• Meaning and Definition CHAPTER 18 Overheads Aggregate of all expenses relating to indirect material cost, indirect labour cost and indirect expenses is known as Overhead. Accordingly, all expenses other than direct material cost, direct wages and direct expenses are referred to as overhead. According to Wheldon, Overhead may be defined as "the cost of indirect material, indirect labour and such other expenses including services as cannot conveniently be charged to a specific unit." Blocker and WeItmer define overhead as follows : "Overhead costs are operating cost of a business enterprise which cannot be traced directly to a particular unit of output. Further such costs are invisible or unaccountable." Importance of Overhead Cost Nowadays business is a dynamic organism. Advancement of technological development and innovation, economic situations and social considerations are the important factors for modernization of industries at mass production to meet its more demand. The overhead charges are heavily increased and they represent major portion of total cost. Therefore, it assumes greater importance for cost control and cost reduction. Classification of Overheads Classification of overheads is the process of grouping of costs based on the features and objectives of the business organization. The following are the important methods on which the overheads are classified: (a) On the basis of Nature. (b) On the basis of Function. (c) On the basis of Variability. (d) On the basis of Normality. (e) On the basis of Control.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

•

Meaning and Definition

CHAPTER 18

Overheads

Aggregate of all expenses relating to indirect material cost, indirect labour cost and indirect expenses is known as Overhead. Accordingly, all expenses other than direct material cost, direct wages and direct expenses are referred to as overhead.

According to Wheldon, Overhead may be defined as "the cost of indirect material, indirect labour and such other expenses including services as cannot conveniently be charged to a specific unit."

Blocker and WeItmer define overhead as follows :

"Overhead costs are operating cost of a business enterprise which cannot be traced directly to a particular unit of output. Further such costs are invisible or unaccountable."

Importance of Overhead Cost

Nowadays business is a dynamic organism. Advancement of technological development and innovation, economic situations and social considerations are the important factors for modernization of industries at mass production to meet its more demand. The overhead charges are heavily increased and they represent major portion of total cost. Therefore, it assumes greater importance for cost control and cost reduction.

Classification of Overheads

Classification of overheads is the process of grouping of costs based on the features and objectives of the business organization. The following are the important methods on which the overheads are classified:

(a) On the basis of Nature.

(b) On the basis of Function.

(c) On the basis of Variability.

(d) On the basis of Normality.

(e) On the basis of Control.

Overheads

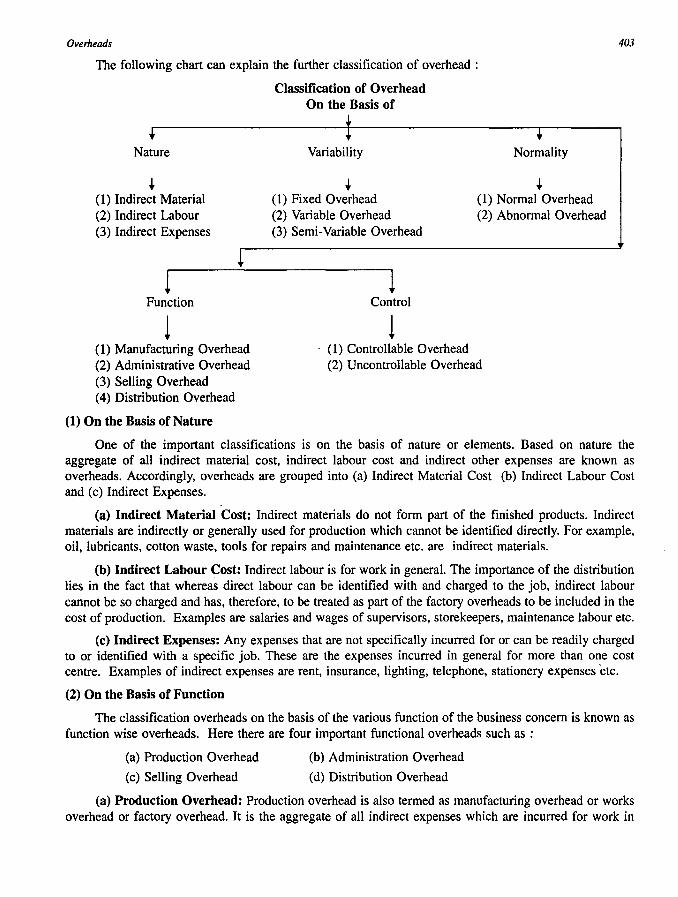

The following chart can explain the further classification of overhead :

Nature

t (1) Indirect Material (2) Indirect Labour (3) Indirect Expenses

1 Function

1 (1) Manufacturing Overhead (2) Administrative Overhead (3) Selling Overhead (4) Distribution Overhead

(1) On the Basis of Nature

Classification of Overhead On the Basis of

Variability

t (1) Fixed Overhead (2) Variable Overhead (3) Semi-Variable Overhead

1 Control

1

Normality

t (1) Normal Overhead (2) Abnormal Overhead

(1) Controllable Overhead (2) Uncontrollable Overhead

403

One of the important classifications is on the basis of nature or elements. Based on nature the aggregate of all indirect material cost, indirect labour cost and indirect other expenses are known as overheads. Accordingly, overheads are grouped into (a) Indirect Material Cost (b) Indirect Labour Cost and (c) Indirect Expenses.

(a) Indirect Material Cost: Indirect materials do not form part of the finished products. Indirect materials are indirectly or generally used for production which cannot be identified directly. For example, oil, lubricants, cotton waste, tools for repairs and maintenance etc. are indirect materials.

(b) Indirect Labour Cost: Indirect labour is for work in general. The importance of the distribution lies in the fact that whereas direct labour can be identified with and charged to the job, indirect labour cannot be so charged and has, therefore, to be treated as part of the factory overheads to be included in the cost of production. Examples are salaries and wages of supervisors, storekeepers, maintenance labour etc.

(c) Indirect Expenses: Any expenses that are not specifically incurred for or can be readily charged to or identified with a specific job. These are the expenses incurred in general for more than one cost centre. Examples of indirect expenses are rent, insurance, lighting, telephone, stationery expenses ·etc.

(2) On the Basis of Function

The classification overheads on the basis of the various function of the business concern is known as function wise overheads. Here there are four important functional overheads such as :

(a) Production Overhead

(c) Selling Overhead

(b) Administration Overhead

(d) Distribution Overhead

(a) Production Overhead: Production overhead is also termed as manufacturing overhead or works overhead or factory overhead. It is the aggregate of all indirect expenses which are incurred for work in

404 A Textbook of Financial Cost and Management Accounting

operation or factory. These costs are normally incurred during the period when the production process is carried on. For example, factory rent, factory light, power, factory employees' salary, oil, lubrication of plant & machinery, etc.

(b) Administrative Overhead: Administrative expenses are incurred in general for management to discharge its functions of planning organizing, controlling, co-ordination and directing. These expenses are not specifically incurred and cannot be identified with the specific job. It is also termed as office cost. For example, office rent, rates, printing, stationery, postage, telegram, legal expenses etc. are the office and administrative costs.

(c) Selling Overheads: Selling expenses are overheads which are incurred for promoting sales, securing orders, creating demand and retaining customers. For example, salesmen's salaries, advertisement, rent and rates of show room, samples, commission etc.

(d) Distribution Overhead: Distribution overhead are incurred for distribution of products or output from producers to the ultimate consumers. For example, warehouse staff salaries, expenses of delivery van, storage expenses, packing etc.

(3) On the Basis of Variability

One of the important classifications is on the basis of variability. According to this, the expenses can be grouped into (a) Fixed Overhead (b) Variable Overhead and (c) Semi-Variable Overhead.

(a) Fixed Overhead: Fixed cost or overhead incurred remain constant due to change in the volume output or change in the volume of sales. For example, rent and rates of buildings, depreciation of plant, salaries of supervisors etc.

(b) Variable Overhead: Variable overhead may be defined as "they tend to increase or decrease in total amount with changes in the volume of output or volume of sales." Accordingly the change is in direct proportion to output. Indirect materials, Indirect labour, repair and maintenance, power, fuel, lubricants etc. are examples of variable overhead costs.

(c) Semi-Variable Overheads: Semi-variable overheads are incurred with a change in the volume of output or turnover. They neither remain fixed nor do they tend to vary directly with the output. These costs remain fixed upto a certain volume of output but they will vary at other part of activity. Semi-variable overheads are mixed cost, i.e., partly fixed and partly variable. For example, power, repairs and maintenance, depreciation of plant and machinery telephone etc.

(4) On the Basis of Normality

Overheads are classified into normal overheads and abnormal overheads on the basis of normality features. According to this normal overheads are incurred in achieving the target output or fixed plan. On the other hand, abnormal overhead costs are not expected to be incurred at a given level of output in the conditions in which the level of output is normally produced. For example, abnormal idle time, abnormal

• wastage etc. Such expenses are transferred to Profit and Loss Account.

(5) On the Basis of Control

It is one of important classifications of overhead on the basis of control. Based on control it is grouped into controllable overhead and uncontrollable overhead. Controllable overhead which can be controlled by the action of a specified number of undertaking. For example, idle time, wastages etc. can be controlled. Uncontrollable overheads cannot be controlled by the action of the executive heading the responsibility centre. For example, rent and rates of building cannot be controlled.

