RISK MANAGEMENT

Risk Management

Dec 25, 2015

talks about the risk involved in banking industry.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RISK MANAGEMENT

“Risk” can be traced to the Latin word “Rescum”

Risk is associated with uncertainty and reflected

by way of change on the fundamental/ basic

Reduction in firms value due to changes in

business environment

RISK …..

Danger that a certain unpredictable contingency can occur, which generates randomness in cashflow

Concentrates more on Systematic Risk

What is risk?

BUSINESS ARRAYS

Balance sheet

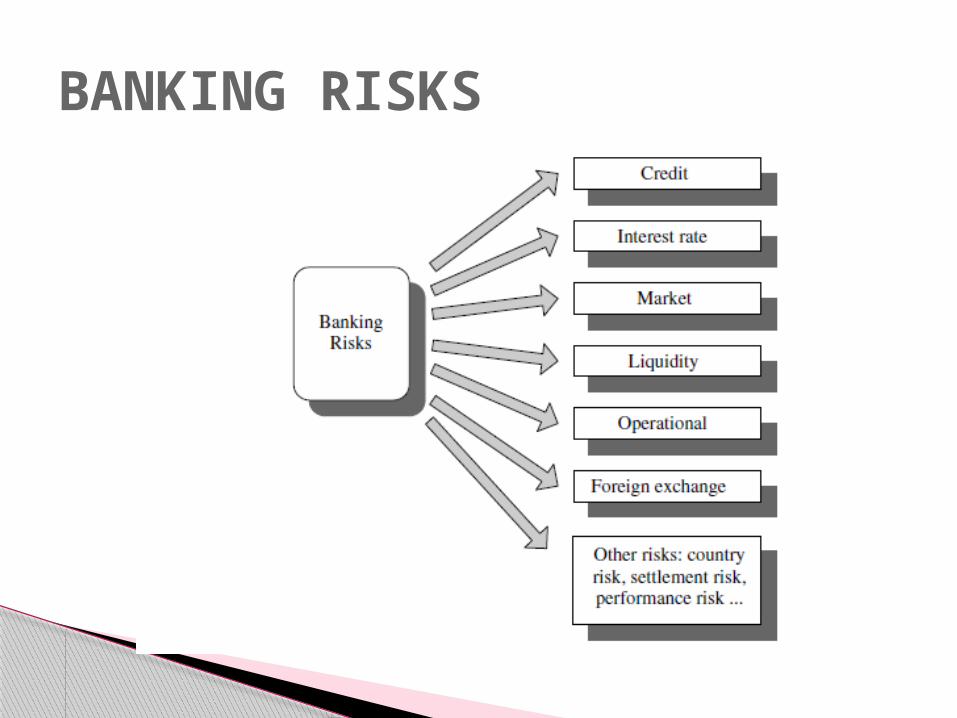

BANKING RISKS

RISK MANAGEMENT

Credit risk is the potential for

financial loss if a borrower or

counterparty in a transaction fails to

meet its obligations.

Credit Risk

Operational risk is the risk of loss

resulting from inadequate or failed

internal processes, people and

systems or from external events.

Operational Risk

Liquidity risk relates to the bank’s

ability to meet its continuing

obligations, including financing its assets.

Liquidity risk

Systematic risk is the risk of asset value change

associated with systematic factors. It is sometimes

referred to as market risk, which is in fact a somewhat

imprecise term. By its nature, this risk can be hedged,

but cannot be diversified completely away. In fact,

systematic risk can be thought of as undiversifiable

risk.

Systematic risk

Market risk is the potential for loss from changes in the value of financial instruments.

The value of a financial instrument can be affected by changes in: ◦Interest rates;◦Foreign exchange rates;◦Equity and commodity prices;◦Credit spreads.

Market Risk

Interest rate risk is the potential loss due to movements in interest

rates. This risk arises because bank assets (loans and bonds) usually have

a significantly longer maturity than bank liabilities (deposits). This risk can

be conceptualized in two ways. First, if interest rates rise, the value of the

longer term assets will tend to fall more than the value of the shorter-term

liabilities, reducing the bank’s equity.

Second, if interest rates rise, the bank will be forced to pay higher interest

rates on its deposits well before its longer term loans mature and it is able

to replace those loans with loans that earn higher interest rates.

Interest rate risk

Foreign exchange risk is the risk that the

value of the bank’s assets or liabilities changes

due to currency exchange rate fluctuations.

Banks buy and sell foreign exchange on behalf of

their customers (who need foreign currency to

pay for their international transactions or receive

foreign currency and want to exchange it to their

own currency) or for the banks’ own accounts.

Foreign Exchange risk

Commodity risk is the potential loss due to

an adverse change in commodity prices.

There are different types of commodities, including

agricultural commodities (e.g., wheat, corn,

soybeans), industrial commodities (e.g.,metals),

and energy commodities (e.g., natural gas, crude

oil). The value of commodities fluctuates a great

deal due to changes in demand and supply.

