Resetting the Table Downstream U.S. refinery crude slate implications of the NA Crude Boom Oil & Gas Strategies Summit The Plaza, New York May 21, 2014 Michael W. Leger, President

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Resetting the Table Downstream U.S. refinery crude slate implications of the NA Crude Boom

Oil & Gas Strategies Summit The Plaza, New York

May 21, 2014

Michael W. Leger, President

• International consulting practice since 1971

• Downstream focus; refinery engineers/analysts

• Industry and financial clients

• Outlook and forecast products - Crude & Refined Products Outlook - Refinery Construction Outlook - NA & World Crude Outlooks - Rebalancing Crude & Products Worldwide – Sept. ‘14

• Special Studies

About TM&C

2

• Regional forecasts in new TO and conventional areas

• Refinery capabilities on a plant-by-plant basis

• Planned/required logistics

• Challenges & opportunities up, mid and downstream

• Rebalances crude & products worldwide

• Forecasts pricing implications

• Available September 2014

2014 NA Crude & Condensate Outlook

3

A Historical Perspective

4

1970s & 1980s

• U.S. crude production in decline – ANS an exception

• Incremental crude was Saudi Lt. and Med. • Oil embargo and demand declines due price

increase result in sharp decline in imports • Saudi prominence rebounds in late 80s as

demand increases and U.S. production decreases

5

1990s and (early) 2000s

• Increasing production of Latin & Canadian heavies result in refinery crude slate shifts

• Significant investment in heavy processing as

U.S. refiners viewed heavy crude as the future – Joint ventures formed in the late 1980s into the 1990s, to secure a

market for some of these difficult to process Latin American heavies – Projects birthed to process Canadian bitumen – Coking capacity grew by more 800 MBPD between 1990 and 2005

6

U.S. Production/Import History

0

2

4

6

8

10

12

1970 1975 1980 1985 1990 1995 2000 2005

Mill

ion

BPD

U.S. Crude Oil Imports

U.S. Crude Oil Production

Alaska North Slope begins production

U.S. Production peaks in 1970

Decline in production, coupled with increasing demand is made up with imports

Alaska North Slope peaks in 1988, begins to decline

U.S. oil consumption begins to fall

Saudis flood market with inexpensive oil. Oil glut takes hold in following years, causes rapid decrease in oil price.

In coming decades, US oil production continues to fall, while demand increases. Imports grow.

Demand peaks around 2005, falls in 2008-2009 due to recession

7

2009

U.S. Crude Slates in Transition

8

Driven by Increasing Domestic Supply

4

5

6

7

8

9

10

1960 1970 1980 1990 2000 2010

Mill

ion

BPD

U.S. Oil Production Peaks in 1970

Alaska North Slope Production Comes Online, Peaks 1988

Despite rising Demand, U.S. Production Falls

Decline Reverses, Rapid Rise in Production

9

N.A. Crude Production

• U.S. production up by over 3 MMBPD since 2008 • Reverses 20+ year trend of declines • Increases dominated by onshore tight oil production; mostly light/sweet • Causing a shift in the U.S. refinery crude slates, reversing heavy/sour trend

• Canadian crude on upward trend for three decades

• Growth accelerating - up by 1 million BPD in last five years • Largest reserve base in the world/unconventional resources • Mostly heavy/sour but production gains not as large as U.S.

• Increases driven by higher prices and technology advances

(fracking, horizontal drilling, in-situ extraction, etc.)

10

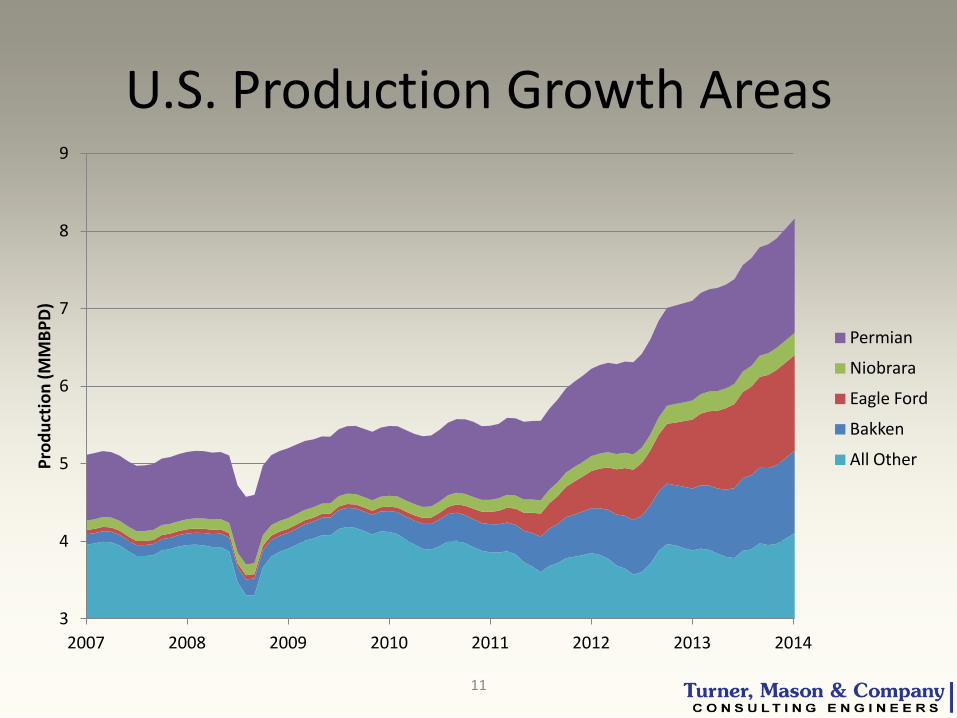

U.S. Production Growth Areas

3

4

5

6

7

8

9

2007 2008 2009 2010 2011 2012 2013 2014

Prod

uctio

n (M

MBP

D)

