C o n f i d e n t i a l 1 Program : MBA Semester : I Subject Code : MBF201 Subject Name : Financial Management Unit number : 8 Unit Title : Capital Budgeting HOME NEXT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 1/25

C o n f i d e n t i a l

1

Program : MBA

Semester : I

Subject Code : MBF201

Subject Name : Financial Management

Unit number : 8

Unit Title : Capital Budgeting

HOME NEXT

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 2/25

C o n f i d e n t i a l

Introduction

2

• All such businesses involve investment decisions. These investmentdecisions that corporates take are known as capital budgeting

decisions.

• Capital budgeting decisions involve evaluation of specific investmentproposals.

• Capital budgeting is a blue-print of planned investments in operating

assets.

• It is the process of evaluating the profitability of the projects underconsideration and deciding on the proposal to be included in thecapital budget for implementation.

• Capital budgeting decisions involve investment of current funds inanticipation of cash flows occurring over a series of years in future.

• Investment of current funds in long-term assets for generation of cash flows in future over a series of years characterises the nature of capital budgeting decisions.

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 3/25

C o n f i d e n t i a l

3HOME NEXTPREVIOUS

Session Objectives:

To understand,• The concept of capital budgeting• The importance of capital budgeting• The complexity of capital budgeting procedures

• Various techniques of appraisal methods• Evaluation of capital budgeting decision

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 4/25

C o n f i d e n t i a l

Importance of Capital Budgeting

Grouping of Decisions• Decision to replace the equipments for maintenance of current level of

business or decisions aiming at cost reductions, known asreplacement decisions

• Decisions on expenditure for increasing the present operating level orexpansion through improved network of distribution

• Decisions for production of new goods or rendering of new services

• Decisions on penetrating into new geographical area

• Decisions to comply with the regulatory structure affecting theoperations of the company, like investments in assets to comply withthe conditions imposed by Environmental Protection Act

• Decisions on investment to build township for providing residentialaccommodation to employees working in a manufacturing plant

4

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 5/25

C o n f i d e n t i a l

The reasons that make the capital budgeting decisions most crucialfor finance managers are:

• These decisions involve large outlay of funds in anticipation of cashflows in future.

• Long time investments of the funds sometimes may change the riskprofile of the firm.

• Capital budgeting decisions involve assessment of market forcompany’s product and services, deciding on the scale of operations,selection of relevant technology and finally procurement of costlyequipment.

5

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 6/25

C o n f i d e n t i a l

• The growth and survival of any firm in today’s business environmentdemands a firm to be pro-active. Capital budgeting decisions help inthis process.

• The social, political, economic and technological forces generate highlevel of uncertainty in future cash flow streams associated with capitalbudgeting decisions. These factors make these decisions highlycomplex.

• Capital budgeting decisions are very expensive. To implement thesedecisions, firms will have to tap the capital market for funds. Thecomposition of debt and equity must be optimal keeping in view theexpectations of investors and risk profile of the selected project.

Therefore capital budgeting decisions for growth have become anessential characteristic of successful firms today.

6

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 7/25C o n f i d e n t i a l

Complexities involved

• Capital expenditure decision involves forecasting of future operatingcash flows.

• Forecasting the future cash flows demands certain assumptions aboutthe behaviour of costs and revenues in future.

• The following are complexities involved in capital budgeting decisions:

– Estimation of future cash flows

– Commitment of funds on long-term basis

– Problem of irreversibility of decisions

7

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 8/25C o n f i d e n t i a l

Phases of CapitalExpenditure decisions

• Identification of investment opportunities.• Evaluation of each investment proposal• Examination of the investments required for each investment proposal• Preparation of the statements of costs and benefits of investment

proposals• Estimation and comparison of the net present values of the

investment proposals that have been cleared by the management onthe basis of screening criteria

• Examination of the government policies and regulatory guidelines, forexecution of each investment proposal screened and cleared based onthe criteria stipulated by the management

• Budgeting for capital expenditure for approval by the management• Implementation• Post-completion audit

8

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 9/25C o n f i d e n t i a l

Identification of investmentopportunities

• A firm is in a position to identify investment proposal only when it isresponsive to the ideas of capital projects emerging from variouslevels of the organisation.

