FACTORS INFLUENCING EMPLOYEES PREPAREDNESS FOR RETIREMENT. A CASE OF EMPLOYEES OF PUBLIC INSTITUTIONS WITHIN MOMBASA COUNTY, KENYA KAHURIA NELSON NYORO BUS-3-7631-3/2012 A RESERCH PROPOSAL SUBMITTED IN PATRTIAL FULLFILMENT OF THE REQUIREMENTS FOR THE AWARD OF THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION OF KENYA METHODIST UNIVERSITY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FACTORS INFLUENCING EMPLOYEES PREPAREDNESS FOR

RETIREMENT.

A CASE OF EMPLOYEES OF PUBLIC INSTITUTIONS WITHIN

MOMBASA COUNTY, KENYA

KAHURIA NELSON NYORO

BUS-3-7631-3/2012

A RESERCH PROPOSAL SUBMITTED IN PATRTIAL FULLFILMENT OF THE

REQUIREMENTS FOR THE AWARD OF THE DEGREE OF MASTER OF BUSINESS

ADMINISTRATION OF KENYA METHODIST UNIVERSITY

OCTOBER, 2014

2

DECLARATION

This research proposal is my original work and has not been

presented for a degree or a Diploma in any other examination

body. No part of this project may be reproduced without the prior

permission of the author and/or the University.

Nelson Nyoro Kahuria ……………………….. ………………

BUS-3-7631-3/2012 Sign

Date

Declaration by Supervisors

This research proposal has been submitted for examination with

our approval as University Supervisor(s).

Name of supervisor Eric Mathuva ………………………..

………………

Sign Date

i

Rosemary Muriiki …………………………

………………

Sign Date

DEDICATION

I dedicate this proposal to God for giving me life and hope. I

also dedicate it to my wife Charity and my daughter Njoki.

ii

ACKNOWLEDGEMENT

This proposal would not have been complete without the critical

guidance and insight of my supervisors Mr. Eric Mathuva and Mrs.

Rosemary Muriiki. I also acknowledge the support of my colleagues

who provided the much need peer support.

iii

ABBREVIATIONS

HRS Health and Retirement Study

FPRS Financial Preparedness for Retirement Scale

KPA Kenya Ports Authority

iv

RBA Retirement Benefit Authority

SACCO Savings and Credit Cooperative Societies

SPSS Statistical Package for Social Sciences

ABSTRACT

v

Life in retirement is a major concern for developing countries,Kenya included particularly with regard to the quality of livesthat the retirees live once out of employment. Empirical datasuggests that there a cadre of employees whose lives takes adrastic change for the worse on leaving their jobs due toinadequate preparation for life in retirement. In Kenya,employees of certain parastatals stand accused living large whileon employment but are ill prepared for life after employment. Adescriptive survey study is designed to show how employees ofKenya Ports Authority (KPA) prepare for retirement. A sample of56 employees of the parastatal will be selected using purposiveand stratified random sampling method to respond to questionnaireitems intended to gauge aspects of their preparation for life inretirement. Data obtained will then be analyzed descriptivelyusing frequency and percentage as well as inferentially usingregression analysis with the aid of statistical Package forSocial Sciences (SPSS) computer software to determine factorsthat influence employees preparedness for retirement..

vi

TABLE OF CONTENTS

DECLARATION....................................................i

DEDICATION....................................................ii

ACKNOWLEDGEMENT..............................................iii

ABBREVIATIONS.................................................iv

ABSTRACT.......................................................v

TABLE OF CONTENTS.............................................vi

LIST OF TABLES..............................................viii

LIST OF FIGURES...............................................ix

CHAPTER ONE: INTRODUCTION......................................1

1.1 Background of the study...................................1

1.2 Statement of the Problem..................................6

1.3 Objectives of the Study...................................7

1.4 Research Questions........................................8

1.5. Scope of the Study.......................................8

1.6. Significance of the Study................................8vii

1.7. Assumption of the Study..................................9

1.8 Limitations of the Study..................................9

1.9 Definition of Terms.......................................9

CHAPTER TWO: LITERATURE REVIEW................................10

2.1 Introduction.............................................10

2.2 Theoretical Review.......................................10

2.2.1 Lifecycle Theory of Saving...........................10

2.3 Empirical Review.........................................13

2.3.1 Socio Demographics..................................13

2.3.2 Financial Literacy...................................14

2.3.3 Financial groupings..................................17

CHAPTER THREE: RESEARCH METHODOLOGY...........................25

3.1 Introduction.............................................25

3.2 ResearchDesign...........................................25

3.3 Target Population........................................26

3.4 Sample Size..............................................26

3.5 Data Collection Instruments..............................27

3.6 Data Collection Procedures...............................28

3.7 Ethical considerations...................................28

3.8 Data Analysis Plan.......................................29

REFERENCES....................................................31

APPENDICES....................................................32

viii

Appendix I Questionnaire....................................32

LIST OF TABLES

Table 3.1: The Sampling Frame and Size

----------------------------------------------------------------------

----27

ix

LIST OF FIGURES

x

Figure 2.1: Elements of Conceptual framework

--------------------------------------------------------22

Figure 2.2: Operational framework

-----------------------------------------------------------------

------24

xi

xii

CHAPTER ONE: INTRODUCTION

1.1 Background of the study

Retirement generally refers to the act of leaving a position of

employment upon reaching a particular stipulated age or due to

other specified reasons (Atchley, 1998). According to the

researcher, it is one of the main transitions in life that

symbolizes the individual leaving one part of a significant

activity and entering into a new period in life. Usually, this

transition often affects many life domains and is often

accompanied by a decline in life satisfaction, self-evaluation,

and quality of life (Lusardi & Mitchell, 2011; Oyuke, 2009).

Pinquart and Schindler, (2007) contends that retirement is

frequently seen as an abrupt switch from being employed one

minute to total ceasing of work activity in the next minute which

is a more complex and progressive transition an assertion to

which Wang (2007) agrees. Thus, having adequate coping skills for

retirement could affect the outcome of this transition which

implies that workers should adequately prepare. However, Oyuke

(2009), maintains that despite the centrality and significance of

1

retirement, preparation towards by most workers it is often

insufficient.

The main purpose of retirement preparation programs is to enable

a worker form realistic perception of retired life and reduce

anxiety about retirement. In other words, it aims at enhancing

prospective retirees’ adaptation to retirement and to provide

assistance in managing this new phase in life ( ). Modigliani

and Brumberg (1980) worked out a theory of spending based on the

idea that people make intelligent choices about how much they

want to spend at each age, limited only by the resources

available over their lives. By building up and running down

assets, working people can make provision for their retirement,

and more generally, tailor their consumption patterns to their

needs at different ages, independently of their incomes at each

age. Employers will continue to play a vital role in helping

workers save for retirement by offering retirement plans along

with education and planning tools and retirement income options.

Moreover, with so many workers planning to work longer, employers

can offer opportunities to help older workers extend their

2

working years and their transition into retirement ( ). However,

to help a worker to adequately prepare for retirement, the person

may need to be excited about the prospects of retiring to become

motivated enough to seek information and advice, and finally to

take action to prepare for retirement. Otherwise it is possible

for the fact that retirement is a reality in a worker’s life to

sink in when it is very late in the individual’s working life, a

trend that is unfortunately said to be apparent with many

employees who retire from long years of service and continue to

struggle with basic needs of life ( ).

Employee preparedness for retirement has been shown to be

dependent on a number of factors. These include environmental

influences, individual differences, and psychological process

factors (Engel, Blackwell, & Miniard, 1990). According to the

researchers, environmental influences include culture, social

class, personal influence, family, and employment situation;

individual differences are characterized by individual resources,

motivation and involvement, knowledge, attitudes, personality,

lifestyles, and demographics while psychological processes

3

include information processing, learning, and attitude and/or

behaviour change. According to Woerheide (2000), work environment

plays a key role in a person’s decision to prepare for retirement

particularly with regard to the type of qualified savings plan

available at work. In general, research has shown that those who

are employed in governmental agencies are more likely to have a

defined benefit plan than other workers (Bureau of Labor

Statistics, 2004), which may impact the employees’ willingness to

save privately for retirement. Similarly, Power and Hira (2004)

found that professional employees are more likely than union

members and clerical staff to have started planning for

retirement. Roszkowski (1996) on his part reported that those

employed in public-sector occupations have greater risk aversion

than those employed in the private sector which is important

because risk tolerance has been shown to be related to

willingness to save and invest (Callan & Johnson, 2002).