Permian

Niobrara

Eagle Ford

Bakken

All Other

11

Changing U.S. Refinery Crude Slates 1985-2014

0.6

0.8

1.0

1.2

1.4

1.6

30.0

30.5

31.0

31.5

32.0

32.5

1985 1990 1995 2000 2005 2010

Sulfu

r, w

t. %

Gra

vity

, API

Domestic Lights Latin American & Canadian Heavies Middle

Eastern Design

Basis ->

12

2013 U.S. Refinery Crude Slate

40%

6% 3% 5% 2%

10%

14%

9%

11% Domestic Light Domestic Medium Domestic Heavy Canadian Light Canadian Medium Canadian Heavy Foreign Light Foreign Medium Foreign Heavy

13

2013 U.S. Refinery Crude Slate

14

Foreign: 5.2 MMBPD

Canadian: 2.6 MMBPD

Domestic: 7.5 MMBPD

Total: 15.3 MMBPD

6.1

< 1.0 0.5

Domestic Light

Domestic Medium

Domestic Heavy

0.8

0.3 1.5

Canadian Light Canadian Medium Canadian Heavy

49%

17%

34%

Domestic Canadian Foreign

2.2

1.3

1.7 Foreign Light

Foreign Medium

Foreign Heavy

2013 U.S. Refinery Crude Slate PADD III

Domestic Light Domestic Medium Domestic Heavy Canadian Light Canadian Medium Canadian Heavy Foreign Light Foreign Medium Foreign Heavy

PADD I PADD IV

PADD V PADD II

15

78% Light Crude

61% Light Crude

56% Light Crude 56% Light Crude

56% Light Crude

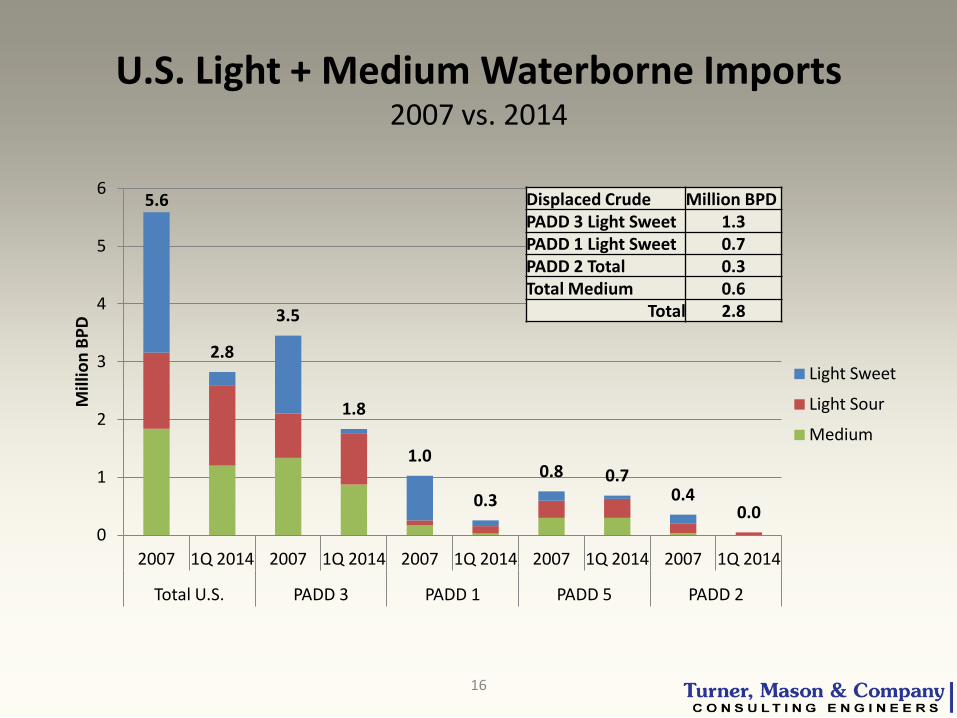

U.S. Light + Medium Waterborne Imports 2007 vs. 2014

16

5.6

2.8

3.5

1.8

1.0

0.3 0.8 0.7

0.4 0.0

0

1

2

3

4

5

6

2007 1Q 2014 2007 1Q 2014 2007 1Q 2014 2007 1Q 2014 2007 1Q 2014

Total U.S. PADD 3 PADD 1 PADD 5 PADD 2

Mill

ion

BPD

Light Sweet

Light Sour

Medium

Displaced Crude Million BPD PADD 3 Light Sweet 1.3 PADD 1 Light Sweet 0.7 PADD 2 Total 0.3 Total Medium 0.6

