Report and Recommendation of the President to the Board of Directors Sri Lanka Project Number: 35304-04 September 2009 Proposed Asian Development Fund Grant for Subprogram 2 Lao People’s Democratic Republic: Private Sector and Small and Medium-Sized Enterprises Development Program

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Report and Recommendation of the President to the Board of Directors

Sri Lanka Project Number: 35304-04 September 2009

Proposed Asian Development Fund Grant for Subprogram 2 Lao People’s Democratic Republic: Private Sector and Small and Medium-Sized Enterprises Development Program

CURRENCY EQUIVALENTS (as of 31 August 2009)

Currency Unit – kip (KN)

KN1.00 = $0.000117 $1.00 = KN8,520.50

ABBREVIATIONS

ADB – Asian Development Bank AFTA – ASEAN Free Trade Area ASEAN – Association of Southeast Asian Nations AusAID – Australian Agency for International Development BOL – Bank of the Lao PDR BSRP – Banking Sector Reform Program CAR – capital asset ratio CBTA – cross-border transit agreement CEPT – common effective preferential tariff CIB – Credit Information Bureau CSP – country strategy and program EA – executing agency EC – European Commission ERO – enterprise registry office ERP – effective rate of protection FDI – foreign direct investment GDP – gross domestic product GMS – Greater Mekong Subregion IA – implementing agency IFC – International Finance Corporation IMF – International Monetary Fund JICA – Japan International Cooperation Agency Lao PDR – Lao People’s Democratic Republic MDG – Millennium Development Goal MOF – Ministry of Finance MOIC – Ministry of Industry and Commerce MPI – Ministry of Planning and Investment NPL – nonperforming loan NSC – National Statistics Center P3D – provincial public–private dialogue PMO – Prime Minister’s Office PPPD – provincial public–private dialogue PSME – Private Sector and SME Development Program RFSDP – Rural Finance Sector Development Program RIA – regulatory impact assessment SEDP – Socio-Economic Development Plan SMEPDO – SME Promotion and Development Office SMEs – small and medium-sized enterprises SOCB – state-owned commercial bank SOE – state-owned enterprise SPS – sanitary and phyto-sanitary standards TA – technical assistance

TBT – technical barrier to trade UNIDO – United Nations Industrial Development Organization VAT – value-added tax WTO – World Trade Organization

NOTES

(i) The fiscal year (FY) of the Government and its agencies ends on 30 September.

(ii) In this report, "$" refers to US dollars.

Vice-President C. Lawrence Greenwood Jr., Operations 2 Director General A. Thapan, Southeast Asia Department (SERD) Country Director G. Kim, Lao PDR Resident Mission Director J. Ahmed, Financial Sector, Public Management and Trade Division,

SERD Team leader K. Bird, Senior Economist, SERD Team members E. Dizon, Administrative Assistant, SERD T. Hla, Economist, SERD S. Ismail, Young Professional (Financial Sector), SERD R. O’Sullivan, Senior Counsel, Office of the General Counsel

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS

Page GRANT AND PROGRAM SUMMARY i

I. THE PROPOSAL 1 II. THE MACROECONOMIC CONTEXT 1

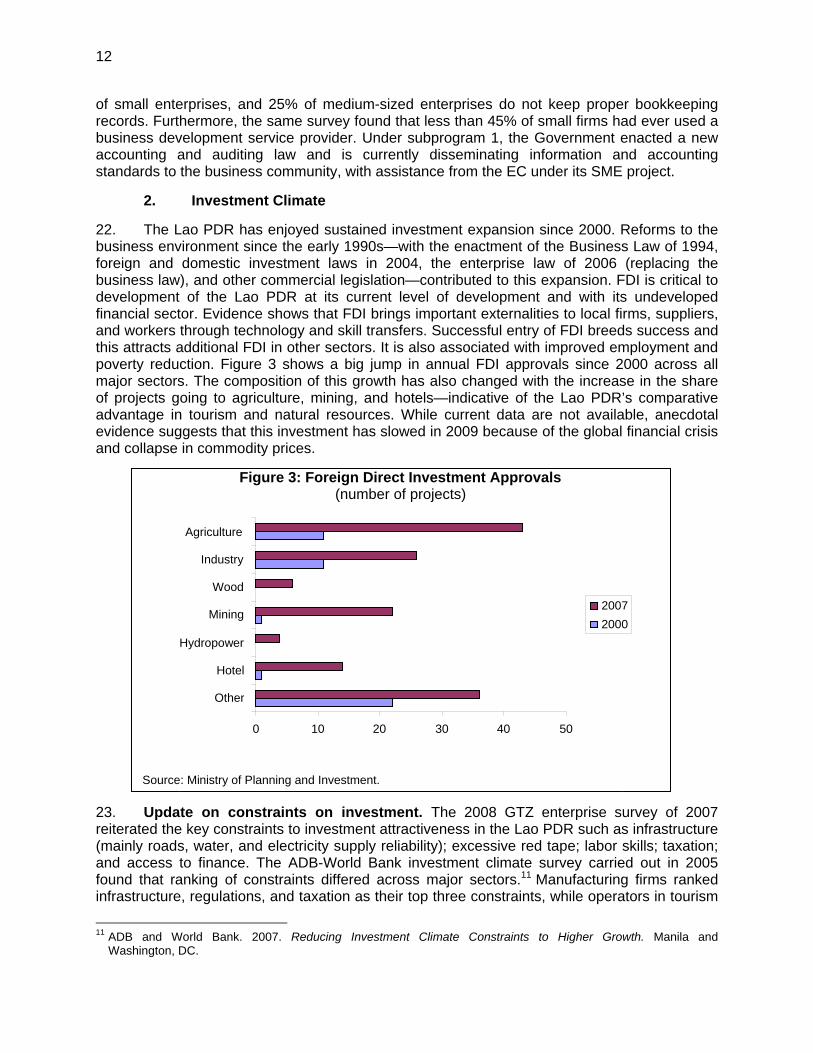

A. The Global Financial Crisis 1 B. The Government's Development Strategy 1 C. The Government and its Development Partners 2

III. THE SECTOR 5 A. Recent Economic Developments and the Impacts of the Global Financial Crisis 5 B. Issues and Opportunities 9 C. Lessons 19

IV. THE PROPOSED PROGRAM 20 A. Impact and Outcome 20 B. Policy Framework and Actions 20 C. Financing Plan 26 D. Implementation Arrangements 27

V. PROGRAM BENEFITS, IMPACTS, ASSUMPTIONS, AND RISKS 30 A. Expected Impacts 30 B. Risks and Mitigating Measures 30

VI. ASSURANCES 31

VII. RECOMMENDATION 31

APPENDIXES 1. Design and Monitoring Framework 32 2. Development Policy Letter 35 3. Policy Matrix for Subprogram 2, Post-Program Monitoring Framework, and Medium-Term Direction 39 4. Development Partners' Coordination Matrix 43 5. Macroeconomic Assessment and Debt Sustainability Assessment 44 6. Private Sector Development Assessment 52 7. Poverty Impact Assessment 61 8. List of Ineligible Items 63 9. Summary Poverty Reduction and Social Strategy 64 10. Performance of Private Sector and SME Development Program Subprogram 2 Triggers 66

GRANT AND PROGRAM SUMMARY Recipient Lao People’s Democratic Republic (Lao PDR) The Proposal A grant of $15,000,000 is proposed for subprogram 2 of the Private

Sector and Small and Medium-Sized Enterprises Development Program (PSME)—the second grant of a program cluster to build on support initiated under subprogram 1, approved by the Asian Development Bank (ADB) in September 2007. Subprogram 2 is to be provided as a single tranche, based on completed prior actions demonstrating satisfactory progress.

