Report and Recommendation of the President to the Board of Directors Project Number: 39516 November 2007 Proposed Program Loan and Technical Assistance Grant Republic of the Philippines: Local Government Financing and Budget Reform Program Cluster (Subprogram 1)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Report and Recommendation of the President to the Board of Directors

Project Number: 39516 November 2007

Proposed Program Loan and Technical Assistance Grant Republic of the Philippines: Local Government Financing and Budget Reform Program Cluster (Subprogram 1)

CURRENCY EQUIVALENTS (as of 30 October 2007)

Currency Unit – peso (P)

P1.00 = $0.02 $1.00 = P44.04 ¥1.00 = $0.008 $1.00 = ¥114.177

ABBREVIATIONS

ADB – Asian Development Bank ADTA – advisory technical assistance AIP – annual investment plan AusAID – Australian Agency for International Development BIR – Bureau of Internal Revenue BLGF – Bureau of Local Government Finance BSP – Bangko Sentral ng Pilipinas (Central Bank of the Philippines) CCD – Coordination Committee on Decentralization COA – Commission on Audit CSP – country strategy and program DBM – Department of Budget and Management DENR – Department of Environment and Natural Resources DILG – Department of the Interior and Local Government DOF – Department of Finance DOH – Department of Health DPSP – Development Policy Support Program EO – executive order GAA – General Appropriations Act GDP – gross domestic product GFI – government financial institution GNP – gross national product GPRA – Government Procurement Reform Act GTZ – Deutsche Gesellschaft für Technische Zusammenarbeit

(German Agency for Technical Cooperation) IRA – internal revenue allotment JBIC – Japan Bank for International Cooperation JMC – joint memorandum circular LBM – local budget memorandum LDC – Local Development Council LDIP – local development investment program LDP – local development plan LFF – LGU financing framework LGC – Local Government Code LGFBR – Local Government Financing and Budget Reform LGFPMS – local government financial performance monitoring system LGPMS – local government performance measurement system LGU – local government unit LIBOR – London interbank offered rate

LOGOFIND – Local Government Finance and Development MDFO – Municipal Development Fund Office MDG – Millennium Development Goal MTPDP – Medium-Term Philippine Development Plan NEDA – National Economic and Development Authority NGAS – New Government Accounting System NGO – nongovernment organization NTRC – National Tax Resource Center OECD – Organisation for Economic Co-operation and Development OPIF – organization performance indicator framework PDAF – Priority Development Assistance Fund PDF – Philippine Development Forum PFM – public financial management PROLEND – Program (policy) lending facility RPT – real property tax SRE – statement of receipts and expenditures TA – technical assistance UBOM – Updated Budget Operations Manual USAID – United States Agency for International Development VAT – value-added tax

NOTES

(i) The fiscal year (FY) of the Government and its agencies ends on 31 December.

(ii) In this report, "$" refers to US dollars.

Vice President C. Lawrence Greenwood Jr., Operations 2 Director General A. Thapan, Southeast Asia Department (SERD) Director J. Ahmed, Governance, Finance, and Trade Division, SERD Team leader T. Niazi, Public Sector Management Specialist, SERD Team members J. Balbosa, Country Specialist (Philippines), SERD C. Buentjen, Senior Capacity Development Specialist, Regional and

Sustainable Development Department R. O’Sullivan, Senior Counsel, Office of the General Counsel V. Tan, Financial Management Specialist, SERD M. van der Auwera, Social Security Specialist, SERD

CONTENTS

Page LOAN AND PROGRAM SUMMARY i

I. THE PROPOSAL 1 II. THE MACROECONOMIC CONTEXT 1 III. THE SECTOR 4

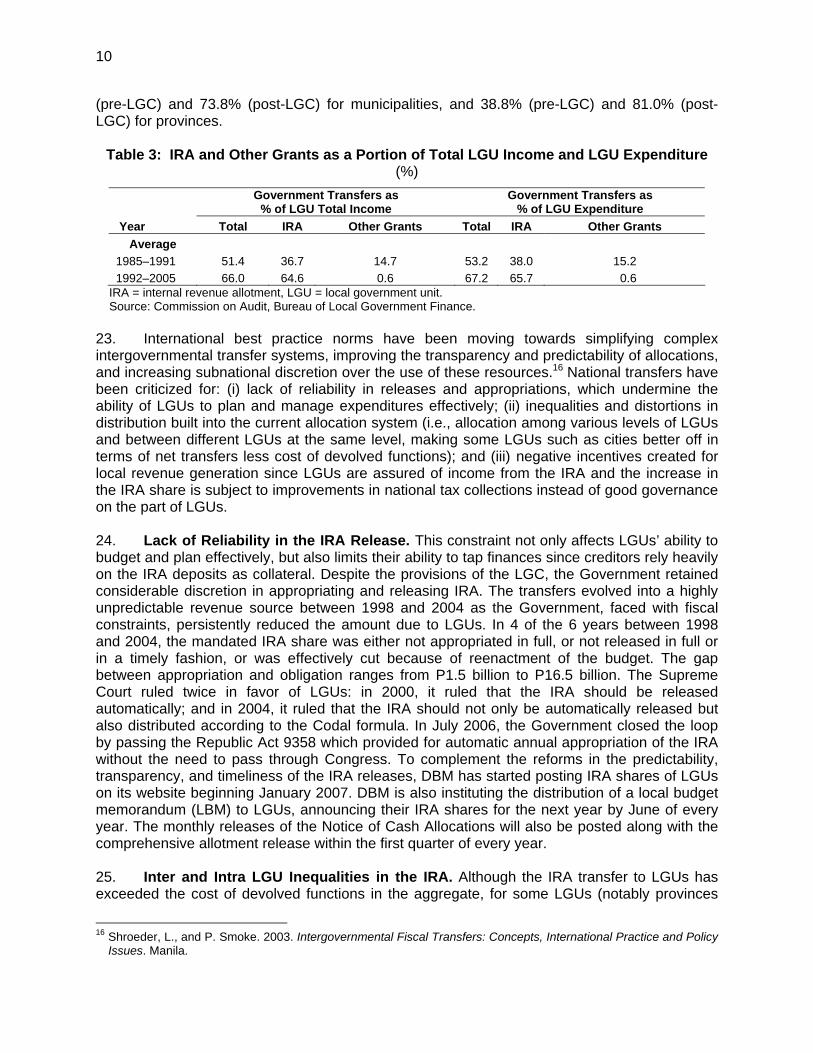

A. Review of the Sector and Performance 4 B. Issues and Opportunities 8 C. Lessons 16

IV. THE PROPOSED PROGRAM 17 A. Impact and Outcome 17 B. Policy Framework and Actions 19 C. LGFBR Medium Term Program: Subprogram 2 Indicative Policy Actions 22 D. Important Features 24 E. Financing Plan 24 F. Implementation Arrangements 25

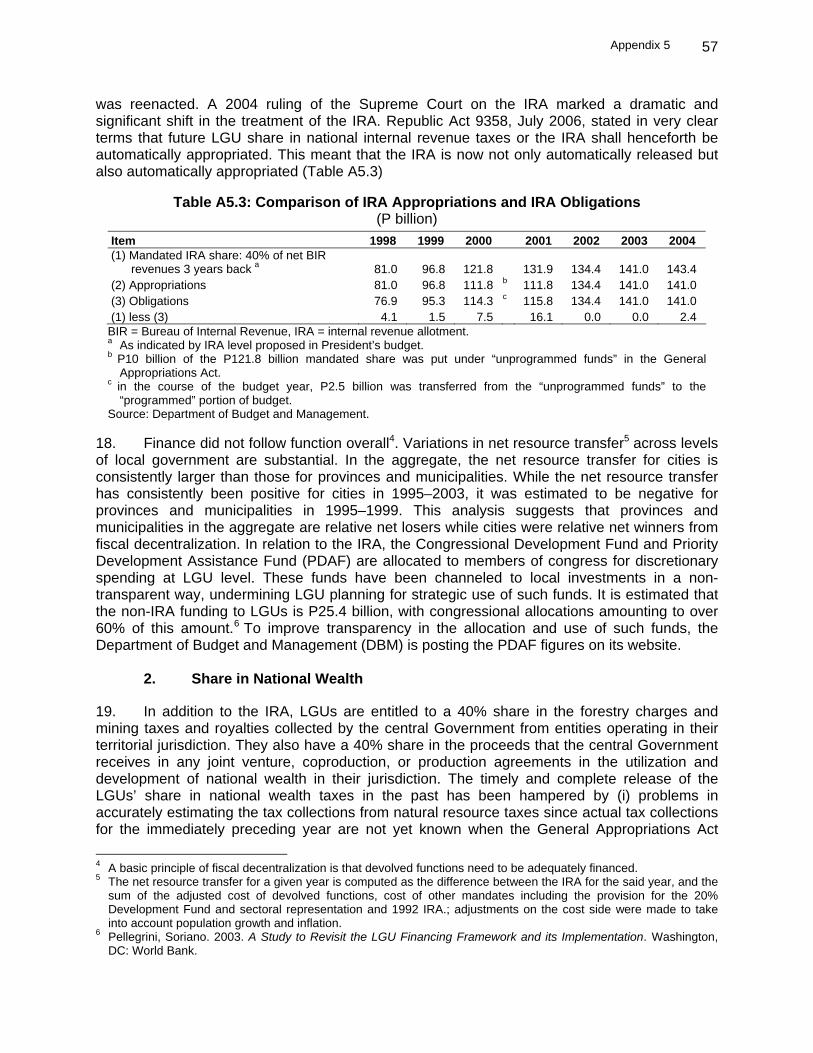

V. TECHNICAL ASSISTANCE 27 VI. PROGRAM BENEFITS, IMPACTS, ASSUMPTIONS, AND RISKS 28

A. Expected Impact 28 B. Risks and Mitigating Measures 29

VII. ASSURANCES 30 VIII. RECOMMENDATION 30 APPENDIXES 1. Design and Monitoring Framework 31 2. Development Policy Letter 35 3. Policy Matrix 42 4. Development Partners’ Coordination Matrix 49 5. Sector Analysis: Decentralization and Governance 52 6. Summary Poverty Reduction and Social Strategy 64 7. List of Ineligible Items 67 8. Advisory Technical Assistance 68

