PLANNING AND COST CONTROL IN A CORPORATE ORGANIZATION: (A MUST FOR ECONOMIC GROWTH AND DEVELOPMENT) BY OJUOLA TOLULOPE DANIEL SUBMITTED TO THE INSTITUTE OF CHARTERED ECONOMISTS OF NIGERIA (ICEN) IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF ASSOCIATE CHARTERED ECONOMIST (ACE)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PLANNING AND COST CONTROL IN A

CORPORATE ORGANIZATION:

(A MUST FOR ECONOMIC GROWTH

AND DEVELOPMENT)

BY

OJUOLA TOLULOPE DANIEL

SUBMITTED TO

THE INSTITUTE OF CHARTERED

ECONOMISTS OF NIGERIA (ICEN)

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT FOR THE AWARD OF ASSOCIATE

CHARTERED ECONOMIST (ACE)

DEDICATION

This project is dedicated to the Almighty God,

the Everlasting, Giver of all good and perfect

gifts, who has made it possible for me to

complete this professional program

successfully, and to my family, the Ojuolas.

ACKNOWLEDGEMENT

I am greatly indebted to the Alpha and Omega,

God Almighty who has granted me grace to

complete this work; also using this medium to

appreciate the entire embodiment of knowledge

that makes up the Institute of Chartered

Economists of Nigeria, on their unrelenting act

to boast our career professionally.

The Registrar Mr. Peter Ikpamejo, FCE, Deputy

Registrar Mr. Giwa Lucky FCE, President Sola S.

Eshiobo FCE, and to my Boss and friend Dr.

Afolabi Ajadi, who encouraged me to undertake

this course, to you I say a very big thank

you.

Table of Content

0.1 Preview

1.1 Introduction

1.2 Objective of the Study

1.3 Research Methodology

1.4 The Survey

2.1 Literature Review

2.2 Management Accounting and the Management

Process

3.0 The Nigerian Environment

3.1 The Nigerian Business Environment

3.2 The Nigerian Economic and Political

Environment

3.3 Accounting Framework and Auditing Standard

in Nigeria

4.0 Survey Results

4.1 Background Data

4.2 Present Function of Management Accountants

4.3 Profitability Analysis

4.4 Budgetary Control

4.5 Performance Reporting

4.6 Appraisal of Capital Budgeting Decisions

4.7 Evolution and Change in Management

Accounting Practice in Nigeria

4.7.1 Cost Determination and Financial

Control

4.7.2 Provision of Information

4.7.3 Waste Reduction through process

Analysis and Cost Management Techniques

4.8 Resent Change

4.9 Expected Changes

5 Summary

5.1 Summary of Findings

5.2 Conclusion

Footnotes

Reference

Appendix

PREVIEW

The conventional view of cost management

suggests that operations managers have direct

control over spending in their area of

responsibility. Activity-based management

(ABM), the process of using activity analysis

for cost management, provides an alternate

view. The premise underlying

Cost control and reduction refers to the

efforts business managers make to monitor,

evaluate, and trim expenditures. These efforts

might be part of a formal, company-wide program

or might be informal in nature and limited to a

single individual or department. In either

case, however, cost control is a particularly

important area of focus for small businesses,

which often have limited amounts of time and

money. “In a small business, you are so busy

serving your customers, you tend to get

lackadaisical about what you’re buying,

“business owner John Clark noted Jane

Applegate’s Strategies for Small Business

Success. Even seemingly insignificant

expenditures – for such items as office

supplies, telephone bills or overnight delivery

services – can add up for small businesses. On

the plus side, these minor expenditures can

often provide sources of cost savings.

Introduction

Revised International management accounting

practice 1 (IMAP #1), published in March 1988

by the Financial Management and Management

Accounting Committee (FMAC) of the

International Federation of Accountants (IFAC)

states that Management accounting is an

activity that is interwoven in the management

processes of all organizations. Management

Accounting refers to that part of the

management process which is focused on adding

value to organizations by attaining the

effective use of resources by people, in

dynamic and competitive contexts. It involves

distinctive technologies (mode of thought and

practice.)

Management accounting, as an integral part of

the management process, distinctly adds value

by continuously probing whether resources are

used effectively by people and organizations –

in creating value for customers, shareholders

or other stakeholders.

In this regard, resources include not only

financial ones, but also all other resources

created and used by organizations as a result

of financial expenditures. Thus, information

and knowledge, work processes and systems,

trained personnel, innovative capacities,

morale, flexible cultures, and even committed

customers may be included as resources – along

with special configurations of resources that

may be identified as strategic capabilities,

core competencies or intellectual capital.

The field of organizational activity

encompassed by management accounting has

developed through four evolutionary yet

recognizable stages, namely; Cost determination

and Financial Control, information for

management planning and control, reduction of

waste of resources in business processed and

creation of value through effective resources

use. The role of Management accountants refer

to the outcome of the process of evolution over

the four stages. It is one of the

organizational activities designed to manage

resources strategically. Each stage is a

combination of the old and the new, with the

old reshaped to fit with the new in addressing

a new set of conditions in the management

environment (IFAC, 1998).

For an organization to survive in the

competitive, ever-changing world, it must put

in place sound management accounting practice.

Managers need information for decision making.

An understanding of cost behaviour is

fundamental to managerial and cost accounting,

and Management Accounting information and the

way it is used can support or hinder action and

change of action in organizations. (Bescos and

Mendoza, 2000, Anderson et al, 2000,

Abrahammson and Helin, 2000).

Surveys of the role of management accountants

have focus mainly on companies in developed

countries. Drury, Braund, Osborne and Tayles

(1993) surveyed management accounting pratices

in U.K. manufacturing company. Copper and

Drury also undertook a study of the nature and

scope of management accounting in U.K.

Universities.

Appleyard and Pallett, 2000 examine the role

played by management accounting of management

accounting differences in the process of

integration in an Anglo-German setting and

identified management accounting problems and

managerial problem as significant obstacle to

integration, reflecting a lack of investment in

managing and controlling the new subsidiary.

Ax and Bjrnenak, 2000 in a study of how

management accounting innovation is

disseminated to other locations to increase

global homogenization of management accounting

practice, conclude that the trend in the world

of management accounting practices may not be

as homogenous and U.S. oriented as they seem to

be.

However, in Nigeria there is apparently no

empirical analysis of the role of management

accounting practices. Therefore there is need

for “triangulation” in the research by

providing evidence from developing countries

like Nigeria. To remedy this we have

undertaken a study with the aim of obtaining a

broad overview of the changing role of

management accounts in Nigeria Corporation

firms.

1.2 Objective of the study

The specific objectives of this study are:

To obtain a broad overview of the nature and

scope of management accounting in Nigerian

Corporate firms and identifies its stage in the

evolution process,

To make policy recommendations on how to

improve the role of management accountants in

corporate firms in Nigeria.

1.3 Research Methodology

Data was gathered principally through

administration of Questionnaires of finance and

management staff of a corporate firm,

supplemented by a review of relevant

documentations. These assisted the author to

have an understanding of the past, present and

future role of management accountants in

Nigerian Corporate firms.

1.4 The Survey

A survey of 55 Nigerian companies was conducted

between September and November 1998. However,

the actual number reported in this study is 50

companies. This is accounted for, by the

unwillingness of some companies to complete the

questionnaire and the bureaucracy associated

with large organizations.

In the rest of this report, section 2 presents

a review of related literature, while Section 3

presents a brief description of Business,

Economic and political environment in Nigeria.

The analysis of the survey results is presented

in section 4 section 5 concludes with a general

overview of summary of the findings, as well as

policy recommendations.

2.1 Literature Review

Evolution and Change in Management Accounting

The field of organizational activity

encompassed by management accounting has

developed through four evolutionary yet

recognizable stages.

Stage 1 – Prior to 1950, the focus was on

cost determination and financial control,

through the use of budgeting and cost

accounting technologies;

Stage 2 – By 1965, the focus had shifted

to the provision of information for

management planning and control through

the use of such technologies as decision

analysis and responsibility accounting;

Stage 3 – By 1985, attention was focused

on the reduction of waste in resources

used in business processes, through the

use of process analysis and cost

management technologies;

Stage 4 – By 1995, attention had shifted

to the generation or creation of value

through the effective use of resources,

through the use of technologies which

examine the drivers of customer value,

shareholder value, and organizational

innovation.

While these four stages are recognizable,

the process of change from one to another

has been evolutionary. Each stage is a

combination of the old and the new, with

the old reshaped to fit with the new in

addressing a new set of conditions in the

management environment. (IFAC, 1998).

