PRIVATIZATION AND FINANCIAL PERFORMANCE OF GOVERNMENT FIRMS IN KENYA BY GEORGE MIGWI MUCHIRI UNITED STATES INTERNATIONAL UNIVERSITY-AFRICA SPRING 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PRIVATIZATION AND FINANCIAL PERFORMANCE OF GOVERNMENT

FIRMS IN KENYA

BY

GEORGE MIGWI MUCHIRI

UNITED STATES INTERNATIONAL UNIVERSITY-AFRICA

SPRING 2020

PRIVATIZATION AND FINANCIAL PERFORMANCE OF GOVERNMENT

FIRMS IN KENYA

BY

GEORGE MIGWI MUCHIRI

A Research Project Report Submitted to the School of Business in Partial

Fulfillment of the Requirement for the Degree of Degree of Master of Business

Administration.

UNITED STATES INTERNATIONAL UNIVERSITY-AFRICA

SPRING 2020

i

STUDENT`S DECLARATION

I, George Migwi Muchiri, declare that this is my original work and has not been submitted

to any other college, institution or university other than the United States International

university-Africa.

Signed………………………….. Date……………………………………………..……

George Migwi Muchiri (ID 656165)

This proposal has been presented for academic purposes with my approval as the appointed

supervisor

Signed …………………………….. Date……………………………………...…………..

Dr. Francis Gatumo

Signed……………………………… Date…………………………………...…………….

Dean Chandaria School of Business

ii

COPYRIGHT

All rights for this proposal are reserved. Printing or reproduction in any form is prohibited

without express permission from the author.

© George Migwi Muchiri, 2020

iii

ABSTRACT

The main purpose of the study was to establish the impact of privatization on the financial

performance of government firms in Kenya. The study was guided by three research

questions which were; 1.4.1 what is the Performance of Firms before Privatization? What

is the Performance of Firms after Privatization? and what are Measures of Improving

Privatization Processs?.

The study applied a quasi-experimental (event study) to carry out the study. The researcher

observed the pre and post-privatization performance of several government firms that were

privatized between 1991 to 2008. The sampling frame for this study was the 6 privatized

government firms. Simple random sampling was used in this study so as to ensure that each

element in the population of an equal chance of being included in the sample. Data forms

were used to collect data for the period of six years. Descriptive statistics such as mean and

standard deviation were used to test the data for its ability to be relied upon for valid

conclusion. Inferential statistic used in the study was regression analysis.

The first research question addressed the performance of government firms before

privatization. The performance was measured by the use of mean and standard deviation.

The study discovered that companies performed better after privatization. This indicated

that they became more stable after privatization. The return on turnover increased after

privatization. Return on assets increased after privatization of the companies. Return on

equity also signified a great improvement after privatization compared to the period before

privatization.

The second research question was to address the financial performance of the privatized

companies. This section used return on assets, return on turnover and return on equity to

measure the financial performance. Each company was analyzed individually. The study

revealed that in the first three years before privatization, KENGEN performed poorly

compared to the three years after privatization. Return on turnover kept on increasing and

decreasing after privatization. National Bank of Kenya performed better after privatization

although all the measures kept on fluctuating from high to low. Kenya Airways Limited

showed an improved financial performance after privatization. Return on total assets kept

on changing from high to low and vice-versa. Kenya Re-insurance Corporation limited

improved its financial performance after privatization. Although the return on assets

iv

improved in the first year, it dropped in the second year after privatization. Housing Finance

Corporation of Kenya`s financial performance improved drastically after the privatization.

Generally, the performance improved although some measures like return on turnover and

return on equity kept on decreasing and increasing after privatization. Mumias Sugar

Company financial performance improved generally after privatization. In the second year

after privatization, all the measures of financial performance decreased and rose

significantly in the third year.

The third research question was to establish the measures which can be used to improve

privatization process. The study revealed that; conducive environment by government

improves privatization process, conducive environment encourages competition in the

market, conducive environment improves the performance of privatized companies and

favorable government policies favor privatization process. The study further revealed that

employment of qualified staff enables smooth privatization process, government should

streamline the privatization process to make it easier and that privatization process should

be short and simple.

The conclusion of the study was that all firms should work hard without considering the

issue of privatization in mind. The government should put measures to ensure that its firms

perform well even before privatization. The privatized firms should motivate its employees

and management throughout the operations so as to ensure healthy and stable performance

of the firm. There should be a good relationship between the management and the

government to avoid conflicts of interests.

The study recommends state owned companies to monitor their performance and that the

companies use both financial and non-financial measures to monitor the performance of

the firms after privatization. The study recommends further research to be done for a longer

period more than five years before and after privatization.

v

DEDICATION

This project is dedicated to my mom, family and friends for their untiring support

throughout my master’s degree and their inspiration that assisted me complete this research

proposal.

vi

ACKNOWLEDGEMENT

I thank God for guiding me through my education journey. I also appreciate my supervisor

Dr. Francis Gatumo for support and guidance through this research study. Finally I give

special thanks to my wife and children for their continued support and inspiration all

through my studies. God bless them all abundantly.

vii

ABBREVIATIONS

ROT- Return on Turnover

ROE- Return on Equity

ROTA- Return on Total Assets

IMF- International Monetary Fund

HFCK- Housing Finance Corporation of Kenya

viii

TABLE OF CONTENTS

STUDENT`S DECLARATION ......................................................................................... i

COPYRIGHT ..................................................................................................................... ii

ABSTRACT ....................................................................................................................... iii

DEDICATION.................................................................................................................... v

ACKNOWLEDGEMENT ................................................................................................ vi

ABBREVIATIONS .......................................................................................................... vii

TABLE OF CONTENTS ............................................................................................... viii

LIST OF TABLES ............................................................................................................. x

LIST OF FIGURES .......................................................................................................... xi

CHAPTER ONE ................................................................................................................ 1

1.0 INTRODUCTION........................................................................................................ 1

1.1 Background of the Study ............................................................................................... 1

1.2 Statement of the Problem ............................................................................................... 5

1.3 Purpose of the Study ...................................................................................................... 6

1.4 Research Objectives ....................................................................................................... 6

1.5. Importance of the Study ................................................................................................ 6

1.6 Scope of the Study ......................................................................................................... 7

1.7 Definition of Terms ........................................................................................................ 7

1.8 Chapter Summary .......................................................................................................... 8

CHAPTER TWO ............................................................................................................... 9

2.0 LITERATURE REVIEW ............................................................................................ 9

2.1 Introduction .................................................................................................................... 9

2.2 Performance of Firms before Privatization .................................................................... 9

2.3. Performance of Firms after Privatization .................................................................... 13

2.4. Measures of Improving Privatization Processs ........................................................... 17

2.5. Chapter Summary ....................................................................................................... 21

CHAPTER THREE ......................................................................................................... 22

3.0. RESEARCH METHODOLOGY ............................................................................ 22

3.1. Introduction ................................................................................................................. 22

3.2. Research Design.......................................................................................................... 22

3.3. Population and Sampling Design ................................................................................ 22

3.4. Data Collection Method .............................................................................................. 24

ix

3.5. Research Procedures ................................................................................................... 24

3.6. Data Analysis Methods ............................................................................................... 25

3.7. Chapter Summary ....................................................................................................... 26

CHAPTER FOUR ............................................................................................................ 27

4.0 RESULTS AND FINDINGS ..................................................................................... 27

4.1 Introduction .................................................................................................................. 27

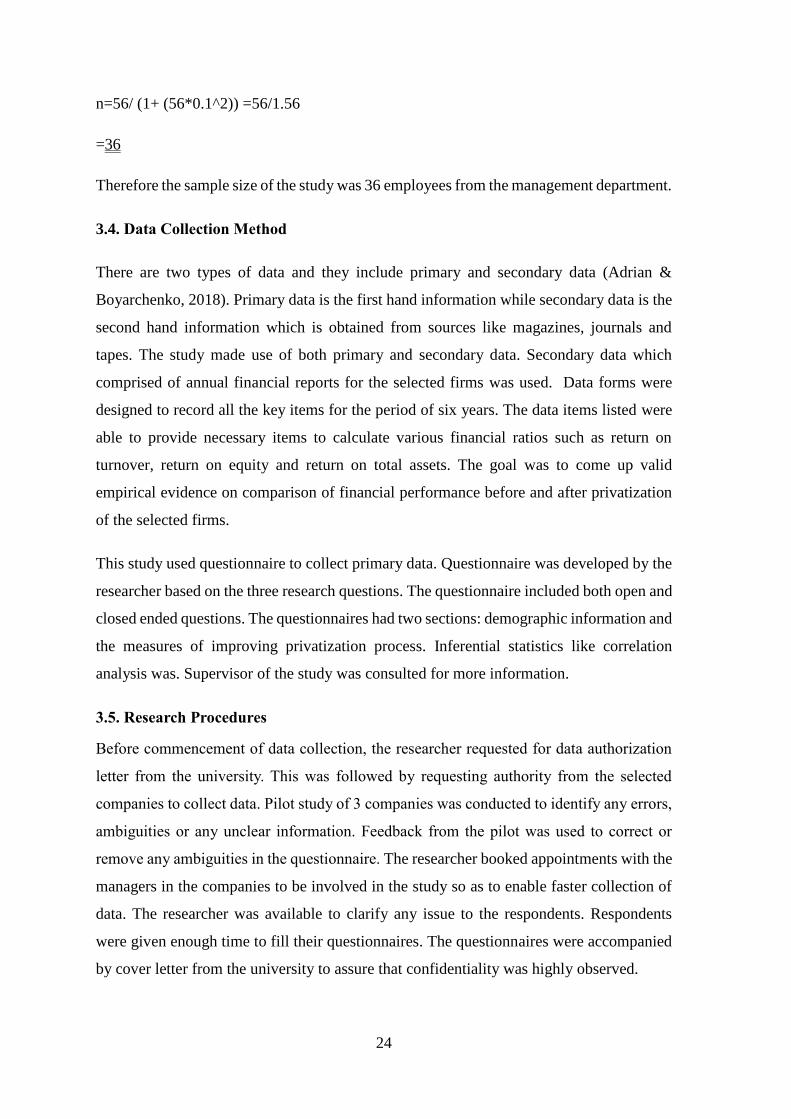

4.2 Demographic Information ............................................................................................ 27

4.3 Performance of Firms before Privatization .................................................................. 31

4.4 Performance of the Privatized Companies after Privatization ..................................... 45

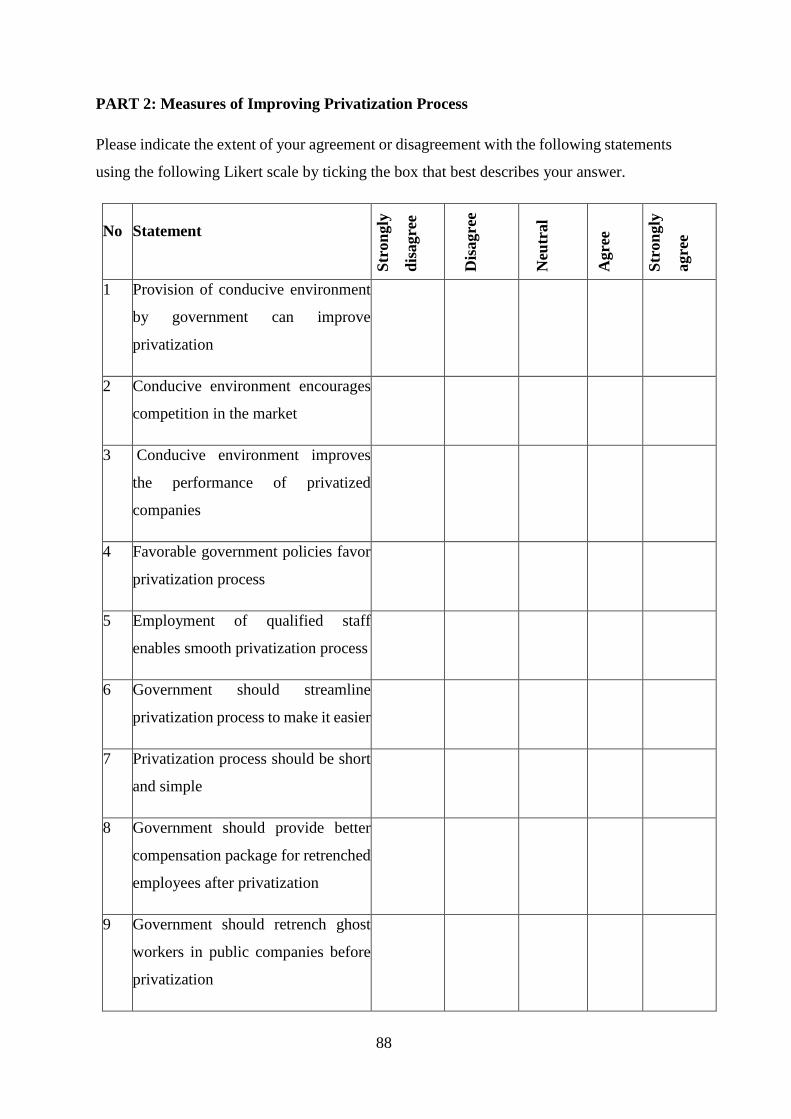

4.5 Measures of Improving Privatization Process ............................................................. 58

4.6 Chapter Summary ........................................................................................................ 66

CHAPTER FIVE ............................................................................................................. 67

5.0 DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS ........................ 67

5.1 Introduction .................................................................................................................. 67

5.2 Summary of the Study ................................................................................................. 67

5.3 Discussion .................................................................................................................... 68

5.4 Conclusions .................................................................................................................. 75

5.5 Recommendation ......................................................................................................... 76

REFERENCES ................................................................................................................. 78

APPENDIX A: INTRODUCTION LETTER

APPENDIX B: QUESTIONNAIRE

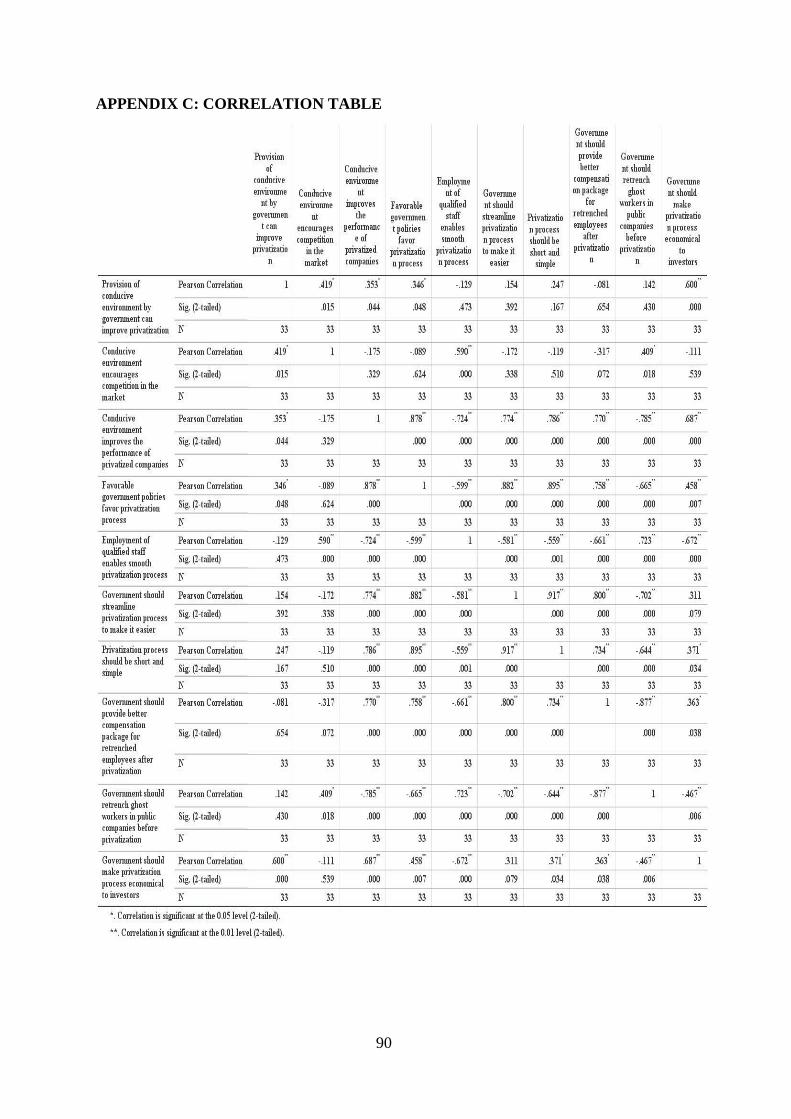

APPENDIX C: CORRELATION TABLE

x

LIST OF TABLES

Table 4. 1 Years of Experience .......................................................................................... 29