Overheads

Usefulness of Overhead Classification

(1) It ensures effective cost control.

(2) It helps the management for effective decision making.

405

(3) The application of marginal costing is essentially for profit planning, cost control, decision making etc. are based on the classification of overheads.

(4) On the basis of classification of fixed and variable cost, flexible budgets are prepared at different levels of activity.

(5) It facilitates fixing of selling price.

(6) Cost classification is useful for break-even analysis. Break-even analysis mainly depends on overall.cost and profi"t which can be useful for making or buying decision.

(7) It helps to find out the unit cost of production.

Codification of Overhead

Codification is a process of representing each item by a number, the digits of which indicate the group, the subgroup, the type and the dimension of the item.

Advantages of Codification

(1) It enables systematic grouping of similar items and avoids confusion caused by long description of the items.

(2) It serves as the starting point of implication and standardization.

(3) It helps in avoiding duplication of items and results in the minimisation of number of items, leading to accurate records.

(4) It ~elps in allocation and apportionment of overheads to different cost centres.

(5) It assists the grouping of overheads for cost control.

(6) It helps in reducing clerical efforts to the minimum.

Methods of Codification

There are different methods used for codification. The following are the three important methods used:

(1) Numerical Codes Method.

(2) Decimal Codes Method.

(3) Codes with a Combination of Numbers and Alphabets.

(1) Numerical Method: Under this method, numerical codes are assigned to each item of expenses. For example,

100 Indirect labour.

400 Power.

500 Maintenance.

800 Fixed charges.

406 A Textbook of Financial Cost and Management Accounting

(2) Decimal Codes: Under this method, the whole numbers are allotted to indicate master group and the decimals indicate the sub-group. For example,

Factory Overheads:

1.1.1 Indirect materials.

1.1.2 Consumable stores.

1.1.3 Lubricating oils.

(3) Codes with a Combination of Numbers and Alphabet : Under this method the alphabet indicates the main group and the type of expenses is indicated by the numerical. For example,

Rl - Repairs to machinery.

R2 - Repairs to plant.

R3 - Repairs to furniture.

Procedure or Steps in Overhead

Overheads are incurred for work in general. Overhead is added tQ the prime cost in order to measure the total cost of production or cost of goods sold. For allocation and apportionment of overhead in the cost of production or cost of goods sold the following procedures are involved:

(1)

(2)

(3)

Classification of Overhead

Collection of Overhead

. Overhead Analysis: :~; "i.;.:~:- '

(a) Distribution of overhead to production and service departments, i.e., AllocatiOllnmd .,,'

Apportionment of overhead to cost centre. ' .

(b) Re-distribution of overhead from service department to production department, i.e., Allocation and Apportionment of service centres to production centres or departments.

(4) Absorption of overhead by cost units, i.e., computation of overhead absorption rates.

(1) Classification Overhead: We have already discussed the classification of overh~ad in the preceding pages, and the discussion on other procedures would follow in this chapter and the subsequent one.

(2) Collection of Overhead: The production overheads or factory overheads are collected and identified under separate overhead code numbers or standing order numbers. These overheads are collected from different sources and documents. The following are the important sources and documents :

Overhead Expenses

(1) Indirect Materials (2) Power and light (3) Indirect wages (4) Salaries (5) Depreciation (6) Rates (7) Rates (8) Office Stationery (9) Postage

Sources and Documents Used

Materials Requisition Meter Reading Time Cards, Pay Rolls, Wage Analysis Salaries Sheet Plant Register, Machinery Register Lease Local Government Assessment Supplier's Invoices Postage Book

Overheads 407

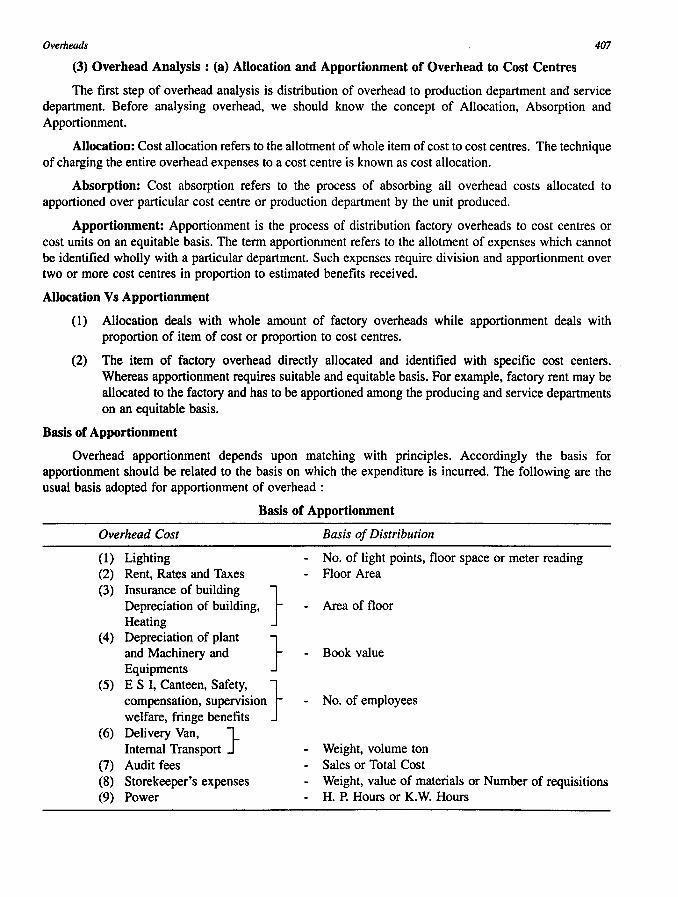

(3) Overhead Analysis : (a) Allocation and Apportionment of Overhead to Cost Centres

The first step of overhead analysis is distribution of overhead to production department and service department. Before analysing overhead, we should know the concept of Allocation, Absorption and Apportionment.

Allocation: Cost allocation refers to the allotment of whole item of cost to cost centres. The technique of charging the entire overhead expenses to a cost centre is known as cost allocation.

Absorption: Cost absorption refers to the process of absorbing all overhead costs allocated to apportioned over particular cost centre or production department by the unit produced.

Apportionment: Apportionment is the process of distribution factory overheads to cost centres or cost units on an equitable basis. The term apportionment refers to the allotment of expenses which cannot be identified wholly with a particular department. Such expenses require division and apportionment over two or more cost centres in proportion to estimated benefits received.

Allocation Vs Apportionment

(1) Allocation deals with whole amount of factory overheads while apportionment deals with proportion of item of cost or proportion to cost centres.

(2) The item of factory overhead directly allocated and identified with specific cost centers. Whereas apportionment requires suitable and equitable basis. For example, factory rent may be allocated to the factory and has to be apportioned among the producing and service departments on an equitable basis.

Basis of Apportionment

Overhead apportionment depends upon matching with principles. Accordingly the basis for apportionment should be related to the basis on which the expenditure is incurred. The following are the usual basis adopted for apportionment of overhead :

Basis of Apportionment

Overhead Cost

(1) Lighting (2) Rent, Rates and Taxes (3) Insurance of building }

Depreciation of building, Heating

(4) Depreciation of plant } and Machinery and Equipments

(5) E S I, Canteen, Safety, } compensation, supervision welfare, fringe benefits

(6) Delivery Van, } Internal Transport

(7) Audit fees (8) Storekeeper's expenses (9) Power

Basis of Distribution

- No. of light points, floor space or meter reading - Floor Area

Area of floor

- Book value

- No. of employees

- Weight, volume ton - Sales or Total Cost - Weight, value of materials or Number of requisitions - H. P. Hours or K. W. Hours

408

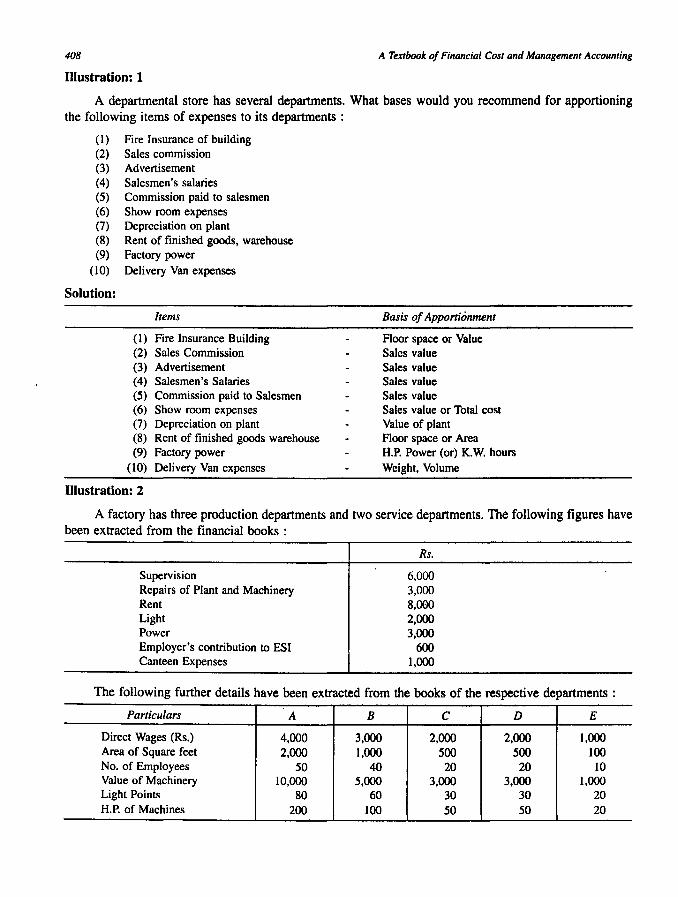

Illustration: 1

A Textbook of Financial Cost and Management Accounting

A departmental store has several departments. What bases would you recommend for apportioning the following items of expenses to its departments :

