Industry Overview PETRONAS GROUP Financial Results Announcement Financial Year ended 31 March 2011 F8

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Industry Overview

PETRONAS GROUP Financial Results Announcement

Financial Year ended 31 March 2011

F8

EMBARGO The information contained herein may only be

released after 6.00 p.m. on 8 June 2011

Industry Overview

Cautionary Statement Forward-looking statements involve inherent risks and uncertainties. Should one or more of these or other uncertainties or risks materialise, actual results may vary materially from those estimated, anticipated or projected. Specifically, but without limitation, capital costs could increase, projects could be delayed, and anticipated improvements in capacity, performance or profit levels might not be fully realised. Although PETRONAS believes that the expectations of its management as reflected by such forward-looking statements are reasonable based on information currently available to it, no assurances can be given that such expectations will prove to have been correct. Accordingly, you are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date they are made. PETRONAS undertakes no obligation to update or revise any of them, whether as a result of new information, future developments or otherwise. All rights reserved. No part of this document may be reproduced, stored in a retrieval system or transmitted in any form or by any means (electronic, mechanical, photocopying, recording or otherwise) without the permission of the copyright owner. PETRONAS makes no representation or warranty, whether expressed or implied, as to the accuracy or completeness of the facts presented. PETRONAS disclaims responsibility from any liability arising out of reliance on the contents of this publication. ©2010 PETROLIAM NASIONAL BERHAD (PETRONAS)

Industry Overview

PETRONAS GROUP Financial Results Announcement

Macro & Industry Overview Dato’ Shamsul Azhar Abbas

President & CEO, PETRONAS

Global Recovery Hindered - shock wave of events from geo political unrest to natural disasters.

Increase in energy and other commodity prices have put upward pressure on headline inflation, triggering global monetary tightening.

The need to be in a “Constant State of Preparedness”.

PETRONAS’ Growth Agenda remains intact to capture opportunities from rising long term demand for oil and gas.

RM 300 billion 5 year planned Capital Expenditure intact to sustain production levels with some growth along our Integrated Value Chain.

Additional Financial Resources required for M & As to drive material Growth and outpace escalating costs to enhance PETRONAS’ global positioning.

MACRO & INDUSTRY OVERVIEW

The face of UNCERTAINTIES Macro Overview

Page 1

15.0 18.0

13.0

7.0 10.0

18.0 18.0

15.0

15.0 13.0

24.0 28.0

22.0

15.9 17.5

FY 06/07 FY 07/08 FY 08/09 FY 09/10 FY10/11

Return on Average Capital Employed (ROACE), %

PETRONAS Group (RM billion) FY

Key Financial Indicators FY 09/10 FY 10/11 +/-

Revenue 210.8 241.2 14.4%

Gross Profit 82.4 97.8 18.7%

Profit For the Period 45.5 63.0 38.5%

EBITDA 83.3 107.9 29.5%

EBITDA Margin 39.5% 44.7% n/a

PETRONAS Group - strong underlying performance

PETRONAS IOC NOC

PETRONAS’ FINANCIAL PERFORMANCE

Group Revenue continues to improve with higher crude prices and volume sold.

EBITDA Margin rose to 44.7%

despite rising costs and the negative impact of strengthening Ringgit vs. the US Dollar.

Total assets improved by 6.8%

mainly due to higher PPE and cash proceeds obtained from the IPO of PCGB and MHB.

Overall performance improved

reflected in the increase of ROACE from 15.9% to 17.5%.

Page 2

Financial Highlights

Note: 1. PPE : Property, plant & equipment 2. ROACE is calculated based on NOPAT which excludes

IPO Gains for PETRONAS, IOCs and NOCs

Anchored on imperatives of:

Ensuring greater Ownership & Accountability

Elevating Governance & Transparency to international standards

Focusing resources to Core Business activities

Establishing clear and visible Succession Planning & Leadership Development

Achievements to date:

A pro-active and effective Board that provides strategic stewardship in steering the course for PETRONAS’ growth

PETRONAS’ group wide corporate restructuring that is driving desired behavioural changes

More transparent practices such as Quarterly Media Briefings

Dynamic & Meritocratic HR policies adapting to the needs of a globally diverse workforce. Robust Talent & Performance Management with commensurating rewards and consequences

PETRONAS TRANSFORMATION

Page 3

PETRONAS Corporate Enhancement Programme

To Enhance Robustness & Re-Energise Growth Momentum

Exploration & Production

Page 4

ACHIEVEMENTS

Malaysia and International – actively pursued with innovative solutions

Group Resource Replenishment Ratio of 2.5x compared to 1.1x last year

Awarded the first Risk Service Contract (RSC) for Berantai field to a consortium comprising Petrofac, Kencana Energy and Sapura Energy Ventures in January 2011

In Malaysia, 11 new PSCs were awarded compared to 4 last year

Sanctioned 2 new Enhanced Oil Recovery (EOR) projects; Tapis and Guntong with ExxonMobil Exploration and Production Malaysia Inc