Table 4. 2 Financial Performance before Privatization ..................................................... 32

Table 4. 3 Financial Performance after Privatization ........................................................ 45

Table 4. 4 Conducive Environment Encourages Competition in the Market .................... 59

Table 4. 5 Favorable Government Policies Favor Privatization Process ........................... 60

Table 4. 6 Government Streamlining Privatization Process to Make It Easier ................. 62

Table 4. 7 Better Compensation Package for the Retrenched Employees ........................ 63

Table 4. 8 Retrenchment of Ghost Workers before Privatization ...................................... 64

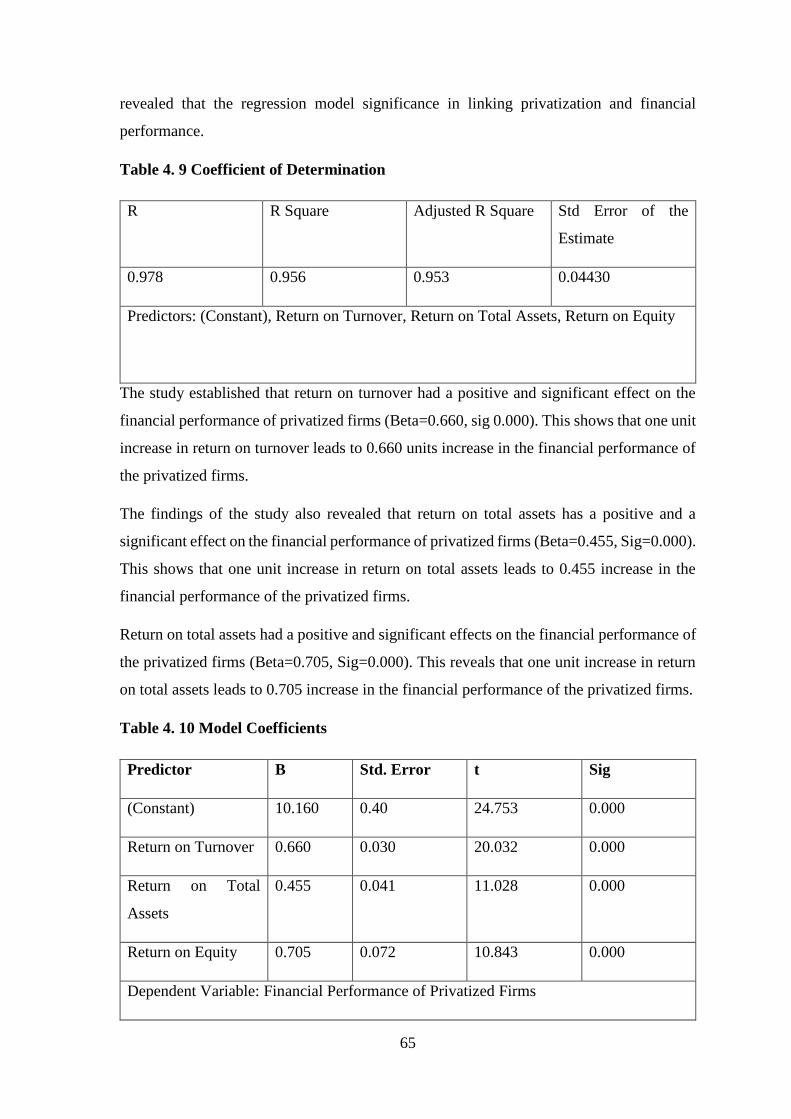

Table 4. 9 Coefficient of Determination ............................................................................ 65

Table 4. 10 Model Coefficients ......................................................................................... 65

xi

LIST OF FIGURES

Figure 4. 1 Management Level .......................................................................................... 27

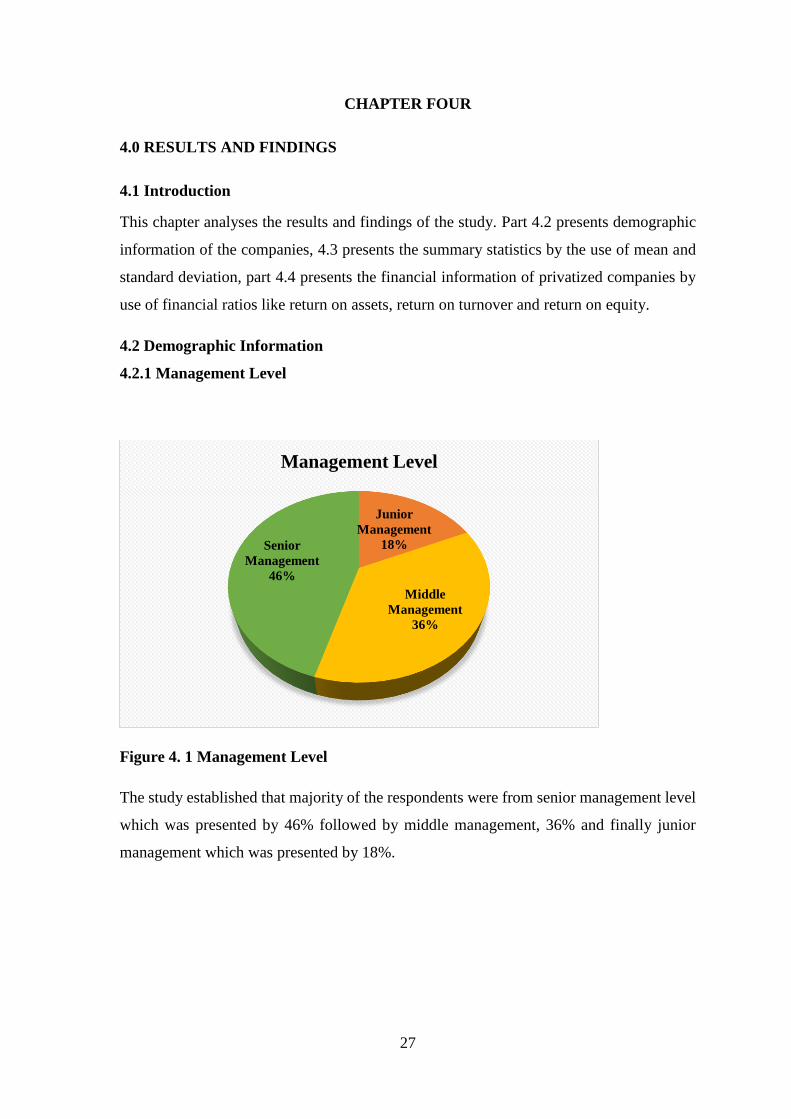

Figure 4. 2 Gender ............................................................................................................. 28

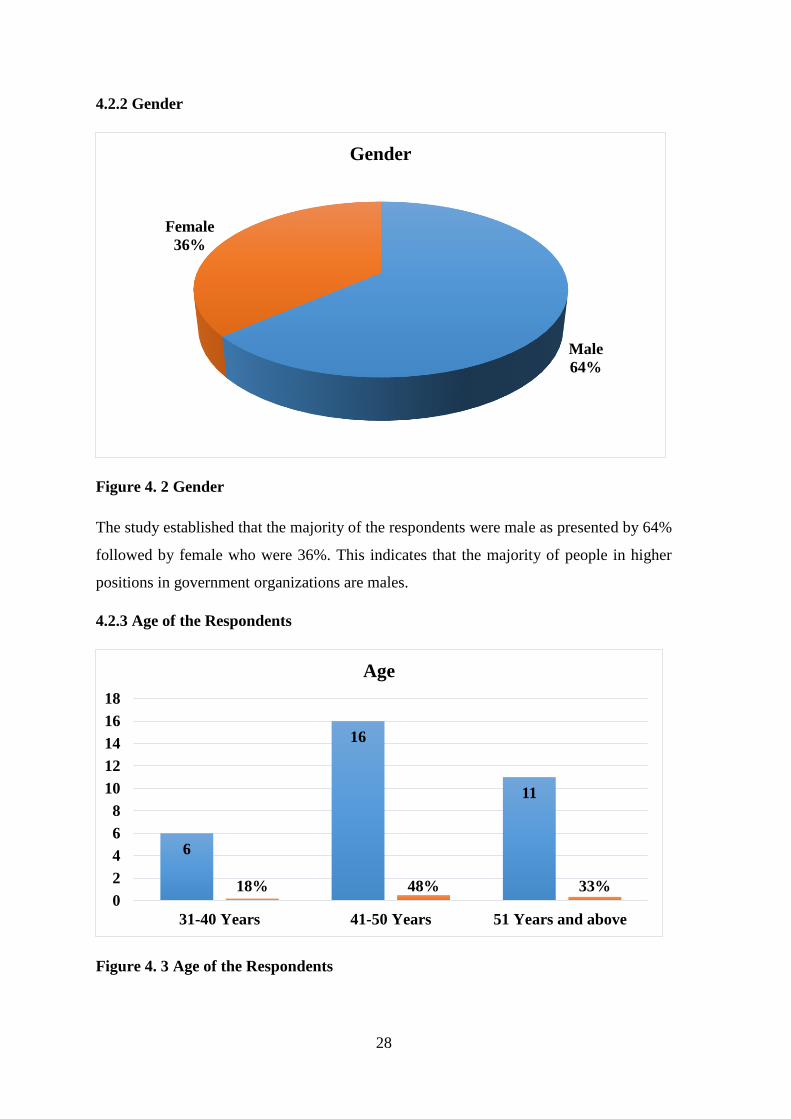

Figure 4. 3 Age of the Respondents ................................................................................... 28

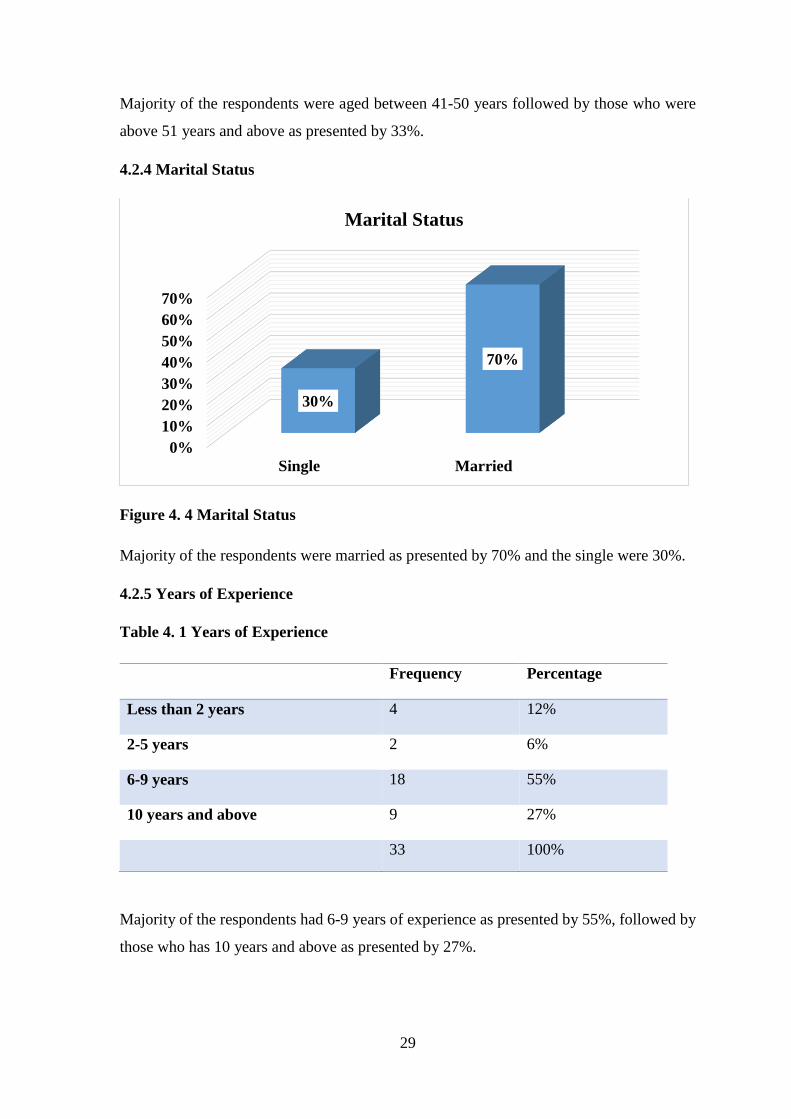

Figure 4. 4 Marital Status................................................................................................... 29

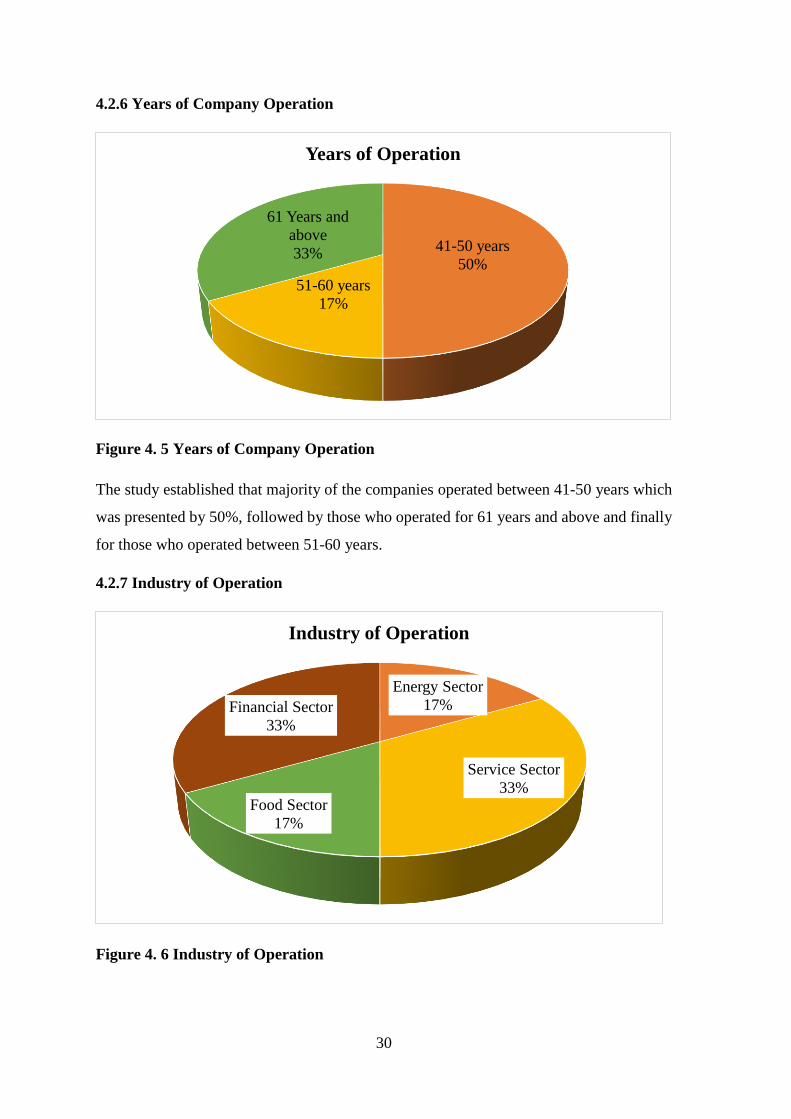

Figure 4. 5 Years of Company Operation .......................................................................... 30