Total 2.8

A Look Ahead

17

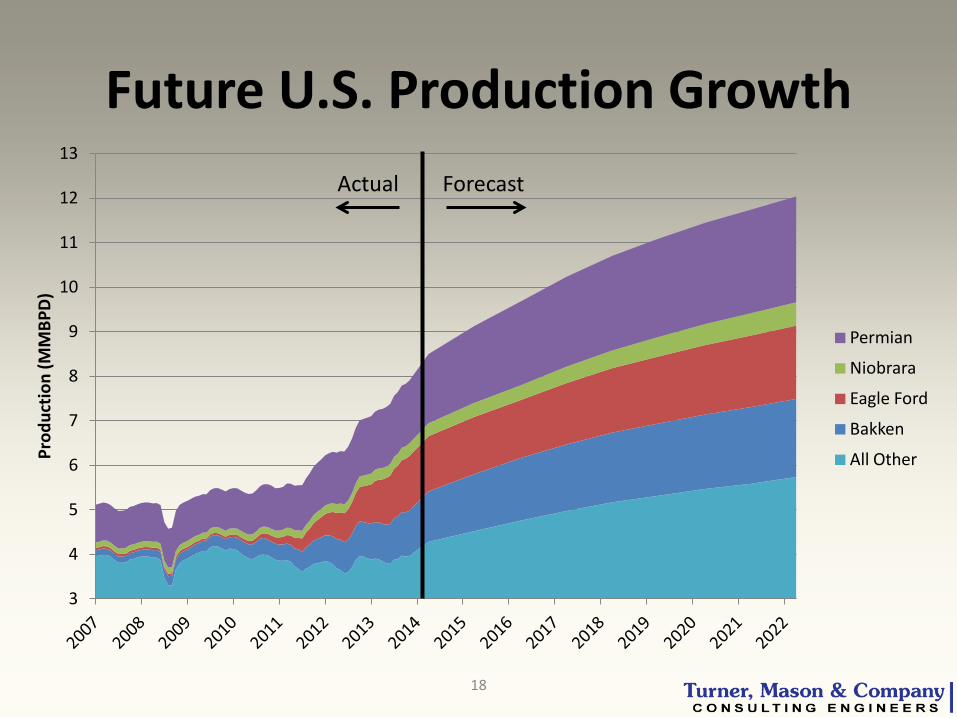

Future U.S. Production Growth

3

4

5

6

7

8

9

10

11

12

13

Prod

uctio

n (M

MBP

D)

Permian

Niobrara

Eagle Ford

Bakken

All Other

18

Actual Forecast

Crude Production Changes by PADD 2013 to 2022

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

PADD I PADD II PADD III PADD IV PADD V

Thou

sand

BPD

Low High

19

Canadian Production Forecast

20

0

1

2

3

4

5

6

Mill

ion

BPD

Eastern

Western Heavy

Western Light+Med

North American Crude Production Forecast Assumptions

• U.S. production = 12 MMBPD by 2022 – Predominantly light sweet; growth mostly in PADDs 2 and 3 – Declines in Alaska & California to continue

• Canadian production = 5.5 MMBPD by 2022 – Primarily heavy production from Western oil sands – Increasing access to tidewater is key

• XL needed to get heavy to USGC • Multiple P/L’s being developed (including XL); significant opposition • Rail proceeding; will be important if P/L’s not built

– All foreign crude imports (including the U.S. ) will be eliminated • Assumptions

– Dated Brent in $80 - $120 range – Limited production from some high potential prospects – Logistical assets built to move crude to markets

• Energy East and TransMountain expansion projects completed by 2020 • Keystone XL/Alberta Clipper/rail allow sufficient access to the U.S.

– Requires significant exports; assumes these are eventually allowed

21

Change in Crude Production by Grade 2013-2020

0

500

1000

1500

2000

2500

3000

3500

4000

Light (>31 API) Medium (24-31 API) Heavy (<24 API)

Thou

sand

BPD

Canada U.S.

22

2020 U.S. Refinery Crude Slate

51%

11%

4% 3%

22%

< 1%

< 1%

8% Domestic Light Domestic Medium Domestic Heavy Canadian Medium Canadian Heavy Foreign Light Foreign Medium Foreign Heavy

23

2020 U.S. Refinery Crude Slate

24

0.4

3.4

Canadian Medium Canadian Heavy

66%

25%

9%

Domestic Canadian Foreign

0.1 0.1

1.2

Foreign Light Foreign Medium Foreign Heavy

7.9

1.8

0.6

Domestic Light Domestic Medium Domestic Heavy

Foreign: 1.4 MMBPD

Canadian: 3.8 MMBPD

Total: 15.6 MMBPD

Domestic: 10.3 MMBPD

2020 U.S. Refinery Crude Slate PADD III

Domestic Light Domestic Medium Domestic Heavy Canadian Light Canadian Medium Canadian Heavy Foreign Light Foreign Medium Foreign Heavy