(I) Fire Insurance of building (2) Sales commission (3) Advertisement (4) Salesmen's salaries (5) Commission paid to salesmen (6) Show room expenses (7) Depreciation on plant (8) Rent of finished goods, warehouse (9) Factory power

(10) Delivery Van expenses

Solution:

Items

(I) Fire Insurance Building (2) Sales Commission (3) Advertisement (4) Salesmen's Salaries (5) Commission paid to Salesmen (6) Show room expenses (7) Depreciation on plant (8) Rent of finished goods warehouse (9) Factory power

(10) Delivery Van expenses

Illustration: 2

Basis of Apportionment

Floor space or Value Sales value Sales value Sales value Sales value Sales value or Total cost Value of plant Floor space or Area H.P. Power (or) K.W. hours Weight, Volume

A factory has three production departments and two service departments. The following figures have been extracted from the financial books :

Supervision Repairs of Plant and Machinery Rent Light Power Employer's contribution to ESI Canteen Expenses

Rs.

6,000 3,000 8,000 2,000 3,000

600 1,000

The following further details have been extracted from the books of the respective departments :

Particulars A B C D E

Direct Wages (Rs.) 4,000 3,000 2,000 2,000 1,000 Area of Square feet 2,000 1,000 500 500 100 No. of Employees 50 40 20 20 10 Value of Machinery 10,000 5,000 3,000 3,000 1,000 Light Points 80 60 30 30 20 H.P. of Machines 200 100 50 50 20

Overheads 409

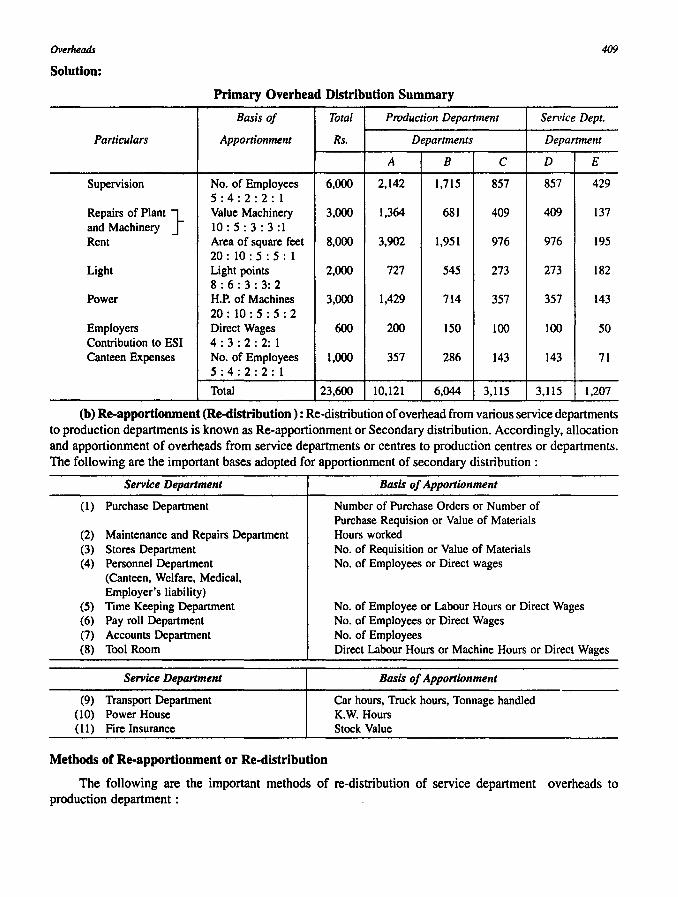

Solution:

Primary Overhead Distribution Summary

Basis of Total Production Department Sen'ice Dept.

Particulars Apportionment Rs. Departments Department

A B C D E

Supervision No. of Employees 6,000 2,142 1,715 857 857 429 5:4:2:2:1

Repairs of Plant } Value Machinery 3,000 1,364 681 409 409 137 and Machinery 10:5:3:3:1 Rent Area of square feet 8,000 3,902 1,951 976 976 195

20:10:5:5:1 Light Light points 2,000 727 545 273 273 182

8: 6: 3 : 3: 2 Power H.P. of Machines 3,000 1,429 714 357 357 143

20:10:5:5:2 Employers Direct Wages 600 200 150 100 100 50 Contribution to ESI 4: 3 : 2 : 2: 1 Canteen Expenses No. of Employees 1,000 357 286 143 143 71

5:4:2:2:1

Total 23,600 10,121 6,044 3,115 3,115 1,207

(b) Re-apportionment (Re-distribution): Re-distribution of overhead from various service departments to production departments is known as Re-apportionment or Secondary distribution. Accordingly, allocation and apportionment of overheads from service departments or centres to production centres or departments. The following are the important bases adopted for apportionment of secondary distribution:

Service Department

(1) Purchase Department

(2) Maintenance and Repairs Department (3) Stores Department (4) Personnel Department

(Canteen, Welfare, Medical, Employer's liability)

(5) Time Keeping Department (6) Pay roll Department (7) Accounts Department (8) Tool Room

Service Department

(9) Transport Department (10) Power House (11) Fire Insurance

Methods or Re-apportionment or Re-distribution

Basis of Apportionment

Number of Purchase Orders or Number of Purchase Requision or Value of Materials Hours worked No. of Requisition or Value of Materials No. of Employees or Direct wages

No. of Employee or Labour Hours or Direct Wages No. of Employees or Direct Wages No. of Employees Direct Labour Hours or Machine Hours or Direct Wages

Basis of Apportionment

Car hours, Truck hours, Tonnage handled K.W. Hours Stock Value

The following are the important methods of re-distribution of service department overheads to production department :

410 A Textbook of Financial Cost and Management Accounting

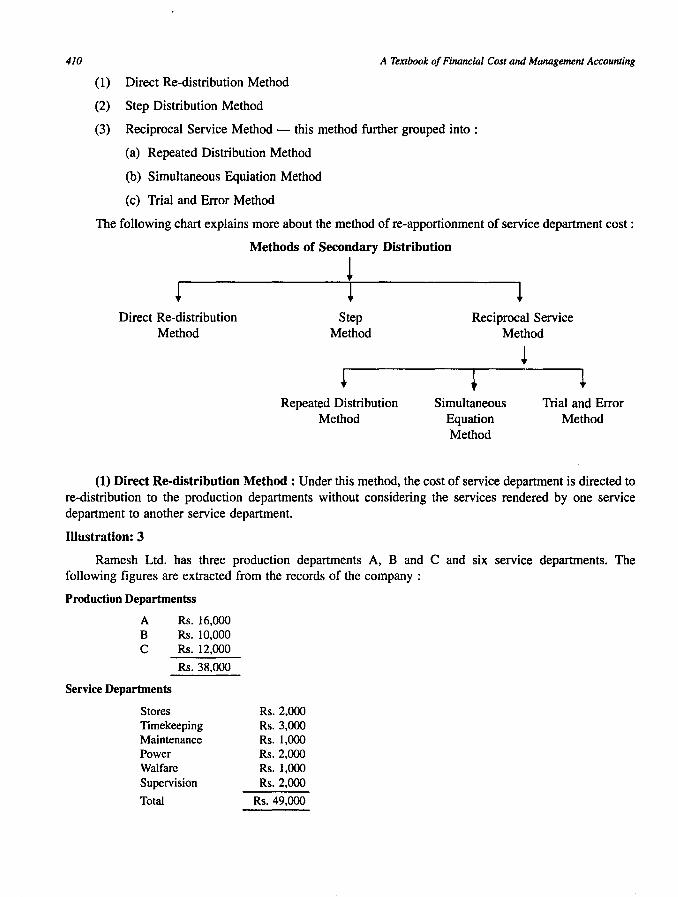

(1) Direct Re-distribution Method

(2) Step Distribution Method

(3) Reciprocal Service Method - this method further grouped into:

(a) Repeated Distribution Method

(b) Simultaneous Equiation Method

(c) Trial and Error Method

The following chart explains more about the method of re-apportionment of service department cost:

Direct Re-distribution Method

Methods of Secondary Distribution

! Step

Method

Repeated Distribution Method

1 Reciprocal Service

Method

Simultaneous Equation Method

Trial and Error Method

(1) Direct Re-distribution Method: Under this method, the cost of service department is directed to re-distribution to the production departments without considering the services rendered by one service department to another service department.