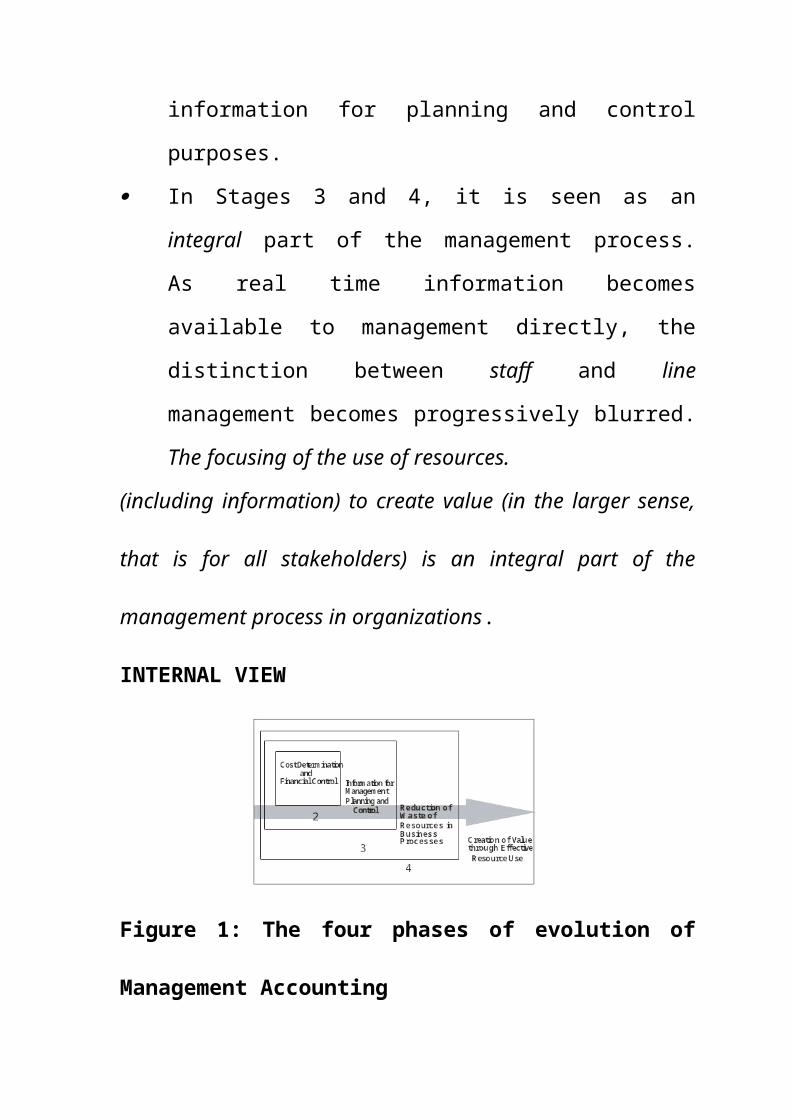

The diagram below illustrates the four

evolutionary stages of management accounting

which is expected to continue in the future.

In Stage 1, it was seen as a technical

activity necessary for the pursuit of

organizational objectives.

By Stage 2, it seen as a management

activity, but in a staff role; it involved

staff (“management”) support to line

management through the provision of

information for planning and control

purposes.

In Stages 3 and 4, it is seen as an

integral part of the management process.

As real time information becomes

available to management directly, the

distinction between staff and line

management becomes progressively blurred.

The focusing of the use of resources.

(including information) to create value (in the larger sense,

that is for all stakeholders) is an integral part of the

management process in organizations.

INTERNAL VIEW

Figure 1: The four phases of evolution of

Management Accounting

Source: IFAC, 1998: Revised International

management accounting practice 1 #1, Finance

Management and Management Accounting Committee

(FMAC), March, pp.6.

Management accounting at its current

evolutionary stage addresses the needs of the

organizations operating in dynamic and

competitive contexts. The new organizational

context implies:

Flat structures;

Use of cross-functional teams;

Management of value chains (remove

division between firm, suppliers and

customers);

Understanding one’s core competencies and

identity within relevant value chains, by

progressively becoming more virtual and

agile;

Developing delegation, trust, devolution

and subsidiary through simultaneously

integrated information systems and

availability of localized information in

real time at points of need;

Less reliance on financial control, by

creating (real time) localized control,

based on Non-financial Performance

Indicators;

Acceptance of ambiguity and paradox as

realities to work with and though; and

Cultural integration through shared

associated with traditional forms of

employment or professional specialization

(IFAC, 1998, IFAC, 2000).

2.2 Management Accounting and the Management

Process

The purpose of management has been

described as making people capable of joint

performance through common goals, common

values, the right structure, and providing the

training and development they need to inform

and to respond to change. The central purpose,

then, of the management process is to secure.

As it faces change, the vitality and endurance

of an organization through the ongoing co-

ordination of activities, efforts and

resources. Thus, the management process

includes:

Establishing organizational directions in

terms of objectives and strategies;

Aligning organizational structures,

process and systems to support

established directions;

Securing the commitment at a requisite

level of those contributing essential

skills and effort; and

Instituting controls that will guide an

organization’s progress towards the

realization of its strategies and

objectives.

The pursuit and realization of organizational

objectives and strategies requires the

mobilization or development of requisite

capabilities through the effective deployment

of resources. Resources are deployed in

structures, “control” mechanisms, and securing

commitments to create the capabilities are

unlikely to be developed; and resources are

likely to be wasted in ineffective structures,

control, and commitments.

Management accounting refers to that part of

the management process focused on the effective

use of resources in

Establishment strategy mixes that support

objectives;

Developing and maintaining the

organizational capabilities necessary for

strategy realization; and

Negotiating the strategy and capability

change necessary to secure ongoing

organizational success and survival.

Management accounting is only one part of the

management process of organization. It

provides a focus and distinctive perspective on

one key dimension of organizational activity –

identifying, obtaining and using resources. In

addition it stands beside and interacts with

other parts of the management process which

focus respectively on other key dimensions of

organizational activity: direct setting,

structuring securing commitment, control, and

change. It is interwoven with other parts of

the management process, by being associated

from a source perspective with

Organizational direction setting,

Organizational structuring,

Organizational commitment building,

Organizational change,

Organizational process design,

Organizational control, and

Organizational information systems

design.

Thus, that part of the management process

concerned with effective resource use over time

can be referred to as the management accounting

function or business process.

The management of the management accounting

function will likely involve establishing

objectives and strategies for the function,

structuring the work of the function, building

the capability of the function, resourcing the

function appropriately, responding creatively

to, or proactively addressing new challenges

bearing on the work of the function and

assessing the ongoing efficiency and

effectiveness of the function (IFAC, 1998).

3. The Nigerian Environment

4.7 The Nigerian Business Environment

The Nigerian business environment comprises of

small, medium and large-scale enterprises.

There is however no clear-cut definition that

distinguishes a small scale enterprise from a

medium scale enterprise in Nigeria, unlike in

countries such as USA, Britain, Canada and

Japan. A small-scale enterprise has been

defined in the monetary policy circular 22 of

1988 of the Central Bank of Nigeria as having

an annual turnover not exceeding 500,000 naira.

The federal government in the 1990 budget,

defined small scale enterprises for purposes of

commercial bank loan as those with an annual

turnover not exceeding 500,000 naira, and for

merchant bank loans, those enterprises with

capital investments not are exceeding 2 million

naira (excluding cost of land) or a maximum of

5 million naira. The national economic

reconstruction fund (NERFUND) set the maximum

limit for small-scale industries at 10 million

naira.

Furthermore, section 37b (2) of the Companies

and Allied Matters Decree (CAMD), 1990 defines

a small company as one with;

(a) an annual turnover of not more than 2

million naira.

(b) Net asset value of not more that 1

million naira only.

Ekpeyong and Nyong, 192 defined small and

medium scale enterprises in Nigeria as those

with investments in machinery and equipment not

exceeding 500,000n naira and two million naira,

respectively with not more that 50 and 100 paid

employees, respective. However, the definition

relates more to medium scale businesses than

small-scale enterprises. Moreover, most of the

large local businesses and strategic business

units of multinationals are listed on either

the first tier or the second tier securities

market. Presently, we have 170 companies

listed on the first tier market and 16

companies listed on the second tier securities

market of the Nigerian Stock Exchange (NSE).

For a companies listed on the First Tier

securities market are expected to have trading

record of at least five years, not less than 25

per cent shares in the hand of the public, and

not less than 500 shareholders. Such companies

are also expected to give quarterly, half-

yearly and yearly reports and there is not

limit to the amount of money that they can

raise from the securities market.

The second tier securities market was

introduced in 1986 with less stringent

conditions to accommodate more companies.

Companies listed on the second tier securities

market of the Nigerian Stock Exchange (NSE) are

expected to have expected to have track record

of at least three years, not less than 25 per

cent shares in the hand of the public, not less

than 100 shareholders and they cannot raise

more than 20 million naira from the securities

market.

3.2 The Nigerian Economic and Political

Environment

It has been overemphasized to the government of

developing countries that financial

liberalization is essential for prosperity.

Instead of discouraging foreign investors, they

are advised to open up so as to have access to

global savings that can be invested in order to

grow fast (The Economist, (1998).

Nigeria has joined other developing countries

to attract foreign investment by removing

bottlenecks and artificial barriers. This is

evidenced by the abolition of the Nigeria

indigenization decree of 1989 and Exchange

Control Act of 1961 which restricted foreign

participation in ownership of corporate firms

in Nigeria to a maximum of 40 per cent and

promulgation of the Nigerian Enterprises

Promotion Decree 16 and 17 of 1995 and the

abolition of capital gains tax in 1998 among

others. Thus foreigners can now own up to 100

per cent shares in Nigeria firms (Adelegan,

2000).

Globalization and financial liberalization is

bringing about more intense competition.

Nigerian corporate firms can no longer shy away

from the challenges presented in an every

changing business environment as we move to the

next millennium.

Prices must not be set too high or low. A

higher than normal price result in declining

sales while, a lower that normal price may

result in losses being incurred. Therefore,

corporate firms must constantly gather

information from external and internal sources,

analyze, process, interpret and communicate

such information within the organization to

assist management in planning, making decisions

and controlling operations.

