SWIFT Nordics Regional Conference 2015 Payments stream - Regulation and mandatory changes in the payments space – what are the real game changers? Copenhagen, 4 – 5 March 2015

Payments stream - Regulation and mandatory changes

Jul 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SWIFT Nordics Regional

Conference 2015

Payments stream - Regulation and

mandatory changes in the payments

space – what are the real game

changers?

Copenhagen, 4 – 5 March 2015

Nordics Regional Conference - Speakers

Jorge B. Jensen, Head of Section Finance, Department of

Consumer Advocacy, Norwegian Consumer Council

(Forbrukerradet)

Kirstine Nilsson, Senior Vice President, SEPA & EU Payment

Regulation Coordinator, Swedbank

Carsten Thaarup, Senior Industry Expert, Nordea Bank

Danmark A/S

Erkki Poutiainen, Senior Vice President, Public Affairs, Nordea

(moderator)

Regulation and mandatory change

Payment stream, SWIFT Nordic Conference

4.-5. March 2015, Copenhagen

Selected approach to the theme

• New payment regulation: PSD2 and its impact

• Managing mandatory change in multi-country

(Nordic) set-up

• SEPA compliance in euro and non-euro countries

• ISO 20022

• New regulations

• Payment services and change seen from customer

perspective

• But first a little wider introduction…

• 26/02/2015

4 •

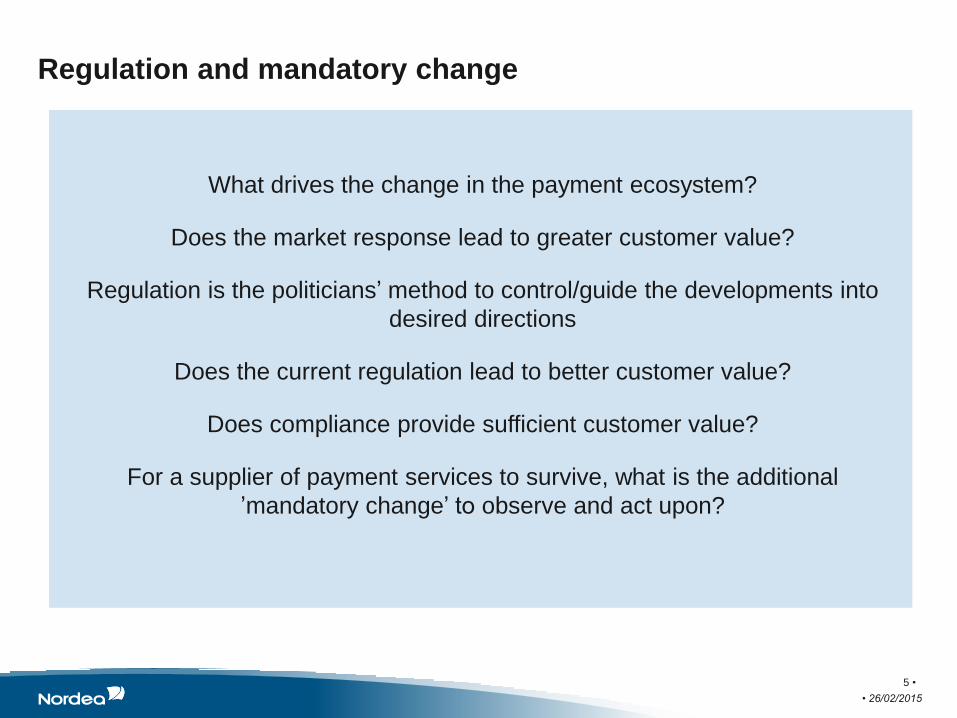

Regulation and mandatory change

What drives the change in the payment ecosystem?

Does the market response lead to greater customer value?

Regulation is the politicians’ method to control/guide the developments into

desired directions

Does the current regulation lead to better customer value?

Does compliance provide sufficient customer value?

For a supplier of payment services to survive, what is the additional

’mandatory change’ to observe and act upon?

