Preparing the SEFA

Feb 24, 2016

Preparing the SEFA. Presentation by Rick Gratza, CPA Kerber, Eck & Braeckel LLP. Topics Covered. What is a SEFA? Why is the SEFA Important? Accumulating the Data Testing the Data Sorting & Summarizing the Data SEFA Note Disclosure Common Deficiencies Resources SEFA Checklist. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Preparing the SEFAPresentation by Rick Gratza, CPA

Kerber, Eck & Braeckel LLP

What is a SEFA? Why is the SEFA Important? Accumulating the Data Testing the Data Sorting & Summarizing the Data SEFA Note Disclosure Common Deficiencies Resources SEFA Checklist

Topics Covered

Schedule of Expenditures of Federal Awards

Required by OMB Circular A-133 if Federal expenditures exceed $500,000 (increase?)

SEFA defined in OMB Circular A-133_.310(b)◦ Auditee’s responsibility defined in _.300(d)◦ Auditor’s responsibility defined in _.505(a)

Supplementary information to the basic financial statements

What is a SEFA?

The SEFA serves as the basis for major program determination- accuracy and completeness of the SEFA is critical.

Auditee is responsible for preparing a complete and accurate SEFA

Auditor is required to assess the District’s internal controls over preparation of the SEFA.

Auditor is required to perform audit procedures to verify the accuracy and completeness of the SEFA.

Why is the SEFA Important?

Prepare preliminary SEFA for auditor’s interim work

Update the SEFA for final audit work

Why is the SEFA Important?- continued

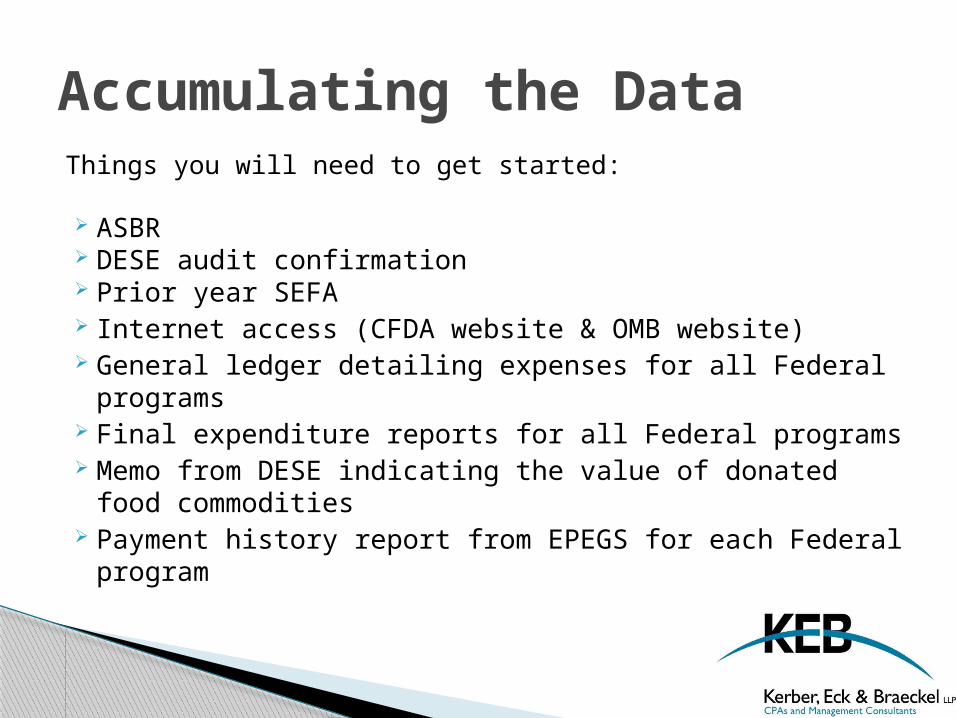

Things you will need to get started:

ASBR DESE audit confirmation Prior year SEFA Internet access (CFDA website & OMB website) General ledger detailing expenses for all Federal programs Final expenditure reports for all Federal programs Memo from DESE indicating the value of donated food

commodities Payment history report from EPEGS for each Federal program

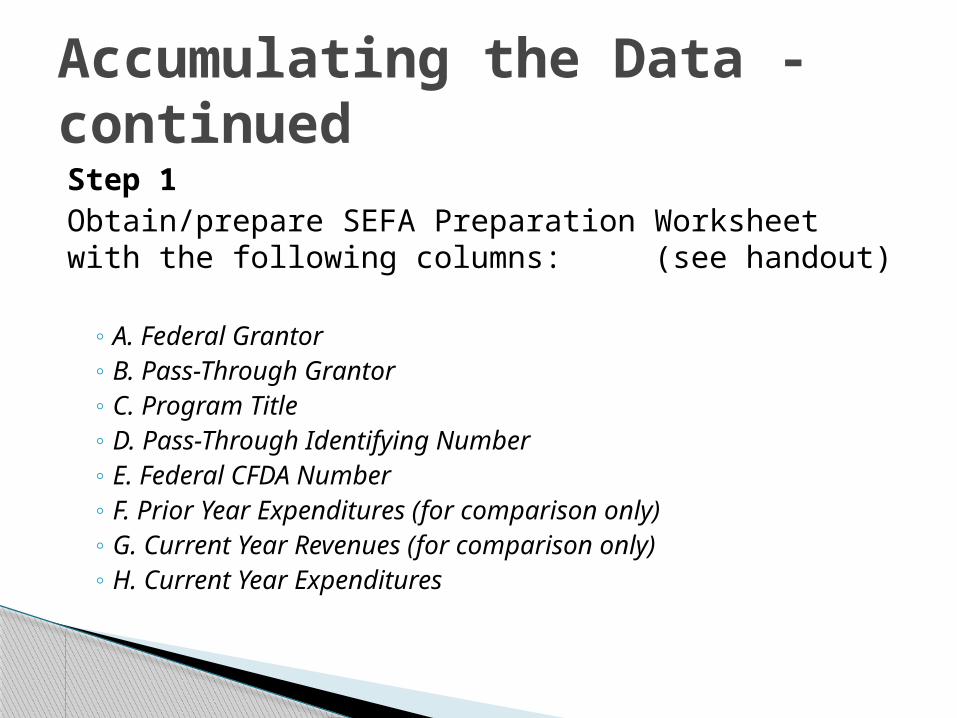

Accumulating the Data

Step 1Obtain/prepare SEFA Preparation Worksheet with the following columns: (see handout)

◦ A. Federal Grantor◦ B. Pass-Through Grantor◦ C. Program Title◦ D. Pass-Through Identifying Number ◦ E. Federal CFDA Number◦ F. Prior Year Expenditures (for comparison only)◦ G. Current Year Revenues (for comparison only)◦ H. Current Year Expenditures

