TRANSFER PRICING AS THE TOOL FOR AVOIDING EROSION OF THE TAX BASE Promoting Voluntary Tax Compliance as a Common Priority of Slovakia and the EU 17. 05. 2013, Hotel Bôrik

Promoting Voluntary Tax Compliance as a Common Priority of Slovakia and the EU 17. 05. 2013, Hotel Bôrik.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TRANSFER PRICING AS THE TOOL FOR AVOIDING EROSION OF THE TAX BASE

Promoting Voluntary Tax Compliance as a Common Priority of Slovakia and the EU

17. 05. 2013, Hotel Bôrik

TOOLS FOR MONITORING THE TAXPAYERS' CONDUCT

INTRODUCTION

Recent works of the OECD and the EU Joint Transfer Pricing Forum (JTPF) have established that the successful resolution of Transfer Pricing disputes rely on: Developing a targeted knowledge strategy Systematic use of appropriate techniques and

methodologies Identifying Best practices and adopting good

governance processEU JTPF – October 2012 - Transfer Pricing Risk management : http://ec.europa.eu/taxation_customs/resources/documents/taxation/company_tax/transfer_pricing/forum/jtpf/2012/jtpf_019_2012_en.pdf

EU JTPF – June 2012 – Discussion Paper on further Work in the Area of Transfer Pricing Risk assessment: http://ec.europa.eu/taxation_customs/resources/documents/taxation/company_tax/transfer_pricing/forum/jtpf/2012/jtpf_011_2012_en.pdf

OECD Draft Handbook on Transfer Pricing Risk assessment (April 2013): http://www.oecd.org/tax/transfer-pricing/Draft-Handbook-TP-Risk-Assessment-ENG.pdf

OECD – Dealing Effectively with the Challenges of Transfer Pricing : http://www.oecd.org/site/ctpfta/49428070.pdf

WHY AND HOW TO MAKE TOOLS EFFICIENT?

Finite Resources for the Tax Administration to balance with complex issues and significant Tax Base erosion risks

An effective and efficient management of transfer pricing cases meets the common interest of Taxpayers and Tax Administration: key for a successful outcome for the Tax Administration and legal certainty/possible neutralization of the tax assessment for the Taxpayers