Illustration: 3

Ramesh Ltd. has three production departments A, Band C and six service departments. The following figures are extracted from the records of the company :

Production Departmentss

A Rs.16,Ooo B Rs.IO,OOO C Rs.12,OOO

Rs.38,OOO

Service Departments

Stores Timekeeping Maintenance Power Walfare Supervision

Total

Rs.2,OOO Rs.3,OOO Rs. 1,000 Rs.2,OOO Rs. 1,000 Rs.2,OOO

Rs.49,OOO

Overheads 411

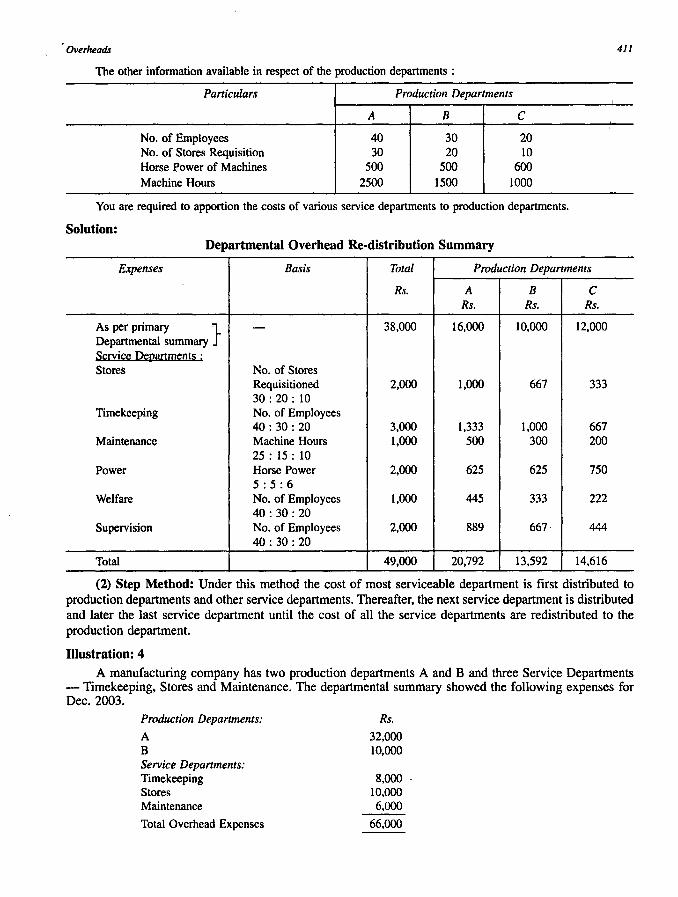

The other information available in respect of the production departments :

Particulars Production Departments ,

A B C I

No. of Employees 40 30 20 No. of Stores Requisition 30 20 10 Horse Power of Machines 500 500 600 Machine Hours 2500 1500 1000

You are required to apportion the costs of various service departments to production departments.

Solution: Departmental Overhead Re-distribution Summary

Expenses Basis Total Production Departments

Rs. A B C Rs. Rs. Rs.

As per primary } - 38,000 16,000 10,000 12,000 Departmental summary S!<rvik~ Del2artm!<!lt§ ; Stores No. of Stores

Requisitioned 2,000 1,000 667 333 30: 20 : 10

Timekeeping No. of Employees 40:30:20 3,000 1,333 1,000 667

Maintenance Machine Hours 1,000 500 300 200 25: 15: 10

Power Horse Power 2,000 625 625 750 5:5:6

Welfare No. of Employees 1,000 445 333 222 40:30:20

Supervision No. of Employees 2,000 889 667 444 40: 30: 20

Total 49,000 20,792 13,592 14,616

(2) Step Method: Under this method the cost of most serviceable department is first distributed to production departments and other service departments. Thereafter, the next service department is distributed and later the last service department until the cost of all the service departments are redistributed to the production department.

Illustration: 4 A manufacturing company has two production departments A and B and three Service Departments

- Timekeeping, Stores and Maintenance. The departmental summary showed the following expenses for Dec. 2003.

Production Departments:

A B Service Departments: Timekeeping Stores Maintenance

Total Overhead Expenses

Rs.

32,000 10,000

8,000 10,000 6,000

66,000

412 A Textbook of Financial Cost and Management Accounting

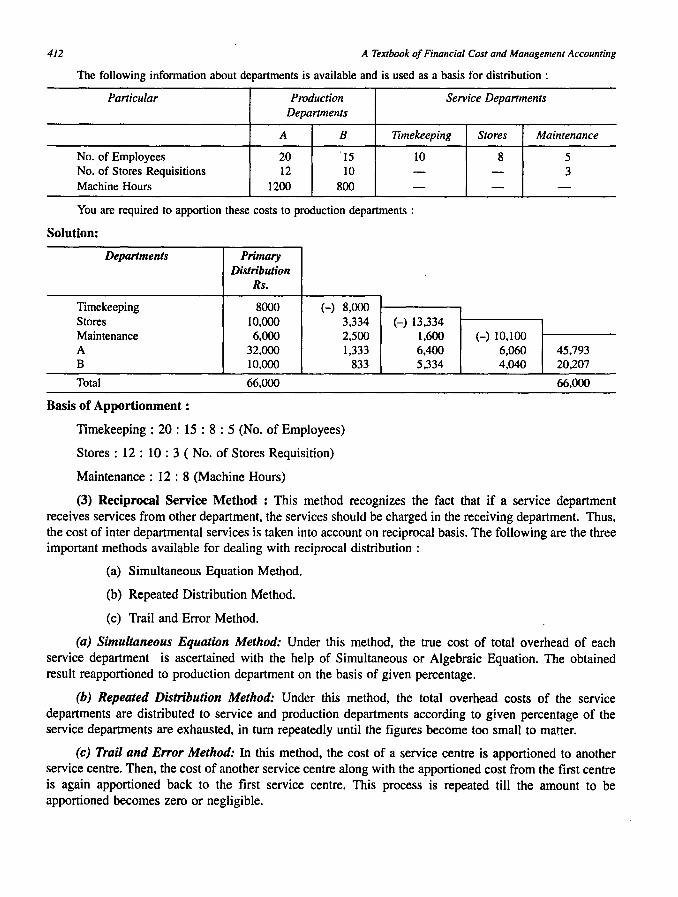

The following information about departments is available and is used as a basis for distribution :

Particular Production Service Departments Departments

A B Timekeeping Stores Maintenance

No. of Employees 20 '15 10 No. of Stores Requisitions 12 10 -Machine Hours 1200 800 -You are required to apportion these costs to production departments :

Solution:

Departments Primary Distribution

Rs.

Timekeeping 8000 (-) 8,000 Stores 10,000 3,334 Maintenance 6,000 2,500 A 32,000 1,333 B 10,000 833

Total 66,000

Basis of Apportionment:

Timekeeping: 20 : 15 : 8 : 5 (No. of Employees)

Stores: 12 : 10 : 3 ( No. of Stores Requisition)

Maintenance: 12 : 8 (Machine Hours)

(-) 13,334 1,600 6,400 5,334

8 5 - 3

- -

(-) 10,100 6,060 45,793 4,040 20,207

66,000

(3) Reciprocal Service Method : This method recognizes the fact that if a service department receives services from other department, the services should be charged in the receiving department. Thus, the cost of inter departmental services is taken into account on reciprocal basis. The following are the three important methods available for dealing with reciprocal distribution :

(a) Simultaneous Equation Method.

(b) Repeated Distribution Method.

(c) Trail and Error Method.

(a) Simultaneous Equation Method: Under this method, the true cost of total overhead of each service department is ascertained with the help of Simultaneous or Algebraic Equation. The obtained result reapportioned to production department on the basis of given percentage.

(b) Repeated Distribution Method: Under this method, the total overhead costs of the service departments are distributed to service and production departments according to given percentage of the service departments are exhausted, in tum repeatedly until the figures become too small to matter.

(c) Trail and Error Method: In this method, the cost of a service centre is apportioned to another service centre. Then, the cost of another service centre along with the apportioned cost from the first centre is again apportioned back to the first service centre. This process is repeated till the amount to be apportioned becomes zero or negligible.

Overheads 413

Illustration: 5

The following particulars related to a manufacturing company has three production departments : P, Q, : and R and two service departments X and Y :

Production Departments:

P Rs.2,ooO Q Rs.l,5oo R Rs.l,ooo

Service Departments:

S Rs. 500 T Rs.4oo

The service department expenses are charged on a percentage basis as folIows :

Productions Departments Service Departments

Service Depts. :

S T

P

20% 30%

Q

30% 30%

R

40% 20%

S

20%

T

10%

Prepare a statement showing the distribution of the two service departments expenses to three production departments under (1) Simultaneous Equation Method and (2) Repeated Distribution Method.

Solution:

(1) Simultaneous Equation Method:

Let X be the total expenses of Departments S Let Y be the total expenses of Department T X = 500 + 0.20 Y Y = 400 + 0.10 X X = 500 + 0.20 (400 + O.IOX) X = 500 + 80 + 0.02X X - 0.20X = 580 (or) 0.98 X = 580

580 .. X = -- = 59l.83

0.98

Y = 400 + 0.10 (592) = 400 + 59

Y =459

Departmental Overhead Distribution Summary

Particulars Production Departments P Q R

Rs. Rs. Rs.

Overhead as per Summary 2,000 1,500 1,000 Department S 118 178 237 Department T 138 137 92

Total 2,256 1,815 1,329

Service Departments S T

Rs. Rs.