5 new Petroleum Arrangements signed internationally

Exited Ethiopia and Timor Lesté, divesting Pakistan

Page 5

Gas & Power

ACHIEVEMENTS

Focused on security of supply for the Nation’s Energy Requirements

Announced the LNG Regasification Terminal project to be completed by July 2012

Executed Final Investment Decision (FID) on Gladstone LNG Project in Australia in January 2011

Maintained world class operating performance for gas processing plants and transmission reliability rates of 99.60% and 99.99%, respectively

Higher LNG sales volume of 26.3 MT compared to 25.1 MT last year

Page 6

Downstream & Others Mega Integrated Project – Malaysia as Regional Petrochemical Hub

ACHIEVEMENTS

Announced project RAPID, an integrated refinery and petrochemical hub in Johor

Embarked on a new fertilizer plant in Sabah

Successful listing of PETRONAS Chemicals Group Bhd (PCGB) in November 2010

Successful listing of Malaysia Marine and Heavy Engineering Holdings Bhd (MHB) in October 2010

MHB entered into an MOU for the proposed acquisition of Sime Darby Engineering’s Pasir Gudang Yard

Pursue a 3.5% CAGR production growth over 5 years

Resource Replenishment Ratio > 1 on a 3 year rolling average basis

Maximise value creation and growth within Malaysia

High grade portfolio of international assets

Anchor capability building on EOR & CO2 development

Explore new play types

Secure supply and maximise value of gas within Malaysia

Strengthen and grow LNG position in Asia Pacific and Atlantic

Establish and grow energy trading in Europe

Grow power and renewable business

Strengthen presence in selected markets and pursue opportunistic growth in

attractive markets

Rationalise non-value adding assets

Grow refining and petrochemical capacity and product range

Build global trading and marketing portfolio

GROWTH IMPERATIVES

Page 7

Key Strategies and Plans

Gas & Power

Exploration & Production

Downstream

Charting PETRONAS’ growth direction and momentum …

GLOBAL ENERGY CHAMPION

Positioned to compete with top industry players

Driven by resilience, supported by robustness and nimbleness to capitalise on opportunities

A Trusted Partner, leveraging on strengths and resources with Industries Best

Explore scope of business beyond conventional plays

CAPEX Quantum will be intensified to outpace rising costs, upgrade asset integrity, enhance yield of

existing/legacy assets, drive growth and venture into more challenging/green field plays such as EOR, Deep Water, Unconventional, etc

Significant CAPEX allocation for downstream expansion will enhance PETRONAS’ Integrated Value Chain

Balancing Resource Allocation and Requirements are KEY SUCCESS FACTORS in driving LONG TERM SUPERIOR PERFORMANCE

… towards being a Global Energy Champion

GLOBAL ENERGY CHAMPION known for its RESILIENCE and DISTINCTIVENESS

PETRONAS’ Aspiration

PRESIDENT’S MESSAGE

Page 8

Industry Overview

PETRONAS GROUP Financial Results Announcement

Financial Highlights Datuk George Ratilal

Executive Vice President

Finance

55

65

75

85

95

105

Apr - Jun2009

Jul - Sep2009

Oct - Dec2009

Jan - Mar2010

Apr - Jun2010

Jul - Sep2010

Oct - Dec2010

Jan-March2011

WTI Brent Tapis OSP

2.60

2.80

3.00

3.20

3.40

3.60

3.80

4.00

4.20

4.40

Mar 09 Jun 09 Sep 09 Dec 09 Mar 10 Jun 10 Sep 10 Dec 10 Mar 11

USD/MYR

FINANCIAL HIGHLIGHTS

PETRONAS Group continues to deliver strong underlying performance Financial Highlights

Benchmark crude prices showed an upward trend backed by robust demand & concerns over

supply…

Q4 PETRONAS Group (RM billion) FY

FY 09/10 FY 10/11 +/- Key Financial Indicators FY 09/10 FY 10/11 +/-

59.2 65.6 10.8% Revenue 210.8 241.2 14.4%

21.7 28.4 30.9% Gross Profit 82.4 97.8 18.7%

22.1 27.3 23.5% EBITDA 83.3 107.9 29.5%

15.6 20.8 33.3% Profit Before Taxation (PBT) 67.3 90.5 34.5%

9.0 12.4 37.8% NOPAT 44.5 52.6 18.2%

26.4% 31.7% n/a Return on Revenue (ROR) 31.9% 37.5% n/a

Page 10

USD/Bbl

Note: WTI = West Texas Intermediate OSP = Official Selling Price Source : Crude Oil Group Report

Note: NOPAT : Net Profit After Tax excluding finance cost, share of profits or associates and jointly controlled entities, net IPO Gains and other-non operating income and expenses; ROR : Based on PBT; EBITDA: Consists of PBT, minority interests with the addition of amounts previously deducted for depreciation, amortization and impairment loss on property, plant and equipment and intangible assets and financing costs, and the exclusion of interest income.

Financials: Rounded up to 1 decimal place (RM billion).

…whilst Ringgit strengthened against USD…

Source : Bloomberg

Revenue for the year increased by 14.4% y-o-y driven by higher prices for all products and higher volume for major products amidst improved economic growth despite strengthening of Ringgit Malaysia against US Dollar.

EBITDA for the year, included a net gain of RM9.2 billion arising from the IPO of

PCGB and MHB. Excluding the said gain, EBITDA increased by 18.5%, in line with higher revenue.