Figure 4. 6 Industry of Operation ...................................................................................... 30

Figure 4. 7 Mean and Standard Deviation before Privatization ......................................... 33

Figure 4. 8 Return on Turnover for KENGEN before Privatization .................................. 33

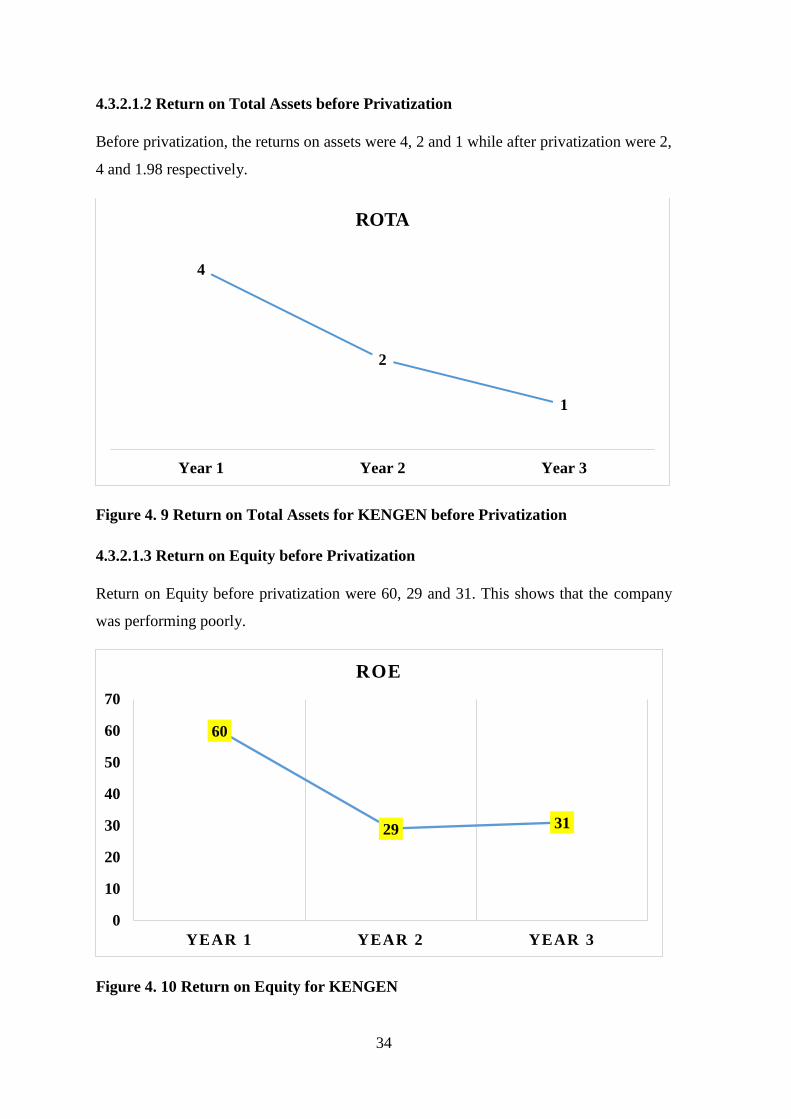

Figure 4. 9 Return on Total Assets for KENGEN before Privatization ............................. 34

Figure 4. 10 Return on Equity for KENGEN .................................................................... 34

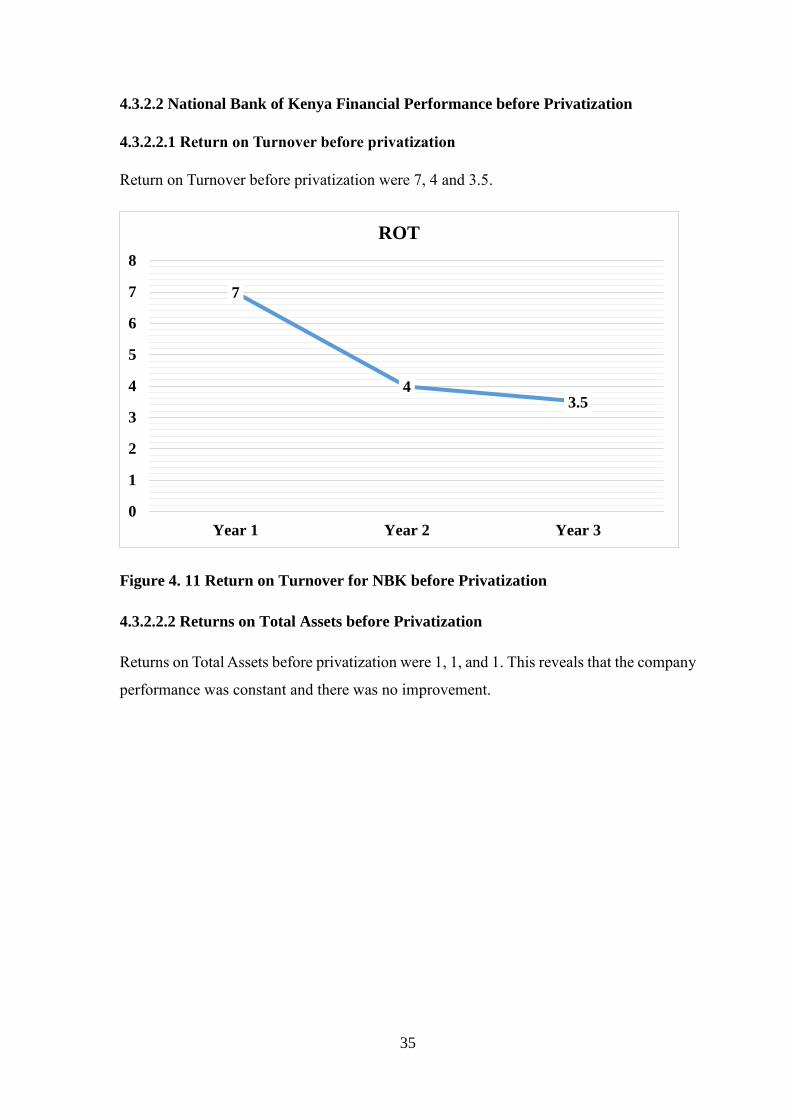

Figure 4. 11 Return on Turnover for NBK before Privatization ........................................ 35

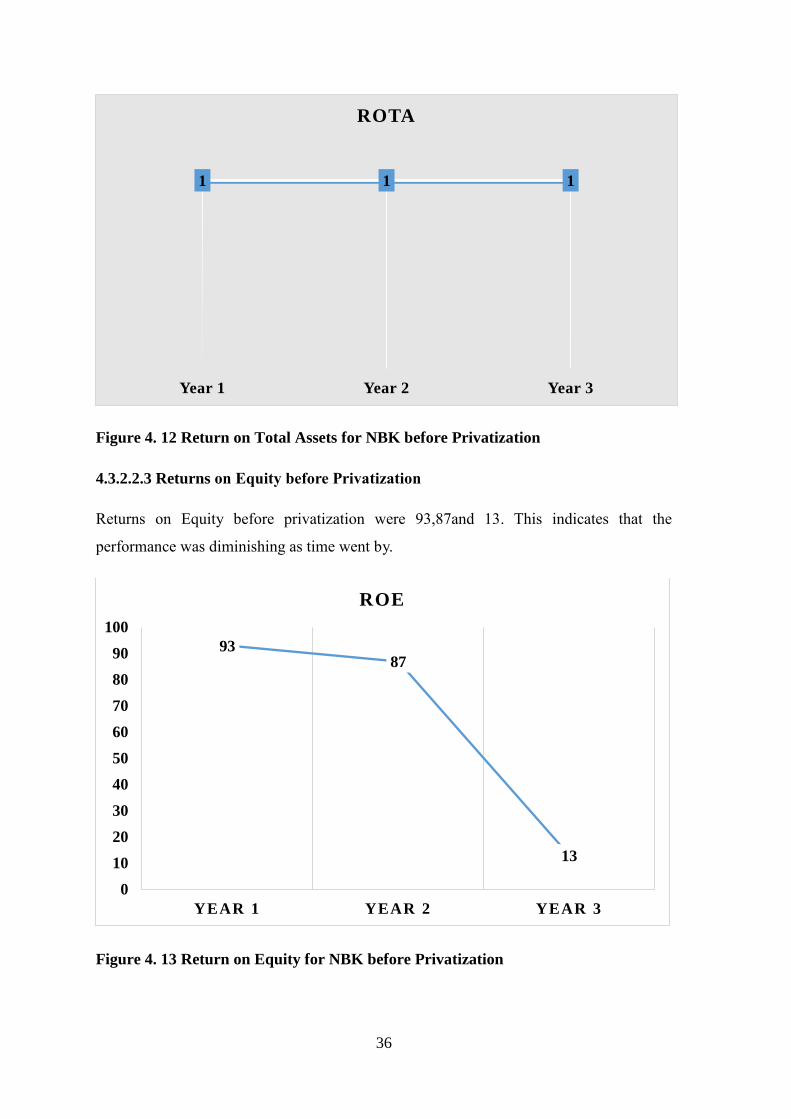

Figure 4. 12 Return on Total Assets for NBK before Privatization................................... 36

Figure 4. 13 Return on Equity for NBK before Privatization ............................................ 36

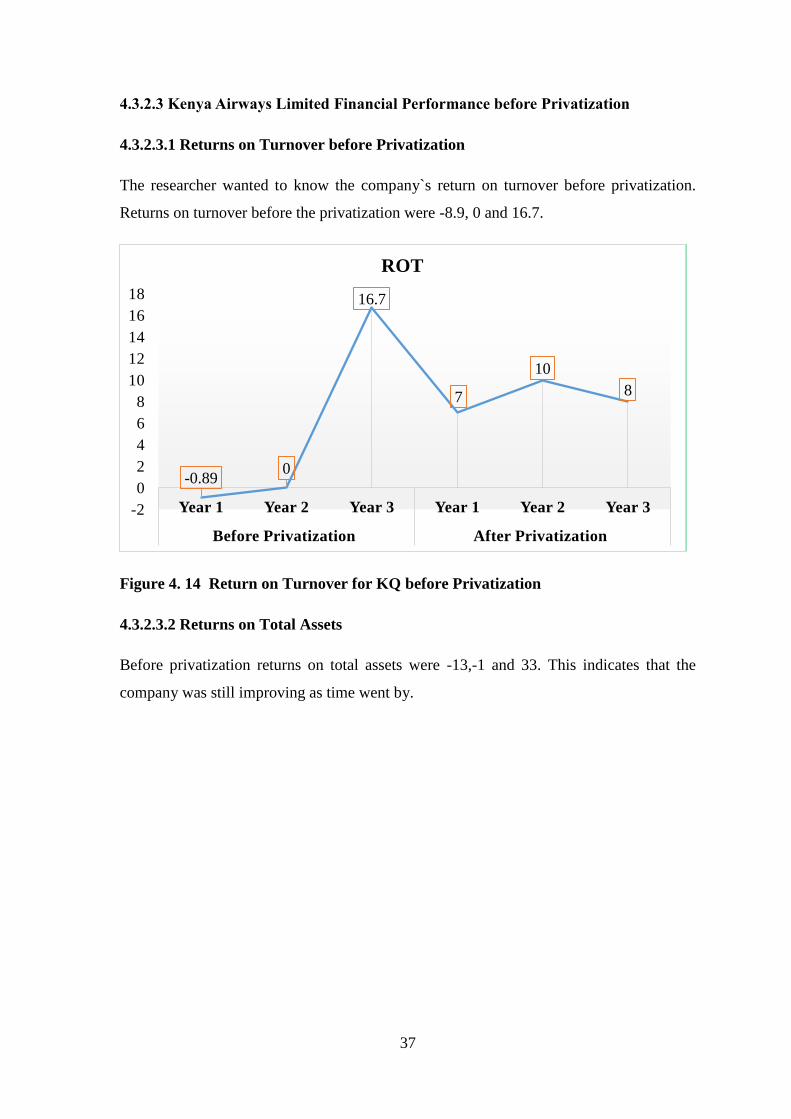

Figure 4. 14 Return on Turnover for KQ before Privatization ......................................... 37

Figure 4. 15 Returns on Total Assets for KQ before Privatization .................................... 38

Figure 4. 16 Return on Equity for KQ before Privatization .............................................. 38

Figure 4. 17 Returns on Turnover for Kenya Re before Privatization ............................... 39

Figure 4. 18 Returns on Total Assets for Kenya Re before Privatization.......................... 40

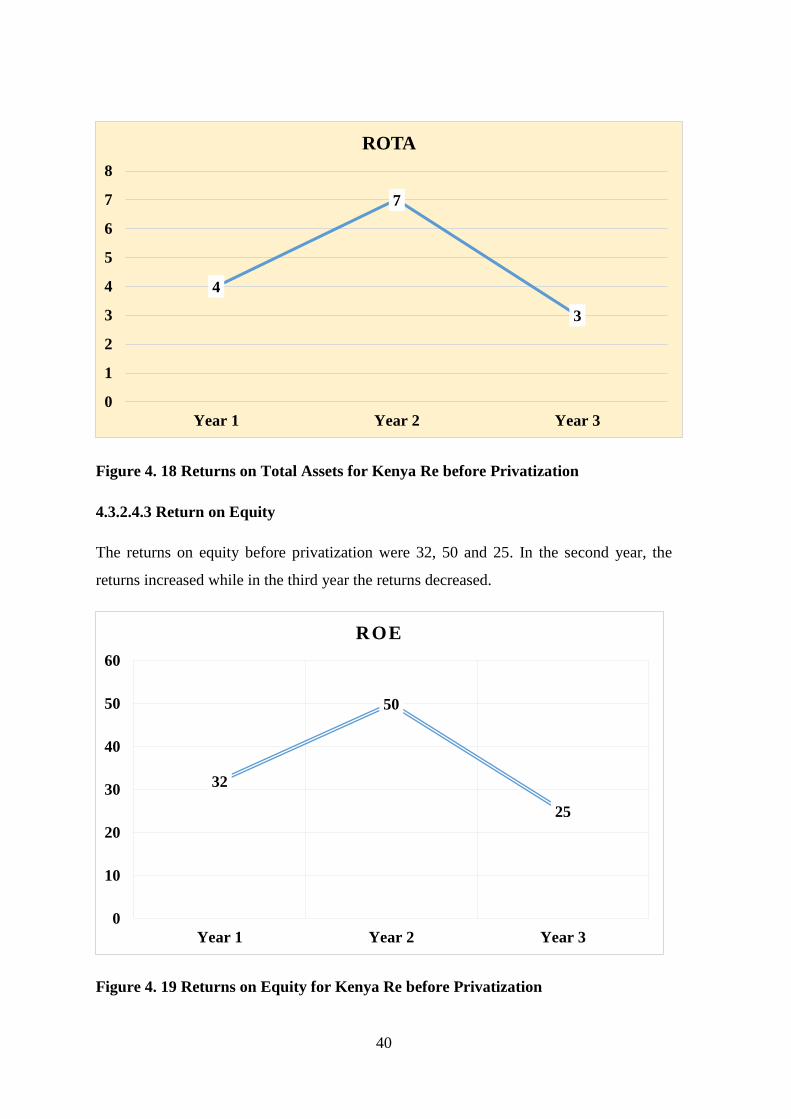

Figure 4. 19 Returns on Equity for Kenya Re before Privatization ................................... 40