With regard to individual differences, one’s attitude toward

retirement has been shown to be important in enabling the

individual adjust satisfactorily to retirement (Atchley, 1991)

4

and attitude about retirement influences the level of confidence

one displays regarding the success of their retirement thus a

probability to start preparing for it well in advance. Hogarth

(1991) found that age, education, gender, income, and marital

status was significant factors influencing saving for the future.

Being older, having attained a higher level of education, being

male, having higher income, and being married were positively

related to saving for the future. Catrambone (1998) also

discussed the significant relationship between gender and

retirement investment as she discussed barriers that women

investors confront in retirement savings. According to the

researcher, women, compared to men, have lower levels of

retirement investments savings. Yuh and DeVaney (1996) on their

part contend that income, years of employment, education and

occupation are significant factors associated with defined

contribution retirement funds of couples. Specifically, they

found that higher income, longer years of employment, better

education, having a skilled occupation (e.g., managerial and

professional) are positively related with the defined

contribution retirement fund levels. DeVaney, Su, Kratzer, and

5

Sharpe (1997) concluded that age, marital status, and income tend

to be significantly related to the amount of money saved for

retirement. By examining factors related to employer provided

retirement benefits, Foster (1998) found that being older with

more income has a significant impact on retirement benefits.

These findings support the positive relationship between age and

being married with retirement savings among other empirical data

on factors impacting preparedness for retirement.

Evidence adduced show that there is limited empirical data on the

extent to which these factors affect workers preparedness in

developing countries. Those in existence allege that old age

poverty rates are increasing in the 21st Century ( ), a fact

that depicts inadequate preparation for retirements. Collinson

(2012) alleges that in America many workers are planning to work

longer and delay retirement. Specifically, the researcher noted

that 56 % of workers plan to work past age 65, including 43 %

who plan to work past age 70 or do not plan to retire and more

than half (54 %) plan to continue working after they retire

though only one in five has a back-up plan if forced into

6

retirement sooner than expected. Duncan (2014) on his part found

that South Africans don’t save enough for retirement a fact

supported by Benchmark (2014) who indicated that only 29 percent

of South African retirees who are members of funds and are able

to maintain their standard of living when they retire.

Similarly, studies conducted by Karatu (1991); Aboderin and

Gachuhi (2007) found that although retirement has various

negative social, psychological and physiological consequences,

that of economic deprivation is the most felt. It further showed

that older persons and their families are usually among the

poorest and have no reliable sources of income and that many of

them are not eligible for pensions or any social protection. In

Kenya, a survey conducted by Retirement Benefits Authority (2009)

for individuals showed that, with rising costs of living, many

Kenyans who started retiring in the 1990s are finding out that

they are going to outlive their life savings. Omondi ( )

alleges that retirement woes are mounting as workers live longer

and that an extended life span is coming with one big problem for

companies that sponsor defined benefits pension plans. With the

7

problem also affecting senior citizens under defined contribution

scheme where companies cover their exposure to living for too

long by buying annuities, a product that guarantees a regular

income for a lifetime ( ) the overall outcome is an indictment

on the workers preparedness for life in retirement.

1.2 Statement of the Problem

Workers in formal and non-formal employment aspire to retire into

a secure and comfortable life thereafter and even leave behind

property to be bequeathed to their loved ones when they are no

more. However to many workers, this aspirations remains to be

true only in theory. According to statistics published by

Retirement Benefits Authority (2009), only less than one percent

of Kenyans plan for retirement or have a savings plan. Out of

those who save for retirement or have a savings plan, less than

half actually know how to do it- that is, what proportion of

their monthly income should go to savings or a pension plan. For

one to have comfortable life after retirement, an individual

should aim to earn at least 75% of what they were earning when

working. The report further shows 31% of those who retire

8

continue to look for more jobs to do after retirement to meet

their needs at retirement. 47% of those who retire depend on

relatives for their upkeep, 16% depend on pension which is barely

enough and only a paltry 6 % retire to comfortable life in the

country. From the analysis it is apparent that 94% of employees

do not prepare for well for retirement.

Theoretically, public institutions which include the civil

service, parastatals, universities, County government are bodies

that pay their employees very well and also offer them many other

benefits including membership to private members clubs. Thus

while in employment, workers are accustomed to life of opulence

as they live large. A little interaction with the same employees

after retirement shows people who are adjusting to hitherto harsh

realities of life. Anecdotal reports allege that some retirees

from some of these institutions are bogged down with loans they

take in retirement with most of the loans being channeled as

school fees and emergency loans all which are consumption type of

loans. The employees are left with very little in their pensions

after that deduction which creates a big challenge to their

9

survival. The basic conclusion is that there is a miss-match

between the lifestyle of employees of some of public institutions

while in employment and their lifestyle after they retire which

is an indictment on their preparedness for retirement while still

in employment. This study is intended to assess what happens

during the working life of employees of public institutions in

order to underscore why life in retirement pose such a big

challenge to some of them in an attempt to make a contribution in

sealing the existing research gap on factors that influence

employees preparedness for retirement.

1.3 Objectives of the Study

The study generally seeks to establish how employees of public

institutions prepare for retirement and the factors that

influence their preparedness. Specifically, it seeks:

1. To determine whether employees’ demographics (Bio data)

influence their preparedness for retirement.

2. To assess whether employees who are members of SACCOS, are

better prepared for retirement than those who are not

members.

10

3. To establish whether there is a relationship between the

level of financial literacy and preparation for retirement

4. To determine whether financial Life cycle is a factor in

preparation for retirement.

1.4 Research Questions

The research seeks to answer the following questions:

1. What is the influence of employees’ background

characteristics on their preparedness for retirement?

2. How does membership of employees to SACCOs affect their

preparedness for retirement?

3. How does access to financial information affect employees’

preparedness for retirement?

4. How does financial life cycle influence employees’

preparedness for retirement?

1.5. Scope of the Study

The study targets permanent and pensionable employees of public

institutions in Mombasa County to assess how prepared they are

for retirement. The researcher will focus on the employees of

11

Kenya Ports Authority, Kenya Ferry Service, County Government of

Mombasa and Technical University of Mombasa who are the main

respondents.

1.6. Significance of the Study

Retirement is a major concern for employers and employees.

Apparently little attention has been given to this otherwise very

important factor of life for the society. The study will thus

provide valuable information to employers on what they need to do

to prepare their employees for a life after retirement. The study

will also come in handy for employees in providing necessary

information on what makes one prepared for retirement. The

information will also serve institutions like Sacco’s and pension

schemes on the best way to handle members and equip them for a

comfortable life in retirement. For scholars the study will

arouse interest in the subject matter of retirement and give

insight of many areas that should be researched on.

1.7. Assumption of the Study

12

That data obtained from respondents through the questionnaire and

interviews will be correct and true. That it will be possible to

control other variables and only focus on the variables under

study without having a great effect on the study.

1.8 Limitations of the Study

Employees of public institutions are relatively very busy people

and as much as there will be an official approval to conduct the

research, it may not be that easy to get all the respondents

conveniently. Similarly the information being sort is somewhat

confidential and some people may not be as comfortable to share

their own information which they consider private.

1.9 Definition of Terms

The following terms will be used in this study to imply

Bio data: information regarding an individual's education and

work history, esp in the context of a selection process

CHAPTER TWO: LITERATURE REVIEW13

2.1 Introduction

The purpose of this chapter is to review literature related to

planning for retirement. Modigliani and Brumberg (1954) provides

the simplest version of the life cycle consumption model without

bequests and uncertainty posits that households accumulate

savings during their working careers up to their retirement, and

de-cumulate wealth thereafter.