SUPPLEMENTARY APPENDIXES (available on request) A. Detailed Sector Analysis: Administrative and Fiscal Decentralization in the Philippines B. Terms of Reference for the Advisory Technical Assistance

LOAN AND PROGRAM SUMMARY Borrower Republic of the Philippines The Proposal The proposal comprises (i) a program cluster to the Republic of

the Philippines for the Local Government Financing and Budget Reform (LGFBR) Program, consisting of two subprograms; (ii) a proposed loan of ¥34,253,100,000 ($300,000,000 equivalent) for Subprogram 1 of the LGFBR Program; and (iii) a technical assistance (TA) grant for $800,000.

Classification Targeting classification: General intervention

Sector: Law, economic management, and public policy Subsector: Public finance and expenditure management Themes: Governance, sustainable economic growth, capacity development Subthemes: Public governance, promoting economic efficiency and enabling markets, organizational development

Environment Assessment

Category C

Program Rationale The Local Government Code (LGC), 1991, transferred the main

responsibility for the delivery of basic services (health, education, infrastructure, etc.) to local government units (LGUs). Decentralization has brought choices closer to the people while opening up space for innovative responses and solutions to service delivery issues. The LGC’s “finance follow function” premise set in place an intergovernmental transfer mechanism for sharing in the revenues of the Government of the Philippines (the Government) as well as allowing local governments to raise their own revenues. However, LGUs’ capabilities in discharging their functions continue to be constrained, so the Philippines faces significant challenges in ensuring that stable mechanisms are in place to channel adequate resources to local governments. Financial accountability, transparency, and capacity also represent significant constraints for local governments. Finally, significant improvement is needed in service delivery, governance, and performance measurement. While the scope of decentralization includes fiscal, administrative, and political dimensions, the LGFBR focuses mainly on the fiscal dimension where the implementation difficulties have been most challenging and are perceived as binding. It supports the Government’s ongoing efforts to improve local financing (facilitating access of LGUs to development credit), service delivery (credit financing for devolved services) and governance (improving public financial management and implementation of the Government Procurement Reform Act of 2003 at the local level). The LGFBR program will broaden the reform program in five target areas: (i) improving the completeness, timelines, and transparency of local government shares in national revenues; (ii)

ii

deepening reforms in fiscal management, planning, and public expenditure management by enhancing efficiency and accountability in these areas; (iii) enhancing effectiveness and transparency in the delivery of critical public services at the local level; (iv) improving LGUs’ access to public and private sources of capital for financing policy reforms and development projects; and (v) reducing LGU dependency on the internal revenue allotment (IRA) by developing buoyant sources of revenues at the local level, thereby reducing fiscal pressure on the Government. Asian Development Bank (ADB) support to the Philippines is determined by the four pillars of the country strategy and program (CSP) 2005–2007: (i) fiscal consolidation, (ii) strengthening investments, (iii) good governance, and (iv) support for achieving the Millennium Development Goals (MDGs). The proposed LGFBR program contributes to fiscal consolidation, good governance, and achieving the MDGs by: (i) lessening LGU dependence on national government transfers through improved mobilization of own-source revenues and enhanced predictability of resource flows, thereby promoting fiscal consolidation; (ii) supporting improved delivery of essential services through improved LGU access to developmental credit, thereby promoting activities for achieving the MDGs; and (iii) supporting sector efficiency and improved governance by establishing transparent and accountable LGU financial and administrative management systems for coordinated development planning, thereby promoting good governance at the local level. The reform program was prepared by a joint team of representatives of the Government and ADB working concertedly since 2006.

Impact and Outcome The proposed LGFBR program supports the Government in its

efforts to help LGUs develop enhanced capacities to plan and budget for the general welfare of their constituent communities in a transparent and accountable way. It contributes to increased efficiency and effectiveness in the delivery of basic public services to residents by increasing fiscal resources and financing options for the LGUs. The intended impact is achieved by strengthening the policy, financing, financial, and regulatory framework for decentralization as well as developing capacities at the local government level.

Financing Plan A loan of ¥34,253,100,000 ($300,000,000 equivalent) from the

ordinary capital resources of ADB will be provided under the London interbank offered rate (LIBOR)-based lending facility for subprogram 1 of the LGFBR program. The loan will have a 15-year term including a grace period of 3 years, an interest rate to be determined in accordance with ADB’s LIBOR-based lending facility, a commitment charge of 0.75% per annum, and such other terms and conditions set forth in the draft program loan agreement. ADB’s Board of Directors has discounted the commitment charge to 0.25% for loans approved from 1 July 2007 up to and including 30 June 2008.

iii

Period and Tranching The program cluster period is from January 2006 to December 2010, with a single tranche loan of ¥34,253,100,000 ($300 million equivalent) to be disbursed under subprogram 1 when the Government has met the conditions for effectiveness. Subprogram 2 will be submitted for Board consideration approximately 36 months after the effectiveness of subprogram 1, subject to adequate progress of reforms and the Government’s readiness to continue with its reform agenda.

Counterpart Funds The Government will use the local currency counterpart funds

generated by the loan proceeds to meet program expenditures and associated costs of local reforms.

Executing Agency Department of Finance (DOF) Implementation Arrangements

The Department of Interior and Local Government (DILG), Department of Budget and Management (DBM), National Economic and Development Authority (NEDA), Bureau of Local Government Finance (BLGF), and Municipal Development Finance Office (MDFO) will be the Implementing Agencies responsible for implementing the Program. An LGFBR coordination committee (the Committee) has been established and is chaired by the undersecretary of DOF and comprises officials from DILG, DBM, and NEDA. It is responsible for coordinating the implementation of the LGFBR program reform actions. The Committee meets quarterly to monitor progress and oversee implementation of the Program, and provides guidance and direction to the executing and implementing agencies.

Procurement and Disbursement

The loan proceeds will be used to finance the full foreign exchange costs (excluding local duties and taxes) of items produced and procured in ADB member countries, excluding ineligible items and imports financed by other bilateral and multilateral sources. The loan proceeds will be disbursed to the Borrower in accordance with the provisions of ADB’s Simplification of Disbursement Procedures and Related Requirements for Program Loans.

Program Benefits and Beneficiaries

The LGFBR program will provide significant benefits and will have a positive impact on local service delivery, financing, and governance issues. The key expected benefits are as follows:

(i) Streamlined intergovernmental fiscal relations as a result of completeness, timeliness, and transparency in the release and reporting of LGU shares in national government revenues—thereby improving the accuracy of local budgeting and programming of local expenditures.

(ii) Improved transparency, efficiency, and accountability in planning, public expenditure management, and financial management as a result of rationalized and streamlined national government oversight functions and strengthened local capacity.

iv

(iii) Enhanced delivery of critical public services at the local level by providing additional financing options and linking them to performance outcomes as well as improved national government-LGU arrangements for devolved functions.

(iv) Greater LGU access to public and private sources of capital as a result of an improved policy and institutional environment, thereby contributing to increasing LGU ability to finance the delivery of local public services.

(v) Increased LGU own-source revenues to fund social and development expenditures as a result of strengthened LGU capacity to generate revenues from real property and business taxes—thereby reducing LGU reliance on national government transfers, and consequently reducing the Government’s fiscal burden.

Risks and Assumptions While some of risks are irreducibly political—outside the scope of

the Program to mitigate directly—core elements of the Program and advisory TA contribute to mitigating these risks through greater transparency and accountability mechanisms that strengthen the capacity of local authorities and provide active monitoring by civil society groups. The potential risks to subprogram 1 and underlying assumptions are the following:

(i) Political delays. Delays may be experienced in engaging the LGUs for the second phase since the election for their League officers are held in the third quarter of 2007. However, the Leagues have endorsed the phase one and two triggers and it is expected that no major changes in policy orientation will occur despite changes in the Executive Board of the Leagues.

(ii) External pressures. Deterioration in the external environment may trigger internal financial problems and may encourage the Government not to release the IRA amount fully to the LGUs. A portion of the IRA was withheld during the 1997 financial crisis since it was determined to be an “unmanageable public sector deficit”. However, the Government is strongly committed to achieving its fiscal consolidation objectives to maintain macroeconomic stability. In addition, legislative and legal measures are now in place to prevent a recurrence of the 1997 chain of events.

(iii) Coordination and capacity constraints. The willingness for coordination among oversight agencies for harmonization of local planning, investment programming, revenue administration, budgeting, and expenditure management may weaken over time. However, the Government is committed to implementing the joint memorandum circular (JMC) 2007-1. To resolve possible issues and ensure continued progress, a technical committee is being organized to oversee JMC implementation.

v

(iv) Resource constraints. The Government may run out of resources for capacity development activities planned under this Program. Although these are heavily funded by current ADB projects, it is possible that some training programs may be underfunded. An advisory TA is being provided to fill any such gaps. However, many donors are also providing TA grants for reforms and capacity development at the local level.