• 26/02/2015

5 •

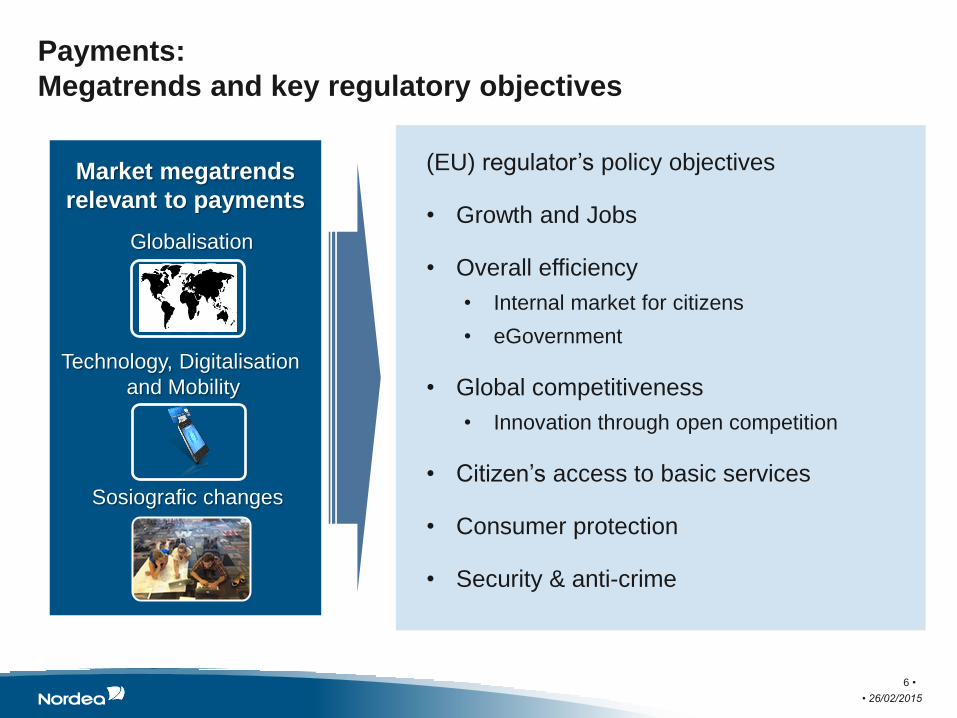

Payments:

