Chua Sock Koong Group Chief Executive Officer Riding the digital wave Singtel Investor Day ▪ 13 June 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chua Sock KoongGroup Chief Executive Officer

Riding the digital waveSingtel Investor Day ▪ 13 June 2018

Forward looking statement – Important note

2

The following presentation contains forward looking statements by the management of Singapore

Telecommunications Limited ("Singtel"), relating to financial trends for future periods, compared to

the results for previous periods.

Some of the statements contained in this presentation that are not historical facts are statements of

future expectations with respect to the financial conditions, results of operations and businesses,

and related plans and objectives. Forward looking information is based on management's current

views and assumptions including, but not limited to, prevailing economic and market conditions.

These statements involve known and unknown risks and uncertainties that could cause actual

results, performance or events to differ materially from those in the statements as originally made.

Such statements are not, and should not be construed as a representation as to future performance

of Singtel. In particular, such targets should not be regarded as a forecast or projection of future

performance of Singtel. It should be noted that the actual performance of Singtel may vary

significantly from such targets.

“S$” means Singapore dollars, "A$" means Australian dollars and “US$” means United States dollars

unless otherwise indicated. Any discrepancies between individual amounts and totals are due to

rounding.

Our Strategy

3

We are enabling

people &

businesses…

.. underpinned by

significant

investments…

Connectivity Digital services

Network & spectrum Technology

Lean cost

structure

Customer-centric

digitalisation.. as we transform

ourselves to drive

sustainable growth

in the digital era.

Talent

Growth engines

Cyber

security

Digital

marketing

OTT

video

ICT

We have made good progress with our strategy1

4

Scale in digital

CAGR3 in ICT revenue 8%

Decline in traditional carriage2 business

CAGR3 in traditional carriage2 revenue-2%

Revenue diversification

1. All figures based on FY18 unless otherwise stated.

2. Comprises Group Consumer & Group Enterprise less ICT.

3. Compound annual growth rate for FY14 to FY18.

Robust growth in ICT

2

CAGR3 in digital business revenue61%

S$16.8b S$17.5b

86%76%

13%6%

1%

18%

FY18FY14

Digital Businesses

Traditional carriage

ICT

Data services as a % of mobile revenues• 62% in Singapore• 79% in Australia

Growth drivers• Cyber security• Smart nation• Cloud services

>S$1 billion in digital marketing revenues

Deepen telco digitalisation

5

Services

Self-serve

Omni-channel

Unmanned store

Revamped shops

My Singtel/ My Optus apps

Livebots/ chatbots

Delighting the

customer

Higher

efficiency &

lower

operating

costs

E-shop

Extend ICT leadership

6

3.1

2.5

2.3

FY16FY14 FY18

+8%

Group Enterprise ICT revenue

1. IDC MarketScape: Asia/Pacific Next-Generation Telcos: Telecom Services 2018.

Recognised leader in ICT services in APAC1

S$’b

Strategies

Cap

ab

ilities

Cyber

security

Smart

nationCloud

services

Growth Drivers

CAGR

Vodafone

Orange

AT&T

BT

Singtel

Telstra

Tata Communications

Verizon

T-Systems

NTT Com

GCX

Contenders

Major

players

Leaders

Participants

Scaling cyber security to the next level

7

Progress global

organisation

Drive operational

synergies

Accelerate path

to scale

1. 2018 Gartner “Magic Quadrant for Managed Security Services, Worldwide”.

1

Global managed security services leader

Completeness of vision

Ab

ility

to

exe

cute

Establishing leading ad tech platform

8

Gain scale

Grow profitability

Working with

>2,000 advertisers

Best technology platform

+ve

EBITDA

>S$1b

Revenue

Harnessing scale of our associates

9

Subs

Data

DigitalEcosystem

~700m mobile

customers

Growing

adoption of data services

Regional payments

OTT video

Gaming & eSports

IoT

Services to meet

consumers’ digital

lifestyles

New content

Advancing our transformation

10

FY18

76%

FY23E

17,532

24%

Non-carriage (ICT & digital businesses)

Traditional carriage

Reshaping our revenue

‘Best in class’ execution

Accelerate growth in ad-tech & cyber

security

Digital services partnerships

New business & capabilities

Delivering shareholder value

11

6.8 6.8 6.8

10.7 10.7 10.7

3.0

FY16

17.5

FY18

20.5

FY17

17.5

Sin

gap

ore

cen

ts p

er

share

Interim dividend Final dividend Special dividend

Expect to maintain 17.5 cents payout

for FY19 & FY20

Robust financial position

net debt1S$9.8b

net debt gearing224.9%

1. Gross debt less cash and bank balances adjusted for related hedging balances.

2. The ratio of net debt to net capitalisation. Net capitalisation is the aggregate of net

debt, shareholders’ funds and minority interests

1.3xnet debt: EBITDA & share of associates’ pre-tax profits

Singtel Investor Day 2018Consumer Singapore

Yuen Kuan MoonCEO Consumer Singapore

Strategic Focus Areas

Drive telcoindustry growth by offering higher value services

2

Digitise our core to engage customers better

Excite our customers and fulfil our employees

Safeguard our core and drive new growth

▪ Almost all government services in Singapore to go digital by 2023

▪ Opportunity to drive growth in digital and mCommerce services

▪ Leverage digitisation technology to improve operational costs

▪ Digitise customer engagement – service available 24/7

▪ Next generation retail experience

Q4FY16 Q4FY17 Q4FY18

RazerPhone

Provide mobile data to enable customer’s content rich lifestyles

Average monthly usage per postpaid subscriberBigger Data Offers for customers to access enhanced content

Exciting exclusive phone launches

FY16 FY17 FY18

Mobile Data Revenue

2.4GB3.5GB

4.2GB

Google Pixel 2XL

3

16%CAGR

Singtel Music continues to bring customers closer to live eventsOur customers get access to priority sales

Excite customers with digital business

4

Dash - 1st to support SG QR, in line with government vision of

convenient cashless payments

Exciting services to support our customers’ digital lifestyle

5

Pay on buses, trains and taxis

Tap and pay at >20,000 locations

One-stop for recipes, restaurant recommendations & bookings

Expanding into ticketed events

Magzter Gold - premium content at lowest subscription rates with no data charges

Best roaming coverage at affordable rates

Australia • Brunei • Cambodia • Indonesia • Laos •

Malaysia • New Zealand • Philippines • Thailand

[+] China • Hong Kong • India • Japan • Macau •

Myanmar • South Korea • Taiwan • Vietnam

[+] Austria, Bangladesh, Belgium, Canada, Croatia,Czech Republic, Denmark, Egypt, Fiji, Finland,France, Germany, Ghana, Greece, Hungary, Ireland,Israel, Italy, Kenya, Mexico, Mongolia, Netherlands,Nigeria, Norway, Pakistan, Poland, Portugal, Qatar,Russia, Saudi Arabia, Spain, Sri Lanka, Sweden,Switzerland, Turkey, UAE, UK, USA

6

$12 for 9 destinations

$20 for 18 destinations

$35 for 56 destinations

Drive broadband user experience with WiFi mesh & value-added services

Improved broadband in-home coverage with WiFi Mesh

Value-added services for the home

QustodioParental Control

Samsung Connect Home

Airties

Askey

7

Providing end-to-end fibre service to customer’s home

8 4

connected watches

personal and asset trackers

smart home devices

“”

One app for everything connectedCapture growth of connected consumer devices

8

connected healthcare and wellness devices

Monthly active app users (‘k)1

Digitising core operating model – driving productivity & better customer experience

% of online sales transactions2

% of self-help transactions2,3

9

840877

929 931

Q4FY18Q1FY18 Q3FY18Q2FY18

My Singtel users

1. Customers who access the My Singtel app at least once a month2. Includes mobile, broadband and Pay TV services3. Self-help transactions include activation, recharge, payments, usage & billing enquiries

Q3FY18

20%

Q2FY18

18%

Q1FY18

17%

Q4FY18

21%

Q4FY18

57%

Q3FY18

55%

Q2FY18

51%

Q1FY18

50%

1010

Enquiry RewardsTroubleshooting Local usage display

Data usage breakdown

Plan name & entitlement

Bill cycle

Re-contract eligibility / contract end date (Home & Mobile)

Display eligible vouchers

Deals and promotions

Reward summary

Message Inbox: list, read, link-out, delete

Manage inbox settings

Internet connectivity test

Troubleshooting guides

Roaming plan purchase

Manage My add-ons (Home & Mobile)

Display relevant add-ons for purchase (Home & Mobile

Prepaid Top-up charged to Postpaid bill

Transactional Contact Us Message Us

Network feedback

Share My SingtelApp

Enable a broad digital experience via My Singtel App

10

Digital first for prepaid customers with hi!App & Retailer App

Retailer App has halved average transaction time for customers

hi!App and hi!Rewards

Integration to improve customer engagement & loyalty

11

Query Interface

Selected product for top-up

Product Menu

Add products to favourites

Enter customer number

Tip: Slide the menu away, or tap anywhere outside of the menu to hide it

Fuss Free SellingNew User Interface

Select your denomination

Done!