• The proposal may be to:– Add new products to the company’s product line,– Expand capacity to meet the emerging market at demand for

company’s products– Add new technology based process of manufacture that will

reduce the cost of production.

• Generation of ideas with the feasibility to convert the same intoinvestment proposals occupies a crucial place in the capital budgetingdecisions.

• Proactive organisations encourage a continuous flow of investmentproposals from all levels in the organisation.

9

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 10/25C o n f i d e n t i a l

Important Points for consideration

• Analysing the demand and supply conditions of the market for thecompany’s product could be a fertile source of potential investmentproposals.

• Market surveys on customer’s perception of company’s product couldbe a potential investment proposal to redefine the company’sproducts in terms of customer’s expectations.

• Reports emerging from R & D section could be a potential source of investment proposal.

• Economic growth of the country and the emerging middle classendowed with purchasing power could generate new businessopportunities in existing firms.

• Public awareness of their rights compels many firms to initiateprojects from environmental protection angle.

10

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 11/25C o n f i d e n t i a l

Rationale of Capital BudgetingProposals

• The investors and the stake-holders expect a firm to functionefficiently to satisfy their expectations.

• The stake- holders’ expectation and the performance of the companymay clash among themselves.

• The one that touches all these stake- holders’ expectation could bevisualised in terms of firm’s obligation to reduce the operating costson a continuous basis and increasing its revenues.

• Therefore, capital budgeting decisions could be grouped into twocategories:

– Decisions on cost reduction programmes– Decisions on revenue generation through expansion of installedcapacity

11

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 12/25C o n f i d e n t i a l

12

C i l B d i

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 13/25C o n f i d e n t i a l