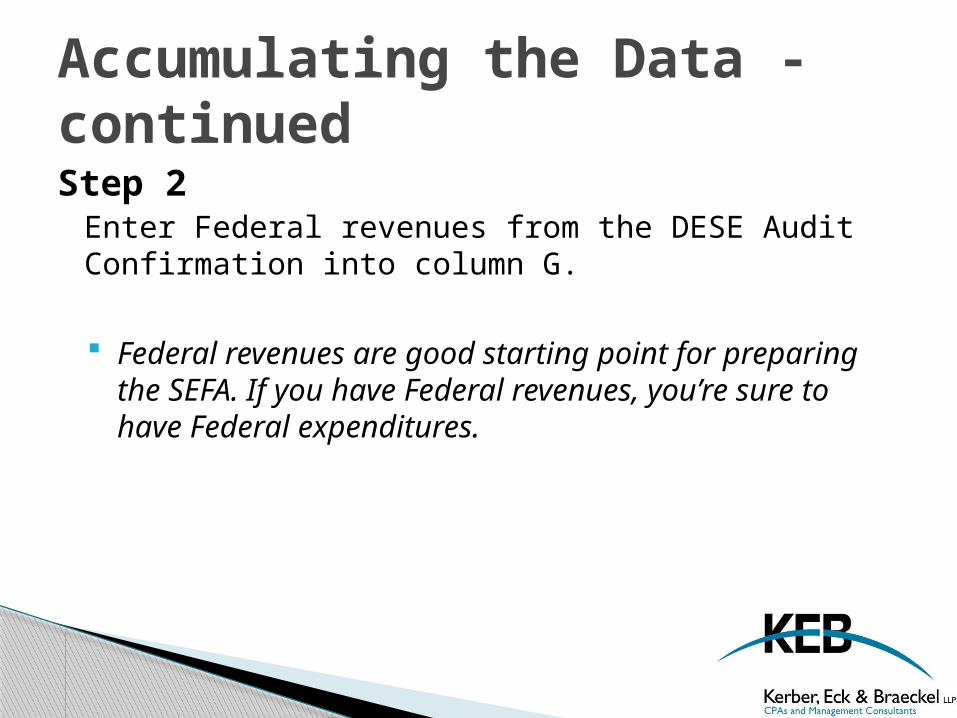

Accumulating the Data - continued

Step 2Enter Federal revenues from the DESE Audit Confirmation into column G.

Federal revenues are good starting point for preparing the SEFA. If you have Federal revenues, you’re sure to have Federal expenditures.

Accumulating the Data - continued

Step 3Enter the amount of any non-cash federal assistance received during the year in columns G and H.

This includes the value of donated food commodities communicated to the District in a letter from DESE usually in August.

Any other noncash federal assistance?

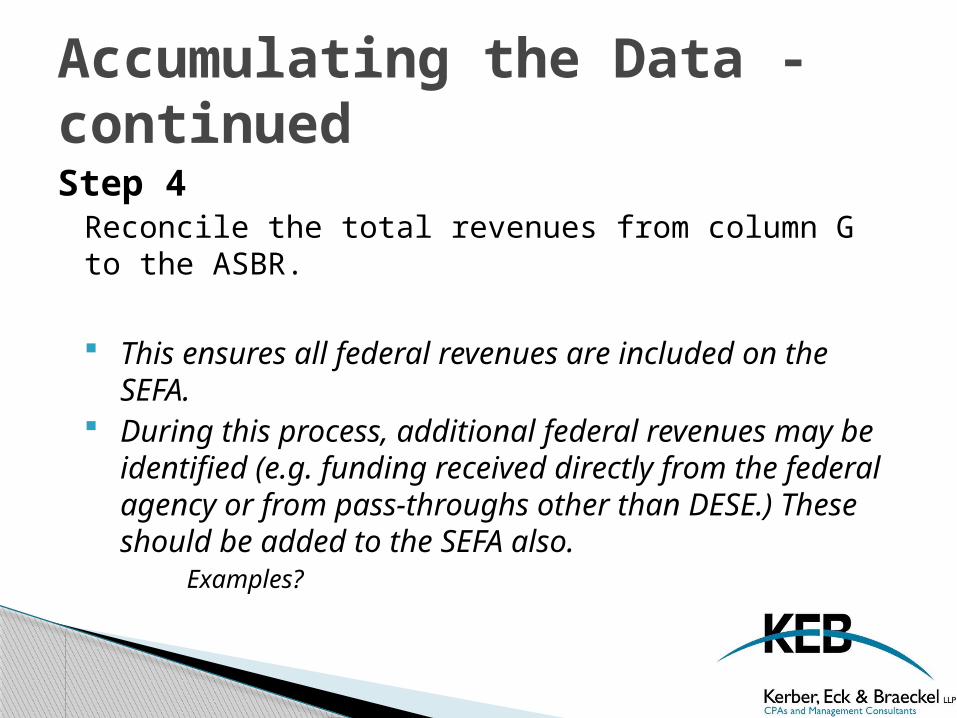

Accumulating the Data - continued

Step 4Reconcile the total revenues from column G to the ASBR.