PADD I

PADD II

PADD IV

PADD V

25

80% Light Crude 52% Light Crude

56% Light Crude 52% Light Crude

46% Light Crude

2020 U.S. Refinery Crude Slate

26

0

2

4

6

8

10

12

2013 2020 2013 2020 2013 2020

Domestic Canadian Foreign

Mill

ion

BPD

Light

Medium

Heavy

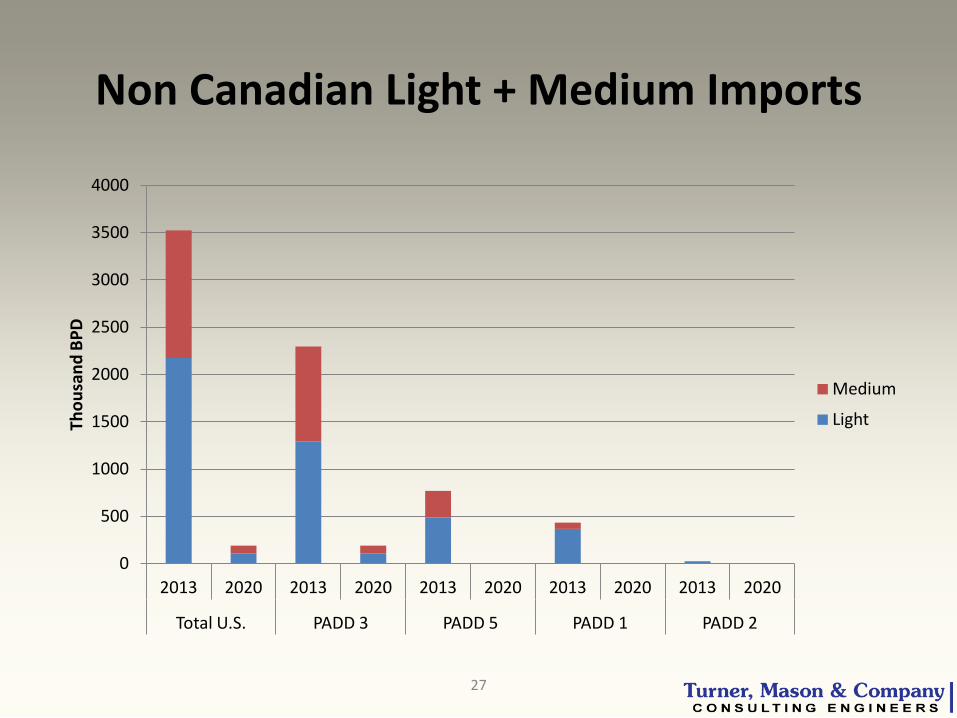

Non Canadian Light + Medium Imports

27

0

500

1000

1500

2000

2500

3000

3500

4000

2013 2020 2013 2020 2013 2020 2013 2020 2013 2020

Total U.S. PADD 3 PADD 5 PADD 1 PADD 2

Thou

sand

BPD

Medium

Light

28

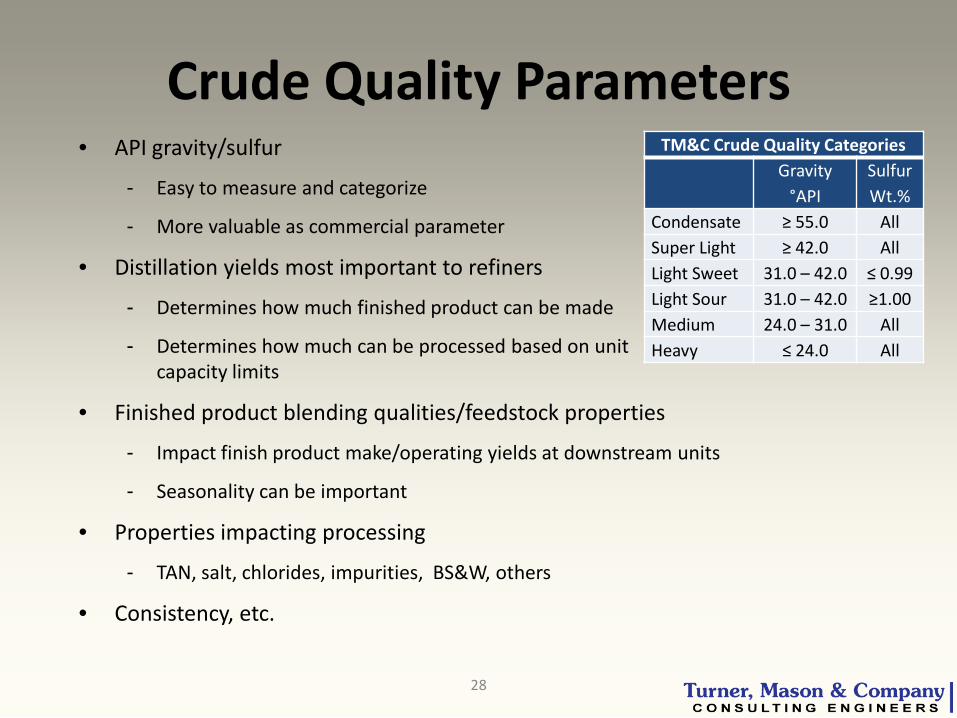

Crude Quality Parameters • API gravity/sulfur

- Easy to measure and categorize

- More valuable as commercial parameter

• Distillation yields most important to refiners

- Determines how much finished product can be made

- Determines how much can be processed based on unit capacity limits

• Finished product blending qualities/feedstock properties

- Impact finish product make/operating yields at downstream units

- Seasonality can be important

• Properties impacting processing

- TAN, salt, chlorides, impurities, BS&W, others

• Consistency, etc.