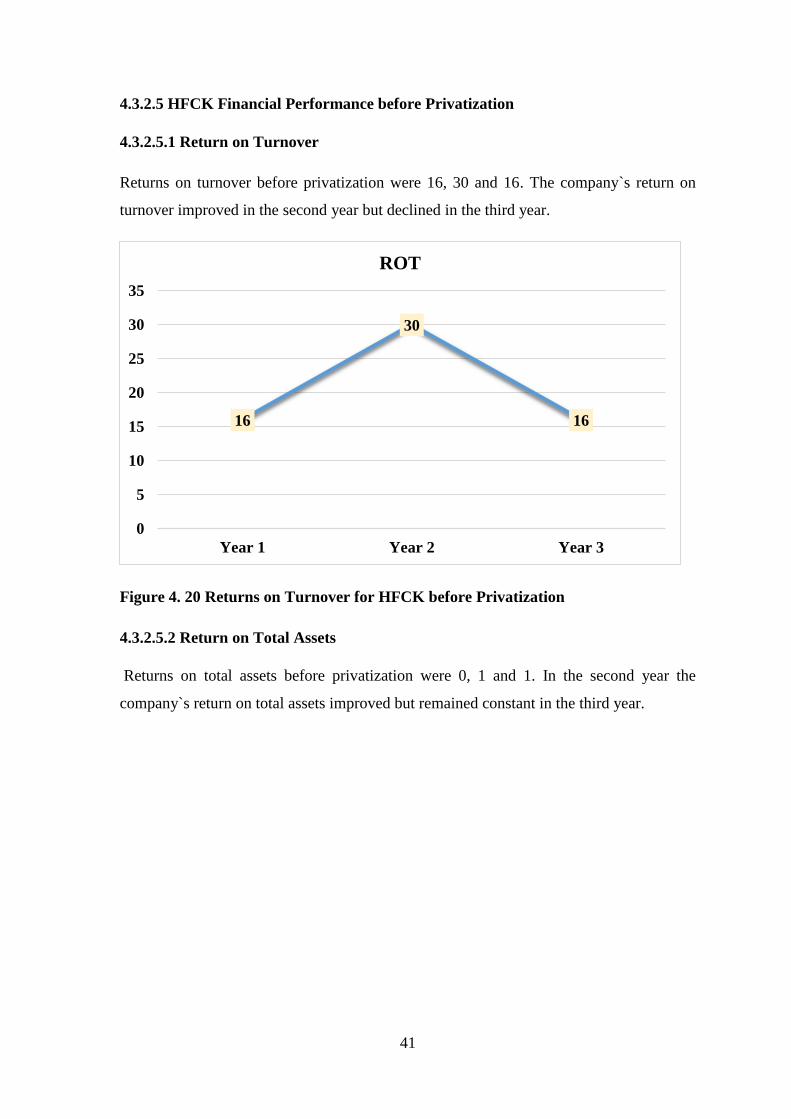

Figure 4. 20 Returns on Turnover for HFCK before Privatization .................................... 41

Figure 4. 21 Returns on total assets for HCFK before Privatization ................................. 42

Figure 4. 22 Returns on Equity for HCFK before Privatization ........................................ 42

Figure 4. 23 Returns on Turnover for Mumias before Privatization ................................. 43

Figure 4. 24 Returns on Total Assets for Mumias before Privatization ............................ 44

Figure 4. 25 Returns on Equity for Mumias before Privatization ...................................... 44

Figure 4. 26 Mean and standard deviation After Privatization .......................................... 46

Figure 4. 27 Return on Turnover for KENGEN after Privatization .................................. 47

Figure 4. 28 Return on Total Assets for KENGEN after Privatization ............................. 47

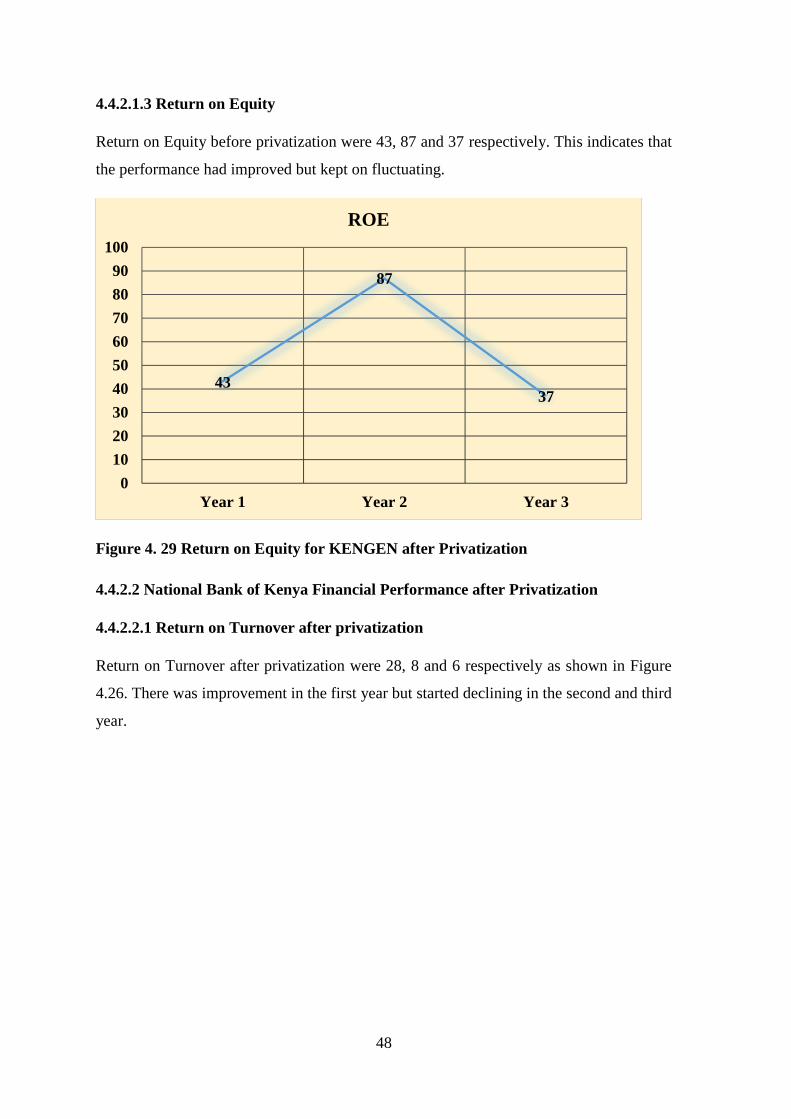

Figure 4. 29 Return on Equity for KENGEN after Privatization ....................................... 48

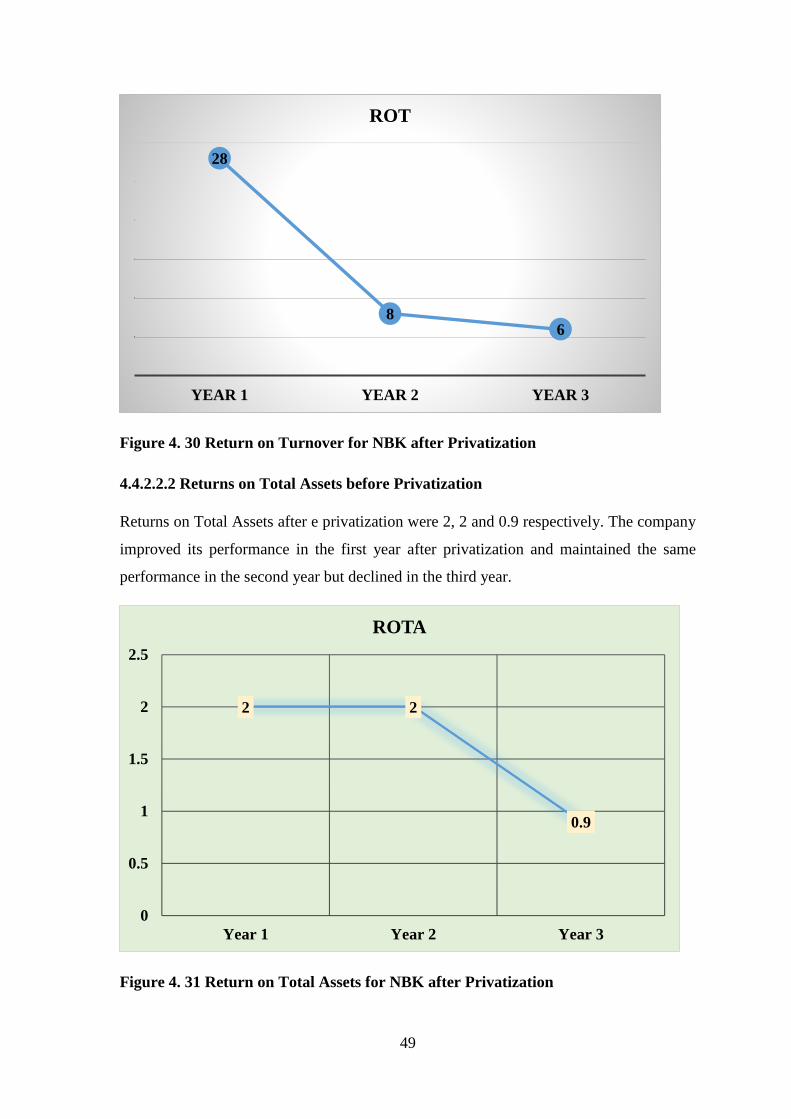

Figure 4. 30 Return on Turnover for NBK after Privatization .......................................... 49

Figure 4. 31 Return on Total Assets for NBK after Privatization ..................................... 49

Figure 4. 32 Return on Equity for NBK after Privatization .............................................. 50

xii

Figure 4. 33 Return on Turnover for KQ after Privatization ............................................. 50

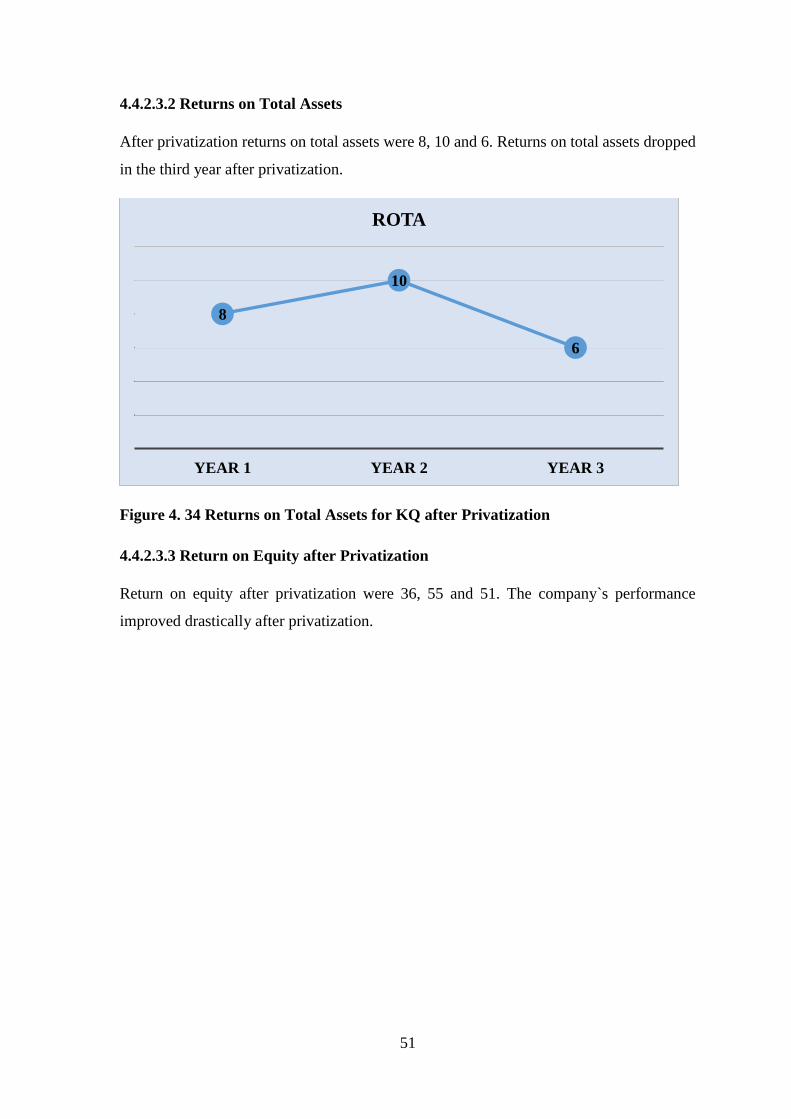

Figure 4. 34 Returns on Total Assets for KQ after Privatization ....................................... 51

Figure 4. 35 Return on Equity for KQ after Privatization ................................................. 52

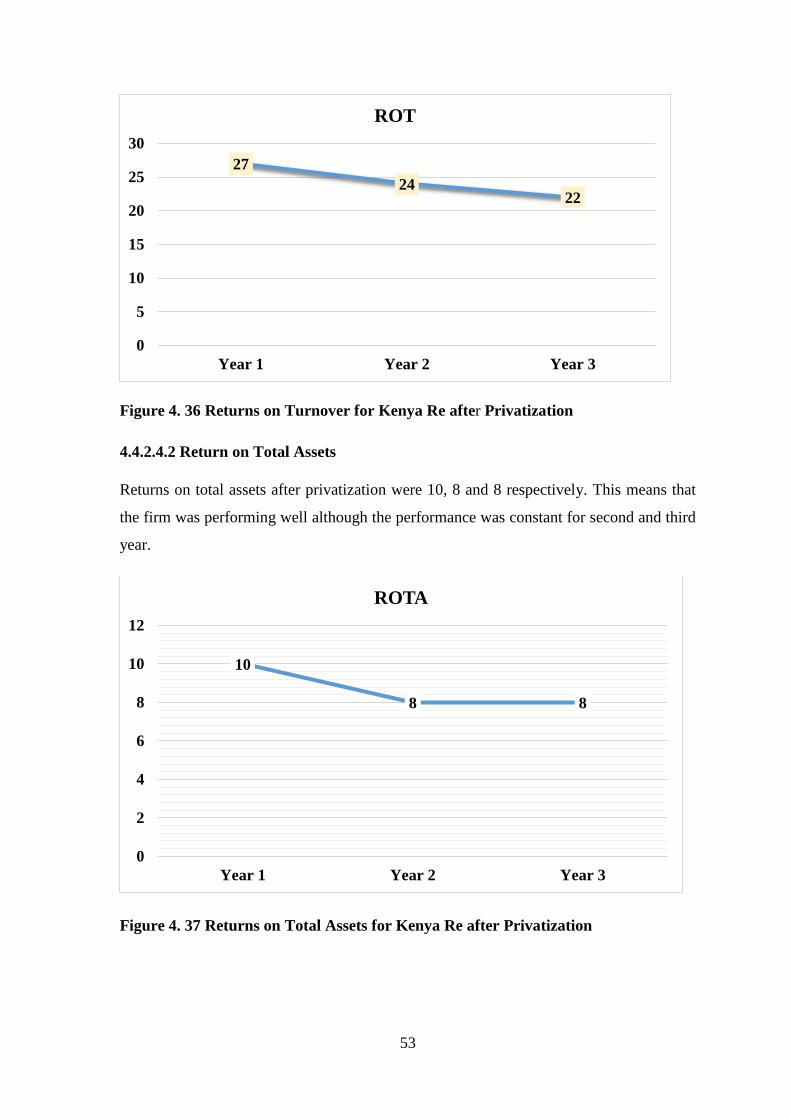

Figure 4. 36 Returns on Turnover for Kenya Re after Privatization ................................. 53

Figure 4. 37 Returns on Total Assets for Kenya Re after Privatization ............................ 53