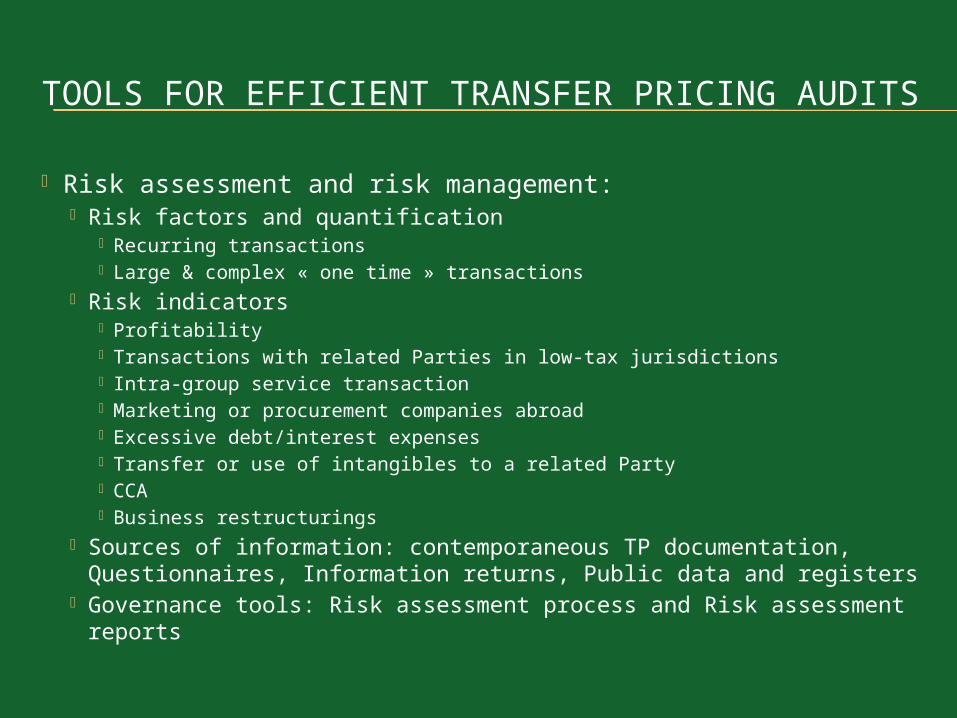

TOOLS FOR EFFICIENT TRANSFER PRICING AUDITS

Risk assessment and risk management: Risk factors and quantification

Recurring transactions Large & complex « one time » transactions

Risk indicators Profitability Transactions with related Parties in low-tax jurisdictions Intra-group service transaction Marketing or procurement companies abroad Excessive debt/interest expenses Transfer or use of intangibles to a related Party CCA Business restructurings

Sources of information: contemporaneous TP documentation, Questionnaires, Information returns, Public data and registers

