PROCEEDINGS OF THE INSURANCE OMBUDSMAN, DELHI (Under Rule 13 r/w 16 of the Insurance Ombudsman Rules, 2017) Ombudsman: Shri Sudhir Krishna Case of Nand Kishore versus The United India Insurance Company Ltd. Complaint Ref. No.: DEL-H-051-2122-0269 1. Name & Address of the Complainant ShriNand Kishore House No. 128, IInd Floor, Pocket-17, Sector-24, Rohini, New Delhi-110085 2. Policy No. Type of Policy Policy term/policy period 5001002818P109891131 Group Health Insurance Policy 01.10.2018 to 30.09.2019 3. Name of the insured Name of the policy holder Nand Kishore Indian Banks’ Association A/c Corporation Bank 4. Name of insurer The United India Insurance Company Ltd. 5. Date of repudiation 24.04.2020 6. Reason for grievance Rejection of post hospitalization Mediclaim 7. Date of receipt of the complaint 26.07.2021 8. Nature of complaint Rejection of post hospitalization Mediclaim 9. Amount of claim Rs.2,50,000/- 10. Date of partial settlement N.A 11. Amount of partial settlement N.A 12. Amount of relief sought Rs.2,50,000/- 13. Complaint registered under Rule No. of the Insurance Ombudsman Rules 2017 Rule 13(1)(b)- Any Partial or total repudiation of claims by an Insurer 14. Date of hearing 24.08.2021 Place of hearing Delhi, Online Video Conferencing via Cisco WebEx App 15. Representation at the hearing For the Complainant Shri Nand Kishore, the Complainant For the Insurer Smt. Pamela Pinto, Deputy Manager (LCD), Mumbai 16. Date of Award/Order Recommendation under Rule 16/ 24.08.2021 17. Brief Facts of the Case: Shri Nand Kishore (hereinafter referred to as the Complainant) has filed this complaint against the decision of The United India Insurance Company Ltd. (hereinafter referred to as the Insurers) alleging wrong rejection of post hospitalization Mediclaim. 18. Cause of Complaint: a) Complainant's Argument: The Complainant was admitted in the Chetna Neuropsychiatry Hospital in emergency and was diagnosed as a case of major depression. He was discharged from the hospital on 22.06.2019 and advised for day care treatment from 24.06.2019 to 07.07.2019. During hospitalization, 8 sittings of electro convulsive therapy were given. For continuous supervision of his health, hospital also advised him to attend weekly programme on 14.07.2019 and 21.07.2019. He claimed hospitalization bill from his individualHealth Insurance Policy & the same was settled by them. As his Sum Insured was exhausted in the Individual Health Insurance Policy, he claimed post hospitalization expenses from the subject policy. TheInsurers rejected his claim by citing many clauses i.e.5.D (Procedure to follow), 5.E.3(Authorization letter), 2.10 (Day Care center), hospitalization less than 24 hours and hospitalization not justified. Further all these conditions were applicable for admission inhospital whereas he was claiming for post hospitalization expenses.He approached the Grievance Cell of the Company but his claim was not settled. b)Insurer's Argument: The Insurance Company, vide its Self Contained dated 22.07.2021, has stated that on 01.06.2019 the Complainant was taken to Chetna Neuropsychiatry Centre by his family members with c/o restlessness, low mood, loss of appetite with gastric complaints. During hospitalization he underwent various series of investigations. After hospitalization he was shifted to Day Care Centre from 24.06.2019 to 07.07.2019 and was

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PROCEEDINGS OF THE INSURANCE OMBUDSMAN, DELHI

(Under Rule 13 r/w 16 of the Insurance Ombudsman Rules, 2017)

Ombudsman: Shri Sudhir Krishna

Case of Nand Kishore versus The United India Insurance Company Ltd.

Complaint Ref. No.: DEL-H-051-2122-0269

1. Name & Address of the Complainant ShriNand Kishore House No. 128, IInd Floor, Pocket-17, Sector-24, Rohini, New Delhi-110085

2. Policy No. Type of Policy Policy term/policy period

5001002818P109891131 Group Health Insurance Policy 01.10.2018 to 30.09.2019

3. Name of the insured Name of the policy holder

Nand Kishore Indian Banks’ Association A/c Corporation Bank

4. Name of insurer The United India Insurance Company Ltd.

5. Date of repudiation 24.04.2020

6. Reason for grievance Rejection of post hospitalization Mediclaim

7. Date of receipt of the complaint 26.07.2021

8. Nature of complaint Rejection of post hospitalization Mediclaim

9. Amount of claim Rs.2,50,000/-

10. Date of partial settlement N.A

11. Amount of partial settlement N.A

12. Amount of relief sought Rs.2,50,000/-

13. Complaint registered under Rule No. of the Insurance Ombudsman Rules 2017

Rule 13(1)(b)- Any Partial or total repudiation of claims by an Insurer

14. Date of hearing 24.08.2021

Place of hearing Delhi, Online Video Conferencing via Cisco WebEx App

15. Representation at the hearing

For the Complainant Shri Nand Kishore, the Complainant

For the Insurer Smt. Pamela Pinto, Deputy Manager (LCD), Mumbai

16. Date of Award/Order Recommendation under Rule 16/ 24.08.2021

17. Brief Facts of the Case: Shri Nand Kishore (hereinafter referred to as the Complainant) has filed this complaint

against the decision of The United India Insurance Company Ltd. (hereinafter referred to as the Insurers) alleging wrong

rejection of post hospitalization Mediclaim.

18. Cause of Complaint:

a) Complainant's Argument: The Complainant was admitted in the Chetna Neuropsychiatry Hospital in emergency and

was diagnosed as a case of major depression. He was discharged from the hospital on 22.06.2019 and advised for day

care treatment from 24.06.2019 to 07.07.2019. During hospitalization, 8 sittings of electro convulsive therapy were

given. For continuous supervision of his health, hospital also advised him to attend weekly programme on 14.07.2019

and 21.07.2019. He claimed hospitalization bill from his individualHealth Insurance Policy & the same was settled by

them. As his Sum Insured was exhausted in the Individual Health Insurance Policy, he claimed post hospitalization

expenses from the subject policy. TheInsurers rejected his claim by citing many clauses i.e.5.D (Procedure to follow),

5.E.3(Authorization letter), 2.10 (Day Care center), hospitalization less than 24 hours and hospitalization not justified.

Further all these conditions were applicable for admission inhospital whereas he was claiming for post hospitalization

expenses.He approached the Grievance Cell of the Company but his claim was not settled.

b)Insurer's Argument: The Insurance Company, vide its Self Contained dated 22.07.2021, has stated that on

01.06.2019 the Complainant was taken to Chetna Neuropsychiatry Centre by his family members with c/o

restlessness, low mood, loss of appetite with gastric complaints. During hospitalization he underwent various series

of investigations. After hospitalization he was shifted to Day Care Centre from 24.06.2019 to 07.07.2019 and was

treated for depression. As per documents submitted, details were insufficient and were not evident for concluding

the payability of claim. Hence following quarries were raised:-

1. Pre numbered cash receipt for the amount collected from the patient on 24.06.2019 for Rs.2 lakh 2. Attested copy of Indoor case papers because as per final bill, period was from 24.06.2019 to 21.07.2019 whereas

as per ICP attached, period was from 01.06.2019 to 22.06.2019. 3. Clarification from hospital for making day care bill. 4. Detailed discharge summary in original.

Reply was received from the Complainant but no clarification was provided by the treating doctor. Hence claim was

repudiated as per Policy clause 5.D, 5.E.3, 2.9 & 2.10.

19. Reason for registration of Complaint: Rejection of post hospitalization Mediclaim.

20. The following documents were placed for perusal.

a) Copy of policy. b) Copy of GRO Letter, discharges summaries, bill, claim form, rejection letters. c) SCN of the Insurers along with enclosures.

21. Result of hearing with the parties (Observations and Conclusion):

Case called. Parties are present and recall their arguments as noted in Para 18 above.

At this stage, the Insurers offer to review the claim for the Daycare treatment undertaken by the Complainant from

24.06.2019 to 21.07.2019 in terms of the Bill No. 1514 of the Chetna Neuropsychiatry Centre and settle the same as per

the terms and conditions of the policy, within 30 days. The Insurers also agree to pay to the Complainant interest on the

settlement amount in terms of the provisions of the IRDAI (Protection of Policyholders’ Interest) Regulation 2017. The

Complainant accepts this offer. Thus an agreement of conciliation could be arrived at between the Complainant and the

Insurers, which I consider as fair and reasonable for both the parties.

Award

The complaint is resolved in terms of the agreement of conciliation arrived at between the Complainant and the

Insurers. Accordingly, the Insurers shall review the claim for the Daycare treatment undertaken by the Complainant

from 24.06.2019 to 21.07.2019 and settle the same as per the terms and conditions of the policy, along with interest

on the settlement amount, as mentioned above, within 30 days.

(Sudhir Krishna) Insurance Ombudsman, Delhi

PROCEEDINGS BEFORE

THE INSURANCE OMBUDSMAN, STATES OF A.P., TELANGANA & YANAM

(Under Rule 16(1)/17 of The Insurance Ombudsman Rules, 2017)

Ombudsman - Shri Suresh Chandra Panda

Case between: Mr. B SAIDULU……………The Complainant

Vs

M/s THE NEW INDIA ASSURANCE CO.LTD.,…………The Respondent

Complaint Ref. No. I.O.(HYD).H .049.2122.0226

Award No.: I.O.(HYD)/A/HI/0039/2021-22

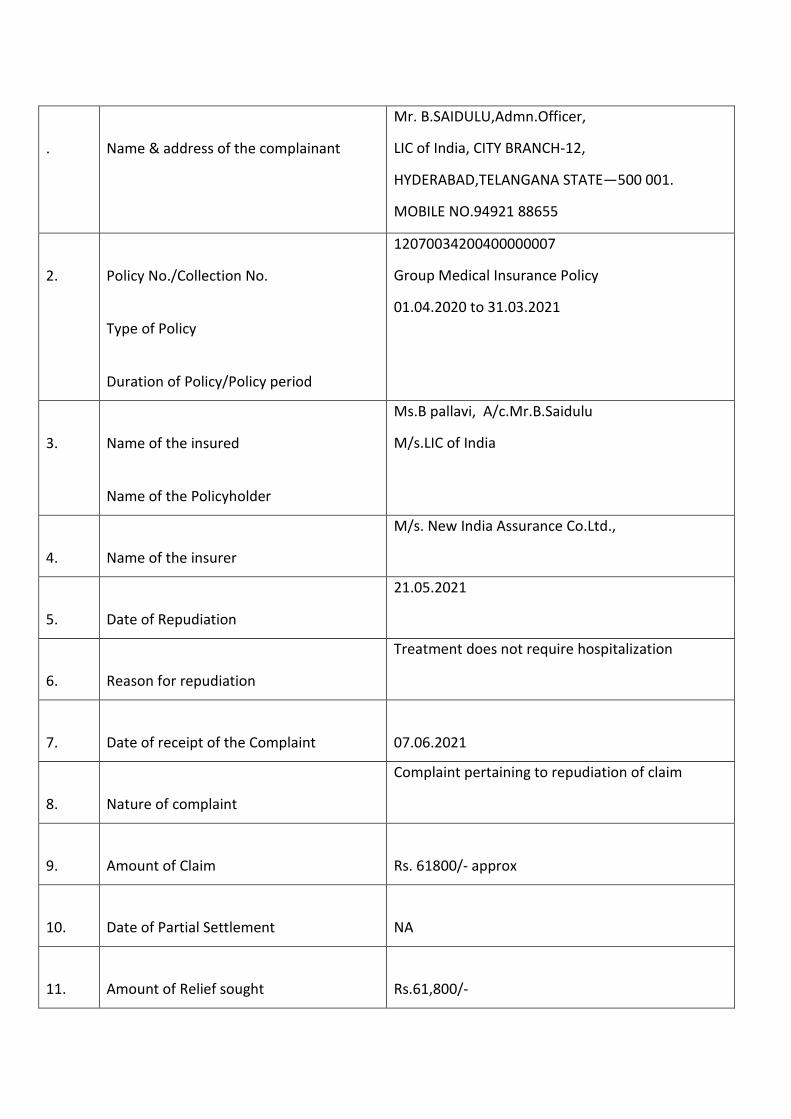

. Name & address of the complainant

Mr. B.SAIDULU,Admn.Officer,

LIC of India, CITY BRANCH-12,

HYDERABAD,TELANGANA STATE—500 001.