Reply “1” to

confirm purchase

3

1 2

App Navigation Menu

App Homepage Menu

• Personalised eQueue

• Instant buy with QR code

• Interactive touch wall

• Café zone with vending kiosks

• Live Video Bots to reduce wait time

• 24-hr self-serve lobby with Singtel-exclusive parcel lockers

• Smart surrounds to track location of connected customers

• Electronic queue ticket on personal devices

• 24/7 Kiosks for customers to self-serve bill payment & replace SIM cards

• Automated check-out for instant purchases

• Crowd analytics to understand customers better

Transform flagship Comcentre shop into an intelligent storeTransformation award for Telecommunications at Singapore Business Review Listed Companies Awards

12

Smart innovative experience

Technology showcase

Understands ContextRecognise question context instead ofpicking up keywords only

Handles Complex QuestionProvide relevant answer to question withmultiple keywords

Richer PresentationDisplay richer and more interactiveanswers, instead of just plain text

Shirley is the 1st agent to respond to customer enquiries onMessage Us

Shirley on Message Us

Evolve our chat bot Shirley using AI, to better serve customers

Shirley on Singtel Website

13

14

Differentiate through digitisation

Create an effortless customer experience

Any Time, Anywhere, Any Mode

• Retail Transformation

• Collect @ Store

• Expand Prepaid self-serve

• Intelligent Comcentre Store

• Collect @ Singtel Retailers

• Live Video Bots & Self-Serve Kiosks

Online

Offline

OnlineOffline

Online Offline

Omni-channel

Omni-channel

Fully integrated omni-channel

OnlineOffline

Omni-channel

• Boost productivity through technology and digitisation

• Drive shift towards online

• Industry-leading omni-channel experience

Empower our customers Any Time, Anywhere, Any Mode

14

Q&A

15

Disclaimer: This material that follows is a presentation of general background information about Singtel’s activities current at the date of the presentation. The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. It is information given in summary form and does not purport to be complete. It is not to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. This material should be considered with professional advice when deciding if an investment is appropriate.

Allen Lew – CEO Consumer Australia13 June 2018

Singtel Investor Day 2018Consumer Australia

2

Strong market position

Portfolio of strong brands

Multi-channel sales and service

1.2mFixed

10.1mMobile

• HFC – 396k

• ULL – 339k

• NBN – 453k

• Other – 57k

Consumer services Call centres in Australia, India, Philippines

Over 350 stores

Online

2.2m My Optus App users

SMB & MVNO partnerships

Consumer Australia is uniquelypositioned for growth

• Postpaid – 5.3m

• Prepaid – 3.7m

• MBB – 1.1m

3Notes: 1. Based on P3 test in December 2017. P3 is a globally recognised company which performs independent measurement of mobile network performance.

Strong underlying business trends

Grew NPS

Delivered revenue growth

Acceleratednetwork

Excited customers

+10for Consumer Australia

$7.2b In FY18Best

in test in Australia1

Delivered EBITDAgrowth

$2.5bIn FY18

Acceleratednet adds

+384kacross postpaid and prepaid handset, and mobile broadband

Up 4%Up 4%

4

Future growth is fueled by four pillars

Lead in customer experience

Lead in mobile networks

Differentiate with exclusive premium content

Lead in business productivity

Lead in customer experience

Self-service viaMy Optus App

Big data analytics for proactive customer care

Improving end to end problem resolution

6

Continue 4G LTE excellence through extending coverage, densifying cell sites and Massive MIMO

Deploy 5G Fixed Wireless with commercial launch in 2019

Start virtualising core and implement intelligent EDGE network

Lead in mobile networks

Differentiate with exclusive premium content

Extended Premier League rights until May 2022

Encouraging take up of National Geographic

Engaging more customers with Optus Sport App starting with World Cup

8

Lead in business productivity

Operational excellence BOTS for customer interactions and AI in key processes

Product andprocesses simplification

Lean and agile organization accelerated decisions and improved collaboration

9

Thank you!

Singtel Investor Day 2018Bill Chang, CEO, Group Enterprise and

Country Chief Officer Singapore

13 June 2018

>12,000

#1 International

IPVPN in APeJ

#1 EVPN and Eline

in APeJ

#1 IPLC in

Singapore3

11Data Centres

>70 Offices in

>25 Countries

Singtel Group Enterprise at a glance

1. Gartner IT Services, Apr 20172. IDC Telecom Services Database Asia-Pacific 1H2017, Jan 20183. Leased line + Eline market revenue for Local Singapore4. Frost & Sullivan 2016 Asia Pacific Telco Cloud Service Provider of the Year

> 3,000 Industry Certifications

> 2,000 Cyber Security Experts

3

Group Enterprise : Our 3 Year Vision

Robotics and IoTAnalytics/ AICyber Security

Digital Capabilities

To be the key enabler of smart cities & digital enterprises with deep capabilities

Cloud Services

4

Our strategic transformation

ADrive leadership and value creation in core business

BAccelerate growth engines in Digital and ICT Services

CDouble down on cost transformation as part of DNA

DTransform into a leading Digital Enterprise in 3 years

5

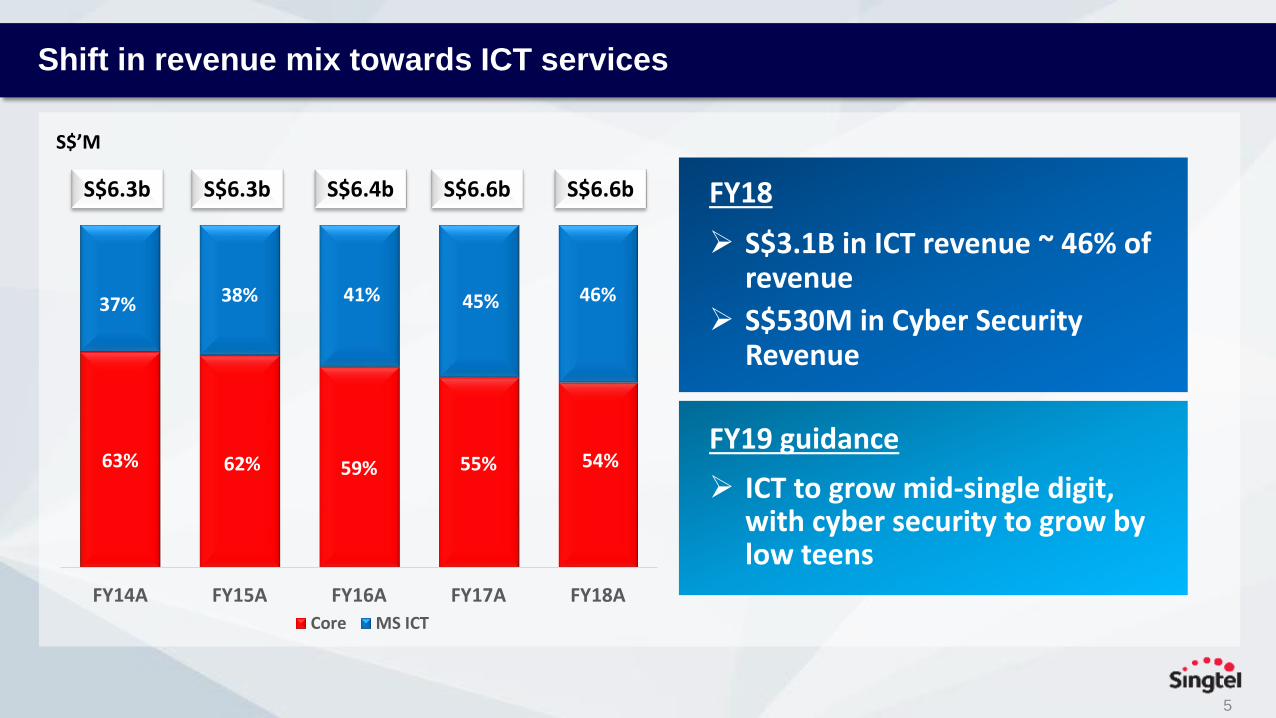

Shift in revenue mix towards ICT services

S$’M

FY18

S$3.1B in ICT revenue ~ 46% of revenue

S$530M in Cyber Security Revenue

FY19 guidance

ICT to grow mid-single digit, with cyber security to grow by low teens

63% 62% 59% 55% 54%

37% 38% 41% 45% 46%

FY14A FY15A FY16A FY17A FY18A

Core MS ICT

S$6.3b S$6.3b S$6.4b S$6.6b S$6.6b

6

Leadership in APAC Enterprise data services

Source: IDC Telecom Services Database Asia-Pacific 1H2017, Dec 2017

Singtel 21.8%

6.7%

6.1%

5.8%

5.2%4.5%

Others49.9%

Int’l IPVPNUS$1.51B

Singtel 16.2%

11.5%

7.5%

7.2%

6.1%5.9%5.4%

Others40.3%

Int’l Leased Circuit

US$453M

Singtel 23.4%

13.1%

9.9%7.0%6.3%

5.6%

Others34.5%

E-LineUS$294M

Singtel 17.5%

11.1%

8.8%

4.9%4.8%4.7%

Others48.3%

E-VPNUS$248M

Lead in Software Defined Network Services leveraging our network infrastructure and capabilities