Classification Targeting Classification: General intervention

Sector (subsector): Public sector management (economic and public affairs management Themes (subthemes): Private sector development (policy reforms), governance (economic and financial governance), economic growth (promoting macroeconomic stability) Location impact: National (low impact)

Environment Assessment

Category C

The Program Rationale

The core objective of the Government’s Sixth National Socio-Economic Development Plan (SEDP6) 2006–2010 is sustaining high rates of economic growth (about 7%–8% per annum) with poverty reduction. The SEDP6 targets a poverty incidence rate of 23% by 2015 as well as the creation of 652,000 productive jobs from 2006 to 2010. Private sector expansion is considered a key mechanism for achieving these objectives. Poverty rates have declined in the Lao PDR in the past two decades from 46% in 1992 to 33% in 2003, and estimated at 28% in 2008. This reduction has been remarkable, considering the rapid population growth during this period—with as much as 50% of the population now under the age of 20 years. It has been driven by economic expansion, opening up the economy to trade and investment, an increase in rice production, greater urbanization, and an increase in remittances from Laotian workers abroad. It is common to see a sharp reduction in poverty once a country passes a per capita income threshold, as Lao PDR has done. Achieving a further reduction in the poverty rate, of a similar magnitude as the SEDP6 target, will depend on sustaining economic growth at the current rate of 7% per annum over the medium term and mobilizing additional fiscal resources to support long-term development and social spending objectives. The Lao PDR has the potential to accomplish these goals and the private sector will be increasingly relied on to accomplish them.

The ADB country strategy and program (CSP) for 2007–2011 identifies private sector development as a key priority. It has set expansion of formal private sector firms by 15% per annum as an outcome indicator for private sector development. Small and medium-sized enterprises (SMEs) are the overwhelmingly dominant business form in the

ii

Lao PDR, and sound policy suggests that SMEs should be treated as the private sector norm and not the exception. This suggests that the reform agenda should be broad-based, focusing on reducing the transaction costs of doing business and improving predictability in the investment climate. Reforms supporting institutional development in SME policy formulation, access to finance, strengthening the investment climate, and completing the unfinished trade policy regime are crucially important for reducing transaction costs and expanding the private sector, putting economic growth on a more sustainable path, and contributing to poverty reduction.

These measures are taking place in the context of a collapse in commodity prices and severe recession in major export markets. While much of the Government’s current focus is on addressing exigencies arising from the crisis and related fiscal situation, it sees the crisis as an opportunity to build consensus among stakeholders on difficult policy reform issues and to advance its medium-term objectives related to private sector/SME development—recognizing that these reforms are fundamental to supporting higher economic growth rates, lessening reliance on the resource sector for income creation, and reducing unemployment and poverty reduction.

Under subprogram 1, the Government implemented a series of reform measures to the investment climate aimed at reducing the cost of doing business in the Lao PDR. These included the enactment of the Law on Enterprises of 2006, and commencing its implementation, as well as measures aimed at chipping away at its import and export management system. The Government is also committed to preparing for World Trade Organization (WTO) accession talks; this process is influencing the way the Lao PDR views its business climate and trade policy over the medium term. Subprogram 2 builds on reforms initiated under subprogram 1, with the core focus on implementing the enterprise law, including the establishment of the enterprise registry offices, starting a process for regulatory reform, advancing trade policy reforms, and enhancing capacity and staff training on trade policy formulation. These reforms are designed to accomplish: (i) improve institutional coordination in SME policy formulation and better access to finance,(ii) strengthen investment climate, and (iii) improve trade policy and capacity development. In response to the global economic crisis, a post-program monitoring framework is added at the subprogram 2 phase. The Government and ADB have agreed to a post-PSME framework in the next 12 months, creating the basis for continuous policy dialogue and engagement during the critical period of 2009–2010. The monitoring framework focuses on the Government’s short-term plan advancing its reforms in business climate, trade policy, and trade facilitation (a new component) supported by ADB and other development partners’ technical and program assistance. It may provide the basis for a second-generation PSME in the future.

iii

The reform program was prepared by a joint team of representatives of the Government and ADB.

Impact and Outcome

The impact of subprogram 2 of the PSME is to achieve sustainable economic growth in the non-resource sector, supported by increased contribution of the private sector and SMEs. The outcome of subprogram 2 is an improved business environment where the private sector and SMEs operate efficiently and effectively. The PSME includes a series of policy reforms that underpin the key priorities of the Lao PDR’s Sixth Socio-Economic Development Plan and its sector strategies. These reforms are designed to accomplish the following results.

(i) Improve institutional coordination for SME policy and access to finance by (a) strengthening the institutional framework for SME policy formulation; and (b) improving SME access to finance through improvements in accounting rules and guidelines and development of nonbank financial instruments.

(ii) Strengthen investment climate by (a) implementing the enterprise law, and (b) other policy reforms aimed at reducing transaction costs of doing business in the Lao PDR; and (c) more transparency in the regulatory environment affecting SMEs.

(iii) Improve trade policy and capacity development by (a) reforming the import–export management system including making measures more transparent and over the medium term, reforming the controlled list of imports; and (b) strengthening indigenous capacity to carry out trade policy analysis.

Financing Plan A grant of $15,000,000 from ADB’s Special Funds resources will be

provided for subprogram 2 of the PSME with terms and conditions set forth in the draft Grant Agreement.

Period and Tranching

The subprogram 2 period is from October 2007 to September 2009, with a single tranche grant of $15 million to be disbursed when the Government has met the conditions for grant effectiveness.

Counterpart Funds The Government will use the local currency counterpart funds

generated by the grant proceeds to meet program expenditures and associated costs of reform and to help maintain current levels of social expenditure.

Executing Agency Ministry of Industry and Commerce (MOIC). MOIC will be responsible

for coordinating the implementation and sustaining of PSME reform actions.

iv

Implementation Arrangements

The Bank of Lao PDR (BOL), Ministry of Finance (MOF) and the Ministry for Planning and Investment (MPI) are the Implementing Agencies (IAs). MOIC will establish a PSME steering committee, chaired by the minister of industry and commerce and comprising senior officials from BOL, MOF, and MPI. The committee will meet twice a year to monitor progress and oversee implementation of the PSME, and to provide guidance and direction to the Executing Agency (EA) and IAs.

Procurement The grant proceeds will be used to finance the full foreign exchange

costs (excluding local duties and taxes) of items produced and procured in ADB member countries, excluding ineligible items and imports financed by other bilateral and multilateral sources.

Program Benefits and Beneficiaries

The program cluster will provide the following benefits.

(i) Improved investor confidence through completion of implementation of the new enterprise law and a new investment law that provides for national treatment.

(ii) Lower transaction costs for business because of streamlined business start-up procedures, a reduction in red tape, and reform of remaining non-tariff barriers, which will open new opportunities, increase investment and productivity, boost the economy, and increase incomes and create jobs, and sustainable reduction in poverty.

(iii) Strengthened institutional development through raising capabilities in the EA and IAs to carry out trade, investment, and SME policy analysis with the aim of improving the quality of policy, institutional processes for policy making. Posting regulations on the SME Promotion and Development Office (SMEPDO) website will also contribute to institutional development through better regulatory transparency.

Risks and Assumptions

The Program is firmly embedded in the SEDP6, the Government’s new SME strategy, and ongoing business climate reforms. The assumptions underlying the Program include the following:

(i) Macroeconomic stability is maintained. (ii) The Government will stay on course with key business

regulatory reform measures. (iii) The Government stays on track with its preparations for

WTO accession. However, there are risks to the Program:

(i) In transitional economies, maintaining macroeconomic stability––reflected in low inflation and a stable exchange rate––is critical for investor confidence and private sector growth. The Lao PDR is particularly vulnerable to macroeconomic instability because of weak institutions. It also faces emerging fiscal stress and macroeconomic

v

challenges in the context of the fall in resource revenues, which threaten to undermine recent gains in social spending and poverty reduction. The Government recognizes these risks and is undertaking measures to raise revenue and strengthen public expenditure management, with the assistance of development partners including ADB.

(ii) The capacity of agencies to implement reforms may be constrained by resources and other emerging priorities. The PSME reduces this risk by limiting the policy triggers to a small number of high-priority, high-impact policy reforms under the jurisdiction of the EA and a limited number of IAs (BOL, MPI, and MOF), and by attaching technical assistance (TA) to each policy trigger.

(iii) There will be resistance to some of the reforms from vested interests, including the dominance of the state enterprise sector in some sectors. Reforms to the import–export management system and institutionalizing economic governance reforms––i.e., red tape review process––are likely to be a lengthy process. Resistance may also come from entrenched cultural and political economy factors that may slow market economy reforms and market competition. However, these risks are mitigated by the following factors: (a) the PSME strategic approach is to focus efforts on supporting the Government’s initiatives, and (b) reforms will focus on areas where there is political will and some measure of capacity. This has been demonstrated by the successful implementation of the enterprise law and establishment of the enterprise registry, which has resulted in substantial cuts in business compliance costs and 5,000 enterprises registering for the first time ever.