Technical Assistance In connection with the LGFBR program, the Government has

asked ADB for an advisory TA grant. The TA is estimated to cost a total of $1,100,000, of which ADB will finance $800,000 on a grant basis from the Japan Special Fund, funded by the Government of Japan. The TA will support the development of a medium-term reform agenda in local government financing and governance and its implementation, as well as provide the Government with just-in-time policy advice. It will include the following areas: (i) support creation and functioning of a Coordination Committee on Decentralization to promote, coordinate, and oversee decentralization reforms, including the changes envisaged in the LGFBR program policy matrix; (ii) analysis of existing capacities for planning and budget management at city level, development and pilot testing of revised planning and budgeting systems, and preparation and dissemination of city planning guidelines; and (iii) development of the local government performance measurement system to be used as a tool to link access to intergovernmental transfers, grants, and capacity development support with service delivery performance. A total of 95 person-months of national consultancy will be required. All recruitment and engagement will be undertaken in accordance with ADB’s Guidelines on the Use of Consultants (2007, as amended from time to time).

I. THE PROPOSAL

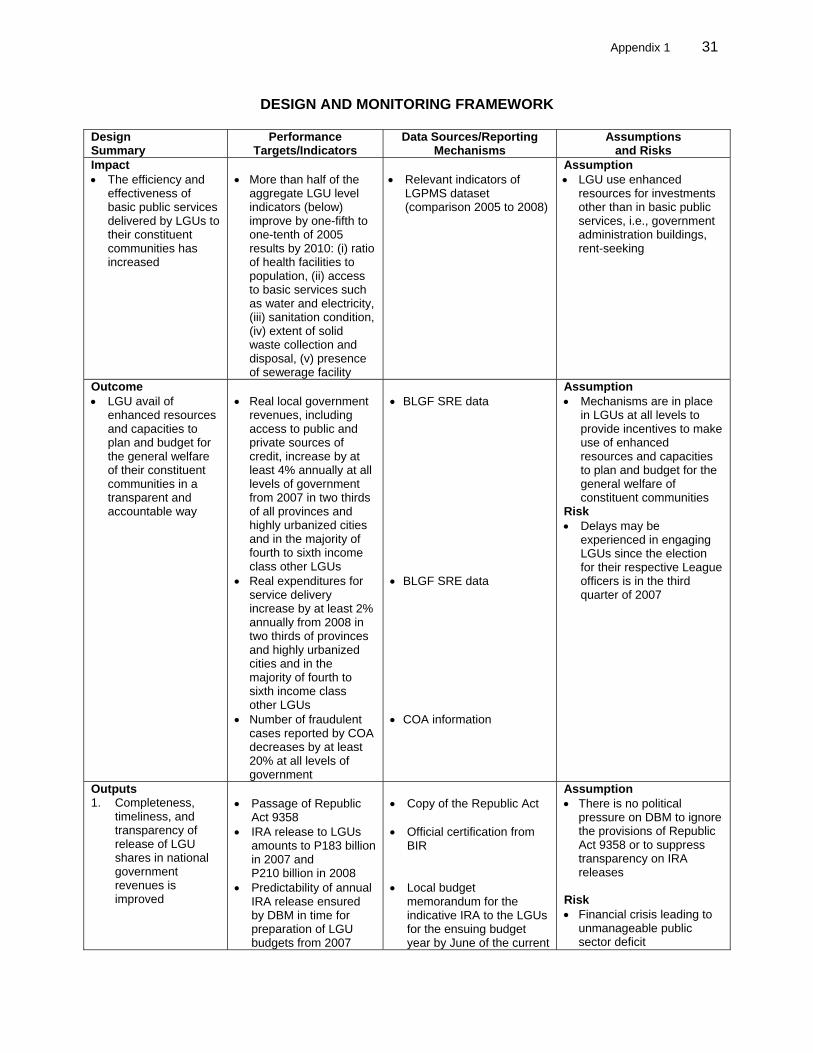

1. I submit for your approval the following report and recommendation on (i) a proposed program cluster to the Republic of the Philippines for the Local Government Financing and Budget Reform (LGFBR) program comprising two subprograms, and (ii) a proposed loan for subprogram 1 of the LGFBR. The LGFBR program was prepared by a joint team of representatives of the Government of the Philippines (the Government) and the Asian Development Bank (ADB). This report also describes proposed technical assistance (TA) for developing capacity for oversight agencies. If the Board approves the proposed loan, I, acting under the authority delegated to me by ADB’s Board of Directors, will approve the TA. The program design and monitoring framework is in Appendix 1.

II. THE MACROECONOMIC CONTEXT

2. The basic premise of the Medium-Term Philippine Development Plan (MTPDP) 2004–2010 is to fight poverty by building prosperity for the greatest number of the Filipino people. The MTPDP outlines the strategy of the administration in the 10-point legacy agenda, one of which focuses on good local governance through decentralized development, and decongestion of Metro Manila and creation of new growth centers across the country. The MTPDP reinforces and supports the principles outlined in the Local Government Code (LGC). 3. Consistent with the MTPDP, the Philippines country strategy and program (CSP) 2005–20071 is based on an analysis and prioritization of binding constraints to more rapid growth, greater inclusiveness, and faster poverty reduction. The CSP breaks with ADB’s past model for engaging with the Philippines in fundamental ways by introducing a thematic, rather than sector-based, strategic focus; greater project selectivity; and a results-based partnership with high lending contingent on macroeconomic performance. The strategy outlined in the CSP supports and advances the objectives of decentralization and good local governance, and is aligned with the Government’s reform agenda. When endorsing the CSP in mid-2005, ADB’s Board noted that new public sector lending commitments could be up to $1.5 billion for the 3 years, depending on the pace and quality of fiscal consolidation and sector reforms. Because of the large budget deficit of 2.7% of gross domestic product (GDP) in 2005, new lending commitments were low ($175 million). Subsequently, fiscal consolidation gained traction as the deficit dropped to 1% of GDP in 2006 and is expected to fall to 0.9% in 2007 and a balanced budget by 2008. This created the policy space for ADB to move to a “high case” lending scenario, with lending of $650 million in 2006 and an expected $700 million in 2007. 4. The improved macroeconomic performance and stability achieved in 2006 continued into 2007. The Philippine economy ended 2006 with overall annual real GDP growth of 5.4%. This was slightly up from 5% in 2005 and above the average growth rate of 4.3% per annum from 1990 to 2005. Table 1 presents data on key indicators for 2005 and 2006 to show the sustained positive macroeconomic performance and stability since 2004. Economic growth accelerated to 7.5% in the second quarter of 2007, among the highest growth rates in Southeast Asia. Services continued to be the fastest growing sector with average annual growth of 6.7% since 2003, contributing to almost 60% of economic growth, followed by manufacturing and utilities. Second quarter 2007 growth was led by the services sector growing by 8.4% year on year, with industry following at 8%. On the demand side, consumption spending contributed to 70–80% of economic growth, followed by a strong pickup in electronics and garments exports. In the second quarter of 2007, consumer spending rose by 6% while government spending rose by

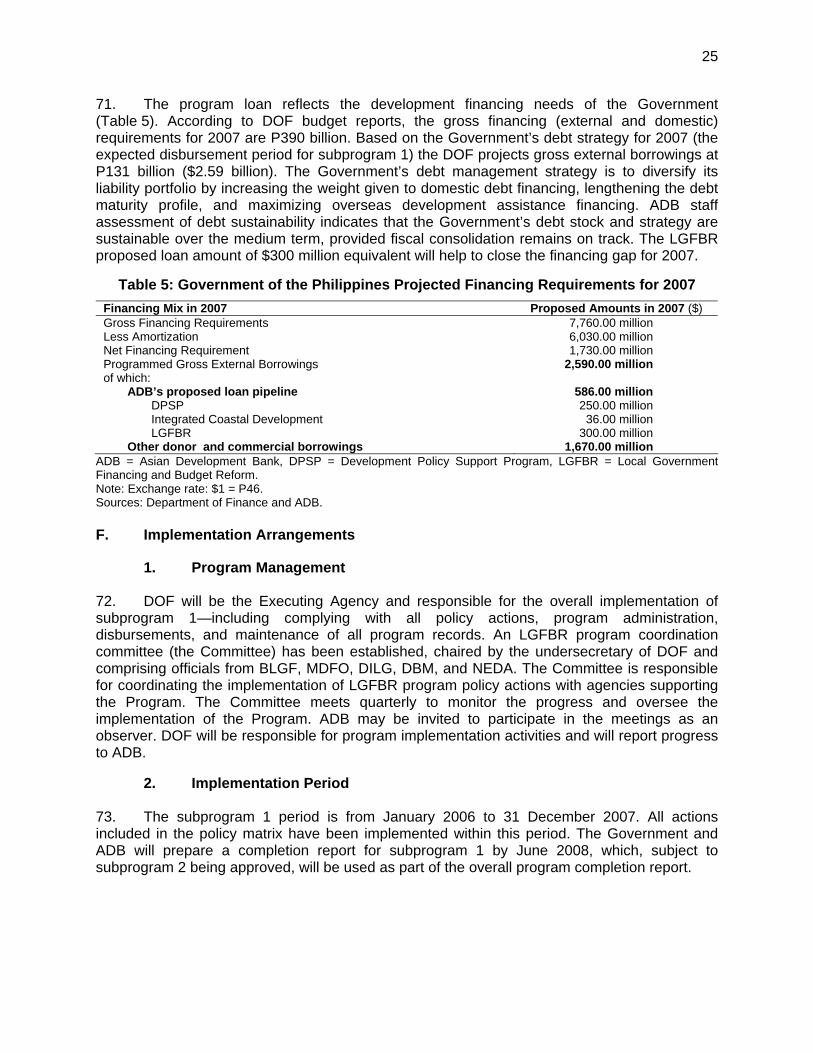

1 ADB. 2005. Country Strategy and Program (2005–2007): Philippines. Manila.

2

13.5%, making them the main drivers of growth. The upturn in the economy in 2006 and the continued expansion into 2007, despite higher oil prices, indicates that the Philippine economy is now more resilient.