Simplified endpoint

Telco Cloud Forum Awards 2017Best Telco Cloud SDN/NFV Project

Asia Telecoms Innovation Summit & AwardsEnterprise Service Innovation (SD Hybrid NW)Software & Applications Innovation (C+ SD WAN)

Deep VisibilitySimplified central management

Agile Service ProvisioningMinimise footprint, quick deployment and on-demand

Smart Predictive NetworkML/AI driven actionable insights

SD - LAN SD - WAN SDN

Singtel Hybrid Network

Cloud Connect

MPLS

Internet

Centralized management

Public Safety Next-Generation Electronic Road Pricing System

Smart Urban InfrastructureRetail Analytics

Core & Digital capabilities

Telco, Video, Social & Customer

Data Analytics

Cloud InfrastructureCyber Security& OT Security

Sensors & IOTManagement

AI, Machine Learning, RPA

Geographic Information System

Pharmacy Robotic Dispensary

Proven Track Record of Smart City and Digital Enterprise Transformation

Citizen Engagement with Smart Apps

Automation & Robotics for Enterprises

Cyber Defence for Enterprises

Collaboration with Research Institutions to develop local IP, build deep capabilities and drive Innovations.

Singtel Cognitive and AI Lab (SCALE@NTU) & Singtel-A*STAR Master Research Collaboration on 4 Dec 17 by DPM Teo Chee Hean

Advanced Remanufacturing and Technology Centre (ARTC) as 47th

member to focus on Industrie 4.0

NUS-Singtel Cyber Security Research and Development Laboratory in Oct 16

Supported by:

10

16.8 18.6 20.4 22.9 25.5 28.5

20.622.3

23.926.0

28.230.6

17.819.0

20.021.2

22.6

24.0

2016 2017 2018 2019 2020 2021

TS

PS

MS

55.359.9

64.3

70.1

76.4

83.2

in US$’

billions

Global Cyber Security Market growing at 8.5% annually

Source: Gartner, Forecast: Information Security, Worldwide, 2015-2021, 4Q17 Update, , 5 February 2018Chart created by Singtel based on Gartner’s ResearchMS: Managed Security Service: Remote management and/or monitoring of IT security functions delivered via remote security operations centers (SOCs), not through personnel on-site.

PS: Professional Services includes professional / advisory services to help companies analyze business operations and technology strategies. Include two subsegments: business and IT consulting. Includes Security TestingTS: Includes Hardware Support and Implementation

CAGR +8.5%

CAGR

6.1%

8.2%

11.1%

Carriers

SystemIntegrators

ProductVendors

Pure-PlayMSSPs

4 types of players compete in MSS

11

Leading edge technology ecosystem & R&D investments

Our key cyber capabilities

Global ASOC network and market access

Developing automated Managed Detection & Response platform

Cyber Security Institute

12

Leader

TW is a leader in Gartner’s 2018 MSS MQ

The only new leader in Gartner

MSS MQ 2018

2015

2016

2018

2017

Highlights from Gartner

“Trustwave is a competitive provider with both, proprietary products and services”

“…able to support a large client base up to larger global organizations”

“Expanded global footprint across APAC and NA via

strategic partnerships”

“Spiderlabs enhances the value of MSS through integration of threat intelligence data and SpiderLabs' analysts serving as a higher tier of skills for advanced triage”

SOURCE: Gartner

We have established a Global Leadership Position in Managed Security …

13

Industry wins and recognition in 2017

CloudTelco | MS

Cyber Security

Frost & Sullivan APAC Best Practices Awards 2017

Singapore Managed Security Service Provider of the Year

(2016 – 2017)

Frost & Sullivan Asia Pacific ICT Awards 2016Telecom Group of the Year (2016-2017)

NetworkWorld Asia Information Management Awards 2017Disaster Recovery & Business Continuity (2014 -2017)

NetworkWorld Asia Readers’ Choice

AwardsManaged Infrastructure Services (2012 – 2017)

NetworkWorld Asia Readers’ Choice Product

Excellence Awards Security-as-a-Service

(2012 - 2017)Regional Security Operations Center

Telco Cloud Forum Awards 2017Best Telco Cloud SDN/NFV Project

Telecom Asia Awards 2017 Best Managed Services Provider

Telecom Asia Awards 2017 Most Innovative Approach to

Mobile Security

Digital

FinTechInnovation Awards 2017Innovation in Big Data and Analytics Solution (NCS)

SC Awards 2017Best Managed Security

Service (Trustwave)

Asia Communications Awards 2017Satellite Operator of the Year (2015-2017)

Computerworld Hong Kong Awards 2017Global WAN Connectivity Service Provider of the Year (2015 – 2017

Frost & Sullivan Asia Pacific ICT Awards 2016Singapore Managed Cloud Service Provider of the Year (2017)

2018 Gartner’s Magic Quadrant for MSS, Worldwide

Leaders’ Quadrant (Trustwave)

HWM + Hardwarezone.com Tech Awards• Best Mobile Operator –

Singapore (2010-2013)• Best Telco – Singapore (2014 –

2017)• Best Fibre Broadband Service,

Singapore (2010 – 2017)

APAC Insider Singapore Business Awards 2018Best Mobile Network Operator

TMT Technology Awards 2017Best Mobile Service Provider -Singapore

TMT Global Excellence Awards 2018 Recognised Leader in Telecommunications - Singapore

Disclaimer: This material that follows is a presentation of general background information about Singtel’s activities current at the date of the presentation. The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. It is information given in summary form and does not purport to be complete. It is not to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. This material should be considered with professional advice when deciding if an investment is appropriate.

Group

Digital Life

Creating new scalable

engines of growth for the

Singtel Group

Samba NatarajanCEO, Group Digital Life

13 June 2018

Singtel Investor Day 2018

2

Singtel Group Digital Life at a glance

Digital Marketing

Over the Top Video

Innovation Engine

Creating new scalable engines of growth for the Singtel Group

Data Analytics

Core businesses VC Fundone the largest

independent buy-side marketing technology providers in the world

~S$1 Billion

Revenue

Working with

>2000advertisers

Leading subscription video service in the emerging

markets MILLION

>20

Downloads

#1 in app downloads and

branding in Indonesia

Rollout of Free to Air Live TV in

FY19

Delivering mobility intelligence insights leveraging carrier data

65+ Investments

Offices in:San Francisco, Beijing, Israel, Sydney, Singapore

US$250million evergreen fund

Group Digital Life

FinancialsS$1.16b

Actual+ 86%vs FY17

FY18 Revenue

S$71m vs FY17FY17 : -S$-122 FY18 : -S$51m

FY18 EBITDA

Data-as-ServiceMobility Intelligence ReportsData Science Consulting

Increased by

3

Amobee

900+Employees

2,000Advertisers

23Offices

$1BRevenue

Providing Data Driven Solutions for the World’s Largest Brands

San Diego Chicago London Tel Aviv Singapore SydneySan Francisco Los Angeles New York Melbourne

4

About AmobeeWholly Owned subsidiary of Singtel - Over $1Billion invested

Leading Mobile and DataPlatform for Operators, Advertisers and Publishers.

US$340MAcquired in 2012

True Cross Channel AdvertisingCross channel & cross device targeting, powered by INK.

US$240MAcquired in 2014

Real Time Brand IntelligenceAnalyzing and targeting the world’s

content consumption.

US$150MAcquired in 2014

Integrated data, analytics and activation platformUsed by agencies and advertisers worldwide

US$310MAcquired in 2017

• Founded in 2005 in California, wholly owned subsidiary of Singtel.

• Acquired Turn on February 22, 2017, adding to our advertising technology capabilities.

• Now one of the largest independent buy-side marketing technology providers in the world, providing unparalleled solutions for our clients.

• Turned EBITDA positive for the first time in FY18

5

• Brand Sentiment and Market Trends• Advanced Audience Modeling• Cross-Platform Performance• Consumer Journey Management• Customized Analysis

Amobee Marketing PlatformWorld-class technology enables you

to transform insights into action.

Amobee DMP: Built to understand your consumer at a molecular level.

• Branding and Direct Response Planning and Activation

• Omnichannel Campaign Management• Brand Safety• In-Flight Optimization

Advanced Analytics: The industry’s most powerful

intelligence engine built for marketers.

Amobee DSP: Orchestrate exceptional consumer experiences.

• Data Centralization• Audience Management

and Segmentation

Our Integrated Programmatic Stack

6

The #1 video on demand service for the emerging markets

1. Bringing the ‘Best of Hollywood and the Best of Local’ for me time, family time, and kids time

2. Access anytime, anywhere, on any device (especially mobile)3. All for less than the price of a trip to the movies

Value Proposition:

Launched in 2015, HOOQ is a joint venture between Singtel, Sony Pictures and Warner Bros

HOOQ is now live in five markets including Philippines, Thailand, India, Indonesia and Singapore

Leading over the top service in SE Asia with over 20M downloads in the Playstore

Premium content offering Hollywood + Local + Kids in every country we operate, with average 40,000 hours.