ROR for the year is 37.5% despite rising costs which reflects stronger prices and the Group’s continuous drive for operational efficiencies.

45.4

3.2 2.3 2.4 0.5

53.8

FY 09/10 E&P Gas& Power

Downstream Corporate& Others

FY 10/11

RM

bill

ion

E&P Gas & Power

Downstream Corporate & Others

81.5

53.6

115.4

21.0 93.3

64.0

130.0

19.1

30.8 34.0

8.9 11.2

4.8

7.2 0.9

1.4

FY 09/10 FY 10/11

FINANCIAL HIGHLIGHTS Revenue & NOPAT

Analysis

Note: Gross Revenue and Gross NOPAT include both third party and inter-segments transactions Financials: Rounded up to 1 decimal place (RM billion).

RM

bill

ion

Page 11

45.4 53.8

Gross NOPAT by Business Segment Gross Revenue by Business Segment

RM 271.5 billion RM 306.4 billion

FY 10/11 FY 09/10

Corporate & Others Gas & Power Downstream E&P

Movement in Gross NOPAT by Business Segments Higher prices and robust demand resulted in improved performance

for all core businesses.

Gross revenue increased by 12.9% with Downstream Business being the biggest revenue contributor at 42.4% of total Gross Revenue.

Gross NOPAT for the business segments increased by RM8.4 billion for the year with the highest incremental contribution coming from E&P Business.

Gross Revenue and NOPAT strengthened on the back of higher prices and robust demand

103.7 106.1

36.3 49.2

(30.0 ) (6.5 ) (0.9 )

16.8

FY 09/10 Cash fromOperations

Capex Dividends toGovernment

Dividends toMI

OtherInvesting

IPO FY 10/11

FINANCIAL HIGHLIGHTS

Group’s Balance Sheet remains healthy Financial Highlights Balance Sheet &

Cash Flows

PETRONAS Group (RM billion) 31 March 2010

Restated

31 March 2011

+/- Selected Balance Sheet Highlights

Property, Plant & Equipment (PPE) 189.5 191.6 1.1%

Total Assets 410.9 439.0 6.8%

Shareholder’s Funds 242.9 263.8 8.6%

Borrowings 51.9 47.8 (7.9%)

ROTA 11.1% 12.3% n/a

Return on Average Capital Employed (ROACE) 15.9% 17.5% n/a

Gearing 16.2% 13.9% n/a

Page 12

Note: 1. ROTA: Based on NPAT; 2. ROACE: based on NOPAT; divided by average shareholders’ equity and long term debt during the year. 3. Financials: Rounded up to 1 decimal place (RM billion).

Balance Sheet remains robust with PPE and total assets growing at 1.1% and 6.8% respectively, driven by the Group’s expansion strategy.

ROTA & ROACE increased to 12.3% and 17.5% respectively due to higher profit for the year.

Cash from Operations was RM70.8 billion compared to RM56.1 billion in the previous year, representing an increase of 26.2% mainly due to better earnings.

CAPEX accounts to RM34.9 billion mainly spent towards intensifying exploration and production activities and continuing EOR/IOR efforts.

Dividend payment to Government amounts to RM30 billion.

Changes in Group Cash Balance

RM

Bill

ion

140.0 155.3

Fund & Other Investments

Cash and cash equivalents

70.8 (34.9)

20.2 20.2 18.3 16.3 17.7

31.1 35.8

31.9 29.5 28.1

48.2 49.3

41.5 39.5

40.9

44.7

FY 06/07 FY 07/08 FY 08/09 FY 09/10 FY10/11

EBITDA / Revenue, %

22.1

22.1

18.2

13.4 15.7

23.0

21.5

19.8

12.7

14.4

25.9

28.1

23.0

11.1

18.5

20.6

FY 06/07 FY 07/08 FY 08/09 FY 09/10 FY10/11

Return on Total Assets (ROTA), %

19.5 18.2 18.3

21.4 18.8

31.2

27.5

31.5 31.6 28.0

17.4 15.8 15.9 16.2

13.9

FY 06/07 FY 07/08 FY 08/09 FY 09/10 FY10/11

Gearing Ratio, %

Industry Benchmarking

FINANCIAL HIGHLIGHTS

Note:

1. Results of oil majors (IOCs) and national oil companies (NOCs) were adjusted to the same financial period to PETRONAS based on publicly available information.

2. PETRONAS’ financial year end based on 31 Mar.

3. IOCs = ExxonMobil, Chevron, RD Shell & Total SA ;

4. NOCs = Petrobras, PetroChina , Rosneft & Statoil ASA

5. ROACE is calculated based on NOPAT which excludes IPO Gains for PETRONAS, IOC and NOC

PETRONAS’ improved performance is in line with big players of the industry

Page 13 WITH IPO Gain IOC NOC PETRONAS

15.0

18.0 13.0

7.0

10.0

18.0 18.0

15.0

15.0 13.0

24.0

28.0

22.0

15.9 17.5

FY 06/07 FY 07/08 FY 08/09 FY 09/10 FY10/11

Return on Average Capital Employed (ROACE)5, %

Improvement in the market forces had delivered favorable results to all players in the industry.