Against a background of a rapidly changing

world, it is for the Nigerian Management

Accountant to continue to ensure the financial

health of corporate firms.

From 1986 to 1998 corporate firms in Nigeria

operated in an uncertain environment

characterized by political uncertainly under

military dictatorship and frustrated democracy,

irregular power supply, poor implementation of

budgets and economic policies. And frequent

changes and sometimes conflicting government

monetary policies THE Federal government of

Nigeria introduced the Structural adjustment

programme in 1986 to ameliorate deteriorating

economic situation. Since the strategy of

liberalization and deregulation of interest

rates was implemented, interest rates have

continued to increase making it difficult for

companies to obtain credit. Consequently,

industrial capacity utilization remained low

and the expected growth in corporate earnings

was not achieved while naira remained further

devalued.

In 1998 budget and its predecessors, the dual

exchange rate was in operations and the

government preferential exchange rate was 22

naira to US 1 Dollar. In 1999, the dual

exchange rate was abolished and the single

official rate of 86 naira to US 1 Dollar was

the prevailing applicable rate. Furthermore

naira remained further devalued to one US

dollar to one hundred naira and one UK pound to

one hundred and sixty naira.

3.3 Accounting Framework and Auditing Standard

in Nigeria

Only members of the Institute of Chartered

Accountants of Nigeria (ICAN) are established

by the Act of parliament number 15 of 1965 are

entitled to practice as accountant in Nigeria

in accordance with the provision of section

18(2) of companies Act, 1965.

Accounting practices in Nigeria is governed by

the guidelines issued by the Nigerian

Accounting Standard Board (NASB). These

guidelines are complementary to the

requirements of Companies and Allied Matters

Decree (CAMD), 1990, other relevant laws and

regulations in Nigeria and International

accounting Standards.

Auditing standards are issued by the public

practice section of ICAN to support accounting

firms in the conduct of their audit in order to

improve the quality of their work and reporting

system. It sets out guidelines on basis

principles guiding an audit:

Infrastructural requirements,

Pre-engagement basics of an adult,

Planning the audit, performance of the audit

and quality control.

Sections 358 to 364 of the Companies and Allied

Matters Decree (CAMD), 1990 clearly specified

the rights, duties and privileges of company

auditors in Nigeria. Auditing practice in

Nigeria I also controlled by International

auditing guidelines.

However, where there is disparity between

specifications of the local standards and the

international standards, the local standards

will be applied.

According to section 4 and 5 of the guidelines

of ICAN on Professional conduct of members,

“Every member must conform to the technical

standards promulgated by the institute or the

Nigerian Accounting Standard from time to time.

It is duty of the member to carry out

efficiently and economically and, in conformity

with the technical standards, the wishes and

instructions of his employer or client in so

far as they are not incompatible with the

requirements of the law, independence,

integrity and objectivity.

In doing so, it is the duty of the member to

bring to bear on any assignment that degree of

knowledge and skill that qualifies him for the

membership of the institute and right to offer

professional accounting and related services to

clients or employers.

Every member is expected to carry out his work

with a high degree of technical competence. In

particular, he should approach his work with

due professional skill and care having regard

to generally accepted accounting principles and

practice and in the conformity with standards

laid down by the institute from time to time.

He should not carry out professional work for

which he is not himself competent except he

obtains adequate advice and assistance

necessary for the completion”.

4. Survey Results

The main respondents are the financial

Directors and Management Accountants of the

companies. However, where there is no

management Accounting department, the principal

respondent is the head of finance section.

Each questionnaire has has thirty-six

questions. Section one focused on background

information, activities of the organization,

the existence or non-existence of the

management accounting function and the size of

the function.

The second section contained questions related

to organization structure, functions of the

function management accounting in Nigeria.

4.1 Background Data

The companies used in this study are from

banking, manufacturing, agricultural.

Pharmaceutical and oil and chemical marketing

(see table 1). 34 percent of the companies

have turnover and profit over Ten Million Naira

(N10 million)1 while, 3 percent and 12 percent

less than Five Hundred Thousand Naira (N0.5

Million) turnover and profit respectively. 62

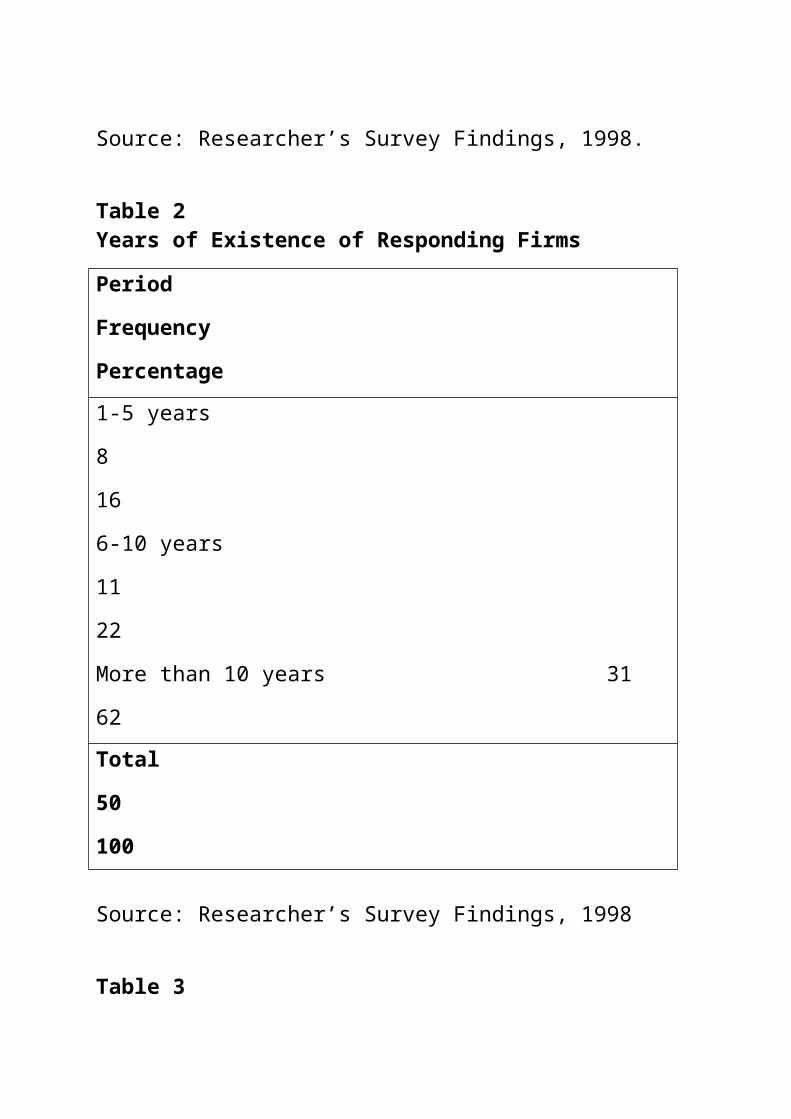

percent of the companies have been in existence

for more than 10 years, 22 percent for 6 to 10

years and 16 percent for 1 to 5 years. (see

table 2). Majority of the companies studied

have their major activities as services and

productions.

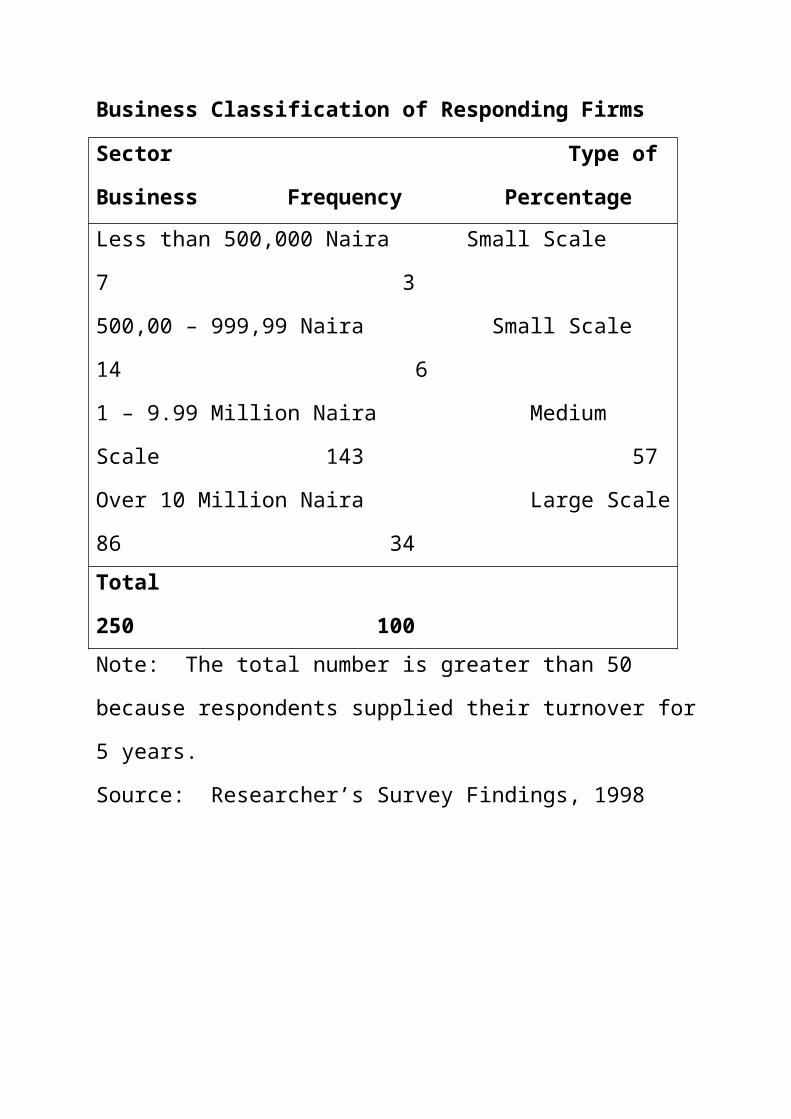

In this study, businesses are classified on the

basis of turnover. The author define small

scale businesses as companies with turnover not

exceeding 1,000,000 Naira, medium scale

business as having turnover between 1 Million

and 10 Million Naira and large scale businesses

as having turnover of over 10 Million Naira.