7

1st in SEA to develop pipeline of original series with premium program titles

HOOQ remains #1 in Indonesia and is one of the two leaders in SEA

maintains its position in the region and will launch a transformed business model to scale in FY19

Freemium layer for Monthly Active

Users

Sachet plans for

occasional users

SVOD

Launching transformed business model in FY19

1. Freemium layer to retain monthly active users• Free-to-air LIVE TV streaming• Sample of premium : first episode of premium content

2. Sachet plans for occasional users• e.g 1 day plan launched in Indonesia for occasional users

3. Existing premium SVOD

8

Industry leader for carrier-based data-driven software solutions that transform raw spatial temporal signals into mobility intelligence

Anonymized data from telcooperators, mobile SDKs and other

sources of mobility data

DataSpark’s Mobility Genome™ processes data and turns location data into rich actionable insights.

Mobility intelligence insights into people, places and movements, which can power applications in transport, retail, telco network optimization amongst others

*Non-exhaustive list

9

Applications

Telecommunications

Products

DataSpark’s Mobility Intelligence Capabilities

Mobility Genome™ FrameworkPowerful framework of technologies and algorithms to transform anonymized telco data into insights on people, places and movement

Telco Network Planning and DataSpark CAPEX Optimizer

• Optimizes performance and profitability of network infrastructure, and quality of customer experience

• Combines network and subscriber data with mobility intelligence to optimize CAPEX and network planning

Transport

Retail OOH Marketing

Events and Tourism

Data-as-a-Service APIS

• APIs provide users with programmatic access to DataSpark’s rich mobility intelligence dataset.

Mobility Intelligence Reports

• Provides snapshots of commercial buildings across Singapore • Daily footfall• Profiling of visitors by age

and gender• Home and work locations

AD

Billboard

10

Innovation Engine – Innov8

Our Mission

To help Singtel Group:

Adopt new innovative technologies / solutions Strengthen existing Singtel Group business Seek new growth opportunities Foray into new markets

Our Objectives

Reinforce Singtel as a Thought Leader

Drive adoption of innovative technologies

StartupInvestments

Identify trends and insights

Our Global Presence

Offices in Global Innovation Hubs100% owned subsidiary of

US$250MEvergreen Fund

with Own Decision Making Structure

Our Fund

Beijing

Sydney

11

Innov8 FY18 Highlights

Innov8 remains an active investor and has made 9 investments in FY18.

Since its establishment in 2010, Innov8 has invested in over 70 companies globally in various verticals including cyber security, digital marketing, mobile video and big data.

Innov8 launched ICE71 in conjunction with NUS Enterprise -The region’s first cybersecurity

startup hub

The Innovation Cyber Security Ecosystem at Block 71 (ICE71) aims to catalyse, develop and grow the cyber security start-up ecosystem in Singapore and the region.

Established Innov8’s presence in

China

The growth of China’s economy over

the decade has generated global interest in its tech scene. To capture this opportunity, Innov8 has re-established its presence in Beijing to extend its network and reach to start-ups in the Chinese market.

CHINA

12

111

184

369

511

626

1163

0

300

600

900

1200

1500

FY13 FY14 FY15 FY16 FY17 FY18

GDL Revenue

-104

-170

-180

-137

-122

-51

-200

-180

-160

-140

-120

-100

-80

-60

-40

-20

0FY13 FY14 FY15 FY16 FY17 FY18

GDL EBITDAS$m S$m

Group Digital Life Financials

Singtel Investor Day

Advanced Info Service Plc.

13 June 2018

Ticker: ADVANC (SET)AVIFY (ADR)

Add AIS IR LINE@

AIS: Digital Life Service Provider

Partner to offer differentiated “Digital service”

Lead and digitally transform in “Mobile”

Grow stronger in“Fixed broadband”

Aim to be a significant player in 2020• Leverage existing nationwide fibre

infrastructure • Defensive value to core mobile

business

4th year of operation in 2018

Mark leadership in mobile data• Nationwide 4G/3G/2G coverage

with focus on network quality• Focus on scale to maintain cost

advantage

Pursue long-term growth with integrated services• Emphasize partnership &

ecosystem• Leverage the large sub base and

telecom infrastructure

2

Mobile money

IoT

Video

48%

25%

27%

1Q18

Mobile revenue market share

covering 50 key cities out of 77 provinces

expect to cover 6mn homepass* out of total 21.5m households

Digital life service provider with convergence products

40%

60%

Mobile revenue

Bt31bn

Mobile data

Voice

81%57%

19%43%

subs % to mobilerevenue

prepaid postpaid

40.1mn

1Q18 breakdown39%

33%21%

7%

1Q18

*Homepass is defined as a number of households within AIS fibre service area. This includes the homes that require additional investment i.e. port, last miles to be able to get connected.

Subscriber market share(approx.8.4mn)

Focused on FOUR key areas

EnterpriseBusiness

• > 90% cloudification

• Network virtualization ready for 5G

AIS’ digital transformation toward 2020

• Digitize all customer journeys

• AI/Chatbots embedded into all self-service channels

• Deployment of OMNI channels

• 5G future-proof networks

• IT legacy transformed to Cloud-friendly network architecture

• AI for network operation

Data-drivenanalysis based on customer insights:

Bundle mobile, fibre & content via FMC

Network Function Virtualization & Cloudification

Customer Value Management

Full Service Digitization

Next Generation Network

New opportunities:• IoT• SME & R-SME• Managed

Security• Mobile Digital

Marketing

Maximize value of contents in customer retention and branding

Contents and Enterprise Segments

Next Generation Economy

Next Generation Xperience

• Organizationreadiness for digital disruption

• Leveragecapabilities and create synergies in value chain supporting digital business objectives

Organization Transformation

Next Generation Team

• Expand revenue contribution of enterprise business from 9% to 25%

• Move to ARPH• Improve revenue

assurance and add valued users

• Provide shops & services that never sleep

• Data-driven organization & culture

Targ

et 2

020

Str

ateg

y to

war

d 2

020

3

1Q18 Quarterly Summary

4

Service revenue improved in all segments

(Bt mn)

Strategic executions

Cost controlled resulted in profit expansion

Expand into enterprise market▲6.5% YoY▲2.5% QoQ

18,905 -

5,000

10,000

15,000

20,000

EBITDA (Bt mn)

1Q18

▲3.1% YoY▲0.5% QoQ

NPAT (Bt mn)

• Improved service revenue

• Lower regulatory fee, network OPEX, and controlled handset subsidies

▲9% YoY▲2.4% QoQ

1,418

962

1,013

31,172

34,565

IC &equipment rental

Others

FBB

Mobile

Servicerevenue

8,037 -

2,000

4,000

6,000

8,000

10,000

▲4.5% YoY▲4.4% QoQ

1Q18

• 7.6GB/sub of mobile data consumption

• 51k of FBB net addition• CSL revenue

consolidation

• Paid Bt3.4bn for 81.47% of CSL’s shares

• Fully consolidated since Feb-18• Incurred goodwill of Bt2.8bn• Final tender offer until 6-Jul at Bt7.80/share▲85% YoY

▲6% QoQ

▲63% YoY▲51% QoQ

▲31% YoY▲28% QoQ

IC &Equipment

rental • Paid Bt788mn to buy 1/3 JV stake with Rabbit and LINE

• Utilize each party’s strength in subscriber

base, distribution channel, and brand

Widen e-service/mobile payment to Thai users

Officially signed 2100MHz contract

• Agreements effective since 1-Mar• Equipment rental agreement• Roaming agreement

• Net financial impact remains relatively the same at a net cost of Bt3.9bn/year

5

FY18 Guidance (maintained)

Item FY18 Guidance

Service revenue

(ex. IC)+7-8% YoY

• 2% of which comes from CSL• Increasing data usage on 4G and fixed broadband

subscriber base• Moderate growth in enterprise business with synergy from

CSL

Sale revenueDecline and make near-zero margin

• More targeted marketing campaigns

EBITDA margin 45-47% • Improving revenue and continuing cost management

Cash CAPEX Bt35-38bn • Strengthen 4G capacity to support mobile data growth

using advanced technology• Expand fixed-broadband coverage and last miles

Dividend policyMinimum 70% payout of NPAT

• Preserve financial health and flexibility for future growth

Mobile: Drive 4G users through valued offerings

6

Business direction in 2018

• Increasing 4G penetration and data usage

Key

dri

ver

Str

ateg

y

• Continue to improve network and brand perception

• Target uplifted offerings through customer value managementprogram

• Convergence of mobile, FBB, and video content targeting revenue per household and brand value

32 7.6

Subscriber(mn)

+14%YoY

-5%YoY

• Postpaid segment grew robustly following popularity of video streaming on mobile