2.2 Theoretical Review

A theoretical framework is a collection of interrelated ideas

based on theories. It is reasoned set

of prepositions, which are derived from and supported by data or

evidence. It accounts for or

explains phenomena. It attempts to clarify why things are the way

they are on theories (Kombo

and Tromp, 2000). BMO retirement Institute (2012) observed that

as people approach retirement, the question of whether they are

financially prepared becomes top of mind. Questions regarding

financial sufficiency may be raised by several trends, such as

employers moving away from offering traditional defined-benefit

14

pension plans and certain government pension benefits being

decreased and delayed. These trends serve to shift the

responsibility to individuals to save for their own retirement.

In addition, some may still be struggling to rebuild retirement

funds depleted by events of financial crisis.

2.2.1 Lifecycle Theory of Saving

According to Modigliani (1954) one of the most important motives

for putting money aside was the need to provide for retirement.

Young people will save so that when they are old and either

cannot or do not wish to work, they will have money to spend. The

life-cycle story is one in which the wealth of the nation gets

passed around; the very young have little wealth, middle aged

people have more, and peak wealth is reached just before people

retire. As they live through their golden years, retirees sell

off their assets to provide for food, housing, and recreation in

retirement. The assets shed by the old are taken up by the young

who are still in the accumulation part of the cycle.

15

The simplest version of the life cycle consumption model without

bequests and uncertainty posits that households accumulate

savings during their working careers up to their retirement, and

decumulate wealth thereafter (Modigliani and Brumberg, 1954).

This type of saving behaviour enables households to smooth their

marginal utility of consumption over the life cycle. However,

there are many reasons why household consumption and wealth

follow patterns different than that predicted by the life cycle

model, and the standard model can be easily adjusted to account

for these reasons (Browning and Lusardi, 1996).

A research by Modigliani and Brumberg (1954) showed that

consumption is proportional to life-time resources or, what is

more or less the same thing, to average income over the life

span. Yet it was well-known prior to 1950, and it remains true

today, that the share of consumption in

income is lower for better-off households or, equivalently, that

the saving rate rises with income.

16

Indeed the data often show negative saving rates among those in

the lower part of the income distribution. These facts had

influenced the way that Keynes thought about consumption, and his

“fundamental law” that consumption increased with current income,

but not so rapidly.

Modigliani and Brumberg (1954) argue that the proportionality of

consumption and income in the long-run is entirely consistent

with the cross-sectional facts because, as we move up the income

distribution, a higher and higher fraction of people are there on

a temporary basis, with high transitory income, and thus a

temporarily high saving ratio. The same argument explains why

savings rates rise more rapidly with income among households who

are farmers or small- business proprietors, whose income tends to

be relatively volatile, and why, at a comparable income level,

black families save more than white families. Black families have

lower incomes than whites on average, so for a black group and a

white group with the same average income, transitory income is

higher among the former. In the macroeconomic context, argued in

Modigliani and Brumberg (1980), the same line of argument shows

17

that, for the economy as a whole, the saving ratio should be

constant over the long-run (provided the rate of growth of the

economy doesn’t change), but will vary pro-cyclically over the

business cycle. Over the business-cycle, as over the life-cycle,

consumption is smoother than income.

Many Studies like Hubbard, Skinner and Zeldes, 1995, longevity

and bequests (Hurd, 1989), have highlighted the role of

precautionary saving motives different economic opportunities

across cohorts (Kapteyn , Alessie and Lusardi, 2005), self-

control problems (Laibson, 1997; Benartzi and Thaler, 2004;

Ameriks, Caplin, Leahy and Tyler, 2007). None of these studies

have focused on the role of financial literacy in accumulating

wealth; however, more financially sophisticated individuals may

face lower barriers to gathering and processing information and

thus be better equipped to both accumulate and manage their

savings.

2.3 Empirical Review

18

Available empirical data attributes employees preparedness to

retirement to various factors. The study will examine literature

that looks at how socio demographics, financial literacy,

financial life cycle and membership to financial groupings

affects employees preparation to retire.

2.3.1 Socio Demographics

BMO retirement institute (2012) in a research report to test

whether moderating variables such as age, education, income,

number of dependents, planned retirement age and years to

retirement had an influence on involvement in financial

preparation for Canadians showed that factors such as age and

gender were not significantly related to financial preparedness

for retirement scale (FPRS) when compared with other variables

such as education, income and number of dependents. The findings

showed that for men and women in same salary scale there was

significant difference in their level of preparedness to

retirement. The research further revealed that the FPRS score is

best explained by years to retirement and education, which appear

to be the two key drivers of retirement preparedness. However

19

Pauline (2013) in her study found that; age, gender, marital

status, parents’ socio-economic status, availability of

retirement information, monthly income, retirement planning and

the availability of reliable social support systems significantly

influenced retirement happiness. Two studies, Yuh et al. (1998a)

and Yao et al. (2003), model observed that the likelihood that a

household is adequately prepared for retirement is more dependent

on financial variables as the driving forces and not as much the

demographic variables.

2.3.2 Financial Literacy

Worthington, (2005) defines financial literacy as the ability to

make informed judgments and to take effective decisions regarding

the use and management of money. Remund (2010) on the other hand

defines it as a measure of understanding key financial concepts.

In other words financial literacy refers to a situation in which

an individual possess the knowledge sufficient to make informed

decisions in regard to planning for retirement. The authors

suggest that financially literate population is able to make

20

informed decisions and take appropriate actions on matters

affecting their financial wealth and well-being. Financial

knowledge enables individuals to build their financial skills and

gives them confidence to undertake financial decisions for their

pension schemes (Agnew, Szykman, Utkus, & Young, 2007). Knowledge

on savings and plans to save is critical for effective long term

financial decision making that is relevant to pension funds

(Gitari, 2012).

The Retirement Confidence Survey conducted by Helman and

Greenwald (2013) reports that only 23 percent of pre-retirees in

South Africa who obtained advice on retirement planning which

suggests that three out of four people might have little idea of

how much to save for retirement. Without a savings goal a

comfortable retirement is unlikely, even for the rich. This gives

credence to a study by Felicity Duncan (2014) shows that South

Africans don’t save enough for retirement. According to a survey

by Benchmark (2014), an annual review of the retirement industry,

only 29 percent of South African retirees who are members of

funds are able to maintain their standard of living when they

21

retire; that falls to 10 percent when all retirement age South

Africans are considered. And even that statistic obscures the

true nature of South Africa’s retirement landscape. OECD (2005),

defines financial literacy as the combination of consumers and

investors understanding of financial products and concepts and

their ability and confidence to appreciate financial risks and

opportunities, to make informed choices, to know where to go for

help, and to take other effective actions to improve their

financial well-being (Miller et al., 2009).

Onyango (2008) in his study observed that having knowledge of

retirement issues is positively related to attitude toward

retirement. Studies have found that those who believe that they

know more about financial planning are more likely to have

prepared for retirement. Garret et al (2003) while analyzing

other studies concluded that training and intervention programs

designed to boost financial knowledge should improve financial

preparedness by triggering advanced planning activities.

According to Taylor (1997) retirement education could improve

employees’ knowledge and behaviors related to retirement

22

planning, and in turn, attitudes toward retirement and

preparation for retirement. Bernheim and Garrett (2003) in their

study investigated cross-sectional relationships between the

availability of financial education provided by employers and

savings. They found that employer-based financial education

increased both saving in general and saving for retirement.

Further, the study found that brief training programs stimulated

individual’s saving behaviors and decision-making competencies.

Clark and d’Ambrosio (2003) investigated the effects of one-hour

retirement seminars on retirement attitudes and behaviors. They

found that participation in seminars changed individual’s

retirement goals and retirement savings behaviors in a positive

way. Similarly, Taylor-Carter et al (1997) found that informal

financial planning had a positive effect on anticipated financial

expectation and that formal retirement education seminars which

included financial management had positive effects on anticipated

retirement satisfaction. According to Chan and Stevens (2008)

households base pension and retirement saving decisions upon

limited and sometimes incorrect pension knowledge. One may argue

23

whether financial literacy affects knowledge of pensions and

Social Security benefits.