9 percent of the respondent companies can be

categorized as small scale, 58 percent as

medium scale and 34 percent as large scale

businesses (see table 3).

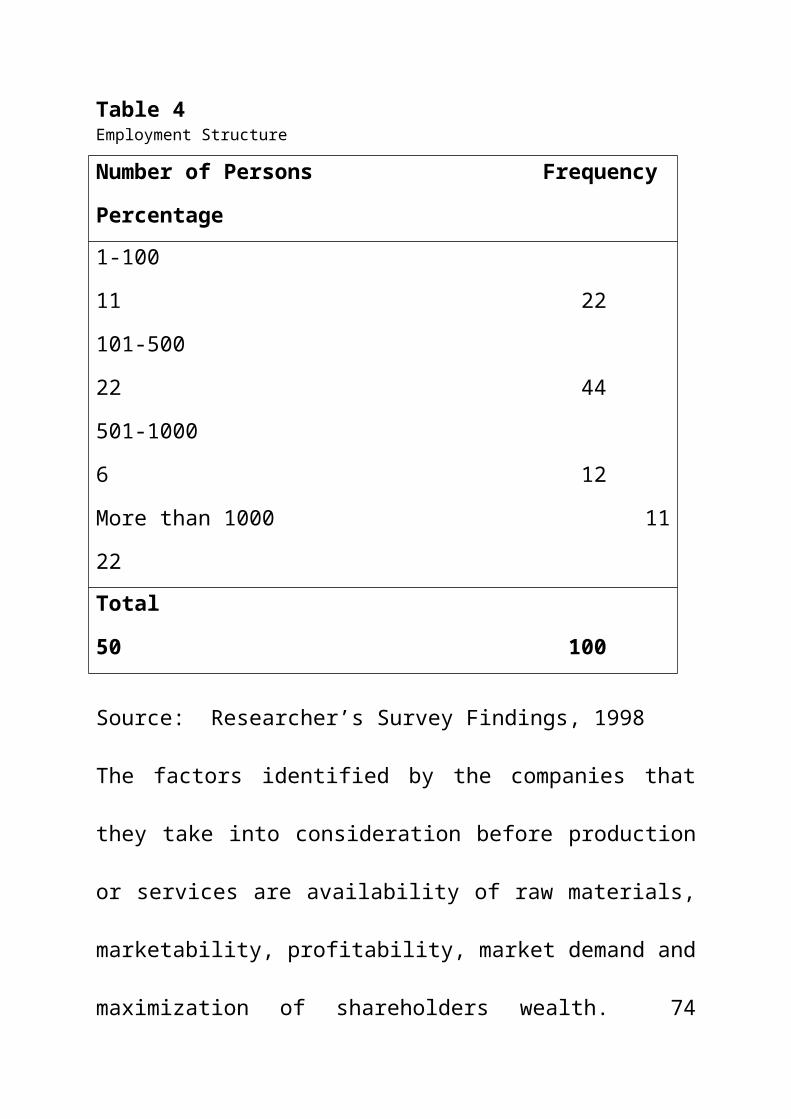

22 percent of the responding firms have more

than 1000 staff, 12 percent have between 501

and 1000 staff, 44 percent and 22 percent have

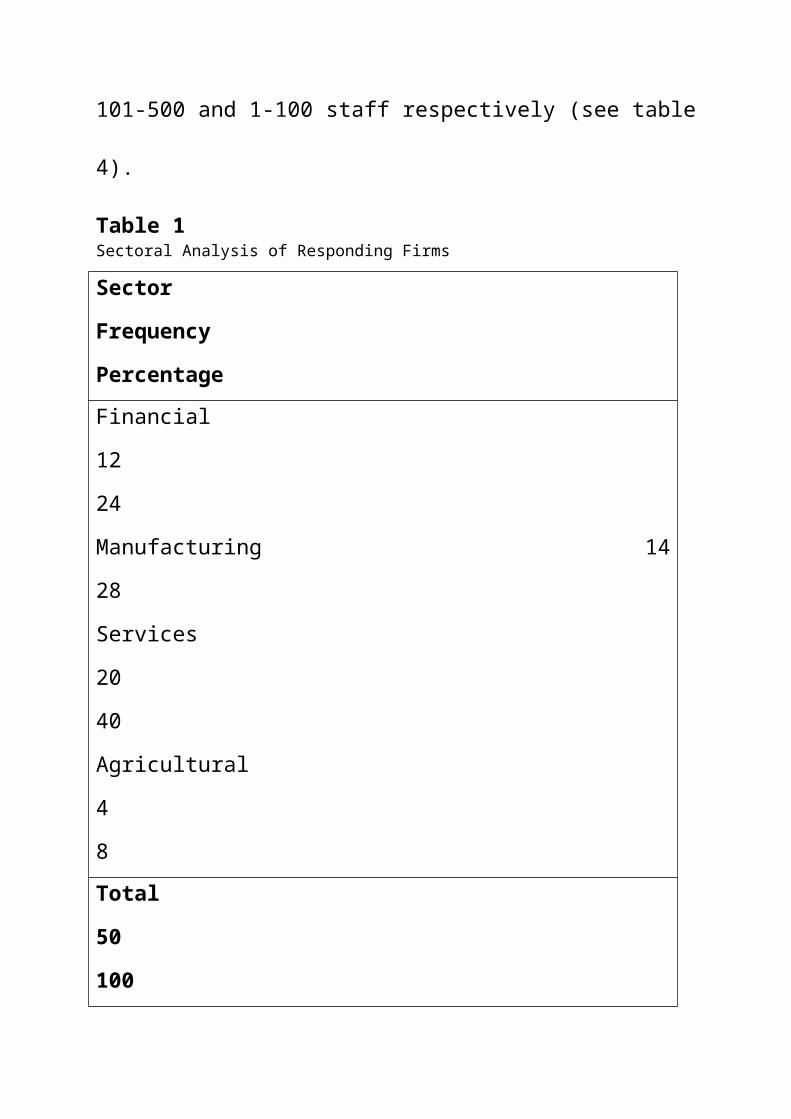

101-500 and 1-100 staff respectively (see table

4).

Table 1Sectoral Analysis of Responding Firms

Sector

Frequency

PercentageFinancial

12

24

Manufacturing 14

28

Services

20

40

Agricultural

4

8 Total

50

100

Source: Researcher’s Survey Findings, 1998.

Table 2Years of Existence of Responding Firms

Period

Frequency

Percentage1-5 years

8

16

6-10 years

11

22

More than 10 years 31

62 Total

50

100

Source: Researcher’s Survey Findings, 1998

Table 3

Business Classification of Responding Firms

Sector Type of

Business Frequency PercentageLess than 500,000 Naira Small Scale

7 3

500,00 – 999,99 Naira Small Scale

14 6

1 – 9.99 Million Naira Medium

Scale 143 57

Over 10 Million Naira Large Scale

86 34Total

250 100Note: The total number is greater than 50

because respondents supplied their turnover for

5 years.

Source: Researcher’s Survey Findings, 1998

Table 4Employment Structure

Number of Persons Frequency

Percentage1-100

11 22

101-500

22 44

501-1000

6 12

More than 1000 11

22Total

50 100

Source: Researcher’s Survey Findings, 1998

The factors identified by the companies that

they take into consideration before production

or services are availability of raw materials,

marketability, profitability, market demand and

maximization of shareholders wealth. 74

percent of the companies claimed that they have

a management accounting department while, 26

percent do not have. However, an average of 98

percent of the responding companies claimed to

have a section in their organization that is

responsible for formulation of policies,

directing, organizing, planning and controlling

of activities. Where there is no management

accounting department, such activities are

carried out in the finance or accounts section.

12 percent of respondent companies have over

fifty staff in the Management Accounting

Department (MADEP), 30 percent have between 10

and 50 staff. 38 percent of the MADEP is

headed by a chartered Accountant, 18 percent by

master’s holders and 26 percent by first

degree/higher diploma holder. 14 percent and

52 percent of respondent companies have 6 to 10

and 1 to 5 departments respectively. In most

of the questionnaires analyzed, the head of

management accounting division reports to the

financial controller who in turn reports to the

managing director.

22 percent of the responding companies have

less than 100 staff, 44 percent have between

101 and 500 staff, 12 percent have between 501

and 1000 staff members, while 22 percent have

more than 1000 employees.