I. THE PROPOSAL

1. I submit for your approval the following report and recommendation on a proposed grant to the Lao People’s Democratic Republic (Lao PDR) for subprogram 2 of the Private Sector and Small and Medium-Sized Enterprises Development Program (PSME). The program design and monitoring framework is in Appendix 1.

II. THE MACROECONOMIC CONTEXT

A. The Global Financial Crisis

2. The proposed second subprogram of the PSME comes at a critical moment for the Lao PDR. It is designed to maintain the momentum of key development efforts at a challenging time of lower commodity prices and a recession last seen in 1998. The impact on the Lao PDR economy of the first round effects of the global financial crisis has been negligible because of the low level of development of the Lao PDR financial sector and limited exposure to international credit markets. The major impact arises from the second round effects of the collapse in commodity prices and recession in major export markets on the real sector and the Government’s fiscal situation. Copper prices, for instance, have fallen by more than half in the last 12 months, significantly affecting revenue flows to the national budget. The Government expects further stress on the fiscal situation in 2010 as tax revenue from the commodity sector is expected to drop substantially as corporate losses are carried over. In the real sector, the Lao PDR economy is also closely linked with the Thai economy, so it is vulnerable to shocks transmitted from Thailand through channels such as extensive border trade, investment, tourism, and remittances from overseas workers. Thailand began to experience recessionary conditions in the fourth quarter of 2008 and this has clearly had an impact (albeit lagged) on the Lao PDR real sector through a subsequent drop in tourist arrivals and border trade. 3. The International Monetary Fund (IMF) projects an economic slowdown in the Lao PDR from a 7.5% economic growth rate in 2008 to 4.5% in 2009. Also the international consensus is that the global economy may only experience a gradual recovery in 2010 and this will affect Lao PDR's economic growth prospects next year. Given constraints on raising budget financing, the Government has opted not to provide a fiscal stimulus—instead, it will protect and maintain public spending and therefore its poverty reduction goals. With declining resource revenues, the Government is projecting a budget deficit of about 5% of gross domestic product (GDP) in 2009, including a budget financing shortfall of about $50 million–$60 million. While much of the Government’s current focus is necessarily on addressing exigencies arising from the crisis and related fiscal situation, it also views the crisis as an opportunity (i) to build consensus among stakeholders on difficult policy reform issues, and (ii) to advance its medium-term objectives related to private sector and small and medium-sized enterprises (SMEs) development. It recognizes that these reforms are fundamental to supporting higher economic growth rates, lessening reliance on the resource sector for income creation, and reducing unemployment and poverty. B. The Government’s Development Strategy

4. In 2006, the Government announced its Sixth Five-Year National Socio-Economic Development Plan (SEDP6), 1 2006–2010, setting out the country’s development priorities,

1 Committee for Planning and Investment, Government of the Lao PDR. 2006. National Socio-Economic

Development Plan, 2006–2010. Vientiane.

2

policy agenda, programs, and projects for the current period. A key pillar of the SEDP6 is to achieve higher and more sustainable economic growth and create jobs through private sector development—with emphasis on commercial agriculture, rural development, infrastructure development, and fostering SMEs. To help implement the SEDP6 priority for private sector growth, the Government adopted a range of sector-specific strategies, most with a time-bound implementation plan and clearly defined ministerial responsibilities, some of which are supported by Asian Development Bank (ADB) sector programs and technical assistance (Figure 1). The SME strategy outlines a road map for longer term development of the sector, including regulatory reform and improved access to finance. The Law on Enterprises of 2006 reflects reform priorities under the SME strategy and its implementation, and is the responsibility of the Ministry of Industry and Commerce (MOIC). MOIC’s trade policy priorities are anchored in its World Trade Organization (WTO) accession efforts, and include reforming its import and export management system and trade facilitation (such as enhancing its sanitary and phytosanitary regulatory system). The Ministry of Finance (MOF) has a public financial management reform program with supporting technical assistance (TA) from ADB and other development partners, and includes the development of a medium-term expenditure framework, internal control systems, and accounting reforms. The Government has also drafted a financial sector development strategy (up to 2020), which has been submitted to the Prime Minister’s Office (PMO) for approval. The strategy covers development of the banking sector, nonbank financial institutions, microfinance, the capital market, and financial sector infrastructure. C. The Government and its Development Partners

5. ADB’s country strategy and program (CSP) 2007–2011 for the Lao PDR identified private sector development as a key thematic initiative.2 The CSP emphasizes that ADB will assist the Government to improve the climate for private sector development through support for policy, institutional, and regulatory reform in sectors in which ADB operates—transforming the agriculture sector from subsistence farming to a commercial orientation, improving basic transport and power infrastructure, strengthening the regulatory regime governing financial institutions, restructuring state-owned commercial banks, improving investment regulations, fostering SME growth, mobilizing resources and broadening access to financing for private sector development, and enhancing the soundness and sustainability of public finance. 6. The PSME program operationalizes the CSP by providing support for business climate and trade reforms and related capacity building at the relevant agencies. The program is structured as a cluster and aims to help the Government achieve its medium- to long-term goals of sustained economic growth of 7%–8% per annum, expansion of the private sector, and poverty reduction. The PSME focuses on three core areas directly affecting private sector development and growth: (i) institutional coordination in SME policy formulation and access to finance, (ii) investment climate, and (iii) trade policy and capacity development. Besides advancing the policy reform agenda, a core objective of the PSME program is capacity development at the relevant agencies, and staff training to undertake analytical work and strengthen policy formulation. The PSME builds on and continues ADB’s policy dialogue with the Government in this area, which has been ongoing since 2004. This engagement has contributed to a number of significant developments in recent years, including formulation of a new enterprise law, its implementing decrees such as the negative list, as well as development of the SME strategy.

2 ADB. 2006. Country Strategy and Program (2007–2011): Lao People’s Democratic Republic. Manila.

3

7. Medium-term programmatic approach. Key features of the PSME include (i) two single tranche operations, with a well-defined, medium-term framework specified at the outset and including completion of high-impact reforms prior to consideration by ADB’s Board of Directors; (ii) triggers for the subsequent subprogram to support continuity of dialogue with the Government, development partners, and other stakeholders; and (iii) a limited number of well-targeted policy actions aimed at achieving high-impact outcomes regarding improvement of the enabling environment for private sector development. In this way, the Program provides a

Government Sector Strategies

PSME Cluster Series of two single tranche grants from 2007 to 2009 Post-program monitoring framework, 2009–2010

ADB Sector Programs and TA

Core Area 1 Institutional coordination for SME policy and access to finance

SME Strategy

Draft financial sector strategy

Banking Sector Reform Program (completed March 2009)

Rural Finance Sector Development Program (ongoing)

Proposed TA on enhancing banking sector supervision

Core Area 2 Strengthening the investment climate

Implementation of the 2006 Law on Enterprises

Reform of the investment laws

Red tape reform

GMS cross-border transit agreement

Strengthening Private Sector and SME Development TA

Core Area 3 Improving trade policy and capacity development

WTO accession efforts

Reforms to the import and export management system

Reforms to customs and other trade facilitation

GMS Trade Facilitation and Investment Group

Strengthening Private Sector and SME Development TA

Figure 1: Overview of the PSME Program Cluster Strategic Framework: Lao PDR Sixth Five-Year

National Socio-Economic Development Plan, 2006–2010

Key Economic and Social Outcomes of the SEDP6: (i) Economic growth rises to 7%–8% per annum by 2015 (ii) Private sector and SME expansion (iii) Reduction in the incidence of household poverty from 33% in 2001 to 23% by 2015

ADB = Asian Development Bank, GMS = Greater Mekong Subregion, Lao PDR = Lao People’s Democratic Republic, PSME = Private Sector and SME Development Program, SEDP = Socio-Economic Development Plan, SMEs = small and medium-sized enterprises, TA = technical assistance, WTO = World Trade Organization. Source: ADB. 2007. Report and Recommendation of the President to the Board of Directors on a Proposed Asian Development Fund Grant to the Lao People's Democratic Republic for the Private Sector and Small and Medium-Sized Enterprises Development Program Cluster (Subprogram 1). Manila.