As a result, our competitors successfully improved their performance translated by higher EBITDA Margin, ROACE and ROTA whilst reducing their gearing.

PETRONAS’ own performance was also in trend with our competitors, indicating another year of resilient performance by the Group.

Exploration and

Production Business Dato’ Wee Yiaw Hin

Executive Vice President

Exploration & Production

E&P Highlights

EXPLORATION & PRODUCTION BUSINESS

Awarded first Risk Service Contract (RSC) for Berantai field as a new petroleum arrangement solution

157 ventures in Malaysia and International operations, with 17 new ventures secured during the year

Achieved total production of 2,132 kboe/d, 24% of which was contributed by International operations

Total group discovered resources stands at 28.3 Bboe, up by 4% from FY 09/10 Group Overall Resource Replenishment Ratio of 2.5x for combined oil and gas resources

Strong financial performance with NOPAT of RM 34.0 billion, 10% increase from FY 09/10

E&P business continues to deliver strong performance and is geared for growth

Page 15

Financial Highlights E&P business registered strong financial performance with increase in Revenue & NOPAT by 14% & 10% respectively

EXPLORATION & PRODUCTION BUSINESS

Q4 Key Financial Indicators FY

FY 09/10 FY 10/11 +/- RM billion FY 09/10 FY 10/11 +/-

22.6 27.2 20% Revenue 81.5 93.3 14%

5.6 10.4 86% NOPAT 30.8 34.0 10%

Revenue RM Bil

64.4 74.0

17.1 19.3

FY 09/10 FY 10/11

Malaysia International

81.5 93.3

NOPAT RM Bil

26.4 28.4

4.4 5.6

FY 09/10 FY 10/11

Malaysia International

30.8 34.0

Higher revenue and NOPAT for FY10/11 attributable to higher realised price for crude and condensate.

International operations account for 21% of total revenue.

Increase in NOPAT for both Malaysia and International operations by 8% and 27% respectively.

Page 16

Acquisition of blocks in Venezuela, Australia and Brunei

Divesting 3 International countries as part of portfolio high-grading

5 first production from Vietnam Pearl & Topaz, Sudan Teng Mish Mish, Muda Jeng-A and JDA MDD Project (MTJDA)

All 4 ventures in Iraq achieved Pre-Development Plan approval and on track to achieve FCP in 2012 and 2013

Addition of resources through discoveries in Uzbekistan, Sudan and Vietnam and IOR in Sudan

Operators Ventures Country

Africa Region 21 8

South East Asia 30 5

Central Asia 7 3

Middle East 6 3

Arctic 6 1

Others 5 3

75 23

EXPLORATION & PRODUCTION BUSINESS

Operational Highlights

International

Malaysia

11 new PSCs awarded

First Risk Service Contract (RSC) for Berantai field

New PITA tax incentives to drive exploration and development of challenging resources

3 first production from new fields

10 exploration discoveries

2 major enhance recovery projects sanctioned

3 pipeline replacements completed

Operators Total PSCs

PETRONAS Carigali 32

Shell 12

Murphy 6

ExxonMobil 5

Talisman 5

Newfield 4

Nippon 2

Lundin 4

BHP Biliton 2

Others 10

82

E&P business remains vibrant amidst challenging environment

Page 17

EXPLORATION & PRODUCTION BUSINESS Malaysia entitlement remains intact despite decrease in production, while International entitlement was affected by PSC effect of higher oil price

Production

1,631 1,614

637 518

FY 09/10 FY 10/11

Malaysia International

Higher Malaysia gas offtake from customer.

Crude natural depletion in Malaysia and Sudan.

Lower International gas from expiry of Iran service contract and reservoir performance in Egypt.

2,268 2,132

Total Production (kboe/d)

535 512

122 115

974 987

FY 09/10 FY 10/11

Crude Condensate Gas

1,631 1,614

Malaysia Production by Hydrocarbon Type (kboe/d)

239 225

26 27

272 266

100

FY 09/10 FY 10/11

Crude Condensate Gas Iran Gas

637

518

International Production by Hydrocarbon Type (kboe/d)