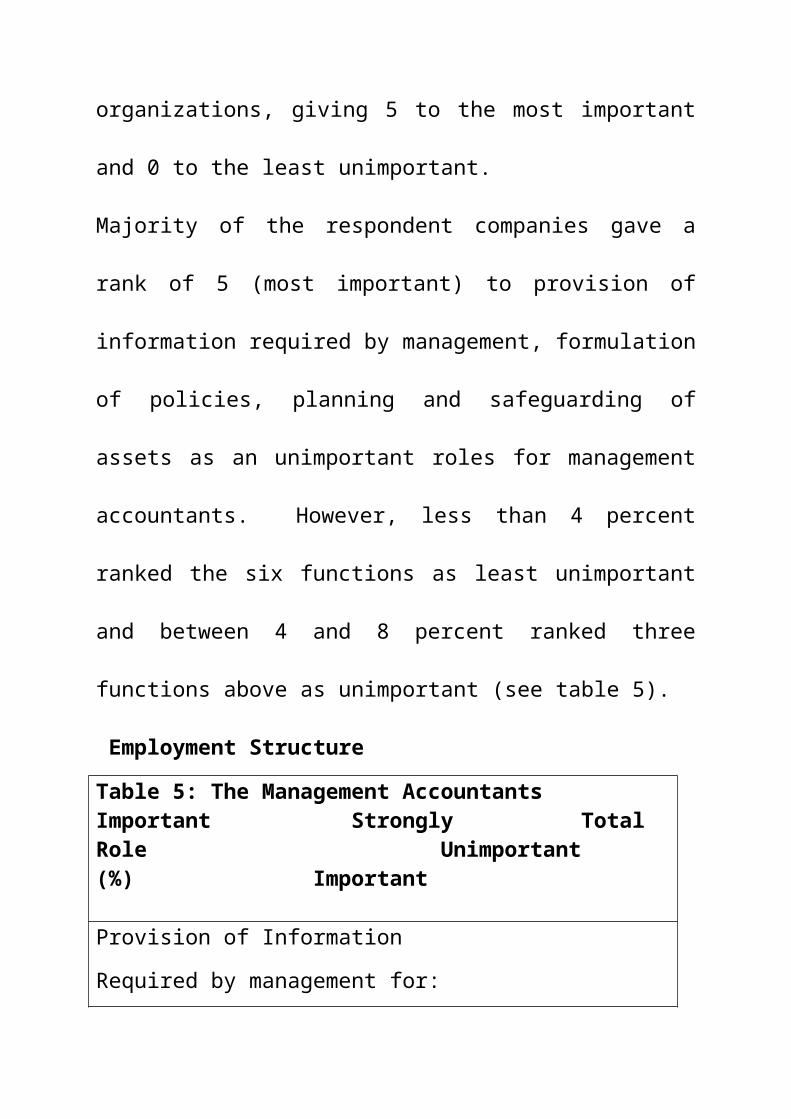

4.2 Present Functions of Managing Accountants

Companies were given six scales (0-5) to rank

the role of management accountants in their

organizations, giving 5 to the most important

and 0 to the least unimportant.

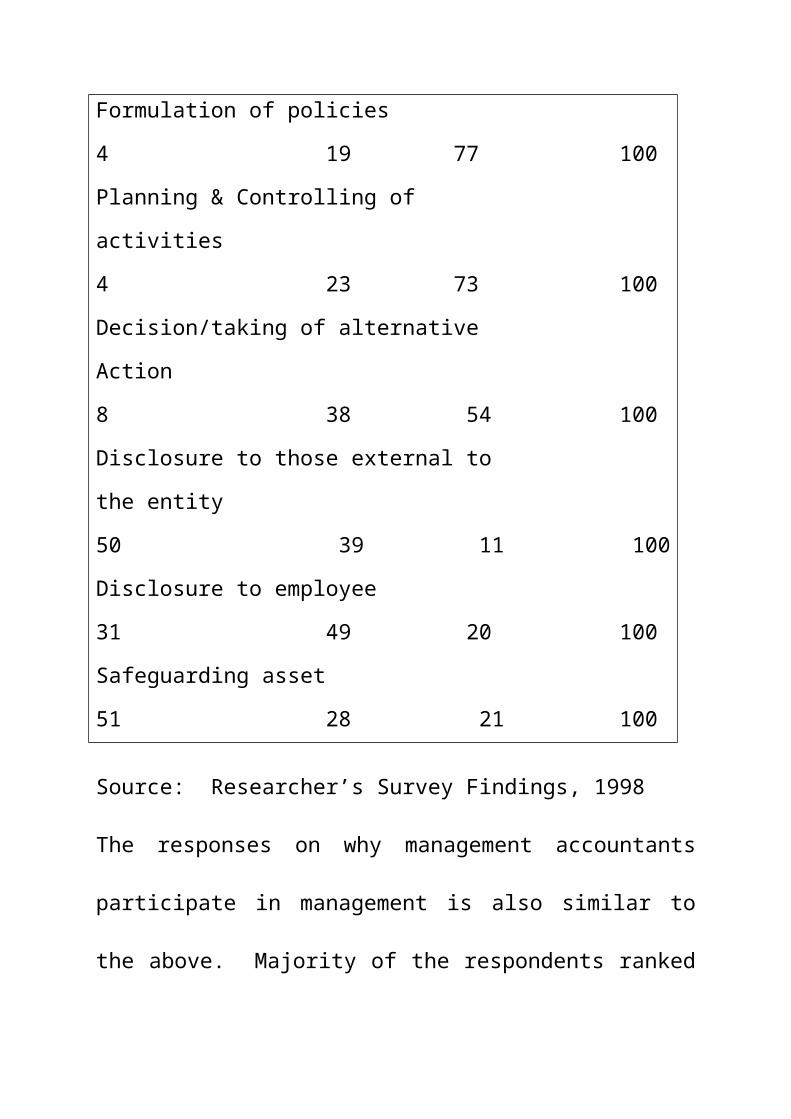

Majority of the respondent companies gave a

rank of 5 (most important) to provision of

information required by management, formulation

of policies, planning and safeguarding of

assets as an unimportant roles for management

accountants. However, less than 4 percent

ranked the six functions as least unimportant

and between 4 and 8 percent ranked three

functions above as unimportant (see table 5).

Employment Structure

Table 5: The Management Accountants Important Strongly Total Role Unimportant (%) Important

Provision of Information

Required by management for:

Formulation of policies

4 19 77 100

Planning & Controlling of

activities

4 23 73 100

Decision/taking of alternative

Action

8 38 54 100

Disclosure to those external to

the entity

50 39 11 100

Disclosure to employee

31 49 20 100

Safeguarding asset

51 28 21 100

Source: Researcher’s Survey Findings, 1998

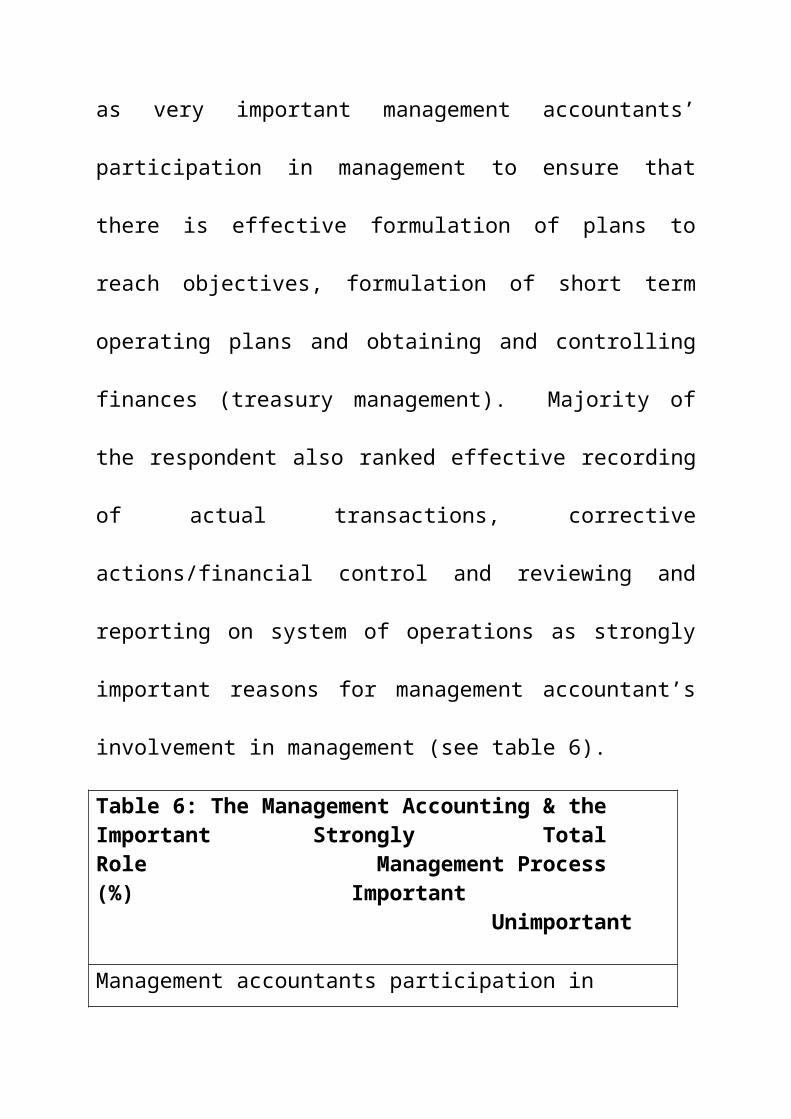

The responses on why management accountants

participate in management is also similar to

the above. Majority of the respondents ranked

as very important management accountants’

participation in management to ensure that

there is effective formulation of plans to

reach objectives, formulation of short term

operating plans and obtaining and controlling

finances (treasury management). Majority of

the respondent also ranked effective recording

of actual transactions, corrective

actions/financial control and reviewing and

reporting on system of operations as strongly

important reasons for management accountant’s

involvement in management (see table 6).