4

coherent medium-term reform strategy with two discrete but linked subprograms and a strong emphasis on performance, as the decision on whether to proceed with the next subprogram is contingent on overall satisfactory performance of the triggers. It recognizes the necessity for flexibility in the reform measures, with provisions for incorporating lessons and responding to changes in the external environment in the design of subprogram 2. 8. The Program has the following three phases:

(i) Subprogram 1. Financed by ADB ($5 million) in 2007, subprogram 1 focused on key legislative reforms to the enterprise registration regime; it began the process for SME policy and institutional strengthening, and trade policy reforms; and created the basis for continuous policy dialogue and engagement over 2007–2009 (subprogram 2).3

(ii) Subprogram 2. The current phase, to be financed by ADB ($15 million), focuses on implementing business climate reforms and SME institutional development. Subprogram 2 supports the Government’s efforts to improve trade policy capacity, especially as the Lao PDR increases its efforts preparing for WTO accession.

(iii) Post-program monitoring framework. In response to the global economic crisis, a post-program monitoring framework is a new instrument added to subprogram 2. The Government and ADB have agreed to a post-PSME program framework in the next 12 months, creating the basis for continuous policy dialogue and engagement during the critical period of 2009–2010. The monitoring framework focuses on the Government’s short-term plan advancing its reforms in business climate, trade policy, and trade facilitation (a new component) supported by ADB and other development partners' technical and program assistance. It may provide the basis for a second-generation PSME program in the future.

9. Government and development partner coordination. The PSME program works closely with other development partners—the Australian Agency for International Development (AusAID), the European Commission (EC), German development cooperation through GTZ, the International Finance Corporation (IFC), Japan International Cooperation Agency (JICA), and the World Bank—and stakeholders to provide support to private sector development in the Lao PDR (Appendix 4). In particular, the EC is providing parallel financing for TA (€3 million) designed to support implementation of the PSME program cluster and to work closely with ADB to broaden the private sector and SME reform agenda, and support the Government’s efforts to strengthen institutional capacity for policy formulation. The ADB and EC teams are joint members of the Government’s SME steering committee, chaired by the minister of industry and commerce, established under the PSME program. Program progress is reported to the steering committee every semester. ADB also participates in the Lao Business Forum and works with the Mekong Private Sector Facility of the IFC. The forum, established in 2005, comprises representatives from the Lao PDR private sector, senior government officials, stakeholders, and development partners. The primary purpose of the forum is as a vehicle to promote ongoing dialogue between the private sector, the Government, and other stakeholders on private sector development issues.

3 ADB. 2007. Report and Recommendation of the President to the Board of Directors on a Proposed Asian

Development Fund Grant and Technical Assistance Grant to the Lao People's Democratic Republic for the Private Sector and Small and Medium-Sized Enterprises Development Program Cluster (Subprogram 1). Manila.

5

III. THE SECTOR

A. Recent Economic Developments and the Impacts of the Global Financial Crisis

10. Sustained economic growth. In 2008, the Lao PDR economy continued the strong expansion that began in 2005. The economy is estimated to have grown by 7.2% in 2008, which is similar to rates achieved in 2006 and 2007 and well above the average growth rate of 6% per annum from 1990 to 2004. Table 1 presents data on key indicators over 2004–2008 to show the improved macroeconomic performance in recent years. Robust growth in 2008 has occurred across all the major economic sectors—the mining and power sectors, and to a lesser extent manufacturing, were the main engines of growth, followed by services and agriculture. In 2007, exports of goods and services increased by 17% to reach $1.3 billion and they are estimated to have grown about 24% in 2008. Tourism also performed well. More than 1.6 million tourists visited the Lao PDR in 2007, generating over $200 million. About 1.8 million visitors are estimated to have visited the Lao PDR in 2008, providing impetus for continuation of a construction boom in Vientiane and Luang Prabang, two major tourist destinations. Indicators of investment goods (such as domestic cement sales, other construction materials, and imports of capital goods) suggest investment growth was strong in 2007 and 2008. Foreign investment in the non-mining sector increased, with investments in sectors where the Lao PDR has a comparative advantage (tourism and commercial agriculture). 11. Macroeconomic conditions. The current account in the balance of payments remained in deficit at 16% of GDP in 2008, driven by investments in the resource sectors. Grants and foreign investment flows lifted gross international reserves in 2007 and the first half of 2008, but international reserves declined in the second half of 2008 as investment inflows slowed with the onset of the global financial crisis. Overall, the import coverage of gross international reserves was 3.4 months at the end of December 2008. Inflation was a problem in the first half of 2008, as the surge in international food prices transmitted into domestic inflation—reaching 11% in August 2008 on a year-on-year basis—but it has since fallen to –1.5% in July 2009. Other macroeconomic indicators (such as the public debt–GDP ratio) continue to improve. Estimates of the budget outturn for the fiscal year (FY) 2008 indicated revenues slightly surpassing the budget program target and expenditures in line with the budget program, resulting in an overall national government budget deficit of 2.1% of GDP, down from 2.8% (Appendix 5).4 12. Remarkable progress in reducing poverty. Using the national poverty line, the incidence of poverty in the Lao PDR has declined from 46% in 1992 to an estimated 28% in 2008. The reduction in the poverty rate took place as the economy began to recover from the Asian financial crisis in the late 1990s, and much of it took place in the poorest parts of the country. Factors contributing to this remarkable reduction in poverty incidence include sustained per capita income expansion, greater labor mobility between rural and urban areas and urbanization, higher rice production, private sector expansion, and improvements in market access both domestically and in neighboring countries. The Lao PDR is on track in terms of meeting the income poverty Millennium Development Goals (MDGs) by 2015. 13. Impact of global financial crisis on the Lao PDR. The direct and indirect effects of the global financial crisis on the Lao PDR banking system have been limited, as financial sector assets account for less than 15% of GDP, its exposure to international credit markets is limited, and the Government does not access international commercial credit markets to finance its budget. The major impact on the Lao PDR economy comes from the second round effects of 4 Based on the IMF definition of the overall budget balance. The IMF definition differs slightly from the Government’s

definition in that the IMF excludes amortization of debt from the calculation of the budget balance.

6

global demand destruction, the collapse in international commodity prices, and their feedback into the Government’s fiscal situation. In particular, the Lao PDR economy is linked to Thailand’s economy. ADB staff estimates indicate that a 1% decline in Thai economic growth will result in a 1%–2% decline in Lao PDR economic growth in the non-resource sector. Thailand began to experience recessionary conditions in the fourth quarter of 2008 and the economy contracted by 6% in the first quarter of 2009 on a year-on-year basis. The impact on the Lao PDR real sector has not been immediate; instead, a transmission lag is being observed through a subsequent drop in tourist arrivals of about 10% in the last 6 months, with spillovers to tourism-related sectors and sluggish border trade. Garment exports—mainly to the European markets—fell in 2008 and are expected to drop significantly from the second quarter of 2009 onward.

14. With this background, the Government has revised its macroeconomic framework and projects growth of 5.5% in 2009. The IMF projects lower economic growth of 4.5% based on faltering garment exports, a fall in resource revenues, and a slowdown in foreign investment. This translates to a negative output gap of 2.5% of GDP (i.e., actual economic growth is 2.5 percentage points below the potential economic growth rate, Figure 2e). It is the potential feedback from a slowing real sector to the banking sector that has increased vulnerabilities of the domestic banking sector. While the banking sector is in a better financial situation in 2009 than 3 years ago, the capital asset ratios of the state-owned commercial banks are still low and they remain vulnerable to relatively modest shocks. Banks will be tested through the impact of the crisis on their borrowers, with the number of nonperforming loans expected to rise if the poor economic conditions persist (Appendix 5).

15. Feedback to fiscal policy. The global financial crisis has affected fiscal policy in two ways. First, the collapse in commodity prices, especially copper (the main mineral export), from the third quarter of 2008 has reduced resource revenue flows to the national budget by about 1% of GDP below budget target. Fiscal stress is expected to increase in 2010 as profit taxes from the resource sector shrink further on the carryover of losses from FY2009. Second, because of constraints in budget financing, the Government is unable to provide for a fiscal stimulus; instead, its priority is to maintain public spending. As a result of the shortfalls in resource revenues, the Government projects that its budget deficit will rise from the initial target of 3.4% of GDP to about 5% in 2009, creating a budget shortfall of $50 million–$60 million. The deficit could be higher if non-resource tax collection falls short of its budget target in 2009. Based on the IMF definition of the overall budget balance, the deficit could be as high as 7.9% (Appendix 5). The fiscal constraint is putting at risk the recent gains in social spending, especially in education.