PETRONAS Share

1,112 1,112

PETRONAS Share

345 328

PETRONAS Share

1,457 1,440

Page 18 Note: kboe/d = kilo barrels of oil per day

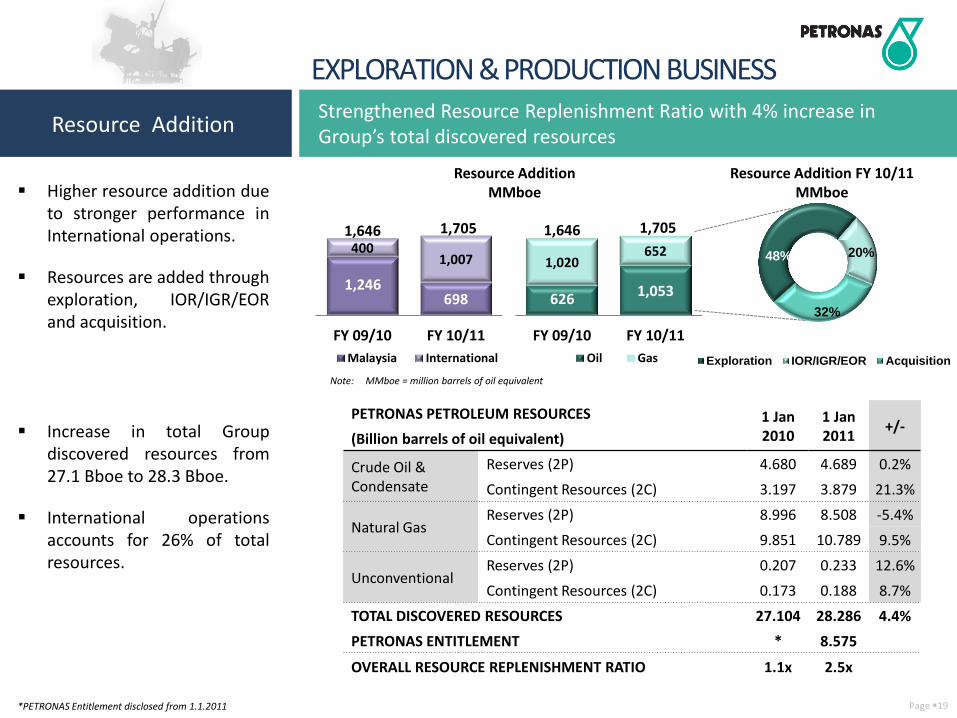

EXPLORATION & PRODUCTION BUSINESS Strengthened Resource Replenishment Ratio with 4% increase in Group’s total discovered resources

Resource Addition

48% 20%

32%

Exploration IOR/IGR/EOR Acquisition

1,246 698

400 1,007

FY 09/10 FY 10/11

Malaysia International

1,646 1,705

Resource Addition FY 10/11 MMboe

Resource Addition MMboe

626 1,053

1,020 652

FY 09/10 FY 10/11

Oil Gas

1,646 1,705

Higher resource addition due to stronger performance in International operations.

Resources are added through exploration, IOR/IGR/EOR and acquisition.

Increase in total Group discovered resources from 27.1 Bboe to 28.3 Bboe.

International operations accounts for 26% of total resources.

PETRONAS PETROLEUM RESOURCES 1 Jan 2010

1 Jan 2011

+/- (Billion barrels of oil equivalent)

Crude Oil & Condensate

Reserves (2P) 4.680 4.689 0.2%

Contingent Resources (2C) 3.197 3.879 21.3%

Natural Gas Reserves (2P) 8.996 8.508 -5.4%

Contingent Resources (2C) 9.851 10.789 9.5%

Unconventional Reserves (2P) 0.207 0.233 12.6%

Contingent Resources (2C) 0.173 0.188 8.7%

TOTAL DISCOVERED RESOURCES 27.104 28.286 4.4%

PETRONAS ENTITLEMENT * 8.575

OVERALL RESOURCE REPLENISHMENT RATIO 1.1x 2.5x

*PETRONAS Entitlement disclosed from 1.1.2011 Page 19

Note: MMboe = million barrels of oil equivalent

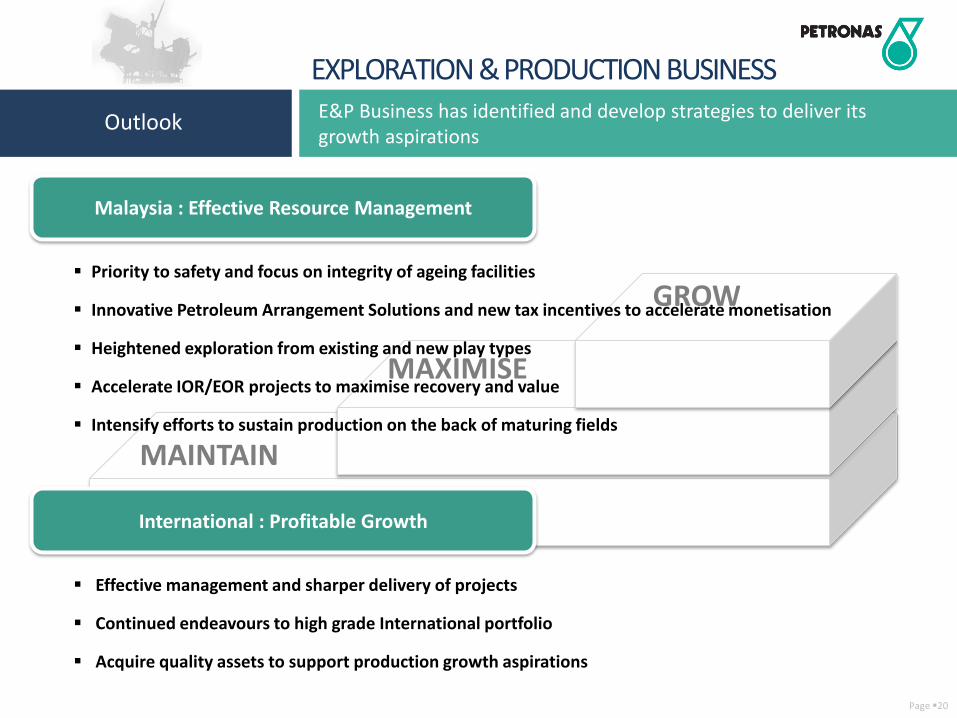

EXPLORATION & PRODUCTION BUSINESS

MAINTAIN

MAXIMISE

GROW

E&P Business has identified and develop strategies to deliver its growth aspirations