500 400 (-) 592 59

92 (-) 459

- -

414 A Textbook of Financial Cost and Management Accounting

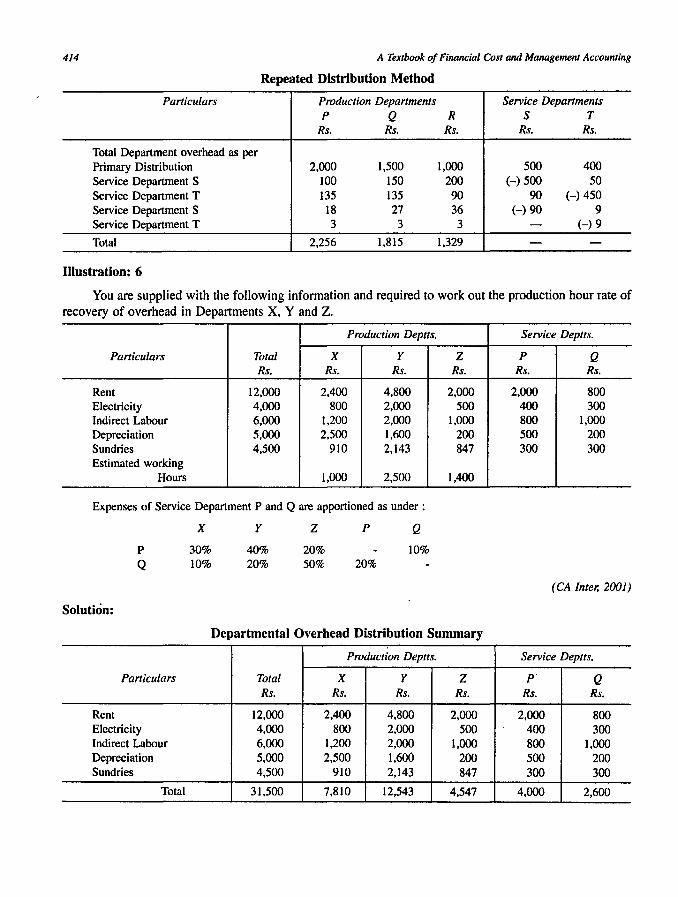

Repeated Distribution Method

Particulars Production Departments Service Departments P Q R S T

Rs. Rs. Rs. Rs. Rs.

Total Department overhead as per Primary Distribution 2,000 1,500 1,000 500 400 Service Department S 100 150 200 (-) 500 50 Service Department T 135 135 90 90 (-) 450 Service Department S 18 27 36 (-) 90 9 Service Department T 3 3 3 - (-) 9

Total 2,256 1,815 1,329 - -

Illustration: 6

You are supplied with the following infonnation and required to work out the production hour rate of recovery of overhead in Departments X, Y and Z.

Production Deplts.

Particulars Total X Y Z Rs. Rs. Rs. Rs.

Rent 12,000 2,400 4,800 2,000 Electricity 4,000 800 2,000 500 Indirect Labour 6,000 1,200 2,000 1,000 Depreciation 5,000 2,500 1,600 200 Sundries 4,500 910 2,143 847 Estimated working

Hours 1,000 2,500 1,400

Expenses of Service Department P and Q are apportioned as under :

Solution:

P Q

Particulars

Rent Electricity Indirect Labour Depreciation Sundries

Total

X

30% 10%

y

40% 20%

z 20% 50%

P Q

10% 20%

Departmental Overhead Distribution Summary

Production Deptts.

Total X Y Z Rs. Rs. Rs. Rs.

12,000 2,400 4,800 2,000 4,000 800 2,000 500 6,000 1,200 2,000 1,000 5,000 2,500 1,600 200 4,500 910 2,143 847

31,500 7,810 12,543 4,547

Service Deptts.

P Q Rs. Rs.

2,000 800 400 300 800 1,000 500 200 300 300

(C7A Inter, 2Ck71)

Service Deptts.

P' Q Rs. Rs.

2,000 800 400 300 800 1,000 500 200 300 300

4,000 2,600

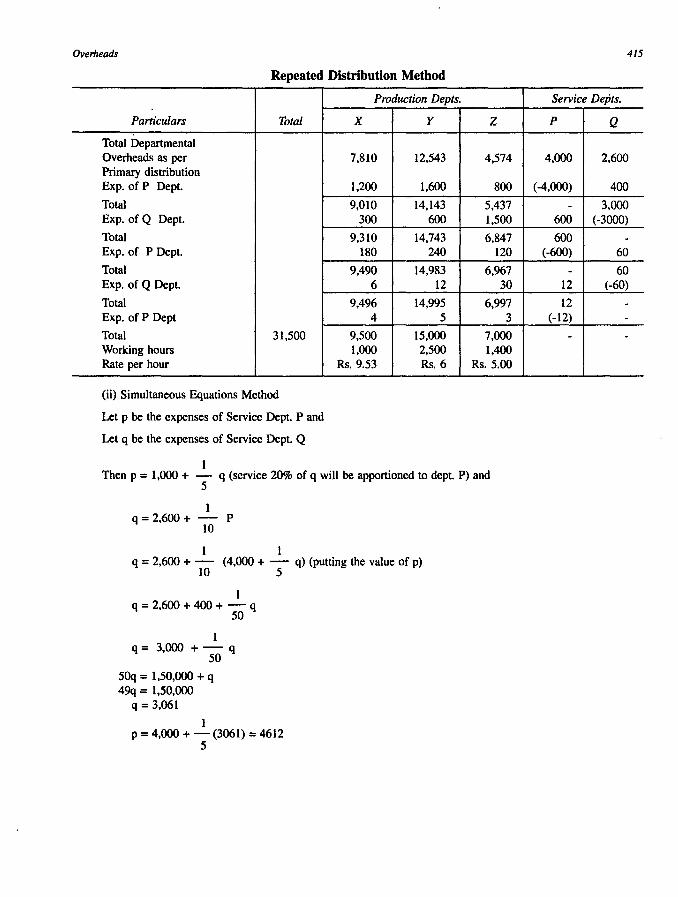

Overheads

Repeated Distribution Method

Particulars Total

Total Departmental Overheads as per Primary distribution Exp. of P Dept

Total Exp. of Q Dept.

Total Exp. of P Dept.

Total Exp. of Q Dept.

Total Exp. of P Dept

Total 31.500 Working hours Rate per hour

(ii) Simultaneous Equations Method

Let p be the expenses of Service Dept. P and

Let q be the expenses of Service Dept. Q

1

Production Depts.

X Y

7.810 12.543

1.200 1.600

9.010 14.143 300 600

9.310 14.743 180 240

9.490 14.983 6 12

9,496 14.995 4 5

9.500 15.000 1.000 2.500

Rs.9.53 Rs.6

Z

4.574

800

5,437 1.500

6.847 120

6.967 30

6.997 3

7.000 1,400

Rs.5.oo

Then p = 1,000 + - q (service 20% of q wi\1 be apportioned to dept. P) and 5

1 q=2,600+ - P

10

1 1 q = 2.600 + - (4,000 + - q) (putting the value of p)

10 5

1 q = 2,600 + 400 + - q

50

1 q= 3,000 + - q

50

50q = 1,50,000 + q 49q = 1,50.000

q = 3,061

1 P = 4.000 + - (3061) = 4612

5

415

Service Depts.

P Q

4.000 2.600

(-4.000) 400

- 3.000 600 (-3000)

600 -(-600) 60

- 60 12 (-60)

12 -(-12) -

- -

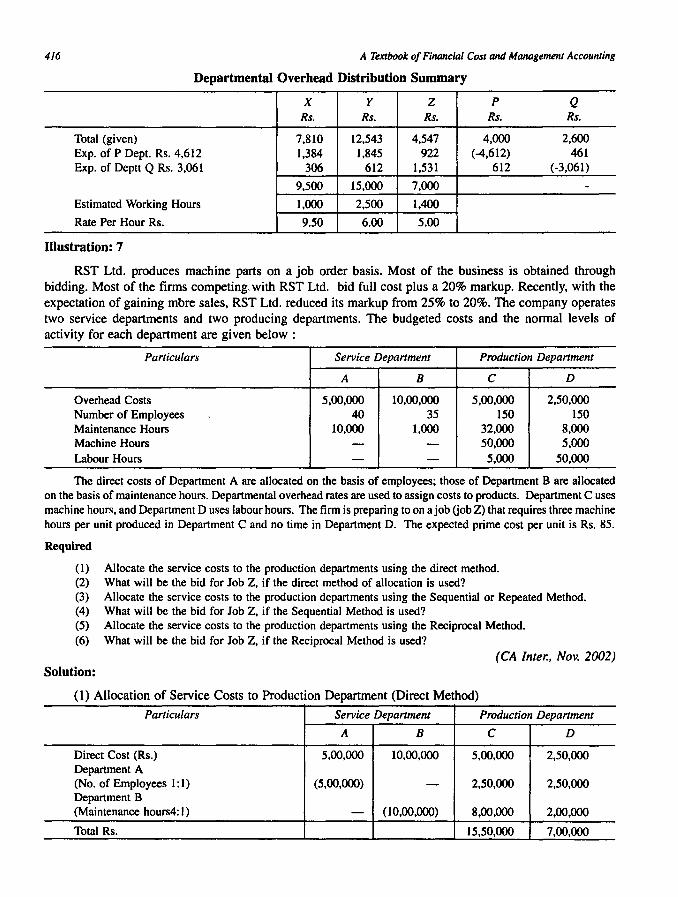

416 A Textbook of Financial Cost and Management Accounting

Departmental Overhead Distribution Summary

x y z P Q Rs. Rs. Rs. Rs. Rs.