This ensures all federal revenues are included on the SEFA. During this process, additional federal revenues may be

identified (e.g. funding received directly from the federal agency or from pass-throughs other than DESE.) These should be added to the SEFA also.

Examples?

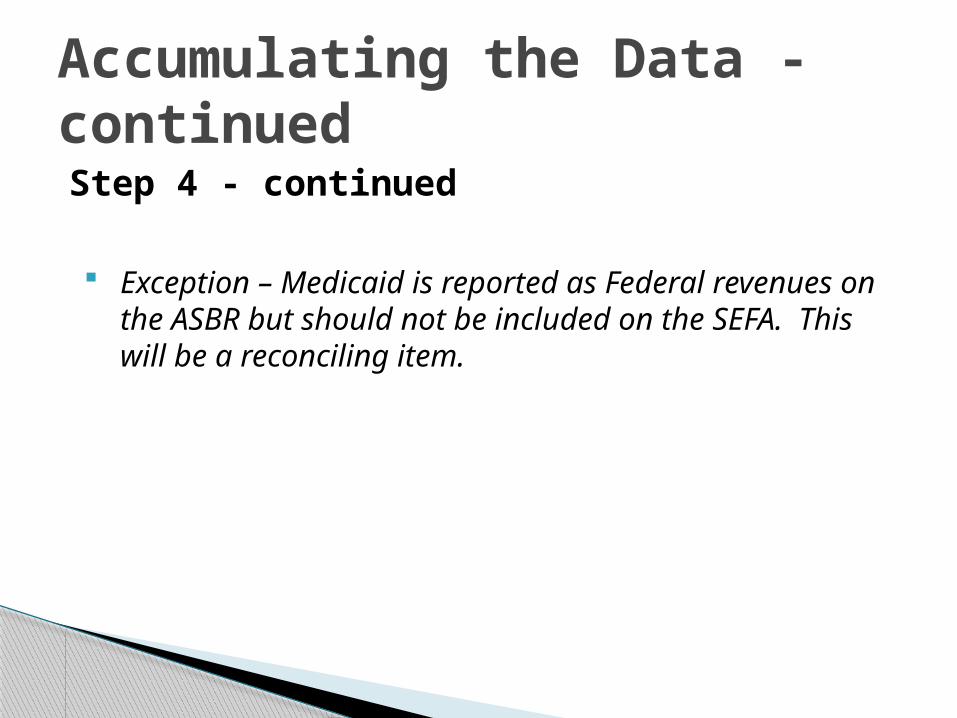

Accumulating the Data - continued

Step 4 - continued

Exception – Medicaid is reported as Federal revenues on the ASBR but should not be included on the SEFA. This will be a reconciling item.

Accumulating the Data - continued

Step 5Enter the corresponding CFDA number from the DESE Audit Confirmation or grant agreement into column E.

Each Federal program is assigned a unique CFDA number. The complete CFDA number is a five digit number, XX.XXX The first two digits represent the Funding Agency and the second

three digits represent the program. e.g. 84.010

84 = Department of Education.010 = Title I Grants to Local Education Agencies

Accumulating the Data - continued

Step 5 - continued

If the pass-through grantor failed to indicate the CFDA number, either contact the pass-through or use a key word search on the CFDA website to find it.

Some programs may be funded by more than one CFDA number. In that case, each CFDA has to be listed separately on its own line. (e.g Title I source of funds #5451 could be funded by both cfda #84.010 and 84.377).

Accumulating the Data - continued

Step 6Enter the name of the pass-through grantor in column B.

For school districts, the most common pass-through grantor is DESE.

If received directly from the Federal government, enter “Direct”.

Accumulating the Data - continued

Step 7Look up the CFDA number entered in column E from the Catalog of Federal Domestic Assistance website and enter the Federal grantor name in column A and the program name in column C.

Programs can be searched by CFDA # or keyword. Enter the program name from the CFDA website, do NOT

use the name given to the program by the District or DESE. Recovery Act awards must be identified separately on the

SEFA - add prefix “ARRA” to the name of program.

