OVERVIEW: Industry: Alloys and Others: Stainless steel is essentially a steel alloy of iron (with a minimum of 10.5% chromium) which exhibits properties of exceptional strength, corrosion resistance, is malleable and ductile and therefore can be rolled into sheets, wires, tubes, plates etc. to cater to the demand of heavy industries, building & construction, consumer goods etc. As per Data Bridge Market Research, the global stainless steel market is an estimated value of USD143.03bn by 2026 registering a CAGR of 5.6% in the forecast period. Moreover, the Stainless Steel Forgings Market has been emerging as an astoundingly approved sector. Apart from the stainless steel alloys, the market has been trying to find low volume high value niche and innovative products. One of which are the Master Alloys. On the basis of the type of alloys produced, the market has been divided into chromium alloys, vanadium alloys, molybdenum alloys, copper master alloys, aluminium master alloys, etc. Among these, aluminium master alloys which are extensively used in automobiles and consumer goods industry are projected to hold the largest market share by 2024. On the basis of application, the market has been segmented into stainless steel, iron, titanium production, superalloys, aluminum industry, powder metallurgical, metal anhydride alloys etc. The market for high performance alloys is anticipated to grow at a gradual but steady growth rate. The growth is expected to arise due to increasing demand from the aerospace and defense industry. In addition to this, the oil & gas industry also has a significant market share and represents one of the major end-user industries for the high-performance alloys market. A large number of players across the globe are trying to tap the opportunities arising from the niche and innovative segment of exotic metal alloys. On the basis of market segmentation by types, exotic alloys can be classified as stainless steel, alloy steel and carbon steel while on the basis of applications; the same is classified as aerospace, automotive, energy field and others. A large number of market participants in the business of stainless steel alloys and super alloys are looking at exploring opportunities related to titanium and allied products. Titanium is a silver grey coloured metal which exhibits the properties of high melting point, corrosion resistant properties, good thermal properties and strength to weight ratio. Due to these superior properties, titanium is used in production of super light high speed aircrafts, satellites, space crafts and ships. Aerospace & aviation industry is the major end user of titanium. The global demand for titanium related products market will be propelled by rising demand in aircraft carriers, defence equipment’s and various other chemical processing industries such as oil & gas. Titanium and its alloys are highly compatible with carbon fiber which are known to improve the tensile strength of the aircraft frame and also provides excellent prevention to metal corrosion. Aerospace grade Ti-6Al-4V alloy typically consists of Vanadium (V) of 4 wt% and aluminium (Al) of 6 wt%.Titanium and its alloys also have high thermal coefficient which provides enhanced stability to the aircraft at high engine temperature. Moreover, Titanium alloys provide protection from galvanic corrosion in the joints of the aircraft. As a result of this, titanium alloys are replacing aluminium alloys and steel-based materials in areas where high strength is required. Titanium alloys also have applications in the marine industry where the same is used in ocean engineering for desalination pipes, offshore oil drilling pumps, valves, pipes etc. Titanium products exhibit properties like inertness to UV rays and self-cleaning properties and thus has applications in healthcare industry for making pacemakers, defibrillators etc. In addition to the properties mentioned earlier, titanium has anti-corrosion and biocompatible properties and ability to join with human bone; thus titanium becomes an essential element in the medical field, ranging from surgical titanium instruments to orthopaedic titanium rods, pins & plates and dental titanium. CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months SNAPSHOT 52 week H / L Mcap (INR mn) 160 / 100 22,986 Face value: 10 BSE Code NSE CODE 541195 MIDHANI Annual Performance (Rs mn) FY17 FY18 FY19 FY20E Total Revenue 7,733 6,617 7,108 8,087 EBITDA 1,853 1,909 1,837 2,123 EBITDA (%) 24.0 28.8 25.8 26.3 Other Income 234 292 369 370 Interest 47 86 64 69 Depreciation 177 196 232 298 PBT 1,864 1,919 1,911 2,126 PAT 1,263 1,312 1,306 1,424 Equity ( Rs mn) 1,873 1,873 1,873 1,873 EPS (INR) 7 7 7 8 Ratio Analysis Parameters (Rs mn) FY17 FY18 FY19 FY20E EV/EBITDA (x) 11.4 12.1 12.3 10.7 EV/Net Sales (x) 2.7 3.5 3.2 2.8 M Cap/Sales (x) 3.0 3.5 3.2 2.8 M Cap/EBITDA (x) 12.4 12.0 12.5 10.8 Debt/Equity (x) 0.1 0.2 0.3 0.2 ROCE (%) 24.5 22.4 17.7 16.2 Price/Book Value (x) 3.3 2.9 2.8 2.5 P/E (x) 18.2 18.4 17.6 16.2 Shareholding Pattern as on 31st March, 2019 Parameters No of Shares % Promoters 138,631,600 74.00 Institutions 37,489,150 20.01 Public 11,219,250 5.99 TOTAL 187,340,000 100.00 Quarterly Performance Parameters (Rs mn) Jun-18 Sep-18 Dec-18 Mar-19 Sales (Net) 1,060 1,152 1,532 3,364 EBITDA 211 348 172 1,107 EBITDA (%) 20 30 11 33 Other Income 66 44 135 124 Interest 12 11 18 22 Depreciation 52 60 60 60 PAT 118 208 169 795 Equity ( Rs mn) 1,873 1,873 1,873 1,873 Page No 1 Mishra Dhatu Nigam Limited July 09, 2019 PICK OF THE MONTH VOL-5, NO-5 Please Turn Over BUY Source: Annual Report Note: All the data is calculated as per Market Price on 08th July, 2019