MOBILE NO.94921 88655

2. Policy No./Collection No.

Type of Policy

Duration of Policy/Policy period

12070034200400000007

Group Medical Insurance Policy

01.04.2020 to 31.03.2021

3. Name of the insured

Name of the Policyholder

Ms.B pallavi, A/c.Mr.B.Saidulu

M/s.LIC of India

4. Name of the insurer

M/s. New India Assurance Co.Ltd.,

5. Date of Repudiation

21.05.2021

6. Reason for repudiation

Treatment does not require hospitalization

7. Date of receipt of the Complaint 07.06.2021

8. Nature of complaint

Complaint pertaining to repudiation of claim

9. Amount of Claim Rs. 61800/- approx

10. Date of Partial Settlement NA

11. Amount of Relief sought Rs.61,800/-

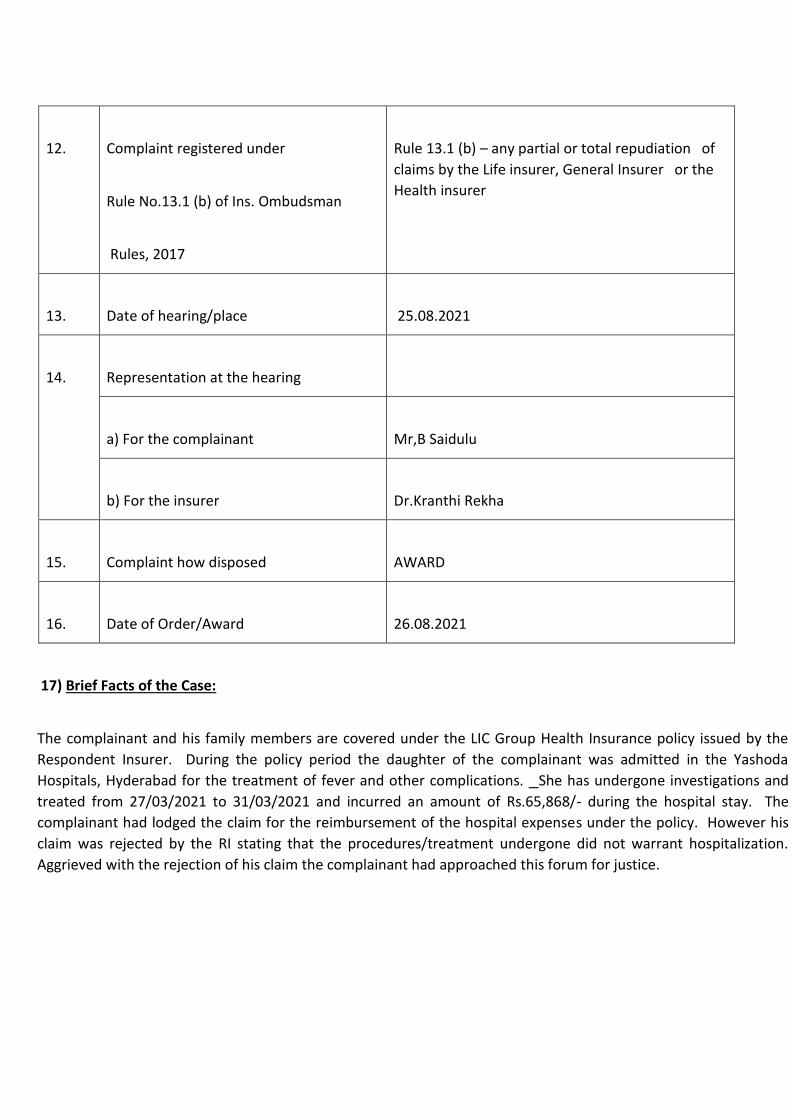

12. Complaint registered under

Rule No.13.1 (b) of Ins. Ombudsman

Rules, 2017

Rule 13.1 (b) – any partial or total repudiation of

claims by the Life insurer, General Insurer or the

Health insurer

13. Date of hearing/place 25.08.2021

14. Representation at the hearing

a) For the complainant Mr,B Saidulu

b) For the insurer Dr.Kranthi Rekha

15. Complaint how disposed AWARD

16. Date of Order/Award 26.08.2021

17) Brief Facts of the Case:

The complainant and his family members are covered under the LIC Group Health Insurance policy issued by the

Respondent Insurer. During the policy period the daughter of the complainant was admitted in the Yashoda

Hospitals, Hyderabad for the treatment of fever and other complications. She has undergone investigations and

treated from 27/03/2021 to 31/03/2021 and incurred an amount of Rs.65,868/- during the hospital stay. The

complainant had lodged the claim for the reimbursement of the hospital expenses under the policy. However his

claim was rejected by the RI stating that the procedures/treatment undergone did not warrant hospitalization.

Aggrieved with the rejection of his claim the complainant had approached this forum for justice.

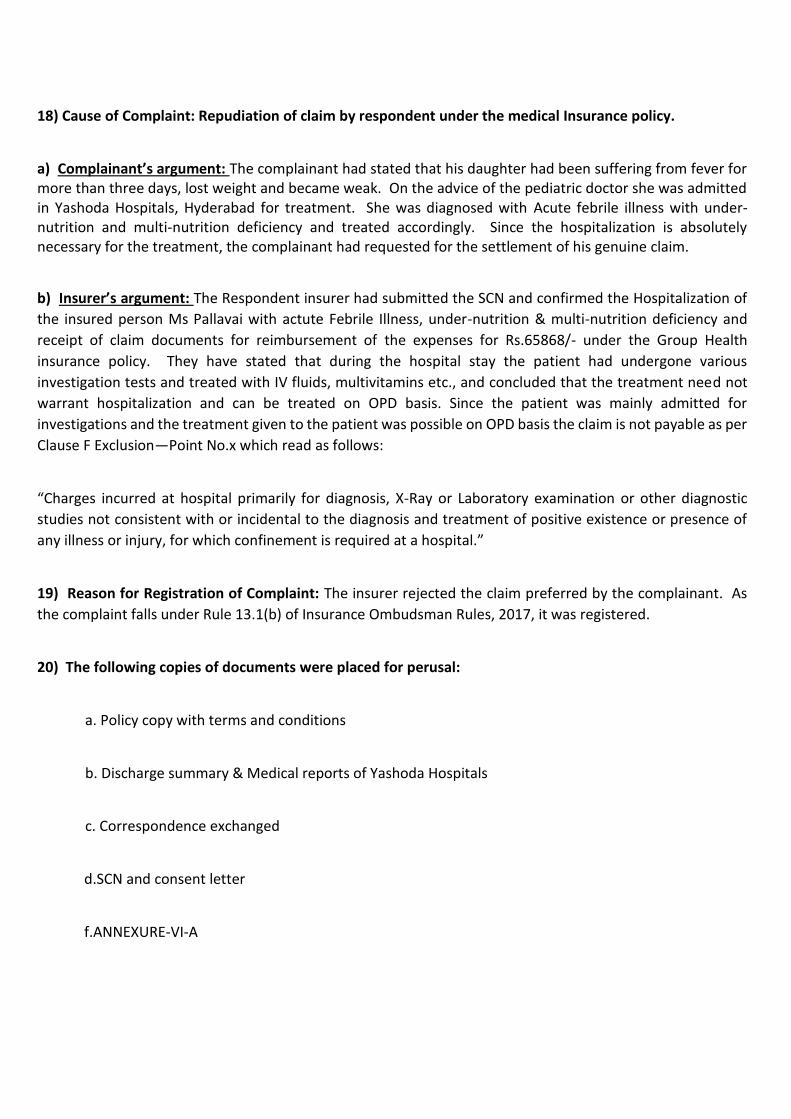

18) Cause of Complaint: Repudiation of claim by respondent under the medical Insurance policy.

a) Complainant’s argument: The complainant had stated that his daughter had been suffering from fever for more than three days, lost weight and became weak. On the advice of the pediatric doctor she was admitted in Yashoda Hospitals, Hyderabad for treatment. She was diagnosed with Acute febrile illness with under-nutrition and multi-nutrition deficiency and treated accordingly. Since the hospitalization is absolutely necessary for the treatment, the complainant had requested for the settlement of his genuine claim.

b) Insurer’s argument: The Respondent insurer had submitted the SCN and confirmed the Hospitalization of

the insured person Ms Pallavai with actute Febrile Illness, under-nutrition & multi-nutrition deficiency and

receipt of claim documents for reimbursement of the expenses for Rs.65868/- under the Group Health

insurance policy. They have stated that during the hospital stay the patient had undergone various

investigation tests and treated with IV fluids, multivitamins etc., and concluded that the treatment need not

warrant hospitalization and can be treated on OPD basis. Since the patient was mainly admitted for

investigations and the treatment given to the patient was possible on OPD basis the claim is not payable as per

Clause F Exclusion—Point No.x which read as follows:

“Charges incurred at hospital primarily for diagnosis, X-Ray or Laboratory examination or other diagnostic

studies not consistent with or incidental to the diagnosis and treatment of positive existence or presence of

any illness or injury, for which confinement is required at a hospital.”

19) Reason for Registration of Complaint: The insurer rejected the claim preferred by the complainant. As

the complaint falls under Rule 13.1(b) of Insurance Ombudsman Rules, 2017, it was registered.

20) The following copies of documents were placed for perusal:

a. Policy copy with terms and conditions

b. Discharge summary & Medical reports of Yashoda Hospitals

c. Correspondence exchanged

d.SCN and consent letter

f.ANNEXURE-VI-A

21) Result of the personal hearing with both the parties:

Pursuant to the notices given by this Forum both parties attended the OnLine hearing held on 25.08.2021 and

presented their arguments in support of their contentions. The complainant stated that his daughter was

admitted in the hospital on the advice of the pediatric doctor for treatment of fever and Loss of Weight. During

the hospitalization she was referred to various doctors, underwent investigations and treated accordingly. He

has stated that hospitalization is absolutely required for the said treatment and objected on the repudiation

of his claim on wrong premise. The insurer has argued that the treatment given to the insured person can be

done on OPD basis and does not warrant hospitalization. Since the treatment comes under policy Exclusion

the RI has justified the rejection of the claim.

Having heard the arguments and scrutinized the documents available, the Forum has observed that the insured

person was admitted in Yashoda Hospitals, Hyderabad on the advice of the consultant Pediatrician Dr. Pallavi

Bhukya. She was diagnosed with Acute Febrile Illness with undernutrition and multi-nutrition deficiency. She

underwent various investigations and referred to the doctors of Gynecology, Psychiatry, and Endocrinology

and treated for Primary amenorrhea, short stature etc., She was treated with IV Fluids, medicines and other

supportive treatment and discharged in a stable condition. In view of the above observations, the forum felt

that the insured person was hospitalized on the advice of the medical practitioner for investigations, evolution

and consequent treatment. The treatment given was in consistent and incidental to the diagnosis of

malnutrition, acute febrile illness etc.The administration of IV fluids and evolution by different doctors is not

possible as an outpatient.

In view of the above observations the forum felt that the rejection of the claim by the RI under the Policy

Exclusion No. F( x) is not consistent with the said policy exclusion. On careful study of the exclusion clause the

Forum felt that the clause is applicable only when the admission is primarily for diagnosis, x-ray or laboratory

examinations not consistent with or incidental to the diagnosis and the treatment of positive existence for

which confinement is required at a hospital. In the present instance, the insured person was admitted on the

positive existence of illness which is incidental and in consistent with the Laboratory examinations and other

diagnostic studies. The complaint has opted for hospitalization on the advice of the medical practitioner and

complied the policy condition A.1. under COVERAGES. Hence the Forum felt that the repudiation of claim under

Policy Exclusion No.F( x ) is not justified and violates the guidelines of the IRDAI on settlement of claims.

Under the circumstances of the case, the Forum finds that the repudiation of claim by the Respondent Insurer

is not in order and directs RI to settle the claim in accordance with terms and conditions of the policy.

Accordingly the Complaint is ALLOWED.

A W A R D

Taking into account the facts & circumstances of the case and the submissions made by both the parties during the course of the OnLine Hearing and the information/documents placed on record, the Respondent Insurer is directed to settle the claim as per the existing terms and conditions of the policy.

The complaint is ALLOWED.

22) The attention of the Insurer is hereby invited to the following provisions of Insurance Ombudsman Rules,

2017:

a) According to Rule 17(6), the insurer shall comply with the award within 30 days of the receipt of the award and intimate compliance to the same to the Ombudsman.

b) According to Rule 17(7), the complainant shall be entitled to such interest at a rate per annum as specified in the regulations, framed under the Insurance Regulatory & Development Authority of India Act from the date the claim ought to have been settled under the Regulations till the date of payment of the amount awarded by the Ombudsman.

c) According to Rule 17 (8), the award of Insurance Ombudsman shall be binding on the Insurers.

Dated at Hyderabad on the26 th day of AUGUST , 2021.

( SURESH CHANDRA PANDA )

OMBUDSMAN

FOR THE STATES OF A.P.,

TELANGANA AND YANAM CITY

PROCEEDINGS BEFORE

THE INSURANCE OMBUDSMAN, STATES OF A.P., TELANGANA & YANAM

(Under Rule 16(1)/17 of The Insurance Ombudsman Rules, 2017)

Ombudsman - Shri Suresh Chandra Panda

Case between: Mr. B SHANKARAIAH……………The Complainant

Vs

M/s THE NEW INDIA ASSURANCE CO.LTD.,…………The Respondent

Complaint Ref. No. I.O.(HYD).H .049.2122.0227

Award No.: I.O.(HYD)/A/HI/ 0040 /2021-22

1. Name & address of the complainant

Mr. B.SHANKARAIAH,

LIC of India, BHONGIR BRANCH OFFICE,

TELANGANA STATE—500 001.