• Prepaid segment softened due to prepaid-to-postpaid conversion and competition

Focus on postpaid and maintain competitiveness in prepaid

35% 39% 42%46%

50%56% 53%

49%

46%43%

0%

10%

20%

30%

40%

50%

60%

4G handset penetration3G handset penetration

4G adoption continued uptrend

53% 55% 58% 59% 60%

1Q17 2Q17 3Q17 4Q17 1Q18

Mobile data revenue (% to mobile revenue)

17 13

Revenue(Bt bn)

3.6%

1.4%

Churn rate(/month)

7 9.2

VOU(GB/month)

184 578

ARPU(Bt/month)

Prepaid statistics in 1Q18 Postpaid statistics in 1Q18

+14%YoY

-5%YoY

+2%YoY

flat

+61%YoY+100%

YoY

7

Mobile: Build end-to-end customer satisfaction

Product differentiation

Great network quality

Strong branding

End-to-end customer engagement

Ensure proper investment and strong spectrum position

Focus on valued-product proposition

Increase brand perception in both online & teen segment

Reinforce OMNI channel and privilege

55MHz

Low- and high-band spectrum

Advanced solutions with pre-5G network planning

FMCIncrease revenue per household

Maintain level of profitable subsidies

Targeted offerings

Partner with CH3 to co-market “Love Destiny”

Zeed SIM for teenagers

5.4 6.2 7.2 8.2 8.4

26% 29% 34% 38% 39%

FY14 FY15 FY16 FY17 1Q18

Broadband users (mn)

% household peneration

FBB: Industry expanding into fibre-to-the-home

Total est.8.4mn users

Thai fixed broadband market FBB subscriber market share Industry ARPU

Maintained at around Bt600/month

39% market penetration with majority using xDSL

510541

600

637635

4Q16 1Q17 2Q17 3Q17 4Q17

ARPU (Bt/month)

Competitive fibre pricing with higher speed at same price

8

200

400

600

800

1000

0 20 40 60 80 100 120

Download speed (Mbps)

ARPU (Bt/month)

Typical package for new fixed broadband customers remained at Bt600, targeting new and ADSL users

100Mbps packages are recently affordable at below Bt1,000

Current fibre plans

39%

33%21%

7%

1Q18

Join AIS Fibre + up to 4 AIS mobile numbers, get extra privileges for a family

AIS Fibre continues to focus on quality customers

with improved acquisition rate

9

374 446 482 521 572 541

600 637 635 618

350

450

550

650

-

200

400

600

800

1,000

1,200

1Q17 2Q17 3Q17 4Q17 1Q18

72 72

36 40 51

-

50

100

1Q17 2Q17 3Q17 4Q17 1Q18

FBB subscriber (‘000)

ARPU (Baht/month)

FBB net additions (‘000)

• Acquire quality subscribers through convergence services of “Power4” and “Family Extra” packages

Free 2GBMobile data

Free call to 1 AIS number

HBO movies & series on mobile + World class cartoons at home

Get privileges forSerenade Emeraldand extra meals & movies

privileges

AIS Fibre performance

Synergy with CSL in condo segment

Focus on existing

50 cities, covering 6mn homepass

86%14%

Pure fixed broadband Convergence

AIS Fibre customers by segment

Digital services: add on variety of contents &

expand further into digital money segment

Digital contents

10

• On 5th March 2018 ,AIS, through mPAY, has entered into 33.33% stake (Bt788mn) in a joint venture with Rabbit LINE Pay, an e-Money platform that connect with Bangkok Mass Transits and is embedded in Line chat application.

• Strengthen AIS’ digital life service provider

position by leveraging customer bases, platform, channels of AIS and partners to enhance mobile money for both AIS and non-AIS customers

+2.6mn users

AIS Rabbit LINE-PayDigital contents

2 new channels including CNN and Cartoon Network, available on AIS PLAY and PLAYBOX

Continued to add value and create differentiation through digital contents

Korean series

Hollywood movies

Karaoke

On top packages: Mao Mao Entertain

+

Bt19/day512Kbps*

Bt34/day for UL 4Mbps

or

Free internet in ViU, Hook, Karaoke apps

*FUP: speed drop to 64kbps after 300MB

+45mn users +8.5mn users

available on both AIS PLAY and AIS PLAYBOX

on the go at home

18%

5%

Enterprise: CS LOXINFO Business Integration

11

Strengthen position inenterprise market

COST SYNERGY

✓ Operate CSL’s services with lower OPEX

REVENUE SYNERGY✓ Cross sell & upsell potential from larger customer

base and complementary product portfolio✓ Widen Data Center propositions and target

segments

OPERATIONAL EFFICIENCY✓ Sales & Marketing alignment✓ Leverage sale and technical expertise ✓ Align product roadmap

Expected to realize synergy in 1-2 years

Asset light models

Data center outside BKKLarge size corporate customers

Sizable corporate mobile base

Data center in inner BKKMid-size corporate customersWell-known brand with good service quality

Before M&A After M&A

Enterprise revenue market share

Bt56bnICT & Mobile enterprise

market in 2017

Lower inter. bandwidth costOwn fiber infrastructure

Economies of scale Strong and experienced sales and technical support in ICT

23%

Disclaimers

Contact usIR website: http://investor.ais.co.thEmail: [email protected]: +662 029 5014

Some statements made in this material are forward-looking statements with the relevant assumptions, which are subject to various risks and uncertainties. These includestatements with respect to our corporate plans, strategies and beliefs and other statements that are not historical facts. These statements can be identified by the use offorward-looking terminology such as “may”, “will”, “expect”, “anticipate”, “intend”, “estimate”, “continue” “plan” or other similar words.The statements are based on our management’s assumptions and beliefs in light of the information currently available to us. These assumptions involve risks anduncertainties which may cause the actual results, performance or achievements to be materially different from any future results, performance or achievementsexpressed or implied by such forward-looking statements. Please note that the company and executives/staff do not control and cannot guarantee the relevance,timeliness, or accuracy of these statements.

Digital Airtel.

1

We are Airtel#1

Operator in India

413.8 mncustomers

#2 Operator in Africa

50Bn USD Cumulative investment in Telecom

Ranked #1 by Transparency International

3rd Largest Telecom

operator in the world

Presence in 16

Countries

2/12

We are India’s #1 Operator

RMS

Leader in India Revenue & Customer Market Share

3/12

Key Pillars of Our Digital Strategy

Wynk Music Airtel TV My Airtel App Airtel Payments Bank

Full Suite of Digital Products at Scale

80 Mn+Cumulative Monthly

Active Users on our digital assets already

Mobile Advertising Platform for smart targeting

Source: App Annie, April 2018 4/12

Wynk Music in NumbersIndia’s #1 Music App

80 MnTotal Downloads

20 MnMonthly Active Users

1.5 BnMonthly Song Streams

Strong Alliances with

the biggest Music Labels

in India

Wynk 2.0 with personalization

& regional as pillars

Wynk Music

5/12

Airtel TV in NumbersIndia’s Most Downloaded

Video Streaming App in Q1 2018

50 MnTotal Downloads

20 MnMonthly Active Users

800 MnMinutes Streamed Monthly

Integrated with leading video content partners

370+Live TV

Channels

10000+Movies

and TV Shows

Re-launched with Live TV as

the core pillar

Airtel TV

6/12

Airtel TVContent Sampling

Cross Sell | Up Sell

Lock In Customers for all Future Recharges

Ensure Bundle Continuity

Airtel Payments Bank Account| Transactions

Acquisition

Care

Payments

Lifecycle

DigitalizedCustomer Journey

TouchpointsCustomer Experience & Self Care

My Airtel AppFully Serves all LOBs – Mobility, Telemedia & DTH

60% reduction in calls per customer in last two years

7/12

• Access, Microwave, Transmission

• Customer Experience Index

• Automated Root Cause Analysis

• Complaints correlated with network performance

• Fault assurance

• Performance assurance

• Service assurance

• End to end workflow automation

• Field force management

• Material Management

Planning

Deployment

Operations

Experience

Network Planning & Optimization

Network DigitisationAcross Planning, Deployment, Operations

8/12

For DistributorsReal Time Inventory & LAPU Control, transfer to FSEs

Mitra For RetailersOne of the Highest transacting

apps on Play Store

For Sales TeamPerformance Tracking and sales through KPIs

For PromotersProvides custom sales pitch to customers and track performance

For FSEsTransfer LAPU & Inventory to Retailers

Allows retailers to drive Acquisition, recharges,

verification, check commissions

Sales & Distribution Automation

Suite of Apps to power DistributionWe do more orders per day than Amazon,

Flipkart and Snapdeal combined

9/12

Airtel Devices Platform Homes PlatformOne Bill for All Connections

CatalogDevices from top OEMPartners

ServicesPostpaid Plans & Handset Insurance

Loan Offers Virtual Warehouses

Airtel OR/FR Stores

Devices and Homes Platforms

Devices and & Homes PlatformUnified Proposition for users on devices and

across all connections

10/12

Airtel Digital BrainA future ready data warehouse and learning

system to power digitization

The Airtel Digital Brain

Brain

Real Time Triggers

CRM (All LOBs)