Megatrends and key regulatory objectives

(EU) regulator’s policy objectives

• Growth and Jobs

• Overall efficiency

• Internal market for citizens

• eGovernment

• Global competitiveness

• Innovation through open competition

• Citizen’s access to basic services

• Consumer protection

• Security & anti-crime

Market megatrends

relevant to payments

Globalisation

Technology, Digitalisation

and Mobility

Sosiografic changes

• 26/02/2015

6 •

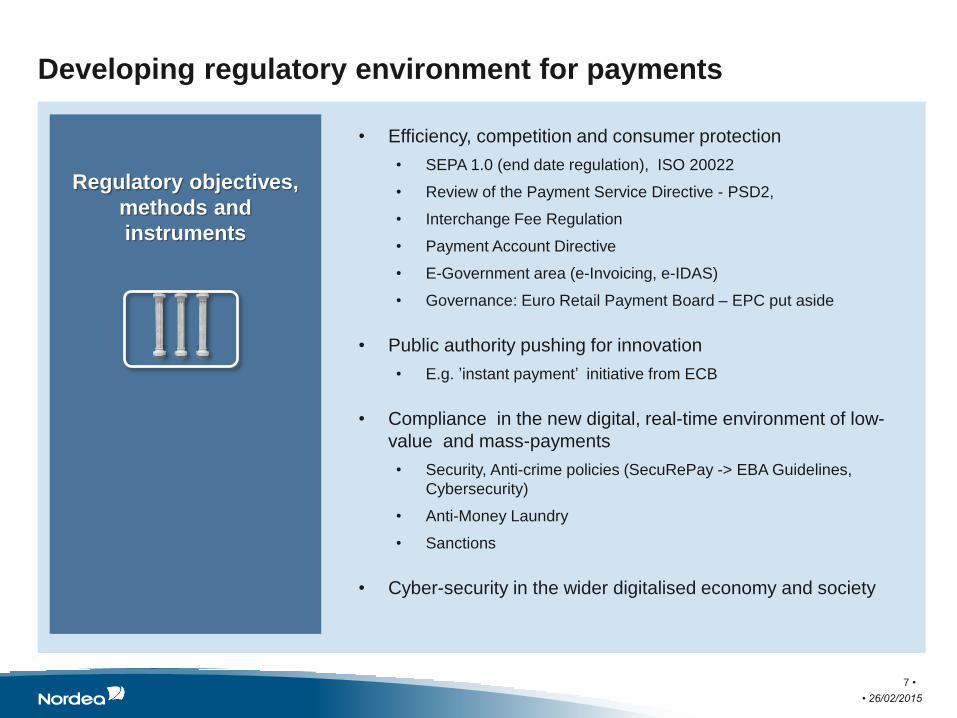

Developing regulatory environment for payments

• Efficiency, competition and consumer protection

• SEPA 1.0 (end date regulation), ISO 20022

• Review of the Payment Service Directive - PSD2,

• Interchange Fee Regulation

• Payment Account Directive

• E-Government area (e-Invoicing, e-IDAS)

• Governance: Euro Retail Payment Board – EPC put aside

• Public authority pushing for innovation

• E.g. ’instant payment’ initiative from ECB

• Compliance in the new digital, real-time environment of low-

value and mass-payments

• Security, Anti-crime policies (SecuRePay -> EBA Guidelines,

Cybersecurity)

• Anti-Money Laundry

• Sanctions

• Cyber-security in the wider digitalised economy and society

Regulatory objectives,

methods and

instruments

• 26/02/2015

7 •

Bank

account

Payment regulation and connections to the services

Basic payment

account

• Electronic administration and

orders

• Payment card (incl. Internet

payments)

• No credit, no limits

TPP access to

bank account

One leg out,

Other currencies

Transparency,

reporting

Strong

authentication

PSD2

Payment

Account

Directive

(PAD) Credit

transfer

Direct debit

Debit/

credit card

Online

credentials

E-& m-

payments

SEPA

end-date

AMLD4

SecuRePay

Guidelines

Interchange Fee

Regulation

Paym

ent

pro

cessin

g

Funds Transfer

Directive (FATF)