MOBILE NO.93943 57306

2. Policy No./Collection No.

Type of Policy

Duration of Policy/Policy period

12070034200400000007

Group Medical Insurance Policy

01.04.2020 to 31.03.2021

3. Name of the insured

Name of the Policyholder

Mrs.B Maheshwari A/c.Mr.B.Shankaraiah

M/s.LIC of India

4. Name of the insurer

M/s. New India Assurance Co.Ltd.,

5. Date of Repudiation

03.03.2021

6. Reason for repudiation

Claim falls under the exclusion clause F Vi of

policy

7. Date of receipt of the Complaint 08.07.2021

8. Nature of complaint

Complaint pertaining against repudiation of

claim

9. Amount of Claim Rs. 190,000/- approx

10. Date of Partial Settlement NA

11. Amount of Relief sought Rs.190,000/-

12. Complaint registered under

Rule No.13.1 (b) of Ins. Ombudsman

Rules, 2017

Rule 13.1 (b) – any partial or total

repudiation of claims by the Life insurer,

General Insurer or the Health insurer

13. Date of hearing/place 25.08.2021

14. Representation at the hearing

a) For the complainant Mr.B.Sankaraiah

b) For the insurer Dr.Kranthi Rekha

15. Complaint how disposed AWARD

16. Date of Order/Award 26.08.2021

17) Brief Facts of the Case: The complainant and his family members were covered under the LIC Group Health Insurance Policy issued by the Respondent Insurer. During the policy period his wife was admitted in Neelima Hospitals, Hyderabad with complaints of abdominal distension and swelling in supra umbilical area. She was diagnosed with Para Umbilical Hernia for which she underwent Laparoscopic Hernioplasty and discharged in stable condition. The complainant had lodged claim with the Respondent Insurer for the reimbursement of the expenses. However his claim was rejected by the Respondent Insurer stating that the cause of hospitalization comes under Obesity which was excluded under the policy exclusion Clause F Vi. However the complainant had represented that the present hospitalization of Para Umbilical Hernia was not related to Obesity and objected for applying the exclusion which was not relevant for the present illness and approached this forum for justice.

18) Cause of Complaint: Partial Repudiation of claim by respondent under the medical Insurance policy.

a) Complainant’s argument: The complainant had stated that he had admitted his wife for the treatment of

Para Umbilical Hernia and underwent Hernioplasty. He had spent Rs.190,000/- and applied for reimbursement

of medical expenses. However his claim was rejected on the grounds that Umbilical Hernia was occurred due

to Obesity which was excluded under the policy exclusion Clause F Vi. The complainant argued that his wife

was treated for Para Umbilical Hernia which was not connected with the Obesity and its complications. He has

also produced the Certificate from the Neelima Hospitals confirming that the treatment did not relate to

Obesity. He had reiterated that the treatment undergone by his wife was not related to obesity and its

complications and should not apply the policy exclusion Clause of F Vi. He had objected on rejecting the claim

on false pretexts and prayed for justice.

b) Insurer’s argument: The RI has submitted the SCN on 17/08.2021 and confirmed the admission of the

Insured person in Neelima hospital from 24/12/2020 to 01/01/2021 with chief complaints of abdominal

distension since 2 years, swelling in supra umbilical area, DM+,HTN+,History of LSCS. She was diagnosed with

Para Umbilical Hernia and underwent Laparoscopic Mesh Hernioplasty on 31/12/2020 and discharged on

01/01/2021. However, the RI had stated that the Umbilical Hernia can develop when fatty tissue or a part of

the bowel pokes through into an area near the naval and attributed the factors that can cause the Umbilicical

Hernia to overweight or obese, straining while moving or lifting heavy objects. Since the insured person was

an obese with morbid obesity(BMI >35) they have concluded that the main cause for the Paraumbilical Hernia

is obesity which comes under the policy exclusion clause F (vi) which states that the Company shall not be

liable for expenses connected with or in respect of “Convalescence, general debility, Run Down condition or

rest cure, OBESITY TREATMENT AND ITS COMPLICATIONS, congenital external disease/defects or anomalies,

infertility, sterility, use of intoxicating drugs/alcohol, use of tobacco leading to cancer.”

Hence the RI had justified the rejection of the claim as per the terms and conditions of the policy.

19) Reason for Registration of Complaint:

The insurer rejected the claim preferred by the complainant. As the complaint falls under Rule 13.1(b) of

Insurance Ombudsman Rules, 2017, it was registered.

20) The following copies of documents were placed for perusal:

a. Policy copy with terms and conditions

b. Discharge summary

c. Correspondence with the Insurer

d. ANNEX-VI-A

e.SCN

21) Result of the personal hearing with both the parties:

The Forum after perusing the complaint and relevant documents arranged the OnLine Hearing on 25.08.2021.

Both the parties have attended the Hearing from their respective places and submitted the arguments in

support of their contentions. During the course of the interaction the complainant has stated that the

treatment was not related to obesity and the claim is payable under the policy. However the RI has referred

the Medical journals and Reference Books and justified their conclusion of obesity as the proximate cause for

the present illness.

The Forum has carefully gone through all the documents placed before the forum and heard the arguments of

both parties. Based on the arguments and documents available with this forum it is observed that the insured

person was admitted in Neelima Hospital, Hyderabad with complaints of abdominal distention since 2 years

and swelling in supra umbilical area, DM+, HTN+, History of LSCS. She was diagnosed with PARA UMBILICAL

HERNIA and underwent Laparoscopic Hernioplasty. The complainant has lodged the claim with RI for the

reimbursement of the medical expenses incurred during the hospitalization. However the claim was rejected

by the RI stating that the insured person was obese with morbid obesity which is the main cause for

Paraumbilical Hernia and comes under the policy exclusion F vi. The Forum has noted that the most common

causes for Umbilical hernia in adults are Chronic health conditions that raise abdominal pressure, Carrying

excessive belly fluid (ascites), chronic cough, difficulty urinating due to an enlarged prostate, prolonged

constipation, repetitive omitting, obesity, straining such as during child birth or weight lifting. The forum has

observed that obesity may be one of the contributory factor for Paraumbilical Hernia and other factors may

not be ruled out for causing Paraumbilical Hernia. In fact the obesity has a higher chance of developing the

health problems of High Blood glucose or diabetes, High Blood Pressure(HTN), High Blood cholesterol and

triglycerides, Heart attacks, heart failure and stroke, Bone and joint problems, sleep apnea, gallstone and liver

problems etc., Hence if we apply the obesity and its complications for admissibility of claims under the policy

no claim is payable under the policy.

On careful examination of the policy exclusion F vi. the forum has observed that the policy excludes OBESITY

TREATMENT AND ITS COMPLICATIONS which may be inferred as Obesity treatment and the complications of

obesity treatment i.e. after effects of obesity treatment. The Forum accepts that the policy is the evidence of

contract and subject to terms conditions and exclusions. However while interpreting the policy exclusions the

RI should not deviate from the main purpose of the contract i.e. to cater medical expenses incurred by the

insured.

Hence the forum felt that the RI has misinterpreted the policy exclusion and rejected the claim on assumptions

and presumptions.

In view of the above discussions, the forum finds that the repudiation of claim by the Respondent Insurer is

not in order and directs the RI to settle the claim in accordance with the terms and conditions of the policy.

Accordingly the complainant is ALLOWED.

A W A R D

Taking into account the facts & circumstances of the case and the submissions made by both the parties during

the course of the OnLine Hearing and the information/documents placed on record, the Respondent Insurer is

directed to settle the claim under the existing policy terms and conditions.The complaint is ALLOWED.

22) The attention of the Insurer is hereby invited to the following provisions of Insurance Ombudsman Rules,

2017:

d) According to Rule 17(6), the insurer shall comply with the award within 30 days of the receipt of the award and intimate compliance to the same to the Ombudsman.

e) According to Rule 17(7), the complainant shall be entitled to such interest at a rate per annum as specified in the regulations, framed under the Insurance Regulatory & Development Authority of India Act from the date the claim ought to have been settled under the Regulations till the date of payment of the amount awarded by the Ombudsman.

f) According to Rule 17 (8), the award of Insurance Ombudsman shall be binding on the Insurers.

Dated at Hyderabad on the 26th day of AUGUST , 2021.

( SURESH CHANDRA PANDA )

OMBUDSMAN

FOR THE STATES OF A.P.,

TELANGANA AND YANAM CITY

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, STATE OF KARNATAKA (UNDER RULE NO: 17 OF THE INSURANCE OMBUDSMAN RULES, 2017)

OMBUDSMAN – POONAM BODRA In the matter of MR. ABHISHEK BHEEM RAO Vs THE NEW INDIA ASSURANCE CO. LTD.

Complaint No: BNG-H-049-2021-0814

Award No.: IO/(BNG)/A/HI/0041/2021-22

1 Name & Address of the Complainant Mr. Abhishek Bheem Rao #3/1, 1st Cross, New Guddadahalli, Mysore Road, Near Osteen Kids School, Belgaum, Karnataka - 560026 Mobile no: 9972733997 Email ID: [email protected]

2 Policy Number Type of Policy Duration of Policy/ Policy Period

12020034190400000028 Group Mediclaim 31.03.2020 to 30.03.2021

3 Name of the Policyholder/Proposer Name of the Insured

Conversant SDCMS Mr. Abhishek Bheem Rao

4 Name of the Insurer The New India Assurance Company Limited

5 Date of repudiation NA

6 Reason for repudiation NA

7 Date of receipt of the Annexure VI A 29.03.2021

8 Nature of complaint Short Settlement of health claim (COVID-19)

9 Amount of claim Rs,1,71,282/-

10 Date of Partial Settlement 18.09.2020

11 Amounts of relief sought Rs.84,779/-

12 Complaint registered under Rule no. 13 (1) (b) of Insurance Ombudsman Rules, 2017

13 Date of hearing through Online VC 23.07.2021

14 Representation at the hearing

a) For the Complainant Self

b) For the Respondent Insurer Mrs. Rajalakshmi K (Asst. Manager)

15 Complaint how disposed Allowed

16 Date of Award/Order 03.08.2021

17. Brief Facts of the Case: The complaint emanated from short settlement of health claims by Respondent insurer (hereafter referred to as RI). The Complainant represented to Grievance Redressal Officer (GRO) of RI for reconsideration of his claim. However his plea was not considered favourably. Hence the Complainant approached this Forum for resolution of his grievance.

18. Cause of Complaint: a) Complainant’s arguments: The Complainant (Insured Person – IP) submitted that he was covered under group mediclaim policy with RI vide policy no. 12020034190400000028 for the period 31.03.2020 to 30.03.2021. The IP was diagnosed with COVID-19 and admitted at P. M. Santhosha Hospital wherein he had undergone conservative treatment for the same. The reimbursement claim for the medical expenses incurred towards hospitalisations was settled by the RI for Rs.84,779/- against the claimed amount of Rs.1,71,282/-. The IP represented with GRO of RI for settlement the balance amount. Aggrieved of no favourable outcome from the RI, IP approached this forum for the resolution of his grievance.

b) Respondent Insurer’s Arguments: The RI in their Self Contained Note (SCN) dated 13.07.2021 whilst admitting insurance coverage and settlement of claim, submitted that the reimbursement claim was settled as per GIC council rates for Covid treatment as per GIC council circular dated 20.06.2020. The total claim including pre and post hospitalisation was settled as:

For 7 days room rent at 7200 *7 = Rs.50,400/- Medicines = Rs. 6,328/- Consultation charges 1250*7 = Rs. 8,750/- Lab test = Rs. 6,000/- Total comes as ...........................…. Rs.71,478/-

However they settled the claim for Rs.86,503/- which is in excess of the total amount.

In view of their submissions, the RI prayed for passing an appropriate order.

19. Reason for Registration of complaint: The complaint falls within the scope of the Insurance Ombudsman Rules, 2017.

20. The following documents were placed for perusal: Complaint along with enclosures, Respondent Insurer’s SCN along with enclosures and Consent of the Complainant in Annexure VIA & and Respondent Insurer in VII A

21. Result of personal hearing with both the parties (Observations & Conclusions): The dispute is whether settlement of health claims under the policy is in order or not.

Personal hearing by the way of online Video-conferencing through GoTo Meet was conducted in the said case. Complainant and Representatives of RI joined using online VC and presented their case. Confirmation from all the participants about the clarity of audio and video was taken to which the participants responded positively. Both the parties reiterated her earlier submissions.

Forum has perused the documentary evidence available on record and the submissions made by both the parties during the personal hearing.

Forum notes that IP was diagnosed with COVID-19 and he was hospitalised at P. M. Santhosha Hospital, Bangalore from 25.07.2020 to 01.08.2020. The IP filed a reimbursement claim of Rs.1,71,282/- for the medical expenses incurred by him. The claim was settled by RI for Rs.86,503/- considering tariff rate of GIC guidelines for the settlement of the Covid claim.