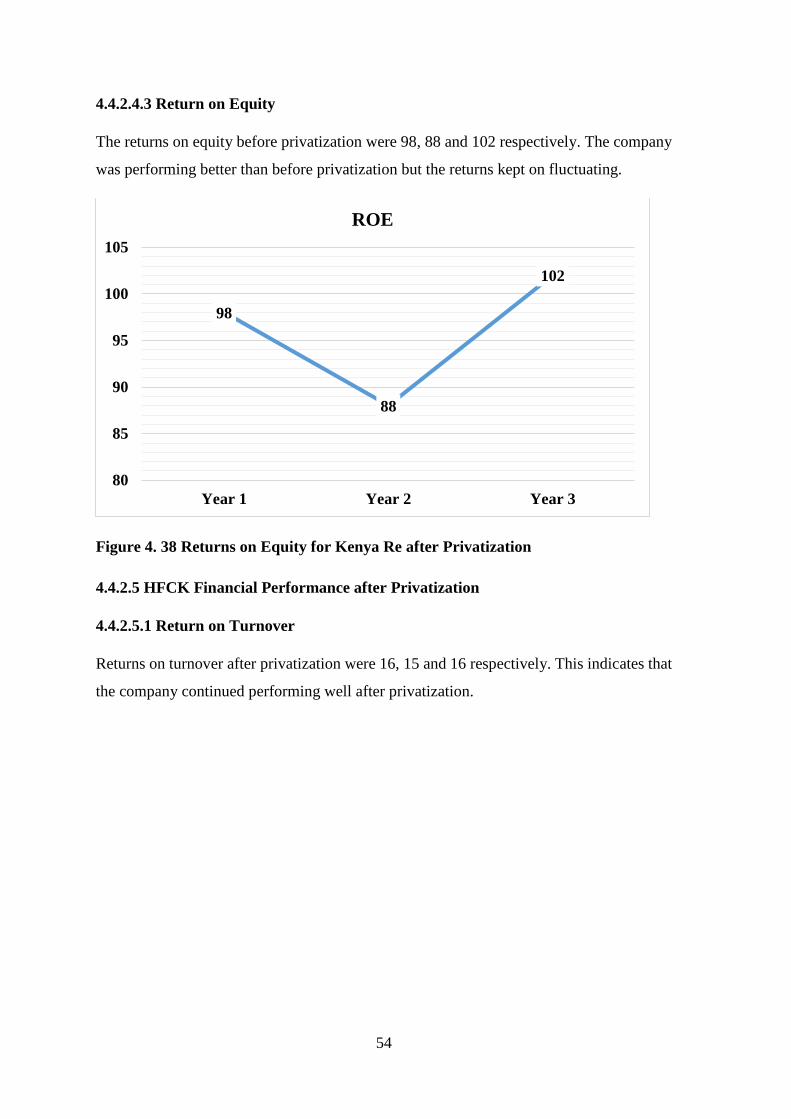

Figure 4. 38 Returns on Equity for Kenya Re after Privatization ...................................... 54

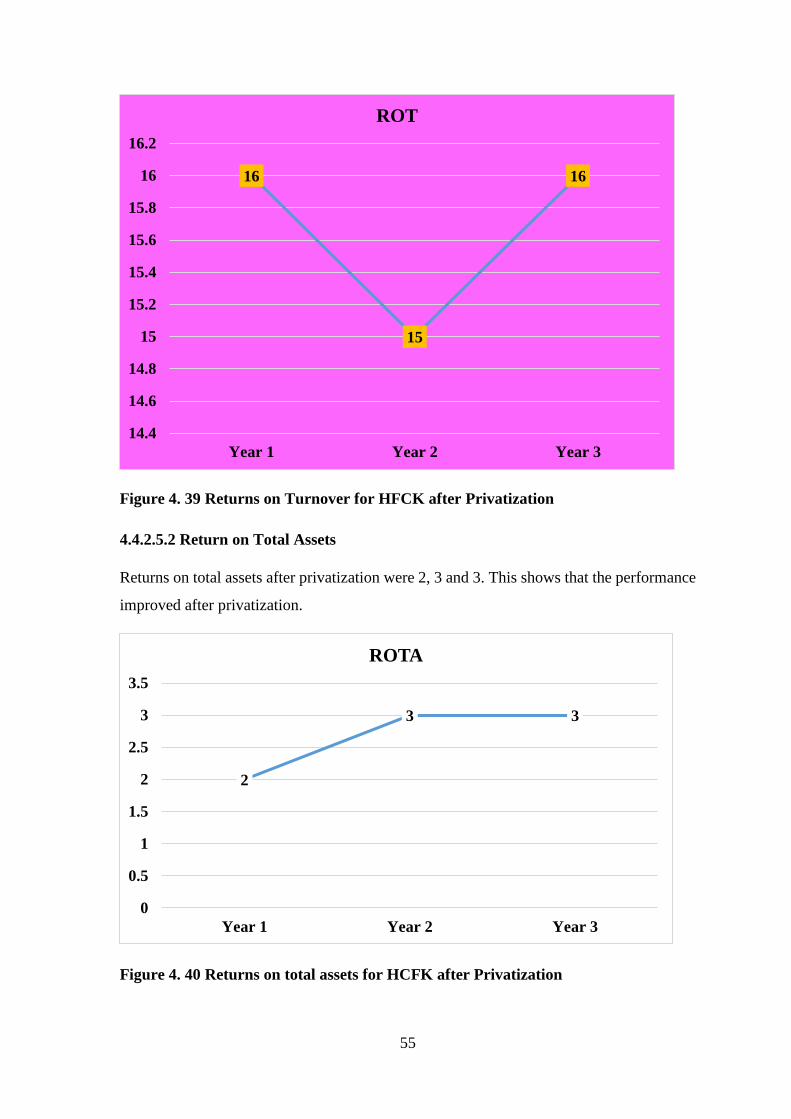

Figure 4. 39 Returns on Turnover for HFCK after Privatization ....................................... 55

Figure 4. 40 Returns on total assets for HCFK after Privatization .................................... 55

Figure 4. 41 Returns on Equity for HCFK after Privatization ........................................... 56

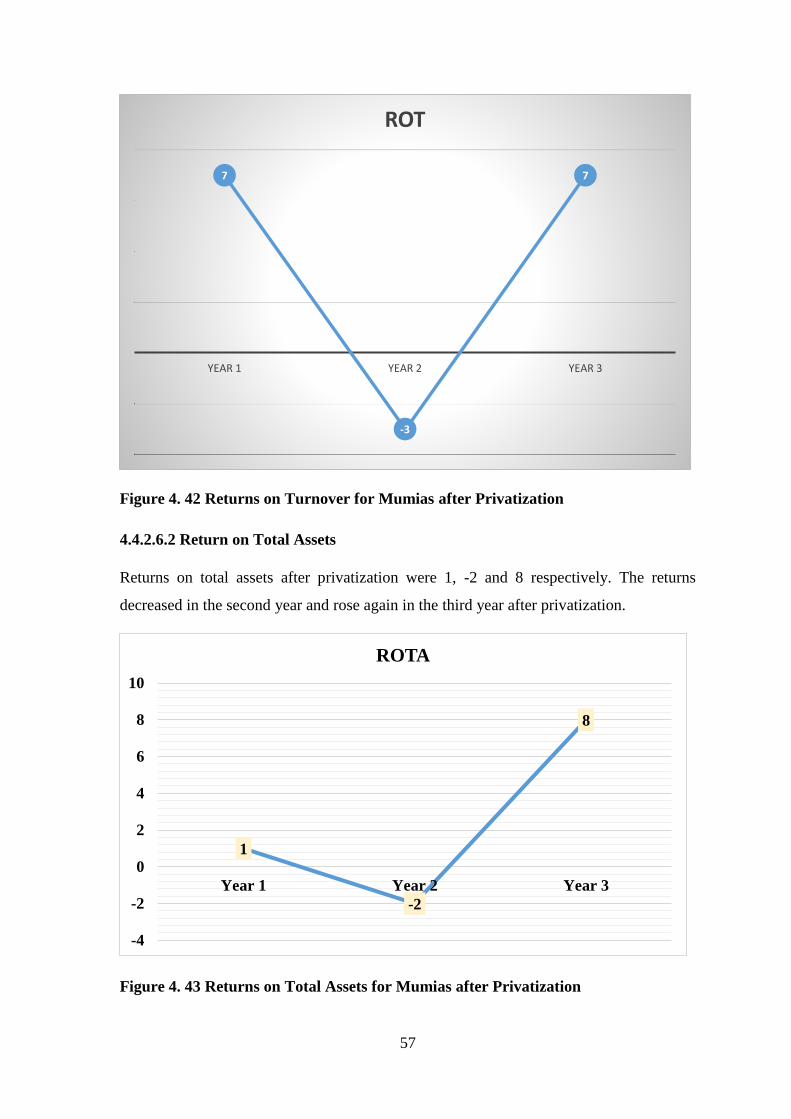

Figure 4. 42 Returns on Turnover for Mumias after Privatization .................................... 57

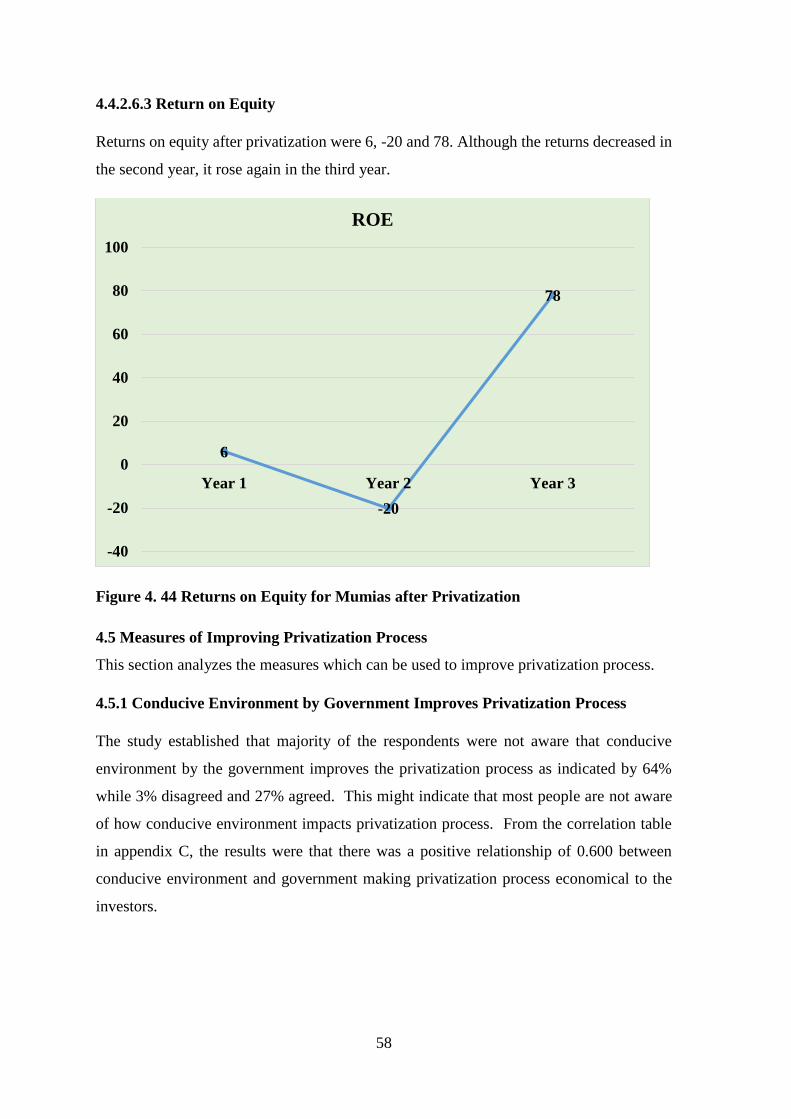

Figure 4. 43 Returns on Total Assets for Mumias after Privatization ............................... 57

Figure 4. 44 Returns on Equity for Mumias after Privatization ........................................ 58

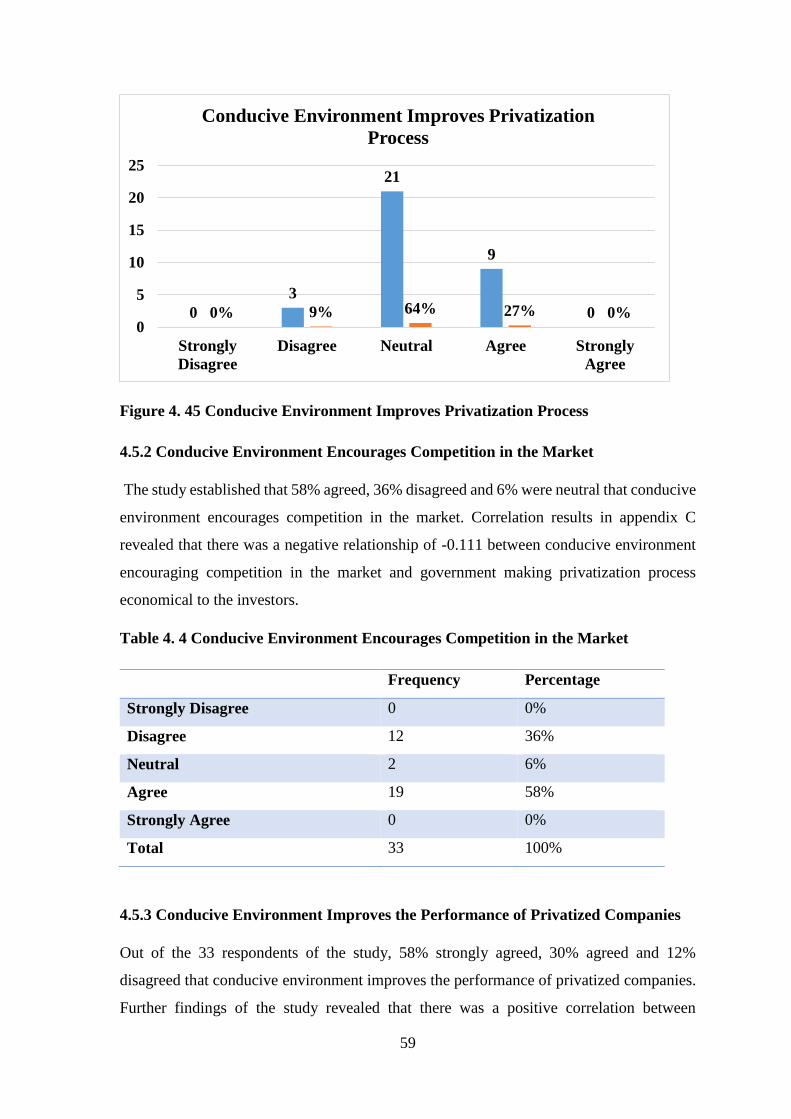

Figure 4. 45 Conducive Environment Improves Privatization Process ............................. 59

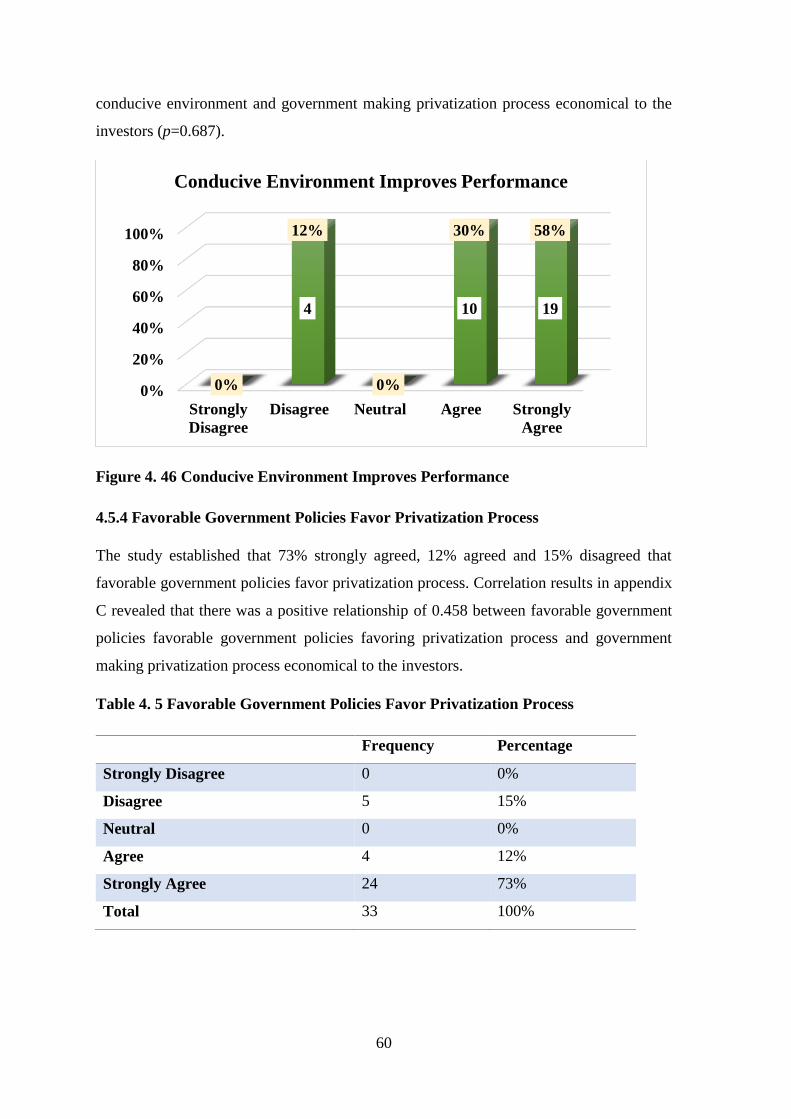

Figure 4. 46 Conducive Environment Improves Performance .......................................... 60