Governance tools: Risk assessment process and Risk assessment reports

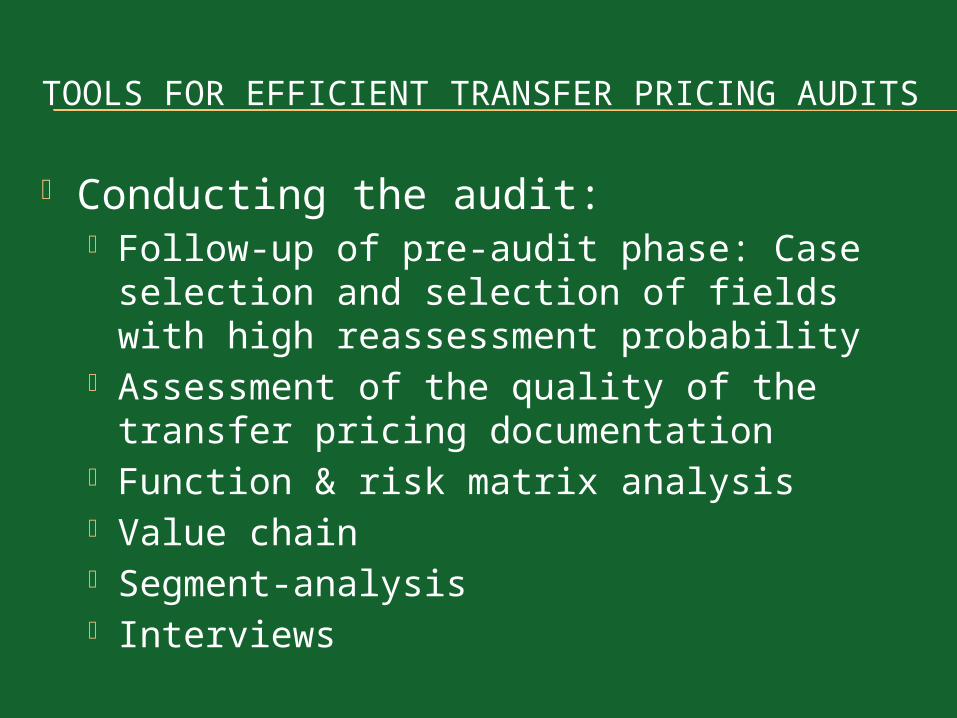

TOOLS FOR EFFICIENT TRANSFER PRICING AUDITS

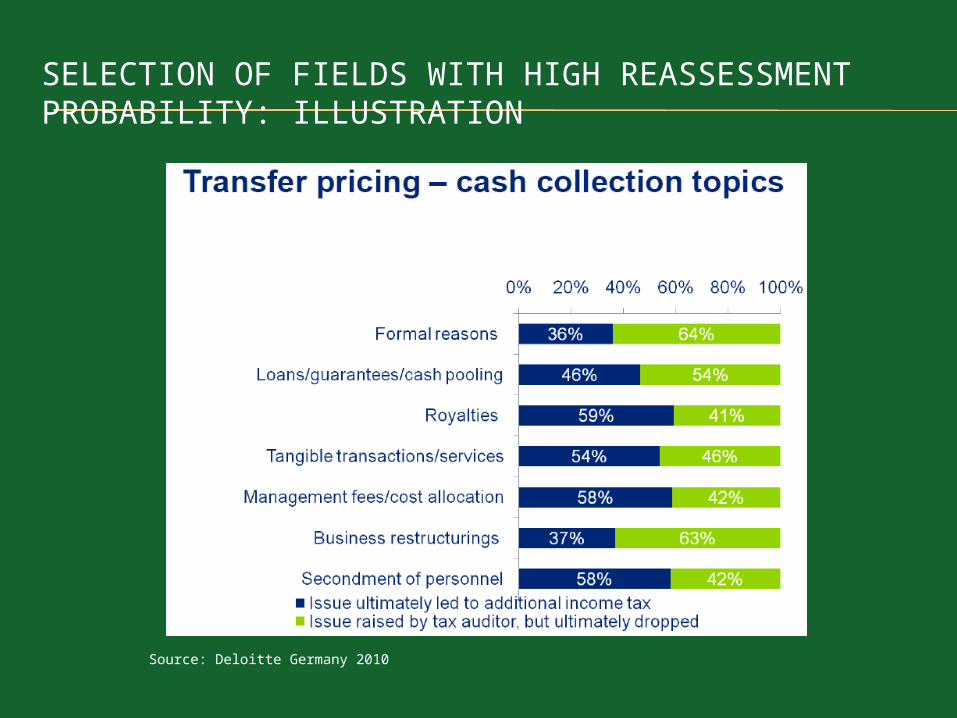

Conducting the audit: Follow-up of pre-audit phase: Case

selection and selection of fields with high reassessment probability

Assessment of the quality of the transfer pricing documentation

Function & risk matrix analysis Value chain Segment-analysis Interviews

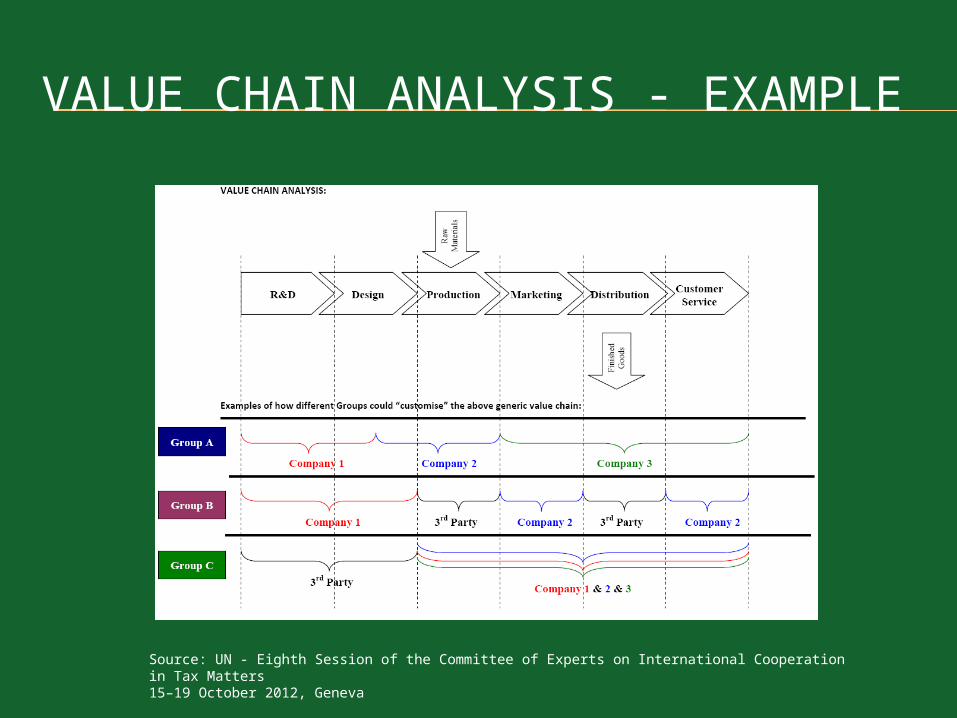

VALUE CHAIN ANALYSIS - EXAMPLE

Source: UN - Eighth Session of the Committee of Experts on International Cooperation in Tax Matters15–19 October 2012, Geneva