Table 1: Aggregate Economic Performance (%) Indicator

2005 Actual

2006 Actual

2006 MTPDP Targets

Gross National Product Growth Rate (%) 5.6 6.2a 6.5–7.5 GDP Growth Rate (%) 5.0 5.4a 6.3–7.3 Investment/Nominal GDP (%) 15.1 14.8 28.0 Inflation Rate (%) 7.6 6.2 4.0–5.0 91-Day T-Bill Rate (%) 6.4 5.4 7.5–8.5 Fiscal Balance (% of GDP) (2.7) (1.1) (2.9) Consolidated Public Sector Fiscal Position (% of GDP) (1.9) 0.2 (5.3) Exports of Goods, Growth Rate (%) 3.8 14.6 10.0 Import of Goods, Growth Rate (%) 8.0 10.6 11.0 Current Account Balance ($ million) 1,984.0 5,022.0 1,029.0 Current Account Balance (% of GDP) 2.0 4.3 1.0 Poverty Incidence (% of families) — 24.4d 22.9–23.9 Unemployment Rate (%) 7.8e 7.9 — Memo Items: Dubai Oil Prices, Average ($/barrel) 49.3 61.5 29.2 Peso-US Dollar Exchange Rate 55.1 51.3 55.0–57.0

( ) = negative, MTPDP = Medium-Term Philippine Development Plan, GDP = gross domestic product,. a As of January 2007. b Preliminary. c As computed by the Central Bank of the Philippines. d Based on the 2003 official poverty estimates. e Average of April, July, and October labor force surveys. Sources: National Economic Development Authority, National Statistical Coordination Board, Central Bank of the Philippines (BSP), Bureau of Treasury, National Statistics Office, and Department of Finance.

5. Reducing Fiscal Deficit. The Government has attempted to trim the fiscal deficit by raising the tax effort and improving expenditure management. After implementing several difficult tax and fiscal measures, the consolidated public sector deficit declined from a peak of 5.2% of GDP in 2003 to 1.9% in 2005, and almost balanced in 2006 (deficit of 0.2% of GDP), surpassing its target of a 2% deficit. The small consolidated public sector deficit was aided by a fall in the Government’s budget deficit of 1.1% of GDP in 2006, well below its programmed target deficit of 2.1%, and substantial reduction in the deficit of the National Power Corporation. The Government’s fiscal deficit for the first 5 months of 2007 reached P41.8 billion or stabilized around 1.0–1.5% of GDP, on track to meet its programmed target for 2007.2 Tax revenues performed strongly in 2006, growing by 22%, with revenues from value-added tax (VAT) growing by about 64% because of the implementation of reforms that increased the tax-GDP ratio to 14.3% in 2006 from 13% in 2005. Local government units (LGUs), social security institutions, and government financial institutions (GFIs) all recorded surpluses. Because of the improved fiscal position, the Government was able to reduce its borrowings in 2006; the borrowing cost also decreased.

6. The medium-term outlook for the Philippines remains positive. Projections for economic growth this year range between 5.4% and 6.0%, with an increase in growth expected in 2008 led by consumption and exports, and with recovery in investment. Notwithstanding the economy’s improved performance, GDP and gross national product (GNP) growth rates remain

2 Bureau of Treasury, Department of Finance. 2007. Budget Report for May 2007. Manila. Available:

http://www.treasury.gov.ph/

3

below the targets set by the MTPDP of 6.3–7.3% (GDP) and 6.5–7.5% (GNP). Higher growth is required to address the goals of poverty reduction and attainment of the Millennium Development Goals (MDGs). The Philippines appears on track to achieve several MDG targets but it is behind targets in health, education, and environment because of expenditure compression adopted by the Government to reduce the fiscal deficit. For the MTPDP’s macroeconomic reform efforts to bear fruit, the Government needs to address wide-ranging policy and institutional issues at the subnational level. More fundamentally, it has to take advantage of the initial gains arising from decentralization and devolution initiatives of the past decade, which have encouraged growth in the regions and the LGUs. While the macroeconomic and fiscal consolidation reforms have provided an enabling context for economic growth, reforms need to be more widely implemented at the LGU level. In many important ways, the LGUs are now the fulcrum of the development process and are recognized as the most important agents for pursuing sustained national growth and alleviating overall poverty. 7. Since 2004, the Government-led Philippine Development Forum (PDF) has evolved as a potent platform for advancing the country’s development agenda. Through its Working Group on Decentralization and Local Government, the PDF 3 provides a forum for dialogue on core development issues, including those concerning local governments (finance, capacity development, performance benchmarking, and policy reforms on devolution). PDF serves as a vehicle through which all stakeholders—development partners, government agencies, LGUs, private sector, and civil society organizations––coordinate their efforts by sharing information and discussing reform programs. PDF has also provided policy advice and technical backstopping to LGU Leagues4 to enhance their advocacy to key government agencies. ADB plays a major role in this working group, serving as co-chair of the sub-working group for LGU capacity development, and participating actively in development partner dialogues concerning local development. Through the PDF, ADB and the Government have shared the policy measures outlined in the LGFBR program with other development partners. 8. Moreover, the CSP encourages ADB to widen its constituency of partners to enhance the quality and relevance of its activities. Since 2005, ADB’s program has included more intensive interaction with the LGUs through loans and TA projects that support capacity development, public expenditure management, investment planning, widening access to financing sources, improved service delivery, and performance monitoring. 5 The LGFBR program is the first policy-based program cluster for the Philippines that tackles major policy issues to strengthen local governance as envisioned in the MTPDP and the CSP. It complements the broader policy support provided by the Development Policy Support Program (DPSP). While the LGFBR strengthens the LGUs and government institutions that directly support local development, the DPSP supports a broader national strategy of policy reforms in four target areas: (i) fiscal consolidation and macroeconomic stability, (ii) public financial management and anticorruption, (iii) investment climate and infrastructure, and (iv) protecting 3 Available: http://pdf.ph/decentralization_1.htm 4 LGU Leagues were created under the LGC to act as a coordinating and advocacy body for each level of local

government. These associations are the League of Provinces of the Philippines, League of Cities of the Philippines, League of Municipalities of the Philippines, and Liga ng mga Barangay (village league).

5 ADB. 2006. Technical Assistance to the Republic of the Philippines for Local Governance and Fiscal Management Project. Manila (TA 4778-PHI for $1.8 million); ADB. 2005. Technical Assistance to the Republic to the Philippines for the Local Government Finance and Budget Reform Project. Manila (TA 4556-PHI for $850,000); ADB. 2005. Technical Assistance to the Republic of the Philippines for Harmonization and Managing for Results. Manila (TA 4686-PHI for $700,000); and ADB. 2004. Technical Assistance to the Republic of the Philippines for Strengthening Provincial and Local Planning and Expenditure Management. Manila (TA 4512-PHI for $350,000) are playing key roles in reviewing the implementation of the LGC, capacity development, and implementation of the LGFBR policy actions.

4

CSP Pillars

the budget provisions for social sectors. The LGFBR program will deepen the reforms in fiscal consolidation, good governance, and improved service delivery down to the local government level. This dual-policy approach of ADB provides a comprehensive package to support the Government’s overarching objective of reducing poverty and enhancing equitable growth. Figure 1 captures the links between the two programs under the MTPDP and the CSP.

III. THE SECTOR

A. Review of the Sector and Performance

9. Unlike in many other countries, decentralization is well grounded in both the constitution and legal framework of the Philippines. The economic rationale for decentralization that it can improve governance by making public service delivery more efficient was an important consideration in shaping reforms. Local governments are in closer contact with citizens than the national Government, so they are better placed to respond to citizens’ preferences, which allow them to match services to local needs. In practice, however, decentralization reforms were mostly driven by political considerations. In the Philippines, the decision was sparked by strong reactions to a period of centralized authority. This was reflected in the 1987 Constitution, which

CSP Pillars

MTPDP Priority Areas

1. Economic growth and job creation. 2. Energy independence. 3. Social justice and basic needs. 4. Education and youth opportunities. 5. Anticorruption and good

governance.

1. Economic and fiscal reforms. 2. Governance and anti-corruption. 3. Growth and investment climate. 4. MDGs and social progress. 5. Decentralization and local

government. 6. Sustainable rural development 7. Mindanao

PDF Working Groups

LGFBR Core Areas

1. Fiscal consolidation. 2. Governance. 3. Investment climate. 4. Social sectors.

1. Intergovernmental fiscal relations. 2. Fiscal management, planning and

expenditure management. 3. LGU performance measurement and

service delivery. 4. Credit financing. 5. Local own-source revenues.