Commodity Risk

Performance risk exists when the transaction risk depends more on how the

borrower performs for specific projects or operations than on its overall credit

standing.

Performance risk appears notably when dealing with commodities. As long as

delivery of commodities occurs, what the borrower does has little importance.

Performance risk is ‘transactional’ because it relates to a specific transaction.

Moreover, commodities shift from one owner to another during transportation.

The lender is at risk with each one of them sequentially.

Risk remains more transaction-related than related to the various owners

because the commodity value backs the transaction. Sometimes, oil is a major

export, which becomes even more strategic in the event of an economic crisis,

making the financing of the commodity immune to country risk.

Performance Risk

Solvency risk is the risk of being unable to absorb losses, generated by all types of risks, with the available capital.

Solvency risk is equivalent to the default risk of the bank.

Solvency is a joint outcome of available capital and of all risks. The basic principle of ‘capital adequacy’, promoted by regulators, is to define what level of capital allows a bank to sustain the potential losses arising from all current risks and complying with an acceptable solvency level.

SOLVENCY RISK

Business Risk derives from a reduction of margins not due to market, credit or operational risks, but to changes in the competitive environment and in customer behavior.

Specifically, it mainly concerns future changes in margins and their impact on the Group's value and capitalization levels.

Business risk

Real estate risk comprises potential losses from

adverse fluctuations in the market value of the

real estate portfolio owned by the Group.

Customers' properties subject to mortgage and

leased property are not included.

REAL ESTATE RISK

Reputational risk is the current or future risk

of a decline in profits as a result of a

negative perception of the bank's image by

customers, counterparties, bank

shareholders, investors or the regulator.

Reputational risk:

Strategic risk arises from unexpected changes in the

competitive environment, from the failure to recognize

ongoing trends in the banking sector or from making

incorrect conclusions regarding these trends. The

impacts of decisions that are detrimental to long-term

objectives and that may be difficult to reverse are also

considered.

Strategic risk

Legal risks are endemic in financial contracting and are separate from the legal ramifications of credit, counterparty, and operational risks. ◦ For example, environmental regulations have radically

affected real estate values for older properties and imposed serious risks to lending institutions in this area.

A second type of legal risk arises from the activities of an institution's management or employees. Fraud, violations of regulations or laws, and other actions can lead to catastrophic loss.

Legal Risk

Sovereign risk, which is the risk of default of sovereign issuers, such as central banks or government sponsored banks. The risk of default often refers to that of debt restructuring for countries.

A deterioration of the economic conditions. This might lead to a deterioration of the credit standing of local obligors, beyond what it should be under normal conditions. Indeed, firms’ default frequencies increase when economic conditions

deteriorate. A deterioration of the value of the local foreign currency in terms of

the bank’s base currency. The impossibility of transferring funds from the country, either

because there are legal restrictions imposed locally or because the currency is not convertible any more.

Convertibility or transfer risks are common and restrictive definitions of country risks.

A market crisis triggering large losses for those holding exposures in the local markets.

Country risk

Model risk is significant in the market universe, which traditionally makes relatively intensive usage of models for pricing purposes.

Model risk is growing more important, with the extension of modelling techniques to other risks, notably credit risk, where scarcity of data remains a major obstacle for testing the reliability of inputs and models.

The model used to predict the relationship may not be

accurate due to the variables considered and

assumptions made.