7

Table 1: Key Macroeconomic Indicators in the Lao People’s Democratic Republic (percentage of GDP, unless otherwise indicated)

Indicator

2005 2006 2007

2008 Real Sector Real GDP growth (%) 7.1 8.1 7.9 7.2

Agriculture 2.5 3.5 6.2 2.0 Industry 15.9 21.5 6.5 10.0 Services 6.7 5.3 12.1 9.7

Merchandise trade ($ million)a Exports 697.0 1,133.0 1,321.0 1,639.0 Imports 1,270.0 1,589.0 2,156.0 2,816.0

International visitor arrivals (’000) 1,095.0 1,215.0 1,623.0 1,767.0 Monetary Sector Annual inflation (%, average of period) 7.2 6.8 4.5 7.6 Annual inflation (%, end of year) 8.8 4.7 5.6 3.2 Broad money (% annual growth) 8.1 17.2 38.7 18.4 External public debt (end period) 81.0 63.0 59.1 53.1 External public debt service ratio (% of exports)

7.7 5.7 12.5

10.3

Current account balance (17.8) (10.3) (15.8) (16.5) Gross official reserves ($ million) 238.0 336.0 528.0 636 Public Finances National government overall budget balance (authorities definition)

(3.0) (2.9) (2.0)

(3.4)

National government overall budget balance (IMF definition)b

(3.3) (3.1) (2.8) (2.1)

Revenues and grants 14.5 15.8 15.6 15.9 Tax and nontax revenues 12.4 14.0 14.3 14.5 Of which resources 1.1 2.2 2.7 2.9 Grants 2.0 1.7 1.3 1.5 Expenditures 17.4 18.6 17.7 19.3 Current expenditures 9.1 8.9 10.3 11.3 Capital and onlending 7.2 8.1 7.0 7.1

( ) = negative, GDP = gross domestic product, IMF = International Monetary Fund, Lao PDR = Lao People’s Democratic Republic. a Estimate only. b The IMF definition of overall budget balance differs slightly from the Government’s definition in the treatment of amortization of debt and other terms. Consequently, based on the IMF definition, the overall budget balance was 2.1% in 2008 compared to the government-defined budget estimated at 3.4% of GDP.

Sources: Ministry of Finance, Ministry of Industry and Commerce, and Department of Statistics, Lao National Tourism Authority, and IMF. 2009. Article IV Consultation 2009.

8

Figure 2: Key Economic Indicators (a) Lao PDR and Thailand economic growth rates (b) Inflation rates in the Greater Mekong Region

-15

-12

-9

-6

-3

0

3

6

9

1219

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

08

Lao PDR Lao PDR (NR) Thailand

0

5

10

15

20

25

30

Jul-0

3

Nov-03

Mar-04Ju

l-04

Nov-04

Mar-05Ju

l-05

Nov-05

Mar-06Ju

l-06

Nov-06

Mar-07Ju

l-07

Nov-07

Mar-08Ju

l-08

Viet Nam Cambodia NE Thailand Lao PDR

(c) Monetary aggregates and credit expansion (d) Fiscal deficit % of GDP

-40

-20

0

20

40

60

80

Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07

M1 M2 Credit to the economy

0

1

2

3

4

5

6

7

2001 2002 2003 2004 2005 2006 2007 2008

defic

it %

GD

P

0.0

1.0

2.0

3.0

4.0

5.0

6.0

depo

sits

% G

DP

Overall Deficit Overall Deficit (NR) Gov deposits

(d) International prices of gold and copper (e) Output gap and fiscal stance

0

2000

4000

6000

8000

10000

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

0

200

400

600

800

1000

1200

Copper Gold

-3

-2

-1

0

1

2

3

4

2004 2005 2006 2007 2008 2009

Output Gap Fiscal Stance

Positive output gap/fiscal expansion

Negative output gap/fiscal contraction

Note: NR = non-resource sector budget refers to the national government budget less resource revenue inflows; M1 (or money supply) refers to cash in circulation and demand deposits; M2 (broad money supply) equal M1 plus term deposits. GDPp = potential GDP growth and is estimated using the Hodrick-Prescott filter, which estimates a non-linear trend. The output gap is the difference between potential and actual economic growth. Fiscal stance is calculated as the percentage point change in the ratio of the overall government budget deficit to GDP. Sources: Bank of the Lao PDR, International Monetary Fund, and Asian Development Bank staff calculations.

9

B. Issues and Opportunities

16. The private sector is characterized by the dominance of micro, small, and medium-sized enterprises. The most recent data on firm numbers and size is from the 2006 industrial census carried out by the National Statistics Office (Table 2).5 The census reports 126,913 enterprises operating in the Lao PDR in 2006, of which 23% are located in Vientiane. Only 2.4% of enterprises have 10 or more employees, of which less than 0.2% (or 198) have more than 100 employees. The bulk of establishments (123,800) are micro- and small-scale enterprises with less than 10 workers. Almost two-thirds of enterprises operate in the domestic trade services sector, followed by 19% in the manufacturing sector. This pattern of size distribution in the economy is typical for small, low-income developing economies. In the initial stages of development, the private sector is dominated by small-scale enterprises, and as the economy expands, competitive SMEs may grow and add to the pool of larger firms. Findings from a recent survey of 490 registered establishments in 2007 by GTZ indicate that these growth dynamics are occurring in the economy.6 The survey found small but still significant increases in the share of large enterprises in terms of the total number of enterprises as well as employment from levels in 2005. The majority of SMEs operate informally, with only an estimated 40% holding an enterprise certificate.

17. Private sector growth and development. Measures of productivity and trade facilitation costs, as well as large recent investments in infrastructure, suggest that conditions for growth of the Lao PDR economy are improving. This improvement in efficiency of the economy, located beside the two fastest growing economies in the world (the People’s Republic of China and Viet Nam), and middle-income Thailand, as well as expected higher budget revenues from the resource sector in the longer term, provide the Lao PDR with tremendous potential for private sector growth and development over the longer term. However, attainment of this potential is held back by a range of issues that slow economic integration with neighbors, deter investment, and dampen productivity growth. These include (i) a weak institutional framework for SME policy coordination and access to finance, (ii) high transaction costs and unpredictability in the investment regime, and (iii) relatively high costs involved in importing and exporting goods (Appendix 6).

5 Lao PDR, The Steering Committee on Economic Census. 2007. Report of Economic Census, 2006 Volume 1,

National Statistics Centre, Vientiane. 6 GTZ. 2008. The Enterprise Survey of 2007. Vientiane.

10

Table 2: Number of Firms by Employment Size and Major Economic Sector (2006) Total

Economic Sector Less than 5 persons

5–9 persons

10–99 persons

100 + persons No. %

Agriculture, forestry and fishing 3,511.0 539.0 258.0 10.0 4,319.0 3.4 Manufacturing 21,925.0 1,366.0 923.0 114.0 24,331.0 19.2 Wholesale and retail trade; repair 79,728.0 1,615.0 416.0 10.0 81,780.0 64.4 Transportation and storage 3,511.0 172.0 110.0 5.0 3,799.0 3.0 Accommodation and food service 2,341.0 771.0 319.0 8.0 3,439.0 2.7 All other industries 7,576.0 805.0 809.0 51.0 9,245.0 7.3 Total 118,592.0 5,268.0 2,835.0 198.0 126,913.0 100.0 % of total 93.4 4.2 2.2 0.2

Note: Figures may not add up to totals as no detailed data were recorded for a few enterprises. Source: Lao PDR, The Steering Committee on Economic Census. 2007. Report of Economic Census, 2006 Volume 1, National Statistics Centre, Vientiane.