1. Fiscal consolidation. 2. Strengthening investments. 3. Good Governance. 4. Support for achieving

Millennium Development Goals.

DPSP Core Areas

Figure 1: Links between the Medium-Term Philippine Development Plan Philippine Development Forum, ADB’s CSP, and the LGFBR Program

CSP = country strategy and program, DPSP = Development Policy Support Program, LGFBR = Local Government Financing and Budget Reform, LGU = local government unit, MTPDP = Medium-Term Philippine Development Plan, PDF = Philippine Development Forum. Note: Bold letters show interlinks. Source: Asian Development Bank.

5

assured autonomy to local governments. The 1991 LGC outlined key aspects of the intergovernmental system by defining local functional assignments, allocating a share for LGUs in the national revenues, and allowing LGUs to raise their own revenues.6 However, while the basic structure for decentralization is now in place, there is a need to improve local fiscal capacity and to fine tune the intergovernmental relations in above areas. 10. Local Autonomy and Governance. The LGC created important local bodies like the Local Development Council (LDC) and mandated participatory planning to strengthen accountability. The LGC elaborates on local autonomy by providing the following governance features: (i) accountability, with the term of office set at 3 years; (ii) transparency, with local officials mandated to submit their statements of assets and liabilities, and members of the Sanggunian (legislative assembly) required to disclose their business interests; and (iii) participation, with local governments mandated to create local special bodies for school, health, peace, and development with representation from nongovernmental organizations (NGOs). Although decentralization can strengthen accountability, a number of key governance risks emanating from the inherently political nature of decentralization could weaken the economic benefits of decentralization: (i) state/elite capture, (ii) clientelism, (iii) capacity constraints, (iv) power struggle between levels of government, and (v) weaknesses in interregional informational flows that are critical for effective competition (Appendix 5). Powers in the LGUs tend to be concentrated in the executive, with weak representation from institutions that are to check on state capture, such as the judiciary. This is mitigated partly by the countervailing forces of empowerment of, and widening participation by, communities in local affairs. Civil society groups in the Philippines have mushroomed at the local level. 11. Local Autonomy and Service Delivery. The LGC devolved responsibilities of the Government to the LGU level at three tiers (Figure 2). LGUs were made responsible for the “general welfare” of their constituencies by: (i) devolving the service delivery functions of national government agencies to LGUs, (ii) transferring the regulatory functions of certain national government agencies to LGUs (these include zoning and reclassification, watershed management and fishing vessels operating within 15 km radius of LGU shoreline); and (iii) enhancing the governmental and corporate powers of LGUs to enable them to discharge the devolved powers and functions effectively. The LGC transferred to LGUs the main responsibility for the delivery of basic services and the operation of facilities for land use planning, agricultural extension and research, community-based forestry, solid waste disposal system, environmental management, primary health care, hospital care, social welfare services, municipal services and enterprises, and local infrastructure facilities. The construction of public school buildings became a shared function between the Department of Education and LGUs. The provinces are assigned functions that involve the inter-municipal provision of services such as operation and maintenance of district and provincial hospitals. The municipalities are responsible for the delivery of basic services, such as primary health care, and construction and maintenance of public elementary schools. The sub national share of expenditure in the Philippines is around 26 percent of the total government expenditure (as compared to 46% for Vietnam and 10% for Thailand).7Appendix 5 and Supplementary Appendix A analyze the structure, functions, and issues relating to LGUs.

6 It transfers the authority for decision making, finance, and management to quasi-autonomous units of local

government; and disperses the responsibility for certain services to regional branch offices. It also transfers responsibility for decision making and the administration of public functions to local governments not wholly controlled by the central Government, but wholly accountable to it.

7 World Bank. 2005. East Asia Decentralizes. Washington, DC. There is some evidence, however, that a more accurate measure of the extent of decentralization is the share of own-source revenues: in the Philippines this ratio exceeds that of Vietnam considerably (see page 14, para 37).

6

Figure 2: Structure of the Local Government System in the Philippines

Level 1

Level 2

Level 3

Total number of cities = 118; total number of barangays = 41,995. Source: National Statistics Coordination Board (as of March 2007).

12. Administrative and Political Dimension of Decentralization. Under the LGC, provinces have administrative oversight over component cities and municipalities—except highly urbanized and independent component cities. Cities and municipalities have administrative oversight over barangays(villages). Each level of government up to the barangay has its own budget. At the national government level, five agencies have varying degrees of oversight over the LGUs. The Department of Finance (DOF) through the Bureau of Local Government Finance (BLGF) provides oversight through local treasurers and assessors regarding local revenue management and taxation. The Department of Budget and Management (DBM) oversees budget and expenditure matters. The National Economic and Development Authority (NEDA) oversees local planning at the provincial level while the Department of Interior and Local Government (DILG) oversees local planning at the city and municipal level. The Commission on Audit (COA) has oversight of accounting and audit matters. Of the five agencies, only COA has regulatory powers over LGUs. 13. Fiscal Dimension of Decentralization––Resources. In the Philippines, the concept of “finance follows function” is adhered to, which means greater local autonomy is synonymous with greater fiscal and financial autonomy. In this context, it is not surprising that most of the issues that have arisen from the implementation of the LGC relate to Book II of the LGC (Fiscal Matters and Taxation). These include issues related to intergovernmental transfers and the extent of LGUs’ taxing powers. Issues in Book III (Local Government Units), such as the conversion of municipalities to cities, also have fiscal implications. The efforts of municipalities to become cities, so that they can get larger share of transfers, is a case in point. The LGC provided greater fiscal autonomy to LGUs by entitling them to (i) a 40% share in the collection of national revenue taxes referred to as Internal Revenue Allotment (IRA), (ii) a share in the incremental revenue from the collection of VAT, and (iii) a 40% share in the tax collected from utilization of natural resources in their respective geographical areas. In addition, LGUs are empowered to levy taxes, charges, and user fees not imposed by the Government; issue debt to

National Government (20 National Government Departments)

Highly -Urbanized City

(28)

Province(81)

IndependentComponent City

(4)

Component City (86)

Municipality (1,510)

Barangays (2,726)

Barangays(211)

Barangays(3,858)

Barangays (35,200)

7

the private sector; enter into nontraditional business arrangements such as build-operate-transfer and joint venture agreements; and operate income-generating or economic enterprises. 14. Fiscal Dimension of Decentralization––Development Spending. Since the objective of decentralization is for LGUs to provide for the general welfare of their communities, the efficient and effective delivery of basic services becomes the standard by which outcomes are measured. In line with the transfer of functions and more resources at their disposal, the total LGU expenditure expanded relative to GNP and total government expenditure. Total LGU spending doubled from an average of 1.6% of GNP in 1985–1991 to 3.4% of GNP in 1992–2005. Similarly, the share of LGUs in total general government expenditure, net of debt service, rose from an average of 11.0% in the pre-Code period to an average of 24.2% in the post-Code period (Appendix 5, Table A5.1). The major increase in LGU spending on social services between 1991 and 2005 went to health and education. Aggregate LGU expenditure on health rose almost threefold from 0.1% of GNP in 1991 to 0.3% of GNP in 2005, while LGU spending on education doubled from 0.1% of GNP to 0.2% of GNP. Table 2 presents the distribution of LGU social expenditure during 2001–2005 and shows that education and health comprise more than 78% of total social expenditures. However, social expenditures for housing and community development and social welfare have been declining or stagnant over the same period.

Table 2: Subsectoral Distribution of LGU Social Expenditure, 2001–2005 (percent at current prices)

Year

Education

Health, Nutrition, and

Population Control

Labor and

Employment

Housing and Community

Development

Social

Welfare

Total Social Expenditure

2001 27.1 44.0 0.6 16.8 11.6 100.0 2002 25.5 45.7 0.6 17.2 11.0 100.0 2003 30.1 47.6 0.5 10.5 11.3 100.0 2004 29.9 49.7 0.3 9.3 10.8 100.0 2005 31.9 46.8 0.3 10.0 11.0 100.0

LGU = local government unit. Source: Department of Finance: Bureau of Local Government Finance-Statement of Receipts and Expenditures. 15. Service Delivery in Health and Education. The increase in education spending largely reflects the higher priority that local officials assign to this sector, as the LGUs did not have to absorb devolved personnel. On the other hand, the increase in health spending was largely because LGUs absorbed the devolved health personnel, which constituted over half the total cost of all devolved personnel. Studies show that average annual improvement in the percentage of underweight children per 1,000 declined from 0.93% in the pre-devolution period to 0.19% in the post-devolution period, and average annual improvement in the number of deaths per 1,000 declined from 0.70% in the pre-devolution period to 0.34% in the post-devolution period.8 On the other hand, the average annual improvement in infant mortality rate increased from 0.3% in the pre-devolution period to 1.5% during the post-devolution period. The elementary level participation rate increased from 84.6% in the pre-devolution period to 88.9% in the post-devolution period, while secondary level participation rate increased from 54.7% in the pre-devolution period to 61.7% in the post-devolution period9.

16. The major bottlenecks that constrain improvements in local service delivery and governance can broadly be attributed to four factors: (i) unclear expenditure assignments, (ii) lack of resources, (iii) weak fiscal and expenditure management, and (iv) lack of performance

8 Bautista, V.A. 2002. Philippine Experience in Health Service Decentralization. Manila: University of the Philippines. 9 Department of Education.

