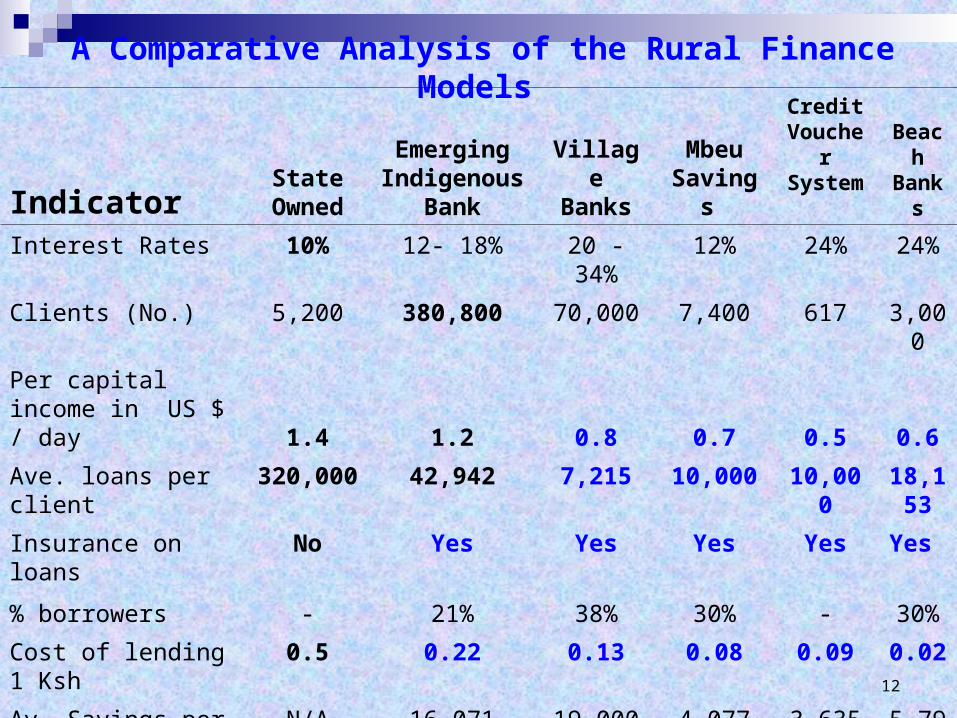

A Comparative Analysis of the Rural Finance Models

IndicatorState

Owned

Emerging Indigenous

BankVillage Banks

Mbeu Savings

Credit Voucher System

Beach Banks

Interest Rates 10% 12- 18% 20 - 34% 12% 24% 24%

Clients (No.) 5,200 380,800 70,000 7,400 617 3,000

Per capital income in US $ / day 1.4 1.2 0.8 0.7 0.5 0.6

Ave. loans per client 320,000 42,942 7,215 10,000 10,000 18,153

Insurance on loans No Yes Yes Yes Yes Yes

% borrowers - 21% 38% 30% - 30%

Cost of lending 1 Ksh 0.5 0.22 0.13 0.08 0.09 0.02

Av. Savings per client N/A 16,071 19,000 4,077 3,635 5,797

13

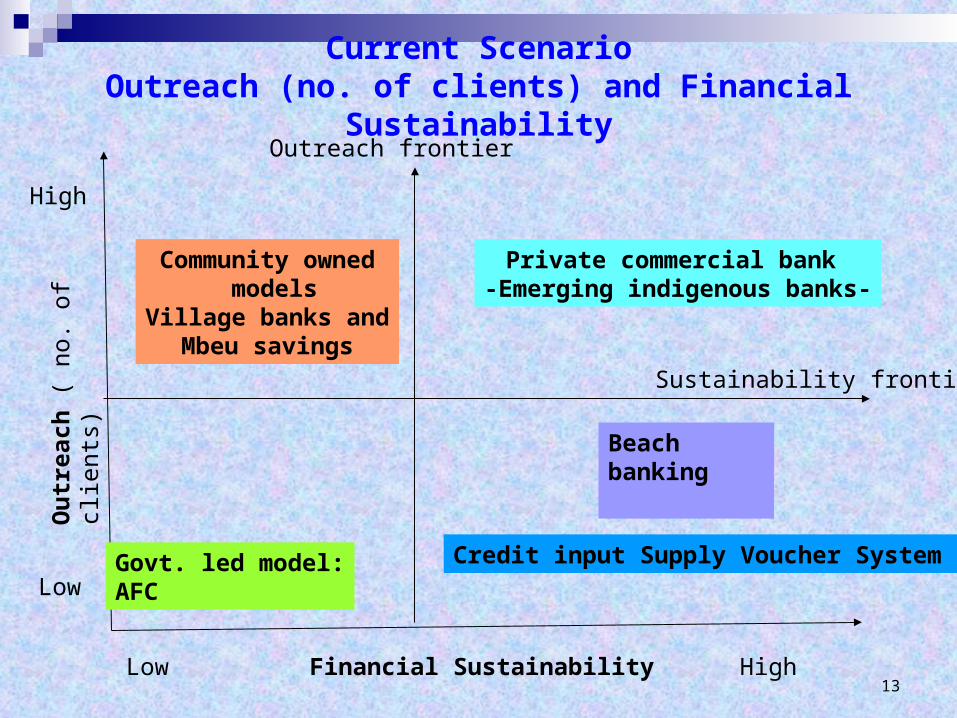

Govt. led model:AFC

Financial Sustainability HighLow

Low

High

Community owned models

Village banks and Mbeu savings

Ou

trea

ch (

no.

of

clie

nts)