1. Need for Institutional Coordination on SME Policy and Access to Finance 18. Need for more coherent approach to policy formulation and implementation. For many developing economies, the problem of coordination failure between the public and private sector is a constraint on private sector and SME development. In the Lao PDR, with a large number of government agencies involved in the formulation of policies and regulations that affect the private sector, lack of a systematic, consultative process for formulation of policy and regulation has provided scope for policy unpredictability and increased the likelihood of regulations that unduly hinder private sector development. Decentralization adds a further layer of complexity to the business environment for firms, with local governments responsible for a range of regulations that have cost and operational implications. Recent reforms, however, have helped establish the framework for a more coherent approach to private sector development. A key step in this regard was the establishment of the SME Promotion and Development Office (SMEPDO) in 2004, providing a focal point for championing reforms aimed at improving the enabling environment for SMEs in particular and the private sector more generally. Under subprogram 1 of the PSME, SMEPDO formulated the national strategy for SME development (2007—2012) in 2007 and is charged with overseeing its effective implementation.7 The strategy provides a comprehensive action plan for assisting SMEs in addressing constraints to growth, including creating an enabling environment for businesses to operate. The strategy was approved by the PMO in early 2008 after extensive dialogue and consultation with stakeholders in the private sector through the Lao Business Forum, the Lao National Chamber of Commerce and Industry, other groups, and development partners. In 2008, SMEPDO established the monitoring unit in response to demand from both internal (SMEPDO) and external stakeholders of SMEPDO for transparent information, good management, and delivery of results under the strategy. The first monitoring report was produced in the first quarter of 2009 and notes that, while implementation was slow at first, it has accelerated in recent months (para 51). 19. Strengthening public–private dialogue. While an institutional mechanism exists (i.e., Lao Business Forum) to support dialogue between the business community and relevant authorities at the central government level, similar arrangements have been missing at the provincial level although local governments are responsible for the issuance, implementation, and/or enforcement of many regulations that impact the private sector. To provide an effective channel for feedback from the private sector on issues facing firms at the provincial level, the Government (with support from GTZ) has initiated provincial public–private dialogues (P3Ds) in 7 SMEPDO. 2008. The Lao Small and Medium-Sized Enterprises Strategy. Vientiane.

11

a number of pilot provinces.8 These are intended to provide a regular forum to bring issues facing firms to the attention of relevant local authorities for resolution at the local level. While the piloted P3Ds are in their infancy, they have highlighted common issues facing firms such as skill shortages in the workforce, the need for consistent application of taxes, and overly bureaucratic processes involved in compliance with regulations. While not all issues can be quickly or readily resolved, the ability to bring them to the attention of relevant authorities on a regular basis through a public forum is a significant new development that has the potential to spur more responsive and transparent public administration at the local level. In recognition of their value, the Government is institutionalizing the P3Ds process in the four pilot provinces and plans to replicate it in other provinces going forward. P3Ds, once effectively institutionalized, can also serve as a natural mechanism for the conduct of stakeholder consultations under key initiatives supported by the Program such as pilot testing regulatory impact assessments. 20. Access to finance. The finance sector of the Lao PDR is shallow, with the banking system constituting the main form of formal financial intermediation. Microfinance institutions are expanding to serve the needs of microenterprises but coverage remains low. Consequently, SMEs have had limited access to formal sources of financing, and generally rely on retained earnings and informal sources. The 2008 GTZ enterprise survey of 2007 found that 50% of entrepreneurs surveyed reported access to capital as a major constraint to their growth (footnote 6). The Government, with assistance from ADB through the Banking Sector Reform Program (BSRP) completed in March 2009 9 and the Rural Financial Sector Development Program (RFSDP)10 on track to be completed in 2011, have helped to restore the health of the banking sector gradually, improving the competitive environment and developing microfinance institutions. The Lao Development Bank, a state-owned commercial bank, has refocused its market segment to serving SMEs. 21. However, SMEs face legal and capacity constraints in accessing finance, and these need to be addressed if SMEs are going to benefit from recent banking sector developments. Constraints include weak protection of creditors’ rights, which means that banks largely rely on the use of fixed assets (e.g., land and buildings) as collateral to secure loans, placing SMEs generally at a disadvantage in accessing credit. The Government is addressing this through reforms such as preparation of a draft decree on secured transactions that would provide a framework for using a wider range of assets (including movable assets) as collateral for loans. Another critical constraint is limited credit information on customers that allows banks to assess credit risk. Currently, requests by banks for such information are processed by the central bank’s Credit Information Bureau (CIB) using an inefficient manual paper-based system—that can often take up to a week to generate responses. Upgrading to a system based on a centralized database that allows commercial banks to search for and update customer credit information in real time could significantly reduce the time and costs involved in credit assessment. Another constraint is the limited range of alternative financial products to bank loans available to SMEs. Under the BSRP, the Government drafted and submitted a lease financing decree to the PMO in February 2008 establishing a regulatory framework for the leasing industry, with the aim of developing the sector. The decree was approved in July 2009. A final constraint is the poor accounting and financial reporting capacity of SMEs, which also limits access to finance. According to the GTZ enterprise survey, 75% of microenterprises, 54% 8 Champasak, Louangphrabang, Louang-Nam Tha, and Savannakhet. 9 ADB. 2009. Report and Recommendation to the President to the Board of Directors on a Proposed Loan and

Technical Assistance Grant to Lao People's Democratic Republic for the Banking Sector Reform Program. Manila. 10 ADB. 2009. Report and Recommendation to the President to the Board of Directors on a Proposed Loan and

Technical Assistance Grant to Lao People's Democratic Republic for the Rural Financial Sector Development Program. Manila.

12

of small enterprises, and 25% of medium-sized enterprises do not keep proper bookkeeping records. Furthermore, the same survey found that less than 45% of small firms had ever used a business development service provider. Under subprogram 1, the Government enacted a new accounting and auditing law and is currently disseminating information and accounting standards to the business community, with assistance from the EC under its SME project.

2. Investment Climate 22. The Lao PDR has enjoyed sustained investment expansion since 2000. Reforms to the business environment since the early 1990s—with the enactment of the Business Law of 1994, foreign and domestic investment laws in 2004, the enterprise law of 2006 (replacing the business law), and other commercial legislation—contributed to this expansion. FDI is critical to development of the Lao PDR at its current level of development and with its undeveloped financial sector. Evidence shows that FDI brings important externalities to local firms, suppliers, and workers through technology and skill transfers. Successful entry of FDI breeds success and this attracts additional FDI in other sectors. It is also associated with improved employment and poverty reduction. Figure 3 shows a big jump in annual FDI approvals since 2000 across all major sectors. The composition of this growth has also changed with the increase in the share of projects going to agriculture, mining, and hotels—indicative of the Lao PDR’s comparative advantage in tourism and natural resources. While current data are not available, anecdotal evidence suggests that this investment has slowed in 2009 because of the global financial crisis and collapse in commodity prices.

Figure 3: Foreign Direct Investment Approvals (number of projects)

Source: Ministry of Planning and Investment. 23. Update on constraints on investment. The 2008 GTZ enterprise survey of 2007 reiterated the key constraints to investment attractiveness in the Lao PDR such as infrastructure (mainly roads, water, and electricity supply reliability); excessive red tape; labor skills; taxation; and access to finance. The ADB-World Bank investment climate survey carried out in 2005 found that ranking of constraints differed across major sectors.11 Manufacturing firms ranked infrastructure, regulations, and taxation as their top three constraints, while operators in tourism

11 ADB and World Bank. 2007. Reducing Investment Climate Constraints to Higher Growth. Manila and

Washington, DC.