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

OVERVIEW: Industry:

Alloys and Others:

Stainless steel is essentially a steel alloy of iron (with a minimum of 10.5%

chromium) which exhibits properties of exceptional strength, corrosion

resistance, is malleable and ductile and therefore can be rolled into sheets,

wires, tubes, plates etc. to cater to the demand of heavy industries, building

& construction, consumer goods etc. As per Data Bridge Market Research,

the global stainless steel market is an estimated value of USD143.03bn by

2026 registering a CAGR of 5.6% in the forecast period. Moreover, the

Stainless Steel Forgings Market has been emerging as an astoundingly

approved sector.

Apart from the stainless steel alloys, the market has been trying to find low

volume high value niche and innovative products. One of which are the

Master Alloys. On the basis of the type of alloys produced, the market has

been divided into chromium alloys, vanadium alloys, molybdenum alloys,

copper master alloys, aluminium master alloys, etc. Among these,

aluminium master alloys which are extensively used in automobiles and

consumer goods industry are projected to hold the largest market share by

2024. On the basis of application, the market has been segmented into

stainless steel, iron, titanium production, superalloys, aluminum industry,

powder metallurgical, metal anhydride alloys etc.

The market for high performance alloys is anticipated to grow at a gradual

but steady growth rate. The growth is expected to arise due to increasing

demand from the aerospace and defense industry. In addition to this, the oil

& gas industry also has a significant market share and represents one of the

major end-user industries for the high-performance alloys market. A large

number of players across the globe are trying to tap the opportunities

arising from the niche and innovative segment of exotic metal alloys. On

the basis of market segmentation by types, exotic alloys can be classified as

stainless steel, alloy steel and carbon steel while on the basis of

applications; the same is classified as aerospace, automotive, energy field

and others.

A large number of market participants in the business of stainless steel

alloys and super alloys are looking at exploring opportunities related to

titanium and allied products. Titanium is a silver grey coloured metal

which exhibits the properties of high melting point, corrosion resistant

properties, good thermal properties and strength to weight ratio. Due to

these superior properties, titanium is used in production of super light high

speed aircrafts, satellites, space crafts and ships. Aerospace & aviation

industry is the major end user of titanium. The global demand for titanium

related products market will be propelled by rising demand in aircraft

carriers, defence equipment’s and various other chemical processing

industries such as oil & gas. Titanium and its alloys are highly compatible

with carbon fiber which are known to improve the tensile strength of the

aircraft frame and also provides excellent prevention to metal corrosion.

Aerospace grade Ti-6Al-4V alloy typically consists of Vanadium (V) of 4

wt% and aluminium (Al) of 6 wt%.Titanium and its alloys also have high

thermal coefficient which provides enhanced stability to the aircraft at high

engine temperature. Moreover, Titanium alloys provide protection from

galvanic corrosion in the joints of the aircraft. As a result of this, titanium

alloys are replacing aluminium alloys and steel-based materials in areas

where high strength is required. Titanium alloys also have applications in

the marine industry where the same is used in ocean engineering for

desalination pipes, offshore oil drilling pumps, valves, pipes etc. Titanium

products exhibit properties like inertness to UV rays and self-cleaning

properties and thus has applications in healthcare industry for making

pacemakers, defibrillators etc. In addition to the properties mentioned

earlier, titanium has anti-corrosion and biocompatible properties and ability

to join with human bone; thus titanium becomes an essential element in the

medical field, ranging from surgical titanium instruments to orthopaedic

titanium rods, pins & plates and dental titanium.

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

SNAPSHOT

52 week H / L Mcap (INR mn)

160 / 100 22,986

Face value: 10

BSE Code NSE CODE

541195 MIDHANI

Annual Performance

(Rs mn) FY17 FY18 FY19 FY20E

Total Revenue 7,733 6,617 7,108 8,087

EBITDA 1,853 1,909 1,837 2,123

EBITDA (%) 24.0 28.8 25.8 26.3

Other Income 234 292 369 370

Interest 47 86 64 69

Depreciation 177 196 232 298

PBT 1,864 1,919 1,911 2,126

PAT 1,263 1,312 1,306 1,424

Equity ( Rs mn) 1,873 1,873 1,873 1,873

EPS (INR) 7 7 7 8

Ratio Analysis

Parameters (Rs mn) FY17 FY18 FY19 FY20E

EV/EBITDA (x) 11.4 12.1 12.3 10.7

EV/Net Sales (x) 2.7 3.5 3.2 2.8

M Cap/Sales (x) 3.0 3.5 3.2 2.8

M Cap/EBITDA (x) 12.4 12.0 12.5 10.8

Debt/Equity (x) 0.1 0.2 0.3 0.2

ROCE (%) 24.5 22.4 17.7 16.2

Price/Book Value (x) 3.3 2.9 2.8 2.5

P/E (x) 18.2 18.4 17.6 16.2

Shareholding Pattern as on 31st March, 2019

Parameters No of Shares %

Promoters 138,631,600 74.00

Institutions 37,489,150 20.01

Public 11,219,250 5.99

TOTAL 187,340,000 100.00

Quarterly Performance

Parameters (Rs mn) Jun-18 Sep-18 Dec-18 Mar-19

Sales (Net) 1,060 1,152 1,532 3,364

EBITDA 211 348 172 1,107

EBITDA (%) 20 30 11 33

Other Income 66 44 135 124

Interest 12 11 18 22

Depreciation 52 60 60 60

PAT 118 208 169 795

Equity ( Rs mn) 1,873 1,873 1,873 1,873

Page No 1

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

Please Turn Over

BUY

Source: Annual Report

Note: All the data is calculated as per Market Price on 08th July, 2019

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

BUY

OVERVIEW: Industry (contd.)