NIS

Network and

information security

• 26/02/2015

8 •

New (regulated) parties in the payment value chain

• 26/02/2015

9 •

Consumer Merchant

Consumer’s

account

Bank A

Consumer’s

account

Bank A

Online

bank Online

bank E-

payment POS

Card

Service layer

Payment infrastructure

Cards, Credit transfers, Direct debits

Third party payment

service provider Third party payment

service provider Third party payment

service provider Third party payment

service provider

Regulation

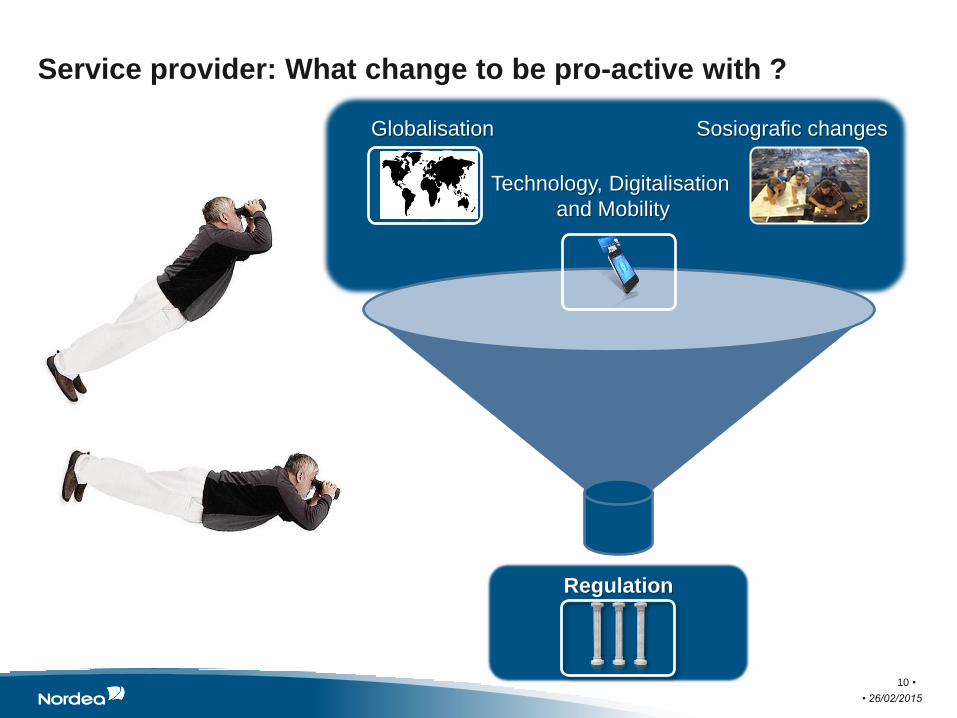

Service provider: What change to be pro-active with ?

Globalisation

Technology, Digitalisation

and Mobility

Sosiografic changes

• 26/02/2015

10 •

How does this sound to the customer?

• The change is bringing new supplier parties

to the game

• Observations

• Benefits?

• Concerns?

• Further wishes?

• 26/02/2015

11 •

Session participants

• Jorge B. Jensen, Head of Section Finance, Department of Consumer Advocacy,

Norwegian Consumer Council (Forbrukerradet)

• Kristine Nilsson, SEPA & EU Payment Regulation Coordinator, Swedbank

• Carsten Thaarup, Senior Industry Expert, Nordea

• Erkki Poutiainen, Senior Vice President, Public Affairs, Nordea (moderator)