Outlook

Malaysia : Effective Resource Management

Priority to safety and focus on integrity of ageing facilities

Innovative Petroleum Arrangement Solutions and new tax incentives to accelerate monetisation

Heightened exploration from existing and new play types

Accelerate IOR/EOR projects to maximise recovery and value

Intensify efforts to sustain production on the back of maturing fields

Effective management and sharper delivery of projects

Continued endeavours to high grade International portfolio

Acquire quality assets to support production growth aspirations

International : Profitable Growth

Page 20

Gas & Power Business

Datuk Anuar Ahmad

Executive Vice President

Gas & Power

Key Messages Profitable year for G&P despite operational challenges

At RM11.2 billion, registered 26% increase in NOPAT compared to last financial year.

Faced continuing challenges to meet Peninsular Malaysia gas demand with tight gas supply from offshore Peninsular.

Going forward, initiatives are being undertaken to ensure security of gas supply for Malaysia.

Gas processing and transmission continue to be operating at world class standards.

At 24.34 million tonnes, PLC achieved highest LNG production level.

Page 13

GAS & POWER BUSINESS

Page 21

Financial Highlights Registered improved financial results in FY10/11

Q4 Key Financial Indicators FY

FY 09/10 FY 10/11 +/- RM billion FY 09/10 FY 10/11 +/-

16.8 17.9 6.5% Revenue 53.6 64.0 19.4%

3.2 1.0 -68.8% NOPAT 8.9 11.2 25.8%

GAS & POWER BUSINESS

Source : Japan Tariff Association, Platts & Bloomberg

FY10/11 FY 09/10

Infrastructure, Utilities & Power

Global LNG

Revenue

15.6

11.5

-4.4

-2.6

-10 -5 0 5 10 15 20

FY 10/11

FY 09/10

NOPAT

Global LNG Infrastructure, Utilities & Power

RM 8.9 billion

RM53.6 billion

37.6

16.0 17.1

RM64.0 billion

46.9

Revenue of RM64.0 billion was 19% higher than last year, on the back of higher LNG prices and volumes sold.

NOPAT for the year stood at RM11.2 billion, 26% higher than last year, in line with revenue growth.

RM 11.2 billion

Page 22

50

60

70

80

90

100

110

Q1FY09/10

Q2FY09/10

Q3FY09/10

Q4FY09/10

Q1FY10/11

Q2FY10/11

Q3FY10/11

Q4FY10/11

USD

/bb

l

JCC (USD/bbl)

Higher LNG volume sold on the back of 5% increased PLC production

PETRONAS LNG COMPLEX SALES FY 10/11

LNG volume brought to market (million tonnes)

Operational Highlights LNG

At 26.3 million tonnes, LNG sales for the year was higher compared to last year, driven by higher volumes from PETRONAS LNG Complex (PLC) in Bintulu.

PETRONAS LNG Ltd (PLL) continues to effectively play its role as system balancer by handling 0.8 million tonnes over and above its trading volume.

PLC achieved its highest LNG production volume for the year as a result of improved operational performance.

Exports of LNG from Bintulu were shipped mainly to Japan at 60%, South Korea at 18% and Taiwan at 13%.

60% 18%

13%

5% 4%

Japan S. Korea Taiwan China Others

GAS & POWER BUSINESS

22.8 23.9

FY 09/10 FY 10/11

PETRONAS LNG Complex Egyptian LNG Traded Volume

25.1

26.3

23.9 MT

0.4

0.4

2.0 1.9

Page 23

1,176 1,087

787 819

125 141

FY 09/10 FY 10/11

POWER NON-POWER EXPORTGPP = Gas Processing Plants , PGU = Peninsular Gas Utilisation