GOI Push:

The GOI has been constantly contemplating to give a push to the steel industry in India. In an attempt to curb the imports of

stainless steel products and continue on the same path to push the ‘Make in India’ project, the GOI has imposed an additional 2.5%

customs duty on imported stainless steel and other alloy steel products in the recent budget proposals in July 2019. Thus, the same

activity will be attracting customs duty of 7.5% from the earlier 5%.

In the recent budget speech in July 2019, Union Finance Minister Nirmala Sitharaman lauded the Indian space power. As per

reports, India has emerged as a major space power house with technology and ability to launch satellites and other space products at

globally low cost. This will pave way to harness the ability for commercial production. The new company New Space India Limited

(NSIL) is intended to tap the benefits of the R&D carried out by Indian Space Research Organisation (ISRO) as also spearhead

commercialisation of various space products. On the other hand, it has been reported that space agency wants to give a big push for

production of the Small Satellite Launch Vehicle (SSLV) where the demand for the same is anticipated to be about two to three

rockets per month. In the long run, the vision is also to increase the production of Polar Satellite Launch Vehicle (PSLV). ISRO has

been constantly developing technologies, materials, chemicals etc. which can be transferred to companies. In addition to

commercialising launch vehicles, NSIL will also help the transfer of technology and marketing space market products. Moreover,

one must also not forget while presenting the interim budget, Mr. Piyush Goyal had pointed out to the seventh dimension of vision

for the next decade aiming at the outer skies under the space programme viz Gaganyaan.

As per a recent article in The Times of India in May 2019, quoted, the Centre has made it mandatory for all Defence PSUs (DPSUs)

to initiate projects related to Artificial Intelligence (AI). The Ministry of Defence (MoD) has realized the potential of AI and has

already formed a special committee under the guidance of the Chairman of Tata Sons to look into the feasibility and adaptation of

AI for various industrial applications. This clearly is a strategy initiated by GOI to enhance defence capabilities by inducing new

state-of-the-art equipments. To start with, BEL has decided to invest around Rs400mn to Rs500mn per annum on AI-related projects

in the coming three years. Along with Hindustan Aeronautics Limited (HAL), six other DPSUs i.e. Bharat Dynamics Limited

(BDL), BEML Ltd; Mishra Dhatu Nigam Ltd (MIDHANI); Mazagon Dock Shipbuilders Ltd (MDL); Garden Reach Shipbuilders &

Engineers Ltd (GRSE); Goa Shipyard Ltd (GSL) and Hindustan Shipyard Ltd (HSL) are also taking up projects in AI.

A new trend of recycling higher volume and greater variety of scrap metals has been in vogue recently which also aims at efficient

and accurate sorting of specific alloy and grade of the material. Many companies across the globe are finding this process lucrative

in bringing the issues related to cost of raw materials down. Thus, this is a small strategically approach to minimise risk and

maximizing profits in a small way.