8

measurement. Unclear expenditure assignments result from an inappropriate matching of expenditure assignments or functions and resources both at the inter-governmental level (i.e., national government and LGUs) and intra-governmental levels (i.e., between provinces and cities). The lack of resources is mainly due to insufficient access of LGUs to development credit from public sources for social projects and private capital markets for income-generating projects, uncertainty in national transfers, and insufficient generation of local own-source revenues. Weak fiscal and expenditure management can be attributed to a lack of clear guidance and support from national government oversight agencies and weak local capacity. The ineffective performance measurement system is due to insufficient resources to improve existing systems and lack of incentives for LGUs to be more performance-oriented. These limiting factors have been categorized in the next section. B. Issues and Opportunities

1. Unclear Expenditure Assignments and Overlapping Service Delivery

Mandates 17. Although the main responsibility for the delivery of basic services has been devolved to LGUs, the institutional arrangements are not always clear. National government agencies continue to play a significant role in the planning and implementation of functions that have legally been devolved. Although Section 17 (b) of the LGC enumerates the basic services that LGUs are expected to deliver, Sections 17 (c)10 and (f)11 encourage a two-track delivery system where both the Government and LGUs can initiate devolved activities. This complicates what should have been a clear-cut assignment of service deliveries and blurs expenditure responsibilities. It has proven difficult to separate the oversight functions of line agencies from service delivery functions, as line agencies also tend to engage in direct service delivery for devolved functions. Many of the devolved national government agencies remain accountable for service delivery in their respective areas. For example, the Department of Health (DOH) continues to be in charge of the country’s overall state of health, just as the Department of Environment and Natural Resources (DENR) is still held responsible for national environmental management. Therefore, they feel compelled to make full use of Section 17 (f) of the Code, so the budgets of national agencies continue to grow disproportionately. The justification given by the agencies is that there is a need to ensure that national policy objectives are met. Furthermore, oversight agencies, such as DBM, have insufficient capacity and mechanisms to control spending for devolved functions by line agencies. There is a need to develop more indirect instruments for ensuring that policy objectives are met, such as specific grants. 18. The ability of LGUs to provide devolved services at their own discretion is further constrained by many unfunded mandates left to them by the Government. For example, LGUs are expected to provide budgetary support (either in the form of additional personnel benefits or outlays for maintenance and other operating expenses) to many national government agencies operating at the same level such as the police, fire protection, and local courts. LGUs also have to comply with nationally prescribed controls on their local budget allocations, especially in personnel services. They are required to comply with standardization of salaries in the public sector and continue to provide for additional benefits to devolved health workers under the Magna Carta for Health Workers. 10 “Notwithstanding [LGU mandate to deliver enumerated basic services and facilities], facilities, programs, and

services funded by the National Government … are not covered by the [devolution] except in those cases where the [LGU] concerned is duly designated as the implementing agency for such …”

11 “The National Government ... may provide or augment the basic services and facilities assigned to the ... LGU when the services or facilities are not made available or … are inadequate …”

9

19. Recent Developments. There is a need to clarify the expenditure assignments and functional roles of various levels of the Government to eliminate jurisdictional overlaps and to reduce the gaps between mandates and funding. This will make the expenditure and budget needs of LGUs more transparent and improve accountability in the management of their resources. Executive Order (EO) 366 was issued in 2004 requiring government departments to strategically review their operations and organizational structures. Staffing levels were to be rationalized to remove overlaps and duplications, redirect resources to vital services, and improve the quality and efficiency of service delivery. In July 2005, EO 444 was issued directing DILG to conduct a strategic review of the devolution of government services and functions. DILG is reviewing decentralization in five priority departments—Department of Agriculture, Department of Social Welfare and Development, DOF, DOH, and DENR. The review is being done in consultation with the Leagues, departments concerned, and oversight agencies. It is expected to be completed in 2008.12 20. To address the issues emerging from devolution—especially in the light of rationalization of the bureaucracy, recurring problems emerging from implementation of the LGC, and the need to review its provisions (an action prescribed in the LGC every 5 years)—the Government is exploring the possibility of constituting the Coordination Committee on Decentralization (CCD). Membership of the CCD will be drawn from the legislature, executive (oversight agencies), LGU Leagues, and others. The committee will discuss solutions to such issues and, if necessary, propose amendments to the Code.

2. Lack of Completeness, Timeliness, and Transparency in Intergovernmental Fiscal Transfers 21. National Transfers. Government transfers to LGUs are of three types: (i) formula-based block grants (i.e., IRA); (ii) origin-based share in national government revenues (i.e., share in national wealth and other taxes); and (iii) ad hoc categorical grants. Under the LGC, the aggregate IRA of LGUs is set at 40% of the actual internal revenue tax collections of the Government 3 years prior to the current year. The aggregate IRA is then divided among different local government levels as follows: 23% to provinces, 23% to cities, 34% to municipalities, and 20% to barangays. The IRA share of each tier of local government is then apportioned to individual LGUs based on population (50%), land area (25%), and equal sharing (25%)13. 22. The IRA is the most significant revenue source, especially for third to sixth income class LGUs14. For example, IRA accounts for 88% of the regular income of third income class provinces, 94.5% of fourth income class provinces, and 80% of third to fifth income class municipalities.15 The IRA surged from 3.9% of government revenues (3.3% of government expenditures or 0.6% of GNP) in 1985–1991 to 14.6% of government revenues (12.3% of government expenditures or 2.2% of GNP) in 1992–2005. The contribution of the IRA to total LGU income net of borrowings expanded from 36.7% in 1985–1991 to 64.6% in 1992–2005 for all LGUs combined (Table 3). This trend is more prominent in provinces and municipalities than cities. It increased from 33.2% (pre-LGC) to 46.2% (post-LGC) in cities, compared to 38.3%

12 ADB. 2006. Technical Assistance to the Republic of the Philippines for Local Governance and Fiscal Management

Project. Manila (TA 4778-PHI for $1.8 million) is assisting the Government in reviewing devolution of functions. 13 Equal sharing is 25% of IRA for a particular LGU level divided by the number of LGUs in that level. 14 Bureau of Local Government Finance classifies LGUs in 6 classes based on a four year average of their regular

income with 1 being the wealthiest. 15 Bureau of Local Government Finance. 2005. Statement of Income and Expenditures. Manila.

10

(pre-LGC) and 73.8% (post-LGC) for municipalities, and 38.8% (pre-LGC) and 81.0% (post-LGC) for provinces.

Table 3: IRA and Other Grants as a Portion of Total LGU Income and LGU Expenditure (%)

Government Transfers as

% of LGU Total Income Government Transfers as

% of LGU Expenditure Year Total IRA Other Grants Total IRA Other Grants

Average 1985–1991 51.4 36.7 14.7 53.2 38.0 15.2 1992–2005 66.0 64.6 0.6 67.2 65.7 0.6

IRA = internal revenue allotment, LGU = local government unit. Source: Commission on Audit, Bureau of Local Government Finance. 23. International best practice norms have been moving towards simplifying complex intergovernmental transfer systems, improving the transparency and predictability of allocations, and increasing subnational discretion over the use of these resources.16 National transfers have been criticized for: (i) lack of reliability in releases and appropriations, which undermine the ability of LGUs to plan and manage expenditures effectively; (ii) inequalities and distortions in distribution built into the current allocation system (i.e., allocation among various levels of LGUs and between different LGUs at the same level, making some LGUs such as cities better off in terms of net transfers less cost of devolved functions); and (iii) negative incentives created for local revenue generation since LGUs are assured of income from the IRA and the increase in the IRA share is subject to improvements in national tax collections instead of good governance on the part of LGUs. 24. Lack of Reliability in the IRA Release. This constraint not only affects LGUs’ ability to budget and plan effectively, but also limits their ability to tap finances since creditors rely heavily on the IRA deposits as collateral. Despite the provisions of the LGC, the Government retained considerable discretion in appropriating and releasing IRA. The transfers evolved into a highly unpredictable revenue source between 1998 and 2004 as the Government, faced with fiscal constraints, persistently reduced the amount due to LGUs. In 4 of the 6 years between 1998 and 2004, the mandated IRA share was either not appropriated in full, or not released in full or in a timely fashion, or was effectively cut because of reenactment of the budget. The gap between appropriation and obligation ranges from P1.5 billion to P16.5 billion. The Supreme Court ruled twice in favor of LGUs: in 2000, it ruled that the IRA should be released automatically; and in 2004, it ruled that the IRA should not only be automatically released but also distributed according to the Codal formula. In July 2006, the Government closed the loop by passing the Republic Act 9358 which provided for automatic annual appropriation of the IRA without the need to pass through Congress. To complement the reforms in the predictability, transparency, and timeliness of the IRA releases, DBM has started posting IRA shares of LGUs on its website beginning January 2007. DBM is also instituting the distribution of a local budget memorandum (LBM) to LGUs, announcing their IRA shares for the next year by June of every year. The monthly releases of the Notice of Cash Allocations will also be posted along with the comprehensive allotment release within the first quarter of every year.

25. Inter and Intra LGU Inequalities in the IRA. Although the IRA transfer to LGUs has exceeded the cost of devolved functions in the aggregate, for some LGUs (notably provinces

16 Shroeder, L., and P. Smoke. 2003. Intergovernmental Fiscal Transfers: Concepts, International Practice and Policy

Issues. Manila.