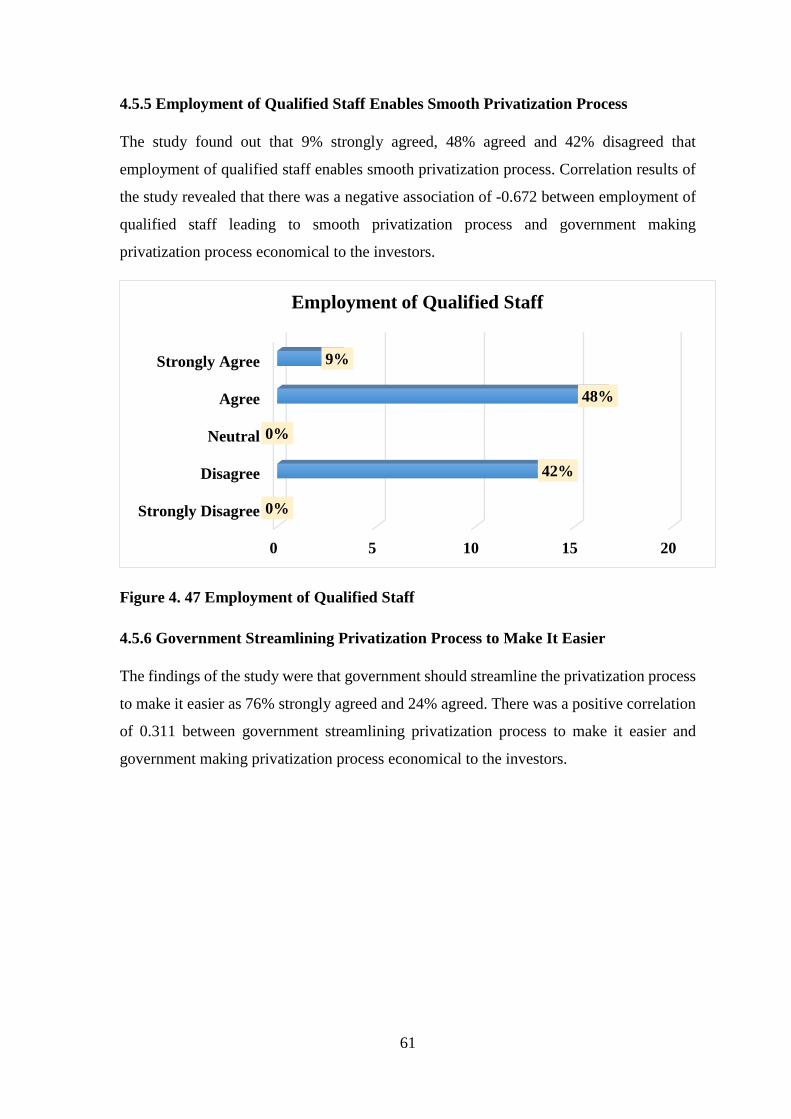

Figure 4. 47 Employment of Qualified Staff ..................................................................... 61

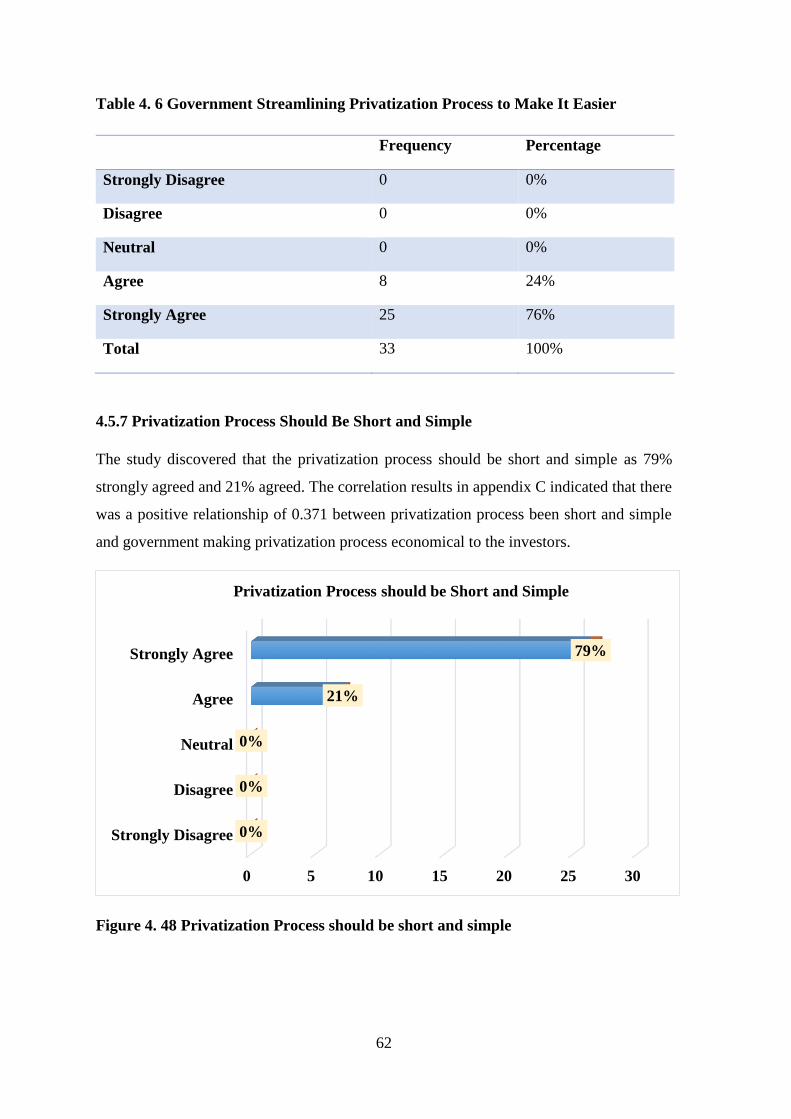

Figure 4. 48 Privatization Process should be short and simple.......................................... 62

xiii

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

Privatization is the act of reducing the responsibility of the government and increasing the

responsibility of the private sector in an activity or in the ownership of the states (Osman,

2014). According to Mercille and Murphy (2017) privatization is the political context in

which there is shift of activities of functions from the state to the private sector or transfer

of production of goods and services from public sector to private. The privatization of state-

owned enterprises (SOEs) has become a common process all over the world and was

considered a major component of the New Public Management (Bachiller, 2017).

Privatization, began in 1979 in the UK and spread to European and developing countries in

South America, Asia and Africa alike, has become a major economic phenomenon in recent

decades (Alipour, 2013).

Privatization of state-owned enterprises is considered one of the most important changes in

the structure of the capital market .However, SOEs lack essential efficiency and this can be

improved by the privatization process. The main importance of privatization is to offer

room for competition, develop the market system, and advance the performance of private

businesses. A Study done in UK about impact of privatization on firm performance found

out that companies privatized by public offerings obtain a better performance than

companies privatized using other methods, such as private sale or voucher privatization,

and do not support the common-place assumption that privatization in developing countries

does not improve financial performance (Bachiller, 2017).

Europe is under privatization trend which began in the 1970s in Britain and most of the

other European countries have realized the exceptional benefits which privatization

provides (Wright, 2015). Government can privatize its state owned corporations through

sale of shares where the government sells its shares through public flotation, pre-emptive

rights, competitive sale and sale of assets through open tenders, direct sale, public auction

and liquidation of assets (Lesorogol, 2010). The government can also privatize through

management buyouts and employee buyouts, equity dilutions, transfer of assets and shares,

joint ventures, restitutions and management contracts (Makokha, 2013). Over the last

decade, privatization has become a common phenomenon in the developing countries

2

whereby SOE`s are being privatized at an increasing percentage (Mercille and Murphy,

2017).

Privatization became common in the developing and transition countries due to the debt

crisis which emerged in 1981 to 1982 (Lieberman, 2007). Developing countries were

unable to continue absorbing the fiscal burden of their State Owned Enterprises.

Ramamurti (2016) argued that privatization increases government cash flows by reducing

subsidies and capital infusions to SOE`s, refining resource deployment, improving profits

and encouraging common capitalism through possession of shares. Privatization also

confines power of trade unions in the public sector, reallocates incomes and rents within

the society, satisfies foreign donors through decreasing of government`s role in the

economy and specifically improving effectiveness and the performance of SOE`s based on

the basis that the private sector performs well compared to the public sector (Schiffler,

2015).

According to Chari (2015), privatization began in the 1990`s in Kenya immediately after

modification by International Monetary Fund (IMF) in 1980`s on Sub Saharan African

countries. The International Monetary Fund conditions for African countries were to assist

in evaluating credit and support in funds (Lurie, 2018). African countries encouraged

privatization to take advantage of the conditions given by IMF. In 1992, the Kenyan

government wrote a paper which defined the policies and guidelines for privatization of

public companies in Kenya. In 1994, the Kenyan government came up with a committee to

supervise the process of privatization (Otieno, 2015). In the year 2002, the Kenyan

government committed itself with the privatization process of Kenya Commercial Bank,

Telkom Kenya and Kenya Rail ways.

Since privatization was introduced in Kenya, company like Kenya Airways has improved

in terms of efficiency and increased profits. Boehmer, Nash and Netter (2005), concluded

that empirical research reveals that private owned companies are more efficient and

profitable compared to the public owned companies. There is that assumption that

privatization generates enough funds and operate efficiently after privatization. Profits from

private owned companies are used to repay the public debt and this has led to high rate of

disassociation of public owned companies from production of goods and services

(Boubakri, Cosset & Guedhami, 2005). Privatizations pressurizes managers to pay close

attention in achieving the goals and objectives of the company as they are under private

3

ownership and the management is always responsible to the shareholders wealth (Crowder,

2012).

In privatization, control rights and cash flow rights are transferred from politicians to the

managers of the company. Privatization changes the role of government to provision of

social and economic services in an efficient manner (Michigan, 2001). After privatization,

firms employ their own human resources, financial resources and information technology

resources efficiently so as to improve the profits of the company (Lurie, 2018). After

privatization, the sales revenue are expected to rise as the company is able to offer fair

incentives, more access to financing opportunities and great entrepreneurial initiatives. A

study done by Shiffer (2018) in Israel about the impact of privatization in public companies

established that debts in the capital structure decreased as the cost of borrowing increased

and the companies were able to access public equity markets.

After the privatization process takes place, bankruptcy costs are removed to the newly

privatized firm and therefore this leads to reduced debts (Bachiller, 2017). Most of the

public owned companies experience the problem of over-staffing and after privatization,

the level of employment decreases as the private company is no longer able to receive

government subsidies. However, a newly-privatized company productivity increases and

also the employees income is improved (Worsnop, 1992). With privatization, the policies

allows more firms to present their products in the market and therefore increasing

competition in the market (Lurie, 2018). Most firms consider the aggressiveness to enter

into the competitive markets and increasing risk taking to develop new services, products

and processes (Zarei, Amanati, & Amanati, 2017) .It is through this competition whereby

efficiency is improved. On the other hand competition in the market is also influenced by

the nature of the industry (Ohemeng & Grant, 2008). Through the selling of shares to the

stock market, government raises revenue and therefore provides better services to the public

(Fungacova & Hanousek, 2006).

Financial performance is the measure of the financial health of a company after a period of

time and can be used for comparison for companies in the same industry or for comparing

different industries (Association of Accounting Technicians, 2013). According to Libby,

Short, Kanaan and Sterling (2017), financial performance are the outcomes of the company

policies and operations in monetary value. Financial performance of the company is

indicated by return on assets, return on investment and return on sales among others.

4

Financial performance can be measured using profitability ratios, Activity ratios, Liquidity

Ratios, shareholder ratios, turnover ratios and solvency ratios (Penning, 2012). Liquidity

ratios measure the ability of the company to meet its short term obligations within the

specified period (Tullio & Wolters, 2004). Shareholder ratios predicts or forecast the

interest of the shareholders and check if they are satisfied. Activity ratios measures if the

assets of the company are effectively and efficiently used by the management.

Kenya is the best performing economy in East Africa and has been privatizing its

companies in order to stay competitive in the market (Anyang'Nyong'o, 2000).

Privatization has been ehnannced in kenya by having a simple privatization process,

engagement of both parties in the privatization process and sensitizing the general ublic on

its importance to the economy. Privatization commission in Kenya helps the government

in privatization through the sale of shares (McGuckin & Dougherty, 2002). Some the

government companies proposed for the privatization include Western sugar companies

like Chemelil sugar company, Nzoia Sugar Company Limited, South Nyanza Sugar

Company Limited, Muhoroni Sugar Company and Miwani Sugar Company (Sammy,

2004). The government affirmed to sell 51% shareholding in each of these companies to

strategic investors and 24%to be sold to employees while the rest to be sold to Kenyan

farmers and members of the public. Although privatization has for some years led to

retrenchment of employees, it has had a great impact to the economic growth of Kenya.

Privatization has also led to the improved performance of the government firms which were

initially performing poorly.

Other companies privatized in Kenya include Kenya Wine Agencies, Kenya Ports

Authority, National Bank of Kenya, Kenya Meat Commission, Kenya Pipeline Company

Limited, New Kenya Co-operative Creameries Limited and Agro Chemical and Food

Company (Debrah & Toroitich, 2005). A good example of successful privatization is

Kenya Airways. It was the first to be privatized in African Airline industry. The whole

process of privatization of Kenya Airways took two years whereby 77% of the shares were

sold to private investors. In the year 1987 to 1996 the company was generating losses due

to the inefficiency in operation. Since 1996 the company has been reporting some profits.

In 2014, Kenyan government invited investors to help in the operations in Eldoret

Container Terminal, construct the new Kipevu Terminal and develop berths 11, 12, 13 and

14 at a cost of US$1.5 billion. Privatization of Kenya Ports Authority was aimed at

5

consolidating East Africa’s biggest sea port as neighboring Eritrea, Djibouti and Tanzania

scaled up efforts to expand their ports.

1.2 Statement of the Problem

Privatization has become an important part of the public policy in the developing countries

since 1980`s. The main aim of the government to encourage privatization to improve

efficiency in the State Owned Firms, reduce the budget of state owned firms and to capital

markets more vibrant. There has been increased privatization of government firms in recent

past and it has become a very widespread phenomenon. This has created a mixed reactions

on the players as to the outcome of this acquisitions. There has been a number of studies

both here in Kenya and the world at large where there has been no agreement as to whether

privatization improve the financial performance of a firm or not. There are studies that have

shown that the financial performance of privatized firms have improved there after

acquisition ( Kithinji, 2007: Azhagaiah and Kumar 2011: Korir, 2006: Ramaswany and

Waegelein, 2003). On the other hand there has been some studies that have point out that

the privatized firms do not have any financial benefits to them (Ndura, 2010). The firm

been privatized in most cases in the short run have its stakeholders get good returns. The

shareholders in the privatized firms on the other hand may have some undervalued share

price in the short run but with no overall wealth gains. There is also decreased EPS by the

privatized firm due to reduced earnings.