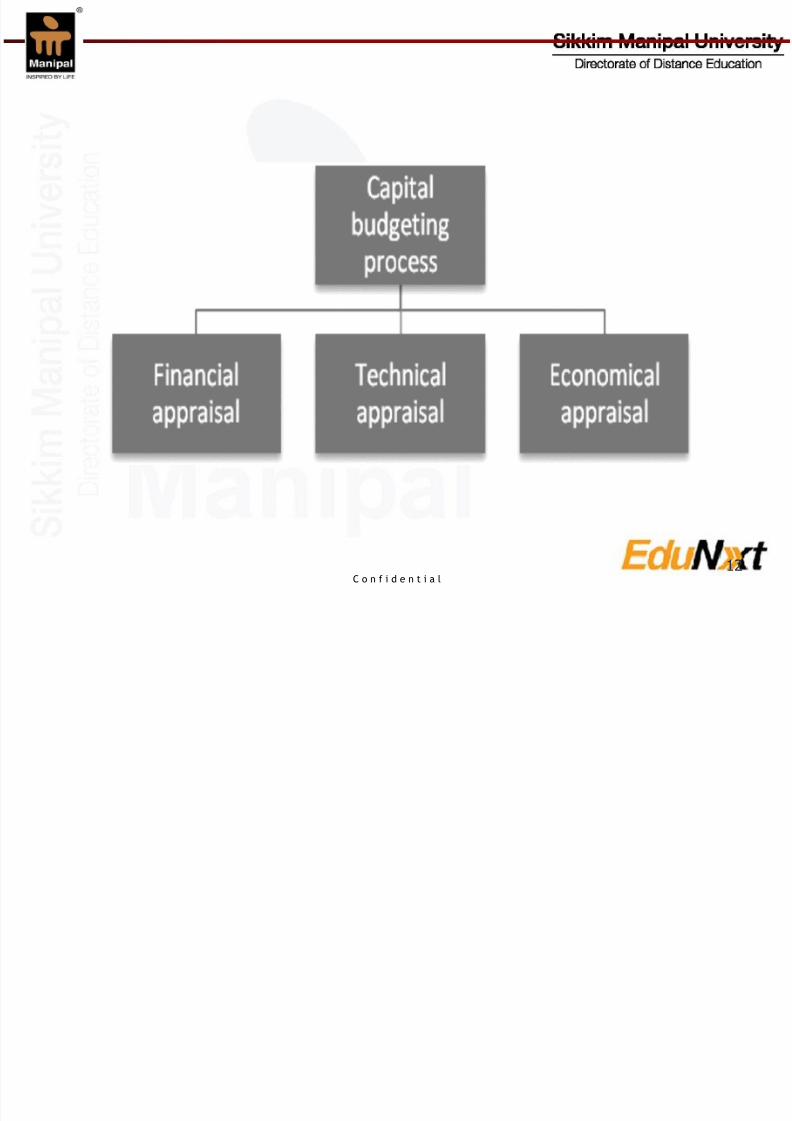

Capital BudgetingProcess

The technical aspects of the project are:

• Selection of process know-how• Decision on determination of plant capacity• Selection of plant, equipment and scale of operation• Plant design and layout• General layout and material flow• Construction schedule

Economic Appraisal / social cost benefit analysis examines:

• The impact of the project on the environment

• The impact of the project on the income distribution in the society• The impact of the project on fulfilment of certain social objective likegeneration of employment and attainment of self sufficiency

• Will the project materially alter the level of savings and investment inthe society?

13

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 14/25C o n f i d e n t i a l

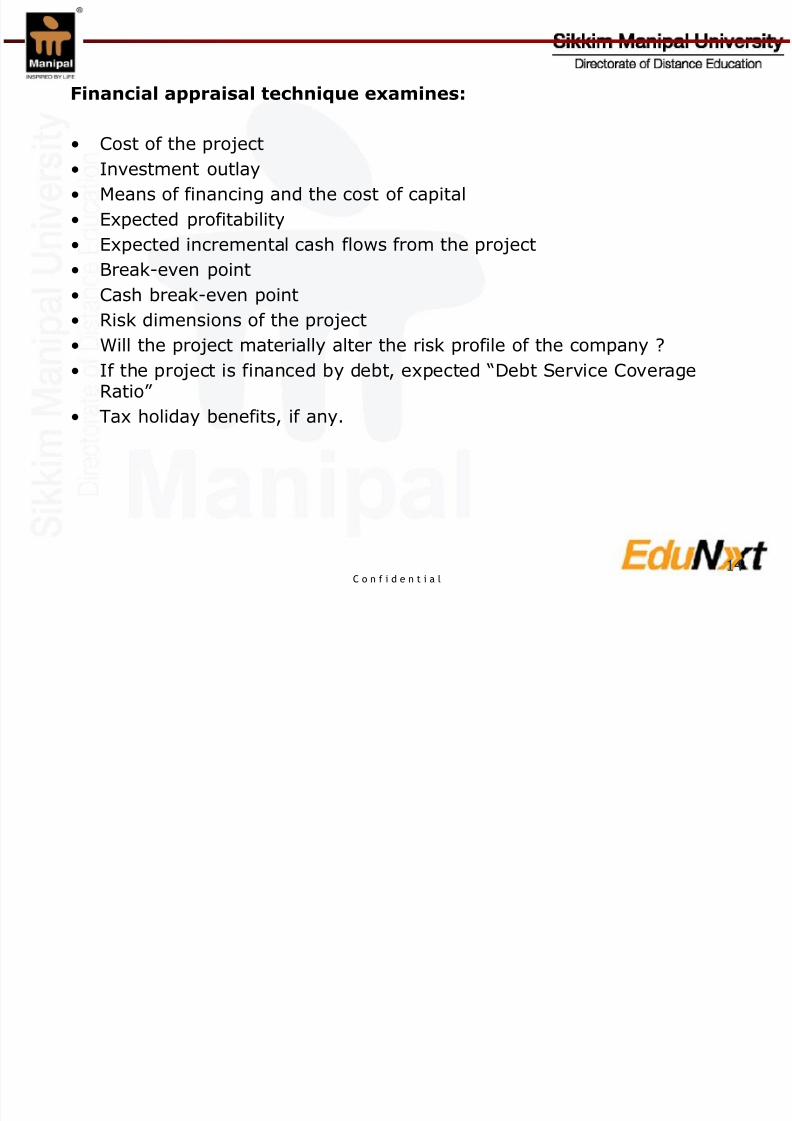

Financial appraisal technique examines:

• Cost of the project• Investment outlay• Means of financing and the cost of capital• Expected profitability• Expected incremental cash flows from the project

• Break-even point• Cash break-even point• Risk dimensions of the project• Will the project materially alter the risk profile of the company ?• If the project is financed by debt, expected “Debt Service Coverage

Ratio”

• Tax holiday benefits, if any.

14

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 15/25C o n f i d e n t i a l

Investment Evaluation

Steps involved in the evaluation of any investment proposal are:

• Estimation of cash flows both inflows and outflows occurring atdifferent stages of project life cycle

• Examination of the risk profile of the project to be taken up andarriving at the required rate of return

• Formulation of the decision criteria

Estimation of cash flows

• Capital outlays are estimated by engineering departments afterexamining all aspects of production process.

• Marketing department on the basis of market survey forecasts theexpected sales revenue during the period of accrual of benefits fromproject executions.

• Operating costs are estimated by cost accountants and productionengineers. 15

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 16/25C o n f i d e n t i a l

• Incremental cash flows and cash out flow statement is prepared bythe cost accountant on the basis of the details generated in the abovesteps.

Estimation of incremental cash flows

• Incremental cash flows stream of a capital expenditure decision hasthree components.

– Initial cash outlay (Initial investment)

– Operating cash inflows

– Terminal cash inflows

16

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 17/25C o n f i d e n t i a l

