Maruti Suzuki Limited “We expect that A-star will enable our company to reach a different level in our exports. Last year, Maruti Suzuki exported 53,000 cars to over 40 countries. This was the highest ever annual export in our history. However, with the A-star, we are targeting to make a quantum jump, and scale up our exports to around 200,000 cars in 2010-11.” – Shinzo Nakanishi, Managing Director and CEO, Maruti On 19th Nov 2008, India’s largest car maker, Maruti Suzuki launched its strategic model ‘A-star’ a Euro V compliant model in A-segment to explore new markets in domestic as well as overseas and primarily to boost its exports in the coming years. A-star is the fifth world strategic model of its parent company Suzuki, as a part of its global market strategy for small cars segment and to leverage the low cost manufacturing capabilities of the company. This car has been designed to keeping in mind aspirations of the urban environment conscious customers. Company has used latest technologies to make it as most fuel efficient petrol car. In addition it represents a green car, capable of being 85% of it being recycled. This would help to make the car more acceptable. With this launch company has the opportunity to re-launch itself in the European markets, which it had left two years back because lack of suitable model. Now it is targeting a yearly volume of 100,000 in Europe and other parts of the world. Company had already entered into an export contract for this new model, with Nissan a European auto giant. Company sources believe that this would take its exports to around 200,000 cars by FY 11. In domestic front also, company expect this model to be well accepted of its sporty and compact look, matching with the earlier success full launched models Swift, Dzire, and SX4. The company had already built a new technology world class manufacturing facilities at Manesar to manufacture one million units per year. In partnership with Adani Group Company build new export cargo infrastructure facilities to support its ambitious export plans. Maruti Suzuki wants to celebrate their silver jubilee by exploring new growth opportunities with this launch and plans to maintain its leadership position which it has for the last 25 years in the domestic market of Indian Automobile Industry. Industry Overview The automotive industry in India was de-licensed in July 1991, which put the industry on a new growth track, attracting foreign auto giants to set up their production facilities in India to take advantage of various benefits the latter offered. As a result, production increased manifold – from 5.3 million units in 2001-02 to 10.8 million units in 2007-08. Other reasons that attracted global auto manufacturers to India are – India’s huge middle class population, fast growth in earning power, strong technological capability, and availability of trained manpower at competitive prices. In 2006-07, the Indian automotive industry provided direct employment to more than 300,000 people, exported auto components worth around US$2.87 billion; and its contribution to the GDP reached 5%. In recognition of the large contribution of automotive industry to the national economy, the Indian government lifted the requirement of forging joint ventures for foreign companies, and thereby leading the global players to establish their production facilities in India.

project report on mariti suzuki

Jul 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Maruti Suzuki Limited

“We expect that A-star will enable our company to reach a different level in our exports.

Last year, Maruti Suzuki exported 53,000 cars to over 40 countries. This was the highest

ever annual export in our history. However, with the A-star, we are targeting to make a

quantum jump, and scale up our exports to around 200,000 cars in 2010-11.”

– Shinzo Nakanishi,

Managing Director and CEO, Maruti

On 19th Nov 2008, India’s largest car maker, Maruti Suzuki launched its strategic model ‘A-star’

a Euro V compliant model in A-segment to explore new markets in domestic as well as overseas

and primarily to boost its exports in the coming years. A-star is the fifth world strategic model of

its parent company Suzuki, as a part of its global market strategy for small cars segment and to

leverage the low cost manufacturing capabilities of the company. This car has been designed to

keeping in mind aspirations of the urban environment conscious customers. Company has used

latest technologies to make it as most fuel efficient petrol car. In addition it represents a green car,

capable of being 85% of it being recycled. This would help to make the car more acceptable.

With this launch company has the opportunity to re-launch itself in the European markets, which it

had left two years back because lack of suitable model. Now it is targeting a yearly volume of

100,000 in Europe and other parts of the world. Company had already entered into an export

contract for this new model, with Nissan a European auto giant. Company sources believe that this

would take its exports to around 200,000 cars by FY 11. In domestic front also, company expect

this model to be well accepted of its sporty and compact look, matching with the earlier success

full launched models Swift, Dzire, and SX4.

The company had already built a new technology world class manufacturing facilities at Manesar

to manufacture one million units per year. In partnership with Adani Group Company build new

export cargo infrastructure facilities to support its ambitious export plans. Maruti Suzuki wants to

celebrate their silver jubilee by exploring new growth opportunities with this launch and plans to

maintain its leadership position which it has for the last 25 years in the domestic market of Indian

Automobile Industry.

Industry OverviewThe automotive industry in India was de-licensed in July 1991, which put the industry on a new

growth track, attracting foreign auto giants to set up their production facilities in India to take

advantage of various benefits the latter offered. As a result, production increased manifold – from

5.3 million units in 2001-02 to 10.8 million units in 2007-08. Other reasons that attracted global

auto manufacturers to India are – India’s huge middle class population, fast growth in earning

power, strong technological capability, and availability of trained manpower at competitive prices.

In 2006-07, the Indian automotive industry provided direct employment to more than 300,000

people, exported auto components worth around US$2.87 billion; and its contribution to the GDP

reached 5%. In recognition of the large contribution of automotive industry to the national

economy, the Indian government lifted the requirement of forging joint ventures for foreign

companies, and thereby leading the global players to establish their production facilities in India.

