RISK IN ISLAMIC BANKS: EVIDENCE FROM EMPIRICAL RESEARCH BY NORAINI MOHD. ARIFFIN AND SIMON ARCHER Prepared by: Noor Fadhlika Mohd Ramlan 0723118 Nursyakilla Lokman 0823280 Nur Suhailah Mohd. Safaai 0823796 Nurul Izzati Mohd. Aminuddin Zaki 0838968

risk mgt

Nov 10, 2014

risk

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RISK IN ISLAMIC BANKS: EVIDENCE FROM EMPIRICAL

RESEARCH BY NORAINI MOHD. ARIFFIN

AND SIMON ARCHER

Prepared by:Noor Fadhlika Mohd Ramlan 0723118

Nursyakilla Lokman0823280Nur Suhailah Mohd. Safaai 0823796

Nurul Izzati Mohd. Aminuddin Zaki0838968

INTRODUCTION

INTRODUCTION

Unique characteristics of Islamic Banks: profit-sharing loss-bearing

Transparent in reporting risks because Investment Account Holder (IAH) need to:

Monitor their investment Assess potential risks and rewards Protect their interest

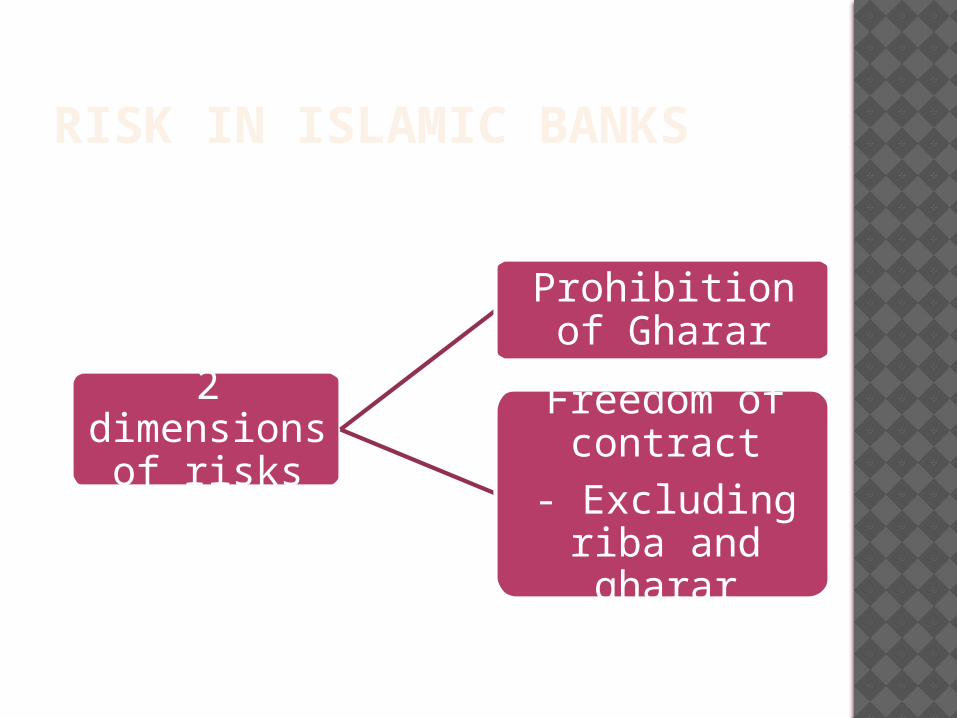

RISK IN ISLAMIC BANKS

2 dimensions

of risks

Prohibition of Gharar

Freedom of contract

- Excluding riba and gharar

Gambling

• Creation of risks for chance of very high gain

• Zero-sum game (create no wealth)

Risk taking

• Part of the real economic activity that creates economic value

• Permissible and desirable

RISKS FACED BY ISLAMIC BANKS AND CONVENTIONAL COMMERCIAL BANK

• Asymmetric information problem• Capital Impairment RiskCredit Risk• Cannot hold return-producing cash

equivalents• Lack of sufficient Shari’a compliant liquid

instrumentsLiquidity Risk

• Currency fluctuationsCurrency Risk

• Not ApplicableInterest-rate Risk

Risk of trade and

investmentFiduciary Risk – operational risk or the risk of breach of the Mudaraba contract or misconduct or

negligenceDisplaced commercial risk – rate of return risk

RESEARCHMETHODOLO

GY

RESEARCH METHODOLOGY

Questionnaire survey & contacting the banks directly

(e-mail or post)

Sample – 28 Islamic banks in 14 countries

RESEARCH METHODOLOGY (CONT)

How does the risk perception of Islamic bankers differ from

conventional bankers with respect to the market in

which Islamic banks typically operate?

Do Islamic banks use the more technically

advanced risk measurement techniques?

Apart from using similar risk mitigation approaches as in conventional banks, do Islamic banks widely use Shari‘ah-compliant

risk mitigation approaches?

Which risk mitigation process used by

conventional banks are not used by Islamic banks?