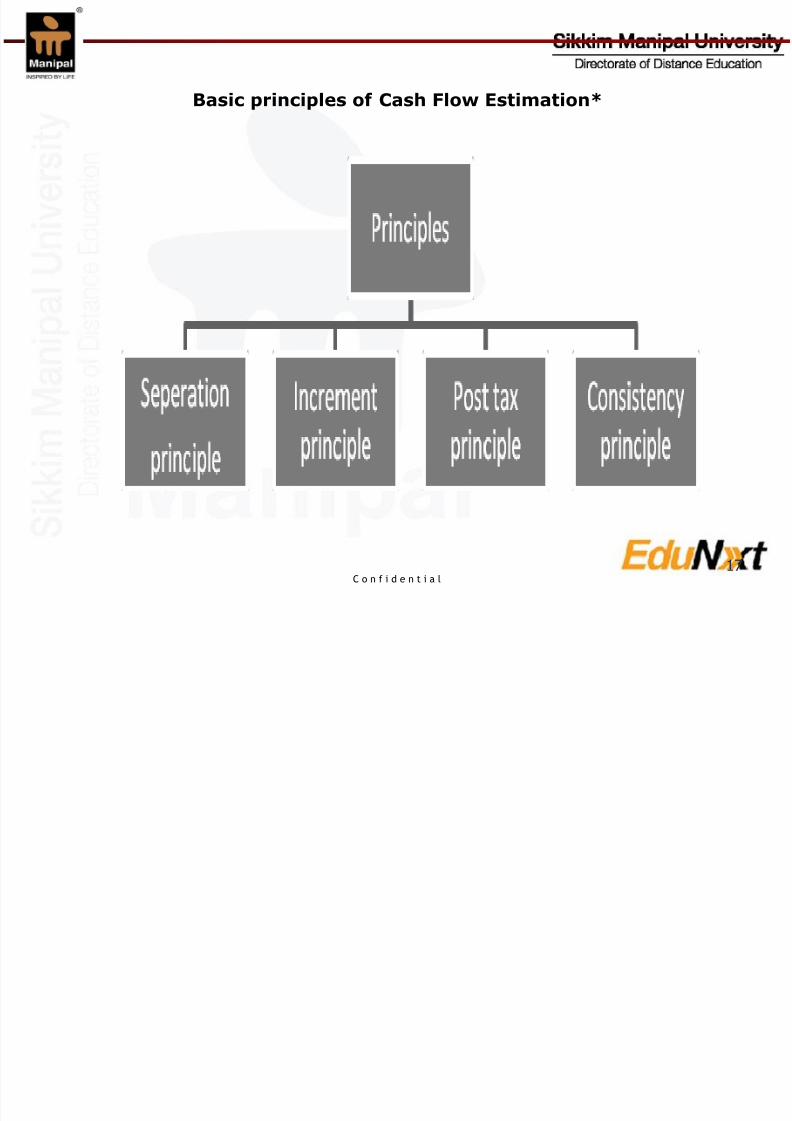

Basic principles of Cash Flow Estimation*

17

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 18/25C o n f i d e n t i a l

• Separation principle : The essence of this principle is the necessity

to treat investment element of the project separately (i.e.independently) from that of financing element.

The rate of return expected on implementation if the project is arrivedat by the investment profile of the projects.

Interest on debt is ignored while arriving at operating cash inflows.The following formula is used to calculate profit after tax

Incremental PAT = Incremental EBIT (1-t)(Incremental) (Incremental)

Where, EBIT = earnings (profit) before interest and taxes, t = taxrate

18

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 19/25C o n f i d e n t i a l

• Incremental principle : This principle states that cash flows of aproject are to be considered in incremental terms.

Following aspects have to be taken into account:

– Ignore sunk costs– Consider opportunity costs

– Need to take into account all incident effect– Cannibalisation

• Post tax principle : All cash flows should be computed on post taxbasis

• Consistency principle : Cash flows and discount rates used inproject evaluation need to be consistent with the investor group andinflation.

19

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 20/25C o n f i d e n t i a l