Page No 2 Please Turn Over

Exhibit 01: Product Range

Source: http://www.midhani-india.in/doc/processflow1.pdf

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

BUY

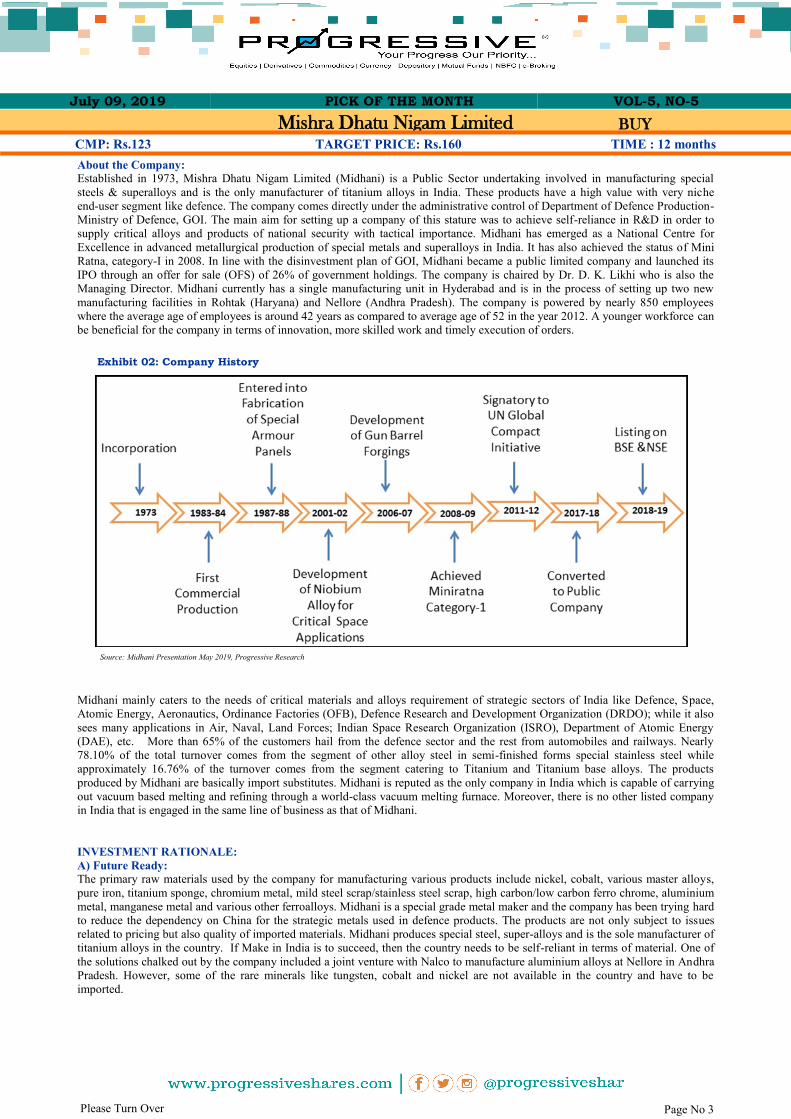

About the Company:

Established in 1973, Mishra Dhatu Nigam Limited (Midhani) is a Public Sector undertaking involved in manufacturing special

steels & superalloys and is the only manufacturer of titanium alloys in India. These products have a high value with very niche

end-user segment like defence. The company comes directly under the administrative control of Department of Defence Production-

Ministry of Defence, GOI. The main aim for setting up a company of this stature was to achieve self-reliance in R&D in order to

supply critical alloys and products of national security with tactical importance. Midhani has emerged as a National Centre for

Excellence in advanced metallurgical production of special metals and superalloys in India. It has also achieved the status of Mini

Ratna, category-I in 2008. In line with the disinvestment plan of GOI, Midhani became a public limited company and launched its

IPO through an offer for sale (OFS) of 26% of government holdings. The company is chaired by Dr. D. K. Likhi who is also the

Managing Director. Midhani currently has a single manufacturing unit in Hyderabad and is in the process of setting up two new

manufacturing facilities in Rohtak (Haryana) and Nellore (Andhra Pradesh). The company is powered by nearly 850 employees

where the average age of employees is around 42 years as compared to average age of 52 in the year 2012. A younger workforce can

be beneficial for the company in terms of innovation, more skilled work and timely execution of orders.

Midhani mainly caters to the needs of critical materials and alloys requirement of strategic sectors of India like Defence, Space,

Atomic Energy, Aeronautics, Ordinance Factories (OFB), Defence Research and Development Organization (DRDO); while it also

sees many applications in Air, Naval, Land Forces; Indian Space Research Organization (ISRO), Department of Atomic Energy

(DAE), etc. More than 65% of the customers hail from the defence sector and the rest from automobiles and railways. Nearly

78.10% of the total turnover comes from the segment of other alloy steel in semi-finished forms special stainless steel while

approximately 16.76% of the turnover comes from the segment catering to Titanium and Titanium base alloys. The products

produced by Midhani are basically import substitutes. Midhani is reputed as the only company in India which is capable of carrying

out vacuum based melting and refining through a world-class vacuum melting furnace. Moreover, there is no other listed company

in India that is engaged in the same line of business as that of Midhani.

INVESTMENT RATIONALE:

A) Future Ready:

The primary raw materials used by the company for manufacturing various products include nickel, cobalt, various master alloys,

pure iron, titanium sponge, chromium metal, mild steel scrap/stainless steel scrap, high carbon/low carbon ferro chrome, aluminium

metal, manganese metal and various other ferroalloys. Midhani is a special grade metal maker and the company has been trying hard

to reduce the dependency on China for the strategic metals used in defence products. The products are not only subject to issues

related to pricing but also quality of imported materials. Midhani produces special steel, super-alloys and is the sole manufacturer of

titanium alloys in the country. If Make in India is to succeed, then the country needs to be self-reliant in terms of material. One of

the solutions chalked out by the company included a joint venture with Nalco to manufacture aluminium alloys at Nellore in Andhra

Pradesh. However, some of the rare minerals like tungsten, cobalt and nickel are not available in the country and have to be

imported.

Page No 3 Please Turn Over

Source: Midhani Presentation May 2019, Progressive Research

Exhibit 02: Company History

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

BUY

INVESTMENT RATIONALE:(contd.)

A) Future Ready: The products manufactured by Midhani are essentially low

volume and high value products. Currently Midhani is a single

location company and growth in the long run will come either by

exploring greenfield or brownfield developmental projects,

essentially focusing on further development of technologies.

Moreover, the company is currently looking at upgrading and

modernizing its existing manufacturing equipment’s and facilities

to fetch better operational efficiencies. Some of the new projects

planned by the company for the next three years include:

(a) Construction of spring manufacturing plant for manufacture

and supply of helical compression springs where railways and

earth moving equipment’s suppliers would the target

(b) Development of aero quality carbon fibers

(c) Exploring further opportunities in Tungsten powder etc.

Geographical expansion too is on the check list of the company

and Management intends to operate from multiple locations. The

company intends to start two new manufacturing units based at

Rohtak (Haryana) and Nellore (Andhra Pradesh).