11

and municipalities) the transfers do not completely cover the cost of devolved functions. Generally, cities have emerged as relative winners in accessing transfers while provinces and municipalities have not fared favorably (118 cities share 23% while 1,510 municipalities share 34% of the IRA). This has created incentives for municipalities to lobby to become a city. This points to the need for strengthening the capacity of the Government to equalize fiscal capacity and to monitor the financial performance of LGUs. DILG is currently commissioning a study to recommend amendments to the IRA allocation formula with a more equalizing factor. 26. Non-IRA Transfers: Grants. The Priority Development Assistance Fund (PDAF) is allocated to members of Congress for discretionary spending at LGU level. These funds have been channeled to local investments in a non-transparent way, undermining LGU planning for strategic use of such funds. It is estimated that non-IRA funding to LGUs is P25.4 billion, with Congressional allocations amounting to over 60% of this amount.17 To improve transparency in the allocation and use of such funds, DBM is posting the PDAF figures on its website. 27. Non-IRA Transfers: Share in National Wealth. Some LGUs are entitled to a 40% share in tax collections and royalties from the exploitation of their natural resources. These special shares include mining taxes, tax on energy resources, forestry charges, and mining royalties. The timely and complete release of LGU shares in national wealth taxes was hampered by: (i) problems in accurately estimating the tax collections from natural resources since actual tax collections for the immediately preceding year are not yet known when the General Appropriations Act (GAA) is prepared; and (ii) lack of information on the situs18 of the tax. In February 2006, DBM, DOF, DENR, and Department of Energy issued Joint Circular No. 2006-1 which streamlined estimation and determination of the situs and procedures for release of LGU shares in national wealth by reducing the documentary requirements from five to two.

3. Weak Governance and Systems in Public Financial Management, Local Development Planning, and Expenditure Management

28. Planning and Budgeting Linkage. The LGC prescribes a participatory approach to planning and mandates that each LGU should have a comprehensive, multi-sectoral development plan formulated by its LDC and approved by its legislature. However, only 30–50% of LGUs have LDCs in place. In addition, the LGC mandates that 25% of LDC members should come from NGOs, but compliance is poor. Weak coordination between the Government and LGU planning has resulted in a break in the planning chain—occurring between the regional and provincial levels. Local officials report that their investment plans are formulated independent of regional and national investment plans and vice versa. Less than 70% of provinces have up-to-date local development plans (LDPs) and annual investment plans (AIPs), which often are not linked to each other. Furthermore, AIPs do not appear to be anchored in clear goals, strategies, and programs as many LGUs do not perform systematic evaluation of projects’ costs and benefits. The integrity of local budgeting is distorted by poor revenue estimates during the budget formulation process.19 29. Recent Developments. Some recent initiatives by the Government strengthen the planning and budgeting link. In March 2007, DBM, DOF, DILG, and NEDA jointly issued joint memorandum circular (JMC) No. 1—Guidelines on the Harmonization of Local Planning, Investment Programming, Revenue Administration, Budgeting, and Expenditure Management.

17 World Bank. 2003. A Study to Revisit the LGU Financing Framework and its Implementation. Washington, DC. 18 Situs refers to the site or location of the taxable entity. 19 ADB/World Bank. 2005. Decentralization in the Philippines. Washington, DC.

12

Its purpose is to: (i) provide guidelines on the harmonization and synchronization of local planning, investment programming, revenue administration, budgeting, and expenditure management; (ii) strengthen coordination between LGUs and national government agencies on mutually supporting approaches to planning, investment programming, revenue administration, budgeting, and expenditure management; and (iii) clarify responsibilities among DILG, NEDA, DOF, and DBM relative to local planning, investment programming, revenue administration, budgeting, and expenditure management. DBM has completed and issued the Updated Budget Operations Manual (UBOM), which contains basic principles and guidelines that will form the platform for performance-based budgeting. Although it is unlikely that the organization performance indicators framework (OPIF) will be introduced to LGUs within the next 3 years, given that the priority is to internalize this effectively within the national agencies first, the directions leading towards the OPIF can be initiated through the UBOM. DBM plans to implement the UBOM in all 81 provinces and 28 highly urbanized cities by 2010. 30. Gender and Development. Guidelines for the preparation of an annual gender and development plan and budget (Joint Circular No. 2004-1 by DBM, NEDA, and the National Commission on the Role of the Filipino Women) provide guidance on the identification of gender-responsive programs, activities, and projects for inclusion in agencies’ gender and development budgets (GAA mandates all departments and agencies to set aside at least 5% of their appropriations for projects that address gender issues), and the formulation of performance indicators that will form the bases for monitoring and evaluating the agencies’ accomplishments and achievements on gender and development.20 31. Procurement. As part of expenditure management reforms, the Government Procurement Reform Act (GPRA) was passed in 2003 to: (i) address the proliferation of laws on public sector procurement, which facilitated rent-seeking and inefficiencies; (ii) reorganize and strengthen agency and local government bids and award committees and procurement units; and (iii) strengthen the system of reward and punishment in the performance of the procurement function. Implementation of the GPRA has been intensified at the LGU level. The Government Procurement Policy Board of DBM has reported that 86% of all LGUs have implemented the law as of June 2007. To address problems that LGUs are still encountering in implementation of the GPRA, DBM will develop a manual for simplified procurement procedures for LGUs and a procurement manual for barangays. 32. Financial Reporting and Audit. COA is an independent constitutional body and the Philippines’ supreme audit institution. It has introduced a National Government Accounting System (NGAS) at all levels of the Government to simplify government accounting, conform to international accounting standards, and generate periodic financial statements for better performance monitoring. The audited statements of LGUs, in accordance with NGAS, need to be made publicly available and accessible. BLGF is currently harmonizing its LGU financial reporting system for local treasurers—the statement of receipts and expenditures (SRE)— with the NGAS to achieve this. 20 Sections 446, 457, and 467 of the LGC address gender participation by explicitly providing women representation

in local councils at the three major subnational levels, although there are concerns regarding the quality of such participation. The advisory TA, Local Governance and Fiscal Management Project (footnote 5) and the TA on Strengthening Provincial and Local Planning and Expenditure Management (footnote 5) will be providing training to local development council members, including women, on participatory budget and planning process.

13

4. Lack of Effective Performance Measurement System 33. In recent years, there has been increased interest on the part of LGUs, government agencies, and international organizations in the assessment of LGU fiscal, financial, and service delivery performance. In the past, many tools were developed to evaluate the performance of local governments, but most did not prove very effective or addressed only narrow concerns. The Local Government Performance Measurement System (LGPMS) of DILG is the most promising initiative to date. It provides LGUs with a tool to assess their strengths and weaknesses in the performance of their roles and responsibilities, and uses indicators derived largely from the LGC. The LGPMS measures performance in 4 areas (governance, administration, social services, and economic development) by collecting data for 111 input and output indicators in 17 service areas. Service areas to measure performance for governance include local legislation, transparency, and participation. Service areas to measure performance in administration include revenue generation, resource allocation and utilization, financial accountability, customer service, and human resource management and development. Service areas to measure performance in social services include health and nutrition, education, housing and basic utilities, and peace, security, and disaster risk management. Service areas to measure performance in economic development include agriculture and fisheries development and entrepreneurship, business, and industry promotion. DILG has reported that the LGPMS has been introduced in all LGUs in 2007. Although under implementation, DILG (in cooperation with DOF, DBM, and NEDA) is continuously fine-tuning and improving the LGPMS, by developing a framework for its use by executive agencies. 21 The LGPMS is a self-diagnostic tool for LGUs, which may lead to quality issues that clearly limit the usefulness of the data for purposes such as performance-based grant allocation. It is envisioned that, with greater comfort of LGUs, disaggregated data for each LGU will be made available in the medium term. 34. BLGF is also setting up a database called the local government financial performance monitoring system (LGFPMS). Currently, the LGFPMS is being linked to the LGPMS to allow integration of financial data with development and service delivery data, and strengthen the linkage between measuring outputs and allocating inputs. Out of the 16 LGFPMS indicators, 11 indicators are being integrated into LGPMS. These indicators are revenue target accomplishment rate, real property tax accomplishment rate, cost of collection rate, revenue per capita, social expenditure ratio, economic expenditure ratio, personal services expenditure ratio, internal financing ration, expenditures per capita, debt servicing ratio, and public enterprises profitability rate.

5. Lack of Access of LGUs to Development Credit Financing 35. Credit financing is used by LGUs to support the development of infrastructure, capital investment, and a portion of operating expenses. Sources include domestic banks, GFIs, and loans through the Government from foreign sources. Although LGUs are empowered to borrow, the LGC puts a ceiling on debt servicing which should not exceed 20% of their regular income. The Government’s long-term vision is for the capital market, rather than national agencies, to play a dominant role in financing LGUs, although little progress has been made to end LGU reliance on GFIs, despite the initial adoption of the LGU financing framework (LFF) in 1996. Private lending is still not substantial. GFIs and the Municipal Development Fund Office (MDFO) continue to be the dominant source of LGU financing, accounting for 76% (GFIs) and 7% (MDFO) of total LGU borrowing in 2006. GFIs have an advantage in the LGU credit market

21 This will be considered under improvements to the LGPMS in the Local Governance and Fiscal Management

Project (footnote 5) and the advisory TA.