Total (given) 7,810 12,543 4,547 4,000 2,600 Exp. of P Dept. Rs. 4,612 1,384 1,845 922 (-4,612) 461 Exp. of Deptt Q Rs. 3,061 306 612 1,531 612 (-3,061)

9,500 15,000 7,000 -Estimated Working Hours 1,000 2,500 1,400

Rate Per Hour Rs. 9.50 6.00 5.00

Illustration: 7

RST Ltd. produces machine parts on a job order basis. Most of the business is obtained through bidding. Most of the firms competing. with RST Ltd. bid full cost plus a 20% markup. Recently, with the expectation of gaining mbre sales, RST Ltd. reduced its markup from 25% to 20%. The company operates two service departments and two producing departments. The budgeted costs and the normal levels of activity for each department are given below:

Particulars Service Department Production Department

A B C D

Overhead Costs 5,00,000 10,00,000 5,00,000 2,50,000 Number of Employees 40 35 150 150 Maintenance Hours 10,000 1,000 32,000 8,000 Machine Hours - - 50,000 5,000 Labour Hours - - 5,000 50,000

The direct costs of Department A are allocated on the basis of employees; those of Department B are allocated on the basis of maintenance hours. Departmental overhead rates are used to assign costs to products. Department C uses machine hours, and Department D uses labour hours. The firm is preparing to on ajob Gob Z) that requires three machine hours per unit produced in Department C and no time in Department D. The expected prime cost per unit is Rs. 85.

Required

(1) Allocate the service costs to the production departments using the direct method. (2) What will be the bid for Job Z, if the direct method of allocation is used? (3) Allocate the service costs to the production departments using the Sequential or Repeated Method. (4) What will be the bid for Job Z, if the Sequential Method is used? (5) Allocate the service costs to the production departments using the Reciprocal Method. (6) What will be the bid for Job Z, if the Reciprocal Method is used?

(CA Inter., Nov. 2002) Solution:

(1) Allocation of Service Costs to Production Department (Direct Method)

Particulars Service Department Production Department

A B C D

Direct Cost (Rs.) 5,00,000 10,00,000 5,00,000 2,50,000 Department A (No. of Employees 1: 1) (5,00,000) - 2,50,000 2,50,000 Department B (Maintenance hours4: 1) - (10,00,000) 8,00,000 2,00,000

Total Rs. 15,50,000 7,00,000

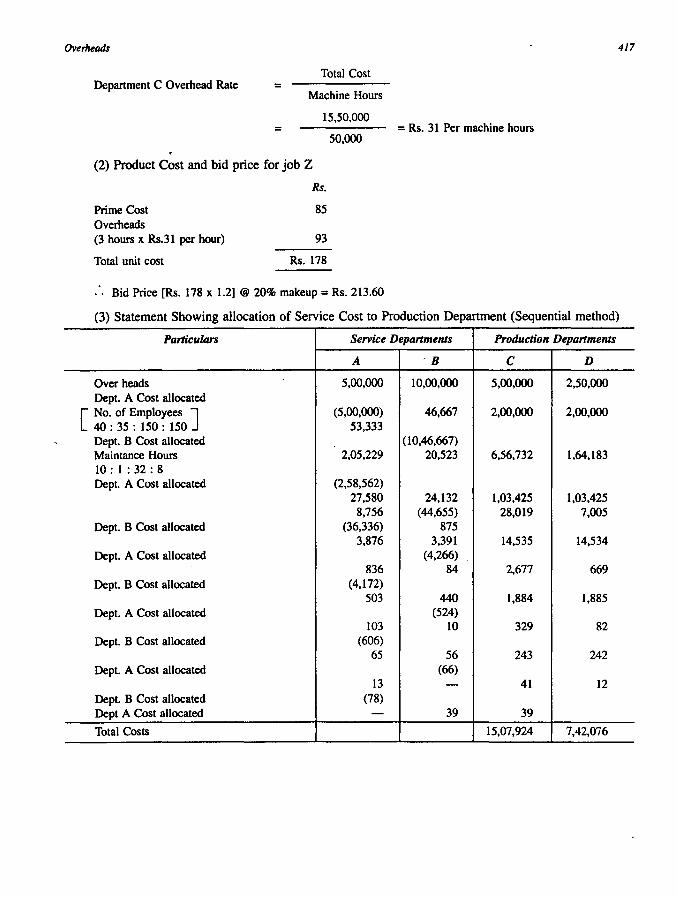

Overheads

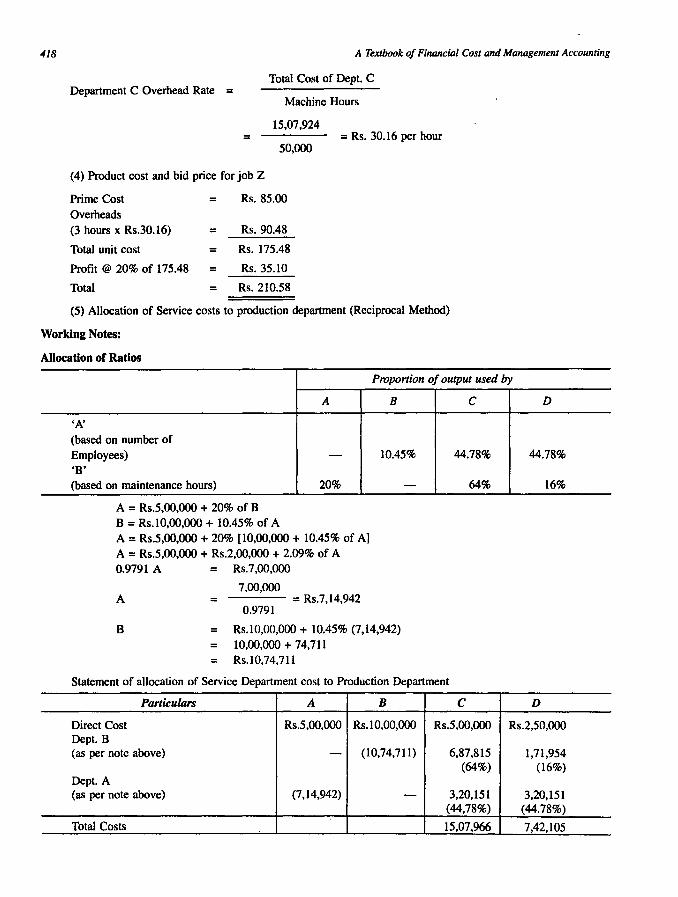

Total Cost Department C Overhead Rate =

Machine Hours

15,50,000 =

50,000

(2) Product Cost and bid price for job Z

Rs.

Prime Cost Overheads (3 hours x Rs.31 per hour)

Total unit cost

85

93

Rs. 178

:. Bid Price [Rs. 178 x 1.2] @ 20% makeup = Rs. 213.60

417

= Rs. 31 Per machine hours

(3) Statement Showing allocation of Service Cost to Production Department (Sequential method)

Particulars Service Departments Production Departments

A '8 C D

Over heads 5,00,000 10,00,000 5,00,000 2,50,000 Dept. A Cost allocated

[ No. of Employees ] (5,00,000) 46,667 2,00,000 2,00,000 40 : 35 : 150 : 150 53,333 Dept. B Cost allocated (l0,46,667) Maintance Hours 2,05,229 20,523 6,56,732 1,64,183 10 : 1 : 32 : 8 Dept. A Cost allocated (2,58,562)

27,580 24,132 1,03,425 1,03,425 8,756 (44,655) 28,019 7,005

Dept. B Cost allocated (36,336) 875 3,876 3,391 14,535 14,534

Dept. A Cost allocated (4,266) 836 84 2,677 669

Dept. B Cost allocated (4,172) 503 440 1,884 1,885

Dept. A Cost allocated (524) 103 10 329 82

Dept. B Cost allocated (606) 65 56 243 242

Dept. A Cost allocated (66) 13 - 41 12

Dept. B Cost allocated (78) Dept A Cost allocated - 39 39

Total Costs 15,07,924 7,42,076

•

418 A Textbook of Fi1Ul1lciai Cost and Management Accounting

Department C Overhead Rate =

=

Total Cost of Dept. C

Machine Hours

15,07,924

50,000 = Rs. 30.16 per hour

(4) Product cost and bid price for job Z

Prime Cost = Rs.85.00

Overheads (3 hours x Rs.30.16) = Rs.90.48

Total unit cost = Rs. 175.48

Profit @ 20% of 175.48 = Rs.35.10

Total = Rs.210.58

(5) Allocation of Service costs to production department (Reciprocal Method)

Working Notes:

Allocation of Ratios

Proportion of output used by

A

'A' (based on number of Employees) -'B' (based on maintenance hours) 20%

A = Rs.5,00,000 + 20% of B B = Rs.IO,OO,OOO + 10.45% of A A = Rs.5,00,000 + 20% [10,00,000 + 10.45% of A] A = Rs.5,00,000 + Rs.2,00,000 + 2.09% of A 0.9791 A = Rs.7,OO~OOO

7,00,000 A = = Rs.7,14,942

0.9791

B

10.45%

-

B = Rs.IO,OO,OOO + 10.45% (7,14,942)