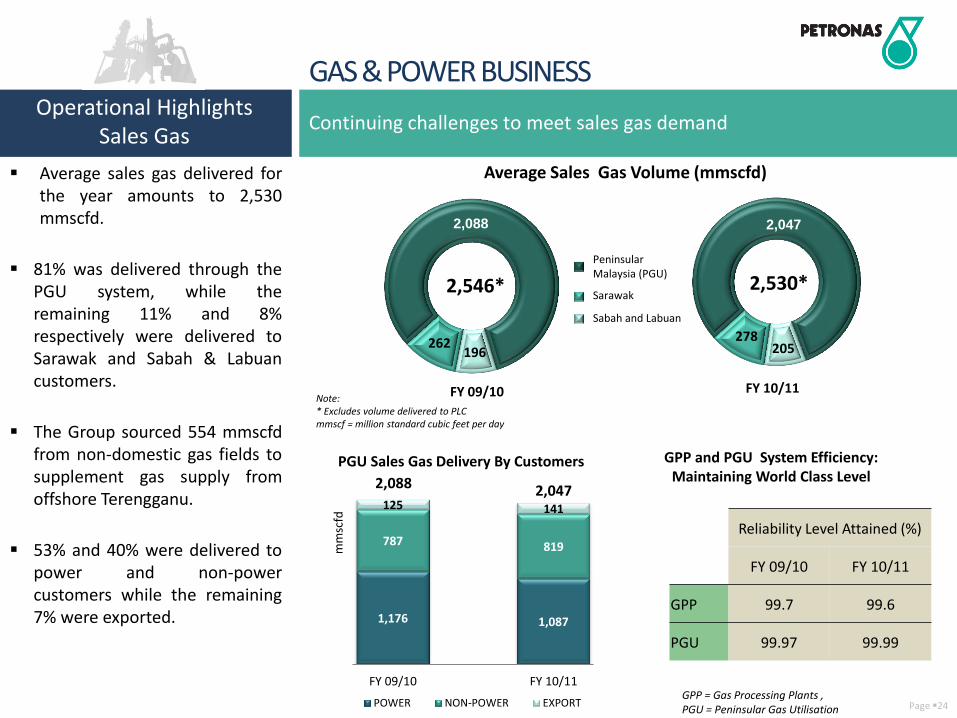

Average sales gas delivered for the year amounts to 2,530 mmscfd.

81% was delivered through the PGU system, while the remaining 11% and 8% respectively were delivered to Sarawak and Sabah & Labuan customers.

The Group sourced 554 mmscfd from non-domestic gas fields to supplement gas supply from offshore Terengganu.

53% and 40% were delivered to power and non-power customers while the remaining 7% were exported.

GPP and PGU System Efficiency: Maintaining World Class Level

PGU Sales Gas Delivery By Customers

Continuing challenges to meet sales gas demand

GAS & POWER BUSINESS Operational Highlights

Sales Gas

mm

scfd

2,088 2,047

2,088

FY 09/10

196 262

2,047

FY 10/11

205 278

Average Sales Gas Volume (mmscfd)

2,546* 2,530* Sarawak

Peninsular Malaysia (PGU)

Sabah and Labuan

Reliability Level Attained (%)

FY 09/10 FY 10/11

GPP 99.7 99.6

PGU 99.97 99.99

Note: * Excludes volume delivered to PLC mmscf = million standard cubic feet per day

Page 24

GAS & POWER BUSINESS Key Milestones &

Achievements In FY10/11 Gas & Power achieved numerous key milestones

March 2011 EPCC awarded for the Kimanis Power Plant (KPP) project

January 2011 Front End Engineering Design (FEED) contract signed for the Floating LNG (FLNG) project

January 2011 Achieved Final Investment Decision (FID) for the Gladstone LNG (GLNG) Project

January 2011 EPCIC awarded for the first Re-gasification Terminal (RGT) in Peninsular

November 2010 EPCC awarded for the Plant Rejuvenation & Revamp 2 (PRR2) project in PGB

Page 25

GAS & POWER BUSINESS

Moving Forward

Secure and maximise value of gas within Malaysia

Strengthen and grow LNG position in Asia Pacific and Atlantic

Establish and grow energy trading in Europe

Grow power and renewable business

Aim to deliver PETRONAS’ long term sustainable growth …

Page 26

Downstream Business Datuk Wan Zulkiflee Wan Ariffin

Executive Vice President

Downstream

External Environment High price environment amidst global economic recovery

DOWNSTREAM BUSINESS

Global economic growth in FY10/11 generally contributed by improved demand mainly from the emerging economies.

Crude and petroleum products prices moved in tandem with the improved market conditions and trended sharply upwards mainly due to the weaker US Dollar and geopolitical tensions in the Middle East and North Africa during the second half of the financial year.

Petrochemical prices were also higher attributable to the strong demand for major products.

60

70

80

90

100

110

120

130

Jan - Mar2010

Apr - June2010

Jul - Sep2010

Oct - Dec2010

Jan - Mar2011

Gasoil ULG95Brent Tapis OSP

Crude & Petroleum Product Prices

USD

/Bb

l

Source : Platts Note: Product prices Mean of Platts Singapore

(MOPS) , Official Selling Price (OSP)

- 100 200 300 400 500

Oct - Dec2009

Jan - Mar2010

Apr - June2010

Jul - Sep2010

Oct - Dec2010

Jan - Mar2011

Methanol IPEX

Urea

Petrochemical Prices

600 800

1,000 1,200 1,400 1,600 1,800

Ethylene PP

Source : ICIS, CMAI

USD

/mt

-10

10

30

50

70

90

110

130

150

-8

-6

-4

-2

0

2

4

6

8

Q42007

Q12008

Q22008

Q32008

Q42009

Q12009

Q22009

Q32009

Q42010

Q12010

Q22010

Q32010

Q42011

World oil demand growth (LHS) World GDP growth (LHS) Brent (RHS)

Source: CIRU, MF, IHS CERA, Bloomberg

USD/ barrel % y-o-y World GDP growth, world oil demand and Brent prices

Page 28

DOWNSTREAM BUSINESS Sustaining refinery operational excellence whilst optimising production economics

Refining

Malaysian refineries achieved higher utilisation rate y-o-y contributed by higher volumes post Malaysian Refining Company’s revamp and capacity expansion.