A study by Gustman, Steinmeier and Tabatabai (2010) indicates

that there is no any direct relationship between basic cognitive

skills (numeracy) and knowledge of retirement plan

characteristics and Social Security. While there is a positive

relationship between pension wealth and knowledge. The study

argues that the causality is more likely to run from pension

wealth to pension knowledge than the other way around, and that

the positive numeracy–wealth relationship should not be taken as

evidence that increasing cognitive skills and numeracy will

increase the wealth of households as they enter into retirement.

A study carried by Bernheim (1998) was among the first to note

that policymakers and researchers might have overlooked the

importance of financial literacy to explain savings and

differences in saving behaviour. Since then many studies have

emphasized the role of financial

24

knowledge but, in the absence of specific literacy measures,

resort to crude proxies. The disadvantage of these proxies is

that there is no way to disentangle the effect of financial

literacy from the effect of the proxy variable. For example, by

using education as a measure of financial literacy, one is not

able to separate the independent effect of financial knowledge

from the impact of the education level, per se; in many

regressions, education also serves as a proxy for lifetime

income.

In the past few years researchers have increased their efforts to

develop specific measures of financial knowledge and have also

investigated the relationship between financial literacy and

financial decision-making. Hilgert, Hogarth and Beverly (2003)

developed a set of true/false questions to measure financial

knowledge and explored the relationship between financial

knowledge and money management. Lusardi and Mitchell (2011)

pioneered a module to measure financial literacy that was part of

the 2004 Health and Retirement Study (HRS). They showed there is

strong positive association between financial literacy and

25

retirement planning. According to Kefela (2010), financial

knowledge is directly correlated with self-beneficial financial

behavior and so financial education should take a wholesome

perspective to include the fundamentals of finance since without

understanding the basic finance principles, pension education

would be ineffective. In the words of Kefela (2010,), “

participants who are less financially literate are more likely to

have problems with debt, are less likely to save, are more likely

to engage in high cost mortgages and are less likely to plan for

retirement” and by extension are less likely to make better

choices for their pension schemes.

2.3.3 Sacco Membership

Savings and Credit Cooperative societies (SACCOS) are voluntary

associations or cooperative financial institution owned and

controlled by their members and operated for the purposes of

promoting saving, providing credit at low interest rates and

providing other financial services to its members (Waweru 2011).

Members regularly pool their savings, and subsequently may obtain

loans which they may use for different purposes. Generally, the

26

idea behind establishment of SACCOS is to promote savings and

make credits available to the members. SACCOS are the important

micro-financing institutions for mobilization of financial

resources for various development activities.

Co-operatives are autonomous association of persons united

voluntarily to meet their common economic, social, cultural needs

and aspiration through a jointly owned, democratically controlled

enterprise (RoK, 2008). As mentioned above, the sole objective of

these societies involves mobilization of resources from which

individual co-operators may benefit. Generally, co-operatives are

organized into service and producer cooperatives (Branco, 2005).

In Africa, the idea of saving and credit societies was first

described and discussed in 1955 in Jipara, a small town the upper

west town of Ghana, the idea was brought by the Roman Catholic

priest, Father John McNulty from Ireland. He decided to assist

this village to form a saving and co-operative, he then trained

60 people mainly teachers. The success Jipara story has been

widely replicated throughout the African continent (Alila & Obado

27

1990).Cooperative societies are characterized by the intrinsic

values and principles on which they are founded. They are based

on the values of self-help, self-responsibility, democracy,

equality, equity, and solidarity. The end product of these co-

operatives is to attain the high living standards of its members.

RBA (2010) carried out a research where a sample of employees

drawn from the members of the different pension schemes across

Kenya was interviewed. The results indicated that the pension

scheme members have higher level of knowledge on pension scheme

practices than general financial literacy issues and identify the

lack of forum for involvement and lack of understanding of

pension fund matters as the major hindrances to participation in

pension scheme affairs, both of which can be addressed through

appropriate finance and pension literacy programs. Keven( 2012)

alludes that to be a billionaire is not an easy thing, but women

and men in Kimilili District have found an alternative way to

conquer this dilema through self-help initiatives or groups

commonly referred to as Chama’s. In the society that sees white

collar jobs, as the only way to gain financial independence and

28

bring home money today, the women and men have come together to

form groups (Chama’s) to empower and cushion themselves against

these tough times.

2.3.4 Financial Lifecycle

The Study by BMO institute (2012) illustrated that time

remaining to retirement, and not age, is a key indicator of an

individual’s financial preparedness for retirement. The Study

indicates that young adults under the age of 35 are the least

prepared, based on an analysis that considered attitudes and

behaviour as key measurements for financial preparedness for

retirement. These findings can be helpful to the younger

generations as common wisdom states that the earlier people start

to save for retirement, the greater the potential that they will

achieve future financial security. Tina (2012) in her study

observed that the closer people are to their target retirement

date, the more likely they are to be prepared for retirement.

However, the Research indicates that the key indicator is the

time remaining to retirement, not the actual age of the

individual. For example, in certain cases, it may be possible for

29

a younger person to actually have less time before his or her

desired retirement age than an older person (i.e., a 40-year-old

who desires to retire at the age of 50, and therefore has ten

years left before retirement, compared with a 50-year-old who

aims to retire at the age of 65, and therefore has 15 years

left). Nevertheless, as expected, the Research based on attitudes

and behaviour concluded that the youngest generation of adults is

the least prepared for retirement, because in all probability,

their retirement date is the furthest away. Interestingly, the

Study findings suggest that young adults under the age of 35 may

be overly optimistic, since as many as 41 per cent expect to

retire early (i.e. before age 60) In addition to the time

remaining until the target retirement date, the Research revealed

that a person’s level of education was another indicator of

financial preparedness for retirement It was found that higher

levels of education can greatly influence people’s motivation and

involvement in taking a more active role in planning their

retirement by, for example, attending seminars or consulting

financial planners, which are behaviors that increase basic

financial education and empower people to make sound financial

30

decisions and take action accordingly .This is why improving the

financial literacy of all Canadians is so important, and it may

also explain why government and financial institutions have taken

an active role in advocating the promotion of financial literacy

through diverse national campaigns and initiatives.

According to Tina (2012) in her study indicates that young

adults under the age of 35 are the least prepared, based on an

analysis that considered attitudes and behaviors as key

measurements for financial preparedness for retirement. These

findings can be helpful to the younger generations as common

wisdom states that the earlier people start to save for

retirement, the greater the potential that they will achieve

future financial security. Strengthening efforts at improving

their financial education can go a long way to modifying

attitudes and behaviors so that their level of involvement may

increase sufficiently to drive positive information-seeking

behavior and lead them to take action. Onyango (2008), in his

article What Price Pension Reform if Retirees Remain Poor?

Observed that quite often, the elderly people were not

31

necessarily poor when younger . Old age poverty comes about

because, safe and reliable long term savings are rare and they

rarely provide opportunities to convert lump sum savings into

annuities or other instruments which provide a stream of payments

throughout one’s retirement.

According to a study by BMO Institute (2012), to help adequately

prepare for retirement, a person may need to be excited about the

prospects of retiring to become motivated to seek information and

advice, and finally to take action to save for retirement. The

stronger the attitudes and behaviors are before taking the actual

step of saving in retirement accounts, the greater the likelihood

that the chosen financial action will help ensure a comfortable

future retirement. This means that attitudes and behaviors can be

strong predictors of financial preparedness for retirement, and

the earlier these can be shaped, the better prepared a person can

be for retirement.

Carroll (1997), In his study, precautionary saving, has shown

that people with uncertain future earnings who are sufficiently

32

prudent will never borrow, if there is the possibility, however

remote, that they will not earn enough to be able to repay their

debts. If such people expect their earnings to grow over time,

they will nevertheless keep their consumption within their

current incomes, thus inducing a close articulation, or

“tracking,” between consumption and income. In this case,

although people are maximizing their expected life time utility,

as postulated by the life-cycle theory under uncertainty, their

consumption is effectively constrained by their current incomes.

Such behavior is directly contrary to one of the central insights

of the Modigliani model, that the profile of consumption can be

detached from the profile of income, and much more like the pre-

Modigliani and Keynesian accounts of saving.