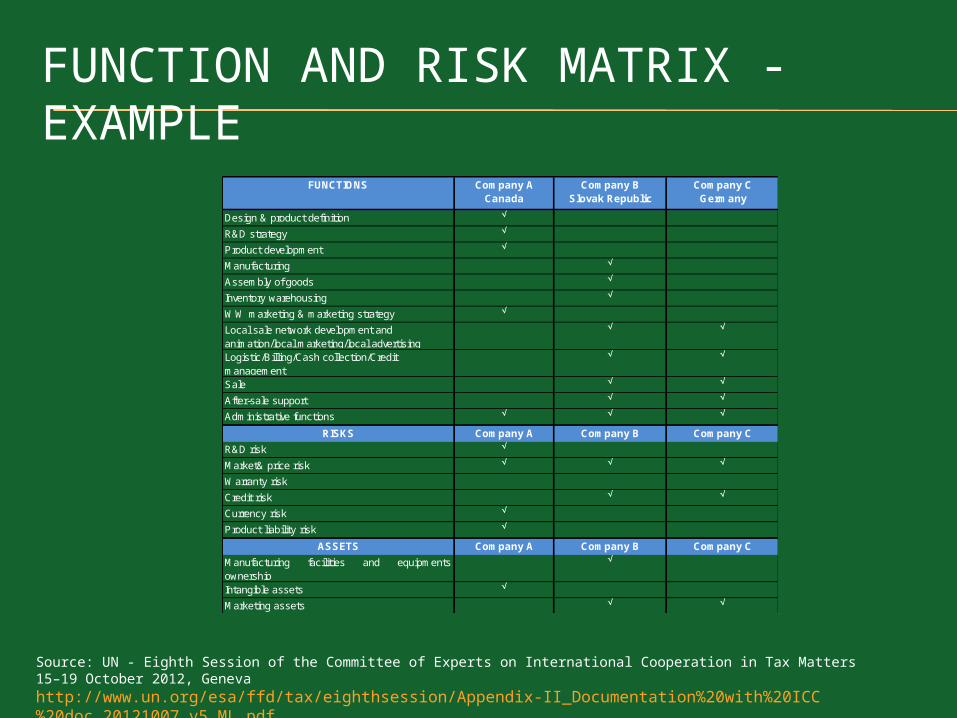

FUNCTION AND RISK MATRIX - EXAMPLE

Source: UN - Eighth Session of the Committee of Experts on International Cooperation in Tax Matters15–19 October 2012, Genevahttp://www.un.org/esa/ffd/tax/eighthsession/Appendix-II_Documentation%20with%20ICC%20doc_20121007_v5_ML.pdf