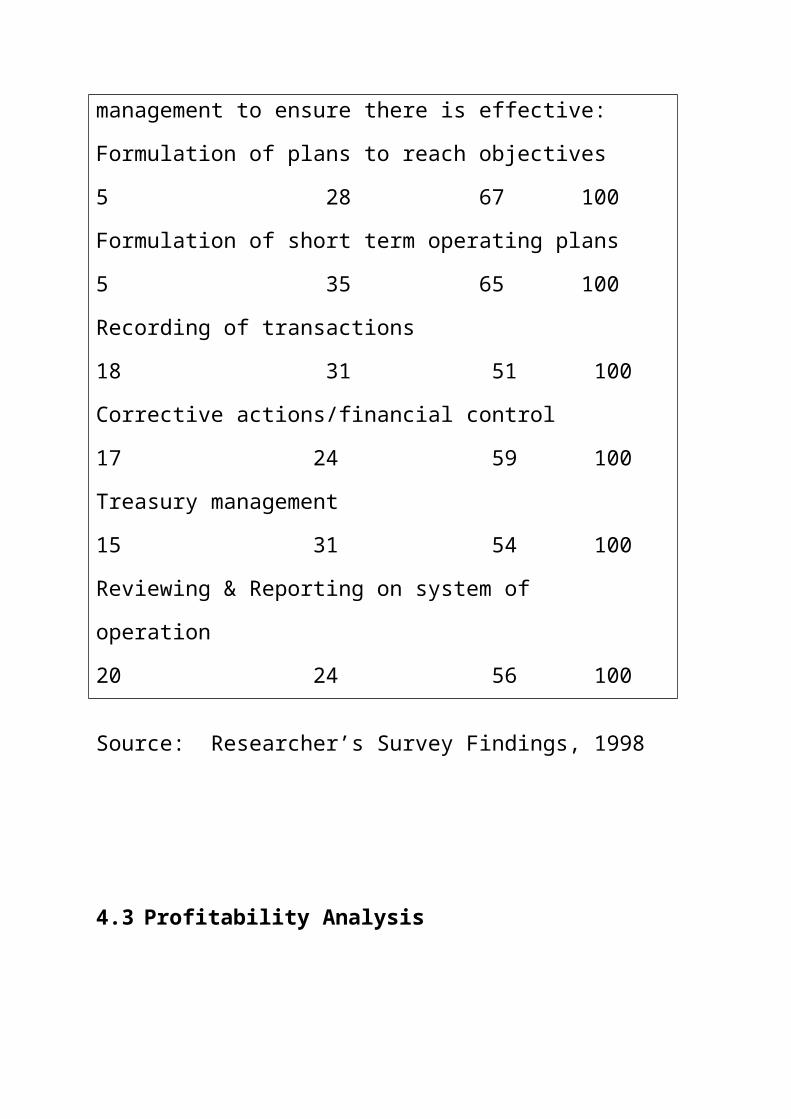

Table 6: The Management Accounting & the Important Strongly Total Role Management Process (%) Important Unimportant

Management accountants participation in

management to ensure there is effective:

Formulation of plans to reach objectives

5 28 67 100

Formulation of short term operating plans

5 35 65 100

Recording of transactions

18 31 51 100

Corrective actions/financial control

17 24 59 100

Treasury management

15 31 54 100

Reviewing & Reporting on system of

operation

20 24 56 100

Source: Researcher’s Survey Findings, 1998

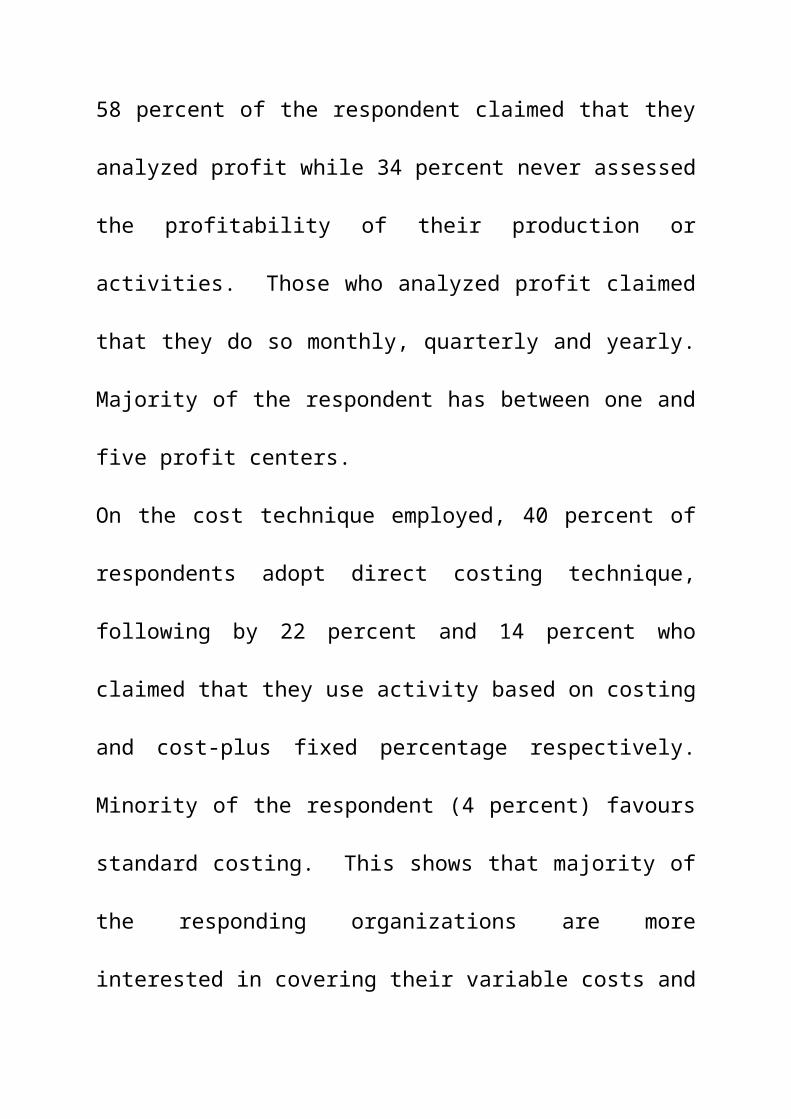

4.3 Profitability Analysis

58 percent of the respondent claimed that they

analyzed profit while 34 percent never assessed

the profitability of their production or

activities. Those who analyzed profit claimed

that they do so monthly, quarterly and yearly.

Majority of the respondent has between one and

five profit centers.

On the cost technique employed, 40 percent of

respondents adopt direct costing technique,

following by 22 percent and 14 percent who

claimed that they use activity based on costing

and cost-plus fixed percentage respectively.

Minority of the respondent (4 percent) favours

standard costing. This shows that majority of

the responding organizations are more

interested in covering their variable costs and

making contributions towards fixed costs and

profit. This is a good approach in the short

run. In the long run all cost must be covered

for a company to be a going concern.

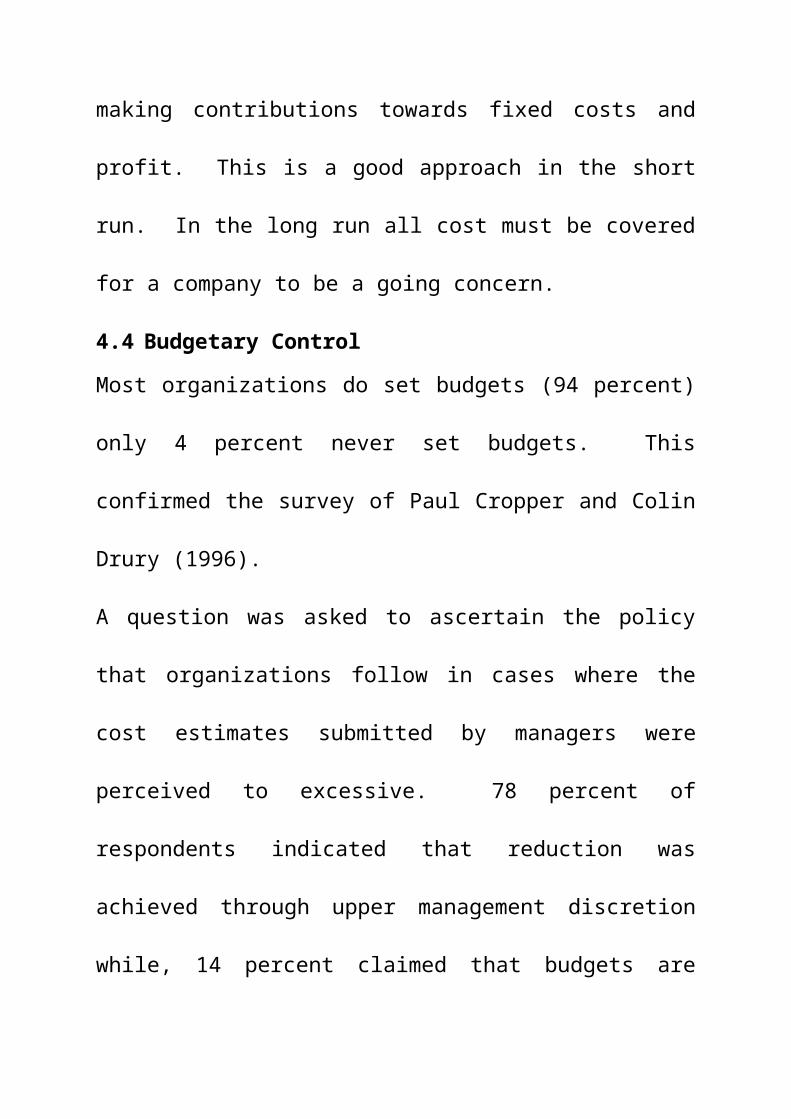

4.4 Budgetary Control

Most organizations do set budgets (94 percent)

only 4 percent never set budgets. This

confirmed the survey of Paul Cropper and Colin

Drury (1996).