Very much the same result can be obtained in a theoretical model

in which people want to borrow but cannot. People can save to

smooth out their consumption, but they cannot have consumption

greater than their income, except when they already have some

assets in the bank. In these extreme precautionary or “liquidity

constrained” accounts of saving, consumption is smoothed, not

33

over the whole life-cycle, but over much shorter periods of a few

years at a time.

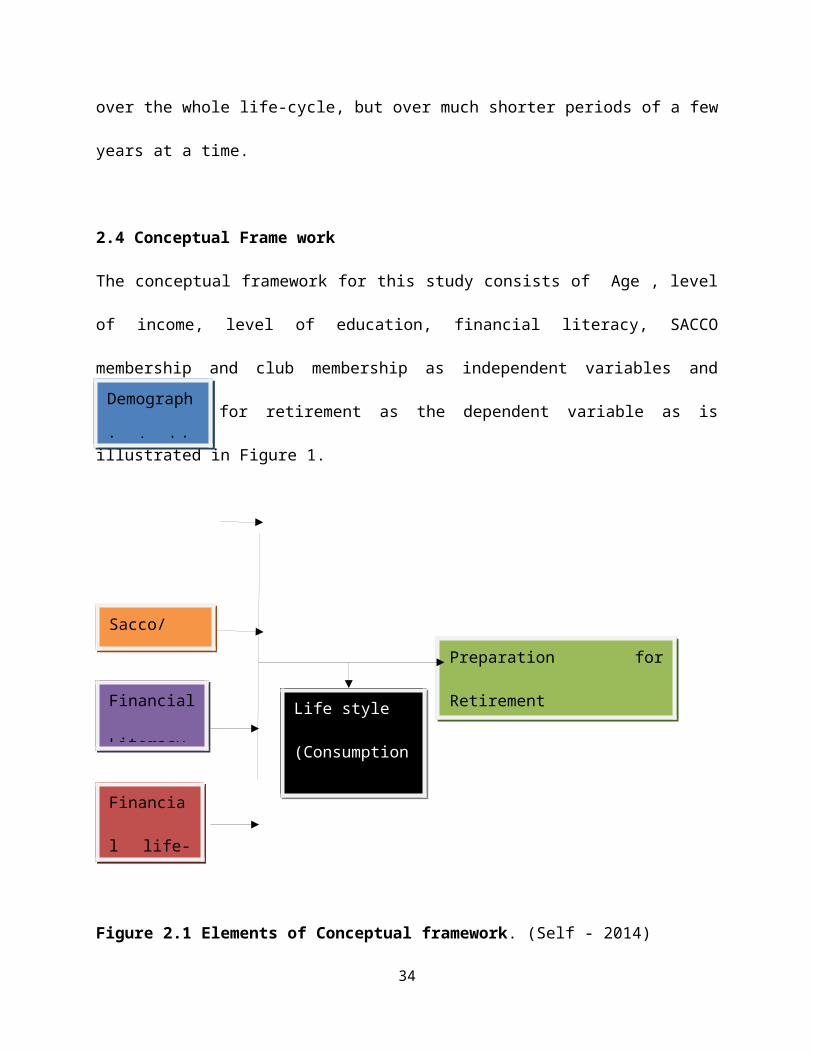

2.4 Conceptual Frame work

The conceptual framework for this study consists of Age , level

of income, level of education, financial literacy, SACCO

membership and club membership as independent variables and

preparation for retirement as the dependent variable as is

illustrated in Figure 1.

Figure 2.1 Elements of Conceptual framework. (Self - 2014)

34

Demograph

ics/ bio

Sacco/

Club

Financial

Literacy

Financia

l life-

Preparation for

RetirementLife style

(Consumption

habits)

All the elements under study are significant in determining how

an employee prepare for retirement. Many scholars have alluded to

the fact that employees with very little income have very

difficult balancing consumption and savings. That means that

employers need to look at their pay structure to support

employees ability to spare some money for retire. However it is

possible for people earning the same amount of money to prepare

differently for retirement because of their lifestyles

(Consumption Habits). Similarly the number of dependents one has

influences the consumption level and thus the amount saved for

retirement. While preparation for retirement is seen by many as a

personal matter scholars agree that investment groups and chamas

help their members to plan for retirement. Chamas and investment

groups provide avenues for saving, investing and provide

financial information. Financial literacy is the variable

considered most significant in supporting one to prepare for

retirement. In fact financial literacy is rated higher than the

socio demographic factors as observed by many scholars. Financial

lifecycle has been considered by scholars as a factor stronger

than age. It has been argued that the closer one is to retirement

the more prepared they are to retire stronger than their age.

That basically means a person planning to retire young will

prepare for retirement more than their age mate or even older

people who want to stay longer in employment. This study will

examine how these factors influence the employees of KPA and the

extent to which other factors might influence their preparation.