After privatization of Kenya Airways, the company realized a gross profit of KES.237,

204,000 from an earlier gross loss of KES.53, 867,000 in the year 1992. For the year ended

December 1994, earnings per share increased from -1.11 to -0.09 in 1993. Return on

investment rose from -0.103 to -0.007 between 1989 to 1998. A study carried out in Kenya,

70% of the respondents believed that efficiency in the public sector improved after

privatization, 20% indicated that expenditure in the public sector reduced after privatization

and 3% held the believe that privatization assisted the former public firms to operate on the

heart of market principles, operational independence and the improvement of

accountability (Augustyniak, Brooks, Rinaldo, Bogner, & Hodges, 2009). A study done to

evaluate the effect of organizational change and privatization on the performance of state-

owned enterprises (SOEs) using the data from Iranian firms during the period 1998-2006,

and to test whether privatization leads to improved performance (Alipour, 2013).

The performance of these firms before and after privatization was examined. The results

6

show that privatization had no positive effect on the profitability of the firms listed on the

Tehran Stock Exchange; rather, the effect was negative.

Empirically, studies have found conflicting results of financial performance before and

after privatization. Due to the above varying results, the question of the impact of

privatization on the performance of firms remains pertinent. This study aimed to close the

gap and give a clear picture on the impact of privatization on the performance of firms.

1.3 Purpose of the Study

The main purpose of the study was to establish the impact of privatization on the financial

performance of government firms in Kenya

1.4 Research Objectives

The research objectives of the study were:

1.4.1 What Is the Performance of Firms before Privatization?

1.4.2 What Is the Performance of Firms after Privatization?

1.4.3 What are t Measures of Improving Privatization Process?

1.5. Importance of the Study

1.5.1 Public Companies

Public companies were able to understand the benefits associated with privatization and the

process involved. They were also in a position to weigh the benefits and disadvantages of

privatization and come up with the best solution.

1.5.2 Researchers

The study was of great benefit to the researchers as they were able to understand better the

meaning of privatization, the challenges involved and also the benefits. In addition they

were in a position to advice the government on the best move to take in regards to

privatization.

1.5.3 Financial managers

Financial managers of public companies were able to understand the benefits of

privatization and were in a position to convince the government to convert from public

owned companies to private own companies.

7

1.5.4 Investors

Foreign and domestic investors gained knowledge about privatization and therefore knew

better whether to invest in public owned companies or private companies. It is only through

this research whereby they were able to make wise decisions concerning investments.

1.5.5 Business People

This study enabled business people to get a clear understanding of privatization and how it

can affect the performance of the businesses. From this study business people were able to

know if carry out business with private company or private owned companies.

1.6 Scope of the Study

The study was carried out in privatized government firms in Kenya. This study was limited

to the importance of privatization of government firms on financial performance,

performance of government firms before and after privatization and Measures of Improving

Privatization Process. The study was carried out between August 2018 to December 2019.

1.7 Definition of Terms

1.7.1 Privatization

Privatization is the process of transferring an enterprise or industry from the public sector

to the private sector (Crowder, 2012). This leads to a reduced scope, limits the functions

and weakens the influence of government on the operations of the privatized company. In

this study privatization refers to the possession of public firms by private firms or investors.

1.7.2 Firm

A firm is a business organization, such as a corporation, limited liability company or

partnership, which sells goods or services to make a profit (Lesorogol, 2010). A firm can

be a corporation, Limited Liability Company, public limited company, partnership business

or a sole proprietor business which has either products or services for sale. In this study, a

firm refers to the government companies who desire to privatize.

1.7.3 International Monetary Fund (IMF)

The International Monetary Fund (IMF) is an international organization created for the

purpose of standardizing global financial relations and exchange rates. The IMF generally

8

monitors the global economy, and its core goal is to economically strengthen its member

countries. (International Monetary Fund & International Monetary Fund, 2014).

1.7.4 Financial Performance

Financial performance is the measure of financial health of a firm after a period of time and

can be used for comparison for companies in the same industry or for comparing different

industries (Association of Accounting Technicians, 2013). In this study, financial

performance refers to the financial health of the firm.

1.7.5 Efficiency

Comparison of what is actually produced or performed with what can be achieved with the

same consumption of resources (Chen, 2017). Efficient firms are capable of maximizing

outputs from the available resources while at the same time minimizing the costs.

Therefore, it means that firms can improve efficiency by cost reduction.

1.8 Chapter Summary

Chapter one has described the background of the study, specific objectives, and statement

problem. The introduction and background of the study has reviewed the benefits of

privatization and different types of privatization in the world. The scope of the study has

been outlined with the aim of investigating impact of privatization of government firms in

regards to the importance, challenges and measure of improving privatization in

government firms Performance of before and after Privatization and the Measures of

Improving Privatization Process. The importance of the study has also been identified and

the definition of words as well. Chapter two reviews literature review based on the three

research questions: what is the Performance of Firms before Privatization? What is the

Performance of Firms after Privatization? What are Measures of Improving Privatization

Process?. Chapter two covers literature review, chapter three research methodology,

chapter four analyses results and findings of the study and chapter five covers discussion,

conclusions and recommendations of the study.

9

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

This chapter reviews literature on the effect of privatization on the financial performance

of government firms. The literature discusses the Performance of Firms before

Privatization, Performance of Firms after Privatization, The Measures of Improving

Privatization Process.

2.2 Performance of Firms before Privatization

Improved performance of privatized firms cannot be taken for granted merely by

ownership change. Privatization must be accompanied by other economic adjustments such

as adjustment of the capital market and formulation of corporate rules and regulations

(Bachiller, 2017). A study done to evaluate the effect of organizational change

and privatization on the performance of state-owned enterprises (SOEs) using the data

from Iranian firms during the period 1998-2006, and to test whether privatization leads to

improved performance (Alipour,2013).The performance of these firms before and

after privatization was examined. The results show that privatization had no positive effect

on the profitability of the firms listed on the Tehran Stock Exchange; rather, the effect was

negative. Moreover, the results revealed that privatization of these firms has had no effect

on their sales effectiveness and efficiency; instead, the debts and risks of these firms has

increased.

2.2.1 Profits

Privatization usually affects the profits generated. Many studies have been done about

privatization and found out that privatization usually improve the profitability of a company

resulting from proper management. Bachiller (2017) argued that companies privatized by

public offerings obtain a better performance than companies privatized using other

methods, such as private sale or voucher privatization, and do not support the assumption

that privatization in developing countries does not improve financial performance . A study

by Astami, Tower, Rusmin, and Neilson, (2010) to investigate whether partially privatized

companies perform significantly better than fully public owned companies in the

developing country of Indonesia found out that private owned companies had higher levels

10

of performance than those fully owned by the government. The study also established that

there were significant differences in financial leverage, firm size, assets‐in‐place, financial

statement reliability, and industry variances between private companies and public owned

companies.

2.2.2 Liquidity

Liquidity is the ability of a company to pay its short term obligations (Bachiller, 2017).

Liquidity ratio usually evaluates the incurred liabilities of a company and the assets it has

to cover them. Example of liquidity ratio is the current ration which is calculated by

dividing current assets by the current liabilities. Privatization improves the liquidity of the

company. When the company is public owned, the government is always liable for the debts

and therefore the managers don’t mind whether the company performs well or not (Clark,

Munro, & Sumaila, 2010). This is what explains well the difference between balance sheet

of public and private owned companies. Private companies have high levels of liquidity

compared to public companies (Vo, Swierczek, & Nguyen, 2013).

A research done by Huang, Watson and Chen (2013), to investigate the relationship

between privatization and share market capitalization, liquidity and share ownership found

out that privatizations considerably increased share market capitalization and had impact

on the market liquidity. In general, anyone investing in privatized companies' portfolios

should receive higher returns than investing in public company`s portfolio (Kerr & Qiu,

2007). As the managers of privately owned companies are more focused than those of

private companies, the liquidity ratio increases as they are accountable for anything which

transpires in the company (Arcas & Bachiller, 2010). A study done to analyze how

privatization influenced corporate culture and employee wellbeing in the privatized

companies revealed that although, the employees were pressurized in private companies,

privatization prepared them to a change in corporate culture and also reduce work place

stress. In addition, corporate culture changed the employees towards a greater emphasis on

performance and people orientation and on organizational integration (Cunha & Cooper,

2002).

2.2.3 Efficiency in Operations

Efficiency in firms operations results from good management of the firm. Most public

companies suffer from inefficiency due to poor management. Bachiller (2009) did a

11

research on the impact of privatization on the efficiency of five of the biggest Spanish state‐

owned companies and found out that the improvements in efficiency were related to the

privatization. Public owned firms faced challenges of inefficiency in operations and

therefore decreased profits and the government of Malaysia decided to privatize those firms

and by the end of two years the companies started yielding profits (Linz & Rakhovsky,

2011). Another study by Hidalgo-Gallego, Román and Núñez-Sánchez (2017) about

Allocative Efficiency in Airports for a Pre-Privatization Period found out that in the initial

period, when the government encouraged decentralized management of airports and

privatization of the largest airports, allocative efficiency improved from 2009 to 2012. In

addition, during the second period when the government focused on centralized airport

management and privatization of the system as a whole from 2012 to 2014, inefficiencies

slightly increased again.

Ownership of company greatly influences the performance of a company. A study done to

examine the effects of ownership on companies` performance in Malaysia revealed that

private owned companies performed better than government owned companies due to

efficiency in operations (Fauzi & Musallam, 2015). A study done by Tiemann and

Schreyögg (2012) about Changes in hospital efficiency after privatization found out that

the efficiency gains after a conversion to private for-profit status were achieved through

substantial decreases in staffing ratios in all analyzed staff categories with the exception of

physicians and administrative staff. Type of ownership can affect efficiency of operations

in companies. Arocena and Oliveros (2012) did a research to establish if the type of

ownership makes any difference in the efficiency of firms. The study found out that the

efficiency of newly privatized firms significantly increased after their privatization, while

private competitors showed no significant improvement during the same post-privatization

period.

2.2.4 Company Leverage

Leverage is the ability of the firm to meet its obligations whether long term or short term

(Hutton et al., 2012). It gives an overview on how likely the company will be able to meet

its obligations. It usually gives an overview of the relationship between finances provided

by owners of the company and the ones provided by the creditors of that company

(Paramasivan & Subramanian, 2009). Privatization of companies leads to decreased debts

because the government will not be liable again. A study done in large US companies to

12

investigate their capital structures established that private firm capital structure is not

measured by leverage but also the issuance of specific debt instruments (Adrian &

Boyarchenko, 2018). Leverage, debt type usage, and debt specialization are dynamic and

strongly related to observable firm characteristics and industry characteristics are strong

determinants of leverage levels and debt specialization (McCumber, 2015).

Relationship of employees and management of company also influences the level of

leverage. A research by Wieland and Flavel (2015), to investigate the relationship between

employee orientation and both financial performance and leverage found out that

investments in employee-orientated activities, such as career opportunities, and secondary

benefits and work–life balance, lead to improved financial performance. A study done by

Ims and Seiffert (2015) on the effects of post-privatization government divestments on the

financial and operating performance of state owned enterprises in Scandinavia found out

that Leverage levels increased, while capital investment, dividend payouts and employment

levels decrease as the state divested its shares.

2.2.5 Dividend Payout

Dividend in private companies increase because investors demand their dividend payments

to be paid and this therefore improves concentration of managers and their employees

(Ohemeng & Grant, 2008). Newly privatized firms increase dividends and also pay

significantly higher dividends compared to public firms. A study done across 26 in US

countries showed that the dividend premium is significantly positively related to new

agency costs induced by privatization and is associated with levels of increased operating

efficiency and higher earnings (Baker, Chang, Dutta, & Saadi, 2012).

Private companies usually pay dividends so as to maintain Return on Equity (ROE) rather

than accumulating excess assets in the company (McCumber, 2015). Accumulation of

excess assets dampens returns for all owners, so dividends help shareholders with current

returns and the maintenance of acceptable returns going forward. A study done at

Australian firms revealed that returns tend to be large if no dividends are paid and then

decrease with the dividend payout ratio (Li, 2016). Another study in China found out that

momentum profit is the largest for the stocks that do not make dividend payment but appear

similar for the stocks that pay dividends and that stock momentum tends to be much

stronger than value stock momentum and no dividend stock momentum beats dividend

stock momentum (Zhang, 2013).

13

Another reason why private companies pay dividends is to provide shareholders with

regular returns. The most important determinants of a firm’s dividend policy are the level

of current earnings, stability of earnings, and needs of current shareholders (Baker &

Jabbouri, 2016). A study done to investigate the factors influencing dividend policy,

dividend issues, and explanations for paying dividends in Moroccan firms and those of

USA, Canadian, Indonesian, and Indian firms found out that dividend policy affects firm

value Managers viewed multiple theories including signaling, agency, catering, and life

cycle explanations as credible and contribute in explaining why their firms pay dividends

(Anastassiou, 2017).

2.3. Performance of Firms after Privatization

2.3.1 Profits

Few studies have examined the functioning and financial performance of freshly privatized

corporations in developing countries. A study done by Alipour (2013) to evaluate the gains

or losses resulting from the privatization of 12 firms operating mostly in non-competitive

marketplaces in 4 countries which included Chile, Malaysia, Mexico and United Kingdom.

They found net welfare gains in 11 of the 12 cases. Productivity improved in 9 of the 12

cases and stayed unchanged in the other three. The study established that no case in which

employees lost completely from privatization. They appealed that the results offered

evidence in sustenance of net welfare gains even when they strained to isolate the effect of

privatization from the effects of other factors like changes in market structures and in

macroeconomic situations.

In contrast, a done by study by Arcas and Bachiller (2010) to compare the pre- and post-

privatization financial and operating performance for 61 companies from 18 countries over

the period between 1961 and 1990 found out that there was a prove or evidence that, after

privatization, the firms became more profitable, improved their real sales and their

investment expenditure and enhanced their operating efficiency. In addition, the firms

significantly decreased their debt levels and improved dividend payments. More

unexpectedly, they found that no proof that employment levels decreased after

privatization. As an alternative, they reported a growth in the mean and median

employment and they discovered that 64 percent of the companies hired more workers after

privatization. Privatization of public companies makes the managers to be focused on

creating more profits as they are the ones responsible to the shareholders in case the

14

company makes losses (Winston, 2010). A study done to investigate the effect of

privatization on corporate entrepreneurship in Telecommunication Company of Iran found

out that after privatization, the company acts more entrepreneurially and becomes

aggressive in competition through entering competitive markets and increasing risk taking

to develop new services, products and processes (Zarei, Amanati, & Amanati, 2017).

Government owned firms comprise of a large and speedily growing sector of the economy

in most of the countries in the world (Obadan, 2008). He further argued that there are many

reasons which included organizing industrialization in the countries with small sacle

industries, promotion of industries seemed to be of importance, creation of lines of tasks

with inadequate incentives for private investments, establishments of projects which need

large amounts of capital, unable to raise privately in the current structure of capital markets,

securing of the threatened jobs, prevention of foreign firms, expansion of the public sector,

raising of more capital for the government, elimination of monopoly power over strategic

firms, reduction of prices of goods and services especially for the poor customers and for

other political or social reasons.

2.3.2 Operational Efficiency

Chari (2015) did a study in 75 newly privatized companies in 21 developing countries that

experienced full or partial privatization between 1980 and 1992. The study compared

operating efficiency, capital investment, actual sales, entire employment and dividends.