Credit input Supply Voucher System

Private commercial bank -Emerging indigenous banks-

Current ScenarioOutreach (no. of clients) and Financial Sustainability

Beach banking

Sustainability frontier

Outreach frontier

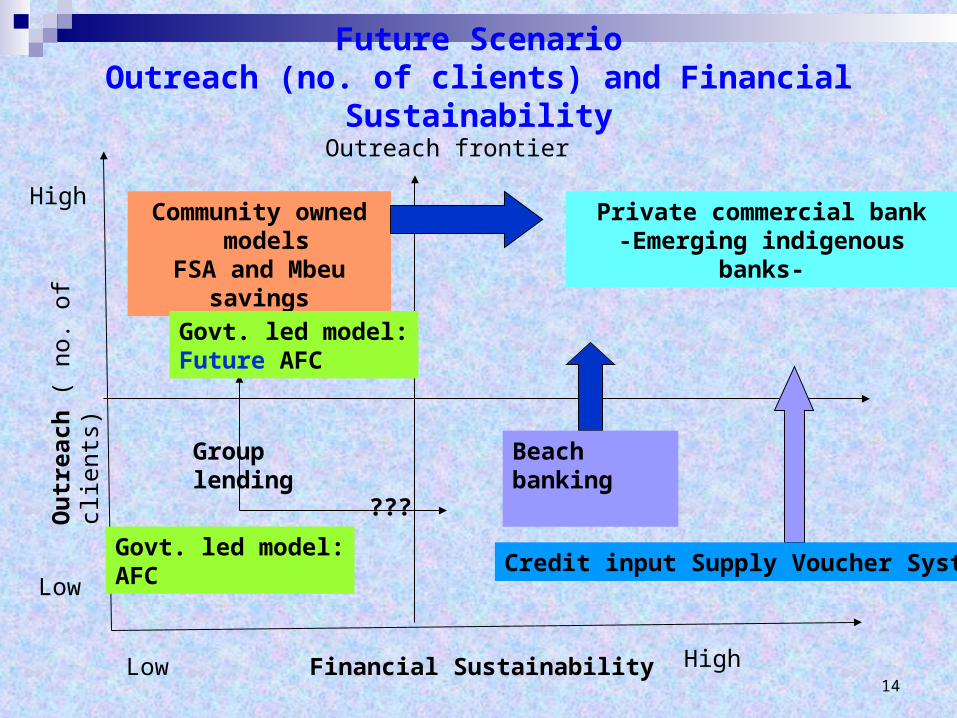

14 Financial Sustainability HighLow

Low

HighCommunity owned

modelsFSA and Mbeu savings

Ou

trea

ch (

no.

of

clie

nts)

Private commercial bank-Emerging indigenous banks-

Future ScenarioOutreach (no. of clients) and Financial Sustainability

Outreach frontier

Govt. led model:AFC

Govt. led model:Future AFC

Group lending

???

Beach banking

Credit input Supply Voucher System

15

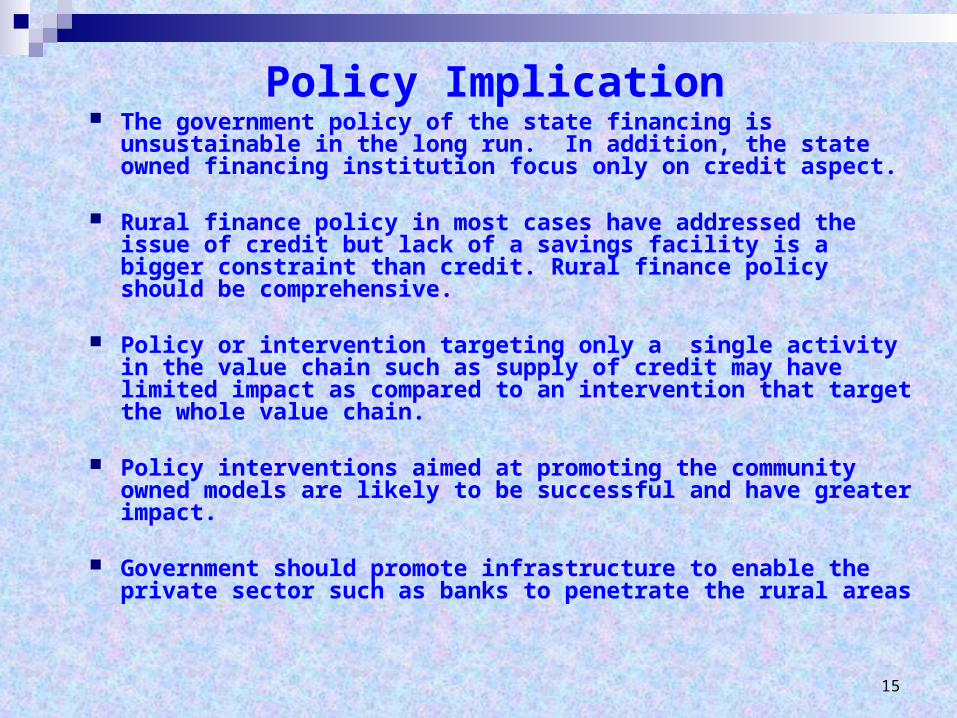

Policy Implication The government policy of the state financing is unsustainable in the

long run. In addition, the state owned financing institution focus only on credit aspect.

Rural finance policy in most cases have addressed the issue of credit but lack of a savings facility is a bigger constraint than credit. Rural finance policy should be comprehensive.

Policy or intervention targeting only a single activity in the value chain such as supply of credit may have limited impact as compared to an intervention that target the whole value chain.

Policy interventions aimed at promoting the community owned models are likely to be successful and have greater impact.

Government should promote infrastructure to enable the private sector such as banks to penetrate the rural areas

Related Documents