Design & product definition

R&D strategy

Product development

Manufacturing

Assembly of goods

Inventory warehousing

WW marketing & marketing strategy

Local sale network development and animation/local marketing/local advertising

Logistic/Billing/Cash collection/Credit management

Sale

After-sale support

Administrative functions

RISKS Company A Company B Company C

R&D risk

Market& price risk

Warranty risk

Credit risk

Currency risk

Product liability risk

ASSETS Company A Company B Company C

Manufacturing facilities and equipments'ownership

Intangible assets

Marketing assets

FUNCTIONS Company ACanada

Company BSlovak Republic

Company CGermany

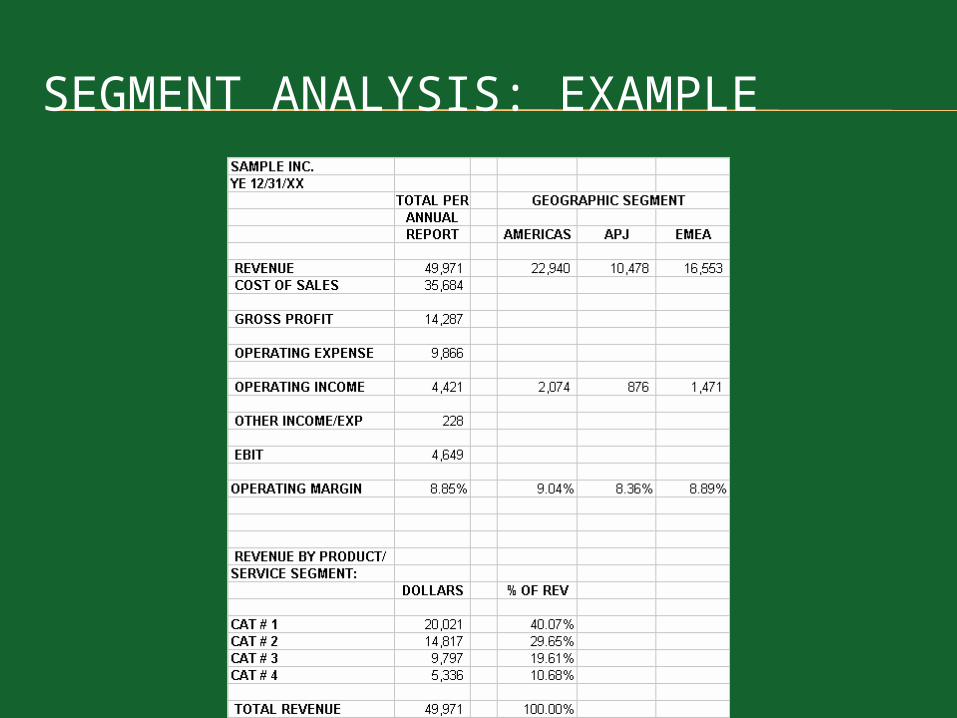

SEGMENT ANALYSIS: EXAMPLE

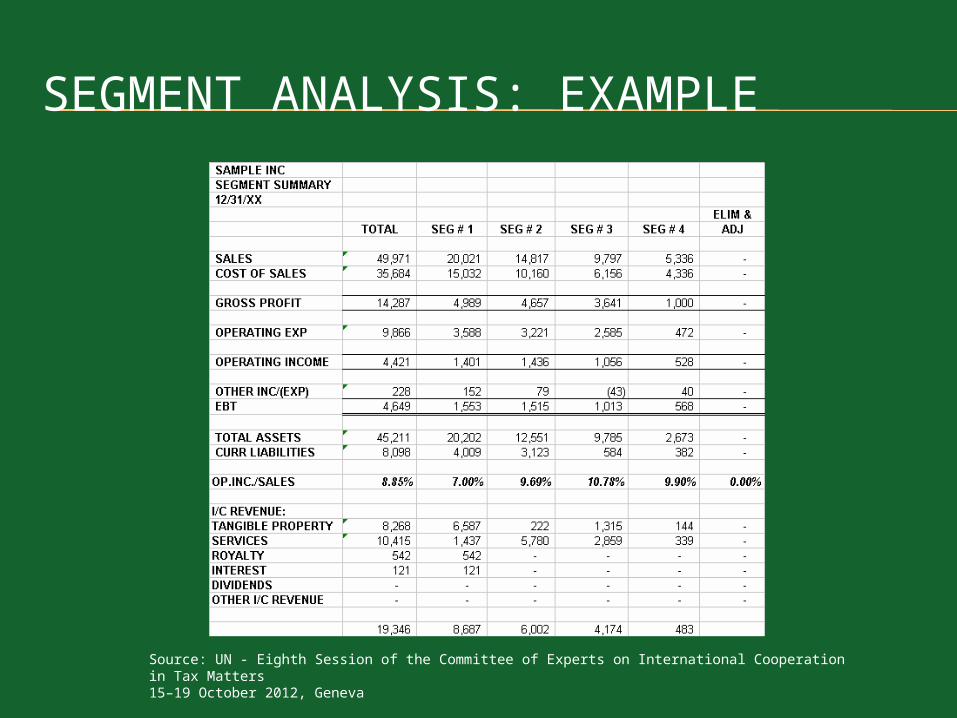

SEGMENT ANALYSIS: EXAMPLE

Source: UN - Eighth Session of the Committee of Experts on International Cooperation in Tax Matters15–19 October 2012, Geneva