Forum notes that as per IRDAI circular reference no IRDAI/HLT/REG/CIR/011/01/2021 dt 13.01.2021 regarding Communication on settlement of health insurance claims against General Insurance Council’s instructions dated 20th June 2020 on “Reference Rates for COVID-19”, Insurance Companies were directed to ensure that the “Reimbursement claims” under a health insurance policy shall be settled as per the terms and conditions of the respective policy contract. Hence, the insurers shall honor all the health insurance claims as per the terms and conditions of the policy contract.

The same was reiterated in IRDAI circular reference no IRDAI/HLT/MISC/CIR/102/04/2021 dt 23.04.2021. Hence the contention of RI that the claim settlement as per of GIC is untenable. Accordingly during the course of personal hearing the RI was asked to submit the eligible claim amount as per the policy terms and conditions and the RI vide their email dated 30.07.2021 submitted the payable amount as follows:

Charge Type Bill Amount

Payable Amount

Non Pay Amount

Non Payable Reason

Hospital Charges 112000 112000 0

Investigation & Lab Charges 6650 6650 0

Miscellaneous Charges 850 300 550 Registration, Administration

Consultant Charges 16120 6642 9478 9478/-Discount

Pharmacy & Medicine Charges 10139 10139 0

Procedure charges 35000 25200 9800 PPE kit paid at 3600 per day

Total 180759 160931 19828

Forum observes that the RI has already settled an amount of Rs.86,503/- vide claim settlement letter dated 18.09.2020, the balance amount of 74,428/- (i.e. 160931-86503) is to be paid to the IP. The complaint is allowed.

A W A R D

Taking account of the facts and circumstances of the case and the submissions made by both the parties and documents submitted during the course of the Personal Hearing, the Respondent Insurer is directed to settle the claim for balance amount of Rs.74,428/- without interest.

The Complaint is Allowed.

Dated at Bangalore on the 3rd day of August, 2021.

(POONAM BODRA) INSURANCE OMBUDSMAN

ADDITIONAL CHARGE FOR THE STATE OF KARNATAKA

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, STATE OF KARNATAKA (UNDER RULE NO: 17 OF THE INSURANCE OMBUDSMAN RULES, 2017)

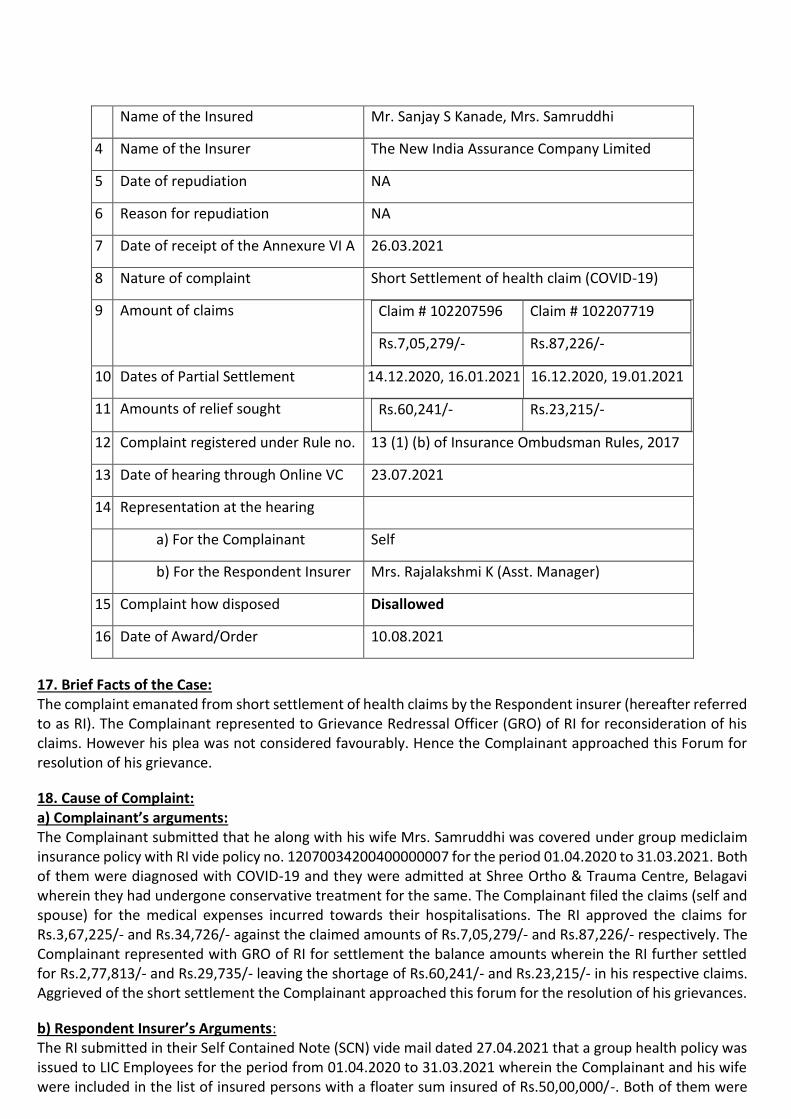

OMBUDSMAN – POONAM BODRA In the matter of MR. SANJAY S KANADE Vs THE NEW INDIA ASSURANCE CO. LTD.

Complaint No: BNG-H-049-2021-0798

Award No.: IO/(BNG)/A/HI/0050/2021-22

1 Name & Address of the Complainant Mr. Sanjay S Kanade

H # 3406, Samadev Galli

Belgaum, Karnataka - 590001

Mobile no: 9480432360

Email ID: [email protected]

2 Policy Number

Type of Policy

Duration of Policy/ Policy Period

12070034200400000007

Group Mediclaim

01.04.2020 to 31.03.2021

3 Name of the Policyholder/Proposer LIC of India

Name of the Insured Mr. Sanjay S Kanade, Mrs. Samruddhi

4 Name of the Insurer The New India Assurance Company Limited

5 Date of repudiation NA

6 Reason for repudiation NA

7 Date of receipt of the Annexure VI A 26.03.2021

8 Nature of complaint Short Settlement of health claim (COVID-19)

9 Amount of claims Claim # 102207596 Claim # 102207719

Rs.7,05,279/- Rs.87,226/-

10 Dates of Partial Settlement 14.12.2020, 16.01.2021 16.12.2020, 19.01.2021

11 Amounts of relief sought Rs.60,241/- Rs.23,215/-

12 Complaint registered under Rule no. 13 (1) (b) of Insurance Ombudsman Rules, 2017

13 Date of hearing through Online VC 23.07.2021

14 Representation at the hearing

a) For the Complainant Self

b) For the Respondent Insurer Mrs. Rajalakshmi K (Asst. Manager)

15 Complaint how disposed Disallowed

16 Date of Award/Order 10.08.2021

17. Brief Facts of the Case: The complaint emanated from short settlement of health claims by the Respondent insurer (hereafter referred to as RI). The Complainant represented to Grievance Redressal Officer (GRO) of RI for reconsideration of his claims. However his plea was not considered favourably. Hence the Complainant approached this Forum for resolution of his grievance.

18. Cause of Complaint: a) Complainant’s arguments: The Complainant submitted that he along with his wife Mrs. Samruddhi was covered under group mediclaim insurance policy with RI vide policy no. 12070034200400000007 for the period 01.04.2020 to 31.03.2021. Both of them were diagnosed with COVID-19 and they were admitted at Shree Ortho & Trauma Centre, Belagavi wherein they had undergone conservative treatment for the same. The Complainant filed the claims (self and spouse) for the medical expenses incurred towards their hospitalisations. The RI approved the claims for Rs.3,67,225/- and Rs.34,726/- against the claimed amounts of Rs.7,05,279/- and Rs.87,226/- respectively. The Complainant represented with GRO of RI for settlement the balance amounts wherein the RI further settled for Rs.2,77,813/- and Rs.29,735/- leaving the shortage of Rs.60,241/- and Rs.23,215/- in his respective claims. Aggrieved of the short settlement the Complainant approached this forum for the resolution of his grievances.

b) Respondent Insurer’s Arguments: The RI submitted in their Self Contained Note (SCN) vide mail dated 27.04.2021 that a group health policy was issued to LIC Employees for the period from 01.04.2020 to 31.03.2021 wherein the Complainant and his wife were included in the list of insured persons with a floater sum insured of Rs.50,00,000/-. Both of them were

hospitalised for COVID-19, at Shree Ortho & Trauma Centre, Belagavi and they were admitted in general category and not in ICU. Thus the eligible limit for the room rent per day is Rs.4,000/- but as a Covid case the claim was settled as per Rs.7,500/- room rent per day and the proportionate deductions were applied. As the claimant is already paid extra amount over and above amount payable as per terms of the policy, no further amount is payable in the claims.

In view of their submissions, the RI prayed for passing an appropriate order.

19. Reason for Registration of complaint: The complaint falls within the scope of the Insurance Ombudsman Rules, 2017.

20. The following documents were placed for perusal: a) Complaint along with enclosures, b) Respondent Insurer’s SCN along with enclosures

and c) Consent of the Complainant in Annexure VIA &

and Respondent Insurer in VII A

21. Result of personal hearing with both the parties (Observations & Conclusions): Personal hearing by the way of online Video-conferencing through GoTo Meet was conducted in the said case. The Complainant and Representative of RI joined using online VC and presented their case. Confirmation from all the participants about the clarity of audio and video was taken to which the participants responded positively. Both the parties reiterated their earlier submissions. The Complainant strongly argued that the claims should be settled as per terms and conditions of the policy. The RI strongly contended that considering the GIC circular they have paid more than the eligible amount as per policy terms and conditions.

The Forum directed the RI to furnish the calculation as per policy terms and conditions which they submitted after the hearing vide their email dated 05.08.2021.

Forum notes that the complainant filed a single complaint mentioning two claim numbers towards self and spouse. Both the claims were considered under single complaint. The Forum has perused the documentary evidence available on records and the submissions made by both the parties during the personal hearing pertaining to both the Claim Nos.

The dispute is whether partial settlement of health claims under the policy is in order or not.

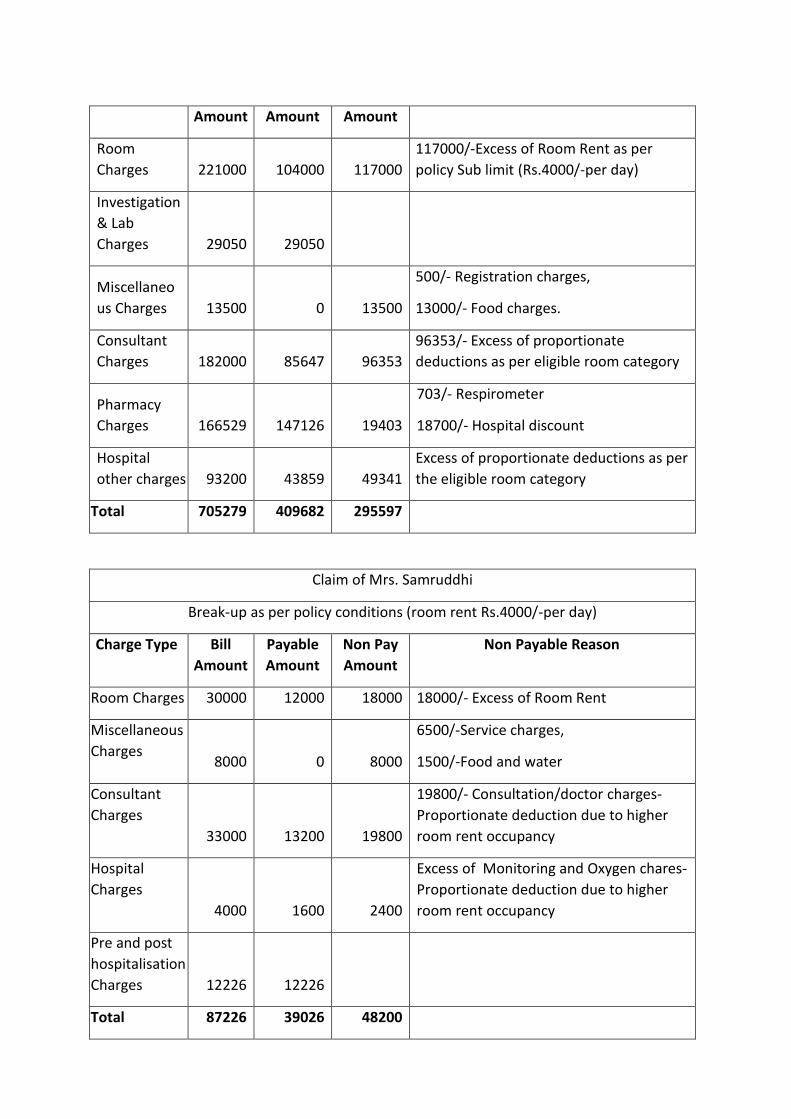

Forum notes that Mr. Sanjay S Kanade and his wife Mrs. Samruddhi were diagnosed with COVID-19 and they were hospitalised at Shree Ortho & Trauma Centre, Belagavi on 20.09.2021. Mr. Sanjay S Kanade was discharged on 15.10.2020 whereas Mrs. Samruddhi was discharged on 23.09.2020. The Complainant filed reimbursement claims for self and spouse of Rs.7,05,279/- and Rs.87,226/- respectively. The RI has initially processed the claims as per GIC circular dt.20.06.2020 considering the room rent tariff of Rs.7,500/- per day and settled Rs.3,67,225/- vide claim no. 1017932176 and Rs.29,375/- vide claim no. 102207719 respectively for both the claims. After the representation from the complainant they reprocessed the claim and paid an additional amount of Rs.2,77,813/- and Rs.34,726/- under new claim nos. 102207596 and 101885268 respectively. Hence the total amount paid under both the claims works out to Rs.6,45,038/- and Rs.64,101/- considering room rent tariff of Rs.7500/- per day.