TM&C Crude Quality Categories Gravity

°API Sulfur Wt.%

Condensate ≥ 55.0 All Super Light ≥ 42.0 All Light Sweet 31.0 – 42.0 ≤ 0.99 Light Sour 31.0 – 42.0 ≥1.00 Medium 24.0 – 31.0 All Heavy ≤ 24.0 All

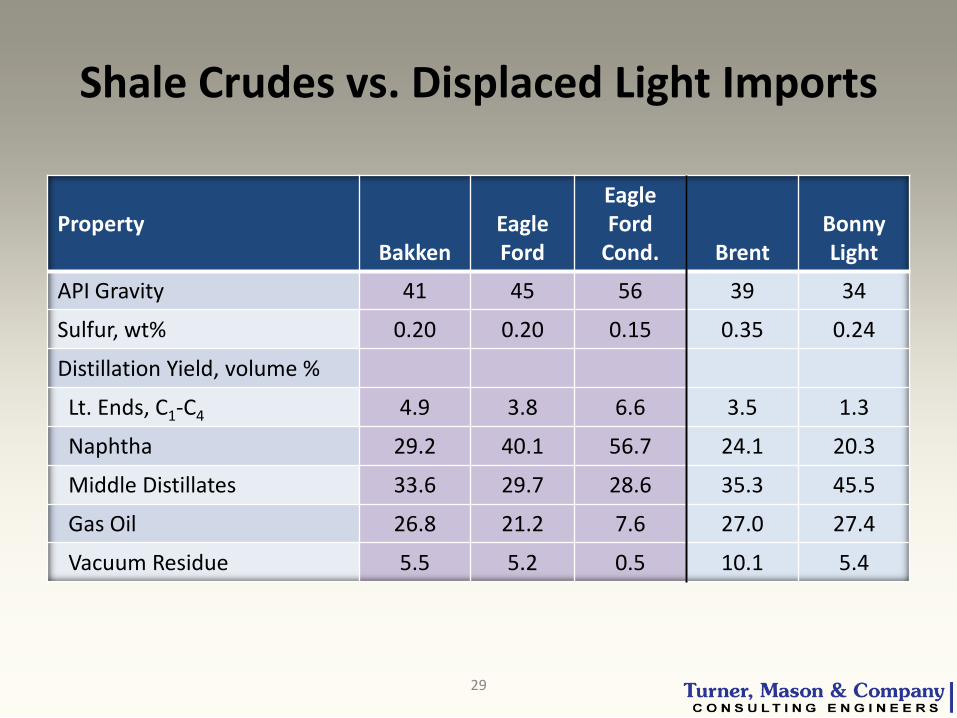

Shale Crudes vs. Displaced Light Imports

Property

Bakken

Eagle Ford

Eagle Ford

Cond.

Brent

Bonny Light

API Gravity 41 45 56 39 34

Sulfur, wt% 0.20 0.20 0.15 0.35 0.24

Distillation Yield, volume %

Lt. Ends, C1-C4 4.9 3.8 6.6 3.5 1.3

Naphtha 29.2 40.1 56.7 24.1 20.3

Middle Distillates 33.6 29.7 28.6 35.3 45.5

Gas Oil 26.8 21.2 7.6 27.0 27.4

Vacuum Residue 5.5 5.2 0.5 10.1 5.4

29

Canadian Heavy vs. Latin Heavies

Property

Canadian

Heavy (Current)

Canadian

Heavy (2020)

Mexican

Maya

Venez. Merey

API Gravity 20.3 20.3 20.5 16.0

Sulfur, wt% 3.4 3.5 3.7 2.5

TAN, mg KOH/gm 1.15 1.50 0.20 0.70

Distillation Yield, volume %

Lt. Ends, C1-C4 2.7 4.9 0.9 0.1

Naphtha 14.0 14.9 16.0 7.1

Middle Distillates 21.7 17.8 23.1 24.1

Gas Oil 33.7 31.2 27.0 34.2

Vacuum Residue 27.8 31.1 33.0 34.5

30

Implications for Refiners

31

32

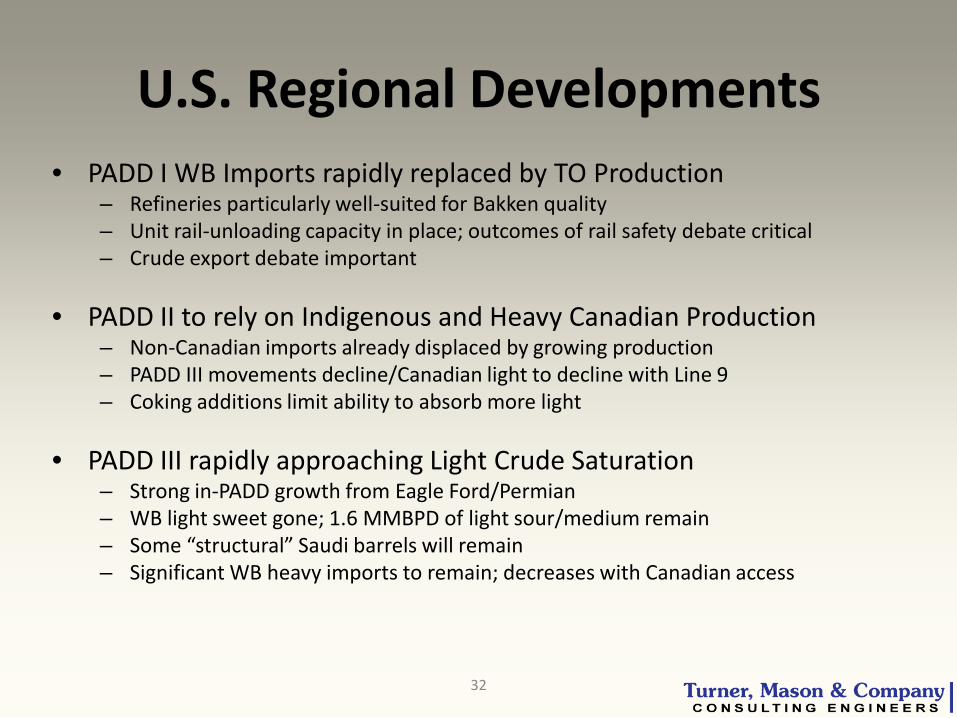

U.S. Regional Developments • PADD I WB Imports rapidly replaced by TO Production

– Refineries particularly well-suited for Bakken quality – Unit rail-unloading capacity in place; outcomes of rail safety debate critical – Crude export debate important