Besides the ones mentioned above, Management has also laid down ambitious projects including:

(a) Armour Project: the company aims to provide bullet proof products where Defence Forces and Central Armed Police Forces

are their target audience. In pursuit of the same, Midhani is setting up a dedicated Armour unit with full-fledged production capacity

and technological capabilities at IMT, Rohtak.

(b) Closed Die Forging Facility: the company plans to establish Closed Die Forging facility (in a phased manner). This facility will

provide opportunities to manufacture and supply specific value added products with complex shapes through closed die forging

route. Major capital equipment procurement is currently under process.

(c) Tungsten & Tungsten Carbide Powder Production Facilities: Tungsten powder is the main ingredient for production of high

kinetic energy penetrators and pre-fragments for Defence applications which is currently imported. Moreover, there is a huge

potential market for Tungsten Carbide powder for making Cutting tools. With an aim to indigenise these materials, Midhani plans to

establish facilities and cater to the demand. The company has partnered with another PSU i.e. NMDC Limited and was in

discussions with a Vietnam-based company Masan Resources to acquire minority stake in a Tungsten mine.

(d) Carbon Fiber Manufacturing: Midhani has also proposed to set up a Carbon Fiber production plant to fulfill and meet the

strategic requirements of our country.

(e) Aluminium Alloys Plant: the company has signed a MoU with NALCO for setting up High end Aluminium Alloys Production

plant. Land for the greenfield project which is around 110 acres is allotted by the Andhra Pradesh government through Andhra

Pradesh Industrial Infrastructure Corporation (APIIC).

Thus, all these upcoming projects and planned capex provides a visibility of growth in the next 2-3 years.

Page No 4 Please Turn Over

Exhibit 04: High-end Engineering Application

Source: Midhani Presentation May 2019, Progressive Research

Exhibit 03: Product Range

Source: Midhani Annual Report FY2018, Progressive Research

Source: Midhani Presentation May 2019, Progressive Research

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

BUY

INVESTMENT RATIONALE: (B) Make In India:

In January 2019, Midhani signed an agreement (non-equity) to work

together on development and production of advanced materials for the

energy sector with Tubacex, a Spanish multinational. The agreement

essentially aims at fostering technological alliance and promotion of

local manufacturing capacities which will be used for both domestic

consumption as well as export markets. India has immense potential of

becoming a world leader in the development of nuclear energy, if the

issues related to the industry in terms of safety, quality and energy

efficiency are dealt properly. On the other, Tubacex sees immense

potential in some key multi annual projects via the strategic tie-up.

Earlier in 2015, Tubacex had entered India through the acquisition of

Prakash Steelage, a Gujarat based company. Tubacex has nearly 20

manufacturing plants spread across various markets and is looking at

further expansion. Exports account for nearly 80% of the production for

them. Once again, keeping the Make in India project in sight, the

agreement will not only help boost the country’s domestic requirements but also propel exports to other markets. In the initial stage,

the alliance intends to focus on oil & gas and energy sectors and later focus on other energy efficiency segments. The joint

development would also allow exploring the potential of advanced materials for the energy sector which particularly would focus on

super critical power projects and promotion of local manufacturing capacities at the same time.

In May 2019, Hindustan Shipyard Limited (HSL), Bharat Heavy Electricals Limited (BHEL) and Mishra Dhatu Nigam Ltd

(Midhani) have recently come together to float a consortium for building submarine. These three firms have come together to

express their interest in building six submarines. Under the Make in India campaign and in line with the intend of indigenous

construction of these conventional submarines is envisaged by Ministry of Defence (MoD). The agreement also intends to combine

the expertise of the three companies and construct the submarines domestically.