A question was asked to ascertain the policy

that organizations follow in cases where the

cost estimates submitted by managers were

perceived to excessive. 78 percent of

respondents indicated that reduction was

achieved through upper management discretion

while, 14 percent claimed that budgets are

reduced through negotiation. However 8 percent

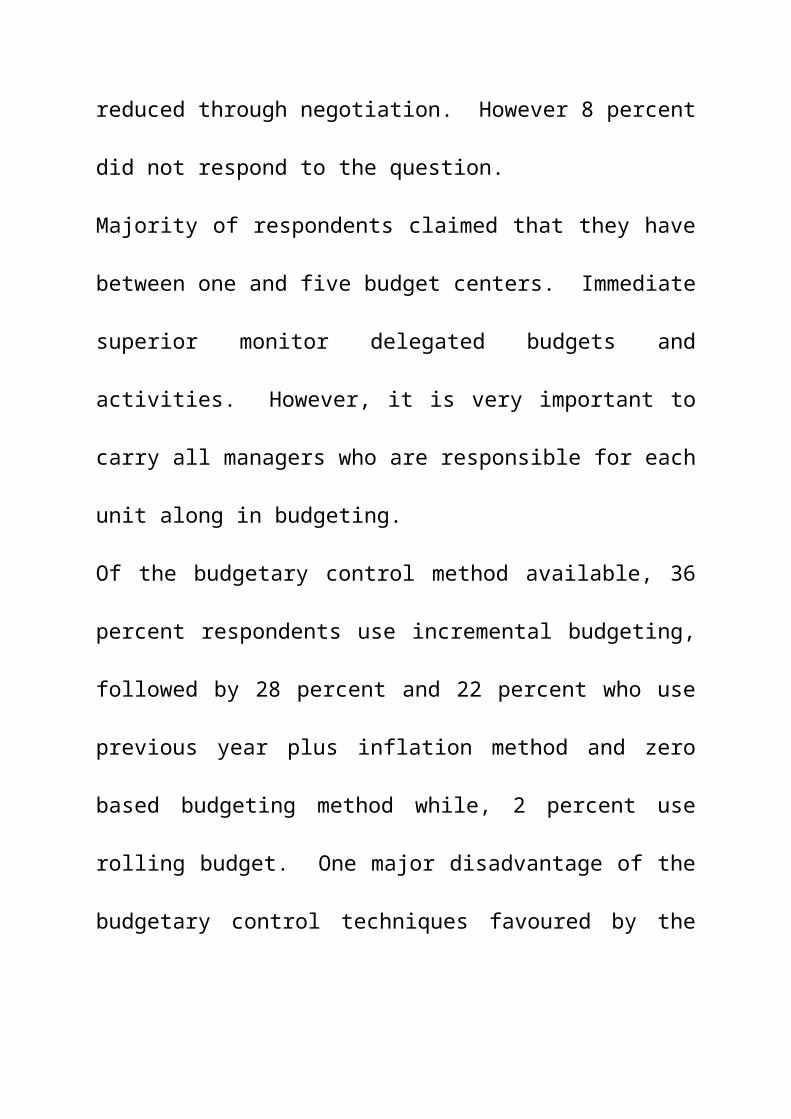

did not respond to the question.

Majority of respondents claimed that they have

between one and five budget centers. Immediate

superior monitor delegated budgets and

activities. However, it is very important to

carry all managers who are responsible for each

unit along in budgeting.

Of the budgetary control method available, 36

percent respondents use incremental budgeting,

followed by 28 percent and 22 percent who use

previous year plus inflation method and zero

based budgeting method while, 2 percent use

rolling budget. One major disadvantage of the

budgetary control techniques favoured by the

respondent is that past inefficiencies are

perpetuated.

4.5 Performance ReportingA question sought to ascertain how the

performance of managers are evaluated. 36

percent place a strong emphasis on a manager’s

success in meeting budgets, 42 percent

emphasized manager’s performance relative to

others within the organization, 30 percent and

24 percent respondents favoured manager’s

ability to control cost and financial

performance respectively. Only 14 percent of

respondents indicated that they compare their

manager’s performance relative to competitors.

4.6 Appraisal of Capital Budgeting Decisions

Majority of respondents (72 percent) indicated

that they appraised their capital investment

decisions. A combination of the investment

appraisal techniqu8es was favoured most. 18

percent and 14 percent of respondents favoured

return on capital employed and payback period

technique respectively. Only 12 percent, 6

percent and 4 percent respondents favoured net

present value, internal rate of return and

accounting rate of return respectively. A

reason for the high support of a combination of

all the investment appraisal technique could be

as a result of the different kind of investment

opportunities requiring different financing

methods.

4.7 Evolution and Change in Management Accounting

Practice in Nigeria4.7.1 Cost Determination and Financial

Control

94 percent of the responding companies claimed

that they set budget and 2 percent use rolling

budgets. 78 percent use upper management

discretion when cost activities is excessive.

4.7.2 Provision of Information

Environmental scanning by corporate firms for

opportunities, threats, weakness and strength,

choosing between alternatives, planning,

controlling and performance appraisal are

necessary and sufficient conditions for the

ultimate aim of maximizing profit and

shareholders’ wealth will be accomplished.

Majority of the responding firms has selections

providing information for management for

planning and controlling its operations among

others. Most of the respondents see

formulation of policies and planning and

controlling of activities as important roles of

management accountants.

Majority of respondent does not consider

disclosure to those external to the entity and

disclosure to employees as important functions

of management accounting.

4.7.3. Waste Reduction through process Analysis and Cost management Techniques

Management Accounting practice in Nigeria also

involves evaluation of performance on the basis

of performance relative to others in the

organization, ability to reduce cost and

financial performance.

4.8 Recent Changes

Majority of respondent (94 percent) claimed

that they perform management audit. Most

respondents (80 percent) review their

management/cost accounting system when need

arises. 21 percent have upgraded their

computers system, while 17 percent changed

their investment appraisal techniques. 11

percent have diversified their operations;

another 11 percent have streamlined operations.

14 percent and 13 percent have changed their

performance evaluation technique and budgeting

control technique.

4.9 Expected changes

Most respondents favoured reviewing of their

management accounting system when need arises.

22 percent favoured annual review of Management

Accounting System (MAS), while 12 percent

favour a further quarterly review. 28 percent

never or rarely do review.

A further question sought to ascertain the type

of change the company expected in the next

year.

Majority of the respondent expects a highly

computerized financial information system

manpower development, cost reduction and growth

induced policy, and overall economic change as

a result of political stability expected to be

brought about by the transition to civilian

rule.

On the expected role of management accounting

system in this millennium, respondents

indicated as highly important provisions of

timely information to support decision making,

improved cash flow, standard costing and

reduction in operating cost, financial

leadership and global networking.

Majority of respondents indicate that the

financial liberalization will have a positive

effect on their organization by improving

accessibility to fund and reduced cost of

capital, improvement of capital base, increase

in profit, expansion of operations, more

sensitivity to environmental issue and keen

competition.

In addition to the above respondents also

identified increased global competition,

increased profit and improved data availability

as expected effects of economic integration and

globalization on their companies. Most

respondents expect their return on investment

as a result of the new economic order to be

between 21 percent and 40 percent.

A question was asked to determine how

management accounting system (MAS) help in

creating value for the owners of the companies.

Respondents indicate that MAS helps to create

value by ensuring profitability analysis, cost

savings, control and reduction, planning and

controlling of the organizations operations,

provision of valuable, timely and accurate

information for sound decision. Ultimately,

MAS creates value for owners of the companies

by maximizing the value of the firm and the

returns on capital employed.

5 Summary and Conclusion

5.1 Summary of Findings

Management Accounting is a part of the

management process of organizations of Nigeria.

It is concerned with the process of cost

determination and financial control using

budgets and cost accounting technologies and

budgetary control techniques, provision of

information for management planning and control

and reduction of waste in business processes

through the use of decision analysis, and

responsibility accounting.

Management Accounting provides information

aimed at assisting management in formulation of

policies, directing, organizing, planning and

controlling of activities.