Maruti2009-07

The past few years witnessed a rapid change in all the segments of the Indian passenger vehicle industry. International competition, increase in the number of participants, and the need to counter

pressure on margins made it a buyer’s market rather than a seller’s market. Today, customers have an array of models to choose from. Especially the customers comprising young adults with their

rising income levels, coupled with the low Equal Monthly Installments (EMIs), found vehicle purchase affordable. With increased foreign competition in passenger vehicles, domestic

participants are quickly moving to catch up and compete with them by investing in R&D, and improving overall efficiency. The Indian automobile market is currently dominated by

two-wheeler segment; but in future, the demand for passenger cars and commercial vehicles will increase with industrial development and also, because India has low vehicle presence (with

passenger car stock of only around 11 per 1,000 population in 2008). Taking these factors into consideration, automobile manufacturers now intend to provide cars in every segment with

widened price range so as to reach more potential customers.

Total capacity for passenger vehicles PV in India stood at around 2.5 million units in 2007-08

against 1.25 million units in 2002-03, a CAGR of around 15%. However, the capacity utilization of the industry fell to around 71% in 2007-08 from 87% in 2006-07. During 2007-08, the total

capacity increased by almost 40%. This was on account of major capacity expansions undertaken by OEMs like Honda Siel, Maruti and Hyundai towards the end of 2007-08. Moving forward, car

manufacturers announced ambitious capital expenditure plans over the next 2-3 years. Driven by high domestic demand and increasing exports, the capacity is expected to touch 3.9 million units

by 2009-10 (CRISIL).

Industry Value ChainFigure 1: Automobile Value Chain

Source: Icfai Research Team.

First the company conducts research on consumer wants and needs; and on the basis of results

obtained, designing of various models is done. Raw Material includes rubber, glass, steel, plastic

and aluminum. Tires, windshields, and airbags are examples of parts. While the automobile

industry as a whole has become more consolidated, the auto component sector remains highly

fragmented. Due to the combination of rising raw material costs and consumer’s search for the

lowest price, companies are looking for ways to cut costs out of the manufacturing process. Recent

trends to reduce costs include using fewer parts in each vehicle component, minimizing industrial

waste and pollution, and having parts delivered to assembly plants on a just-in-time basis.

Marketing is an integral part of the value chain. Automakers and individual dealers work together

to create national, regional, and local marketing strategies. Firms have now started advertising

more online. After production is complete, distribution takes place and automobiles are shipped to

local, national and to dealerships around the world to be sold.

100

Maruti2009-07

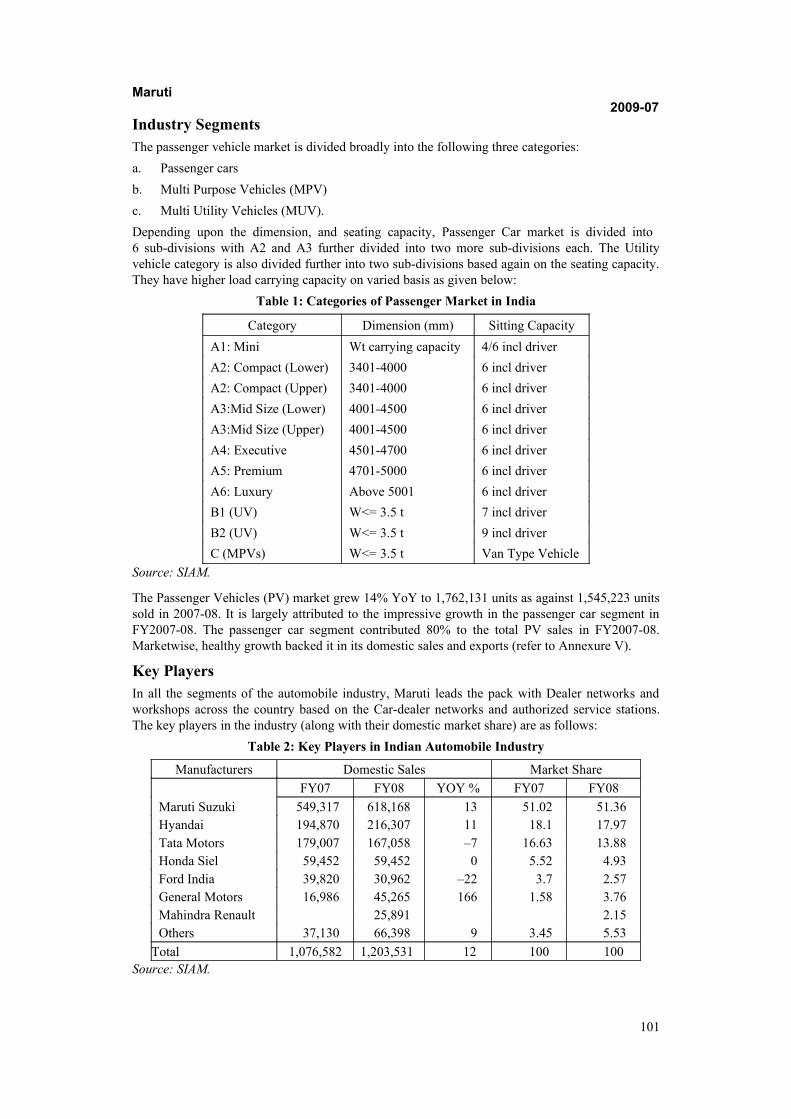

Industry SegmentsThe passenger vehicle market is divided broadly into the following three categories:

a. Passenger cars

b. Multi Purpose Vehicles (MPV)

c. Multi Utility Vehicles (MUV).