0 10 20 30 40 50

Other

Hotel

Hydropower

Mining

Wood

Industry

Agriculture

2007 2000

13

ranked infrastructure, inadequate skills, and taxation as their major business constraints. Investors also found that some constraints have improved while others may have deteriorated since 2005. According to the GTZ survey, more investors feel that excessive red tape and finding skilled labor are bigger problems in 2007 than in 2005, while competitive pressures are less of a problem in 2007, and no change has been observed in infrastructure (Appendix 6). Some caution should be taken when comparing changes in perception over time as these are shaped from a combination of first-hand experiences as well as exposure to new knowledge about best international or regional practices (which may be particularly significant in transition economies like the Lao PDR). On a global comparison, the Lao PDR ranks relatively low. The Doing Business report 2009 ranks the Lao PDR 165th out of 181 countries, slipping three places over its ranking in 2008 (Appendix 6).12 24. Progress on business registration. Until recently, several steps were required to register an enterprise—involving several agencies, depending on the sector, and an excessive amount of documentation. Firms were required to produce 18 documents and obtain pre-approval from relevant line ministries and other authorities to qualify for registration. Under this system, it took firms 60 days on average to obtain a basic registration certificate, along with the expenditure of significant staff and other resources. Reregistration was required each year, so such costs were incurred on an annual basis. These costs provided a significant disincentive for firms to register, weakening the Government’s ability to increase the tax base or monitor private sector development effectively. Significant costs were also imposed on the Government, arising from the resources required to administer such a system (well over 300 staff were employed in this regard). A 2009 ADB study (red tape study) estimated that the enterprise registration system cost the business community more than $6 million annually to comply with the registration process.13 25. The Government has made significant progress in modernizing the business licensing process. Notably, under the new enterprise law, registration procedures have been markedly streamlined, and the period allowed for registration of enterprises not on the negative list has been limited to 10 days (compared with 60 days on average in practice under the previous regime).14 To help meet these targets, the Government is modernizing its enterprise registration system. MOIC, with ADB technical assistance has simplified enterprise registration procedures and developed a computerized system that allows for more efficient implementation of the registration process as well as monitoring of firms, through use of a centralized database in Vientiane linked via internet to client systems in provincial enterprise registry offices. 15 The new system began operation in August 2008 with four pilot provinces and is being rolled out nationwide in a phased manner—with coverage of all 17 provinces expected to be complete by late 2010 (para. 57). 26. Investment law. The Foreign Investment Law and the Domestic Investment Law were amended in 2004 and were important milestones in the Lao PDR’s transition to an open market economy, as they set out a broad framework to promote investment. However, they have major weaknesses. As foreign and domestic investors are covered under different investment laws and approval conditions, national or equal treatment is compromised. There is an element of

12 World Bank. 2009. Doing Business 2009. Washington, DC. 13 ADB. 2009. Options for a Regulatory Review Program and an Office of Best Regulatory Practice. Manila. 14 Owners can now register their enterprises directly at the enterprise registry office for any economic activity not on

the negative list. Only those wishing to register a firm for operation in sectors on the list must first seek approval from the relevant line ministry.

15 ADB. 2007. Technical Assistance to Lao People's Democratic Republic for Strengthening Private Sector and SME Development. Manila.

14

unpredictability in the administration of investment incentives, as the duration of some incentives appears to be open-ended. The list of sectors closed to foreign investment, or open under certain conditions, is not consistent with the negative list under the enterprise law of 2006. Most countries have shifted away from using a positive list for foreign investment to a negative list, as it increases transparency and predictability for investors. Ideally, the list of conditional or closed sectors under the investment law should be synchronized with those on the negative list under the enterprise law; i.e., the list of sectors on both lists should be consistent. Given the importance of FDI to Lao PDR development, these issues in the investment regime need to be addressed. 27. Excessive red tape. While the enterprise law addresses problems with registration, it does not deal with other operating business licenses issued by line agencies. There is excessive red tape affecting business operations. Under current practice, regulations are often formulated in an ad hoc manner by technical staff in line ministries subject to tight deadlines, which leaves little room for stakeholder consultation or assessment of costs to individual firms or the economy as a whole. This has helped contribute to an existing stock of business-related regulations that are unduly burdensome and costly for the private sector, serving to undermine the competitiveness of Lao PDR firms and weakening the country’s attractiveness to investment. 28. The ADB red tape study estimates that firms incur annual average expenses of KN4.1 million to comply with the three most common types of licenses (referred to as permissions in Lao PDR)—enterprise registration certificate, sector operation license, and tax certificate (footnote 13). This cost the business community an estimated KN266 billion annually in 2008, or 0.7% of GDP (Figure 4a). Firms typically have to comply with dozens of regulations, depending on their line of business, which adds to business compliance costs. A realistic estimate of total compliance costs would be 1.5%–3.0% of GDP. The major component of business compliance costs is the enterprise’s staff time and own financial resources used to prepare documentation and apply for the license. The burden of business regulatory costs falls disproportionately on small enterprises. On an employee basis, business compliance costs are much higher in small enterprises (KN258,442) than in medium-sized enterprises (KN120,000) and large firms (KN27,000). This illustrates how the regulatory burden falls most heavily on small enterprises in the formal sector, and becomes a barrier to the formalization and growth of small enterprises. 29. Need to improve quality of regulations and reduce compliance costs. The Government lacks a system whereby laws and regulations affecting licensing and inspection are reviewed to determine the impact on the private sector. As a result, the regulatory compliance costs imposed on the private sector are not appreciated. To help improve the quality of regulations and minimize compliance costs for the private sector, a more systematic approach needs to be taken in their formulation and/or review. Ideally, and following international best practice on regulatory impact assessment, this would involve use of a systematic approach to assess and make transparent the costs of particular regulations for individual firms as well as the economy as a whole (Appendix 6). This is a long-term effort. As a starting point, the Government should start with raising public awareness on the need for a regulatory reform program, and achieve broad agreement on the appropriate plan and institutional set-up for addressing red tape over the longer term.

15

Figure 4: Business Compliance Costs (a) Compliance costs by common licenses (b) Composition of compliance costs

500 800 1,100 1,400 1,700 2,000

Drug registration

Operational license

Tax certificate

Entertainment license

Import certificate

Enterprise registration

Professional certificate of pharmacy

Amount per firm (KN'000)

Enterprises' staff Time Costs

61%

Official fees32%

Facilitation fees7%

(c) Compliance costs by firm sizea (d) Compliance cost by sector

0

50

100

150

200

250

300

Micro-ennterprises

Smallenterprises

Mediumenterprises

Largeenterprises

Am

ount

per

em

ploy

ee K

N'0

00

2.0

3.0

4.0

5.0

6.0

7.0

Manufacturing Trading Pharmaceuticals Tourism

Am

ount

KN

'000

a Compliance costs per employee of the three main licenses—enterprise registration, operational license, and tax certificate.

Source: ADB. 2009. Options for a Regulatory Review Program and an Office of Best Regulatory Practice. Manila.

3. Trade Policy and Capacity Development 30. WTO accession. The Government considers WTO accession a key foreign trade policy priority and this is accelerating the momentum for finishing the trade reform agenda. The Government’s preparations for WTO accession have had an influence on the way it views trade policy and the business climate. In this regard, MOIC is considering ways to accelerate reforms to the import and export management system. It intends to continue to reduce the number of sectors on the import control list, and streamline and simplify import and export procedures and regulations. The WTO accession efforts follow on from the Lao PDR’s commitments to the Common Effective Preferential Tariff (CEPT) schedule under the Association of Southeast Asian Nations (ASEAN) Free Trade Agreement (AFTA). The Government has made progress in implementing the CEPT schedule for items in the inclusive list (0%–5%), which covers 98% of all tariff lines. As a consequence of a process of market-oriented reforms that began in the late 1980s, the average customs duty has fallen to about 10%, which is among the lowest in the region. Going forward, it is opportune to advance the reform momentum toward reducing the remaining non-tariff barriers and investment distortions—including technical barriers to trade (TBTs); reform of trade facilitation (logistics, sanitary and phyto-sanitary standards systems, or