Billing (All LOBs)

Retail

Wynk

MyAirtel

Airtel TV

Data

Customer

Network

Customer Persona

RecommendationEngine

CommsHub

Predictive Analytics

Next Best Action

Digital Advertising

Customer Lifecycle Management

Omni ChannelConsumer Experience

Data Monetization

11/12

Investment Rationale

Bharti AirtelInvestment Rationale

1Presence in underpenetrated markets of India and Africa with large residual opportunity

2Leading operator with scale and diversified businesses across markets

3Bulk investments already in place; best in class spectrum bank in markets of operations

4 Demonstrated superior execution capabilities

5Strong balance sheet enabling ample headroom for expansion

6Experienced management, diversified board, marquee partners and shareholders; highest standards of corporate governance 12/12

Singtel Investor Day13 June 2018 | The St. Regis Singapore

Key Investment Thesis

As the Filipinos’ preferred brand for digital lifestyles, Globe is reaping the benefits of the robust growth in data services

2

Fixed broadband provides new catalysts for growth, given low penetration and growing demand for home broadband

Expanding avenues of growth through prudent investments into adjacencies in the digital space

Remaining focused towards creating greater corporate value via efficient capital management

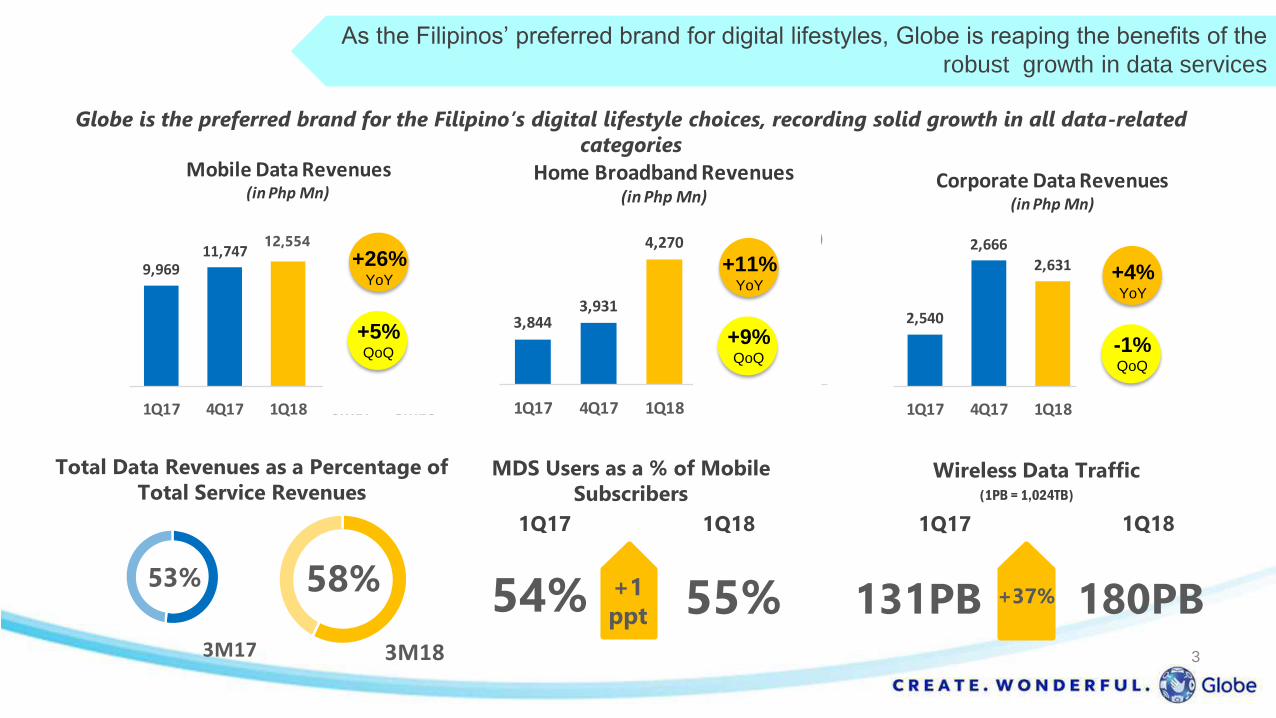

12,302 9,969

12,302 11,747 9,969

3M183M171Q184Q171Q17

Mobile Data Revenues(in Php Mn)

3M17

2,631

2,540

2,631

2,666

2,540

3M183M171Q184Q171Q17

Corporate Data Revenues(in Php Mn)

4,270

3,844

4,270

3,931 3,844

3M183M171Q184Q171Q17

Home Broadband Revenues(in Php Mn)

3M18

As the Filipinos’ preferred brand for digital lifestyles, Globe is reaping the benefits of the

robust growth in data services

Globe is the preferred brand for the Filipino’s digital lifestyle choices, recording solid growth in all data-related

categories

Total Data Revenues as a Percentage of

Total Service Revenues (1PB = 1,024TB)

58%53%

Wireless Data Traffic

131PB 180PB+37%

1Q17 1Q18

MDS Users as a % of Mobile

Subscribers

54% 55%+1

ppt

1Q17 1Q18

+4%

3

+5%QoQ

+26%YoY

+9%QoQ

+11%YoY

-1%QoQ

+4%YoY

12,554

We bring new innovations and partnerships to remain relevant to data users, being the preferred mobile

brand for data services

ENTERTAINMENT SOCIAL NETWORKINGMUSIC

SPORTS

Get 30 days of

Spotify Premium

for only P129!

Spotify is also

available with the

new Tattoo home

broadband plans.

Spotify

GAMES

Games BundleStep into the exciting worlds of

Clash of Clans, Clash Royale,

Candy Crush and more!

With Unlichat, you can

enjoy all-day use of

Viber, FB Messenger,

Kakao, GMessage and

other major chat apps

like LINE & WeChat!

No need for a WIFI

connection to use all

these!

UNLICHAT

As the Filipinos’ preferred brand for digital lifestyles, Globe is reaping the benefits of the

robust growth in data services

4

Content Partnerships

Watch the regular season,

NBA All-Star, Playoffs,

Finals, and on-demand

NBA Hardwood Classics

on your tablet, mobile, or

desktop.

We provide superior data experience to our customers through continuous investments in our data network

As the Filipinos’ preferred brand for digital lifestyles, Globe is reaping the benefits of the

robust growth in data services

Roll-out of LTE frequencies in full swing Home Broadband roll-out

• As of April, Globe deployed 934 more LTE sites for increased

capacity and coverage.

• Deployment ramping up progressively, targeting sites with

high demand.

• Per Opensignal’s latest report on Philippine operators, Globe

consistently rates highest in 3G and LTE service availability

both on a regional and nationwide basis.

• In 1Q18, rolled out an additional 59,000 lines with remainder

to be deployed progressively

Globe deploys massive MIMO technology

• Globe deploying massive MIMO technology which utilizes LTE

spectrum to accommodate more users at higher data rates

with better reliability.

Fast-tracking the roll-out of LTE service

using frequencies from SMC deal

Globe in talks with third parties for creation

of independent tower companyGlobe launches WiFi service in

MRT and LRT Stations

5

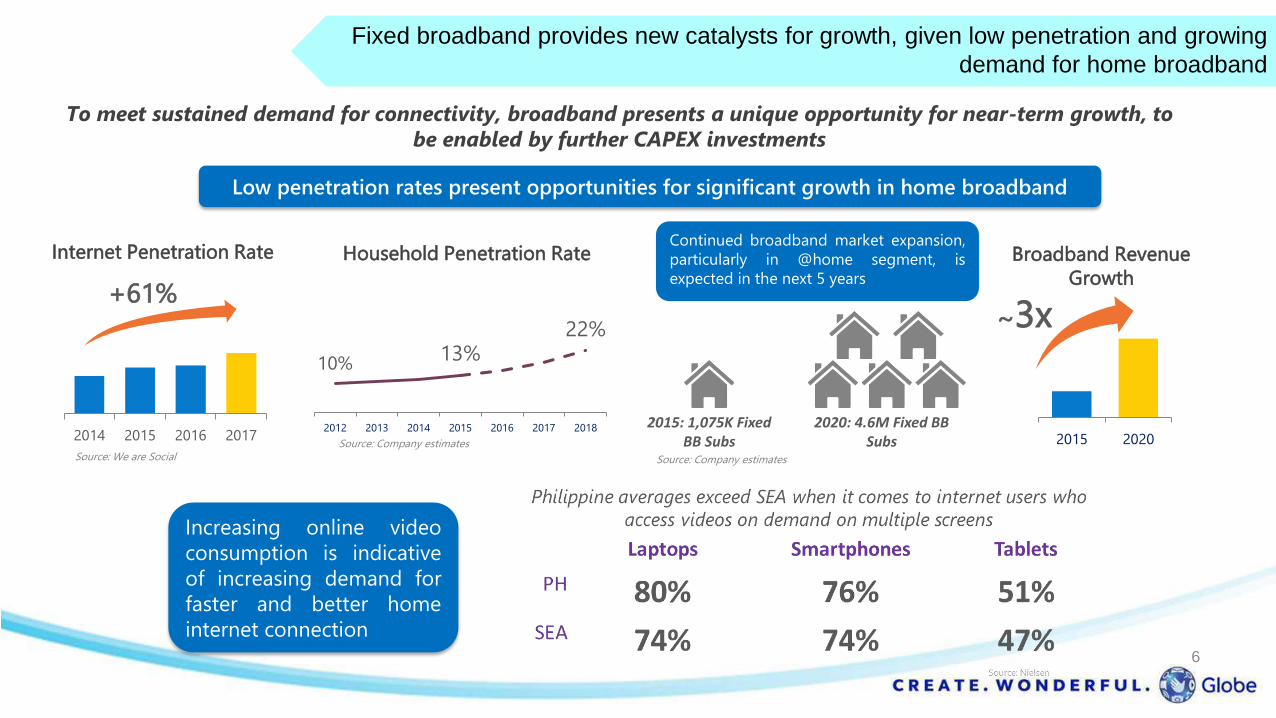

To meet sustained demand for connectivity, broadband presents a unique opportunity for near-term growth, to