Depending upon the dimension, and seating capacity, Passenger Car market is divided into 6 sub-divisions with A2 and A3 further divided into two more sub-divisions each. The Utility vehicle category is also divided further into two sub-divisions based again on the seating capacity. They have higher load carrying capacity on varied basis as given below:

Table 1: Categories of Passenger Market in India

Category Dimension (mm) Sitting Capacity

A1: Mini Wt carrying capacity 4/6 incl driver

A2: Compact (Lower) 3401-4000 6 incl driver

A2: Compact (Upper) 3401-4000 6 incl driver

A3:Mid Size (Lower) 4001-4500 6 incl driver

A3:Mid Size (Upper) 4001-4500 6 incl driver

A4: Executive 4501-4700 6 incl driver

A5: Premium 4701-5000 6 incl driver

A6: Luxury Above 5001 6 incl driver

B1 (UV) W<= 3.5 t 7 incl driver

B2 (UV) W<= 3.5 t 9 incl driver

C (MPVs) W<= 3.5 t Van Type Vehicle

Source: SIAM.

The Passenger Vehicles (PV) market grew 14% YoY to 1,762,131 units as against 1,545,223 units sold in 2007-08. It is largely attributed to the impressive growth in the passenger car segment in FY2007-08. The passenger car segment contributed 80% to the total PV sales in FY2007-08. Marketwise, healthy growth backed it in its domestic sales and exports (refer to Annexure V).

Key PlayersIn all the segments of the automobile industry, Maruti leads the pack with Dealer networks and workshops across the country based on the Car-dealer networks and authorized service stations. The key players in the industry (along with their domestic market share) are as follows:

Table 2: Key Players in Indian Automobile Industry

Manufacturers Domestic Sales Market Share

FY07 FY08 YOY % FY07 FY08

Maruti Suzuki 549,317 618,168 13 51.02 51.36Hyandai 194,870 216,307 11 18.1 17.97Tata Motors 179,007 167,058 –7 16.63 13.88Honda Siel 59,452 59,452 0 5.52 4.93Ford India 39,820 30,962 –22 3.7 2.57General Motors 16,986 45,265 166 1.58 3.76Mahindra Renault 25,891 2.15Others 37,130 66,398 9 3.45 5.53

Total 1,076,582 1,203,531 12 100 100Source: SIAM.

101

Maruti2009-07

Regulatory Norms

Automotive Mission Plan 2006-2016

Prime Minister Dr. Manmohan Singh released India’s ‘Automotive Mission Plan’ (AMP)

2006-2016, which envisions India’s endeavors towards becoming a global auto hub. The Ministry of Heavy Industries & Public Enterprises has drawn the AMP. The AMP calls for auto sector

investments of $40 billion over the next ten years to achieve a turnover of $145 billion from the current $35 billion by 2016, accounting for 10 per cent of GDP. The Plan also focuses on

increasing India’s auto sector exports, which are presently worth $4.1 billion, to at least $35 billion so as to make India a prominent player in the global market. It is a 25-point plan to make India a

global manufacturing and export hub for small cars, multi-utility vehicles, two and three-wheelers, tractors, and auto components. The 25-point Automotive Mission Plan includes – establishment of

National Automotive Testing and R&D Infrastructure Development Project (NATRIP), several initiatives for creation and fulfillment of automotive demands, for the betterment of society and

environment, and for acting as a catalyst in generating an additional 25 million jobs.

In 2002, the Indian Government formulated an Auto Policy aimed at promoting an integrated

growth of the industry, which involved Investment Incentives by the State Governments. Some of the incentives that different states provide include: Customized incentives for Large Investments,

Automatic Approval for Foreign equity investment up to 100% and absence of minimum investment criteria. Apart from these, manufacturers engaged in in-house research and R&D

activities will get weighted tax deduction up to 150%. Also Government’s emphasis on low emission fuel auto technologies and availability of appropriate auto fuels and encouragement to

construction of safer bus/truck bodies (unorganized sector) also to 16% excise duty on body building activity as in case of OEMs.

PerformanceAs a result of various regulations, the cumulative growth in the PV segment during April 2007-March 2008 was 12.17 % in the domestic market. The growth in Passenger Cars was 11.79

%, Utility Vehicles was 10.57 %, and Multi Purpose Vehicles was 21.39% during this period. The growth in the Commercial Vehicles segment was marginal at 4.07 %. While growth in Medium &

Heavy Commercial Vehicles declined by 1.66 %, Light Commercial Vehicles recorded a growth of 12.29%. Three Wheelers sales fell by 9.71% with sales of Goods Carriers declining

significantly by 20.49% and Passenger Carriers declined by 2.13% during FY2008 compared to last year.

Automobile Exports registered a growth of 22.30% during the current financial year. The growth was led by two-wheelers segment, which grew at 32.31 percent. Commercial Vehicles and

Passenger Vehicles exports grew by 19.10 % and 9.37% respectively. Exports of Three Wheelers segment declined by 1.85%.