RESEARCH QUESTIONS

PROPOSITION

Proposition 1 – Salam and Istisna’a are perceived as

more risky than Murabaha and Ijarah

Proposition 2 – Profit-sharing contracts (Musharaka and

Mudaraba) are perceived as more risky than mark-

up based contracts (Murabaha, Salam,

Istisna’a, and Ijarah)

Proposition 3 – Not many Islamic banks use the

more technically advanced risk measurement approaches

Proposition 4 – Islamic banks use a number of risk mitigation methods that are different from

methods used by conventional banks, as they are designed to be

Shari’a compliant

FINDINGS

FINDINGS

SUB-SECTIONS

(1)RISK PERCEPTIONS

(2)RISK MEASUREMENT

(3)RISK MANAGEMENT

1- RISK PERCEPTIONS Using the 5-Likert scale,

1- RISK PERCEPTIONS CONT. Link the type of risks with the products

Operational

Market Credit Liquidity

Mudaraba

Musharakah

MMQ

Ijarah

Istisna’

Murabahah

Sukuk

Salam

1- RISK PERCEPTIONS CONT. Link the type of risks with the products

1- RISK PERCEPTIONS CONT. Finding shows that;

PROPOSITION 1 is supported by the findings since both Salam and Istisna’a contracts are riskier than Ijarah and Murabahah.

PROPOSITION 2 is partly supported by the findings because Mudarabah and Musharakah is perceived to be riskier than Murabahah and Ijarah and Istisna’a, not to Salam.

Mudarabah and Musharakah contribute to the banks earnings, but they attract more risks to the banks.I. Rate of return risk;II. Liquidity risk;III. FOREX risk; andIV. Operational risk

1- RISK PERCEPTIONS CONT. Link between the risks and countries

1- RISK PERCEPTIONS CONT. All countries opinion that credit risk is

the most important risk.Consistent with the study in conventional

banks.Basel Committee reports, weak credit

management practice and poor credit quality are major factors of bank failures and banking crises.

Malaysia consider operational risk is important as credit risk.Match with emphasis in Basel 2 on

operational risk in banks and the collapse of several companies.

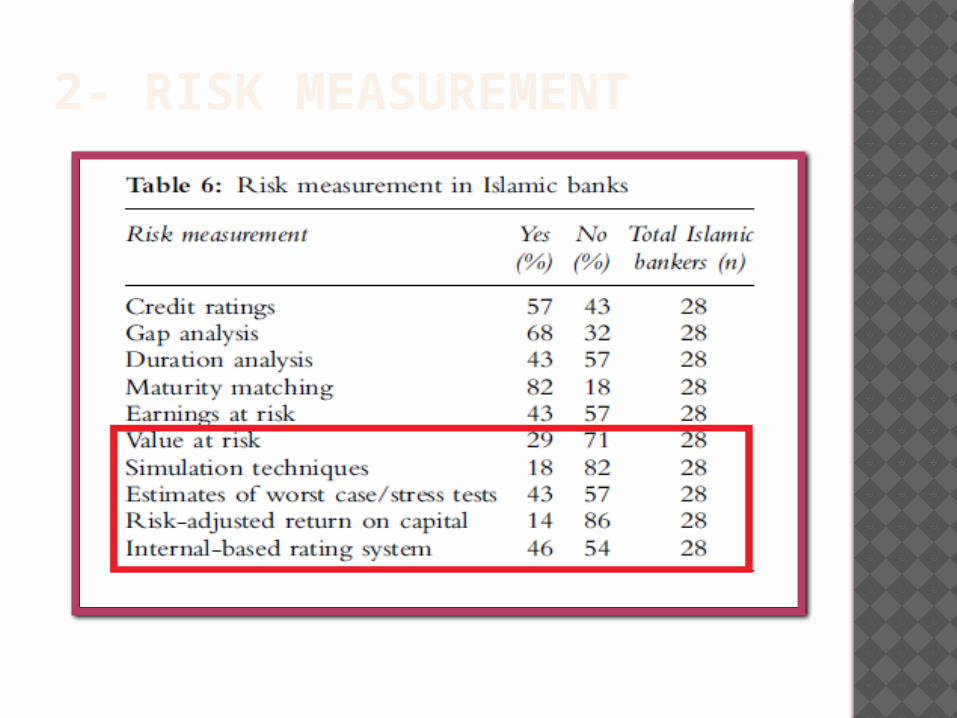

2- RISK MEASUREMENT

2- RISK MEASUREMENT CONT. Majority of the Islamic bankers prefer to

use traditional risk measurement. Minority of them use more technically

advanced risk measurement except for the internal-based rating system(46%) and estimates of worse case(43%).

The finding supported the argument in PROPOSITION 3.

3- RISK MANAGEMENT

3- RISK MANAGEMENT CONT. Islamic banks use similar methods of

risk management as the conventional banks.

Less usage of Shariah compliance techniques is due to the different interpretation by the Shariah scholars, and Salam and Istisna’a is not fully practiced by the banks.

Thus, PROPOSITION 4 is not been supported by the finding.

CONCLUSION

CONCLUSION Different contracts have different

implications for the importance of each risk

Each risk should be assessed separately to facilitate appropriate risk management.

Islamic banks perceived to use less technically advanced risk measurement techniques

Islamic banks are not fully using the Shari’a compliant risk mitigation method

THANK YOU FOR LISTENING(^_^)

Related Documents