The Forum finds that as per the policy terms and conditions the complainant is eligible for room rent tariff of Rs.4000/-per day. Accordingly the claims work out as under:

Claim of Mr. Sanjay S Kanade

Break-up as per policy conditions (room rent Rs.4000/-per day)

Charge Type Bill Payable Non Pay Non Payable Reason

Amount Amount Amount

Room

Charges 221000 104000 117000

117000/-Excess of Room Rent as per

policy Sub limit (Rs.4000/-per day)

Investigation

& Lab

Charges 29050 29050

Miscellaneo

us Charges 13500 0 13500

500/- Registration charges,

13000/- Food charges.

Consultant

Charges 182000 85647 96353

96353/- Excess of proportionate

deductions as per eligible room category

Pharmacy

Charges 166529 147126 19403

703/- Respirometer

18700/- Hospital discount

Hospital

other charges 93200 43859 49341

Excess of proportionate deductions as per

the eligible room category

Total 705279 409682 295597

Claim of Mrs. Samruddhi

Break-up as per policy conditions (room rent Rs.4000/-per day)

Charge Type Bill

Amount

Payable

Amount

Non Pay

Amount

Non Payable Reason

Room Charges 30000 12000 18000 18000/- Excess of Room Rent

Miscellaneous

Charges 8000 0 8000

6500/-Service charges,

1500/-Food and water

Consultant

Charges

33000 13200 19800

19800/- Consultation/doctor charges-

Proportionate deduction due to higher

room rent occupancy

Hospital

Charges

4000 1600 2400

Excess of Monitoring and Oxygen chares-

Proportionate deduction due to higher

room rent occupancy

Pre and post

hospitalisation

Charges 12226 12226

Total 87226 39026 48200

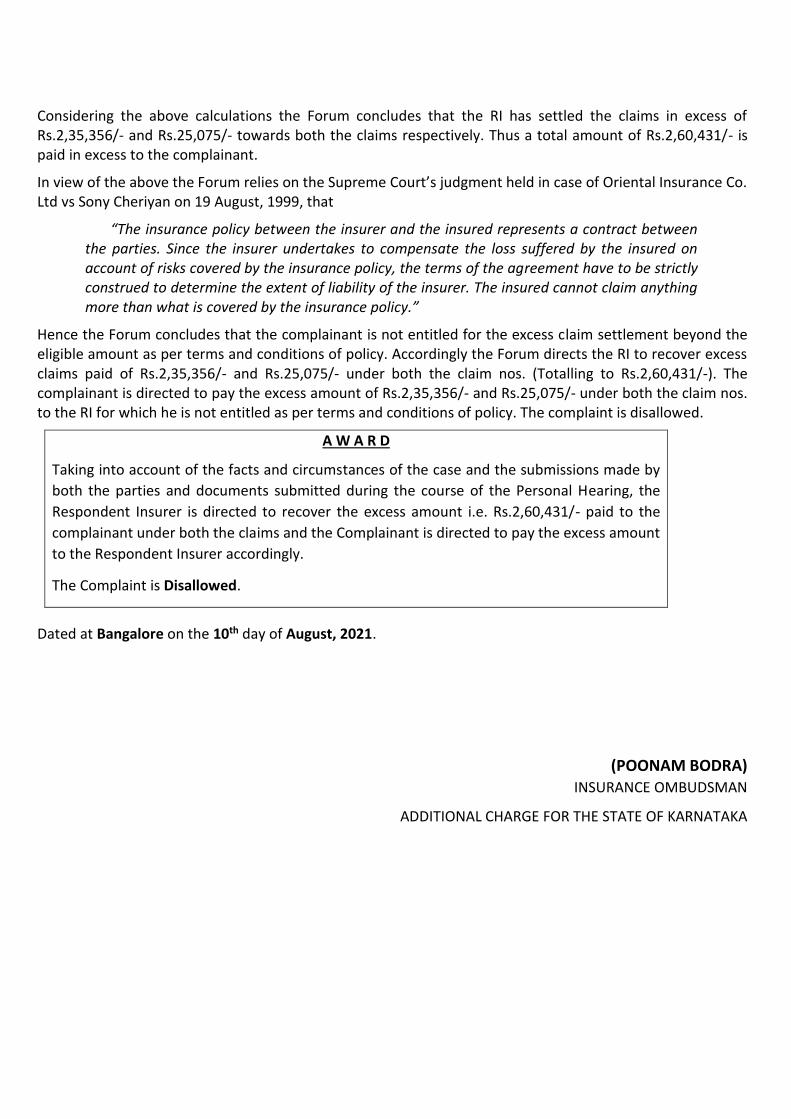

Considering the above calculations the Forum concludes that the RI has settled the claims in excess of Rs.2,35,356/- and Rs.25,075/- towards both the claims respectively. Thus a total amount of Rs.2,60,431/- is paid in excess to the complainant.

In view of the above the Forum relies on the Supreme Court’s judgment held in case of Oriental Insurance Co. Ltd vs Sony Cheriyan on 19 August, 1999, that

“The insurance policy between the insurer and the insured represents a contract between the parties. Since the insurer undertakes to compensate the loss suffered by the insured on account of risks covered by the insurance policy, the terms of the agreement have to be strictly construed to determine the extent of liability of the insurer. The insured cannot claim anything more than what is covered by the insurance policy.”

Hence the Forum concludes that the complainant is not entitled for the excess claim settlement beyond the eligible amount as per terms and conditions of policy. Accordingly the Forum directs the RI to recover excess claims paid of Rs.2,35,356/- and Rs.25,075/- under both the claim nos. (Totalling to Rs.2,60,431/-). The complainant is directed to pay the excess amount of Rs.2,35,356/- and Rs.25,075/- under both the claim nos. to the RI for which he is not entitled as per terms and conditions of policy. The complaint is disallowed.

A W A R D

Taking into account of the facts and circumstances of the case and the submissions made by

both the parties and documents submitted during the course of the Personal Hearing, the

Respondent Insurer is directed to recover the excess amount i.e. Rs.2,60,431/- paid to the

complainant under both the claims and the Complainant is directed to pay the excess amount

to the Respondent Insurer accordingly.

The Complaint is Disallowed.

Dated at Bangalore on the 10th day of August, 2021.

(POONAM BODRA) INSURANCE OMBUDSMAN

ADDITIONAL CHARGE FOR THE STATE OF KARNATAKA

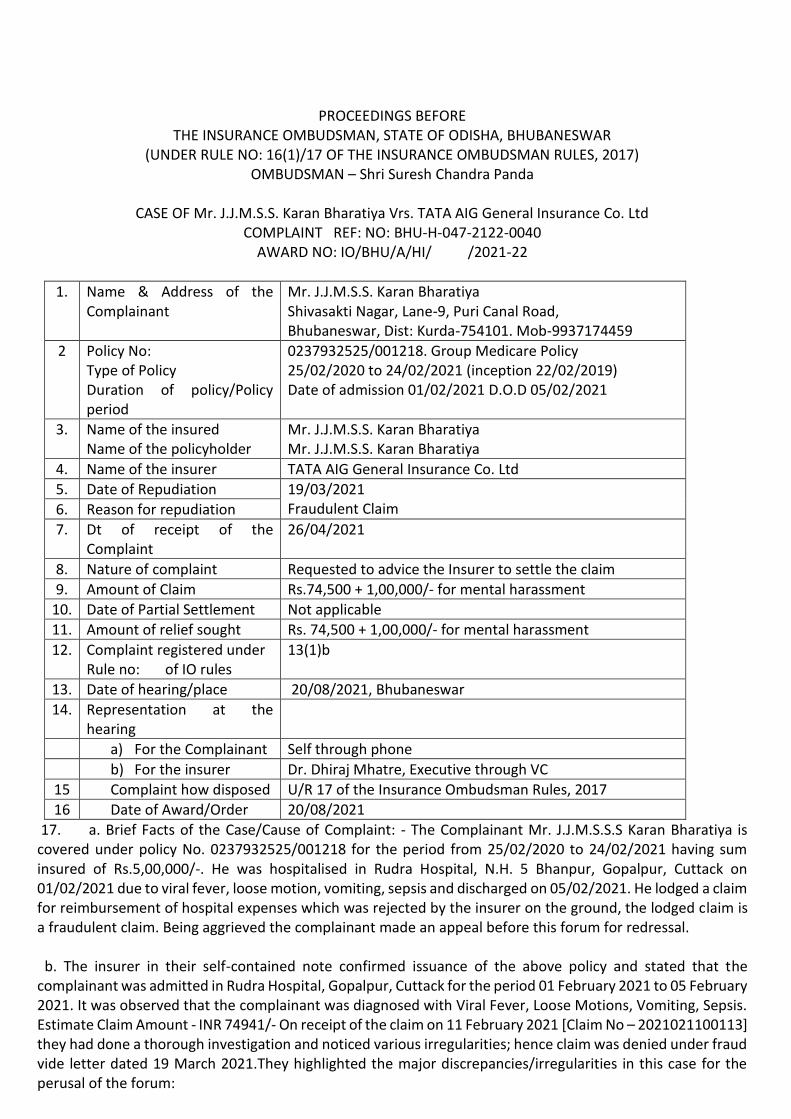

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, STATE OF ODISHA, BHUBANESWAR

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULES, 2017) OMBUDSMAN – Shri Suresh Chandra Panda

CASE OF Mr. J.J.M.S.S. Karan Bharatiya Vrs. TATA AIG General Insurance Co. Ltd

COMPLAINT REF: NO: BHU-H-047-2122-0040 AWARD NO: IO/BHU/A/HI/ /2021-22

1. Name & Address of the Complainant

Mr. J.J.M.S.S. Karan Bharatiya Shivasakti Nagar, Lane-9, Puri Canal Road, Bhubaneswar, Dist: Kurda-754101. Mob-9937174459

2 Policy No: Type of Policy Duration of policy/Policy period

0237932525/001218. Group Medicare Policy 25/02/2020 to 24/02/2021 (inception 22/02/2019) Date of admission 01/02/2021 D.O.D 05/02/2021

3. Name of the insured Name of the policyholder

Mr. J.J.M.S.S. Karan Bharatiya Mr. J.J.M.S.S. Karan Bharatiya

4. Name of the insurer TATA AIG General Insurance Co. Ltd

5. Date of Repudiation 19/03/2021 Fraudulent Claim 6. Reason for repudiation

7. Dt of receipt of the Complaint

26/04/2021

8. Nature of complaint Requested to advice the Insurer to settle the claim

9. Amount of Claim Rs.74,500 + 1,00,000/- for mental harassment

10. Date of Partial Settlement Not applicable

11. Amount of relief sought Rs. 74,500 + 1,00,000/- for mental harassment

12. Complaint registered under Rule no: of IO rules

13(1)b

13. Date of hearing/place 20/08/2021, Bhubaneswar

14. Representation at the hearing

a) For the Complainant Self through phone

b) For the insurer Dr. Dhiraj Mhatre, Executive through VC

15 Complaint how disposed U/R 17 of the Insurance Ombudsman Rules, 2017

16 Date of Award/Order 20/08/2021

17. a. Brief Facts of the Case/Cause of Complaint: - The Complainant Mr. J.J.M.S.S.S Karan Bharatiya is covered under policy No. 0237932525/001218 for the period from 25/02/2020 to 24/02/2021 having sum insured of Rs.5,00,000/-. He was hospitalised in Rudra Hospital, N.H. 5 Bhanpur, Gopalpur, Cuttack on 01/02/2021 due to viral fever, loose motion, vomiting, sepsis and discharged on 05/02/2021. He lodged a claim for reimbursement of hospital expenses which was rejected by the insurer on the ground, the lodged claim is a fraudulent claim. Being aggrieved the complainant made an appeal before this forum for redressal. b. The insurer in their self-contained note confirmed issuance of the above policy and stated that the complainant was admitted in Rudra Hospital, Gopalpur, Cuttack for the period 01 February 2021 to 05 February 2021. It was observed that the complainant was diagnosed with Viral Fever, Loose Motions, Vomiting, Sepsis. Estimate Claim Amount - INR 74941/- On receipt of the claim on 11 February 2021 [Claim No – 2021021100113] they had done a thorough investigation and noticed various irregularities; hence claim was denied under fraud vide letter dated 19 March 2021.They highlighted the major discrepancies/irregularities in this case for the perusal of the forum:

Below mentioned spelling errors found;

Source Error Actual Real Spelling

Discharge Card, Claim form Sepesies Sepsis

Discharge Card Disorented Disoriented

Discharge Card Louse motions Loose motions

Hospital Bill Himoglobin Hemoglobin

Dishcarge Card Controlly Controlling

It is highly unlikely that a qualified Doctor would do such spelling errors. In final diagnosis “loose motions & vomiting” is mentioned. Generally, these terms are never used in final Diagnosis in Discharge card. All physicians use “Gastroenteritis/Dysentery” in final diagnosis. For Sepsis & Kidney Failure patient, following investigations are not done; Blood/Urine Culture & Sensitivity C Reactive Protein [CRP] Chest X Ray ECG Stool Routine Abdomen Sonography Signature of Consultant Pathologist & Lab Technician is missing from diagnostic reports. Hemoglobin values of 12.4 is same on 01, 02, 03 February 2021. It is highly unlikely that Hemoglobin value would remain same for consecutive 3 days in Sepsis patient. Generally Hemoglobin value changes due to multiple factor like infection/Sepsis, Hydration, Food Intake etc. Patient was drowsy on 01, 02, 03 February 2021. Below mentioned things are missing; a. CNS [Central Nervous System] Examination in detail like Tone, Power, Reflexes. b. CT/MRI Brain c. EEG d. Reference to Consultant Neurologist A cursory look at the Indoor Case papers show that they were written by one person at a stretch. When a person is admitted for 5 days it is unlikely that the treating doctor/nurse was on duty 24 hours a day during the course of admission. Generally in Indoor Case papers, before writing daily notes all Physicians write,”S/B Dr.XYZ”. but such comments are missing. Also, generally Physicians write their time of visit to patient, however time of visit is also missing from Indoor Case papers. In hospital indoor case papers [especially in admission notes] other systemic examination like R.S. [Respiratory system] C.V.S. [Cardio Vascular System] C.N.S [Central Nervous System] etc is missing. Since Kidney Failure patient was admitted for 5 days, it was expected that treating Doctor would do thorough systemic examination. Lab report values not noted in indoor case papers. After viewing Lab reports, generally Physicians note those values in their notes in indoor case papers so that Doctor who sees patient thereafter observes that earlier Doctor has taken cognizance of those lab tests results. On admission, Serum potassium levels were lower than normal – 3.0 [Normal Range – 3.5 to 5.5 mmol/L, still Potassium supplement like injectable/syrup format was not given nor “Electrolyte Imbalance” mentioned in final Diagnosis in Discharge card. Even Serum Sodium level was lower than normal – 128.4 [Normal Range – 135 to 155 mmol/L.

On admission, Serum Creatinine levels were higher than normal – 2.0 [Normal Range – 0.5 to 1.5 mg/dl, still “Acute Renal Failure” was not mentioned in final Diagnosis in Discharge card. Insured was not catheterized. Catheterization orders not found in indoor case papers nor purchase of Catheter, Urobag, Urometer is seen in chemist bills. Thus, he was passing urine by himself. As per Input/ Output chart, patient was seen passing 600, 700, 800, 1000 ml urine at one time. The typical human bladder will hold between 300 - 500 ml before the urge to empty occurs, but can hold considerably more. Hence passage of urine > 600 ml at one time is not understood. Patient was admitted for total 5 days. In 5 days, stools passed or not is never mentioned in indoor case papers. Surprisingly Prepost hospitalization claim documents not submitted. Generally patient with so many complications visits Doctor after discharge for follow-up. In admission case paper, as a routine, treating Physician has mentioned battery of tests to be done after admission. In those tests, TLC [Total Leucocyte Count] was also advised to assess level of infection [White Blood Cells] in the body. Surprisingly on the same paper, Injection Meropenum 1 gram was also written. Total 13 Injections Merofit purchase shown for INR 31,200/- Generally Meropenum is given to seriously ill complicated ICU patient battling life threatening infections. In this case insured was in private room. In claim form, in question No – 4 towards “Are you presently covered with any other Mediclaim/Health Insurance Policy”, insured has mentioned “No”, whereas he is holding Star Health Policy also. In question No -8 in investigator’s questionnaire also insured has replied in negative. In question No – 10 of investigator’s questionnaire, insured has written that complaints started since 31 January 2021 ie just 1 day before admission. However as per admission case paper & in question No - 3 in investigator’s questionnaire [treating Doctor section], complaints started for 3 days. Food orders are missing in indoor case papers, like NBM [Nill by Mouth], Liquid diet, soft diet etc. In a Hospitalisation case there are dietary restrictions placed on the patient. However, food orders like NBM [Nil by Mouth], Liquid diet, soft diet etc are missing in Indoor case papers. On admission Lipid profile was done in this non cardiac patient, which showed normal Values. Hospital billed INR 500/- towards same in bill No – B4578 dated 01 February 2021. Still again Hospital has charged INR 500/- on 02 February 2021 in bill No – B4580. On admission RBS [Random Blood Sugar] was done in this non-Diabetic patient, which showed normal Value [129mg/dl]. Hospital billed INR 50/- towards same in bill No –B4578 dated 01 February 2021. Still again Hospital has charged INR 50/- on 02 February 2021 in bill No – B4580. Again, Hospital has charged INR 50/- on 03 February 2021 in bill No – B4597. Below abuse noted in chemist bills;

1-Feb 2-Feb 3-Feb 4-Feb 5-Feb Total

NS 500 ml

3 3 2 2 2 12

RL 1 1 2 3 7

DNS 2 2

21 IV bottles for 5 days admission seems to be abuse. In chemist bills, total 15 Injection Infupar [Paracetamol] purchase seen for INR 7485/- still from 01 February 2021 to 04 February 2021 continuous fever [>100-degree Fahrenheit] noted. Generally, after giving one single Paracetamol injection, temperature comes to normal for at least 4-5 hours. Another Paracetamol injection by brand name Febrinil / Aeknil also comes for 10-20 Rupees per injection & it also reduces fever like injection Infupar does. Inspite of daily fever till 04 February 2021, how discharge was given 05 February 2021 is not understood. Generally, Physician makes sure that patient doesn’t

have fever for last 48 hours, then only he advises discharge & ask patient to come with certain lab tests after few days during follow up visit.

1-Feb 2-Feb 3-Feb 4-Feb 5-Feb Total

Inj. Infupal Quantity

3 3 3 3 3 15

Cost 1497 1497 1497 1497 1497 7485

In chemist bills,total 5 Injection Xetox 600 mg [Glutathione] purchase seen for INR 6495/-. In this patient as per lab reports, his Liver function was within normal limits. Hence indication of administration of Injection Xetox is not understood. Medical Literature of Injection Xetox is annexed with SCN

1-Feb 2-Feb 3-Feb 4-Feb 5-Feb Total

Inj. Xetox 600 mg Quantity 1 1 1 1 1 5

1299 1299 1299 1299 1299 6495

Room No, Bed No, Dr’s name, Patient’s name is missing from Vital Chart & Input/Output Chart. Generally, on each chart, hospitals write these basic details to avoid mixing of case sheets with another patient in order to prevent further calamity. Relative/friend’s signature is missing from admission consent form. In admission form, generally any hospital takes relative’s name/contact Number/Signature. It is quite surprising that not a single relative accompanied to hospital with disoriented patient with low urine output. Insured was admitted during Covid pandemic & was having classical Covid symptoms like fever, vomiting, loose motions, still surprisingly Covid Swab test was not done. On 02 February 2021, Temparature-104-degree Fahrenheit & patient was in Sepsis. Surprisingly, Pulse rate-84/min [Normal Range: 60 to 100/Minute]. Generally, Fever causes Tachycardia [increase Heart Rate] & Sepsis causes reflex Tachycardia. With this kind of High-grade fever & Sepsis, Pulse rate should have been > 100/minute. As per Discharge Card & Admission Form, time of Admission is 07.22 PM, but as per Medication chart, drugs have been administered since 11 am in the morning. As per Vital chart, Pulse/BP recorded from 11 am in the morning. As per Input/Output chart, 200 ml urine was passed on 11 am in the morning. Even in question No – 14 of investigator’s questionnaire, insured has written TOA-11.30 am. Also, there was discrepancy regarding Discharge date & time as below;

Source Date of Discharge Time of Discharge

Discharge Card 5-Feb-21 12.54 P.M. 9Afternoon)

Insured Declaration 5-Feb-21 4.30 P.M. (Evening)

Hospital Bill 6-Feb-21 09.08 AM (Morning)

Also there was discrepancy in Payment Receipts as below ; Payment Receipt No MR2021-194 dated 05/02/2021 at 12:55 PM Payment Receipt No MR2021-194 dated 06/02/2021 at 09:05 PM Same receipt Number / Same amount but Issue date/Time is Different. On 01 February 2021, three times Blood Pressure measured during entire day [11 am, 2 pm, 6 pm, 10 pm]. Surprisingly every time same Blood Pressure recorded – 110/70 mm of Hg..On 03 February 2021, four times temperature taken during entire day [6 am, 2 pm, 6 pm, 10 pm]. Surprisingly every time same temperature recorded – 102 Degree Fahrenheit.

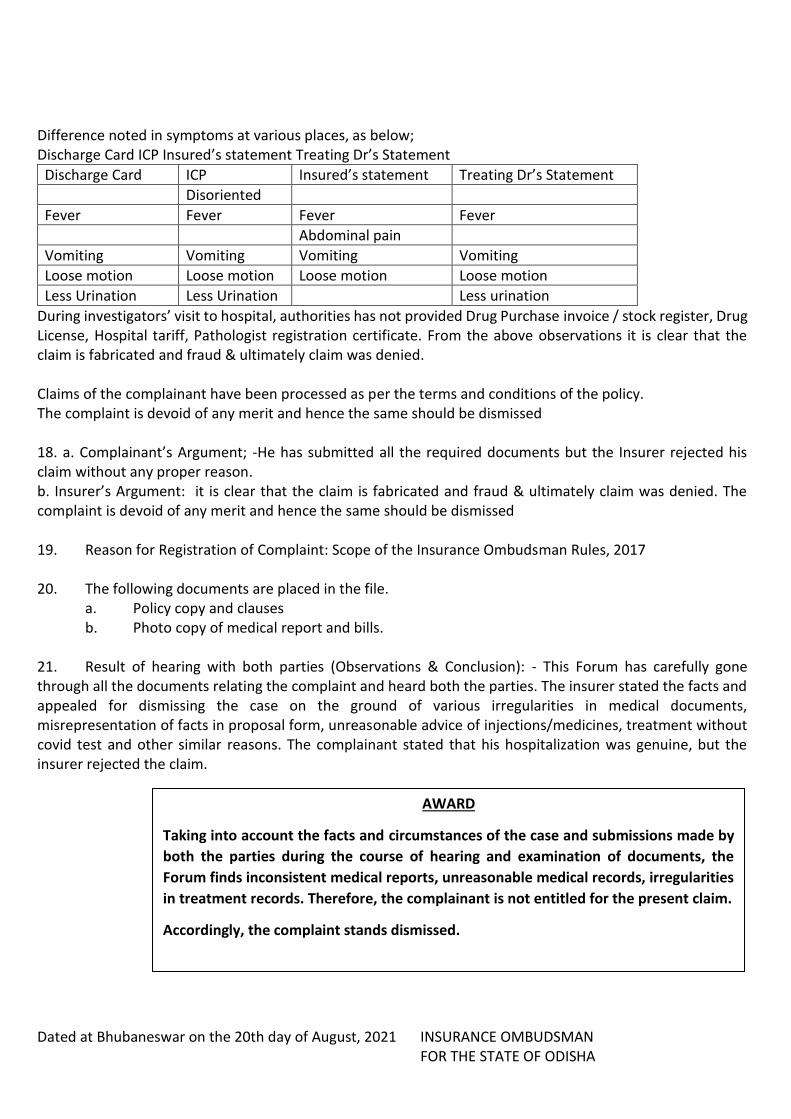

Difference noted in symptoms at various places, as below; Discharge Card ICP Insured’s statement Treating Dr’s Statement

Discharge Card ICP Insured’s statement Treating Dr’s Statement

Disoriented

Fever Fever Fever Fever

Abdominal pain

Vomiting Vomiting Vomiting Vomiting

Loose motion Loose motion Loose motion Loose motion

Less Urination Less Urination Less urination

During investigators’ visit to hospital, authorities has not provided Drug Purchase invoice / stock register, Drug License, Hospital tariff, Pathologist registration certificate. From the above observations it is clear that the claim is fabricated and fraud & ultimately claim was denied. Claims of the complainant have been processed as per the terms and conditions of the policy. The complaint is devoid of any merit and hence the same should be dismissed 18. a. Complainant’s Argument; -He has submitted all the required documents but the Insurer rejected his claim without any proper reason. b. Insurer’s Argument: it is clear that the claim is fabricated and fraud & ultimately claim was denied. The complaint is devoid of any merit and hence the same should be dismissed 19. Reason for Registration of Complaint: Scope of the Insurance Ombudsman Rules, 2017 20. The following documents are placed in the file.

a. Policy copy and clauses b. Photo copy of medical report and bills.