Future OutlookAutomotive industry is moving upward rapidly in the country and in Asian regions, principally due to a saturation of the automotive industry in the western world. Indian automobile industry is

playing a major role in Asian Automobiles markets along with the Association of South-East Asian Nations (ASEAN) and China. Various financial institutions and rating agencies analyzed the

growth rate of India’s economy and have forecast a growth in the economy in future at the rate of 8%. Although the industry bears the brunt of recession, the sales figures of December ’08 are true

indicators of global slow down. India’s growing middle class, strong economy (although recession has hit the economy, but on an optimistic and positive note, it will soon come over and bounce

102

Maruti2009-07

back), and trained workforce indicate a bright future for the automobile industry. All the big foreign players – General Motors, Mercedes Benz, Skoda Auto – are eyeing the Indian market and

all these have big plans for India and are willing to invest huge funds. Hyundai has already invested huge amounts in India and is positioned as the small car-manufacturing hub of the world,

which reflects a spiraling demand from domestic and international markets. Auto sector is emerging as one of the fastest growing manufacturing sectors both in India and across the globe.

As per the Automotive Mission Plan 2006-16, automobile industry’s contribution to the GDP would increase to 10.4% by 2015 while its size is expected to be worth US$145 billion; and also

generating a total employment of 25 million by 2016.

Maruti Suzuki India Ltd: OverviewMaruti Suzuki India limited (MSIL) is the largest passenger car manufacturer in India with a

market share of over 50%. MSIL formerly Maruti Udyog Limited (MUL) was established in Feb 1981 through an act of parliament, as a government company with Suzuki Motor Corporation of

Japan holding 26 per cent stake. Its actual production commenced in 1983 with the Maruti 800 car based on the Suzuki Alto keicer, which was the only modern car available in India at that time; its

only competitors were Hindustan Ambassador and Premier Padmini. Till 2004, it remained India’s largest selling compact car ever since its launch while MSIL remained the Indian car market leader

for over two decades. In 2002, Government of India (GOI) ceded majority control to Suzuki through rights issue. The GOI subsequently sold 25.6% of its stake to investors in an IPO. Now,

Suzuki owns 54.21% of Maruti.

Figure 2: Shareholding Pattern as on December 31, 2008

Source: www.bseindia.com

Suzuki chose Maruti to be its small car-manufacturing hub for the European market and also as an R&D center. Currently, Maruti offers a gamut of cars – from entry level Maruti 800 & Alto to

stylish hatchback A-Star, Swift, Wagon R, Estillo and sedans DZire, SX4 and Sports Utility Vehicle Grand Vitara. MSIL has two state-of-the-art manufacturing facilities in India.

The Gurgaon Facility (300 acres)

Gurgaon facility houses three fully integrated plants. The three plants have a total installed

capacity of 350,000 cars per year. Several productivity improvements or shop floor kaizens over the year have enabled the company to manufacture nearly 700,000 cars per year at the Gurgaon

facility.

The Manesar Facility (600 acres)

Manesar facility is designed to suit Suzuki Motor Corporation (SMC) and Maruti Suzuki India Limited’s (MSIL) global ambitions. The plant was inaugurated in February 2007. The World Car

derived from concept A-Star would be manufactured here. At present the plant rolls out World

103

Maruti2009-07

Strategic Models – Swift, SX4, and DZire. The plant has several in-built systems and mechanisms. The plant at Manesar is the company’s fourth car assembly plant. It started with an initial capacity

of 100,000 cars per year and presently increased to 170,000 cars per year.

Diesel Engine Facility at Manesar

The factory is situated about 20 kilometers away from the Gurgaon car plant. The diesel engine factory currently manufactures one-lakh engines, which is slated to scale to 3 lakh by 2010 with an

investment of Rs.2500 crore.

Table 3: Key Milestones of the Company

Year Events

2000 • The Company was awarded the Highest Exporter Award in New Delhi.

• The ICRA assigned ‘LAAA’ rating to the Rs.2 billion worth long-term non-convertible debenture program and ‘A1+’ rating to the Rs. One billion Commercial Paper program of the company.

2001 • Rights issue of equity in Maruti Udyog Limited, would lead to an eventual sell-off of the Government’s equity in the passenger car joint venture.

• Maruti Udyog launched its first factory-fitted CNG vehicle in a bid to promote use of eco-friendly vehicles in the domestic market.

2002 • The government on May 14, 2002 set into motion big-ticket disinvestments in 2002-03 by announcing a two-stage process to exit from Maruti Udyog Limited, a joint venture with Suzuki Motor Company.

• Suzuki takes over control in Maruti Udyog by hiking its stake in the company from 50% to 54.2%; Maruti Udyog becomes the subsidiary of Suzuki.

2003 • Company included in Morgan Stanley Capital International (MSCI) India Index.

2004 • Ties up with MRF to boost motor sports in India.

• Maruti join hands with India Times to buy and sell used cars.

• Maruti Udyog Limited’s (MUL) ties with State Bank of India for car financing.

2005 • MUL forms JV with Suzuki to sell cars.

• Maruti tops in IQS 2005 awards.

2006 • MUL unveils new WagonR in Punjab.

2007 • On May 07, 2007, Maruti Udyog Limited has launched SX4 sedan, a bold, muscular and feature-packed car, powered by the global M-series engine and built on a brand new platform.

2008 • Maruti and Mundra Port and Special Economic Zone Limited (MPSEZL) on February 20, 2008 signed an agreement for a mega car terminal at Mundra, District Kutch, Gujarat.

• Maruti Suzuki India Limited inaugurated its next-generation KB-series engine plant. The new series engine is another significant initiative the Company has undertaken in its efforts to offer the latest technology to its customers.

104

Maruti2009-07

Sources: Company Website.