In addition to these, they participate in

management to ensure there are effective:

Formulation of plan to reach objectives,

Formulation of short term operating plans,

Recording of actual transactions,

Corrective actions /Financial control,

Obtaining and controlling finance/Treasury and

Reviewing and reporting on System of

Operations.

It has also evolved to reduce cost through

evaluation of managers on the basis of cost

control and reduction.

80 per cent of the responding firms claim that

they review their Management/Cost Accounting

System. Management Accounting in Nigeria is

still evolving and will continue to do so in

the future.

5.2 Conclusion

The results of the study shows that management

accounting practice in Nigeria has fully passed

the second phase for most companies, and has

only evolved into the third and forth phase for

few companies. However, in majority of the

case studied, management accounting practice is

just evolving into the third phase.

Management Accounts are more involved in

producing information aimed at assisting

management in the formulation of policies,

directing, organizing, planning and controlling

of activities. The body of thought and practice

encompassed by management accounting has

changed and evolved in Nigeria and it will

continue to do so.

However, the third and forth phase of

management accounting process is described by

reference to leading edge practice of large

corporate firms internationally.

Each stage is a combination of the old reshaped

to fit with the new in addressing a new set of

conditions in the management environment.

Footnotes

1) The exchange rate is 100 naira to 1 US dollar and 160 naira to 1 UK pounds.

References

Abrahammson, G and Helin, S (2000):

“Continuous Improvement-Work

Under Ambiguity-the Role of

Management Accounting Control”, a

paper presented at the 23rd Annual

Conference of The European

Accounting Association, in Munich,

Germany, March 29-31, 2000.

Appleyard, T and Pallet, S (2000): “Management

Accounting Issues in

Cross-Border Acquisitions: Evidence

from an Anglo-

German Case Study a paper presented

at the 23rd Annual Conference of the

European Accounting Association, in

Munich, Germany, March 29-3, 2000.

Ax,C and Bjornenak, T (2000): The Bundling and

Diffusion of Management

Accounting Innovations - The Case

of the Balanced Scorecard in

Scandinavia”, a paper presented at

the 23rd Annual Conference of the

European Accounting Association, in

Munich, Germany, March 29-31, 2000.

Adelegan, O.J. (2000): “An Empirical Analysis

of the relationship between

Cash flow and Dividend Changes in

Nigeria”, a paper presented at the

23rd Annual Conference of the

European Accounting Association, in

Munich, Germany, March 29-31, 2000.

Akinyewre, A. (1998): “Management Information

System: Concepts and

Development”. The accountant,

July/Sept., Vol. 31, no3 p.14-18.

Allen, D. (1993): “Strategic Financial

Management”. The Nigerian

Accountant, Vol. 26, no.3

July/Sept. p.9-11.

Baxter, W. (1989): “Asset and Liability

Values”, The Nigerian, Vol. 27 no.4.

Bescos P and Mendoza, C (2000): “Management

Accounting and Decision

Making: Why Managers’ Need

Information”. A paper presented at

The 23rd Annual Conference of the

European Accounting Association in

Munich, Germany, March 29-31, 2000.

Cropper P. and Drury C. (1996): “Management

Accounting Practice in

Universities, CIMA Management.

Accounting, Feb1996. p.28-30, Vol.

74,no.2.

Ekpeyong D.B and Nyong M.O (1992): “Small and

Medium-Scale

Enterprises in Nigeria: Their

Characteristics, problems and

sources of finance”, African

Economic Research Consortium,

Research Paper 16, Dec. 1992

Federal Government of Nigeria (1990):

“Companies and Allied Matters

Decree, 1990, Federal Government of

Nigeria, 1990.

International Federation of Accountants (1998):

International Management

Accounting Practice Statement #1.

Management Accounting Concept,

Financial and Management accounting

Committee, March.

Innaga E.L. and Emenuga C (1996): “Taxation of

Financial Assets and

Capital Market Development in

Nigeria”, African Economic Research

Consortium, Research Paper 47, Dec.

1996. Institute of Chartered

Accountants of Nigeria (1994):

Professional Conduct of Members,

ICAN, p 10-11

(1999): “Membership Yearbook ’98, ICAN, p.VI,.

(2000): “Auditing Guidelines for members of The

Public Practice Section

Planning and Control”, The Nigerian

Accountant, p 50-51, Vol.,33, No.2.

Lebas M.J. (2000): “Implications of revised

Statement #1 of the Finance

Management and Management

Accounting Committee (FMAC) of IFAC

on Practice and Education in

Managerial Accounting”,

International Management

Accounting’s Annual Conference,

June 25, 2000.

Sundem G.L (2000): “Comments on Management

accounting Concepts,

an International Management

accounting practice statement of

FMAC of IFAC”, International

Management Accounting’s Annual

Conference, June 25, 2000.

The Nigeria Stock Exchange (1999): “Fact book

1999, Walshad, Lagos,

NSE, p.10-31.

Ogwumike F.O. and Omole D.A. (1997):

“Mobilizing Dosmestic Resources for Economic

Research Consortium, Research Paper 56, Dec.

1997

Seed Khawaja A (1996): “Synergy: Concepts and

Relevance to

Management

Accounting”,

The Nigeria Accountant, Vol.29,

no.3, July/Srpt., pg.26-29.

Tricker, R.J. (1989): The Management Accountant

as Strategist, CIMA

Management

Accountancy, Vol. 67, no.11,

Dec., 1989 pg. 26-28.

Appendix

MANAGEMENT ACCOUNTING

SECTION A

1. What is the name of your Company?

2. When did it Commence Operation?

3. Number of Staff in the Company?

4. Major Production Activities?

5. What Factor do you take into account before

going into production/activities?

6. Do you have a management accounting

Department?

7. Do you have a section in your organization

for producing information aimed at

assisting Management in:

i. Formulation of Policies Yes/Noii. Directing Yes/Noiii. Organizing Yes/Noiv. Planning of Activities Yes/Nov. Controlling of Activities Yes/No

1. If yes to 7 above, how many staff are in

that department, and what is the

qualification of the head of the

department.

SECTION B

Please rank 0-5 in each of the following

functions, giving 5 to the most

important and 0 to the least unimportant

function in your organization:

Least

unimportant; 0 Important: 3

Unimportant: 1 Strongly Important: 4

Ambivalent: 2

Very Strongly Important: 5

2. Could you please rank the following factors

as functions of the Management Accounting in

your Organization?

a. Provision of information required by

Management/formulation of policies

b. Planning and Controlling of activities.

c. Decision/taking of alternative action.

d. Disclosure to those external to the entity.

e. Disclosure to Employee.

f. Safeguarding assets.

1. Please Rank 0-5 if the Management

accounting participate in Management to

ensure that there are effective: ……………….

a. Formulation of Plans to each objectives.

b. Formulation of short term operating plans.

c. Recording of actual Transactions.

d. Corrective actions/financial control.

e. Obtaining and Controlling finances –

Treasury

f. Reviewing and reporting on system of

operation.

1. Does your Company perform internal audit

and management audit?

2. What is the organizational structure of

your company? Make a sketch of it.

3. How many department or product unit do you

have?

4. Do you analyze profit made by each

department?

5. If yes to 14, how often

6. If not to question 14, why?

7. What type of costing techniques do you use

in your organization?

a. Directing Costing d. Activity

based costing

b. Full cost e. Any other

method… specify

c. Cost plus Fixed Percentage

8. Do your organization set budgets? Yes/No

9. If yes, which budgeting control method do

you use?...................

a. Previous Year Plus Inflation method

b. Incremental budgeting method

c. Zero based budgeting method

d. Any other method… specify

1. Which policy do you follow if the cost

activities submitted by any manager is

perceived to be excessive?

a. Negotiation b. Upper management

discretion

2. How many budget/profit centers do you have?

3. How do you monitor delegated budget?

4. How do you evaluate the performance of a

manager?....according to success….

a. Success in meeting budgets

b. Performance relative to others within

the organization?

c. Performance relative to competitors

inside the organization

d. Ability to control cost

e. Financial performance

f. Dismal performance

g. Any other……Specify

1. Do you use any technique to appraise

investment?

2. If yes, which one do you use?.............

a. Payback period technique e. Return on

Capital employed

b. Accounting rate of return f. Any

other specify

c. Net present value g. Combination

of some of the above, specify

d. Internal rate return

3. Do you review your management/cost

accounting systems

If yes, when?

If no, why…. Give reasons

4. Which type of change occurred…………..?

a. Handling of Management information

Yes/No

b. Investment appraisal techniques

Yes/No

c. Budgeting Control Technique

Yes/No

d. Performance Evaluation Technique

Yes/No

e. Upgrading of Computer System

Yes/No

f. Diversification

Yes/No

1. If yes to any of the above, to what extent

is the change?

2. How often do you intend to review your

management accounting system?

3. What type of change do you expect in the

next 5 years

4. What do you think are the expected role of

your management accounting

system (MAS) in the next millennium? Please

specify?

5. What effect will financial liberalization

have on your management accounting

system, please specify.

6. What effect will economic integration and

globalization have on your Management

Accounting system?

7. What is the expected rate of return on

investment of your company? Please specify

8. What was the turnover and profit of your

company for the past 5 years……?

YEAR PROFIT TURNOVER (SALES)19931994199519961997

How does your Management accounting systems

help to create value for the owner

of the company? Please specify………..

Related Documents