SELECTION OF FIELDS WITH HIGH REASSESSMENT PROBABILITY: ILLUSTRATION

Source: Deloitte Germany 2010

TOOLS FOR DISPUTE AVOIDANCE OR ALTERNATIVE DISPUTE RESOLUTION

Advance Price Agreements (APAs) Alternative administrative procedures,

e.g. Safe harbors « Enhanced engagement approach »:

the UK and Netherlands examples

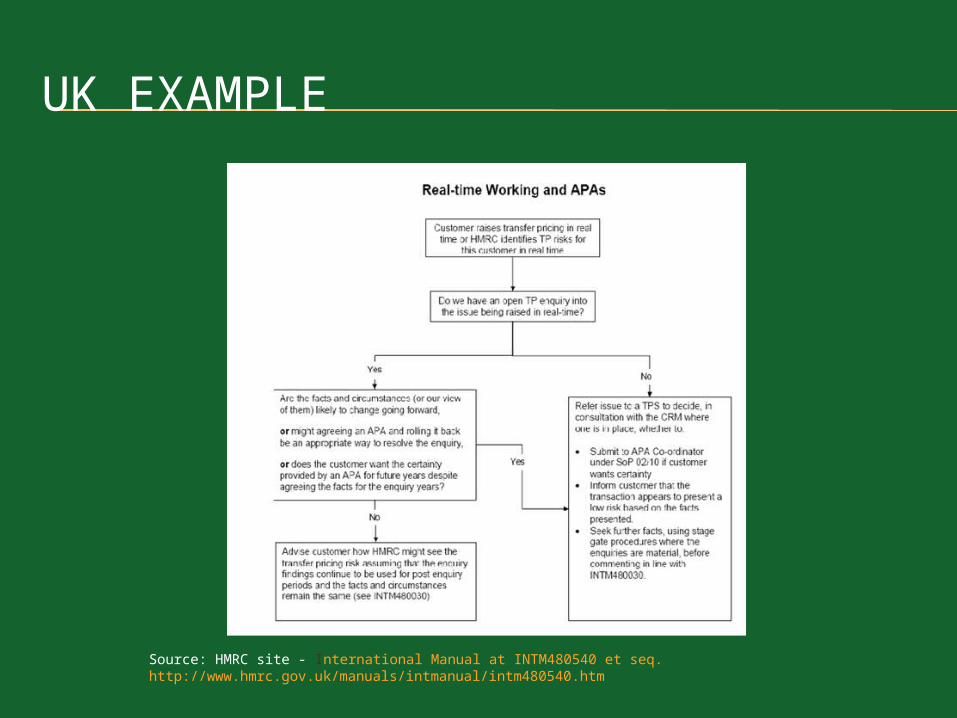

UK EXAMPLE

Source: HMRC site - International Manual at INTM480540 et seq. http://www.hmrc.gov.uk/manuals/intmanual/intm480540.htm

THE NETHERLANDS EXAMPLE

Source: HM Site – Horizontal monitoring within the Medium to Very Large Business Segment http://download.belastingdienst.nl/belastingdienst/docs/horizontal_monitoring_very_large_businesses_dv4061z1pleng.pdf

TAX EVASION PREVENTIVE MEASURES

RECENT RECOMMENDATIONS

Observation: overall effect of BEPS structures is to associate more profit with legal constructs and intangible rights and to shift risk intra-group, reducing share of profit associated with substantive operations

Improvements or clarifications to transfer pricing rules to address specific areas where current rules produce « undesirable results from a policy perspective »

Current project on intangibles Simplified appication of the TP guidelines Documentation requirements

Measures in relation to the shifting of risks and intangibles, the artificial splitting of ownership of assets between legal entities: Germany and Sweden examples