• 26/02/2015

12 •

© Swedbank

PSDII… Third Party Payment Service Provider

- introducing the specialised middleman

Copenhagen 2015-03-04

Kirstine Nilsson

© Swedbank

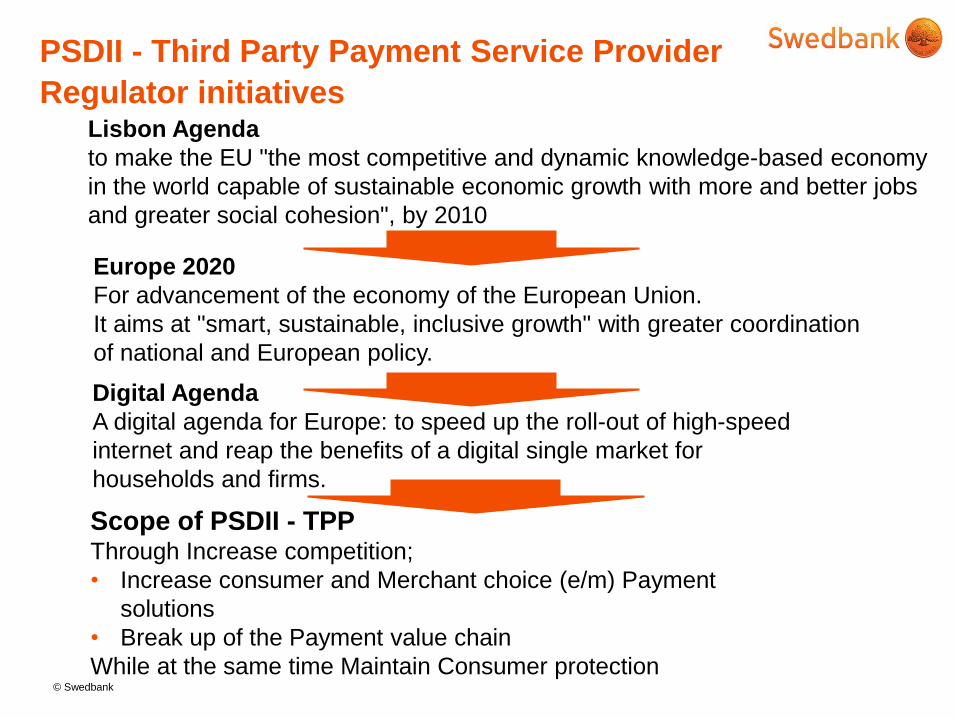

PSDII - Third Party Payment Service Provider

Regulator initiatives Lisbon Agenda

to make the EU "the most competitive and dynamic knowledge-based economy

in the world capable of sustainable economic growth with more and better jobs

and greater social cohesion", by 2010

Europe 2020

For advancement of the economy of the European Union.

It aims at "smart, sustainable, inclusive growth" with greater coordination

of national and European policy.

Digital Agenda

A digital agenda for Europe: to speed up the roll-out of high-speed

internet and reap the benefits of a digital single market for

households and firms.

Scope of PSDII - TPP Through Increase competition;

• Increase consumer and Merchant choice (e/m) Payment

solutions

• Break up of the Payment value chain

While at the same time Maintain Consumer protection

© Swedbank 15

PSDII - Third Party Payment Service Provider

Customer requirements

Swedish Post Office in cooperation with Svensk Distanshandel and HUI Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

E-Merchant; Reach, Conversion, Fair cost

© Swedbank 16

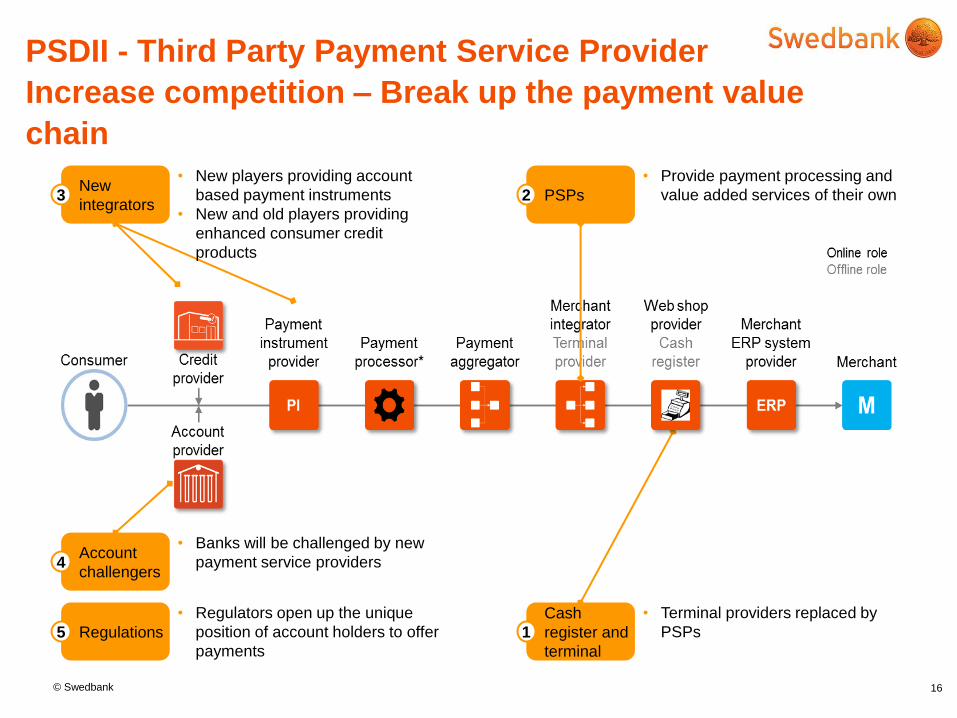

PSDII - Third Party Payment Service Provider

Increase competition – Break up the payment value

chain

Cash

register and

terminal

• Terminal providers replaced by

PSPs 1

• Provide payment processing and

value added services of their own New

integrators

• New players providing account

based payment instruments

• New and old players providing

enhanced consumer credit

products

3

Account

challengers

• Banks will be challenged by new

payment service providers 4

Regulations

• Regulators open up the unique

position of account holders to offer

payments

5

PSPs 2

© Swedbank

PSDII - Third Party Payment Service Provider

The payment value chain

17

- is only as strong as the

weakest link.