Furthermore they used both raw and market accustomed performance measures so as to

segregate the effect of privatization from the effect of macroeconomic changes on the

financial and operating performance of government owned firms. Performance of

government owned firms had been poor as observed by (Augustyniak, Brooks, Rinaldo,

Bogner, & Hodges, 2015). Specifically, financial rates of return had been generally lower

for government enterprises compared to the private sector, financial profitability of the

firms had been affected by price controls, government firms had over and over again put

large burdens on government budgets, government firms influenced the intensification of

the external debt in most developing countries and countries in which government firms

accounted for higher shares of gross domestic investment which led to lower rates of

economic growth (Wieland & Flavel, 2015).

According Domney, Wilson and Chen (2015), several reasons led to the poor performance

of government firms and one of the reasons was lack of incentives to the management.

15

Some countries used performance bonuses or sharing of profits to motivate the top

management. Other countries managers were made to be part of the civil service so that

they can work hard. Even where they were not part of profit sharing and being part of the

civil service, their pay was lower compared to the one of private sector (Maude, 2014).

Despite the prestige and difficulty of managing what were often the biggest corporations in

the country, would occasionally reimburse for lower pay, low salaries tended to discourage

experienced managers and therefore increased employee turnover (Crump, 2011).

Lesorogol (2010) did a study to compare pre- and post-privatization financial and operating

performance of 85 companies in the period between 1990 to 1996. The study compared

output, operating efficiency and dividend payments. The findings of the study were that

profits, outputs, operating efficiency and dividend payments increased significantly and

leverage ratios decreased immediately after privatization. Shortage of skilled managers was

another cause for the poor performance in government firms as observed by (Baggiarini,

2015). He argued that the increasing number of government firms in most of Sub-Saharan

African and other countries, led to a chronic deficiency of management. This shortage was

sometimes worsened by program for speedy indigenization. Majority of senior posts were

left vacant and filled by unqualified employees. The organization therefore became too

reliant on its principal executive. The shortage of managers also led to a high rate of

employee turnover as experienced people were shifted around to lead the disturbed

government firms (Bjørnskov and Potrafke, 2011). In addition, the countries who had

shortage of managers changed the managers of state owned firms with damaging frequency

as the selection of top management was based on nepotism and political patronage.

2.3.3 Industry Competition

The other reason for poor performance of government owned firms was due to lack of

competition in the industry. According to Bortolotti and Siniscalco (2014), many

government firms were monopolies producing goods and services that were never traded

globally or that the government desired to manufacture domestically for national security

purposes. In other cases the economy was very small to maintain another domestic

manufacturer. Similarly, managers were not given preference to respond to competitive

pressures which would mean decreasing staff or termination loss-making service (Chari,

2015). Libby, Libby, Short, Kanaan and Sterling (2017) found insignificant changes in the

capital expenditures to sales measures in the post privatization. The study concluded that

16

privatization improved the financial and operating performance of freshly divested firms

and these improvements were the outcomes of socially advantageous perfections in

production efficiency and entrepreneurial effort and that privatization worked in a wide

variety of countries, industries and competitive environments.

An additional contribution to poor performance Mládek (1997) noted, that there was the

little weight put on profitability and efficiency by governments. The government firms were

not instructed to optimize profits or even to decrease costs since fine-tuning administered

prices typically comprised of practical and political difficulties. Additionally, government

owned firms were frequently required to perform non-commercial activities such as

employing extra staff to increase employment in a specific area to improve regional

development to achieve diversification. These contradictory goals often decreased profits

(Ohemeng & Grant, 2008).

According to United States, Hanford Site Wash, United States, Kelly and Fh (2014), only

a few countries made use of organized public pressure as a method of improving the

efficiency of government firms. Governments firms rarely took an action to eradicate

inefficient managers of these firms. Additionally, governments were hardly prepared to use

the authorization of liquidation. This lack of operational accountability led to poor

performance by the government firms. Different government agencies interfered with

government enterprises decisions that were a privilege to the management (Haugen &

Musser, 2011). Also, the management failed to coordinate their actions as they had no

control over them. Policy that fluctuated between autonomy and central control could

prevent intelligible direction of government firms. Many efforts to reduce illogical

interference by government had become counterproductive, replacing one form of

bureaucratic involvement for another.

2.3.4 Internal Management Systems

In many developing countries the internal management information systems of government

firms were lacking or non-existent, noted World Bank (1991). The companies were not

audited according to uniform standards. This was due to lack of a trained body practitioners

and qualified accountants as well as lack of active plans designed to focus efforts on

improving efficiency and monitoring results. Government firms were frequently expected

to contribute to the wide-range goals of government policy. The outcomes could be

perverse. For instance, public enterprises' prices could be controlled to benefit the poor or

17

to assist counter-inflationary policies. But these firms' consumers were often large

industrial users or wealthy people, so they did not benefit the poor most. It is estimated that

three-quarters of the energy and food subsidies in Egypt went to the relatively more affluent

urban areas and about two-thirds of these went to the richer half of the urban population,

observed World Bank.

According to Kay et al., (1986) the main goals of privatization could be summarized

therefore: the reduction of the state sector; promotion of wide share ownership; greater

efficiency within privatized entities, coupled with profit motivated decisions; raising

revenue for the government; reduced government interference, increasing speed of decision

making; introduction or enhancement of competition; exposure to the disciplines and

opportunities of private sector markets for capital and other resources. These objectives

needed not be equally important for all state-owned enterprises. Also, these goals were not

mutually exclusive. Obviously, the government in each country needed to consider local

factors and individual industry circumstances in determining the mix of goals (In Merino,

2014).

2.4. Measures of Improving Privatization Process

2.4.1 Conducive Environment

Government should provide Conducive environment to encourage competition. New

Zealand, Britain, Mexico, and Chile have been successful privateers and the reason behind

their success was that their governments provided Conducive environment which

encouraged competition (Naito, 2013). Another example of successful privatization is in

Chille as the efficiency of operations improved. In the implementation of privatization in

Chille, it first sold the public companies to the large banks. The banks subjected themselves

to risks by giving loans to their own companies when Chille suffered a crisis almost the

same as United States savings and loan crisis. Privatization works well when the programs

are put in place to create an environment which improves efficiency (Haugen & Musser,

2011). Programs may include encouragement of competition through export, price reforms,

regulatory reforms safeguarding competition by removing obstacles to private entry and

exit; and legal reforms assuring proper disclosure, enforcement of contracts, and due

process.

Improved performance of private companies is not effective enough unless other factors

like regulations are considered (Haugen & Musser, 2011). A study at china found out that,

18

Performance improvement of privatized firms cannot be taken for granted merely by

ownership change; instead, the performance gains of privatization could be realized only

in concert with other institutional arrangements, including market openness, the modest

and short‐term bureaucratic control after privatization, and corporate health prior to

privatization (Wu, 2007). For a firm too compete in the global economy, they must become

more efficient, more flexible and, above all, more customer‐oriented (Chaurasia, Garg, &

Agarwal, 2016). The competitive edge of firms is determined not only by their own

strategic choices, but also by what their respective governments do in terms of providing a

supportive infrastructure that helps them compete (Halachmi, 2002).

2.4.2 Government Policies

Government policies should be in a position to favor private companies .They should be

free from political interference and should be handled by specialized professionals with a

full knowledge of how public sectors reform. Government interventions lead inevitably to

both cooperation and conflict with the private sector (Lam, 2016). After privatization it is

very important for the government to ensure that the personnel of the privatized companies

are well trained to ensure efficient management. Privatization process can be better only if

the procedures are not many and few requirements are needed. Mexico successfully sold

its public companies with only seven people carrying out the transactions (Lam, 2016).

Instead of relying on Mexican banks and international banks, the decision making was done

by the seven people while the cabinet secretary acted as government`s watchdog. Mexican

process of privatization was centralized and transparency was exercised and everything was

explained well on how and why the privatization was done. Determining the value of a

public company is usually very difficult and that is why government engages an expert to

give an advice (Naito, 2013). Even in developed countries like Canada face the challenge

of assessing the value of their public companies even after engaging experts

2.4.3 Long Privatization Process

Privatization process in Kenya is usually very long. A good example is the case of the five

government owned sugar factories in Kenya. These factories were embarked on

privatization program and approved by cabinet in the year 2008 and debts written off by

parliament. The purpose of privatization was to transform the industry towards commercial

orientation and injection of new capital from the private investors. However, the

Parliamentary Departmental Committee on Finance, Planning and Trade passed a

19

resolution on 9th January, 2013 “that the privatization of the public Sector Sugar

Companies should be postponed until such a time when all legislation affecting the

Agriculture Sector (sugar) and the County Governments have been put in place”. In order

to kick start the privatization process, the approval of the Parliamentary Committee on

Finance, Planning and Trade is required. The process is already 9 years old since the

privatization began and this can lower the demand of the private investors.

Arcas and Bachiller (2010) argued that governments are good in streamlining firms before

privatization by enhancing the trustworthiness of the process. This trustworthiness view is

important in face of the huge political costs of labor streamlining (Arocena & Oliveros,

2012). This is because willingness to overcome worker resistance may be understood as an

indicator of commitment to change. Another view that supports preceding streamlining is

the social view whereby any social costs of streamlining, particularly labor-related

streamlining, may be solved adequately by governments. For example, by guaranteeing

payment of severance obligations and social safety net measures. Public sector may be in a

better position to bargain with the unions if the government has mechanisms to assist the

retrenched employees. The government can do so by re-educating employees, helping

employees to look for new jobs and paying good compensation (Baggiarini, 2015).

The government should make the public companies more attractive to the buyers so that

they can sell at a good price and investors to be happy to invest in a well-managed entity.

This can be achieved by eliminating debts from the company`s balance sheet (Chaurasia,

Garg, & Agarwal, 2016). Liabilities such as pension funds, claims for environmental

damage, are greater deterrents to privatization due to the inestimable scope of these

liabilities. Removal of these liabilities can be an added advantage to the company.

Government should try to retrench ghost workers and unproductive workers before

privatization (Spearin, 2005). Many buyers usually shy away from the public companies

where they must layoff some employees. Despite that unemployment can result from

privatization, it should not be seen as the bad side of privatization as it helps in cutting the

operational costs and therefore increased profits (Lam, 2016).

2.4.4 Compensation Benefits

When a public function is privatized the employees get paid less and lose benefits, but other

state agencies pick up the costs that occur when people get paid less. Private Managers and

executives get a big chunk of the savings and then there are the costs to the larger economy

20

from ever more people making less and less (Spearin, 2005). Government should prepare

employees for privatization by treating them fairly. Governments usually have programs to

compensate employees for job loss (Chaurasia, Garg, & Agarwal, 2016). These programs

include working within the rate of natural attrition, encouraging or requiring first

consideration by contractors, offering early retirement incentives and allowing public

departments to bid for contracts (Richardson, 1991).

The privatization program is likely to come under fire from various sections of the

community who may challenge the principle of transferring assets out of state control and

criticize the methods and terms of individual sales (Mahmoud, 2012). The government

should embark on a vigorous debate and educational programs focusing on the credible

reasons for privatization such as capital requirements and efficiency argument while

resolving the emotional and political rhetoric regarding Public ownership by offering shares

widely to the public (Lurie, 2018).

An important feature of a successful public offering is that the enterprise under offer must

be observed to be an attractive investment to the public (Alipour, 2013). As such, major

privatizations are no different from other major stock market floatation's and apart from the

special consideration of dealing with the government as a client, there are no fundamentally

different criteria for a privatization issue; the vendor and his advisor will be obliged to

follow the full requirements of securities legislation Profitability is a key criterion in an

assessment of a company suitability for a stock market floatation. In circumstances where

the government wishes to sell off operations which do not meet acceptable standards of

profitability, it may decide to make sale by private tender or by direct negotiation (Adrian

& Boyarchenko, 2018).

The privatization program would not succeed unless the directors of the enterprises not

only supporting the privatization approach in principle, but are also effective in selling the

investment to prospective shareholders (Bachiller, 2017). Since it is often the case that

public companies are run by representatives from political pressure groups rather than a

well-balanced group of directors drawn from the variety of skill bases demanded of a

typical successful company, the board of directors of these enterprises may need expanding

and be of sufficient standing. This is in order to give comfort and confidence to the in

vesting public, endorse the valuation and provide ongoing protection to the investors of the

new shareholders (Chari, 2015). In addition, the management team should be fully prepared

21

for the changes that follow from being in the private sector particularly for those companies

that are floated on the stock exchange. Management of companies being privatized would

be required to devote a substantial proportion of its time and effort in preparation for

privatization.

2.5. Chapter Summary

This chapter has reviewed the literature on the importance of privatization on the financial

performance of government firms, the challenges facing privatization in government firms

and the measures that can improve the challenges facing privatization in government firms.

Each specific objective has been discussed in detail. The next chapter which is chapter three

discusses the research methodology applied in the research.

22

CHAPTER THREE

3.0. RESEARCH METHODOLOGY

3.1. Introduction

Research methodology used in the study was discussed in this chapter. It included the

research design, population and sampling design, data collection methods, research

procedures and data analysis methods to be used in the study. This chapter ends with a

summary.

3.2. Research Design

Research design is an action or plan chosen to incorporate the different constituents of the

study in a logical way, certifying effective address of the research problem (Chari, 2015).

The researcher applied a quasi-experimental (event study) to carry out the study. An event

study conducted on a specific company looks at the changes in its stock price relative to

the news or event. A study on the overall market looks at the effects of the change in supply

and demand. The researcher used both event study and descriptive research design. Event

study was used to assess whether there are any abnormal or excess returns earned by

security holders accompanying specific events where there are an abnormal or excess

return. The researcher observed the pre and post-privatization performance of several

government firms that were privatized between 1991 to 2008.

Descriptive research design was used to explain in detail about the measures of improving

privatization in Kenya. According to Sekaran and Bougie (2009), descriptive studies are

used to gather information that explains the features of a population or event. This study

chose descriptive studies to aid in knowing the characteristics of the population and to

inaugurate all the facets of the study, to draw conclusions and recommendations of the

study grounded on the results and findings of the study. This study was guided by three

research questions which included Performance of Firms before Privatization, Performance

of Firms after Privatization and the Measures of Improving Privatization Process?

3.3. Population and Sampling Design

3.3.1. Population

Population is the total collection of components about which the researcher wishes to make

inferences (Cooper & Schindler, 2008). Target population comprises of all members of a

23

group of people where the researcher intends to generalize results of the study (Kuada,

2012). The target population of the study was the companies which were partially or

substantially owned by the government of Kenya but where the government ownership has

been diluted between 1991 and 2008. Population of the study comprised of 56 employees

in the management department. Primary data was collected from the employees in the

management department of the privatized companies.

3.3.2. Sampling Design

3.3.2.1. Sampling Frame

Sampling frame is a list of elements from which a sample may be drawn (Zikmund, Babin,

Carr and Griffin, 2013). The definition includes the purpose of sampling frames, which is

to provide a means for choosing the specific members of the target population to be

interviewed in the survey. The sampling frame consisted of the targeted population. The

sampling frame for this study was the 6 privatized government firms.

3.3.2.2. Sampling Technique

Sampling techniques include: judgment, simple random, stratified and cluster sampling.

Simple random sampling was used in this study so as to ensure that each element in the

population of an equal chance of being included in the sample.

3.3.2.3. Sample Size

Cooper and Schindler (2008), defined sample as a group of participants, events or records

consisting of a portion of target population, carefully selected to represent that population.

To get a sample size, the firm must been in operation for at least three years before

privatization and has continued in operation for three years after privatization. By use of

this method, only six firms were selected for review.

For the primary data, a sample size formula was used to get the sample size.

Sample size formula n= N/(1+N(e)^2, where

N=the population

n=sample size

e=margin of error, in this case 10%

24

n=56/ (1+ (56*0.1^2)) =56/1.56

=36

Therefore the sample size of the study was 36 employees from the management department.

3.4. Data Collection Method

There are two types of data and they include primary and secondary data (Adrian &

Boyarchenko, 2018). Primary data is the first hand information while secondary data is the

second hand information which is obtained from sources like magazines, journals and

tapes. The study made use of both primary and secondary data. Secondary data which

comprised of annual financial reports for the selected firms was used. Data forms were