The Durban refinery recorded lower utilisation rate due to prolonged scheduled shutdown.

Total refineries utilisation rate is at par with the average global refinery utilisation rate, while Malaysian refineries trended higher at 91%.

97 97

86 91

92 86 81 82

FY 07/08 FY 08/09 FY 09/10 FY 10/11

Malaysian Refineries Total Refineries Average Global

Refinery Utilisation (%)

104.0

34.1

107.6

26.8

Malaysian Refineries Overseas Refinery

FY 09/10 FY 10/11

Crude Refining Volume (million bbl)

Source : BP Statistical Review of World Energy 2010, IHS CERA Note: FY07/08 is based on average Global Utilisation rate from year 2000 until 2007

Page 29

Sales volume grew 6% y-o-y in tandem with the economic recovery.

Volume growth was in all segments with 42% coming from Retail, represented by the global service stations network.

Increased number of service stations contributed mainly by Engen’s acquisition of Chevron’s assets in 7 Sub-Saharan African countries whilst in Malaysia, the network expanded by 30 stations to keep pace with competition.

Downstream Marketing Strengthening market leadership in selected markets

163.5

69.4 48.1 46.0

175.9

72.9 48.9 54.1

Total Retail Commercial Others

FY 09/10 FY 10/11

Sales Volume by Segment (million bbl)

Note : ‘Others’ includes Lubricants, Aviation & LPG segments

50.4

49.6

Sales Volume by Geography (%)

Malaysia

International

FY10/11

DOWNSTREAM BUSINESS

Global Retail Presence by Region – Number of Service Stations

FY09/10 FY10/11 +/-

Malaysia 925 955 30

International 1,684 1,775 91

Global Retail Presence 2,609 2,730 121

Page 30

DOWNSTREAM BUSINESS

Delivered higher sales volume despite lower utilisation rate Petrochemicals

Overall, plant utilisation rate for the year was slightly lower mainly due to shutdowns of some plants.

However, higher sales volume was achieved for the year mainly due to additional volume from newly acquired subsidiaries, Optimal Glycols (Malaysia) Sdn Bhd, Optimal Chemicals (Malaysia) Sdn Bhd and Polyethylene (Malaysia) Sdn Bhd.

1.7

6.2

1.8

6.7

Q4 Q4 YTD

FY 09/10 FY 10/11

Total Sales Volume (million tonnes)

82.5 81.0

Nexant

Utilisation Rate (%)

FY 09/10 FY 10/11

Note : Based on Nexant

Page 31

Petrochemical 9%

Refining & Trading

56%

Downstream Marketing

35%

Revenue contribution by Business Segment – FY10/11

Petrochemical 40%

Refining & Trading

39%

Downstream Marketing

21%

NOPAT contribution by Business Segment – FY10/11

Key Financial Highlights Full year profits increased by 50% reflecting strong results across all business segments

DOWNSTREAM BUSINESS

Q4 Key Financial Indicators FY

FY 09/10 FY 10/11 +/- RM billion FY 09/10 FY 10/11 +/-

31.7 34.6 9.1% Revenue 115.4 130.0 12.7%

1.2 2.1 75.0% NOPAT 4.8 7.2 50.0%

Revenue rose by 13% y-o-y driven by higher crude and product prices coupled with higher petroleum products sales volume.

NOPAT improved by 50% y-o-y due to better margins realised.

Refining and Trading segment contributed approximately 56% of the Downstream revenue whilst Petrochemical Business contributed about 40% of the total Downstream NOPAT.

Page 32

Strategic Initiatives achieved in FY 2010/11

DOWNSTREAM BUSINESS

Collaboration with BASF to study expansion into high value specialty chemicals (MOU signed December 2010)

Strengthened downstream marketing presence in selected markets:

Acquired Chevron’s retail assets in 7 sub-Sahara African countries and Shangdong St. Maria Lubricating Oil Company Limited in China

Growing lubricant volumes through service fill lubricant supply to Mercedes OEM and strengthening the brand via development of Fluid Technology Solution™ (FTS) for Mercedes GP team in Formula 1

Positioning Downstream Business to deliver higher sustainable value

Listed PETRONAS Chemicals Group Berhad (PCGB)

Restructured global marketing and trading of crude oil and petroleum products under a single entity

Enhanced risk management system on trading

Business Enhancement

Growth

Page 33

DOWNSTREAM BUSINESS

Project RAPID in Johor

Fertilizer Plant in Sabah Growing lubricant business

Ensuring safe and reliable operations

Sustaining operational excellence, benchmarked to

world-class standards Active Portfolio Management

Business Enhancement

Growth

Downstream Business focus will be on… Moving Forward

Page 34

Summary In conclusion…

The high price environment contributed favourably to Downstream Business

Utilisation rates for the refineries and petrochemical plants can be further improved

Downstream registered a commendable 50% increase in NOPAT y-o-y

Strategically grew marketing volumes in selected markets globally

Safety continues to be our top priority

DOWNSTREAM BUSINESS

Page 35

Industry Overview

PETRONAS GROUP Financial Results Announcement

Q&A

Industry Overview

PETRONAS GROUP Financial Results Announcement

Thank You

Related Documents