© Swedbank

PSDII - Third Party Payment Service Provider

THANK YOU FOR LISTENING

Kirstine Nilsson

SEPA & EU Payment

Regulation Coordinator

Swedbank [email protected]

EU Regulation for a bank operating inside and

out of Euroland

SWIFT Nordics Conference

Carsten Thaarup 5 March 2015

SEPA Coverage

20 •

EU, non-Euro zone

countries

(9)

Bulgaria

Croatia

Czech Republic

Denmark

Great Britain

Hungary

Poland

Romania

Sweden

EFTA

countries

(6)

Iceland

Norway

Liechtenstein

Monaco*

Switzerland*

San Marino*

*Not part of the EEA Agreement, but has a bilateral agreement with the EU

EU, Euro zone

countries

(19)

Austria

Belqium

Cyprus

Estonia

France

Finland

Germany

Greece

Ireland

Italy

Latvia

Lithuania

Luxenbourg

Malta

Netherlands

Portugal

Slovak Republic

Slovenia

Spain

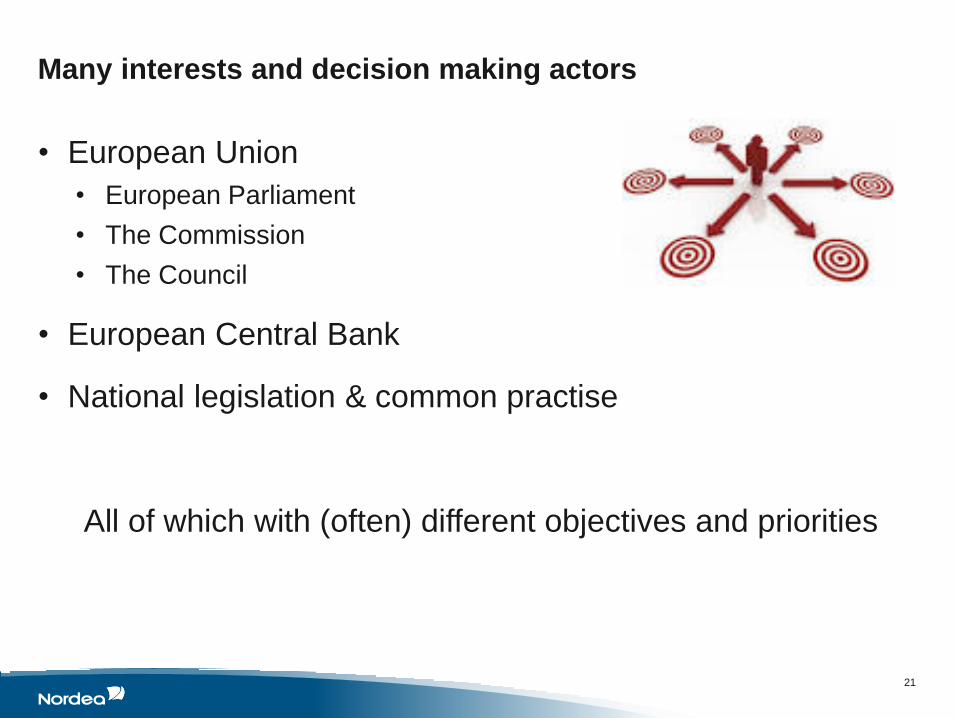

Many interests and decision making actors

• European Union

• European Parliament

• The Commission

• The Council

• European Central Bank

• National legislation & common practise

All of which with (often) different objectives and priorities

21

22

•

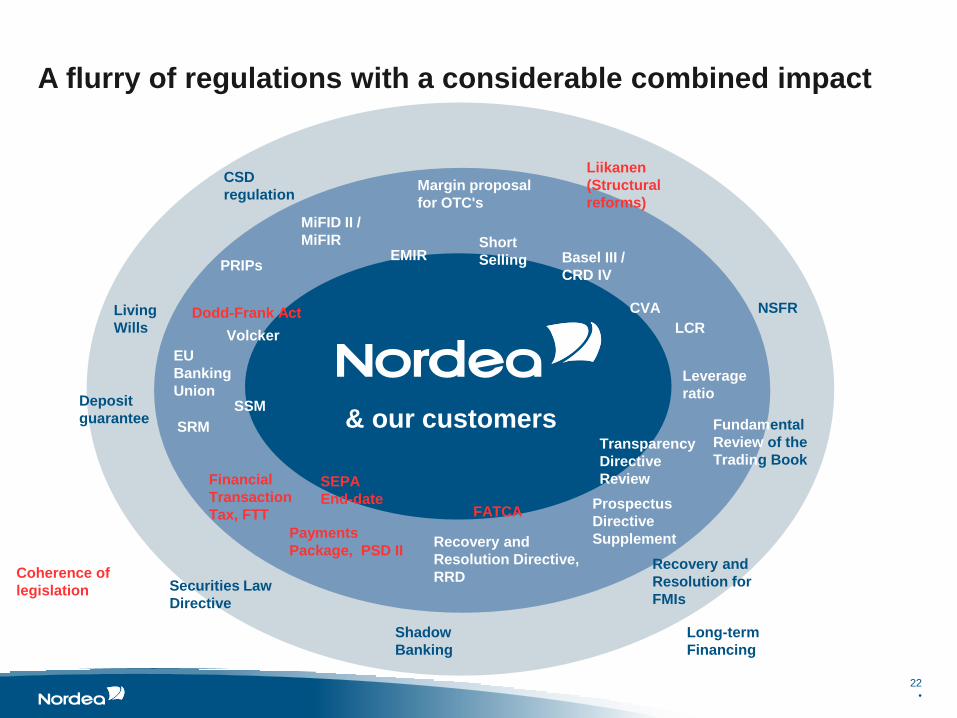

A flurry of regulations with a considerable combined impact

Securities Law

Directive

Financial

Transaction

Tax, FTT

Recovery and

Resolution for

FMIs

Liikanen

(Structural

reforms)

Shadow

Banking

MiFID II /

MiFIR EMIR

Short

Selling

CSD

regulation

PRIPs

Margin proposal

for OTC's

Dodd-Frank Act Living

Wills

EU

Banking

Union

Basel III /

CRD IV

Leverage

ratio

LCR

CVA

Fundamental

Review of the

Trading Book