21. Result of hearing with both parties (Observations & Conclusion): - This Forum has carefully gone through all the documents relating the complaint and heard both the parties. The insurer stated the facts and appealed for dismissing the case on the ground of various irregularities in medical documents, misrepresentation of facts in proposal form, unreasonable advice of injections/medicines, treatment without covid test and other similar reasons. The complainant stated that his hospitalization was genuine, but the insurer rejected the claim. Dated at Bhubaneswar on the 20th day of August, 2021 INSURANCE OMBUDSMAN

FOR THE STATE OF ODISHA

AWARD

Taking into account the facts and circumstances of the case and submissions made by

both the parties during the course of hearing and examination of documents, the

Forum finds inconsistent medical reports, unreasonable medical records, irregularities

in treatment records. Therefore, the complainant is not entitled for the present claim.

Accordingly, the complaint stands dismissed.

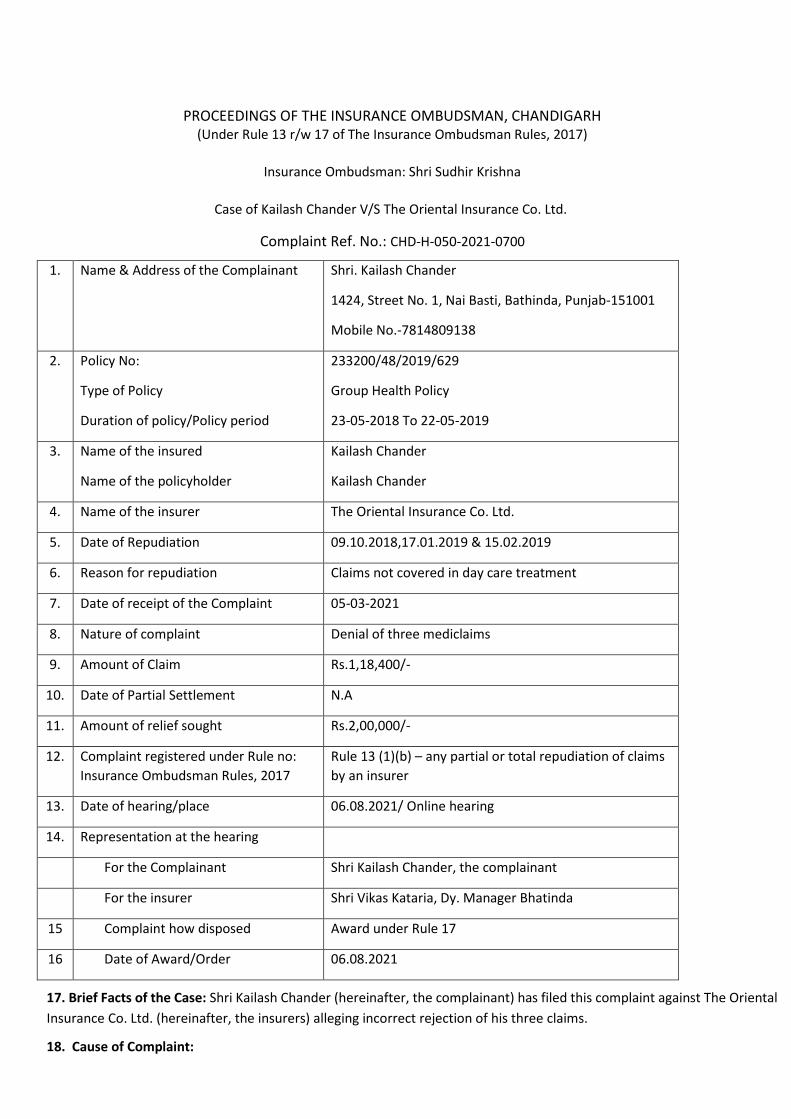

PROCEEDINGS OF THE INSURANCE OMBUDSMAN, CHANDIGARH (Under Rule 13 r/w 17 of The Insurance Ombudsman Rules, 2017)

Insurance Ombudsman: Shri Sudhir Krishna

Case of Kailash Chander V/S The Oriental Insurance Co. Ltd.

Complaint Ref. No.: CHD-H-050-2021-0700

1. Name & Address of the Complainant Shri. Kailash Chander

1424, Street No. 1, Nai Basti, Bathinda, Punjab-151001

Mobile No.-7814809138

2. Policy No:

Type of Policy

Duration of policy/Policy period

233200/48/2019/629

Group Health Policy

23-05-2018 To 22-05-2019

3. Name of the insured

Name of the policyholder

Kailash Chander

Kailash Chander

4. Name of the insurer The Oriental Insurance Co. Ltd.

5. Date of Repudiation 09.10.2018,17.01.2019 & 15.02.2019

6. Reason for repudiation Claims not covered in day care treatment

7. Date of receipt of the Complaint 05-03-2021

8. Nature of complaint Denial of three mediclaims

9. Amount of Claim Rs.1,18,400/-

10. Date of Partial Settlement N.A

11. Amount of relief sought Rs.2,00,000/-

12. Complaint registered under Rule no:

Insurance Ombudsman Rules, 2017

Rule 13 (1)(b) – any partial or total repudiation of claims

by an insurer

13. Date of hearing/place 06.08.2021/ Online hearing

14. Representation at the hearing

For the Complainant Shri Kailash Chander, the complainant

For the insurer Shri Vikas Kataria, Dy. Manager Bhatinda

15 Complaint how disposed Award under Rule 17

16 Date of Award/Order 06.08.2021

17. Brief Facts of the Case: Shri Kailash Chander (hereinafter, the complainant) has filed this complaint against The Oriental

Insurance Co. Ltd. (hereinafter, the insurers) alleging incorrect rejection of his three claims.

18. Cause of Complaint:

a) Complainant’s argument: His daughter developed disease of RRMS on 20.02.2018 and claim of Rs.44260/- was paid by

the insurer vide their letter No. RTI/230000/2018/108 dated 20.02.2018. But subsequent three claims were denied on the

ground that day care treatment is not covered. He had sent treatment papers for reimbursement on 18.08.2018 for

Rs.11600/- but TPA closed the file as No Claim due to non-consideration of day care treatment. On 29.11.2018 treatment

papers for Rs.80600/-were again sent. The complainant again sent treatment papers on 17.01.2019 for the period

04.08.2018 to 06.01.2019 along with the details of the treatment expenses but insurer denied his claims for Rs.1,18,400/-

only. In support of Day Care Treatment he submitted Delhi Heart Institute certificate dated 17.10.2018 certifying that during

admission the patient is observed for any untoward reaction as antipyretic and antihistamine given. The complainant further

stated that he represented to TPA vide reminder on 15.01.2019 for settlement of claim and to insurer on 23.03.2019 and

25.05.2019 that claims may please be paid but they denied these claims vide letters no nil dated 09.10.2018, 17.01.2019

and 15.02.2019.

b) Insurers’ argument: TPA has rejected three claims of Rs.11600/-, Rs.80,600/- and Rs.37800/- with remarks “Case of RRMS

(Relapsing Remitting Multiple Sclerosis) managed conservatively. There was less than 24 hrs of admission. Neither

Chemotherapy was given and nor the given treatment falls in Day care list. Minimum 24 Hrs. hospitalization is required as

per policy terms and conditions. So the claim is recommended to be non-payable as per clause 3.18 as expenses on

hospitalization are admissible only if hospitalization is for minimum period of 24 hours. Insurers stated that Patient was

admitted as a case of RRMS and treated with injection Intra muscular (INF), which can be given on OPD basis and does not

require hospitalization. This treatment does not require 24 hours hospitalization nor listed under day care list. Hence claims

remain non-payable.

19. Reason for Registration of Complaint: Incorrect denial of claims.

20. The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21. Result of Personal hearing with both parties (Observations & Conclusion):

Case called. Parties are present and recall their arguments as noted in Para 18 above.

As has been amply explained in Para 18b above, the treatment administered to the insured would not come under the

category of hospitalization and is also not covered in the list of Admissible Daycare Procedures vide Appendix-I of the Policy.

Therefore, the Insurers were justified in repudiating the claim. Pursuantly, the complaint shall deserve to be rejected.

Award

The complaint is rejected.

(Sudhir Krishna)

Insurance Ombudsman

August 06, 2021

PROCEEDINGS OF THE INSURANCE OMBUDSMAN, CHANDIGARH

(Under Rule 13 r/w 16 of The Insurance Ombudsman Rules, 2017)

Insurance Ombudsman: Shri Sudhir Krishna

Case of Mahabir Parshad Sharma v/s The United India Insurance Co. Ltd.

Complaint Ref. No.: CHD-H-051-2021-0747

1. Name & Address of the Complainant Shri Mahabir Parshad Sharma

H. No. 191-P, Sector 20, Huda, Sirsa, Haryana- 125055

Mobile No.- 9050248191

2. Policy No:

Type of Policy

Duration of policy/Policy period

5001002819P112263948

Group Mediclaim Policy

01-11-2019 To 31-10-2020

3. Name of the insured

Name of the policyholder

Mahabir P Sharma & Shakuntla Sharma

Indian Bank’s Association A/c PNB

4. Name of the insurer The United India Insurance Co. Ltd.

5. Date of Repudiation 04.12.2020

6. Reason for repudiation Repudiated as per clause 2.19 & 3.3

7. Date of receipt of the Complaint 22-03-2021

8. Nature of complaint Repudiation of claims

9. Amount of Claim Rs. 294416/-

10. Date of Partial Settlement NA

11. Amount of relief sought Rs. 294416/-

12. Complaint registered under Rule no:

Insurance Ombudsman Rules, 2017

Rule 13 (1)(b) – any partial or total repudiation of claim

by an insurer

13. Date of hearing/place 20.08.2021/ Online hearing

14. Representation at the hearing

For the Complainant Shri Mahabir Parshad Sharma, the complainant

For the insurer Smt. Pamela Pinto, Deputy Manager (LCD), Mumbai

15 Complaint how disposed Recommendation under Rule 16

16 Date of Award/Order 20.08.2021

17. Brief Facts of the Case: Shri Mahabir Parshad Sharma (hereinafter, the Complainant) has filed this complaint against the

United India Insurance Co. Ltd. (hereinafter, the Insurers) for non-settlement of health claims.

18. Cause of Complaint:

a) Complainants argument: He retired from PNB on 30.06.2019. His wife Smt. Shakuntla Sharma is suffering from Metastatic

Carcinoma-breast and is under treatment since July 2016. Since then the chemotherapy (Trastuzumab) is being given at an

interval of every 21 days w.e.f 18.07.2016 and every month w.e.f. 11.10.2019 in day care. TPA/UIIC has sanctioned and paid

all the claims of above treatments till 30.10.2019. They started rejection of claims from November 2019, i.e. for the policy

period 01.11.2019 to 31.10.2020 although there was no change in the terms and conditions of the policy from the previous

year policy. Eleven claims amounting to Rs.294416/- were rejected, while one claim of Rs. 29610/- (DOA – 12.09.20) was paid

on 15.12.2020. Rejected claims are of Rs.28378/-(Date of admission-08.11.19), 28806/- (DOA-09.12.2019), 28918/- (DOA-

08.01.2020), 44667/- (DOA-08.02.2020), 29317/- (DOA-11.03.2020), 28639/- (DOA-10.04.2020), 29121/- (DOA-11.05.2020),

34930/- (DOA-13.06.2020), 8723/- (DOA-13.07.2020), 27927/- (DOA-14.08.2020), 4990/- (DOA-14.10.2020). The HITPA/UIIC

has rejected these claims of chemotherapy day care treatment and has informed the reason: ‘As per documents submitted

the patient was admitted for carcinoma breast and underwent injection Trastuzumab, this treatment was not listed under day

care procedure hence the claim is recommended for repudiation under clause 3.3”. As per complainant, all the above claims

of chemotherapy day care treatment are very much covered and listed under Sr.No.13 (Chemotherapy including parental

chemotherapy) of clause 3.3 of relevant policy.

b) Insurers’ argument: The insured Smt. Shakuntla Sharma was suffering from Metastatic Carcinoma – breast. Various claims of

Rs. 324026/- were lodged by the insured. As per claim documents, patient was treated by intravenous administration of

injection Trastuzumab + Injection Zolendronic Acid + Tablet Anastrozole (oral) without any chemotherapy drug being

administered. Trastruzumab is a monoclonal antibody treatment and Zolendronic Acid is to treat the high level of calcium in

the blood while Anastrozole is a non-steroidal inhibitor, which blocks estrogen synthesis. The period of hospitalization was

less than 24 hours. As per clause 2.19, Hospitalization means admission in a hospital/nursing home for a minimum period of

24 in-patient care consecutive hours except for the specified day care procedures/treatments, where such admission could

be a period of less than 24 consecutive hours. The intravenous administration of injection Trastuzumab + Injection Zolendronic

Acid + Tablet Anastrozole (oral) without any chemotherapy drug being administered does not come under the list of

procedures mentioned under clause 3.3 of the policy. In view of the same the claims were repudiated under clause 2.19 and

3.3 of the policy. Company also informed that claim no. 201100113300 for Rs. 29610/- was inadvertently paid by them

subsequently on 15.12.2020 under the STU Policy. Hence the insured is claiming for balance Rs. 294416/-.