Products and ServicesMaruti offers a gamut of products, ranging from Maruti 800, Maruti Omni, Gypsy, Wagon-R, Maruti Versa, Maruti Zen Estilo, Maruti Suzuki Swift, Maruti Suzuki SX4, Suzuki Grand Vitara, and Maruti DZiRE. Currently, Maruti Alto is the largest selling car in India. Maruti A-star was launched in December 2008. The upcoming model of MSIL is Maruti Splash, which will be ready to run on the roads next year. Maruti has an unparalleled service network in India. To ensure the vehicles they sold are serviced properly, Maruti has 2628 listed Authorized Service Stations and 30 Express Service Stations on 30 highways across India. Maruti provides vehicle insurance (launched in 2002) to its customers in association with the National Insurance Company, Bajaj Allianz, New India Assurance, and Royal Sundaram. As part of its corporate social responsibility, Maruti Udyog launched the Maruti Driving School in Delhi. Later these services were extended to other cities of India as well.

Business Model

Figure 3: Maruti Business Model

Source: Company Website, Icfai Research Team.

Company’s Strategies

Based on its Business model, Maruti has been offering various passenger cars. In most of the segments, it is the undisputed market leader. The Company launched three new models in the year 2008, including Premium sedan SX4, a luxury Sports Utility Vehicle Grand Vitara, and an entry-level sedan Swift DZire (in both petrol and diesel versions) even while Alto continued to be India’s largest selling car. Maruti services businesses include sale and purchase of pre-owned cars (True Value), lease and fleet management service for corporate (N2N), Maruti Insurance and

105

Maruti2009-07

Maruti Finance. The Company, in association with various banks, launched innovative financing schemes. Regular advertising is also a major activity for the company. Maruti makes available leasing services for corporate and other customers and it earns through this route also. Maruti’s revenue stream includes passenger cars, automobile financing, insurance intermediary, leasing and fleet management, pre-owned car business, and spare parts and accessories. The size of pre-owned car market is bigger than the market for new cars; thus Maruti is actively focusing on it. Since it has large product portfolio and better reach through its distribution networks, it engaged in insurance intermediary activity through tie-ups with national insurance companies.

New Engine Facility

The Company is setting up a new gasoline engine plant at its Gurgaon facilities. The new engines

produced will be more fuel-efficient and help to serve the customer better. The plant will be commissioned by producing engines for ‘A-Star’ followed by other models in the coming years. In

the year 2007-08, the Company signed two joint venture agreements with global component manufacturers for cost reduction through localization of components for Maruti Suzuki cars. The

first was with Magneti Marelli, aimed at the production of Electronic Control Units (ECU) for diesel engines and the second with Futaba Industrial Company, Japan, for production of exhaust

system parts. The focus area for component cost reduction is raw material yield improvement across all manufacturing processes, like sheet metal, castings, forgings, and machining. Every

component is studied in detail and innovative ideas tried to reduce the input material weight for the same component output. The total cost of raw material as a percentage of net sales ranges from

15% to 20%.

Performance

With the implementation of the strategies, Gross revenue of the company for FY08 stood at Rs.188,238 million, as against Rs.152,523 million in the previous year up by 23.42% backed by growth in volumes. The A3 segment (Sedans) helped co in increasing its market share from 15% to 22% due to a good demand for SX4 and Swift Dzire during the year. The Company maintained its leadership position in the A2 segment with the market share remaining above 58%. While there is intense competition for this segment, Swift drives the demand mainly. Earnings Before Depreciation, Interest, Tax and Amortization (EBDITA) stood at Rs.31,308 million against Rs.25,888 million in the previous year, recording a jump of 20.9%. Revision of the estimated useful life of certain assets resulted in depreciation being higher by Rs.2,122 million for the current year with a corresponding reduction in profit for the year and net fixed assets. Profit Before Tax (PBT) stood at Rs.2, 5030 million against Rs.22798 million in the previous year showing a growth of 9.8% and Profit After Tax (PAT) stood at Rs.17308 million against Rs.15,620 million in the previous year showing a growth of 10.8%.