Accumulating the Data - continued

Step 8Enter the prior year expenditures from the prior year SEFA in column F.

This column is not technically part of the SEFA but will be used to test the reasonableness of the data in a following step.

Accumulating the Data - continued

Step 9Enter the current year expenditures from the general ledger in column H.

The SEFA should be prepared on the same basis of accounting (i.e. cash, modified accrual) as the financial statements.

The SEFA must include both direct and indirect costs, and exclude cost sharing or matching amounts.

If the program is funded by a combination of both federal and state or local funds, list only the federal share on the SEFA. Examples?

Accumulating the Data- continued

Step 1For each program, reconcile current year expenditures (column H) to the Final Expenditure Report (FER) submitted to the federal grantor or pass-through agency (i.e. DESE).

Attach the supporting reconciliation. Your auditors will want this.Reconciling items could include:

◦ Expenditures obligated in the prior year and reported in the prior year FER but paid for (accrued) in the current year

◦ Expenditures obligated in the current year and reported in the current year FER but paid for (accrued) in the subsequent year.

Testing the Data

Step 1 – Continued◦ Example:

A purchase order is issued for Title 1 supplies in May 2013. The supplies are received in July 2014 and paid for in August 2015.

Expenditure reported on the FY2013 FER since it was obligated in FY2013

Expenditure reported on the FY2014 SEFA since the supplies were received and paid for in 2014

Testing the Data - Continued

Step 2Compare current year expenditures (column H) to prior year expenditures (column F) for reasonableness.

Any significant differences between the current and prior year should be explained.

Set a threshold - (e.g. explain variances > 10%)

Testing the Data - continued

Step 3Compare current year expenditures (column H) to the current year revenues (column G) and explain any significant differences.

Could be timing differences- expenses reported in the SEFA in one fiscal year may not be reimbursed by DESE until the following fiscal year.

Check the payment history report on EPEGS for each grant. The final payment indicated on the payment history report should agree to the difference, if any, between revenues and expenses.

Testing the Data - continued

Sort the data by CFDA number (column E) so that all of the financial assistance from the same federal program is grouped together on the schedule.

Provide subtotals for programs with the same CFDA numbers (e.g. Special Education programs).

Provide a subtotal for each federal grantor.

Provide a total for all federal programs.

Sorting & Summarizing the Data

Notes to the SEFA should include these common disclosures:

Significant accounting policies used in preparing the schedule

Value of noncash assistance expended

Clusters of programs - groupings of closely related programs that have similar compliance requirements identified in OMB Circular A-133 Compliance Supplement

SEFA Note Disclosure

Other required disclosures, if applicable, include:

Amounts provided to sub-recipients

Amount of insurance in effect from federal insurance program

Loans and loan guarantees outstanding

SEFA Note Disclosure - Continued

NOTE A—BASIS OF PRESENTATION

The accompanying schedule of expenditures of federal awards includes the federal grant activity of ABC School District under programs of the federal government for the year ended June 30, 201X. The information in this schedule is presented in accordance with the requirements of OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations.

NOTE B—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIESExpenditures reported on the schedule are reported on the (identify basis of accounting) basis of accounting. Such expenditures are recognized following the cost principles contained in OMB Circular A-87, Cost Principles for State, Local and Indian Tribal Governments, wherein certain types of expenditures are not allowable or are limited as to reimbursement.

SEFA Note Disclosure - Continued

NOTE C—SUBRECIPIENTS Of the federal expenditures presented in the schedule, ABC School District provided federal awards to subrecipients as follows:

NOTE D—FOOD DONATIONNonmonetary assistance is reported in the schedule at the fair market value of the food commodities received and disbursed during the year ended June 30, 201X.