be enabled by further CAPEX investments

10%13%

22%

2012 2013 2014 2015 2016 2017 2018

Low penetration rates present opportunities for significant growth in home broadband

Household Penetration RateContinued broadband market expansion,

particularly in @home segment, is

expected in the next 5 years

Source: Company estimates

2015: 1,075K Fixed BB Subs

2020: 4.6M Fixed BB Subs 2015 2020

Broadband Revenue

Growth

~3x

Fixed broadband provides new catalysts for growth, given low penetration and growing demand for home broadband

Increasing online video

consumption is indicative

of increasing demand for

faster and better home

internet connection

Source: We are Social

2014 2015 2016 2017

Internet Penetration Rate

+61%

6

Source: Company estimates

Evolving from traditional telco services, we are establishing the building blocks in adjacent spaces to ensure

continued growth in the world of data

• 24/7 health hotline service available nation-wide for all mobile

customers.

• Call anytime, anywhere in the Philippines

• Connect with licensed doctors

• Flexible, affordable plans

• Partnered with Mexican telephone medical assistance firm Salud

Interactiva, a leader in the health hotline space

• Over 230,000 subscribers acquired

Financial Services Telehealth

Expanding avenues of growth through prudent investments into adjacencies in the digital space

• Mynt is Globe’s Fintech service that addresses

financial inclusion through mobile money, micro-

loans and technology

• In Sept. 2017, Ant Financial (Ant) and Ayala

Corporation (Ayala) entered into a strategic

partnership with Globe and invested into Mynt

• At closing, Globe and Ant each held 45% with

Ayala 10%

• Mynt customer base of 5.1 million with

monthly transaction value of Php 6 Billion

• Fuse offers personal and business loans

using an alternative credit scoring model

with 66,000 total number of loans

disbursed

No bank accounts

or formal means

to save money

70%No credit score,

making it difficult

to secure a loan

90%Daily interest rate

charged by

informal lenders

20%Cities and

municipalities with

no physical banks

40%

7

National average

of doctors to

patients

3.5:10,000Percentage of

licensed physicians

who are active

54%

Digital and Mobile Advertising

Evolving from traditional telco services, we are establishing the building blocks in adjacent spaces to ensure

continued growth in the world of data

Business Incubation / Venture Capital

#startupPH #area55 #raidthefridge

• AdSpark‘s mission: To accelerate digital and mobile advertising in the Philippines.

• AdSpark works closely with both top brands and advertising agencies, providing expert and

customized digital and mobile advertising solutions for the SME market.

• AdSpark intends to capitalize on the emerging digital lifestyle of a predominantly young Filipino

population where mobile advertising only accounts for a meager share of total industry ad spend

• Kickstart’s mandate is to (1) source innovation;

(2) nurture early-stage startups to scale; and (3)

invest for portfolio return.

• Fund 1 = Php150M; Fund 2 = up to USD50M

• Investment portfolio focused on delivering

solutions for e-lifestyle, e-commerce, B2B,

software-as-a-service (SaaS), and social impact

Expanding avenues of growth through prudent investments into adjacencies in the digital space

8

Consolidated Financial Highlights

* OPEX & Subsidy includes interconnect expenses

** Core NIAT excludes forex, mark-to-market gains and losses, and non-recurring items

*** Beginning 2018, Globe adopted PFRS 9 and PFRS 15 for financial reporting purposes

Remaining focused towards creating greater corporate value via efficient capital management

9

32.136.7

42.5

6.6

2015 2016 2017 3M18

Gross debt at Php127.9 Billion, remains within covenant ratios

Historical CAPEX Breakdown

Covenant = 3:1

Covenant = 2.5:1

Gross Debt

Gross Debt/Equity

Gross Debt/EBITDA

CAPEX

Remaining focused towards creating greater corporate value via efficient capital management

105,729 131,529 127,850

2016 2017 3M18

1.67

1.98 1.96

2016 2017 3M18

2.15

2.43

2.25

2016 2017 3M18

15% 15% 11% 7%20%

10% 8% 10% 9%

14%27% 30%

14%2%

2%

49% 48%65%

82%64%

2014 2015 2016 2017 3M18

Business Support Others Core Data10

Cash Dividends: Sustained commitment to delivering value to our shareholders

Cash Dividend per

Common Share:Php 22.75

Record Date: May 21, 2018

Payment Date: June 1, 2018

2Q18 Dividend: Key Information

800

2702

1533

2010 2011 2012 2013 2014 05/06/2015 2015 2016 2017 25/05/2018

Historical Share Price

All-time high

Remaining focused towards creating greater corporate value via efficient capital management

11

12,095 12,092 11,682 11,017 9,953

2018*2017201620152014

Dividends Paid(in Php Mn)

* Annualized

Disclaimer

This presentation contains certain forward-lookingstatements. These forward-looking statements generally canbe identified by the use of statements that include words orphrases such as Globe or its management “believes,”“expects,” “anticipates,” “intends,” “plans,” “foresees,” orother words or phrases of similar import. Similarly,statements that describe Globe’s objectives, plans or goalsare also forward-looking statements. All such forward-looking statements are subject to certain risks anduncertainties that could cause actual results to differmaterially from those contemplated by the relevantforward-looking statements.

12

S I N G T E L

I N V E S T O R D A Y

2 0 1 8

Singapore, 13 June 2018

A l i s t a i r J o h n s t o n

H e r i S u p r i a d i

1

TABLE OF CONTENTS

1 T E L K O M S E L

P E R F O R M A N C E

2 I N D O N E S I A D I G I T A L T R E N D S

3 T E L K O M S E L

D I G I T A L I N I T I A T I V E S

2

TELKOMSEL

Performance

3

4

Company’s Profile

Main Products

• Started operations in 1995, Telkomsel is the subsidiary of PT Telekomunikasi Indonesia Tbk (65%) and Singapore Telecom Mobile Pte Ltd (35%)

• Within 23 years, Telkomsel has established itself as the leading cellular operator in Indonesia with 193 million customers and more than 5,400 employees

• It has the widest network coverage with more than 167,600 BTS On-Air covering ± 99% of population

TELKOMSEL IN BRIEF

Positioned as the postpaid brand of

choice for professionals and corporate

customers segment

Positioned as the prepaid brand for

the savvy middle class segment

Positioned as an affordable and value

prepaid brand for the mid-low segment

Positioned as youth segment prepaid

brand with focus on offering attractive

Data and Digital Services

Key Performances 2015-2017

2015 2016 2017

Revenuesin trillion Rupiah

76.1

86.793.2

+7.5%

2015 2016 2017

42.6

49.853.6

EBITDA & EBITDA Marginin trillion Rupiah

+7.7%

EBITDA

Margin

56.0%57.4%

57.5%

Net Income & Net Income Marginin trillion Rupiah

2015 2016 2017

22.4

28.230.4

NI

Margin

29.4%32.5%

32.6%

+7.8%

2015 2016 2017

Total Customer Basein million

152.6

173.9

196.3

+12.9%

2015 2016 2017

Total BTS On-Air & Total 3G/4G BTSin thousand

103.3

129.0

160.7

+24.5%

3G/4G

BTS

54.9

78.7

110.4

4

5

Indonesia Telco Industry Overview

Population Coverage: ± 99% with 3G Coverage: ± 85% & 4G Coverage: ± 80%

Sumatera

CB portion: 27%

Greater Jakarta &

West Java

CB portion: 24%

Java & Bali

CB portion: 28%

Papua, Maluku,

Sulawesi, Kalimantan

CB portion: 21%

Mature industry with estimated 135% SIM-card penetration (±75% population-based). Rapidly shifting dynamics industry with transition of Legacy to Data services

Growing Data Business with around 70% of which were 3G/4G BTS and 59% 3G/4G

capable device penetration

Tremendous growth in Digital Business with Data traffic and Data revenue grew by 146% and 21% YoY, respectively in 1Q-2018