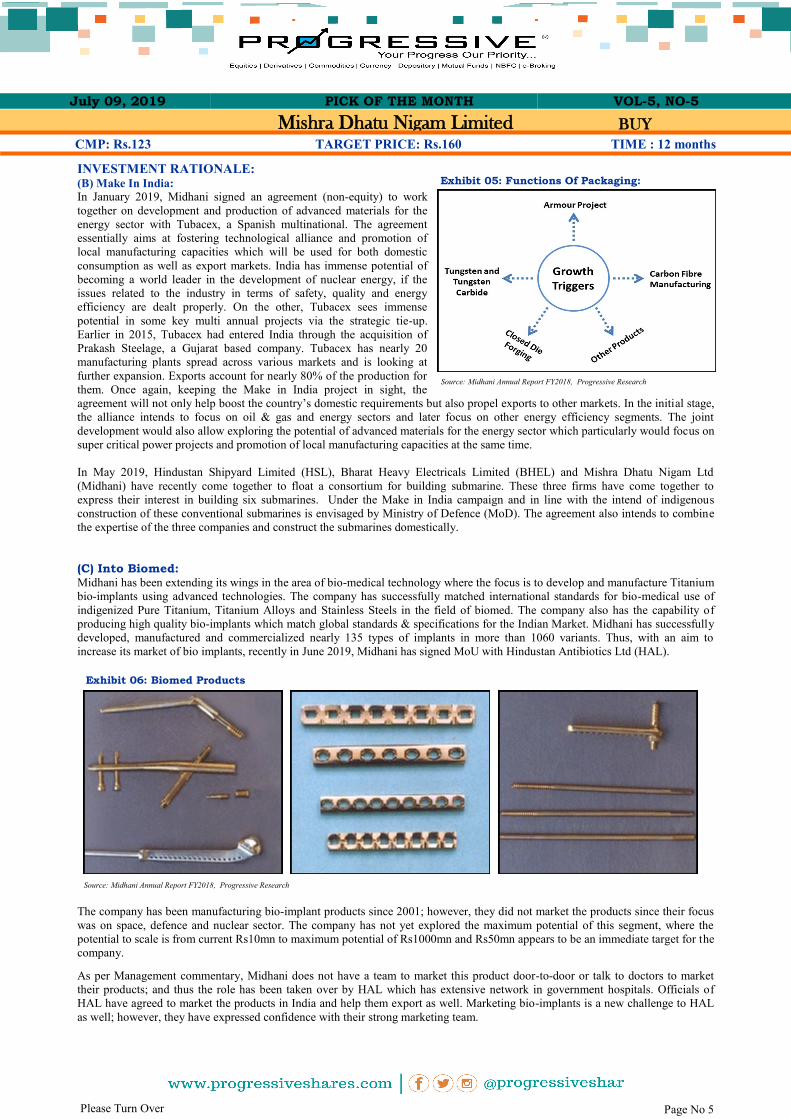

(C) Into Biomed: Midhani has been extending its wings in the area of bio-medical technology where the focus is to develop and manufacture Titanium

bio-implants using advanced technologies. The company has successfully matched international standards for bio-medical use of

indigenized Pure Titanium, Titanium Alloys and Stainless Steels in the field of biomed. The company also has the capability of

producing high quality bio-implants which match global standards & specifications for the Indian Market. Midhani has successfully

developed, manufactured and commercialized nearly 135 types of implants in more than 1060 variants. Thus, with an aim to

increase its market of bio implants, recently in June 2019, Midhani has signed MoU with Hindustan Antibiotics Ltd (HAL).

The company has been manufacturing bio-implant products since 2001; however, they did not market the products since their focus

was on space, defence and nuclear sector. The company has not yet explored the maximum potential of this segment, where the

potential to scale is from current Rs10mn to maximum potential of Rs1000mn and Rs50mn appears to be an immediate target for the

company.

As per Management commentary, Midhani does not have a team to market this product door-to-door or talk to doctors to market

their products; and thus the role has been taken over by HAL which has extensive network in government hospitals. Officials of

HAL have agreed to market the products in India and help them export as well. Marketing bio-implants is a new challenge to HAL

as well; however, they have expressed confidence with their strong marketing team.

Page No 5 Please Turn Over

Exhibit 05: Functions Of Packaging:

Source: Midhani Annual Report FY2018, Progressive Research

Exhibit 06: Biomed Products

Source: Midhani Annual Report FY2018, Progressive Research

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

BUY

INVESTMENT RATIONALE:

(C) Into Biomed (contd.):

Furthermore, Midhani is reported to have undertaken design, development and supply of various types of custom-made shoulder

prosthesis, hinged knee joints and total femur prosthesis. The company has developed these bio-implants and prosthesis via

interaction with leading orthopaedic and surgical oncologists. Many of these products have been well received in the Medical

Industry. These have been appreciated by medical experts for their workmanship, quality, mechanical properties and (affordable)

pricing. Some analysts have estimated an annual worth to a tune of more than Rs2500mn. Midhani products are used by prominent

hospitals, Cancer Institutes in Chennai, Apollo Hospital, Kamineni Hospital, Osmania General Hospital, Gandhi Hospital in

Hyderabad, Tata Memorial Centre in Mumbai and many more institutes. With an objective to prevent inferior products from coming

into the market and to offer better Health Care to the patients, in a recent development, the Union Health Ministry has brought

Medical Devices under the Drugs and Cosmetics Act to safeguard the same. Bio Products by Midhani are approved by Drug Control

Authority for Bio-Implants & Prosthesis from Drug Administration Department, Andhra Pradesh. Midhani has the capacity and

capability to meet the requirement for the critical orthopaedic implants in India.

In a recent newspaper article, the Management also cited about company’s future plans to foray into stents used in cardiac medical

surgeries. These products are currently in the evaluation phase of R&D and will be launched once the company has enough

evaluation data. Moreover, the Management also mentioned about Kazakhstan government via UKTMP (a representative firm of the

country) expressing its willingness in collaborating with Midhani to produce bio-implants, which is subject to due diligence and

viability of such projects and developments if any. This clearly looks like a strategy to mitigate risks, when the defence orders could

be sluggish.

(D) Expansion-cum-Diversification:

There are no two thoughts that Midhani is on an expansion-cum-diversification mode. The company is reported to have being

setting up an integrated plate mill, a 3D printing facility for alloy powders & carbon fibre materials and is at an advanced stage of

finalising plans for a Rs40bn unit with Nalco. In January 2019, the company was reported to be in the process of implementing

Rs5bn expansion plan, including Rs4bn versatile plate mill, a 3D printing facility along with other infrastructure upgradation across

units. The Rohtak facility of Midhani is being upgraded and expanded, the same is anticipated to finalise plans for a 3D printing

facility for material powders.

There is an outright growth in traction for value added downstream products related to aluminium related products. In recent

developments, Nalco has formed a joint venture with Midhani for the production of special alloys. The JV is anticipated to be named

Special Aluminium Company and the same has got the seal of approval from NITI Aayog as well. Funds for the same are

anticipated to be raised through a mix of debt and equity in the ratio of 70:30. Moreover, Nalco is seeking a technology partner who

can acquire up to 10% stake in the joint venture. (Source: Business Standard).