SEFA Note Disclosure - Continued

CFDA Number

Program Name

Amount Provided to Subrecipients

93.600 Head Start $ 123,965

NOTE E – CLUSTERSClusters of programs are groupings of closely related programs that share common compliance requirements. Total expenditures by cluster are:

Child Nutrition Cluster 10.553, 10.555 $6,210,726

SEFA Note Disclosure - Continued

Amounts reported in the SEFA did not reconcile to financial records (i.e. g/l & FER)

The SEFA did not indicate whether the awards were direct or pass-through.

Notes did not disclose the basis of accounting.

The sub-grant awards numbers assigned by the pass-through entities were not included on the schedule.

Common Deficiencies

The names of the pass-through entities or grantor federal agencies were missing.

Multiple lines for CFDA numbers were shown, but the total expenditures for the CFDA number was not included.

The correct CFDA number was not reported

The correct name of the program was not reported

Common Deficiencies - Continued

Catalog of Federal Domestic Assistance◦ www.cfda.gov

OMB Circular A-133, Audits of States, Local Governments and Non-Profit Organizationso http

://www.whitehouse.gov/sites/default/files/omb/assets/a133/a133_revised_2007.pdf

OMB Circular A-133 Compliance Supplement◦ http://www.whitehouse.gov/omb/circulars/A133_COMPLIANCE_SUPPLEMENT_

2012

AICPA’s Schedule of Expenditures of Federal Awards (SEFA) Practice Aids (look for link to auditee practice aids)◦ http://www.aicpa.org/InterestAreas/GovernmentalAuditQuality/Resources/AuditPra

cticeToolsAids/Pages/Single%20Audit%20Practice%20Aids.aspx

Resources

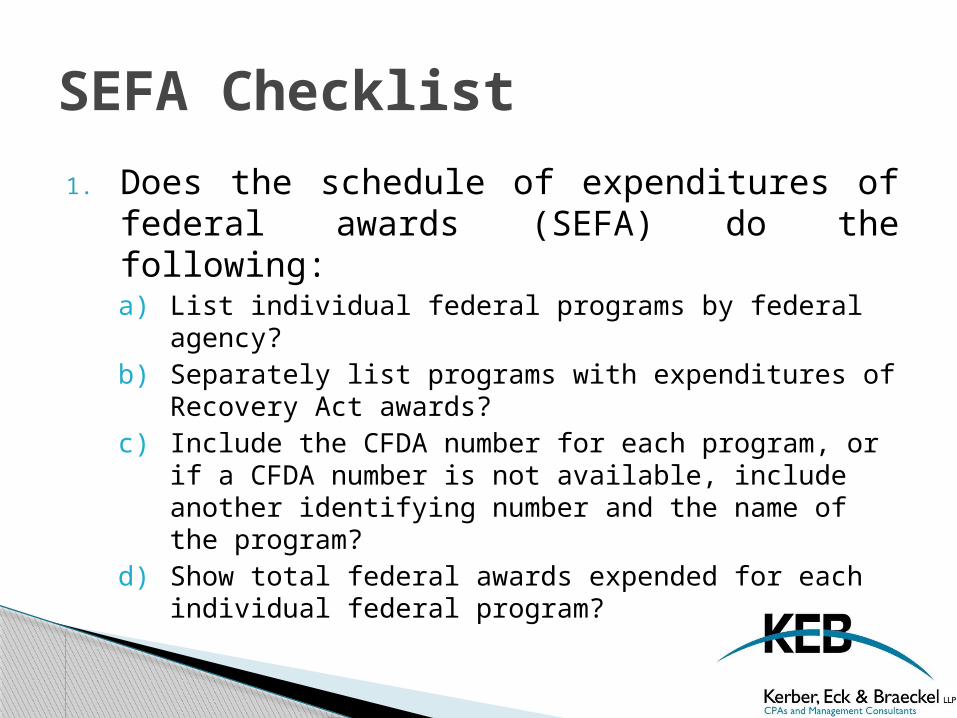

1. Does the schedule of expenditures of federal awards (SEFA) do the following:a) List individual federal programs by federal agency?b) Separately list programs with expenditures of Recovery Act

awards?c) Include the CFDA number for each program, or if a CFDA

number is not available, include another identifying number and the name of the program?

d) Show total federal awards expended for each individual federal program?