35

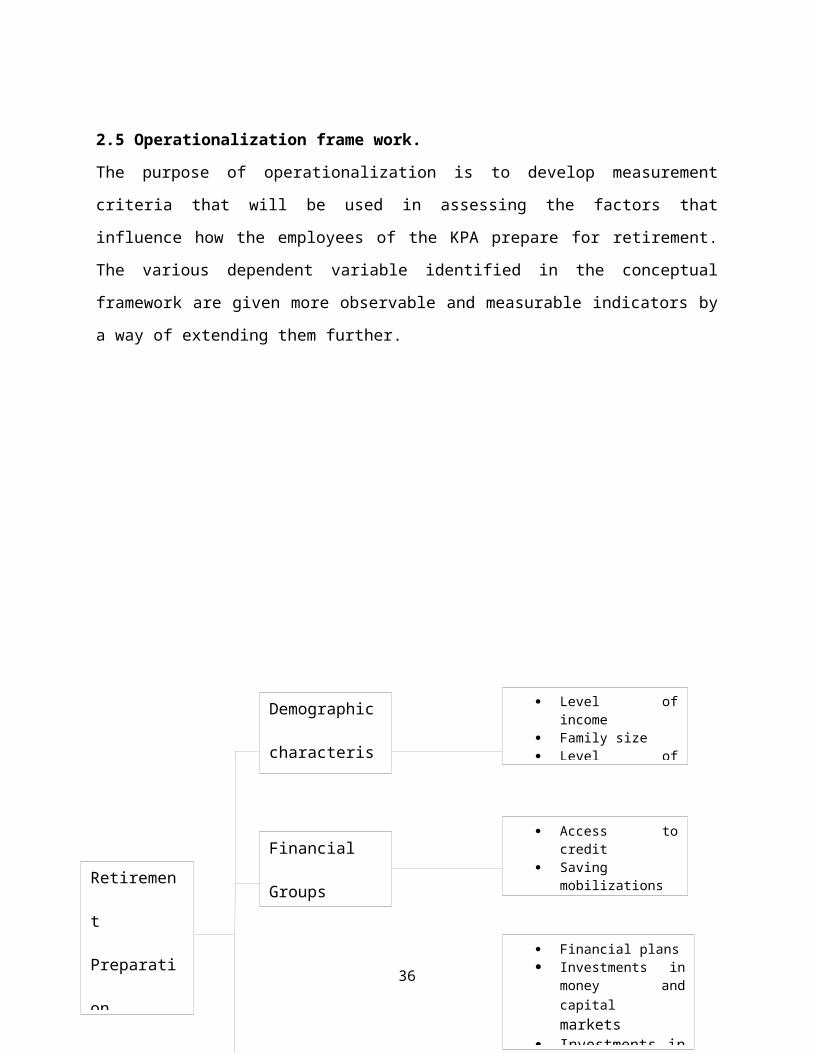

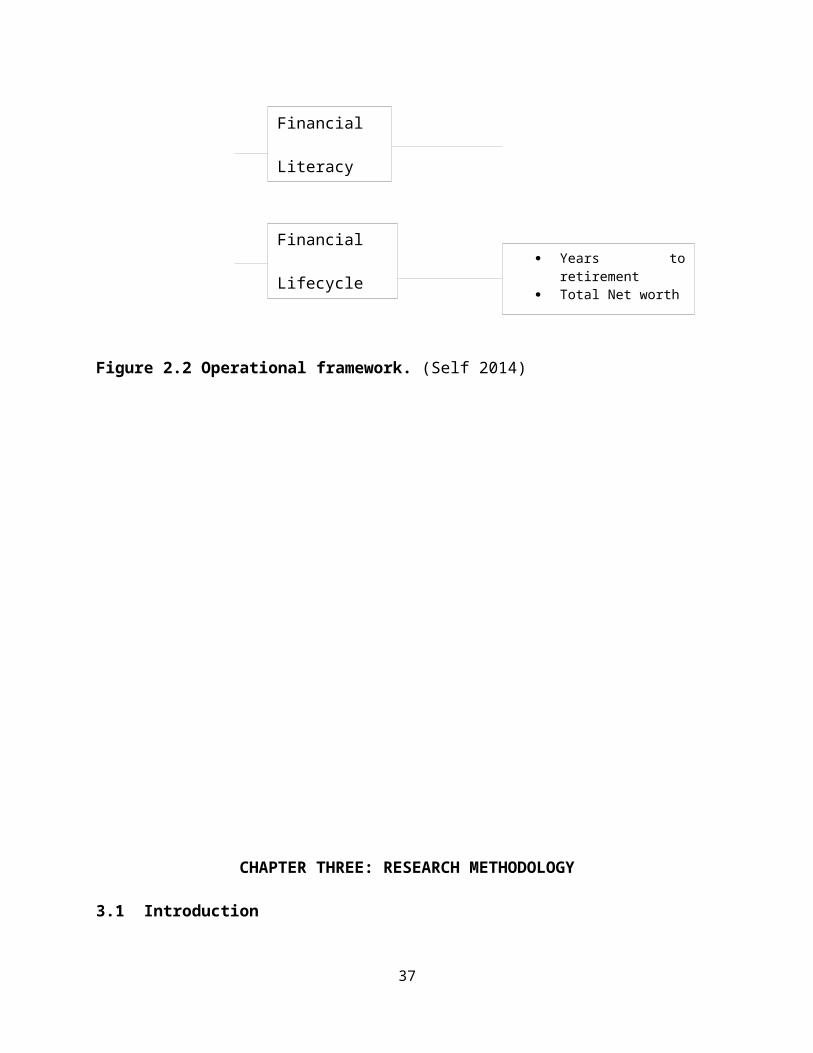

2.5 Operationalization frame work.

The purpose of operationalization is to develop measurement

criteria that will be used in assessing the factors that

influence how the employees of the KPA prepare for retirement.

The various dependent variable identified in the conceptual

framework are given more observable and measurable indicators by

a way of extending them further.

36

Retiremen

t

Preparati

on

Demographic

characteris

tics

Financial

Groups

Access tocredit

Savingmobilizations

Level ofincome

Family size Level of

Financial plans Investments in

money andcapitalmarkets

Investments in

Figure 2.2 Operational framework. (Self 2014)

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction

37

Financial

Literacy

Financial

Lifecycle Years to

retirement Total Net worth

This chapter discusses in detail the research methodology that is

to be used to enable the researcher study factors that influence

employees preparedness for their retirement. It includes research

design, target population, sample size, data collection

instruments, data collection procedure and analysis plan.

3.2 Research Design

The researcher will employ descriptive survey design to make an

inference on the factors that influence employees’ preparedness

for retirement. According to Mugenda and Mugenda (1999) a survey

is an attempt to collect data from members of a population in

order to determine the current status of that population with

respect to one or more variables. Descriptive research design is

a scientific method which involves observing and describing the

behavior of a subject without influencing it in any way. It is a

valid method for researching specific subjects and as a precursor

to more quantitative studies. Descriptive studies report summary

data such as measures of central tendency including the mean,

median, mode, deviance from the mean, variation, percentage, and

correlation between variables. Survey research commonly includes

38

that type of measurement, but often goes beyond the descriptive

statistics in order to draw inferences (Signer's, 1991) .Whilst

there are some valid concerns about the statistical validity, as

long as the limitations are understood by the researcher, this

type of study is an invaluable scientific tool.

3.3 Target Population

A population refers to an entire group of individuals, events or

objects having a common observable characteristic (Mugenda and

Mugenda, 1999). The population for this study comprises of the

7044 employees of KPA, 289 of Kenya Ferry service, 1018 of

Technical University of Mombasa and 4700 from the County

government of Mombasa totalling to 13,051.

3.4 Sampling Technique and Sample Size

A sample is any number of cases less than the total number of

cases in the population from which it is drawn (Ingule and

39

Gatumu, 1996). The sample size will be calculated based on

Yamane’s formula

n = N/(1+Ne2) where:

n= the sample size; N= the size of population; e= the error of 5

percentage points

n=13051 / (1+13051x0.052)

= 388.

Sampling saves time and expenses of studying the entire

population (Borg and Gall, 1989). It is the procedure a

researcher uses to gather people, places or things to study or

the process of selecting a number of individuals or objects from

a population such that the selected group contains elements

representative of the characteristics found in the entire group.

The researcher will use stratified random sampling technique in

selecting the sample representative of the entire workers

population in the selected public institutions. The population

would first be divided into mutually exclusive groups that are

relevant and appropriate and meaningful in the context of the

40

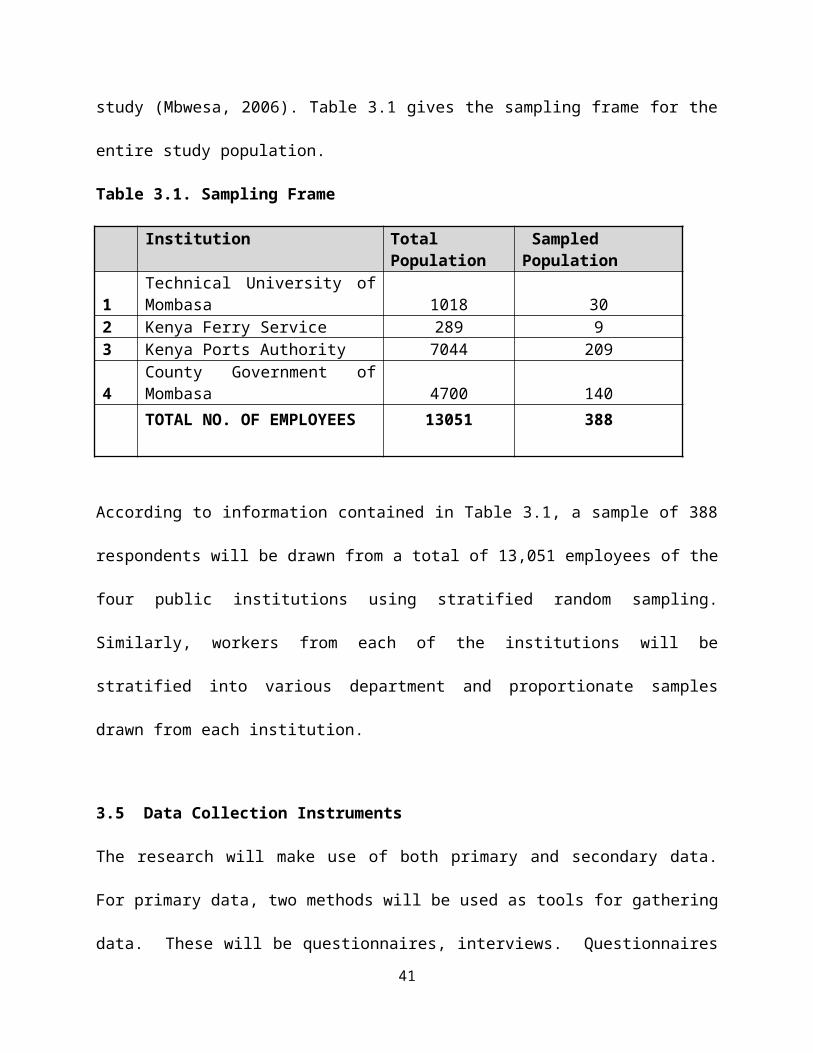

study (Mbwesa, 2006). Table 3.1 gives the sampling frame for the

entire study population.