= 10,00,000 + 74,711

= Rs.IO,74,711

C

44.78%

64%

Statement of allocation of Service Department cost to Production Department

Particulars A B C

Direct Cost Rs.5.00,000 Rs.IO,OO,OOO Rs.5,00,000 Dept. B (as per note above) - (10,74,711) 6,87,815

(64%) Dept. A (as per note above) (7,14,942) - 3,20,151

(44,78%)

Total Costs 15,07,966

D

44.78%

16%

D

Rs.2,50,000

1,71,954 (16%)

3,20,151 (44.78%)

7,42,105

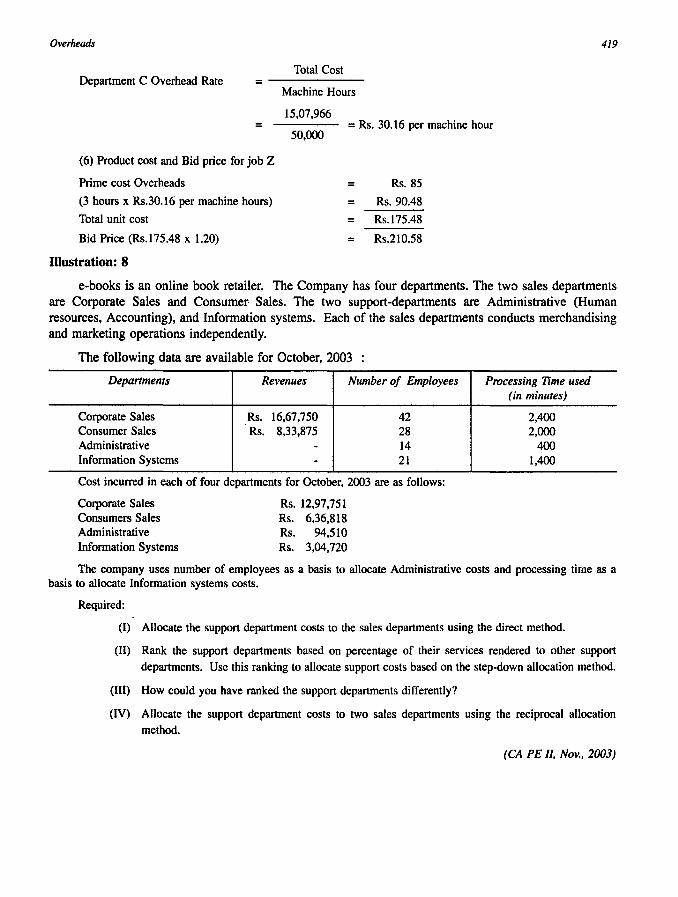

Overheads

Total Cost Department C Overhead Rate =------

=

(6) Product cost and Bid price for job Z

Prime cost Overheads

(3 hours x Rs.30.16 per machine hours)

Total unit cost

Bid Price (Rs.l75.48 x 1.20)

Illustration: 8

Machine Hours

15,07,966

50,000 = Rs. 30.16 per machine hour

= Rs.85

= Rs.90.48

= Rs.175.48

= Rs.210.58

419

e-books is an online book retailer. The Company has four departments. The two sales departments are Corporate Sales and Consumer Sales. The two support-departments are Administrative (Human resources, Accounting), and Information systems. Each of the sales departments conducts merchandising and marketing operations independently.

The following data are available for October, 2003 :

Departments Revenues Number of Employees

Corporate Sales Rs. 16,67,750 42 Consumer Sales Rs. 8,33,875 28 Administrative - 14 Information Systems - 21

Cost incurred in each of four departments for October, 2003 are as follows:

Corporate Sales Consumers Sales Administrative Information Systems

Rs. 12,97,751 Rs. 6,36,818 Rs. 94,510 Rs. 3,04,720

Processing TIme used (in minutes)

2,400 2,000

400 1,400

The company uses number of employees as a basis to allocate Administrative costs and processing time as a basis to allocate Information systems costs.

Required:

(I) Allocate the support department costs to the sales departments using the direct method.

(II) Rank the support departments based on percentage of their services rendered to other support

departments. Use this ranking to allocate support costs based on the step-down allocation method.

(III) How could you have ranked the support departments differently?

(IV) Allocate the support department costs to two sales departments using the reciprocal allocation method.

(CA PE II, Nov., 2003)

420

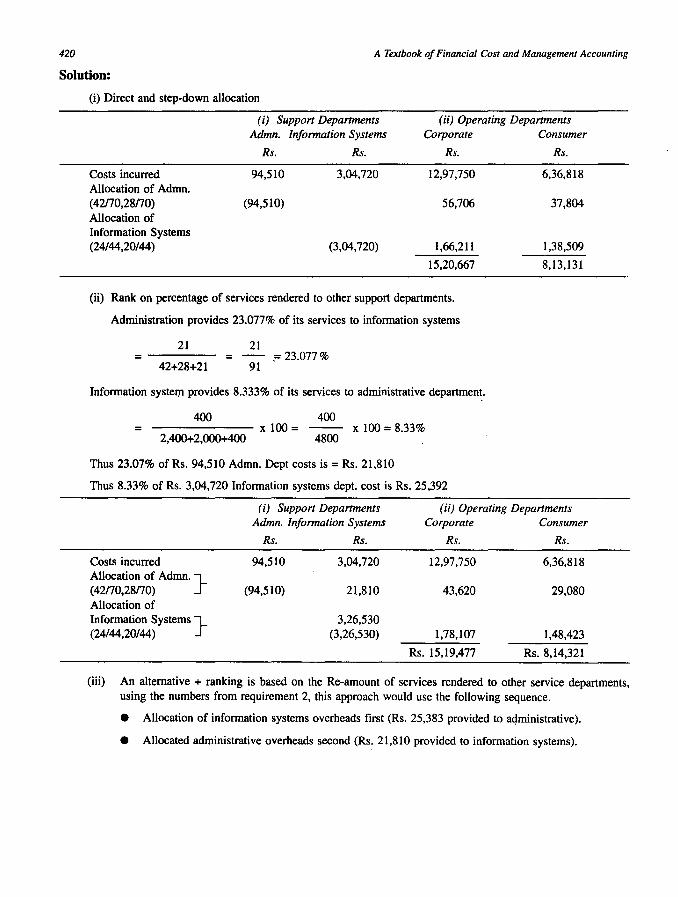

Solution:

A Textbook of Financial Cost and Management Accounting

(i) Direct and step-down allocation

Costs incurred Allocation of Admn. ( 42nO,28nO) Allocation of Information Systems (24/44,20/44)

(i) Support Departments Admn. Information Systems

Rs. Rs.

94,510 3,04,720

(94,510)

(3,04,720)

(ii) Operating Departments Corporate Consumer

Rs. Rs.

12,97,750 6,36,818

56,706 37,804

1,66,211 1,38,509

15,20,667 8,13,131

(ii) Rank on percentage of services rendered to other support departments.

Administration provides 23.077% of its services to information systems

21 21 = = - ,= 23.077%

42+28+21 91

Information system provides 8.333% of its services to administrative departmen~.

400 400 = x 100 = -- x 100 = 8.33%

2,400+2,000+400 4800

Thus 23.07% of Rs. 94,510 Admn. Dept costs is = Rs. 21,810

Thus 8.33% of Rs. 3,04,720 Information systems dept. cost is Rs. 25,392

(i) Support Departments Admn. Information Systems

(ii) Operating Departments Corporate Consumer

Rs. Rs. Rs. Rs.

Costs incurred 94,510 3,04,720 12,97,750 6,36,818 Allocation of Admn. } (42n0,28nO) (94,510) 21,810 43,620 29,080 Allocation of Information Systems} 3,26,530 (24/44,20/44) (3,26,530) 1,78,107 1,48,423

Rs. 15,19,477 Rs. 8,14,321

(iii) An alternative + ranking is based on the Re-amount of services rendered to other service departments, using the numbers from requirement 2, this approach would use the following sequence.

• Allocation of information systems overheads first (Rs. 25,383 provided to a4ministrative).

• Allocated administrative overheads second (Rs: 21,810 provided to information systems).