The company is in advance talks with NMDC and is hopeful its partner will complete the due diligence for finalising acquisition of

minority stake in a tungsten mine at in Vietnam. The two companies had signed up in 2016 to explore tungsten assets in India and

abroad with a view for investment and development and convert it to Ammonium Para Tungsten. Masan group of Vietnam which

operates a mine that produces big quantities of this strategic input used in defence applications. Midhani is in the process of setting

up a plant in Hyderabad which will enable them to make tungsten products which is independent of the progress with NMDC and its

acquisition of stake in Masan whereas NMDC stake buy will secure raw material.

In the long run, companies which are innovative and technologically advanced will survive while the rest will either dissolve or

merge with other advanced companies. With view of the necessary technological development Midhani is also focusing on new

process based technologies such as closed–die forgings, investment castings, isothermal forging and using special alloys to further

improve our existing products and add new products to our product portfolio.

Financials: The company is a low volume but a high value manufacturer of niche products. It will thrive well and earn profits through push on

value-added products and reduction in cost at the same time. Management intends to reduce, reuse and recycle to reduce dependence

on raw materials. Moreover, the Management also intends on retaining and increasing the existing market share and try to enter and

develop new products market.

Nearly 78.10% of the total turnover comes from the segment of other alloy steel in semi-finished forms special stainless steel while

approximately 16.76% of the turnover comes from the segment catering to Titanium and Titanium base alloys.

Both the Indian defence as a segment as well as ISRO appear to have very bright future as result of which the cumulative order book

position of Midhani as on 13th June 2019 is about Rs19bn, which clearly is providing a visibility of growth and a bright future for

the next two years atleast.

The Ebitda margins for the company over the last 3-4 years have been in the range of 24-28% while the Net profit margins have

been in the range of 15.5% to 18.0% in the last 3-4 years. There was sluggishness in the orders in the last 2 years; however, the same

seems to have been overcome. One may notice dividends shared by the company have been gradually increasing over the last

3-4 years. All these factors sum up to the positives of strong upcoming financial years.

Page No 6 Please Turn Over

CMP: Rs.123 TARGET PRICE: Rs.160 TIME : 12 months

Mishra Dhatu Nigam Limited

July 09, 2019 PICK OF THE MONTH VOL-5, NO-5

BUY

Risks and Concerns: Some of the critical raw materials such as nickel,

cobalt, tungsten etc. are imported by the company

from a number of countries like Russia, China and

Australia, which invites exposure to price volatility.

Any shortage in supply of the key raw materials will

lead to an increase in the prices of the products.

Along with this, the company with no doubt is

exposed to forex fluctuations which is difficult to

mitigate. This adds to little uncertainty in terms of

cash flows and revenues generated, thus affecting

the financial condition of the company. Another

major risk is the absolute dependence on ISRO and

other Indian Space explorers which account for

nearly 70% of the total revenues. The Management

has realised the same and is gradually trying to

de-risk this dependency on government orders.

Midhani has to constantly strive for timely and

satisfactory execution of the orders in hand as well

as at the same time develop new technologies. Thus,

one will witness constant volatility, uncertainty,

complexity and ambiguity in business going

forward as well.

Outlook and Recommendations:

The defence sector can many a times enter into a lull period in terms of order flows, which directly impacts all the players catering

to the industry. So one must be aware of this major risk, which is essentially related to the macro and then that related to the budget

allocations in this industry.

Innovation will remain the crux for growth of Midhani. Innovation in production processes along with optimum utilization of

available resources to reduce production costs will improve the profitability of the company. The company also proposes to focus on

new process based technologies such as Closed-Die Forgings, Investment Castings and Isothermal Forging. New products including

Carbon Fiber, Tungsten Powder and Armour products will also be some value additions products which the company has projected

to work on.

The company will not shy away from new collaborations that will help add new products to their portfolio. It seems to be taking

small steps towards exploring exporting opportunities. In order to mitigate the risks associated to undulating nature of the defence

orders; the company appears to have devised a plan to explore opportunities in the biomed division. Business development too will

be an add on to the overall turnover where new sectors like Railways, Oil & Gas, Automobile, Coal Fields etc. are identified by the

Management. All these factors tend to show a promising future for Midhani and thus a cushion for long term investments, thus we

initiate a BUY on the stock with a target price of Rs160 over a horizon of 12 months.