19. Reason for Registration of Complaint: Non-payment of health claims.

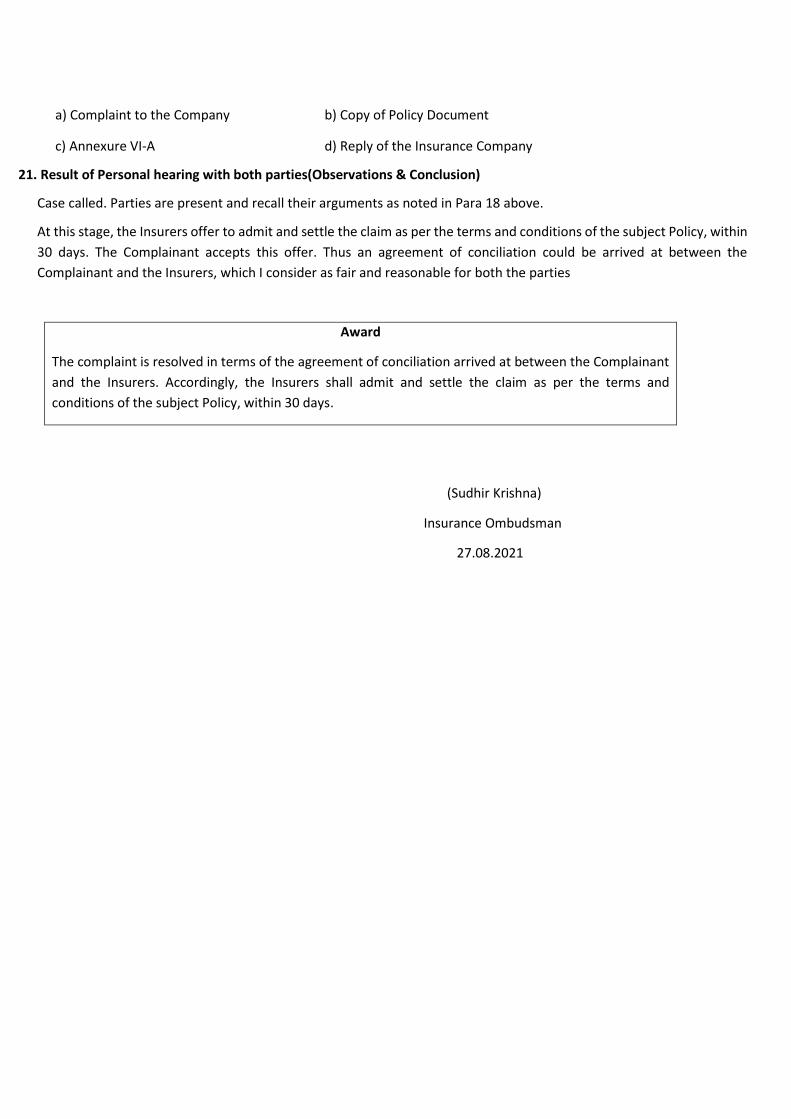

20 The following documents were placed for perusal:

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21. Result of Personal hearing with both parties (Observations & Conclusion):

Case called. Parties are present and recall their arguments as noted in Para 18 above.

At this stage, the Insurers offer to admit and settle the claims including for the pre & post-hospitalisation, within 30 days. The

Complainant accepts this offer. Thus an agreement of conciliation could be arrived at between the Complainant and the

Insurers, which I consider as fair and reasonable for both the parties.

Award

The complaint is resolved in terms of the agreement of conciliation arrived at between the Complainant

and the Insurers. Accordingly, the Insurers shall admit and settle the claims including for the pre & post-

hospitalisation, within 30 days.

(Sudhir Krishna)

Insurance Ombudsman

August 20, 2021

PROCEEDINGS OF THE INSURANCE OMBUDSMAN, CHANDIGARH

(Under Rule 13 r/w 16 of The Insurance Ombudsman Rules, 2017)

Insurance Ombudsman: Shri Sudhir Krishna

Case of Narendra Singh Rana V/S The United India Insurance Co. Ltd.

Complaint Ref. No. : CHD-H-051-2021-0762

1. Name & Address of the

Complainant

Shri Narendra Singh Rana

Flat No. 740 FF, Block- TC, CHD City,

Sector- 45, Karnal, Haryana- 132001

Mobile No.- 9412843972

2. Policy No:

Type of Policy

Duration of policy/Policy period

5001002819P112263948

Group Health Policy

01-11-2019 To 31-10-2020

3. Name of the insured

Name of the policyholder

Narendra Singh Rana & Raj Dulari

Indian Bank’s Association, a/c PNB

4. Name of the insurer The United India Insurance Co. Ltd.

5. Date of Repudiation 06.04.21

6. Reason for repudiation Day care treatment not allowed

7. Date of receipt of the Complaint 26-03-2021

8. Nature of complaint Repudiation of Claims

9. Amount of Claim Rs. 98267/-

10. Date of Partial Settlement NA

11. Amount of relief sought Not specified

12. Complaint registered under Rule

no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation of claim by an

insurer

13. Date of hearing/place 27.08.2021/ Online hearing

14. Representation at the hearing

For the Complainant Shri Narendra Singh Rana, the complainant

For the insurer Smt. Pamela Pinto, Deputy Manager (LCD), Mumbai

15 Complaint how disposed Recommendation under Rule 16

16 Date of Award/Order 27.08.2021

17. Brief Facts of the Case: Shri Narendra Singh Rana (hereinafter, the Complainant), has filed this complaint against the

United India Insurance Co. Ltd. (hereinafter, the Insurers) for non-settlement of health claims on his wife.

18. Cause of Complaint:

a) Complainants argument: His wife Smt. Raj Dulari was under the treatment of AIIMS Delhi and diagnosed NHL – B

(Cancer). The reimbursement of medical bills was in proper way but TPA of UIIC had stopped the payment without any

information. When contacted, TPA informed that there were changes in the policy during 2019-20. The unsettled claims

are for Rs. 35222, Rs. 16103/-, 14107/-, 8834/-, 24500/-. One bill of Rs. 5061/- had been passed for the same disease.

b) Insurers’ argument: Shri Narendra Singh Rana and spouse Smt. Raj Dulari covered under IBA –PNB retired employees

without domiciliary policy. Smt. Raj Dulari was suffering from Indolent B–Non Hodgins Lymphoma and undergoing

treatment for the same. Following claims were lodged by the insured:

Claim No. DOA- DOD Amount Claimed

201100068097 01.03.20 to 01.03.20 35222

201100088379 12.05.20 to 12.05.20 16104

201100193271 10.07.20 to 11.07.20 24500

201100193017 10.09.20 to 10.09.20 14107

201100193025 Pre post Hosp. expenses of Claim no.

201100193017

8334

Total 98267

As per claim documents, it was observed that the patient was being treated by intravenous administration of injection

Rituximab on standalone basis without any chemotherapy drug being administered. The period of hospitalization was

less than 24 hours. As per clause 2.19, hospitalization means admission in a hospital/nursing home for a minimum period

of 24 in-patient care consecutive hours except for specified day care procedures/treatments, where such admission

could be for a period of less than 24 consecutive hours. The administration of injection Rituximab, which is an antibody

therapy on standalone basis does not come under the list of procedures mentioned under Clause 3.3 of the policy. In

view of the same, the claims were repudiated citing clause 2.19 and 3.3 of the policy terms and conditions.

19. Reason for Registration of Complaint: Non-settlement of health claims.

20. The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21. Result of Personal hearing with both parties(Observations & Conclusion)

Case called. Parties are present and recall their arguments as noted in Para 18 above.

At this stage, the Insurers offer to admit and settle the claim as per the terms and conditions of the subject Policy, within

30 days. The Complainant accepts this offer. Thus an agreement of conciliation could be arrived at between the

Complainant and the Insurers, which I consider as fair and reasonable for both the parties

Award

The complaint is resolved in terms of the agreement of conciliation arrived at between the Complainant

and the Insurers. Accordingly, the Insurers shall admit and settle the claim as per the terms and

conditions of the subject Policy, within 30 days.

(Sudhir Krishna)

Insurance Ombudsman

27.08.2021

PROCEEDINGS BEFORE

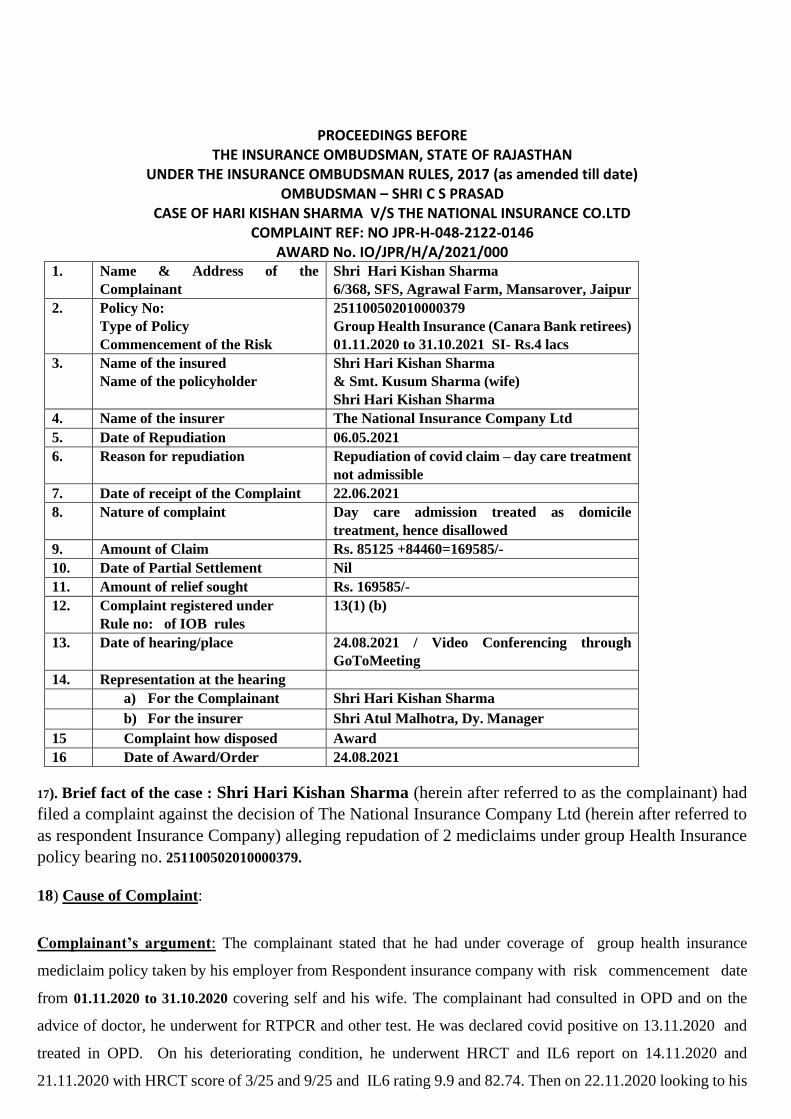

THE INSURANCE OMBUDSMAN, STATE OF RAJASTHAN UNDER THE INSURANCE OMBUDSMAN RULES, 2017 (as amended till date)

OMBUDSMAN – SHRI C S PRASAD CASE OF HARI KISHAN SHARMA V/S THE NATIONAL INSURANCE CO.LTD

COMPLAINT REF: NO JPR-H-048-2122-0146 AWARD No. IO/JPR/H/A/2021/000

1. Name & Address of the

Complainant

Shri Hari Kishan Sharma

6/368, SFS, Agrawal Farm, Mansarover, Jaipur

2. Policy No:

Type of Policy

Commencement of the Risk

251100502010000379

Group Health Insurance (Canara Bank retirees)

01.11.2020 to 31.10.2021 SI- Rs.4 lacs

3. Name of the insured

Name of the policyholder

Shri Hari Kishan Sharma

& Smt. Kusum Sharma (wife)

Shri Hari Kishan Sharma

4. Name of the insurer The National Insurance Company Ltd

5. Date of Repudiation 06.05.2021

6. Reason for repudiation Repudiation of covid claim – day care treatment

not admissible

7. Date of receipt of the Complaint 22.06.2021

8. Nature of complaint Day care admission treated as domicile

treatment, hence disallowed

9. Amount of Claim Rs. 85125 +84460=169585/-

10. Date of Partial Settlement Nil

11. Amount of relief sought Rs. 169585/-

12. Complaint registered under