• PADD II to rely on Indigenous and Heavy Canadian Production

– Non-Canadian imports already displaced by growing production – PADD III movements decline/Canadian light to decline with Line 9 – Coking additions limit ability to absorb more light

• PADD III rapidly approaching Light Crude Saturation – Strong in-PADD growth from Eagle Ford/Permian – WB light sweet gone; 1.6 MMBPD of light sour/medium remain – Some “structural” Saudi barrels will remain – Significant WB heavy imports to remain; decreases with Canadian access

33

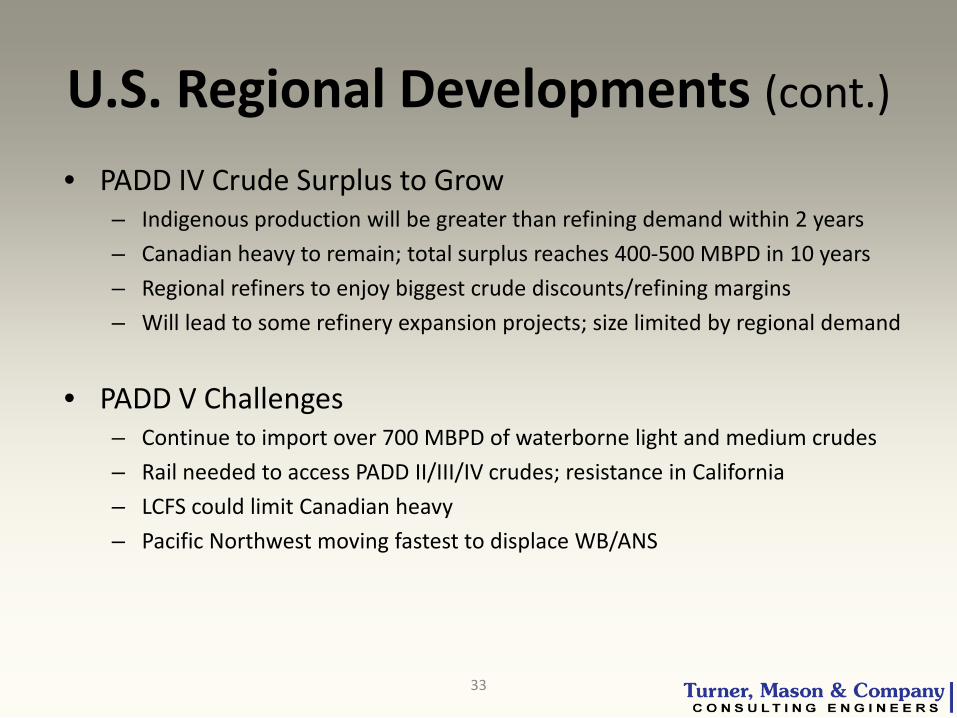

U.S. Regional Developments (cont.)

• PADD IV Crude Surplus to Grow – Indigenous production will be greater than refining demand within 2 years – Canadian heavy to remain; total surplus reaches 400-500 MBPD in 10 years – Regional refiners to enjoy biggest crude discounts/refining margins – Will lead to some refinery expansion projects; size limited by regional demand

• PADD V Challenges – Continue to import over 700 MBPD of waterborne light and medium crudes – Rail needed to access PADD II/III/IV crudes; resistance in California – LCFS could limit Canadian heavy – Pacific Northwest moving fastest to displace WB/ANS

Factors Affecting U.S. Shift to Domestic Lights

• Operating impacts • Yield impacts

• Crude and product exports • Saudi and other structural crude imports

•Downstream investment

34

Operating Impacts • Influx of light/super light crude reduces capacity

– Loss is 10%+ at refineries designed for heavier crudes

– Units impacted include crude units, gas plants, debutanizers, naphtha units, others – Crude discounts incentivizing investment – Solutions are refinery specific; could require new crude units, preflash towers, expansion of

naphtha HDS, etc.

• Other concerns

– Higher TAN from Canadian dilbits will require capital/treating costs; could limit volumes at certain refineries - bigger issue at USGC plants

– Potential compatibility issues associated with blending dissimilar crudes

– Loss of access to imports will decrease crude slate flexibility

• Benefits

– Lower resid yield/metals content of shale oil will facilitate resid cracking

– Sulfur plant limited refineries will benefit from sweeter crudes

35

Specific Issues – Light Shale Crude

• Bakken – Very high level of reformer feed (30%) causes naphtha handling issues – Does have decent distillate yield and blending properties – Good resid cracker feed properties; fits well with East Coast refineries – Refining value a bit higher than Brent and WTI, lower than LLS

• Eagle Ford

– The most challenging for refiners; rapid growth/high volume of lights

– Lightest barrels particularly difficult; can contain over 60% naphtha or lighter