Model risk

RISK MANAGEMENT PROCESS

VERTICAL

◦ TOP DOWN

◦ BOTTOM UP

HORIZONTAL

RISK MANAGEMENT PROCESS

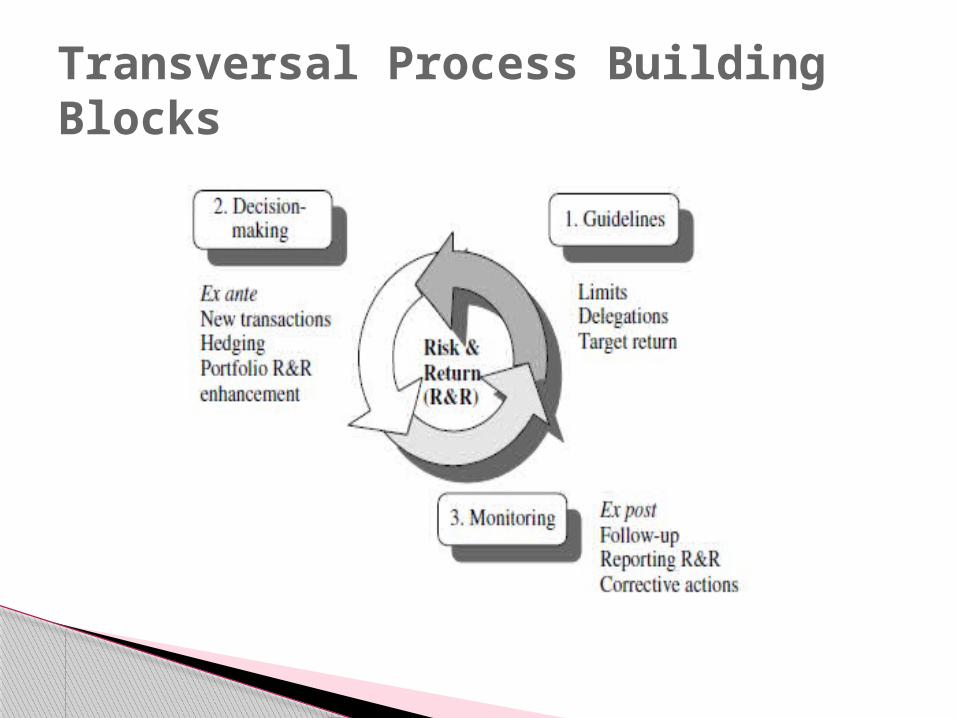

Transversal Process Building Blocks

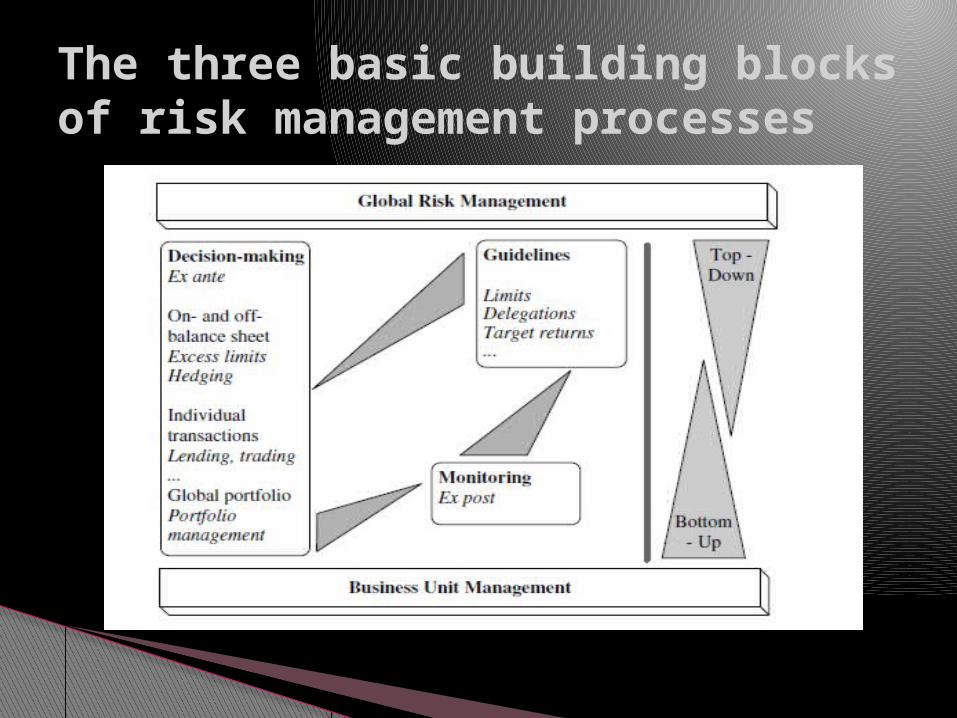

The three basic building blocks of risk management processes

Overall views of risk processes and risk–return

Function of Central units and of the risk department

ALM is the unit in charge of managing the interest ra

The ALM Committee (ALCO) ◦ is in charge of implementing ALM decisions, ◦ The ALCO agenda includes ‘global balance sheet

management’ and the guidelines for making the business lines policy consistent with the global policy.

ALM

SCOPE OF ALM

RISK DEPARTMENT

IT and RISK MANAGEMENT

Standard deviation of stock prices

Standard deviation of net income

Standard deviation of ROE and ROA

MEASURES OF OVERALL RISK

The ratio of non performing assets(past due 90 days or more) to total loans and leases

The ratio net charge offs(worthless and written off) of loans to total loans and leases

The ratio of annual provision for loan losses to total loans and leases or to equity capital.

The ratio of non performing assets to equity capital

Total loans to total deposit ratio

Credit risk measure

Cash and due from balances held at other depository institutions to total assets

Cash assets and government securities to total assets.

Liquidity risk measure

The ratio of book value of the asset to the estimated market value of those same assets

The ratio of book value of the equity to the market value of the equity capital

The market value of the common and preferred stock per share reflecting investor perception of financial institution risk.

MARKET RISK – PRICE RISK

The ratio of interest sensitive assets to interest sensitive liabilities◦IS Assets > IS Liabilities risk when interest rate falls and vice versa if IS Liabilities > IS Assets

Interest Rate Risk

Interest rate spread between market yield on debt issues and market yield on government securities of the same maturity.◦ Risk – if increase in spread

Ratio of stock price per share to EPS. ◦ Risk if ratio falls

The ratio of equity capital to total assets. ◦ Decrease in equity funding risk for the

shareholders and debtors

CAPITAL RISK MEASURE

Related Documents