Table 3.1. Sampling Frame

Institution TotalPopulation

SampledPopulation

1Technical University ofMombasa 1018 30

2 Kenya Ferry Service 289 93 Kenya Ports Authority 7044 209

4County Government ofMombasa 4700 140

TOTAL NO. OF EMPLOYEES 13051 388

According to information contained in Table 3.1, a sample of 388

respondents will be drawn from a total of 13,051 employees of the

four public institutions using stratified random sampling.

Similarly, workers from each of the institutions will be

stratified into various department and proportionate samples

drawn from each institution.

3.5 Data Collection Instruments

The research will make use of both primary and secondary data.

For primary data, two methods will be used as tools for gathering

data. These will be questionnaires, interviews. Questionnaires41

will be particularly preferred since they save time and expenses

which would otherwise be incurred going to the port for many

days. They also increase the chances of getting honest responses

as they provide anonymity of the respondent. The researcher will

also use observation schedules with a few items on how the port

workers behave when in their membership clubs.

The instruments will be prepared in a manner that ensures

validity and reliability of the data so collected. Validity of

research instrument refers to the extent to which a test or

instrument measures what it was intended or supposed to measure

(Mbwesa, 2006). While Reliability of research instruments refers

to the degree to which a research instrument yields consistent

results or data after repeated trials (Mugenda and Mugenda,

1999).

3.6 Data Collection Procedures

After sampling and ensuring of content validity, the researcher

will obtain authority to carry out the study from the Kenya

Methodist University, through the academic supervisors which will

42

enable the researcher to apply for a permit from the KPA. This

will be preceded with the preparation of the research

instruments, testing them and ensure that they are admissible.

This research study will rely on both primary and secondary

sources of data. The primary data will be collected through

questionnaires and through interview schedules. The secondary

data will be collected from archival data got from the SACCOs,

clubs and the Human resource department.

3.7 Ethical considerations

The researcher will adhere to all ethical standards in the course

of the study. The information obtained will be treated with

utmost confidentiality given that its very nature is intimate to

the respondents and is private. This information will thus be

coded to ensure that it does not pose any embarrassment to the

respondent. This is one of the values upon which the respondents

will be willing to respondent to the questions with confidence.

3.8 Data Analysis Plan

43

Data analysis refers to examining what has been collected in a

survey or experiment, and making

deductions and inferences (Kombo and Tromp, 2006). It also refers

to a variety of activities and

processes that a researcher administers to a database in order to

draw conclusions and make certain decisions regarding the data

collected from the field. Activities of analysis involve

summarizing large quantities of raw data, categorizing,

rearranging and ordering data (Mbwesa,

2006).

The data gathered will be analyzed by use of Statistical Package

for Social Sciences (SPSS). The raw data collected will be

treated. This method will include cleaning, coding, data base

creation and analysis. Results of the analysis will be presented

using frequency distribution tables. The relationships will be

investigated using regression analysis. The value of the

coefficient of correlation (R) will be computed to determine the

magnitude and direction of the relationship. The model

44

constructed using the conceptual framework earlier discussed is

as follows:

Y = β0 + β1X1 + β2X2+ β3X3+ β4X4 + ε

Y is the dependent variable representing retirement preparedness;

β0 is a constant factor which is also the value of the dependent

variable when X1, X2, X3, X4 are equal to zero. X1 is the

demographics or bio data of the employees, X2 is the membership

to financial grouping variable, X3 is level of financial literacy

variable and X4 is the financial lifecycle all associated with

preparation to retirement as being explored in this study. β1, β2,

β3 and β4 are constants associated with X1, X2, X3, and X4

respectively. Random error ε represents all other minor effects

on the model which have not been captured. The measures that will

be used in this study will be derived from several criteria,

which have been conceptualized and used in previous empirical

studies on retirement (Danaher & Mattson, 1994).

REFERENCES

45

Alessie, R. and Lusardi, A. ( 2011). Financial literacy adretirement preparation

Journal of Pension Economics and Finance .

Agarwal, S., and D. Laibson, (2009) The age of reason: Financialdecisions over the lifecycle, Brookings Papers on Economic Activity,Fall 2009, 51-101.

Lusardi, A. and O. Mitchell,( 2009). How ordinary consumers makecomplex economic decisions: Financial literacy and retirementreadiness, NBER Working Paper, 15350.

Binswanger, J., and D. Schunk,( 2008). What is an adequatestandard of living during retirement?, CentER Discussion Paper,82.

Bovenberg, L. and C. Teulings, 2007, Saving and investing overthe life cycle and the role of collective pension funds, DeEconomist, 155, 347-415.

Agnew, J., and J. Young, (2007) Literacy, Trust and 401(k) SavingsBehavior. Boston; Center for Retirement Research.

Franco Modigliani (2005). The Life Cycle Theory of Consumption. Rome;Convegno Internazionale

Ameriks, J., & S. Zeldes (2004) How do household portfolio sharesvary with age?, mimeo,

Columbia Graduate School of Business.

Thaler, and Shlomo Benartzi, ( 2004). Save more tomorrow,Journal of Political Economy, London

Ameriks, J., and J. Leahy,( 2003). Wealth accumulation and thepropensity to plan,

Quarterly Journal of Economics,

46

Hilgert, M. and S. Beverly,( 2003). Household financialmanagement: The connection between knowledge and behavior,Federal Reserve Bulletin, 309-322.

Bernheim, D., and D. Garrett,( 2003) The effects of financialeducation in the workplace: Evidence from a survey ofhouseholds. Journal of Public Economics,

Duflo, E., & E. Saez, ( 2003) The role of information and socialinteractions in retirement plan decisions: Quarterly Journal ofEconomics,118, 815-842.

Bernheim, D.,& D. Maki, (2001). Education and saving: The long-term effects of high school financial curriculum mandates,Journal of Public Economics, 80, 435-565.

Bernheim, D.& S. Weinberg, (2001). What accounts for thevariation in retirement wealth among U.S. households? AmericanEconomic Review, 91, 832-857.

APPENDICES

Appendix I Questionnaire

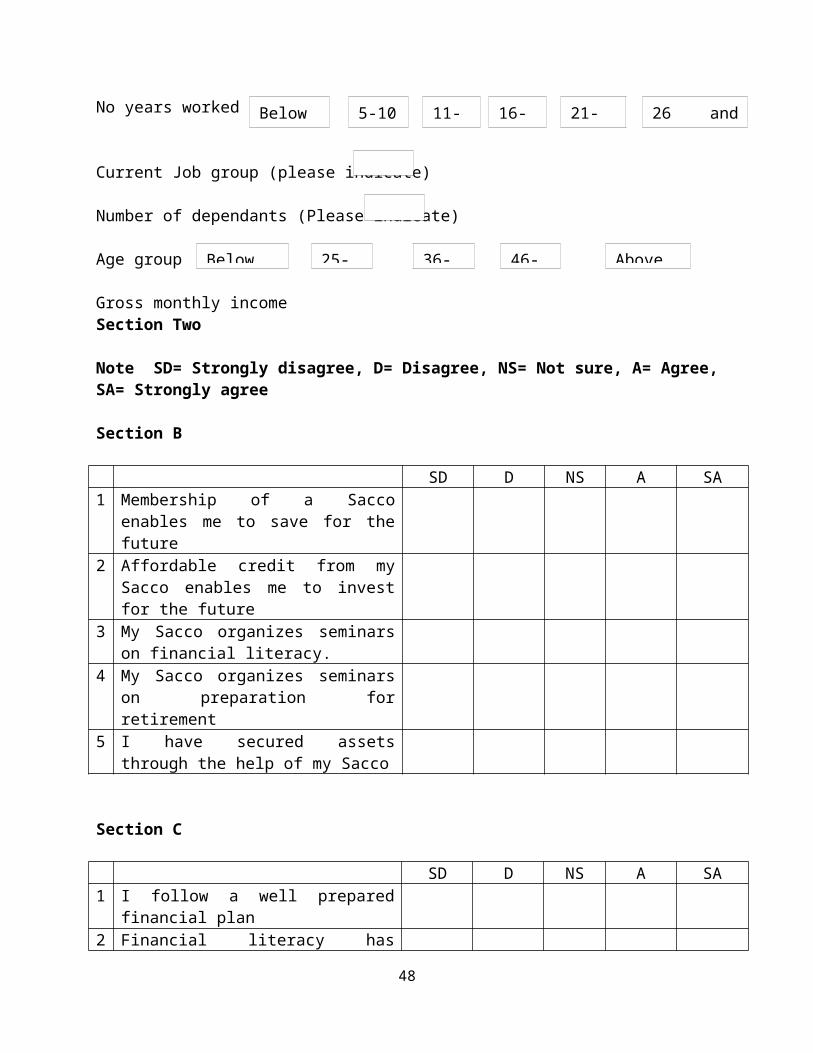

Please fill this questionnaire openly and honestly.Confidentiality will be strictly adhered to, and there will be nomention of your personal name. Provide the following informationby ticking or writing in the appropriate box/ space.