– Compatibility issues when blending with heavy crudes

– Refining value several dollars per barrel below LLS

• Others

– Growing Permian production lighter than historical WTI

– Niobrara has both heavier (<40 API) and condensate barrels

– Utica similar to Eagle Ford; very light/significant condensate volumes

36

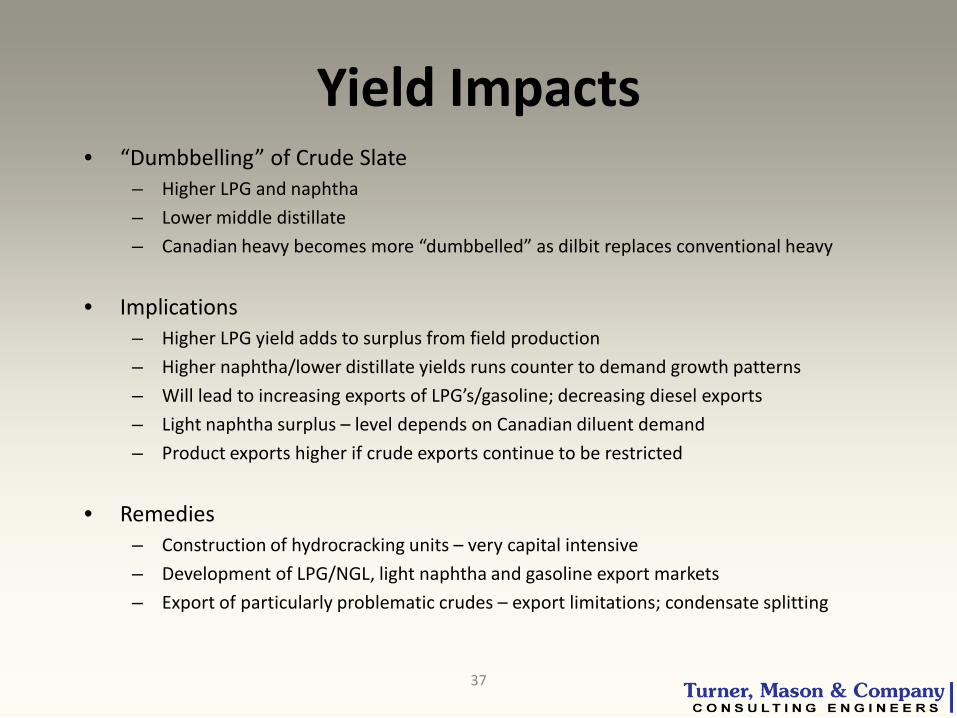

Yield Impacts • “Dumbbelling” of Crude Slate

– Higher LPG and naphtha – Lower middle distillate – Canadian heavy becomes more “dumbbelled” as dilbit replaces conventional heavy

• Implications – Higher LPG yield adds to surplus from field production – Higher naphtha/lower distillate yields runs counter to demand growth patterns – Will lead to increasing exports of LPG’s/gasoline; decreasing diesel exports – Light naphtha surplus – level depends on Canadian diluent demand – Product exports higher if crude exports continue to be restricted

• Remedies – Construction of hydrocracking units – very capital intensive – Development of LPG/NGL, light naphtha and gasoline export markets – Export of particularly problematic crudes – export limitations; condensate splitting