16

sanitary and phyto-sanitary standards, and customs); consolidation of other incentives that negatively affect investment and trade decisions; and support for implementation of the Lao PDR’s WTO commitments once it accedes to the WTO (tentatively planned for 2012). Subprogram 2 deals with a subset of these reform areas. Other areas (especially trade facilitation and post-WTO implementation) are a long-term agenda requiring strong coordination among development partners. 31. Effective rates of protection. The degree of protection afforded to domestic industry through imposition of custom duties, non-tariff barriers, and domestic taxes on products can be measured by estimates of the effective rate of protection (ERP). A positive estimate of the ERP indicates the height of protection afforded to domestic industry while a negative estimate indicates the height of negative protection (or disincentive to produce) afforded to domestic industry. Variations in estimates of ERPs for different sectors of the economy reveal the extent of resource misallocation (or distortions) within the economy caused by the trade and tax policy regime, and provide a useful tool for assessing a country’s trade policy and promoting transparency. ADB and MOIC staff estimates of ERPs show that pockets of significant protection to industry remain, such as in food, beverages, and tobacco (Table 3). The trade policy and incentives regime appears to be biased against sectors that have potential to be export-oriented, as reflected in sizeable negative protection in some of these sectors (agriculture and textile and garments). Once the AFTA CEPT schedule is completed, protection in some of these sectors (auto and motorcycle assembly, and some processed foods) will disappear. Sector-specific reforms may be needed in some of the others (e.g., cement) to enhance economic efficiency (Appendix 6). The estimates do not include fiscal investment incentives, which are considered generous and vary across sectors and across firms within sectors. If these are included, the variation in ERPs could be larger. A comprehensive assessment of investment incentives is necessary. 32. Import licensing and administrative procedures. These are the major remaining non-tariff barriers, but are being phased out by the Government to be consistent with WTO rules. The Lao PDR operates an import–export management and control system, identical to the one operated in Viet Nam until recently. There are two key features of the import and export management system. The first feature is the import licensing regulation and its identification of items subject to restrictive import licensing. It categorizes imports into three categories: (i) prohibited goods,16 (ii) controlled goods, and (iii) general goods that are easily imported. Goods may be prohibited based on public safety, environmental, or moral concerns, but not to protect domestic producers. The controlled category deals with licenses for imports that are not banned but managed by MOIC. Until October 2006, these included about 25 broadly defined items such as prepared foods and all raw and semi-manufactured products used in manufacturing. MOIC is reforming the import and export management system and has made substantial reforms since 2006 to reduce trade facilitation costs. The list of items on the controlled list was revised in October 2006. Under subprogram 2, the Government has revised the import regulation to be consistent with WTO requirements, including the use of non-automatic and automatic licenses. The number of import items subject to non-automatic licenses on the controlled list has also been further reduced (para 61).

16 The list of prohibited goods and controlled goods set out in MOIC notice No. 1376 of October 2006. Previous MOIC notices of prohibited goods and controlled goods were set out in notices No. 284 and 285 of March 2004.

17

Table 3: Industry Protection—Effective Rates of Protection (%)

Sector Export or

Import Sector ERP Crops E (5.0) Livestock and poultry E (8.0) Forestry and logging E (11.8) Mining and quarrying E (11.0) Food, beverages, and tobacco I 104.8 Textiles, garments, and leather products E (6.8) Wood and paper products, printing, and publication E (0.4) Chemical products I 2.0 Non-metallic mineral products I (4.3) Metal products, machinery I 9.5 Other manufactured products I 6.1

( ) = negative, E = export-oriented sector, ERP = effective rate of protection, I = import-oriented sector. Source: Asian Development Bank and Ministry of Industry and Commerce staff estimates.

33. The second feature of the import–export management system in need of reform has been the import administrative procedures as defined under prime minister's decree 205 and its circulars. Over the last 3 years, however, these have been significantly rationalized with the removal of MOIC officials at customs posts as well as the requirement for producers to provide import plans. The Government is preparing revisions to the regulation to ensure consistency with WTO rules, especially in relation to trading rights and administration of quotas. 34. Technical barriers to trade. In preparation for WTO accession, the Government is reviewing technical barriers to trade, such as those related to sanitary and phyto-sanitary standards (SPS), with a view to making them consistent with WTO rules. This will involve establishing procedures for notifying SPSs and other TBTs to the WTO, and designating an inquiry point within government for such notifications. Early progress has been made in strengthening the SPS regulatory environment to ensure consistency with the WTO, as a series of decrees was issued related to food safety management—including principles for application of SPSs and technical measures for food safety management, plant protection, and quarantine law. As the Government considers completion of WTO commitments important for its world trade integration efforts, it must strengthen the capacity to implement the required policy reforms and to establish compliance notification procedures across relevant agencies. 35. Capacity building in trade policy. The institutional arrangements and processes for making trade policy are just as important as reforms to the trade policy regime. The Department of Foreign Trade Policy at MOIC sets the broad trade policy framework and agenda. It is taking the lead in WTO preparations and has responsibility for AFTA. With only 30 staff, it is overstretched and under-resourced to conduct adequate trade policy analysis—an area that will be critical to support further trade reform and effective participation in the WTO. 36. While the Department of Foreign Trade Policy has a key role in determining trade policy, a number of other agencies also play significant parts, including the Department of Export and Import Management that sets import and export procedures, and compiles the controlled import list. The ministries of agriculture, health, communication, transport, post, and construction—as well as MOIC—control import licensing in their respective sectors and produce TBTs, including SPSs. Ensuring consistency of trade policy across the whole Government will be a challenge, as in most countries. It is also important for the Lao PDR to continue to build its own capacity to carry out policy analysis on its merits for the Lao PDR. Under ADB technical assistance (footnote 15) training on trade policy tools has been provided to staff at MOIC and other ministries, and staff from the Department of Foreign Trade Policy worked with ADB staff to

18

develop capacity to estimate ERPs. Other activities included writing and presentation skills, media communication for senior officials, and training on trade policy tools. ADB staff also provided training on free trade agreements. It will be important to continue this longer term capacity development to support the reform momentum. 37. Trade facilitation. The performance of trade logistic services is critical to determine if the Lao PDR can trade goods and services on time and at low costs. A cross-country study conducted by the World Bank17 suggests that high logistics costs and, more importantly, low level of services are barriers to trade and hence, growth. Available indicators suggest that Lao PDR businesses bear a higher cost of logistics than other countries in the region (Figure 5). The logistics performance index ranks the Lao PDR above most countries in the region, meaning it is less efficient (costly and time-consuming). This index is developed based on a comprehensive survey of supply chain performance, including customs procedures, logistic costs, infrastructure quality, and the competence of the domestic logistics industry. 38. SPS are crucial to microeconomic infrastructure to improve the private sector’s access to the international market for agro-based products. Lao PDR exports of such products are in their infancy, and inadequate SPS management systems are an obstacle to development of such exports. The Lao PDR coffee industry has an estimated export value of $60 million only. When it accedes to the WTO, the Lao PDR will have agreed to SPS compliance within a transitional period, usually 5 years. Based on the experience of Cambodia, it is unlikely to achieve this commitment on time. It will require a comprehensive assessment of the regulatory regime and supporting institutions. There are no internationally accredited assessors in the Lao PDR and the technical capacity of laboratories to undertake SPS-related testing is very limited. Therefore, much needs to be done to strengthen the regulatory environment, including promoting competition in the sector, developing private sector providers, upgrading equipment, and testing procedures and staff training in the laboratories. The Government recognizes that much needs to be done to strengthen SPS management systems and capacity, and that this is a longer term effort. It had developed an action plan for SPS under the integrated framework diagnostic study undertaken in 2006. The action plan will need to be reviewed in light of WTO accession efforts and developments in the region, and its implementation started. ADB’s Greater Mekong Subregion (GMS) trade facilitation activities are considering ways to harmonize trade facilitation, including SPS systems, across the GMS.

17 World Bank. 2007. Connecting to Compete: Trade Logistics in the Global Economy. Washington, DC.

19

Figure 5: Trade Facilitation—International Comparison (a) Cross-Country Export Time and Cost (b) Cross-Country Import Time and Cost

0

10

20

30

40

50

60

Eas

t Asi

a &

Pac

ificEa

ster

n E

urop

e &

Cen

tral

Asi

a

Latin

Am

eric

a &

Car

ibbe

an

Mid

dle

East

& N

orth

Afri

ca

OE

CD

Sout

h A

sia

Cam

bodi

a

Lao

PD

R

Viet

Nam

Thai

land

Sri

Lank

a

Ban

glad

esh

-2004006008001,0001,2001,4001,6001,8002,000

Time for export (days) (LHS axis)

Cost to export ($ per container)(RHS axis)

0

10

20

30

40

50

60

Eas

t Asi

a &

Pac

ific

Eas

tern

Eur

ope

& C

entra

lA

sia

Latin

Am

eric

a &

Car

ibbe

an

Mid

dle

East

& N

orth

Afri

ca

OE

CD

Sou

th A

sia

Cam

bodi

a

Lao

PD

R

Vie

t Nam

Thai

land

Sri L

anka

Bang

lade

sh

02004006008001,0001,2001,4001,6001,8002,000

Time for import (days) (LHS axis)

Cost to import ($ per container)(RHS axis)

OECD = Organisation for Economic Co-operation and Development, Lao PDR = Lao People's Democratic Republic, LHS = left hand side, RHS = right hand side. Source: World Bank. 2007. Connecting to Compete: Trade Logistics in the Global Economy. Washington, DC. C. Lessons