Overheads

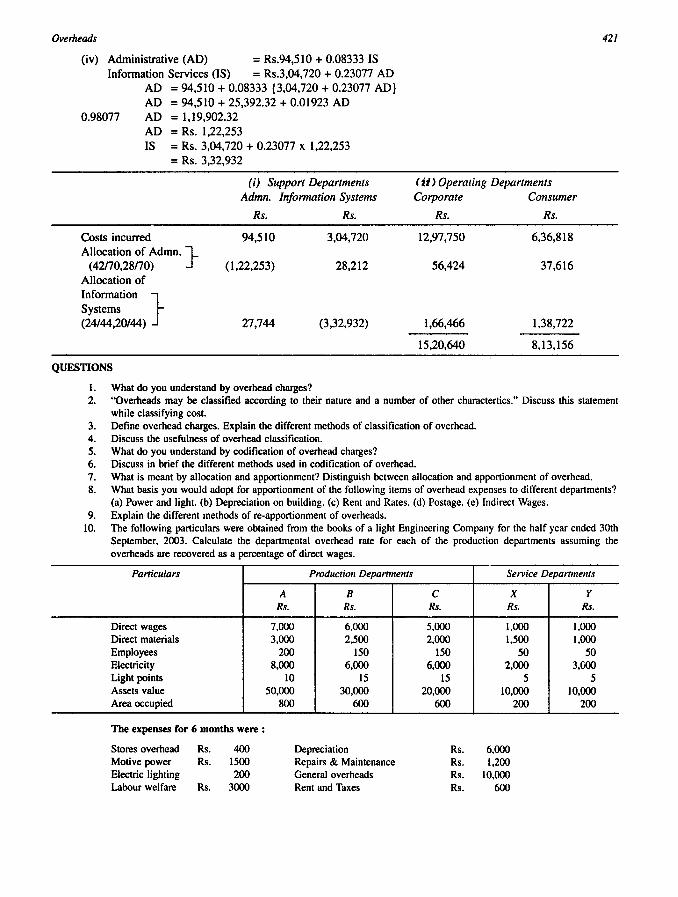

(iv) Administrative (AD) = Rs.94,510 + 0.08333 IS Information Services (IS) = Rs.3,04,720 + 0.23077 AD

AD = 94,510 + 0.08333 {3,04,720 + 0.23077 AD} AD = 94,510 + 25,392.32 + 0.01923 AD

0.98077 AD = 1,19,902.32 AD = Rs. 1,22,253 IS = Rs. 3,04,720 + 0.23077 x 1,22,253

= Rs. 3,32,932

Costs incurred Allocation of Admn. }

( 42170,28nO) Allocation of Information } Systems (24/44,20/44)

QUESTIONS

(i) Suppon Depanments Admn. Information Systems

Rs. Rs.

94,510 3,04,720

(1,22,253) 28,212

27,744 (3,32,932)

1. What do you understand by overhead charges?

( it ) Operating Departments Corporate Consumer

Rs. Rs.

12,97,750

56,424

1,66,466

15,20,640

6,36,818

37,616

1,38,722

8,13,156

421

2. "Overheads may be classified according to their nature and a number of other charactertics." Discuss this statement while classifying cost.

3. Define overhead charges. Explain the different methods of classification of overhead. 4. Discuss the usefulness of overhead classification. S. What do you understand by codification of overhead charges? 6. Discuss in brief the different methods used in codification of overhead. 7. What is meant by allocation and apportionment? Distinguish between a\1ocation and apportionment of overhead. 8. What basis you would adopt for apportionment of the fo\1owing items of overhead expenses to different departments?

(a) Power and light. (b) Depreciation on building. (c) Rent and Rates. (d) Postage. (e) Indirect Wages. 9. Explain the different methods of re-apportionment of overheads.

10. The following particulars were obtained from the books of a light Engineering Company for the half year ended 30th September, 2003. Calculate the departmental overhead rate for each of the production departments assuming the overheads are recovered as a percentage of direct wages.

Particulars Production Departments Service Departments

A B C X Y Rs. Rs. Rs. Rs. Rs.

Direct wages 7,000 6,000 S,OOO 1,000 1,000 Direct materials 3,000 2,SOO 2,000 I,SOO 1,000 Employees 200 ISO ISO SO SO Electricity 8,000 6,000 6,000 2,000 3,000 Light points 10 IS IS S S Assets value SO,OOO 30,000 20,000 10,000 10,000 Area occupied 800 600 600 200 200

The expenses for 6 months were :

Stores overhead Rs. 400 Depreciation Rs. 6,000 Motive power Rs. IS00 Repairs & Maintenance Rs. 1,200 Electric lighting 200 General overheads Rs. 10,000 Labour welfare Rs. 3000 Rent and Taxes Rs. 600

422 A Textbook of Financial Cost and Management Accounting

Apportion the expenses of Department X in the ratio of 4 : 3 : 3 and that of department Y, in proportion of direct wages, to departments A, B, and C respectively. [ ADS: Total overheads cost: A - Rs.1l396, B - Rs.8663, C - Rs.7341 Dept. overhead rate: A - 162.8%, B - 144.4%, C - 146.8%]

11. A company has three departments A, B, and C and two service departments X and Y. The expenses incurred by them during the month of may 2003 are incurred by them during the month of may 2003 are : A- 8000 B -7000 C - 5000 X - 2340 Y - 3000 The expenses of service departments are apportioned to the production departments in the following basis : Particulars ABC X Y Expenses of X 20% 40% 30% 10% Expenses of Y 40% 20% 20% 20% Show clearly as to how the expenses of X and Y departments would be apportioned to A, Band C departments under Simultaneous Equitation Method [Ans : Total cost of service department X = Rs. 3000 Total cost of service department Y = Rs. 3300]

12. You are supplied with the following information and required to work out the production hour rate of recovery of overheads A, B, and C under the Repeated Distribution Method.

Production Departments Service Departments ABC P Q

Rs. Rs. Rs. As per primary } Distribution summary 7,810 12,543 4,547 Expenses of service departments P and Q are apportioned as under:

ABC P P 30% 40% 20% Q 10% 20% 50% 20%

Estimated working hours of production are as under: Departments :

A-l,ooo hours B - 2,500 hours C - 1,400 hours

[Ans : Total Overhead cost of Dept. A - Rs. 9,500 Dept. B - Rs. 1,5000 Dept. C - Rs. 7,000 Overhead Rate: A - Rs. 9.50; B - Rs. 6; C - Rs. 5]

Rs.

4,000

Q 10%

Rs.

2,600

13. A factory consists of three Production Departments, viz., Turning. Milling and Grinding. Though maintenance is done by the departments, the factory keeps four service departments too, viz., Stores, Planning, Canteen and Time Office. For the month of November 2003 the Direct Departmental Expenses were recorded as follows: Turning Rs. 72,000 Stores Rs. 36,000 Milling Rs. 84,000 Planning Rs. 60,000 Grinding Rs. 1,08,000 Canteen Rs. 48,000

Time Office Rs. 12,000 The expenses of stores are to be distributed on a percentage basis, viz., 20%, 40% to Turning. Milling and Grinding respectively. The expenses of Planning are to be apportioned on the basis of Machine Hours worked and those of Canteen and Time Office according to number of men employed in Production Departments. Men employed No. of hours worked

22 10,000 Turning 32 15,000 Milling 46 25,000 Grinding

Prepare a statement showing the distribution of the Service Department's Expenses to the Production Departments and also determine the final absorption rate. [Ans: Total of Turning Rs. 1,04,400; Milling Rs. 1,35,600; Grinding Rs. 1,80,000; Aborption rate per hour 10.44:9.04 and 7.20]

Overheads 423

14. The following particulars relate to a manufacturing company which has three production departments, A, B, C and two service departments X and Y :

Depanments A B C X Y

Total departmental Overhead as primary distribution Rs.63,OOO 74,000 28,000 45,000 20,000

The company decided to charge the service departments cost on the basis of the following percentages: Service Dept. Production Depts. Service Dept. ABC X Y

X 40% 30% 20% 10% Y 30% 30% 29% 20% Find the total overheads of production departments charging service departmental costs to production on the repeated distribution method. [Ans : A Rs. 90,500; B Rs. 96,500; C Rs. 43,000]

15. In a factory, there are two service departments P and Q and three production departments A, Band C. In April 1988 the departmental expenses were:

Depanments Rs.

A 6,50,000 B 6,00,000 C 5,00,000 P 1,20,000

Q 1,00,000

The service departments, expenses are allocated on a percentage basis as follows : Service Dept. Production Depts. Service Dept.

ABC X Y X 30% 40% 15% 15% Y 40% 30% 25% 5%

Prepare a statement showing the distribution of the two service departments expenses to the tree departments under the "Repeated Distribution Method." [Ans : Rs. 7,35,340; Rs. 6,86,045; Rs. 5,48,615]

16. A manufacturing concern has three production departments and two service departments. In July 2003, the departmental expenses were as follows :

Production Departments X Y Z

Service Depanments p

Q

Rs. 16,000 13,000 14,000

4,000 6,000

The service department expenses are charged out on a percentage basis, viz. :

Expenses of dept. P Expenses of dept. Q

X " Z P 20% 25% 35% 25% 25% 40% 10%

Prepare a statement of secondary distribution under repeated distribution method.

Q 20%

[Ans: Total Cost of Dept. X Rs. 18,674; Dept. Y Rs. 15,908; Dept. Z Rs. 18,418] 17. A Company has three production departments and two service departments and distribution summary of overhead is as

follows: Production Depanments

A B C

Service Depanment X Y

Rs. 30,000 20,000 10,000

Rs. 2,340 3,000

424 A Textbook of Financial Cost and Management Accounting

The expenses of service departments are charged on a percentage basis which is as follows : ABC X Y

Service Dept. X 20% 40% 30% 10% Service Dept. Y 40% 20% 20% 20% [Ans: Dept. A Rs. 65,340; Dept. B Rs.31,920; Dept. C Rs. 11,560]

18. In a factory, there are two service departments, P and Q and three production departments A, Band C. In March 2003 the departmental expenses were.

A Rs .6,50,000 P Rs. 1,20,000 B Rs.6,oo,ooo Q Rs. 1,00,000 C Rs. 5,00,000

The service department expenses are allocated on a percentage basis as follows. X Y Z P Q

Dept. P 3% 40 15% 15% Dept. Q 40% 30% 25% 5% Prepare Q statement showing the distribution of two service departments expenses to three departments under simultaneous equation method. [Ans: Dept. A Rs.7,35,342; Dept. B Rs.6,86,046 Dept. C Rs.5,48,612]

000

Related Documents