37

0.6

0.8

1

1.2

1.4

1.6

30

30.5

31

31.5

32

32.5

1985 1990 1995 2000 2005 2010 2015 2020

Sulfu

r, w

t. %

Gra

vity

, API

Changing U.S. Refinery Crude Slates

1985-2022

Domestic Lights Latin American & Canadian Heavies Middle

Eastern Design

Basis ->

38

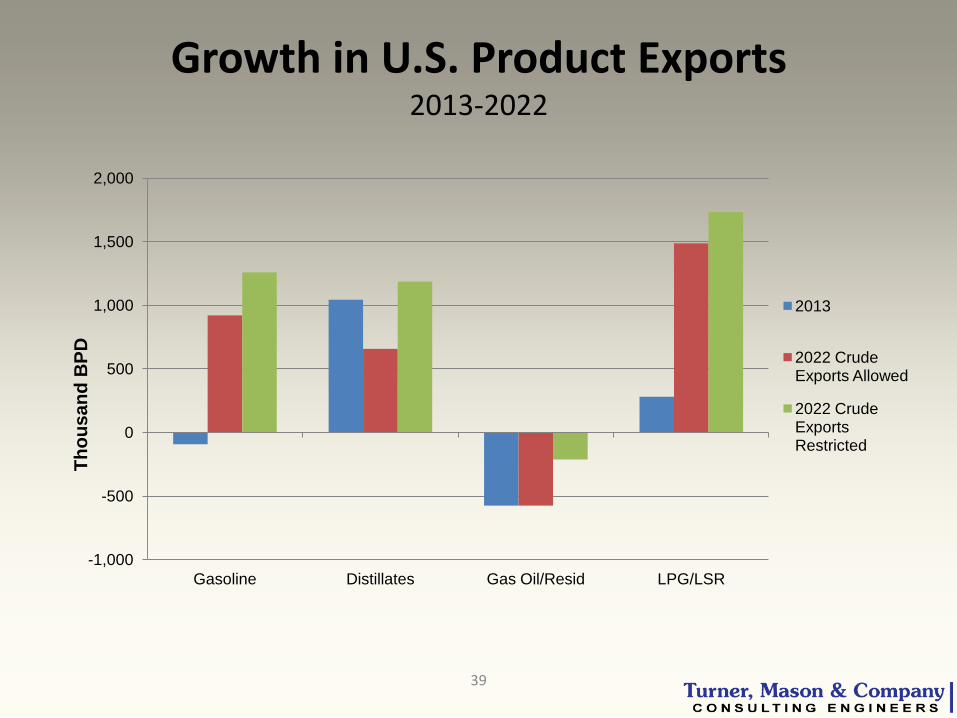

Growth in U.S. Product Exports 2013-2022

-1,000

-500

0

500

1,000

1,500

2,000

Gasoline Distillates Gas Oil/Resid LPG/LSR

Thou

sand

BPD

2013

2022 Crude Exports Allowed

2022 Crude Exports Restricted

39

40

Refinery Investments • Projects to Allow Processing of Advantaged Oil

– USGC (Eagle Ford), OH/KY (Utica), Permian Basin (WTI), ND/PADD IV (Bakken, Uinta, Hvy. Canadian)

– Projects very refinery and crude specific

• Midstream Sponsored Condensate Splitters – Primarily Eagle Ford projects on the USGC – 150 MBPD under construction; 200 to 300+ MBPD being proposed – Export policy will be important factor

• Diesel Focused Projects

– Incentivized by favorable diesel vs. gasoline demand patterns – Both new and revamped hydrocrackers

• Export Restriction Driven “Crude-to-Product” Projects

– Done in response to binding U.S. export restrictions – Also midstream sponsored/condensate splitters and diesel hydroskimmers – USGC locations; investment would be delayed by regulatory uncertainty

41

Refinery Expansions/Advantaged Oil

Eagle Ford Operator Location MBPD* Startup

Flint Hills Corpus Christi, TX 30 Late 2014 Valero Houston, TX 90 2Q 2015 Valero Corpus Christi, TX 70 3Q 2015

Utica Operator Location MBPD* Startup

Marathon Canton, OH 10 2014 Marathon Catlettsburg, KY 35 2015

Permian Operator Location MBPD Startup

Valero McKee, TX 25 2015 *Project will allow refinery to run higher volumes of very light crude and condensate from regional tight oil production. Estimated total expansion of crude capacity is not necessarily equal to capacity of new condensate splitter or preflash tower and is TM&C's estimate.

42

Refinery Expansions/Advantaged Oil

Bakken Operator Location MBPD Startup

Calumet Dickinson, ND 20 4Q 2014

Uinta Operator Location MBPD Startup

Tesoro Salt Lake City, UT 4 2H 2014 HollyFrontier Woods Cross, UT 29 2015/16

Heavy Canadian Operator Location MBPD Startup

Calumet Great Falls, MT 10 3Q 2015

43

Condensate Splitters Under Construction

Operator Location MBPD Startup Kinder Morgan, Phase 1 Houston, TX 50 2Q 2014 Kinder Morgan, Phase 2 50 2Q 2015 Trafigura Corpus Christi, TX 50 4Q 2014

Proposed Operator Location MBPD Startup

Magellan Corpus Christi, TX 50 2H2016 Martin Midstream Corpus Christi, TX Up to 100 1-2Q 2016 Targa Resources TBD TBD TBD Castleton Commodities Corpus Christi, TX TBD TBD Phillips 66 Sweeny, TX TBD TBD

44

Diesel Expansion Projects Completed

Operator Location MBPD* Startup Valero Port Arthur, TX 60 Late 2012 Valero St. Charles, LA 60 Late 2013

Under Construction/Proposed Operator Location MBPD* Startup

Philadelphia Energy Solutions Philadelphia, PA 15 2014 Valero Meraux, LA 20 2015 Husky Lima, OH 25 2017 Marathon Garyville, LA 34 2018 Valero Port Arthur, TX 15 2018 Valero St. Charles, LA 15 2018

*Reflects size of hydrocracker expansion

Final Thoughts

45

46

Final Thoughts

• Production Boom is a Generational Event for NA Oil Industry – Provides both opportunities and challenges for all industry segments – Moving from energy importer to exporter – Significant Implications economy-wide and internationally

• Implications for Refining Sector – Lower crude and natural gas costs add to existing advantages – Makes U.S. refineries perhaps the most competitive in the world – Regions with best access to growing crude will be most advantaged – Investment will be needed to handle quality issues – Incentivizing new capacity as limited by demand – Finding homes for growing levels of product exports is a key challenge

47

Final Thoughts (cont.) • Implications for Midstream Sector

– Many new opportunities developing (pipelines, rail, marine) – Becoming more involved in processing (condensate splitters, etc.) – Challenges from NIMBY, environmental, other groups will continue

• Implications for Upstream Sector

– Build-out of midstream infrastructure is key – especially for Canada – Tight oil well depletion rates high; finding new prospects critical – Crude export policy especially important to this sector

• Government Policy Challenges – Costs/Demand/Access – Increase cost – Tier 3, NSPS, LCFS, rail car standards, fracking rules – Decrease demand – CAFE, RFS, alternative fuels policies – Access – midstream permitting, Jones Act, access to reserves, crude export

policy

Today’s Speaker

Michael W. Leger, P.E. President [email protected] 214-754-0898

LSU Chemical Engineer Formerly with Texaco, Cities Service Company & CITGO Strategic planning, FMV, ventures Directs firm activities

48

Related Documents