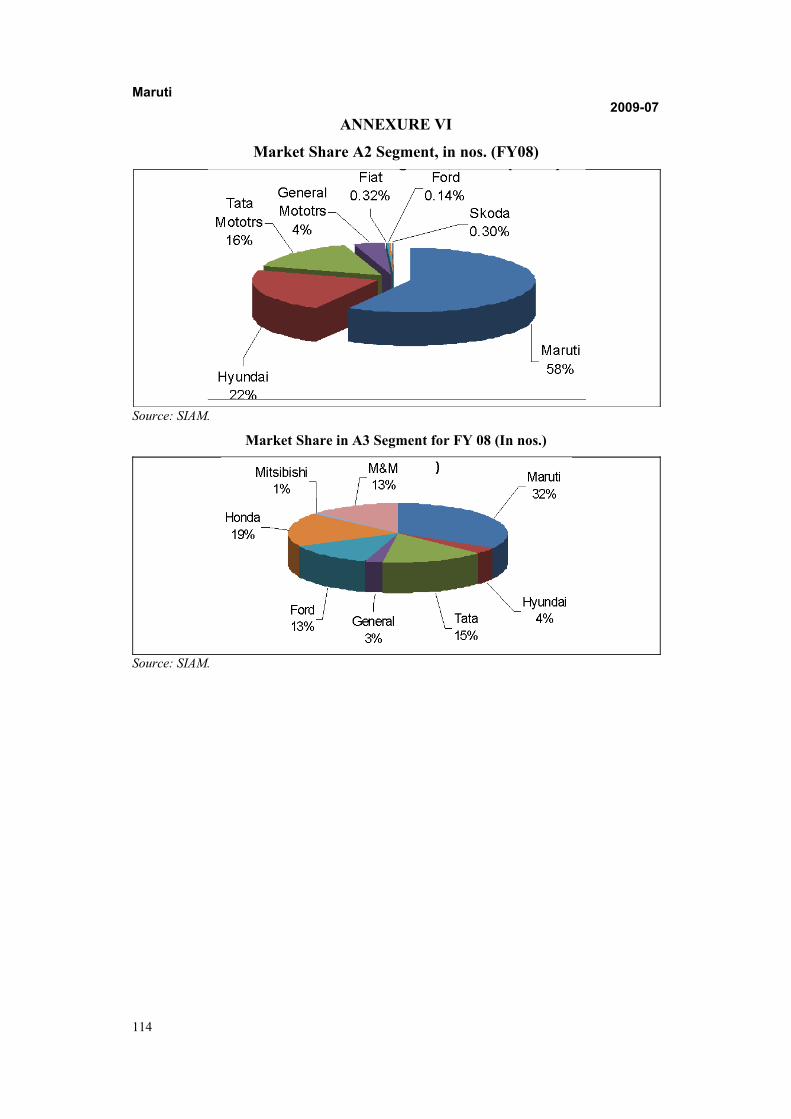

Maruti Suzuki is leader in A1 (Mini) segment mostly Maruti 800 and its variants, and has almost 100% share, while in A2 (Compact) segment it holds nearly 60% of share and models dominating here are namely, Alto, WagonR and Swift. In the A2, the main competitor is Hyundai Motors India Limited with 22% market share. A3 segment is growing at scorching pace due to rise in salary levels and demographic factors. Maruti is the market leader in this segment as well with 32% market share. There is intense competition in this segment with slew of launches in the coming season. Models dominating here are – SX4, Verna, Esteem and Swift Dzire. Swift Dzire is growing in a big way (Refer to Annexure VI).

Dominance Due to Large Sales Network

Maruti enjoys the largest sales network and service network with additions made every New Year reaching new cities and achieving scaling. The company has been taking aggressive initiatives for targeting different segments of buyers and launching the schemes for the same. Some of them are – ‘Wheels of India’ for state government employees, ‘First Class Offer’ for Railway employees, ‘Power Deal’ for NTPC employees, ‘Steel Wheel’ for SAIL employees, ‘Teachers’ Scheme’ and ‘Dil Se’ for Non-Resident Indians.

106

Maruti2009-07

The Company is ranked first for Customer Satisfaction for eight successive years in the annual survey conducted by J D Power Asia Pacific. It was the only player above industry average despite the large number of customers it has to serve. The Company dealers and authorized service stations serviced more than 10 million cars in the year.

Segmental Analysis

Vehicle Business Domestic

In Domestic market, Maruti fared well in 2007-08 as compared to 2006-07. But in FY09, its sales figures are found sliding recording the largest fall in August and November 2008, where it registered negative growth due to negligible demand from consumer side (Refer to Annexure VII).

A2 is the Driver Segment

A2 (Compact) segment is the main driver of growth. Although this year (FY09) particularly the first quarter overall sales figures declined somewhat the A2 segment is still main driver and the product mix is nearly about 66.5%. In A2 growth driver is mainly Alto and much growth is observed in swift in recent months. Foray into alternate fuel segments (with LPG powered Wagon R and diesel powered Swift) saw a very encouraging response from customers (Refer to Annexure VII).

Exports

Exports show considerably good increase in volumes due to focus on compact cars. The company

is boosting exports by adding markets such as Indonesia, Chile and Egypt for its existing models

like M800, Alto and Zen and by launching the ‘A Star’ to cater exclusively to Europe. Company

has an export target of 250,000 cars per year by 2010-11(Refer to Annexure VII).

Spares and Accessories Business

The company draws competitive advantage from the fact that its car parts are priced competitively and affordable. In FY08, the company achieved new milestone of a gross turnover of Rs.10 billion in the spares and accessories business. This marked a growth of 19% over the previous year. Company established spares stockyard in select centers across the country to meet customer requirements faster. The business is supported by a robust back end operation, which employs technology and competence in logistics to deliver on time to customers across the country.

Service Business

The service business of the company, after some initial wavering, has now taken off. It aims at enhancing all customer-related services in a transparent manner under one roof. Company believes in offering the entire range of car-related services in a convenient and transparent manner and implementing standards to improve customer service. Further, with a car population of nearly 6.5 million Maruti Suzuki cars, service maintenance and repairs make a healthy contribution to profitability of dealerships.

Pre-Owned Car Business

The pre-owned car business, or True Value is a major driver of sales performance, which facilitates new car sales through exchange and trade-ins and also contributes to dealer profitability.

In FY 08 a total of 84,323 new cars were sold in exchange, accounting for 12 percent of total new car sales.

107

Maruti2009-07

Future Outlook

By scrutinizing the its segmental performance backed by Government’s policy to encourage the

auto component manufacturers made Suzuki to take up the decision to source compact cars from India and sell them in Europe. And A-Star is the latest one on Suzuki’s map to achieve that dream.