Page No 7

Source: Midhani Annual Report FY2018, Progressive Research

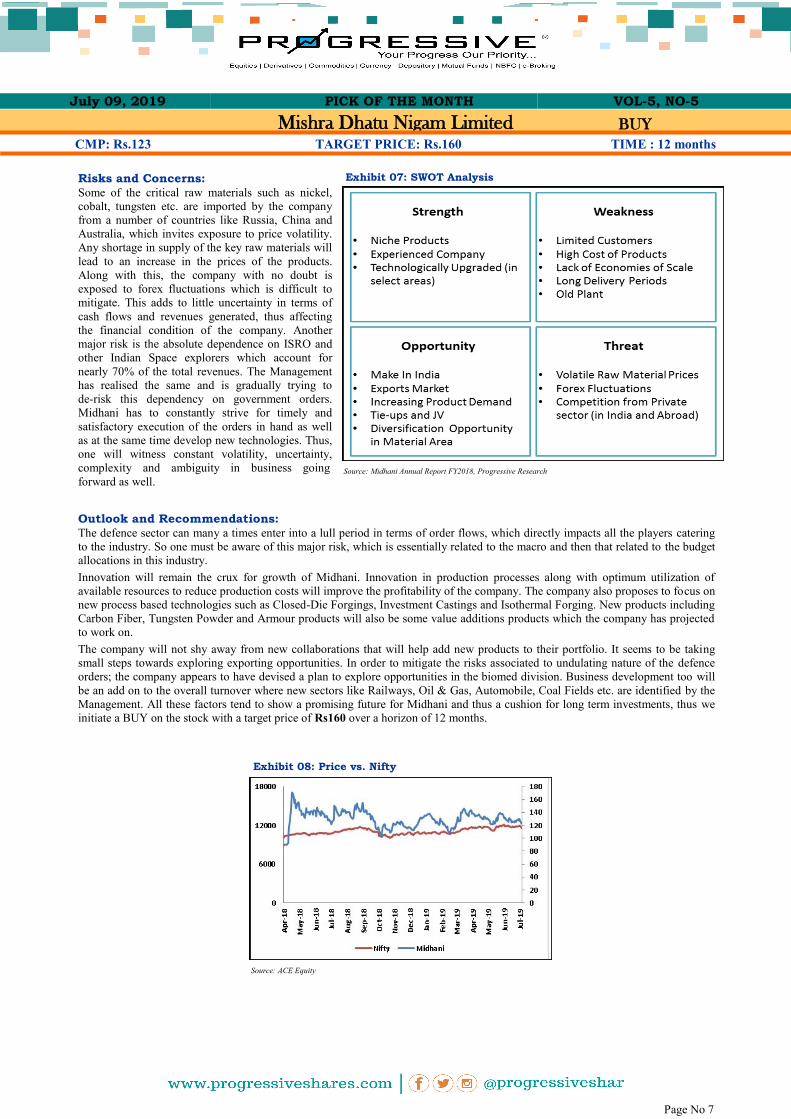

Exhibit 07: SWOT Analysis

Exhibit 08: Price vs. Nifty

Source: ACE Equity

DISCLAIMERS AND DISCLOSURES- Progressive Share Brokers Pvt. Ltd. and its affiliates are a full-service, brokerage and financing group. Progressive Share Brokers Pvt. Ltd. (PSBPL) along with its affiliates are participants in virtually all securities trading markets in India. PSBPL started its operation on the National Stock Exchange (NSE) in 1996. PSBPL is a corporate trading member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE) for its stock broking services and is Depository Participant with Central Depository Services Limited (CDSL) and is a member of Association of Mutual Funds of India (AMFI) for distribution of financial products. PSBPL is SEBI registered Research Analyst under SEBI (Research Analysts) Regulations, 2014 with SEBI Registration No. INH000000859. PSBPL hereby declares that it has not defaulted with any stock exchange nor its activities were suspended by any stock exchange with whom it is registered in last five years. PSBPL has not been debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has its certificate of registration been cancelled by SEBI at any point of time. PSBPL offers research services to clients as well as prospects. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Other disclosures by Progressive Share Brokers Pvt. Ltd. (Research Entity) and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to the subject company (s) covered in this report-: · PSBPL or its associates financial interest in the subject company: NO · Research Analyst (s) or his/her relative's financial interest in the subject company: NO · PSBPL or its associates and Research Analyst or his/her relative's does not have any material conflict of interest in the subject company. The research Analyst or research entity (PSBPL) has not been engaged in market making activity for the subject company. · PSBPL or its associates actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of Research Report: NO · Research Analyst or his/her relatives have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of Research Report: NO · PSBPL or its associates may have received any compensation including for brokerage services from the subject company in the past 12 months. PSBPL or its associates may have received compensation for products or services other than brokerage services from the subject company in the past 12 months. PSBPL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report. Subject Company may have been client of PSBPL or its associates during twelve months preceding the date of distribution of the research report and PSBPL may have co-managed public offering of securities for the subject company in the past twelve months. · The research Analyst has served as officer, director or employee of the subject company: NO PSBPL and/or its affiliates may seek investment banking or other business from the company or companies that are the subject of this material. Our sales people, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses (if any) may make investment decisions that may be inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest including but not limited to those stated herein. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution publication, availability or use would be contrary to law or regulation or which would subject PSBPL or its group companies to any registration or licensing requirement within such jurisdiction. If this document is sent or has reached any individual in such country, especially, USA, the same may be ignored. Unless otherwise stated, this message should not be construed as official confirmation of any transaction. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of PSBPL. All trademarks, service marks and logos used in this report are trademarks or registered trademarks of PSBPL or its Group Companies. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Indian Securities Market. In so far as this report includes current or historic information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Terms & Conditions: This report has been prepared by PSBPL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of PSBPL. The report is based on the facts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained from publicly available media or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. PSBPL will not treat recipients as customers by virtue of their receiving this report. Compliance Officer:

Mr. Shyam Agrawal, Email Id: [email protected], Contact No.:022-40777500.

Registered Office Address: Progressive Share Brokers Pvt. Ltd, 122-124, Laxmi Plaza, Laxmi Indl Estate, New Link Rd, Andheri West, Mumbai-400053; www.progressiveshares.com Contact No.:022-40777500.

Related Documents