14

because of their role as LGU depository banks22 while MDFO has access to an IRA intercept mechanism in the event of a loan default. Private banks have indicated that the mandated use of GFIs as depository banks for LGUs is a significant structural impediment to their entry into the market of lending to LGUs. This is compounded by lack of reliable information on LGU creditworthiness. Nonetheless, the pool of potential LGU bond issuers has slowly grown, as specific LGUs develop a firm financial foundation. This was facilitated by the creation of the Local Government Unit Guarantee Corporation, which guarantees debt issues of LGUs from private sources. 36. Recent Developments. In February 2007, DOF issued a memorandum officially adopting the LFF and the Government’s cost-sharing arrangement, and clarifying a number of issues. The memorandum explicitly states that provision of credit to LGUs by the Government will be governed “through a policy of market segmentation, hand-in-hand with the policy to graduate creditworthy LGUs to private sources of capital”. MDFO is also commissioning a study to develop a framework for allowing LGUs to open depository accounts in private banks. The framework will improve access of LGUs to private capital markets while taking into consideration the implications this will have on GFIs and the moral hazard problems that may arise from allowing private banks open access to LGU financial accounts. Under the Local Government Finance and Development (LOGOFIND) project and the Community-Based Resource Management (CBRM) project, MDFO is lending to third to sixth income class LGUs for urban infrastructure, health, and environmental projects. In addition, the P2 billion program-policy lending facility (PROLEND), which provides provinces with a program loan for pursuing policy reforms, and the P500 million MDG fund have been launched in 2007. Both these facilities will be financed through the second-generation fund of MDFO.

6. Inadequate Local Own-Source Revenues and Inefficient Tax Administration

37. The estimated own-source revenue of sub national governments as percentage of total LGU revenue is 31.1 percent, the highest in the region (for Thailand it is 10.9% and for Vietnam it is <5%).23 In the Philippines, tax revenues accounted for 25% of total LGU income in 2006. However, studies have shown that LGUs have created revenue codes with a huge array of taxes, fees, and charges.24 Many of these are under-collected or not collected at all. In addition, many low yielding taxes impose substantial collection and administrative costs and contribute to a lack of transparency. For example, taxes on peddlers, fishing vessels, and radio fees, each bring in an average of no more than 0.02% of LGUs’ total own-source revenue. In Bacolod City, there are over 200 different rates for the mayor’s business permit fee, all of which depend on the type of establishment. There is a need to focus on taxes, fees, and charges that have high yield potential, and to improve their administration and collection. 38. Although LGUs have greater taxation powers under the LGC, local governments face disincentives to improve collections because of lack of critical tax information and inconsistent financial policy guidelines. LGUs are authorized to levy business taxes as a percentage of the gross sales of businesses. To remedy this, the LGU Leagues have actively lobbied BIR for implementation of Section 171, which requires BIR’s revenue district offices to share their tax information with the local treasurer. However, this has met with resistance from BIR which 22 GFIs do not have an IRA intercept mechanism to protect against default. They protect themselves through a “back-

to-back” agreement by requiring LGUs to sign an agreement that authorizes the GFI lender, in the event of a default for payment of interest and amortization of principal, to debit the LGUs’ IRA depository account in the GFI.

23 World Bank. 2005. East Asia Decentralizes. Washington, DC. 24 This can be attributed to the Code itself. Section 143, Tax on Business, has a very detailed schedule of fees that

can be simplified.

15

considers this to be in conflict with tax information secrecy provisions. The policy environment relating to LGU tax administration also needs to be improved. Some implementing regulations on local taxation are not favorable to all LGUs. Key among this is the guideline for taxation of bank branches in favor of the head office, and hence the LGU hosting the head office.25 The current interpretation of the relevant LGC provision has caused the bulk of the bank’s revenues to be posted to the head office—causing the bank branches, usually in less wealthy LGUs, to face a lower basis for imposition of their business tax. 39. DOF is currently reviewing sets of instructions, which will have a significant impact on the taxation powers and capacity of LGUs. The first is a draft EO that will implement Section 171 of the Code on the sharing of tax information between BIR and LGUs. The second is an amendment to Local Finance Circular 1-93 that will require banks to reflect sharing of their gross sales, in terms of amount of loans approved, at the bank branch where the loan application originated. This will increase the gross sales of these branches and give LGUs higher revenue on which to base their business tax. The third is the local finance circular, which will guide LGUs in the imposition of business taxes on mining projects. Local tax administration is severely inadequate in many LGUs. This is highlighted by the declining trend in the collection efficiency of real property tax (RPT) of both provinces and cities in the post-Code period (Appendix 5, Table A5.5). Consequently, the contribution of LGUs to total government revenues (central Government and LGUs combined) remains low—an average of 7.1% in 1992–2005 compared to 4.9% in 1985–1991 (Table 4).

Table 4: Share of National and Subnational Governments to General Government Revenue (%)

Total Revenues Tax Non-Tax Year GG NG LG GG NG LG GG NG LG

Average 1985–1991 100.0 95.1 4.9 100.0 96.1 3.9 100.0 90.9 9.1 1992–2005 100.0 92.9 7.1 100.0 93.8 6.2 100.0 87.4 12.6 1985–2003 100.0 93.4 6.6 100.0 94.2 5.8 100.0 88.1 11.9

GG = general government, NG = national government, LG = local government. Source: Commission on Audit, Bureau of Local Government Finance. 40. LGU tax administration is weighed down by three overarching deficiencies: (i) low professional qualifications of staff, (ii) inadequate automation of core tasks, and (iii) weaknesses in supporting policies at the national government level.26 The low capacity of LGU tax staff is manifested by inadequate cash controls, weak internal audit, absence of effective management, and lack of independent oversight. Some LGUs are investing in information technology (IT) to improve assessment and collection of RPT and business fees, but for a majority it remains an expensive proposition. National government bodies or local government associations, such as the League of Municipalities, have not explored adoption of a common IT platform for tax or licensing. In addition, the LGC is not completely consistent with local autonomy criteria. While boosting local tax authority, it also constrains local revenue collection through rules on rates, assessments, appeals and administrative responsibilities—leaving LGUs little control over one

25 Department of Finance. 1993. Local Finance Circular 1-93. Manila. 26 ADB/World Bank. 2005. Decentralization in the Philippines, Washington, DC.

16

of the main levers for mobilizing revenues.27 RPT amounting to 37% of local revenues is one such tax.28

41. Capacity Development in Resource Mobilization. BLGF has a critical role to play in providing technical support to LGUs in local finance and local tax administration. Its ongoing efforts include important areas such as: (i) establishing an LGU financial, fiscal, and debt monitoring system to make information available to the public; (ii) developing and disseminating a manual on various modalities for LGU finance; (iii) developing and disseminating a manual on good LGU debt management and a manual of operations for computing and establishing LGU debt service and borrowing capacity; (iv) reviewing the consistency of various local tax rulings; (v) harmonizing the SRE manual with the NGAS; and (vi) updating the Local Treasurer’s Manual. MDFO is also providing substantial capacity development support and training in standardized project financing and other areas of resource mobilization. As of June 2007, MDFO had conducted 2,551 training programs for 513 LGUs in resource mobilization and updating of local revenue code. To encourage LGUs to improve RPT collection, MDFO has provided a credit window for such improvements as part of their project. In an effort to improve RPT collection, BLGF has developed valuation standards as part of their Assessor’s Manual for code of ethics, mass appraisal, and market values as valuation basis. It is also providing training in RPT valuation standards and collection. 42. Recent Issues Advocated by the LGU Leagues. Since 1999, the LGU Leagues have been actively advocating to the Government their concerns on the IRA—including its automatic release, deductions which were outside the Codal formula, and its automatic appropriation. As a result, the Supreme Court ruled in their favor on the first two issues. In 2006, the legislature and the executive closed the remaining IRA issue by passing a law on the automatic appropriation of the IRA. Currently, the LGU Leagues are advocating more transparent and timely release of their shares in national wealth. Through the PDF, the LGU Leagues have also raised a number of issues related to the improvement of own-source revenues. They presented position papers on sharing of tax information by BIR with LGUs, the situs of tax on bank branches, and situs of tax on mining firms. C. Lessons

43. International development work on decentralization and local governance in the last two decades has generated an extensive database of knowledge and practical experience from which a number of lessons were considered while designing the LGFBR program. These include the following. 29

(i) Sustainability. A major decentralization challenge is long-term sustainability. Program design should therefore embody sustained support over a period, with exit strategies and plans for up-scaling or institutionalizing program activities. The adopted phased approach imparts flexibility to the LGFBR program to exit or upscale as the reform situation warrants.

(ii) Central Government commitment. Implementation of decentralization is not always supported by top-level central government commitment. Programs of support should be holistic, taking into consideration the interrelationships

27 United States Agency for International Development (USAID). 1999. The Governance and Local Democracy

Project (GOLD): Summary Assessment. Manila. 28 World Bank. 2005. East Asia Decentralizes. Washington, DC. 29 Organisation for Economic Co-operation and Development (OECD). 2004. Lessons Learned on Donor Support to

Decentralization and Local Governance. France.

17

between the central and local governments. The LGFBR program involves the national oversight agencies and strives to institutionalize a coordination mechanism to deal with decentralization issues on a regular basis.

(iii) Donor coordination. To ensure more effective coordination between donors and partner governments, joint government-donor forums may be established for implementing reforms and information sharing. PDF provides a joint forum for government and development partners, from which the LGFBR program has benefited.

(iv) Fiscal decentralization support. Programs designed to improve financial management (e.g., planning, budgeting, accounting) have been more successful than other fundamental improvements. Program design should take into account reforms of local tax systems, assignments, types of taxes, and tax sharing arrangements. The LGFBR program includes measures to strengthen these areas.