The diesel engine plant in Manesar is established to give this a fillip. Also, the Company is focusing on the global compact car segment besides maintaining its domestic share.

Due to fluctuations in steel prices, raw material costs as percentage of sales had risen in previous three quarters and considering the global trend may continue. Currently, fall in commodity prices

will help MSIL to benefit from 1QFY10, as 2HFY09 will continue to witness higher RM cost due to inventory, contracts and adverse currency movement on imports The situation needs to be

addressed by better production planning, which include entering into long-term sourcing contracts, hedging the risks and resorting to value analysis, and value engineering to reduce wastages and

cost. Maruti is already taking steps in the right direction. Also better localization will definitely lead to cut in costs and improved efficiency.

Easy availability of low cost finance is a key demand driver for automobile sector. However, the sharp fall in commodity prices, clogging up of inventory lines, liquidity crunch faced by the Indian

banking system, drying up the other funds sources and uncertainty with respect to demand prompted the Indian corporate to either abandon or defer their Capex plans and go slow on fresh

Capex announcements.

Unlike two wheeler or commercial vehicle sector, PV market is fairly fragmented. There are 14

players and more than 80 models in the market. So, there exists high competition in the segment. Increased competition has led to fierce price competition, which in turn has resulted in reduced

margins for players. Now with increase in the cost of inputs, competition can result in further reduction in the profitability.

108

Maruti2009-07

ANNEXURE I

Additional Information

• The sales of the company will grow at the rate of 9.5%, 20% and 20% annually for the FY09, FY10 and FY11 respectively.

• Cost of goods sold will continue to remain same for FY09 and will be 82% and 80% for next two years.

• The rate of dep. will be 6.5% on gross assets for the FY09, FY10and FY11 respectively.

• Financial charges of the company for the next three years will be 8%.

• Other income for the next three years will be 5% for next three years.

• The effective tax rate will be 31%.

• Assets turnover ratio of the company will be 1.34, 1.32 and 1.33 for next three years.

• Current assets turnover ratio for the FY 09, 10 and 2011 will be 5.09, 5.01 and 5.01respectively.

• Current ratio will be 1.17, 1.20 and 1.23 for the three consecutive years.

• Perpetual growth rate for the company will be 8%.

• Risk free rate -10 year bond rate 7.6%.

• Risk premium country wise-7%.

• Company plans to invest Rs. 20,000 million CAPEX in capacity expansion in the each next three years.

Source: Icfai Research Team.

109

Maruti2009-07

ANNEXURE II

Profit and Loss Account of Maruti Suzuki for FY 2006, FY 2007 and FY 2008

Rs. in million

Particulars FY06 FY07 FY08

Net Sales 120522 146539 179362

% Growth 10% 22% 22%

Total Operating Income 124814 152523 188238

% Growth 10% 22% 23%

EXPENDITURES

Staff Costs 4644 2884.2 3562

Other Manufacturing/Operating costs 98772.4 122284 146494

Miscellaneous Expenses 839.6 1466.8 6874

Total Expenditures 104256 126635 156930

% of Net Sales 87% 86% 87%

EBITDA 16266 19904 22432

Depreciation & Amortization 2854 2714 5681.7

EBIT 13412 17190 16750.3

Financial Charges 204 376 596.2

Other Income 4292 5984 8876

PBT 17500 22798 25030.1

Pre-tax Margin % 15% 16% 14%

Tax 5609 7178 7722.3

Adjusted PAT 11891 15620 17307.8

Extraordinary Income 0 0 0

Reported PAT 11891 15620 17307.8

Source: Company Annual Report.

110

Maruti2009-07

ANNEXURE III

Balance Sheet of Maruti Suzuki for the FY 2006, FY 2007 and FY 2008

Rs. in Million

Particulars 2006 2007 2008

Sources of Funds

Shareholder’s fund

Capital 1445 1445 1445

Reserve and Surplus 53081 67094 82709

Loan Funds

Secured Loans 717 635 1

Unsecured Loans 0 5673 9001

Deffered Tax 779 1675 1701

Total Liabilities 56022 76522 94857

Application of Funds

Fixed Assets

Gross Block 49546 61468 72853

Less: Depreciation 32594 34871 39888

Net block 16952 26597 32965

Capital work in progress 920 2507 7363

Total Fixed Assets 17872 29104 40328

Investments 20512 34092 51807

Current Assets Loans and Advances

Inventories 8812 7014 10380

Sundry Debtors 6461 7474 6555

Cash and bank Balances 14016 14228 3240

Other current Assets 458 384 331

Loans and Advances 7662 9241 10403

Total Current Assets 37409 38341 30909

Less : Current liabilities and provisions

Liabilities 15058 20110 24492

Provisions 4713 4905 3695

Net current assets 17638 13326 2722

Total Assets 56022 76522 94857

Source: Company Annual Report.