Recovery and

Resolution Directive,

RRD

& our customers

Long-term

Financing

Transparency

Directive

Review

NSFR

SSM

SRM

Deposit

guarantee

SEPA

End-date

Payments

Package, PSD II

Volcker

FATCA Prospectus

Directive

Supplement

Coherence of

legislation

Other actors

• Financial Institutions

• Channel & product functionality

• Processors

• Organisations

• Financial organisations like European Banking Federations, Savings

Banks, Co-Op Banks

• Trade & Industry organisations

• Standardisation bodies

• ISO, Common Global Implementations (CGI), EPC etc.

• ERP Vendors

23

Our customers view of European payment services ?

24

Lack of flexibility

Complexity

25

All banks support and assist their customers on their way into

the European unknown market, by . . .

• Having a good product offering that will support the

customers requirements

• Making the products simpler for their customers by e.g.

using ‘conversion products’

• Moving towards CGI offerings in order to support also non-

euro based products

• Ensure to coordinate with ERP vendors and guide them

when needed

26

And the future . . .

We are now all moving fast into a more common use of ISO

20022 XML in all countries – mainly driven by the SEPA

initiative for euro

This also the case for ERP Vendors and will therefore benefit

our corporate customers

Will we have a fully harmonised payment market in Europe?

Not in the foreseeable future, but

some of the players in the future ‘payment’ market will have a

very different profile compared to those seen today

Related Documents