TELKOMSEL IN BRIEF

5

REVENUES

In Million

YEAR-ON-YEAR

In TrillionCAPEX

TOTAL ASSET BTS ON AIRIn Thousand

CUSTOMER In Trillion

Legacy

DigitalBusiness

EBITDA NET INCOMEIn TrillionIn Trillion

Margin

55%59%

Margin

29%35%

In Trillion

Accelerated transition of Legacy to Data Services & continuous intense competition landscapeTSEL was able to still booked a substantial amount of Revenues, EBITDA & Net Income

PERFORMANCE HIGHLIGHTS 1Q-2018

-1%

13.911.4

8.410.5

1Q17 1Q18

22.3 21.9

-1.9%

+24.8%

-18.1% 1Q17 1Q18

-9.2%

13.2

12.0

1Q17 1Q18

7.7 6.4

-16.7%

1Q17 1Q18

2.83.6

+27.6%

1Q17 1Q18

-1.0%

92.9

91.9

1Q17 1Q18

169.4

192.8

+13.8%

1Q17 1Q18

136.1167.6

+23.2%

6

DIGITAL BUSINESS

REVENUEIn MillionIn Trillion

DATA USER DATA TRAFFIC In PB

3G/4G CAPABLE

DEVICE In Million

3G & 4G BTS

ON AIR In Thousand

Digital Business:

Continue to Focus on Digital BusinessEngine of growth and accounted for 48% of Total Revenues

PERFORMANCE HIGHLIGHTS 1Q-2018

0.8 1.3

7.69.2

1Q17 1Q18

Digital Services

Broadband

8.410.5

+24.8%

+20.8%

+61.1%

1Q17 1Q18

89.6108.7

+21.3%

1Q17 1Q18

357.4

878.5

+145.8%

1Q17 1Q18

83.8

113.3

+35.2%

75.2 82.2

11.1

35.1

1Q17 1Q18

3G

4G

86.3

117.3

+35.9%

YEAR-ON-YEAR

+215.5%

+9.4%

7

EBITDA (Rp.Tn)

Customer Base (Mn)

Net Income (Rp.Tn)

12%

Margin

17%

Cellular Revenue (Rp.Tn)

12%

Margin

1Q17 1Q18 1Q17 1Q18

1Q17 1Q18 1Q17 1Q18

4G

3G

2G

1Q17 1Q18 1Q17 1Q18

1Q17 1Q18 1Q17 1Q181Q17 1Q18

ARPU (Rp.000)

43 35 33 3022 12

BTS On Air (000)

17% 17%

BTS Addition (000)

1Q17 1Q18 1Q17 1Q181Q17 1Q18 1Q17 1Q18

1Q17 1Q18

TSEL

69%

ISAT

14%

XL

17%

Rev

share

+1.6ppt

Industry Growth (BIG-3) -5.4%

1Q17 1Q18

59% 55% 35% 36%43% 34%

TSEL

56%ISAT

28%

XL

16%

-2.5ppt

+0.5ppt

Marketshare

Industry Growth (BIG-3) +9.7%

+2.5ppt

+2.0ppt

35% 29% 1% 0%

-4.1ppt

1Q17 1Q18 1Q17 1Q18

3% -8%

1Q17 1Q18

BIG 3 PERFORMANCE (1Q-2018 YoY)

22.3 21.9

-1.9%

6.14.4

-27.0%

5.3 5.5

+4.5%

13.2 12.0

-9.2%

3.1 1.9

-37.3%

1.8 2.0

+7.5%7.7

6.4

-16.7%

0.2

-0.5

-320.5%

0.0 0.0

-66.8%

169.4192.8

+13.8%

95.6 96.2

+0.6%

48.0 54.5

+13.5%

136.1

167.6

+23.2%

8%

55%

37%

21%

49%

30%

58.2

64.4

+10.7%

9%

49%

42%

14%

48%

38%

87.6

105.8

+20.7%

12%

45%

43%

19%

45%

36%

7.1

6.9

-1.6%

100%

68%

41%

-8%

100%1.7

3.0

+78.4%

43%46%10%

61%

29%10%

3.2

4.7

+48.5%

67%

32%1%

59%

42%

-1%

8

Revenue Inline with or slightly above market growth

EBITDA Margin Slightly decline compared to last year

BTS roll out Focus on 4G roll out

CAPEX Approximately 15-17% over revenue

2018 GUIDANCE

9

Indonesia

Digital Trends

10

In 2017, invested money in Start

Up

$ 2,932 Miorising 60x larger than 2016

Start Up Market

E-commerce industry growth for the last 4 years+38%

Total E-Commerce Sales reached in 2017$7.1Bio

Financial Technology(Fintech) players in Dec 2017>230

By going digital, Indonesia can unleash the next level

of economic growth – to the tune of $ 150 Bio in

annual economic impact by 2025

Indonesia – An emerging market with digital growth potential

*source:

CBInsights (Sept’2017), DBSInsight (2018),

Katadata (2018), McKinsey&Company

(Oct’2016), Fintech Indonesia (2018) 11

TELKOMSEL

Digital

Initiatives

12

Digital Business

Solutions

Digital Channel

Video Music Games Tcash Tap & QR

Big Data Internet of Things Digital Advertising Enterprise Solutions

MyTelkomsel Apps Telkomsel.com LOOPKita Apps

Digital Lifestyle

TELKOMSEL Continued To Transform All Aspects Of The Digital Business To Become A Digital Telco Company And Leading Mobile Digital Business

13

MyTelkomsel App becomes the best selfcare app in Indonesia and will

focus to expand from only feature delivery to business driven execution

STR

ATG

Y &

IN

ITIA

TIV

ES

• FEATURES AND UI/UX Continue Improve

MyTsel UI/UX based on UI/UX heuristic

benchmarks

• TACTICAL TRADITONAL CHANNEL ACTIVITIES through traditional channels ( Grapari, UMB,

Email etc ) and tactical events

• PRODUCT AND OFFERS Offering introductory

products and personalized Offers to drive app

adoption

• PARTNERSHIP collaboration with 3rd

parties to give more Values.

• DIGITAL MARKETING drive awareness and

engagement on digital marketing channel

• TECHNOLOGY AND CORE PLATFORM enhance

scalability, capability and performance at

current technology infrastructure

ACHIEVEMENTS

WH

AT

WE H

AV

E D

ON

E

KEY MILESTONE

The Best Customer Self

Service App

(Selular Award 2018)

53.5 MioDownloaders

3.7 MioPackage User

11.6 MioActive User

14

Video - The strategy is to increase relevancy and utility of VideoMAX and

shift portion of video payload into VideoMAXW

HA

T W

E H

AV

E D

ON

E

Partners

STR

ATG

Y &

IN

ITIA

TIV

ES

• With MAXStreamcapability to playout, portion of youtube is expected to go lower. MAXStream to

contribute 14% of video payload in Q1’19

• By increased of utility of VideoMAX and numbers of MAXStream users, it becomes

opportunity for us to monetize thru add-on package

• Engagement with device manufacturer, smartTV, and setup box will be established as well

Present:

Next:

Launched Maxstream on

5 Jun’18

Maxstream is a video application that features thousands of movies, TV shows and Cartoons as well as offers wide range of attractive VideoMax package

15

GAMES - Telkomsel Plays In Payment, Direct Distribution, E-Sport And Media

Along The Game's Value ChainW

HA

T W

E H

AV

E D

ON

E

STR

ATG

Y &

IN

ITIA

TIV

ES

D. E-Sport..

A. Telco Billing..

B. Dataplan Bundling..

C. Platforms - Dunia Games..

Event Stadium Team

A. Payment

B. Direct Distribution

C. Marketing and Media | Media

D. Marketing and Media | e-Sport

• Provides payment infrastructure for moving cash into the game ecosystem.

• Distribute games and its items to the users.

• Create or distribute media content

• Organize, host and market gaming tournaments online and offline

16

LangitMusik - Has introduce Multimedia experience through video W

HA

T W

E H

AV

E D

ON

E

STR

ATG

Y &

IN

ITIA

TIV

ES

A. Langit Musik

B. MusicMax

C. RBT

A. Langit Musik

B. MusicMax

C. RBT

• Introduce Multimedia experience through Video on LM (Live Streaming

and Interactive)

• Introduce Data Quota special to access Music Apps

• Expand to Bundle with Premium (Joox VIP+1GB)

• Maintain positive YoY growth on Digital Era

• Introduce various RBT improvement : Pricing, Smart Campaign, etc.

• Continue to enhance LM platform with introduce : UGC capability, distribute to 3rd Party, etc.

• Start to monetize through new revenue stream: Ads, In Apps Purchase, Pay Per View, etc.

• More partnership with Global Partner (Spotify, Tidal, etc)

• Modify Quota with bundle All Access Data

• Introduce Video RBT to bring RBT to Digital Era

• Develop UGC capability on RBT to acquire more millennials user.

17

THANK

YOU!

18

Related Documents