111

Maruti2009-07

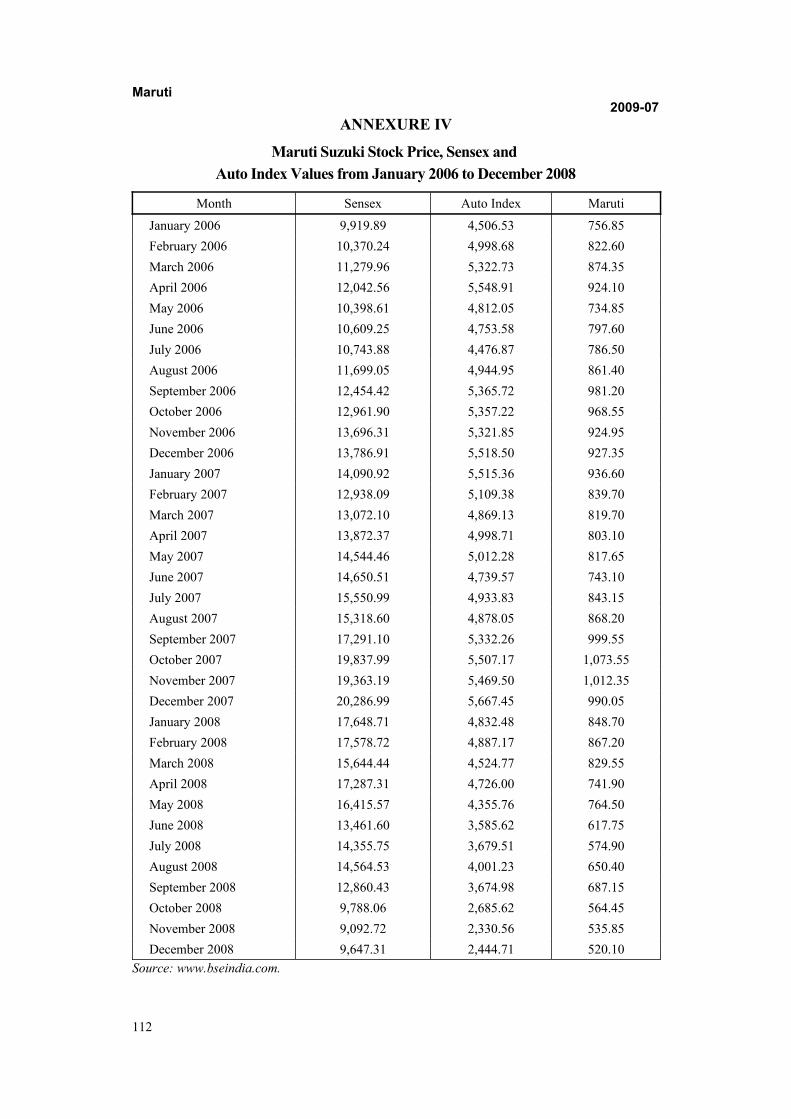

ANNEXURE IV

Maruti Suzuki Stock Price, Sensex and Auto Index Values from January 2006 to December 2008

Month Sensex Auto Index Maruti

January 2006 9,919.89 4,506.53 756.85

February 2006 10,370.24 4,998.68 822.60

March 2006 11,279.96 5,322.73 874.35

April 2006 12,042.56 5,548.91 924.10

May 2006 10,398.61 4,812.05 734.85

June 2006 10,609.25 4,753.58 797.60

July 2006 10,743.88 4,476.87 786.50

August 2006 11,699.05 4,944.95 861.40

September 2006 12,454.42 5,365.72 981.20

October 2006 12,961.90 5,357.22 968.55

November 2006 13,696.31 5,321.85 924.95

December 2006 13,786.91 5,518.50 927.35

January 2007 14,090.92 5,515.36 936.60

February 2007 12,938.09 5,109.38 839.70

March 2007 13,072.10 4,869.13 819.70

April 2007 13,872.37 4,998.71 803.10

May 2007 14,544.46 5,012.28 817.65

June 2007 14,650.51 4,739.57 743.10

July 2007 15,550.99 4,933.83 843.15

August 2007 15,318.60 4,878.05 868.20

September 2007 17,291.10 5,332.26 999.55

October 2007 19,837.99 5,507.17 1,073.55

November 2007 19,363.19 5,469.50 1,012.35

December 2007 20,286.99 5,667.45 990.05

January 2008 17,648.71 4,832.48 848.70

February 2008 17,578.72 4,887.17 867.20

March 2008 15,644.44 4,524.77 829.55

April 2008 17,287.31 4,726.00 741.90

May 2008 16,415.57 4,355.76 764.50

June 2008 13,461.60 3,585.62 617.75

July 2008 14,355.75 3,679.51 574.90

August 2008 14,564.53 4,001.23 650.40

September 2008 12,860.43 3,674.98 687.15

October 2008 9,788.06 2,685.62 564.45

November 2008 9,092.72 2,330.56 535.85

December 2008 9,647.31 2,444.71 520.10

Source: www.bseindia.com.

112

Maruti2009-07

ANNEXURE V

Passenger Vehicles Sales in India

Source: SIAM.

113

Passenger Vehicles

Maruti2009-07

ANNEXURE VI

Market Share A2 Segment, in nos. (FY08)

Source: SIAM.

Market Share in A3 Segment for FY 08 (In nos.)

Source: SIAM.

114

Maruti2009-07

ANNEXURE VII

Passenger Vehicles Domestic Monthly Sales

Monthly Sales of Passengers Vehicles

Export Volume Monthly

Source: Company Website.

115

Maruti2009-07

References

1. www.marutisuzuki.com

2. www.siam.com

3. www.atma.com

4. www.acma.com

5. www.bseindia.com

6. www.automotive.com

7. www.businessline.in

8. www.businessstandard.com

9. www.economictimes.com

10. www.wikiedia.com

11. www.moneycontrol.com

12. www.rbi.org.in

13. www.dhi.nic.in.

116

Related Documents