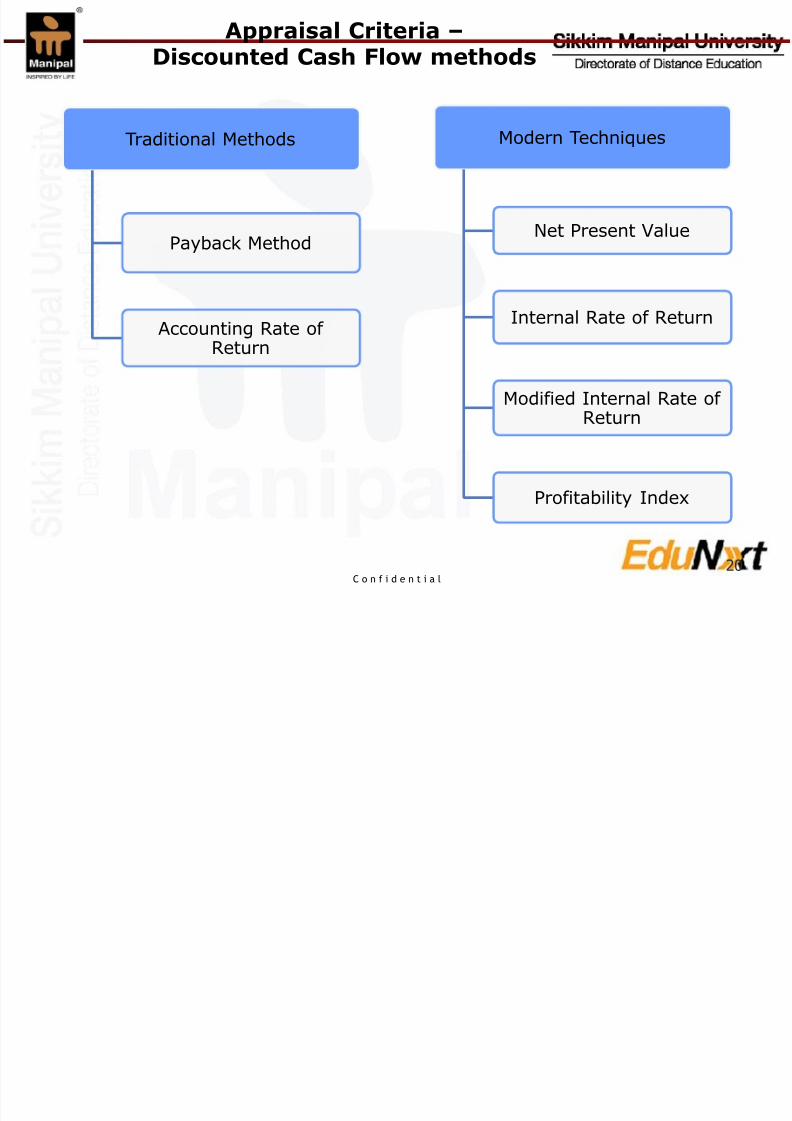

Appraisal Criteria – Discounted Cash Flow methods

Traditional Methods

Payback Method

Accounting Rate of Return

Modern Techniques

Net Present Value

Internal Rate of Return

Modified Internal Rate of Return

Profitability Index

20

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 21/25

C o n f i d e n t i a l

• Payback period is defined as the length of time required to recoverthe initial cash out lay.

(Year Prior to full recovery + Balance of initial out lay to be recoveredof initial out lay at the beginning of the year in which full) / Cashinflow of the year in which full recovery takes place

• Accounting rate of return (ARR) measures the profitability of investment (project) using information taken from financialstatements:

ARR = Average income / Average investment

ARR = Average of post tax operating profit / Average investment

Average investment = (Book Value of the investment at the beginning+ Book Value of investment at the end of the life of the project orinvestment) / 2

21

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 22/25

C o n f i d e n t i a l

• Net present value (NPV) method recognises the time value of money. It correctly admits that cash flows occurring at different timeperiods differ in value.

Accept or reject criterion can be summarised as given below:– NPV > Zero = accept– NPV < Zero = reject

• Internal rate of return (IRR) is the rate (i.e. discount rate) whichmakes the NPV of any project equal to zero.

IRR is the rate of interest which equates the PV of cash inflows withthe PV of cash outflows.

IRR can be determined by solving the following equation:

where t = 1 to n22

t

t

r

C CF

)1(0

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 23/25

C o n f i d e n t i a l

• Modified internal rate of return (MIRR) is a distinct improvementover the IRR.

Managers find IRR intuitively more appealing than the rupees of NPVbecause IRR is expressed on a percentage rate of return. MIRRmodifies IRR.

MIRR is a better indicator of relative profitability of the projects. MIRRis defined asPV of Costs = PV of terminal value

cash inflow (1+r) n-t

cash outflow / (1+r) n-t

MIRR is obtained on solving the following equation.

PV of costs = TV/ (1 + MIRR) n

23

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 24/25

C o n f i d e n t i a l

• Profitability index is also known as benefit cost ratio.

Profitability index is the ratio of the present value of cash inflows toinitial cash outlay.

The discount factor based on the required rate of return is used todiscount the cash inflows.

PI = Present value of cash inflows / initial cash outlay

Accept or reject criteria– Accept the project if PI is greater than 1

– Reject the project if PI is less than 1

If PI = 1, then the management may accept the project because thesum of the present value of cash inflows is equal to the sum of present value of cash outflows. It neither adds nor reduces theexisting wealth of the company.

24

8/3/2019 Ppt Unit 08 Mbf201

http://slidepdf.com/reader/full/ppt-unit-08-mbf201 25/25

Summary

You have learnt:

• What is Capital Budgeting• Importance of Capital Budgeting• Complexities involved• Capital Budgeting process

• Investment Evaluation• Appraisal techniques – Traditional and modern methods

25

Related Documents