See Business restructurings and Transfer Pricing in Sweden and Germany hj.diva-portal.org/smash/get/diva2:159038/FULLTEXT01 - Företagsomstruktureringar och internprissättning i Tyskland och Sverige

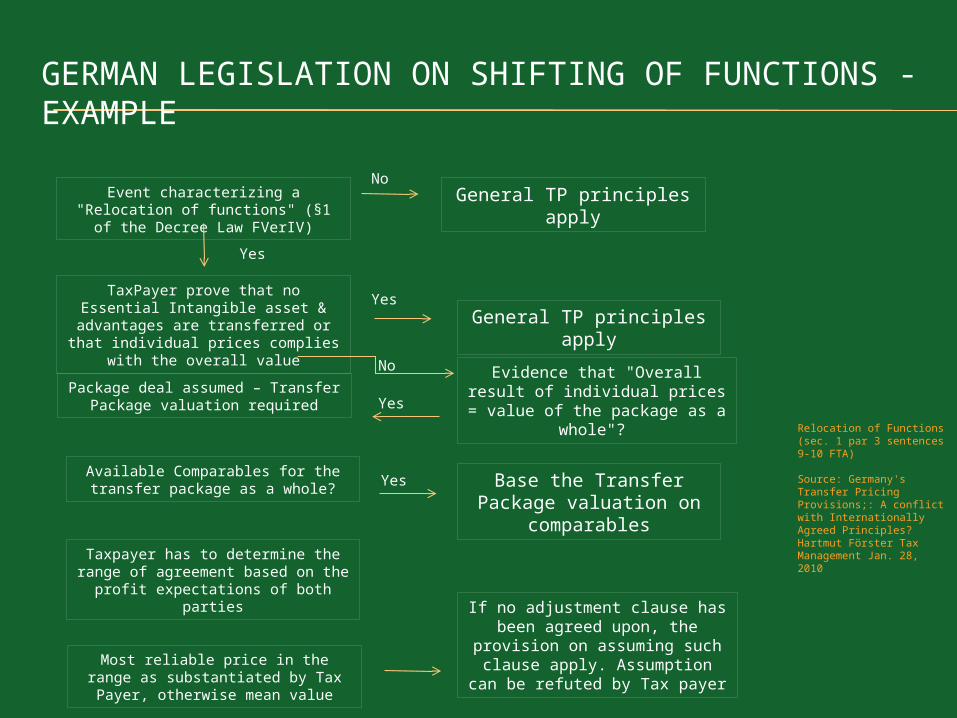

GERMAN LEGISLATION ON SHIFTING OF FUNCTIONS - EXAMPLE

Event characterizing a "Relocation of functions" (§1 of the Decree Law FVerIV)

Yes

General TP principles apply

TaxPayer prove that no Essential Intangible asset & advantages are transferred or that individual prices

complies with the overall value

Package deal assumed – Transfer Package valuation required

Available Comparables for the transfer package as a whole?

Taxpayer has to determine the range of agreement based on the profit

expectations of both parties

Most reliable price in the range as substantiated by Tax Payer,

otherwise mean value

No

General TP principles apply

Yes

Evidence that "Overall result of individual prices = value of the

package as a whole"?

Base the Transfer Package valuation on

comparables

If no adjustment clause has been agreed upon, the provision on assuming such clause apply. Assumption can be refuted by

Tax payer

Yes

No

Yes

Relocation of Functions (sec. 1 par 3 sentences 9-10 FTA)

Source: Germany's Transfer Pricing Provisions;: A conflict with Internationally Agreed Principles? Hartmut Förster Tax Management Jan. 28, 2010

CONSENSUS ON EXCHANGE OF INFORMATON

EU approach: exchange of information, simultaneous audits

The examples of BRICs and Australia

AUSTRALIA

JOINT COMMUNIQUE OF THE HEADS OF REVENUE OF BRICS – NEW DEHLI JAN. 18, 2013

« SIDE » MEASURES

How to adjust and adopt a consistent approach in terms of penalties

How to manage double taxation issues

Related Documents