SECTION A: PERSONAL PROFILE

Gender

Highest level of education

47

Male Female

HighPrimar Colle

No years worked

Current Job group (please indicate)

Number of dependants (Please indicate)

Age group

Gross monthly incomeSection Two

Note SD= Strongly disagree, D= Disagree, NS= Not sure, A= Agree,SA= Strongly agree

Section B

SD D NS A SA1 Membership of a Sacco

enables me to save for thefuture

2 Affordable credit from mySacco enables me to investfor the future

3 My Sacco organizes seminarson financial literacy.

4 My Sacco organizes seminarson preparation forretirement

5 I have secured assetsthrough the help of my Sacco

Section C

SD D NS A SA1 I follow a well prepared

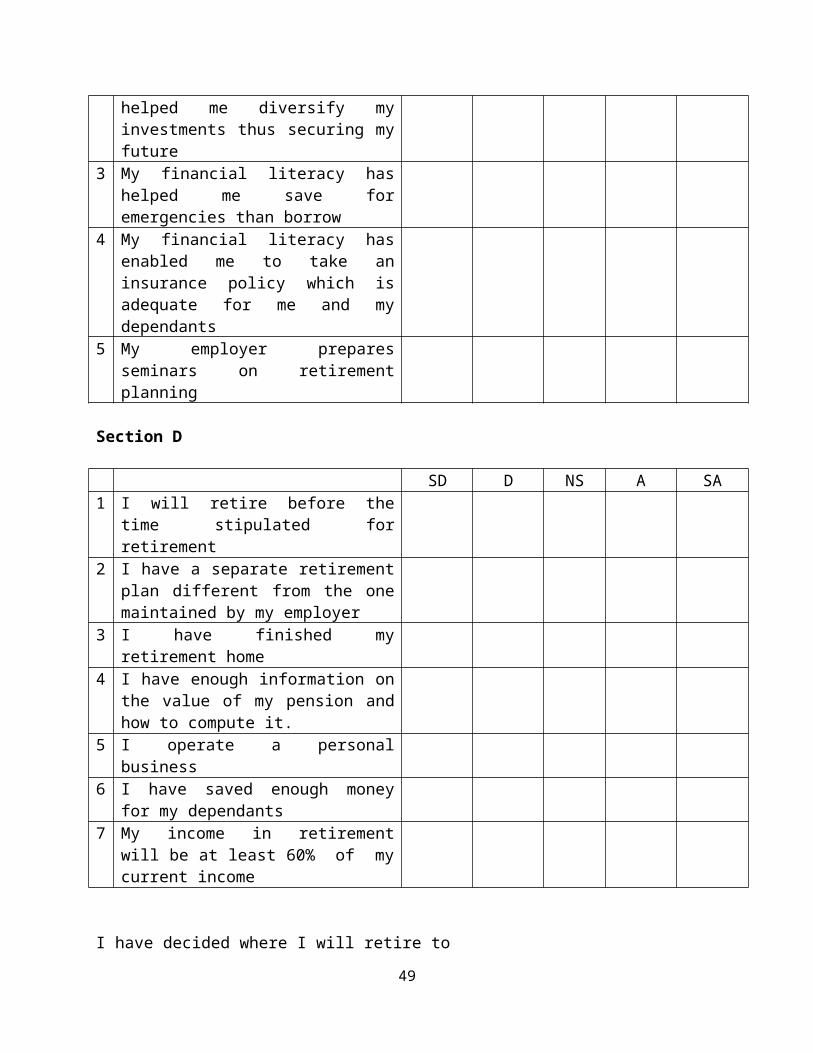

financial plan2 Financial literacy has

48

Below 5-10 11- 16- 21- 26 and

Below 25- 36- 46- Above

helped me diversify myinvestments thus securing myfuture

3 My financial literacy hashelped me save foremergencies than borrow

4 My financial literacy hasenabled me to take aninsurance policy which isadequate for me and mydependants

5 My employer preparesseminars on retirementplanning

Section D

SD D NS A SA1 I will retire before the

time stipulated forretirement

2 I have a separate retirementplan different from the onemaintained by my employer

3 I have finished myretirement home

4 I have enough information onthe value of my pension andhow to compute it.

5 I operate a personalbusiness

6 I have saved enough moneyfor my dependants

7 My income in retirementwill be at least 60% of mycurrent income

I have decided where I will retire to

49

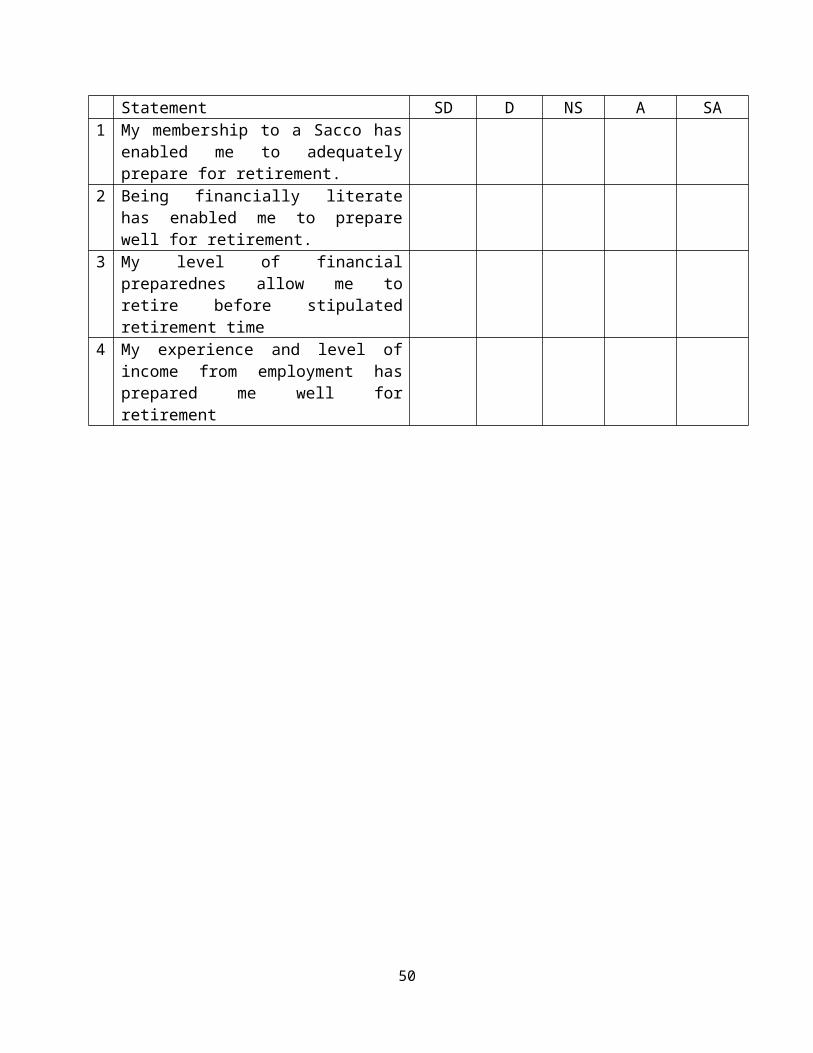

Statement SD D NS A SA1 My membership to a Sacco has

enabled me to adequatelyprepare for retirement.

2 Being financially literatehas enabled me to preparewell for retirement.

3 My level of financialpreparednes allow me toretire before stipulatedretirement time

4 My experience and level ofincome from employment hasprepared me well forretirement

50

Related Documents