SEFA Checklist

e. For research and development (R&D) clusters, list federal awards expended either by individual award or by federal agency and major subdivision within the agency.

f. For all other clusters of programs, list the individual awards within the cluster?

g. Include the name of the pass-through entity and identifying number assigned by the pass-through entity for federal awards received as a sub-recipient?

h. Identify, to the extent practical, the total amount provided to sub-recipients from each federal program? (Alternatively, this information may be included in the notes.)

SEFA Checklist- continued

2. Do notes to the SEFA appropriately and completely describe the significant accounting policies used in preparing the SEFA and the basis of accounting?

3. Does the SEFA (preferably) or a note to the SEFA include the value of federal awards expended in the form of:a) Noncash assistance?b) The amount of insurance in effect during the year?c) The amount of loans or loan guarantees, including interest

subsidies, outstanding at year end?

SEFA Checklist- continued

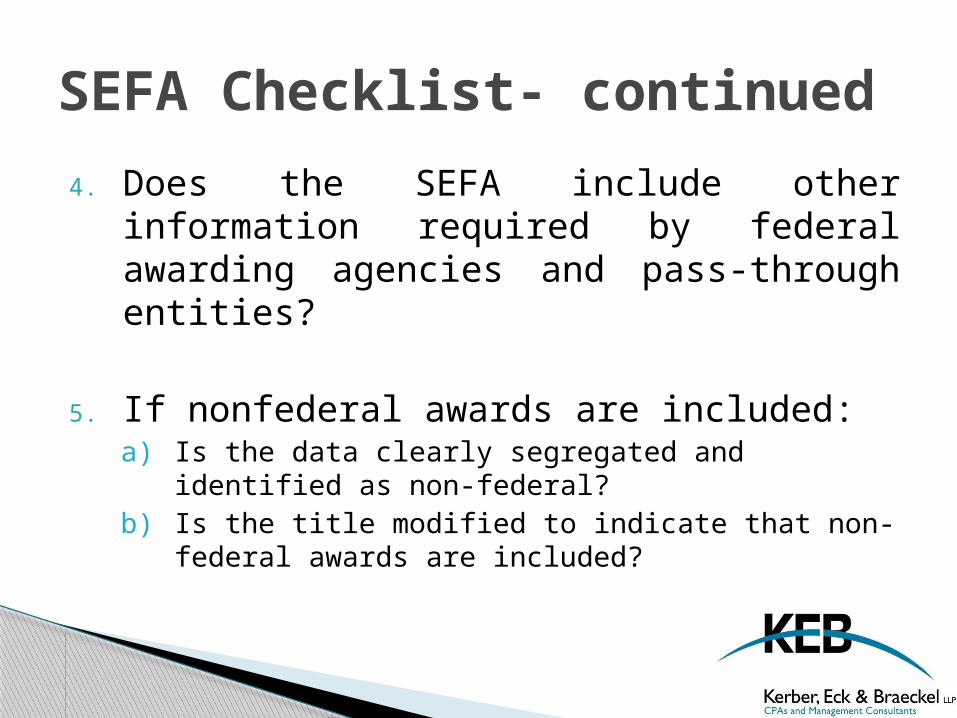

4. Does the SEFA include other information required by federal awarding agencies and pass-through entities?

5. If nonfederal awards are included:a) Is the data clearly segregated and identified as non-federal?b) Is the title modified to indicate that non-federal awards are

included?

SEFA Checklist- continued

Questions?

New guidance in the AICPA Audit and Accounting Guide, State and Local Governments regarding Required Supplementary Information (RSI) applicable to cash basis Districts.

Under previous guidance, financial statements prepared on the cash basis of accounting were to include Management’s Discussion and Analysis and budgetary comparison information for the General Fund and major Special Revenue funds consistent with financial statement prepared in accordance with GAAP.

While this information may still be included with the financial statements, it is no longer required and therefore, should not be labeled Required Supplementary Information (RSI).

Update

Related Documents